1 Viktor Sekmakas Senior Vice President, Industrial Coatings and President, PPG Europe Ri k Z lk May 17, 2012 Rick Zoulek Vice President, Industrial Coatings, Americas Information current as of 5/17/2012 Statements contained herein relating to matters that are not historical facts are forward‐looking statements reflecting PPG’s current view with respect to future events and financial performance. These matters within the meaning of Section 27A of the Securities Act of 1933, as amended, and Section 21E of the Securities Exchange Act of 1934, as amended, involve risks and uncertainties that may affect PPG’s operations, as discussed in PPG’s filings with the Securities and Exchange Commission pursuant to Sections 13(a), 13(c) or 15(d) of the Exchange Act, and the rules and regulations promulgated thereunder. Accordingly, many factors could cause actual results to differ materially from the forward‐looking statements contained herein. Such Forward‐Looking Statements factors include global economic conditions, increasing price and product competition by foreign and domestic competitors, fluctuations in cost and availability of raw materials, the ability to maintain favorable supplier relationships and arrangements, the realization of anticipated cost savings from restructuring initiatives, difficulties in integrating acquired businesses and achieving expected synergies therefrom, economic and political conditions in international markets, the ability to penetrate existing, developing and emerging foreign and domestic markets, foreign exchange rates and fluctuations in such rates, fluctuations in tax rates, the impact of future legislation, the impact of environmental regulations, unexpected business disruptions, and the unpredictability of existing and possible future litigation, including litigation that could result if the asbestos settlement discussed in PPG’s filings with the Securities and Exchange Commission does not become effective. However, it is not possible to predict or identify all such factors. Consequently, while the list of factors presented here and in PPG’ s Form 10‐K for the year ended December 31 2011 are considered 2 factors presented here and in PPG s Form 10 K for the year ended December 31, 2011 are considered representative, no such list should be considered to be a complete statement of all potential risks and uncertainties. Unlisted factors may present significant additional obstacles to the realization of forward‐ looking statements. Consequences of material differences in results compared with those anticipated in the forward‐looking statements could include, among other things, business disruption, operational problems, financial loss, legal liability to third parties and similar risks, any of which could have a material adverse effect on PPG’s consolidated financial condition, results of operations or liquidity. All information in this presentation speaks only as of May 17, 2012, and any distribution of this presentation after that date is not intended and will not be construed as updating or confirming such information. PPG undertakes no obligation to update any forward‐looking statement, except as otherwise required by applicable law.

Transcript

1

Viktor SekmakasSenior Vice President, Industrial Coatings and

President, PPG EuropeRi k Z l k

May 17, 2012

Rick ZoulekVice President, Industrial Coatings, Americas

Information current as of 5/17/2012

Statements contained herein relating to matters that are not historical facts are forward‐looking statementsreflecting PPG’s current view with respect to future events and financial performance. These matters withinthe meaning of Section 27A of the Securities Act of 1933, as amended, and Section 21E of the SecuritiesExchange Act of 1934, as amended, involve risks and uncertainties that may affect PPG’s operations, asdiscussed in PPG’s filings with the Securities and Exchange Commission pursuant to Sections 13(a), 13(c) or15(d) of the Exchange Act, and the rules and regulations promulgated thereunder. Accordingly, many factorscould cause actual results to differ materially from the forward‐looking statements contained herein. Such

Forward‐Looking Statements

factors include global economic conditions, increasing price and product competition by foreign and domesticcompetitors, fluctuations in cost and availability of raw materials, the ability to maintain favorable supplierrelationships and arrangements, the realization of anticipated cost savings from restructuring initiatives,difficulties in integrating acquired businesses and achieving expected synergies therefrom, economic andpolitical conditions in international markets, the ability to penetrate existing, developing and emergingforeign and domestic markets, foreign exchange rates and fluctuations in such rates, fluctuations in tax rates,the impact of future legislation, the impact of environmental regulations, unexpected business disruptions,and the unpredictability of existing and possible future litigation, including litigation that could result if theasbestos settlement discussed in PPG’s filings with the Securities and Exchange Commission does not becomeeffective. However, it is not possible to predict or identify all such factors. Consequently, while the list offactors presented here and in PPG’s Form 10‐K for the year ended December 31 2011 are considered

2

factors presented here and in PPG s Form 10 K for the year ended December 31, 2011 are consideredrepresentative, no such list should be considered to be a complete statement of all potential risks anduncertainties. Unlisted factors may present significant additional obstacles to the realization of forward‐looking statements. Consequences of material differences in results compared with those anticipated in theforward‐looking statements could include, among other things, business disruption, operational problems,financial loss, legal liability to third parties and similar risks, any of which could have a material adverse effecton PPG’s consolidated financial condition, results of operations or liquidity. All information in thispresentation speaks only as of May 17, 2012, and any distribution of this presentation after that date is notintended and will not be construed as updating or confirming such information. PPG undertakes no obligationto update any forward‐looking statement, except as otherwise required by applicable law.

2

Industry Profile

3

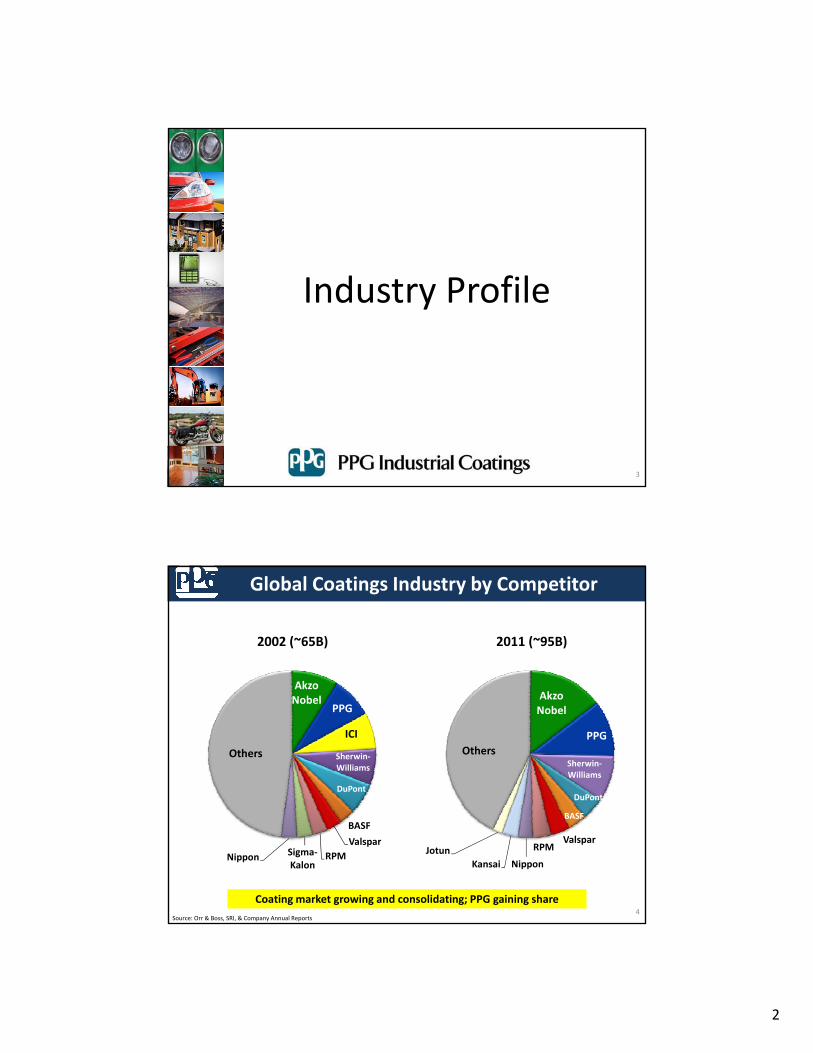

2011 (~95B)

Akzo

2002 (~65B)

Global Coatings Industry by Competitor

Akzo Nobel

PPG

Sherwin‐Williams

DuPont

Others

Akzo Nobel

PPG

ICI

Sherwin‐Williams

DuPont

Others

BASF

Valspar RPM

NipponKansaiJotun

Coating market growing and consolidating; PPG gaining share

BASF

Valspar RPMSigma‐

KalonNippon

4Source: Orr & Boss, SRI, & Company Annual Reports

3

Coatings Industry

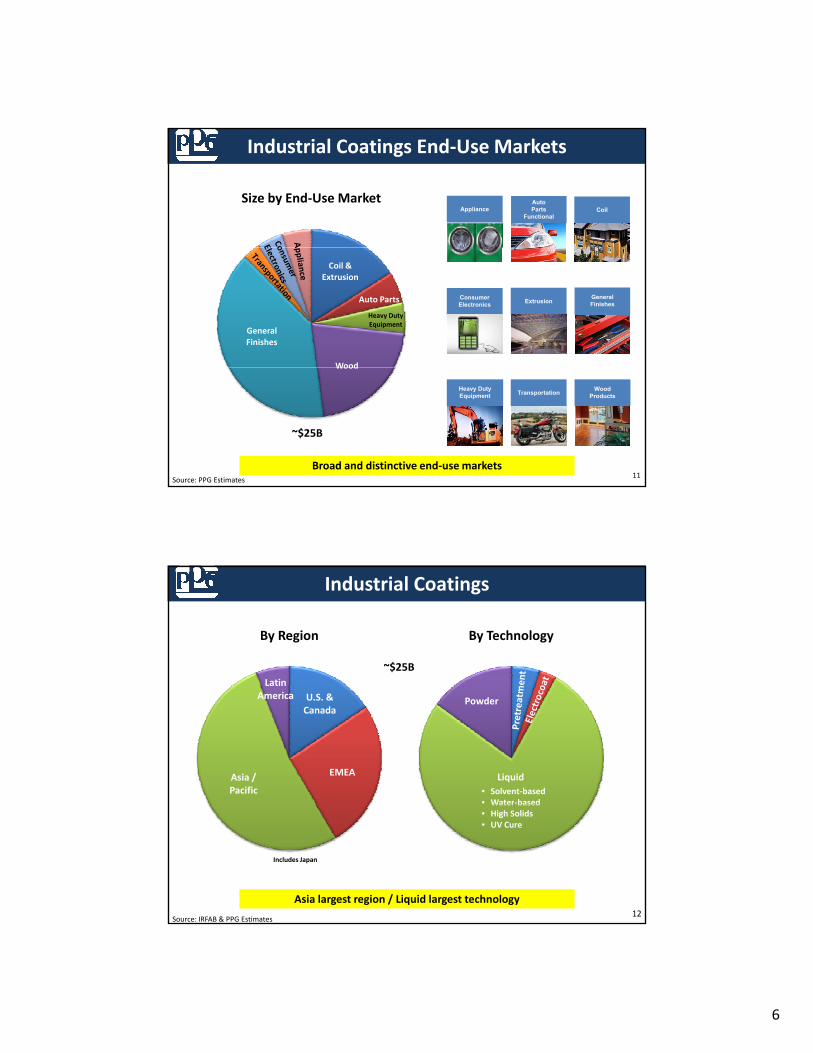

Industry End‐Market Mix by Dollar Value of Sales (~$95B)

