Sell‐Side Due Diligence: Preparing a Business For Sale August 17, 2017 DHG Birmingham CPE Seminar 1 Sell-Side Due Diligence: Preparing a Business For Sale Dustin Hamilton 2 transaction advisory Sell-Side Due Diligence

Transcript

Sell‐Side Due Diligence: Preparing a Business For Sale

August 17, 2017

DHG Birmingham CPE Seminar 1

1transaction advisory

Sell-Side Due Diligence: Preparing a Business For SaleDustin Hamilton

2transaction advisory

Sell-Side Due Diligence

Sell‐Side Due Diligence: Preparing a Business For Sale

August 17, 2017

DHG Birmingham CPE Seminar 2

3transaction advisory

What is Sell-Side Due Diligence

4transaction advisory

What is Sell-Side Due Diligence?

Sell-side due diligence challenges and assists the seller to look at their business and financial position from a critical perspective, and rationally assess the opportunities and risks facing their company.

Sell‐Side Due Diligence: Preparing a Business For Sale

August 17, 2017

DHG Birmingham CPE Seminar 3

5transaction advisory

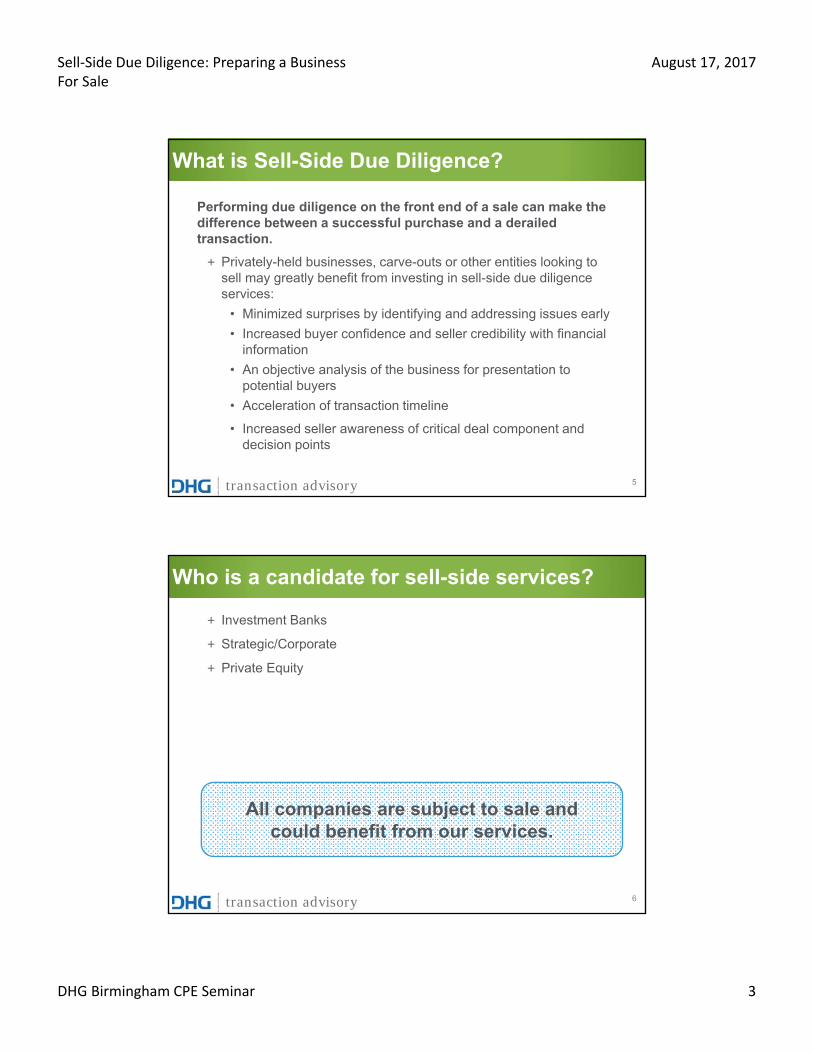

What is Sell-Side Due Diligence?

Performing due diligence on the front end of a sale can make the difference between a successful purchase and a derailed transaction.

+ Privately-held businesses, carve-outs or other entities looking to sell may greatly benefit from investing in sell-side due diligence services:

• Minimized surprises by identifying and addressing issues early

• Increased buyer confidence and seller credibility with financial information

• An objective analysis of the business for presentation to potential buyers

• Acceleration of transaction timeline

• Increased seller awareness of critical deal component and decision points

6transaction advisory

Who is a candidate for sell-side services?

+ Investment Banks

+ Strategic/Corporate

+ Private Equity

All companies are subject to sale and could benefit from our services.

