72

Seeking sustainable growth The luxury and cosmetics financial factbook 2015 edition

Seeking sustainable growthThe luxury and cosmetics financial factbook2015 edition

Contents Statistics and key facts

Index evolution

2 Executive summary

A. Financial parameters

B. Operating aggregates

C. Advertising expenses

D. SOTP and segment analyses

E. Trading multiples

F. Transaction multiples

8 DCF and valuation parameters

G. Global luxury goods market

H. Global cosmetics market

I. Points of view from EY’s global sector specialists and outside experts

36 Industry overview

Approach and SOTP analyses

Sample selection

Focus on Jimmy Choo

64 Methodology

67 Glossary

68 Contact us

The luxury and cosmetics financial factbook 2015

Executive summaryWelcome to the fifth edition of EY’s annual financial factbook for the luxury and cosmetics sector. The factbook combines publicly available data with input from our sector leaders based on their work with the world’s leading luxury and cosmetics companies. It looks at current industry trends, the evolution of operating aggregates and key financial parameters.

For the second year in a row, the industry experienced an overall contraction in growth: the value of the global market for personal luxury goods grew by 3.0%, reaching €224b. After a decade of double-digit growth, fueled by the “retail rush,” brand extensions and the quest for the highest product positioning, the industry has now entered a period of maturity. Firms are now focusing on more sustainable growth rates, effective and cost-conscious retail investments, and how to balance different distribution strategies. Despite a generally more favorable outlook in Western countries, the economic environment remains complex. Currency fluctuations and the growing importance of travel retail, are affecting pricing strategies. And while major emerging markets, such as China and Russia, show negative trends, Japan and other Asian-Pacific markets are gaining pace.

In terms of profitability, the slowdown in sales has clearly negatively impacted operating margins: the average margin of the industry’s listed companies declined by 1 percentage point compared with last year. Overall however, expectations for annual growth for the industry remain unchanged, in the range of 4% to 6% through 2017. This continued positive performance will be supported by the growth of luxury consumers and high-net-worth individuals (HNWIs), accessories and the continued development of online sales.

The global cosmetics market grew by 3.6% in line with the previous year, reaching €181b in 2014. We expect a positive long-term trend in this segment. Steady growth will be led mainly by middle-class consumers’ aspiration for high-quality and innovative products. We also see development opportunities in the natural products and men’s segments.

Flavie LacaultFactbook global coordinator, Fashion & Luxury — [email protected]

Executive summaryPage 2

Roberto BonacinaDirector, Lead Advisory M&A, Fashion & Luxury — [email protected]

Marco Pier MazzucchelliPartner, Head of TAS* Mediterranean — [email protected]

Note: *Transaction Advisory Services

Page 3

The luxury and cosmetics financial factbook 2015

Exec

utiv

e su

mm

ary

The industry faces three main challenges in the year ahead:

• Manage demand worldwide — This year, the industry has been impacted by currency volatility: many consumers have abandoned local markets and shopped abroad instead, to benefit from pricing differences. Most dramatically, while domestic consumption in mainland China dropped 3% in 2014, Chinese consumers increased their spending globally by 8%. Luxury companies have started to re-think the idea of a consistent offer throughout the world, to minimize further effects of currency variations. The choice is between maintaining a consistent pricing policy without adapting to specific local fluctuations, or presenting a variable price for each area, chasing exchange rates and purchasing power.

• Defineanomni-channelstrategy — Most companies are refocusing their strategies on the customer experience: omni-channel, flawless retail management, people excellence. Brands are seeking to take control of their operations by managing a dedicated retail network. In parallel, companies have to deploy their presence worldwide and thus continue to develop their wholesale portfolio, focusing on the high quality of their partners. Digital is increasingly important, both as a marketing tool and as a sales channel. Companies can no longer focus on a single channel: they have to define a consistent strategy for all distribution networks and adapt their DNA specifically for each channel, including social media.

• Fine-tunetheretailmodel — The muscular retail strategy carried out by the major international brands in worldwide tier-one cities has lowered the return of top-line growth that can be obtained by increasing direct distribution networks. Today clients are well informed about what they want to buy because of a combination of continuous on-line/off-line switches, word of mouth, social communities. This may lead to a partial redefinition of retail strategies, with selected closures of less-performing retail shops, focus on core locations and well-positioned flagships, reduction in the average size of directly operated stores (DOS) to improve main sale ratios and reduce costs.

This edition of the factbook, based on your feedback, offers operational and financial aggregates on the industry, along with key valuation parameters and multiples. It looks at the industry’s future trends and includes input from our sector leaders. We hope you find this report insightful and that it provokes constructive thought and discussion within your organization.

Do not hesitate to contact us for any comments or suggestions.

Roberto Bonacina [email protected]

Flavie [email protected]

Page 3Executive summary

Marco Pier Mazzucchelli [email protected]

The luxury and cosmetics financial factbook 2015

Statistics and key facts

Global cosmetics market remains a supply-driven market, fueled by innovation where consumers are always looking for quality, performance and perceived results.

China continues to be the top consumer country ( of the total market).

Retail remained a key growth driver in 2014, but the market saw a slowdown in retail network expansion, illustrating the players’ objective to focus on organic growth.

Accessories have become the largest category within luxury goods and have grown the fastest lately.

Global personal luxury marketgrew byin 2014.

3%The online luxury market has grown twelvefold in the past 11 years and now makes up of total sales.

The global cosmetics market grew by 3.6% in 2014.

Asia-Pacific and Latin America represented almost half of the global cosmetics market in 2014.

Demand is still growing, mainly sustained by the touristic consumption, which has been heavily influenced by currency fluctuations and local regulations.

The growth was helped by the sharp depreciation of the euro, which left the sector with an unbalanced price structure across regions.

The digital revolution has opened up huge opportunities for both luxury and cosmetics industry.

For the second year running, dermocosmetics was the most dynamic market, with growth of 5.1%.

Executive summaryPage 4

5%

1/3

The luxury and cosmetics financial factbook 2015

Source: Capital IQ Note: 1) Compound annual growth rate

EY luxury and cosmetics index evolution compared to major indices (base 100 as of 1 January 2008)

The analysis reported in the graph below shows that the EY luxury and cosmetics index (represented by the companies we included in the EY factbook) has outperformed the market over the last seven years with a total return of 87%, corresponding to an average yearly significant return of 9%, despite the economic downturn. This relative performance actually illustrates the appetite of investors for an industry that is characterized by solid financial fundamentals in terms of sales growth, major profitability, resilient international client base and exposure to growing markets, attributing higher valuations to companies-related securities. The EY index is a representation of those luxury and cosmetics companies analyzed within the factbook. A specific weight has been attributed to each company included in the EY index based on its market capitalization and revenues (each of these two parameters weighing for a half). The relative weights have been revised at every company inclusion after its initial public offering (IPO). Finally, the evolution of the EY index has been compared to these of the S&P 500 and STOXX Europe 600 indexes using 1 January 2008 as a starting date (rebased to 100).

Index evolution

Exec

utiv

e su

mm

ary

0

50

100

150

200

250

EY INDEX STOXX S&P

As of 31 March 2015

9%

5%

1%

187

143

111

CAGR08-15

1

85

90

95

100

105

110

115

120

EY INDEX STOXX S&P

111

118

116

Page 5Executive summary

(Base 100 as of 1 March 2014)

PAGE 6 OPENING

LUXURY AND COSMETICS THE EY FINANCIAL FACTBOOK 2014

DCF and valuation parameters

Page 7Opening

DCF

and

val

uatio

n

para

met

ers

Financial parameters A

B Operating aggregates

C Advertising expenses

D SOTP and segment analyses

E Trading multiples

Transaction multiplesF

The luxury and cosmetics financial factbook 2015

DCF and valuation parameters Page 8

Financial parameters A

Source:

• WACC and LTGR: based on consensus of several broker reports for each company • Market capitalization and beta: EY elaboration based on S&P Capital IQ

• Gearing: companies’ financial statements

Notes:

• Market capitalization is based on a one-month average as of 31 March 2015. • Gearing is defined as net financial debt/enterprise value. • Beta corresponds to levered beta measured on a weekly basis over a two-year

period. • Beta figure for Moncler and Jimmy Choo might be influenced by an insufficient

number of observations on the considered period.

WACC and LTGR by company

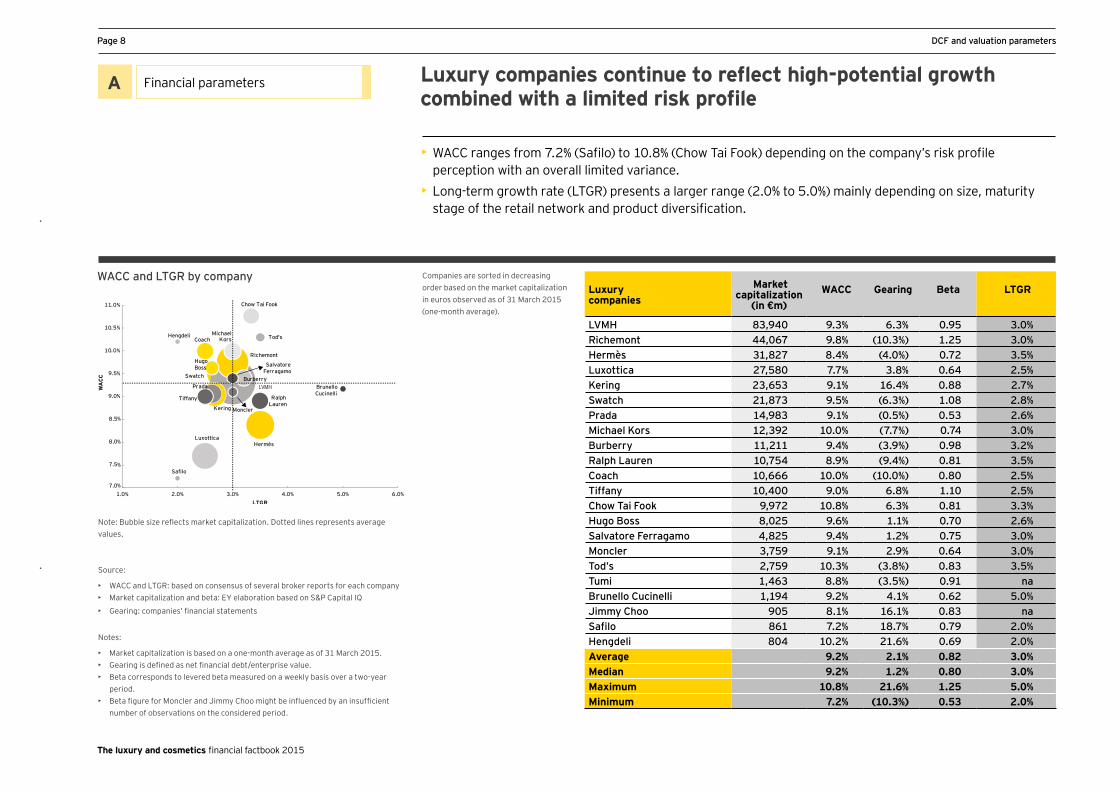

• WACC ranges from 7.2% (Safilo) to 10.8% (Chow Tai Fook) depending on the company’s risk profile perception with an overall limited variance.

