18

1 EHR Vendor Marketplace: Which Stars Are Rising—And Which Are Falling Robin Settle Partner Introduction

1

EHR Vendor Marketplace: Which Stars Are Rising—And Which Are FallingRobin Settle

Partner

Introduction

2

2015 | © Kurt Salmon | 3

Presentation Overview

We’ll provide an unbiased look at who the big players are now, the differentiated disruptors and who plays well with others—or doesn’t

The state of the industry

› How have these developments impacted the marketplace?

› What are the new tools?

› How can we support existing systems?

Goals

› Identify the big players in the EHR marketplace

› Gain objective understanding of their customers, reputations and what makes them different

› Name new vendors, their offerings and what to ask them in a selection process

› Ask informed IT vendor evaluation questions (e.g., function, response to changing dynamics and technologies)

2015 | © Kurt Salmon | 4

The fully integrated EHR needs to support the continuum of care …

Essential Elements of a Fully Integrated EHR

PATIENT CARECONTINUUM

MANAGING FOR CLINICAL EFFECTIVENESS

InpatientCare

SpecialistPrimary Care Long‐TermCare

HomeCare

Prevention UrgentCare

DiagnosticAncillariese.g., imaging

EmergencyCare

RehabCare

SkilledNursing

End‐of‐Life Care

Traditional focus of hospitals within the “care continuum”

Extension of capabilities to ACO, partnerships

Extension of capabilities to community, teaching, research

Treatment Ancillariese.g., surgery

3

2015 | © Kurt Salmon | 5

Scope tends toward clinical enterprise/health system, affiliated physicians and patients/families

Delivered through unified/single database platform and/or interoperable solutions; in‐house or remote hosted solutions

Small group of dominant commercial vendors; new cloud‐based solutions emerging but immature

Focus is on patient‐centric, enterprise solutions for clinicals (acute, ambulatory, subacute, departmental, specialties, ancillaries), access and revenue cycle, population health, and analytics

A Deeper Dive into the Vendor Marketplace

2015 | © Kurt Salmon | 6

A Deeper Dive into the Vendor Marketplace (cont’d)

Vendors enabling faster deployment through robust “starter” systems, prepackaged content and more streamlined implementation methodologies

Major functional emphasis on:

Process/workflow automation to improve quality/efficiency/effectiveness

Automated information capture and delivery

Clinical activity based on evidence‐based protocols

Proactive, “intelligent” alerts to improve patient care

Analytics to support outcomes management, performance improvement, quality, population health, etc.

