STATE OF CALIFORNIA STATE BOARD OF EQUALIZATION 450 N STREET, SACMENTO, CALIFORNIA PO BOX 942879, SACRAMENTO, CALIFORNIA 94279-0092 1-916-324-2830 • FAX 1-916-322-4530 w.boe.ca.qov SEN GEORGE RUNNER (Ret) First District. Lanster FIONA , CPA Secd o,w,ct. San Fransco JEROME E HORTON Third Distri. Los geles County DIE l HARKEY Fouh Distnct. Orange Cwntv 8ETTYL YEE State ConlrOller OAVIOJ GAU Executive o,reor May 26, 2017 Dear Interested Party: Enclosed is the Second Discussion Paper on Regulation 4076, Wholesale Cost of Tobacco Products and proposed Re-g ulation 4077, Tobacco Product Manufacturer. Before the issue is presented at the Board's August 29-31, 2017 Business Taxes Committee meeting, staff would like to invite you to discuss the issue and present any additional suggestions or comments. Accordingly, an interested parties meeting is scheduled as llows: June 6, 2017 Room 122 at 10:00 a.m. 450 N Street, Sacramento, CA If you would Jike to participate by teleconrence, call 1-888-808-6929 and enter access c.ode 7495412. You are also welcome to submit your comments to me at the address or fax number in this letterhead or via email at Trista.Gonzalezboe.ca.gov by June 22, 2017, You should submit written comments including proposed language if you have suggestions you would like considered during this process. Copies of the materials you submit may be provided to other interested parties, therefore, ensure your comments do not contain confidential information. Please fee) ee to publish this information on your website or distribute it to others that may be interested in attending the meeting or presenting their comments. If you are interested in other Business Taxes Committee topics refer to the BOE webpage at (http://www.boe.ca.gov/meetings/btcommiltee.htm) r copies of discussion or issue papers, minutes, a procedures manual, and calendars arranged accordjng to subject matter and by month. Thank you r your consideration. Staff Jooks rward to your comments and suggestions. Should you have any questions, please feel ee to contact Business Taxes Committee staff member Mr. Michael Patno at l-916-323-9676, who will be leading the meeting. Sincerely, 'f���l Tax Policy Division Business Tax and Fee Depament TG:map Enclosures SDI'_ 4076_CovcrWcb.docx

Transcript

STATE OF CALIFORNIA

STATE BOARD OF EQUALIZATION 450 N STREET, SACRAMENTO, CALIFORNIA PO BOX 942879, SACRAMENTO, CALIFORNIA 94279-0092

1-916-324-2830 • FAX 1-916-322-4530

www.boe.ca.qov

SEN GEORGE RUNNER (Ret) First District. Lancaster

FIONA MA, CPA Second o,w,ct. San Franclsco

JEROME E HORTON Third District. Los Angeles County

DIANE l HARKEY Foul1h Distnct. Orange Cwntv

8ETTYL YEE State ConlrOller

OAVIOJ GAU Executive o,rector

May 26, 2017

Dear Interested Party:

Enclosed is the Second Discussion Paper on Regulation 4076, Wholesale Cost of Tobacco Products and proposed Re-g ulation 4077, Tobacco Product Manufacturer. Before the issue is presented at the Board's August 29-31, 2017 Business Taxes Committee meeting, staff would like to invite you to discuss the issue and present any additional suggestions or comments. Accordingly, an interested parties meeting is scheduled as follows:

June 6, 2017

Room 122 at 10:00 a.m.

450 N Street, Sacramento, CA

If you would Jike to participate by teleconference, call 1-888-808-6929 and enter access c.ode 7495412. You are also welcome to submit your comments to me at the address or fax number in this letterhead or via email at Trista.Gonzalez@,boe.ca.gov by June 22, 2017, You should submit written comments including proposed language if you have suggestions you would like considered during this process. Copies of the materials you submit may be provided to other interested parties, therefore, ensure your comments do not contain confidential information. Please fee) free to publish this information on your website or distribute it to others that may be interested in attending the meeting or presenting their comments.

If you are interested in other Business Taxes Committee topics refer to the BOE webpage at (http://www.boe.ca.gov/meetings/btcommiltee.htm) for copies of discussion or issue papers, minutes, a procedures manual, and calendars arranged accordjng to subject matter and by month.

Thank you for your consideration. Staff Jooks forward to your comments and suggestions. Should you have any questions, please feel free to contact Business Taxes Committee staff member Mr. Michael Patno at l-916-323-9676, who will be leading the meeting.

Sincerely,

'f���l;( Tax Policy Division Business Tax and Fee Department

cc: (all with enclosures, via email and/or hardcopy as requested) Honorable Diane L. Harkey, Chairwoman Honorable George Runner, Vice Chair Honorable Fiona Ma, CPA, Second District Honorable Jerome E. Horton, Third District Honorable Betty T. Yee, State Controller, c/o Ms. Yvette Stowers (MIC 73) Mr. Russell Lowery, Board Member's Office, Fourth District Mr. Ted Matthies, Board Member's Office, Fourth District Ms. Lisa Renati, Board Member's Office, fourth District Mr. Clifford Oakes, Board Member's Office, Fourth District Mr. Sean Wallentine, Board Member's Office, First District Mr. Lee Williams, Board Member's Office, First District Mr. Brian Wiggins, Board Member's Office, First District Mr. Cary Hux.son, Board Member's Office, First District Mr. Alfred Buck, Board Member's Office, First District Mr. David Duran, Board Member's Office, First District Ms. Genevieve Jopanda, Board Member's Office, Second District Ms. Kathryn Asprey, Board Member's Oflice, Second District Mr. Tim Morland, Board Member's Office, Second District Ms. Natasha Ralston Ratcliff, Board Member's Office, Second District Ms. Kari Hammond, Board Member's Office, Third District Ms. Kristine Cazadd, Board Member's Office, Third District Ms. Cynthia Bridges, Board Member' s Office, Third District Ms. Linda Cheng, Board Member's Office, Third District Mr. Chris Armenta, Board Member's Office, Third District Mr. David Gau (MIC 73) Ms. Brenda Fleming (MIC 73) Ms. Amy Kelly (MIC 83) Ms. Susanne Buehler (MIC 43) Ms. Debra Kalfsbeek (MIC 62) Mr. Richard Parrott (MIC 57) Ms. Lisa Sherrod (MIC 31) Ms. Sandy Barrow (MIC 31) Mr. Todd Gilman (MIC 70) Mr. Wayne Mashil1ara (MIC 47) Mr. Kevin Hanks (MIC 49) Mr. Mark Durham (MIC 67) Mr. Robert Tucker (MIC 82) Mr. Jeff Vest (MIC 85) Mr. Jeff Angeja (MIC 85) Mr. David Levine (MIC 85) Ms. Dana Brown (MIC 85) Ms. Casey Tichy (MIC 85) Ms. Nikki Mozdyniewicz {MIC 85) Mr. Rick ZeHmer (MIC 85) Mr. Bradley Heller (MIC 82) Mr. Lawrence Mendel (MIC 82) Mr. Stephen Smith (MIC 82)

Interested Party -3- May 26, 2017

Ms. Pamela Bergin (MIC 82) Ms. Kirsten Stark (MIC 50) Ms. Lynn Whitaker (MIC 50) Mr. Marc Alviso (MIC 73) Mr. Chris Lee (MIC 73) Ms. Laureen Simpson (MIC 70) Ms. Karina Magana (MIC 47) Mr. Bradley Miller (MIC 92) Mr. Bill Benson (MIC 67) Mr. Paul Campky (MIC 50) Mr. Michael Patno (MIC 50)

SECOND DISCUSSION PAPER Regulation 4076, Wholesale Cost of Tobacco Products &

Regulation 4077, Tobacco Product Manufacturer

Issue

Whether the Board should approve the proposed revisions to Regulation 4076, Wholesale Cost of Tobacco Products and proposed Regulation 4077, Tobacco Product Manufacturer, to interpret and clarify the changes made to the Cigarette and Tobacco Products Tax Law (CTPTL) due to the passage of Proposition 56, the California Healthcare, Research and Prevention Tobacco Tax Act of 2016 (Prop. 56).

Staff Recommendation

Staff proposes revisions to Regulation 4076 and proposes Regulation 4077 as provided in Exhibits 1 and 2. Staff’s proposed revisions:

• Provide clarity for the definition and terms used for electronic cigarettes which are included in the definition of Other Tobacco Products (OTP) as of April 1, 2017.

• Include examples to assist taxpayers in their understanding of the Cigarette and Tobacco Products tax and the effect of Prop. 56 on them.

Other Alternative(s) Considered

Mr. Brent Chambers of Nu Mark LLC (Nu Mark) sent a letter expressing Nu Mark’s disagreement with staff’s recommendations proposed in its first discussion paper. In their submission (see Exhibit 3) Nu Mark explained its position that:

• Items not “used during the operation of device” should not be included in the definition of an electronic cigarette and therefore not subject to the OTP tax.

