Embassy of the United Stales of America Lima, Peru Monday, March I1,2019 Subject: RFQ for 19PE5019Q0062 Audit Services Enclosed is a Request for Quotation (RFQ) for a contractor to provide Audit Services for the International Narcotics and Law Enforcement Affairs Section (INL) in Lima. If you would like to submit a quotation, follow the instructions in Section 3 - Solicitation Provisions ofthe solicitation, complete the required portions of the attached document, and submit it to the Address shown on the Standard Form 1449 that follows this letter. The RFQ does not commit the U.S. Embassy Lima, Peru to make any award. The U.S. Embassy Lima, Peru may cancel this RFQ or any part of it. For a proposal to be considered, you must complete and submit (5) hard copies of the following documentation in English: Volume I: - sF - 1449 - Section I - Supplies or Services and Price/Cost Volume II Section 3 - Information requested under Solicitation Provisions (Audit plan, Gantt, etc) Section 5 - Representation and Certifications and other statement of offerors, including proof of System for Award Management (SAM) Registration. The U.S. Govemment intends to award a contract to the responsible company submitting an acceptable quotation at the lowest price. We intend to award a contract order based on initial quotation, without holding discussion, although we may hold discussions with companies in the competitive range if he is a need to do so. Any questions about this solicitation shall be addressed to EspinozaSE(rilstate.eov in English only in writing until Friday, March22,2019 at l2:00 pm (local time and date). Your proposal must be submitted in a seal envelop marked "Proposal Enclosed" to Noemi Davila, Contracting Offrcer, Av. Lima Polo block 2, Monterrico, Surco no later than Friday, April 05, 2019 at l2:00 pm (local time and date). No quotations will be accepted after this date and time. cerely, mi Davil a Enclosure; As stated tracting Officer OO To: Prospective Offeror:

Transcript

Embassy of the United Stales of America

Lima, PeruMonday, March I1,2019

Subject: RFQ for 19PE5019Q0062 Audit Services

Enclosed is a Request for Quotation (RFQ) for a contractor to provide Audit Services for theInternational Narcotics and Law Enforcement Affairs Section (INL) in Lima. If you wouldlike to submit a quotation, follow the instructions in Section 3 - Solicitation Provisions ofthesolicitation, complete the required portions of the attached document, and submit it to theAddress shown on the Standard Form 1449 that follows this letter.

The RFQ does not commit the U.S. Embassy Lima, Peru to make any award. The U.S.Embassy Lima, Peru may cancel this RFQ or any part of it. For a proposal to be considered,you must complete and submit (5) hard copies of the following documentation in English:

Volume I:- sF - 1449- Section I - Supplies or Services and Price/CostVolume II

Section 3 - Information requested under Solicitation Provisions (Audit plan, Gantt,etc)Section 5 - Representation and Certifications and other statement of offerors,including proof of System for Award Management (SAM) Registration.

The U.S. Govemment intends to award a contract to the responsible company submitting anacceptable quotation at the lowest price. We intend to award a contract order based on initialquotation, without holding discussion, although we may hold discussions with companies inthe competitive range if he is a need to do so.

Any questions about this solicitation shall be addressed to EspinozaSE(rilstate.eov in Englishonly in writing until Friday, March22,2019 at l2:00 pm (local time and date). Your proposalmust be submitted in a seal envelop marked "Proposal Enclosed" to Noemi Davila,Contracting Offrcer, Av. Lima Polo block 2, Monterrico, Surco no later than Friday, April05, 2019 at l2:00 pm (local time and date). No quotations will be accepted after this date andtime.

cerely,

mi Davila

Enclosure; As stated

tracting Officer

OO

To: Prospective Offeror:

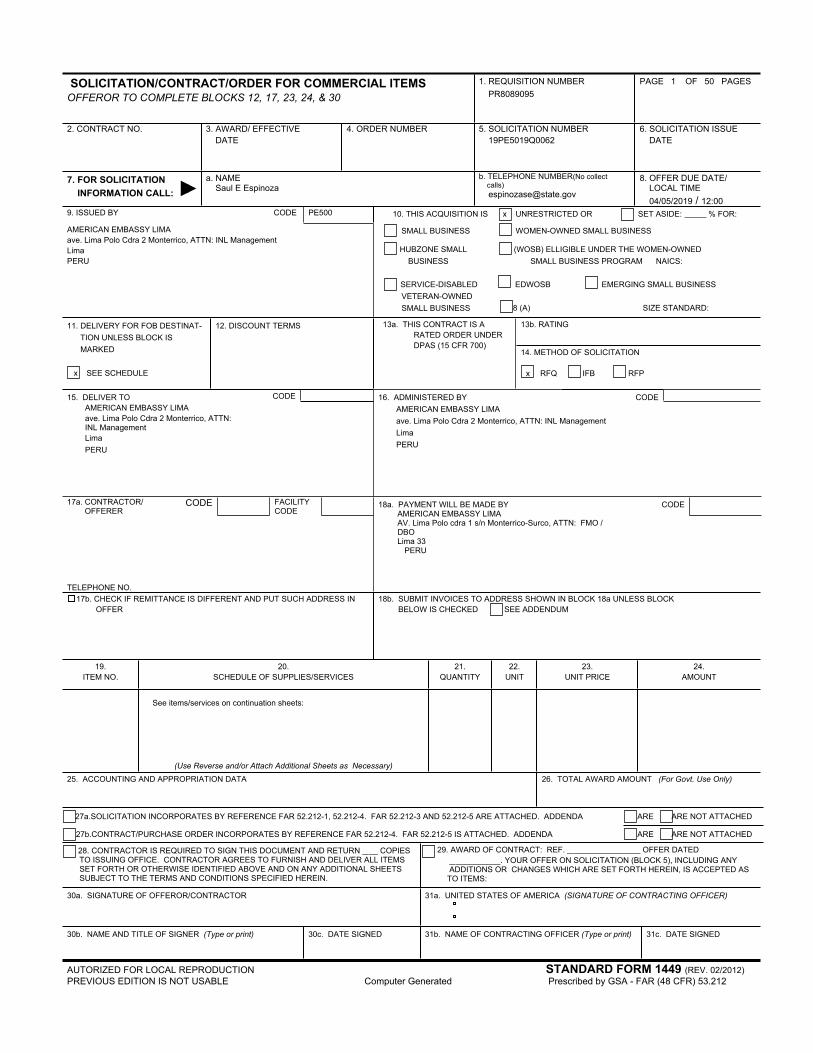

AUTORIZED FOR LOCAL REPRODUCTION STANDARD FORM 1449 (REV. 02/2012) PREVIOUS EDITION IS NOT USABLE Computer Generated Prescribed by GSA - FAR (48 CFR) 53.212

SOLICITATION/CONTRACT/ORDER FOR COMMERCIAL ITEMSOFFEROR TO COMPLETE BLOCKS 12, 17, 23, 24, & 30

1. REQUISITION NUMBERPR8089095

PAGE 1 OF 50 PAGES

2. CONTRACT NO. 3. AWARD/ EFFECTIVE DATE

4. ORDER NUMBER 5. SOLICITATION NUMBER 19PE5019Q0062

9. ISSUED BY CODE PE500 10. THIS ACQUISITION IS x UNRESTRICTED OR SET ASIDE: % FOR:

SMALL BUSINESS WOMEN-OWNED SMALL BUSINESS

HUBZONE SMALL BUSINESS

(WOSB) ELLIGIBLE UNDER THE WOMEN-OWNED SMALL BUSINESS PROGRAM NAICS:

EDWOSB EMERGING SMALL BUSINESS

AMERICAN EMBASSY LIMAave. Lima Polo Cdra 2 Monterrico, ATTN: INL ManagementLima PERU

SERVICE-DISABLED VETERAN-OWNED SMALL BUSINESS 8 (A) SIZE STANDARD:

13b. RATING11. DELIVERY FOR FOB DESTINAT-TION UNLESS BLOCK ISMARKED

x SEE SCHEDULE

12. DISCOUNT TERMS 13a. THIS CONTRACT IS A RATED ORDER UNDER DPAS (15 CFR 700)

14. METHOD OF SOLICITATION

x RFQ IFB RFP

15. DELIVER TO CODE 16. ADMINISTERED BY CODEAMERICAN EMBASSY LIMAave. Lima Polo Cdra 2 Monterrico, ATTN: INL ManagementLimaPERU

AMERICAN EMBASSY LIMAave. Lima Polo Cdra 2 Monterrico, ATTN: INL ManagementLimaPERU

CODE FACILITY CODE

17a. CONTRACTOR/ OFFERER

TELEPHONE NO.