Personalization (not customization) based on user needs/practice

Integration of multimedia, biomedical devices, wearables, emerging technologies

4

The Big Players

EHR Marketplace

2015 | © Kurt Salmon | 8

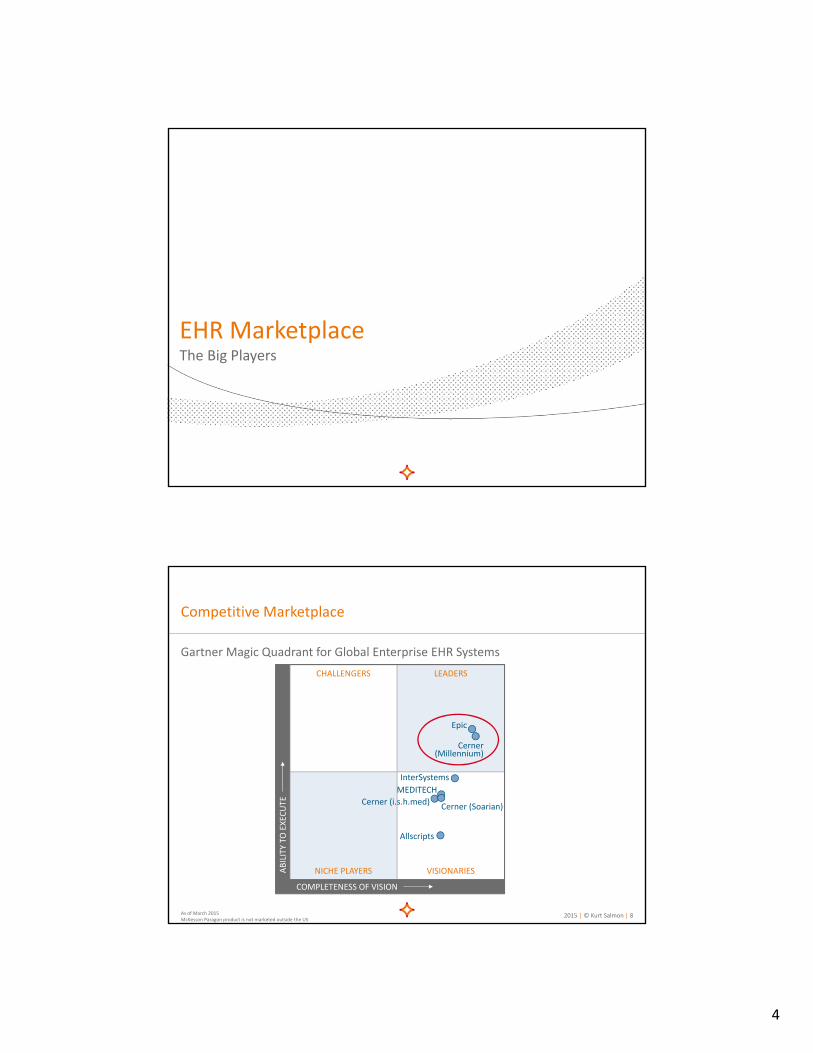

Gartner Magic Quadrant for Global Enterprise EHR Systems

Competitive Marketplace

As of March 2015McKesson Paragon product is not marketed outside the US

Epic

Cerner(Millennium)

InterSystems

MEDITECH

Cerner (Soarian)Cerner (i.s.h.med)

Allscripts

CHALLENGERS LEADERS

NICHE PLAYERS VISIONARIESABILITY TO

EXECUTE

COMPLETENESS OF VISION

5

2015 | © Kurt Salmon | 9

User Feedback

Healthcare IT News

2015 | © Kurt Salmon | 10

Total Market Share by Hospital Size

0

200

400

600

800

1000

EPIC MEDITECH CERNER McKESSON CPSI SIEMENS MEDHOST(HMS)

HEALTHLAND ALLSCRIPTS

© 2014 KLAS Enterprises LLC. All Rights Reserved. www.klasresearch.com

OVER 600 BEDS

401–600 BEDS

201–400 BEDS

101–200 BEDS

26–100 BEDS

1–25 BEDS

6

2015 | © Kurt Salmon | 11

EPIC

CERNER

MEDITECH*

MCKESSON*

SIEMENS*

CPSI

HEALTHLAND

MEDHOST (HMS)