Sell‐Side Due Diligence: Preparing a Business For Sale

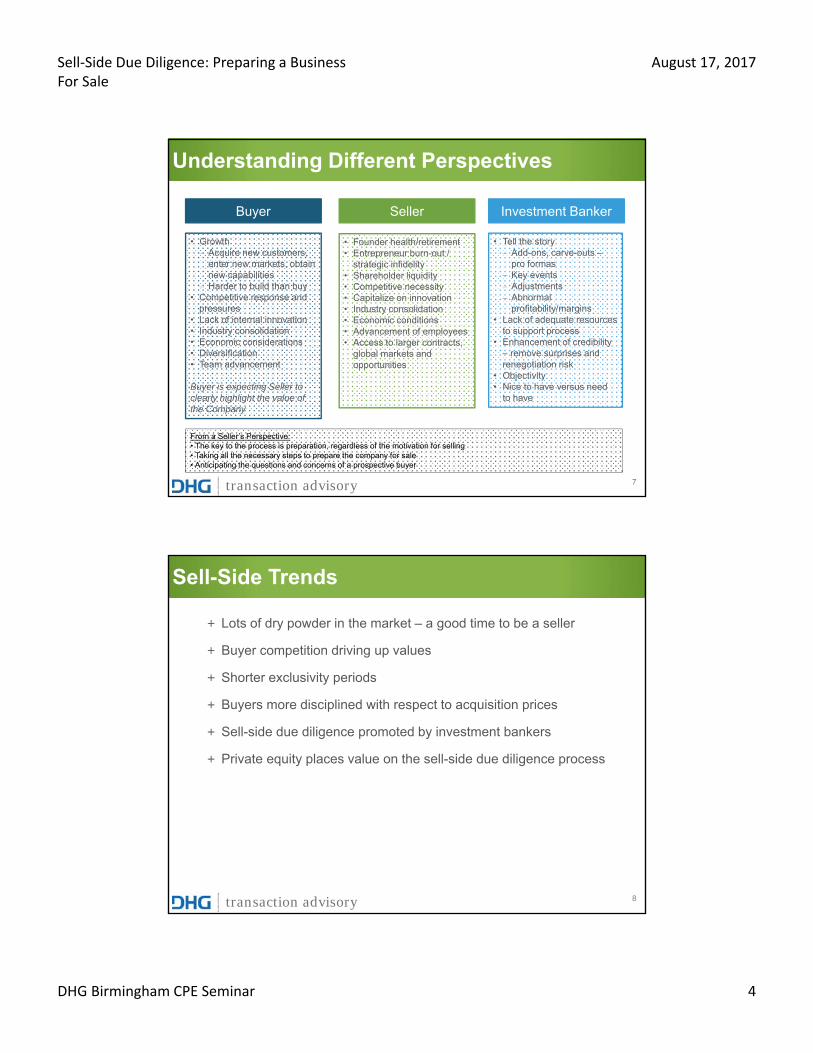

strategic infidelity• Shareholder liquidity• Competitive necessity• Capitalize on innovation• Industry consolidation• Economic conditions• Advancement of employees• Access to larger contracts,

global markets and opportunities

• Growth‒ Acquire new customers,

enter new markets, obtain new capabilities

‒ Harder to build than buy• Competitive response and

pressures• Lack of internal innovation• Industry consolidation• Economic considerations• Diversification• Team advancement

Buyer is expecting Seller to clearly highlight the value of the Company

From a Seller’s Perspective:• The key to the process is preparation, regardless of the motivation for selling• Taking all the necessary steps to prepare the company for sale• Anticipating the questions and concerns of a prospective buyer

