35

SEPA - A Guide for Business Customers SEPA Credit Transfer (SCT) SEPA Direct Debit Core Scheme (SDD Core) Version: 2.1 (effective 20 th November 2016) Published: November 2016

SEPA - A Guide for Business Customers

SEPA Credit Transfer (SCT)

SEPA Direct Debit Core Scheme (SDD Core)

Version: 2.1 (effective 20th November 2016)

Published: November 2016

SEPA Guide for Business Customers Version 2.1 V2 May 2016 Page 2

Table of contents

SEPA Guide for Business Customers Version 2.1 V2 May 2016 Page 3

1 Purpose of the Document

The purpose of this document is to provide information to business customers on the following SEPA

payment schemes:

SEPA Direct Debit Core (SDD)

SEPA Credit Transfer (SCT)

The information is provided as a guide only and should be used in conjunction with the SEPA Scheme

Rulebooks and associated Implementation Guidelines published by EPC.

The complete SEPA Scheme Rulebooks and associated Implementation G

-cep.eu) The Scheme Rulebooks are published

in November each year, and any amendments may require this guide to be updated year on year.

engage with their own bank for information on SCT and SDD set up and processing. Creditors

must also contact their own bank in relation to Rulebook Version 9.2 changes, effective

November 2016, and particularly for details of the new submission times for SDD files.

This document does not cover the optional SEPA B2B scheme (Business to Business scheme).

Customer must contact their own bank for further information on the scheme.

This document will be updated by Banking & Payments Federation Ireland (BPFI), as required and

the most recent version will be published on BPFI website www.bpfi.ie. It is the us

to ensure they are referring to the most up to date version of the guide.

The document replaces the previous published SEPA Creditors Guide.

Disclaimer

While every effort has been made to ensure the accuracy of information included in this document, BPFI can accept no responsibility for errors contained herein.

The information in this publication may change from time to time users are advised to refer to the latest available version.

SEPA Guide for Business Customers Version 2.1 V2 May 2016 Page 4

1.1 Document History

Version Number Brief Description Date Published

V1.0 SEPA A guide for Business Customers replaces the previous published SEPA Creditors Guide

December 2015

V2 Updated based on SDD Core Rule Book V9.2effective date Nov 2016

All Collections presented for the first time, on a recurrent basis or as a one-off Collection can be presented up to D-1 Inter-Bank Business Day (D-1)

(FRST) in a first of a recurrent series of Collections is no longer mandatory (i.e. a first Collection can be identified in the same way as a subsequent

SMNDA

indicate Same Mandate with a New Debtor Agent - the definition of the acronym

Same Mandate with a New Debtor Account.

May 2016

V 2.1 Updated to note Creditors offering Phone & Internet sign up must provide a paper mandate for non irish iban.

Nov 2016

SEPA Guide for Business Customers Version 2.1 V2 May 2016 Page 5

2 SEPA Executive Summary

2.1 About SEPA

The Single Euro Payments Area (SEPA) is a European-wide initiative to standardise the way retail

electronic payments are made and processed in euro. Using SEPA, payments throughout Europe can

be as fast, safe and efficient as when using national payment systems. SEPA enables customers to

make payments (Direct Debits, Credit Transfers) to anyone located within the SEPA zone. The

jurisdictional scope of the SEPA Schemes currently consists of the 28 EU Member States plus

Iceland, Norway, Liechtenstein, Switzerland, Monaco and San Marino.

SEPA live date was 1st February 2014, an extra transition period of six months was allowed

and the final migration date to SEPA was 1st August 2014

The EPC developed the SEPA payment schemes as defined in the SEPA Credit Transfer

(SCT) and SEPA Direct Debit (SDD) Rulebooks. The rulebooks contain sets of rules and

standards for the execution of SEPA payment transactions that have to be followed by

adhering payment service providers (PSPs).

The SEPA mandatory payment schemes are as follows

payment schemes:

SEPA Direct Debit Core (SDD) the scheme replaced the existing domestic legacy Direct

Debit schemes throughout Europe

SEPA Creditor Transfer (SCT) the scheme replaced the existing domestic retail Credit

Transfer schemes throughout Europe

Overview of SEPA payments:

SEPA covers transactions in euro only

cross border and

domestic

XML formats is used for SEPA file formats

Returns/Rejects processing is an automated process

Overview of SEPA processing:

SEPA payments (one-off or bulk payment files) are submitted by customers to their bank

(CSM) at various times during

the day

CSM processes the files and manages the settlement process. CSM issues output files to

the banks for processing to customer accounts

Banks process the output files and update their customer accounts

Further information on SEPA is available on the European Payments Council website:

http://www.europeanpaymentscouncil.eu/

SEPA Guide for Business Customers Version 2.1 V2 May 2016 Page 6

2.2 SEPA Credit Transfer Scheme

The SEPA Credit Transfer Scheme facilitates the execution of Credit Transfers in euro between

customer accounts located in SEPA. Credit Transfers can be single payments (one-off payments) or

bulk payments e.g. payroll, supplier payments. The PSPs executing the credit transfer must formally

adhere to the SCT Scheme. BPFI is the EPC appointed NASO (National Adherence Support

Organisation) for Ireland.

Glossary of terms

The Originator: Customer who initiates the Credit Transfer instruction

The Originator Bank: The Bank that receives the Credit Transfer instruction from the

Originator and processes the payment instruction

The Beneficiary Bank: The Bank that receives the Credit Transfer instruction from

the Originator Bank and credits the account of the Beneficiary

The Beneficiary: The customer identified in the Credit Transfer instruction who

receives the funds by means of a credit to its account

Provisions of the SCT scheme

The following provisions are available through the SCT scheme:

- -

payments can be made to any SEPA country

Originator (payer), Beneficiary (payee) and their banks are identified using BIC and IBAN

Beneficiary will receive funds within one business day of the payment being executed

The full amount of a payment will always be received by the Beneficiary

Transaction costs for cross border SEPA payments will be equal to the transaction costs for

corresponding national payments

Originator and Beneficiary can each only be charged by their own payment service provider

More detailed remittance information can be included with a payment as up to 140 characters

are permitted

Rejects and Returns are automatically returned to the Originator

Overview of the SCT process

Originator creates a payment file and submits it to its Bank within the agreed cut off time

usually via their Online Banking channel

The payment file can be submitted up to 14 days before the payment date but at the latest

one business day before the payment date

Originator s Bank checks/validates the SCT file & debits the Originator s account

Payment file is sent by Originator Bank for processing & settlement via the SEPA clearing

mechanism CSM, known as STEP2

STEP2 issues output payment files to the Beneficiary Banks for processing

Beneficiary Banks credit the Beneficiary account during the business day

For more information:

Business customers must contact their own Bank on how to become an Originator and how to submit

SCT payment files for processing.

For a definitive source of information regarding the rules and obligations of the scheme, refer to the

SCT Rulebook and the accompanying Implementation Guidelines approved by the EPC.

SEPA Guide for Business Customers Version 2.1 V2 May 2016 Page 7

2.3 SEPA Direct Debit Core Scheme (SDD)

The SEPA Direct Debit Core Scheme is a standard payment scheme across Europe for the collection

of funds between a Debtor (payer) and the Creditor (payee). The SDD Scheme allows for the

collection of Direct Debit payments in euro across all SEPA countries. The payment service providers

executing the direct debit transaction must formally participate in the SDD Scheme. IPSO is the EPC

appointed NASO (National Adherence Support Organisation) for Ireland.

Glossary of Terms

Creditor: The originator of the SEPA Direct Debit on the basis that the Debtor has signed/authorised a Direct Debit Mandate, previously known as the Originator

Creditor Bank: The Bank where the SEPA Direct Debit Creditor holds his/her account and who will process the Direct Debit instruction

Debtor: The person who pays the Direct Debit and has signed/authorised the SEPA

Direct Debit Mandate

Debtor Bank: The Bank where the Debtor holds his/her account

Mandate: The authorisation given by the Debtor to the Creditor to allow the

Creditor to debit the specified Debtor

Overview of the SEPA DD processes

Creditor applies to their Bank to become a SEPA Creditor and applies for a SEPA Creditor

Identifier number (CI)

Creditor creates and issues a Mandate to its customer

Customer completes the Mandate and returns it to the Creditor

Creditor stores the Mandate

Creditor creates a SEPA Direct Debit file which includes mandate details (XML file format)

Creditor submits the file to its Creditor Bank for processing

Creditor Bank validates the file - submits it to STEP2, the SEPA clearing mechanism (CSM)

for clearing

STEP2 issues output files to the Banks

Banks process the output files and update their customers bank accounts

Provisions of the SDD scheme

SDD provides a standardised direct debit payment service that enables consumers to pay for goods

and services in any SEPA reachable country without having to open a bank account in that country.

Some key points to note regarding the SDD Scheme:

The Creditor and Debtor must each hold an account with a financial institution located in

SEPA

A BIC1

(Business Identifier Code) and IBAN (International Bank Account Number) are

required to set up a SDD

The transfer of funds between Creditor and Debtor always takes place in euro

The SDD may be used for single or recurrent direct debit collections

The Creditor is responsible for issuing, storing and maintaining the Mandate

1

(Optional for national transactions2 mandatory for cross border EEA transactions until 31 January 2016 - Mandatory for cross border non-EEA transactions) 2

Unless the Member State has opted for the derogation defined in Article 16(6) of the SEPA Regulation

SEPA Guide for Business Customers Version 2.1 V2 May 2016 Page 8

SDD supports two Mandate types: - Mandates, used to collect single payments, and

ent Mandates, where the Creditor can indefinitely continue to collect payments for the

purposes described on the Mandate

Advance notice of the date and the amount of each direct debit must be provided by the

Creditor to the Debtor. The advance notice period is generally fourteen days, or in some

cases seven days or less if agreed by all parties, before the direct debit is collected

SEPA Guide for Business Customers Version 2.1 V2 May 2016 Page 9

2.4 BIC & IBAN

Since 1st

January 2007, BIC (Business Identifier Code) and IBAN (International Bank Account

Number), are the only beneficiary customer account identifier and bank routing designation accepted

by banks in the EU/EEA area for all intra-EU/EEA euro cross-border credit transfers.

