Welcome to the September 2011 edition of the ViewPoint Newsletter from Steve Stanganelli, CFP(R) of Clear View Wealth Advisors, a fee-only RIA located in Massachusetts. In this issue, retirement income planning, college funding strategies and tax tips for business owners and those going through divorce are shared.

6

Clear View Wealth Advisors, LLC is an independent Registered In- vestment Advisor providing finan- cial planning, tax preparation, and investment advisory services to individuals and couples throughout Massachusetts. Clear View works on a FEE ON- LY/FEE-for-SERVICE basis. www.ClearViewWealthAdvisors.com Free Rollover Helpline 978-388-0020 Call for Your Free Guide “Six Best & Worst IRA Rollover Decisions” V IEWPOINT September 2011 Four Retirement Financing Risks About Clear View Steve Stanganelli, CFP®, CRPC® By Steve Stanganelli, CFP® As Americans live longer, the task of managing money after retirement gets more complex. A retiree in his or her mid-60s typically has a different risk profile than an individual approaching 90. It may be helpful to look at various types of risk from the vantage point of how they affect retirees at different life stages. Here are four key risks to consider. 1.Investment Risk -- Balancing risk and return takes on a different meaning for indi- viduals as they age. A negative rate of return during the early years of retirement could leave an individual with a significantly smaller nest egg when compared with negative returns later in the retirement life cycle. We can help you craft an investment mix with the goal of smoothing out returns over the long term and increasing the chances that your assets will last throughout your lifetime. 2. Longevity Risk -- Withdrawing too much from a portfolio during the early years of retirement may heighten the chance of depleting your assets during your later years. For this reason, many financial advisors recommend limiting annual withdrawals to 5% or less of a portfolio's value, adjusted for inflation, to make assets last as long as possible. A better tactic is to prepare a personalized withdrawal plan based on the “endowment” spending policy highlighted in a prior issue of the ViewPoint. 3. Inflation Risk -- Because younger retirees typically are planning for a time horizon of 20 years or more, it’s important that their portfolios include a source of growth that is likely to exceed inflation over the long term. To complement this potential growth, many retirees rely on more conservative investments that may generate income and help to balance risk and potential return. One way to counter this risk is by including dividend-paying stocks and alternative investments like REITs, commodities and convertible bonds to your investment mix. 4. Health Care Risk -- It is not unusual for medical costs to increase as retirees age, and it may be prudent to plan for these costs before the need is immediate. Pre- retirees and younger retirees may want to explore options for medical insurance that supplements Medicare, as well as long-term care insurance, to reduce the possibility of dipping into personal assets to finance illness- or accident-related expenses. Also, remember that those who retire before age 65 need to find an alternate source of medical insurance prior to becoming eligible for Medicare. Reviewing these and other challenges associated with retirement planning with a Clear View financial advisor may increase your confidence that you have considered all scenarios. While it may not be possible to prepare for every situation, plan- ning ahead may help you cope with financial issues that come your way. “Using Convertibles to Protect & Grow Wealth” Amesbury * Wilmington * Woburn FREE White Paper Clear View Wealth Advisors, LLC

Clear View works on a FEE ON-LY/FEE-for-SERVICE basis.

www.ClearViewWealthAdvisors.com

Free Rollover Helpline978-388-0020

Call for Your Free Guide“Six Best & Worst IRA Rollover

Decisions”

V IEWPOINT

September 2011

Four Retirement Financing Risks

About Clear View

Steve Stanganelli, CFP®, CRPC®

By Steve Stanganelli, CFP®

As Americans live longer, the task of managing money after retirement gets morecomplex. A retiree in his or her mid-60s typically has a different risk profile than anindividual approaching 90. It may be helpful to look at various types of risk from thevantage point of how they affect retirees at different life stages. Here are four keyrisks to consider.

1.Investment Risk -- Balancing risk and return takes on a different meaning for indi-viduals as they age. A negative rate of return during the early years of retirementcould leave an individual with a significantly smaller nest egg when compared withnegative returns later in the retirement life cycle. We can help you craft an investmentmix with the goal of smoothing out returns over the long term and increasing thechances that your assets will last throughout your lifetime.

