SOUTH EAST EUROPE WHOLESALE MARKET OPENING Final report – updated with Ukraine and Moldova December 2011 Public Disclosure Authorized Public Disclosure Authorized Public Disclosure Authorized Public Disclosure Authorized Public Disclosure Authorized Public Disclosure Authorized Public Disclosure Authorized Public Disclosure Authorized

Transcript

SOUTH EAST EUROPE WHOLESALE MARKET OPENING

Final report – updated with Ukraine and Moldova December 2011

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

wb425962

Typewritten Text

68653

SOUTH EAST EUROPE WHOLESALE MARKET OPENING

PÖYRY MANAGEMENT CONSULTING

NORD POOL CONSULTING

ACKNOWLEDGEMENT

The South East Europe Wholesale Market Opening technical assistance project (the Project) is co-financed by two multi-donor trust funds, ESMAP and PPIAF.

The Energy Sector Management Assistance Program (ESMAP) is a global technical assistance program which helps build consensus and provides policy advice on sustainable energy development to governments of developing countries and economies in transition. For more information on the program see the website: www.esmap.org

The Public-Private Infrastructure Advisory Facility (PPIAF) is a multi-donor technical assistance facility aimed at helping developing countries to improve the quality of their infrastructure through private sector involvement. For more information on the facility see the website: www.ppiaf.org

The Word Bank is managing the Project as a part of its support to the development of the Energy Community. For information about the World Bank's energy sector activities see the website: www.worldbank.org/energy

The Consultant has used the following terminology throughout the report: (with reference to the United Nations Security Council Resolution 1244 for point 1 and 2):

UNMIK – when referring to the Contracting Party

Kosovo when referring to the geographic territory

Former Yugoslav Republic of Macedonia or FYR of Macedonia

Local – not national

Contracting Party – instead of country

The term Contracting Party will now also include Ukraine and Moldova

Jurisdictions when referring to both Contracting Parties, Bulgaria, and Romania

DISCLAIMER

Pöyry Management Consulting (Sweden) AB and Nord Pool Consulting AS retain all rights (including copyrights, brand rights, patent rights) related to the information in this report.

Pöyry Management Consulting (Sweden) AB and Nord Pool Consulting AS do not permit partial quotes from the study report as this can lead to misleading conclusions.

While Pöyry Management Consulting (Sweden) AB and Nord Pool Consulting AS considers that the information and opinions given in this work are sound, all parties must rely on their own skill and judgement when making use of it.

Pöyry Management Consulting (Sweden) AB and Nord Pool Consulting AS does not make any representation or warranty, expressed or implied, as to the accuracy and completeness of the information contained in this report and assumes no responsibility for the accuracy or completeness of such information,

Pöyry Management Consulting (Sweden) AB and Nord Pool Consulting AS will not assume any liability to anyone for any loss or damage arising out of the provision of this report.

SOUTH EAST EUROPE WHOLESALE MARKET OPENING

3

PÖYRY MANAGEMENT CONSULTING

NORD POOL CONSULTING

[This page is intentionally blank]

