Brenen Sieber focuses exclusively on serving clients through mergers and acquisitions. Prior to rejoining Baker Tilly Capital in 2006, Brenen helped lead the mergers and acquisitions department of a $5+ billion international manufacturer Brenen has extensiveof a $5+ billion international manufacturer. Brenen has extensive experience managing sell-side processes of privately held companies, private equity group portfolio companies, and corporate divestitures.

2

Your presenters

Bill Chapman, CPAManaging DirectorBaker Tilly Capital, LLC

Bill Chapman has led numerous due diligence engagements focused on quality of earnings, quality of assets, tax compliance and structure, information technology, and commercial and operational issues Bill has also led numerous corporate financeoperational issues. Bill has also led numerous corporate finance engagements helping clients recapitalize their business by arranging for senior debt, subordinated debt, and equity.

3

Your presenters

Corey Vanderpoel DirectorBaker Tilly Capital, LLC

Corey Vanderpoel has over ten years experience working within the investment banking industry. Corey has focused his career exclusively on serving clients through mergers and acquisitions and has a long history of leading sell side and buy side engagementshas a long history of leading sell-side and buy-side engagements. Corey has extensive experience preparing companies for sale to create value, developing sell-side and buy-side strategies and marketing processes, contacting potential targets, executing auction processes, and negotiating transaction terms.

4

Agenda

> M&A market> Overview of the sell-side process> Preparing your business for sale> Case studies from the trenches> Questions

These materials may not be used or relied upon for any purpose other than as authorized by written agreement with Baker Tilly Capital, LLC. Baker Tilly Capital, LLC does not guarantee the accuracy, completeness, or suitability of the content of the materials for any purpose. Any comments made in the materials are opinions with no guarantee that any expressed course of events will actually transpire. Securities are

5

offered through Baker Tilly Capital, LLC, Member FINRA and SIPC. Baker Tilly Capital, LLC is an affiliate of Baker Tilly Investment Advisors, an investment adviser, and both are wholly owned subsidiaries of Baker Tilly Virchow Krause, LLP, an accounting firm. Baker Tilly Virchow Krause, LLP is an independently owned and managed member of Baker Tilly International.

Overview of current M&A market

6

Overview of current M&A market

7

Overview of current M&A market

Cash and Short-Term Investments of S&P 500 (in billions) Source: Pitchbook Data, Inc.Private equity capital raised (in billions)Private Equity Capital Raised (in billions)

$

$800

$1,000

$1,200

$1,400

$200

$300

$400

$500

Source: Pitchbook Data, Inc.

$0

$200

$400

$600

2008 2009 2010 2011 Q4 2012

$0

$100

$200

2008 2009 2010 2011 2012

As published in the most recent Baker Tilly Capital M&A and Capital Markets Update there is

Source: Capital IQ, excludes financial companies; Q4 2012 includes latest reported quarter data Aggregate Annual raised capitalSource: Pitchbook Data, Inc.

As published in the most recent Baker Tilly Capital M&A and Capital Markets Update, there is significant cash available to corporations and private equity groups…they’re aggressively looking to

make acquisitions to realize growth, which is driving up values for successful companies.

8

Overview of current M&A market

Private equity deals are averaging 2.2x EBITDA in senior debt and the average deal in the first half of 2012 included 49.6% equity investment

A il bl fi i i d l ifi d di ll l b d i bili f h fl

9

Available financing is deal specific depending on collateral base and sustainability of cash flow

Preparing your business for sale

> Understand the prospective value of your b i d h it i d t i dbusiness and how it is determined What is the current environment for a business like

yours?yours?

What variables could affect the price or structure?

10

Preparing your business for sale

11

Preparing your business for sale

> Putting the team togetherL l l Legal counsel

Tax advisor

Investment banker

Internal staff

> Get organized Books and records

Appearance

12

Reverse or vendor due diligence

Reverse and vendor due diligence are the process of the seller hiring an outside advisor(s) to perform aseller hiring an outside advisor(s) to perform a comprehensive due diligence study on themselves.> Reverse versus vendor due diligenceg> What should be included in such a study?

An assessment of the quality of earnings q y g» EBITDA

» Free cash flows (EBITDA - change in net working ( g gcapital - capital expenditures - cash taxes paid)

13

Reverse or vendor due diligence

An assessment of the quality of assets» Accounts receivables

» Inventory

P bl» Payables

» Net working capital

Fi d t» Fixed assets

A search for debt-like items

14

Reverse or vendor due diligence

Operational risksf» Revenue and gross profit concentrations

» Operational leverage

K i» Key man issues

Taxation» Federal

» State and local

I t ti l» International

Legal and other

15

Reverse or vendor due diligence

> Advantages of vendor due diligenceP id h ll h i f ll Provides the seller the opportunity to correct or fully explain any previously unknown issues that may be perceived as a flaw by prospective buyersp y p p y

Assists the investment banker by:» Being able to provide, now vetted, data in the

Confidential Memorandum and in the data room» Answering many of the questions a prospective buyer

would otherwise have, keeps more participants in the , p p pprocess longer

» Identifying potential deal issues in advance, the investment banker can anticipate and mitigate the

16

investment banker can anticipate and mitigate the impact on price and structure

Reverse or vendor due diligence

Minimizes surprises in the buyers due diligence

Helps to minimize the exclusivity period

Minimizes the risk and cost of broken deals for the buyerbuyer

17

Reverse or vendor due diligence

> When should vendor due diligence be id d?considered?

