22

Sevan Marine ASA Pareto Conference 2017 Sept 13 th 2017 Reese McNeel CEO / CFO

| Date post: | 24-Apr-2018 |

| Category: |

Documents |

| Upload: | nguyenquynh |

| View: | 248 times |

| Download: | 5 times |

Sevan Marine ASA

Pareto Conference

2017

Sept 13th 2017

Reese McNeel

CEO / CFO

Page 2

Important information

All rights reserved. This publication or parts thereof may not be reproduced or transmitted in any form or by any means, including photocopying or recording, without the prior

written consent of Sevan Marine ASA.

Important information

Sevan Marine

Asset light technology provider

No vessel ownership

Debt free and cash rich

Cost competitive

~20%+ CAPEX savings and significant OPEX savings

Proven - 11 cylindrical units built

HiLoad offloading and FSRU

11 units built, over 35 years in operation

Hummingbird Spirit Voyageur Spirit Goliat FPSO Western Isles FPSO

Sevan Driller Sevan Brasil Sevan Louisiana Sevan Developer

Arendal Spirit Stavanger Spirit

2 Accommodation Units

4 Drilling Units (MODUs)

5 Floating Production Units (FPSOs)

Piranema Spirit UK sector

CAPEX SAVINGS

OPEX SAVINGS

Benefits from cylindrical hull FPSO

WAVES

FLEXIBILITY

No swivel/turret - cost & complexity out

~ 500 MUSD ~ 250 MUSD

Harsh environment swivel/turret examples

Facsimile from Upstream Technology no.1/2016, by permission from Upstream.

Sevan Marine solution

Current activities globally

Americas • ExxonMobil

• FSRU - FRD

North Sea • Western Isles

• UK sector

• Redeployments

Barents Sea • Goliat

• Alta Gotha

• Wisting

Far East / Asia • FPSO

• FSRU - FRD

Australia • FLNG

• Gas processing units

Sevan FPSO – Western Isles field

• Commissioning

• First oil Q4 2017

• Maximum production to be 40k

boepd

• Estimated field life of 15 years

• License fee

Sevan FPSO – UK sector prospect

• Penguins project

• License agreement in place

• Detailed engineering complete

• Engineering support during EPC

Barents Sea prospects

•Cost saving

•Barents Sea experience

•Flexible tie-ins and relocation

•Excellent motion characteristics

Alta/Gohta

Goliat

Wisting

Castberg

• Cost saving for harsh environment

• Flexible

• Excellent motion characteristics

• No show stoppers

FLNG

Mid-water harsh environment drilling

• Most attractive offshore drilling market

• Further concept development

• Cost saving

Fish farming

• Attractive market

• New concept development

• Cylindrical design

Hiload LNG - Offloading

• Low CAPEX

• Any LNGC

• Safe

• High Uptime

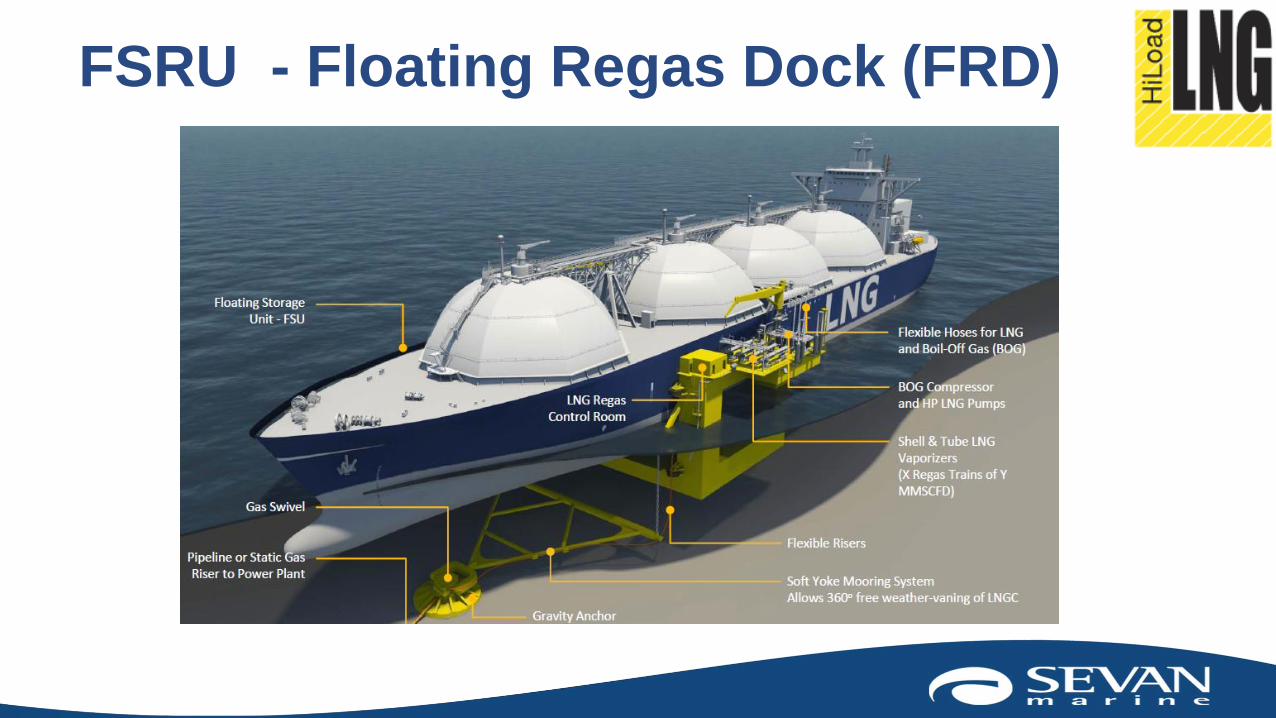

FSRU- Floating Regas Dock (FRD)

FSRU - Floating Regas Dock (FRD)

Strong cash position • MNOK 179 / MUSD 23

No interest bearing debt • 90% equity

Financial strength

0

50

100

150

200

250

Assets Equity and Liabilities

Cash

Current receivables

Non-current assets

Equity

Current liabilities

Balance sheet composition 30 June, 2017 NOK million

Improving perfomance 34,1

21,9

18,3

12,1 13,1

Q2 2016 Q3 2016 Q4 2016 Q1 2017 Q2 2017

Revenues continued operations NOK million

-22,8

-5,9

-16,0 -16,7

-12,9

Q2 2016 Q3 2016 Q4 2016 Q1 2017 Q2 2017

EBITDA continued operations NOK million

Higher revenue • Activity picking up from Q2 2017

• Western Isles likely before year end

Lower operating cost • Continuing cost reduction initiatives

• Impacted by one-off legal and restructuring costs

Positive closure of 2012 legacy tax issue • MNOK 32 including interest paid, MNOK 41 million in P&L effect

• Net profit first half 2017 of MNOK 14.9

Focus on core • Exit of process related businesses complete (KANFA sold)

Recent developments

• Increased activity

• Declining costs

• Strong balance sheet

• Successful closure of 2012 tax

issue

• Exit of KANFA – Focus on core

designs

• Supporting oil majors to reduce

costs

Outlook

• Western Isles license before year end

• UK Sector FPSO project decision

• Court and arbitration hearings on

Logitel

• Development of fish farming

application

• FSRU concept

• New opportunities on horizon

20

Positive outlook

Q&A

Thank you!