ALLSCRIPTS

QUADRAMED

GE HEALTHCARE

‐80 ‐60 ‐40 ‐20 0 20 40 60 80 100

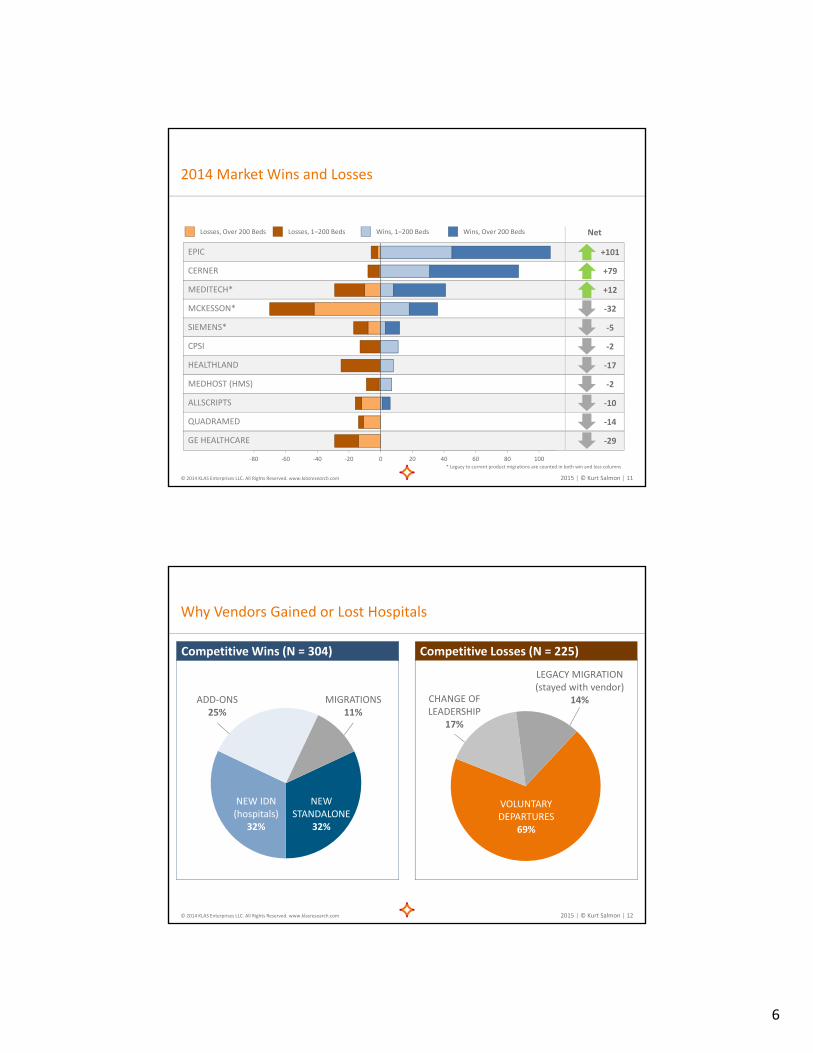

2014 Market Wins and Losses

© 2014 KLAS Enterprises LLC. All Rights Reserved. www.klasresearch.com

* Legacy to current product migrations are counted in both win and loss columns

Losses, Over 200 Beds Losses, 1–200 Beds Wins, 1–200 Beds Wins, Over 200 Beds

+101

+79

+12

‐32

Net

‐2

‐5

‐2

‐17

‐10

‐14

‐29

2015 | © Kurt Salmon | 12

Why Vendors Gained or Lost Hospitals

© 2014 KLAS Enterprises LLC. All Rights Reserved. www.klasresearch.com

Competitive Wins (N = 304) Competitive Losses (N = 225)

ADD‐ONS25%

MIGRATIONS11%

NEW IDN (hospitals)

32%

NEW STANDALONE

32%

LEGACY MIGRATION (stayed with vendor)