100% = $95 Billion

Companies(#)

Company Size (Sales)

Aerospace2%

Packaging3%

Competitive Landscape

10% Hundreds < $100MM

20% ~60 $0.1 B ‐ $1.0 B

45% 17 $1 ‐ $10 B

Protective & Marine

13%

Architectural 43%

Refinish 7%

Auto OEM 6%

25% 2 > $10 B

Industrial 26%

Few large global players Industrial 2nd largest segment5

Source: Coatings World, Company Annual Reports, Orr & Boss and SRI

Position by End Use Market

Global Position

Arch.~$42B

Industrial~$25B

Protective & Marine~$12B

Refinish/Collision~$6B

Auto OEM~$6B

Packaging~$3B

Aerospace~$1B

Position by Vertical

PPG #2

Akzo #1

SHW #3

DuPont #4

Valspar #5

BASF #6

■ #1 Position ■ #2 Position ■ #3 Position #4+ Position ■ No Participation

Source: PPG estimates

PPG only company with participation in all end‐use markets6

4

Industrial Coatings

77

• Diverse end‐use markets– Tied to multiple industries

• Broad technology spectrum

Industrial Coatings Overview

• Broad technology spectrum– Increased focus on sustainable coatings

Automotive Parts and Accessories – Functional and decorative coatings for Tier II and Tier III parts suppliers for automotive applications. Functional coatings protect from corrosion and wear. Decorative coatings provide color and gloss for visual appearance to match OEM body color.

Industrial Coatings: CoilCoil – Decorative and functional (corrosion protection) coatings applied to coiled sheet metal that is then fabricated into parts or products (also referred to as prepaint).

• Building and ConstructionExamples

• Metal roofing• Metal building panels• Rainware & gutters• Siding & trim

Consumer Electronics – Functional and decorative coatings for electronic devices.

• Mobile phonesExamples

p• Laptops• Computers and accessories• GPS systems• Tablets• e‐Readers

18

10

Industrial Coatings: Extrusion

Examples

Extrusion – Decorative and functional (weather resistance) coatings applied over extruded aluminum shapes used in residential and commercial construction and specialized applications.

• Building and Construction• Commercial windows• Curtain wall• Column covers• Residential windows

• Transportation• RV and bus windows• Windshield frames

• Specialty• Sports equipmentp q p• Solar panels

19

Industrial Coatings: General Finishes

General Finishes – Decorative and functional (hardness, corrosion resistance) coatings used in a wide variety of end uses not included in any of the other sub‐segments.

Industrial Coatings: Heavy Duty EquipmentHeavy Duty Equipment – Decorative and functional coatings for agricultural, construction, mining and excavation equipment.

Wood – Functional and decorative factory‐applied coatings supplied to various wood product manufacturers.

• Wood and resilientflooring

• Window assemblies

Examples

Window assemblies• Doors and door frames• Flooring accessories• Architectural moldings• Kitchen cabinets• Furniture• Factory‐finished siding

23

Industrial Coatings Technology Options

Primary Technology Offerings:• Pretreatment ‐ cleaners & phosphate chemicals to condition metal before paint is appliedto condition metal before paint is applied

• Electrocoat – coating applied by electrically charged immersion

• Liquid – traditional primers and topcoats in a full array of chemistries

P d lid ti li d b l t t ti• Powder – solid coating applied by electro‐static spray

24

13

Technical Solutions

End‐Use Market Pretreat Electrocoat Liquid Powder

Automotive Parts &

Appliance

Automotive Parts & Accessories

Coil Coatings

Consumer Electronics

Extrusion Products

General Finishes

25

Finishes

Heavy Duty Equipment

Transportation

Wood

■ Primary ■ Secondary ■ No UseSource: PPG Illustration

Competitive Technology Profile

Supplier: North America Europe Asia Pacific South America

Basis: Notable market presence

26

Liquid Ecoat Powder Pretreatment

PPG is the only coatings supplier with a complete technology portfolio in each region

14

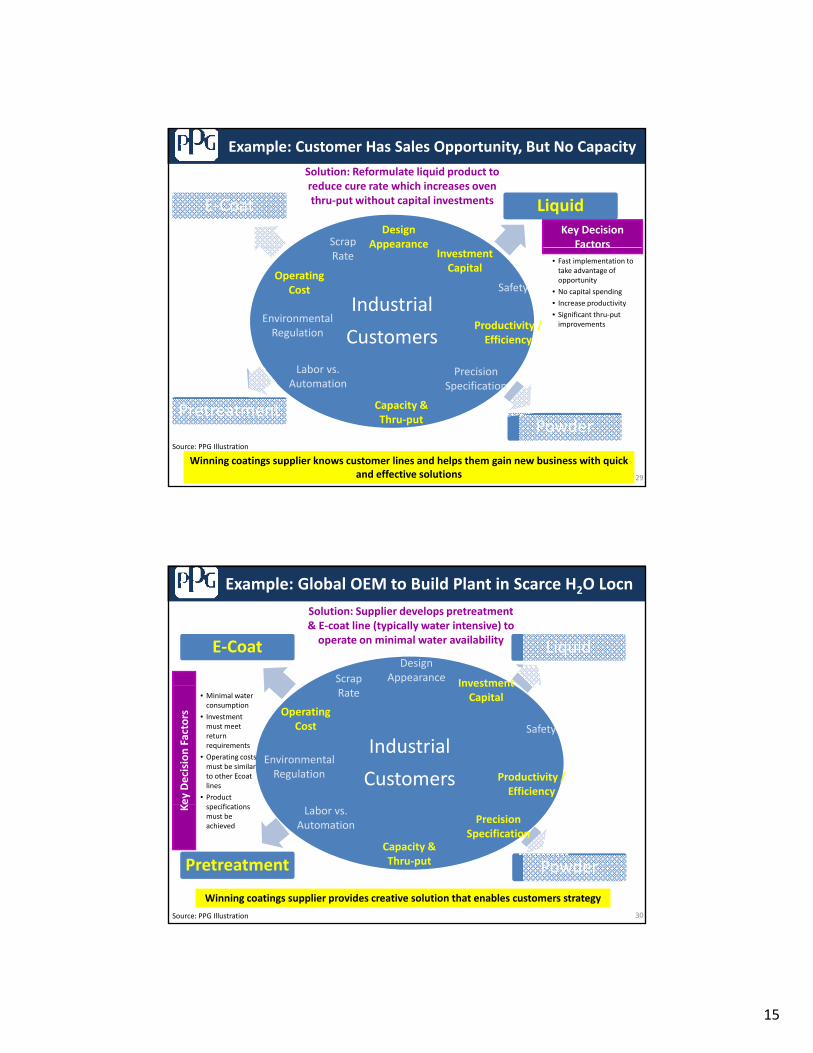

Customers’ Coatings Decision Factors

E‐Coat LiquidDesign

AppearanceInvestment Capital

Scrap Rate

Key Factors• Superior coverage,

adhesion, appearance and corrosion

Key Factors• All substrates

• Best color control

• Highest design flexibility

Industrial

Customers

CapitalOperating

Cost

Environmental Regulation

Labor vs. Automation

Precision Specification

Safety

Productivity / Efficiency

resistance

• High capital investment

• Metal substrates

Highest design flexibility

• Moderate capital investment

Key factors for customer success: process selection, coating technology & paint line operation

Pretreatment PowderCapacity & Thru‐put

27

Key Factors• Metal substrates

• Used in critical adhesion applications (prior to other 3 technologies)

Key Factors• Environmentally friendly

• Minimal capital investment

• Low cost finish

• Metal substrates

Example: Customer Required to Reduce VOC Emissions

E‐Coat LiquidDesign

AppearanceInvestment

Scrap Rate • Complies with

Solution: Customer converts from Low‐Solids, High‐VOC liquid to No‐VOC Powder

Industrial

Customers

Investment Capital

Operating Cost

Environmental Regulation

Labor vs. Precision

Safety

Productivity / Efficiency

Rate • Complies with new regulation

• Controls costs and maintains current output level

• Require minimal investment

• Product finish appears unchangedKe

y Decision Factors

Winning coatings supplier is able to help customer comply with new regulations

Pretreatment Powder

Automation Specification

Capacity & Thru‐put

28Source: PPG Illustration

15

Example: Customer Has Sales Opportunity, But No Capacity

E‐Coat LiquidDesign

AppearanceScrap

Solution: Reformulate liquid product to reduce cure rate which increases oven thru‐put without capital investments

Key Decision Factors

Industrial

Customers

AppearanceInvestment Capital

Operating Cost

Environmental Regulation

Labor vs

Safety

Productivity / Efficiency

Rate • Fast implementation to take advantage of opportunity

• No capital spending

• Increase productivity

• Significant thru‐put improvements

Factors

Winning coatings supplier knows customer lines and helps them gain new business with quick and effective solutions

PretreatmentPowder

Labor vs. Automation

Precision Specification

Capacity & Thru‐put

29

Source: PPG Illustration

E‐Coat LiquidDesign

Appearance InvestmentScrap

Example: Global OEM to Build Plant in Scarce H2O LocnSolution: Supplier develops pretreatment & E‐coat line (typically water intensive) to operate on minimal water availability

Industrial

Customers

Investment Capital

Operating Cost

Environmental Regulation

Safety

Productivity / Efficiency

Rate• Minimal water consumption

• Investment must meet return requirements

• Operating costs must be similar to other Ecoatlines

• Product ifi tiKe

y Decision Factors

Pretreatment Powder

Labor vs. Automation Precision

SpecificationCapacity & Thru‐put

30

specifications must be achieved

K

Source: PPG Illustration

Winning coatings supplier provides creative solution that enables customers strategy