• Long-term growth rate (LTGR) presents a larger range (2.0% to 5.0%) mainly depending on size, maturity stage of the retail network and product diversification.

Luxurycompaniescontinuetoreflecthigh-potentialgrowthcombinedwithalimitedriskprofile

Companies are sorted in decreasing order based on the market capitalization in euros observed as of 31 March 2015 (one-month average).

The luxury and cosmetics financial factbook 2015

Note: Bubble size reflects market capitalization. Dotted lines represents average values.

Luxury companies

Market capitalization

(in €m) WACC

Gearing

Beta

LTGR

LVMH 83,940 9.3% 6.3% 0.95 3.0%Richemont 44,067 9.8% (10.3%) 1.25 3.0%Hermès 31,827 8.4% (4.0%) 0.72 3.5%Luxottica 27,580 7.7% 3.8% 0.64 2.5%Kering 23,653 9.1% 16.4% 0.88 2.7%Swatch 21,873 9.5% (6.3%) 1.08 2.8%Prada 14,983 9.1% (0.5%) 0.53 2.6%Michael Kors 12,392 10.0% (7.7%) 0.74 3.0%Burberry 11,211 9.4% (3.9%) 0.98 3.2%Ralph Lauren 10,754 8.9% (9.4%) 0.81 3.5%Coach 10,666 10.0% (10.0%) 0.80 2.5%Tiffany 10,400 9.0% 6.8% 1.10 2.5%Chow Tai Fook 9,972 10.8% 6.3% 0.81 3.3%Hugo Boss 8,025 9.6% 1.1% 0.70 2.6%Salvatore Ferragamo 4,825 9.4% 1.2% 0.75 3.0%Moncler 3,759 9.1% 2.9% 0.64 3.0%Tod’s 2,759 10.3% (3.8%) 0.83 3.5%Tumi 1,463 8.8% (3.5%) 0.91 naBrunello Cucinelli 1,194 9.2% 4.1% 0.62 5.0%Jimmy Choo 905 8.1% 16.1% 0.83 naSafilo 861 7.2% 18.7% 0.79 2.0%Hengdeli 804 10.2% 21.6% 0.69 2.0%Average 9.2% 2.1% 0.82 3.0%Median 9.2% 1.2% 0.80 3.0%Maximum 10.8% 21.6% 1.25 5.0%Minimum 7.2% (10.3%) 0.53 2.0%

Page 9DCF and valuation parameters

Financial parameters A

WACC and LTGR by company

• Natura’s (Brazil) long-term growth rate continues to be significantly higher than the average sample, driven by its geographical coverage.

• WACC sample levels are balanced by the two extremes of Natura (Brazil geographical risk) and Shiseido (Japan).

The cosmetic sample is characterized by a smaller number of companies,whichsignificantlyimpactsthevarianceoffinancialparameters

Companies are sorted in decreasing order based on the market capitalization in euros observed as of 31 March 2015 (one-month average).

Natura

L'Oréal

Beiersdorf

Estée Lauder

L'Occitane

Coty

4.0%

5.0%

6.0%

7.0%

8.0%

9.0%

10.0%

11.0%

0.0% 1.0% 2.0% 3.0% 4.0% 5.0% 6.0% 7.0%

WA

CC

LTGR

The luxury and cosmetics financial factbook 2015

Source:

• WACC and LTGR: based on consensus of several broker reports for each company • Market capitalization and beta: EY elaboration based on S&P Capital IQ

• Gearing: companies’ financial statements

Notes:

• Market capitalization is based on a one-month average as of 31 March 2015. • Gearing is defined as net financial debt/enterprise value. • Beta corresponds to levered beta measured on a weekly basis over a two-year

period.

Note: Bubble size reflects market capitalization. Dotted lines represents average values.

DCF

and

val

uatio

n

para

met

ers

Cosmetics companies

Market capitalization

(in €m) WACC Gearing Beta LTGR

L’Oréal 93,163 7.9% 2.3% 0.71 2.0%Estée Lauder 28,982 8.3% 0.9% 1.04 2.5%Beiersdorf 18,242 7.8% (4.4%) 0.77 2.3%Coty 7,444 8.0% 23.5% 0.99 1.8%Shiseido 6,788 4.1% 9.3% 0.72 naL’Occitane 3,628 9.1% (5.3%) 0.68 3.0%Natura 3,237 10.0% 17.0% 0.87 6.0%Average 7.9% 6.2% 0.83 2.9%Median 8.0% 2.3% 0.77 2.4%Maximum 10.0% 23.5% 1.04 6.0%Minimum 4.1% (5.3%) 0.68 1.8%

Page 10 DCF and valuation parameters

Financial parameters

WACC Beta Gearing LTGR

Source: data based on consensus of several brokers reports for each companyNote: LTGR data was not available for Tumi, Shiseido and Jimmy Choo

EY luxury and cosmetics sample: summaryoffinancialparameters

The luxury and cosmetics financial factbook 2015

A

4.1%

7.2%

7.7%

7.8%

7.9%

8.0%

8.1%

8.3%

8.4%

8.8%

8.9%

8.9%

9.0%

9.1%

9.1%

9.1%

9.1%

9.2%

9.3%

9.4%

9.4%

9.5%

9.6%

9.8%

10.0%

10.0%

Shiseido

Safilo

Luxottica

Beiersdorf

L'Oréal

Coty

Jimmy Choo

Estée Lauder

Hermès

Tumi

Average

Ralph Lauren

Tiffany

Kering

Prada

L'Occitane

Moncler

Brunello Cucinelli

LVMH

Burberry

Swatch

Hugo Boss

Richemont

Michael Kors

Coach

Natura

Hengdeli

Tod's

Chow Tai Fook

WACC9.2%

Industry benchmarkLow High

WACC 8.9%

Industry benchmarkLow High

10.0%

10.2%

10.3%

10.8%

Salvatore Ferragamo

(10.3%)

(10.0%)

(9.4%)

(7.7%)

(6.3%)

(5.3%)

(4.4%)

(4.0%)

(3.9%)

(3.8%)

(3.5%)

(0.5%)