14%CHANGE OF LEADERSHIP

17%

VOLUNTARY DEPARTURES

69%

7

2015 | © Kurt Salmon | 13

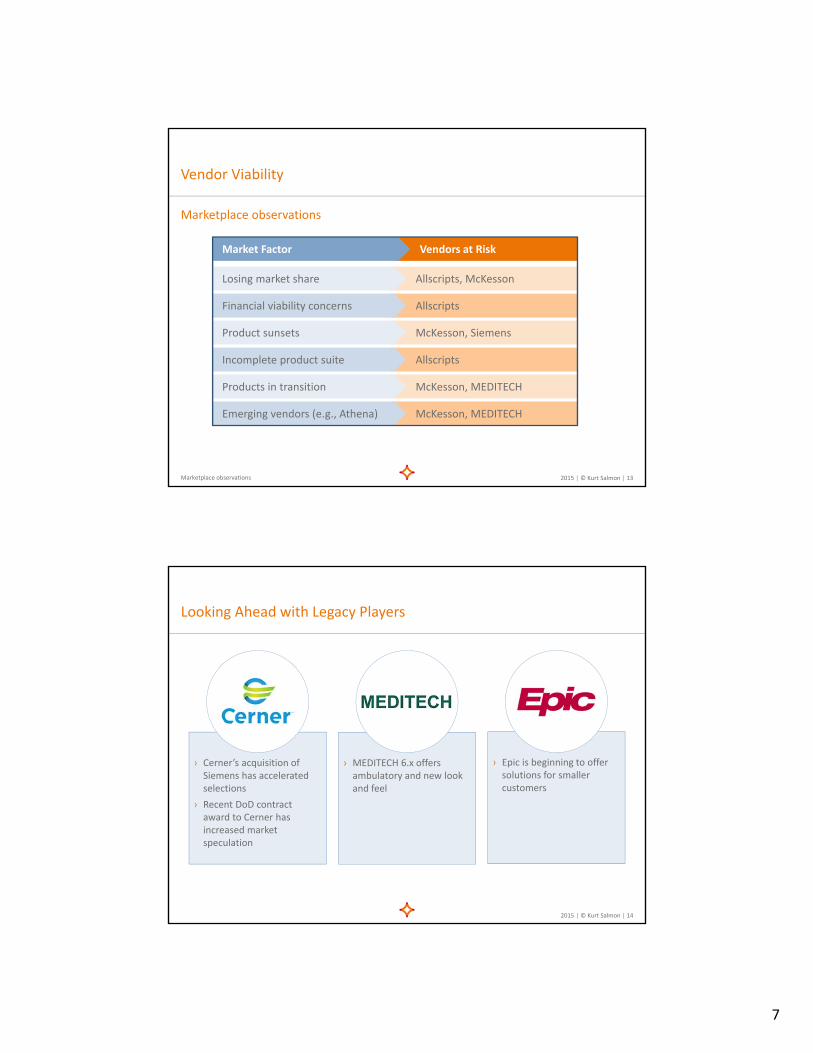

Vendor Viability

Marketplace observations

Marketplace observations

Vendors at Risk

Allscripts, McKessonLosing market share

AllscriptsFinancial viability concerns

McKesson, Siemens Product sunsets

AllscriptsIncomplete product suite

McKesson, MEDITECHProducts in transition

McKesson, MEDITECHEmerging vendors (e.g., Athena)

Market Factor

2015 | © Kurt Salmon | 14

› Cerner’s acquisition of Siemens has accelerated selections

› Recent DoD contract award to Cerner has increased market speculation

Looking Ahead with Legacy Players

› MEDITECH 6.x offers ambulatory and new look and feel

› Epic is beginning to offer solutions for smaller customers

8

2015 | © Kurt Salmon | 15

BUT … the market is ripe for disruption with cloud‐based, leading‐edge technology

Emerging Vendors Are Making Waves

Few new market entrants have been successful

Development partnerships with vendors

have largely failed

In‐house–developed solutions are largely being replaced with commercial

solutions

Product Availability and Integration

9

2015 | © Kurt Salmon | 17

Vendors Are Moving Toward Fully Unified Platforms

Professional BillingBed Management

Enterprise SchedulingEligibility Verification

Registration AmbulatoryContract Management

Patient Access, Health Information Management & Revenue Cycle Systems

E‐Health, Mobile Integration & Other Tools

Department, Specialty & Ancillary Systems

But no vendor yet offers a completely self‐contained solution that provides every IT module

Mobile WayfindingTelehealthDevice IntegrationPatient/Family PortalReporting/Analytical Tools

Behavioral HealthPatient PortalRetail PharmacyCritical CareHospice

2015 | © Kurt Salmon | 18

› Cerner, Epic and MEDITECH are moving more and more to integrated solutions vs. interoperability across the continuum of care

› McKesson Paragon is still missing many modules requiring interfaced solutions

› Health information exchange is here to stay

Hospitals will continue to have partnerships with organizations with different EHR vendors