16

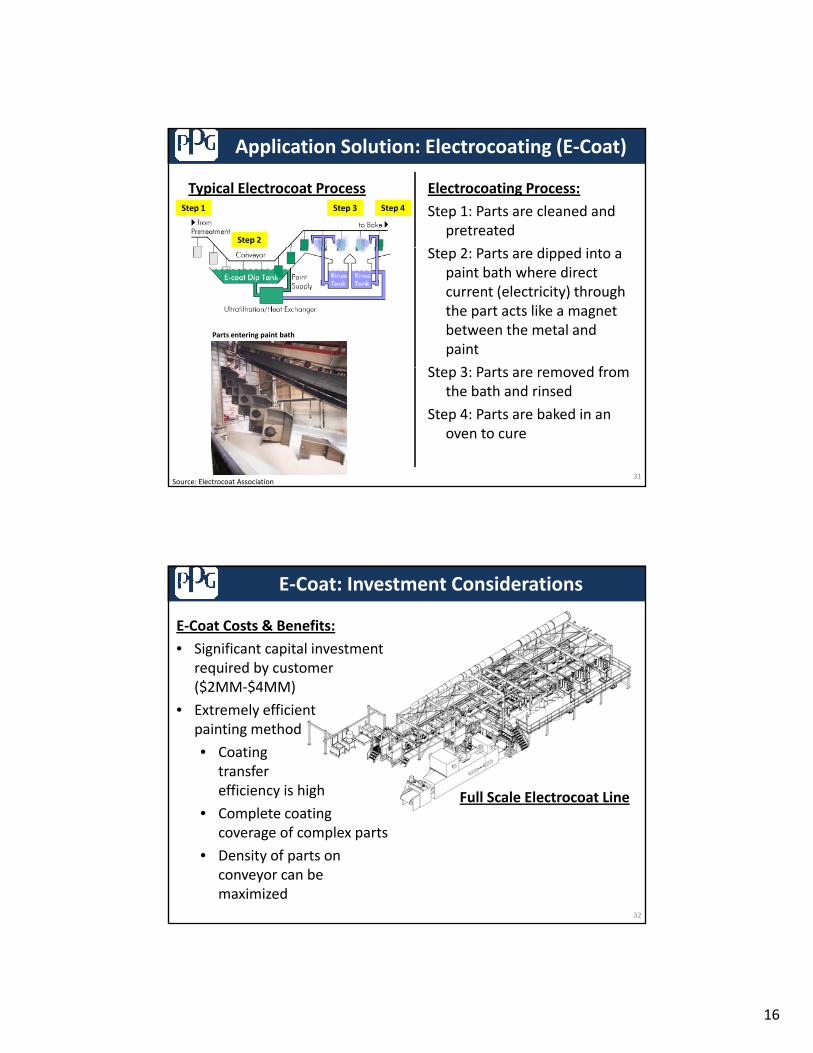

Application Solution: Electrocoating (E‐Coat)

Electrocoating Process:

Step 1: Parts are cleaned and pretreated

d d

Typical Electrocoat ProcessStep 1

Step 2

Step 3 Step 4

Step 2: Parts are dipped into a paint bath where direct current (electricity) through the part acts like a magnet between the metal and paint

S 3 P d f

Parts entering paint bath

Source: Electrocoat Association

Step 3: Parts are removed from the bath and rinsed

Step 4: Parts are baked in an oven to cure

31

E‐Coat: Investment Considerations

E‐Coat Costs & Benefits:

• Significant capital investment required by customer ($2MM $4MM)($2MM‐$4MM)

• Extremely efficient painting method

• Coating transferefficiency is high Full Scale Electrocoat Line

• Complete coatingcoverage of complex parts

• Density of parts on conveyor can be maximized

32

17

Electrocoat Dip

Electrocoat Application Comparison

Capital Investment High

Operating Cost per Part (ex: utilities, labor, maintenance)

Low

Performance Specification High performance

Capacity / Thru‐put High

Occurrence FrequencySole application method for

lOccurrence Frequency

electrocoat

End‐Use MarketAppliance, Auto Parts, General Finishes, Heavy Duty Equipment,

Transportation

Examples

Mass produced parts includingautomobile suspension

35*Primary liquid applications, not all application methods have been included

Application Solution: Powder Coatings

Fluidized BedElectrostatic Spray

Process that charges the particle of powder and then attracts it to the grounded part

before being oven cured.

Preheated parts are dipped into a bed of fluidized powder. Upon contact with the heated parts, the powder melts and adheres to the parts. The parts are then passed through a second oven for curing.

Source: Coatings Method, Inc36

19

Electrostatic Spray Fluidized Bed

Capital Investment Medium High

Powder Coatings Application Comparison

Capital Investment Medium High

Operating Cost per Part (ex: utilities, labor, maintenance)

Medium High

Object ShapeNon‐intricate shapes and must fit on

conveyorIntricate shapes; must fit on

pulleys & tank must be big enough

Finish Specification Textures may prevent full coverageSubject to variation in film thickness, any texture

Capacity / Thru‐put High Medium

Occurrence Frequency Most common method Rare

End‐Use Market(excludes Coil and Wood)

Appliance, Auto Parts, Consumer Electronics, Extrusion, General Finishes, Heavy Duty Equipment,

Transportation

Auto Parts, Consumer Electronics, General Finishes, Heavy Duty

Equipment

Examples Aluminum wheels, window screening Dishwasher racks and metal pipes

37*Primary powder applications, not all application methods have been included

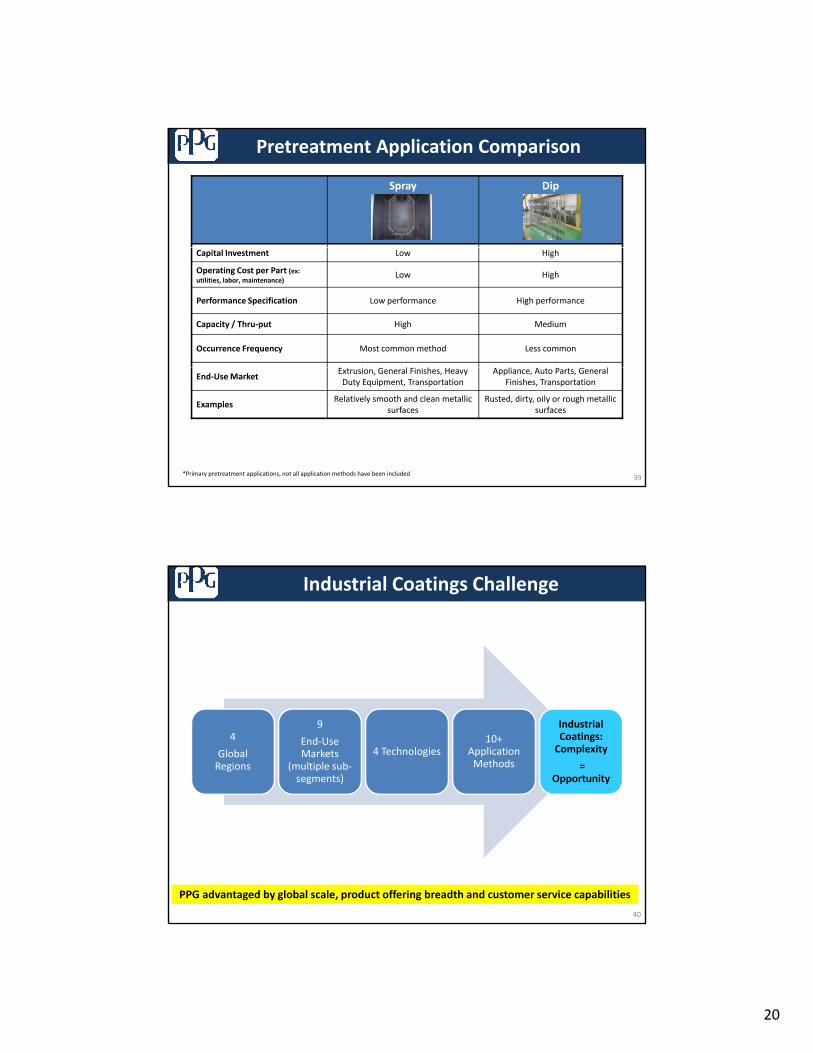

Application Solution: PretreatmentDipSpray

Pretreatment is applied via automated spray system

Pretreatment is applied via submersion into the system

38

20

Spray Dip

Pretreatment Application Comparison

Capital Investment Low High

Operating Cost per Part (ex: utilities, labor, maintenance)

Low High

Performance Specification Low performance High performance

Capacity / Thru‐put High Medium

Occurrence Frequency Most common method Less common

End‐Use MarketExtrusion, General Finishes, Heavy Duty Equipment, Transportation

Appliance, Auto Parts, General Finishes, Transportation

ExamplesRelatively smooth and clean metallic

surfacesRusted, dirty, oily or rough metallic

surfaces

39*Primary pretreatment applications, not all application methods have been included

Industrial Coatings Challenge

4

Global Regions

9

End‐Use Markets

(multiple sub‐segments)

4 Technologies10+

Application Methods

Industrial Coatings: Complexity

= Opportunity

40

PPG advantaged by global scale, product offering breadth and customer service capabilities

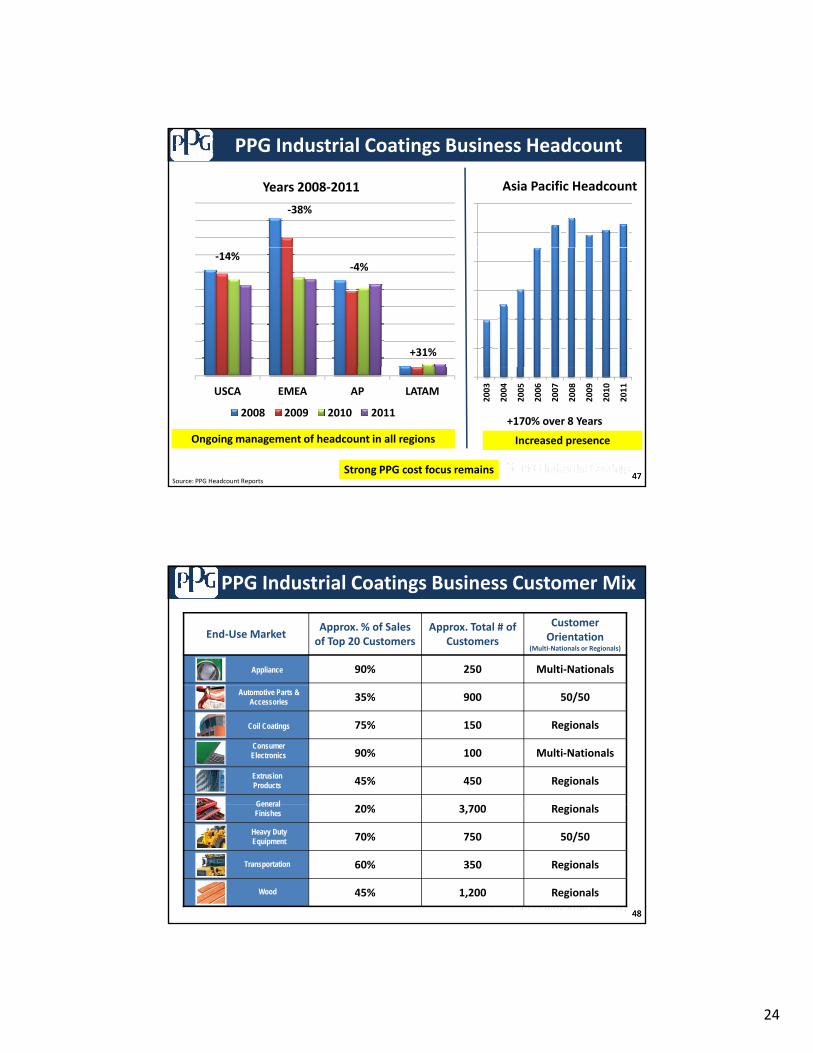

End‐Use MarketApprox. % of Sales of Top 20 Customers

Approx. Total # ofCustomers

Customer Orientation

(Multi‐Nationals or Regionals)