When the systems or controls are less sophisticated

I l t ti h “ t” In a complex transaction such as a “carve-out”

Lack of seller resources to properly prepare for sale

The seller has never had an audit

18

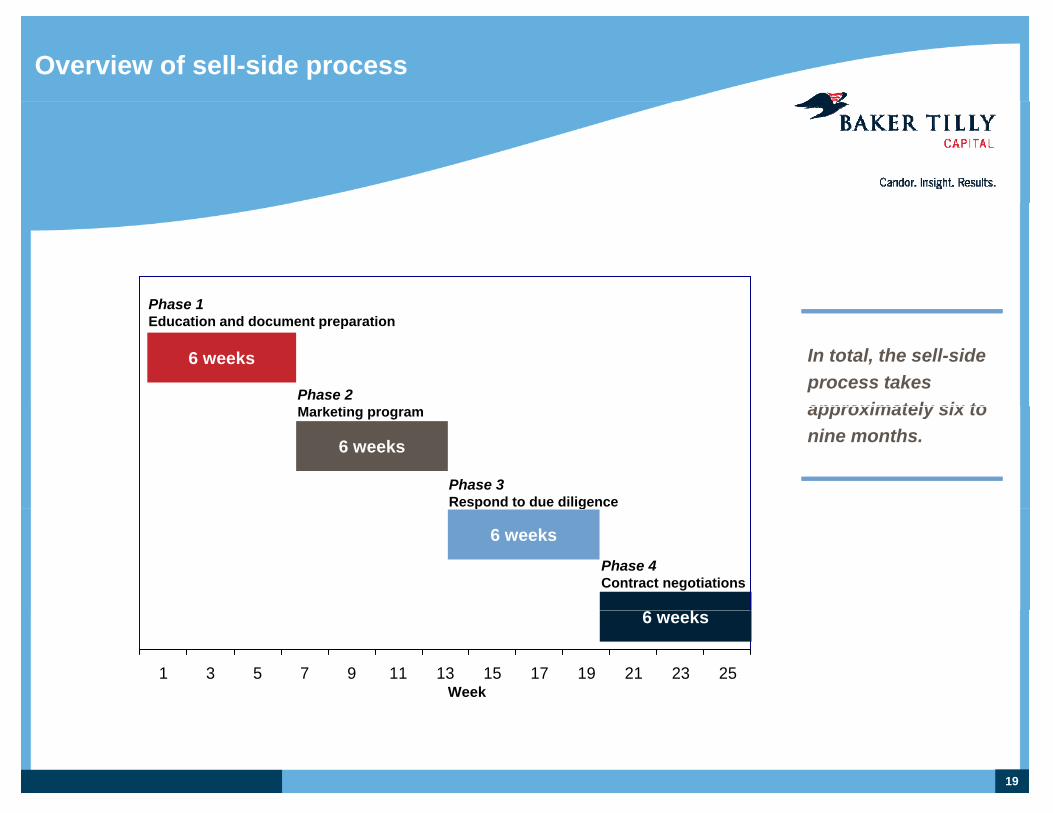

Overview of sell-side process

Phase 1

6 weeks

Phase 1Education and document preparation

Phase 2M k ti

In total, the sell-side process takes approximately six toMarketing program

Phase 3Respond to due diligence

6 weeks

approximately six to nine months.

p g

6 weeksPhase 4Contract negotiations

1 3 5 7 9 11 13 15 17 19 21 23 25Week

6 weeks

19

Overview of sell-side process

• Gather information about your company• Review market and industry data

Phase 1 • Review market and industry data• Discuss strategy and set objectives• Create Confidential Information Memorandum (CIM)

Education and document preparation

• Develop database of potential buyers• Develop database of potential buyers• Proactively market• Manage distribution of CIM sale books• Qualify interest levels

Phase 2 Marketing program

Phase 3• Respond to buyer due diligence requests• Convey company’s strengths and opportunities

Phase 3 Respond to due

diligence

• Conduct early negotiations• Conduct early negotiations• Maximize value within Letters of Intent received• Establish timelines and facilitate responses to potential buyers’ questions• Communicate economic and tax considerations to be used in negotiations• Negotiate detailed Letter of Intent to address buyer terms and conditions• Review documents with legal counsel• Close successful sale

Phase 4 Contract negotiations

20

Case studies from the trenches

> Creating value before the sale> Options, options, options> It’s not what you sell it for, it’s what you net> Ownership options> The true profitability of the business

21

Case studies from the trenches

Creating value before the sale> Customer diversification> Cleaning up the facilityg p y> Optimize working capital> Transitioning owner responsibilitiesg p

22

Case studies from the trenches

Options, options, options> Exclusivity> Choosing your partnerg y p> Keeping contacts warm

23

Case studies from the trenches

It’s not what you sell it for, it’s what you net> Structuring the deal

Existing corporate structure (S corporation, C corporation, LLC)

Stock versus asset

Allocation – depreciation recapture

> Certain transactions toward the end of 2012 had purchase price adjustments related to year-end closings

24

Case studies from the trenches

Ownership employment options> Exit business

Mitigating ownership transition risk» Making it easier for a buyer

Could retain interest (equity or seller note)

> Retain employment Transition to new culture

Shift from owner to employee

Could retain interest (equity or seller note)

25

Could retain interest (equity or seller note)

Case studies from the trenches

The true profitability of the business> Communicating value drivers> Add-backs

Why shouldn’t you get paid for the true profitability?

What qualifies as an add-back» Nonrecurring

» Extraordinary

» Non-operating

26

Contact information

Brenen Sieber, CPAM i Di tManaging DirectorBaker Tilly Capital, LLC414 777 [email protected]

Bill Chapman, CPAManaging DirectorBaker Tilly Capital, LLCy p ,312 729 [email protected]

Corey B. VanderpoelDirectorBaker Tilly Capital, LLC414 777 5404