• Staff’s definition for “Sold in Combination With” (SICW) should exclude promotional offers not packaged as a single unit.

In addition to Mr. Chamber’s comments, Mr. Jesse McClellan of McClellan Davis LLC on behalf of California Smoke Free Organization (CSFO) had concerns with staff’s definition involving electronic cigarettes and for refunds/credits involving the OTP tax (see Exhibit 4); Mr. McClellan asked staff to address:

• The clarification of the definition for SICW and the possibility a retailer of OTP could be a “de facto distributor” if they package nicotine products and devices as one set and sell them at a single price.

• Refunds or credits for the tax paid on OTP distributions that were sold for use or consumption out-of-state.

Background

In November 1988, California voters passed Proposition 99, known as the “Tobacco and Health Protection Act of 1988” (Prop. 99). Among other things, Prop. 99 imposed a surtax on every distributor (as defined in Revenue and Taxation Code (RTC) section 30011) of cigarettes at the rate of 12.5 mills ($0.0125) per cigarette or $0.25 per pack ($0.0125 x 20 cigarettes) distributed. Prop. 99 also imposed a tax on every distributor of tobacco products (as defined in RTC section 30121(b)) other than cigarettes (collectively referred to as “other tobacco products” or “OTP”),

Page 1 of 7

SECOND DISCUSSION PAPER Regulation 4076, Wholesale Cost of Tobacco Products &

Regulation 4077, Tobacco Product Manufacturer including, for example, cigars, smoking and chewing tobacco, and snuff, at a rate equivalent to the combined rate of the tax imposed on cigarettes, under various provisions of the CTPTL. Prop. 99’s surtax on the distribution of cigarettes and equivalent tax on the distribution of OTP are both codified in RTC section 30123, and they apply to the “distribution” (as defined in RTC section 30008) of cigarettes or OTP.

In 1998, California voters passed Proposition 10, known as “The Children and Families First Act” (Prop. 10). The purpose of Prop. 10 was to create county commissions to provide early childhood medical care and education. Prop. 10 imposed an additional tax on every distributor of cigarettes at the rate of 25 mills ($0.025) per cigarette or $0.50 per pack, as well as an equivalent tax on every distributor of OTP (as defined in RTC section 30131.1 (b), which is identical to RTC section 30121(b)). Prop. 10’s tax on the distribution of cigarettes and equivalent tax on the distribution of OTP are both codified in RTC section 30131.2. The taxes codified in and imposed by RTC sections 30123 and 30131.2 do not apply to “the sale of cigarettes or tobacco products by the original importer to a licensed distributor if the cigarettes or tobacco products are manufactured outside the United States” (as provided by RTC section 30105).

The Board is responsible for enforcing the CTPTL, including the taxes imposed on distributors of OTP under RTC sections 30123 and 30131.2. Pursuant to RTC sections 30123, 30126, 30131.2, and 30131.5, the Board is required to calculate the combined tax rate on OTP on an annual basis based on the wholesale cost of tobacco products as of March 1, and the rate determined by the Board is effective during the state’s next fiscal year, which begins on July 1. This combined rate is applied by distributors to the “wholesale cost” of distributed OTP to calculate the amount of excise tax due, and the resulting tax is then required to be reported and paid to the Board under chapter 4 of the CTPTL. RTC section 30017 defines “wholesale cost” as “the cost of tobacco products to the distributor prior to any discounts or trade allowances.”

Board staff clarified the meaning of wholesale cost of tobacco products in 2016 with the creation of Regulation 4076. “Wholesale cost” means the cost of the tobacco products to the distributor prior to any discounts or trade allowances. If a manufacturer is also the distributor, the wholesale cost of tobacco includes all manufacturing costs, the cost of raw materials (including waste materials not incorporated into the final product), the cost of labor, any direct and indirect overhead costs, and any federal excise and/or U.S. Customs taxes paid. Wholesale cost does not include domestic freight or transportation charges for shipment of a finished product from the supplier to the distributor. In most cases, the wholesale cost will be the invoiced price of the tobacco products without any allowance for discounts.

Excise taxes are imposed upon the distribution of cigarettes and tobacco products in California. Distributors must be licensed to conduct these transactions and have an account number to remit the excise taxes owed. The cigarette tax and the cigarette and tobacco products surtax are collected on cigarettes and tobacco products distributed in California.

Cigarettes Cigarettes are subject to both the cigarette tax and the cigarette and tobacco products surtax, collectively referred to as taxes. The taxes are assessed on each cigarette distributed in California. Distributors are required to affix a tax stamp to each pack of cigarettes before distribution. Prior to April 1, 2017, distributors were allowed a purchase discount of 0.85% of the total tax value per purchase order to help offset the cost of affixing cigarette tax stamps.

Page 2 of 7

SECOND DISCUSSION PAPER Regulation 4076, Wholesale Cost of Tobacco Products &

Regulation 4077, Tobacco Product Manufacturer Distributors pass the excise taxes on to their customer, and the taxes become part of the retail selling price of the cigarettes.

Tobacco Products Prior to April 1, 2017, tobacco products included, but were not limited to, all forms of cigars (except “little cigars”), smoking tobacco (including shisha), chewing tobacco and snuff, and any other articles or products made of or containing at least 50 percent tobacco. Tobacco products do not include cigarettes. The OTP tax, which is a component of the cigarette and tobacco products surtax, is paid by tobacco products distributors.

Proposition 56 (California Healthcare, Research and Prevention Tobacco Tax Act of 2016) On November 8, 2016, California voters approved the passage of Prop. 56. By doing so, the California electorate approved, among other things, the following:

• Amending RTC section 30121, changing the definition of tobacco products. • Increasing the cigarette tax by $2.00, raising it from $0.87 per pack to $2.87 per pack. • Establishing a cap on the amount of the distributor’s purchase discount of 0.85% to the

first $1.00 of the value of the cigarette tax stamp. • Every cigarette dealer and wholesaler shall pay a floor stock tax based on the inventory

of cigarettes in their possession or under their control. • Cigarette distributors shall pay a cigarette indicia adjustment tax based on their inventory

of California cigarette tax stamps in their possession or under their control, whether they are affixed to any package of cigarettes or not.

RTC section 30126 requires the Board's annual determination of the OTP tax rate pursuant to subdivision (b) of section 30123. The new rate is effective July 1, 2017, and will remain in effect for the 2017-18 fiscal year. It is based on the wholesale premium brand cigarette price as of March 1, 2017, as published by the Tobacco Merchants Association, and was set at 65.08% during the April 2017 Board Meeting. This rate is significantly higher than the fiscal year 201617 rate of 27.30% due to the passage of Prop. 56.

Discussion

Staff distributed their initial discussion paper on this topic on March 27, 2017, and held the first interested parties meeting on April 11, 2017. After the meeting, staff received two submissions providing alternative language and a third submission sharing concerns and asking questions. Each of those submissions will be addressed in this discussion paper.

Definition of Electronic Cigarettes Prop. 56 provided a lengthy description of what encompasses electronic cigarettes and what is and what is not included within the definition. Nu Mark, citing RTC section 30121(c) which defines electronic cigarettes, emphasized this sentence contained in the statute:

Electronic cigarettes include any component, part, or accessory of such a device that is used during the operation of the device when sold in combination with any liquid or substance containing nicotine.

Page 3 of 7

SECOND DISCUSSION PAPER Regulation 4076, Wholesale Cost of Tobacco Products &

Regulation 4077, Tobacco Product Manufacturer Nu Mark believes that the statutory definition of electronic cigarettes includes any component, part, or accessory of such a device that is “used during the operation of the device.” Nu Mark explains that items sold not only have to be sold in combination with nicotine products but also have to be used in the operation of an electronic cigarette.

In the example Nu Mark provided, a packaged kit contains: 10 cartridges, a battery, a carrying case, and a wall charger. It stated that the statute supports that the OTP tax would be applied to the wholesale cost of the cartridges and battery as they are used during the vaping process; however, the case and charger would not be subject to the tax. While sold in combination with a tobacco product, the two items are not used during the vaping process. Nu Mark concluded that items contained in electronic cigarette kits that are not used during the operation of the electronic cigarette should not be included in the computation of wholesale cost of tobacco products.

Staff has reviewed Nu Mark’s submission and does not agree with its interpretation of the statute. Staff acknowledges the sentence Nu Mark refers to in their submission; however, also within section 30121(c), staff notes the following sentence:

Electronic cigarettes do not include any device not sold in combination with any liquid or substance containing nicotine, or any battery, battery charger, carrying case, or other accessory not used in the operation of the device if sold separately.