8transaction advisory

Sell-Side Trends

+ Lots of dry powder in the market – a good time to be a seller

+ Buyer competition driving up values

+ Shorter exclusivity periods

+ Buyers more disciplined with respect to acquisition prices

+ Sell-side due diligence promoted by investment bankers

+ Private equity places value on the sell-side due diligence process

Sell‐Side Due Diligence: Preparing a Business For Sale

August 17, 2017

DHG Birmingham CPE Seminar 5

9transaction advisory

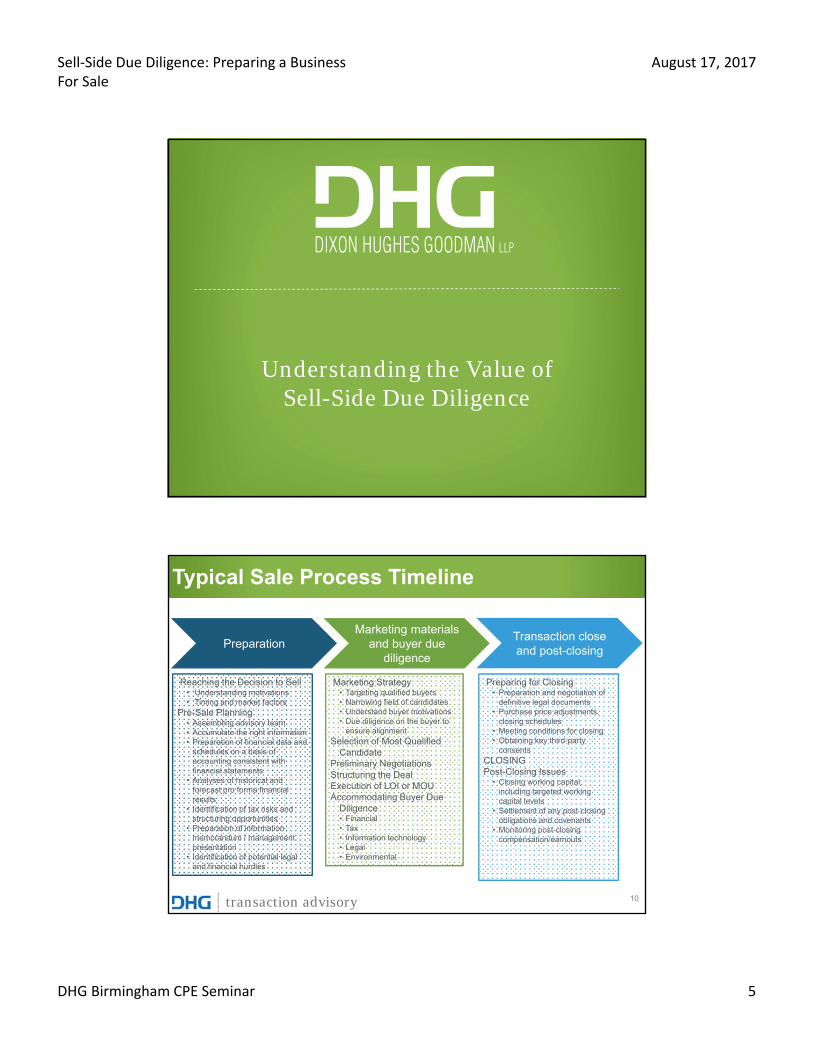

Understanding the Value of Sell-Side Due Diligence

10transaction advisory

Typical Sale Process Timeline

PreparationMarketing materials

and buyer due diligence

Transaction close and post-closing

Reaching the Decision to Sell• Understanding motivations• Timing and market factors

Pre-Sale Planning• Assembling advisory team• Accumulate the right information• Preparation of financial data and

schedules on a basis of accounting consistent with financial statements

• Analyses of historical and forecast pro forma financial results

• Identification of tax risks and structuring opportunities

• Preparation of information memorandum / management presentation

• Identification of potential legal and financial hurdles

Marketing Strategy• Targeting qualified buyers• Narrowing field of candidates• Understand buyer motivations• Due diligence on the buyer to

ensure alignmentSelection of Most Qualified

CandidatePreliminary NegotiationsStructuring the Deal Execution of LOI or MOUAccommodating Buyer Due

