40

Self-Directed IRAs The Added Costs of Legal Opinions Loan Originator Compensation | | | Summer 2015

Self-Directed IRAs

The Added Costs of Legal Opinions

Loan Originator Compensation

|

|

|

Summer 2015

Points of Interest Summer 2015 Page 1

Inside This Issue From the President .................................................2

From the Editor ....................................................... 3

Sacramento Summary ...........................................5

Self-Directed IRAs .................................................. 6

Local Points of Interest ......................................... 9

2015 Summer Seminar ........................................ 10

Spring Seminar Photos ....................................... 14

Spring Seminar Sponsors ................................... 16

Spring Seminar Exhibitors ...................................17

PAC Contributors .................................................. 19

A New Leverage Risk to Consider – the Added Costs of Legal Opinions.................. 22

Consumer-Paid Transactions Under the CFPB Rule on Loan Originator Compensation .................................. 25

Get to Know Your CMA Board Members:Chuck Hershson

Odell Murry Michelle Rodriguez ........................................... 28

Stricktly Strickland ................................................31

Welcome New Members .....................................37

2520 Venture Oaks Way, Suite 150Sacramento, CA 95833

(916) 239-4080 – phone • (916) 924-7323 – [email protected]

www.californiamortgageassociation.com

Points of Interest is published by the California Mortgage Association, a voluntary trade association serving California mortgage and trust deed brokers and lenders.

2014-2015 BOARD OF DIRECTORS

Odell Murry – PresidentMAI Financial Services, Inc.

Stephen Pollack – Vice PresidentAnchor Loans, Inc.

Steve Anderson – SecretaryDFI Funding, Inc.

Mark Forbes – TreasurerF.E. Forbes Company, Inc.

Steve Belleville – Real Estate Lending Group, Inc.George Eckert – The Money Brokers

Noah Furie – Budget Mortgage CorporationGlenn Goldan – ReProp Investments, Inc.John Graziano – BaySierra Financial, Inc.

Charles Hershson – Fidelity Mortgage Lenders, Inc.David Herzer – Herzer Financial Services, Inc.

Elizabeth Knight – PLM Lender ServicesJoffrey Long – Southwestern Mortgage

Lori Randich – Redwood Mortgage CorporationMichelle Rodriguez – Woodland Hills Mortgage Corp.Pam Sosa – Standard Mortgage Financial Services, Inc.

Richard Temme – R.C. Temme CorporationRichard Wachter – Wachter Investments, Inc.

Michael Arnold & Michael Belote, Esq.Legislative Advocates

Phillip M. Adleson, Esq. Brad Rogerson, Esq. Legal Counsel Securities Counsel

CMA HEADQUARTERS STAFF

Jennifer Blevins, CMPDirector of Management Services

John BerkowitzPublications Director

Jen Gross, CMPMeeting Planner

Michael CochranWebmaster / IT Manager

Lexi HowardExecutive Director

Stephanie SchoenExhibits / Sponsors

Teresa ExciniaMembership / Advertising

Tricia Schrum, CPAAccounting

From the PresidentBy Odell Murry • 2014-2015 CMA President

Page 2 Summer 2015 Points of Interest

As my term as CMA President comes to a close, I would like to thank you all for the opportunity to lead

this wonderful organization. It has been both an honor and a privilege to serve as president, and I hope I have been able to make a positive impact on the future of CMA.

During the past two years, CMA has accomplished much and has reached many milestones, to the thanks of many, including our Vice President Steve Pollack, our Secretary Steve Anderson, our Treasurer Mark Forbes, our attorneys Phil Adleson and Brad Rogerson, our lobbyists Mike Arnold and Mike Belote, our incredible board members, various committees, and the CMA membership at large. Know that you made a difference, and be proud of your many accomplishments.

In the last two years:

■ Our Advertising and Vendors Committee, lead by Chairman Steve Rexrode, embraced new technologies to improve advertising methods for our vendors. For the first time, WiFi was provided for seminar attendees, sponsored by our vendors. We cherish our loyal vendors

Farewell Messageand greatly appreciate their unwavering support of CMA and its members. Many of our vendors and some of our members have sent CMA marketing materials to their email databases.

■ Our Amicus Committee, headed by Chairman Noah Furie and CMA Legal Counsel Phil Adleson, has done an outstanding job of staying on top of the many legal cases throughout the State of California, in addition to filing important amicus briefs on behalf of CMA where necessary. Noah Furie is a walking encyclopedia of mortgage policies and procedures; we couldn’t have a better person leading this committee. CMA hit the lottery when we engaged the services of attorney Phil Adleson. Phil has worked tirelessly and has prepared mountain after mountain of documents and training materials for CMA.

■ Our Education Committee Chairman Joffrey Long, in addition to doing an incredible job of bringing to every seminar the best private mortgage lending training programs available, established a new focus group/broker forum called The Basics of Private

Money Lending. Thanks to all Education Committee members, and, in addition to Joffrey Long, a special thanks goes to Lori Randich, Glenn Goldan, Rich Temme, and Phil Adleson.

■ The Dodd-Frank Committee, chaired by Michelle Rodriquez, broke down the very complex Dodd-Frank Act, and put in place several programs to address specific concerns, as well as created a three-part Dodd-Frank webinar series. Also, I would like to take this opportunity to thank Michelle for going the extra mile to update our organization and to draft several comment letters relating to items such as Amendments to the 2013 Mortgage Rules under the Regulation X and Regulation Z; and the Los Angeles City Foreclosure Registry Program. We also don’t want to overlook the enormous contributions made by Rich Temme, that we have all benefited from.

■ Our Ethics Committee and CMA Vice President, Steve Pollack, created and presented CMA’s revised code of ethics, which was then approved by the board.

continued on page 33

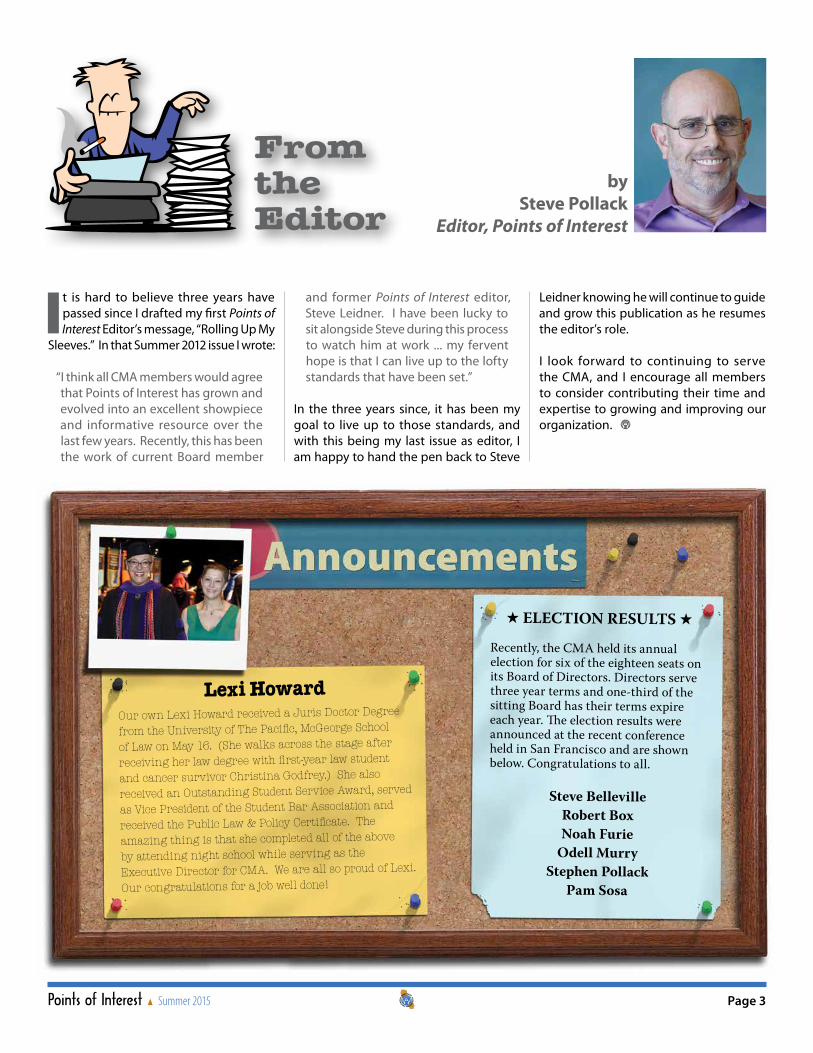

★ ELECTION RESULTS ★

Recently, the CMA held its annual election for six of the eighteen seats on its Board of Directors. Directors serve three year terms and one-third of the sitting Board has their terms expire each year. The election results were announced at the recent conference held in San Francisco and are shown below. Congratulations to all.

Steve BellevilleRobert BoxNoah Furie

Odell MurryStephen Pollack

Pam Sosa

Lexi HowardOur own Lexi Howard received a Juris Doctor Degree

from the University of The Pacific, McGeorge School

of Law on May 16. (She walks across the stage after

receiving her law degree with first-year law student

and cancer survivor Christina Godfrey.) She also

received an Outstanding Student Service Award, served

as Vice President of the Student Bar Association and

received the Public Law & Policy Certificate. The

amazing thing is that she completed all of the above

by attending night school while serving as the

Executive Director for CMA. We are all so proud of Lexi.

Our congratulations for a job well done!