0.9%

1.1%

1.2%

2.3%

2.9%

3.1%

3.8%

4.1%

6.3%

6.3%

6.8%

9.3%

16.1%

16.4%

17.0%

18.7%

21.6%

23.5%

Richemont

Coach

Ralph Lauren

Michael Kors

Swatch

L'Occitane

Beiersdorf

Hermès

Burberry

Tod's

Tumi

Prada

Estée Lauder

Hugo Boss

L'Oréal

Moncler

Average

Luxottica

Brunello Cucinelli

Chow Tai Fook

LVMH

Tiffany

Shiseido

Jimmy Choo

Kering

Natura

Safilo

Hengdeli

Coty

9.2%

Industry benchmarkLow High

Gearing 3.1%

Industry benchmarkLow High

Salvatore Ferragamo

0.53

0.62

0.64

0.64

0.68

0.69

0.70

0.71

0.72

0.72

0.74

0.75

0.77

0.79

0.80

0.81

0.81

0.82

0.83

0.83

0.87

0.88

0.91

0.95

0.98

0.99

1.04

1.08

1.10

1.25

Prada

Brunello Cucinelli

Moncler

Luxottica

L'Occitane

Hengdeli

Hugo Boss

L'Oréal

Shiseido

Hermès

Michael Kors

Beiersdorf

Safilo

Coach

Ralph Lauren

Chow Tai Fook

Average

Tod's

Jimmy Choo

Natura

Kering

Tumi

LVMH

Burberry

Coty

Estée Lauder

Swatch

Tiffany

Richemont

9.2%

Industry benchmarkLow High

Beta 0.82

Industry benchmarkLow High

Salvatore Ferragamo

1.8%

2.0%

2.0%

2.0%

2.3%

2.5%

2.5%

2.5%

2.5%

2.6%

2.6%

2.7%

2.8%

3.0%

3.0%

3.0%

3.0%

3.0%

3.0%

3.0%

3.2%

3.3%

3.5%

3.5%

3.5%

5.0%

6.0%

Coty

Safilo

Hengdeli

L'Oréal

Beiersdorf

Coach

Tiffany

Luxottica

Estée Lauder

Prada

Hugo Boss

Kering

Swatch

Average

Richemont

Michael Kors

SalvatoreFerragamo

Moncler

L'Occitane

LVMH

Burberry

Hermès

Ralph Lauren

Tod's

BrunelloCucinelli

Natura

9.2%

Industry benchmarkLow High

LTGR 3.0%

Industry benchmarkLow High

Chow Tai Fook

Sales CAGR, FY13A–FY16E – luxury companies

Source: Data based on consensus of several brokers’ reports for each company

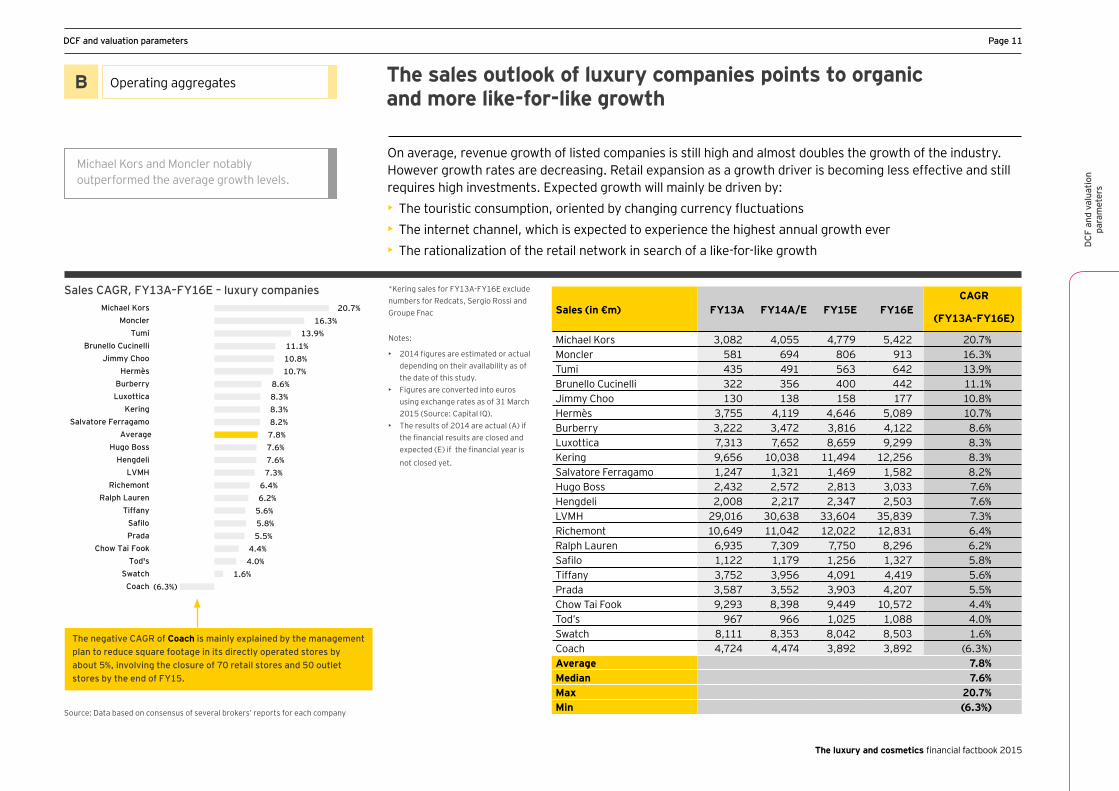

On average, revenue growth of listed companies is still high and almost doubles the growth of the industry. However growth rates are decreasing. Retail expansion as a growth driver is becoming less effective and still requires high investments. Expected growth will mainly be driven by: • The touristic consumption, oriented by changing currency fluctuations • The internet channel, which is expected to experience the highest annual growth ever • The rationalization of the retail network in search of a like-for-like growth

Michael Kors and Moncler notably outperformed the average growth levels.

The sales outlook of luxury companies points to organic andmorelike-for-likegrowth

*Kering sales for FY13A-FY16E exclude numbers for Redcats, Sergio Rossi and Groupe Fnac

Notes:

• 2014 figures are estimated or actual depending on their availability as of the date of this study.

• Figures are converted into euros using exchange rates as of 31 March 2015 (Source: Capital IQ).

• The results of 2014 are actual (A) if the financial results are closed and expected (E) if the financial year is

not closed yet.

Page 11DCF and valuation parameters

(6.3%)1.6%

4.0% 4.4%

5.5% 5.8% 5.6% 6.2% 6.4%

7.3% 7.6% 7.6% 7.8% 8.2% 8.3% 8.3% 8.6%

10.7% 10.8% 11.1%

13.9% 16.3%

20.7%

Coach Swatch

Tod's Chow Tai Fook

Prada Safilo

Tiffany Ralph Lauren

Richemont LVMH

Hengdeli Hugo Boss

Average Salvatore Ferragamo

Kering Luxottica Burberry

Hermès Jimmy Choo

Brunello Cucinelli Tumi

Moncler Michael Kors

B Operating aggregates

DCF

and

val

uatio

n

para

met

ers

The negative CAGR of Coach is mainly explained by the management plan to reduce square footage in its directly operated stores by about 5%, involving the closure of 70 retail stores and 50 outlet stores by the end of FY15.

Sales (in €m) FY13A FY14A/E FY15E FY16E CAGR

(FY13A-FY16E)

Michael Kors 3,082 4,055 4,779 5,422 20.7%Moncler 581 694 806 913 16.3%Tumi 435 491 563 642 13.9%Brunello Cucinelli 322 356 400 442 11.1%Jimmy Choo 130 138 158 177 10.8%Hermès 3,755 4,119 4,646 5,089 10.7%Burberry 3,222 3,472 3,816 4,122 8.6%Luxottica 7,313 7,652 8,659 9,299 8.3%Kering 9,656 10,038 11,494 12,256 8.3%Salvatore Ferragamo 1,247 1,321 1,469 1,582 8.2%Hugo Boss 2,432 2,572 2,813 3,033 7.6%Hengdeli 2,008 2,217 2,347 2,503 7.6%LVMH 29,016 30,638 33,604 35,839 7.3%Richemont 10,649 11,042 12,022 12,831 6.4%Ralph Lauren 6,935 7,309 7,750 8,296 6.2%Safilo 1,122 1,179 1,256 1,327 5.8%Tiffany 3,752 3,956 4,091 4,419 5.6%Prada 3,587 3,552 3,903 4,207 5.5%Chow Tai Fook 9,293 8,398 9,449 10,572 4.4%Tod’s 967 966 1,025 1,088 4.0%Swatch 8,111 8,353 8,042 8,503 1.6%Coach 4,724 4,474 3,892 3,892 (6.3%)Average 7.8%Median 7.6%Max 20.7%Min (6.3%)

The luxury and cosmetics financial factbook 2015

Page 12 DCF and valuation parameters

The luxury and cosmetics financial factbook 2015

Source: data based on consensus of several brokers’ reports for each company

Sales CAGR, FY13A–FY16E – cosmetic companies

Majority of players are expected to grow at lower single digits except for L’Occitane and Natura. The cosmetics market is still driven by: • Innovation and emphasis on quality and new ideas • Increased focus on customized and green cosmetics • A regional focus on new markets to compensate the slow growth expected in Europe

L’Occitane and Natura significantly outperformed the cosmetics sample expectations.

Sales growth expectations for cosmetics players are lower than for the luxury segment but still show an average annual growth of5%overtheFY13A-FY16Eperiod

Notes:

• 2014 figures are estimated or actual depending on their availability as of the date of this study.

• Figures are converted into euros using exchange rates as of 31 March 2015 (Source: Capital IQ).

0.7%

3.0%

4.2%

4.3%

4.6%

5.4%

9.5%

11.7%

Coty

Shiseido

Beiersdorf

L'Oréal

Estée Lauder

Average

Natura

L'Occitane

B Operating aggregates

Sales (in €m) FY13A FY14A/E FY15E FY16E CAGR

(FY13A-FY16E)

L’Occitane 1,055 1,180 1,333 1,471 11.7%Natura 2,040 2,155 2,438 2,676 9.5%Estée Lauder 9,478 10,210 10,142 10,833 4.6%L’Oréal 22,124 22,532 24,033 25,136 4.3%Beiersdorf 6,141 6,285 6,595 6,946 4.2%Shiseido 5,913 5,972 5,695 6,455 3.0%Coty 4,328 4,237 4,195 4,422 0.7%Average 5.4%Median 4.3%Max 11.7%Min 0.7%

The luxury and cosmetics financial factbook 2015

Source: Data based on consensus of several brokers’ reports for each company

The slightly lower 2014 EBITDA margin vs 2013 is mainly due to: • Lower growth experienced in the emerging markets • Sharp currency movements leading to unprecedented price cuts putting pressure on margins • Partially compensated by the good performance of accessories

EBITDA remains largely above 20% with few notable exceptions higher than 30%.

The luxury sample average earnings before taxes, depreciation andamortization(EBITDA)marginshowsthatprofitabilitywillnotmateriallygrow,evenifitstillreachessignificantlevel

Average EBITDA margin, FY13A–FY16E — luxury companies

*Kering margin for FY12A-FY15E exclude numbers for Redcats, Sergio Rossi and Groupe Fnac

Note: the 2014 EBITDA margin is computed on the basis of either actual or estimated figures for 2014 sales, depending on their availability. As some groups are listed under different jurisdictions around the world, they may use different generally accepted accounting principles (GAAP), and therefore a direct comparison of EBITDA may be less meaningful than if their results were presented under the International Accounting Standards.