From 1st

effect. Creditors/Originators will only be

required to provide an IBAN (not the BIC) for the purpose of making a payment (credit transfer/direct

The Banking & Payments Federation Ireland website www.bpfi.ie provides a BIC & IBAN mobile app

d account

number to BIC & IBAN.

2.4.1 BIC

The BIC or Business Identifier Code is a unique address which in payment messages identifies

precisely the Bank/Business (not the Branch) involved in financial transactions. When used in

conjunction with the IBAN it identifies the bank at which the account of the beneficiary is held.

A valid BIC can be eight or eleven characters, although most banks in Ireland use eight character

BICs. The optional three characters can be used by the Bank/Business to identify a branch. In some

2.4.2 IBAN

An IBAN (International Bank Account Number) is an internationally agreed standard created to

uniquely identify the account of a customer at a financial institution.

The IBAN consists of up to 34 alphanumeric characters; the first two letters denote the country code,

then two check digits, and finally a country-specific Basic Bank Account Number (BBAN which

includes the domestic bank account number, branch identifier, and potential routing information).

There are standard lengths and formats of alphanumeric characters for IBANs in respect of each

country e.g. in Ireland, the standard is 22 characters.

SEPA Guide for Business Customers Version 2.1 V2 May 2016 Page 10

3 Participating in the SEPA Direct DebitScheme

Customers need to apply to their Bank to become a Creditor so that they can collect SEPA Direct

Debits. Each Bank applies its own prudential criteria for assessing the suitability of a customer as a

Creditor for inclusion in the SEPA Direct Debit Scheme.

3.1 SEPA Creditor Identifier Number (CI)

Each Creditor is identified with a SEPA Creditor Identifier (CI). This is a unique identification

number in the SDD scheme for each Creditor. The CI is used when submitting SEPA Direct

Debit files to the Bank for processing

A CI can be used by a Creditor for collections in all SEPA countries so if a Creditor moves

Bank it can continue to use the same CI

The CI will be issued to Creditors by their Bank

A central record of CI

Creditors in the Republic of Ireland

3.2 Creditor Identifier Information

The Creditor Identifier (CI) is a unique identification of Creditors, meaning that each CI only

refers to one Creditor

A single Creditor, however, is free to use more than one CI or only to use one CI for the

initiation of collections in all SEPA countries

Most communities have their own specific procedures for providing a CI to Creditors. In

Ireland the CI is issued by the Creditor Bank to the Creditor.

The following is a general structure for the CI:

Position 1-2 filled with the ISO country code

Position 3-4 filled with the check digit according to ISO 7064 Mod 97-10

Position 5-7 filled with the Creditor Business Code, if not used then filled with ZZZ.

Position 8 onwards filled with the country specific part of the identifier being a national

identifier of the Creditor

3.3

Obtain and use a Creditor Identifier when effecting SEPA Direct Debits

Use a Mandate which complies with the SEPA standards and has been approved by its Bank

if required

Comply with the terms of Mandates agreed with its Debtors

Collect and process data related to the Mandates in accordance with the rules as outlined in

the SEPA DD Scheme

Pre-notify Debtors in relation to Collections in advance of any debit on their account (at least

14 calendar days before collecting the payment or as agreed with Debtor)

Initiate Collections with the Bank in accordance with the relevant timing requirements set out

in the Scheme.

Confirm cut-of times for file submission with your bank.

Perform all operational tasks allocated to Creditors under the Scheme

Effect all Rejects, Returns and Refunds in relation to its Collections presented through the

Creditor Bank

SEPA Guide for Business Customers Version 2.1 V2 May 2016 Page 11

Provide any Creditor Bank with Mandate collection information and/or copy of Mandate,

where requested and within the timelines outlined in the Scheme

Comply with any guidance for Creditors issued from time to time in relation to risk mitigation

Resolve any disputes concerning the underlying contract and the related payments directly

with the Debtor

SEPA Guide for Business Customers Version 2.1 V2 May 2016 Page 12

4 About Mandates

In order to collect funds via a SEPA Direct Debit, the Creditor must have the Debtor

authorisation to debit the account in the form of a Mandate. The Mandate is the

authorisation given by the Debtor to the Creditor to allow the Creditor to initiate Collections

for debiting the specified Debtor's account

A Mandate can be a paper document which is physically signed by the Debtor

A Creditor should forward a copy of the Mandate to their Creditor Bank for approval

A Mandates this is available for

Irish Debtors only see Section 4.3 for further information on Paperless Mandates Phone

and Internet Sign Up

The Creditor dematerialises the Mandate, the process of dematerialisation consists of the

conversion of the Mandate information into electronic form. The data elements of the signed

Mandate must be dematerialised by the Creditor without altering the content of the Mandate

.

The signed Mandate must be stored by the Creditor for as long as the Mandate exists

The paper Mandate can be stored either as the original document or in any digitalised

format subject to the national legal requirements

The Mandate must not be forwarded to the Debtor

All Mandates together with any related amendments / history must be retained by the

Creditor for the life of the Mandate and after expiry, for a period of 13 months after the date

of the last collection

The Creditor must be able to present a copy of the Mandate to the Debtor

request. If the Creditor is not able to do so, a refund and compensation will be required if the

Debtor objects to the debit

The Debtor can cancel the Mandate at any time. If the Debtor does not cancel the Mandate,

it automatically expires 36 months after the last collected direct debit

Once the Mandate has expired/or has been cancelled, it cannot be used again for that

Debtor

SEPA Guide for Business Customers Version 2.1 V2 May 2016 Page 13

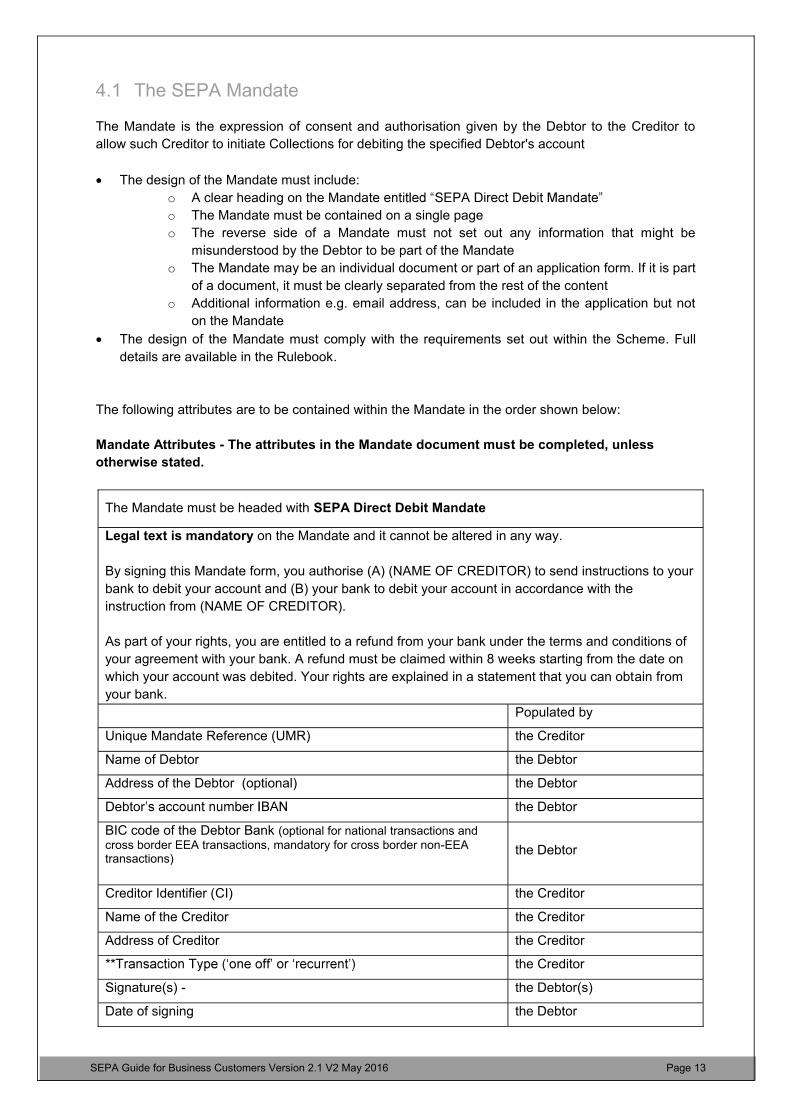

4.1 The SEPA Mandate

The Mandate is the expression of consent and authorisation given by the Debtor to the Creditor to

allow such Creditor to initiate Collections for debiting the specified Debtor's account

The design of the Mandate must include:

A clear heading on the Manda

The Mandate must be contained on a single page

The reverse side of a Mandate must not set out any information that might be

misunderstood by the Debtor to be part of the Mandate

The Mandate may be an individual document or part of an application form. If it is part

of a document, it must be clearly separated from the rest of the content

Additional information e.g. email address, can be included in the application but not

on the Mandate

The design of the Mandate must comply with the requirements set out within the Scheme. Full

details are available in the Rulebook.

The following attributes are to be contained within the Mandate in the order shown below:

Mandate Attributes - The attributes in the Mandate document must be completed, unless

otherwise stated.

The Mandate must be headed with SEPA Direct Debit Mandate

Legal text is mandatory on the Mandate and it cannot be altered in any way.

By signing this Mandate form, you authorise (A) (NAME OF CREDITOR) to send instructions to your

bank to debit your account and (B) your bank to debit your account in accordance with the

instruction from (NAME OF CREDITOR).

As part of your rights, you are entitled to a refund from your bank under the terms and conditions of

your agreement with your bank. A refund must be claimed within 8 weeks starting from the date on

which your account was debited. Your rights are explained in a statement that you can obtain from

your bank.