Points of Interest Summer 2015 Page 3

From the Editor

bySteve Pollack

Editor, Points of Interest

t is hard to believe three years have passed since I drafted my first Points of Interest Editor’s message, “Rolling Up My

Sleeves.” In that Summer 2012 issue I wrote:

“I think all CMA members would agree that Points of Interest has grown and evolved into an excellent showpiece and informative resource over the last few years. Recently, this has been the work of current Board member

and former Points of Interest editor, Steve Leidner. I have been lucky to sit alongside Steve during this process to watch him at work ... my fervent hope is that I can live up to the lofty standards that have been set.”

In the three years since, it has been my goal to live up to those standards, and with this being my last issue as editor, I am happy to hand the pen back to Steve

Leidner knowing he will continue to guide and grow this publication as he resumes the editor’s role.

I look forward to continuing to serve the CMA, and I encourage all members to consider contributing their time and expertise to growing and improving our organization.

Page 4 Summer 2015 Points of Interest

SACRAMENTO SUMMARYBy Michael J. Arnold & Michael Belote, Esq.

Legislative Advocates

Points of Interest Summer 2015 Page 5

We are in the middle of the first year of the 2015-2016 legislative session. The Legislature has been

quite busy with the 2,500 bills which have been introduced for consideration during 2015. Your CMA legislative team is actively following 102 pieces of legislation!

On May 14, 2015 Governor Jerry Brown released his “May Revision” of the 2015-2016 California State Budget. The Governor stated in his press conference that “the state is on the rebound.” He said that the finances of the State of California have stabilized.

In January, when the Governor released his initial budget proposal, he said there would not be much money available to increase spending. However, since then, the state has seen an unexpected increase in revenue. Over $3 billion more than anticipated has come in this year. Most of that new money, if not all, will be directed

to public schools and community colleges under the state’s education funding law. Any additional funds will be deposited into the state’s rainy day fund. Also, Medi-Cal costs have soared, with over 12 million Californians now obtaining their health care coverage under this government program.

We are pleased to report that our CMA sponsored bill, SB 647 (Morrell), is moving forward in the process. The bill passed the State Senate and is now awaiting further consideration in the Assembly. The bill will 1) set the LTV limits for land producing income from crops, timber or minerals at 60%; 2) clarify that a broker has no obligation to obtain a suitability questionnaire from current investors in years when no investments are made by the investors; and 3) eliminates certain unnecessary reporting obligations for

“whole note” investments.

We have been successful, working with other groups, in challenging the following proposals to which CMA has been opposed:

AB 244 – would have included a “successor in interest” in the definition of borrower with additional changes complicating the lending law.

AB 396 – would have prohibited the owner of a rental housing accommodation from inquiring about a criminal record of an applicant.

SB 8 – would have expressed legislative intent to expand the sales tax to services, including mortgage lending fees, etc.

CMA’s legislative advocates will be busy this summer with dozens of remaining bills that have passed the house of origin and will be further considered in the second house.

Page 6 Summer 2015 Points of InterestPage 6 Summer 2015 Points of Interest

Points of Interest Summer 2015 Page 7Points of Interest Summer 2015 Page 7

continued on page 8

ecause of the volatility of the f inancial markets, mergers & acquisitions within Wall Street, and

the “fear factor” perpetrated by financial advisors, for the past ten years Americans have been seeking other options for their retirement portfolios – just as 79 million Baby-Boomers come of age!

In 2012, $1 trillion in mutual fund investments were “redeemed or cashed in” by American retail clients due to the lack of confidence within the Traditional Asset sector, as reported by Sixty Minutes in June, 2013. In recent years, due to pressure from regulators (SEC, FINRA) to inform investors of return on investment (ROI), clients have begun to question the $15 billion in “hidden” mutual fund fees and dismal returns, that have been averaging 1-3%.

Additionally, the American Investor is asking questions which demand rational answers that are not being provided by

broker-dealers, which may explain why 49% of all financial advisors were fired by their client in 2014.1 Conversely, the Alternative Asset sector is making historical headway with an influx of capital mounting to $6 trillion as of the 4th quarter of 2014. Real Estate and Private Notes leads the Asset Class for American investors seeking alternatives to the dismal returns within traditional financial markets.

Fortunately, inquisitive and determined investors found their answer in I.R.S. Code Section 408, whereby one may invest their IRA or 401(k) in “any type of asset other than a life insurance policy or a collectible item,” thereby establishing the inroads to Self-Directed IRAs and 401(k)s. Major financial institutions and banks only provide Americans with the prospect of trading stocks, bonds, annuities and mutual funds within the confines of a Retirement Savings account, yet the specific group of investors

Self-Directed IRAs

byBelinda Savage

IRA Services Trust Company

Page 8 Summer 2015 Points of Interest

Self-Directed IRAs – continued from page 7

with Self-Directed IRAs and 401(k)s (4-5% of all Americans) averaged ROI between 6-12%.

Self-Directed IRAs and 401(k)s have been in existence for 40 years, yet people are still asking, “What is a Self-Directed IRA”? As opposed to banks, broker-dealers and mutual fund companies that offer stocks, bonds and various combinations of those two asset sectors, IRA Trust Custodians are not in the business of selling you investments or providing investment advice. Trust Custodians are the “Switzerland” of IRAs and 401(k)s in that they provide, the investor or the Investment Sponsor, a service to custody clients’ retirement accounts which then can be invested in real estate, multi-family or commercial rentals or fix & flips, small businesses, technology start-ups, charter schools, vacation rentals, marina or hotel leasing, trust deeds and promissory notes. The investor chooses the project and the terms of that project.

Here is an investment example using simplified figures: Client has $100,000 in his 401(k), and plans to invest $50,000 into a fix & flip project with his brother, who is also contributing $50,000 to the property. Cost of the foreclosed house is $75,000 and it will require approximately $25,000 in rehab costs. Client establishes a Self-Directed IRA Account and transfers $50,0002 to establish the account. Then, the client authorizes the IRA to purchase the property with his brother as co-tenants in common. Brother of the client works with a contractor on the property to prepare it for sale. After refurbishing the property, client contracts the house to sell at $125,000. The brothers split the $25,000 profit and the client’s IRA receives a 25% ROI.

The key to wise investing is Education, Due-Diligence and associating with people who share your vision.

Belinda Savage may have developed her roots in the foundations of Wall Street, as an institutional bond trader in the Canadian

markets & Regional Operations Manager & Compliance Director for several national and regional broker/dealers, but she now has her focus on the leading growth sector: Alternative Assets for American investment portfolios, more specifically, retirement accounts on the Self-Directed Platform!

Ms. Savage has extensive experience and expertise within the financial markets and alternative assets- RE, Private Equity/Debt, Intellectual Property – permitting her to network with a multiplicity of professionals and associations throughout the U.S. – NYREIA, AICPA, FPA, California Mortgage Association and REIAs in CA and New York.

Presently, Belinda serves as a Consultant – Business Development – for the management team headed by Dr. Edwin Blue, Gary Shumm and Michael McNair at IRA Services Trust, which will expand their sales and marketing efforts on the West Coast and in the major metropolitan areas of America, as baby-boomers capitalize on the Alternative Asset sector.

Points of Interest Summer 2015 Page 9

ear Fellow CMA Members,

San Diego has arguably held a culinary precedent in California, given the history of Chino Farm

in Rancho Santa Fe. For over 60 years, the Chino-family run farm has served as the source of inspiration of many well-reputed chefs, including Alice Waters of Chez Panisse, Wolfgang Puck and Carl Shroeder of The Market Restaurant in Del Mar, to name a few. Visitors to the farm will discover an array of heirloom varieties of tomatoes (brandywine, cherokee purple, zebra et al.), cucumbers, mouse melons (a fruit that looks like a watermelon and tastes like a cucumber), cruciferous vegetables, cabbages, kale, lettuces, peppers, figs, and their unparalleled mara de bois strawberries, when they are in season.

Given the presence of Chino Farm in North County of San Diego, it is essential to dine at those restaurants that utilize Chino’s treasures of the earth. One of my favorites is The Market Restaurant in Del Mar where Chef Schroeder exclusively utilizes Chino’s produce, truly highlighting the brilliance of flavors that he imparts in his food. Every time I visit The Market, I order an “off the menu” salad item that comprises a mosaic of most of the produce sourced that day from Chino Farm. Whether you are vegan/vegetarian or not, order the vegetable platter entrée as a side for the table just to enjoy the diversity of preparations in Chef Schroeder’s creative use of Chino’s produce. The restaurant also has a bar/lounge that offers its own menu, including a pizza baked in a wood burning oven that equals the pie gold standard of the country (i.e., Una Pizza Napoletana in San Francisco,

Pizza Bianco in Phoenix, and Luzzo’s in East Village of Manhattan). In addition to the fine dining experience at The Market, Chef Schroeder also provides his dedicated fan base with a gourmet-gastropub alternative utilizing the same superlative ingredients from Chino Farm at the San Diego-based location, Banker’s Hill. Anything you order at Banker’s Hill will be to your comfort food liking and, like The Market, the produce will be season driven.

In San Diego you have the opportunity to experience “Farm to Table” dining at its best, thanks to the enduring passion, dedication, and integrity of the Chino Family who have blessed us all with greater jaw-dropping flavors that a chef like Carl Schroeder is extraordinarily skilled at harnessing.