18a. PAYMENT WILL BE MADE BY AMERICAN EMBASSY LIMAAV. Lima Polo cdra 1 s/n Monterrico-Surco, ATTN: FMO / DBOLima 33

PERU

CODE

17b. CHECK IF REMITTANCE IS DIFFERENT AND PUT SUCH ADDRESS IN OFFER

18b. SUBMIT INVOICES TO ADDRESS SHOWN IN BLOCK 18a UNLESS BLOCK BELOW IS CHECKED SEE ADDENDUM

19.ITEM NO.

20.SCHEDULE OF SUPPLIES/SERVICES

21.QUANTITY

22.UNIT

23.UNIT PRICE

24.AMOUNT

(Use Reverse and/or Attach Additional Sheets as Necessary)

25. ACCOUNTING AND APPROPRIATION DATA 26. TOTAL AWARD AMOUNT (For Govt. Use Only)

27a.SOLICITATION INCORPORATES BY REFERENCE FAR 52.212-1, 52.212-4. FAR 52.212-3 AND 52.212-5 ARE ATTACHED. ADDENDA ARE ARE NOT ATTACHED

27b.CONTRACT/PURCHASE ORDER INCORPORATES BY REFERENCE FAR 52.212-4. FAR 52.212-5 IS ATTACHED. ADDENDA ARE ARE NOT ATTACHED

28. CONTRACTOR IS REQUIRED TO SIGN THIS DOCUMENT AND RETURN _ __ COPIES TO ISSUING OFFICE. CONTRACTOR AGREES TO FURNISH AND DELIVER ALL ITEMS SET FORTH OR OTHERWISE IDENTIFIED ABOVE AND ON ANY ADDITIONAL SHEETS SUBJECT TO THE TERMS AND CONDITIONS SPECIFIED HEREIN.

29. AWARD OF CONTRACT: REF. _ _______________ OFFER DATED_ __________. YOUR OFFER ON SOLICITATION (BLOCK 5), INCLUDING ANYADDITIONS OR CHANGES WHICH ARE SET FORTH HEREIN, IS ACCEPTED AS

TO ITEMS:

30a. SIGNATURE OF OFFEROR/CONTRACTOR 31a. UNITED STATES OF AMERICA (SIGNATURE OF CONTRACTING OFFICER)

30b. NAME AND TITLE OF SIGNER (Type or print) 30c. DATE SIGNED 31b. NAME OF CONTRACTING OFFICER (Type or print) 31c. DATE SIGNED

See items/services on continuation sheets:

ITEM NO. 20.SCHEDULE OF SUPPLIES/SERVICES

21.QUANTITY

22.UNIT

23.UNIT PRICE

24.AMOUNT

32a. QUANTITY IN COLUMN 21 HAS BEEN

RECEIVED INSPECTED ACCEPTED, AND CONFORMS TO THE CONTRACT, EXCEPT AS NOTED: _______________________________

32b. SIGNATURE OF AUTHORIZED GOVERNMENT REPRESENTATIVE

32c. DATE 32d. PRINTED NAME AND TITLE OF AUTHORIZED GOVERNMENT REPRESENTATIVE

32e. MAILING ADDRESS OF AUTHORIZED GOVERNMENT REPRESENTATIVE 32f. TELEPHONE NUMBER OF AUTHORIZED GOVERNMENT REPRESENTATIVE

32g. E-MAIL OF AUTHORIZED GOVERNMENT REPRESENTATIVE

33. SHIP NUMBER 34. VOUCHER NUMBER 35. AMOUNT VERIFIEDCORRECT FOR

36. PAYMENT 37. CHECK NUMBER

PARTIAL FINAL COMPLETE PARTIAL FINAL38. S/R ACCOUNT NO. 39. S/R VOUCHER NO. 40. PAID BY

41.a. I CERTIFY THIS ACCOUNT IS CORRECT AND PROPER FOR PAYMENT 42a. RECEIVED BY (Print) 41b. SIGNATURE AND TITLE OF CERTIFYING OFFICER 41C. DATE

42b. RECEIVED AT (Location)

42c. DATE REC’D (YY/MM/DD) 42d. TOTAL CONTAINERS

STANDARD FORM 1449 (REV. 2/2012) BACK

Solicitation 19PE5019Q0062

Page 3 of 50

Table of Contents

SECTION 1 - THE SCHEDULE ................................................................................... 4 SF 1449 cover sheet .................................................................................................. 4

Continuation To SF-1449, RFQ Number - 19PE5019Q0062 Prices, Block 23 ........ 4 Continuation To SF-1449, RFQ Number 19PE5019Q0062 Schedule Of

Solicitation Provisions ............................................................................................. 30 A. Summary Of Instructions. ........................................................................... 30

Evaluation Factors ................................................................................................... 34 Addendum to Evaluation Factors FAR and DOSAR Provision(s) not Prescribed in

Part 12 .......................................................................................................... 35

SECTION 5 - REPRESENTATIONS AND CERTIFICATIONS .............................. 36

Offeror Representations and Certifications ............................................................. 36

Solicitation 19PE5019Q0062

Page 4 of 50

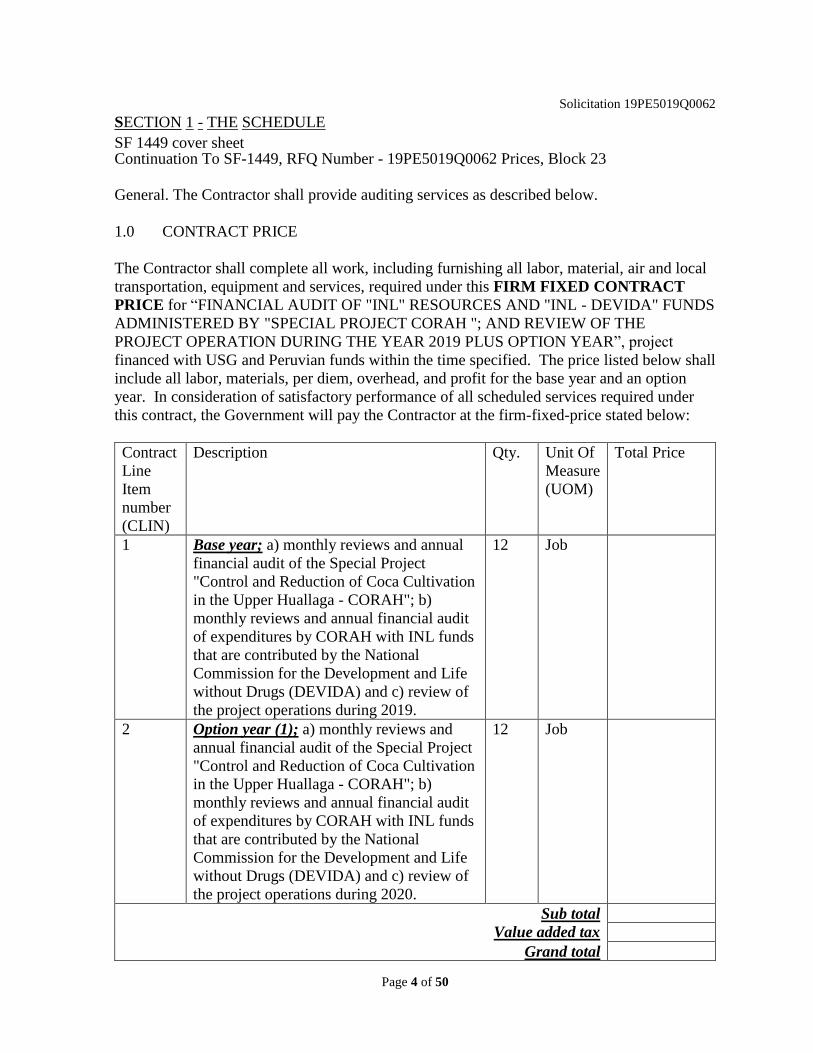

SECTION 1 - THE SCHEDULE

SF 1449 cover sheet Continuation To SF-1449, RFQ Number - 19PE5019Q0062 Prices, Block 23

General. The Contractor shall provide auditing services as described below.

1.0 CONTRACT PRICE

The Contractor shall complete all work, including furnishing all labor, material, air and local

transportation, equipment and services, required under this FIRM FIXED CONTRACT

PRICE for “FINANCIAL AUDIT OF "INL" RESOURCES AND "INL - DEVIDA" FUNDS

ADMINISTERED BY "SPECIAL PROJECT CORAH "; AND REVIEW OF THE

PROJECT OPERATION DURING THE YEAR 2019 PLUS OPTION YEAR”, project

financed with USG and Peruvian funds within the time specified. The price listed below shall

include all labor, materials, per diem, overhead, and profit for the base year and an option

year. In consideration of satisfactory performance of all scheduled services required under

this contract, the Government will pay the Contractor at the firm-fixed-price stated below:

Contract

Line

Item

number

(CLIN)

Description Qty. Unit Of

Measure

(UOM)

Total Price

1 Base year; a) monthly reviews and annual

financial audit of the Special Project

"Control and Reduction of Coca Cultivation

in the Upper Huallaga - CORAH"; b)

monthly reviews and annual financial audit

of expenditures by CORAH with INL funds

that are contributed by the National

Commission for the Development and Life

without Drugs (DEVIDA) and c) review of

the project operations during 2019.