Meaningful use regulations require the exchange of clinical data with EHR

› Future technologies

Vendor Interoperability vs. Integration Conclusions

10

IT Vendor Evaluation Questions

2015 | © Kurt Salmon | 20

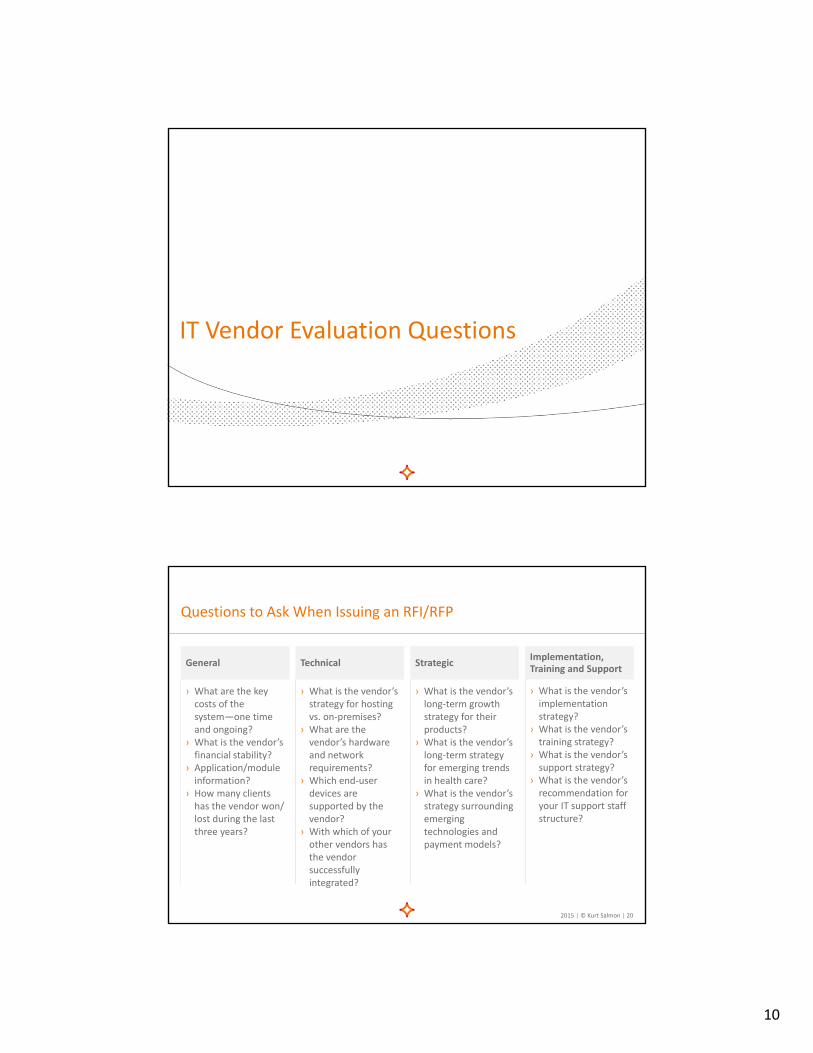

Questions to Ask When Issuing an RFI/RFP

General

› What are the key costs of the system—one time and ongoing?

› What is the vendor’s financial stability?

› Application/module information?

› How many clients has the vendor won/ lost during the last three years?

Strategic

› What is the vendor’s long‐term growth strategy for their products?

› What is the vendor’s long‐term strategy for emerging trends in health care?

› What is the vendor’s strategy surrounding emerging technologies and payment models?

Technical

› What is the vendor’s strategy for hosting vs. on‐premises?

› What are the vendor’s hardware and network requirements?

› Which end‐user devices are supported by the vendor?

› With which of your other vendors has the vendor successfully integrated?

Implementation, Training and Support

› What is the vendor’s implementation strategy?

› What is the vendor’s training strategy?

› What is the vendor’s support strategy?

› What is the vendor’s recommendation for your IT support staff structure?

11

Appendix

2015 | © Kurt Salmon | 22

KLAS Enterprise EHR Vendors Ratings

iCare not rated by KLAS© 2014 KLAS Enterprises LLC. All Rights Reserved. www.klasresearch.com

HOW THE SUITES PERFORM AGAINST ALL OTHER ENTERPRISE SUITES

Rank

Summary Score

Sales & Contracting

Implementation & Training

Functionality & Upgrades

Service & Support

Overall Satisfaction

Would You Buy Again?

Recommend to Peer/Friend?

Part of Long‐Term Plans

85.7 73.7 71.6 70.6 69.6 69.5 69.1 65.0 61.4

Well Above Average/ Above Average

AverageBelow Average/ Well Below Average

12

2015 | © Kurt Salmon | 23

KLAS Research Data: Acute Care EMR

iCare not rated by KLASSource: Best in KLAS 2014: Software & Services; published 2015

RANKPREVIOUS RANK

VENDOR PRODUCTOVERALL SCORE

RATING CHANGE

CONFIDENCE LEVEL

1 1 Epic EpicCare Inpatient EMR 89.3 +1% √√√

2 2 Cerner Millennium PowerChart 79.1 +1% √√√

3 3 Allscripts Sunrise Clinical Manager 75.4 +5% √√√

4 5 MEDITECH C/S Enterprise Medical Record 6.0 67.2 ‐5% √√√

5 6 Siemens Soarian Clinicals 64.9 ‐7% √√√

6 4 McKesson Paragon Clinicals 59.2 ‐16% √√√

2015 | © Kurt Salmon | 24

3.3%

3.4%

3.9%

3.9%

4.1%

7.3%

8.3%

17.0%

18.3%

30.5%

Current U.S. EMR Market Share (Live, Installed Systems*)

HIMMS Analytics, 7/2015 – Clinical Data Repository Vendor – Live & Operational Does not include new contracts or current system implementationsMisc. Vendors/Systems includes legacy systems that are currently supported but no longer offered (e.g., Siemens Invision, MEDITECH MAGIC/Client Server, McKesson Horizon)

For the purposes of this research, a hospital’s CDR vendor was assumed to be the core clinical information system vendor at that site.