7.8%

10.6%

12.8%

17.2%

18.3%

18.4%

20.4%

20.5%

21.0%

21.4%

22.0%

22.5%

23.6%

23.6%

23.8%

23.9%

25.3%

27.1%

27.1%

29.2%

32.5%

33.4%

36.0%

Hengdeli

Safilo

Chow Tai Fook

Jimmy Choo

Ralph Lauren

Brunello Cucinelli

Luxottica

Kering

Tod's

Tumi

Salvatore Ferragamo

Average

Hugo Boss

Swatch

LVMH

Burberry

Tiffany

Coach

Richemont

Prada

Michael Kors

Moncler

Hermès

Page 13DCF and valuation parameters

B Operating aggregates

DCF

and

val

uatio

n

para

met

ers

EBITDA margin FY13A FY14A/E FY15E FY16E Average ratio

(FY13A-FY16E)

Hermès 36.0% 35.1% 36.2% 36.7% 36.0%Moncler 33.0% 33.5% 33.4% 33.8% 33.4%Michael Kors 32.9% 32.5% 32.5% 32.0% 32.5%Prada 31.7% 26.8% 28.5% 29.6% 29.2%Richemont 26.8% 28.2% 26.5% 26.9% 27.1%Coach 33.2% 27.2% 23.3% 24.5% 27.1%Tiffany 23.9% 25.5% 25.6% 26.1% 25.3%Burberry 24.7% 23.4% 23.3% 24.1% 23.9%LVMH 24.6% 23.0% 23.4% 24.2% 23.8%Swatch 24.8% 21.6% 23.9% 24.0% 23.6%Hugo Boss 23.2% 23.0% 23.8% 24.2% 23.6%Salvatore Ferragamo 20.8% 22.2% 22.1% 22.9% 22.0%Tumi 21.5% 21.2% 21.6% 21.3% 21.4%Tod’s 24.0% 19.9% 19.8% 20.4% 21.0%Kering 21.2% 19.8% 20.1% 20.9% 20.5%Luxottica 19.5% 20.1% 20.8% 21.2% 20.4%Brunello Cucinelli 18.6% 18.4% 18.1% 18.4% 18.4%Ralph Lauren 18.7% 17.6% 18.0% 18.7% 18.3%Jimmy Choo 15.2% 16.8% 18.1% 18.8% 17.2%Chow Tai Fook 12.4% 13.0% 13.1% 12.9% 12.8%Safilo 10.0% 9.4% 11.0% 12.0% 10.6%Hengdeli 8.0% 7.2% 7.8% 8.0% 7.8%Average 23.0% 22.1% 22.3% 22.8% 22.5%Median 23.6% 21.9% 22.7% 23.5% 22.8%Maximum 36.0% 35.1% 36.2% 36.7% 36.0%Minimum 8.0% 7.2% 7.8% 8.0% 7.8%

Page 14 DCF and valuation parameters

The luxury and cosmetics financial factbook 2015

Source: Data based on consensus of several brokers’ reports for each company

Average EBITDA margin, FY13A–FY16E — cosmetics companies

Cosmeticcompaniesconfirmedlastyear’saverageEBITDAof17.4%fortheFY13A-FY16Eperiod

Cosmetics companies are expected to improve their operating margin in the coming years. The key drivers of margin growth are: • Higher sales of prestige products (which bear higher price tags and margins) in emerging markets • Consumers still aspiring to more innovating and high-quality products

Natura and L’Oréal are showing outperforming profitability.

Note: the 2014 EBITDA margin is computed on the basis of either actual or estimated figures for 2014 sales, depending on their availability. As some groups are listed under different jurisdictions around the world, they may use different GAAP, and therefore a direct comparison of EBITDA may be less meaningful than if their results were presented under the International Accounting Standards.

9.8%

15.2%

15.7%

17.4%

18.6%

19.3%

21.2%

21.9%

Shiseido

Coty

Beiersdorf

Average

L'Occitane

Estée Lauder

L'Oréal

Natura

EBITDA Margin FY13A FY14A/E FY15E FY16E Average ratio

(FY13A-FY16E)

Natura 22.8% 21.1% 21.6% 22.2% 21.9%L’Oréal 20.5% 21.1% 21.5% 21.8% 21.2%Estée Lauder 18.0% 20.2% 18.8% 20.3% 19.3%L’Occitane 17.4% 18.2% 19.1% 19.5% 18.6%Beiersdorf 15.1% 15.5% 16.0% 16.4% 15.7%Coty 14.3% 13.9% 16.1% 16.6% 15.2%Shiseido 12.0% 8.1% 9.5% 9.6% 9.8%Average 17.1% 16.9% 17.5% 18.1% 17.4%Median 17.4% 18.2% 18.8% 19.5% 18.6%Maximum 22.8% 21.1% 21.6% 22.2% 21.9%Minimum 12.0% 8.1% 9.5% 9.6% 9.8%

B Operating aggregates

The luxury and cosmetics financial factbook 2015

Source: Data based on consensus of several brokers’ reports for each company

Average capex ratio, FY13A–FY16E — luxury companies

The average capital expenditure (capex) sales ratio of the sample confirmsanindustrywithintensivecapitalrequirements

The stable average level of 5% to 6% of the capex sales ratio is mainly explained by the requirements of the retail network (openings, renovations, etc.).

Note: the 2014 capex ratio is computed on the basis of either actual or estimated figures for 2014 sales, depending on their availability.

0.3%

2.0%

3.1%

3.7%

4.7%

5.1%

5.2%

5.5%

5.7%

5.8%

5.8%

5.9%

6.0%

6.0%

6.0%

6.1%

6.9%

7.2%

7.4%

7.8%

8.2%

8.5%

Hengdeli

Chow Tai Fook

Safilo

Luxottica

Kering

Ralph Lauren

LVMH

Tod's

Richemont

Average

Tiffany

Moncler

Tumi

Salvatore Ferragamo

Hugo Boss

Hermès

Coach

Burberry

Michael Kors

Brunello Cucinelli

Jimmy Choo

Swatch

Prada 10.9%

Page 15DCF and valuation parameters

DCF

and

val

uatio

n

para

met

ers

Prada continues to outperform on capex ratio; however it is expected to moderate as the company slows down its store expansion pace.

Capex ratio FY13A FY14A/E FY15E FY16E Average ratio

(FY13A-FY16E)

Prada 15.3% 10.2% 9.0% 9.0% 10.9%Swatch 7.1% 12.4% 7.3% 7.1% 8.5%Jimmy Choo 7.7% 9.1% 7.9% 8.1% 8.2%Brunello Cucinelli 9.3% 8.8% 7.8% 5.4% 7.8%Michael Kors 5.6% 9.1% 8.1% 6.7% 7.4%Burberry 6.4% 7.9% 7.4% 6.9% 7.2%Coach 4.8% 4.6% 10.5% 7.7% 6.9%Hermès 5.6% 6.8% 6.1% 5.8% 6.1%Hugo Boss 7.1% 5.0% 6.0% 5.8% 6.0%Salvatore Ferragamo 6.6% 6.3% 6.4% 4.7% 6.0%Tumi 5.4% 6.9% 5.8% 5.7% 6.0%Moncler 5.6% 7.1% 5.8% 5.2% 5.9%Tiffany 5.5% 5.8% 6.0% 6.0% 5.8%Richemont 6.0% 5.3% 5.8% 5.5% 5.7%Tod’s 5.1% 6.5% 5.3% 5.2% 5.5%LVMH 5.4% 5.0% 5.3% 5.2% 5.2%Ralph Lauren 5.2% 5.4% 5.0% 4.8% 5.1%Kering 6.9% 1.8% 5.0% 4.9% 4.7%Luxottica 3.7% 3.7% 3.8% 3.7% 3.7%Safilo 3.2% 3.2% 3.1% 3.0% 3.1%Chow Tai Fook 1.7% 3.0% 1.8% 1.4% 2.0%Hengdeli 0.9% (1.6%) 0.9% 0.9% 0.3%Average 5.9% 6.0% 5.9% 5.4% 5.8%Median 5.6% 6.0% 5.9% 5.4% 5.9%Maximum 15.3% 12.4% 10.5% 9.0% 10.9%Minimum 0.9% (1.6%) 0.9% 0.9% 0.3%

B Operating aggregates

Page 16 DCF and valuation parameters

The luxury and cosmetics financial factbook 2015

Source: Data based on consensus of several brokers’ reports for each company

Average capex ratio, FY13A–FY16E — cosmetic companies

Overall,thecapitalrequirementsarelowerforthecosmeticssample, with the exception of those with retail networks

Natura and L’Occitane capex ratios outperform the sample due to their retail profiles.

Note: the 2014 capex ratio is computed on the basis of either actual or estimated figures for 2014 sales, depending on their availability.

3.1%

3.4%

4.0%

4.4%

4.5%

4.6%

5.7%

6.3%

Shiseido

Beiersdorf

Coty

L'Oréal

Average

Estée Lauder

L'Occitane

Natura

Capex ratio FY13A FY14A/E FY15E FY16E Average ratio

(FY13A-FY16E)

Natura 7.6% 6.8% 5.6% 5.2% 6.3%L’Occitane 5.7% 6.3% 5.5% 5.5% 5.7%Estée Lauder 4.5% 4.7% 4.8% 4.6% 4.6%L’Oréal 4.6% 4.4% 4.4% 4.4% 4.4%Coty 3.6% 4.4% 4.2% 4.0% 4.0%Beiersdorf 3.5% 4.3% 3.3% 2.7% 3.4%Shiseido 1.4% 2.7% 4.3% 3.8% 3.1%Average 4.4% 4.8% 4.6% 4.3% 4.5%Median 4.5% 4.4% 4.4% 4.4% 4.4%Maximum 7.6% 6.8% 5.6% 5.5% 6.3%Minimum 1.4% 2.7% 3.3% 2.7% 3.1%

B Operating aggregates

Source: Data based on consensus of several brokers’ reports for each company

Average sales CAGR Average EBITDA margin Average capex ratio

EY luxury and cosmetics sample: summary of operating aggregates

21.6%

24.1%24.6%

24.0%

22.5%

20%

21%

22%

23%

24%

25%

FY11 FY12 FY14 FY14 FY15

Ebitda Margin

4.7% 4.9%

5.8% 5.6% 5.9%

0%

1%

2%

3%

4%

5%

6%

7%

FY11 FY12 FY14 FY14 FY15

Capex ratio

9.7%

11.8% 12.3%

10.1%

7.8%

0%

2%

4%

6%

8%

10%

12%

14%

FY11 FY12 FY14 FY14 FY15

Sales Growth

The luxury and cosmetics financial factbook 2015

Page 17DCF and valuation parameters

DCF

and

val

uatio

n

para

met

ers

The charts below show the evolution of selected operating aggregates (sales CAGR, EBITDA margin, capex ratio) over the past editions of the EY luxury and cosmetics factbook. While growth and average profitability are decreasing within the increasingly competing and challenging environment, capex are not. The market still demands a high operating leverage.

