64

United States Department of Agriculture Agricultural Cooperative Service ACS Research Report Number 83 as an Alternative Method of Financing for Agricultural Cooperatives

United StatesDepartment ofAgriculture

AgriculturalCooperativeService

ACS ResearchReportNumber 83

as an Alternative Method of Financingfor Agricultural Cooperatives

Abstract

Leasing as an Alternative Method of Financingfor Agricultural Cooperatives

Glenn D. Pederson and Eric E. GillDepartment of Agricultural and Applied EconomicsUniversity of Minnesotaunder a cooperative research agreement withAgricultural Cooperative Service,U.S. Department of AgricultureWashington, D.C.

Economic incentives for agricultural cooperatives to lease capital assets such asstructures, machinery, equipment, and other depreciable items are explored andillustrated. Selected aspects of lease contracts are reviewed. The lease or purchaseproblem is analyzed using capital budgeting (discounted cash flow) and whole-firm financial simulation methods. Results for a case farmer cooperative situationare compared under pre- and post-1986 Tax Reform Act rules and various interestrate and lease rate conditions. The analyses suggest that the attractiveness offacility leasing for cooperatives has declined in the post-1986 period. However,leasing will likely continue to be used selectively by farmer cooperatives.

Key Words: Agricultural cooperatives, finance, leasing, capital budgeting, simulation,lease contracts.

ACS Research Report 83February 1990

Preface

Leasing is an economic alternative to traditional debt financing of capital invcst-ments. Leasing provides the use of, and usually the option to acquire, capitalassets. For agricultural cooperatives, certain changes in the economy might forcecooperatives to try to selectively improve both cash flow and profit performancethrough use of long-term capital leasing arrangements. The economic incentivesfor agricultural cooperatives to lease structures, machinery, equipment, and otherdepreciable assets are primarily financial and tax-related issues. The advantagesof leasing such capital assets depend on a careful analysis of the options andterms that are available.

This study had two primary objectives: (1) to identify the economic incentivesfor agricultural cooperatives to use finance (capital) leases, and (2) to evaluate therelative economic advantages and impacts of finance leases at the project andwhole-firm levels using an agricultural cooperative illustration.

This report attempts to provide a background on leasing activities in agriculture,a discussion of lease contracts and concepts, and a set of illustrations that providedirection to cooperative managers on what to consider when evaluating a lease.

The authors are indebted to numerous individuals for their assistance during thedevelopment of this report, They are Edward Barchenger, Vicki Knapp, DouglasLeicht, and Kenneth Reiners at Farm Credit Leasing Services Corporation: BruceHatteberg of Harvest States Cooperatives; Frank Smith at the University of Minnc-sota; Donald Scott at North Dakota State University; and Charles Kraenzle, JeffreyRoyer, and Donald Frederick at Agricultural Cooperative Service. Susan Pohlodprovided excellent typing support on earlier drafts and the final report. Thisproject was completed under cooperative research agreement 58-3J31-4-1010between North Dakota State University and Agricultural Cooperative Service.

Contents

Highlights . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . iii

Introduction ........................................................................................................... 1Background on Leasing Activity ........................................................................ 3Study Objectives ............................................................................................... 5

Investment Financing Alternatives.. ...................................................................... 6Changing Financial Structure of Large Cooperatives ........................................ 6Small Cooperatives ........................................................................................... 7Financing Alternatives ....................................................................................... 9

Debt Financing .............................................................................................. 9Lease Financing ............................................................................................ 11

Agricultural Cooperative Tax Management Alternatives ....................................... 19Cooperatives and the Investment Tax Credit (ITC) ........................................... 19

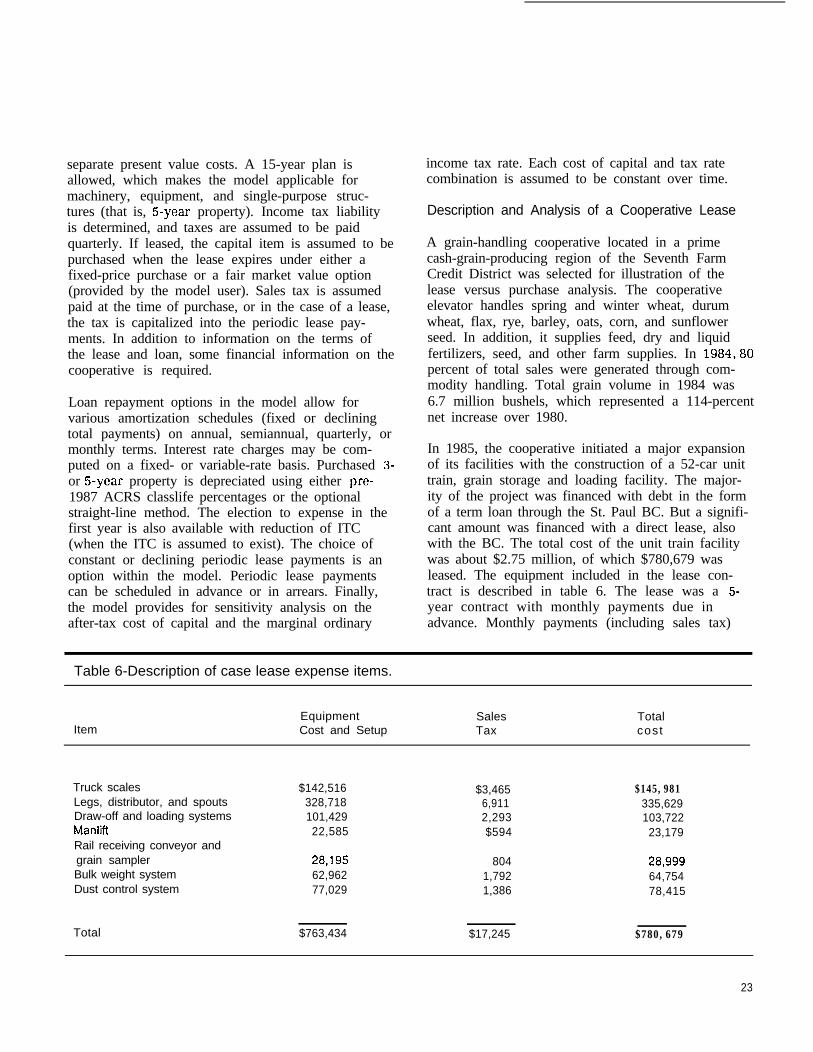

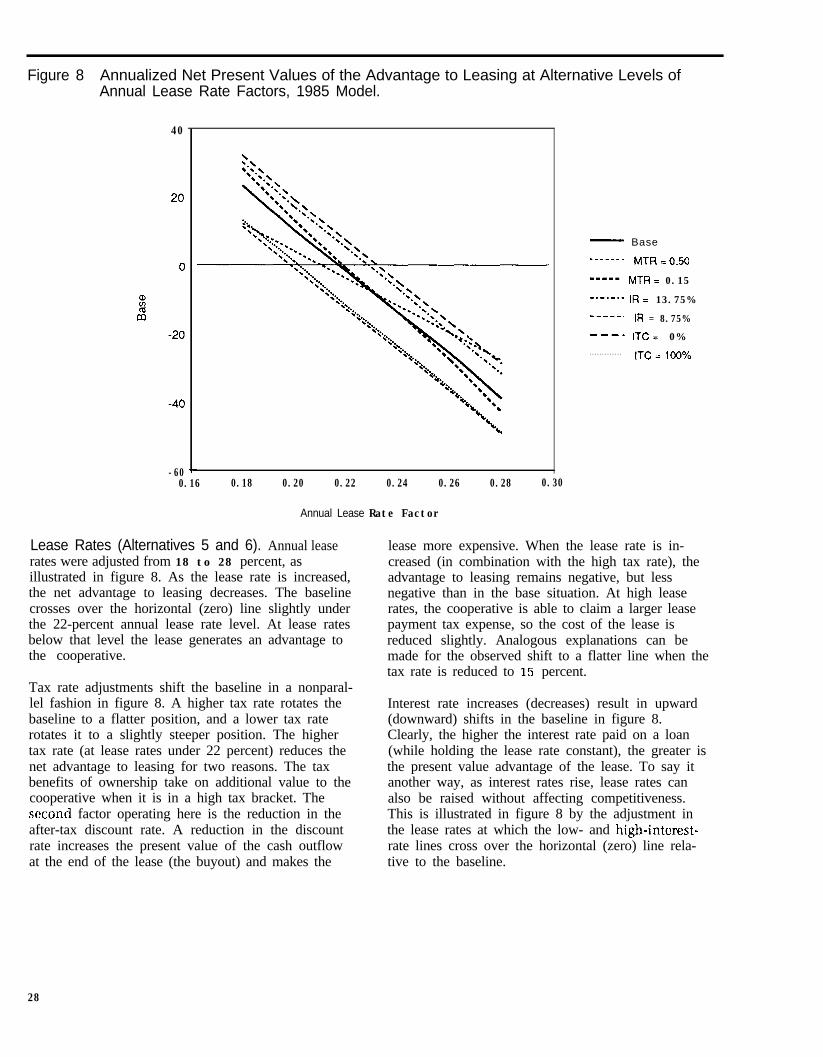

Summary of Lease-Related Federal Tax Law ...................................................... 21Lease Versus Purchase Option.. ....................................................................... 21Capital Budgeting Model ................................................................................... 22Description and Analysis of a Cooperative Lease ............................................. 23Strategy of Analysis .......................................................................................... 24Results of 1985 Analysis ................................................................................... 25Results of 1987 Analysis ................................................................................... 29