Staff focused on the final phrase, “if sold separately” in its disagreement with Nu Mark. Staff’s interpretation does not make the term “used during the operation of the device” superfluous as described by Nu Mark but rather it becomes one of two criteria needed in order to not be considered an electronic cigarette. Both elements must be met in order to be excluded from the definition.

Definition of Sold in Combination With (SICW) As stated previously, Prop. 56 defined electronic cigarettes and the SICW phrase used in that definition was clarified by staff’s initial discussion paper. Nu Mark and CSFO submitted language they thought would better explain the meaning of electronic cigarettes. In addition, while Ms. Kari Hess of Californians for Tobacco Harm Reduction (CATHR) did not suggest language, she shared her concerns about the proposed definition of SICW as being “complex” and also questioned if a retailer needed a distributor’s license to sell combined tobacco products (Exhibit 5).

With regard to SICW, Nu Mark suggested the following definition:

The term "sold in combination with" refers to kits, systems, or packages that usually include atomizers, cartomizers or similar type device, component pieces, accessories, and liquids containing nicotine that are all sold and packaged as one single product for a single price. Items shall not be considered sold in combination with nicotine products if such products are not packaged as a single unit.

Although staff now agrees with the general concept in Nu Mark’s suggestion, staff has concerns with the usage of the phrase “and packaged” in the definition. Our interpretation of “and” in the definition means individual items marketed online or sold in a physical packaging as a set could

Page 4 of 7

SECOND DISCUSSION PAPER Regulation 4076, Wholesale Cost of Tobacco Products &

Regulation 4077, Tobacco Product Manufacturer just be itemized in the online buyer’s “cart” or on an invoice to avoid the OTP tax. That is, Nu Mark’s definition requires both actions, packaged as a single product and sold for a single price, to occur to be considered SICW. Staff does not believe Prop. 56’s intent was to define electronic cigarettes in this manner and that Nu Mark’s language may be inconsistent with the new statute.

CSFO suggested the following definition for SICW:

The term “sold in combination with” refers to kits, systems, or sets that usually include atomizers, cartomizers or similar type device, component pieces, accessories, and liquids containing nicotine that are sold as one set in original manufacturing packaging, or packaged or wrapped as one set or sold for a single price by a licensed distributor. Kits, systems, or sets that usually include atomizers, cartomizers or similar type device, component pieces, accessories, and liquids containing nicotine that are purchased by a retailer physically separate and for a separate price will not be considered to be “sold in combination with,” notwithstanding how those items are sold by the retailer.

Staff is concerned that this definition is too complicated and might confuse taxpayers. However, staff agrees with CSFO’s intent to better explain to retailers, who after paying the OTP tax on products may combine normally separately sold non-tobacco products, such as accessories or clothing for promotional purposes. Its concern was that a retailer, in such an example, could be considered a distributor and the accessories and clothing considered sold in combination with a tobacco product.

Upon review of the comments made by interested parties, staff has revised the definition of SICW that was presented at the April 11, 2017 interested parties meeting to the following:

The term “sold in combination with” refers to kits, systems, or sets that usually include atomizers, cartomizers or similar type device, component pieces, accessories, and liquids containing nicotine that are in their original manufacturer packaging as one unit or sold for a single price.

Staff believes including the phrase “in their original manufacturer packaging” addresses the concerns involving retailers who package their products into kits after buying them separately. This language was included in CSFO’s submission and used in the recently approved Regulation 4001, Retail Stock. In reviewing industry websites for electronic cigarettes it appears the kits and systems are marketed as an “all in one” unit and advertised for a single price. Staff believes this change addresses the “de facto distributor” issue, because it is assumed that a typical retailer would not be able to package kits or systems with the manufacturer’s original packaging. A person who is registered with the Board only as a retailer would not need to report the OTP tax as the product they sell was purchased tax paid and considered already distributed. That is because they must purchase their nicotine products from a licensed tobacco products distributor. Therefore, any promotional packaging of accessories or clothing would not be subject to the OTP tax as the tobacco product has already been distributed. In addition to the changes made to the term, “sold in combination with,” staff also revised the first three examples in the new

Page 5 of 7

SECOND DISCUSSION PAPER Regulation 4076, Wholesale Cost of Tobacco Products &

Regulation 4077, Tobacco Product Manufacturer subdivision (f) to illustrate staff’s revised definition of the term SICW. Staff is also proposing to add Examples 5 and 6 to subdivision (f) to explain how Prop. 56 will apply to retailers.

Example 5 addresses the specific concerns CSFO and CATHR raised regarding retailers, such as a vape shop, being “de facto distributors.” Staff agrees that typical retailers should not be identified as a distributor by audit staff if they packaged separately purchased products for promotional reasons. The example demonstrates that a business, registered as a retailer only, should be acquiring all of its OTP tax-paid prior to repackaging them into a promotional item. Staff believes this also addresses CSFO’s and CATHR’S concerns about records needed to prove OTP tax was paid because a retailer would only need to maintain the records they currently do in the regular course of their operations.

Example 6 has been added to explain a typical bundling scenario. In this situation, if 10 cartridges of e-juice containing nicotine were purchased, then the buyer is given their choice of an accessory. If the accessory is not packaged together with the cartridges in original manufacturer packaging and is also separately stated on an invoice or buyer’s “cart,” when purchased via the Internet, the free accessories will not be considered sold in combination with a nicotine product.

Proposed Regulation 4077 Another question raised at the interested parties meeting was clarification regarding the term “manufacturer.” Given the changes to the definition of tobacco products with the passage of Prop. 56, there were questions raised about who should be regarded as a manufacturer, specifically in regards to the electronic cigarette industry. Staff is proposing a new regulation primarily for the sector of the industry that mixes liquid nicotine with flavoring to customize e-juice for personal consumption.

Staff looked at federal law for guidance as to what constitutes manufacturing of electronic cigarettes. Specifically, staff looked at guidance put forth by the United States Food and Drug Administration. Staff has drafted language for proposed Regulation 4077 to align the Board with the federal government.

Subdivision (a) of proposed Regulation 4077 sets forth the general rule that a tobacco product manufacturer is any person, including any repacker and/or relabeler, who manufactures, fabricates, assembles, processes, or labels a finished tobacco product. Subdivision (b) applies more specifically to tobacco products retailers. It provides that if such a retailer mixes, prepares, or combines liquid nicotine with other components of tobacco products, that retailer is also a tobacco products manufacturer.

A person who both manufactures tobacco products and makes retail sales of tobacco products to consumers must also register with the Board as a tobacco products distributor. The distributor would report tax on their distributions as set forth in subdivision (b)(2) of Regulation 4076, which explains what is included in wholesale cost when a person is both a manufacturer and a distributor. A person with all three licenses – manufacturer, distributor, and retailer – could use their distributor’s license to buy untaxed liquid nicotine from a licensed manufacturer. On the other hand, proposed Regulation 4077 explains that a retailer is not engaged in manufacturing if it sells liquid nicotine to consumers and allows the consumer to mix the liquid nicotine with other components of a tobacco product following the sale.

Page 6 of 7

SECOND DISCUSSION PAPER Regulation 4076, Wholesale Cost of Tobacco Products &

Regulation 4077, Tobacco Product Manufacturer Refunds and Credits for OTP Shipped Out of State At the meeting and in its submission, CSFO brought up the issue of whether a distributor may obtain a refund when it purchases tax-paid OTP from another distributor and then ships the OTP out of state prior to consumption. It based its interpretation on CTPTL section 30176.1, Refunds; exported tax-paid tobacco products, and provided an example of Distributor A selling to Distributor B tax-paid OTP and then Distributor B shipping the OTP out of state pursuant to a contract. It concluded that the statute should entitle Distributor B, or at least Distributor A, to a refund or credit.

Staff disagrees with this conclusion. First, the OTP tax is imposed when product is distributed in this state. In CSFO’s scenario, that distribution occurred when Distributor A sells to Distributor B. CTPTL section 30176.1 provides that refunds are allowed when tax has been “paid on the distribution of tobacco products which are shipped to a point outside the state.” Distributor A makes a distribution of OTP, but does not ship the product outside the state, so Distributor A is not entitled to a refund. Distributor B does not make a distribution, so it also is not entitled to a refund. Staff further notes CTPTL section 30361 provides that the Board must issue refunds to the person who paid the tax to the Board. Again, Distributor A cannot receive a refund because its distribution is not exempt, and Distributor B cannot receive a refund because it did not pay the tax to the Board. A legislative change would be required to allow refunds or credits to Distributors A or B under the scenario described by CSFO.

Summary

Staff welcomes any comments, suggestions and input from interested parties regarding the issues described above. Interested parties are encouraged to participate in the June 6, 2017, interested parties meeting. If you plan to attend via teleconference, please let staff know and an agenda or other material(s) for the meeting may be emailed to you. The deadline for interested parties to provide written responses regarding this second discussion paper is June 22, 2017.

