20

Security analysts’ updates Analyst Ticker John Marek CVX Brian von Hein INTC Altaf Ali MSFT Chad Clark SYK Noel Szczepanski WAG Bobak Khodaie FCX 1

| Date post: | 26-Dec-2015 |

| Category: |

Documents |

| Upload: | godwin-summers |

| View: | 217 times |

| Download: | 3 times |

1

Security analysts’ updatesAnalyst Ticker

John Marek CVX

Brian von Hein INTC

Altaf Ali MSFT

Chad Clark SYK

Noel Szczepanski WAG

Bobak Khodaie FCX

2

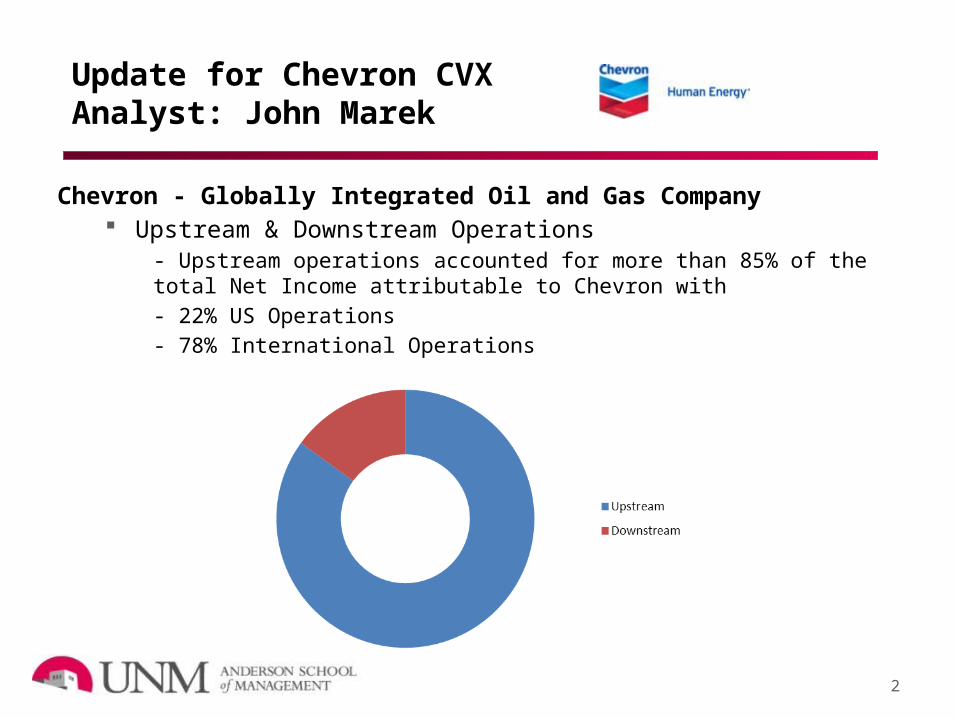

Update for Chevron CVXAnalyst: John Marek

Chevron - Globally Integrated Oil and Gas Company Upstream & Downstream Operations

- Upstream operations accounted for more than 85% of the total Net Income attributable to Chevron with

- 22% US Operations

- 78% International Operations

3

Chevron Profitability & Return Healthy Margins

Gross Margin Chevron 33.59 (4th Best - Industry) Operating Margin Chevron 19.15 (2nd Best - Industry) Net Profit Margin Chevron 10.89 (2nd Best - Industry)

Investor Return Dividend Yield 3.3% (26th annual consecutive increase) Share Repurchase Program (Net) Total Stockholder Return as of 12/31/2012

5 Year TSR 6.5% above peer group ( BP, RDS, TOT, XOM) and S&P 10 Year TSR 16.3% above peer group ( BP, RDS, TOT, XOM) and S&P Future performance not indicative of past performance

4

Chevron Opportunities & Threats Shale Oil and Gas Projects

Vaca Muerta formation in Argentina and Permian Basin Natural Gas is a by product of shale drilling

Liquefied Natural Gas LNG

- Angola LNG Project Running, Wheatstone and Gorgon LNG Project in Western Australia

- LNG emits less carbon, tougher rules on carbon emissions, new technology using natural gas in commercial fleet

Continues Deep Water Drilling Operations Recent Favorable Litigation Outcome in Ecuador and Brazil Alternative Energy Sources and Shale/Tight Oil Plays