90% 250 Multi‐NationalsAppliance

35% 900 50/50

75% 150 Regionals

90% 100 Multi‐Nationals

45% 450 Regionals

% i l

Automotive Parts & Accessories

Coil Coatings

Consumer Electronics

Extrusion Products

General

4848

20% 3,700 Regionals

70% 750 50/50

60% 350 Regionals

45% 1,200 Regionals

General Finishes

Heavy Duty Equipment

Transportation

Wood

25

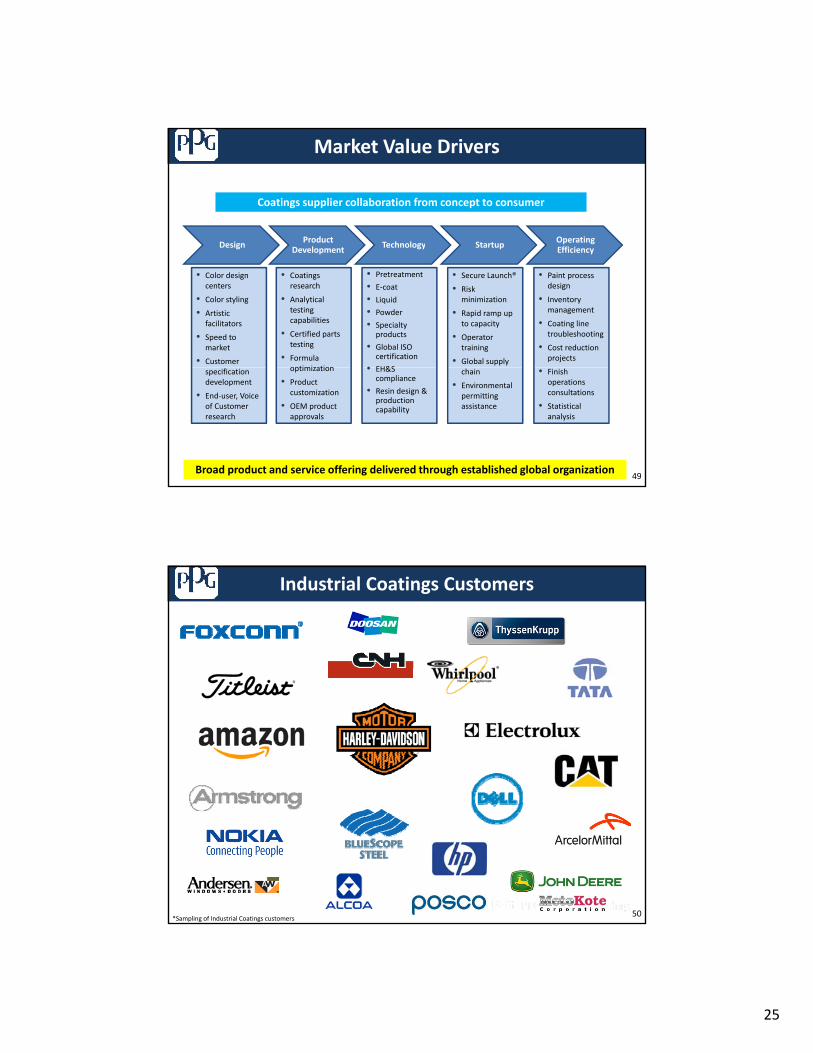

Market Value Drivers

Design Product D l t Technology Startup Operating

Effi i

Coatings supplier collaboration from concept to consumer

Design Development Technology Startup Efficiency

• Color design centers

• Color styling

• Artistic facilitators

• Speed to market

• Customer

• Coatings research

• Analytical testing capabilities

• Certified parts testing

• Formula optimization

• Pretreatment

• E‐coat

• Liquid

• Powder

• Specialty products

• Global ISO certification

• EH&S

• Secure Launch®

• Risk minimization

• Rapid ramp up to capacity

• Operator training

• Global supply

• Paint process design

• Inventory management

• Coating line troubleshooting

• Cost reduction projects

49

specification development

• End‐user, Voice of Customer research

optimization

• Product customization

• OEM product approvals

• EH&S compliance

• Resin design & production capability

chain

• Environmental permitting assistance

• Finish operations consultations

• Statistical analysis

Broad product and service offering delivered through established global organization

Industrial Coatings Customers

50*Sampling of Industrial Coatings customers

26

Industrial Coatings Asia/Pacific Customers

51*Sampling of Industrial Coatings customers

• Strong market position– All geographies

PPG Competitive Advantage

– All technologies

– Customer mix

• History of sustained investment in capabilities and technology leadership

• Global customer support

52

27

PPG Service Culture• Developing, deploying and demonstrating service culture over a very long

period of time

• Consistently winning the service battle

• Recognition of commitment in the marketplace

Product Development

TechnicalService

Customer Relationship

Product Research

Exam

ples of V

alue

Service

Areas

• Innovative solutions to meet customer needs

• Resin synthesis capabilities

• Dedicated Coatings Research Center

• Next generation

• Product formulated to paint line conditions

• Products with new colors or textures

• Customer & end‐use market‐focused labs in each region

• Global and regional account coordination

• Sponsorship of customer interests

• Partnership focus on end‐user market

• Solving coating line issues

• Driving customer cost improvement and savings

• Ensuring coatings lines are running optimally

PPG Service Culture

53Cultural demonstration of commitment to key customer requirement

Leadership

Program Evolution

Service

Foun

dation

sKe

y technology program • Emergency response capability

Training (i.e., “Knowledge College”, in‐plant)

80%

90%

100%

st

Customer Applied Paint Cost Model

All Operating Costs to Run a Paint Line:

• Non‐paint operating expenses 80%‐85% of t t l li d t

Total Customer Applied Cost of Coatings

20%

30%

40%

50%

60%

70%

% of Total App

lied Co

s

Application Cost

C ti

to Run a Paint Line:• Labor• Supervision• Operating

Supplies• Utilities• Depreciation• Rework

total applied cost

• Choice of technology, supplier and management of application process are all factors

• Overall productivity improvement

0%

10%

Customer Coating

Operation

54

Coatings Cost

Cost of Procured Paint & Pretreatment

improvement opportunity is significant

Deliver value by understanding application process and improving itSource: PPG Illustration

28

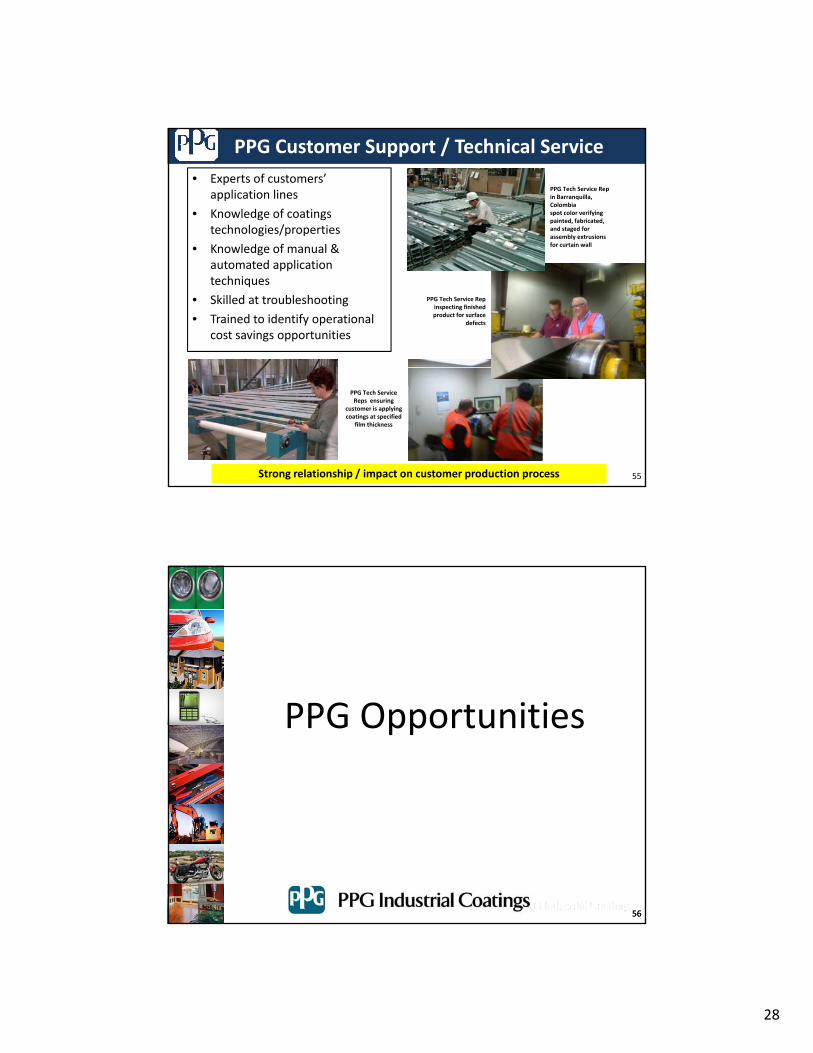

PPG Customer Support / Technical Service• Experts of customers’

application lines

• Knowledge of coatings technologies/properties

• Knowledge of manual &

PPG Tech Service Rep in Barranquilla, Colombiaspot color verifying painted, fabricated, and staged for assembly extrusions for curtain wall• Knowledge of manual &