12 Job

2 Option year (1); a) monthly reviews and

annual financial audit of the Special Project

"Control and Reduction of Coca Cultivation

in the Upper Huallaga - CORAH"; b)

monthly reviews and annual financial audit

of expenditures by CORAH with INL funds

that are contributed by the National

Commission for the Development and Life

without Drugs (DEVIDA) and c) review of

the project operations during 2020.

12 Job

Sub total

Value added tax

Grand total

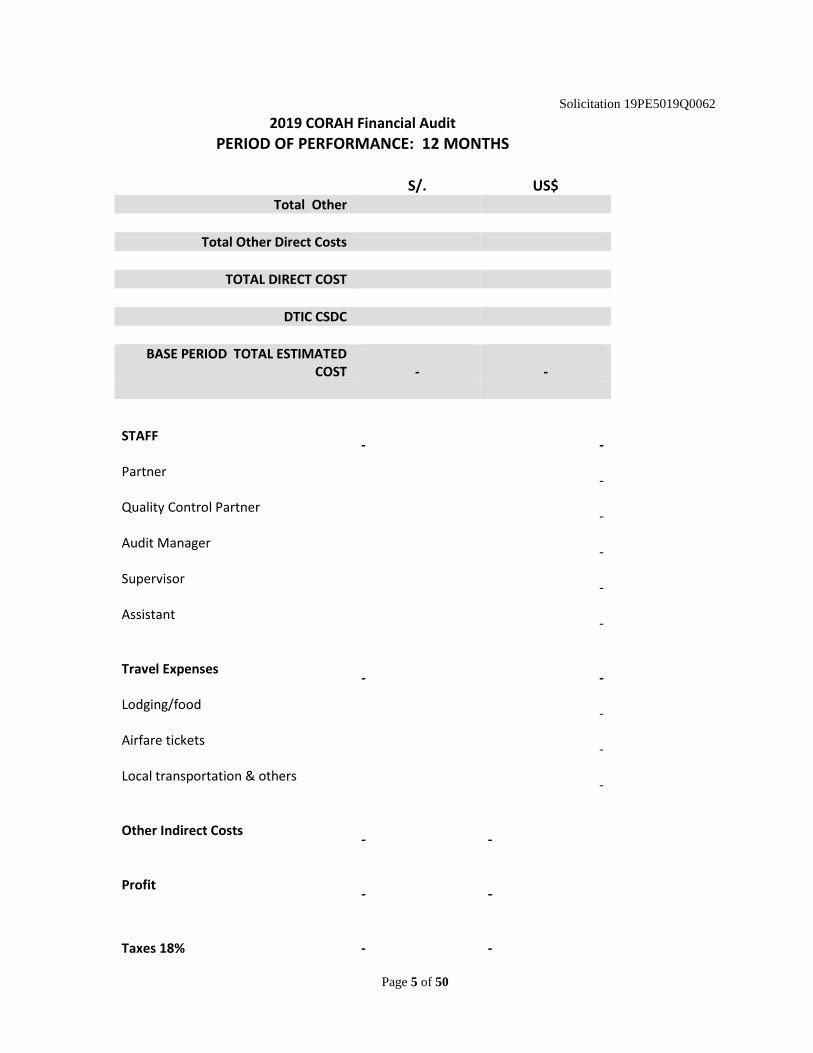

Solicitation 19PE5019Q0062

Page 5 of 50

2019 CORAH Financial Audit

PERIOD OF PERFORMANCE: 12 MONTHS

S/. US$ Total Other

Total Other Direct Costs

TOTAL DIRECT COST

DTIC CSDC

BASE PERIOD TOTAL ESTIMATED COST

-

-

STAFF -

-

Partner -

Quality Control Partner -

Audit Manager -

Supervisor -

Assistant -

Travel Expenses -

-

Lodging/food -

Airfare tickets -

Local transportation & others -

Other Indirect Costs -

-

Profit -

-

Taxes 18% -

-

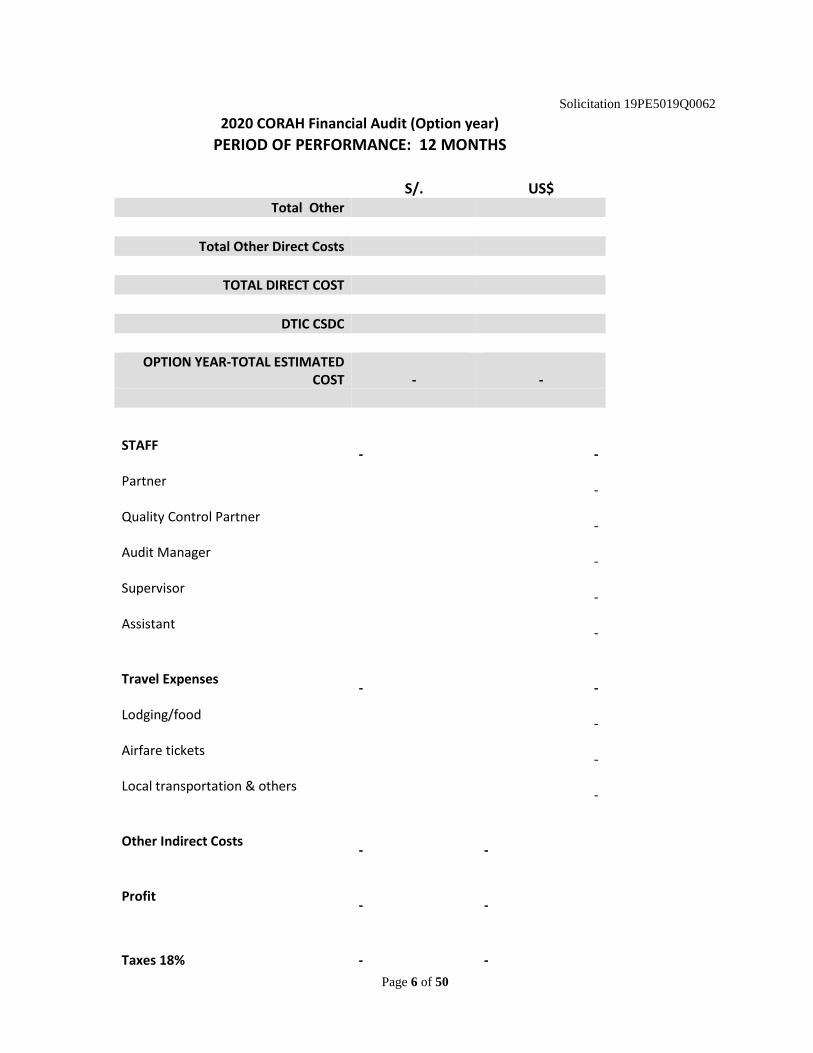

Solicitation 19PE5019Q0062

Page 6 of 50

2020 CORAH Financial Audit (Option year)

PERIOD OF PERFORMANCE: 12 MONTHS

S/. US$ Total Other

Total Other Direct Costs

TOTAL DIRECT COST

DTIC CSDC

OPTION YEAR-TOTAL ESTIMATED COST

-

-

STAFF -

-

Partner -

Quality Control Partner -

Audit Manager -

Supervisor -

Assistant -

Travel Expenses -

-

Lodging/food -

Airfare tickets -

Local transportation & others -

Other Indirect Costs -

-

Profit -

-

Taxes 18% -

-

Solicitation 19PE5019Q0062

Page 7 of 50

1.1 VALUE ADDED TAX VALUE ADDED TAX. Value Added Tax (VAT) is not included in the CLIN rates. Instead, it will be priced as a separate Line Item in the contract and on Invoices. Local law dictates the portion of the contract price that is subject to VAT; this percentage is multiplied only against that portion. It is reflected for each performance period. The portions of the solicitation subject to VAT are:

1.2 PAYMENT IN USD

All payments made to the Contractor under this contract shall be in USD

Continuation To SF-1449, RFQ Number 19PE5019Q0062 Schedule Of Supplies/Services, Block 20 Description/Specifications/Work Statement

1.0 STATEMENT OF WORK:

The United States Government, through the United State Embassy – International

Narcotics and Law Enforcement Affairs (INL) Section in Lima-Peru, has a

requirement for an independent Financial Audit Of "INL" Resources And "INL -

DEVIDA" funds administered by the "Control and Reduction of Coca Cultivation in

the Upper Huallaga – CORAH, Special Project CORAH "; And Review Of The

Project Operation During The Year 2019 plus an option year.