The Market is located at 3702 Via De La Valle, Del Mar, CA 92014. The hours are Sun-Thurs 5:30 pm to 9:30 pm, Fri-Sat 5:30 pm to 10:00 pm. The bar opens nightly at 5:00 pm, (858) 523-0007, www.marketdelmar.com.

Banker’s Hill is located at 2202 4th Avenue, San Diego, CA 92101. The hours are Sun-Thurs 4:30 pm to 9:30 pm, Fri-Sat 4:30 pm to 10:30 pm, with a Sunday Brunch from 10:00 am to 2:30 pm (619) 231-0222, www. bankershillsd.com.

For culture, there are a few notable events. First, don’t miss the San Diego Padres who play

the Marlins on July 23rd and 24th. Second, check out the San Diego Symphony’s performance of The Divas of Disco Starring Radiance on July 24 at 7:30 pm. Finally, for the theatre lovers, check out Kiss Me Kate and Shakespeare’s Twelfth Night at The Old Globe.

Enjoy!

Culturally yours, Elliot M. Shirwo, Bolour Associates, The Entrepeneur’s Bridge Lender of Choice (www.bolourassociates.com). For more information on FOODWINEART, see www.elliotshirwofoodwineart.weebly.com.

Pre-

Sort

edFI

RST-

CLAS

SU.

S. P

OSTA

GE

PAID

SACR

AMEN

TO, C

APe

rmit

#187

6

Calif

orni

a M

ortg

age

Ass

ocia

tion

2520

Ven

ture

Oak

s W

aySu

ite 1

50Sa

cram

ento

, CA

958

33

Del Toro Loan Servicing

FIFIDDELITYELITYMORMORTGAGE LENDERSTGAGE LENDERS, IN, INC.C.C O M M E R C I A L • R E S I D E N T I AC O M M E R C I A L • R E S I D E N T I A LL

Calif

orni

a M

ortg

age

Asso

ciat

ion Sponsored By

• New Connections• New Concepts• New Knowledge• Connect with

Your Friends!

Your competitor just signed up.

Will you?

CMA San Diego. CMA

San

Dieg

o Join Us In San Diego • July 23-24, 2015

CMA

San

Die

goCalifornia Mortgage Association

WEBINAR MARKETING: More Clients, More Deals!

Securities: Protecting Your Exemptions, and What You Can Do

NEW Combined GFE/TIL: You Need It August 1 (2015)

Local Foreclosure Ordinances: Avoiding a Minefi eld

Employee Law Compliance: a Quick Brush-Up

Advertising – Good ... Advertising for Trouble – Bad

Attorney Roundtables & Speed Networking

Installation LuncheonWayne Bell*, Commissioner, California Bureau of Real EstateTom Pool, Deputy Director, California Bureau of Real Estate

Thursday Cocktail Hour

*Not confi rmed as of printing date.

California Mortgage Associationwww.californiamortgageassociation.com

Summ

er Seminar

General InformationLOCATION:

The CMA Summer Seminar will be held July 23 and 24 at the Wyndham San Diego Bayside Hotel, located at 1355 North Harbor Drive, San Diego, CA 92101. For room reservations, call the hotel at 619-232-3861 or 800-996-3426. Ask for the “California Mortgage Association” rate. Room rate is $179 per night for Standard/Single/Double through June 23, 2015 or until sold out. Discounted overnight self-parking is $20 + tax per vehicle per day, and valet parking is $32 + tax per vehicle per day. Discounted daytime event parking is $10 + tax per vehicle per day.

SEMINAR FEES:

Full registration includes all seminar events, materials, cocktail/networking reception and Friday lunch.

Registration received on or before

July 16, 2015

Registrationreceived from July 17, 2015

to date of seminar

CMA Regular Member $370 $420

Additional Attendee Same Company $320 $370

Educational Member $370 $420

Non-Member $570 $620

REFUND POLICY:

Cancellations received in writing on or before July 9, 2015 will receive a credit toward a future seminar. Cancellations not received in writing by July 9, 2015 will not receive any credit or refund.

CMA DISCLAIMER STATEMENT:

Views, statements, information, and materials provided at CMA seminars do not necessarily refl ect the views of the California Mortgage Association, its Offi cers, Directors, or Members. When considering any document, opinion, publication, or other material obtained at or from CMA or from any CMA event, attendees and recipients of the information are advised to seek qualifi ed counsel as to the suitability of that material or information for their own business operation or use.

MISCELLANEOUS:

Please wear name badges to all functions. Tickets are required for various events. Please be courteous of others and place mobile phones on silent mode. Program and speakers are subject to change without notice.

Thursday, July 23, 20157:30 am - 8:30 am Continental Breakfast / Networking in Exhibitor Area

7:30 am - 4:00 pm Registration

7:30 am - 4:00 pm Exhibitor Fair Open

8:30 am - Speed Networking – Build Contacts and Build Your Business!10:00 am MODERATORS: Pam Sosa, President, Standard Mortgage Financial Services, Inc.; Randy Newman, President, Total Lender Solutions Back by popular demand – bring a HUGE stack of business cards. You’ll be surprised by HOW MANY people

you meet! How much money are YOU losing, because you haven’t met people you see all the time at CMA? ... Scary! Be prepared to discuss what you offer – fast, and a lot! Find out who can help you! Maximize your exposure and your NET RETURN from the event!

10:00 am - 10:20 am 20 Minute Networking Break

10:20 am - Marketing – Yes! But Don’t Advertise for Trouble12:00 pm Michelle Rodriguez, Woodland Hills Mortgage Corp.; Martin T. McGuinn, Kirby & McGuinn; S. Guy Puccio, S. Guy Puccio & Associates You market and advertise your business – do you know the rules regarding advertising and marketing? How

much do you know about the BRE advertising rules, TILA, the DO NOT CALL, and other state or federal regulations? Comprehensive, practical overview of these rules along with a checklist you can take back to the offi ce. Don’t let your competitors turn you in, or regulators audit you, all because of violations of advertising rules.

12:00 pm - 2:00 pm Luncheon and PAC Drawings

2:00 pm - Distressed Property Ordinances – Your Roadmap Through the Minefi eld3:30 pm Randy Newman, President, Total Lender Solutions; Jeanee Chapman, Vice President, LRES Corp. 133 counties, cities or towns have passed ordinances regarding distressed property. Are they all the same?

No, no, no. Local “leadership” puts their own horrible stamp on ordinances and keeping up with them – it’s impossible. Got “distressed property” in your portfolio? This phrase covers a variety of descriptions. Get a list of all of the ordinances, fi nd out what to do, and avoid potential fi nes of $1,000 a day!

3:30 pm - 3:50 pm 20 Minute Networking/Refreshment Break Sponsored by Ross Diversifi ed Insurance Services

3:50 pm - New GFE/TIL – Required in 7 Days, 8 Hours, and 10 Minutes from this Seminar!5:00 pm Michelle Rodriguez, Woodland Hills Mortgage Corp. You attended the seminars, webinars, received bulletins, and did the research. Now, you’re ready to use the

new Good Faith Estimate/TILA disclosure, called TRID. Are you? Here’s YOUR last chance to get questions answered before it all starts – August 1, 2015.

5:00 pm Seminar Concludes

Friday, July 24, 2015— Open to All Attendees —

Summer Seminar— July 23-24, 2015 • San Diego, CA —

REGISTRATION FORM

3 easy ways to register!

1. Register online at

www.californiamortgageassociation.com

2. Complete and fax this form

3. Complete and mail this form

Advanced registration is recommended. Call to confi rm space availability. Please check all applicable boxes.

Attendee Name: ______________________________ Attendee Name: ______________________________

Company: ______________________________________________________________________________

Address: ___________________________________ City/State/Zip: _______________________________

Phone: _________________ Fax:____________________ E-mail: _______________________________

Dietary Restrictions (please detail): ___________________________________________________________

PAYMENT OPTIONS

Check enclosed (payable to California Mortgage Association) Please charge my Visa MasterCard AmEx

Account Number: ______________________________________ Exp. Date: ___________ CID #: ________

Name on Card: __________________________________________________________________________

Billing Address: ______________________________ City/State/Zip: _______________________________

Signature: ______________________________________________________________________________

I am opting out of the onsite binder in favor of the eBinder data link in advance of the seminar. I understand I will not receive an onsite binder.

Please provide a CMA binder at a charge of $45 (we’ll send you a link to the eBinder, too).

Please contact me about sponsorship, exhibiting, and advertising opportunities.

Please mail or fax this form with payment to:CALIFORNIA MORTGAGE ASSOCIATION

2520 Venture Oaks Way, Suite 150Sacramento, California 95833

(916) 239-4080 • (916) 924-7323 Faxwww.californiamortgageassociation.com

7:30 am - 8:30 am Continental Breakfast

7:30 am - 5:00 pm Seminar Registration

8:00 am - 10:00 am Exhibitor Set-Up

10:00 am - 6:00 pm Exhibitor Fair Open

Special Members-Only Focus Group Sessions:CMA Focus Group Sessions are open only to CMA Members.

8:30 am - Broker/Roundtables – Get Attorney ANSWERS on the Spot!10:30 am MODERATOR: Stephen Leidner, President, Lantern Financial Your questions – answered by TOP attorneys. They move from group to group, letting you ask them

DIRECTLY, getting critical knowledge and answers. Ask and hear from Dennis Doss, Ben Levinson, Martin McGuinn, Randy Newman, Michelle Rodriguez, Brad Rogerson, and Julia Wei. You’ll like the small size of the groups – giving you more opportunities to ask YOUR questions.