Luxury

After the rebound due to the financial crisis, reaching a peak of 12.3% in FY13, the estimated CAGR of sales for FY15 reached its minimum over the past five years. Nevertheless, the pace is still significant, and the foreseen growth around 8% reflects a reduced but more sustainable development rate. Actually, after a phase of accelerated development (mainly driven by retail expansion, product diversification and geographic extension), companies are now more focused on organic growth.This slowdown in sales growth directly impacts the EBITDA margin aggregates, also showing a slight contraction over the considered period, as a consequence of the slowdown of emerging markets and a higher pressure on margins.The capex ratio has remained close to 6%, at its highest over the past five years, confirming the need of high operating leverage of the industry.

B Operating aggregates

Page 18 DCF and valuation parameters

The luxury and cosmetics financial factbook 2015

Source: data based on consensus of several brokers reports for each company

EY luxury and cosmetics sample: summary of operating aggregates

The charts below show the evolution of selected operating aggregates (sales CAGR, EBITDA margin, capex ratio) over the past editions of the EY luxury and cosmetics factbook.

Cosmetics

• The cosmetics sector on average has lower sales CAGR and EBITDA margin than the luxury sector. • Sales CAGR observed in 2014 is in line with the 2013 figure, at the lowest point over the last five years. • The EBITDA margin has remained globally stable over the considered period, at a solid level of around 17-18%. • The capex ratio is slightly lower than for the luxury companies, mostly stable at 4.5%, which illustrates the lower exposition to retail and thus a lower requirement for investment.

Average sales CAGR Average EBITDA margin Average capex ratio

17.0%

18.1%18.3%

17.4% 17.4%

16%

17%

18%

19%

FY11 FY12 FY14 FY14 FY15

Ebitda Margin

3.3%

4.0%4.4%

4.7% 4.5%

0%

1%

2%

3%

4%

5%

FY11 FY12 FY14 FY14 FY15

Capex ratio

8.2%7.7%

8.8%

5.4% 5.4%

0%1%2%3%4%5%6%7%8%9%

10%

FY11 FY12 FY14 FY14 FY15

Sales Growth

B Operating aggregates

The luxury and cosmetics financial factbook 2015

Source: Data based on actual or estimated numbers based on availability as of the date of this report

• Marketing and advertising represent a significant cost component for both global luxury and cosmetics manufacturers. • Advertising expenses will remain a major operating topic, especially for cosmetics companies focusing on top-line growth and brand awareness sustainability. • Cosmetics advertising expenses are significantly influenced by their mass-market positioning. • Luxury companies have a lower incidence of advertising costs; however, in addition to advertising, one should consider the additional costs/investments to promote their brands embedded in flagship stores and ambassadors.

Advertising remains a key cost of the industry

Page 19DCF and valuation parameters

C Advertising expenses

4.8% 5.0% 5.2% 6.6% 6.7% 6.7%9.2%

11.0% 11.4%

23.9%25.9%

29.1%

0.0%

5.0%

10.0%

15.0%

20.0%

25.0%

30.0%

35.0%

Coa

ch

Tum

i

Pra

da

Her

mès

Salv

ator

eFe

rrag

amo

Mon

cler

Tiff

any

Luxo

ttic

a

Ric

hem

ont

Safil

o

LVM

H

Bei

ersd

orf

Cot

y

Shis

eido

Esté

eLa

uder

L'O

réal

Luxury companies Cosmetics companies

Average 6.6%

Average 25.1%

2.7% 3.1%

23.2% 23.5%

DCF

and

val

uatio

n

para

met

ers

Selected companies — advertising expenses as a percentage of sales, FY14A/E

Page 20 DCF and valuation parameters

The luxury and cosmetics financial factbook 2015

Sales breakdown FY15E (in €b) EBIT breakdown FY15E (in €b) Enterprise value breakdown FY15E (in €b)

Source: SOTP based on EY analysis and on the following brokers reports: RBC Capital (11 February 2015), Deutsche Bank AG (23 February 2015) and JP Morgan (23 March 2015)

• LVMH SOTP analysis implies a total enterprise valuation of €100.6b in FY15E. • The fashion and leather goods segment is the largest contributor both in terms of sales (35%) and EBIT (57%).

LVMH: SOTPD SOTP and segment analyses

35%

13%

9%

13%

31%

Fashion andleather goods

Perfumes andcosmetics

Watches andjewelry

Wines andspirits

Selectiveretailing

Eliminations Total

34.710.9

3.1

4.4

4.4

(0.4)

12.2

57%

7%5%

20%

16%

-5%

Fashion andleather goods

Perfumes andcosmetics

Watches andjewelry

Wines andspirits

Selectiveretailing

Eliminations Total

6.61.1

0.3

0.5

1.3

(0.3)

3.7

55%

8%5%

22%

14%

-4%

0%

Fashion andleathergoods

Perfumesand

cosmetics

Watches andjewelry

Wines andspirits

Selectiveretailing

Elimination Total

100.6

5.2

8.0

22.6

55.1

13.9

(4.4)

0.3

Surplusassets

Luxury products(excluding spirits)

Luxury products(excluding spirits)

Luxury products(excluding spirits)

Source: SOTP based on EY analysis and on the following brokers reports: RBC Capital (11 February 2015),JP Morgan (11 February 2015), Societe Generale (18 February 2015) and Deutsche bank (23 February 2015)

• Kering SOTP analyses imply a total enterprise value of €28.1b in FY15E. • Contributing around 97% of the total EBIT for 69% of sales, Gucci group is the most profitable segment in terms of operating margin.

Kering: SOTP

The luxury and cosmetics financial factbook 2015

Page 21DCF and valuation parameters

DCF

and

val

uatio

n

para

met

ers

D SOTP and segment analyses

Sales breakdown FY15E (in €b) EBIT breakdown FY15E (in €b) Enterprise value breakdown FY15E (in €b)

69%

7.829%

0.3 11.30.03.2

3.0%0%

Gucci Group Puma Other brands Eliminations Total

97%

1.9 8%

.00 2.0

(0.1)

0.2

1.0%

-6%

Gucci Group Puma Other brands Eliminations Total

100%

28.1 8%

0.2 28.1

(2.4)

2.2

1.0%

-8%

Gucci Group Puma Other brands Eliminations Total

Luxury Sport and lifestyle Luxury Sport and lifestyle Luxury Sport and lifestyle

Page 22 DCF and valuation parameters

Sales breakdown FY15E (in €b) EBIT breakdown FY15E (in €b) Enterprise value breakdown FY15E (in €b)

Source: SOTP based on EY analysis and on the following brokers reports: RBC Capital (11 February 2015),

JP Morgan (11 February 2015), Societe Generale (18 February 2015) and Deutsche bank (23 February 2015)

• Gucci Group SOTP analyses imply an enterprise value of €28.1b in FY15E. • Within the Gucci Group segment, the Gucci brand alone represents 49% of the top line and 61% of EBIT in FY15E, meaning that the Gucci brand is expected to constitute the largest segment within the Gucci Group and also the most profitable in terms of operating margin.

Kering: further analysis of Gucci Group through SOTP approach

49%

17%

11%

23%

Gucci brand Bottega Veneta YSL Other brands Gucci Group

7.81.8

0.9

1.3

3.8

The luxury and cosmetics financial factbook 2015

D SOTP and segment analyses

61%

22%

7%

10%

Gucci brand Bottega Veneta YSL Other brands Gucci Group

1.90.2

0.1

0.4

1.2

54%

25%

9%

12%

Gucci brand Bottega Veneta YSL Other brands Gucci Group

28.13.3

2.4

7.0

15.3

The luxury and cosmetics financial factbook 2015

L’Oréal:segmentanalysis

• The two main divisions of L’Oréal are Consumer Products and L’Oréal Luxe, accounting together for 76% of the group’s revenues and 90% of the EBIT. In particular, the L’Oréal Luxe division accounts for 28% of the total sales in FY14A.

• This division is expected to register a sales growth at a CAGR of 7.8% over the 2013A-17E period when its operating income is anticipated to grow from €1.17b to €1.65b (or at a CAGR of 8.9%) over the same period.

• The L’Oréal Luxe division will remain one of the biggest divisions within L’Oréal.

Sales breakdown FY13A–FY17E (in €b) EBIT breakdown FY13A–FY17E (in €b) EBIT margin FY13A-FY17E

Page 23DCF and valuation parameters

DCF

and

val

uatio

n

para

met

ers

D SOTP and segment analyses

20% 20% 21% 21% 21%

17% 18% 18% 18% 18%

0%

5%

10%

15%

20%

25%

2013A 2014A 2015E 2016E 2017E

L’Oréal Luxe Total cosmetics

Source: Analyst research H2 2014

13% 13% 14% 13% 13%

49% 48%48% 47% 47%

27% 28%28% 28%

29%7% 7%

7%7%

7%

4% 4%

4%4%

4%

0

5

10

15

20

25

30

2013A 2014A 2015E 2016E 2017E

Professional Products Consumer ProductsL’Oréal Luxe Active CosmeticsBody Shop

22.1 22.5

25.1

27.626.3

CAGR7.8%

CAGR4.6%

16% 16% 15% 15% 15%

58% 56% 56% 55% 56%

31% 33%

33% 33%34%9% 10%

10% 10%

10%

(16%) (16%) (15%) (15%) (15%)

2% 2%

2%2%

2%

-1

0

1

2

3

4

5

6

2013A 2014A 2015E 2016E 2017EProfessional Products Consumer ProductsL’Oréal Luxe Active CosmeticsEliminations Body Shop

3.8

4.94.6

4.4

3.9

CAGR8.9%

CAGR5.5%

Page 24 DCF and valuation parameters

The luxury and cosmetics financial factbook 2015

Levelofmultiplesillustratesthestill-highattractivenessoftheluxury industry

• The level is quite stable with respect to last year’s figures, even considering the slightly lower margins, showing a good resilience of the industry and confidence of the analysts in future strong growth and significant margins.

• The decreasing trend observed over the years is actually explained by the expected improvement of the operating performance.