Populated by

Unique Mandate Reference (UMR) the Creditor

Name of Debtor the Debtor

Address of the Debtor (optional) the Debtor

Debtor the Debtor

BIC code of the Debtor Bank (optional for national transactions andcross border EEA transactions, mandatory for cross border non-EEA transactions)

the Debtor

Creditor Identifier (CI) the Creditor

Name of the Creditor the Creditor

Address of Creditor the Creditor

the Creditor

Signature(s) - the Debtor(s)

Date of signing the Debtor

SEPA Guide for Business Customers Version 2.1 V2 May 2016 Page 14

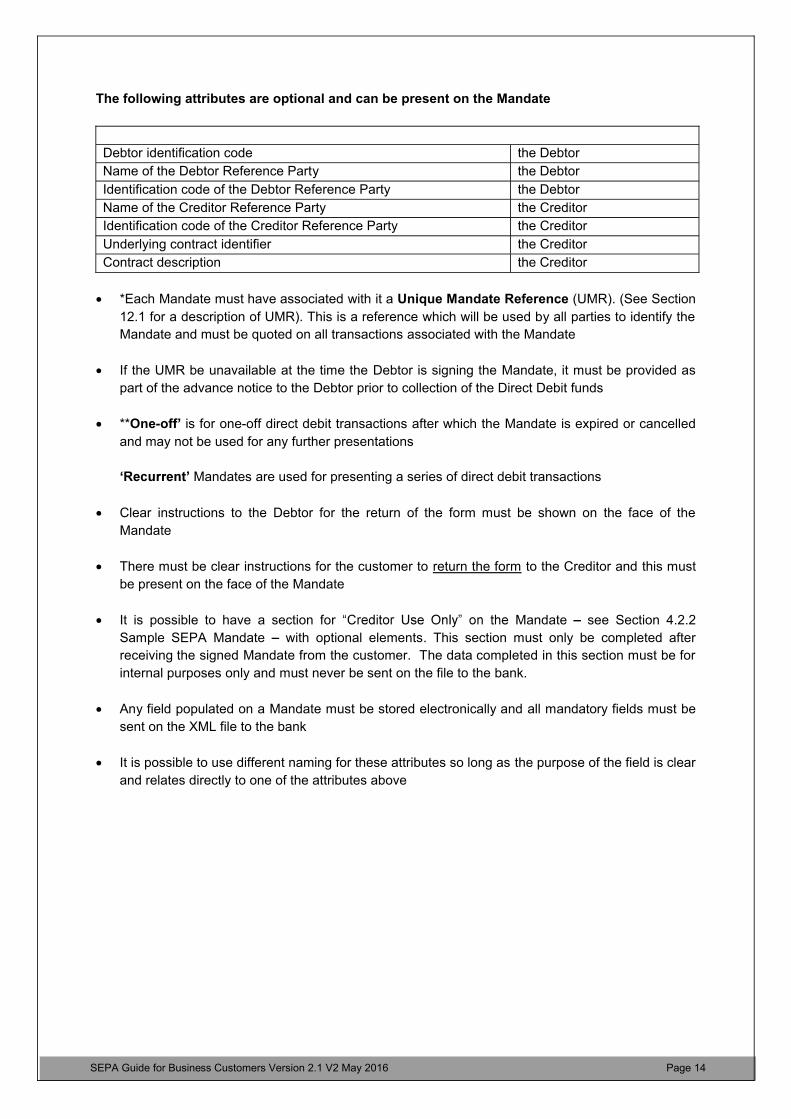

The following attributes are optional and can be present on the Mandate

Debtor identification code the Debtor

Name of the Debtor Reference Party the Debtor

Identification code of the Debtor Reference Party the Debtor

Name of the Creditor Reference Party the Creditor

Identification code of the Creditor Reference Party the Creditor

Underlying contract identifier the Creditor

Contract description the Creditor

*Each Mandate must have associated with it a Unique Mandate Reference (UMR). (See Section

12.1 for a description of UMR). This is a reference which will be used by all parties to identify the

Mandate and must be quoted on all transactions associated with the Mandate

If the UMR be unavailable at the time the Debtor is signing the Mandate, it must be provided as

part of the advance notice to the Debtor prior to collection of the Direct Debit funds

**One- is for one-off direct debit transactions after which the Mandate is expired or cancelled

and may not be used for any further presentations

Mandates are used for presenting a series of direct debit transactions

Clear instructions to the Debtor for the return of the form must be shown on the face of the

Mandate

There must be clear instructions for the customer to return the form to the Creditor and this must

be present on the face of the Mandate

It is possible to have a section for Mandate see Section 4.2.2

Sample SEPA Mandate with optional elements. This section must only be completed after

receiving the signed Mandate from the customer. The data completed in this section must be for

internal purposes only and must never be sent on the file to the bank.

Any field populated on a Mandate must be stored electronically and all mandatory fields must be

sent on the XML file to the bank

It is possible to use different naming for these attributes so long as the purpose of the field is clear

and relates directly to one of the attributes above

SEPA Guide for Business Customers Version 2.1 V2 May 2016 Page 15

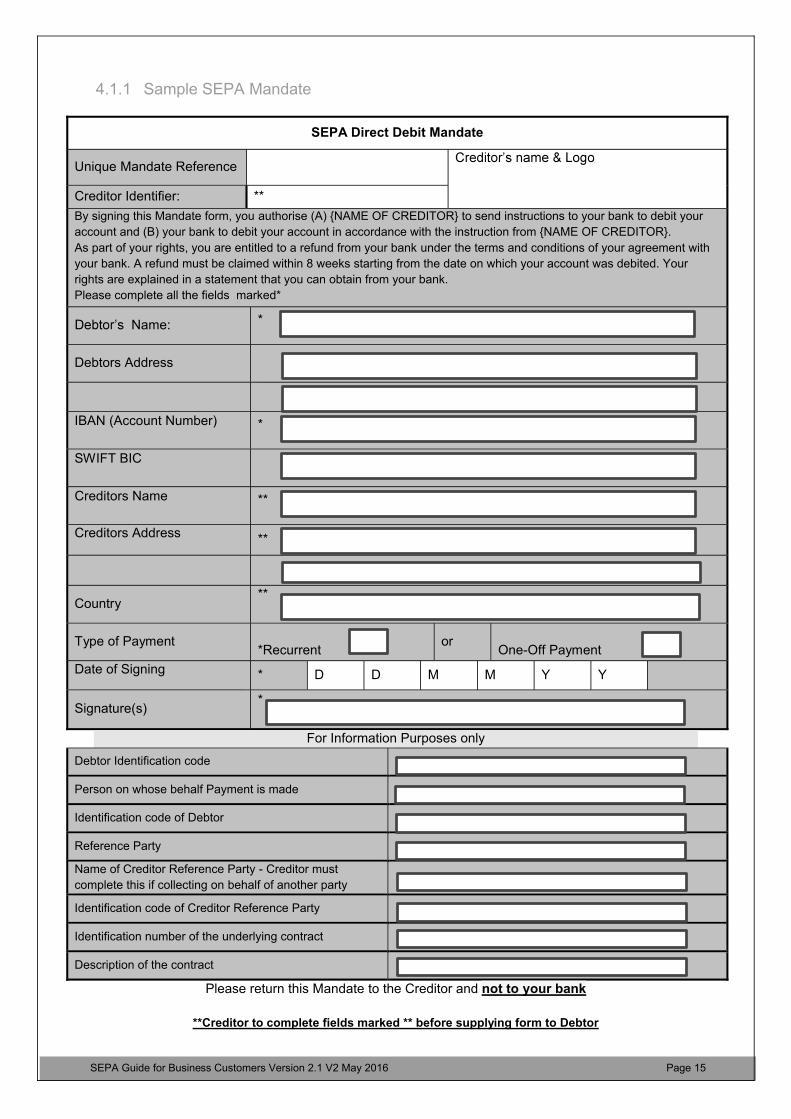

4.1.1 Sample SEPA Mandate

SEPA Direct Debit Mandate

Unique Mandate Reference

Creditor Identifier: **

By signing this Mandate form, you authorise (A) {NAME OF CREDITOR} to send instructions to your bank to debit your

account and (B) your bank to debit your account in accordance with the instruction from {NAME OF CREDITOR}.

As part of your rights, you are entitled to a refund from your bank under the terms and conditions of your agreement with

your bank. A refund must be claimed within 8 weeks starting from the date on which your account was debited. Your

rights are explained in a statement that you can obtain from your bank.

Please complete all the fields marked*

Name: *

Debtors Address

IBAN (Account Number) *

SWIFT BIC

Creditors Name **

Creditors Address **

Country**

Type of Payment *Recurrent

orOne-Off Payment

Date of Signing * D D M M Y Y

Signature(s)*

For Information Purposes only

Debtor Identification code

Person on whose behalf Payment is made

Identification code of Debtor

Reference Party

Name of Creditor Reference Party - Creditor must

complete this if collecting on behalf of another party

Identification code of Creditor Reference Party

Identification number of the underlying contract

Description of the contract

Please return this Mandate to the Creditor and not to your bank

**Creditor to complete fields marked ** before supplying form to Debtor

SEPA Guide for Business Customers Version 2.1 V2 May 2016 Page 16

4.2 Paperless Mandates - Phone & Internet Sign Up

Creditors operating the SEPA Direct Debit Scheme can obtain authorisations from debtors to collect

SEPA Direct Debits via the Phone or Internet subject to the following:

Debtors must have an Irish Bank account Debtors with European Bank accounts must sign a paper

Mandate

Creditors must contact their Bank to apply to operate paperless Mandates

Creditors must provide a paper mandate to debtors with European bank accounts to allow

setup of a direct debit

Creditors must submit their phone/internet templates including the confirmation letter to their

Bank for approval to operate phone & internet sign up

Creditors must keep a copy of the phone recording as proof of Mandate together with any

related amendments/history/confirmation letter must be retained by the Creditor for the life

of the Mandate and after expiry, for a period of 13 months after the date of the last collection

Creditors must keep a record of the Internet application as proof of Mandate together with

any related amendments /history must be retained by the Creditor for the life of the Mandate

and after expiry, for a period of 13 months after the date of the last collection

Creditors must issue a confirmation letter to the Debtor within 3 working days of the

phone/internet sign up. The confirmation letter/email must include the following:

Debtor Name, Address & Bank details (BIC if provided by debtor & IBAN)

Creditor ID

Unique Mandate Reference

Type of Payment: One-off or Recurrent

Date of Signing

Standard Legal Text (the authorisation and the Refund right)

The confirmation letter or email should be substantially in accordance with the sample in the

Guide

Creditors must keep a copy of the confirmation letter which was sent to the Debtor.