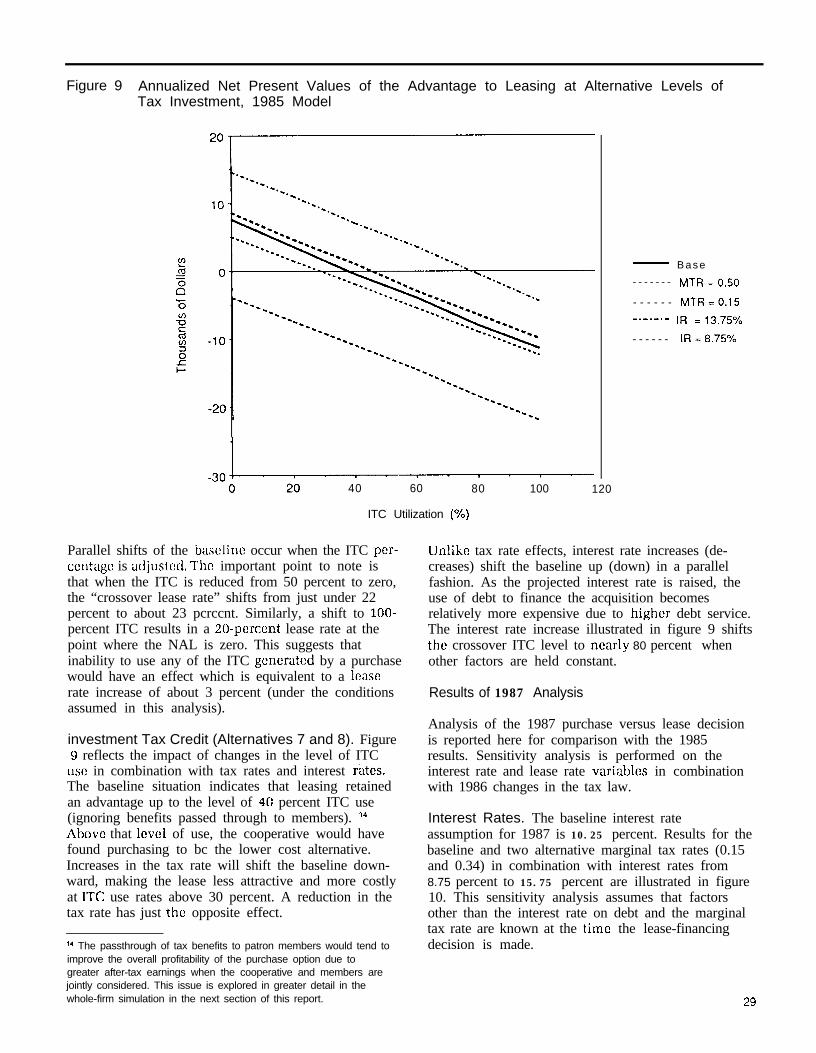

Whole-Firm Lease Simulation Analysis ................................................................ 32Description of the Simulation Model .................................................................. 32Simulation Strategy ........................................................................................... 341985 Model ....................................................................................................... 361987 Model ....................................................................................................... 41Simulation of Tax Law Change Effects ............................................................. 41

Bibliography . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 43

Appendix A: Glossary of Leasing Terms . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 45Appendix B: Sample Lease Agreements Representative of Lease Arrangements 48Appendix C: Summary of Federal Tax Law Related to Leasing . . . . . . . . . . . . . . . . . . . . . . . . . . . 49

ii

Highlights

Leasing Activity

Concern about the financial condition and performance of agricultural coopera-tives has increased because of the farm sector recession of the early and mid-1980’s. Escalating debt levels and interest expense are contributing factors to theerosion of cooperative income. Both the decline of internally generated equityand reliance on debt financing increase the exposure of agricultural cooperativesto financial risk. Under such conditions, cooperative managers and directors needto consider the potential for alternative financial arrangements to rebuild andstabilize cooperatives. Leasing is one such financial option.

The use of leasing by agricultural cooperatives is small and has grown at a slowerpace when compared with that observed in the computer, transportation, and tele-communications industries. The reasons for this slower growth appear to be alack of:

l acceptance of leasing by agricultural managers, with a traditional preference fordebt-financed ownership,

l knowledge by small potential agricultural lessees concerning the advantages,and how to evaluate the financial impacts, of leasing, and

l widespread lessor familiarity with agriculture’s capital needs, and acorresponding lack of available leasing services in rural areas.

As a result, only large cooperatives tend to be users of financial leases and relatedpurchase-leaseback arrangements.

Large cooperatives typically negotiate larger lease deals through national leasingcompanies and regional commercial banks, where leasing expertise exists. Theleasing needs of large, regional farmer cooperatives tend to be similar to their non-agricultural, corporate counterparts. Therefore, leasing services have tended to bemore easily adapted to large cooperative situations. Financial performance anddocumentation of large regional cooperatives also tend to be more acceptable tolarge leasing entities, as compared with the financial picture presented by smallfarmer cooperatives. Another reason for less use of financial leasing by smallcooperatives is the relative absence of leasing services in rural business communi-ties. Finally, where large cooperative financial managers have sought out leasingopportunities, small farmer cooperative managers have often lacked managementexperience and rejected leasing in favor of traditional debt-financing arrange-ments.

The lease-financing option is explored in two related ways: First, the incentivesto leasing that represent the basic underlying reasons for leasing an asset (asopposed to debt financing or a cash purchase). These incentives include im-proved financial risk control through diversified financing, increased cooperativeprofitability, and the cooperative’s own management of cash and working capital.Second, analysis of the conditions that potentially favor leasing requires the use ofcapital budgeting techniques to adequately compare leasing and debt-financedpurchase of capital assets. Alternatively, a simulation analysis can be used to

Capital Budgetingand Simulation

compute the financial impacts on both future cooperative financial performanceand patron benefits. Systematic analysis of these conditions requires that cashflows be evaluated in terms of profitability and feasibility of each financingchoice under a variety of assumptions.

Leasing as a financial choice is investigated under two sets of economic condi-tions-those prevailing in 1985 and those in 1987 (to represent pre- and post-1986 Tax Reform Act conditions). Results from capital budgeting confirm similaranalyses that have appeared in the applied leasing literature. Sensitivity analysisis performed on a case lease using the 1985 capital budgeting model. Resultsfrom the 1985 analysis indicate that while the base lease situation faced by thecooperative slightly favored debt financing at all tax rate levels, variations in theinterest rate on borrowed funds and potential nonuse of investment tax credit(ITC) were sufficiently large to support the cooperative’s actual decision to lease.In this regard, opposing changes in interest rates, tax rates, and lease rates can bepotentially more important than (and different from) single-factor effects. Forexample, the availability of a slightly lower interest rate on debt can be com-pletely offset by the inability to use the ITC generated by purchasing, thus makingthe lease attractive.

Results from the 1987 capital budgeting model are similar to those obtained withthe 1985 model. However, debt financing for 1987 appears to be more highlyfavored given the elimination of the ITC and decline of interest rates. In thiseconomic environment, a slight reduction in the lease rate makes the lease rea-sonably competitive with the debt-financing alternative. Capital budgetingresults are shown to provide useful information to cooperative decisionmakersregarding the most profitable financing choice. Moreover, capital budgetingallows the cooperative manager to consider which factors are most critical to thefinancing choice.

Simulation results indicate that leasing versus debt financing can be evaluated bytheir impacts on future cooperative financial performance and the stream ofpatron benefits. Patron benefits (especially cash refunds) are shown to be quitesensitive to the lease rate, patron tax rates, and interest rate levels. A lowerinterest rate is highly favorable to patron cash refunds with (or without) the lease.A lower lease rate provides a similar but smaller effect when the lease-financingoption is selected (the lease is only 10 percent of the modeled capital structure).Other patron benefits (retirement of member debt and the revolving fund) re-spond similarly to cash refunds when rate adjustments are made.

Debt financing is found to produce the highest present value of patron benefits inall situations that are simulated. However, cooperative financial performancevaries depending on the model being used. The 1985 model produces strongercooperative financial performance with the lease when interest rates were al-lowed to rise, business rates of return and business volume were declining, and

iv

Future CooperativeLeasing

the annual lease rate was held constant. In sharp contrast, the 1987 model indi-cates that debt financing produces higher cooperative net savings and cashavailability in all situations that are analyzed. This consistent result under arange of assumptions suggests that the attractiveness of selected leases (such asthe facility lease modeled here) has declined in the post-1986 (Tax Reform Act)period.

The future use of leasing by agricultural cooperatives remains uncertain. First,changes in tax and financial market conditions, volatile financial performance,and the availability of alternative interest rate pricing arrangements throughbanks for cooperatives have reduced the incentives for small cooperatives toengage in facility leases. However, small-to middle-sized farmer cooperativescontinue to successfully use leases to finance vehicles and other “rolling-stock”capital investments.

Second, farmer cooperatives are recovering from a difficult financial era, and bothreorganization and restructuring are occurring. The scenario of rising interestrates on loans, falling returns on cooperative assets, constant business volume,and market-level lease rates (simulated in the 1987 model in this report) result ina high probability that a business plan for expansion will be financially infeasibleunder both debt and lease financing. As cooperatives emerge from the mid-1980’s period and experience improved financial conditions, caution needs to beexercised regarding asset acquisitions. Additional economic analysis of thefinancial returns and risk is advisable before assuming new lease and debt obliga-tions.

The “leasing is dead” view expressed by some observers tends not to be generallycorrect for large cooperatives. Large cooperatives continue to negotiate leases andlease-purchase deals. Several cooperatives are in the process of selective finan-cial restructuring, and others are developing joint ventures where lease financingis playing a role. A financial lease will likely continue to be the higher cost altcr-native for most farmer cooperatives, and better-than-average leases will be re-quired to be competitive with debt-financed purchases, as long as interest ratesremain relatively low and stable. The methods of analysis presented in this studyare important for cooperative decisionmakers to use in identifying profitableleasing opportunities.