SOUTH EAST EUROPE WHOLESALE MARKET OPENING

4

PÖYRY MANAGEMENT CONSULTING

NORD POOL CONSULTING

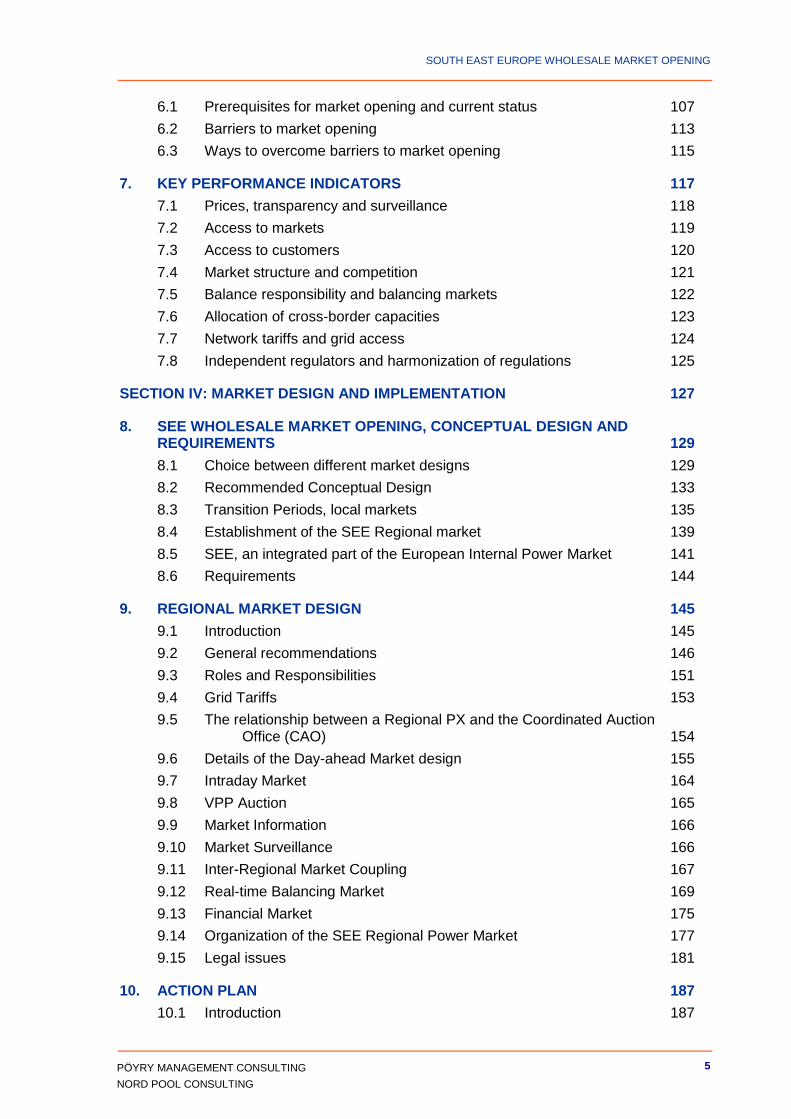

TABLE OF CONTENTS

REPORT SUMMARY 10

SECTION I: HIGH LEVEL RECOMMENDED MARKED DESIGN 16

1. SUMMARY OF RECOMMENDED MARKET DESIGN AND IMPLEMENTATION 18

1.1 Prerequisites 18

1.2 Choice between different Market Design Options 19

1.3 Conceptual Market Design 23

1.4 Business Processes 26

1.5 Integration with Neighbouring Markets 28

1.6 Transition phase: From regulated prices to market prices 28

1.7 CAO – Coordinated Auction Office 33

1.8 VPP Auctions, Bilateral Auctions and Physical Forward Markets arranged by the Local Market Operators 34

1.9 Gap Analysis 34

1.10 Action Plans 36

SECTION II: BACKGROUND 44

2. THE CURRENT STATE OF MARKET OPENING IN SEE REGIONAL ELECTRICITY MARKET 46

2.1 Introduction 46

2.2 Electricity generation and demand 46

2.3 Regional trade in electricity 55

2.4 Market structure, market opening and market model 62

2.5 Prices and tariffs 69

2.6 Current Balance Management in SEE 71

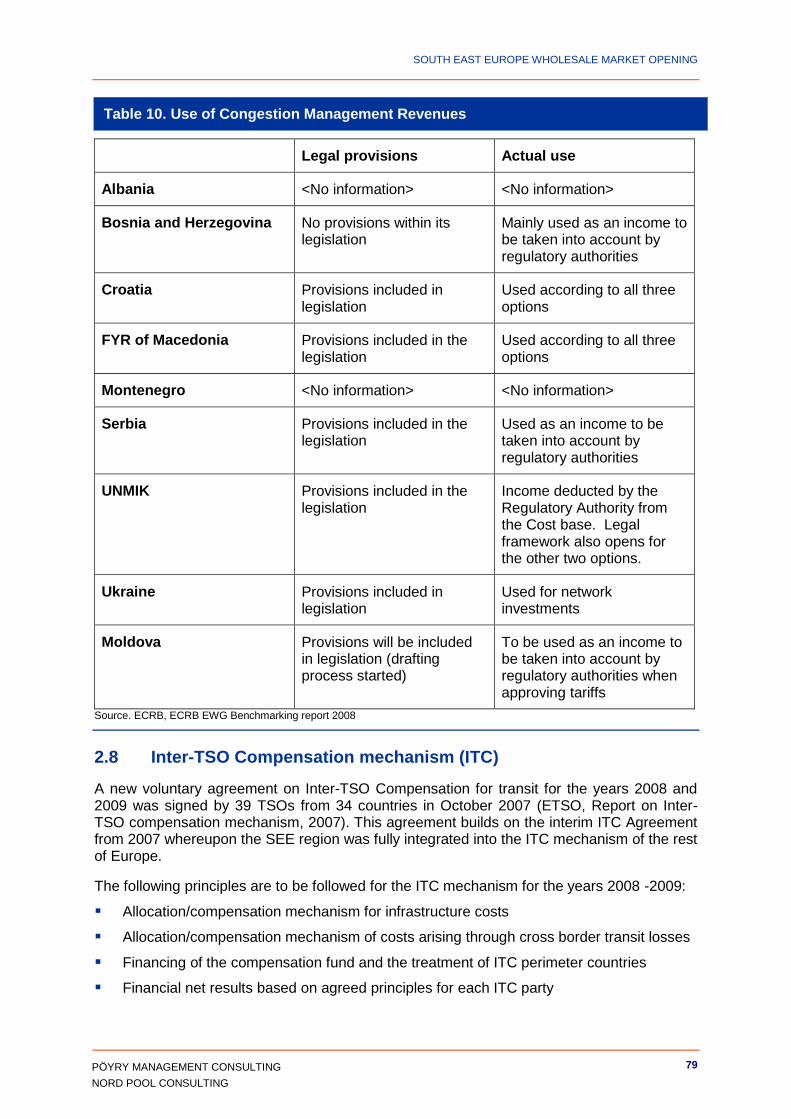

2.7 Congestion management and cross-border capacity allocation 72

2.8 Inter-TSO Compensation mechanism (ITC) 79

3. EXPERIENCES FROM OTHER REGIONAL MARKETS 81

3.1 Selected Local and regional markets 81

3.2 Review of Regional Markets 89

3.3 Conclusion 94

SECTION III: ANALYSIS 95

4. POSSIBLE CAUSES FOR HIGH PRICES IN THE REGION 97

5. RISKS AND OPPORTUNITIES FOR NON-HOUSEHOLD CUSTOMERS 103

5.1 Key risks 103

5.2 Opportunities 104

6. BARRIERS TO MARKET OPENING 107

SOUTH EAST EUROPE WHOLESALE MARKET OPENING

5

PÖYRY MANAGEMENT CONSULTING

NORD POOL CONSULTING

6.1 Prerequisites for market opening and current status 107

6.2 Barriers to market opening 113

6.3 Ways to overcome barriers to market opening 115

7. KEY PERFORMANCE INDICATORS 117

7.1 Prices, transparency and surveillance 118

7.2 Access to markets 119

7.3 Access to customers 120

7.4 Market structure and competition 121

7.5 Balance responsibility and balancing markets 122

7.6 Allocation of cross-border capacities 123

7.7 Network tariffs and grid access 124

7.8 Independent regulators and harmonization of regulations 125

SECTION IV: MARKET DESIGN AND IMPLEMENTATION 127

8. SEE WHOLESALE MARKET OPENING, CONCEPTUAL DESIGN AND REQUIREMENTS 129

8.1 Choice between different market designs 129

8.2 Recommended Conceptual Design 133

8.3 Transition Periods, local markets 135

8.4 Establishment of the SEE Regional market 139

8.5 SEE, an integrated part of the European Internal Power Market 141

8.6 Requirements 144

9. REGIONAL MARKET DESIGN 145

9.1 Introduction 145

9.2 General recommendations 146

9.3 Roles and Responsibilities 151

9.4 Grid Tariffs 153

9.5 The relationship between a Regional PX and the Coordinated Auction Office (CAO) 154

9.6 Details of the Day-ahead Market design 155

9.7 Intraday Market 164

9.8 VPP Auction 165

9.9 Market Information 166

9.10 Market Surveillance 166

9.11 Inter-Regional Market Coupling 167

9.12 Real-time Balancing Market 169

9.13 Financial Market 175

9.14 Organization of the SEE Regional Power Market 177

9.15 Legal issues 181

10. ACTION PLAN 187

10.1 Introduction 187

SOUTH EAST EUROPE WHOLESALE MARKET OPENING

6

PÖYRY MANAGEMENT CONSULTING

NORD POOL CONSULTING

10.2 Regional Action Plan 187

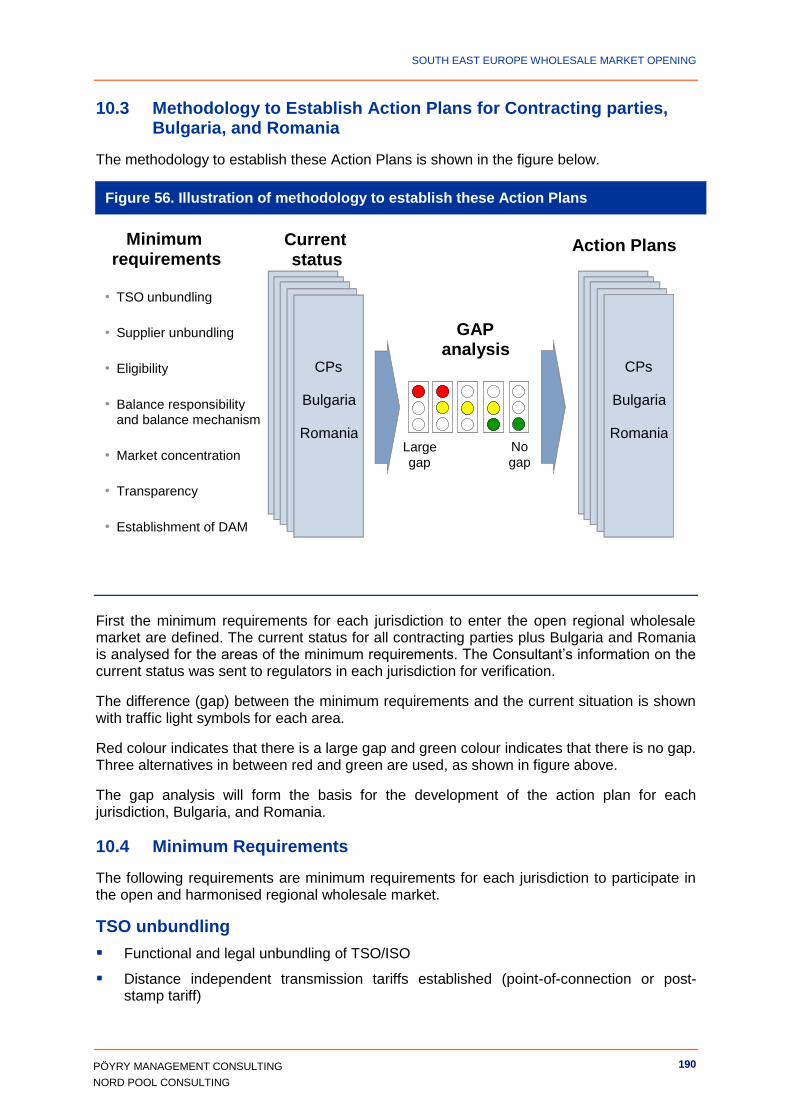

10.3 Methodology to Establish Action Plans for Contracting parties, Bulgaria, and Romania 190

10.4 Minimum Requirements 190

10.5 Proposed General Decisions and Commitments 192

10.6 Template for the Action Plans 192

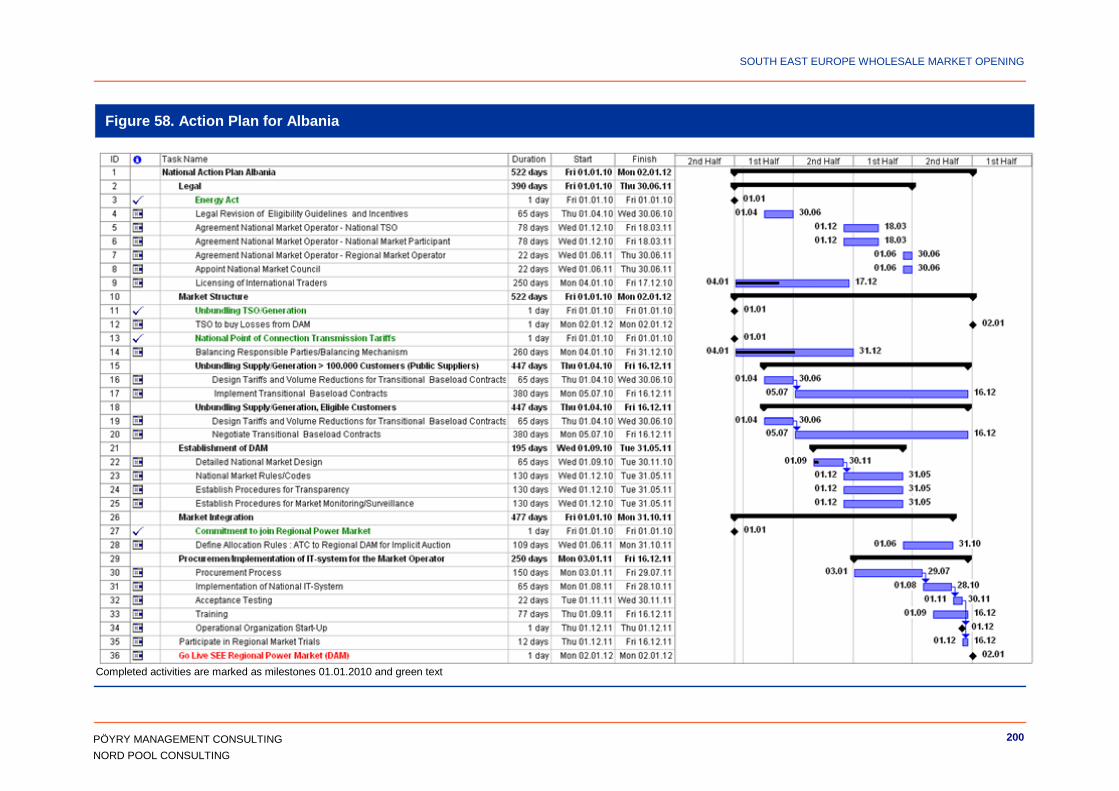

10.7 Action Plans for Contracting Parties, Bulgaria, and Romania 197

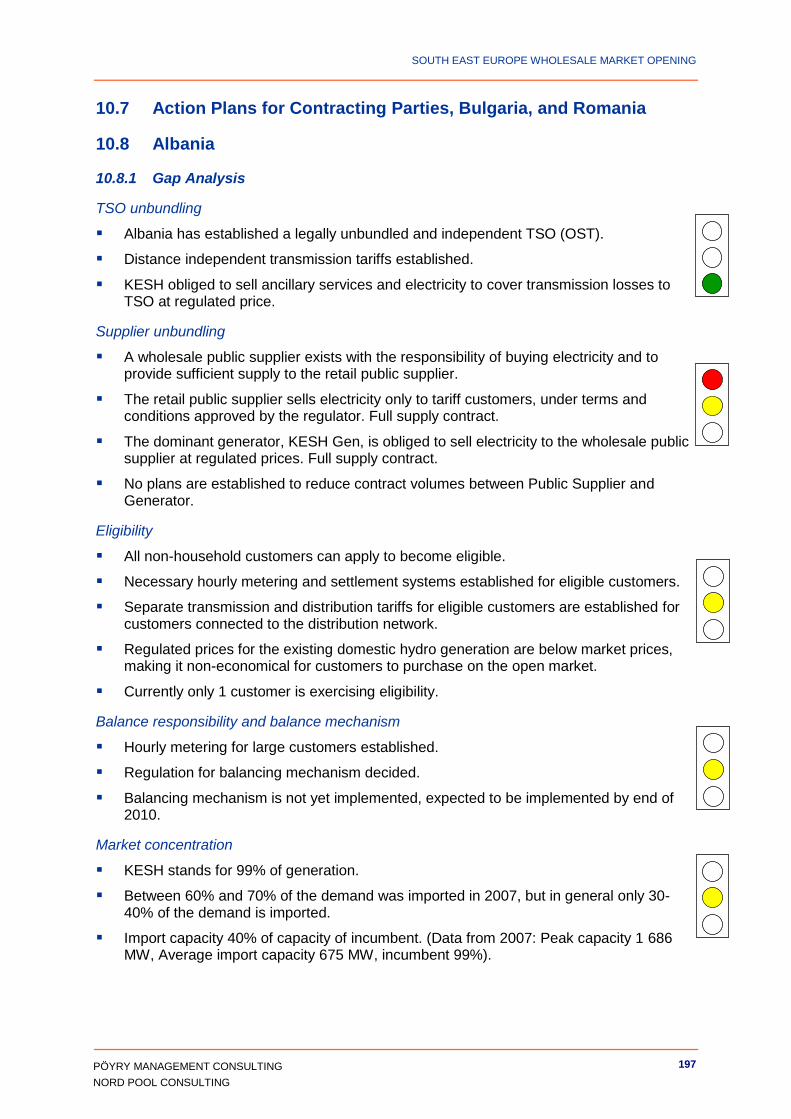

10.8 Albania 197

10.9 Bosnia and Herzegovina 201

10.10 Croatia 205

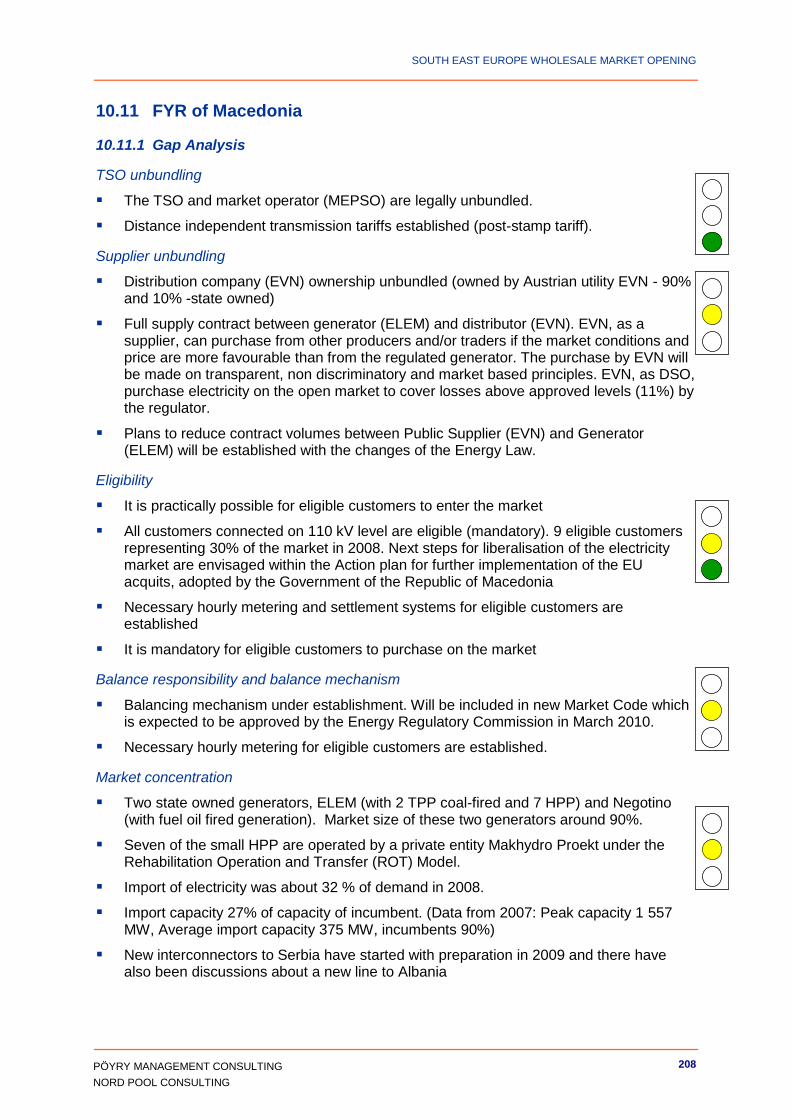

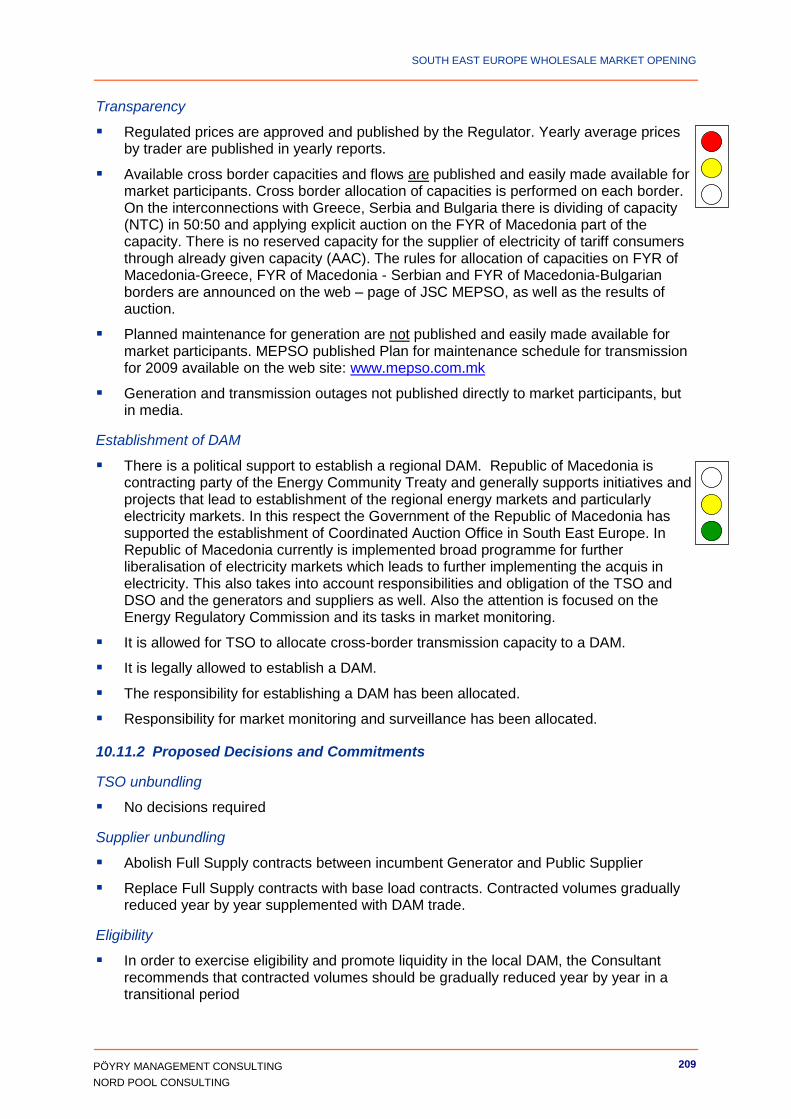

10.11 FYR of Macedonia 208

10.12 Montenegro 212

10.13 Serbia 216

10.14 UNMIK 220

10.15 Bulgaria 224

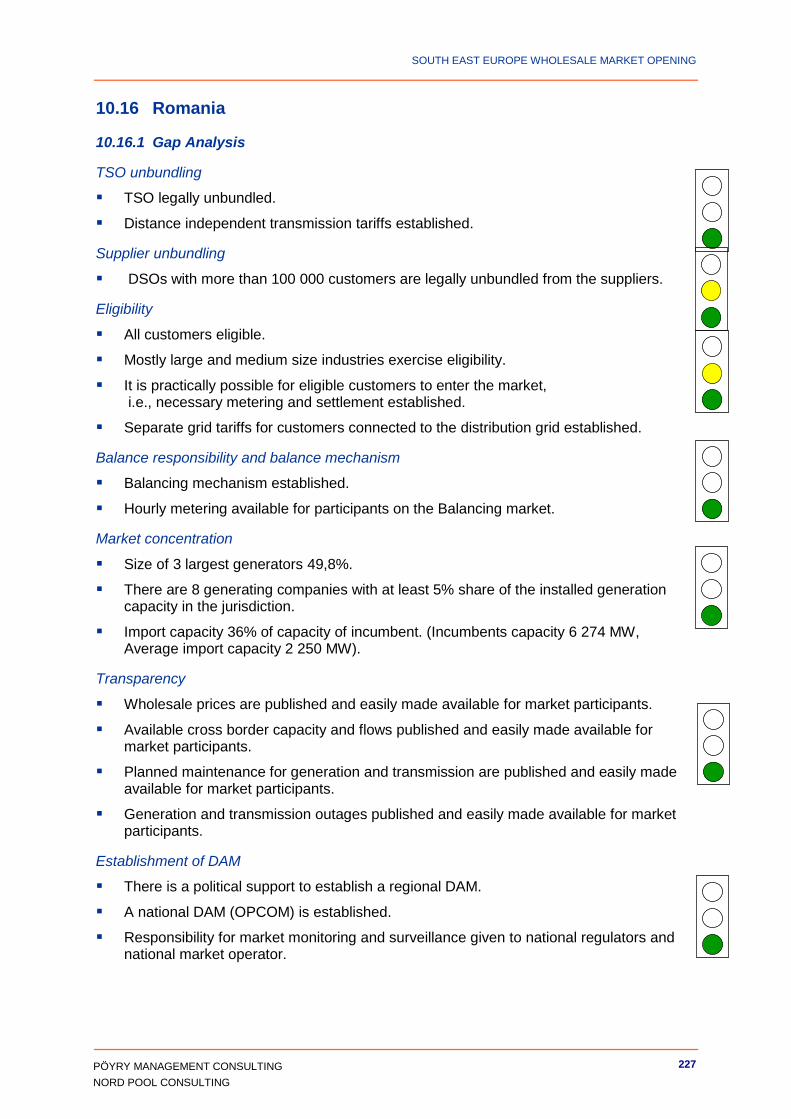

10.16 Romania 227

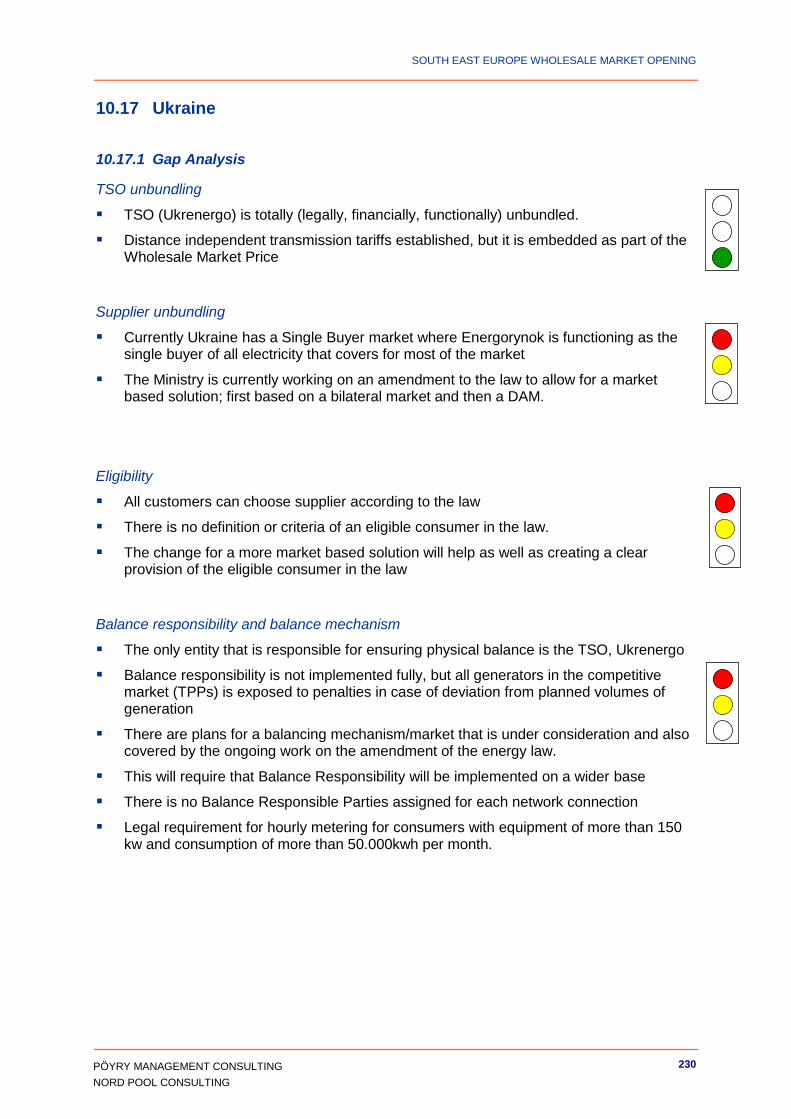

10.17 Ukraine 230

10.18 Moldova 234

ANNEX A LIST OF REFERENCES 241

ANNEX B GLOSSARY 243

SOUTH EAST EUROPE WHOLESALE MARKET OPENING

7

PÖYRY MANAGEMENT CONSULTING

NORD POOL CONSULTING

[This page is intentionally blank]

SOUTH EAST EUROPE WHOLESALE MARKET OPENING

8

PÖYRY MANAGEMENT CONSULTING

NORD POOL CONSULTING

EXECUTIVE SUMMARY

The 11th Athens Forum Meeting requested the World Bank to develop a study on Wholesale Market Opening in South East Europe for the benefit of all Contracting Parties to the Treaty establishing the Energy Community.

Pöyry Management Consulting and Nord Pool Consulting were commissioned by the World Bank to develop a study on Wholesale Market Opening for the electricity market in South East Europe (SEE). The key outputs of the study are a Regional Market Design (RMD) and an action plan for its implementation.

A new version of the study was developed during 2011 to include Ukraine and Moldova in the study on the same level as the original Contracting Parties.

Based on the findings from carrying out the various tasks that were assigned, the Consultant recommends the following:

1. To secure liquidity and transparency in the initial operational phase of the wholesale market, local authorities need to support the implementation of SEE Day-Ahead Market (DAM) through the introduction of proper incentives for market participants.

Experience from implementation of DAM projects in Europe indicates that the largest obstacles in the initial stage of operation are the lack of liquidity in the day-ahead market.

2. Carry out a staged implementation of a regional wholesale market with respect to both participating jurisdictions and to market functions

Expanding the geographical scope of the regional wholesale market by gradually adding new jurisdictions, starting with a nucleus consisting of Romania, Serbia and Bulgaria

Transition from 100% regulated prices to 100% market prices, exposing market participants to spot prices on marginal volumes from day one of market opening. Each jurisdiction decides at what speed the transition shall proceed. It is of high importance that demand side volumes are brought to the DAM.

3. Facilitate harmonisation of rules and regulations between the SEE Contracting Parties and relevant EU directives and regulations

A common playing field is a prerequisite for all regional market activities.

4. Set a target completion date of January 1st 2012 for the start up of a SEE DAM market and a target date of Jan 1st 2015 for the full SEE electricity wholesale market opening including a financial forward electricity market.

An ambitious plan is required to comply with the commitments made by signing the EC Treaty by all Contracting Parties including Bulgaria and Romania,

SOUTH EAST EUROPE WHOLESALE MARKET OPENING

9

PÖYRY MANAGEMENT CONSULTING

NORD POOL CONSULTING

To achieve these target dates the following decisions by Ministries are recommended:

Give incentives to eligible customers to trade at the DAM

Base load contracts at favorable prices (current tariffs). Remaining volumes must be sourced from DAM

Unbundling of supply and generation functions

Generator – Supplier unbundling, at least removal of traditional Full Supply Contracts between Generators and Suppliers/Eligible Customers

Base load contracts between incumbent generators and suppliers to serve tariff customers. Remaining volumes to be sourced from the DAM

To achieve these target dates the following decisions by TSOs/Regulators ought to be made:

Cross border capacities should be allocated to DAM

Balance responsibility for all wholesale market participants

TSOs to purchase main grid losses at the DAM

Local Market Operators to set up physical forward markets within their jurisdiction with local incumbents as market makers.

Characteristics of the open and competitive SEE wholesale electricity market

Enhanced investment climate in the SEE Region

Merit order in generation and optimal use of cross border transmission capacities

A market model which allows for a quick integration with neighboring CEE- and CWE countries through market coupling. Links to other neighboring countries can be handled like it is done today through explicit auctioning of cross border capacities.

A flexible solution for the regional/local market operators, allowing each jurisdiction to decide which functions to be handled by the local market operator or to be outsourced to the regional entity

Transparency of relevant market information and prices secured by a DAM in parallel with auctioning of bilateral contracts

Equal market access to all

Co-existence of bilateral and exchange trading

SOUTH EAST EUROPE WHOLESALE MARKET OPENING

10

PÖYRY MANAGEMENT CONSULTING

NORD POOL CONSULTING

REPORT SUMMARY

Introduction

The main geographical focus of the report is the updated nine Contracting Parties to the Treaty that established the Energy Community, i.e. Albania, Bosnia and Herzegovina, Croatia, FYR of Macedonia, Montenegro, Serbia, UNMIK, Ukraine, Moldova and also the former contracting parties Bulgaria and Romania.

The Contracting Parties to the Energy Community Treaty have legally binding commitments to the creation of an internal market for network energy.

The regional market provided for by the Treaty is to be connected to the EC internal market. Through the Energy Community Treaty, the Contracting Parties are bound to implement the “acquis communautaire on energy”1, the “acquis communautaire on environment” and also follow the principles laid out in the acquis on competition insofar as it may affect the trade of network energy between the Parties. According to the Treaty the Parties shall also implement the renewables Directive 2001/77/EC (promotion of electricity produced from renewable sources) and Directive 2003/30/EC (promotion of the use of bio fuels or other renewable fuels for transport).2

Under the Treaty the regulators are cooperating within the Energy Community Regulatory Board (ECRB). The ECRB advises the Ministerial Council and Permanent High Level Group (PHLG) on details of statutory, technical and regulatory rules and make recommendations in the case of cross-border disputes between the regulators.