Creditors must keep record of the confirmation letter for the life of the Mandate and after

expiry, for a period of 13 months after the date of the last collection

The Creditor must be able to present a copy of the Mandate instruction & confirmation letter

to the Debtor

Creditors are responsible for ensuring their Phone/Internet sign up process and procedures

are complaint with any regulatory/security requirements

SEPA Guide for Business Customers Version 2.1 V2 May 2016 Page 17

4.2.1 Guide to SEPA Direct Debit Phone Sign-Up

Sample Script for SDD Telephone Sign-up

Confirm with customer that he/she agrees to pay by SEPA Direct Debit and that the Mandate

will be set up via the phone

Bank/Building Society/Credit Union Name, Business Identifier

Code (BIC) (optional) and IBAN.

Request confirmation that :

customer is authorised to allow direct debits to be collected from this account

the account is suitable for /can accept a Direct Debit

- then the Direct Debit cannot be set up Close call

Request confirmation that:account is an Irish bank account

- a paper Mandate must be sent to the Debtor for completion. Close call.

Agree the payment schedule i.e. day of the month the money is to come out of account

- process as follows:

series of payments or (b) through a monthly / bi-monthly bill / invoice. You will receive

this notification XX days in advance of the collection date (confirm how notification will

Advice the customer of the following:

Unique Mandate Reference (UMR) If the UMR is not available at the application

stage, it must be advised by the Creditor to the Debtor before the first initiation of a

collection

if there is a change to the date, amount or frequency of the Direct Debit, notification

in advance of the account being debited will be provided (confirm how notification will

be made via post, email or text)

the Direct Debit can be cancelled by writing in good time to (the Company name) and

informing their Bank/Building Society/Credit Union (by whatever means is acceptable

by their bank)

Confirm the Bank/ Building Society/Credit Union account details as follows:

Your account name is ABC, your IBAN is xxxx xxxx xxxx xxxx xx and your

Business Identifier Code is yyyyyyyyyyy ( if provided by the debtor)

Confirm the SEPA Direct Debit Mandate has been completed and advise the customer that

he/she will be sent confirmation of this agreement in the post within 3 working days of the

phone call see section 4.3.3 for sample confirmation letter

SEPA Guide for Business Customers Version 2.1 V2 May 2016 Page 18

4.2.2 Guide to SEPA Direct Debit Internet Sign-Up

The following are mandatory fields which must be presented online and must be completed:

Creditor details should be pre-filled

Creditor Name and Company Logo

Creditor Identifier Number (CI)

Unique Mandate Reference (UMR) If the UMR is not available at the application stage, it

must be advised by the Creditor to the Debtor before the first initiation of a collection

Creditor Postal Address

Debtor Details to be inputted by Debtor

Debtor(s) Name

BIC (optional)

IBAN

Is Bank account a ROI bank account? Yes or No*

Is more than one signatory required to sign on your account? Yes**or No

Can bank account accept Direct Debit? Yes or No*

Is Direct Debit Recurrent or One-Off?

The following optional fields can be used by the Creditor:

Originator Contact phone number / email address

Debtor contact number / email address

Debtor completes and submits the form to the Creditor.

The Creditor must provide confirmation by letter or email to the Debtor within three working days of

sign-up see section 4.3.3 for sample confirmation letter.

The confirmation letter/email must include the following:

Debtor Name, Address & Bank details (BIC (if provided by the debtor & IBAN)

Creditor Identifier Number

Unique Mandate Reference

Type of Payment: One-off or Recurrent

Date of Signing

Standard Legal Text

The confirmation letter or email should be substantially in accordance with the sample in the Guide.

* if No - the Internet application process should cease and a suitable error message presented to the

customer

** if Yes - the Internet application process should cease and a suitable error message presented to

the customer

SEPA Guide for Business Customers Version 2.1 V2 May 2016 Page 19

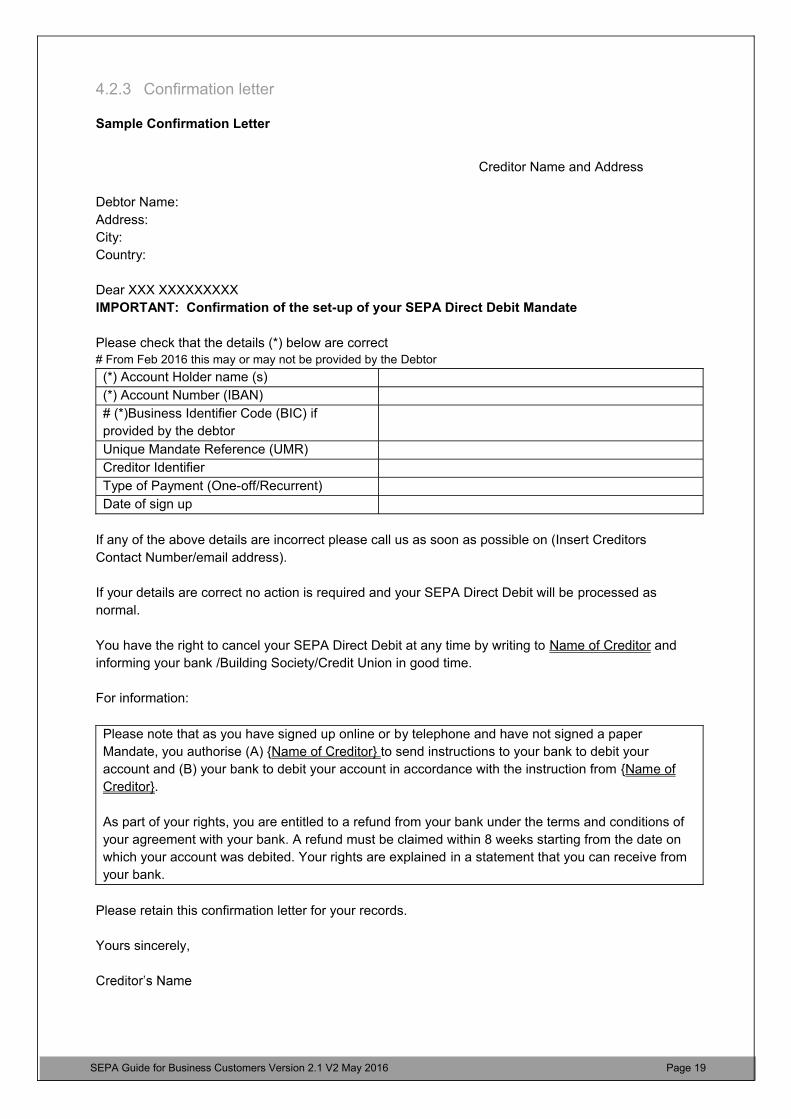

4.2.3 Confirmation letter

Sample Confirmation Letter

Creditor Name and Address

Debtor Name:

Address:

City:

Country:

Dear XXX XXXXXXXXX

IMPORTANT: Confirmation of the set-up of your SEPA Direct Debit Mandate

Please check that the details (*) below are correct# From Feb 2016 this may or may not be provided by the Debtor

(*) Account Holder name (s)

(*) Account Number (IBAN)

# (*)Business Identifier Code (BIC) if

provided by the debtor

Unique Mandate Reference (UMR)

Creditor Identifier

Type of Payment (One-off/Recurrent)

Date of sign up

If any of the above details are incorrect please call us as soon as possible on (Insert Creditors

Contact Number/email address).

If your details are correct no action is required and your SEPA Direct Debit will be processed as

normal.

You have the right to cancel your SEPA Direct Debit at any time by writing to Name of Creditor and

informing your bank /Building Society/Credit Union in good time.

For information:

Please note that as you have signed up online or by telephone and have not signed a paper

Mandate, you authorise (A) {Name of Creditor} to send instructions to your bank to debit your

account and (B) your bank to debit your account in accordance with the instruction from {Name of

Creditor}.

As part of your rights, you are entitled to a refund from your bank under the terms and conditions of

your agreement with your bank. A refund must be claimed within 8 weeks starting from the date on

which your account was debited. Your rights are explained in a statement that you can receive from

your bank.

Please retain this confirmation letter for your records.

Yours sincerely,

SEPA Guide for Business Customers Version 2.1 V2 May 2016 Page 20

4.3 Cancellation of a Mandate

The cancellation of a Direct Debit mandate is the responsibility of the Debtor and the Creditor.

A Debtor can instruct its Bank to cancel a Mandate. Under Payment Regulation banks must

cancel the Mandate if requested to do so by the Debtor, and the Creditor must not represent

on such cancelled Mandates.

Notwithstanding the Debtor

the Debtor the service to cancel a direct debit on their account.

The Debtor can cancel a mandate directly with the Creditor - procedures for the cancellation

of Mandates is the responsibility of the Creditor e.g. written cancellation request is required.

Storing and archiving of cancellation documentation (e.g. letter of cancellation to the Debtor

confirming cancellation) is the responsibility of the Creditor.

Mandates that have been inactive for 36 months must be automatically cancelled by the

Creditor.

Once a Mandate is cancelled it cannot be used again.

4.4 Requests for copy of the Mandate

A copy of a Mandate (paper/scanned) must be made available when requested by your

bank. The copy Mandate or supporting information where the Mandate is paperless must

be sent to the Creditor Bank within 3 working days.

SEPA Guide for Business Customers Version 2.1 V2 May 2016 Page 21

5 Mandate Amendments

Amendments can be made on an existing SEPA Mandate; SEPA caters for this by using the

amendment indicator field within a SEPA Direct Debit XML file.

The amendment of the Mandate is handled between the Creditor and the Debtor.

The Creditor is responsible for communicating the Creditor-related changes to the Debtor and

for retaining a copy of the correspondence with the Mandate.

The Debtor is responsible for communicating Debtor-related changes to their Creditor.