Source: Data based on consensus of several brokers reports for each company

Notes:

• The trading multiples are based on: • Fixed EV computed as market capitalization as of 31 March 2015 (one-month average) and latest-available net financial debt • Projections estimated by analysts for successive years

EV/sales (FY14A/E-16E) EV/EBITDA (FY14A/E-16E) Price to earnings (FY14A/E-16E)

E Trading multiples

3.0x 2.8x

2.5x

2.9x 2.7x

2.5x

0

0.5x

1.0x

1.5x

2.0x

2.5x

3.0x

3.5x

4.0x

2014A/E 2015E 2016E

Average Median

13.3x 11.9x

10.8x

13.4x

12.1x

10.9x

0

3.0x

6.0x

9.0x

12.0x

15.0x

18.0x

2014A/E 2015E 2016E

Average Median

24.1x

21.4x

19.1x

23.4x 21.7x

19.4x

0

5.0x

10.0x

15.0x

20.0x

25.0x

30.0x

2014A/E 2015E 2016E

Average Median

Improvement of multiples level for the cosmetics companies illustrates the growing dynamism of the industry

• Trading multiples of the cosmetics companies are globally in line with those of the luxury industry, even with slightly higher figures for EBITDA multiples, illustrating analysts’ expectations for margins to improve in the next years.

Source: Data based on consensus of several brokers reports for each company

Notes:

• The trading multiples are based on: • Fixed EV computed as market capitalization as of 31 March 2015 (one-month average) and latest-available net financial debt • Projections estimated by analysts for successive years

EV/sales (FY14A/E-16E) EV/EBITDA (FY14A/E-16E) Price to earnings (FY14A/E-16E)

The luxury and cosmetics financial factbook 2015

Page 25DCF and valuation parameters

DCF

and

val

uatio

n

para

met

ers

E Trading multiples

2.6x2.5x

2.3x

2.8x2.6x

2.3x

0

0.5x

1.0x

1.5x

2.0x

2.5x

3.0x

3.5x

2014A/E 2015E 2016E

Average Median

15.6x14.4x

13.0x

16.0x

14.8x

13.3x

0

3.0x

6.0x

9.0x

12.0x

15.0x

18.0x

2014A/E 2015E 2016E

Average Median

27.7x 28.9x

24.4x

28.5x 28.3x

23.9x

0

5.0x

10.0x

15.0x

20.0x

25.0x

30.0x

35.0x

2014A/E 2015E 2016E

Average Median

Page 26 DCF and valuation parameters

EY luxury and cosmetics sample: summary of EV/sales multiples

Source: Data based on consensus of several brokers reports for each companyNote: Market capitalization is based on a one-month average as of 31 March 2015.

The luxury and cosmetics financial factbook 2015

E Trading multiples

EV/sales (FY14A/E) EV/sales (FY15E) EV/sales (FY16E)

0.5x

0.9x

1.3x

1.3x

1.3x

1.8x

2.2x

2.3x

2.5x

2.6x

2.8x

2.8x

2.8x

2.8x

2.9x

2.9x

2.9x

2.9x

3.0x

3.0x

3.1x

3.2x

3.5x

3.6x

3.7x

3.7x

4.2x

4.2x

5.6x

7.4x

Hengdeli

Safilo

Shiseido

Chow Tai Fook

Ralph Lauren

Natura

Coach

Coty

Swatch

Jimmy Choo

Tod's

Beiersdorf

Tiffany

Michael Kors

Estée Lauder

Tumi

Kering

L'Occitane

LVMH

Average

Burberry

Hugo Boss

Brunello Cucinelli

Richemont

Salvatore Ferragamo

Luxottica

Prada

L'Oréal

Moncler

Hermés

9.2%

Industry benchmarkLow High

EV/sales (FY14A/E)3.0x

Industry benchmarkLow High

0.5x

0.8x

1.1x

1.3x

1.4x

1.6x

2.3x

2.3x

2.4x

2.5x

2.5x

2.5x

2.6x

2.6x

2.6x

2.7x

2.7x

2.7x

2.8x

2.8x

2.9x

2.9x

3.1x

3.3x

3.3x

3.4x

3.8x

4.0x

4.8x

6.6x

Hengdeli

Safilo

Chow Tai Fook

Ralph Lauren

Shiseido

Natura

Jimmy Choo

Coty

Michael Kors

Coach

Tumi

Kering

Swatch

L'Occitane

Tod's

Beiersdorf

LVMH

Tiffany

Average

Burberry

Estée Lauder

Hugo Boss

Brunello Cucinelli

Luxottica

Richemont

Salvatore Ferragamo

Prada

L'Oréal

Moncler

Hermés

9.2%

Industry benchmarkLow High

EV/sales (FY15E)

2.8x

Industry benchmarkLow High

0.5x

0.8x

1.0x

1.2x

1.2x

1.5x

2.0x

2.1x

2.2x

2.2x

2.3x

2.4x

2.4x

2.4x

2.5x

2.5x

2.5x

2.6x

2.6x

2.6x

2.7x

2.7x

2.8x

3.1x

3.1x

3.1x

3.6x

3.8x

4.2x

6.0x

Hengdeli

Safilo

Chow Tai Fook

Ralph Lauren

Shiseido

Natura

Jimmy Choo

Michael Kors

Tumi

Coty

L'Occitane

Kering

Swatch

Tod's

Coach

Beiersdorf

LVMH

Average

Tiffany

Burberry

Hugo Boss

Estée Lauder

Brunello Cucinelli

Luxottica

Salvatore Ferragamo

Richemont

Prada

L'Oréal

Moncler

Hermés

9.2%

Industry benchmarkLow High

EV/sales (FY16E)2.6x

Industry benchmarkLow High

EY luxury and cosmetics sample: summary of EV/EBITDA multiples

Page 27DCF and valuation parameters

DCF

and

val

uatio

n

para

met

ers

E Trading multiples

Source: Data based on consensus of several brokers reports for each companyNote: Market capitalization is based on a one-month average as of 31 March 2015.

EV/EBITDA (FY14A/E) EV/EBITDA (FY15E) EV/EBITDA (FY16E)

7.2x

7.6x

8.0x

8.6x

8.7x

9.6x

9.9x

11.1x

11.5x

12.9x

12.9x

13.1x

13.6x

13.7x

13.8x

13.9x

14.2x

14.6x

15.5x

15.7x

16.0x

16.0x

16.6x

16.6x

16.8x

17.9x

18.6x

19.1x

20.1x

21.2x

Hengdeli

Ralph Lauren

Coach

Natura

Michael Kors

Safilo

Chow Tai Fook

Tiffany

Swatch

Richemont

LVMH

Burberry

Tumi

Hugo Boss

Average

Tod's

Estée Lauder

Kering

Jimmy Choo

Prada

L'Occitane

Shiseido

Coty

Moncler

Salvatore Ferragamo

Beiersdorf

Luxottica

Brunello Cucinelli

L'Oréal

Hermés

9.2%

Industry benchmarkLow High

EV/EBITDA (FY14A/E)

13.8x

Industry benchmarkLow High

6.3x

7.0x

7.4x

7.4x

7.7x

8.7x

10.7x

10.7x

10.8x

11.6x

11.7x

12.0x

12.2x

12.5x

12.6x

12.6x

12.6x

13.1x

13.4x

13.5x

14.4x

14.7x

14.8x

15.2x

15.4x

15.9x

16.6x

17.3x

18.1x

18.4x

Hengdeli

Ralph Lauren

Michael Kors

Natura

Safilo

Chow Tai Fook

Tiffany

Coach

Swatch

LVMH

Tumi

Burberry

Hugo Boss

Average

Kering

Richemont

Jimmy Choo

Tod's

Prada

L'Occitane

Moncler

Shiseido

Coty

Salvatore Ferragamo

Estée Lauder

Luxottica

Beiersdorf

Brunello Cucinelli

Hermés

L'Oréal

9.2%

Industry benchmarkLow High

EV/EBITDA (FY15E)

12.5x

Industry benchmarkLow High

5.8x

6.3x

6.6x

6.6x

6.7x

8.0x

9.8x

10.2x

10.2x

10.3x

10.5x

10.8x

11.0x

11.1x

11.3x

11.4x

11.6x

12.0x

12.0x

12.0x

12.6x

12.7x

13.3x

13.6x

13.8x

14.6x

15.4x

15.4x

16.3x

17.4x

Hengdeli

Ralph Lauren

Natura

Michael Kors

Safilo

Chow Tai Fook

Tiffany

Swatch

Coach

Tumi

LVMH

Jimmy Choo

Burberry

Hugo Boss

Average

Kering

Richemont

L'Occitane

Tod's

Prada

Moncler

Shiseido

Estée Lauder

Salvatore Ferragamo

Coty

Luxottica

Brunello Cucinelli

Beiersdorf

Hermés

L'Oréal

9.2%

Industry benchmarkLow High

EV/EBITDA (FY16E)

11.3x

Industry benchmarkLow High

The luxury and cosmetics financial factbook 2015

Page 28 DCF and valuation parameters

The luxury and cosmetics financial factbook 2015

Regression analysis: EV/sales multiple vs EBITDA margin

E Trading multiples

• Regression analyses show strong correlation between EV/sales levels and profitability. • Actually, this analysis illustrates that the premium paid on multiples is mainly explained by the good profitability performance.

Source: Data based on consensus of several brokers reports for each company

Notes: Market capitalization is based on a one-month average as of 31 March 2015.The analyses based on sales growth are not presented, as they resulted in an absence of correlation between sales multiples and growth.For information, the results of the analyses performed are: R2 for EV/sales multiple vs sales growth 2015: 6%; R2 for EV/sales multiple vs sales growth 2016: 0%.