This report does not address the broader issue of combining leases and/or termdebt with nonqualified notices of allocation. Additional research could produc-tively focus on how to develop financing strategies that increase the present valueof future patron benefits under alternative assumptions about the future course ofinterest rates, tax rates, tax benefits of ownership, lease rates, and cooperativeearnings. Presumably, a cooperative gains additional financial flexibility andgcncratcs greater benefits to patrons if all three financing options arc jointlyconsidered.

Leasing as an Alternative Methodof Financing for Agricultural CooperativesGlenn D. Pede’rson, Associate ProfessorEric E. Gill, Research AssistantDepartment of Agricultural and Applied EconomicsUniversity of Minnesota

Introduction

Public concern about the financial condition of agri-cultural cooperatives and other agribusiness firmshas increased as a result of the farm sector economicrecession during the early and mid-1980’s. Farmercooperatives participated in that recession becauseof their reliance on farm sector sales and profitabil-ity. Reduced farm earnings have been reflected inthe impaired earnings (net margins) of farmer coop-eratives between 1980 and 1984 (Royer, 1985). Theproblem has been documented as more criticalamong cooperatives that carry relatively heavy debtloads (Cinder et al., 1985).

Turner (1985) compared the 1984-85 financial auditsof 480 grain and farm supply cooperatives in theOmaha Farm Credit District. Thirty-five percent (170firms) reported operating losses, and 65 percent (310firms) reported net savings. One of the more signifi-cant contrasts between these two groups was thehigh average term-debt/equity capital ratio reportedby the cooperatives with losses and the low leverageratio reported by profitable cooperatives.

The escalation of both debt levels and interestexpense has been one of the major factors contribut-ing to the selective erosion of cooperative profits. Inaddition, the recession in agriculture has reduced

the ability of farmers to invest funds in their coop-eratives. The combination of these events raisesquestions about how cooperatives will be capitalizedin the future.

Boehlje and Pederson (1988) suggest that one of themajor lessons to be learned from financial stress ofthe 1980’s is that the financial base of agriculture istoo narrow. Heavy reliance has been placed oninternally generated equity and debt financing. As aconsequence, the exposure to, and consequences of,financial risk are great for farm and agribusinessfirms. They argue that agricultural managers,financial institutions, and policy makers need toconsider the potential for new financial arrange-ments and instruments in the mix of alternativesused to rebuild and stabilize the financial position ofagricultural businesses. Leasing of production assetsis part of that array of financing options.

This study looks at the past, present, and future roleof leasing in financing agricultural cooperativeinvestments. This report also investigates theimpacts which selective changes in the federal taxlaw during 1986 will have on leasing and its attrac-tiveness to farmer cooperatives.

1

Figure la Types of Equipment Under Financing Lease Arrangements, 1983-1987.

*

---__ --_

~**~--~*~ Telecommunications

- Trucks, Trailers

- Agricultural__-. Aircraft

-*-*-** Computers

? 1983 1984 1985 1986 1987 1988

Figure 1 b Types of Equipment Under Leveraged Lease Arrangements,1 983-l 987.

30

20iiiii

10

:982 1983 1984 1985 1986 1987 1’98t

_-**-- Telecommunications

- Trucks, Trailers

- Agricultural-_-_ Aircraft

-*-.-*- Computers

Background on Leasing Activity

Generally, leasing (including agricultural leasing)has been increasing during the 1980’s. The Depart-ment of Commerce estimates that about $90.6 billionin equipment was purchased for lease in the UnitedStates during 1987. That represents about 29 percentof all business investment in durable capital equip-ment (American Association of Equipment Lessors,1988). Despite the loss of investment tax credit andthe introduction of the alternative minimum tax(AMT), the outlook for aggregate U.S. leasing volumeis that it would reach $108 billion in 1987 (Berg).

In contrast, agricultural equipment has not beenamong the active areas in this growing industry.Figures la and lb indicate that direct (financing) andleveraged leases of agricultural equipment haveaccounted for a small percentage of total new leasingbusiness volume during 1983-87 (American Associa-tion of Equipment Lessors, 1988). Computers,aircraft, and telecommunications remained thedominant forms of leased equipment, through 1987.Leveraged leasing of computers declined dramati-cally in 1987 (fig. lb).

Reasons for the lack of past agricultural leasingactivity can be suggested along three lines: (1) lackof acceptance of this form of financing by agricul-tural decisionmakers because of traditional prefer-ences for ownership, (2) lack of knowledge of poten-tial agricultural lessees about the advantages ofleasing, and (3) lack of lessor familiarity with agri-culture’s capital needs, and the perception thatagricultural firms (farms and cooperatives) are not agrowth market.

Use of capitalized financial leases has occurredprimarily among the largest 100 cooperatives, with31 using leasing in 1986 to provide 6.8 percent oftheir total borrowed capital (Davidson and Kane,1987, 1988). Although the volume of agriculturalleasing has been small relative to the total industry,the range of assets leased by agricultural firms isquite extensive. For example, equipment directlyleased includes automobiles, light-duty trucks,tractors, fertilizer equipment, trailers, forklifts, plantequipment, storage tanks, and an array of othermiscellaneous small equipment. Mid-size and larger

scale leased assets include computers, transportationequipment, processing equipment, office buildings,warehouses, grain elevators, service facilities,railroad cars, and storage facilities.

As part of the growth in agricultural leasing activity,10 of the 12 district banks of the Farm Credit System(FCS) jointly acquired the Interregional ServiceCorporation (ISC) in 1984. Between 1971 and 1984,ISC had served the leasing needs of Midwest andSoutheast regional cooperatives and their affiliates.The new leasing entity, Farm Credit Leasing ServicesCorporation (FCL), expanded the range of leasingservices beyond what ISC had provided.

FCL provided direct leases through 1986, by whichinvestment tax credits were “passed through” tocooperative leases. FCL continues to provide tax-oriented leases, but ownership is retained by FCLand the capital item is leased to the cooperative foran annual rental fee. FCL provides direct financeand leveraged lease services and syndicates leasesfor the FCS. The majority of FCL’s leasing volume isin the form of operating leases. Property under oper-ating lease contracts was $86.3 million in 1985,$74.8 million in 1986, and $87.4 million in 1987(Farm Credit Leasing Services). Net investment indirect finance leases increased from about $7.5million in 1984 to nearly $16 million in 1985, $33.8million in 1986, and $52.8 million in 1987.

FCL’s equipment lease portfolio in 1986 and 1987was dominated by autos, trucks, and truck trailersand bodies (fig. 2a). The geographic distribution ofFCL’s 1987 lease portfolio is illustrated in fig. 2b.The St. Paul and Columbia Farm Credit Districtsaccount for the largest shares of FCL’s lease volume.A majority of FCL’s lease volume was under fixed-rate leasing arrangements (68 percent) in 1987.Variable-rate leases accounted for the remaining 32percent of lease value.

Prior to 1986, the Farm Credit System’s banks for co-operatives (BC’s) became an active lessor to coopera-tives. The St. Paul BC tripled its direct lease andleveraged lease loan volumes between 1984 and1985, reflecting the selective growth in tax-orientedleasing business in the Seventh Farm Credit District.A significant proportion of the BC’s 1984-85 lease

3

Figure 2a Farm Credit Leasing Services Lease Portfolio by Equipment Type, 1986-87.

Other

Office &CommunicationsEquip.

~~;;facturing

Ag.Structures

MaterialHandling

Ag. Field andlrngation Equip.

Trailers andTruck Bodies

Trucks

Autos andLight Trucks

0 10 2 0

Percentage of Portfolio

q 1986q 1987

Figure 2b Farm Credit Leasing Services Lease Portfolio by Farm Credit District, 1986-87.

Springfield

Baltimore

Columbia

Louisville

Jackson

St. Louis

St. Paul

Omaha

Wichita

Texas

Sacramento

Spokane

q 1986q 1987

10 20 30 40

Percent of Current PortfolioSource: Farm Credit Leasing Services Corporation

A

volume was generated on a few large lease contractswith rural electric cooperatives. Leasing activity atthe St. Paul BC declined sharply in 1986 (the bankgenerated less taxable income and less incentive towrite tax-oriented leases), and FCL expanded its roleas lessor to BC customers.

Federal tax policy is a major determinant of leasingindustry activity. A favorable tax treatment ofleasing transactions is influential in attracting firmsinto leasing and in shaping the terms of lease con-tracts, making them more competitive with tradi-tional debt financing. Underlying a lease transactionis the general assumption that it is the productive useof a depreciable asset, rather than its ownership, thatresults in profits necessary to operate a business.Based on that approach, an investing firm would firstdetermine which projects are profitable to undertake,then determine how best to finance those projects.Tax policies play a role by either enhancing or reduc-ing the underlying profitability of the project on anafter-tax basis.

The 1986 U.S. Congress modified the income tax lawas it applies to depreciable assets. The modificationsthat have particular relevance for financial leasingare: (1) repeal of the investment tax credit on itemspurchased after December 31,1985 I, (2) adjustmentof expensing provisions and rules for depreciation,(3) consolidation of tax brackets and reduction of thetop rate (with elimination of selected business de-ductions), and 4) application of the alternative mini-mum tax provision.

These modifications in the tax code have signifi-cantly altered the tax incentives for lessors to writeleases and will potentially lead to changes in thecharacteristics of lease contracts that will be offeredin the future. Leasing contracts will likely be restruc-tured (with some leasing options discontinued) andrepriced to reflect the loss of selected tax benefits.