The electricity sector in South East Europe is characterized by small, but in many cases fast growing markets. The size of the markets in terms of final electricity consumption varies between 3.2 TWh (UNMIK) and 25.6 TWh (Serbia) in the seven original Contracting Parties. With the addition of Ukraine, they are by far the biggest Contracting Party with final electricity consumption of 123.1 TWh. The region exhibits a mixed generation structure with primarily conventional thermal - and hydro power plants. The nine Contracting Parties are in total import dependent, and some of them are suffering from severe shortages.

The general flow of electricity in the region is from the north to the south. Bosnia and Herzegovina is the only contracting party among the seven that has a surplus and the region as a whole is an importer.

Losses (commercial and technical) are in many cases very high and the economies in the region are generally characterized by high energy intensities/low energy efficiency. The Local markets are in most cases dominated by one (state-owned) generator that supplies at regulated rates to tariff customers. The regulated tariffs, although they might cover the current costs, are generally low and not sufficient to cover the cost of new investments. The tariffs do however vary considerable within the region.

1 Directive 2003/54/EC of the European Parliament and of the Council of 26 June 20003

concerning common rules for the internal market in electricity, Directive 2003/55/EC of the European Parliament and of the Council of 26 June 2003 concerning common rules for the internal market in natural gas, Regulation 1228/2003/EC of the European Parliament and of the Council of 26 June 2003 on conditions for access to the network for cross-border exchanges in electricity.

2 The Treaty establishes that the Parties shall present a plan to implement the directives within one year of the date of entry into force of the Treaty.

SOUTH EAST EUROPE WHOLESALE MARKET OPENING

11

PÖYRY MANAGEMENT CONSULTING

NORD POOL CONSULTING

A large number of reports have previously been developed covering these or closely related issues related to regional market integration.

One key question has been, should a regional power exchange be established or should there be a continued reliance on purely bilateral contracts?

Furthermore, the market model currently under development relies on explicit auctioning of cross-border transmission capacities. An alternative option would be the use of implicit auctioning. This would require a liquid market place under a „market splitting‟ approach, or „market coupling‟ between several liquid markets.

According to the Terms of Reference for this study, these options should be reviewed, and based on this review a Regional Market Design should be developed, taking into account the possibility of a staged implementation.

The study assignment included the following eight defined tasks:

Task 1: Review of the current state of market opening in SEE

Task 2: Examine barriers to advancing market opening and liberalisation

Task 3: Identify risks and opportunities posed by market opening in electricity supply to non-household customers

Task 4: Review lessons learned from other regional markets

Task 5: Define indicators to measure and monitor progress in opening the electricity market in SEE

Task 6: Developing the SEE Regional Market Design (RMD) and Action Plan for Implementation

Task 7: Workshops for non-household consumers and other market participants on electricity market opening; and

Task 8: Implementation Support

Below, a high level summary is presented for the work covered under each of the assigned tasks.

Task 1: Review of the current state of market opening in SEE

The review of the current state of market opening in SEE conducted by the Consultant, has found that the market opening process has been initiated at local level within all the contracting parties, Bulgaria, and Romania. It has, however, in the various jurisdictions reached different levels of progress.

For some crucial elements of the opening process, e.g. TSO unbundling and establishing a competent regulatory entity, the progress is very satisfactorily, while for other elements, e.g. competition and transparency, the development is only in its infancy.

Lack of market price penetration to final customers is probably the most serious obstacle against establishing an efficient electricity sector. There are generally no publically available and generally trusted reference prices for electricity. Although the possibility for secondary trading of cross-border capacities exists in a few cases these are not liquid and well-functioning markets. Long-term trade in electricity may function reasonable well, but no organized market place for trade in electricity currently exists.

The key findings made by the Consultant are used in establishing the design of the initial open wholesale electricity market in SEE

SOUTH EAST EUROPE WHOLESALE MARKET OPENING

12

PÖYRY MANAGEMENT CONSULTING

NORD POOL CONSULTING

Task 2: Examine barriers to advancing market opening and liberalization

The Consultant has identified several potential barriers to advancing market opening and liberalisation.

Many important prerequisites for a regional market opening are only fulfilled to a limited degree.

The Consultant has defined minimum requirements related to the following issues as a prerequisite to wholesale market opening.

TSO Unbundling

Supplier Unbundling

Eligibility

Balance Responsibility and Balancing Mechanisms

Market Concentration

Transparency

Establishment of a Regional DAM

Fulfilling these minimum requirements leads to a removal of identified barriers in each jurisdiction.

Task 3: Identify Risks and Opportunities Posed by Market Opening in Electricity Supply to Non-Household Customers

The Consultant has identified some key risks for non-household customers posed by market opening:

Risk of increased prices:

Risk of unfair competition

Risk of market power

Volatile prices

Risk of limited real market access

While there are risks that may arise which the customers need to be prepared for, there are also several opportunities arising from market opening:

New investments and increased security of supply

Access to a large base of suppliers

New service offerings

Demand side participation.

Investments in own generation

Improved utilisation of generation and transmission

SOUTH EAST EUROPE WHOLESALE MARKET OPENING

13

PÖYRY MANAGEMENT CONSULTING

NORD POOL CONSULTING

Task 4: Review lessons learned from other regional markets

The Consultant has reviewed the various market developments and lesson learned in local and regional markets in EU including the Nordic market.

The most important lesson learned seems to be that there must be a strong political will among the countries involved to create an open electricity market. It seems equally important that the cooperative environment within and between the states involved are good and that the politicians dare to take the necessary steps to create a regional market even though the resistance from some parties can be high.

Task 5: Define indicators to measure and monitor progress in opening the electricity market in SEE

The Consultant has defined 50 Key Performance Indicators (KPIs) to monitor the progress of the SEE wholesale market opening. The KPIs will show the pace of progress and make it possible to take measures, if the process is haltering. Some of the indicators measure whether a necessary instrument that can support the desired development is in place or not, while other indicators measure how well these function. The KPIs have been grouped in the following areas:

Prices, transparency and surveillance

Access to markets

Access to customers

Market structure and competition

Balance responsibility and balancing market

Allocation of cross-border capacities

Network tariffs and grid access

Independent regulators and harmonisation of regulation

Task 6: Developing the SEE Regional Market Design (RMD) and Action Plan for Implementation

The main task of this study has been the development of the SEE Regional Market Design and Action Plan for Implementation.

As a reference for this design the Consultant has chosen as benchmarks the successful implementation of competitive wholesale markets in Europe, which are mainly EPEX, Nord Pool, and TLC.

A starting point has been the findings made by the Consultant regarding the current state of market opening in SEE (Task 1) and the barriers to advancing market opening and liberalization. (Task 2)

These findings reveal major gaps between the current state and what is considered as minimum requirements to proceed with a market opening.

SOUTH EAST EUROPE WHOLESALE MARKET OPENING

14

PÖYRY MANAGEMENT CONSULTING

NORD POOL CONSULTING

The large gaps that exist today in most of the jurisdictions, confirm that the transition to an open wholesale market is a major step for the SEE region. A staged approach to a market opening, combined with certain incentives for eligible consumers and public suppliers to source from the open market to secure and promote market liquidity, is therefore an embedded part of the design

In order to co-ordinate the wholesale market opening process in the region an action plan is developed.

This plan comprises decisions/activities that must be fulfilled prior to market opening and is made jurisdiction specific. First the minimum requirements for establishment of a regional DAM are defined. The current status for all Contracting Parties plus Bulgaria and Romania is analysed against these minimum requirements. The difference (gap) between requirements and current situation forms the basis for each local action plan.

A common feature seems to be that TSO unbundling and separation of grid tariffs are very well established in the region. Within Supplier/Generator unbundling, however, much work has to be done. Incumbents hold a much too strong grip on customers. Local authorities have to be engaged in creating incentives for customers and Suppliers to trade at organized market places, such as local DAMs.