5

Chevron Q & A

6

Update for Intel (Ticker: INTC)Closing 10/2 22.89Analyst: Brian von Hein

What is good Data Center Group

- Cloud Storage7 Software Services

- McAfee 2011 Acquisition

What is bad PC client segment in decline

- Shift to more lightweight flexible options Other Intel Operating Segments

- Streaming TV- Smartphone

Time for R&D to turn into final product

7

Update for Intel (Ticker: INTC)Analyst: Brian von Hein

Next Generation Technology Good

FasterLess EnergyJust as powerfulHandles new technology Intel dedicated to R&D

BadCost

7nm: others will not try

8

Update for Microsoft Corporation (MSFT)Analyst: Altaf Ali

CEO Steve Ballmer’s Retirement Positive investor reaction

• Stock price rose 7% on 8/23 Total return declined 22.45% since 2000

• XLK declined 31.96%• SPY increased 48.21%

Lack of innovation (consumer & commercial)• Too focused on Windows• Shifting consumer demand• See Google, Apple• See BlackBerry

9

Update for Microsoft Corporation (MSFT)Analyst: Altaf Ali

Nokia Acquisition Total cost of $7.2B

• $5.0B for Devices & Services (patents, brands)• $2.2B for licensing IP for 10 years • “Offshore cash” will be used for payment

Defensive acquisition• Nokia is the primary OEM for Windows phones (80%)• Nokia may have failed or been acquired by competition• Facilitates MSFT’s shift to “devices & services” (phones, tablets)

10

Update for Microsoft Corporation (MSFT)Analyst: Altaf Ali

Division Reorganization Shift from “software” to “devices and services” company

• “One Microsoft”• Reliance on subscription model• Focused on Gross Margin (Amy Hood, FAC 2013)• dd

Old Divisions New Divisions

Windows(Windows OS, Outlook/Skydrive, Surface, PC accs.)

D&C Licensing (Windows OS, Outlook/SkyDrive, Office, Windows Phone)

Servers & Tools(Windows/SQL Server, Visual Studio, System Center, Windows Embedded,

Azure, Consulting services)

D&C Hardware(Surface, Xbox, PC accessories)

Online Services(Bing, Bing Ads, MSN)

D&C Other(Online Marketplace, Office 365, Search Advertising, 1st party games, retail)

Microsoft Business(Office, Dynamics ERP/CRM, Office 365)

Commercial Licensing(Windows/SQL Server, Visual Studio, System Center, Windows Embedded, non-OEM Windows licensing, Commercial Office, Dynamics ERP, Skype)

Entertainment & Devices(Xbox, Skype, Windows Phone)

Commercial Other(Enterprise/Consulting services, Dynamics CRM, Azure)

14

Stryker Corporation (SYK)Analyst: Chad Clark

Overview:Stryker Corp. is “one of the world’s leading medical technology companies” with 2012 sales of $8.657 billion and net earnings of $1.298 billion. –Stryker 2012 Annual Report