Study Objectives

An evaluation of finance and tax developments at boththe National and the agricultural levels is clearlybeyond the scope of this study. The more limitedconcern here is to explore capital leasing by agricul-tural cooperatives as an innovation that may selec-tively improve cooperative financial performancewithin this changing economic environment.

Two general objectives of this study are to:

1. Identify the economic incentives for agriculturalcooperatives to use finance (capital) leases, and

2. Evaluate the impacts of finance leases at the projectand whole-firm levels using an agricultural coopera-tive illustration.

The economic incentives for farmer cooperatives tolease structures, machinery, equipment, and otherdepreciable items are primarily finance and tax-related issues. The advantages of leasing such capitalassets depend on a careful analysis of the financingoptions and terms that are available. The current andprojected tax situations of the cooperative and itsfarmer members are of equivalent importance in theleasing decision. These factors, and associated incen-tives are identified in this study through a review ofselected changes in financing terms and lease-relatedtax laws.

The financial impacts of capital leases are analyzed by(1) studying the profitability of the lease or purchasealternative using capital budgeting, and(2) simulating the whole-firm financial effects for afarmer cooperative employing equity, debt, and leasecapital. The results are then evaluated after makingselective adjustments to the tax and financial vari-ables.

’ Farm Finance Leases (as a special category) were allowed theinvestment tax credit through December 31, 1987.

5

Investment Financing Alternatives

Financial capital is required in all phases of coopera-tive management: initial formation, daily operationand maintenance, asset replacement, and plantexpansion. Capital acquisition and funding of theseactivities can occur through the use of equity, debt,and/or leases. Although use of these sources offunds by cooperatives has changed in recent years,balance sheet statistics indicate that those changesarc not widespread by cooperatives regardless ofsize.

Changing Financial Structureof Large Cooperatives

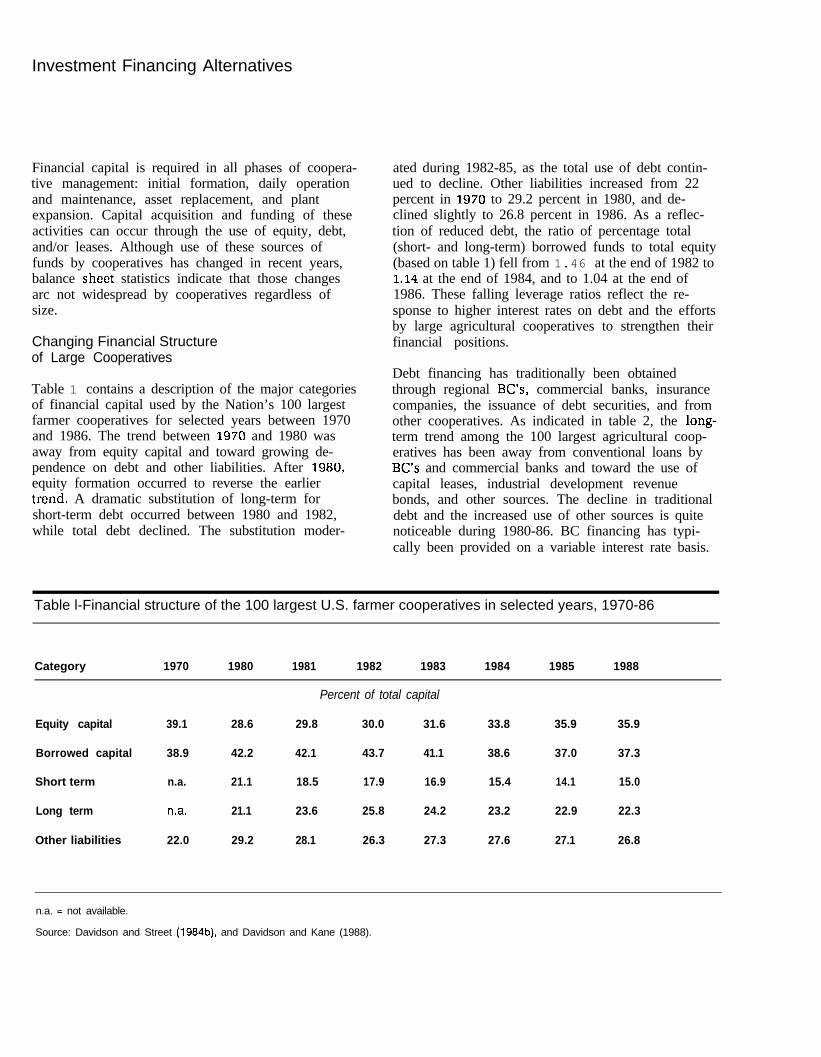

Table 1 contains a description of the major categoriesof financial capital used by the Nation’s 100 largestfarmer cooperatives for selected years between 1970and 1986. The trend between 1970 and 1980 wasaway from equity capital and toward growing de-pendence on debt and other liabilities. After 1980,equity formation occurred to reverse the earliertrend. A dramatic substitution of long-term forshort-term debt occurred between 1980 and 1982,while total debt declined. The substitution moder-

ated during 1982-85, as the total use of debt contin-ued to decline. Other liabilities increased from 22percent in 1970 to 29.2 percent in 1980, and de-clined slightly to 26.8 percent in 1986. As a reflec-tion of reduced debt, the ratio of percentage total(short- and long-term) borrowed funds to total equity(based on table 1) fell from 1.46 at the end of 1982 to1.14 at the end of 1984, and to 1.04 at the end of1986. These falling leverage ratios reflect the re-sponse to higher interest rates on debt and the effortsby large agricultural cooperatives to strengthen theirfinancial positions.

Debt financing has traditionally been obtainedthrough regional BC’s, commercial banks, insurancecompanies, the issuance of debt securities, and fromother cooperatives. As indicated in table 2, the long-term trend among the 100 largest agricultural coop-eratives has been away from conventional loans byBC’s and commercial banks and toward the use ofcapital leases, industrial development revenuebonds, and other sources. The decline in traditionaldebt and the increased use of other sources is quitenoticeable during 1980-86. BC financing has typi-cally been provided on a variable interest rate basis.

Table l-Financial structure of the 100 largest U.S. farmer cooperatives in selected years, 1970-86

Category 1970 1980 1981 1982 1983 1984 1985 1988

Equity capital 39.1 28.6

Borrowed capital 38.9 42.2

Short term n.a. 21.1

Long term n.a. 21.1

Other liabilities 22.0 29.2

Percent of total capital

29.8 30.0 31.6

42.1 43.7 41.1

18.5 17.9 16.9

23.6 25.8 24.2

28.1 26.3 27.3

33.8 35.9 35.9

38.6 37.0 37.3

15.4 14.1 15.0

23.2 22.9 22.3

27.6 27.1 26.8

n.a. = not available.

Source: Davidson and Street (1984b), and Davidson and Kane (1988).

Consequently, interest expense on BC borrowingshas been rising and less stable in the post-1979period. Farmer cooperatives have sought opportuni-ties to convert to fixed-rate debt and insulate theirearnings from rate fluctuations.

Financial leases, industrial revenue bonds and othersources have provided some opportunity to “lockin”interest rates on these liability items. Capital leasestotaled $368 million in 1983, $377 million in 1984,$398 million in 1985, and $390 million in 1986(Davidson and Street, 1984; Davidson and Kane,1988). Industrial revenue bonds showed a similarsmall increase from $394 million in 1983 to $400million in 1985, and fell to $364 million in 1986. In1986 the “other sources” category accounted for 16.8percent of total debt. This included CommodityCredit Corporation and other Government sources(5.3 percent), commercial paper (2.2 percent), othernonfinancial businesses-cooperative and noncoop-erative (3.6 percent), insurance companies (5.4percent), and various others (1.6 percent).

Small Cooperatives

Balance sheet data obtained from the St. Paul Bankfor Cooperatives for three major types of farmercooperatives (dairy, grain, and farm supply) indi-cates no consistent pattern of financial restructuringoccurred among smaller farmer cooperatives in theSeventh Farm Credit District during 1980-85 [table3). In 1985, these smaller cooperatives varied inaverage total investment from nearly $17.5 millionamong dairy, $2.7 million among grain, and $2.5million among farm supply cooperatives. By com-parison, the Nation’s largest 100 cooperatives re-ported an average total investment of about $165million in 1984.

Table 3 contains percentages of financing by liabilitycategory. Although these data are not available in aform that is directly comparable with the largest 100cooperatives, they do suggest that dairy cooperatives(the largest number of the three categories) have alsomoved toward an increased use of industrial revenue

Table 2-Sources of debt capital for the 100 largest U.S. farmer cooperatives in selected years, 1970-85

Source 1970 1976 1980 1981 1982 1983 1984 1985

Banks forCooperatives

Debt Certificates l

Commercial Banks

Leasing/IndustrialRevenueBonds

Other

Percent of total liabilities

62.0

23.4

10.7

n.a.

3.92

56.9

22.7

10.0

4.8

5.6

58.4 57.7 51.7 51 .o 54.6 48.2

13.6 15.5 16.0 16.8 16.3 15.9

12.4 5.9 5.9 5.2 5.3 6.7

7.8 9.2 9.7 11.0 12.3 13.8

7.8 11.7 16.7 16.0 11.5 15.4

n.a. = not available.

’ Debt certificates include bonds, notes, and certificates issued by cooperatives.