2. Longevity Risk -- Withdrawing too much from a portfolio during the early years ofretirement may heighten the chance of depleting your assets during your later years.For this reason, many financial advisors recommend limiting annual withdrawals to5% or less of a portfolio's value, adjusted for inflation, to make assets last as long aspossible. A better tactic is to prepare a personalized withdrawal plan based on the“endowment” spending policy highlighted in a prior issue of the ViewPoint.

3. Inflation Risk -- Because younger retirees typically are planning for a time horizonof 20 years or more, it’s important that their portfolios include a source of growth thatis likely to exceed inflation over the long term. To complement this potential growth,many retirees rely on more conservative investments that may generate income andhelp to balance risk and potential return. One way to counter this risk is by includingdividend-paying stocks and alternative investments like REITs, commodities andconvertible bonds to your investment mix.

4. Health Care Risk -- It is not unusual for medical costs to increase as retirees age,and it may be prudent to plan for these costs before the need is immediate. Pre-retirees and younger retirees may want to explore options for medical insurance thatsupplements Medicare, as well as long-term care insurance, to reduce the possibilityof dipping into personal assets to finance illness- or accident-related expenses. Also,remember that those who retire before age 65 need to find an alternate source ofmedical insurance prior to becoming eligible for Medicare.

Reviewing these and other challenges associated with retirement planning with aClear View financial advisor mayincrease your confidence that youhave considered all scenarios.

While it may not be possible toprepare for every situation, plan-ning ahead may help you copewith financial issues that comeyour way.

“Using Convertibles to Protect & Grow Wealth”

Amesbury * Wilmington * Woburn

FREE White Paper

Clear View Wealth Advisors, LLC

Viewpoint is produced by Clear View Wealth Advisors, LLC for the benefit of its clients and allied professionals. Although the information here is gathered from reliable sources, readers should notact upon it without professional advice. Past performance is no guarantee of future results. Examples with hypothetical returns illustrated are not representative of a specific investment. Clear ViewWealth Advisors, LLC 12 Amidon Ave., Amesbury, MA 01913 & 25 Lowell St., Wilmington, MA 01887 Tel: 978 388-0020 Email: [email protected]

September 2011Page 2

Federal law requires that participants in em-ployer-sponsored retirement plans designatetheir spouse as their beneficiary unless thespouse waives this right in writing. Assumingthat you and your spouse adhered to this prac-tice, a document known as a Qualified Domes-tic Relations Order (QDRO), which is part of adivorce settlement, specifies how retirementassets are divided.

A QDRO specifies the amount or portion of aplan participant's benefits that are paid to aspouse, former spouse, child, or other party.

A QDRO typically governs assets within a re-tirement plan such as a pension, profit-sharingplan, or a tax-sheltered annuity. Benefits paidto a former spouse typically are considered in-come for tax purposes. If you contributed toyour retirement plan, a prorated share of yourinvestment is used to determine the taxableamount.

Former spouses on the receiving end of a lump-sum distribution mandated by a QDRO may beable to roll over the money tax free to a tradi-tional individual retirement account or to an-other qualified retirement plan. Following sucha transfer, assets within the plan are subject torules that would normally apply to the retire-ment plan. If you transfer assets within a tradi-tional IRA to your spouse as part of a divorcedecree, the transfer is not considered taxableand the assets are treated as your formerspouse's IRA.

Procedural Issues

QDROs are governed by rules established bythe U.S. Department of Labor. In most instanc-es, a judge must formally issue a judgment orapprove a settlement agreement before it isconsidered a QDRO. The fact that you and yoursoon-to-be-former spouse have signed anagreement is not adequate for a QDRO to takeeffect.

Also, following an order issued by a judge, theadministrator of the retirement plan affectedby the QDRO must determine whether the

ASK THE ADVISERWhat Happens to My Retirement Assets If I GetDivorced ? by Steve Stanganelli, CFP®

court order qualifies as a QDRO according tothe rules of the labor department.