The Creditor must retain a copy of the amendment notification from the Debtor or the resulting

updated Mandate confirmation letter to the Debtor with the original Mandate for the lifetime of

the Mandate plus 13 months.

Mandate amendment requests cannot be taken by the banks.

-1) at the

very latest, prior to the due date of the transaction.

5.1 Amendments to SEPA Mandates can be made for the following

reasons:

1. The Creditor defines a new Unique Mandate Reference (UMR)

2. The Creditor changes the Creditor Identifier information (CI)

3. The Name of the Creditor has changed

4. The Debtor changes the account to be debited in the same bank

5. The Debtor changes the account to be debited in another bank

The new amendment data must be electronically stored by the Creditor and sent as part of the next

collection to the Creditor Bank. The following actions are required in relation to these amendments:

1. New Unique Mandate Reference (UMR)

The Creditor must advise the Debtor of the new UMR in advance of the next payment

The Creditor must amend the file sent to their bank as follows:

the original UMR is present in AT-19

the new UMR is present at AT-01

2. The Creditor has changed the Creditor Identifier information (CI)

The Creditor must notify the Debtor of the change, in advance of the next payment

The Creditor must amend the file sent to the bank as follows:

original Creditor Identifier is present at AT-18

the new Creditor Identifier is present at AT-02

3. The Creditor changes its name

The Creditor must notify the Debtor of the change, in advance of the next payment

The Creditor must amend the file sent to the bank as follows:

SEPA Guide for Business Customers Version 2.1 V2 May 2016 Page 22

ginal AT-

the new Creditor Name must be present in AT-03

4. The Debtor changes the account to be debited in the same bank

The Debtor must advise the Creditor of the change in account details

The Creditor must amend the file sent to the bank as follows:

original Debtor Account is present at Original Debtor IBAN Field

the Debtor Account must be present in AT-07 (Debtor IBAN Field)

Mandate Signed Date field does not change

5. The Debtor changes the account to be debited in another bank

The Debtor must advise the Creditor of the change in account details

The Creditor must amend the file sent to the bank as follows:

the Debtors new IBAN (AT-07) must be present in the file

the Original Debtor

the original Debtor IBAN must not be provided

Mandate Signed Date field does not change

Note: SMNDAIn the previous versions of the C2B (Customer to Bank) Implementation Guidelines, theacronym S was used to indicate Same Mandate with a New Debtor Agent.However, when the Creditor only receives the IBAN it will not always be possible to derive if an account change took place in the same or in another bank. To better accommodate this situation the definition of the acronym S has been updated to indicate SameMandate with a New Debtor Account. It is now used by the Creditor to indicate that the Debtor has provided a payment account held at another Debtor Bank.

Note: Creditors should refer to their software provider for instructions on how to complete Mandate

amendments within software packages.

SEPA Guide for Business Customers Version 2.1 V2 May 2016 Page 23

6 SEPA Transaction/Sequence Types

Important change: As of the effective date of November 2016 of the SEPA Core Direct Debit Rulebook version 9.2, all Collections presented for the first time, on a recurrent basis or as a one-off Collection can be presented up to D-1 Inter-Bank Business Day (D-1).

Note: Creditors should contact their bank for details of the submission times for SDD files

T

longer mandatory as of the effective date of November 2016 of the SEPA Core Direct Debit Rulebook

version 9.2 (i.e. a first Collection can be used in the same way as a subsequent Collection with the

First Collection

FRST

Optional - can be used for the first collection of recurrent direct debitMandate.It must be:

received at the Debtor bank at the latest D-1.

Recurrent Collection

RCUR

Used for recurrent direct debits.It must be :

received by the Debtor bank at the latest, D-1

It will be rejected if details (BIC, IBAN and UMR) have been presented previously using an OOFF, or FNAL transaction type.

One off

OOFF

Used for One-Off Mandate and cannot be reused.

It must be:

sent only once after which the Mandate has expired and is

redundant

received by the Debtor bank at the latest, D-1

It constitutes a collection for an amount that can be collected only once.

It will be rejected if details (BIC, IBAN and UMR) have been presented

previously using an OOFF, FRST, RCUR, or FNAL transaction type.

The Final Collection

FNAL

Used for final direct debit in a series of direct debits.

It must be:

received by the Debtor bank at the latest, D-1

Once processed on the account, it will result in the termination of the

Mandate.

It will be rejected if details (BIC, IBAN and UMR) have been presented

previously using a OOFF, or FNAL transaction type.

There is no requirement to use the FNAL transaction type.

The following attributes apply in practice:

SEPA Guide for Business Customers Version 2.1 V2 May 2016 Page 24

A Mandate is deemed to be created when the FRST/RECUR transaction/collection on that

Mandate has reached settlement.

If the FRST or RECUR collection on the Mandate is rejected by either the Creditor bank, CSM or the Debtor bank then the Creditor must submit a FRST or RECUR transaction again -correcting information if necessary.

If the OOFF Mandate is rejected pre-settlement it would be represented as a OOFF

transaction again. However, if the OOFF transaction is returned/reversed or refunded post

settlement, it would not be valid to submit the OOFF transaction/mandate again.

A FNAL transaction type is used to signal the Mandate has completed or is cancelled. It is not

possible to submit another RCUR after submitting a FNAL on a Mandate. Once a FNAL has

been accepted on a Mandate it is not possible to use the same Mandate ID for another

customer. The Mandate ID that was used and is now completed must remain unique for the

Creditor.

SEPA Guide for Business Customers Version 2.1 V2 May 2016 Page 25

7 SEPA File formats

SEPA payment files must be transmitted in XML format.

The legal standard for processing transactions is in XML format (ISO 20022).

Customers must contact their Bank for details on submitting SEPA payment files.

SEPA Guide for Business Customers Version 2.1 V2 May 2016 Page 26

8 Pre Notification/Advance Notice

The direct debit processes respect the following pre-notification requirements:

Pre-notification is the notification provided by the Creditor to the Debtor of:the amountDue date of the collection Creditor Identifier Number

UMR

The notice can be provided as a separate piece of information, or via inclusion in a regular statement, bill, or invoice

The Pre-notification must be sent by the Creditor at the latest 14 Calendar Days before the Due Date unless another time-line is agreed between the Debtor and the Creditor

The pre-notification can take the form of a schedule of payments over an agreed period of

time or an individual advice for each collection (i.e. utility bill)

In the case of a schedule of payments, a new pre- notification is only necessary if the amount

or frequency changes

Delivery methods for the advanced notice is not specified, possible delivery methods include

letter, text, email

SEPA Guide for Business Customers Version 2.1 V2 May 2016 Page 27

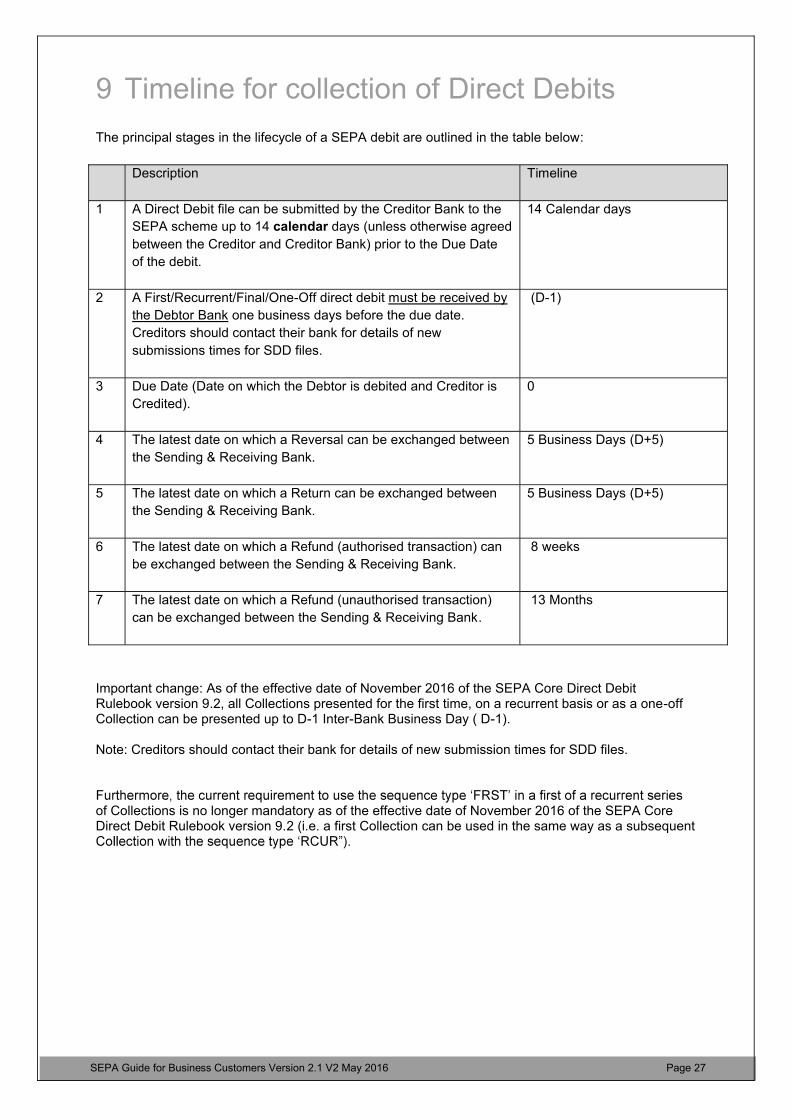

9 Timeline for collection of Direct Debits

The principal stages in the lifecycle of a SEPA debit are outlined in the table below:

Description Timeline

1 A Direct Debit file can be submitted by the Creditor Bank to the

SEPA scheme up to 14 calendar days (unless otherwise agreed

between the Creditor and Creditor Bank) prior to the Due Date

of the debit.

14 Calendar days

2 A First/Recurrent/Final/One-Off direct debit must be received by

the Debtor Bank one business days before the due date.

Creditors should contact their bank for details of new

submissions times for SDD files.

(D-1)

3 Due Date (Date on which the Debtor is debited and Creditor is

Credited).

0

4 The latest date on which a Reversal can be exchanged between

the Sending & Receiving Bank.