2 In 1970 other sources included capitalized leases and industrial revenue bonds.

Source: Davidson and Street (1984), and Davidson and Royer (1986). 7

bonds and contracts. Contracts payable (whichincludes leases) at dairy cooperatives moved up to4.9 percent of total liabilities in 1985. Industrialrevenue bonds provided 3.7 percent of total liabili-ties in 1985. Small-scale grain and general farmsupply cooperatives made increasing (but lesssignificant) use of contracts and revenue bonds assources of funds by 1985.

The relative stability of these balance sheet percent-ages for smaller cooperatives suggests that financialleasing by small cooperatives has been quite limitedwhen compared with the trend among large coopera-tives. This may reflect the relatively recent use offinancial leasing as an option for farmer cooperativesand the absence of leasing services in rural areas.

Table 3-Term liabilities of selected U.S. farmer cooperatives in the Seventh Farm Credit Districtby type of cooperative, 1980-85 l

Cooperative LiabilityType Category 1980 1981 1982 1983 1984 1985

Percent of total liabilities

Dairy Bank for Cooperatives loans 18.0 16.2 19.3 18.4 19.2 17.1Notes payable 0.7 .6 .6 .7 .7 0.4Patron notes payable 1.9 1.8 1.3 .9 1.0 0.9Contracts payable * .4 .3 .7 1.8 2.9 4.9Industrial revenue bonds 2.9 2.3 1.8 1.3 4.5 3.7Other term liabilities 3 .2 .l .l .l .I 0.1

Total 24.1 21.3 23.8 23.2 28.4 27.1

Grain Bank for Cooperatives loans 16.4 17.9 19.3 15.4 15.2 17.5Notes payable .6 .5 .7 .6 .7 .lPatron notes payable 2.3 2.4 2.6 2.0 2.2 2.4Contracts payable .2 .2 .2 .I .2 .8Industrial revenue bonds 1.2 1.1 1.6 1.2 1.2 1.6Other term liabilities 0 0 .2 .I .l .2

Total 20.7 22.1 24.6 19.4 19.6 22.6

General Farm Bank for Cooperatives loans 16.4 19.8 22.4 22.5 21.8 21.83UPPfY Notes payable 1.8 1.4 1.4 2.0 1.9 3.2

Patron notes payable 1.6 1.2 1.1 1.2 1.2 1.3Contracts payable 0.6 0.5 0.7 0.9 0.7 1.3Industrial revenue bonds 1.2 1.1 1.1 0.5 0.5 1.3Other term liabilities 0.2 0 0 0 0.1 0.3

Total 21.8 24.0 26.7 27.1 26.2 29.2

I Only cooperatives which were borrowing from the Seventh District BC were included.

z Contracts payable include financial leases and real estate contracts for deed.

3 Other term liabilities include deferred income tax items and deferred compensation for employees.

Additional explanations would be that the financialcosts and benefits of leases have not been widelyknown by local cooperative decisionmakers, or thatleasing rates were known but were not sufficientlycompetitive to displace the use of term debt. Leasingmay have been more attractive for some cooperatives(for example, dairy) than for others due to the natureof the assets most commonly leased.

The preceding balance sheet trends suggest a highlevel of financial uniformity and stability amongfarmer cooperatives. That uniformity tends toobscure the variety of financing choices available toindividual cooperatives and for individual invest-ment projects of these cooperatives.

Financing Alternatives

The selection of a mode of financing from alternativefinancing sources depends upon economic andnoneconomic factors. For instance, financing at alower projected interest expense is an importanteconomic consideration, but it may be of less impor-tance in some situations than obtaining an owner-ship position. Similarly, a new financing opportu-nity may be rejected in favor of a more traditionalmethod due to a lack of management experiencewith the proposed new financing method.

An additional consideration for a farmer cooperativeis the influence of the financing choice on futurepatron benefits. If an asset is financed with debt,current patrons would gain the tax benefits ofownership, and future patrons would share theinterest costs. The benefits of leasing (lower, stablelease payments) would be distributed among currentand future patrons. This report does not explicitlyanalyze the issue of how financing choice alters thedistribution of patron benefits over time.

Each of the financing methods shown in figure 3 hasdifferent tax, balance sheet, and cash flow character-istics than the other methods of asset control shown.These various financing choices extend from fullownership (through an outright purchase using lOO-percent equity capital) to exclusive use rights withno ownership (through an operating lease arrange-ment). An outright purchase provides the owner

with tax benefits and the right to collateralize or sellthe asset at any time, in addition to its long-term use.At the other extreme, an operating lease conveys justthe contractual right to short-term use of the asset.Between these two extremes the debt-financingalternatives (unsecured loan, mortgage, credit sale,and conditional sale) provide for various levels ofownership and associated rights to claim tax bene-fits, collateralize, or sell the asset prior to maturity.

Debt Financing Interest expense is typically aprimary concern when negotiating a project loanbecause it directly influences the cash flow and thefinancial profitability of the investment project andthe cooperative. Both the level and the variability ofinterest rates paid on debt are important.

Inflationary pressures in the latter 1970’s, coupledwith gradual deregulation of interest rates, pushedinterest rates up during the post-1979 period.Through variable-rate lending, this instabilitytranslated into higher interest expense for coopera-tive borrowers. Variable interest rates on term loansthrough the St. Paul Bank for Cooperatives, forexample, escalated from 7.75 percent in 1978 to13.75 percent in 1982, declined to 11.75 percent in1985, and fell to 10.25 percent in late 1986. Morerecently, the variable rate offered by the St. Paul BChas fluctuated between 10.25 percent in early 1987and 9.25 percent in mid-1988 for middle-sizedcooperatives in relatively strong financial positions.

Variable-rate loans allow for the periodic adjustmentof interest rates when market conditions change. Byadjusting the rate, a lender (for example, the bank forcooperatives) is able to achieve a closer “match”between the interest rate charged and the cost offunds acquired for lending. The disadvantage to theborrower (the farmer cooperative) is that the interest21 expense is not highly predictable in distant years.Situations may occur where interest expensesfluctuate upward at a time when earnings are low,resulting in cash flow stress. If cash reserves aredepleted, the cooperative may find it difficult togenerate cash to make larger debt payments.

9

Figure 3 Alternative Financing Methods in Agriculture for Acquiring Various Levels of AssetOwnership and Use.

Financing Method Description

Ownership and Use::::.::i::::::.:i:::.i:::i.:;.:;:.::.::i::::.

Use

Outright Purchase . . . . . . . . . . . . . . . . . . . . Purchase with own funds

Unsecured Loan . . . . . . . . . . . . . . . . . . . . . . . Purchase with borrowed funds without asecurity interest in the asset

. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . Purchase with borrowed funds with aMortgagesecurity interest in the asset (real estate)

Credit Sale . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . Purchase with financingprovided by the supplier

Conditional Sale . . . . . . . . . . . . . . . . . . . . . . . Purchase with title passing uponcompletion of installment payments

Financial Lease . . . . . . . . . . . . . . . . . . . . . . . . Long-term lease with lessor retainingresidual interest (lessee may have anoption to buy)

Operating Lease . . . . . . . . . . . . . . . . . . . . . . . Short-term rental

IO

Variations in liquidity (due to rising interest ex-pense) is partially manageable through the use offixed-rate financing. In an effort to provide greatercooperative flexibility and control in the term debt-financing decision, some BC’s have initiated lendingprograms that allow variable- or fixed-rate contracts.For example, the St. Paul District BC allows acooperative to finance on a l-year, variable rate or fixthe rate for 1, 3, 5, 7, or 10 years with rate spreads(set according to market interest rate yield curverelationships) to reflect maturity differences. Availa-bility of this form of rate selection flexibility pro-vides a cooperative with additional options forreducing the adverse effects of rising interest rates.It also allows a better choice of debt financing versuslease financing by comparing effective interest rates.

Lease Financing A direct financial lease (fig. 4)provides asset control with generally no ownershiprights, except for the opportunity to acquire the assetat lease termination through a purchase option. Thisfinancing technique has been used by cooperativesfor the past 35 years or so and is typically used tofinance relatively small, short-term asset require-ments. Some tax benefits (for example, investmenttax credit under previous tax law provisions) wereoccasionally “passed through” by the lessor to thelessee under direct finance leasing arrangements.The financial lease is a long-term (typically noncan-celable) financial arrangement and, therefore, differsfrom an annual operating lease. Financing terms ofan operating lease may be adjusted on an annualbasis in contrast with a financial lease where theterms remain unchanged for several years.

A leveraged lease (fig. 5) involves a number ofparties-a cooperative lessee, a lessor (or equityparticipant), a lender, a contractor (or manufacturer),an owner trustee (or indenture trustee), and poten-tially an agent (investment banker). An ownertrustee holds title to the leased asset for the lessor(s)and issues trust certificates to them as evidence ofownership, whereas an indenture trustee holds asecurity intcrcst in the leased property for the benefitof debt lenders. This financing arrangement pro-vides an alternative to the direct financial leasewhen large capital outlays are required on depre-ciable real and personal property. A leveraged lease

operates the same for the lessee as would a directlease. The lessee contracts to make the periodiclease payments and is entitled to the use of the asset.The lessor’s role is altered. The lessor acquires theasset, financing a minor part of it as an equityinvestment, and borrowing to finance the remainingamount. The loan is usually secured by a mortgage,as well as by an assignment of the lease and leasepayments. Since the lessor is a borrower, the leaserate must be set at a level that will cover the interestexpenses incurred under the loan and provide thelessor with an acceptable after-tax rate of return.The lessor is entitled to all tax benefits of deprecia-tion and investment credits that apply.

The leasing option can be explored in two relatedways: (1) the lessee’s incentives to lease, and (2)conditions (factors) that are favorable to lease financ-ing. Incentives to lease include the general underly-ing reasons that a lessee might have for pursuing alease opportunity. Conditions favoring a leaseinclude specific factors that weigh the advantage ofleasing over a debt-financed purchase.