automated application techniques

• Skilled at troubleshooting

• Trained to identify operational cost savings opportunities

PPG Tech Service Rep inspecting finished product for surface

defects

55

PPG Tech Service Reps ensuring

customer is applying coatings at specified

film thickness

Strong relationship / impact on customer production process

PPG Opportunities

5656

29

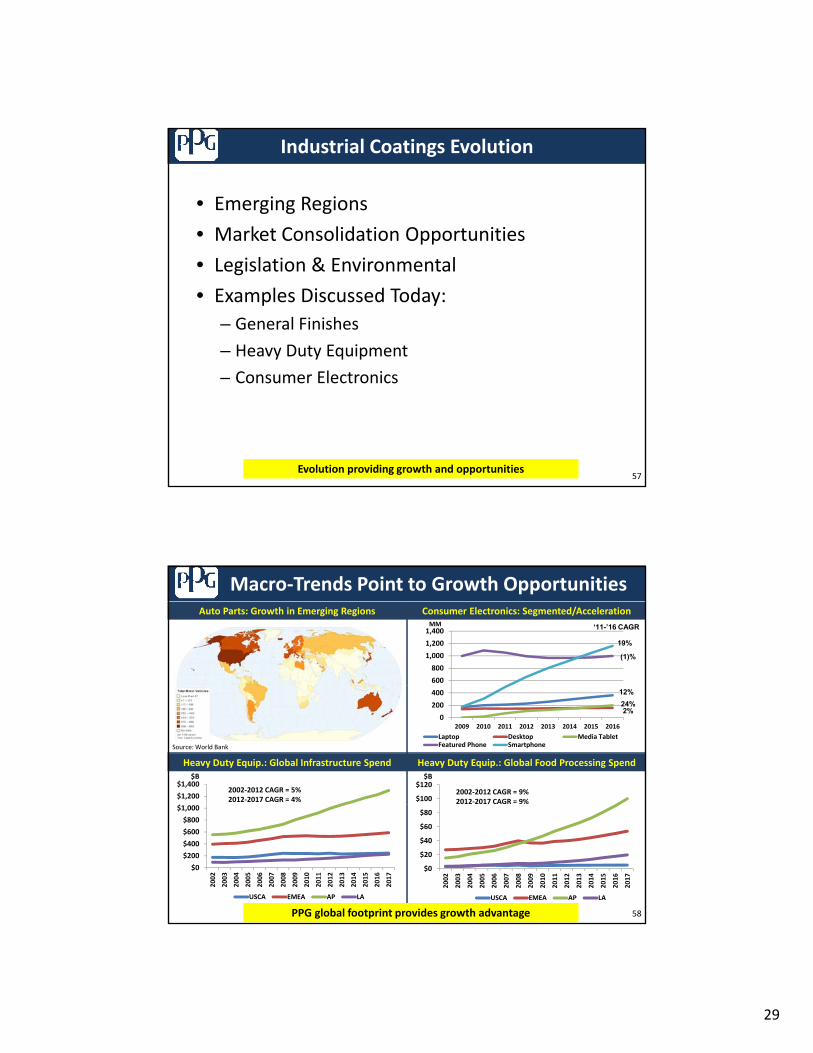

• Emerging Regions

• Market Consolidation Opportunities

Industrial Coatings Evolution

• Legislation & Environmental

• Examples Discussed Today:– General Finishes

– Heavy Duty Equipment

57

– Consumer Electronics

Evolution providing growth and opportunities

Macro‐Trends Point to Growth Opportunities

600

800

1,000

1,200

1,400MM

19%

(1)%

‘11-’16 CAGR

Consumer Electronics: Segmented/AccelerationAuto Parts: Growth in Emerging Regions

0

200

400

2009 2010 2011 2012 2013 2014 2015 2016

Laptop Desktop Media TabletFeatured Phone Smartphone

12%24%2%

Heavy Duty Equip.: Global Infrastructure Spend Heavy Duty Equip.: Global Food Processing Spend