10:30 am - 10:50 am 20 Minute Networking Break

10:50 am - Got Employees? Get Legal – or Pay!11:50 am Pam Sosa, President, Standard Mortgage Financial Services, Inc. Are you the “HR Manager” in a small shop, or are you a LARGE EMPLOYER? Either way, you’re a target. Not

having clear policies in place, in writing, can get you a new relationship – with the Labor Board. That can cost you. Your employees may know the rules – do you? Don’t learn them from your employee’s attorney.

12:00 pm - 6:00 pm Thursday and All Day Friday are Open to All Attendees.

12:00 pm - Installation Luncheon2:00 pm KEYNOTE SPEAKERS: Wayne Bell*, Commissioner of the California Bureau of Real Estate Tom Pool, Deputy Director of the California Bureau of Real Estate

2:00 pm - They’re Securities. What’s Your Exemption?3:30 pm Dennis Doss, Doss Law; Brad Rogerson, HansonBridgett; MODERATOR: Don Hensel, President, Hensel Financial Loans you provide your investors ARE SECURITIES. You knew that. Question is, are they exempt from

registration? How? If you don’t do what is required to protect your exemption from registration – you’re selling unregistered securities. Big problem. What could you miss in preserving your exemption? Out of state investors? Borrowers? Can you do business with them? When? How? Get up to date on latest Federal and State exemptions, broker-dealer and investment advisor compliance. Whole loans? 10 investors or fewer? We’ll cover that as well.

3:30 pm - 3:50 pm 20 Minute Networking/Refreshment Break Sponsored by Total Lender Solutions

3:30 pm - Webinars – The Way to Reach Millions (It’s Possible)5:00 pm Robert Box, President, Equity Funding Resources, Inc.; Sean Morsi, CEO Mor Financial Services, Inc. There are countless reasons to include webinars as part of your marketing strategy. WHY AREN’T YOU DOING

IT? Don’t know how? Bring your laptop for a step by step demonstration of how to host your webinar ... and reach thousands (it’s possible!)

5:00 pm - 6:00 pm Cocktail and Networking Hour Sponsored by SBS Trust Deed Network

*Not confi rmed as of printing date.

EDUCATIONAL SEMINARFees are per person and include all functions unless indicated.

Registration received on or

before July 16, 2015

Registrationreceived from July 17, 2015

to date of seminar

CMA Regular Member $370 $420

Additional Attendee Same Company $320 $370

Educational Member $370 $420

Non-Member $570 $620

Registration Total $______ $______

Voluntary PAC Contribution ($20 or more) $______ $______

TOTAL ENCLOSED $______ $______

— CMA Members Only —Please note which Thursday morning

meeting(s) you will attend.

Attendee Name:____________________________________ Broker/Roundtables – Get Attorney ANSWERS on the Spot! Got Employees? Get Legal – or Pay!

Attendee Name:____________________________________ Broker/Roundtables – Get Attorney ANSWERS on the Spot! Got Employees? Get Legal – or Pay!

These sessions are open only to CMA Members.

Three

Networking

Events

EACH DAY

Don’t Miss

CMA JulyWyndham Bayside Hotel1355 North Harbor Drive

San Diego, CA 92101619-232-3861 or 800-996-3426

General InformationLOCATION:

The CMA Summer Seminar will be held July 23 and 24 at the Wyndham San Diego Bayside Hotel, located at 1355 North Harbor Drive, San Diego, CA 92101. For room reservations, call the hotel at 619-232-3861 or 800-996-3426. Ask for the “California Mortgage Association” rate. Room rate is $179 per night for Standard/Single/Double through June 23, 2015 or until sold out. Discounted overnight self-parking is $20 + tax per vehicle per day, and valet parking is $32 + tax per vehicle per day. Discounted daytime event parking is $10 + tax per vehicle per day.

SEMINAR FEES:

Full registration includes all seminar events, materials, cocktail/networking reception and Friday lunch.

Registrationreceived on or before

July 16, 2015

Registrationreceived from July 17, 2015

to date of seminar

CMA Regular Member $370 $420

Additional Attendee Same Company $320 $370

Educational Member $370 $420

Non-Member $570 $620

REFUND POLICY:

Cancellations received in writing on or before July 9, 2015 will receive a credit toward a future seminar. Cancellations not received in writing by July 9, 2015 will not receive any credit or refund.

CMA DISCLAIMER STATEMENT:

Views, statements, information, and materials provided at CMA seminars do not necessarily reflect the views of the California Mortgage Association, its Officers, Directors,or Members. When considering any document, opinion,publication, or other material obtained at or from CMAor from any CMA event, attendees and recipients of the information are advised to seek qualified counsel as to the suitability of that material or information for their own business operation or use.

MISCELLANEOUS:

Please wear name badges to all functions. Tickets arerequired for various events. Please be courteous of others and place mobile phones on silent mode. Program and speakers are subject to change without notice.

Thursday, July 23, 20157:30 am - 8:30 am Continental Breakfast / Networking in Exhibitor Area

7:30 am - 4:00 pm Registration

7:30 am - 4:00 pm Exhibitor Fair Open

8:30 am - Speed Networking – Build Contacts and Build Your Business!10:00 am MODERATORS: Pam Sosa, President, Standard Mortgage Financial Services, Inc.;

Randy Newman, President, Total Lender SolutionsBack by popular demand – bring a HUGE stack of business cards. You’ll be surprised by HOW MANY people you meet! How much money are YOU losing, because you haven’t met people you see all the time at CMA? ... Scary! Be prepared to discuss what you offer – fast, and a lot! Find out who can help you! Maximize your exposure and your NET RETURN from the event!

10:00 am - 10:20 am 20 Minute Networking Break

10:20 am - Marketing – Yes! But Don’t Advertise for Trouble12:00 pm Michelle Rodriguez, Woodland Hills Mortgage Corp.; Martin T. McGuinn, Kirby & McGuinn;

S. Guy Puccio, S. Guy Puccio & AssociatesYou market and advertise your business – do you know the rules regarding advertising and marketing? How much do you know about the BRE advertising rules, TILA, the DO NOT CALL, and other state or federal regulations? Comprehensive, practical overview of these rules along with a checklist you can take back to theoffi ce. Don’t let your competitors turn you in, or regulators audit you, all because of violations of advertising rules.

12:00 pm - 2:00 pm Luncheon and PAC Drawings

2:00 pm - Distressed Property Ordinances – Your Roadmap Through the Minefield3:30 pm Randy Newman, President, Total Lender Solutions; Jeanee Chapman, Vice President, LRES Corp.

133 counties, cities or towns have passed ordinances regarding distressed property. Are they all the same? No, no, no. Local “leadership” puts their own horrible stamp on ordinances and keeping up with them – it’s impossible. Got “distressed property” in your portfolio? This phrase covers a variety of descriptions. Get a list of all of the ordinances, find out what to do, and avoid potential fines of $1,000 a day!

3:30 pm - 3:50 pm 20 Minute Networking/Refreshment BreakSponsored by Ross Diversified Insurance Services

3:50 pm - New GFE/TIL – Required in 7 Days, 8 Hours, and 10 Minutes from this Seminar!5:00 pm Michelle Rodriguez, Woodland Hills Mortgage Corp.

You attended the seminars, webinars, received bulletins, and did the research. Now, you’re ready to use the new Good Faith Estimate/TILA disclosure, called TRID. Are you? Here’s YOUR last chance to get questions answered before it all starts – August 1, 2015.

5:00 pm Seminar Concludes

Friday, July 24, 2015— Open to All Attendees —

Summer Seminar— July 23-24, 2015 • San Diego, CA —

REGISTRATION FORM

3easy waysto register!

1. Register online at www.californiamortgageassociation.com

2. Complete and fax this form

3. Complete and mail this form

Advanced registration is recommended. Call to confirm space availability. Please check all applicable boxes.

Attendee Name: ______________________________ Attendee Name: ______________________________

Company: ______________________________________________________________________________

Address: ___________________________________ City/State/Zip: _______________________________

Phone: _________________ Fax:____________________ E-mail: _______________________________

Dietary Restrictions (please detail): ___________________________________________________________

PAYMENT OPTIONS

Check enclosed (payable to California Mortgage Association) Please charge my Visa MasterCard AmEx

Account Number: ______________________________________ Exp. Date: ___________ CID #: ________

Name on Card: __________________________________________________________________________

Billing Address: ______________________________ City/State/Zip: _______________________________

Signature: ______________________________________________________________________________

I am opting out of the onsite binder in favor of the eBinder data link in advance of the seminar. I understand I will not receive an onsite binder.

Please provide a CMA binder at a charge of $45 (we’ll send you a link to the eBinder, too).

Please contact me about sponsorship, exhibiting, and advertising opportunities.

Please mail or fax this form with payment to:CALIFORNIA MORTGAGE ASSOCIATION

2520 Venture Oaks Way, Suite 150Sacramento, California 95833

(916) 239-4080 • (916) 924-7323 Faxwww.californiamortgageassociation.com

7:30 am - 8:30 am Continental Breakfast

7:30 am - 5:00 pm Seminar Registration

8:00 am - 10:00 am Exhibitor Set-Up

10:00 am - 6:00 pm Exhibitor Fair Open

Special Members-Only Focus Group Sessions:CMA Focus Group Sessions are open only to CMA Members.