Regression analysis: EV/sales multiple vs EBITDA margin 2015 Regression analysis: EV/sales multiple vs EBITDA margin 2016

Burberry

Prada

LVMHTod's

Ralph Lauren

Coach

Hugo Boss

Safilo

Hermès

Tiffany Swatch

Shiseido

Salvatore Ferragamo

L'Oréal

Richemont

Luxottica

Estée LauderBeiersdorf

Brunello CucinelliMichael Kors

CotyJimmy Choo

R² = 0.64

-

1.0x

2.0x

3.0x

4.0x

5.0x

6.0x

7.0x

0% 5% 10% 15% 20% 25% 30% 35% 40%

2015

EV

/sal

es

2015 EBITDA margin

L'Occitane

Natura

Moncler

Tumi

Kering

Chow Tai

Hengdeli

Burberry

LVMHTod's

Ralph Lauren

Coach

Hugo Boss

Safilo

Hermès

Tiffany

Swatch

Shiseido

Kering

Salvatore Ferragamo

L'Oréal

Richemont

Luxottica

Estée LauderBeiersdorf

TUMI

Brunello Cucinelli

Coty

Jimmy Choo

R² = 0.63

-

1.0x

2.0x

3.0x

4.0x

5.0x

6.0x

7.0x

0% 5% 10% 15% 20% 25% 30% 35% 40%

2016

EV

/sal

es

2016 EBITDA margin

NaturaChow Tai

Michael Kors

Prada

L'Occitane

Hengdeli

Moncler

The luxury and cosmetics financial factbook 2015

Page 29DCF and valuation parameters

DCF

and

val

uatio

n

para

met

ers

Transaction multiples in the luxury industry remain at a significantpremiumtomanyothersectors

Source: Capital IQ

• There are several parameters that influence the valuation multiples. In particular: the brand positioning, the historical and expected growth, profitability and cash flow generation, management and organization, premium to rarity, etc.

• Transaction multiples confirm that the industry kept its attractiveness over the past few years. • The average sales multiple over the last years ranged between 1.4x and 2.0x, where the average EBITDA multiple ranged between 11.7x and 15.3x.

Transaction multiplesF

1.6x1.5x

1.9x

1.4x

2.0x1.8x

1.3x1.2x

1.6x1.8x

0.0x

0.5x

1.0x

1.5x

2.0x

2.5x

2011 2012 2013 2014 1Q15Average Median

15.3x

12.0x13.5x

11.7x

13.5x12.3x

10.7x 11.5x10.2x

13.2x

0.0x

2.0x

4.0x

6.0x

8.0x

10.0x

12.0x

14.0x

16.0x

18.0x

2011 2012 2013 2014 1Q15

Average Median

EV/sales (FY11-1Q15) EV/EBITDA (FY11-1Q15)

Page 30 DCF and valuation parameters

The luxury and cosmetics financial factbook 2015

The M&A deals in the cosmetics industry show a similar trend as the luxury industry

Transaction multiplesF

Source: Capital IQ

• The average sales multiple over the last five years ranged between 1.1x and 1.9x, when the EBITDA multiple ranged between 10.0x and 16.6x.

• 1Q15 multiples went back to previous 2014 levels. 2014 multiples illustrated an exceptionally positive trend, mainly driven by strategic acquisitions carried out by the major players to foster growth in emerging markets, and broaden the products’ offering into innovative segments.

1.1x

1.6x

1.9x

1.4x

1.6x

0.9x1.0x

1.6x

1.5x

1.7x

0.0x

0.2x

0.4x

0.6x

0.8x

1.0x

1.2x

1.4x

1.6x

1.8x

2.0x

2011 2012 2013 2014 1Q15

Average Median

10.0x10.1x

11.7x

16.6x

11.1x10.1x

8.8x10.2x

14.9x

11.1x

0.0x

2.0x

4.0x

6.0x

8.0x

10.0x

12.0x

14.0x

16.0x

18.0x

2011 2012 2013 2014 1Q15

Average Median

EV/sales (FY11-1Q15) EV/EBITDA (FY11-1Q15)

Page 31DCF and valuation parameters

The luxury and cosmetics financial factbook 2015

DCF

and

val

uatio

n

para

met

ers

Analysis of worldwide M&A transactions in the luxury industry since 2011

Transaction multiplesF

• The number of completed deals on global scale is still significant, despite the financial crisis. The M&A activity from both strategic and financial investors in the industry experienced a strong first quarter in 2015 with 18 completed deals.

• PE activity was intense and stable during the past years, showing an always-stronger interest for the industry, confirmed through the creation of dedicated funds. • As presented in the graph about the top 10 markets by the number of completed deals over the FY11-1Q15 period, Italy turns out to be the first country as a target nationality, proving the attractiveness of Italian companies for investors (investors’ interest for ‘‘made in Italy’’ and brands’ high quality).

Number of completed deals in the luxury industry (global)

Number of completed deals by type of buyer (global)

Number of completed deals sorted by nationality of the target over FY11–1Q15 (among the top 10 markets)

Source: Capital IQ, Mergermarket, Factiva

4852

62

44

18

0

10

20

30

40

50

60

70

FY11 FY12 FY13 FY14 1Q15

No.

of d

eals

37

44 42

31

12118

20

13

6

23%

15%

32%

30%

33%

0%

5%

10%

15%

20%

25%

30%

35%

05

101520253035404550

FY11 FY12 FY13 FY14 1Q15Corporate PE PE/total

No.

of d

eals

Italy30%

United States28%

France12%

Switzerland14%

UK8%

India3%

HK1%

China2%

Germany

1%Netherlands

1%

Page 32 DCF and valuation parameters

The luxury and cosmetics financial factbook 2015

Analysis of worldwide M&A transactions in the cosmetics industry since 2011

Transaction multiplesF

• The number of deals completed in 2014 and in the first quarter 2015 illustrates a return to a sustained level of M&A activity after a drop in 2013.

• The dynamism of the cosmetics industry recently attracted a larger number of PE funds, respected to past years: in 2014, they were involved in 62% of the transactions globally.

• As presented in the graph about the number of completed deals by markets, quite interestingly, the first three positions are similar to those of the luxury industry, even if in a different order (US, France and Italy).

30

39

17

26

8

0

5

10

15

20

25

30

35

40

45

FY11 FY12 FY13 FY14 1Q15

No.

of d

eals

22

31

14

10

58

83

16

3

27%21%

18%

62%

38%

0%

10%

20%

30%

40%

50%

60%

70%

0

5

10

15

20

25

30

35

FY11 FY12 FY13 FY14 1Q15

No.

of d

eals

Corporate PE PE/total

United States36%

France23%

Italy8%

Germany7%

South Korea7%

United Kingdom5%

Spain4%

Japan4%

Canada3%

China3%

Number of completed deals (global)

Number of completed deals by type of buyer (global)

Number of completed deals sorted by nationality of the target over FY11-1Q15 (amongst the top 10 markets)

The luxury and cosmetics fi nancial factbook 2015

DCF

and

val

uatio

n pa

ram

eter

s

LUXURY AND COSMETICS THE EY FINANCIAL FACTBOOK 2014

Industry overview

Global luxury goods marketG

Global cosmetics marketH

Points of view from EY’s global sector specialists and outside expertsI

The luxury and cosmetics financial factbook 2015

Indu

stry

ove

rvie

w

The luxury and cosmetics financial factbook 2015

DCF

and

val

uatio

n

para

met

ers

The worldwide personal luxury goods market is estimated to have

grown by 3.0% in 2014. However, at constant exchange rates, the market-observed growth (4.0%) was comparatively slower than the 7.0% recorded in 2013.

Monobrand stores represent close to 30% of the overall market, while monobrand distribution across formats already claims

52%.

The share of company-owned retail sales has gained 10 percentage points and represents nearly one third of the luxury goods market. This reflects a trend of brands increasingly seeking global control of their operations.

In 2014, the historical pattern held true, as accessories grew

4.0% — more than any other personal luxury goods category and more than the market overall.

As accessible status symbols, shoes benefit from strong tailwinds and have been growing faster than the overall leather-goods category for the last three years.

Chinese consumers are now focused on purchasing more from overseas, with

Korea and Japan emerging as hot new destinations.

The Chinese luxury market in 2014 was in line with 2013 at €15 billion, primarily due to slowdown in the demand for watches, men’s wear and leather goods.

The online luxury goods market continued its successful run with the share of online purchases increasing to

5.0% in 2014

from 4.5% recorded last year. Retailers are still the top-performing players online, followed by e-tailers and individual brands.

Global luxury goods market

Page 36 Industry overview

Glossary

Contact us

Title for section

Welcome to the third edition of EY’s annual Financial Factbook for the luxury and cosmetics sector. The Factbook combines financial data, insight from EY’s global team of sector specialists and opinions of external experts.

XSales of industry players are expected to grow at a healthy rate, led by double-digit annual growth rate for L’Occitane and Natura from FY11A to FY14E. X Increased demand through innovative products will cater to underserved emerging markets. X Introduction of eco-friendly, sustainable and naturally derived beauty products and cosmetics will stimulate demand in established geographies.

Source: Data based on consensus of several brokers’ reports for each company.

Notes:Market capitalization is based on a one-month average as of December 2012. The 2012 growth corresponds to the sales growth rate between FY11A and FY12A/E.

Titles for charts

Titles for charts

H Global luxury goods

Sample selection

and specific analyses Executive sum

mary

DCF and valuation

parameters

Industry overview

Methodology

and disclaimer

Page 37DCF and valuation parameters

Sources: Altagamma/Bain and other selected researchNote: 1) Luxury Goods Worldwide Market Study Fall–Winter 2014, Altagamma/Bain

Global personal luxury goods continue to buoy the market, but growth is leveling off

• The worldwide personal luxury goods market is estimated to have grown by 3.0% in 2014. However, at constant exchange rates, the market-observed growth (4.0%) was comparatively slower than the 7.0% recorded in 2013.

• The growth was helped by the sharp depreciation of the euro, which left the sector with an unbalanced price structure across regions.

• Retail remained a key growth driver in 2014, but the market saw a slowdown in the retail network expansion, illustrating the players’ objective to focus on organic growth.

• The online luxury goods market continued its successful run with the share of online purchases increasing to 5.0% in 2014 from 4.5% recorded last year. Retailers are still the top-performing players online, followed by e-tailers and individual brands.