Diligence• Financial• Tax• Information technology• Legal• Environmental

Preparing for Closing• Preparation and negotiation of

closing schedules• Meeting conditions for closing• Obtaining key third-party

consentsCLOSINGPost-Closing Issues

• Closing working capital, including targeted working capital levels

• Settlement of any post-closing obligations and covenants

• Monitoring post-closing compensation/earnouts

Sell‐Side Due Diligence: Preparing a Business For Sale

August 17, 2017

DHG Birmingham CPE Seminar 6

11transaction advisory

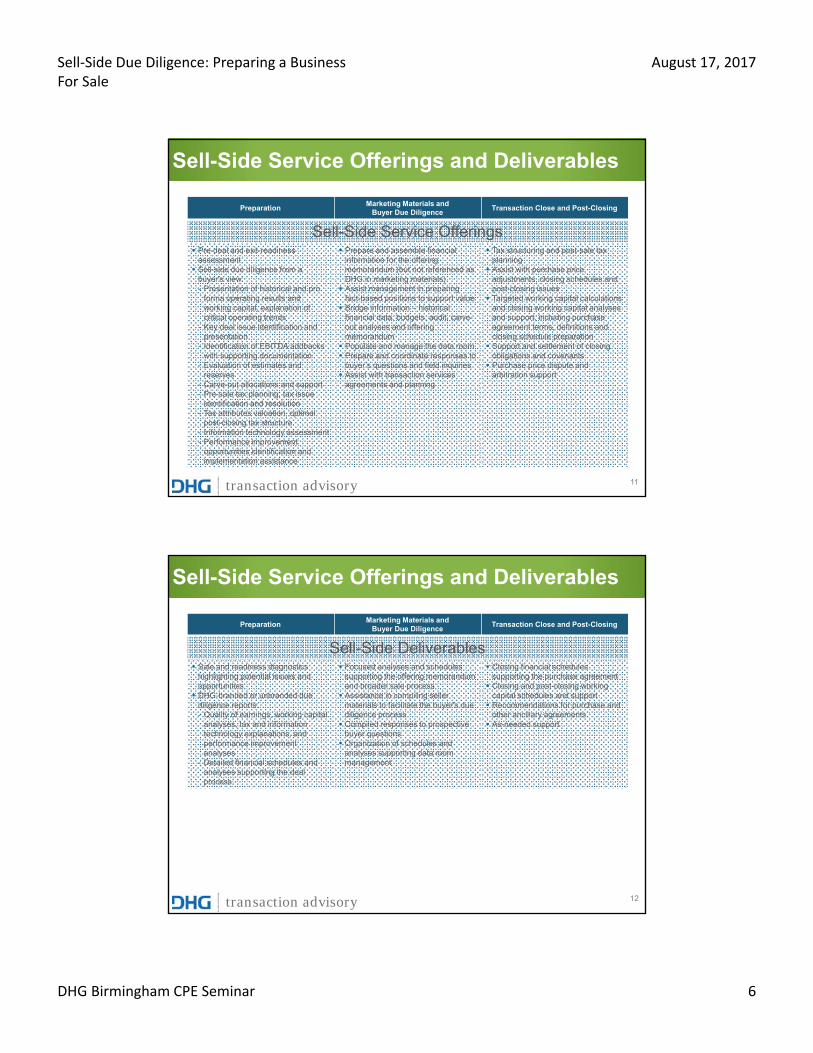

Sell-Side Service Offerings and Deliverables

PreparationMarketing Materials and

Buyer Due DiligenceTransaction Close and Post-Closing

Sell-Side Service Offerings Pre-deal and exit-readiness

assessment Sell-side due diligence from a

buyer's view:- Presentation of historical and pro

forma operating results and working capital, explanation of critical operating trends

- Key deal issue identification andpresentation

- Identification of EBITDA addbacks with supporting documentation

- Evaluation of estimates and reserves

- Carve-out allocations and support- Pre-sale tax planning, tax issue

identification and resolution- Tax attributes valuation, optimal

post-closing tax structure- Information technology assessment- Performance improvement

opportunities identification and implementation assistance

Prepare and assemble financial information for the offering memorandum (but not referenced as DHG in marketing materials) Assist management in preparing

fact-based positions to support value Bridge information – historical

financial data, budgets, audit, carve-out analyses and offering memorandum Populate and manage the data room Prepare and coordinate responses to

buyer’s questions and field inquiries Assist with transaction services

agreements and planning

Tax structuring and post-sale tax planning Assist with purchase price

adjustments, closing schedules and post-closing issues Targeted working capital calculations

and closing working capital analyses and support, including purchase agreement terms, definitions and closing schedule preparation Support and settlement of closing

obligations and covenants Purchase price dispute and

arbitration support

12transaction advisory

Sell-Side Service Offerings and Deliverables

PreparationMarketing Materials and

Buyer Due DiligenceTransaction Close and Post-Closing

Sell-Side Deliverables Sale and readiness diagnostics

highlighting potential issues and opportunities DHG-branded or unbranded due

diligence reports:- Quality of earnings, working capital

analyses, tax and information technology explanations, and performance improvement analyses

- Detailed financial schedules and analyses supporting the deal process

Focused analyses and schedules supporting the offering memorandum and broader sale process Assistance in compiling seller

materials to facilitate the buyer's due diligence process Compiled responses to prospective

buyer questions Organization of schedules and

analyses supporting data room management

Closing financial schedules supporting the purchase agreement Closing and post-closing working