5 Business Days (D+5)

5 The latest date on which a Return can be exchanged between

the Sending & Receiving Bank.

5 Business Days (D+5)

6 The latest date on which a Refund (authorised transaction) can

be exchanged between the Sending & Receiving Bank.

8 weeks

7 The latest date on which a Refund (unauthorised transaction)

can be exchanged between the Sending & Receiving Bank.

13 Months

Important change: As of the effective date of November 2016 of the SEPA Core Direct Debit Rulebook version 9.2, all Collections presented for the first time, on a recurrent basis or as a one-off Collection can be presented up to D-1 Inter-Bank Business Day ( D-1).

Note: Creditors should contact their bank for details of new submission times for SDD files.

of Collections is no longer mandatory as of the effective date of November 2016 of the SEPA Core Direct Debit Rulebook version 9.2 (i.e. a first Collection can be used in the same way as a subsequent

SEPA Guide for Business Customers Version 2.1 V2 May 2016 Page 28

10

Under the SEPA Direct Debit scheme transactions that cannot be processed in the normal way or are

being -transactions -transactions,

rejects, refusals and refunds, and they can occur, pre- settlement (prior to or on D) or post settlement

(after D).

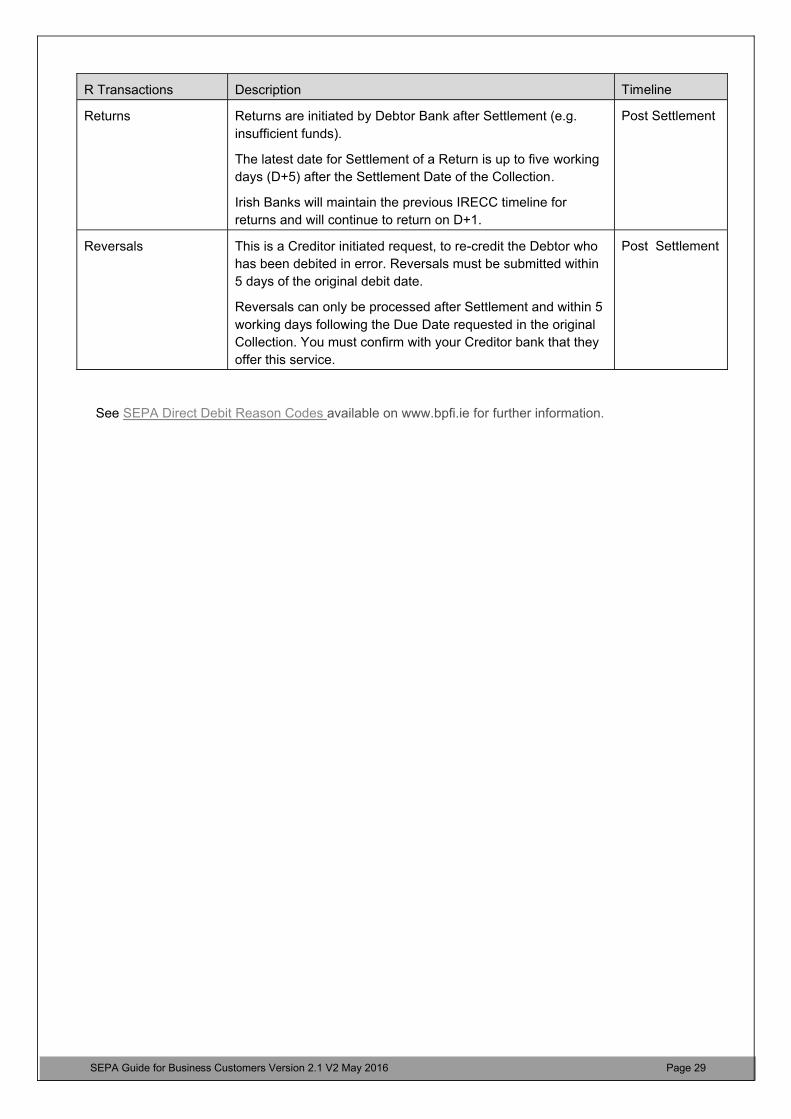

R Transactions Description Timeline

Refunds

(Authorised

transactions within

eight weeks)

Claims by the Debtor for reimbursement of a direct debit.

Debtor

for any SEPA Direct Debit within eight weeks from the date on

which the amount was debited.

Post Settlement

Refunds

(Unauthorised

Transactions)

If the request for a refund concerns an unauthorised

transaction a Debtor must make the claim at the latest 13

months after the disputed debit date. A direct debit is deemed

to be unauthorised for any of the following:

No Mandate existsThe Mandate was invalidThe Mandate has expired (no transactions for 36 months) or is cancelled

There will be an investigation phase before the Debtor can be

refunded.

Post Settlement

Refusals Claims initiated by the Debtor, requesting the Debtor Bank not

to pay a collection, for any reason. Can be requested, up to the

close of business the day before the payment is due.

Pre Settlement

Rejects Direct Debits which are rejected, prior to Settlement for the

following reasons:

Technical reasons: invalid format, wrong IBAN check digit, missing mandatory fields.Debtor Bank is unable to process the Collection e.g.account does not accept direct debits, no Mandate, Mandate cancelled.The Debtor Bank is unable to process the Collection where it is bound by legal obligations covered by National or Community legislation.The Debtor Bank is unable to process the Collection for such reasons as are set out in section 4.2 of the Rulebook (e.g. account closed, customer deceased, account does not accept direct debits).The Debtor made a Refusal request to the Debtor Bank. The Debtor Bank will generate a Reject of the Collection being refused.

Pre Settlement

SEPA Guide for Business Customers Version 2.1 V2 May 2016 Page 29

R Transactions Description Timeline

Returns Returns are initiated by Debtor Bank after Settlement (e.g.

insufficient funds).

The latest date for Settlement of a Return is up to five working

days (D+5) after the Settlement Date of the Collection.

Irish Banks will maintain the previous IRECC timeline for

returns and will continue to return on D+1.

Post Settlement

Reversals This is a Creditor initiated request, to re-credit the Debtor who

has been debited in error. Reversals must be submitted within

5 days of the original debit date.

Reversals can only be processed after Settlement and within 5

working days following the Due Date requested in the original

Collection. You must confirm with your Creditor bank that they

offer this service.

Post Settlement

See SEPA Direct Debit Reason Codes available on www.bpfi.ie for further information.

SEPA Guide for Business Customers Version 2.1 V2 May 2016 Page 30

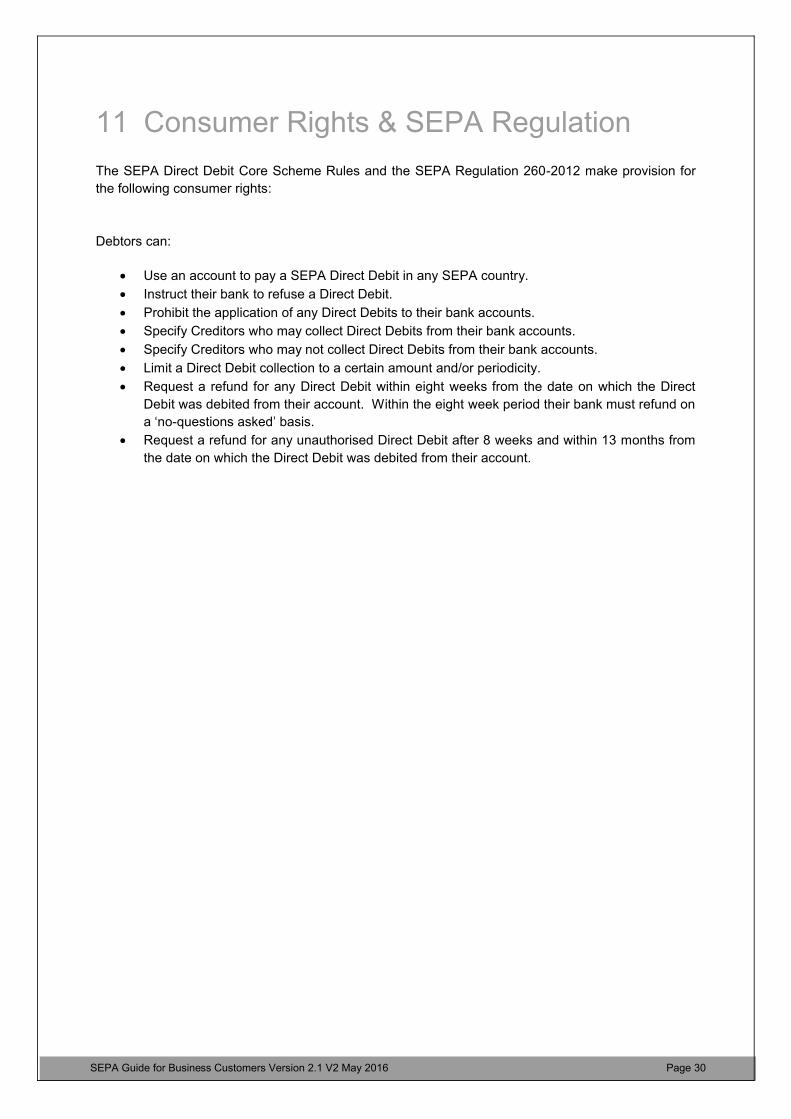

11 Consumer Rights & SEPA Regulation

The SEPA Direct Debit Core Scheme Rules and the SEPA Regulation 260-2012 make provision for

the following consumer rights:

Debtors can:

Use an account to pay a SEPA Direct Debit in any SEPA country.

Instruct their bank to refuse a Direct Debit.

Prohibit the application of any Direct Debits to their bank accounts.

Specify Creditors who may collect Direct Debits from their bank accounts.

Specify Creditors who may not collect Direct Debits from their bank accounts.

Limit a Direct Debit collection to a certain amount and/or periodicity.

Request a refund for any Direct Debit within eight weeks from the date on which the Direct

Debit was debited from their account. Within the eight week period their bank must refund on

a no-questions asked basis.