Note that retirement assets are part of abroader financial picture that may include yourhome, taxable investments, personal property,and other assets. It is not mandated that yourspouse receive a portion of your retirement as-sets in the event of a divorce. You and yourspouse may negotiate another type of arrange-ment that permits you to retain your retire-ment assets while granting other assets to yourspouse.

In addition, a prenuptial agreement, dependingon its provisions, could potentially limit yourspouse's rights to your assets.

You may want to consult a divorce lawyer andyour financial advisor to determine whetherfederal laws relating to retirement accounts ap-ply to your situation.

Source: Financial Planning Association,

Looking to Refinance? Looking for a Mortgage?

Clear View Wealth Advisors can help you or someoneyou know who is looking at buying or refinancing a home orreal estate investment.

Don’t just borrow money. Get a plan to borrow smart andrepay smart.

With the help of a qualified financial planner, you can havea Personal Action Plan that compares your borrowing op-tions and provides a repayment plan that pays off the loanquicker and still fund your other goals for college, retire-ment or whatever is important to you.

We use specialized software tools to help look at your cashflow and your big picture—not just your loan.

We can work with you, your Realtor® and mortgage lenderto analyze different options to find the one that makes themost sense for your situation.

Before you spend thousands on interest, talk with the ClearView team. For less than the cost of a property appraisal,you can have a plan … and peace of mind.

Mortgage Helpline …978-388-0020 or 617-398-7494

Clear View Wealth Advisors, LLC 978-388-0020 or 617-398-7494

Viewpoint is produced by Clear View Wealth Advisors, LLC for the benefit of its clients and allied professionals. Although the information here is gathered from reliable sources, readers should notact upon it without professional advice. Past performance is no guarantee of future results. Examples with hypothetical returns illustrated are not representative of a specific investment. Clear ViewWealth Advisors, LLC 12 Amidon Ave., Amesbury, MA 01913 & 25 Lowell St., Wilmington, MA 01887 Tel: 978 388-0020 Email: [email protected]

September 2011Page 3

Zachary Douglas Stanganelli (8/30/2011) - MagicZack

At the crack of dawn on Tuesday, August 30, after atotal of about 14 hours of labor, Zachary Douglas waswelcomed by his new mom and dad at Exeter Hospi-tal.

Weighing in at 8 lbs. 2 oz. and 20 inches, our newestteam member, affectionately known as MagicZack,arrived as the sun rose on abeautiful late-summer morning.

Zack arrived two days early butif you ask Kristin it was not soonenough.

Zack’s older brother Spencerhappily met his new brother for the first time onWednesday morning and really appreciated the newtoy train set that his new brother gave him as a pre-sent.

Zack’s new grandparents areoverjoyed. And while my dadwas not alive to see him, I seehim in Zack’s features and cer-tain behaviors peculiar to Fred.

All members of Team Stang arehome, doing well (though a little

sleep-deprived) and adjusting to a new schedule.

WELCOME OUR NEW TEAM MEMBERStork Arrives with Spencer’s Brother, MagicZack

by Steve Stanganelli, CFP®

To view other pictures, please visit:

http://www.carepages.com/carepages/MagicZach

Clear View Wealth Advisors, LLC 978-388-0020 or 617-398-7494

Special Offers & CouponsCall or go to Google Placestm, search for Clear ViewWealth Advisors in Wilmington or Amesbury

20% Off Advisor On Call

Peace of Mind Help When You Need It. Phone andEmail support throughout the year to help you withANY financial planning questions. Flat rate.

Planning your future should be more than just guess-work.

Clear View now offers an integrated diagnostic tool thatyou can use that provides you with your own personalbenchmark.