capital schedules and support Recommendations for purchase and

other ancillary agreements As-needed support

Sell‐Side Due Diligence: Preparing a Business For Sale

August 17, 2017

DHG Birmingham CPE Seminar 7

13transaction advisory

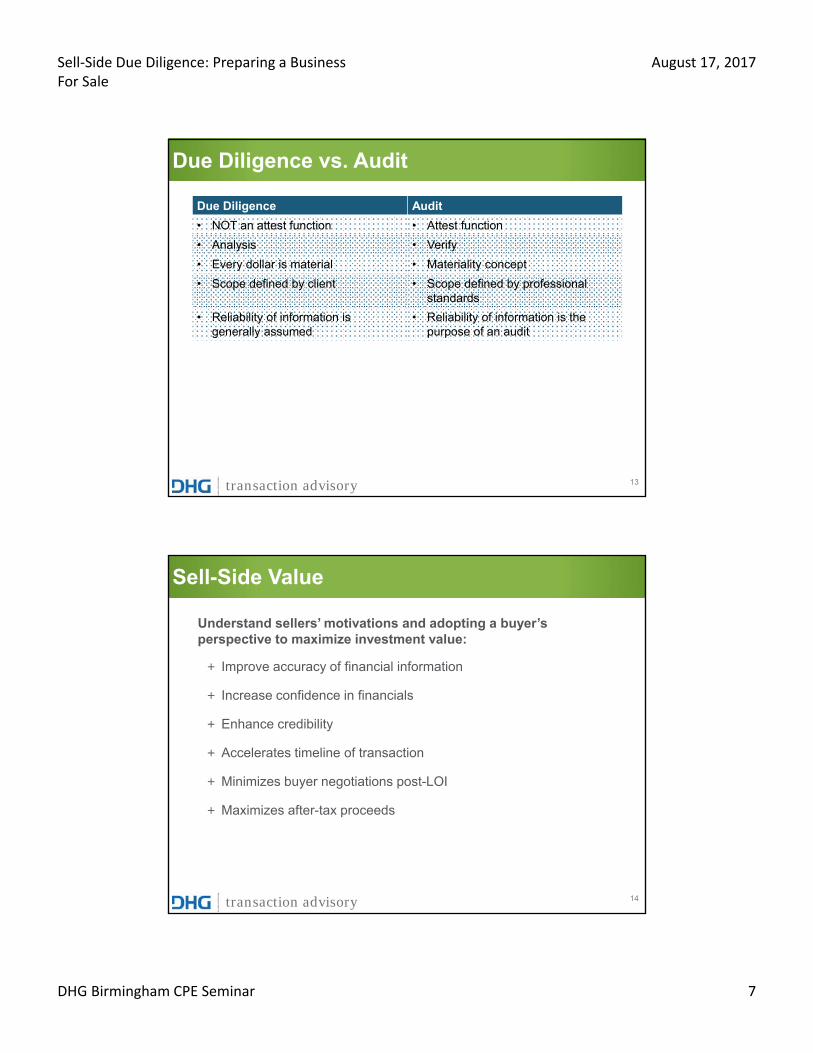

Due Diligence vs. Audit

Due Diligence Audit

• NOT an attest function • Attest function

• Analysis • Verify

• Every dollar is material • Materiality concept

• Scope defined by client • Scope defined by professional standards

• Reliability of information is generally assumed

• Reliability of information is the purpose of an audit

14transaction advisory

Sell-Side Value

Understand sellers’ motivations and adopting a buyer’s perspective to maximize investment value:

+ Improve accuracy of financial information

+ Increase confidence in financials

+ Enhance credibility

+ Accelerates timeline of transaction

+ Minimizes buyer negotiations post-LOI

+ Maximizes after-tax proceeds

Sell‐Side Due Diligence: Preparing a Business For Sale

August 17, 2017

DHG Birmingham CPE Seminar 8

15transaction advisory

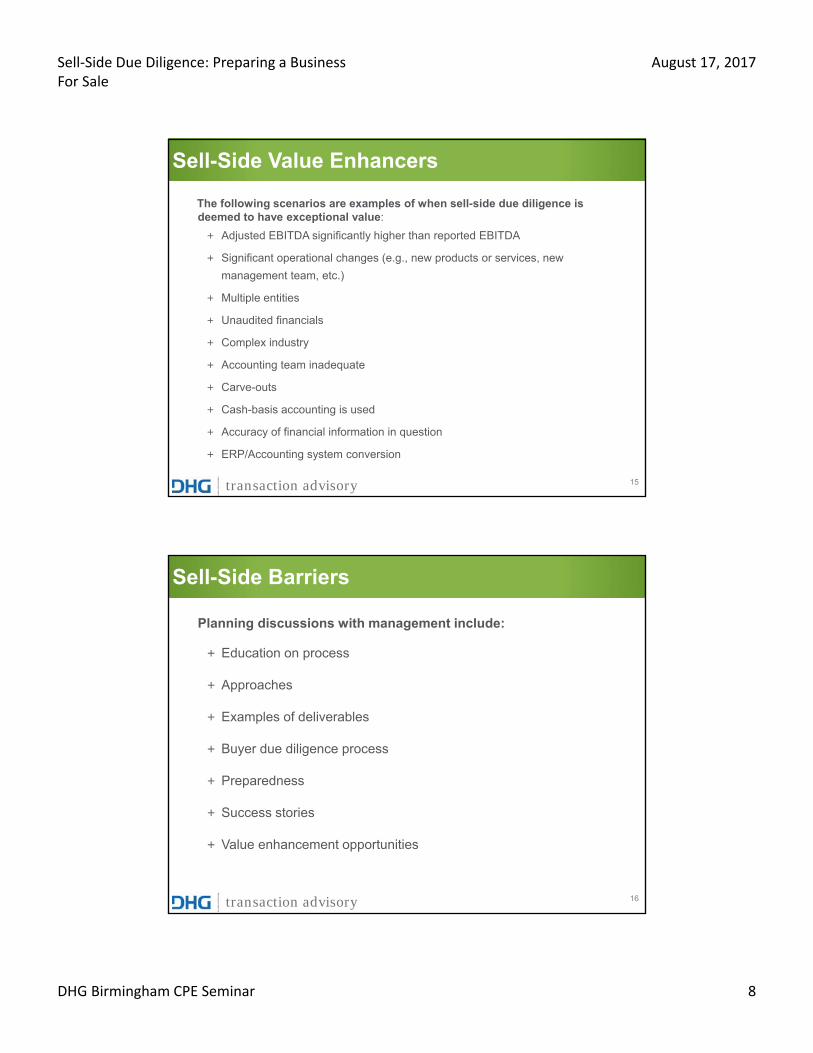

Sell-Side Value Enhancers

The following scenarios are examples of when sell-side due diligence is deemed to have exceptional value:

+ Adjusted EBITDA significantly higher than reported EBITDA

+ Significant operational changes (e.g., new products or services, new

management team, etc.)