Misc. Vendors/Systems

Epic EpicCare

Cerner Millennium

CPSI System 2000

MedHost HMS

MEDITECH 6.X

McKesson Paragon

Self‐Developed

Siemens Soarian (Now Cerner)

Allscripts Sunrise

100% Market Share

13

2015 | © Kurt Salmon | 25

Stage Cumulative Capabilities 2006 2008 2010 2012 20132014 Q4

Stage 7 Complete EMR; CCD transactions to share data; data warehousing; data continuity with ED,

ambulatory, OP0.0% 0.3% 1.0% 1.8% 2.9% 3.6%

Stage 6 Physician documentation (structured templates),full CDSS (variance & compliance), full R‐PACS

0.1% 0.5% 3.2% 7.3% 12.5% 17.9%

Stage 5 Closed‐loop medication administration 0.5% 2.5% 4.5% 11.5% 22.0% 32.8%

Stage 4 CPOE, clinical decision support (clinical protocols)

3.1% 2.5% 10.5% 14.0% 15.5% 14.0%

Stage 3 Nursing/clinical documentation (flow sheets), CDSS (error checking), PACS available outside

Radiology18.7% 35.7% 49.0% 41.7% 30.3% 21%

Stage 2 CDR, controlled medical vocabulary, CDS, may have document imaging; HIE capable

40.0% 31.4% 14.6% 11.4% 7.6% 5.1%

Stage 1 Ancillaries—Lab, Rad, Pharmacy—all installed 17.4% 11.5% 7.1% 4.8% 3.3% 2.0%

Stage 0 All three ancillaries not installed 20.4% 15.6% 10.1% 7.5% 5.8% 3.7%

# Hospitals 4,237 5,166 5,281 5,310 5,458 5,467

Enterprise EMR Marketplace: Industry Inpatient Adoption

AHS is at Stage 6Source: HIMSS Analytics Database

2015 | © Kurt Salmon | 26

100% Market Share

0.5%

1.0%

1.0%

3.9%

7.3%

19.4%

69.9%

Current U.S. HIMSS Stage 7 Hospitals by EMR Vendor*

HIMMS Analytics, 7/2015 – Reported Clinical Data Repository Vendor –Live & Operational/Vendor Websites & Kurt Salmon Research

For the purposes of this research, a hospital’s CDR vendor was assumed to be the core clinical information system vendor at that site.

Epic EpicCare

Cerner Millennium

MEDITECH Client Server

GE/Self‐Developed

Allscripts Sunrise

MEDITECH 6.X

MEDITECH MAGIC

14

2015 | © Kurt Salmon | 27

Allscripts (Sunrise)

Company Overview

› Public HIT company (NASDAQ: MDRX) based in Chicago, Ill.; founded in 1986

› $1.4B 2014 revenue; flat growth 2012–2014

› ~6,000 employees; operating in 11 countries and in over 60,000 facilities worldwide

› Key acquisitions: 2008—Misys; 2010—Eclipsys; 2013—dbMotion

Product Overview

› Fully integrated EMR, Revenue Cycle & Ambulatory; some additional products available (e.g., population health)

› 162 U.S. hospital live installs; 6 additional hospitals contracted/installation in progress (HIMSS database 7/2015)

› 1% of HIMSS Stage 7 U.S. hospitals use Allscripts (2 of 206)

› Ranked #3 of 6 in 2014 KLAS Acute Care EMR (75.4)

› Not ranked in 2014 KLAS Acute Care EMR—Community (68.9)

› Ranked as Visionary in Gartner’s 2015 Magic Quadrant for Enterprise EHR Systems

› Ranked #1 out of 5 in 2014 Black Book EHR Rankings for Academic, Teaching & 300+ Bed Hospitals

Commentary

› Continued focus on turnaround following leadership change in late 2012

› Customers report improved quality, service and implementation

› Strategy focused on interoperability, but has not been fully realized

› Sales challenges due to issues delivering on plans and organizational instability; flat EHR market share

2015 | © Kurt Salmon | 28

Cerner (Millennium)

Company Overview

› Public HIT company (NASDAQ: CERN) based in Kansas City, Mo.; founded in 1979

› $3.4B 2014 revenue; 27% revenue growth 2012–2014

› ~15,800 employees; 14,000+ facilities worldwide

› Key acquisitions: 2010—IMC Health Care; 2011—Clairvia; 2015—Siemens Health Services