Request a refund for any unauthorised Direct Debit after 8 weeks and within 13 months from

the date on which the Direct Debit was debited from their account.

SEPA Guide for Business Customers Version 2.1 V2 May 2016 Page 31

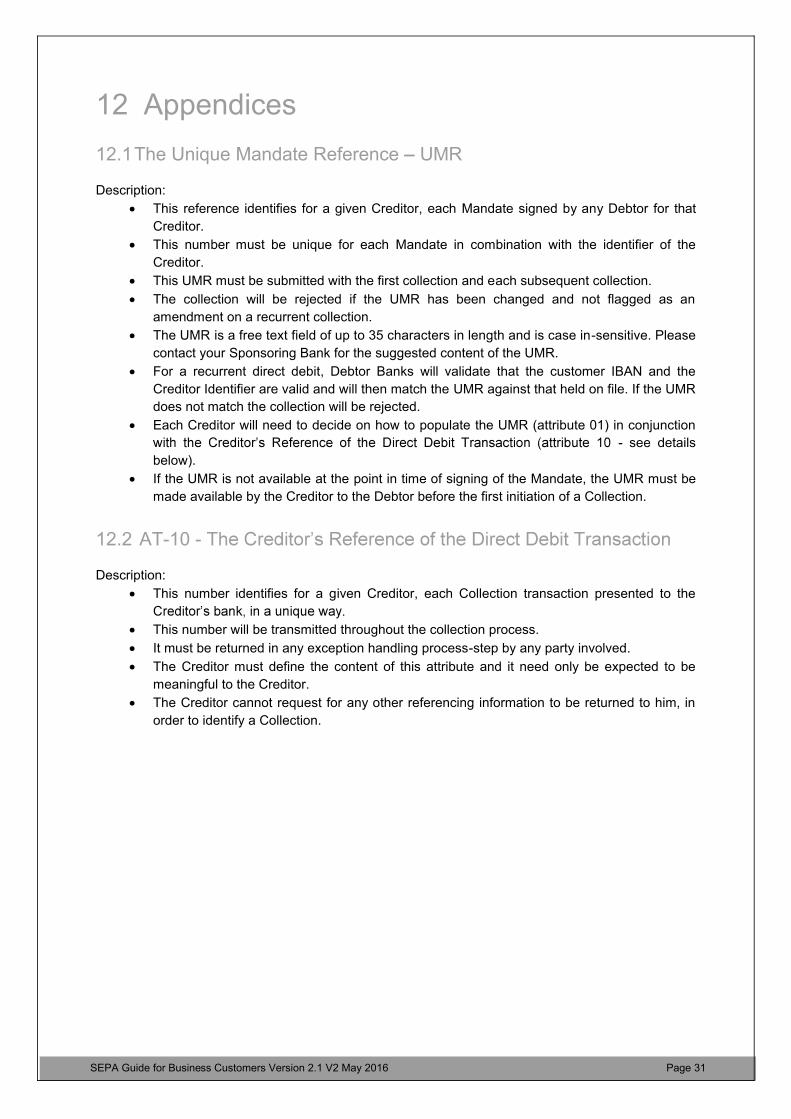

12 Appendices

12.1The Unique Mandate Reference UMR

Description:

This reference identifies for a given Creditor, each Mandate signed by any Debtor for that

Creditor.

This number must be unique for each Mandate in combination with the identifier of the

Creditor.

This UMR must be submitted with the first collection and each subsequent collection.

The collection will be rejected if the UMR has been changed and not flagged as an

amendment on a recurrent collection.

The UMR is a free text field of up to 35 characters in length and is case in-sensitive. Please

contact your Sponsoring Bank for the suggested content of the UMR.

For a recurrent direct debit, Debtor Banks will validate that the customer IBAN and the

Creditor Identifier are valid and will then match the UMR against that held on file. If the UMR

does not match the collection will be rejected.

Each Creditor will need to decide on how to populate the UMR (attribute 01) in conjunction

- see details

below).

If the UMR is not available at the point in time of signing of the Mandate, the UMR must be

made available by the Creditor to the Debtor before the first initiation of a Collection.

12.2 AT-10 -

Description:

This number identifies for a given Creditor, each Collection transaction presented to the

This number will be transmitted throughout the collection process.

It must be returned in any exception handling process-step by any party involved.

The Creditor must define the content of this attribute and it need only be expected to be

meaningful to the Creditor.

The Creditor cannot request for any other referencing information to be returned to him, in

order to identify a Collection.

SEPA Guide for Business Customers Version 2.1 V2 May 2016 Page 32

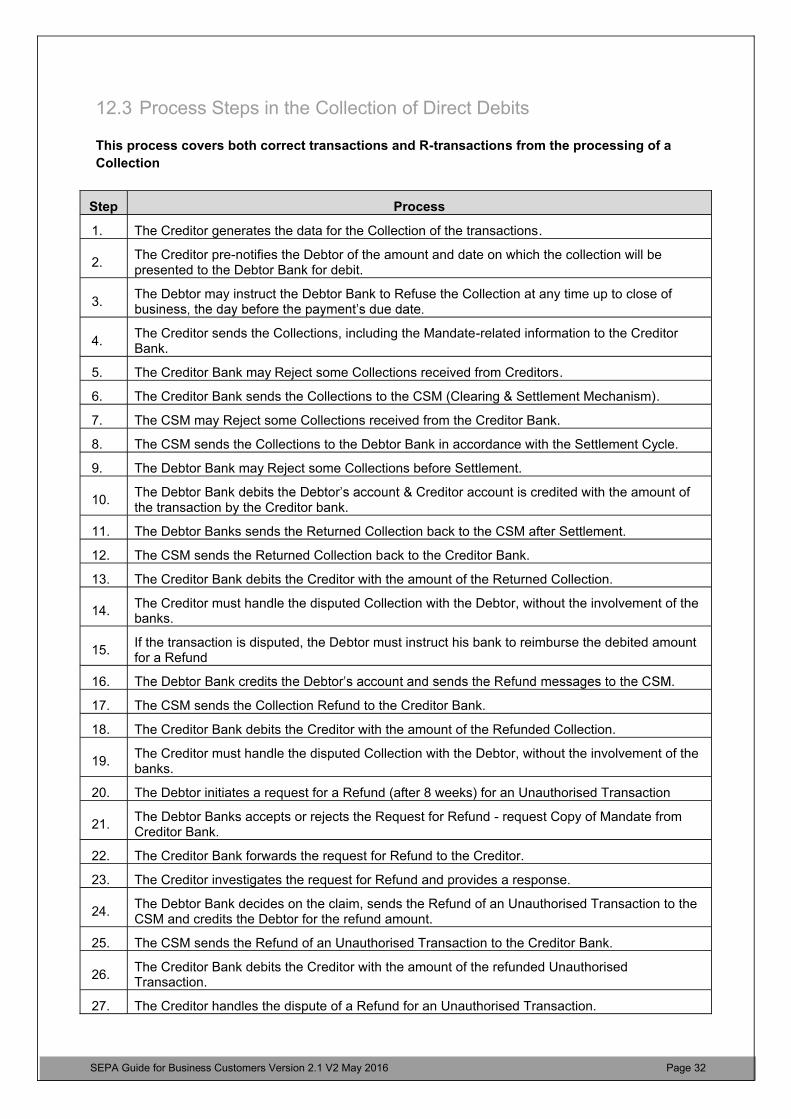

12.3 Process Steps in the Collection of Direct Debits

This process covers both correct transactions and R-transactions from the processing of a

Collection

Step Process

1. The Creditor generates the data for the Collection of the transactions.

2.The Creditor pre-notifies the Debtor of the amount and date on which the collection will be presented to the Debtor Bank for debit.

3.The Debtor may instruct the Debtor Bank to Refuse the Collection at any time up to close of

4.The Creditor sends the Collections, including the Mandate-related information to the Creditor Bank.

5. The Creditor Bank may Reject some Collections received from Creditors.

6. The Creditor Bank sends the Collections to the CSM (Clearing & Settlement Mechanism).

7. The CSM may Reject some Collections received from the Creditor Bank.

8. The CSM sends the Collections to the Debtor Bank in accordance with the Settlement Cycle.

9. The Debtor Bank may Reject some Collections before Settlement.

10.& Creditor account is credited with the amount of

the transaction by the Creditor bank.

11. The Debtor Banks sends the Returned Collection back to the CSM after Settlement.

12. The CSM sends the Returned Collection back to the Creditor Bank.

13. The Creditor Bank debits the Creditor with the amount of the Returned Collection.

14.The Creditor must handle the disputed Collection with the Debtor, without the involvement of the banks.

15.If the transaction is disputed, the Debtor must instruct his bank to reimburse the debited amount for a Refund

16.

17. The CSM sends the Collection Refund to the Creditor Bank.

18. The Creditor Bank debits the Creditor with the amount of the Refunded Collection.

19.The Creditor must handle the disputed Collection with the Debtor, without the involvement of the banks.

20. The Debtor initiates a request for a Refund (after 8 weeks) for an Unauthorised Transaction

21.The Debtor Banks accepts or rejects the Request for Refund - request Copy of Mandate from Creditor Bank.

22. The Creditor Bank forwards the request for Refund to the Creditor.

23. The Creditor investigates the request for Refund and provides a response.

24.The Debtor Bank decides on the claim, sends the Refund of an Unauthorised Transaction to the CSM and credits the Debtor for the refund amount.

25. The CSM sends the Refund of an Unauthorised Transaction to the Creditor Bank.

26.The Creditor Bank debits the Creditor with the amount of the refunded Unauthorised Transaction.