1.1 GENERAL DESCRIPTION

The International Narcotics and Law Enforcement Affairs (hereinafter INL) of the

Embassy of the United States of America in Lima, Peru, requires the services of an

audit firm (hereinafter Auditors) in order to carry out: a) monthly reviews and annual

financial audit of the Special Project "Control and Reduction of Coca Cultivation in the

Upper Huallaga - CORAH" (hereinafter CORAH), b) monthly reviews and annual

financial audit of expenditures by CORAH with INL funds that are contributed by the

National Commission for the Development and Life without Drugs (DEVIDA) and c )

review of the project operations during 2019.

CORAH, a non-profit entity, was created by Supreme Resolution 043-82/AG of the

Ministry of Agriculture, and in accordance with the Convention of "Cooperation to

Reduce the Production, Distribution and Use of Illicit Drugs" signed in 1981 between

the Governments of Peru and the United States of America.

On August 22, 1988, by Ministerial Resolution 0005-88-IN/OFECOD, CORAH came

under the administration and operation of the Executive Office of Drug Control

(OFECOD) of the Ministry of Interior.

Solicitation 19PE5019Q0062

Page 8 of 50

Economic activity

The main economic activity of CORAH is to project, implement and monitor measures

and actions to reduce illicit coca cultivation at a national level. The legal address of the

institution, where its administrative offices are located is Av. Centenario N° 1045,

The objective of this procurement of technical services is that auditors conduct financial

audits of the resources provided by INL and INL-DEVIDA funds administered by CORAH

during 2019, and to review the project operations during this year.

1.2.1. Financial audits (INL resources): will include the following:

a) Monthly: Review of CORAH monthly financial statements, to be prepared and

submitted during 2019, in accordance with accounting principles generally accepted in

Peru.

b) Annual: Review of CORAH financial statements, to be prepared as of December 31,

2019, in accordance with Accounting Principles Generally Accepted in Peru, in order for

auditors to express an opinion on whether these financial statements reasonably present, in

all material aspects, CORAH’s financial position, the results of its activities and its cash