Product Overview

› Fully integrated EMR, Revenue Cycle & Ambulatory Solution; wide array of additional solutions

› 840 U.S. hospital live installs; 117 additional hospitals contracted/installation in progress (HIMSS database 7/2015)

› 19% of HIMSS Stage 7 U.S. hospitals use Cerner (40 of 206); also 1 Stage 7 hospital in Spain

› Ranked #2 of 6 in 2014 KLAS Acute Care EMR (79.1)

› Ranked #1 of 7 in 2014 KLAS Acute Care EMR—Community (74.9) (CommunityWorks Clinical Suite)

› Ranked as Leader in Gartner’s 2015 Magic Quadrant for Enterprise EHR Systems

› Ranked #3 out of 5 in 2014 Black Book EHR Rankings for Academic, Teaching & 300+ Bed Hospitals

Commentary

› Market leader with significant growth in market share

› Fully integrated solution; historical weaknesses in revenue cycle and ambulatory EMR have been focus of development and have improved significantly

› Major improvements in delivery and execution overall

15

2015 | © Kurt Salmon | 29

Epic (EpicCare)

Company Overview

› Private HIT company based in Verona, Wis.; founded in 1979

› $1.8B projected 2014 revenue; 16% growth 2012–2014

› ~7,000 employees; 13,000+ facilities worldwide

› Key acquisitions: None

Product Overview

› Fully integrated EMR, Revenue Cycle & Ambulatory Solution

› 904 U.S. hospital live installs; 193 additional hospitals contracted/installation in progress (HIMSS database 7/2015)

› 70% of HIMSS Stage 7 U.S. hospitals use Epic (144 of 40) (1 Stage 7 hospital in Netherlands)

› Ranked #1 of 6 in 2014 KLAS Acute Care EMR (89.3)

› Ranked as Leader in Gartner’s 2015 Magic Quadrant for Enterprise EHR Systems

› 100% of HIMSS Enterprise Davies Awards past 5 years

› Ranked #2 out of 5 in 2014 Black Book EHR Rankings for Academic, Teaching & 300+ Bed Hospitals

Commentary

› Market leader with significant growth in market share

› Fully integrated solution; historical weaknesses in analytics/reporting have been focus of development and have improved significantly

› Historical concerns about eventual leadership transition and technology platform

2015 | © Kurt Salmon | 30

McKesson (Paragon)

Company Overview

› Public health care company (NYSE: MCK), Technology Solutions division based in Alpharetta, Ga.; founded in 1833

› $179B 2015 revenue (3.1B for Technology Solutions); flat Technology Solutions growth 2012–2014

› ~43,500 employees; 3,100+ facilities worldwide

Product Overview

› EMR, Revenue Cycle, Ambulatory & ERP available, though some products are very immature or come from Horizon or other legacy platforms

› 195 U.S. hospital live installs; 5 additional hospitals contracted/installation in progress (HIMSS database 7/2015)

› No HIMSS Stage 7 U.S. hospitals using McKesson Paragon

› Ranked #6 of 6 in 2014 KLAS Acute Care EMR (59.2)

› Ranked #4 of 7 in 2014 KLAS Acute Care EMR—Community (69.2)

› Not Ranked in Gartner’s 2015 Magic Quadrant for Enterprise EHR Systems

› Ranked #4 out of 5 in 2014 Black Book EHR Rankings for Academic, Teaching & 300+ Bed Hospitals

Commentary

› Significant concern among customers regarding future; some success moving customers from Horizon to Paragon

› Paragon is primarily focused on smaller standalone community hospitals; development is planned to build out functionality required for larger (400+ beds) enterprises

› Not all products yet available on Paragon (e.g., ambulatory)—significant development underway/planned; requires other McKesson solutions

16

2015 | © Kurt Salmon | 31

MEDITECH (6.X)

Company Overview

› Private HIT company based in Westwood, Mass.; founded in 1969

› $517M 2014 revenue; 13.5% revenue decline 2012–2014

› ~4,000 employees; 2,400+ facilities worldwide

› Key acquisitions: 2011—LSS

Product Overview

› Fully integrated EMR, Revenue Cycle & ERP Solution; Ambulatory Solution not fully integrated

› 233 U.S. hospital live installs; 28 additional hospitals contracted/installation in progress (HIMSS database 7/2015)

› 424 and 394 U.S. hospitals still on legacy MAGIC & Client Server platforms, respectively (HIMSS database 7/2015)