15

Stryker Corporation (SYK)Risks & Opportunities

Risks: Healthcare Reform

2.3% Excise Tax (2013) Liability Claims, Recalls, & Legal Settlements

1H’13 Rejuvenate and ABG II hip stem recall: $210 million

Opportunities: International Sales

35% of total sales are outside the U.S. Market Demographics

Aging Population

16

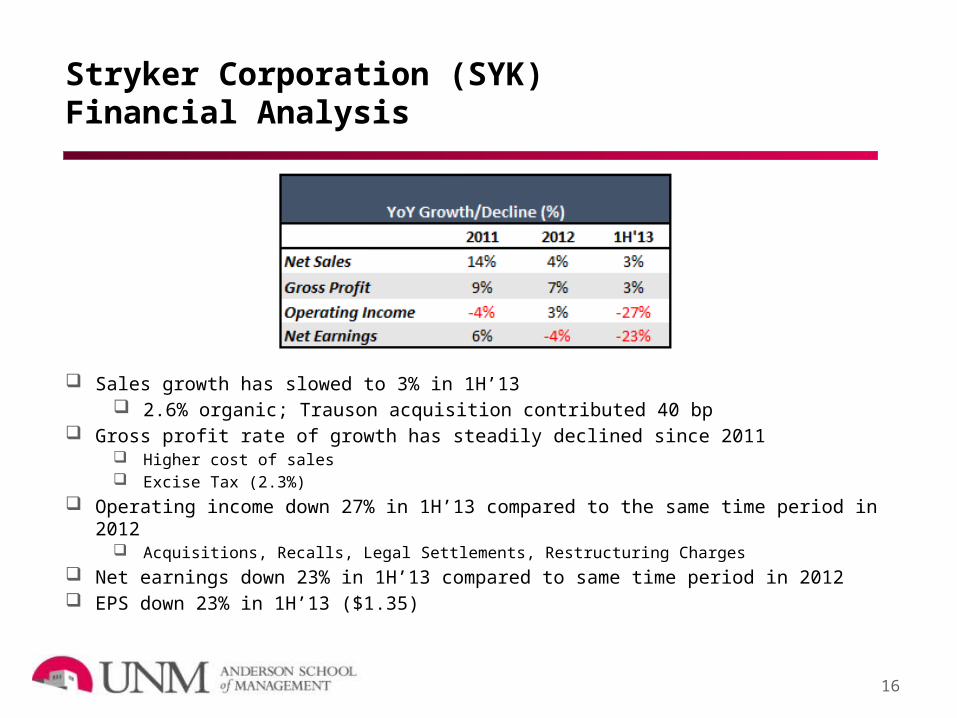

Sales growth has slowed to 3% in 1H’13 2.6% organic; Trauson acquisition contributed 40 bp

Gross profit rate of growth has steadily declined since 2011 Higher cost of sales Excise Tax (2.3%)

Operating income down 27% in 1H’13 compared to the same time period in 2012 Acquisitions, Recalls, Legal Settlements, Restructuring Charges

Net earnings down 23% in 1H’13 compared to same time period in 2012 EPS down 23% in 1H’13 ($1.35)

Stryker Corporation (SYK)Financial Analysis

17

Stryker Corporation (SYK)Outlook

Outlook: Will continue to pursue acquisitions

Trauson Holdings Company Limited (2012) MAKO Surgical Corp. (2013)

Acquired at an 87% premium to FMV Expected to dilute EPS by $0.10-$0.12 (First Year)

Total 2013 sales growth projection adjusted up to 4%- 5.5% (organic) Cost control to maintain margins

5% reduction in global workforce SG&A

Q3’13 Earnings Call October 17th, 2013

Walgreens Corp (WAG)

Noel Szczepanski

SegmentsWalgreens is the leading drug retail chain

in the U.S. Prescription Drugs63%

Front-End37%

Net Income

Prescription Drugs• Branded Margins;

Revenue • Generic Margins;

RevenueFront-End• Fresh Food• Beauty• Beer• Wine

• Personal Care

• Convenience

• Photofinishing

• Non-prescription

SWOT

Strengths Board of Directors Organic Growth Infrastructure

Weaknesses Highly leveraged Decreasing margins Increasing SG&A

Opportunities• Expiring drug patents• Affordable Care Act (ACA)• Mail Order

Threats

• Regulations• Competition• Foreign Exchange

Product Revenue In Millions 2011 2012

CommonSize YoY CommonSize YoYRefined Copper Products $ 10,297 49.32% 0.83% $ 9,699 53.85% 4.54%

Copper In Concentrates $ 5,938 28.44% -1.45% $ 4,589 25.48% -2.96%

Gold $ 2,429 11.63% -0.85% $ 1,741 9.67% -1.97%

Molybdenum $ 1,348 6.46% 0.43% $ 1,187 6.59% 0.13%

Other $ 868 4.16% 1.04% $ 794 4.41% 0.25%

Total $ 20,880 100% $ 18,010 100%

21

Freeport McMoRan (FCX): Q2 Update Presented By: Bobak Khodaie

• Q2 Revenues are down 4.1% compared to Q2 2012• Costs for the period have risen 15% last year.

• Revenues year to date are down 2.3% from last year at this time.• Costs are up nearly 14%

Acquisitions Bobak Khodaie

• June 2013 FCX acquisitions • McMoRan Exploration CO. (MMR) • Plains Exploration and Production Co. (PPX)

• Total Fair Value, Excluding Goodwill:• PPX: $6.18 Billion • MMR: $1.68 Billion

• Goodwill: • PPX: $454 Million• MMR: $1.45 Billion

22

Concerns Bobak Khodaie

• Work Stoppages • Indonesia May- July. • Missed production Goals

• 125 million Pounds of Copper • 125 million Ounces of Gold.

• Peru• Workers Strikes in mining industry over profit sharing.

• Congo • Power issues limit production

• Production reduction of Oil and Gas • Oil and Gas contributed 7.8% to revenues

in Q2

23