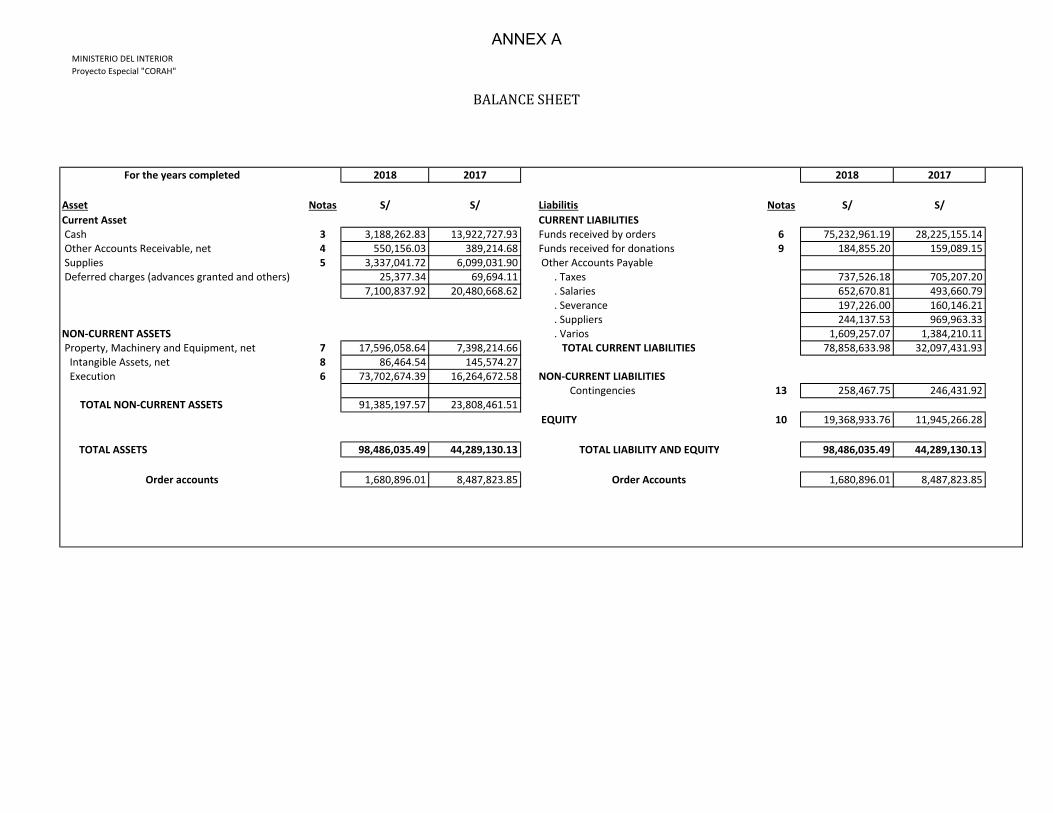

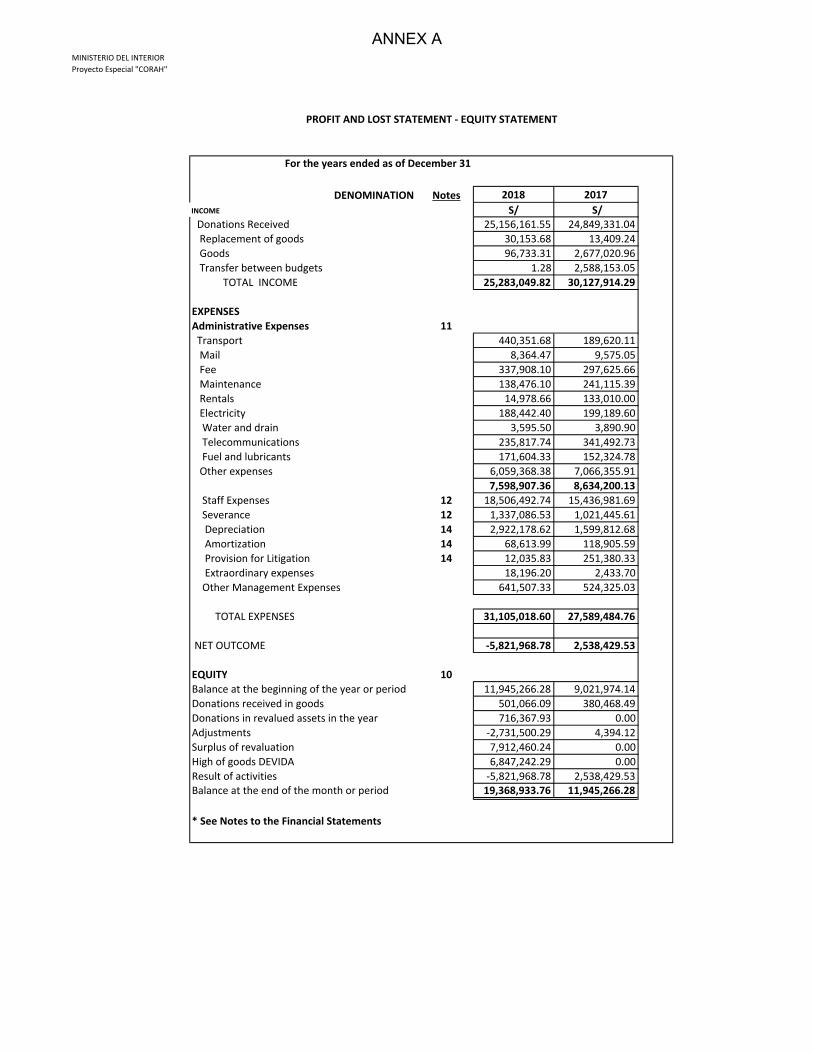

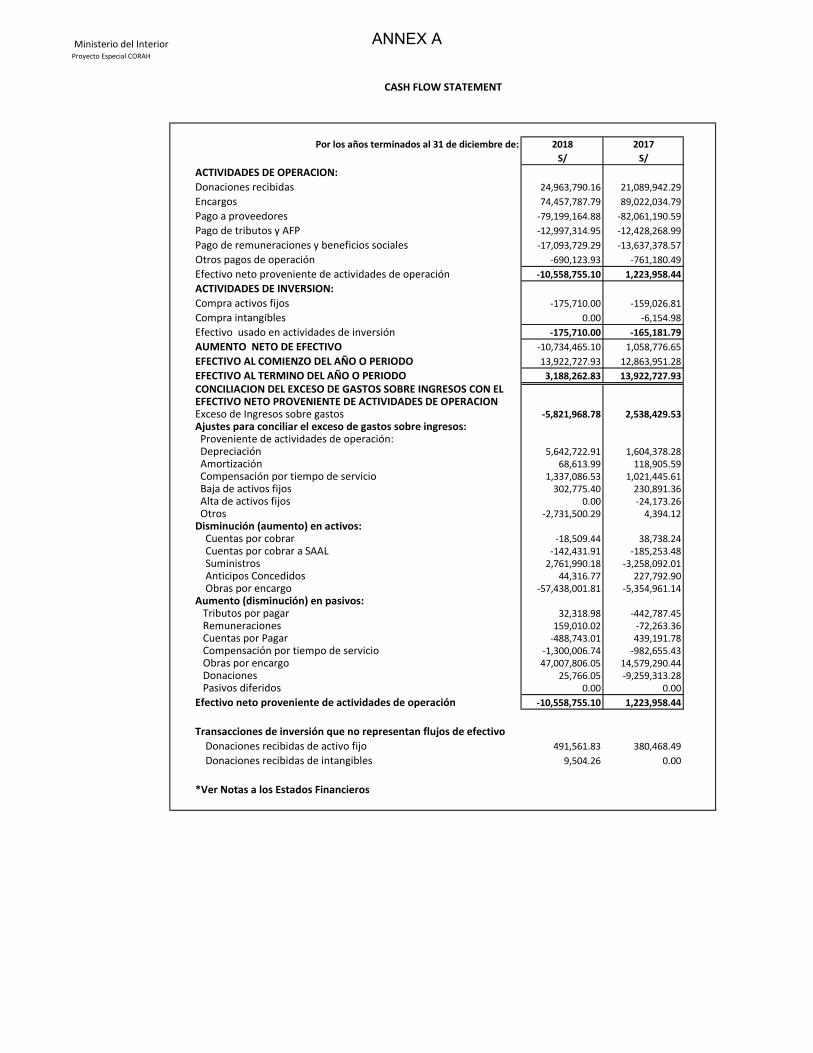

flows for the year ending on that date. See attached annexes "A” for references of financial

statements and budget of this USG financed project.

1.2.2. Financial audits (INL - DEVIDA funds): They will include the following:

a) Monthly: Review the monthly Fund Accountability Statement where received income is shown

(assignments) and the incurred costs (executed disbursements) recorded on a cash basis, which is an

accounting system other than the one based on accounting principles generally accepted in Peru.

b) Annual: Exam of the Fund Accountability Statement of funds provided by INL-

DEVIDA and managed by CORAH, during the period from January 1 to December

31, 2019, to be prepared and submitted on a cash basis, which is an accounting system

different than the one based on accounting principles generally accepted in Peru, in order

for auditors to express an opinion on whether the Fund Accountability Statement reasonably

presents, in all material aspects, the received income and the incurred costs in accordance

with the terms of understanding between INL-DEVIDA and CORAH.

1.2.3. Review of the project operations during 2019.

Monthly review of project operations during 2019, in accordance with the terms described

in Chapter 1.3.3. This review, which covers the administrative and operational systems of

CORAH, must be performed by auditors in accordance with a chronogram and an Annual

Work Plan developed and approved by the auditors and the INL officers. Auditors must

determine the defects and suggest improvements, establish the causes for deviations and

propose corrections, find the source of the problems and propose solutions. For this

purpose, they must conduct a study and an assessment of CORAH’s internal control in

order to obtain sufficient understanding of the design of relevant policies and procedures

and whether these policies and procedures have been applied to CORAH operations. As

part of this work, auditors must review the status of the actions taken as a result of the

findings and recommendations reported in previous audits (internal and external).

Solicitation 19PE5019Q0062

Page 10 of 50

Auditors are not required to discuss or express an opinion regarding whether the objectives,

goals and projections of eradication of CORAH were achieved or not. Besides, auditors are

not required to perform an audit of the CORAH "Results", since this is a responsibility of

the CORAH Executive Staff and the INL Narcotics Control Program Advisor.

1.3 METHODOLOGY AND SPECIFIC OBJECTIVES

1.3.1 Financial audits (INL resources):

a) Monthly

The monthly review of the financial statement prepared based on the operations of the

entire organization must be conducted in accordance with Auditing Standards

Generally Accepted in Peru. These standards require auditors to comply with ethical

requirements and to plan and perform the audit to obtain reasonable assurance that the

CORAH monthly financial statements do not contain material misstatements.

The monthly audit must include the implementation of procedures to obtain audit

evidence about the amounts and disclosures on the financial statements. The selected

procedures will depend on the auditors' judgment, including risk assessment to see if

the financial statements contain material misstatements, whether due to fraud or error.

When conducting the risk assessment, auditors must consider internal control of

CORAH in the preparation and reasonable presentation of the financial statements in

order to design audit procedures in accordance with the circumstances, but not for the

purpose of expressing an opinion on the effectiveness of the CORAH internal control.

The audit must also include an assessment of whether the applied accounting principles

are appropriate and whether the accounting estimates made by management are

reasonable, as well as an assessment of the overall presentation of the financial

statements.

CORAH’s administration will be responsible for preparing and reasonably present the

monthly financial statements in accordance with accounting principles generally

accepted in Peru. This responsibility includes: designing, implementing and

maintaining internal controls relevant to the preparation and reasonable presentation of

financial statements that are free from material misstatement, whether as a result of

fraud or error, selecting and applying appropriate accounting policies, and making

accounting estimates that are reasonable under the circumstances.

The objective of this monthly review is that auditors must issue Comment Letters

addressed to INL with copies to the CORAH Executive Management containing

significant matters that might have the monthly financial statements and internal control

aspects. They must also include suggestions on important matters of CORAH’s

operation that contribute to improve them.

Solicitation 19PE5019Q0062

Page 11 of 50

Because there is no International Accounting Standards dealing with non-profit

organizations, CORAH additionally uses the application of the accounting principles

applied in the United States of America (FASB – Financial Accounting Standards

Board), established under the Accounting National Council. The FASB standards

applied by CORAH are:

• FASB 116 "Accounting for Contributions Received and Contributions Made"

• FASB 117 "Financial Statements of Not- For- Profit Organizations"

The financial statements subject to monthly audits are prepared and presented in

accordance with FASB 117 and are as follows:

• Statement of financial position integral

• Statement of integral results and changes in net institutional equity

• Statement of cash flows, and

• Notes to the financial statements.

In this regard, the statement of CORAH’s financial position includes recording operations

of the following budgets:

CORAH:

- Executive Direction

- Operations Direction

- Administrative Direction

- Infrastructure Direction

- Interdiction Unit

Assignments (controlled in asset and liability accounts):

- Aviation Program and Construction Fund

- Police Program Fund

- Ports Program Fund

- Project and Development Fund

- INL - DEVIDA Fund

The number of samples and the amounts to be reviewed will be determined by the auditors,

covering at least 65 % of the expenditure in each budget. The auditors must necessarily

include, under a reasonable criterion, samples and amounts of the remuneration category,

as well as the goods and services categories.

b) Annual

The audit of the financial statements based on the operations of the entire organization

must be done in accordance with Auditing Standards Generally Accepted in Peru.

These standards require auditors to comply with ethical requirements, and plan and

perform the audit to obtain reasonable assurance that the CORAH annual financial

statements do not contain material misstatements.

Solicitation 19PE5019Q0062

Page 12 of 50

The annual audit must include the implementation of procedures to obtain audit

evidence about the amounts and disclosures on the financial statements. The selected

procedures depend on the auditors' judgment, including an assessment of the risk to see

if the financial statements contain material misstatements, as a result of fraud or error.

When conducting the risk assessment, auditors must consider CORAH’s internal

control at preparing and reasonably presenting the financial statements in order to

design audit procedures in accordance with the circumstances, but not to express an

opinion on CORAH’s internal control effectiveness. The audit must also include an

assessment of whether the accounting principles applied are appropriate and whether

the accounting estimates made by management are reasonable, as well as an assessment

of the overall presentation of the financial statements.

CORAH’s administration will be responsible for preparing and reasonably presenting

the monthly financial statements in accordance with accounting principles generally

accepted in Peru. This responsibility includes: designing, implementing and

maintaining internal control relevant to the preparation and reasonable presentation of

financial statements that are free from material misstatements, whether as a result of

fraud or error, selecting and applying appropriate accounting policies, and making

accounting estimates that are reasonable under the circumstances.

The objective of this annual review is make auditors express an opinion on whether

these financial statements reasonably present, in all material aspects, CORAH’s

financial position as of December 31, 2019, the results of its activities and its cash

flows for the year ending on that date; according to general accepted principles in Peru.

Because there is no International Accounting Standards dealing with non-profit

organizations, CORAH additionally uses the application of the accounting principles

applied in the United States of America (FASB), established under the Accounting

National Council. The FASB standards applied by CORAH are:

• FASB 116 "Accounting for Contributions Received and Contributions Made"

• FASB 117 "Financial Statements of Not- For- Profit Organizations"

The financial statements subjected to monthly audits are prepared and presented in

accordance with FASB 117 and are as follows:

• Statement of financial position

• Statement of integral results and changes in net institutional equity

• Statement of cash flows, and

• Notes to the financial statements.