Prepared by the Tax Policy Division, Business Tax and Fee Department Current as of 05/25/2017

Page 7 of 7

Second Discussion Paper Staff Proposed Revisions to Regulation 4076

Exhibit 1 Page 1 of 5

§ 4076. Wholesale Cost of Tobacco Products.

(a) Definitions.

(1) Arm's-length transaction. An “arm's-length” transaction means a sale entered into in good faith and for valuable consideration that reflects the fair market value in the open market between two informed and willing parties, neither under any compulsion to participate in the transaction.

(2) Discounts or trade allowances. “Discounts or trade allowances” are price reductions, or allowances of any kind, whether stated or unstated, and include, without limitation, any price reduction applied to a supplier's price list. The discounts may be for prompt payment, payment in cash, bulk purchases, related-party transactions, or “preferred-customer” status.

(3) Electronic cigarettes. “Electronic cigarettes” or “e-cigarettes” are devices or delivery systems sold in combination with nicotine that can be used to deliver the nicotine in aerosolized or vapor form to a person. Electronic cigarettes include any component, part, or accessory that is used during the operation of the device when sold in combination with any liquid or substance containing nicotine. Electronic cigarettes also include any liquids (“e-juice” or “e-liquid”) or substances that contain nicotine. If nicotine is not sold in combination with the preceding, then the devices, delivery systems, components, parts, accessories, liquids, or substances, are not considered electronic cigarettes.

(4) Finished tobacco products; finished condition. “Finished tobacco products” and tobacco products in “finished condition” are tobacco products that will not be subject to any additional processing before first distribution in the state.

(5) Sold in combination with. The term “sold in combination with” refers to kits, systems, or sets that usually include atomizers, cartomizers or similar type device, component pieces, accessories, and liquids containing nicotine that are sold in their original manufacturer packaging as one unit or sold for a single price.

(6) Tobacco products. Effective April 1, 2017, the definition of “tobacco products” includes all products containing, made, or derived from tobacco or nicotine that are intended for human consumption. Tobacco products include, but are not limited to, cigars, little or small cigars, electronic cigarettes, pipe tobacco, and snuff but does not include cigarettes.

(b) Wholesale cost.

(1) If finished tobacco products are purchased by a distributor from a supplier in an arm's-length transaction, the “wholesale cost” of the tobacco product is the amount paid for the tobacco product, including any federal excise tax, but excluding any transportation charges for shipment originating within the United States. Discounts and trade allowances must be added back when determining “wholesale cost.”

Second Discussion Paper Exhibit 1 Staff Proposed Revisions to Regulation 4076 Page 2 of 5

(2) If a manufacturer or an importer is also the distributor, the wholesale cost of tobacco includes all manufacturing costs, the cost of raw materials (including waste materials not incorporated into the finished tobacco product) prior to any discounts or trade allowances, the cost of labor, any direct (including freight-in) and indirect overhead costs, and any federal excise and/or U.S. Customs taxes paid. Wholesale cost includes all freight or transportation charges for shipment of materials and/or unfinished product from the supplier to the manufacturer concurrently licensed as a distributor, but excludes domestic freight or transportation charges for shipment of finished tobacco products as defined in subdivision (a)(3).

(3) If tobacco product costs include express, implicit, or unstated discounts or trade allowances, the correct wholesale costs to be reported by the distributor may be determined using any of the methods provided in subdivision (c).

(4) If tobacco products are not purchased in an arm's-length transaction, the correct wholesale costs to be reported by the distributor may be determined using any of the methods provided in subdivision (c).

(c) Alternative methods of estimating or calculating wholesale cost.

The following resources or methods may be used.

(1) A publicly or commercially available price list that the distributor used to determine the prices of tobacco products sold to customers in arm's-length transactions during the time period at issue, less an estimate based on best available information of the distributor's or a similarly situated distributor's profit.

(2) If a publicly or commercially available price list is not available, industry data from the time period to be estimated or calculated that provides reasonable evidence of typical tobacco product costs during such time period, including, but not limited to:

(A) Evidence reasonably indicative of the typical costs of the same or similar tobacco products for similarly situated distributors, with appropriate adjustments to such costs as indicated by all the facts and circumstances.

(B) All the direct and indirect costs that the supplier paid or incurred with respect to acquisition, production, marketing, and sale of the tobacco products sold by the supplier to the distributor, with appropriate adjustments to such costs as indicated by all the facts and circumstances, plus a reasonable estimate of the supplier's profit.

(C) The price of the same or similar tobacco products as reflected in a supplier's price list, with appropriate adjustments to such price as indicated by all the facts and circumstances.

(D) The retail price of the same or similar tobacco products as reflected in a retailer's price list, with appropriate adjustments to such price as indicated by all the facts and circumstances, less reasonable estimates of the retailer's and distributor's profits.

(E) Additional methods not mentioned above, with Board approval.

Second Discussion Paper Exhibit 1 Staff Proposed Revisions to Regulation 4076 Page 3 of 5

(d) Sales not made at arm's-length.

(1) Presumption. Sales, purchases, and transfers of tobacco products are rebuttably presumed to not be at arm's-length if they are between related parties such as: relatives (by blood or marriage, which relationships include, but are not limited to, spouses, parents, domestic partners, children and siblings); partners or a partnership and its partners; a limited liability company or association and its members; commonly controlled corporations; a corporation and its shareholders; or persons, as defined in Revenue and Taxation Code section 30010, and entities under their control or between commonly controlled entities.

(2) Rebuttal of presumption. If the Board determines that a sale, purchase, or transfer of tobacco products was between related parties, the distributor may rebut the presumption that the sale, purchase, or transfer was not at arm's-length by showing that the price, terms, and conditions of the transaction were substantially equivalent to those that would have been negotiated between unrelated parties.

(e) Examples of estimating or calculating the wholesale cost of tobacco:

(1) Example 1: Distributor B produces handmade cigars. B's tobacco product costs include: all manufacturing costs, the cost of raw materials (including waste materials not incorporated into the final product), the cost of labor, any direct and indirect overhead costs, and any federal excise and/or U.S. Customs taxes paid. The cost does not include freight or transportation charges for shipment from the supplier to the distributor.

(2) Example 2: Distributor C purchases tobacco products from a subsidiary corporation in which it owns or controls more than 50 percent of the voting stock. Due to this corporate relationship between seller and buyer, the Board presumes that the sale and purchase were not at arm'slength, and the presumption is not rebutted by C. In the absence of an arm's-length transaction, the methods discussed in subdivision (c) may be used to determine the correct wholesale cost.

(3) Example 3: Distributor D acquires tobacco product free of charge and reports no wholesale cost for the product on its Tobacco Products Distributor Tax Return. However, D acquired such tobacco product at a 100 percent discount or trade allowance. In the absence of an arm's-length transaction, the methods discussed in subdivision (c) may be used to determine the correct wholesale cost.

(4) Example 4: Distributor E, with a tobacco products importers license, acquires tobacco products or finished tobacco products from a supplier outside the United States. E's tobacco product costs include, in addition to all other production or acquisition costs, the costs of all U.S. Customs fees and federal excise taxes paid or incurred by E with respect to such tobacco products.

(5) Example 5: Distributor F receives three tobacco products packaged as one unit, as a “three for the price of two” promotional package, labeled with a single UPC barcode. As the products are packaged together as one inseparable unit, tax is based on the total package price.

Second Discussion Paper Exhibit 1 Staff Proposed Revisions to Regulation 4076 Page 4 of 5

(6) Example 6: Distributor G receives 2 units, to sell as a “buy one, get one free” promotion. Each unit is separately packaged and each unit is labeled with a UPC barcode. Because one unit is being provided for free, tax would apply to the wholesale cost of each separate unit as calculated by a method discussed in subdivision (c).

(7) Example 7: Distributor H receives a three percent discount for paying their supplier within 10 days of receipt of their items. To calculate the wholesale cost, Distributor H must add the three percent discount to the price paid for the products.

(f) In addition to examples in subdivision (e), the following are examples of estimating or calculating the wholesale cost of products that have been defined as tobacco products effective April 1, 2017:

(1) Example 1: Distributor K produces finished nicotine products (e.g., e-juice) intended for human consumption. K’s product costs include: all manufacturing costs, the cost of raw materials (including pure nicotine, any adjuncts and flavorings and waste materials not incorporated into the final product), the cost of labor, any direct and indirect overhead costs, and any applicable federal excise and/or U.S. customs taxes paid. The cost does not include freight or transportation charges for shipment from the supplier to the distributor.