8:30 am - Broker/Roundtables – Get Attorney ANSWERS on the Spot!10:30 am MODERATOR: Stephen Leidner, President, Lantern Financial

Your questions – answered by TOP attorneys. They move from group to group, letting you ask them DIRECTLY, getting critical knowledge and answers. Ask and hear from Dennis Doss, Ben Levinson, Martin McGuinn, Randy Newman, Michelle Rodriguez, Brad Rogerson, and Julia Wei. You’ll like the small size of the groups – giving you more opportunities to ask YOUR questions.

10:30 am - 10:50 am 20 Minute Networking Break

10:50 am - Got Employees? Get Legal – or Pay!11:50 am Pam Sosa, President, Standard Mortgage Financial Services, Inc.

Are you the “HR Manager” in a small shop, or are you a LARGE EMPLOYER? Either way, you’re a target. Not having clear policies in place, in writing, can get you a new relationship – with the Labor Board. That can cost you. Your employees may know the rules – do you? Don’t learn them from your employee’s attorney.

12:00 pm - 6:00 pm Thursday and All Day Friday are Open to All Attendees.

12:00 pm - Installation Luncheon2:00 pm KEYNOTE SPEAKERS: Wayne Bell*, Commissioner of the California Bureau of Real Estate

Tom Pool, Deputy Director of the California Bureau of Real Estate

2:00 pm - They’re Securities. What’s Your Exemption?3:30 pm Dennis Doss, Doss Law; Brad Rogerson, HansonBridgett;

MODERATOR: Don Hensel, President, Hensel FinancialLoans you provide your investors ARE SECURITIES. You knew that. Question is, are they exempt from registration? How? If you don’t do what is required to protect your exemption from registration – you’re selling unregistered securities. Big problem. What could you miss in preserving your exemption? Out of state investors? Borrowers? Can you do business with them? When? How? Get up to date on latest Federal and State exemptions, broker-dealer and investment advisor compliance. Whole loans? 10 investors or fewer? We’ll cover that as well.

3:30 pm - 3:50 pm 20 Minute Networking/Refreshment BreakSponsored by Total Lender Solutions

3:30 pm - Webinars – The Way to Reach Millions (It’s Possible)5:00 pm Robert Box, President, Equity Funding Resources, Inc.; Sean Morsi, CEO Mor Financial Services, Inc.

There are countless reasons to include webinars as part of your marketing strategy. WHY AREN’T YOU DOING IT? Don’t know how? Bring your laptop for a step-by-step demonstration of how to host your webinar ... and reach thousands (it’s possible!)

5:00 pm - 6:00 pm Cocktail and Networking HourSponsored by SBS Trust Deed Network

*Not confi rmed as of printing date.

EDUCATIONAL SEMINARFees are per person and include all functions unless indicated.

Registrationreceived on or

before July 16, 2015

Registrationreceived from July 17, 2015

to date of seminar

CMA Regular Member $370 $420

Additional Attendee Same Company $320 $370

Educational Member $370 $420

Non-Member $570 $620

Registration Total $______ $______

Voluntary PAC Contribution ($20 or more) $______ $______

TOTAL ENCLOSED $______ $______

— CMA Members Only —Please note which Thursday morning

meeting(s) you will attend.

Attendee Name:____________________________________ Broker/Roundtables – Get Attorney ANSWERS on the Spot! Got Employees? Get Legal – or Pay!

Attendee Name:____________________________________ Broker/Roundtables – Get Attorney ANSWERS on the Spot! Got Employees? Get Legal – or Pay!

These sessions are open only to CMA Members.

Three

Networking

Events

EACH DAY

Don’t Miss

CMA JulyWyndham Bayside Hotel1355 North Harbor Drive

San Diego, CA 92101619-232-3861 or 800-996-3426

General InformationLOCATION:

The CMA Summer Seminar will be held July 23 and 24 at the Wyndham San Diego Bayside Hotel, located at 1355 North Harbor Drive, San Diego, CA 92101. For room reservations, call the hotel at 619-232-3861 or 800-996-3426. Ask for the “California Mortgage Association” rate. Room rate is $179 per night for Standard/Single/Double through June 23, 2015 or until sold out. Discounted overnight self-parking is $20 + tax per vehicle per day, and valet parking is $32 + tax per vehicle per day. Discounted daytime event parking is $10 + tax per vehicle per day.

SEMINAR FEES:

Full registration includes all seminar events, materials, cocktail/networking reception and Friday lunch.

Registration received on or before

July 16, 2015

Registrationreceived from July 17, 2015

to date of seminar

CMA Regular Member $370 $420

Additional Attendee Same Company $320 $370

Educational Member $370 $420

Non-Member $570 $620

REFUND POLICY:

Cancellations received in writing on or before July 9, 2015 will receive a credit toward a future seminar. Cancellations not received in writing by July 9, 2015 will not receive any credit or refund.

CMA DISCLAIMER STATEMENT:

Views, statements, information, and materials provided at CMA seminars do not necessarily refl ect the views of the California Mortgage Association, its Offi cers, Directors, or Members. When considering any document, opinion, publication, or other material obtained at or from CMA or from any CMA event, attendees and recipients of the information are advised to seek qualifi ed counsel as to the suitability of that material or information for their own business operation or use.

MISCELLANEOUS:

Please wear name badges to all functions. Tickets are required for various events. Please be courteous of others and place mobile phones on silent mode. Program and speakers are subject to change without notice.

Thursday, July 23, 20157:30 am - 8:30 am Continental Breakfast / Networking in Exhibitor Area

7:30 am - 4:00 pm Registration

7:30 am - 4:00 pm Exhibitor Fair Open

8:30 am - Speed Networking – Build Contacts and Build Your Business!10:00 am MODERATORS: Pam Sosa, President, Standard Mortgage Financial Services, Inc.; Randy Newman, President, Total Lender Solutions Back by popular demand – bring a HUGE stack of business cards. You’ll be surprised by HOW MANY people

you meet! How much money are YOU losing, because you haven’t met people you see all the time at CMA? ... Scary! Be prepared to discuss what you offer – fast, and a lot! Find out who can help you! Maximize your exposure and your NET RETURN from the event!

10:00 am - 10:20 am 20 Minute Networking Break

10:20 am - Marketing – Yes! But Don’t Advertise for Trouble12:00 pm Michelle Rodriguez, Woodland Hills Mortgage Corp.; Martin T. McGuinn, Kirby & McGuinn; S. Guy Puccio, S. Guy Puccio & Associates You market and advertise your business – do you know the rules regarding advertising and marketing? How

much do you know about the BRE advertising rules, TILA, the DO NOT CALL, and other state or federal regulations? Comprehensive, practical overview of these rules along with a checklist you can take back to the offi ce. Don’t let your competitors turn you in, or regulators audit you, all because of violations of advertising rules.

12:00 pm - 2:00 pm Luncheon and PAC Drawings

2:00 pm - Distressed Property Ordinances – Your Roadmap Through the Minefi eld3:30 pm Randy Newman, President, Total Lender Solutions; Jeanee Chapman, Vice President, LRES Corp. 133 counties, cities or towns have passed ordinances regarding distressed property. Are they all the same?

No, no, no. Local “leadership” puts their own horrible stamp on ordinances and keeping up with them – it’s impossible. Got “distressed property” in your portfolio? This phrase covers a variety of descriptions. Get a list of all of the ordinances, fi nd out what to do, and avoid potential fi nes of $1,000 a day!

3:30 pm - 3:50 pm 20 Minute Networking/Refreshment Break Sponsored by Ross Diversifi ed Insurance Services

3:50 pm - New GFE/TIL – Required in 7 Days, 8 Hours, and 10 Minutes from this Seminar!5:00 pm Michelle Rodriguez, Woodland Hills Mortgage Corp. You attended the seminars, webinars, received bulletins, and did the research. Now, you’re ready to use the

new Good Faith Estimate/TILA disclosure, called TRID. Are you? Here’s YOUR last chance to get questions answered before it all starts – August 1, 2015.

5:00 pm Seminar Concludes

Friday, July 24, 2015— Open to All Attendees —

Summer Seminar— July 23-24, 2015 • San Diego, CA —

REGISTRATION FORM

3 easy ways to register!

1. Register online at

www.californiamortgageassociation.com

2. Complete and fax this form

3. Complete and mail this form

Advanced registration is recommended. Call to confi rm space availability. Please check all applicable boxes.

Attendee Name: ______________________________ Attendee Name: ______________________________

Company: ______________________________________________________________________________

Address: ___________________________________ City/State/Zip: _______________________________

Phone: _________________ Fax:____________________ E-mail: _______________________________

Dietary Restrictions (please detail): ___________________________________________________________

PAYMENT OPTIONS

Check enclosed (payable to California Mortgage Association) Please charge my Visa MasterCard AmEx

Account Number: ______________________________________ Exp. Date: ___________ CID #: ________

Name on Card: __________________________________________________________________________

Billing Address: ______________________________ City/State/Zip: _______________________________

Signature: ______________________________________________________________________________

I am opting out of the onsite binder in favor of the eBinder data link in advance of the seminar. I understand I will not receive an onsite binder.

Please provide a CMA binder at a charge of $45 (we’ll send you a link to the eBinder, too).

Please contact me about sponsorship, exhibiting, and advertising opportunities.