27. The Creditor handles the dispute of a Refund for an Unauthorised Transaction.

SEPA Guide for Business Customers Version 2.1 V2 May 2016 Page 33

12.4Glossary of Terms

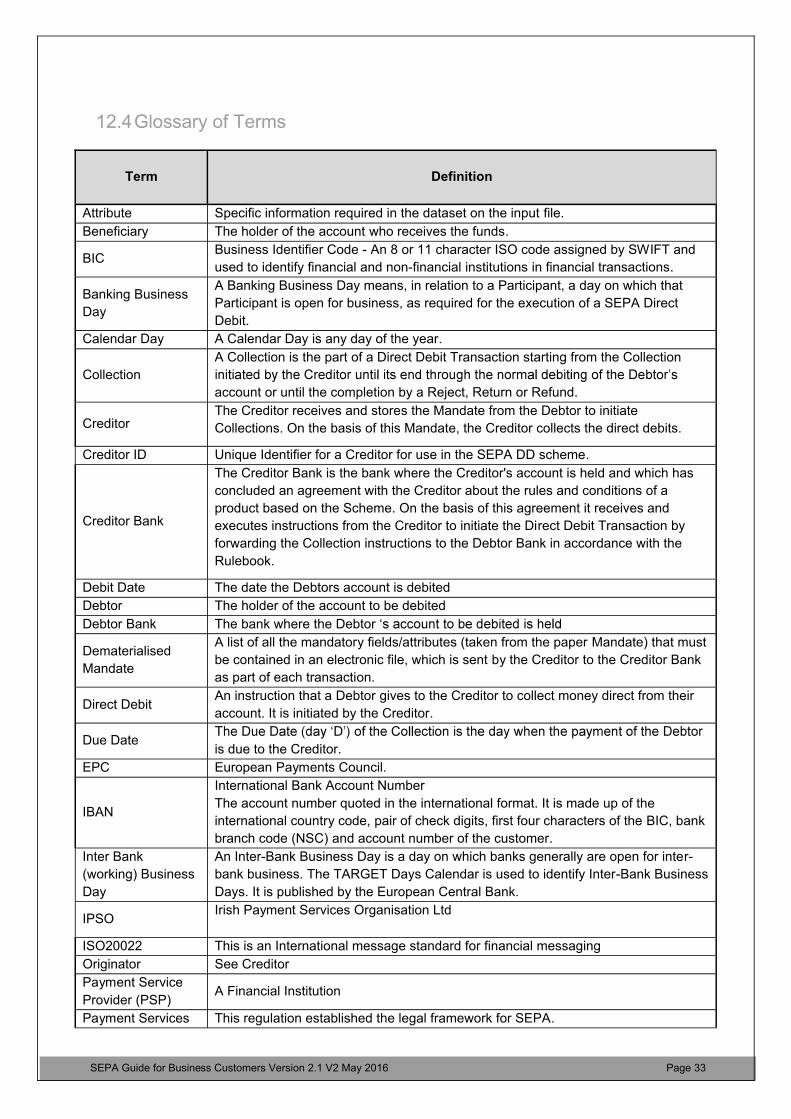

Term Definition

Attribute Specific information required in the dataset on the input file.

Beneficiary The holder of the account who receives the funds.

BICBusiness Identifier Code - An 8 or 11 character ISO code assigned by SWIFT and

used to identify financial and non-financial institutions in financial transactions.

Banking Business

Day

A Banking Business Day means, in relation to a Participant, a day on which that

Participant is open for business, as required for the execution of a SEPA Direct

Debit.

Calendar Day A Calendar Day is any day of the year.

Collection

A Collection is the part of a Direct Debit Transaction starting from the Collection

account or until the completion by a Reject, Return or Refund.

CreditorThe Creditor receives and stores the Mandate from the Debtor to initiate

Collections. On the basis of this Mandate, the Creditor collects the direct debits.

Creditor ID Unique Identifier for a Creditor for use in the SEPA DD scheme.

Creditor Bank

The Creditor Bank is the bank where the Creditor's account is held and which has

concluded an agreement with the Creditor about the rules and conditions of a

product based on the Scheme. On the basis of this agreement it receives and

executes instructions from the Creditor to initiate the Direct Debit Transaction by

forwarding the Collection instructions to the Debtor Bank in accordance with the

Rulebook.

Debit Date The date the Debtors account is debited

Debtor The holder of the account to be debited

Debtor Bank The bank where the Debtor

Dematerialised

Mandate

A list of all the mandatory fields/attributes (taken from the paper Mandate) that must

be contained in an electronic file, which is sent by the Creditor to the Creditor Bank

as part of each transaction.

Direct DebitAn instruction that a Debtor gives to the Creditor to collect money direct from their

account. It is initiated by the Creditor.

Due Dateis due to the Creditor.

EPC European Payments Council.

IBAN

International Bank Account Number

The account number quoted in the international format. It is made up of the

international country code, pair of check digits, first four characters of the BIC, bank

branch code (NSC) and account number of the customer.

Inter Bank

(working) Business

Day

An Inter-Bank Business Day is a day on which banks generally are open for inter-

bank business. The TARGET Days Calendar is used to identify Inter-Bank Business

Days. It is published by the European Central Bank.

IPSOIrish Payment Services Organisation Ltd

ISO20022 This is an International message standard for financial messaging

Originator See Creditor

Payment Service

Provider (PSP)A Financial Institution

Payment Services This regulation established the legal framework for SEPA.

SEPA Guide for Business Customers Version 2.1 V2 May 2016 Page 34

Term Definition

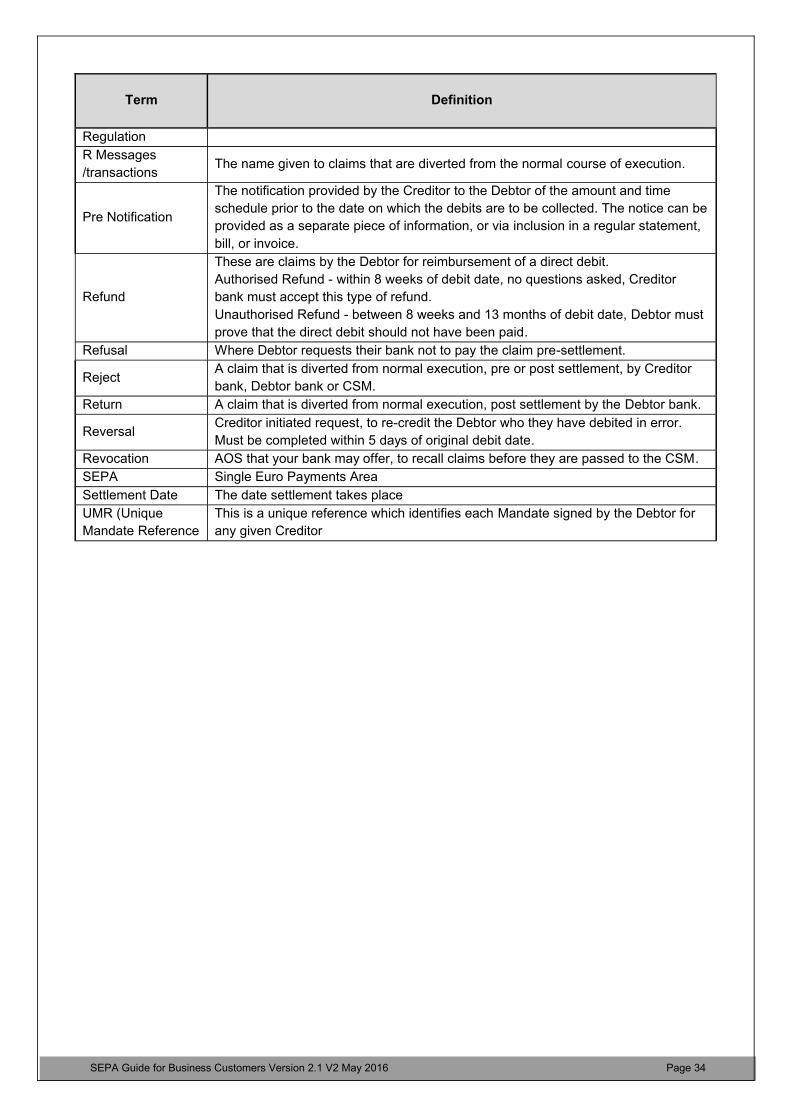

Regulation

R Messages

/transactionsThe name given to claims that are diverted from the normal course of execution.

Pre Notification

The notification provided by the Creditor to the Debtor of the amount and time

schedule prior to the date on which the debits are to be collected. The notice can be

provided as a separate piece of information, or via inclusion in a regular statement,

bill, or invoice.

Refund

These are claims by the Debtor for reimbursement of a direct debit.

Authorised Refund - within 8 weeks of debit date, no questions asked, Creditor

bank must accept this type of refund.

Unauthorised Refund - between 8 weeks and 13 months of debit date, Debtor must

prove that the direct debit should not have been paid.

Refusal Where Debtor requests their bank not to pay the claim pre-settlement.

RejectA claim that is diverted from normal execution, pre or post settlement, by Creditor

bank, Debtor bank or CSM.

Return A claim that is diverted from normal execution, post settlement by the Debtor bank.

ReversalCreditor initiated request, to re-credit the Debtor who they have debited in error.

Must be completed within 5 days of original debit date.

Revocation AOS that your bank may offer, to recall claims before they are passed to the CSM.

SEPA Single Euro Payments Area

Settlement Date The date settlement takes place

UMR (Unique

Mandate Reference

This is a unique reference which identifies each Mandate signed by the Debtor for

any given Creditor

Banking & PaymentsFederation IrelandNassau House

Nassau Street

Dublin 2

Ireland

+353 (1) 6715311

www.bpfi.ie

![SEPA CREDIT TRANSFER SCHEME INTERBANK … · 2018-06-27 · SEPA Credit Transfer Scheme Rulebook 2017 Version 1.1 : EPC [2] - ISO 20022 XML Credit Transfers and Related Messages,](https://static.documents.pub/doc/80x56/5f1c8268f33b3e0e8c06601a/sepa-credit-transfer-scheme-interbank-2018-06-27-sepa-credit-transfer-scheme-rulebook.jpg)

![SEPA CREDIT TRANSFER SCHEME RULEBOOK · SEPA Credit Transfer Scheme Interbank Implementation Guidelines : EPC [3] ISO 13616 . Financial services - International bank account number](https://static.documents.pub/doc/80x56/5ad375be7f8b9abd6c8df8cc/sepa-credit-transfer-scheme-rulebook-credit-transfer-scheme-interbank-implementation.jpg)