Incentives to Lease. The primary incentive to leaseis to capture favorable financing terms of the leasecontract. Proponents of leasing cite the “freeing up”of working capital and the improved cash flow thatresult from favorable leasing terms. An increase inworking capital means that the downpaymentrequired with debt financing exceeds the initialcapital requirements of the lease. Some leases mayrequire a security deposit that, along with the firstlease payment (usually in advance), wouldsignificantly raise the initial cash outlay of the lease.This may compare to a situation where a cooperativecan obtain nearly loo-percent debt financing, given astrong equity position.

Financial leases may be more predictable in terms oftheir cash flow impact than credit line or variablc-rate debt financing, where the interest rate can beperiodically adjusted. Unanticipated increases ininterest rates and the cash flow requirement toservice the project’s debt may make a project in-feasible due to potential cash flow shortages, eventhough the project represents a profitable use offunds over its life. Since the timing of lease and debt

11

Figure 4 Direct (single-investor) Lease Transactions.

Lessor(owner)

1

Contractor or manufacturer

Leased item(s) (equipment, structure)

b

4Lease payments (rents)

Lessee(user)

Ir

Leased Item(s)(equipment, structure)

12

Figure 5 Leveraged Lease Transactions (adapted from Griffen and Finsterstock, 1974).

CooperativeLessee

Owner Lessors(equity)

Equity Funds to

1 TLease Payments Less Principal,

Purchase Asset Interest, and Expenses

Lease Payments(rents)

1

4Leased Item(s)

(equipment,structures)

Owner Trusteeand/or

Indenture Trustee

Purchase

+

1Leased Item(s)

(equipment,structures)

T 1 Principal

Debt Funds and Interest

to Purchase Asset Payments

InstitutionalLenders(debt)

Contractor orManufacturer

13

payments varies, the feasibility of either financing al-ternative requires that cash inflows and outflows ofthe project be listed along with their time of occur-rence to develop a clear picture of the net cash flowstream on at least an annual basis. The cash flowadvantage of leasing over debt financing is stronglyinfluenced by the repayment period of the loan. Aloan with a term shorter than the lease period willfrequently result in a cash flow advantage to leasing.In addition, a lease may free the lessee from loanindenture agreements or other restrictive covenantsthat apply to the use of cash.

A secondary incentive to lease is to avoid obsoles-cence (residual value) risk. Leasing provides thelessee with protection from risks of ownership losseswhen technological advancement reduces the market(resale) value of capital assets. The lease contractprovides the option for the lessee to purchase theasset without a legal requirement to do so. Thepurchase price may be specified as the asset’s “fairmarket value” or as some predetermined, fixedpercentage of the initial value (a “bargain pur-chase”). If the lessee estimates that the asset isworth less than the purchase option price due toobsolescence, the associated loss is borne by thelessor.2 In anticipation of this risk problem, thelessor will typically set the lease term appreciablyshorter than the economic life of the asset andreduce the purchase option price sufficiently toencourage purchase by the lessee.3

Conditions that Favor Leasing. Major economicfactors that may combine to make leasing the pre-ferred financing option are: anticipated income taxbracket, interest rate level, residual value versuspurchase option price, pass through of lessor volumepurchase discounts on leased assets to the lessee,and agreements concerning repairs, insurance, taxes(sales or use taxes and personal property taxes), andlease termination. Each of these items influenceslease profitability either directly or indirectly. A

comparison of purchasing (using debt) and leasingrequires that an analysis of the discounted, after-taxcash flows be completed. Casual observations maybe quite misleading. (A later section of this reportdemonstrates some results using capital budgeting.)

A cooperative that projects a low tax bracket (due toreduced earnings or the method chosen to distributeearnings) may find that the tax benefits from owner-ship would have a lower value to the cooperativeand its members. If the cooperative conveys taxcredits and deductions to a lessor, and receives alower lease rate in return, both parties may gainthrough leasing. The cooperative is still able todeduct annual lease payments as an expense, andthe lessor would likely be in a position to make fulluse of the tax benefits.

The marginal tax rate plays a dual role in profitabil-ity analysis. Cash flows are adjusted to an after-taxbasis using the projected tax bracket of the coopera-tive. A lower tax rate increases the after-tax net cashflows and profitability of both financing options.The tax rate is also used when determining the ap-propriate after-tax discount rate. For a given cost ofcapital, a lower tax rate raises the after-tax discountrate and reduces the profitability of both options, butit may affect one option more than the other due todifferences in timing of cash flows.

A relatively higher interest rate on debt tends tofavor leasing. The effect of an interest rate increase(holding the lease percentage rate constant) wouldmake the lease more profitable than the use of termdebt.’ The advantage of leasing cannot be deter-mined by a simple comparison of the annual per-centage rates (APR) of interest paid on debt and thepercentage lease rate because different tax rulesapply. Also, the quoted lease rate would alreadyreflect tax benefits used by the lessor. Interestingly,simply having a lease rate lower than the interestrate on debt may not be sufficient, by itself, to make

* It is entirely possible that an asset is considered obsolete to agiven lessee but is not obsolete to alternative potential purchasersat the time the purchase option is being negotiated.

3 Adjustments to the tax law in 1981 reduced the “at risk” require-ment for lessors. Additionally, more latitude was provided in thelength of lease term and the expected residual value that could beused when establishing the lease payment amount.

‘The important point to note here is that interest rates on debt andlease rates do not necessarily move in parallel fashion. Divergencebetween these rates results in situations that may favor a givenfinancing option.

14

the lease more profitable. The size of the spreadbetween these two rates and their relative stabilityover time are likely to be more important considera-tions. The interest rate on debt also plays the majorrole of setting the discount rate to be used in profita-bility analysis.

The residual (resale) value of a capital asset canpotentially affect lease costs when the lessee has afair market value purchase option. Since the capitalitem is owned by the lessor, a general increase inmarket values may translate into a larger-than-expected cash outlay by the lessee to purchase theasset at lease termination. This would tend to makea lease with a market value purchase option lessattractive to cooperatives in periods when assetprices are rising due to inflation or other factors.When asset prices are falling, a market value pur-chase option would generate a gain for the leasingcooperative. In response, lessors have increasinglymoved toward low, fixed-price purchase optionleases in agriculture to reduce residual value effectson profitability. Lessees in agriculture have beengenerally quite receptive to these fixed-price pur-chase contracts because uncertainty about cash flowis reduced. It is useful to note that while lesseesgenerally prefer a fixed-price purchase option, thedifference between the purchase price and theanticipated residual value is irrelevant to the lessee’sposition. It is only the magnitude of the actual leaserate charged (which theoretically reflects the differ-ence) that has significance for the lessee.

Contractual agreements by which the lessor makes fi-nancial concessions on repair, insurance, and/or taxitems reduce the lessee’s expected cash outlay andfavor the lease option. Normal maintenance ofequipment and structures is usually the responsibil-ity of the cooperative lessee. Major repairs expenses(those not due to negligence by the lessee) may ormay not be covered by a manufacturer’s warranty orbe paid for by the lessor .5 If major repairs can be

anticipated to occur during the lease period, and arenot covered by a warranty, they should be incorpo-rated into the lease profitability analysis. Sincedisagreements can arise over what constitutes amajor repair, as opposed to normal maintenance, thisshould also be clearly specified in the lease contract.

Insurance expenses are usually borne by the ownerof an asset and are an expense item that the coopera-tive may seek to avoid through leasing. However,payment of insurance premiums may (or may not) bea negotiable item. Whose responsibility it becomesneeds to be specified in the lease. The magnitude ofthe cost saving is usually small when compared withother costs of ownership, but it should be factoredinto the analysis of lease profitability.

“Net lease” is a term frequently used in the leasingindustry. Under a net lease agreement the lesseebecomes responsible for all costs of insurance,maintenance, and taxes (excluding income taxes).The lessee is required to maintain the asset in goodworking condition and appearance, consideringnormal wear and tear.

Termination of leases on structures creates a uniquesituation for the cooperative lessee. Usually, lessorswill set the purchase price option deliberately low toprovide an incentive for the lessee to purchase theasset at lease termination. If the lessee elects to notpurchase the structure at the end of the lease term,however, either the lessor or the lessee will incur anadditional expense associated with disassembly andremoval from the site. It is important that the leasespecify who is responsible for this and the conditionof the site after removal. This is an importantconsideration if there are large structures, whichmight require concrete footings or other site prepara-tion before installation. If the cooperative lessee ismade responsible for removal, lease profitability willcertainly be reduced for the cooperative.

s Lease contracts frequently contain “warranty disclaimer” clausesthat stipulate since the lessor is not a manufacturer nor engaged inthe sale of the equipment, it is not liable for the failure of the assetto perform for its intended use. The lessee’s only recourse is topursue the manufacturer under the provisions of the warranty ifmajor repairs occur. See, for example, section 15 of the samplelease agreement in appendix B.

15

Terms of the Lease. In addition to the conditionsthat favor a lease, several financing terms areimportant to consider. B These “lease contract” itemsmay be negotiable and do frequently influence leaseprofitability- directly or indirectly. It is expectedthat the lessor and the lessee will take opposingviews concerning how leases should be structuredand a compromise must be found.

The following is a partial list of lease contract itemsto consider:

I. Timing of lease payments. Since lease paymentsare typically made in advance, timing of thesepayments (monthly, annually) will alter thepattern of project cash inflows and outflowsduring the year.

2. Security deposit. Although security deposits areprimarily a feature of operating leases, theirpresence in a financial lease increases the cost ofthe lease. Both the size of the deposit andwhether it bears interest should be considered.