In this regard, the statement of financial position CORAH includes recording

operations of the following budgets:

CORAH:

- Executive Direction

Solicitation 19PE5019Q0062

Page 13 of 50

- Operations Direction

- Administrative Direction

- Infrastructure Direction

- Interdiction Unit

Assignments (controlled in asset and liability accounts):

- Aviation Program and Construction Fund (*)

- Police Program Fund

- Ports Program Fund

- Project and Development Fund

- INL - DEVIDA Fund

(*) Liquidations supporting expenses related to construction works are sent to Lima and

reviewed by INL Finance. For purposes of the annual audit, it would be necessary that

auditors make selective examinations of construction costs incurred.

The number of samples and the amounts to be reviewed will be determined by the auditors,

covering at least 65 % of the expenditure in each budget. The auditors must necessarily

include, under a reasonable criterion, samples and amounts of the remuneration category,

as well as goods and services categories.

1.3.2. Financial audits (INL - DEVIDA funds):

a) Monthly

The monthly review of the Fund Accountability Statement of INL-DEVIDA and

managed by CORAH, where income received and expenses incurred each month are

shown, must be performed in accordance with Auditing Standards Generally Accepted

in Peru. These standards require auditors to plan and perform the audit to have

reasonable assurance about whether the revenues and costs recorded in monthly

accounts "Assignments" and "Assignments underway" do not contain material

representations.

The review of received income (Assignments) and incurred costs (Assignments

underway) will be conducted taking into consideration the following accounting

policies:

Income recognition: Funds received are recorded on the date they are deposited in the

bank account held by CORAH – DEVIDA.

Cost recognition: Costs incurred with funds provided by INL - DEVIDA are

recognized on the date of the expenditure.

b) Annual

Annual audit of the Fund Accountability Statement of INL-DEVIDA and managed by

CORAH during the period from January 1 to December 31, 2019 must be conducted

Solicitation 19PE5019Q0062

Page 14 of 50

in accordance with the Auditing Standards Generally Accepted in Peru. These standards

require auditors to plan and perform the audit to obtain reasonable assurance on whether

the accounting is free from material misstatement.

The audit must include the implementation of procedures to obtain audit evidence about

the amounts and disclosures on the Fund Accountability Statement. The selected

procedures will depend on the auditors' judgment, including risk assessment to see if

the Fund Accountability Statement contains material misstatements, whether due to

fraud or error. When conducting the risk assessment, auditors must consider CORAH’s

internal control in preparing and reasonably presenting the Fund Accountability

Statement in order to design audit procedures in accordance with the circumstances,

but not for the purpose of expressing an opinion on the effectiveness of CORAH’s

internal control. The audit must also include an assessment of whether the accounting

principles applied are appropriate and whether the accounting estimates made by

management are reasonable, as well as an assessment of the overall presentation of the

Fund Accountability Statement.

CORAH’s administration will be responsible for preparing and reasonably presenting

the Fund Accountability Statement on a cash basis, which is an accounting system

different than the one based on accounting principles generally accepted in Peru. This

responsibility includes: designing, implementing and maintaining internal controls

relevant to the preparation and reasonable presentation of the Fund Accountability

Statement so they are free from material representations, whether as a result of fraud

or error, selecting and applying appropriate accounting policies under the

circumstances.

The objective of this audit is receive from auditors an opinion whether the Fund

Accountability Statement reasonably presents, in all its material aspects, received

income and incurred costs in accordance with the existing terms of understanding

between INL-DEVIDA and CORAH.

At a minimum for the monthly and annual audit of the Fund Accountability Statement,

the auditor should:

Examine the Fund Accountability Statements, including the budgeted amounts by

category and accounts, the revenues received for the period covered by the audit, as

well as the costs reported by CORAH as incurred during that period. The revenues

received, less the costs incurred, after considering any reconciling items, should

reconcile with the balance of cash-on-hand and/or in bank accounts.

Identify and quantify any questionable cost.

Questionable costs are referred to:

Solicitation 19PE5019Q0062

Page 15 of 50

(a) Ineligible costs which are explicitly questionable because they are unreasonable

and not related with the project’s operations, or prohibited by applicable laws

and/or internal CORAH directives.

(b) Unsupported costs that are not supported with adequate documentation or did not

have the required approvals or authorizations prior to their execution.

All questionable costs resulting from instances of noncompliance with applicable laws

and/or internal CORAH directives should be reported.

1.3.3. Review of project operations during 2019

The auditors’ work will be conducted in accordance with International Standards for the

practice of independent auditing, in order to detect weaknesses by which the design or

implementation of the specific internal control elements does not reduce the risk to a

moderately low level, or errors or frauds that may occur and that are not detected on time

by management, while executing its normal duties.

Auditors must:

a) Develop an Annual Audit Plan including activities to perform. This plan must meet

the following objectives:

Assess design, scope and operation of the internal control system.

Assess effectiveness and efficiency of operations.

Assess compliance with the legal provisions and internal directives governing in

CORAH.

Assess financial information reliability.

Assess the performance of computer systems and mechanisms established by

CORAH for the safety thereof.

Perform ongoing monitoring of the implementation of recommendations from external

and internal audits proposed by INL.

The Plan must include the control activities to be performed on operations within the period

from January 1 to December 31, 2019. The implementation of this plan must reach all

areas of the organization, regardless of the hierarchical level and/or geographical area in

which it operates.

b) Execute control actions previously established in the Annual Audit Plan. Auditors must

perform –but not limited to- the following procedures:

1. Administrative Direction:

a) Logistics Sub Direction:

Solicitation 19PE5019Q0062

Page 16 of 50

Verify that acquisitions are made to suppliers included in the Suppliers Registry.

Verify the physical existence of the suppliers included in the Suppliers Registry.

Verify if the suppliers have the storage and sufficient stock of the products

registered in the Suppliers Registry.

Verify the tax situation of the suppliers included in the Suppliers Registry.

Verify if the Suppliers Registry is updated.

Verify that the prices of products quoted by suppliers are related and reasonable

according to market prices.

Verify that the product Kardex are updated.

Physically verify some products in storage and cross with the Kardex.

Physically observe inventories of supplies and fixed assets scheduled by the

Property Control Area.

Verify that the policies established in the Procedures Manual of the Logistic Sub

Direction are accomplished.

b) Human Resources Sub Direction:

On a random basis, check the staff C.V. to verify if it is according to the profile

established for the position.

Verify if a public contest was called to fill the vacancy of a job position.

Verify staff attendance.

Physically verify staff attendance.

Verify that the hours worked according to the time marker clock are the same as

those included in the payroll.

Verify the existence of overtime and if these have been authorized.

Verify the payment of overtime or compensation of these with rest days.

Verify each of the concepts included in the payroll.

Verify the calculation of contributions and 5th Income tax category.

Verify the Liquidations for Service Time of the retired personnel.

Determine if the calculation of the CTS deposited in banks was properly

determined.

Verify that the policies established in the Manual of Human Resources Sub

Direction are accomplished.

c) Accounting Sub Direction:

Review monthly bank reconciliations of account.

Perform unannounced and surprise CORAH petty cash audits.

Assess software provided by the bank BBVA Continental, which allows access

to consult balances and activities of the CORAH accounts, to make payments

through funds transfers.

Verify that the policies established in the Manual of Accounting Sub Direction

are accomplished.

Solicitation 19PE5019Q0062

Page 17 of 50

d) Information Technology Area:

Perform a software and security evaluation of SIA (Sistema Integrado de

Administración) which has the objective of supporting the administrative

processes, providing agility, efficiency and integrity in the management of

information.

Verify that the policies established in the Manual of the Information Technology

Area are accomplished.

2. Operations Direction:

Include visits to the operational units (camps) where eradication labors are

conducted. In order to visit the operational units, indispensable arrangements

will be made with INL in order to count on the necessary air or ground support,

if applicable.

Physically verify the products in storage and cross this information with the

balance of the physical kardex.

Verify the existence of expired products.

Verify if the brand and quantity of products received at camps correspond with

what was requested in the Purchase Order.

Check the inventory outputs of food for consumption (cold ranch and food

preparation).

Verify that products used in the preparation of food, according to the recipe,

match the quantities that came out of the storage, taking into account the number

of servings.

Verify that the menu of the week has the approval of the responsible Doctor.

Verify the product outputs for the cold ranch against the Eradication Operations

Daily Reports.

Physically verify the medicines in stock with the balance of kardex.

Check if there are expired medicines.

Verify the medicine outputs from storage against the Medicine Delivery Report

signed by the patient.

Check if the people who signed the Medicine Delivery Report actually received

the medications.

Verify that all workers have their medical exams established by law.

Verify the Staff Attendance Control Report (tareos).

Physically verify if workers are at their job positions.