+ Multiple entities

+ Unaudited financials

+ Complex industry

+ Accounting team inadequate

+ Carve-outs

+ Cash-basis accounting is used

+ Accuracy of financial information in question

+ ERP/Accounting system conversion

16transaction advisory

Sell-Side Barriers

Planning discussions with management include:

+ Education on process

+ Approaches

+ Examples of deliverables

+ Buyer due diligence process

+ Preparedness

+ Success stories

+ Value enhancement opportunities

Sell‐Side Due Diligence: Preparing a Business For Sale

August 17, 2017

DHG Birmingham CPE Seminar 9

17transaction advisory

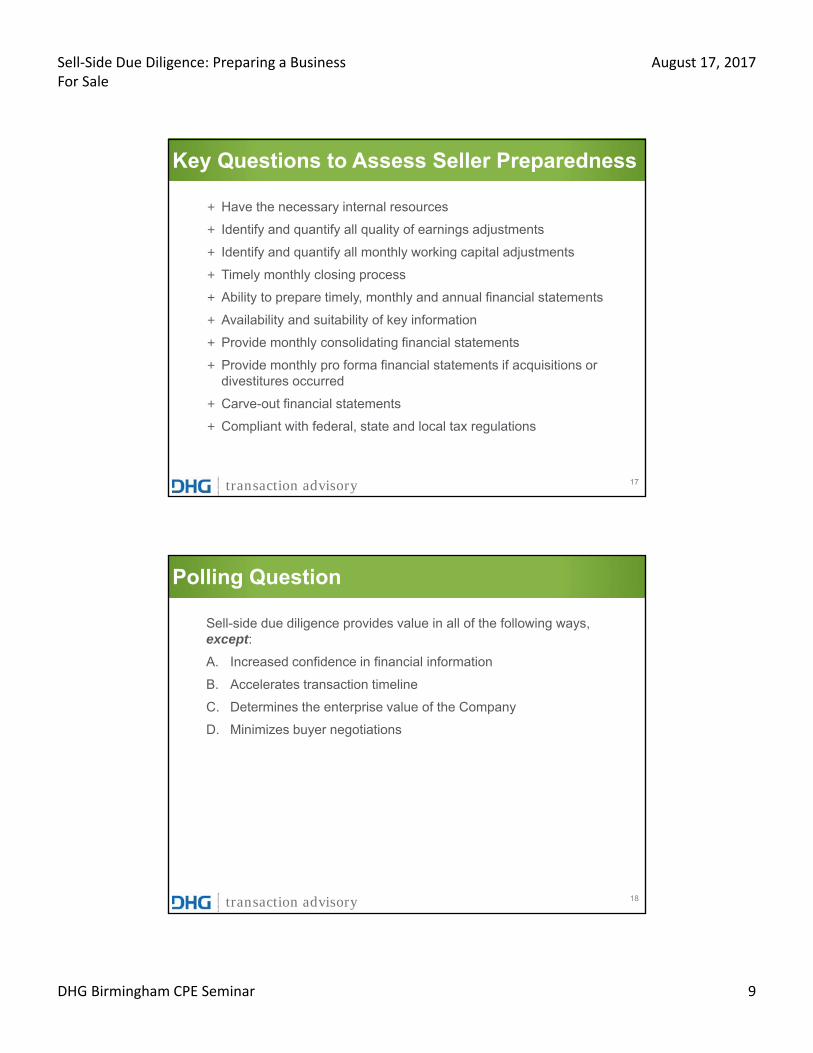

Key Questions to Assess Seller Preparedness

+ Have the necessary internal resources

+ Identify and quantify all quality of earnings adjustments

+ Identify and quantify all monthly working capital adjustments

+ Timely monthly closing process

+ Ability to prepare timely, monthly and annual financial statements

+ Availability and suitability of key information

+ Provide monthly consolidating financial statements

+ Provide monthly pro forma financial statements if acquisitions or divestitures occurred