3. Origination or service fees. When the leasecontract is initiated, a service fee may be appliedat a percentage of the value of the leased asset.Fee charges increase the effective interest costs ofthe lease.

4. Duration. Extension of the lease term directlyaffects the amount of each lease payment. Thelonger the lease, the smaller the lease payment,other factors being constant. Tax laws placeeffective limits on the term of some lease con-tracts.

5. Purchase option. Under the “fair market value”purchase option, purchase price determination isdelayed until the lease terminates. In the case of avehicle lease, a “Terminal Rental AdjustmentClause” (TRAC) may provide the lessor with theoption to adjust the lease rental upward to re-cover the diffcrcnce between the projected andactual value at the termination of the lease.

8 Additional discussion of lease contract terms can be found in lsomand Amembal(1982).

6. Penalties. Failure of the lessee to perform underthe terms of the lease contract may trigger a pen-alty fee, or in extreme cases nullify the lease.Under a noncancelable lease, a penalty may arisedue to lessor or lessee action to cancel. Addition-ally, a prepayment penalty would occur when thelessee attempts to pay off the lease before matur-ity. Late payment penalties are also likely to beimposed on the lessee. Clauses that accelerate thelease payment schedule may be quite severe.

7. Flexible lease options. Several factors that mayadd financial flexibility to the lease are trialperiods, provision of nonfinancial services of thelessor, and sharing of delivery, installation, andlicensing expenses.

8. Lease rate. A fixed-rate lease may be preferred bythe lessee due to the predictability of each pay-ment. In exchange, the lessor may be willing toaccept a variable-term lease arrangement tocompensate for the risk associated with changingborrowing costs.

Most (if not all) of these financing terms appear on alease contract; selected items represent areas forlessee/lessor negotiation.

Appendix B contains sample lease agreements andattendant documents, used by Farm Credit LeasingServices Corporation, which are representative ofdocuments designed for executing lease arrange-ments. An application agreement (of the typeshown) is used to initiate the leasing process. Inaddition to the lease application agreement, a releaseof credit and financial information is typically re-quested of the lessee. The lessee has the option toenter into a lease agreement (like the one shown) foreach leased asset, or into a master lease agreement(not shown) that provides for the current lease andfuture lease transactions under a continuing leasearrangement. A purchase option schedule (shown inthe appendix) may be a part of, or a document that issupplemental to, the lease agreement. A guarantyagreement (shown in the appendix) may also berequired by the lessor, depending on the financialstrength of the lessee. Several other lease documentsmay be important in lease transactions, dependingon the type of lease and applicable State laws. These

16

include: purchase order, invoice, bill of sale (fromthe supplier), acknowledgment of delivery and ac-ceptance, and security agreement.

Lease rates are expressed in various ways dependingon the underlying yield to be generated by the lessorand several of the lease contract items identifiedabove. Factors such as the lessor’s pretax yield, theresidual purchase percentage, the number of advancepayments, the frequency of lease payments, the termof the lease, availability of investment tax credit, andrisk all directly or indirectly enter the lease paymentcomputation and, therefore, are determinants of thelease rate.

The “implicit lease rate” is the discount rate that,when applied to the lease payments (excluding costsof executing the lease) and any unguaranteed resid-ual, results in a present value sum of the cash in-flows equal to the fair market value of the leasedproperty (less any ITC claimed by the lessor) ac-quired at the inception of the leasea This discountrate is commonly referred to as the “internal rate ofreturn” to the lessor. For example, a leased assetwith an initial fair market value of $100,000, an$8,000 ITC, monthly advance lease payments of$2,900 for 47 months, and an expected residual fairmarket value of $18,000 at the end of 48 months,yields an implicit (annual) lease rate of 25.64 per-cent. Elimination of the ITC drops the implicit rateto 21.12 percent (assuming the lease paymentsremain unchanged).

The lease rate factor (which is used to determine thesize of the periodic lease payment) is related to theabove implicit rate calculation. The periodic lease

payment amount ($2,900) is divided by the initiallease investment ($100,000) to derive the monthlylease rate factor (0.029). The corresponding annuallease rate factor is 0.348 (0.029 x 12). As the term ofthe lease is lengthened, the lease rate factor declines,reflecting the smaller periodic lease payments.

Lease applications and lease agreements will fre-quently bear the lease rate factor and correspondingscheduled lease payment amounts. It is importantfor the lessee to distinguish between the lease ratefactor and an annual percentage rate (which is oftenquoted on a loan). Since lease rates reflect the use oftax benefits by the lessor, and interest rates on loansdo not reflect tax benefits of ownership, these tworates cannot be directly compared without signifi-cant computational adjustments.

In addition, special purpose clauses may appear onthe lease contract. A “tax indemnification clause”makes provision for the loss of tax benefits by thelessor if the lease “unwinds,” that is, does not passthe tests for a true lease. In this case, the lesseeindemnifies (insures) the lessor for any loss of taxbenefits. Tax indemnification is a clause that thelessor would want to insert into a tax-oriented leaseagreement in anticipation of any change in the taxlaw that would apply retroactively. A “hell-or-high-water clause” reiterates a lessee’s unconditional legalobligation to make lease payments for the entire termof the lease, regardless of events that may affect theleased equipment or structure and its use, or anychange in the lessee’s circumstances. This no-escapeclause provides the lessor with a high level of assur-ance that the lease payments will be made, barringbankruptcy of the lessee’s business.

’ The “running rate” is occasionally quoted by lessors. It is thediscount rate that sets the present value of the lease payments(excluding the residual asset value) equal to the initial fair marketvalue of the leased asset.

17

Table 4-Monthly lease payments and annual lease rate factors for a $100,000 investment at selectedbuyout percentages and lease terms for two alternative lessor implicit yield levels.

Lessorlmplicit TermYield Level(%) (months) 18

Buyout(purchaseoption)percentage

20 22

10.5 60 $1,903' $1,878 $1,8520.22842 0.2254 0.2220

10.5 72 $1,682 $1,662 $1,6420.2018 0.1994 0.1970

10.5 84 $1,526 $1,510 $1,4940.1831 0.1812 0.1793

11.5 60 $1,957 $1,932 $1,9080.2347 0.2318 0.2290

11.5 72 $1,737 $1,718 $1,6990.2084 0.2062 0.2039

11.5 84 $1,583 $1,567 $1,5520.1899 0.1880 0.1862

1 The lease payment is expressed as a constant monthly amount.

* The lease rate factor is expressed as an annual rate in decimal form.This is done by dividingthe monthly lease payment by the initial investment ($100,000) and multiplying the result by 12.

Leasing contract terms involve tradeoffs that areanalogous to those in loan arrangements. Table 4illustrates the relationships between three factors thatinfluence the lease rate: (1) the lessor’s implicit yield(internal rate of return), (2) the term of the lease, and(3) the buyout percentage.

Increases in the lease term (holding other factorsconstant) significantly reduce the size of the monthlylease payment and the corresponding annual leaserate factor. For example, extension of the leasecontract from 60 to 84 months drops the monthlylease payment from $1,878 to $1,510 (assuming a 20-percent buyout and a 10.5-percent lessor yield). Thecorresponding decrease in the annual lease rate isfrom 0.2254 to 0.1812.

A l-percent increase in the lessor’s implicit yieldfrom 10.5 percent to 11.5 percent increases themonthly lease payment from $1,878 to $1,932 (in the20-percent buyout and 60-month lease situation).The associated annual lease rate factor increases from0.2254 to 0.2318 (or by 0.64 percent). One implica-

tion is that a cooperative seeking longer lease termsmay find that the lessor requires a higher pretax yield(to compensate for the longer financing term) and thelease payment may not be appreciably reduced.

A comparison of monthly payments and annual leaserates in table 4 also shows that increases in thebuyout percentage are as influential as increases inthe length of lease term. When the lessor’s yield is10.5 percent and the purchase option is 18 percent,monthly lease payments fall from $1,903 to $1,526when the lease term is increased form 60 to 84months. This represents a 20-percent decrease in themonthly payment when the lease term increases 40percent. However, an increase of just 4 percent in thepurchase option (from 18 to 22 percent) decreases themonthly payment by about 2.5 percent (from $1,903to $1,852). Leasing cooperatives should evaluate allaspects of leasing and, especially, consider the cashflow impacts of changes in the lease term and thebuyout percentage. This is an important considera-tion when making lease comparisons to identify themost favorable lease contract.

18

Agricultural Cooperative TaxManagement Alternatives

Cooperatives, like other corporations, pay Federalincome taxes. But because of unique cooperativeoperating methods, special rules were established toregulate cooperative and patron taxation. The basicconcept is a single tax on net margins at either thecooperative or patron level. Subchapter T of theInternal Revenue Code regulates cooperative taxa-tion.8 It applies to any corporation, with a few ex-ceptions, operating on a cooperative basis. Thissection reviews some of the tax management alterna-tives available to farmer cooperatives. Specialattention is given to past provisions regarding theuse of the investment tax credit.

A cooperative’s tax management decisions dependon many factors, and each cooperative may finditself in a unique situation. According to SubchapterT, cooperatives are able to manage taxation on netmargins from patronage business at the cooperativelevel. To accomplish this, margins must be distrib-uted on a patronage basis, and special rules must bemet. Cooperatives meeting the rules can deductcertain allocations from gross taxable income.