Task 7: Workshops for non-household consumers and other market participants on electricity market opening

A workshop was organized in Vienna on September 16th 2009 attended by SEE wholesale market participants including EFET representatives.

The agenda was as follows:

1. Introduction/Welcoming Remarks

2. Barriers and Obstacles to Market Opening

3. Risk and Opportunities for Non-Household Consumers

4. Indicators and Monitoring

5. Regional Market Design

6. Action Plan

7. SEE Wholesale Market – Participant perspective

8. Closing Remarks

Task 8: Implementation Support

This task depends on acceptance of proposed market design and implementation plan from all jurisdictions.

SOUTH EAST EUROPE WHOLESALE MARKET OPENING

15

PÖYRY MANAGEMENT CONSULTING

NORD POOL CONSULTING

Reading instruction

The report consists of four main sections as well as three annexes.

Section I (chapter 1) is a high level summary of the recommended market design and action plan. These are the key recommendations from the Consultants and are based on the presentation given at the ECRB meetings and workshop in Vienna in September 2009.

Section II (chapter 2-3) contains background information such as the foundation for the project, the current situation in SEE and experiences from other regional electricity markets. A reader with good insights to the region and the subject may want to skip this section.

Section III (chapter 4-7) contains analysis of possible causes for high prices in the current SEE electricity markets, risk and opportunities for non-household customers in an open and competitive SEE regional electricity market, ,and key performance indicators to monitor the progress of the wholesale market opening.

Section IV (chapter 8-10) contains the market design recommended by the Consultant and the action plan to implement the solution. This section provides more details regarding the recommended market design and details and insight to the high level summary in section I.

SOUTH EAST EUROPE WHOLESALE MARKET OPENING

16

PÖYRY MANAGEMENT CONSULTING

NORD POOL CONSULTING

SECTION I: HIGH LEVEL RECOMMENDED MARKED DESIGN

SOUTH EAST EUROPE WHOLESALE MARKET OPENING

17

PÖYRY MANAGEMENT CONSULTING

NORD POOL CONSULTING

[This page is intentionally blank]

SOUTH EAST EUROPE WHOLESALE MARKET OPENING

18

PÖYRY MANAGEMENT CONSULTING

NORD POOL CONSULTING

1. SUMMARY OF RECOMMENDED MARKET DESIGN AND IMPLEMENTATION

1.1 Prerequisites

The framework for the SEE Wholesale Market Opening is set by the Treaty Establishing the Energy Community ref [30] and the EC Treaty, ref [13].

The recommended market design is based on the following basic requirements:

SEE, an integrated part of European Internal Energy Market

Technical operation of the SEE grid system spans 4 control areas within ENTSO-E. With the inclusion of Ukraine and Moldova, a 5th area from UPS/IPS is added. Trade across local borders within SEE is currently based on bilateral contracts and explicit auctions. The proposed market design will bring no change to TSOs scheduling and accounting. A day-ahead-market (DAM) will replace some bilateral contracts.

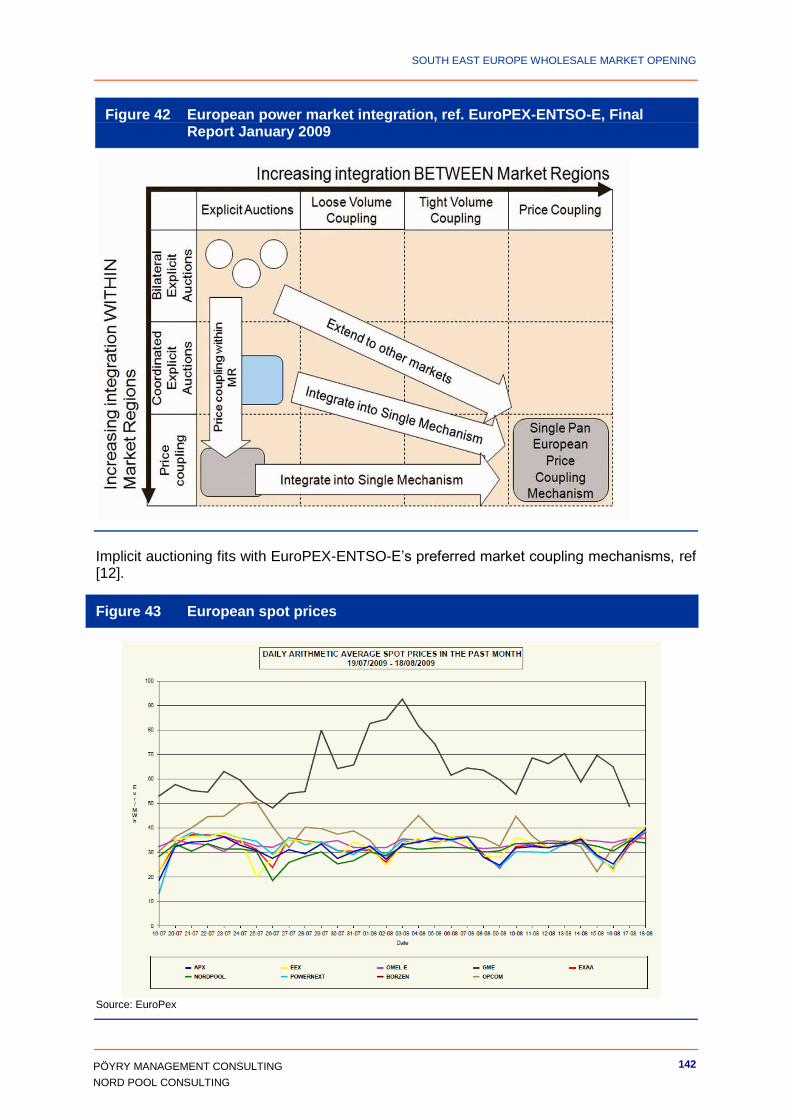

It is recommended that the SEE Wholesale Market Opening should streamline with European trends with price coupling linking local and regional markets in order to enhance efficiency and transparency. Implicit auctioning fits with EuroPEX-ENTSO-E‟s preferred market coupling mechanisms, (ref chapter 8.5 and [12]).

Existing European Power Exchanges (PXs) bring transparency and predictability to market participants and investors across Europe. SEE countries will benefit from harmonization and integration with these markets.

Regional approaches that choose incompatible solutions would obstruct the process of creating an integrated pan-European power market (ref: [12]).

Local control, regional cooperation

The recommended market design aims at having local responsibility of all the trading processes, procedures and trading platforms including the market opening process itself. Regional cooperation and efficient cross-border utilisation will be secured through coupling of local DAMs. TSOs must allocate cross border capacity to DAMs.

Controlled transition from regulated prices to open market

The process of abandoning regulated prices/tariffs is progressing at different speed throughout the SEE region. The recommended design allows for local preferences with respect to further development of this process. Schemes for vulnerable customer sustain.

Quick establishment of incentives to invest

Generator/supplier unbundling and a number of incentives for wholesale market participants to trade at DAM will secure DAM-liquidity. A liquid SEE market coupled to other European power markets with the same trading regimes will soon establish a reliable and trustworthy price reference for the region. As soon as the reference price(s) for the SEE market is established, investors will find it more favourable to come forward. Publishing SEE DAM prices through EuroPEX daily info systems will be a strong indication of market integration.

SOUTH EAST EUROPE WHOLESALE MARKET OPENING

19

PÖYRY MANAGEMENT CONSULTING

NORD POOL CONSULTING

Co-existence of bilateral trade and market operators

Until financial instruments are developed, market participants will need bilateral trade (mid- and long term contracts) to supplement DAM trade to handle price risk

Further development of bilateral markets will be driven by market participants as a response to DAM opening. Auctioning of bilateral contracts rather than or supplementing negotiations should, however be considered to increase transparency in mid- and long term markets.

1.2 Choice between different Market Design Options

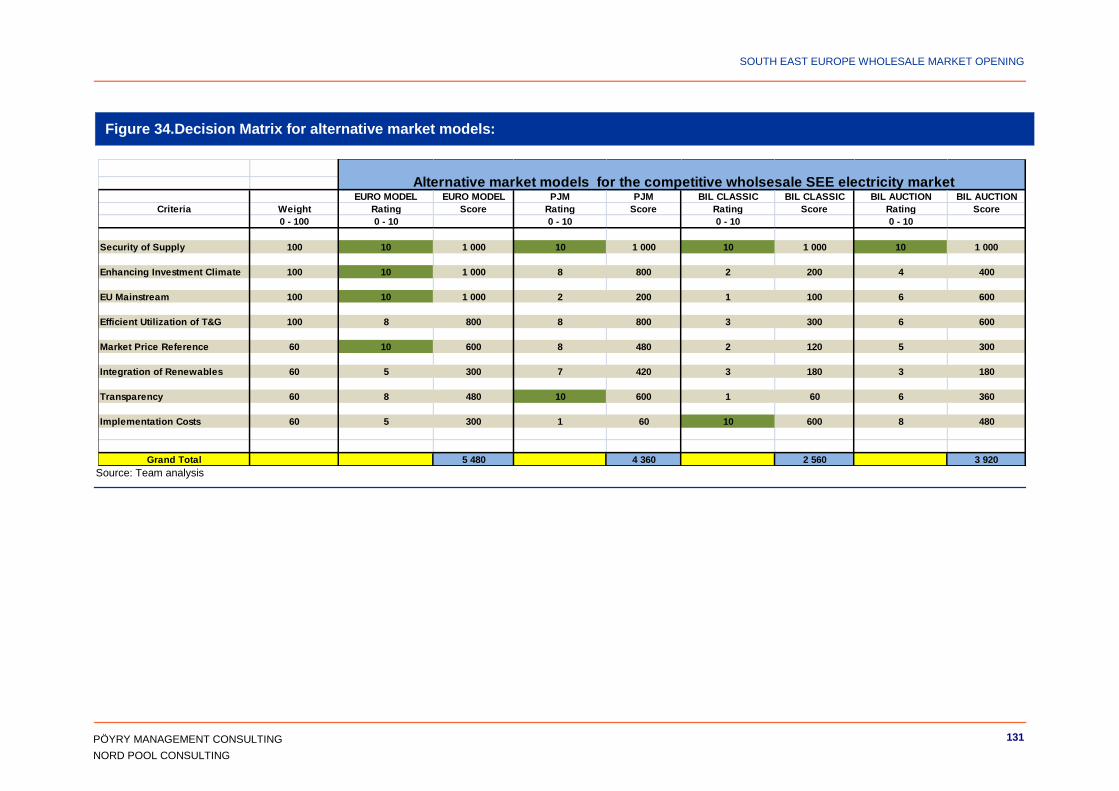

Choosing a specific reference market model as the key building block for a competitive wholesale SEE electricity market design, is probably the most crucial decision in the project as this will influence many other factors, such as cost of implementation, liquidity in the market place, and in the end it might decide whether the new regional market will be a success or not, measured in broader terms.

To assist in this choice, the Consultant has used a classical decision matrix, with criteria, options (four alternative models), weights for criteria (0 – 100), and ratings (0 – 10).

The four alternative models that have been assessed are:

The European Model (Euro Model)

PJM (Pennsylvania, Jersey, Maryland)

Bilateral Classic (existing market model for SEE)

Bilateral Auction (auction of contracts instead of negotiations)

The following criteria are used:

1. Security of Supply

2. Enhancing Investment Climate

3. EU Mainstream

4. Efficient Utilization of Transmission Grids and Generation

5. Market Price Reference

6. Integration of Renewables

7. Transparency

8. Implementation Costs

Criteria 1-4 are the primary ones given a weight of 100, while criteria 5-8 are secondary and given a weight of 60. Each of the models is evaluated against the chosen criteria.

SOUTH EAST EUROPE WHOLESALE MARKET OPENING

20

PÖYRY MANAGEMENT CONSULTING

NORD POOL CONSULTING

The following arguments are used for giving variable scores on how these models match the criteria:

Security of Supply:

Security of Supply is a focal point independent of the model chosen for the wholesale market. It has to be assumed that the necessary measures are taken by the TSOs to maintain the required level for security of supply whichever solution is implemented. Hence the rating is set to 10 (maximum) for all the options.

Enhancing Investment Climate

The Euro Model and PJM are given a high score, while the bilateral models are given a low score.

Investors in generation will also seek a location/market that will offer effective hedging instruments, which will be an effective tool to mitigate the financial risk to an acceptable level. Hedging instrument can range from long term bilateral contracts to liquid financial electricity contracts, where the latter might be the preferred option as it offers a much larger flexibility in adjusting positions in a portfolio

The reason for giving a score of 10 and 8 to the two former models respectively is that the Euro model is in line with the rest of Europe, and will offer especially European investors an alternative to investment in Western Europe. Bilateral market models are given a low score as they offer market places with less transparency and less liquidity, which represent a higher risk scenario to investors

EU Mainstream

The Euro Model is linked to the trends and development of the European electricity market and given the high score of 10.

Efficient Utilization of Transmission grids and Generation

The Euro model and PJM get the high score of 8 since both models provide a merit order use of generation and high utilization of transmission capacities. PJM provides more accurate locational signals through Locational Marginal Pricing (nodal pricing).

Market Price References

The Euro model gets the highest score of 10 as this design provides for the use of zonal rather then nodal market price references.

Integration of Renewables

Large scale integration of renewables is an increasing challenge to any market model worldwide. Different models are however likely to cope with the challenge of renewable and intermittent generation differently. In a future with large amount of renewable and intermittent generation the requirements on the system to handle large fluctuations in output and use of the grid will increase.

The PJM model combines an independent system operator with nodal prices with integrated markets for capacity and ancillary services. This may be a model that is better in handling large amount of renewable generation compared with the Euro model with national or zonal prices and a less strong link between spot markets and transmission companies (see e.g. ref [22]). With this background we have given the PJM model a score of 7, the Euro model a score of 5 and the two bilateral models a score of 3.

SOUTH EAST EUROPE WHOLESALE MARKET OPENING

21

PÖYRY MANAGEMENT CONSULTING

NORD POOL CONSULTING

Transparency

PJM is given the highest score of 10 as it provides more access to cost data for generation. Compared to the other models The Euro model is based on portfolio bidding into each bidding area which gives less transparency and also self dispatch of generation which might provide less information for TSOs entering into real-time operation

Implementation Costs

The bilateral classical model is given the highest score as it requires no major changes compared to the current operation in the SEE region. Experience indicates that the implementation of the PJM model is costly.

Summary assessment

Based on this assessment the Consultant recommends the Euro model market design for the SEE region.

The decision matrix is shown in Table 1.