+ Carve-out financial statements

+ Compliant with federal, state and local tax regulations

18transaction advisory

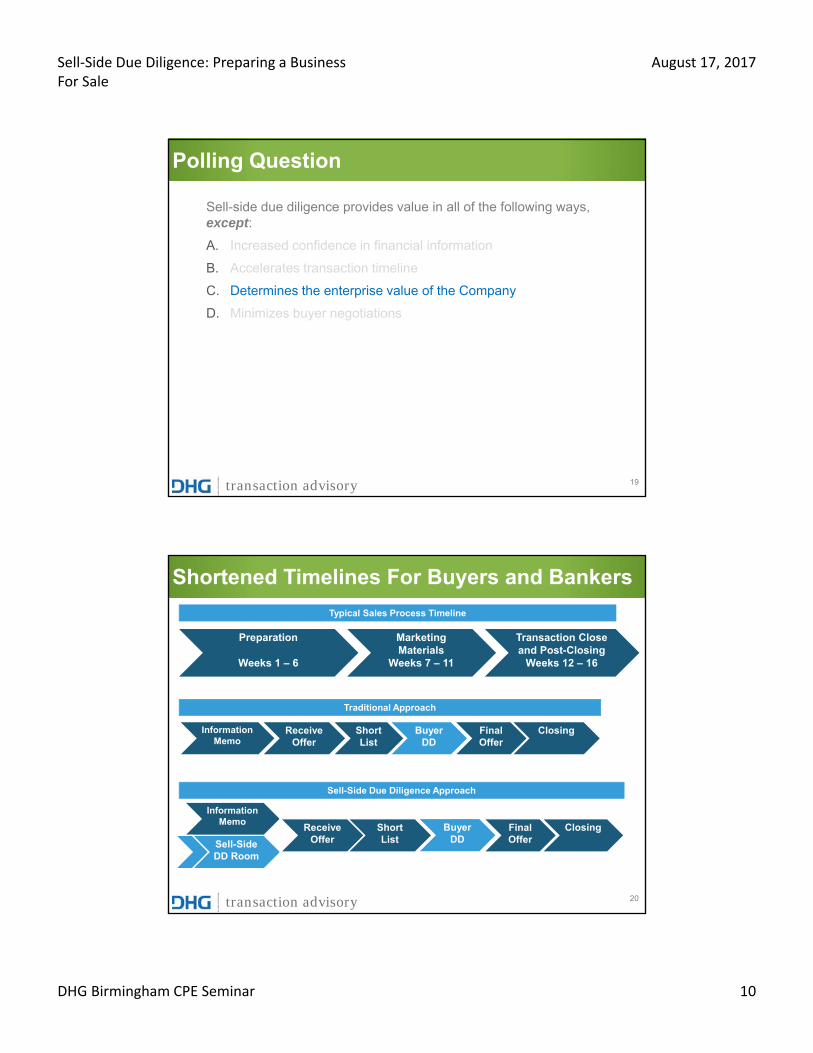

Polling Question

Sell-side due diligence provides value in all of the following ways, except:

A. Increased confidence in financial information

B. Accelerates transaction timeline

C. Determines the enterprise value of the Company

D. Minimizes buyer negotiations

Sell‐Side Due Diligence: Preparing a Business For Sale

August 17, 2017

DHG Birmingham CPE Seminar 10

19transaction advisory

Polling Question

Sell-side due diligence provides value in all of the following ways, except:

A. Increased confidence in financial information

B. Accelerates transaction timeline

C. Determines the enterprise value of the Company

D. Minimizes buyer negotiations

20transaction advisory

Shortened Timelines For Buyers and Bankers

Typical Sales Process Timeline

Preparation

Weeks 1 – 6

Marketing Materials

Weeks 7 – 11

Transaction Close and Post-Closing

Weeks 12 – 16

Traditional Approach

Information Memo

Receive Offer

Short List

Buyer DD

Final Offer

Closing

Sell-Side Due Diligence Approach

Information Memo

Sell-Side DD Room

Receive Offer

Short List

Buyer DD

Final Offer

Closing

Sell‐Side Due Diligence: Preparing a Business For Sale

August 17, 2017

DHG Birmingham CPE Seminar 11

21transaction advisory

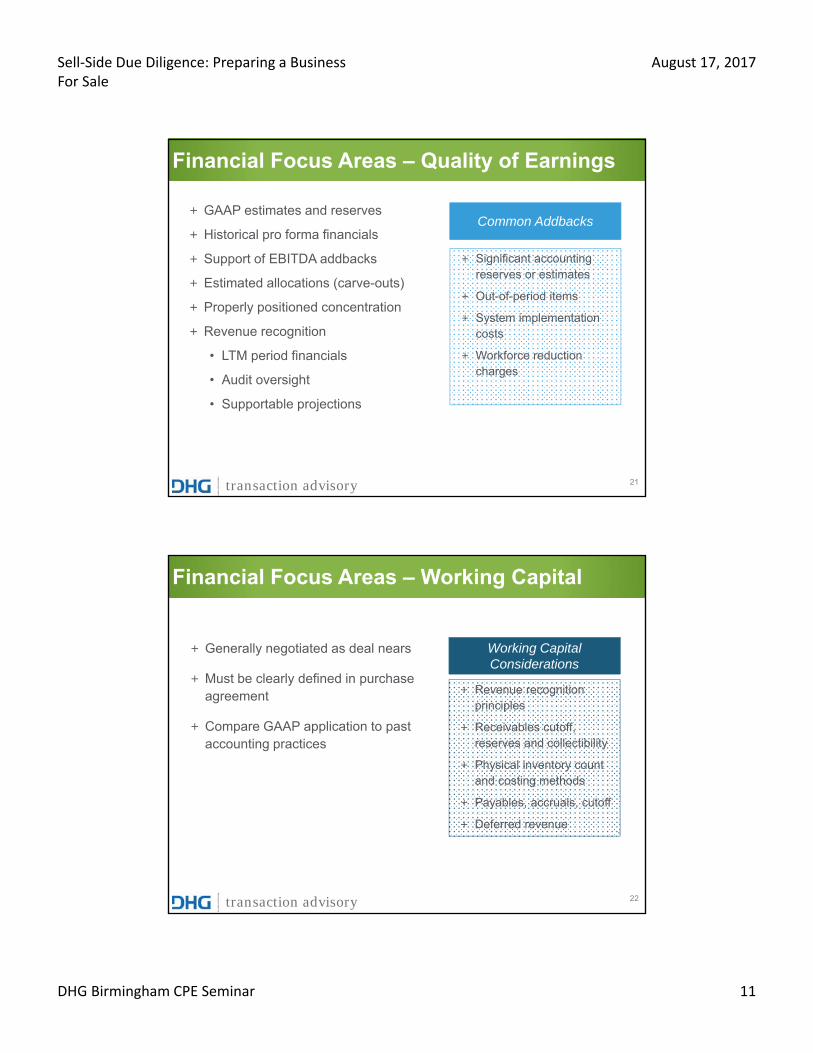

Financial Focus Areas – Quality of Earnings

+ GAAP estimates and reserves

+ Historical pro forma financials

+ Support of EBITDA addbacks

+ Estimated allocations (carve-outs)