(2) Example 2: Distributor L purchases two types of electronic cigarette kits. Both kits are sold as a single unit in their original manufacturer packaging which contain a personal vaping device, tank, atomizer coil, USB charger, A/C adapter and a bottle of finished flavored e-liquid. Kit #1 has 1.80 percent nicotine content in its e-liquid while Kit #2 has no nicotine in its e-liquid. When the product is distributed, Distributor L needs to report the tobacco products tax based on the wholesale cost of the total package price of Kit #1 because the kit contains products still in their original manufacturer packaging and the e-liquid contains nicotine. The tobacco products tax does not apply to Kit #2 as it is not sold in combination with a nicotine product.

(3) Example 3: Distributor M purchases 100 packages of electronic cigarette Kit #3, which the manufacturer packaging states contains the following: a personal vaping device, tank, atomizer coil, USB charger and A/C adapter. Distributor M also purchased 100 packaged bottles of finished, flavored e-liquid containing 3.20 percent nicotine. Distributor M intends to sell both packages to wholesalers and retailers, so the customer will be separately charged for one box containing Kit #3, and one box containing a bottle of the finished, flavored e-liquid as part of the sale. When distributor M sells the packages to other wholesalers and retailers, Distributor M must report the wholesale cost on the finished, flavored e-liquid bottle containing 3.20 percent nicotine, but not on the packages of Kit #3, provided the charges for Kit #3 are separately stated.

(4) Example 4: Distributor N sells closed-system e-cigarettes to wholesalers and retailers. The closed-system e-cigarettes contain finished, flavored nicotine product, and are mechanically self-contained. Consumers cannot add or remove finished, flavored nicotine to the closed-system e-cigarette. Distributor N must report the wholesale cost of the entire closed-system e-cigarette.

Second Discussion Paper Exhibit 1 Staff Proposed Revisions to Regulation 4076 Page 5 of 5

(5) Example 5: Retailer P purchases e-juice tax paid from a licensed tobacco products distributor. Retailer P, as a promotion, will package the e-juice with a battery, a/c adapter and carrying case. The retailer’s packaged product is not subject to tax as the distribution occurred prior to Retailer P’s promotional sale.

(6) Example 6: Distributor Q advertises that if a customer purchases 10 e-cigarette cartridges with a nicotine content of 1.8 percent they will receive their choice of two accessories for free. The billing invoice shows the price charged for the cartridges and a separate charge of $0 for the accessories. The tax applies only to the price of the cartridges as the acc essories are not packaged by the manufacturer as one unit and are not invoiced as one selling price.

(gf) Rate Setting. The Board's annual determination of the rate of tax that applies to other tobacco products shall be made based on the wholesale cost of tobacco products as of March 1 of the current calendar year and shall be effective during the next fiscal year, beginning July 1.

Note: Authority cited: Section 30451, Revenue and Taxation Code. Reference: Sections 30008, 30010, 30011, 30017, 30105, 30121, 30123, 30126, 30131.1, 30131.2, 30131.5, 30201 and 30221, Revenue and Taxation Code.

Second Discussion Paper Staff Proposed Regulation 4077

Exhibit 2 Page 1 of 1

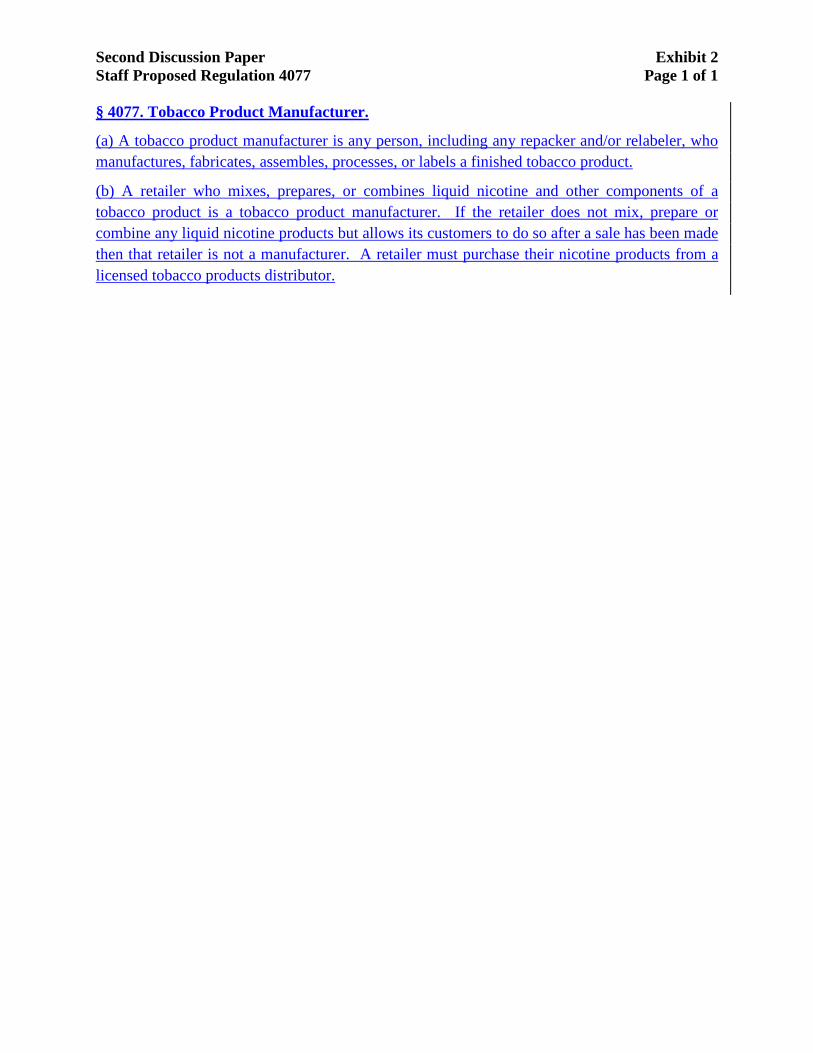

§ 4077. Tobacco Product Manufacturer.

(a) A tobacco product manufacturer is any person, including any repacker and/or relabeler, who manufactures, fabricates, assembles, processes, or labels a finished tobacco product.

(b) A retailer who mixes, prepares, or combines liquid nicotine and other components of a tobacco product is a tobacco product manufacturer. If the retailer does not mix, prepare or combine any liquid nicotine products but allows its customers to do so after a sale has been made then that retailer is not a manufacturer. A retailer must purchase their nicotine products from a licensed tobacco products distributor.

Second Discussion Paper Submission from Nu Mark LLC

Exhibit 3 Page 1 of 5

Brent L. Chambers Director, Global Infrastructure

T {804) 614-9400 NuMarl< An Alt rfa Innovation Company [email protected]

April 26, 2017

VIA EMAIL Ms. Trista Gonzalez [email protected] Chief, Tax Policy Division Business Tax and Fee Department Interested Parties Committee State Board of Equalization 450 N Street Sacramento, California 94279

RE: Nu Mark LLC's Comments on Initial Discussion Paper - Draft Amendments to California Regulation

4076 - Wholesale Cost of Tobacco Products for purposes of clarifying changes made to the Cigarette and Tobacco Products Tax Law due to the passage of Proposition 56, the California Healthcare, Research and Prevention Tobacco Tax Act of 2016 (the "Proposed Regulation")

Dear Ms. Gonzalez:

Please accept these comments regarding the Califorhia Board of Equalization ("the Board") Initial Discussion

Paper and Proposed Regulation on behalf of Nu Mark LLC (" Nu Mark"). Nu Mark is licensed as a manufacturer/ importer and distributor of electronic cigarettes in California. Nu Mark sells its products directly to Licensed California Distributors and also sells directly to California consumers through its e

commerce websites.

Nu Mark submits comments in two primary areas included in the proposed amendment to California Regulation 4076: 1) components, parts, or accessories "used during the operation of the device," and 2)

"sold in combination with."

Proposition 56 provided for a new statutory definition of electronic cigarettes, set forth in Rev. & Tax Code§

30121{c) as follows:

Electronic Cigarettes means any device or delivery system sold in combination with nicotine which can be used to deliver to a person nicotine in aerosolized or vaporized form, including, but not limited to, an e-cigarette, e-cigar, e-pipe, vape pen, ore-hookah. Electronic cigarettes include any

Nu Mark I6603 Wesl 13road Street I Richmond IVA23230

Second Discussion Paper Submission from Nu Mark LLC

Exhibit 3 Page 2 of 5

NuMarl< t\fl ,\It n .1 flnt,1,.it11 ,,. C.om::ia11v

component, part, or accessory of such a device that is used during the operation of the device when sold in combination with any liquid or substance containing nicotine. Electronic cigarettes also include any liquid or substance containing nicotine, whether sold separately or sold in combination with any device that could be used to deliver to a person nicotine in aerosolized or vaporized form.

Electronic cigarettes do not include any device not sold in combination with any liquid or substance containing nicotine, or any battery, battery charger, carrying case, or other accessory not used in the operation of the device if sold separately. Electronic cigarettes shall not include any product that has been approved by the United States Food and Drug Administration for sale as a tobacco cessation product or for other therapeutic purposes where that product is marketed and sold solely for such approved use. As used in this subdivision, nicotine does not include any food products as

that term is defined pursuant to Section 6359.