Please mail or fax this form with payment to:CALIFORNIA MORTGAGE ASSOCIATION

2520 Venture Oaks Way, Suite 150Sacramento, California 95833

(916) 239-4080 • (916) 924-7323 Faxwww.californiamortgageassociation.com

7:30 am - 8:30 am Continental Breakfast

7:30 am - 5:00 pm Seminar Registration

8:00 am - 10:00 am Exhibitor Set-Up

10:00 am - 6:00 pm Exhibitor Fair Open

Special Members-Only Focus Group Sessions:CMA Focus Group Sessions are open only to CMA Members.

8:30 am - Broker/Roundtables – Get Attorney ANSWERS on the Spot!10:30 am MODERATOR: Stephen Leidner, President, Lantern Financial Your questions – answered by TOP attorneys. They move from group to group, letting you ask them

DIRECTLY, getting critical knowledge and answers. Ask and hear from Dennis Doss, Ben Levinson, Martin McGuinn, Randy Newman, Michelle Rodriguez, Brad Rogerson, and Julia Wei. You’ll like the small size of the groups – giving you more opportunities to ask YOUR questions.

10:30 am - 10:50 am 20 Minute Networking Break

10:50 am - Got Employees? Get Legal – or Pay!11:50 am Pam Sosa, President, Standard Mortgage Financial Services, Inc. Are you the “HR Manager” in a small shop, or are you a LARGE EMPLOYER? Either way, you’re a target. Not

having clear policies in place, in writing, can get you a new relationship – with the Labor Board. That can cost you. Your employees may know the rules – do you? Don’t learn them from your employee’s attorney.

12:00 pm - 6:00 pm Thursday and All Day Friday are Open to All Attendees.

12:00 pm - Installation Luncheon2:00 pm KEYNOTE SPEAKERS: Wayne Bell*, Commissioner of the California Bureau of Real Estate Tom Pool, Deputy Director of the California Bureau of Real Estate

2:00 pm - They’re Securities. What’s Your Exemption?3:30 pm Dennis Doss, Doss Law; Brad Rogerson, HansonBridgett; MODERATOR: Don Hensel, President, Hensel Financial Loans you provide your investors ARE SECURITIES. You knew that. Question is, are they exempt from

registration? How? If you don’t do what is required to protect your exemption from registration – you’re selling unregistered securities. Big problem. What could you miss in preserving your exemption? Out of state investors? Borrowers? Can you do business with them? When? How? Get up to date on latest Federal and State exemptions, broker-dealer and investment advisor compliance. Whole loans? 10 investors or fewer? We’ll cover that as well.

3:30 pm - 3:50 pm 20 Minute Networking/Refreshment Break Sponsored by Total Lender Solutions

3:30 pm - Webinars – The Way to Reach Millions (It’s Possible)5:00 pm Robert Box, President, Equity Funding Resources, Inc.; Sean Morsi, CEO Mor Financial Services, Inc. There are countless reasons to include webinars as part of your marketing strategy. WHY AREN’T YOU DOING

IT? Don’t know how? Bring your laptop for a step by step demonstration of how to host your webinar ... and reach thousands (it’s possible!)

5:00 pm - 6:00 pm Cocktail and Networking Hour Sponsored by SBS Trust Deed Network

*Not confi rmed as of printing date.

EDUCATIONAL SEMINARFees are per person and include all functions unless indicated.

Registration received on or

before July 16, 2015

Registrationreceived from July 17, 2015

to date of seminar

CMA Regular Member $370 $420

Additional Attendee Same Company $320 $370

Educational Member $370 $420

Non-Member $570 $620

Registration Total $______ $______

Voluntary PAC Contribution ($20 or more) $______ $______

TOTAL ENCLOSED $______ $______

— CMA Members Only —Please note which Thursday morning

meeting(s) you will attend.

Attendee Name:____________________________________ Broker/Roundtables – Get Attorney ANSWERS on the Spot! Got Employees? Get Legal – or Pay!

Attendee Name:____________________________________ Broker/Roundtables – Get Attorney ANSWERS on the Spot! Got Employees? Get Legal – or Pay!

These sessions are open only to CMA Members.

Three

Networking

Events

EACH DAY

Don’t Miss

CMA JulyWyndham Bayside Hotel1355 North Harbor Drive

San Diego, CA 92101619-232-3861 or 800-996-3426

Page 14 Summer 2015 Points of Interest

Pictures From the Spring Seminar – May 14-15 – San Francisco

To view this member-only content, become a member of CMA

Points of Interest Summer 2015 Page 15

CMA’s positive influence is crucial for our survival. Send your contribution today!

It’s easy to donate:Online at www.californiamortgageassociation.com

— or —Send the additional amount with your monthly CMA dues

— or —Write a check to “CMA PAC” and send it today to:

2520 Venture Oaks Way, Suite 150 • Sacramento, CA 95833

PROTECT YOUR INDUSTRY – CONTRIBUTE TODAY!For more information contact:

Richard Wachter, Chairperson, CMA PAC Fundraising Committee 1-800-308-4961

$ 1 0 0,0 0 0Goal

$58,598raised so far since

July 1, 2014

DON ATE TO THE CM A PAC TODAY !

Our PAC and our advocates in Sacramento always operate in full compliance with all laws and regulations relating to efforts to influence the public policy process. We would never engage in any type of quid-pro-quo on public policy issues or entertain contributions in return for access. We support legislators who are philosophically aligned with the interests of our membership and who work to ensure a business environment which allows our members to flourish.

Pictures From the Spring Seminar – May 14-15 – San Francisco

To view this member-only content, become a member of CMA

Page 16 Summer 2015 Points of Interest

Thank You to Our Spring Seminar Sponsors

— Wi-Fi Services for All Attendees —Fidelity Mortgage Lenders

& Mortgage+Care

— Thursday Evening Cocktail Hour —SBS Trust Deed Network

— Friday Wine & Cheese Networking —PLM Lender Services, Inc. &

Ross Diversified Insurance Services

— Tote Bags —The Mortgage Office

— Thursday Breakfast & Friday Breakfast —Total Lender Solutions

& IRA Services

To view this member-only content, become a member of CMA

Points of Interest Summer 2015 Page 17

Applied Business Software, Inc.2847 Gundry AvenueLong Beach, CA 90755

800.833.3343 – p / 562.279.7404 – fContact: AJ Poulin

E-mail: [email protected]: www.themortgageoffice.com

Product/Service: Loan Servicing Software

Armanino, LLP12657 Alcosta Boulevard, Suite 500

San Ramon, CA 94583925.790.2600 – p / 925.790.2601 – f

Contact: Jason GilbertE-mail: [email protected]

Website: www.armaninollp.comProduct/Service: Accounting

Bolour Associates8383 Wilshire Boulevard, Suite 920

Beverly Hills, CA 90211323.677.0550 – p / 323.677.0522 – f

Contact: Elliot ShirwoE-mail: [email protected]: www.bolourassociates.com

Product/Service: Real Estate Investment / Finance Development

BuildZig1211 Embarcadero Way, Suite D

Oakland, CA 94606800.380.0180 – p / 866.703.5150 – f

Contact: John BohannonE-mail: [email protected]

Website: www.buildzig.comProduct/Service: Real Estate Development /

Funds Control

Del Toro Loan Servicing2300 Boswell Road, Suite 215

Chula Vista, CA 91914619.474.5400 – p / 877.826.7834 – f

Contact: Drew LouisE-mail: [email protected]

Website: www.deltoroloanservicing.comProduct/Service: Loan Servicing / Foreclosure /

Loan Docs

IRA Services Trust Company 1160 Industrial Road, Suite 1

San Carlos, CA 94070650.593.2221 – p / 650.591.2168 – f

Contact: Belinda SavageE-mail: [email protected]: www.iraservices.com

Product/Service: IRA Custodial Services

LendingHome201 Post Street, Floor 12San Francisco, CA 94105

858.945.1393 – pContact: Josh Stech

E-mail: [email protected]: www.lendinghome.comProduct/Service: N / O / O Loans

Mortgage+Care Loan Servicing29222 Rancho Viejo Road, Suite 209

San Juan Capistrano, CA 92675800.481.2708 – p / 650.745.7088 – f

Contact: Bob SpierE-mail: [email protected]

Website: www.mortcare.comProduct/Service: Loan Software

Olympia Financial16633 Ventura Boulevard

Encino, CA 91436818.885.8585 – p / 818.788.8471 – f

Contact: Jeff AronsonE-mail: [email protected]

Website: www.olympiafin.comProduct/Service: Lender

Thank You to Our Spring Exhibitors

To view this member-only content, become a member of CMA

Page 18 Summer 2015 Points of Interest

Peak Corporate Network5900 Canoga Avenue, Suite 400

Woodland Hills, CA 91367818.591.3300 – p / 818.591.2990 – f

Contact: Mike UrbanE-mail: [email protected]: www.peakcorp.com

Product/Service: Loan Servicing / Foreclosure Services

Polycomp3000 Lava Ridge Court, Suite 130

Roseville, CA 95661916.773.3480 – p / 916.773.3484 – f

Contact: Stacy SheetzE-mail: [email protected]: www.polycomp.net

Product/Service: Self-Directed IRA

Private Mortgage Fund, LLC23586 Calabasas Road, Suite 100

Calabasas, CA 91302818.702.2551 – p / 818.222.1793 – f

Contact: Randy Van DueckE-mail: [email protected]: www.pmfundllc.com

Product/Service: Hard Money Fund

Ross Diversified Insurance Services2922 East Chapman Avenue, Suite 203

Orange, CA 92869714.633.7677 – p / 714.633.7788 – f

Contact: Mel BabtkisE-mail: [email protected]: www.rossdiv.com

Product/Service: Insurance Products

SBS Trust Deed Network31194 La Baya Drive, Suite 106

Westlake Village, CA 91362818.991.4600 – p / 818.874.9500 – f

Contact: Mitch WilletE-mail: [email protected]: www.sbstrustdeed.com

Product/Service: Foreclosure Services / REO

Spiegel Accountancy Corp.2033 North Main Street, Suite 365

Walnut Creek, CA 94596925.977.4000 – p / 925.977.4015 – f

Contact: Jeff SpiegelE-mail: [email protected]