+ Properly positioned concentration

+ Revenue recognition

• LTM period financials

• Audit oversight

• Supportable projections

+ Significant accounting reserves or estimates

+ Out-of-period items

+ System implementation costs

+ Workforce reduction charges

Common Addbacks

22transaction advisory

Financial Focus Areas – Working Capital

+ Generally negotiated as deal nears

+ Must be clearly defined in purchase agreement

+ Compare GAAP application to past accounting practices

Working Capital Considerations

+ Revenue recognition principles

+ Receivables cutoff, reserves and collectibility

+ Physical inventory count and costing methods

+ Payables, accruals, cutoff

+ Deferred revenue

Sell‐Side Due Diligence: Preparing a Business For Sale

August 17, 2017

DHG Birmingham CPE Seminar 12

23transaction advisory

Your Audit Firm as Your Sell-Side Advisor

+ All of our clients are subject to sale, so what can we do to assist with the process?

• Educate partners on sell-side services

• Minimize learning curve issues

• Enhance the efficiency of the process and reduce burden on management team

• Coordination on GAAP issues with audit team

24transaction advisory

Sell-Side Tax Issues

Sell‐Side Due Diligence: Preparing a Business For Sale

August 17, 2017

DHG Birmingham CPE Seminar 13

25transaction advisory

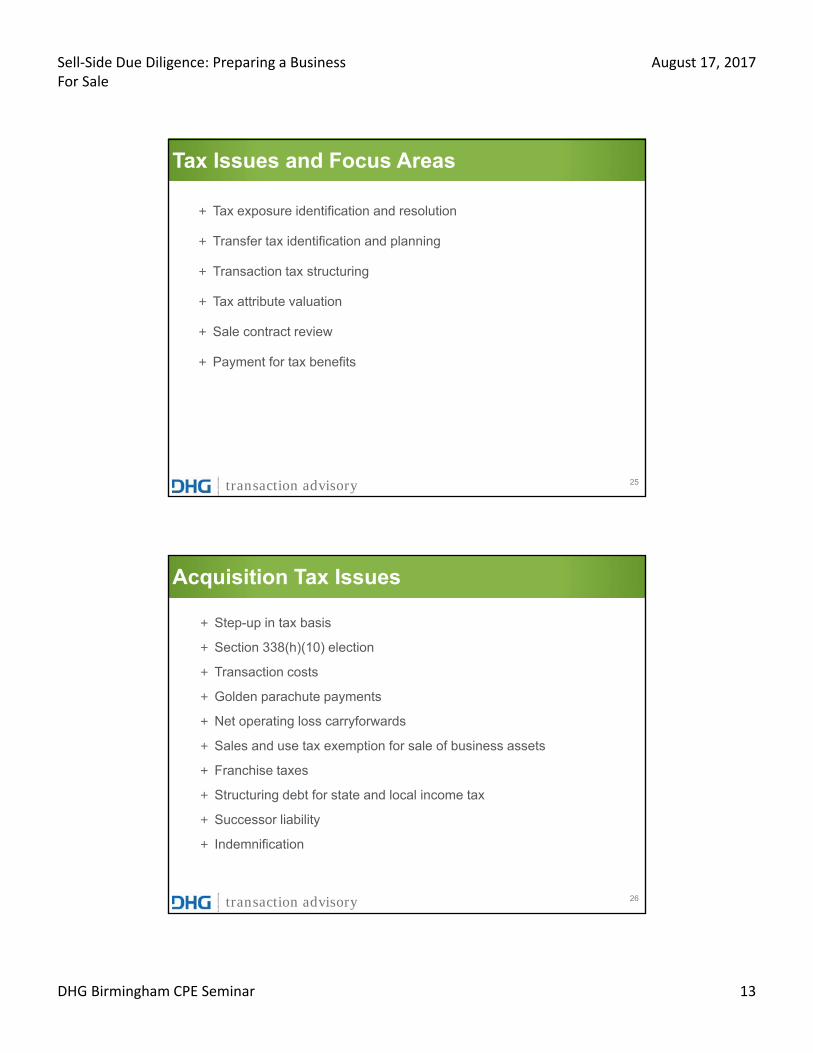

Tax Issues and Focus Areas

+ Tax exposure identification and resolution

+ Transfer tax identification and planning

+ Transaction tax structuring

+ Tax attribute valuation

+ Sale contract review

+ Payment for tax benefits

26transaction advisory

Acquisition Tax Issues

+ Step-up in tax basis

+ Section 338(h)(10) election

+ Transaction costs

+ Golden parachute payments

+ Net operating loss carryforwards

+ Sales and use tax exemption for sale of business assets

+ Franchise taxes

+ Structuring debt for state and local income tax

+ Successor liability

+ Indemnification

Sell‐Side Due Diligence: Preparing a Business For Sale