The Personal Financial Index™ is much like yourcredit score: You have a simple to understand numberand visual tool that tells you how well you are doing inkey areas that you can track:

Savings Positioning Yourself Toward Your Goals Retirement Major Purchases or College Funding Protection

Try out this complimentary service by visiting the ClearView website or by using the URL below:

Viewpoint is produced by Clear View Wealth Advisors, LLC for the benefit of its clients and allied professionals. Although the information here is gathered from reliable sources, readers should notact upon it without professional advice. Past performance is no guarantee of future results. Examples with hypothetical returns illustrated are not representative of a specific investment. Clear ViewWealth Advisors, LLC 12 Amidon Ave., Amesbury, MA 01913 & 25 Lowell St., Wilmington, MA 01887 Tel: 978 388-0020 Email: [email protected]

September 2011Page 4

Late-Stage College Planning—Strategies to Lower Your Costs by Steve Stanganelli, CFP®

Clear View Wealth Advisors, LLC 978-388-0020 or 617-398-7494

Special points of interest:

Complete a financial aid form for every year your student

attends college.

Don’t overestimate asset values on financial aid forms.

Consider summer school and AP tests to finish earlier

Call the Clear View Financial Planning Helpline for help with

personalized education funding strategies at 978-388-0020

or 617-398-7494.

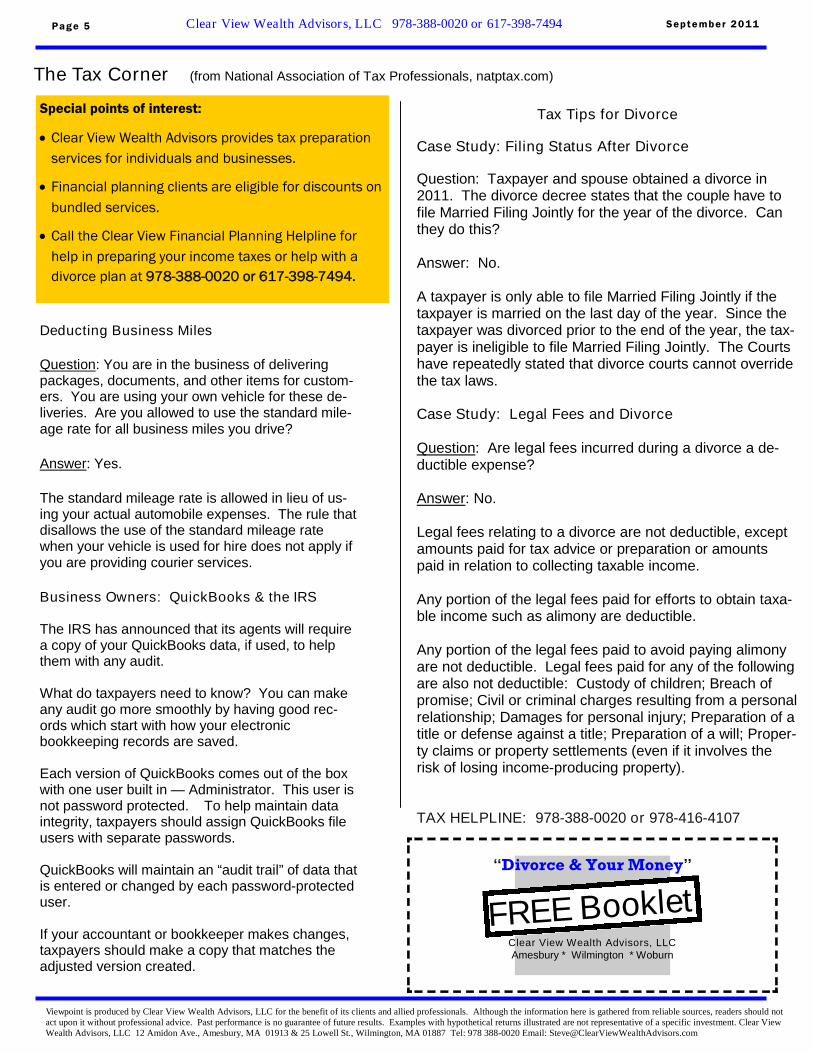

As noted in the charts below, a college degree is stilleconomically worth it in the long run. But college costscontinue to soar.

As tuitions and fees continue to climb at double or tri-ple the average inflation rate, the amount that parentsare able to cover directly has been dropping fromabout 25% in 2007 to about 16% for this academicyear. This has contributed to the increasing amount ofdebt that has saddled new grads from under $10,000in 1993 to nearly $30,000 projected in 2012.