SOUTH EAST EUROPE WHOLESALE MARKET OPENING

22

PÖYRY MANAGEMENT CONSULTING

NORD POOL CONSULTING

Table 1. Decision Matrix evaluating four alternative market models

EURO MODEL EURO MODEL PJM PJM BIL CLASSIC BIL CLASSIC BIL AUCTION BIL AUCTION

Alternative market models for the competitive wholsesale SEE electricity market

SOUTH EAST EUROPE WHOLESALE MARKET OPENING

23

PÖYRY MANAGEMENT CONSULTING

NORD POOL CONSULTING

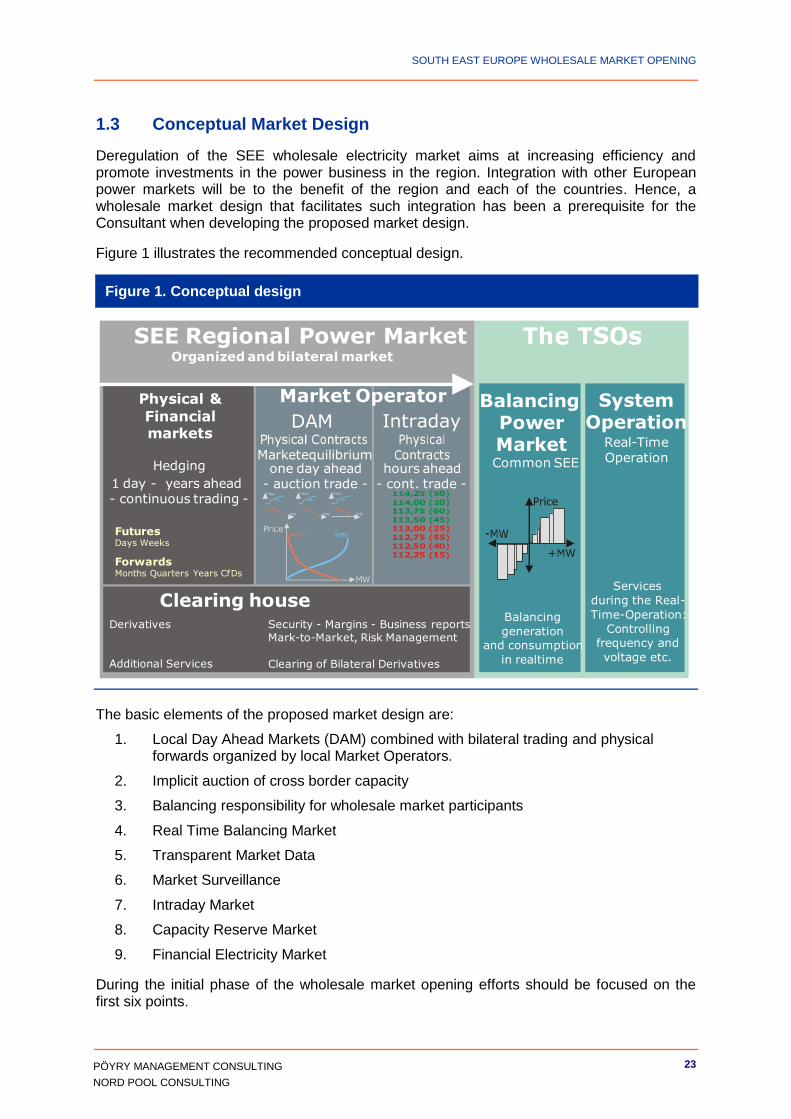

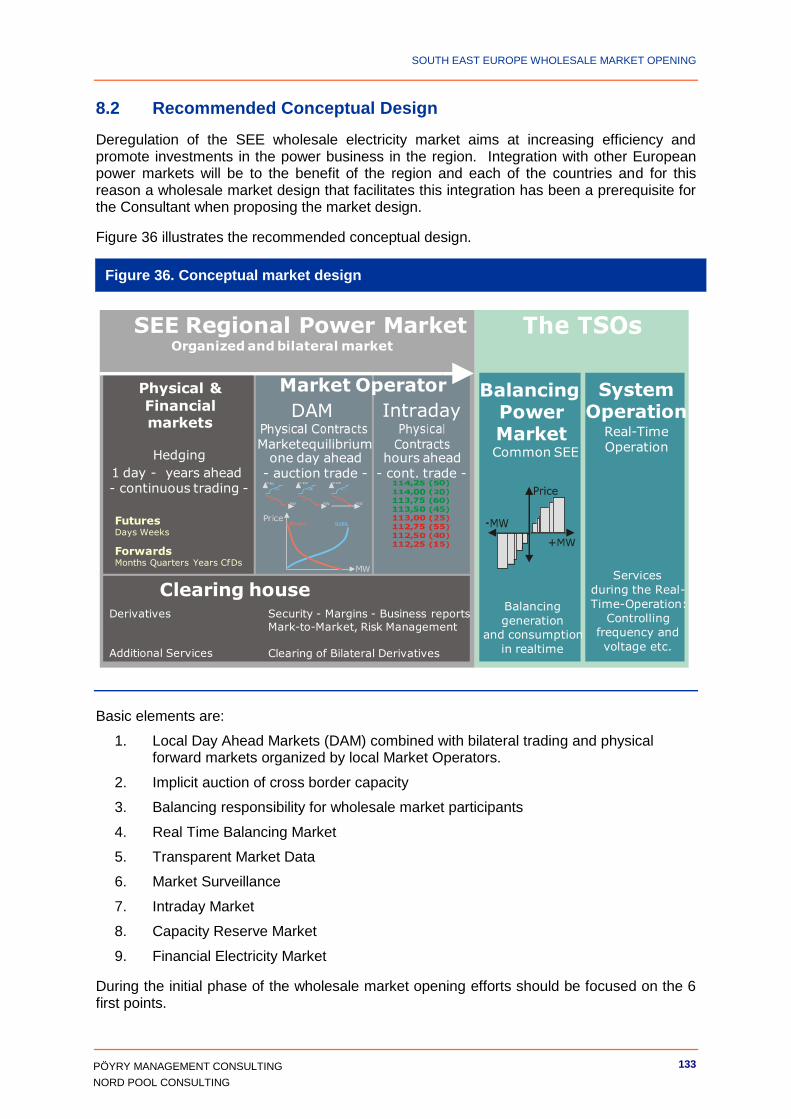

1.3 Conceptual Market Design

Deregulation of the SEE wholesale electricity market aims at increasing efficiency and promote investments in the power business in the region. Integration with other European power markets will be to the benefit of the region and each of the countries. Hence, a wholesale market design that facilitates such integration has been a prerequisite for the Consultant when developing the proposed market design.

Figure 1 illustrates the recommended conceptual design.

Figure 1. Conceptual design

The basic elements of the proposed market design are:

1. Local Day Ahead Markets (DAM) combined with bilateral trading and physical forwards organized by local Market Operators.

2. Implicit auction of cross border capacity

3. Balancing responsibility for wholesale market participants

4. Real Time Balancing Market

5. Transparent Market Data

6. Market Surveillance

7. Intraday Market

8. Capacity Reserve Market

9. Financial Electricity Market

During the initial phase of the wholesale market opening efforts should be focused on the first six points.

SEE Regional Power MarketOrganized and bilateral market

one day ahead- auction trade -

Derivatives

Additional Services

Security - Margins - Business reports

Mark-to-Market, Risk Management

Clearing of Bilateral Derivatives

Physical &

Financial markets

Clearing house

Market Operator

DAM

Marketequilibriumhours ahead

- cont. trade -

Hedging

1 day - years ahead- continuous trading -

Balancing

generation

and consumption

in realtime

Services

during the Real-

Time-Operation:

Controlling

frequency and

voltage etc.

BalancingPowerMarket

SystemOperation

Real-TimeOperation

Intraday

FuturesDays Weeks

ForwardsMonths Quarters Years CfDs

Common SEE

SOUTH EAST EUROPE WHOLESALE MARKET OPENING

24

PÖYRY MANAGEMENT CONSULTING

NORD POOL CONSULTING

A detailed description of the market design is given in Chapter 8 and 9.

This market concept will offer a number of advantages as it will expose market participants – generators and consumers – to market prices on marginal volumes from day one of market opening and thus provide for

Enhanced efficiency within generation; merit order in all jurisdictions

Improved utilization of cross border transmission capacities; hourly aligning cross border flows in the direction low to high area prices

Alleviating grids during peak hours through reduced withdrawal of flexible loads

Market price signals to be used for system (generation and transmission) expansion planning

High level market design elements:

Staged implementation of a regional wholesale market with respect to both participating jurisdictions and market functions

Parallel development of regional and local markets is a must as the high market concentration in each jurisdiction prevents the establishment of independent local markets.

A regional wholesale electricity market founded on a Day-Ahead Market (DAM) with local DAMs linked together through implicit auction

Flexible solutions for the local DAMs. Each jurisdiction decides which functions to implement on its own and which functions to purchase from a regional service provider.

Local Market Operators set up physical forward markets within their jurisdictions with local Incumbents as market makers.

Introduce transitional incentives for eligible consumers and public suppliers to source from the open market to promote and secure market liquidity. During the transitional period, volumes at a regulated and favourable price will be gradually reduced. The local authorities must decide on the duration of the transitional period. As the success of this design depends entirely upon sufficient volumes nominated at DAM (liquidity), political support is strongly recommended to

Incentivize eligible customers to nominate volumes at DAM

Ensure that public suppliers purchase parts of tariff customers‟ consumption from DAM

Make TSO purchase main grid losses from DAM

Eligible customers can be encouraged to trade at DAM in different ways.

Local markets that allow eligible customers to stay under regulated prices can negotiate special base load contracts – with reduced volumes year by year - for eligible customers if they accept to take the remaining volumes from DAM. In this way eligible customers will have predictability over the transitional period

Local markets that have decided to exclude eligible customers from tariff prices, but experience that competition is not working - might as well offer base load contracts to eligible customers given that they take remaining volumes from DAM.

The most important decision to secure DAM volumes will be to cancel full supply contracts between incumbents and public suppliers serving tariff customers. Full supply contracts prevent volumes to come to the market. They should be replaced by base load contracts covering a certain share of tariff customers‟ yearly energy consumption. Volumes will be reduced year by year based on political

SOUTH EAST EUROPE WHOLESALE MARKET OPENING

25

PÖYRY MANAGEMENT CONSULTING

NORD POOL CONSULTING

considerations. The remaining part of tariff customers‟ load should be purchased by public suppliers from DAM

Specific design elements:

Balancing /Ancillary /Reserve markets

Balancing Responsibility for wholesale market participants. This will provide the market participants an incentive to trade into balance before entering real-time operations

Day-Ahead Market and allocation of cross border capacities. It is assumed that the Coordinating Auction Office (CAO), on behalf of the TSOs, calculates the cross-border capacities to be allocated.

Physical forward markets, organized and bilateral

Financial forward markets, organized and bilateral

Linking neighbouring markets to the regional SEE market

Generic design considerations

Promote competition between organized markets and bilateral trade

Ownership and governance of regional and local market entities

Sustaining the current arrangement of providing electricity at favourable tariffs to vulnerable customers

Allow local incumbents to expand beyond domestic markets in the SEE region, rather than splitting up these companies as they are rather small measured in revenue or TWh compared to the 20 largest generators in the European market.

Enhancement in regional investment climate for new generation. A regional open wholesale market linking SEE to a pan European electricity market, will secure the investors transparency in market data and confidence in market prices

Flexibility through hourly DAM contracts for generators and consumers

A Generator will, through his access to DAM, at any time have incentive to reduce his production if DAM offers cheaper power. Consumers with flexible load will in the same way have incentive to reduce marginal demand (controllable load) during periods with very high prices. In this way all generation, consumption and transmission will “adapt” to market prices throughout the SEE region based on bid/offers of marginal volumes in the open market

SOUTH EAST EUROPE WHOLESALE MARKET OPENING

26

PÖYRY MANAGEMENT CONSULTING

NORD POOL CONSULTING

1.4 Business Processes

The Consultant recommends a decentralized design.

Each Contracting Party (CP) has its own Local Market Operator (LMO);

Each market participant has an agreement with his Local Market Operator;

All bidding, settlement, collateral and participant agreements are made between the market participant and the Local Market Operator;

The Local Market Operator will collect and validate all bids from its participants and creates one Net Export Curve (NEC) combining all the bids from its market participants into one aggregated bid curve (thereby anonymous) that is sent to the SEE Market Service Provider (SEESP) acting on behalf of the Regional PX;

SEE Market Service Provider will collect the Net Export Curves from all Local Market Operators, and will get Available Transmission Capacities (ATC) for all interconnections from the CAO. Based on these data, the SEE Market Service Provider will calculate a common price index for all areas and price for all individual areas as well as the flow on each interconnection. These values will be returned to the LMOs;

Local Market Operators will have a service agreement with the SEE Market Service Provider for the price calculation as well as with the CAO for the allocation of ATCs to be utilized for DAM;

Prices and volumes for each market participant are calculated by the Local Market Operators.

This design is based on Price Market Coupling.

The business process overview is illustrated in the figure below and discussed in details in chapter 9:

Figure 2 Business process overview

SOUTH EAST EUROPE WHOLESALE MARKET OPENING

27

PÖYRY MANAGEMENT CONSULTING

NORD POOL CONSULTING

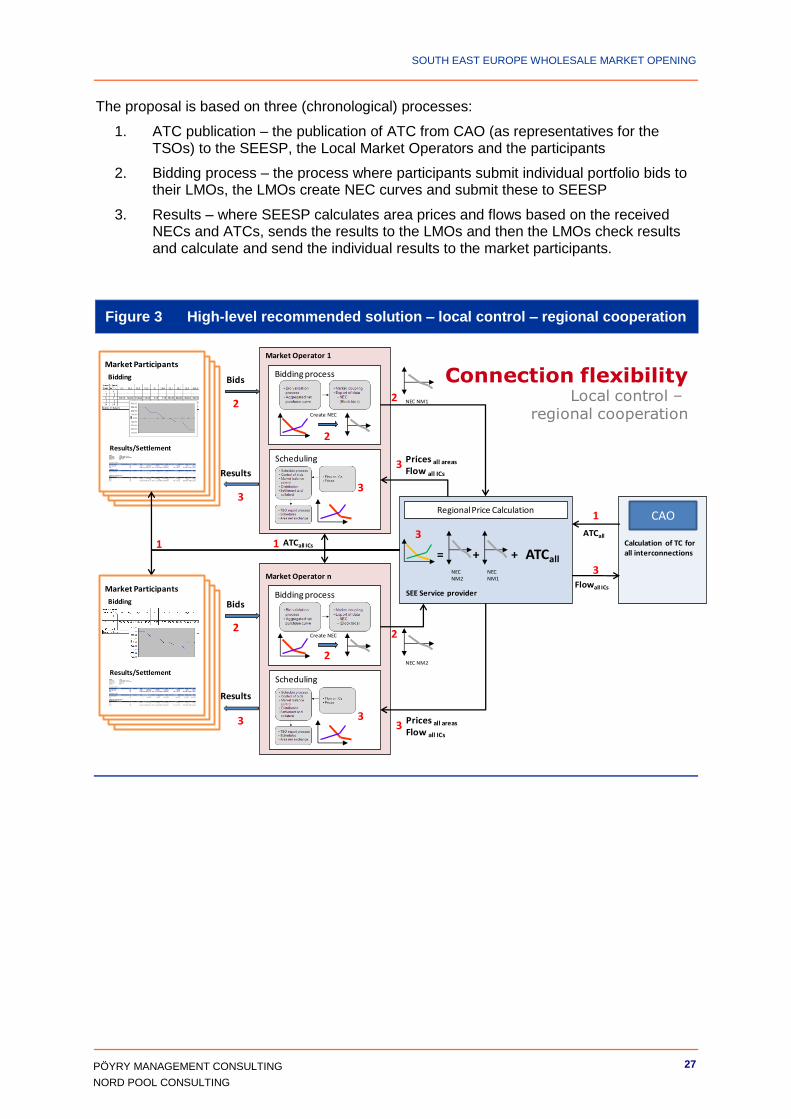

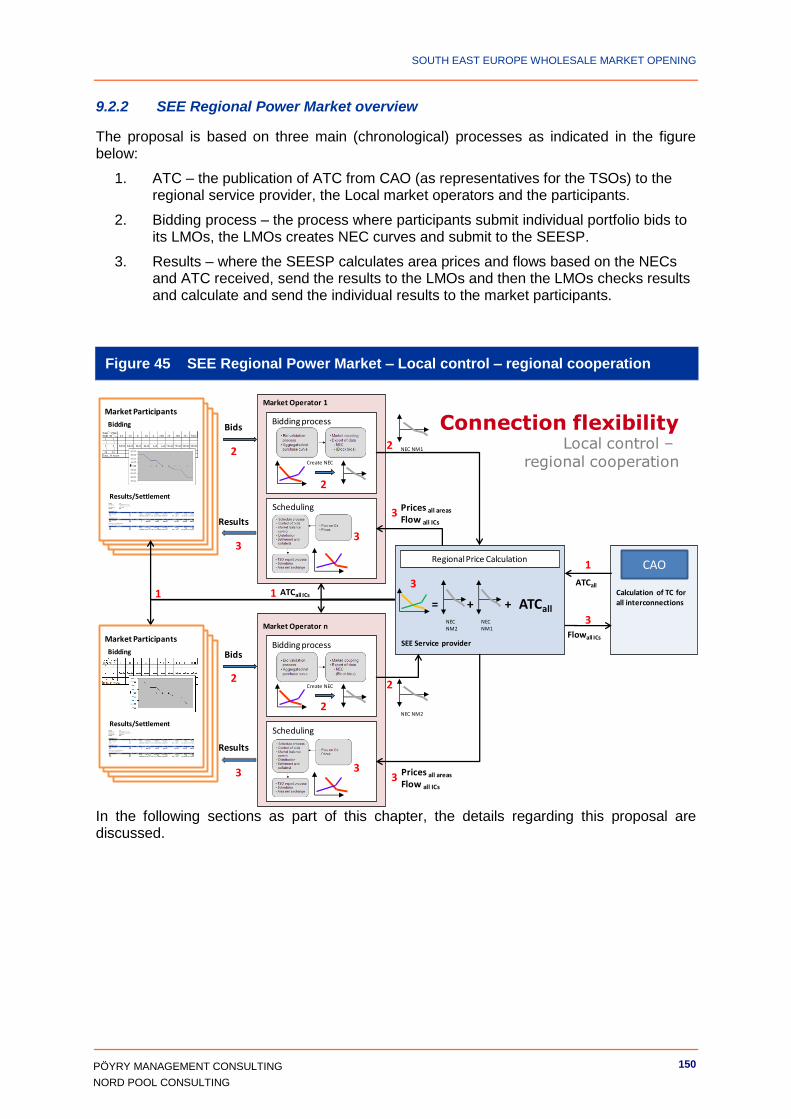

The proposal is based on three (chronological) processes:

1. ATC publication – the publication of ATC from CAO (as representatives for the TSOs) to the SEESP, the Local Market Operators and the participants

2. Bidding process – the process where participants submit individual portfolio bids to their LMOs, the LMOs create NEC curves and submit these to SEESP

3. Results – where SEESP calculates area prices and flows based on the received NECs and ATCs, sends the results to the LMOs and then the LMOs check results and calculate and send the individual results to the market participants.

Figure 3 High-level recommended solution – local control – regional cooperation

Market Participants

Bidding

Results/Settlement

NEC NM2

Regional Price Calculation

SEE Service provider

=NEC NM2

+ + ATCall

ATCall

Flowall ICs

Calculation of TC for all interconnections

CAO

Market Operator 1

Scheduling

Bidding process

Create NEC

Bids

ATCall ICs

Prices all areas

Flow all ICsResults

Market Operator n

Scheduling

Bidding process

Create NEC

Bids

Results

NEC NM1

Prices all areas

Flow all ICs

Market Participants

Bidding

Results/Settlement

NEC NM1

Connection flexibilityLocal control –

regional cooperation

1

1

1

2

2

2

2

3

3

3

3

3

3 3

3

2

2

SOUTH EAST EUROPE WHOLESALE MARKET OPENING

28

PÖYRY MANAGEMENT CONSULTING

NORD POOL CONSULTING

1.5 Integration with Neighbouring Markets

A liquid SEE wholesale market coupled to other European power markets with the same trading regimes will soon establish a reliable and trustworthy price reference for the region and attract investors.

Implicit auctions will link local SEE DAMs to neighbouring DAMs. Transitional solutions with reservation of minor cross border capacities for explicit auctions might be required.

Exchange with neighbouring countries with no DAM will run like today, based on explicit auction and bilateral trade.

Imbalance handling and settlements must be harmonized according to common rule books.

Integration of European spot power markets made a big step forward when The power exchanges APX-Endex, Belpex, EPEX Spot, GME, Nord Pool Spot, and OMEL March 18th this year announced the creation of a six party project aimed at delivering a single price coupling across the Nordic, Central West and Southern European regions, potentially as early as next year. The Price Coupling of Regions (PCR) project will address the implementation of a common price coupling solution through which spot electricity price formation will be coordinated in an area potentially covering approximately 2,900 TWh per year of power consumption. The initiative is open to other power exchanges and market areas joining on fair and equal terms and represents a development towards a truly integrated European spot market for electricity.

1.6 Transition phase: From regulated prices to market prices

Exposing eligible customers fully to market prices from day one of the wholesale market opening process will meet hindrance in most countries due to uncertain market prices and their volatility. For this reason transitional schemes should be considered. The need for such schemes will vary across the region, because each jurisdiction has a different starting point.

Some countries have already taken steps to expose eligible customers to market prices. In general a transition period with steadily decreasing contract volumes supplied at regulated prices is recommended to gain acceptance among market participants. This solution is illustrated in the figure below.

SOUTH EAST EUROPE WHOLESALE MARKET OPENING

29

PÖYRY MANAGEMENT CONSULTING

NORD POOL CONSULTING

Figure 4 Transitional period – market and regulated prices – Eligible Consumers

Incentive contracts should be established prior to market opening as an offer to eligible customers. This will give them the necessary predictability and they will respond to market prices from day one. They can profit from reducing consumption during peak prices.

During the transition phase – or in general in market opening - the challenge is to establish sufficient volumes (liquidity) on the DAM. It is therefore important that the demand side bid for volumes themselves.

Full Supply Contracts - meaning that the customer can consume any quantity at a fixed contract (tariff) price - between Generators and customers are the greatest obstacle to DAM liquidity. In this situation the Generator will give a net bid on the DAM and purchasing volumes will be very low.

Full Supply Contracts between Public Suppliers and customers, on the other hand, can be accepted as long as the Supplier purchases additional volumes on the market and consequently pays market price for marginal volumes.

Base load contracts between Generators and Public Suppliers to serve Tariff Customers will bring remaining volumes from the demand side on the market.

The following figures illustrate how this design works.

SOUTH EAST EUROPE WHOLESALE MARKET OPENING

30

PÖYRY MANAGEMENT CONSULTING

NORD POOL CONSULTING

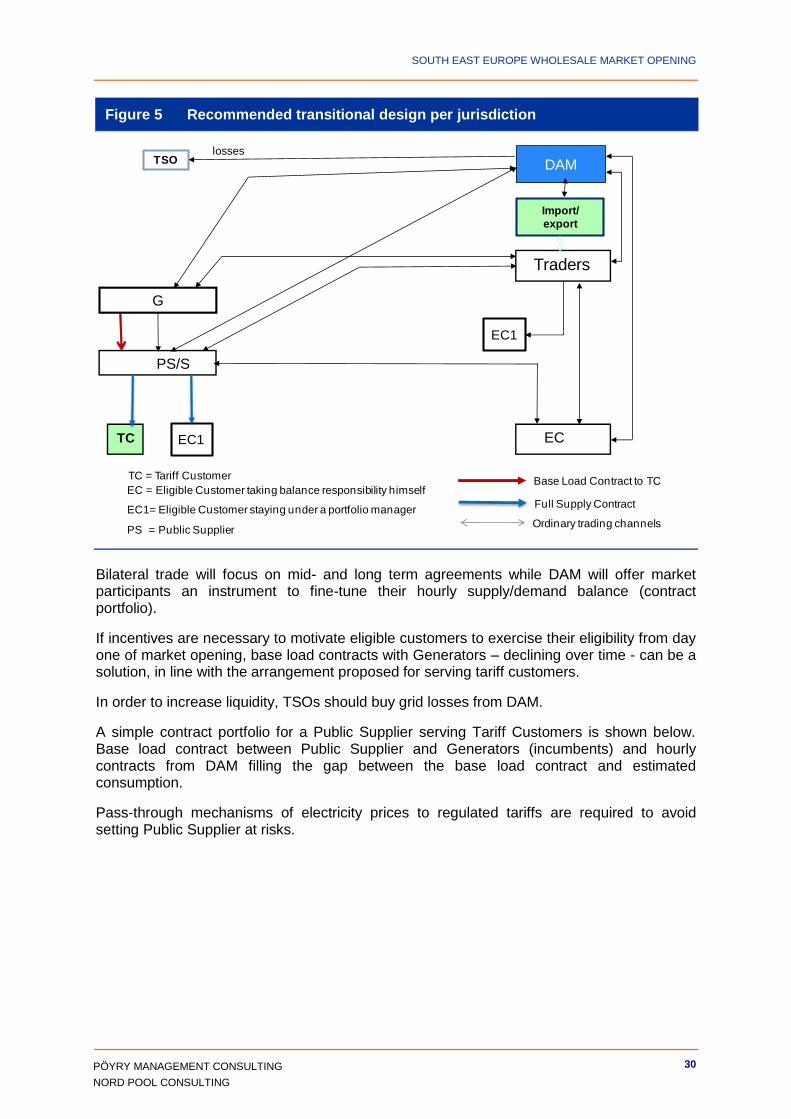

Figure 5 Recommended transitional design per jurisdiction

Bilateral trade will focus on mid- and long term agreements while DAM will offer market participants an instrument to fine-tune their hourly supply/demand balance (contract portfolio).

If incentives are necessary to motivate eligible customers to exercise their eligibility from day one of market opening, base load contracts with Generators – declining over time - can be a solution, in line with the arrangement proposed for serving tariff customers.

In order to increase liquidity, TSOs should buy grid losses from DAM.

A simple contract portfolio for a Public Supplier serving Tariff Customers is shown below. Base load contract between Public Supplier and Generators (incumbents) and hourly contracts from DAM filling the gap between the base load contract and estimated consumption.

Pass-through mechanisms of electricity prices to regulated tariffs are required to avoid setting Public Supplier at risks.

G

PS/S

Traders

TC EC

TC = Tariff Customer

EC = Eligible Customer taking balance responsibility himself

EC1= Eligible Customer staying under a portfolio manager

PS = Public Supplier

PEXDAMTSO

EC1

Import/

export

losses

EC1

Base Load Contract to TC

Full Supply Contract

Ordinary trading channels

SOUTH EAST EUROPE WHOLESALE MARKET OPENING

31

PÖYRY MANAGEMENT CONSULTING

NORD POOL CONSULTING

Figure 6 Public Supplier with trading portfolio for Tariff Customers

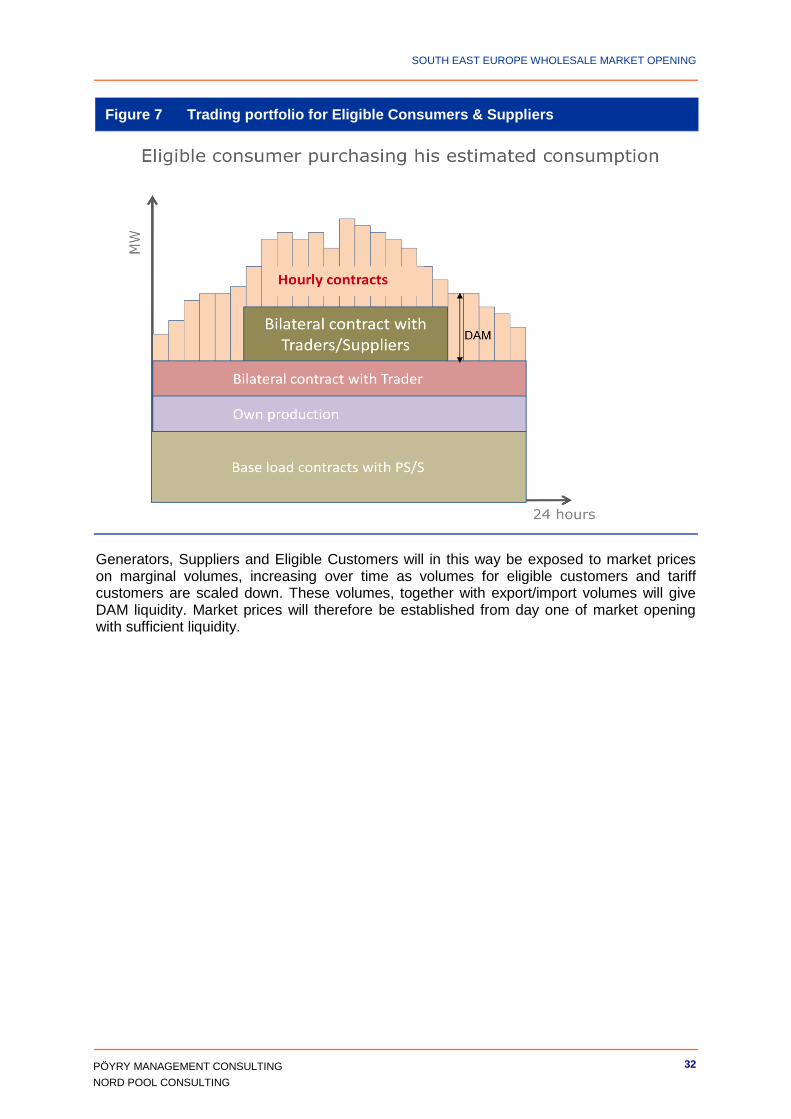

Traders, Eligible Customers and Suppliers will in general have a more complex contract portfolio, established over time in order to minimize cost, but the principles are the same. Hourly contracts from DAM fill the gap between contracted volumes and estimated load. They “trade into balance”.

Deviations from expected load will be handled on the imbalance market – or later when implemented – on the intraday market. The structure of such a contract portfolio is illustrated below.

SOUTH EAST EUROPE WHOLESALE MARKET OPENING

32

PÖYRY MANAGEMENT CONSULTING

NORD POOL CONSULTING

Figure 7 Trading portfolio for Eligible Consumers & Suppliers

Generators, Suppliers and Eligible Customers will in this way be exposed to market prices on marginal volumes, increasing over time as volumes for eligible customers and tariff customers are scaled down. These volumes, together with export/import volumes will give DAM liquidity. Market prices will therefore be established from day one of market opening with sufficient liquidity.

SOUTH EAST EUROPE WHOLESALE MARKET OPENING

33

PÖYRY MANAGEMENT CONSULTING

NORD POOL CONSULTING

1.7 CAO – Coordinated Auction Office

As described in chapter 2.7, when a well-functioning DAM for the whole region is in place, all available transmission capacity should be made available for the implicit auction. This implies that in the final solution, long-term transmission capacity auctions will not be needed. For the SEE Regional Power Market the main function of the CAO is to provide correct transmission capacities to the market independent of the market concept.