3. Infrastructure Direction

Review of the Construction Projects Technical Files (Expediente Técnico) of the

works executed in the year.

Review and evaluation of Construction Projects Budgets.

Evaluate the selection and evaluation of construction service providers.

Physically verify the contractor's facilities.

Solicitation 19PE5019Q0062

Page 18 of 50

Verify if the contractor has enough experience to develop the construction

projects.

Evaluate the reasonableness of the value of the construction projects with the

participation of a construction specialist (engineer).

Verify market prices used in the Construction Projects Budget.

Perform physical verification of the works and determine if they have been

executed according to specifications on Construction Projects Technical Files,

contract, as well as the technical and economic contractor’s proposal.

Verify that the policies established in the Manual of the Infrastructure Direction

are accomplished.

c) Assess to what extent the control observations by previous external auditors are

complied with.

d) If necessary, assist INL staff during monitoring visits to CORAH.

e) Support the Accounting Sub Direction in matters related to accountancy.

f) Prepare audit reports to submit to INL, with copy to CORAH’s Executive Director.

These reports must contain matters arising from the planned and implemented control

actions.

1.4 AUDIT REPORTS

The monthly reports must be issued in electronic format only (Word and PDF), in Spanish

for the CORAH Executive Management, and in Spanish and English for INL. The annual

report must be issued in printed and electronic format (Word and PDF), in Spanish for the

CORAH Executive Management, and in Spanish and English for INL.

The reports are as follows:

a) Comment Letters containing important issues and control matters arising as a

result of the review of the monthly (11) and annual (01) Financial Statements. They

must also include suggestions on important issues that help improve CORAH’s

operability.

b) An annual report containing the financial statements as of December 31, 2019, prepared

on the basis of CORAH’s operations to be conducted in the year, as well as the audit

opinion on whether the financial statements reasonably present, in all material aspects,

the CORAH’s financial situation as of December 31, 2019, and the results of its

operations and its cash flows for the year ending on that date, in accordance with

accounting principles generally accepted in Peru.

Solicitation 19PE5019Q0062

Page 19 of 50

c) Comment Letters containing important issues and control issues arising as a result of

the review of the monthly (11) and annual (01) Fund Accountability Statement. They

must also include suggestions on important issues that help to improve the registration,

control, execution and reporting of costs incurred by CORAH with funds provided

by INL - DEVIDA.

d) Annual Report containing the Fund Accountability Statement for the period January 01

through December 31, 2019, prepared based on the received income and incurred

expenses by CORAH with funds provided by INL – DEVIDA, as well as the

auditors’ opinion as to whether the Fund Accountability Statement for the period

January 01 through December 31, 2019, reasonably presents, in all material aspects,

the received income and incurred costs of the Agreement signed between DEVIDA

and CORAH and prepared on a cash basis, which is an accounting system different

than the one based on accounting principles generally accepted in Peru.

e) Reports as a result of reviewing project operations during 2019, based on the Annual

Audit Plan. This report must contain the reportable conditions, including the

identification of material weaknesses and findings that are conferred in the reportable

conditions, as well as material weaknesses in the internal structure, as a result of the

executions of reviewing project operations.

The findings in this report must include a description of the conditions (what is) and

the criterion (what it should be). Moreover, the cause (why it happened) and effect

(what was the loss caused for not complying with the criteria) must be included in the

report of conclusions if they can be easily determined. In addition and if applicable,

the conclusions must contain recommendations to correct the causes and conditions.

In the absence of internal controls implemented by CORAH for any point of the

agreed procedures, auditors must provide broad recommendations for their

implementation.

Auditors must identify at least the conditions, criteria and possible impacts, in order to

provide sufficient information to INL. This way, we can determine the effect and the

cause to take timely and appropriate corrective actions.

The report must also contain, after each recommendation, the views of the managers

responsible and related to the auditors’ findings, as well as measures taken by

management to implement such recommendations. If possible, the views of the

managers must be obtained in writing. In the event that the managers’ comments

contradict the results, findings or recommendations and that these are not valid at the

auditors’ discretion, the reasons why auditors reject these divergences must be indicated

after the managers’ comments. Conversely, the auditors must modify their report if they

believe the managers’ comments are valid.

These reports must include all findings, grounds or evidence obtained, leading to

conclude that a fraud or an illegal act has occurred or is about to occur and must quantify

its effect. These reports must include identification of all questionable costs, if any, as

Solicitation 19PE5019Q0062

Page 20 of 50

the result of a fraud or an illegal act, regardless if such found questionable costs have

been corrected or if managers agree with them or not.

In the report of material fraud, illegal acts, or other noncompliance, auditors must place

their findings in proper perspective in order to give the reader a basis to judge the

impact and consequences of these conditions.

If auditors conclude that there is enough evidence of a fraud or an illegal act, they must

contact the INL relevant officials and exercise due professional care in monitoring the

indicators of this potential fraud or illegal act, in such a way as not to interfere with

potential future investigations, legal proceedings, or both.

These reports must also contain the auditors’ comment on the status of the

recommendations from previous audits. Auditors must review and report on the

status of actions taken as a result of the findings and recommendations reported by

previous audits. When corrective actions have not been conducted and deficiencies

remain unresolved until the current audit period, and if these deficiencies are again

reported by the current audit, auditors only need to briefly describe the previous

finding.

1.5. WORK TEAM

The Auditors must assign a Firm Partner as the one responsible for the audit, while another

Partner will act as a consulting partner in charge of performed work quality control.

It is essential for auditors to appoint, full-time for not less than 15 days a month, the audit

staff deemed appropriate for planning, directing and executing fieldwork. This term is

required because CORAH and INL need a personalized service.

Due to unexpected circumstances and if it is necessary to replace any member of the team,

the substitute will have the same category and experience of the member that leaves.

1.6. TERMS OF UNDERSTANDING

The Auditors will state the price of the audit as an “all cost “, taking into account the

extension of the labors described in the scope or work and contract objective.

Costs involved in transporting Auditors from the city of Pucallpa to various CORAH

operating units (camps) will be assumed by INL.

If necessary, the auditors will meet INL Office staff in order to get a general idea of the

work. The auditors may decide to conduct a field visit to the CORAH facilities in Pucallpa

in order to assess the extent of their work and estimate their professional fees accurately.

The auditors will assume the costs of this field visit and its date will be coordinated between

INL and CORAH.

Solicitation 19PE5019Q0062

Page 21 of 50

CORAH is responsible for ensuring that all records are available, that all operations and

accounting adjustments are executed and should display great collaboration with auditors,

performing the necessary actions to let them accomplish their work successfully.

Professional fees will be paid monthly by INL after the submission and review of the

corresponding audit reports and invoice. Invoices shall be submitted electronically to

[email protected] Embajada de los Estados Unidos de America - FMO / DBO Avenida La Encalada block 17 s / n, Surco RUC: 20293588776 From Monday to Friday between 09:00 hrs and 14:00 hrs. by the employees entrance in Av. Lima Polo cuadra 2 s/n, Surco.

2.0 DELIVERABLES The Contractor shall comply with the following Delivery Schedule: Draft Report in English. Two (2) copies delivered to the Contracting Officer’s Representative. The Contracting Officer’s Representative will provide the Contractor with comments/request for revision within 15 days of receipt of the draft report. Final Report in English. Two (2) copies delivered to the Contracting Officer’s Representative not later than 15 days after the approval of the draft report. 3.0 QUALITY ASSURANCE AND SURVEILLANCE PLAN (QASP) This plan provides an effective method to promote satisfactory contractor performance. The QASP provides a method for the Contracting Officer's Representative (COR) to monitor Contractor performance, advise the Contractor of unsatisfactory performance, and notify the Contracting Officer of continued unsatisfactory performance. The Contractor, not the Government, is responsible for management and quality control to meet the terms of the contract. The role of the Government is to monitor quality to ensure that contract standards are achieved. Performance Objective Scope of Work Para Performance Threshold Services. Performs all independent financial audit for Embassy INL Section set forth in the scope of work.

5. thru 19.

All required services are performed and no more than one (1) customer complaint is received per month.