Global luxury goods marketG

159

170

167153

173192 212

218 224

250 - 2658%

7%

- 2%

- 8%

13%

11% 10%

3% 3%

-10%

-5%

0%

5%

10%

15%

-200

-150

-100

-50

0

50

100

150

200

250

300

2006 2007 2008 2009 2010 2011 2012 2013 2014e 2017e

Grow

th

€bi

llion

Market size Growth

Worldwide personal luxury goods market trend1

DCF

and

val

uatio

n

para

met

ers

Industry overview Page 37

Indu

stry

ove

rvie

w

The luxury and cosmetics financial factbook 2015

Title for section

Welcome to the third edition of EY’s annual Financial Factbook for the luxury and cosmetics sector. The Factbook combines financial data, insight from EY’s global team of sector specialists and opinions of external experts.

XSales of industry players are expected to grow at a healthy rate, led by double-digit annual growth rate for L’Occitane and Natura from FY11A to FY14E. X Increased demand through innovative products will cater to underserved emerging markets. X Introduction of eco-friendly, sustainable and naturally derived beauty products and cosmetics will stimulate demand in established geographies.

Source: Data based on consensus of several brokers’ reports for each company.

Notes:Market capitalization is based on a one-month average as of December 2012. The 2012 growth corresponds to the sales growth rate between FY11A and FY12A/E.

Titles for charts

Titles for charts

H Global luxury goods

Page 38 DCF and valuation parameters Page 38

The luxury and cosmetics financial factbook 2015

Industry overview

Global personal luxury goods market, by channel and format (2014E)2

Global luxury goods marketG

• Demand is still growing, mainly sustained by touristic consumption, which has been heavily influenced by currency fluctuations and local regulations.

• As illustrated in the graph above, there is a clear dichotomy between area of consumption and nationality, based on the exchange rate evolutions.

• China continues to be the top consumer country (1/3 of the total market), but Chinese customers tend to consume outside their home country.

• Conversely, Europe and Japan will benefit from this trend in 2015, with Japan reaching a growth leadership position and Europe particularly benefiting from dynamic touristic inflows.

1 Currency fluctuations and tourism flows heavily impact luxury consumption

• The share of company-owned retail sales has gained 10 percentage points and represent nearly one third of the luxury goods market. This reflects a trend of brands increasingly seeking global control of their operations.

• Monobrand stores represent close to 30% of the overall market, while monobrand distribution across formats already claims 52%.

• The airport channel has generated a CAGR of 11.0% from 2011 through 2014 and now represents 5.0% of total luxury sales and is particularly critical in Asia and Europe.

• The online luxury market has grown twelvefold in the past 11 years and now makes up 5.0% of total sales, mainly led by the accessories and apparel categories.

2 Company-owned retail continues to gain share

Sources: Altagamma/Bain and other selected researchNotes: 1) Business Monitor International 2) Luxury Goods Worldwide Market Study Fall-Winter 2014, Altagamma/Bain

1%

6%

1%

8%7%

4%

2%

6%

-3%

1%

-4%

-2%

0%

2%

4%

6%

8%

10%

Europe Americas Japan Mainland China ROW

2015

F gr

owth

Nationality Area

29%

27%

25%

9%

5%5%

Monobrand stores Department storesSpecialty stores Off-price storesAirport Online

Luxury goods demand growth by nationality and by area (2015F)1

Luxury goods market by geography and channel

Glossary

Contact us

Title for section

Welcome to the third edition of EY’s annual Financial Factbook for the luxury and cosmetics sector. The Factbook combines financial data, insight from EY’s global team of sector specialists and opinions of external experts.

XSales of industry players are expected to grow at a healthy rate, led by double-digit annual growth rate for L’Occitane and Natura from FY11A to FY14E. X Increased demand through innovative products will cater to underserved emerging markets. X Introduction of eco-friendly, sustainable and naturally derived beauty products and cosmetics will stimulate demand in established geographies.

Source: Data based on consensus of several brokers’ reports for each company.

Notes:Market capitalization is based on a one-month average as of December 2012. The 2012 growth corresponds to the sales growth rate between FY11A and FY12A/E.

Titles for charts

Titles for charts

H Global luxury goods

Sample selection

and specific analyses Executive sum

mary

DCF and valuation

parameters

Industry overview

Methodology

and disclaimer

Page 39DCF and valuation parameters

The Chinese luxury market is experiencing a contraction in growth, yet Chinese consumers continue to represent about a third of the global market

• The Chinese luxury market in 2014 was in line with 2013 at €15 billion, primarily due to slowdown in the demand for watches, men’s wear and leather goods.

• Like-for-like sales struggled the most due to change in customer behavior across demographic groups — increased diversity of preferred brands, and exclusivity, quality and value for money becoming increasingly more important than logos.

• Continued impact of anti-corruption and frugality campaigns undermined luxury demand and was further exacerbated by the economic slowdown.

1 Slowdown across the board

• Chinese consumers are now focused on purchasing more from overseas, with Korea and Japan emerging as hot new destinations. In 2014, there has been a 61% increase in the number of trips by Chinese nationals to these destinations.

• This dominance has further increased with the development of new outlet sites in China and the fact that Chinese travelers have been enthusiastic visitors of the many outlet malls in Europe.

• In terms of outlook, a softer economy and political pressures on gifting and high-end spending are continuing to put pressure on overall spending. However, a weak euro and the low price points are making both travel and shopping in Europe increasingly attractive.

2 Chinese consumers continue to dominate as top global customers

Global luxury goods marketG

Mainland Chinese personal luxury goods market (2011-2014E)1

Top three global personal luxury goods markets (2014E)1

China luxury demand by luxury consumer cohort2

Sources: Altagamma/Bain and other selected researchNotes: 1) Worldwide Luxury Markets Monitor, 2015 Spring Update, May 2015, Altagamma/Bain 2) Europe: Branded Consumer Goods, Goldman Sachs, February 2015

12.9

15.0 15.3 15.3

0.0

4.0

8.0

12.0

16.0

2011 2012 2013 2014E

€bi

llion

72.0

23.217.9

0

1020

3040

5060

7080

US China and HongKong

Japan

€bi

llion

Second position globally after including Hong Kong

23%27%

49%

40%

28%32%

39%36%

25%

0%

10%

20%

30%

40%

50%

60%

Middle class Affluent High net worth

2004 2014 2024

Indu

stry

ove

rvie

w

Industry overview Page 39

The luxury and cosmetics financial factbook 2015

Title for section

Welcome to the third edition of EY’s annual Financial Factbook for the luxury and cosmetics sector. The Factbook combines financial data, insight from EY’s global team of sector specialists and opinions of external experts.

XSales of industry players are expected to grow at a healthy rate, led by double-digit annual growth rate for L’Occitane and Natura from FY11A to FY14E. X Increased demand through innovative products will cater to underserved emerging markets. X Introduction of eco-friendly, sustainable and naturally derived beauty products and cosmetics will stimulate demand in established geographies.

Source: Data based on consensus of several brokers’ reports for each company.

Notes:Market capitalization is based on a one-month average as of December 2012. The 2012 growth corresponds to the sales growth rate between FY11A and FY12A/E.

Titles for charts

Titles for charts

H Global luxury goods

Page 40 DCF and valuation parameters

Accessories remain the biggest category, and it is the fastest growing

Global luxury goods marketG

• Since 2012, accessories have become the largest category within luxury goods and have grown the fastest lately, with a CAGR of 11% from 2010 through 2014.

• In 2014, the historical pattern held true, as accessories grew 4% — more than any other personal luxury goods category and more than the market overall.

• The online channel is developed well in the accessories segment and constitutes 41% of total sales.

• Soft accessories have been the top-performing luxury category in both the short and the long term.

1 Accessories: outperformer

• As accessible status symbols, shoes benefit from strong tailwinds and have been growing faster than the overall leather-goods category for the last three years. Shoe specialists are outpacing lifestyle brands, especially in the men’s segment.

• However, price as a contribution to growth has reached an unsustainable level, and implies the brands have been overpricing, particularly in the leather/accessories category, which is expected to limit the growth in the near future.

• The increase in competition is also expected to put some price pressures in the leather/accessories segment.

2 Soft accessories driving the growth

Global personal luxury goods market by product type (2014E)1

Growth rates of global personal luxury goods market by product type1

Luxury leather goods and shoes, 2011-14E2

Sources: Altagamma/Bain and other selected researchNotes: 1) Worldwide Luxury Markets Monitor, 2015 Spring Update, May 2015, Altagamma/Bain 2) Luxury Goods Worldwide Market Study Fall-Winter 2014, Altagamma/Bain

*Others include “Arts de la table”, textile furniture etc.

Accessories29%

Apparel25%

Hard luxury22%

Beauty20%

Others*4%

15%

4%

9%

5%

11%

0% 5% 10% 15% 20%

Others*

Beauty

Hard luxury

Apparel

Accessories

CAGR 10-14E

29

3436 37

11 12 13 14

0

5

10

15

20

25

30

35

40

2011 2012 2013 2014E

€bi

llion

Luxury leather goods Luxury shoes

Page 40

The luxury and cosmetics financial factbook 2015

Industry overview

The luxury and cosmetics fi nancial factbook 2015

Indu

stry

ove

rvie

w

Global cosmetic goods market

The beauty market is

set to double in size in the next 10 to 15 years, and all the world’s regions will grow, with China, the US, Brazil, India and Japan expected to become the top markets.

The global cosmetics market grew by an

estimated 3.6% during 2013, which was slightly lower than the average of 3.8% observed in the past decade.

With growth of 5.2%, the selective market continued to grow at a steady pace in 2014, bolstered by Asia, the United States and e-commerce. It contributed 29% of global growth.

Skin and hair care account for more than the half of the total market. The consumer

behavior has not changed since the crisis, and

the market has continued to expand steadily.

Cosmetics world has been reinterpreted by the digital arena, illustrating the growing interest for beauty topics in the social world, an interest that comes from a larger and more aware consumer base receptive to new product launches.

The luxury and cosmetics financial factbook 2015

Page 42 Industry overview

Glossary

Contact us

Title for section

Welcome to the third edition of EY’s annual Financial Factbook for the luxury and cosmetics sector. The Factbook combines financial data, insight from EY’s global team of sector specialists and opinions of external experts.