To help lower the cost, consider these tactics:

Don’t count out financial aid. There are a numberof factors that influence whether a student is eligi-ble for aid. Household income is only one factor.So don’t short-change yourself. Plan on filing for

financial aid in January of your student’s senior year ofhigh school

Don’t rule out schools based on “sticker price”: In manyschools fewer than 20% of students actually pay fullprice. And “pricier” private schools may actually offermore aid than public schools.

Control what you can: The biggest determinant of aidis the Expected Family Contribution (EFC). By takingproactive steps with assets, income and tax liability inthe Base Year, the year before your student files forfinancial aid, you may be able to qualify for more aid orreduce your after-tax cost of college.

Lower Your Income: If you are self-employed,consider hiring your kids which lowers your busi-ness and personal income.

Reduce assets held in a student’s name. Don’t cash-in savings bonds. This will increase

reported income. Wait until after aid packages areawarded.

Don’t have grandparents or relatives gift to thechild or pay the school directly. While a goodestate planning tactic for relatives, this will countas a resource and reduce potential aid. Instead,set aside the money and have the grandparentsgift it when the student is out of school.

Use gifting to your advantage. Instead of sellingappreciated assets to write a check, gift them toyour child in the lower bracket or shift them to a529 account and withdraw them tax-free.

COLLEGE HELPLINE: 978-388-0020 or 978-416-4107

Viewpoint is produced by Clear View Wealth Advisors, LLC for the benefit of its clients and allied professionals. Although the information here is gathered from reliable sources, readers should notact upon it without professional advice. Past performance is no guarantee of future results. Examples with hypothetical returns illustrated are not representative of a specific investment. Clear ViewWealth Advisors, LLC 12 Amidon Ave., Amesbury, MA 01913 & 25 Lowell St., Wilmington, MA 01887 Tel: 978 388-0020 Email: [email protected]

September 2011Page 5

The Tax Corner (from National Association of Tax Professionals, natptax.com)

Clear View Wealth Advisors, LLC 978-388-0020 or 617-398-7494

Financial planning clients are eligible for discounts on

bundled services.

Call the Clear View Financial Planning Helpline for

help in preparing your income taxes or help with a

divorce plan at 978-388-0020 or 617-398-7494.

“Divorce & Your Money”

Amesbury * Wilmington * Woburn

FREE BookletClear View Wealth Advisors, LLC

Deducting Business Miles

Question: You are in the business of deliveringpackages, documents, and other items for custom-ers. You are using your own vehicle for these de-liveries. Are you allowed to use the standard mile-age rate for all business miles you drive?

Answer: Yes.

The standard mileage rate is allowed in lieu of us-ing your actual automobile expenses. The rule thatdisallows the use of the standard mileage ratewhen your vehicle is used for hire does not apply ifyou are providing courier services.

Business Owners: QuickBooks & the IRS

The IRS has announced that its agents will requirea copy of your QuickBooks data, if used, to helpthem with any audit.

What do taxpayers need to know? You can makeany audit go more smoothly by having good rec-ords which start with how your electronicbookkeeping records are saved.

Each version of QuickBooks comes out of the boxwith one user built in — Administrator. This user isnot password protected. To help maintain dataintegrity, taxpayers should assign QuickBooks fileusers with separate passwords.

QuickBooks will maintain an “audit trail” of data thatis entered or changed by each password-protecteduser.

If your accountant or bookkeeper makes changes,taxpayers should make a copy that matches theadjusted version created.

Tax Tips for Divorce

Case Study: Filing Status After Divorce

Question: Taxpayer and spouse obtained a divorce in2011. The divorce decree states that the couple have tofile Married Filing Jointly for the year of the divorce. Canthey do this?

Answer: No.

A taxpayer is only able to file Married Filing Jointly if thetaxpayer is married on the last day of the year. Since thetaxpayer was divorced prior to the end of the year, the tax-payer is ineligible to file Married Filing Jointly. The Courtshave repeatedly stated that divorce courts cannot overridethe tax laws.