Website: www.spiegelcorp.comProduct/Service: CPA

Thank You to Our Spring Exhibitors

Total Lender Solutions, Inc.6540 Lusk Boulevard, Suite C238

San Diego, CA 92121866.535.3736 – p / 858.630.5570 – f

Contact: Randy NewmanE-mail: [email protected]

Website: www.totallendersolutions.comProduct/Service: Foreclosure / Default Services

PLM Lender Services, Inc.46 North Second Street

Campbell, CA 95008408.370.4030 – p / 408.370.5484 – f

Contact: Elizabeth KnightE-mail: [email protected]

Website: www.plmweb.comProduct/Service: Loan Servicing / Foreclosure /

Loan Doc Drawing

PENSCO Trust Company595 Market Street, 4th Floor

San Francisco, CA 94105415.395.5729 – p

Contact: Mike HoweE-mail: [email protected]

Website: www.pensco.comProduct/Service: Self-Directed IRA

To view this member-only content, become a member of CMA

Points of Interest Summer 2015 Page 19

Thank You 2014-15 PAC Contributors!$2,000 – $6,800

Anchor Loans, Inc.Calabasas

Equity Funding Resource, Inc.

Sherman Oaks

Southwest MortgageGranada Hills

$1,000 – $1,999

Adleson, Hess & Kelly, a P.C.Campbell

Budget Mortgage Corp.Los Angeles

Creative Realty Marketing & Mortgage

Bakersfield

Fidelity Mortgage Lenders, Inc.Los Angeles

Geraci Law FirmIrvine

Herzer Financial Services, Inc.Redwood City

Lantern Financial Corp.Sherman Oaks

PLM Lender Services, Inc.Campbell

Roza Real Estate Loans Inc.San Francisco

$500 – $999

BaySierra Financial, Inc.Santa Rosa

FCI Lender Services, Inc.Anaheim Hills

Law Office of Benjamin R. Levinson, APC

Campbell

Law Office of Peter N. BrewerPalo Alto

MAI Financial Services, Inc.Toluca Lake

MOR FinancialLos Angeles

Mortgage Securities Inc.Encinitas

National Equity Funding, Inc.Irvine

Redwood Mortgage Corp.San Mateo

Total Lender Solutions, Inc.San Diego

$200 – $499

A.S.K. Investments, Inc.Stanton

Abundance RealtyMilpitas

All California FundingStudio City

Allstar Financial Services, Inc.Woodland Hills

Applied Business SoftwareLong Beach

Bolour AssociatesBeverly Hills

California Home LoansSan Jose

California Western Financial Investments, Inc.

Los Alamitos

Cal-Pac Capital AdvisorsNewport Beach

Cirius CapitalSan Jose

Cushman Rexrode Capital CorporationOakland

David A. Duner, CPAIrvine

Del Toro Loan Servicing, Inc.Chula Vista

Diamond PotransDiamond Bar

Equity Bridge CapitalSan Francisco

Equity Funding Source, Inc.Los Angeles

continued on page 20

Standard Mortgage Financial Services Inc.

Riverside

Stonecrest FinancialSan Jose

Trilion CapitalSan Diego

Wachter Investments, Inc.Burlingame

$1,000 – $1,999 continued

Woodland Hills Mortgage CorpWoodland Hills

Woody Financial Realty Corp.Long Beach

$500 – $999 continued

To view this member-only content, become a member of CMA

Page 20 Summer 2015 Points of Interest

Thank You 2014-15 PAC Contributors!Athas Capital Group

Calabasas Hills

Available Home Loans, Inc.San Bernardino

BayMark Financial Inc.San Mateo

Baypoint Mortgage Inc.,Granada Hills

Best AllianceVan Nuys

Blackburne & BrownSacramento

Buchalter Nemer, A Professional Law Corporation

Los Angeles

Cal-West Home Loans, IncSan Carlos

Capital Benefit, Inc.Newport Beach

Cascade Capital ServicesBuellton

Chuck Birkett TsoongPasadena

Commercial Mortgage CorporationSan Mateo

Cournale & Co.San Francisco

Crawford Investment CompanySan Bernardino

Creative Capital Group, Inc.Seal Beach

Custom Financial Services Inc.Torrance

Dark Horse DevelopmentOakland

Datacom Investment Co.Trabuco Canyon

DFI Funding, Inc.Emeryville

DMA Corp.Cathedral City

Doss LawSilverado

Duane Gomer SeminarsMission Viejo

E.F. Foley & Co., Inc.San Jose

Elmer F. Karpe, Inc.Bakersfield

F.E. Forbes Company Inc.Berkeley

FJM Capital, Inc.San Rafael

Hanson Bridgett LLPSan Francisco

Hensel Financial, Inc.Carlsbad

Kirby & McGuinn, A P.C.San Diego

Mid Valley Services, Inc.Fresno

Monterey Bay Resources, Inc.Soquel

Mortgage Vintage, Inc.Newport Beach

Mortgage+Care LOAN SERVICING SOFTSan Juan Capistrano

Note Servicing CenterChowchilla

Olympia Mortgage & Investment Co., Inc.Grass Valley

Pacific Capital Loans, LLCCalabasas

Pacific Private MoneyNovato

Pacific West Mortgage Fund, LLCTorrance

Private Financial, Inc.Sherman Oaks

Private Mortgage Fund, LLCCalabasas

Redwood Trust Deed Services, Inc.Santa Rosa

ReProp FinancialEureka

Residential First MortgageIrvine

Ross Diversified Insurance Services, Inc.Orange

$200 – $499 continued

S.B.S. Trust Deed NetworkWestlake Village

Salas FinancialSan Diego

Selzer Home LoansUkiah

SFR Ventures, IncWalnut Creek

Showcase Investments, Inc.Glendale

Socotra CapitalSacramento

Sonoma Equity Lending, Inc.Petaluma

Spiegel Accountancy Corp.Walnut Creek

Sterling Pacific Lending, Inc.Watsonville

Sunset MortgageMission Viejo

The Argus GroupWoodland Hills

The Helvetica GroupCarlsbad

Unitrust Mortgage, Inc.San Diego

Val-Chris Investments, Inc.Irvine

Watsonville MortgageWatsonville

Windvest CorporationSan Diego

$200 – $499 continued

continued on page 21

$20 – $199

A-1 Loans & InvestmentsSanta Rosa

Action Funding, Inc.Woodland Hills

Agricultural FinanceHayward

Alliance PortfolioAliso Viejo

$20 – $199 continued

To view this member-only content, become a member of CMA

Points of Interest Summer 2015 Page 21

Thank You 2014-15 PAC Contributors!Peak Corporate Network

Woodland Hills

Pelorus Equity GroupLaguna Hills

Pfeifer & De La Mora, LLPOrange

PMB Capital, Inc.Calabasas

Premier Money Source, Inc.Corona Del Mar

PrideCo Capital Management, LLCNewport Beach

Private Capital InvestmentsAlamo

PROPELIANBeverly Hills

Provident TitleGlendale

R.C. Temme CorpWoodland Hills

Real Estate Lending Group, Inc.San Jose

Realty Capital Lending GroupDowney

Roebuck & CompanyAlameda

Royalty Mortgage CompanyRancho Cucamonga

SDC Capital FundingTarzana

Security Financial ServicesSan Francisco

Sequoian Investments, IncSan Diego

Sterling Pacific Financial, Inc..Santa Rosa

Streit LendingVan Nuys

The Evergreen AdvantageSanta Monica

The Money BrokersSacramento

The Nikols CompanyNewport Beach

The Norris GroupRiverside

The Three WisemenEl Segundo

Twin Pier CapitolSanta Monica

$20 – $199 continuedV.I.P. Trust Deed Company

Montrose

Valley Mortgage Investments, Inc.Bakersfield

Value Point Capital, Inc.Laguna Niguel

Westside Capital Management, LLCLos Angeles

Yale Street MortgagePasadena

Zinc Financial, Inc.Clovis

$20 – $199 continuedEquity Mortgage & Investments

Modesto

Equity Wave LendingIrvine

Excel FinancialSan Jose

Gasbarro Investments, Inc.Calabasas

Golden West Foreclosure Service, Inc.Redwood City

Granite Funding Inc.Rancho Cordova

Hamilton Ridge Asset ManagementSan Jose

Harmon Financial CorporationModesto

Helvetica GroupCalsbad

I.R., Inc. dba Investors RealtyBakersfield

IRA Services Trust CompanySan Carlos

JMJ Financial GroupGarden Grove

La Mesa Fund ControlLa Mesa

Lending Bee, IncNorth Hollywood

LendingHome CorporationSan Francisco

McCormick & CoSanta Rosa

Methven & Associates PCBerkeley

Mortgage Lender Services, Inc.Folsom

N A Nationwide MortgageMission Viejo

Olympia Financial Mortgage Inc.Encino

OnPoint Services, Inc.San Diego

Pacific Horizon Financial, Inc.San Diego

Pacific Loanworks, Inc.Covina

Park West Financial, Inc.Los Angeles

Partner EquitySan Francisco

$20 – $199 continued

PAC Announcements:

• Thursday Cocktail Party – Apple iPad WInner: Sandy MacDougall

• Friday Luncheon – Apple Watch

Winner: San Cohn, National Equity Funding

• Friday Luncheon – Apple iPad

Winner: Shafiq Taymuree, Stonecrest Financial

To view this member-only content, become a member of CMA

Page 22 Summer 2015 Points of Interest

A s a securities attorney I have had many discussions over the years with mortgage fund managers

regarding the use of leverage to enhance the yield of a mortgage fund. These conversations tended to include the usual warnings about the perils of leverage and the need to clearly disclose the additional risks leverage entails in their offering documents. Then, right around 2009 and 2010, the topic ceased to come up. Apparently, lenders that previously made leverage loans to private mortgage funds were off somewhere licking their financial crisis wounds. As we move into the second half of 2015, however, the fog of the financial crisis has all but lifted and leverage lenders have once again appeared that are willing to lend to private mortgage funds.