The following simplified diagram is an illustration of the co-existence of CAO and a SEE Regional Power Market:

Figure 8 CAO functions in the Regional PX

Dedicating cross border capacity to the SEE Regional Power Market is an essential policy decision in order to establish a Regional PX. The CAO will be responsible for determining tradable cross border capacities, performing explicit auctions and providing the Regional PX with daily capacities for the implicit auction. In this way the two concepts mutually support each other.

It is important to stress that explicit and implicit auctions cannot be efficiently implemented on the same electrical borders in the Day-ahead time frame.

A regional balance management concept (BETSEE - Balancing Energy Tool in the SEE) is under consideration among SEE TSOs. This will be a useful instrument to handle imbalances, but it should use free transmission capacity (not allocated) only. Reservation of cross border capacities for balancing purposes will necessarily reduce DAM liquidity. DAM liquidity is the number one requirement when opening the regional wholesale market.

Intraday/

Balancing Mechanism

Long-term auction

(year,quarter,

month, week)(Y% available)

Transfer to DAM(Use It Or Get Paid)(Z)

DAM utilization(TCDAM )

CAO Explicit auctions Day-ahead implicit auction

Calculation of available transmission capacity for DAM implicit auction

(performed at 10:00 D-1):

TCDAM= D + rest of Y + Z + released portion of X

in both directions

The remaining capacity after DAM is available for Intra-day trading

Security margin(X% margin)

DAM reservation(D% reserved)

TSO allocations

SOUTH EAST EUROPE WHOLESALE MARKET OPENING

34

PÖYRY MANAGEMENT CONSULTING

NORD POOL CONSULTING

1.8 VPP Auctions, Bilateral Auctions and Physical Forward Markets arranged by the Local Market Operators

A VPP (Virtual Power Plant) auction is a mandatory auction of generation capacity in order to mitigate incumbents‟ dominant market position. The buyer gets a contract (base or peak) at auction price, but the owner of the VPP operates the plant independently of how the buyer nominates capacity from the plant.

The proposed market solution implies that incumbents serve tariff customers through a base load contract with the public suppliers.

Such a contract reduces incumbents‟ dominant market position in the same way as VPP auctions. The only difference is that prices are set differently.

For this reason, the Consultant does not see the need for VPP auctions from day one of market opening. VPP auctions might be considered later when downsizing of volumes for tariff customers has “strengthened” incumbents‟ potential dominant market position.

VPP Auctions serve however other important missions: They bring transparency to the forward market and offer hedging instruments to market participants.

Auctioning of bilateral contracts brings transparency, but volumes are not guaranteed unless local authorities come up with special regulations.

A market based solution which combines transparency and (minimum) liquidity is much to prefer rather than mandatory schemes. The Consultant recommends a solution in which local Market Operators set up physical forward markets within their jurisdictions with local Incumbents as market makers.

Physical forward markets will soon be changed into financial forwards as this is a much more flexible solution. This process will be driven by market participants.

1.9 Gap Analysis

The restructuring of the local electricity markets has already been initiated. The required unbundling of transmission and generation is completed, while needed transparency of i.e. market information and competition are far from satisfactorily and clearly lagging behind the development in the rest of Europe.

The table below summarizes the gap analysis for all jurisdictions (further details given in Chapter 10).

The gap analysis clearly indicates that major changes have to be implemented if a market opening is going to be successful. This is reflected in the action plans.

.

SOUTH EAST EUROPE WHOLESALE MARKET OPENING

35

PÖYRY MANAGEMENT CONSULTING

NORD POOL CONSULTING

Table 2. Summary of gap analysis

TSO Unbundling

Supplier Unbundling

Eligibility Balance Responsibility, Mechanisms

Market Concentration

Transparency Establishment of DAM

Albania

BiH

Croatia

FYROM

Montenegro

Serbia

UNMIK

Bulgaria

Romania

Ukraine

Moldova

Legend: green = no gap, yellow = minor gap, red = large gap, green +yellow and yellow +red indicate in between gaps

SOUTH EAST EUROPE WHOLESALE MARKET OPENING

36

PÖYRY MANAGEMENT CONSULTING

NORD POOL CONSULTING

1.10 Action Plans

Complete regional and local action plans are given in chapter 10.

It has been stipulated in the action plans that the opening of the wholesale electricity market can be achieved by January 2012. It is important to note that the implementation entails parallel activities at local and regional level. Due to large incumbents in most of the jurisdictions no local market can exist on its own, but only through the co-existence with other local markets forming a regional SEE electricity market.

A bilateral market will operative side by side with an organized DAM. When the market price in a DAM has gained the necessary trust and recognition, a financial electricity mid- and long-term market can offer trade in derivatives with reference to local and regional market price indices.

The completion of these changes in wholesale market operations should be completed by January 2015. The latter is according to the Energy Treaty agreement signed by all contracting parties

1.10.1 Regional Action Plan

The regional action plan contains the following summary activities:

Review and Acceptance of Market Design

It is estimated that the review of the final report and the acceptance of the proposed market design for the SEE wholesale market can be completed by June 30th 2010.

Project Establishment

Following the acceptance of the market design the regional project can be initiated with the following actions:

Select Regional Project Manager (PM)

Establish detailed project plan, budget, and financing plan for SEE Wholesale Electricity Market Opening project

Approve project plans, budget and financing

Appoint project members from each CP/Stakeholder to form the Regional Project Team

Arrange kick-off meeting at the end of August 2010

Regional Activities

It is recommended that the project is organized as part of the EC/Athens Forum process and that the PM reports status to ECRB/PHLG four times annually

SOUTH EAST EUROPE WHOLESALE MARKET OPENING

37

PÖYRY MANAGEMENT CONSULTING

NORD POOL CONSULTING

Legal

A number of agreements have to be negotiated at the regional level. This will entail at least the following:

Agreement Regional Market Operator – Regulators for Contracting Parties

Agreement Regional Market Operator - TSOs for Contracting Parties

Agreement Regional Market Operator - Market Operators for Contracting Parties

The regional entity has been termed Regional Market Operator. This can be established as an agreement only between participating contracting parties. Alternatively a more formal legal entity can be incorporated being the legal counterparty to market operators in all Contracting Parties.

Establish wholesale SEE regional market frameworks and detailed design

Based on the accepted SEE market design and relevant EU directives and regulations, the frameworks and detailed specification for the SEE regional market must be established

Coordinate project activities in Contracting Parties

The Regional Project will be responsible for coordinating the activities including the necessary harmonization of market and grid codes in each Contracting Party

Procurement/Implementation/Installations/Testing of Regional IT systems

This activity must be coordinated with a similar activity for each of the local markets.

Trials and Operations Regional DAM

Regional Market Trials must be run prior to going live with DAM trades. This will be a common activity involving the participating market operators and stakeholders in all the Contracting Parties, Bulgaria and Romania

Go Live SEE Regional Power Market (DAM)

It is stipulated that the Regional DAM can go live January 2012.

Physical/Financial Forward Electricity Market

As soon as a DAM price is established, financial electricity products should be offered in line with requirements from all local participants and international traders.

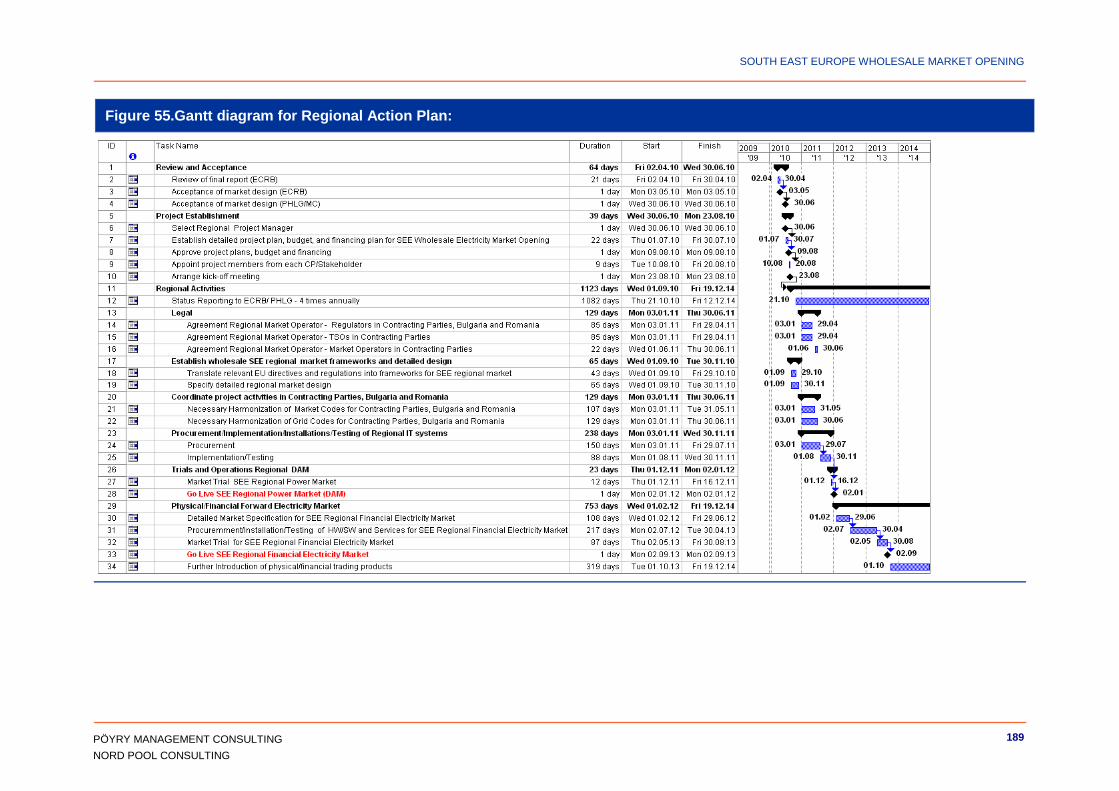

On the next page is shown a detailed Gantt diagram for the regional project. The duration of this project will span from start–up in mid 2010 to the end of 2014.

SOUTH EAST EUROPE WHOLESALE MARKET OPENING

38

PÖYRY MANAGEMENT CONSULTING

NORD POOL CONSULTING

Figure 9 SEE Wholesale Market opening – Initial setup

Impl. auction

Preparing for impl.

auction

Explicit auction

HU

Candidates

MD

UKR

SOUTH EAST EUROPE WHOLESALE MARKET OPENING

39

PÖYRY MANAGEMENT CONSULTING

NORD POOL CONSULTING

Figure 10.Gantt diagram for Regional Action Plan:

SOUTH EAST EUROPE WHOLESALE MARKET OPENING

40

PÖYRY MANAGEMENT CONSULTING

NORD POOL CONSULTING

1.10.2 LOCAL ACTION PLANS

In chapter 10, specific local action plans are developed for each jurisdiction taking into account the gap analysis, where it is documented the deviations between minimum requirements for participating in an open wholesale market and the current status in each jurisdiction.

The list of decisions is tailor made for each jurisdiction within the following areas:

TSO Unbundling

Supplier Unbundling

Eligibility

Balance Responsibility and Balance Mechanism

Market Concentration

Transparency

Establishment of DAM

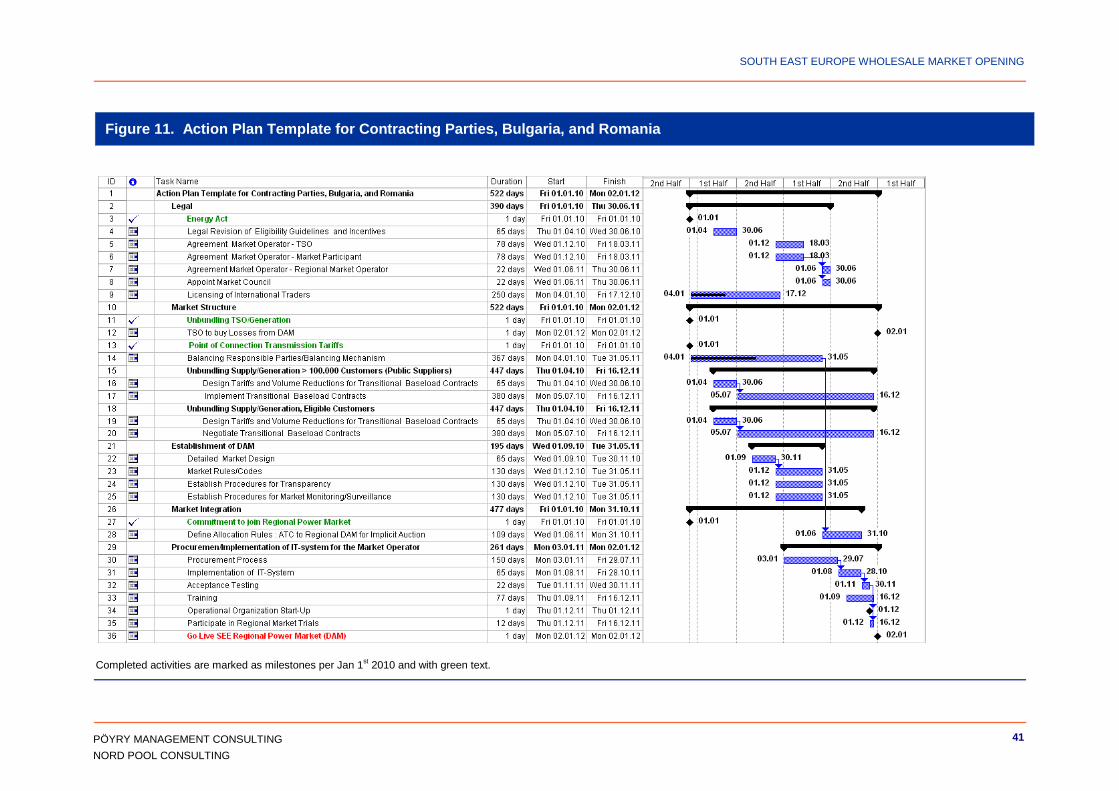

A template Gantt diagram for the local action plans is presented in Figure 11.

SOUTH EAST EUROPE WHOLESALE MARKET OPENING

41

PÖYRY MANAGEMENT CONSULTING

NORD POOL CONSULTING

Figure 11. Action Plan Template for Contracting Parties, Bulgaria, and Romania

Completed activities are marked as milestones per Jan 1st 2010 and with green text.

SOUTH EAST EUROPE WHOLESALE MARKET OPENING

42

PÖYRY MANAGEMENT CONSULTING

NORD POOL CONSULTING

1.10.3 Dry run

A dry run serves several different purposes:

simulate a regional competitive market;

train market participants;

simulate different market setup scenarios.

Prior to market opening such exercises will prepare market participants and facilitate a smooth market opening. The idea is to simulate a DAM through bids and offers from Generators, Suppliers, Traders and Eligible Customers.

Cross border capacities and base load contracts to serve tariff customers have to be allocated. In order to simulate the effect of electricity exchange with neighbouring countries, existing bilateral contracts may be represented by price independent bids in the relevant bidding areas. The DAM simulator will calculate area prices and flows on interconnections.

Training of market participants can go on until real market opening takes place and even beyond to familiarize new market entrants. Simulations of future market development will be ongoing activities.

1.10.4 Action plans – market participants

Generators, Suppliers, Traders and Eligible Customers all have to establish new operational working routines in order to handle new market opportunities and challenges. Long and short term power price variations call for hedging strategies. This will be a core business for Traders, Generators and Suppliers. Eligible Customers will choose different solutions. Large industries could develop their own trading skill (figure below) while small enterprises could buy portfolio management services – including imbalance management - or stay at a market based contract price (fixed or variable).