1. Components, Parts, or Accessories "Used During the Operation of the Device"

The statutory definition of electronic cigarettes includes "any component, part, or accessory of such a device that is used during the operation of the device when sold in combination with any liquid or substance containing nicotine" [Emphasis added] . Rev. & Tax Code§ 30121(c) .

We respectfully submit that pursuant to§ 30121(c), "any component, part, or accessory of such a device" is only taxable when such accessory is both 1) "used during the operation of the device" AND 2) "sold in

combination with any liquid or substance containing nicotine." Both conditions must be satisfied in order for items to be taxed. The Proposed Regulations fail to differentiate between items that are "used during the operation of the device" and items that are not. An interpretation that fails to make this distinction would render the statutory phrase "used during the operation of the device" superfluous.

The specific use of a particular item should dictate whether such "component, part or accessory" is " used during the operation of the device." For example, for electronic cigarettes, carrying cases, chargers, and A/C adapters are generally not "used during the operation of the device," while batteries are. The proposed guidance and examples should clarify that if an item is not "used during the operation of the device," it is not

taxable, even if sold in combination with a nicotine-containing liquid.

We respectfully submit that " kits, systems, or packages" which include items that are both "used during the operation of the deviceh and items that are not "used during the operation of the device" should be subject to tax based on the wholesale cost of only items that are "used during the operation of the device." We suggest the following example be added to clarify this point: Distributor sells a packaged kit containing 10 cartridges, 1 battery, 1 carrying case, 1 wall charger. Assuming the wholesale costs of individual items can

be established, the tax should be based on the wholesale cost of the 10 cartridges and battery, as these items are " used during the operation of the device." The wholesale cost of the carrying case and wall charger should NOT be included, as these items are not used during the operation of the device.

2

Second Discussion Paper Submission from Nu Mark LLC

Exhibit 3 Page 3 of 5

NuMarl<

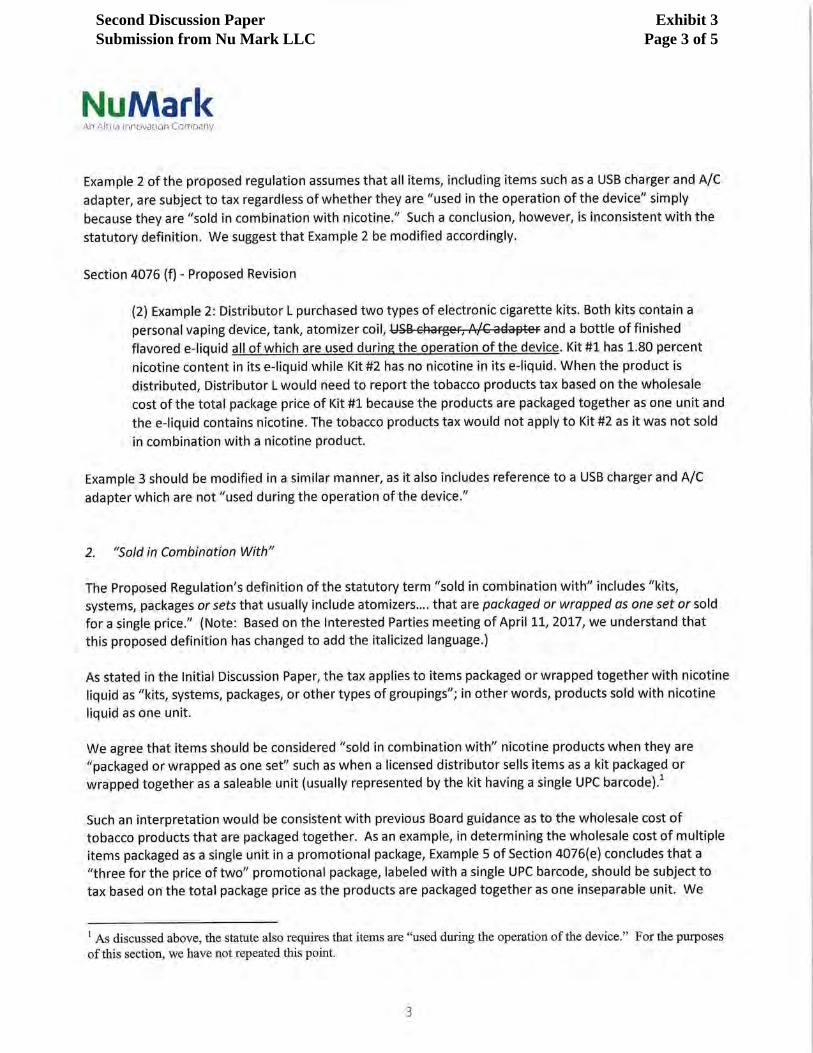

Example 2 of the proposed regulation assumes that all items, including items such as a USB charge r and A/C

adapter, are subject to tax regardless of whether they are " used in the operation of the device" simply

because they are "sold in combination with nicotine." Such a conclusion, however, is inconsistent with the

statutory definition. We suggest that Example 2 be modified accordingly.

Section 4076 (f) - Proposed Revision

{2) Example 2: Distributor L purchased two types of electronic cigarette kits. Both kits contain a

personal vaping device, tank, atomizer coil, USB cl=laFgeF, /I.JC aEJafi)teF and a bottle of finished

flavored e-liquid all of which are used during the operation of the device. Kit #1 has 1.80 percent

nicotine content in its e-liqu id while Kit #2 has no nicotine in its e-liquid. When the product is

distributed, Distributor L would need to report the tobacco products tax based on the wholesale

cost of the total package price of Kit #1 because the products are packaged together as one unit and

thee-liquid contains nicotine. The tobacco products tax would not apply to Kit #2 as it was not sold

in combination with a nicotine product.

Example 3 should be modified in a similar manner, as it also includes reference to a USB charger and A/C

adapter which are not "used during the operation of the device."

2. "Sold in Combination With"

The Proposed Regulation's definition ofthe statutory term "sold in combination with" includes "kits, systems, packages or sets that usually include atomizers .... that are packaged or wrapped as one set or sold for a single price." {Note: Based on the Interested Parties meeting of April 11, 2017, we understand that this proposed definition has changed to add the italicized language.)

As stated in the Initial Discussion Paper, the tax applies to items packaged or wrapped together with nicotine liquid as "kits, systems, packages, or other types of groupings"; in other words, products sold with nicotine

liquid as one unit.

We agree that items should be considered "sold in combination with" nicotine products when they are " packaged or wrapped as one set" such as when a licensed distributor sells items as a kit packaged or wrapped together as a saleable unit (usually represented by the kit having a single UPC barcode).

1

Such an interpretation would be consistent with previous Board guidance as to the wholesale cost of tobacco products that are packaged together. As an example, in determining the wholesale cost of multiple items packaged as a single unit in a promotional package, Example 5 of Section 4076(e) concludes that a " three for the price of two" promotional package, labeled with a single UPC barcode, should be subject to tax based oh the total package price as the products are packaged together as one inseparable unit. We

1 As discussed above, the statute also requires that items are "used during the operation of the device." For the purposes of this section, we have not repeated this point.

3

Second Discussion Paper Submission from Nu Mark LLC

Exhibit 3 Page 4 of 5

NuMarl<

respectfully submit that the determination as to whether or not an item is considered "sold in combination with" should be made in a similar manner.

The inclusion of the phrase "or for a single price" in the Proposed Regulation is not part of the statutory language, nor does it derive from previous Board guidance on the wholesale cost of tobacco products. Here, it would likely result in an overly broad application of "sold in combination with," capturing items that were never intended, particularly as applied to licensed distributors who also sell to consumers. Consider the following examples of promotional offers which are comprised of items that are not packaged together as a single unit by a licensed distributor (who also sells directly to consumers).

There are instances where a licensed distributor sells two distinctly separate products with separate and distinct UPCs for a single price. One such example would be an offer to "buy a device (a battery and an atomizer) and a bottle of e-liquid for one price," where the items are not packaged together. In such a case, the products are not being sold as a single kit or as "one set" and are not packageq together. Rather, the licensed distributor charges one price for two products, one of which should be taxed and one not. These items are not packaged together nor sold as a single unit and therefore should not be viewed as "sold in combination with" merely because they are sold for a single price.

Another example would be a promotional offer by a licensed distributor to purchase a package of nicotine cartridges and receive an accessory of one's choosing at no additional cost. This is a promotional offer of items that are not packaged together as a single unit and therefore should not be viewed as "sold in combination with" nicotine. We further submit that, under this example, providing an additional item at no additional cost should not be considered as "sold for a single price," as the additional item is being offered

for free.