› 9% of HIMMS Stage 7 U.S. hospitals using MEDITECH (18 of 206), 2 are 6.0, as is 1 Canadian Stage 7 hospital

› Ranked #4 of 6 in 2014 KLAS Acute Care EMR (67.2)

› Ranked #2 of 7 in 2014 KLAS Acute Care EMR—Community (71.6)

› Ranked as Visionary in Gartner’s 2015 Magic Quadrant for Enterprise EHR Systems

› Not Ranked in 2014 Black Book EHR Rankings for Academic, Teaching & 300+ Bed Hospitals

Commentary

› Highly successful, but generally with smaller organizations (e.g., < 200 beds)

› Some attrition due to small hospitals becoming part of large IDNs, as well as need to migrate from legacy platforms

› Ambulatory EMR not fully integrated and perceived as having limited functionality and clinical content to date; new integrated Web‐based module in development

2015 | © Kurt Salmon | 32

› What are the key costs of the system—one time and ongoing?

Application and system software

Third‐party software

Hardware

Implementation and other consulting fees

Interfaces

Training

Other

› What is the vendor’s financial stability?

What are the vendor’s key financial metrics?

› What should I know about the application/module information?

What is the current installed base of each application/module?

When was each application/module developed?

Is each application/module fully integrated into the product suite?

› How many clients has the vendor won/lost during the last three years?

Questions to Ask When Issuing an RFI/RFP—General Questions

17

2015 | © Kurt Salmon | 33

› What is the vendor’s long‐term growth strategy for their products?

What is their 10‐year roadmap?

Ask questions specifically surrounding new acquisitions and/or mergers (e.g., Cerner’s acquisition of Siemens Soarian).

› What is the vendor’s long‐term strategy for emerging trends in health care?

What is the vendor’s strategy for population health and how does that enable your organization to pursue your goals?

What is their strategy for health exchanges and, specifically, within your organization’s region?

What is their big data/analytics strategy and how does that align with your organization’s goals and go‐forward strategy?

› What is the vendor’s strategy surrounding emerging technologies and payment models?

What is their go‐forward strategy with mobile and tablet integration?

How do they integrate with wearables (e.g., Apple WatchKit, Fitbit)?

What are they doing with new patient payment models such as Apple Pay?

What is the vendor’s strategy with payment reform, bundled and capitated payments?

Questions to Ask When Issuing an RFI/RFP—Strategic Questions

2015 | © Kurt Salmon | 34

› What is the vendor’s strategy for hosting vs. on‐premises?

Is the vendor already cloud‐based, or are they moving to the cloud? How does this impact pricing?

Does the vendor host the system themselves, or are third‐party vendors used?

› What are the vendor’s hardware and network requirements?

Which server and database software packages are supported by the vendor?

Does the vendor support virtualization?

What other key technologies are supported (e.g., single sign‐on, Citrix)?

What are the vendor’s storage requirements?

What are the vendor’s network requirements?

› Which end‐user devices are supported by the vendor?

Computers/all‐in‐ones/WoWs?

Mobile devices—tablets, phones?

Printers—network and label, barcode scanners, other?

› With which of your other vendors has the vendor successfully integrated?

Third‐party systems (e.g., key applications such as ERP; bolt‐on/niche applications, content providers)?

Medical equipment (e.g., infusion pumps, point‐of‐care devices, bedside monitoring devices)?

Questions to Ask When Issuing an RFI/RFP—Technical

18

2015 | © Kurt Salmon | 35

› What is the vendor’s implementation strategy?

What method does the vendor recommend (i.e., staged vs. big bang)?

What is the specific plan for your organization (i.e., duration, multiple facility)?

What is the vendor’s recommended staffing for the implementation team?

› What is the vendor’s training strategy?

What is the training approach for the project team and end‐users?

How and where is training conducted?

› What is the vendor’s support strategy?

What are the basic included services (availability and location of support resources)?

What are the costs for additional support?

› What is the vendor’s recommendation for your IT support staff structure?

Questions to Ask When Issuing an RFI/RFP—Implementation, Training & Support

1. 2015. Partners’ $1.2b patient data system seen as key to future. The Boston Globe. http://www.bostonglobe.com/business/2015/05/31/partners‐launches‐billion‐electronic‐health‐records‐system/oo4nJJW2rQyfWUWQlvydkK/story.html