A New Leverage Warning

Now, one might think that the return of leverage lenders would prompt me to dust off my usual leverage warnings and to once again focus upon the dire consequences of leverage and failing to fully disclose the additional risks leverage entails. That,

A New Leverage Risk to Consider – the Added Costs of Legal Opinions

however, is not the case ... not today anyway. While all these warnings continue to be true (and how quickly we forget), today I warn not of a risk of nondisclosure or of a potential risk faced by investors in leveraged funds. Today, I bring a warning to the fund manager standing in the unfamiliar shoes of a borrower. Don’t ignore a legal opinion requirement in the term sheet for your leverage loan until it’s too late.

It is an issue I have seen now on more than one occasion and it relates to the structuring of leverage loans by certain lenders as if the loans were part of a much larger asset backed securitization transaction (“ABS transaction”) by requiring: (i) that the borrower be a special purpose, bankruptcy remote entity (“SPE”); and (ii) that the borrower deliver legal opinions usually reserved for ABS transactions as a condition to closing the loan. The use of an SPE itself involves issues that a mortgage fund manager must consider; however, in my experience, it is the opinion requirement that is more easily overlooked or underappreciated by fund managers when assessing the costs and benefits of obtaining these type of loans.

Legal Opinion Requirements

A discussion of the purpose and scope of the various types of legal opinions is beyond the scope of this article; however, given the audience, it might be helpful to think of a legal opinion as similar to an estoppel certificate. Just as a tenant estoppel certificate is relied upon by a lender to preclude the tenant from later arguing about issues pertaining to the status of the lease, a legal opinion allows the recipient to rely on the opinion of borrower’s counsel as to issues related to the borrower and the loan transaction. By obtaining a legal opinion with respect to such matters the lender, rating agency or other recipient of the opinion is ostensibly precluding the borrower from raising these issues in the future.

Legal opinions are nothing new and certain types of legal opinions are very common. In large loan (and other) transactions borrower’s counsel is often called upon to issue opinions for the benefit of the lender

continued on page 23

byBrad Rogerson

Hanson Bridgett, LLP

Points of Interest Summer 2015 Page 23

on certain issues related to the transaction. Generally, these include (i) a “due formation” or “ due authorization” opinions, confirming that the borrower parties have been duly organized and are authorized to enter into the transaction documents; and (ii) an

“enforceability” opinion, establishing (among other things) that the transaction documents are enforceable against the borrower parties under the laws of the state governing such documents. In ABS Transactions, however, one or more additional opinions related to the SPE structure of the transaction are required. Generally referred to as “non-consolidation” opinions and “true sale” opinions (if applicable), these additional opinions, in essence, confirm that the SPE used in the transaction will not be legally affected by the bankruptcy or insolvency of any parent or affiliate of the SPE.

In ABS transactions, due formation, enforceability, non-consolidation and true sale opinions are required by the rating agencies the lender has engaged to rate the asset backed securities being issued in connection with the subsequent ABS transaction. Leverage loans to private

mortgage funds, on the other hand, have traditionally not involved the use of an SPE or required these types of legal opinions. This is because they were usually not considered large enough loan transactions and they were not generally collateralized by the lenders in further ABS transactions.

Recently, however, certain lenders have begun to require the use of SPEs and the issuance of ABS type legal opinions in connection with credit lines being marketed to private mortgage funds. This appears to be true even in cases where the lender is not contemplating engaging in an ABS transaction with respect to the loan and the loan amount is far less than the traditional amount required to warrant costs associated with this structure.

Legal Opinion Considerations

There are two primary questions a mortgage fund manager should immediately consider when assessing loan terms that require the borrower to deliver any legal opinion as a condition of the loan. First, the manager must determine exactly what type of

opinions are being required by the lender and identify the legal counsel that will issue the required opinions. The manager may simply assume that the fund’s usual attorney will give whatever legal opinions are required; however, the fund’s usual attorney may not be willing or able to give one or more of the opinions on the fund’s behalf. For example, if an enforceability opinion is required with respect to loan documents that are governed by the laws of another state, the fund’s attorney may be precluded from giving the required opinion. In that event, the fund may be required to engage local counsel solely for the purpose of issuing such an opinion. Moreover, non-consolidation opinions and true sale opinions relate primarily to bankruptcy and insolvency matters and attorneys or law firms without experience in these areas of law may be unwilling to give these types of opinions as a matter of policy. Again, if that is the case, the fund may be required to engage separate counsel for the sole purpose of issuing the required opinion.

The New Leverage – continued from page 22

continued on page 24

Page 24 Summer 2015 Points of Interest

The New Leverage – continued from page 23

The second issue is, of course, the cost of obtaining the required legal opinions. Legal fees for the various types of legal opinions that may be required vary widely from state to state, firm to firm, and attorney to attorney. So, even if counsel is located that is willing and able to issue the required opinion, the amount of legal fees charged for such opinion should be clearly stated and understood. Many attorneys and law firms view legal opinions as tantamount to issuing an insurance policy for the transaction. If this type of firm has no other involvement in the transaction, the legal fees required just to conduct the adequate due diligence for the opinion can exceed tens of thousands of dollars. If several types of opinions are being issued and more than one issuing attorney is involved, the costs of delivering the opinions alone can reach $50,000 to $75,000 or more very quickly. Depending on the circumstances, however, it may be possible to locate attorneys willing to issue one or more of the required opinions for far less because they either specialize in issuing the required opinion or don’t regard the risks of opinion practice as being so great. If the opinion requirements aren’t identified and

addressed early enough, however, locating and engaging these types of attorneys becomes much more difficult.

Assessments to be Made Prior to Commitment

Given the foregoing, it is important for any fund manager seeking to obtain fund financing to be aware of the issues and costs associated with a legal opinion requirement. Loan terms requiring the use of an SPE should alert the manager that legal opinions may be required; however, other loan structures may also require the delivery of some type of legal opinion. General language in a term sheet referring to the delivery of “customary” or “usual” legal opinions should be immediately clarified with the lender and the specific types of opinions being required should be determined. If one or more opinions can not be eliminated through negotiations with the lender, a clear assessment of who will provide each opinion, and the cost of each opinion, should be made. Most importantly, this assessment should be made prior to execution of the term sheet for the loan or

otherwise obligating the fund with respect to the loan. Failure to identify the issue until after the fund becomes obligated on the loan may prove a costly mistake.

Brad Rogerson (Hanson Bridgett LLP) represents clients in a wide range of real estate finance and business transactions, including debt and equity f inancing, complex workouts, mortgage lending and investment, public and private securities offerings and real estate purchase and sale transactions. Brad devotes a portion of his practice to private mortgage lending and investment and has considerable experience representing California real estate brokers, investment advisors, finance lenders, mortgage funds and other private lenders in connection with licensing requirements, regulatory compliance, audits and enforcement procedures brought by the California Department of Real Estate, the California Department of Corporations and other regulatory agencies. He also represents CMA as its Securities Counsel. He can be reached at (415) 995-5898 or [email protected].

Points of Interest Summer 2015 Page 25

Sixteen months have now passed since the effective date of the CFPB’s rule on loan originator compensation

(the “CFPB Rule”)1 and, given its lack of clarity, it continues to pose significant compliance challenges for the mortgage industry. The earlier Federal Reserve rule on loan originator compensation (the

“Fed Rule”)2 was equally opaque, and one would have hoped that the Bureau, when drafting its Rule, might have offered some definitive guidance on “real life” scenarios that affect the mortgage industry daily. Unfortunately, it didn’t. As a result, many aspects of the CFPB Rule remain a struggle for the mortgage industry, including whether a loan originator’s compensation on a consumer-paid transaction must be the same as it would have been in an equivalent “creditor-paid” transaction with that lender.

While some well-intentioned lenders and mortgage brokers have concluded that consumer-paid compensation may vary from loan to loan, others have

byG. Bradley Hargrave

Medlin & Hargrave

Consumer-Paid Transactions Under the CFPB Rule on Loan Originator Compensation

analyzed the CFPB Rule and arrived at the opposite conclusion. And still others have decided to permit compensation variances between “consumer-paid” and