In the above examples, the items are not packaged for sale as a single unit. We suggest that the Board eliminate the "sold for a single price" standard in determining whether a product is sold in combination with nicotine. Alternative ly, we suggest that the Board clarify that the term "sold for a single price" refers to selling the products as a single unit that includes nicotine, and specifically excludes promotional offers not

packaged as a single unit.

Section 4076(a) Definitions- Proposed Revisions

(5) Sold in combination with. The term "sold in combination with" refers to kits, systems, or packages that usually include atomizers, cartomizers or similar type device, component pieces, accessories, and liquids containing nicotine that are all sold and packaged as one single product for a single price. Items shall not be considered sold in combination with nicotine products if such products are not packaged as a single unit.

For the reasons stated above, we ask that the Board consider these comments and adopt the proposed revisions to Proposed Regulation 4076 as they relate to 1) components, parts and accessories "used during

the operation of the device," and 2) items "sold in combination with" nicotine.

4

Second Discussion Paper Submission from Nu Mark LLC

Exhibit 3 Page 5 of 5

NuMark An ,~lcr1a 111nl,var1on Company

Thank you for your attention.

Sincerely,

s~L. Ck,mhmtv/-rK Brent L. Chambers

Director, Global Infrastructure

Nu Mark LLC

cc: James R. Pulsifer

5

® MCCLELLAN DAVIS, LLC SALES AND USE TAX SPECIALISTS

508 GIBSON DRIVE, SUITE 1 20

ROSEVILLE, CA 95678

(B55) 995·67B9 I (91 6) 7B6·0999

FAX (91 6) 7B8·09B9 I WWW,SALESTAXHELP,COM

JMCCLELLAN@ SALESTAXHELP,COM

Second Discussion Paper Second Discussion Paper Submission Submission on behalf of on behalf of California Smoke Free Organization

Exhibit 4 Page 1 of 6

April 26, 2017

Ms. Trista Gonzalez, Chief State Board of Equalization Tax Policy Division (MIC 92) 450 N Street Sacramento, CA 94279-0092 VIA: Email: [email protected]

Re: Proposition 56 – Regulatory Rule Making

Dear Ms. Gonzalez,

Thank you for providing us with the opportunity to make this submission on behalf of the California Smoke Free Organization (CSFO). This submission is being made in response to the initial discussion paper issued on March 27, 2017, in addition to the interested parties meeting held on April 11, 2017.

The discussion at the interested parties meeting was both productive and beneficial to the process in our opinion. At the meeting, the topics of discussion included the definition of “sold in combination with,” whether the examples provided in the proposed regulation are consistent with the definition of “sold in combination with,” and whether a distributor can obtain a refund or credit for selling tax paid products outside the state. Each of those topics are addressed separately below.

Sold in combination with

Revenue and Taxation Code section 30121, subdivision (b), defines “Tobacco Products,” in relevant part, as, “a product containing, made, or derived from tobacco or nicotine that is intended for human consumption,” including “electronic cigarettes.”1 Code section 30121, subdivision (c), defines electronic cigarettes, in relevant part, as, “any device or delivery system sold in combination with nicotine which can be used to deliver to a person nicotine in

1 All references to Code sections hereafter are to the Revenue and Taxation Code unless otherwise stated.

Second Discussion Paper Second Discussion Paper Submission Submission on behalf of on behalf of California Smoke Free Organization

Exhibit 4 Page 2 of 6

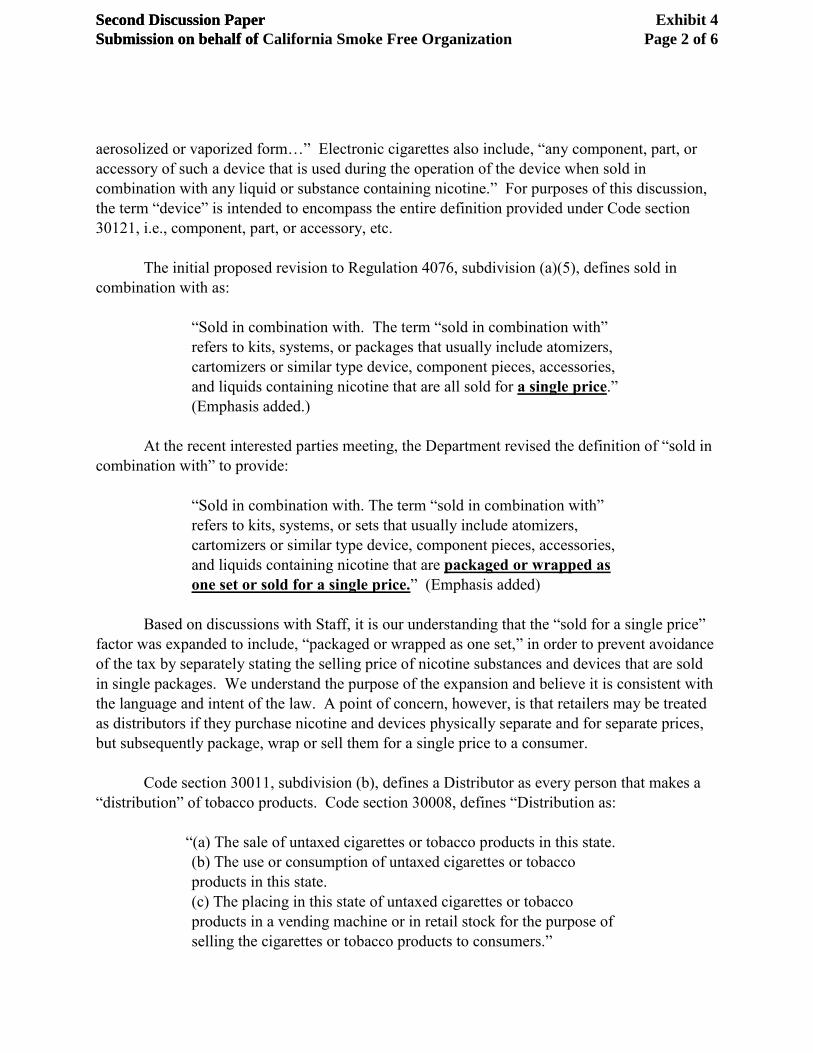

aerosolized or vaporized form…” Electronic cigarettes also include, “any component, part, or accessory of such a device that is used during the operation of the device when sold in combination with any liquid or substance containing nicotine.” For purposes of this discussion, the term “device” is intended to encompass the entire definition provided under Code section 30121, i.e., component, part, or accessory, etc.

The initial proposed revision to Regulation 4076, subdivision (a)(5), defines sold in combination with as:

“Sold in combination with. The term “sold in combination with” refers to kits, systems, or packages that usually include atomizers, cartomizers or similar type device, component pieces, accessories, and liquids containing nicotine that are all sold for a single price.” (Emphasis added.)

At the recent interested parties meeting, the Department revised the definition of “sold in combination with” to provide:

“Sold in combination with. The term “sold in combination with” refers to kits, systems, or sets that usually include atomizers, cartomizers or similar type device, component pieces, accessories, and liquids containing nicotine that are packaged or wrapped as one set or sold for a single price.” (Emphasis added)

Based on discussions with Staff, it is our understanding that the “sold for a single price” factor was expanded to include, “packaged or wrapped as one set,” in order to prevent avoidance of the tax by separately stating the selling price of nicotine substances and devices that are sold in single packages. We understand the purpose of the expansion and believe it is consistent with the language and intent of the law. A point of concern, however, is that retailers may be treated as distributors if they purchase nicotine and devices physically separate and for separate prices, but subsequently package, wrap or sell them for a single price to a consumer.

Code section 30011, subdivision (b), defines a Distributor as every person that makes a “distribution” of tobacco products. Code section 30008, defines “Distribution as:

“(a) The sale of untaxed cigarettes or tobacco products in this state. (b) The use or consumption of untaxed cigarettes or tobacco products in this state. (c) The placing in this state of untaxed cigarettes or tobacco products in a vending machine or in retail stock for the purpose of selling the cigarettes or tobacco products to consumers.”

Second Discussion Paper Second Discussion Paper Submission Submission on behalf of on behalf of California Smoke Free Organization

Exhibit 4 Page 3 of 6

Code sections 30011, 30008 and 30121, taken together, establishes that a distributor includes a person that sells untaxed devices in combination with nicotine. Therefore, a retailer that purchases nicotine and devices physically separate and for separate prices, but subsequently package, wrap them as one set or sell them for a single price to a consumer, may be considered a “distributor” of devices, since the devices under this scenario would constitute untaxed tobacco products. We understand that there is a desire to avoid retailers from being treated as distributors, and therefore believe the definition of “sold in combination with” should be changed to:

Sold in combination with. The term “sold in combination with” refers to kits, systems, or sets that usually include atomizers, cartomizers or similar type device, component pieces, accessories, and liquids containing nicotine that are sold as one set in original manufacturing packaging, or packaged or wrapped as one set or sold for a single price by a licensed distributor. Kits, systems, or sets that usually include atomizers, cartomizers or similar type device, component pieces, accessories, and liquids containing nicotine that are purchased by a retailer physically separate and for a separate price will not be considered to be “sold in combination with,” notwithstanding how those items are sold by the retailer. (Emphasis added to proposed revisions.)