Source: World Bank

$

$1,200

$1,400$B

$100

$120$B

2002‐2012 CAGR = 5%2012‐2017 CAGR = 4%

2002‐2012 CAGR = 9%2012‐2017 CAGR = 9%

58

$0

$200

$400

$600

$800

$1,000

2002

2003

2004

2005

2006

2007

2008

2009

2010

2011

2012

2013

2014

2015

2016

2017

USCA EMEA AP LA

$0

$20

$40

$60

$80

2002

2003

2004

2005

2006

2007

2008

2009

2010

2011

2012

2013

2014

2015

2016

2017

USCA EMEA AP LA

PPG global footprint provides growth advantage

30

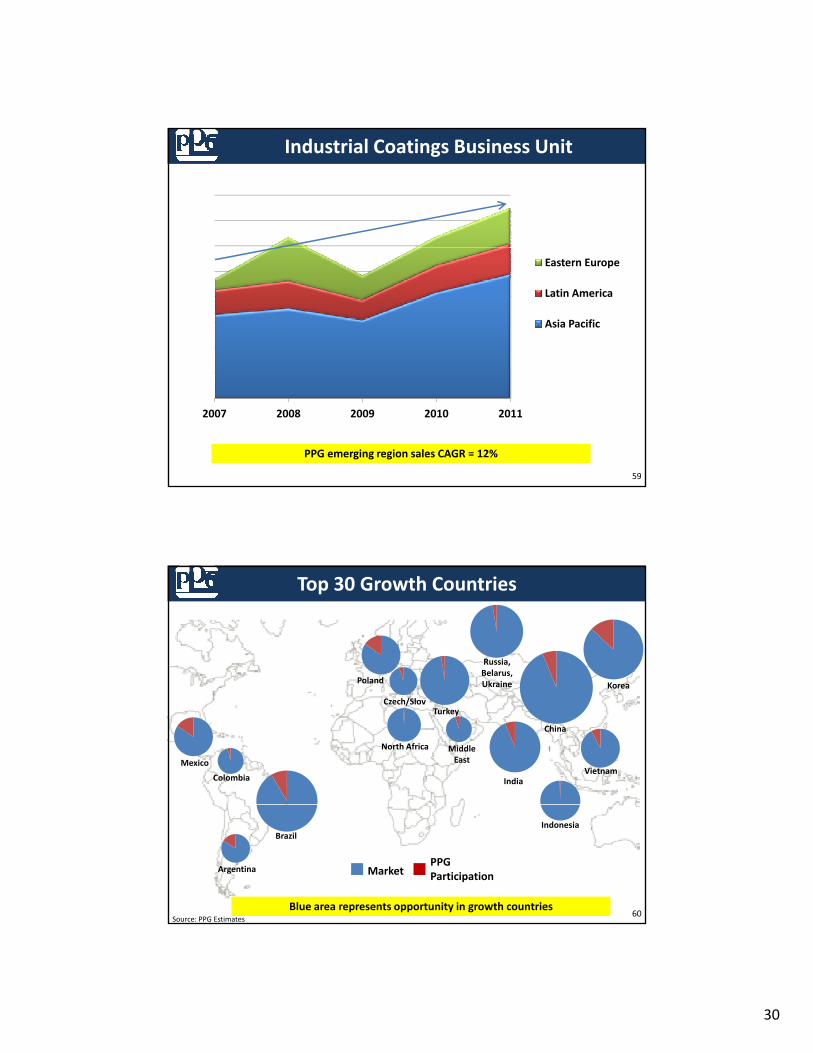

Industrial Coatings Business Unit

Eastern Europe

Latin America

Asia Pacific

59

2007 2008 2009 2010 2011

PPG emerging region sales CAGR = 12%

Top 30 Growth Countries

15%

Poland5%

3%

Russia, Belarus, Ukraine

6%

15%

Korea

2%

16%

Mexico

4%

Colombia 8%

1%

North Africa

4%

Middle East

Czech/Slov

Ukraine

China

Korea

8%

Vietnam1%

Turkey

6%

India

60

Brazil16%

Argentina

Indonesia

MarketPPG Participation

Blue area represents opportunity in growth countriesSource: PPG Estimates

31

Akzo

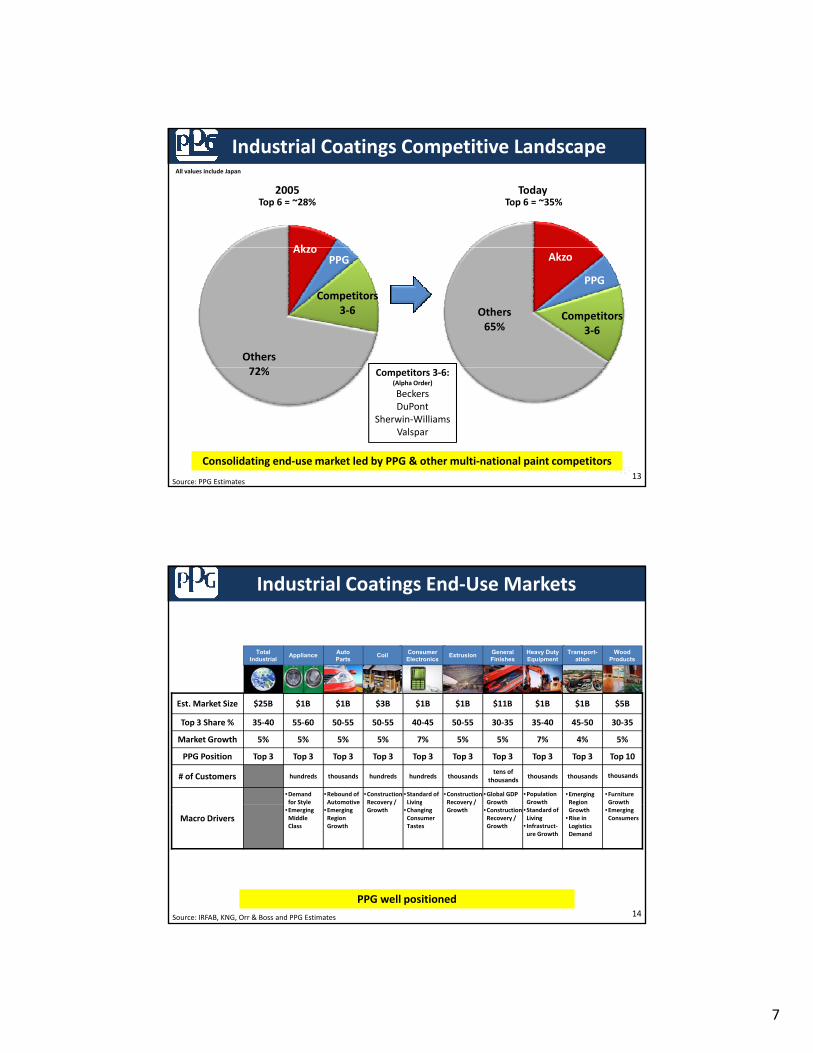

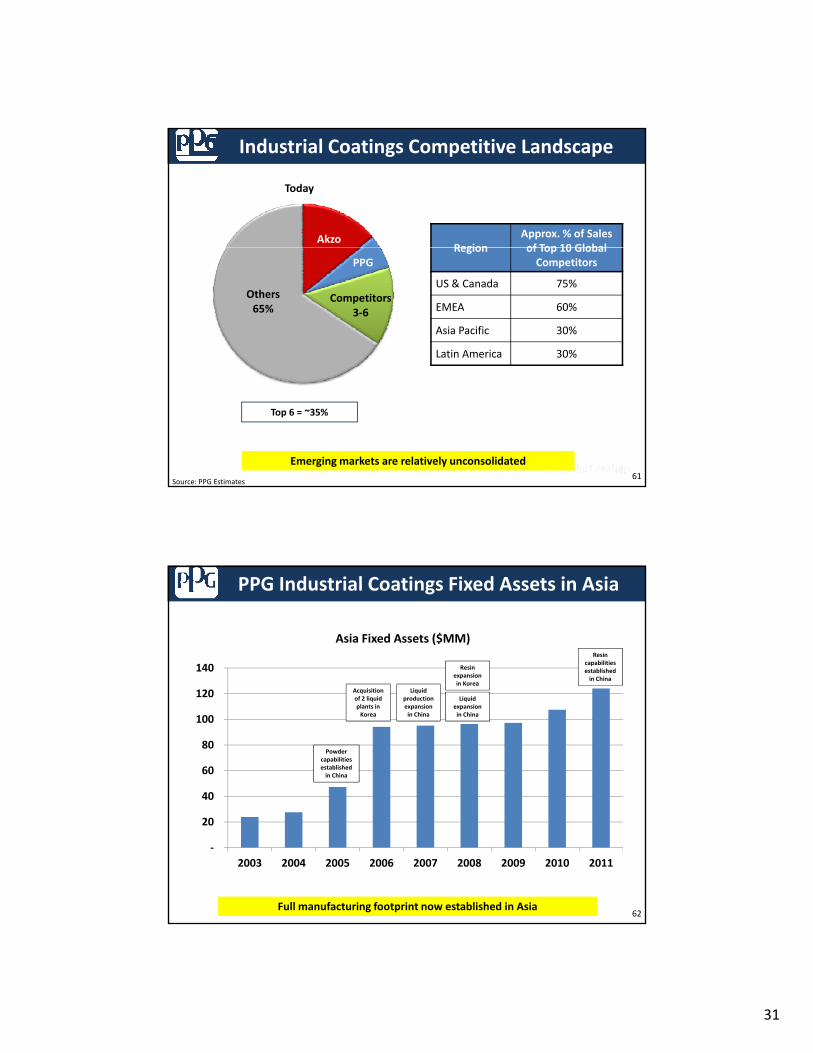

Industrial Coatings Competitive Landscape

Today

RegionApprox. % of Salesof Top 10 Global

PPG

Competitors 3‐6

Others65%

Region of Top 10 Global Competitors

US & Canada 75%

EMEA 60%

Asia Pacific 30%

Latin America 30%

61

Top 6 = ~35%

Emerging markets are relatively unconsolidated

Source: PPG Estimates

PPG Industrial Coatings Fixed Assets in Asia

140 Resin

capabilities established in China

Resin expansion in Korea

Asia Fixed Assets ($MM)

40

60

80

100

120 Liquid production expansion in China

in Korea

Liquid expansion in China

Acquisition of 2 liquid plants in Korea

Powder capabilities established in China

62

‐

20

2003 2004 2005 2006 2007 2008 2009 2010 2011

Full manufacturing footprint now established in Asia

32

Further Consolidation Potential

Thousands

# of Significant Coatings Suppliers

Consolidation Drivers of Smaller Competitors:Mature Regions 1980

Emerging Regions 1980

• Technology evolution

• Legislation / Environmental

• Liquidity / Financial stability

• Raw material volatility

• Globalization of customers

p

Emerging Regions 2010

g

63

Tens

Consolidation in emerging regions to follow

Mature Regions 2010

Source: PPG illustration

Greening of the Global Coatings Industry

Sustainability is profitability

Very low VOC, BPA‐free and metal‐free

Bio‐based raw materials

Compact Processes

Waterborne & PowderElectrocoat

Solvent‐Based High

Solids

Baked Enamels

1950‐1960’s 1970’s 1980’s 1990’s Next Gen Paints2000’s

Market Driver

Benefit

Product lifespan

Durability & c re

VOC standards

Lower cost

Rust

Corrosion resistance

VOC standards

Appearance

Cost

Operating sa in s

Regulatory standards

Environment li

64

PPG research and development providing green solutions in all technologies

Increasing Regulations Will Continue to Drive Coatings Supplier Consolidation

Europe: REACHAsia: IECSC, KECI,

PICCS

Increasing (ex: MSDS, product

stewardship)

small/local paint suppliers

to meet requirements

suppliers able to achieve

compliance

Chemical Control Regulations Affect:• Coatings product formulation• Handling and storage of chemicals• Transport of chemicals

65

PPG has necessary resources and infrastructure required for global compliance

• Transport of chemicals• Customer usage of products containing chemicals• Export and import of raw materials & finished goods related to chemicals• Documentation related to handling and content• Criminal penalties, business restrictions and fines for non‐compliance

Partial list

Industrial Coatings: General Finishes

New Products with Coatings Requirements

&

New Feature End‐Uses

General Finishes

Caskets Toolboxes Mirror

Wire

LIC

Bath FiElectrical

PPG Strategy• “Feature” end‐use markets qualify with growth potential or

critical mass

&Emerging End‐Use Markets Military Pipe

FabricOffice

Furniture

Fixtures

SolarRecreation

Electrical

6666

critical mass• “Feature” end‐use markets receive strategic focus• General Finishes is an incubator for “next end‐use” breakout• Diminishing end‐uses return to General Finishes

– ex: Metal Office Furniture

Strategic management of end‐use markets

34

General Finishes: Light Industrial Coatings

Three Types of Customers• OEM – Small to medium in size

• Custom Coater/Metal Fabricator ‐Typically supports large OEM outsource

What They Buy• Liquid air dry or powder coatings & pretreatment

• Hand spray or limited automation systems

Industry Overview (~$3B)

Customer Requirements

Typically supports large OEM outsource

• Job Shops ‐ Local “one‐off” and small batch work

Single source supplier (only supplier with alltechnologies)

Relational Selling• Trusted sales individual • Global presence (infrastructure)• Respected PPG reputation in industry

35

Heavy Duty Equipment

Accelerating Demand Emerging Region Growth

2009 2011 2015

Projected Market Demand Trend

6 0%

8.0%

Regions with Highest Construction Growth in 2012

Industry Overview

Worldwide Market = $1B

• Tied to agricultural & construction markets

• Also includes lawn & garden material handling

4% CAGR 5% CAGR

Source: IRFAB

7.3%5.9%

5.3%3.9%

0.0%

2.0%

4.0%

6.0%

Asia Pacific Latin America Middle East & Africa

Eastern Europe

2012 Highlights:• Expansion of Panama canal

• Reconstruction from earthquake damage in

69Key drivers: Global infrastructure and improved standard of living

• Also includes lawn & garden, material handling, mining and forestry equipment

• Service intensive industry• Coatings product requirements migrating to extended durability, appearance & weather resistance

• OEM operations with significant Tier I & II outsource components

Source: IHS Global Insight

• Reconstruction from earthquake damage in Japan & New Zealand

• China interior & western region development

• Increased investment in infrastructure & housing in Saudi Arabia

• World Cup and Olympics preparation in Brazil

Global Infrastructure Expanding

• Asia will require +$8 trillion USD in infrastructure upgrades over next 10 years (Source: IHS Global Insight & World Economic Forum)

• 68% new capacity; 32% maintenance & replacement

• In India, 11km of roads used to be constructed each

Emerging Region Economies

Asia

year, now 10km are built daily

• Brazil intends to invest ~$99B on maintenance on and new construction of roads.

• Only ~5‐10% of Brazil’s roads are paved (Source: Trading Economics)

• CNH investing ~$320MM for new construction equipment plant in Brazil

• CNH doubling investment commitment at Argentina plant (Agriculture)

OEM Capacity ActivityLatin America

70PPG well positioned to participate in global growth

Source: CNH & Deere Q1 Results report

CNH doubling investment commitment at Argentina plant (Agriculture)

• Deere making “substantial investment in new products and additional capacity . . . [to] more fully capitalize on world’s growing need for food, shelter and infrastructure . . .”

• Deere expanding production capacity at Orenburg, Russia facility (~$32MM)