Case Study: Legal Fees and Divorce

Question: Are legal fees incurred during a divorce a de-ductible expense?

Answer: No.

Legal fees relating to a divorce are not deductible, exceptamounts paid for tax advice or preparation or amountspaid in relation to collecting taxable income.

Any portion of the legal fees paid for efforts to obtain taxa-ble income such as alimony are deductible.

Any portion of the legal fees paid to avoid paying alimonyare not deductible. Legal fees paid for any of the followingare also not deductible: Custody of children; Breach ofpromise; Civil or criminal charges resulting from a personalrelationship; Damages for personal injury; Preparation of atitle or defense against a title; Preparation of a will; Proper-ty claims or property settlements (even if it involves therisk of losing income-producing property).

TAX HELPLINE: 978-388-0020 or 978-416-4107

Viewpoint is produced by Clear View Wealth Advisors, LLC for the benefit of its clients and allied professionals. Although the information here is gathered from reliable sources, readers should notact upon it without professional advice. Past performance is no guarantee of future results. Examples with hypothetical returns illustrated are not representative of a specific investment. Clear ViewWealth Advisors, LLC 12 Amidon Ave., Amesbury, MA 01913 & 25 Lowell St., Wilmington, MA 01887 Tel: 978 388-0020 Email: [email protected]

September 2011Page 6

About Clear View Wealth Advisors, LLC

Clear View is a Registered Investment Advisor providingfee-only / fee-for-service financial planning, consultingand investment management services.

We help clients make smarter money choices.

THE BOTTOM LINE

When your life savings are at stake, you want advice youcan trust and someone you can count on. You need atrusted advisor that is objective, an advisor that is notpaid more to sell you one product over another. Youneed a relationship with a firm and an advisor that prom-ises to always put your interest first, a firm with provenexperience and the right professional credentials.

To explore how Clear View and Steve Stanganelli, CFP®can help you, call 978-388-0020 today to schedule anexploratory meeting (via phone or in-person). There is nocharge or obligation.————————————————Complimentary 30-Minute Money Tune-Up+ $100 Off Any Road Map Financial Plan Program

Clear View Wealth Advisors, LLC 978-388-0020 or 617-398-7494

Primary Business Address

12 Amidon Avenue

Amesbury, MA 01913

Convenient Meeting Locations in the Merrimack Valley to Boston:

Newburyport Woburn Wilmington Lawrence Boston

Phone: 978-388-0020 or 617-398-7494Fax: 866-654-4301

Visit our website to find out more about our approach and services.

Specials & Coupons Available Online at Yelp.com & Google.com

FREE Online Planning Tool

Get Yours at www.SmartMoneyRoadMap.com

Steve Stanganelli and Clear Viewoffer help in the following services:

Retirement Income Planning IRA Rollovers Roth IRA Conversion Analysis College Funding Strategies &

529 Plans Divorce Settlement Analysis Qualified Plans for Businesses One-to-One Money Coaching Periodic or One-Time Invest-

ment Advice On-Going Investment Manage-

ment & Monitoring Financial Education Programs

for Groups

Late-Stage College PlanningThe More You Know, The Less You PayPart of a Series for Clear View’s Exclusive College Planning Service

For parents with high school juniors and seniors, college is just around thecorner. This doesn’t mean that it’s too late to plan.

In fact, by taking the time to plan now, parents will be in a better position tomanage their cash flows and fund their retirement.

As the “buyer” of a college education for your student, you have a choice tobe an “informed” buyer or an “uninformed” buyer. What you don’t know aboutthe financial aid process and strategies to help pay for college may end upcosting you more now and in retirement.

Need Help Understanding Your Options? Read on. Or join a free webinar.

![Viewpoint [Edition 15]](https://static.documents.pub/doc/80x56/579078e91a28ab6874c4a8a4/viewpoint-edition-15.jpg)

![Viewpoint [Edition 10]](https://static.documents.pub/doc/80x56/568c36c91a28ab0235995a4c/viewpoint-edition-10.jpg)