We believe the above proposed language is consistent with the language and intent of the law and it will adequately protect retailers from being considered de facto distributors if they package or wrap nicotine substances and devices as one set or sell them for a single price at the retail level.2

Examples of sold in combination with

Proposed Regulation 4076, subdivision (f), contains examples of sales of tobacco products. We believe that examples 2 and 3 should be amended as necessary depending on how the regulation ultimately defines “sold in combination with.” Currently, it appears the examples focus on the single price factor.

Refunds or credits for tax paid tobacco products sold outside the state

2 We note that it may be advisable to separately define “devices” in subdivision (a). Doing so would may allow other provisions in the regulation to read more clearly.

Second Discussion Paper Second Discussion Paper Submission Submission on behalf of on behalf of California Smoke Free Organization

Exhibit 4 Page 4 of 6

At the first interested parties meeting, a question was posed by a distributor regarding whether a refund or credit would be provided for tax paid products that are subsequently distributed for use or sale outside the state. Our firm has also received numerous questions regarding this issue from businesses in the e-cigarette industry. In response to the question posed at the interested parties meeting, Staff explained that a credit or refund would not be provided to a distributor unless that distributor is the person that applied tax on its sale in interstate commerce. On the other hand, if, for example, Distributor A sold to Distributor B, the tax applied to that transaction would not be subject to refund or credit in the event that Distributor B sold the products outside the state.

“(a) The board shall, pursuant to regulations prescribed by it, refund or credit to a distributor the tax imposed on tobacco products pursuant to Article 2 (commencing with Section 30121) and Article 3 (commencing with Section 30131) of Chapter 2 which is paid on the distribution of tobacco products which are shipped to a point outside the state for subsequent use or sale out of the state.

(b) This section does not apply to tobacco products delivered to the consumer in this state and subsequently taken outside the state.”

Code section 30176.1 is implemented under Regulation 4063.5, Exported tax-paid

tobacco products, which provides in relevant part:

“The board will refund or credit to a distributor the tax paid on tobacco products which are:

(a) Shipped to a point outside this state, pursuant to a contract of sale, by delivery by the distributor to such point by means of:

(1) facilities operated by the distributor;

(2) delivery by the distributor to a carrier for shipment to a consignee at such point, or

(3) delivery by the distributor to a customs broker or forwarding agent for shipment outside this state. …

Second Discussion Paper Second Discussion Paper Submission Submission on behalf of on behalf of California Smoke Free Organization

Exhibit 4 Page 5 of 6

The distributor must file the claim for refund on Board of Equalization Form BOE-1024-T entitled "Claim for Refund— Exported Tax-Paid Tobacco Products"…”

“When an amount represented by a person to a customer as constituting reimbursement for taxes upon the distribution of tobacco products pursuant to this part is computed upon an amount that is not taxable or is in excess of the tax amount and is actually paid by the customer to the person, the amount so paid shall be returned by the person to the customer upon notification by the State Board of Equalization or the customer that an excess has been ascertained. If the person fails or refuses to do so, the amount so paid, if knowingly or mistakenly computed by the person upon an amount that is not subject to the tax imposed by this part or that is in excess of the tax amount, shall be remitted by that person to this state. Those amounts remitted to the state by the person shall be credited by the board to any amounts due and payable from that customer that are subject to this part and that are based on the same activity, and the balance, if any, shall constitute an obligation due from the person to this state.”

Based on a plain reading of Code section 30176.1, it appears the law provides a distributor with an opportunity to recover tax paid on, “tobacco products which are shipped to a point outside the state for subsequent use or sale out of the state,” even if the person that distributes the tobacco products outside the state is not the same person that paid the tax to the state. For example, if Distributor A applies tax to its distribution of tobacco products to Distributor B, then Distributor B ships the tax paid tobacco products pursuant to a contract of sale to a point outside the state, either Distributor B or at least Distributor A, should be able to obtain a refund or credit. There is no provision under the law that would preclude a refund or credit under this scenario to our knowledge. Further, if the Board of Equalization refuses to provide a refund or credit under this scenario, such an interpretation of the law will encourage sales to be made by distributors outside the state. Such a result would hinder compliance and enforcement, undermine the intent of the law and place California distributors at a competitive disadvantage.

For example, it is our understanding that an unlicensed tobacco distributor which operates outside the state without nexus with California can sell tobacco products to a licensed distributor in California without tax if the products are transferred outside the state, i.e., delivery is made by common carrier with title transfer outside the state. In that case, the California

Second Discussion Paper Second Discussion Paper Submission Submission on behalf of on behalf of California Smoke Free Organization

Exhibit 4 Page 6 of 6

distributor could subsequently sell the products outside the state without tax at a lower price point. In the scenario provided above, however, where licensed California Distributor A sells the same exact product to licensed California Distributor B, tax will apply to that transaction. Under the Staff’s interpretation, if Distributor B then sells those same products outside the state, it will be forced to sell them at a higher price point because the products will be subject to a 65.08 percent tax (as of July 1, 2017) without any opportunity to recover the tax through a refund or credit. From a business perspective, Distributor B would be encouraged to purchase its products from a distributor located outside the state, or move its own business outside the state. Such a result would undermine the intent of the law and it would hinder compliance and enforcement.

To the extent a person applies and reports tax on a sale of (untaxed) tobacco products which are shipped to a point outside the state for subsequent use or sale outside the state, we believe the tax would be subject to refund as excess tax reimbursement to the customer under Code section 30361.5, Excess Tax Reimbursement. To the extent a distributor sells tax paid products which are shipped to a point outside the state for subsequent use or sale outside the state, we believe a refund or credit should be provided pursuant to Code section 30176.1 and Regulation 4063.5.

Notwithstanding Staff’s interpretation of the law in this regard, language should be added to Regulation 4063.5, to clarify its interpretation of the law as it respect tax paid tobacco products that are shipped to a point outside the state pursuant to a contract of sale. Currently, there are no regulatory guidelines that clearly describe the precise circumstances under which a refund or credit may be obtained. Further, Regulation 4063.5 states that “[t]he distributor must

file the claim for refund on Board of Equalization Form BOE -1024-T,” but we were informed that form no longer exists. (Italics added.) The regulation creates an untenable scenario by stating that form 1024 “must” be used, when that form no longer exists.

We thank you for your consideration to our submission and we look forward to working with Staff and other interested parties to help establish clear regulatory guidelines for businesses, the audit staff and investigators.

Sincerely,

Jesse W. McClellan, Esq. On behalf of CSFO

Cc: California Smoke Free Organization

Second Discussion Paper Submission from Californians for Tobacco Harm Reduction

Exhibit 5 Page 1 of 1

April 241 2017

Trista Gonzalez, Chief

Business Tax & Fee Department

Tax Policy Division, Board of Equalization

450 N Street, Sacramento, CA

Subject: Wholesale Cost of Tobacco Products

Dear Ms. Gonzalez,

I am writing on behalf of Californians for Tobacco Harm Reduction (CATHR) to comment on the proposed

regulations for the implementation of Proposition 56 taxation on the wholesale cost of tobacco products.

CATHR is an organization that represents small business owners from across the state that aims to educate and advocate for the sale and use of e-cigarettes as safer alternative to traditional cigarettes,

With the passage of Proposition 56 in 2016, the e-cigarette industry has been hit hard by being defined as a "tobacco product", despite the only similarity being nicotine content. This and other stringent regulations

that have been adopted in recent years have severely damaged thee-cigarette industry and forced many

businesses to either close up shop, or move out of state. It is our hope the Board of Equalization will use

CATHR as a resource and consider the economic impacts as it develops regulations and determines an appropriate equivalency tax.

As for the proposed Regulation 4076 on the wholesale cost of tobacco products, our primary concerns are

with the "in combination with" language. As written, this language is complex and leaves many unanswered

questions. In particular, it is unclear whether an audit at the retail level would require business owners to

prove that tax has been paid on combined products. Additionally, it is unclear whether retailers must also hold a distribution license to sell combined tobacco products. We ask the board to consider adding clarification so that it is easy to understand and comply with.

We also ask that as the board considers the new equivalency tax, along with new regulations, that they continue to engage in a transparent and inclusive process. CATHR is concerned that the new equivalency tax

will disproportionately affect small business owners and cause more companies to move out of state. We

hope that you will work with our organization and others to ensure that any new taxes or regulations are fair and equitable for all.