Cooperatives and the Investment Tax Credit (ITC)

Repeal of the ITC allowance under the 1986 TaxReform Act (effective January 1, 1986) eliminated thetax credit as a financing incentive.Q However, coopera-tive use of the ITC has been a problem area in the pastdue partly to the unique position of cooperatives asrepresentatives for their member/patrons. Prior to1978, a cooperative that met Subchapter T require-ments was limited in the amount of qualified invest-ment property that was eligible for the ITC. The avail-able ITC was based on the amount of taxable incomeretained by the cooperative. In most situations, a siz-able amount of taxable income was distributed topatrons, resulting in little or no ITC available to thecooperative.

Provisions of the Revenue Act of 1978 altered themethods of determining available ITC, making itavailable to cooperatives in the same manner as othercorporations. It was required that any part of thecurrently-generated ITC not usable at the cooperative

B Consisting of sections 1381, 1382, 1383, 1385, and 1388. 9 The effect of eliminating the ITC on the purchase versus leasedecision is analyzed in a later section of this report.

Table 54llustration of the computation and use of the investment tax credit (ITC) under pre-1986 tax rules.

Taxable net savings (annual total)

Income tax before ITC

Qualified investment

ITC (optional) rate

ITC earned

First $25,000 of tax liability

85% over $25,000 (0.85 times $1750)

ITC allowed in the current year

Income tax after ITC ($26,750 - $26,488)

ITC allocated to patrons ($50,000 - $26,488)

$100,000

$26,750

$500,000

X .I0

= $50,000

- $25,000

+ $ 1,488

= $26,488 $26,488

$ 262

$23,512

19

level was to be passed through to patrons. ITC recap-ture remained the responsibility of the cooperative.

Past use of the investment tax credit is illustrated intable 5. Assume the cooperative made a qualifiedinvestment of $500,000 with an 8-year useful life inthe 1985 tax year. The available ITC was $100,000 intaxable net savings and a $26,750 tax liability. TheITC could be used to offset the $25,000 in taxes plus85 percent of the taxes over $25,000. A tax liability of$262 remained and $23,512 of ITC was passedthrough to the cooperative’s patrons. If the co-operative sustained a net operating loss, theentire ITC was passed through to the coopera-tive’s patrons that year. The ITC could not becarried back or forward at the cooperativelevel, but patrons could carry unused credits back orforward.

A potential tradeoff existed between the cooperativeand its member/patrons concerning how to maximizethe benefit of ITC use. If the cooperative projectedsufficiently high tax liability, patrons would benefit ifthe cooperative fully utilized the credit. This wouldraise after-tax net savings and either increase thedistribution of cooperative earnings to the patrons orstimulate cooperative growth (if retained). Alterna-tively, if patrons were expected to face a higher taxbracket than that of the cooperative, an allocation ofITC to the patron level would be a more desirablearrangement. A significant obstacle to implementingthis strategy was the lack of information about the taxsituation of patrons.

20

Summary of Lease-RelatedFederal Tax Law

The Federal income tax law related to leasing hasbeen altered through a series of court cases, InternalRevenue Service rulings and procedures, andchanges in the tax law itself. Most of these develop-ments apply to lessees in general and are not specificto agricultural cooperatives. Appendix C contains amore detailed review of past tax legislation related toleasing.

Two major investment incentives altered the leasingstrategies of many firms: accelerated depreciationdeductions (1954), and the investment tax credit(1962). Tax guidelines were later liberalized withpassage of the Economic Recovery Tax Act (ERTA) of1981. ERTA established “safe harbor” leases as aninvestment incentive for firms unable to take advan-tage of the ITC and accelerated depreciation rules.While safe harbor lease rules stimulated leasingactivity, the result was significant tax revenue lossesto the Federal Government. Provisions of the TaxEquity and Fiscal Responsibility Act (TEFRA) of1982 curbed the problem by gradually eliminatingthe safe harbor lease guidelines. Beginning with1984, TEFRA created “finance leases” to replace safeharbor leases. The new finance lease provisionsserved as transitional rules by placing limits onleasing volume and reducing the tax benefits avail-able to lessors. At the same time, liberalization ofthe rules related to limited-use property and fixed-price purchase options served as incentives tolessees.

The Tax Reform Act of 1984 instituted revisedfinance lease guidelines and postponed, until 1988,rules on finance leases for leases entered into afterMarch 6,1984. Most leases continue to fall underthe pre-safe harbor (pm-ERTA) lease guidelines. Theintent of the pre-ERTA guidelines was to ensure thatthe lessor retained some of the benefits, costs, andrisks of ownership without providing the lessee anequity (ownership) interest in the leased item.

At this time, cooperative leasing transactions arecovered under provisions of the Tax Reform Act of1986 (TRA). The 1986 act generally repealed thestatutes that imposed finance lease rules (those usedto determine whether a transaction is a lease or apurchase, that is, conditional sales contract, for taxpurposes) on contracts entered into after December31,1986. Under the 1984 act, these rules had beenpostponed until after 1987. Under the nonstatutory

lease rules (which applied beginning in 1987) thecourts and the IRS determine property ownership fortax purposes based on the “economic substance” ofthe transaction. Transitional rules enacted in 1984continue to apply for selected contracts (CommerceClearing House 1986). A major change in the 1986Tax Reform Act was the repeal of the investment taxcredit for property placed in service after December31,1985.

Lease Versus Purchase Decision

A financing alternative should be shown to be eco-nomically profitable and financially feasible to beclearly preferred. The profitability test suggests thatthe preferred financing option would be that mini-mizing the present cost (discounted, after-tax cashoutflows) to the firm. Discounting the after-tax, netcash outflows associated with the lease and purchasealternatives using a common, after-tax discount rateplaces the two financing options on the same basisfor direct comparison. It is argued here, and else-where (Van Horne 1983), that the appropriatediscount rate to use is the cooperative’s after-tax costof debt because the firm is analyzing a financingalternative-whether to purchase or lease the asset.

The financial feasibility test involves the comparisonof the two undiscounted, after-tax net cash outflowstreams associated with the project financing alterna-tives be compared with the common cash inflow(revenue) stream of the project. The objective is toidentify if and when cash flow deficits occur. In ad-dition, the magnitude of the annual net cash flowsurplus (deficit) is estimated. With this information,the investor may elect to accept or reject the projectunder either/or both financing arrangements. Finan-cial feasibility becomes an important considerationwhenever outside funds (debt or lease) are involvedin a project.

The analysis of the lease or loan/purchase decisionthat follows concentrates on the profitability testaspect. A computerized capital budgeting modeldeveloped for this purpose is used to evaluate thesensitivity of the lease or purchase decision tochanges in key financial variables. The model isbriefly described, along with an actual cooperativeleasing situation. Analysis of the case lease providesinsight into the importance of conditions and termsthat are favorable to leasing.

21

Capital Budgeting Model

Capital budgeting analysis involves a comparison ofthe net present cost (discounted, after-tax net cashexpenses) of purchasing versus leasing. Thesealternatives are compared over a common holdingperiod to incorporate all of the tax benefits generatedby each financing option.‘O

The net present cost (NPC) of the purchase alterna-tive is most compactly expressed by the accountingequation,

NPC (purchase) = D, +XM Am+ fm C4~~---------

m=l (l+r)m (l+r)q>

The accounting equation states that the net presentcost of purchasing is equal to the initial cashdownpayment (Do), plus the discounted sum of end-of-period (principal and interest) payments (D,),minus the tax savings associated with the discountedsum of annual depreciation allowance (A,) andinterest expense (I,) in each period m, minus theinvestment tax credit (C ) if any, which is taken inperiod q (presumably p&fod zero). By discountingeach of these after-tax net cash flow items at theafter-tax interest rate (r) on debt, and summing, theresulting NPC can be compared to other acquistionalternatives expressed on an after-tax present valuebasis with identical lengths of contract.

Similarly, the net present cost of the lease is

N ‘P” BNNPC(lease) =x ---+----t

N LP” M A,+I -

n = O (l+r)” (l+r)N n=O (l+r)’ m=N+l (l+r)” >

The net present cost of leasing is equal to the dis-counted sum of the periodic advance lease payments(LP,), plus the cash purchase outlay at the end of thelease term (B,), minus the tax savings associatedwith deductibility of the periodic lease payments(expressed as the tax rate times the sum of the dis-counted lease payments) and the sum of the dis-counted tax deductions associated with annualdepreciation allowance (A,) after purchasing theasset at lease termination (in period N). Under the

lease alternative, the ITC (if available) is assumed tobe retained by the lessor. Downpayments, rebates,and other cash expenses are not considered in thelease cash flow estimates.

Results of the capital budgeting computations aresummarized in a set of estimates of the net advantageto leasing (NAL). The NAL is computed as thedifference between the net present costs of the twofinancing alternatives.

NAL = NPC (purchase) - NPC (lease)

When the NAL estimate is positive, the lease willresult in the lowest financing cost to the cooperativeover the life of the lease.” When the NAL is nega-tive, the cooperative should purchase the asset,based on comparison of costs. The NAL tells noth-ing about the size of the alternative net costs, onlythe magnitude of the difference in those costs. Asthe NAL approaches zero, the dollar consequence(gain or loss) from choosing one financing alternativeover another becomes smaller, and other factorsbecome relatively more important considerations inthe decision.

An alternative way of expressing the net advantageto leasing is by “annualizing” the NAL. This is doneby amortizing the net present cost of each financingalternative and then subtracting the annualized netpresent cost of the lease from the annualized netpresent cost of the loan:

NPC (purchase) NPC (lease)NALA =

PVIFA (r,m) PVIFA (r,n)

Where NALA is the annualized net advantage toleasing, PVIFA is the present value interest factor fora discount rate of r, associated with either an m-yearloan or an n-year lease. By annualizing the NPCs,loans and leases with different contract lengths canbe directly compared.

The lease-versus-purchase model is used to generatethe discounted cash flow of these two financingoptions under various terms to determine their