36

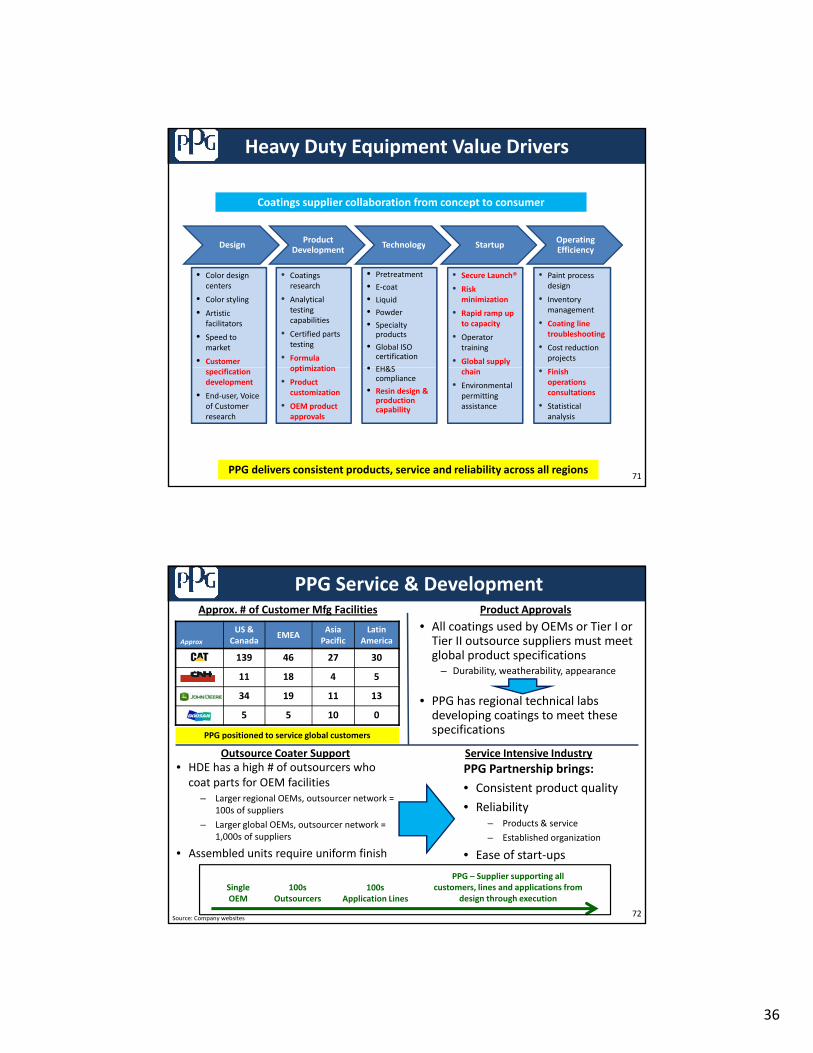

Heavy Duty Equipment Value Drivers

Design Product D l t Technology Startup Operating

Effi i

Coatings supplier collaboration from concept to consumer

Design Development Technology Startup Efficiency

• Color design centers

• Color styling

• Artistic facilitators

• Speed to market

• Customer

• Coatings research

• Analytical testing capabilities

• Certified parts testing

• Formula optimization

• Pretreatment

• E‐coat

• Liquid

• Powder

• Specialty products

• Global ISO certification

• EH&S

• Secure Launch®

• Risk minimization

• Rapid ramp up to capacity

• Operator training

• Global supply

• Paint process design

• Inventory management

• Coating line troubleshooting

• Cost reduction projects

71

specification development

• End‐user, Voice of Customer research

optimization

• Product customization

• OEM product approvals

• EH&S compliance

• Resin design & production capability

chain

• Environmental permitting assistance

• Finish operations consultations

• Statistical analysis

PPG delivers consistent products, service and reliability across all regions

Approx

US &Canada

EMEAAsiaPacific

LatinAmerica

139 46 27 30

11 18 4 5

PPG Service & DevelopmentProduct ApprovalsApprox. # of Customer Mfg Facilities

• All coatings used by OEMs or Tier I or Tier II outsource suppliers must meet global product specifications

– Durability, weatherability, appearance

34 19 11 13

5 5 10 0

PPG Partnership brings:

• Consistent product quality

• Reliabilit

Service Intensive Industry

PPG positioned to service global customers

• PPG has regional technical labs developing coatings to meet these specifications

Outsource Coater Support• HDE has a high # of outsourcers who coat parts for OEM facilities

– Larger regional OEMs, outsourcer network =

72

• Reliability – Products & service

– Established organization

• Ease of start‐ups

100s of suppliers

– Larger global OEMs, outsourcer network = 1,000s of suppliers

• Assembled units require uniform finish

SingleOEM

100sOutsourcers

100sApplication Lines

PPG – Supplier supporting all customers, lines and applications from

design through execution

Source: Company websites

37

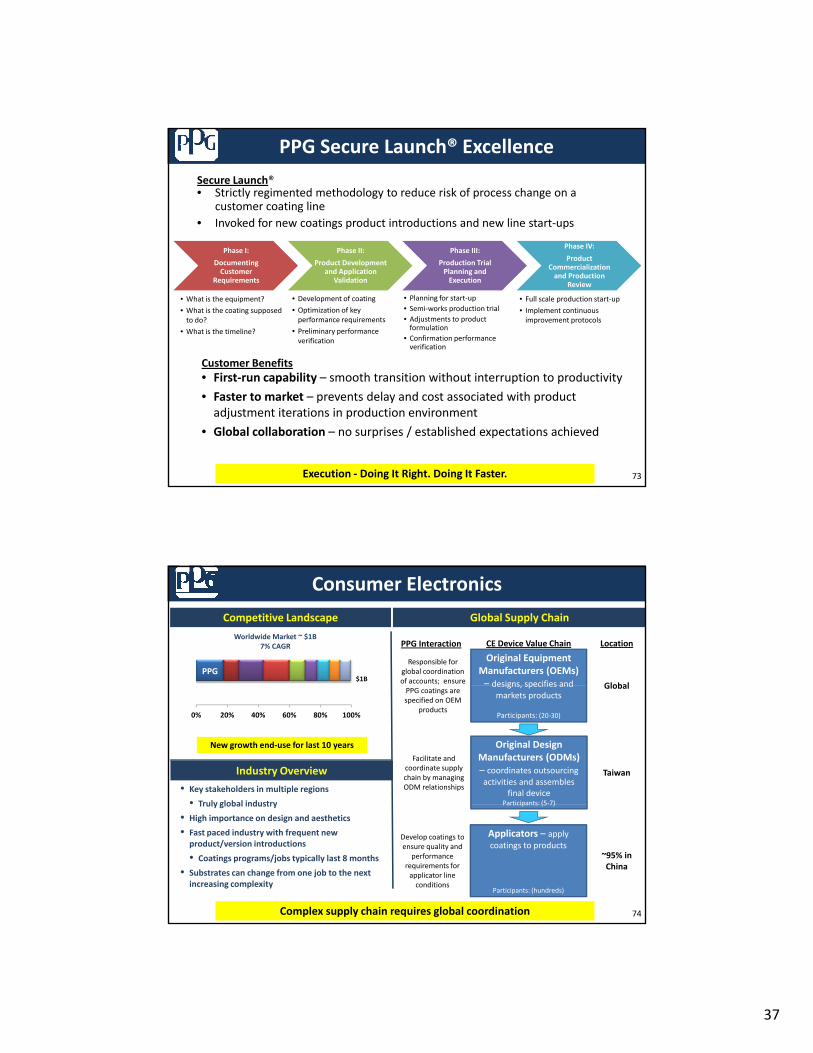

PPG Secure Launch® Excellence

h h h Phase IV:

• Strictly regimented methodology to reduce risk of process change on a customer coating line

• Invoked for new coatings product introductions and new line start‐ups

Secure Launch®

Phase I:

Documenting Customer

Requirements

Phase II:

Product Development and Application

Validation

Phase III:

Production Trial Planning and Execution

Phase IV:

Product Commercialization and Production

Review

Customer Benefits

• What is the equipment?

• What is the coating supposed to do?

• What is the timeline?

• Development of coating

• Optimization of key performance requirements

• Preliminary performance verification

• Planning for start‐up• Semi‐works production trial• Adjustments to product formulation

• Confirmation performance verification

• Full scale production start‐up

• Implement continuous improvement protocols

73

• First‐run capability – smooth transition without interruption to productivity

• Faster to market – prevents delay and cost associated with product adjustment iterations in production environment

• Global collaboration – no surprises / established expectations achieved

Execution ‐ Doing It Right. Doing It Faster.

Consumer Electronics

Competitive Landscape Global Supply Chain

PPG

Worldwide Market ~ $1B 7% CAGR

$1B

Original Equipment Manufacturers (OEMs) – designs specifies and

PPG Interaction CE Device Value Chain Location

Responsible for global coordination of accounts; ensure Global

0% 20% 40% 60% 80% 100%

Industry Overview

• Key stakeholders in multiple regions

• Truly global industry

Original Design Manufacturers (ODMs) – coordinates outsourcing activities and assembles

final deviceParticipants: (5‐7)

designs, specifies and markets products

Participants: (20‐30)

Facilitate and coordinate supply chain by managing ODM relationships

PPG coatings are specified on OEM

products

Taiwan

Global

New growth end‐use for last 10 years

74Complex supply chain requires global coordination

Truly global industry

• High importance on design and aesthetics

• Fast paced industry with frequent new product/version introductions

• Coatings programs/jobs typically last 8 months

• Substrates can change from one job to the next increasing complexity

Participants: (5 7)

Applicators – apply coatings to products

Participants: (hundreds)