Illustration of a big industrial customer‟s possible organization of power sourcing after establishment of a DAM is shown in Figure 13 below.

SOUTH EAST EUROPE WHOLESALE MARKET OPENING

43

PÖYRY MANAGEMENT CONSULTING

NORD POOL CONSULTING

Figure 12 Power sourcing on a liberalized market – example for Industry

A condensed overview of new tasks for market participants is given below.

Figure 13 Action Plans for different types of Wholesale Market Participants

Generators and big Suppliers will need this competence in-house. Eligible Customers can outsource power procurement, balancing and trading in different ways as discussed above.

SOUTH EAST EUROPE WHOLESALE MARKET OPENING

44

PÖYRY MANAGEMENT CONSULTING

NORD POOL CONSULTING

SECTION II: BACKGROUND

SOUTH EAST EUROPE WHOLESALE MARKET OPENING

45

PÖYRY MANAGEMENT CONSULTING

NORD POOL CONSULTING

[This page is intentionally blank]

SOUTH EAST EUROPE WHOLESALE MARKET OPENING

46

PÖYRY MANAGEMENT CONSULTING

NORD POOL CONSULTING

2. THE CURRENT STATE OF MARKET OPENING IN SEE REGIONAL ELECTRICITY MARKET

2.1 Introduction

The following sections set out a quantitative summary of the regional electricity sector under the following topics:

electricity generation and demand;

electricity imports and exports;

market structure and market model; and

prices and tariffs.

Pöyry makes long range electricity and gas market price projections for the region, with the exception of for Ukraine and Moldova, as part of its pan-European market modelling, designed for use by investors in project evaluation, and updated quarterly. Data items with a source labelled "Pöyry EurECa3 analysis" are based on this modelling work. No modelling work has been made explicitly for this project, but we have drawn on results from other studies.

The statistical information in this section sets out a background which emphasises the need for:

efficient dispatch and cross-border trading arrangements between the Parties and with the surrounding countries;

increases in consumer tariffs to economically efficient levels, which will lead to a reduction in inefficient patterns of electricity consumption,

improved levels of payment for electricity; and

very high levels of investment in generation and network infrastructure.

The necessary investment, reduction in inefficient consumption and improvements in the efficiency of generation production can only realistically take place with a move to market-based (marginal) wholesale pricing and regional coordination.

2.2 Electricity generation and demand

Small, but growing, local markets4

Figure 14 shows that the size of the markets, in terms of final energy consumption, varies widely, but also that most of the markets are small. The smallest market in energy terms is UNMIK with a final electricity consumption of 3.2 TWh (2005), closely followed by Albania, Montenegro and Moldova. The largest is Ukraine with a final electricity consumption of 123.1 TWh (2005), followed by Serbia with 25.6 TWh (2005). The final electricity consumption in

3 EurECa is the name given to Pöyry‟s pan-European electricity model. 4 2005 data from IEA has been used to ensure cross-jurisdiction consistency. Later IEA

data does not provide data for all Contracting Parties. A comparison with 2007 data indicates that the regional electricity consumption has increased by approximately 15% between 2005 and 2007. Although there are differences in the consumption growth between countries the overall pattern remains unchanged.

SOUTH EAST EUROPE WHOLESALE MARKET OPENING

47

PÖYRY MANAGEMENT CONSULTING

NORD POOL CONSULTING

Ukraine is then five times as large as in Serbia, as the second largest country, and close to 40 times as large as in UNMIK, the smallest country. Network losses5 are generally quite large ranging from 14% in Croatia, up to 37% in UNMIK, with an average of 21%. The electricity consumption is expected to grow rapidly over the coming years, which implies significant requirements on new generation investments.

Figure 14. Final electricity consumption and network losses (2005) and expected consumption year 2015, TWh

Source: Energy in the Western Balkans, IEA 2008; Eurostat for Bulgaria and Romania; Pöyry EurECa analysis, Energy strategy of Ukraine til 2030, Moldova and Transnistria statistics

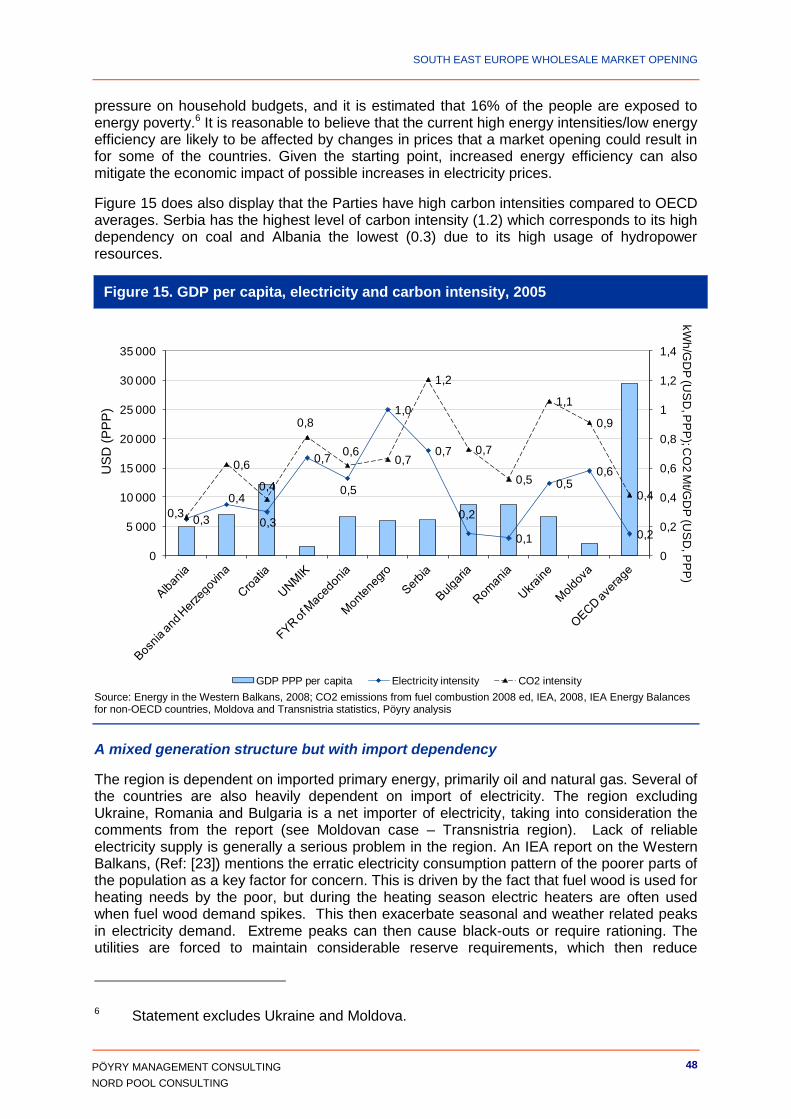

High energy intensities – low energy efficiency

The economies in the region generally have high energy intensities. As is displayed in Figure 15 below, energy intensities are considerably higher than the average OECD level ref [23]. This is explained by the degraded state of energy infrastructure, high energy losses in transformation, transmission and distribution and inefficiency in the end-use sector. The high network losses shown in Figure 15 are an illustration of this.

The energy intensities of Montenegro is a bit misleading in the figure as a large portion (approximately 40%) of the electricity is used by an aluminium plant, KAP.

Croatia has relatively high energy efficiency, but according to IEA (ref [23] the jurisdiction still has an energy savings potential of around 25% of the total primary energy supply. The region as a whole could save 13.4 TWh annually by bringing losses down to the level of Croatia. At the same time high energy prices and high energy consumption put a significant

5 Including transmission and distribution technical losses and commercial losses.

pressure on household budgets, and it is estimated that 16% of the people are exposed to energy poverty.6 It is reasonable to believe that the current high energy intensities/low energy efficiency are likely to be affected by changes in prices that a market opening could result in for some of the countries. Given the starting point, increased energy efficiency can also mitigate the economic impact of possible increases in electricity prices.

Figure 15 does also display that the Parties have high carbon intensities compared to OECD averages. Serbia has the highest level of carbon intensity (1.2) which corresponds to its high dependency on coal and Albania the lowest (0.3) due to its high usage of hydropower resources.

Figure 15. GDP per capita, electricity and carbon intensity, 2005

Source: Energy in the Western Balkans, 2008; CO2 emissions from fuel combustion 2008 ed, IEA, 2008, IEA Energy Balances for non-OECD countries, Moldova and Transnistria statistics, Pöyry analysis

A mixed generation structure but with import dependency

The region is dependent on imported primary energy, primarily oil and natural gas. Several of the countries are also heavily dependent on import of electricity. The region excluding Ukraine, Romania and Bulgaria is a net importer of electricity, taking into consideration the comments from the report (see Moldovan case – Transnistria region). Lack of reliable electricity supply is generally a serious problem in the region. An IEA report on the Western Balkans, (Ref: [23]) mentions the erratic electricity consumption pattern of the poorer parts of the population as a key factor for concern. This is driven by the fact that fuel wood is used for heating needs by the poor, but during the heating season electric heaters are often used when fuel wood demand spikes. This then exacerbate seasonal and weather related peaks in electricity demand. Extreme peaks can then cause black-outs or require rationing. The utilities are forced to maintain considerable reserve requirements, which then reduce

6 Statement excludes Ukraine and Moldova.

0,3

0,4

0,3

0,7

0,5

1,0

0,7

0,2

0,1

0,50,6

0,2

0,3

0,6

0,4

0,8

0,60,7

1,2

0,7

0,5

1,1

0,9

0,4

0

0,2

0,4

0,6

0,8

1

1,2

1,4

0

5 000

10 000

15 000

20 000

25 000

30 000

35 000

kW

h/G

DP

(US

D, P

PP

); CO

2 M

t/GD

P (U

SD

, PP

P)

US

D (

PP

P)

GDP PPP per capita Electricity intensity CO2 intensity

SOUTH EAST EUROPE WHOLESALE MARKET OPENING

49

PÖYRY MANAGEMENT CONSULTING

NORD POOL CONSULTING

potentials for exports and revenues. Low tariffs and payment discipline also limit the revenues.

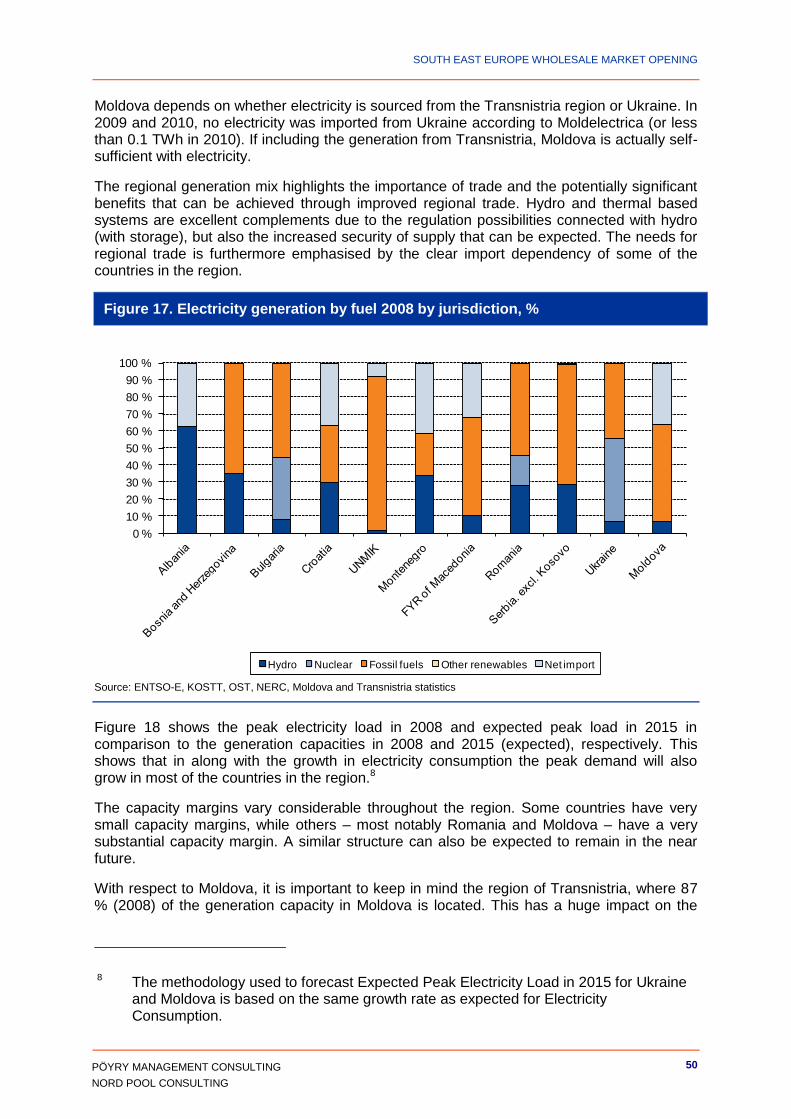

The total electricity generation in the region7 is a mix between conventional thermal generation, hydro plants and nuclear power, as shown in Figure 16. Other renewable sources, besides hydro, have played a very limited role so far.

Figure 16. Regional electricity generation by fuel 2008, %

Source: ENTSO-E, OST, NERC, Moldova and Transnistria statistics

The generation structure is however very different in the different countries, see Figure 17. Albania gets almost all of its domestic generation from hydro power, but is also to a high degree import dependent. This is in particular the case in drought years. Other countries such as Bosnia and Herzegovina, Croatia and Serbia also get a third or more of their generation from hydro power. On the other extreme of the scale is UNMIK, which gets almost all of its domestic generation from thermal plants (lignite) and which is also import dependent. Ukraine shows a large share of domestic generation from nuclear power (49%), and is the only country with nuclear generation of the Contracting Parties. Many of the countries in the region are import dependent, and some of the countries are heavily dependent on import of electricity. Ukraine and Bosnia Herzegovina are the only two of the Contracting Parties which are not dependent on import of electricity, which the possible inclusion also of Moldova.

It is necessary to add a note about Moldova. In the figure, Moldova is shown as a net importer of electricity. This is due to the fact that the largest domestic power plant in Moldova is located in a region known as Transnistria, which de facto cannot be totally controlled by Moldova. In 2008, only 28% of the final consumption was supplied by internal generation, when excluding Transnistria in the data for Moldova. The sub-national import need of

7 Also including Romania and Bulgaria

16%

31%

31%

7%

0%

15%

0%

Hydro Nuclear Coal and Lignite Gas Oil Mixed fossil fuels Other renewables

SOUTH EAST EUROPE WHOLESALE MARKET OPENING

50

PÖYRY MANAGEMENT CONSULTING

NORD POOL CONSULTING

Moldova depends on whether electricity is sourced from the Transnistria region or Ukraine. In 2009 and 2010, no electricity was imported from Ukraine according to Moldelectrica (or less than 0.1 TWh in 2010). If including the generation from Transnistria, Moldova is actually self-sufficient with electricity.

The regional generation mix highlights the importance of trade and the potentially significant benefits that can be achieved through improved regional trade. Hydro and thermal based systems are excellent complements due to the regulation possibilities connected with hydro (with storage), but also the increased security of supply that can be expected. The needs for regional trade is furthermore emphasised by the clear import dependency of some of the countries in the region.

Figure 17. Electricity generation by fuel 2008 by jurisdiction, %

Source: ENTSO-E, KOSTT, OST, NERC, Moldova and Transnistria statistics