Develop coatings to ensure quality and

performance requirements for applicator line conditions

~95% in China

38

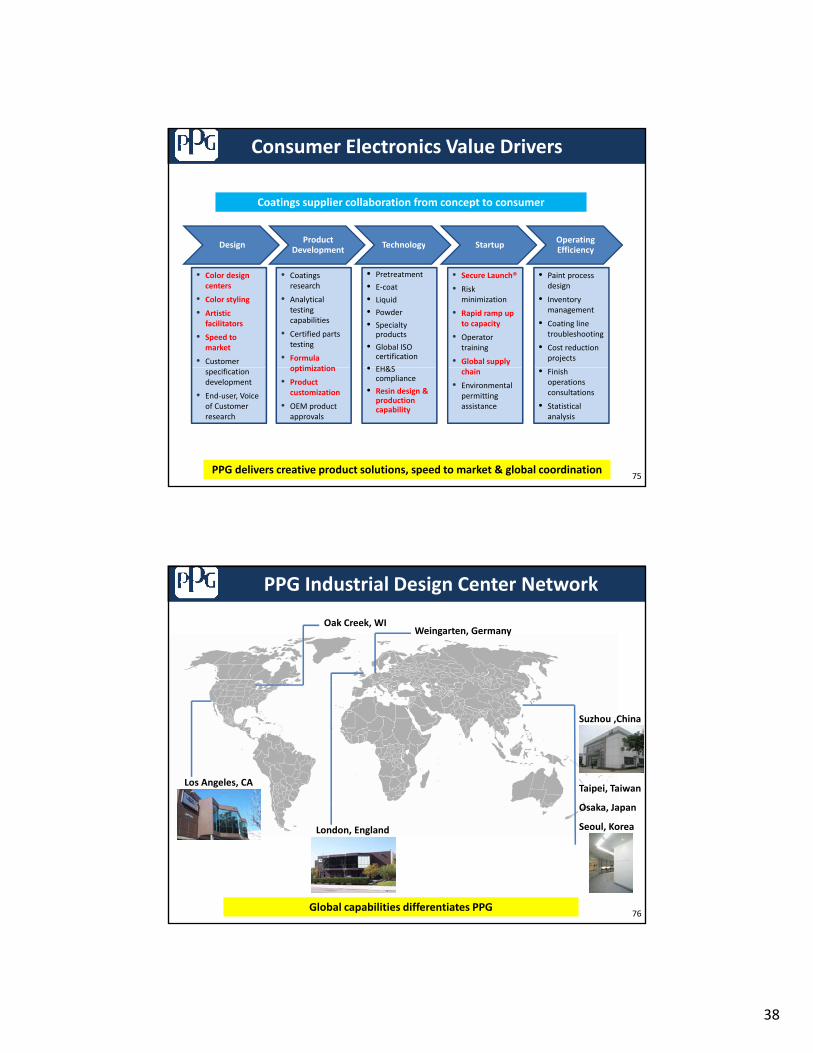

Consumer Electronics Value Drivers

Design Product D l t Technology Startup Operating

Effi i

Coatings supplier collaboration from concept to consumer

Design Development Technology Startup Efficiency

• Color design centers

• Color styling

• Artistic facilitators

• Speed to market

• Customer

• Coatings research

• Analytical testing capabilities

• Certified parts testing

• Formula optimization

• Pretreatment

• E‐coat

• Liquid

• Powder

• Specialty products

• Global ISO certification

• EH&S

• Secure Launch®

• Risk minimization

• Rapid ramp up to capacity

• Operator training

• Global supply

• Paint process design

• Inventory management

• Coating line troubleshooting

• Cost reduction projects

75

specification development

• End‐user, Voice of Customer research

optimization

• Product customization

• OEM product approvals

• EH&S compliance

• Resin design & production capability

chain

• Environmental permitting assistance

• Finish operations consultations

• Statistical analysis

PPG delivers creative product solutions, speed to market & global coordination

PPG Industrial Design Center Network

Oak Creek, WIWeingarten, Germany

Suzhou ,China

Taipei, Taiwan

O k J

Los Angeles, CA

76

Osaka, Japan

Seoul, KoreaLondon, England

Global capabilities differentiates PPG

39

PPG Color Design Process

• Global team with multiple interactive design centers

• Customer design partnershipsD i i i / i• Design innovation/creation

• Multi‐market knowledge• Multi‐input fashion‐color forecasting• Product solutions for “fast to market”

77Design, product quality & speed key factors

PPG Color Workshop

A High Impact Customer Experience

78

• Popular with customer designers• Interactive color palette

development in a facilitated environment

• Ability to create and demonstrate color and coating finish effects

40

Summary

• Industrial is the coating industry’s 2nd largest segment at ~$25B in sales

– PPG is the 2nd largest supplier in this market• Multiple industrial end‐uses present complexity which provide opportunities for growth

– PPG has strong positions in all end‐uses• Multiple end‐use markets, technologies and application methods require customer and supplier expertise

– PPG’s service capabilities provide high value coatings and

79

p p g gapplication expertise to customers

• Emerging regions are a significant growth opportunity–PPG has a strong position in Asia and also is the only global single source coatings supplier

–PPG is positioned to leverage emerging region supplier consolidation

Relationship with Harley

Harley Value PPG Support

Color StylingCustom color palette developments for all annual model introductions and maintenance of classic color palettes

Total Source Supply Purge solvents, pretreatment, Ecoat, liquids and powders

ServiceStrong operations support, product development, technical support, process optimization and onsite problem solving

All 3 Harley Assembly Locations & Outsourcers (95% of total

coatings buy)

PPG supplies all coatings technologies

23 Years

41

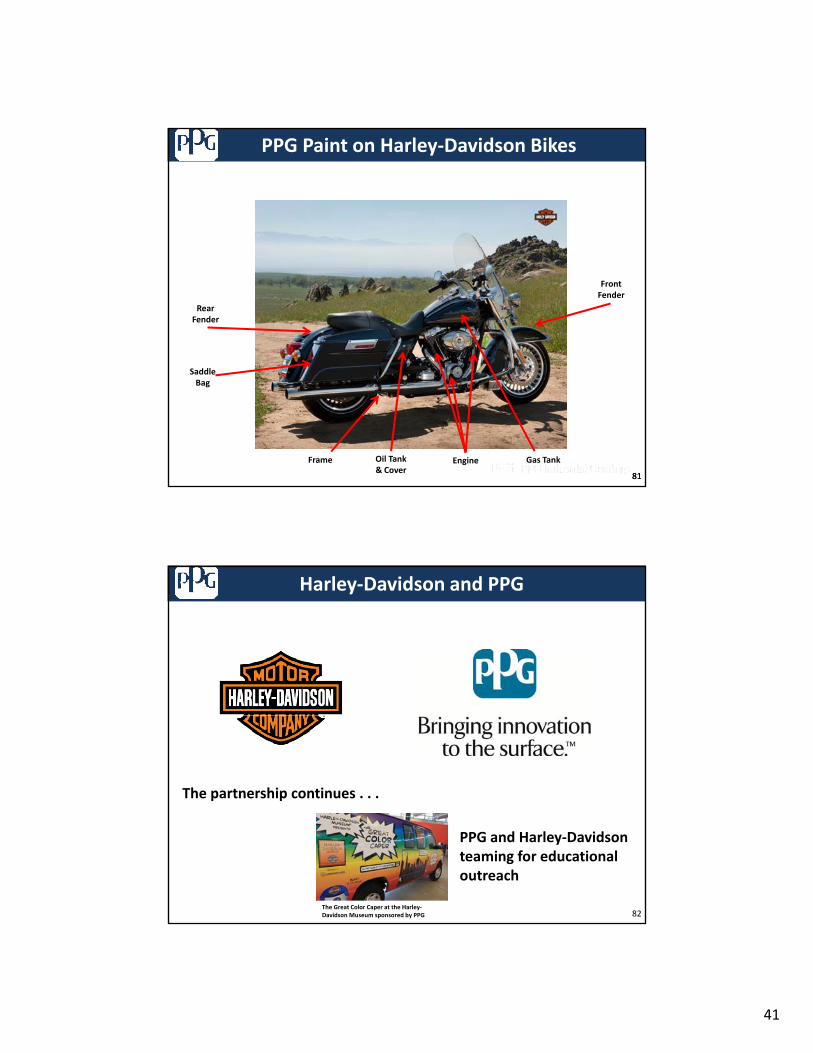

PPG Paint on Harley‐Davidson Bikes

Rear Fender

Front Fender

8181

Engine Gas TankFrame Oil Tank & Cover

Saddle Bag

Harley‐Davidson and PPG

The partnership continues . . .

82The Great Color Caper at the Harley‐Davidson Museum sponsored by PPG

PPG and Harley‐Davidson teaming for educational outreach

42

Appendix

8383

PPG Executive Profiles

David B Navikas Viktoras R Sekmakas

David B. Navikas is senior vice president, finance and chief financial officer of PPG Industries.

He joined PPG as controller in 1995 and was elected vice president in 2000. Navikas assumed his current position in June 2011 and serves on PPG’s executive and operating committees.

Prior to joining PPG, Navikas developed his career through 22 years ith ti fi D l itt & T h LLP H l d li t

David B. Navikas Senior Vice President, Finance and Chief Financial Officer

Viktor Sekmakas is senior vice president, industrial coatings, and president, PPG Europe, of PPG Industries.

Sekmakas joined PPG in 1997 with the acquisition of Lilly Industries’ electrocoat business and became market development manager, powder coatings. He became global director, automotive parts and accessories, in 2000, and then general manager, industrial coatings, Asia/Pacific, in 2001. In 2005, Sekmakas added responsibility as managing director, coatings, Asia/Pacific, to his industrial coatings responsibilities.

He was named vice president, coatings, and managing director, Asia/Pacific, i 2006 I 2008 S k k d id PPG A i /P ifi d i

Viktoras R. Sekmakas Senior Vice President, Industrial Coatings, and President, PPG Europe

8484

with accounting firm Deloitte & Touche LLP. He was lead client service partner for a number of major companies and educational institutions, audit partner and formerly partner in charge of the PPG account, and professional practice director of the Pittsburgh office.

Navikas received an undergraduate industrial management degree from Purdue University and a master's degree in accounting from Syracuse University. He is a native of Lancaster, Pa., and a member of the American Institute of Certified Public Accountants and the Pennsylvania Institute of Certified Public Accountants. Navikas also serves as a director on the board of Family House in Pittsburgh.

in 2006. In 2008, Sekmakas was named president, PPG Asia/Pacific, and in early 2010 he additionally assumed responsibility for PPG’s global industrial coatings business. Upon assuming the role of senior vice president in August 2010, Sekmakas added responsibility for PPG’s global packaging coatings business and became a member of the company’s Operating Committee. In September 2011, Sekmakas moved from PPG’s Asia/Pacific headquarters in Hong Kong to its European headquarters in Rolle, Switzerland, to assume his current role.

Prior to joining PPG, Sekmakas worked for Valspar as new business manager starting in 1990, and for Lilly Industries as electrocoatmarket manager starting in 1995.

Sekmakas earned a BS in chemical engineering from the University of Illinois.

43

PPG Executive Profiles

Richard J. Zoulek is Vice President, Industrial Coatings, Americas of PPG Industries.

After joining PPG in 1989 as an Account Representative with the Adhesives and Sealants business group, Rick rapidly moved through a number of progressively responsible sales, technical development and marketing positions with the Automotive Coatings strategic business unit.

In 1996, he joined Industrial Coatings in the leadership role of Product Manager for Automotive Parts & Accessories. Afterwards, Rick assumed

Richard J. Zoulek Vice President, Industrial Coatings, Americas

Vince Morales is vice president, investor relations, of PPG Industries.

He joined PPG in the corporate controller’s office, Pittsburgh headquarters, in 1985. Progressive finance and accounting assignments with PPG facilities included supervisor, shared accounting services, in Chillicothe, Ohio, and director, information and financial services, in Mt. Zion, Ill.

Morales returned to Pittsburgh in 2000 as manager, chemical revenue recognition, then became director, internal financial reporting, in 2001. He

d di i l i i N b 2004 d hi

Vince J. MoralesVice President, Investor Relations

8585

responsibility for the Transit & Light Rail coatings segment as Market Manager in 2000 and two years later was promoted to the position of Regional Sales Manager for the General Industrial North Region. He was assigned the role of Director, Transportation Coatings in 2004 and assumed global responsibility as General Manager, Consumer Electronics in 2008.

Rick was appointed to the position of General Manager, Industrial Coatings for the United States and Canada in September of 2010. Then, in 2012, he was promoted to his current role of Vice President, Industrial Coatings, Americas.

A native of Michigan, Rick earned his BS in Information Science from the University of Michigan and his MBA from Wayne State University.

was named director, investor relations, in November 2004 and to his current position in October 2007.

A native of Pittsburgh, Morales earned a bachelor’s degree in accounting from Robert Morris University and a Master of Business Administration degree from the Ohio State University.