Contract Clauses FAR 52.212-4 CONTRACT TERMS AND CONDITIONS – COMMERICAL ITEMS (OCT

2018) and (DEVIATION 2017-02) (JUNE 2017),is incorporated by reference. (See SF-1449,

block 27a). 52.212-5 Contract Terms and Conditions Required To Implement Statutes or Executive Orders - Commercial Items (OCT 2018) and (Deviation 2017-02) (June 2017) (a) The Contractor shall comply with the following Federal Acquisition Regulation (FAR) clauses, which are incorporated in this contract by reference, to implement provisions of law or Executive orders applicable to acquisitions of commercial items: (1) 52.203-19, Prohibition on Requiring Certain Internal Confidentiality Agreements or Statements (Jan 2017) (section 743 of Division E, Title VII, of the Consolidated and Further Continuing Appropriations Act, 2015 (Pub. L. 113-235) and its successor provisions in subsequent appropriations acts (and as extended in continuing resolutions)). (2) 52.209-10, Prohibition on Contracting with Inverted Domestic Corporations (Nov 2015). (3) 52.233-3, Protest After Award (Aug 1996) (31 U.S.C. 3553). (4) 52.233-4, Applicable Law for Breach of Contract Claim (Oct 2004)(Public Laws 108-77 and 108-78 (19 U.S.C. 3805 note)). (b) The Contractor shall comply with the FAR clauses in this paragraph (b) that the Contracting Officer has indicated as being incorporated in this contract by reference to implement provisions of law or Executive orders applicable to acquisitions of commercial items: [Contracting Officer check as appropriate.] __ (1) 52.203-6, Restrictions on Subcontractor Sales to the Government (Sept 2006), with Alternate I (Oct 1995) (41 U.S.C. 4704 and 10 U.S.C. 2402). __ (2) 52.203-13, Contractor Code of Business Ethics and Conduct (Oct 2015) (41 U.S.C. 3509)). __ (3) 52.203-15, Whistleblower Protections under the American Recovery and Reinvestment Act of 2009 (June 2010) (Section 1553 of Pub. L. 111-5). (Applies to contracts funded by the American Recovery and Reinvestment Act of 2009.) _x_ (4) 52.204-10, Reporting Executive Compensation and First-Tier Subcontract Awards (Oct 2016) (Pub. L. 109-282) (31 U.S.C. 6101 note). __ (5) [Reserved]. __ (6) 52.204-14, Service Contract Reporting Requirements (Oct 2016) (Pub. L. 111-117, section 743 of Div. C). __ (7) 52.204-15, Service Contract Reporting Requirements for Indefinite-Delivery Contracts (Oct 2016) (Pub. L. 111-117, section 743 of Div. C). __ (8) 52.209-6, Protecting the Government’s Interest When Subcontracting with Contractors Debarred, Suspended, or Proposed for Debarment. (Oct 2015) (31 U.S.C. 6101 note). __ (9) 52.209-9, Updates of Publicly Available Information Regarding Responsibility Matters (Jul 2013) (41 U.S.C. 2313). __ (10) [Reserved]. __ (11)(i) 52.219-3, Notice of HUBZone Set-Aside or Sole-Source Award (Nov 2011) (15 U.S.C. 657a). __ (ii) Alternate I (Nov 2011) of 52.219-3. __ (12)(i) 52.219-4, Notice of Price Evaluation Preference for HUBZone Small Business Concerns (Oct 2014) (if the offeror elects to waive the preference, it shall so indicate in its offer) (15 U.S.C. 657a). __ (ii) Alternate I (Jan 2011) of 52.219-4. __ (13) [Reserved] __ (14)(i) 52.219-6, Notice of Total Small Business Set-Aside (Nov 2011) (15 U.S.C. 644). __ (ii) Alternate I (Nov 2011). __ (iii) Alternate II (Nov 2011).

__ (15)(i) 52.219-7, Notice of Partial Small Business Set-Aside (June 2003) (15 U.S.C. 644). __ (ii) Alternate I (Oct 1995) of 52.219-7. __ (iii) Alternate II (Mar 2004) of 52.219-7. __ (16) 52.219-8, Utilization of Small Business Concerns (Nov 2016) (15 U.S.C. 637(d)(2) and (3)). __ (17)(i) 52.219-9, Small Business Subcontracting Plan (Jan 2017) (15 U.S.C. 637(d)(4)). __ (ii) Alternate I (Nov 2016) of 52.219-9. __ (iii) Alternate II (Nov 2016) of 52.219-9. __ (iv) Alternate III (Nov 2016) of 52.219-9. __ (v) Alternate IV (Nov 2016) of 52.219-9. __ (18) 52.219-13, Notice of Set-Aside of Orders (Nov 2011) (15 U.S.C. 644(r)). __ (19) 52.219-14, Limitations on Subcontracting (Jan 2017) (15 U.S.C. 637(a)(14)). __ (20) 52.219-16, Liquidated Damages.Subcon-tracting Plan (Jan 1999) (15 U.S.C. 637(d)(4)(F)(i)). __ (21) 52.219-27, Notice of Service-Disabled Veteran-Owned Small Business Set-Aside (Nov 2011) (15 U.S.C. 657 f). __ (22) 52.219-28, Post Award Small Business Program Representation (Jul 2013) (15 U.S.C. 632(a)(2)). __ (23) 52.219-29, Notice of Set-Aside for, or Sole Source Award to, Economically Disadvantaged Women-Owned Small Business Concerns (Dec 2015) (15 U.S.C. 637(m)). __ (24) 52.219-30, Notice of Set-Aside for, or Sole Source Award to, Women-Owned Small Business Concerns Eligible Under the Women-Owned Small Business Program (Dec 2015) (15 U.S.C. 637(m)). __ (25) 52.222-3, Convict Labor (June 2003) (E.O. 11755). _x_(26) 52.222-19, Child Labor. Cooperation with Authorities and Remedies (Oct 2016) (E.O. 13126). __ (27) 52.222-21, Prohibition of Segregated Facilities (Apr 2015). __ (28) 52.222-26, Equal Opportunity (Sept 2016) (E.O. 11246). __ (29) 52.222-35, Equal Opportunity for Veterans (Oct 2015)(38 U.S.C. 4212). __ (30) 52.222-36, Equal Opportunity for Workers with Disabilities (Jul 2014) (29 U.S.C. 793). __ (31) 52.222-37, Employment Reports on Veterans (Feb 2016) (38 U.S.C. 4212). __ (32) 52.222-40, Notification of Employee Rights Under the National Labor Relations Act (Dec 2010) (E.O. 13496). _x_ (33)(i) 52.222-50, Combating Trafficking in Persons (Mar 2015) (22 U.S.C. chapter 78 and E.O. 13627). __ (ii) Alternate I (Mar 2015) of 52.222-50 (22 U.S.C. chapter 78 and E.O. 13627). _x_ (34) 52.222-54, Employment Eligibility Verification (Oct 2015). (Executive Order 12989). (Not applicable to the acquisition of commercially available off-the-shelf items or certain other types of commercial items as prescribed in 22.1803.) __ (35)(i) 52.223-9, Estimate of Percentage of Recovered Material Content for EPA–Designated Items (May 2008) (42 U.S.C. 6962(c)(3)(A)(ii)). (Not applicable to the acquisition of commercially available off-the-shelf items.) __ (ii) Alternate I (May 2008) of 52.223-9 (42 U.S.C. 6962(i)(2)(C)). (Not applicable to the acquisition of commercially available off-the-shelf items.) __ (36) 52.223-11, Ozone-Depleting Substances and High Global Warming Potential Hydrofluorocarbons (Jun 2016) (E.O. 13693). __ (37) 52.223-12, Maintenance, Service, Repair, or Disposal of Refrigeration Equipment and Air Conditioners (Jun 2016) (E.O. 13693). __ (38)(i) 52.223-13, Acquisition of EPEAT®-Registered Imaging Equipment (Jun 2014) (E.O.s 13423 and 13514). __ (ii) Alternate I (Oct 2015) of 52.223-13. __ (39)(i) 52.223-14, Acquisition of EPEAT®-Registered Televisions (Jun 2014) (E.O.s 13423 and 13514). __ (ii) Alternate I (Jun 2014) of 52.223-14.

__ (40) 52.223-15, Energy Efficiency in Energy-Consuming Products (Dec 2007) (42 U.S.C. 8259b). _x_ (41)(i) 52.223-16, Acquisition of EPEAT®-Registered Personal Computer Products (Oct 2015) (E.O.s 13423 and 13514). __ (ii) Alternate I (Jun 2014) of 52.223-16. _x_ (42) 52.223-18, Encouraging Contractor Policies to Ban Text Messaging While Driving (Aug 2011) (E.O. 13513). __ (43) 52.223-20, Aerosols (Jun 2016) (E.O. 13693). __ (44) 52.223-21, Foams (Jun 2016) (E.O. 13693). __ (45)(i) 52.224-3, Privacy Training (JAN 2017) (5 U.S.C. 552a). __ (ii) Alternate I (JAN 2017) of 52.224-3. __ (46) 52.225-1, Buy American.Supplies (May 2014) (41 U.S.C. chapter 83). __ (47)(i) 52.225-3, Buy American.Free Trade Agreements.Israeli Trade Act (May 2014) (41 U.S.C. chapter 83, 19 U.S.C. 3301 note, 19 U.S.C. 2112 note, 19 U.S.C. 3805 note, 19 U.S.C. 4001 note, Pub. L. 103-182, 108-77, 108-78, 108-286, 108-302, 109-53, 109-169, 109-283, 110-138, 112-41, 112-42, and 112-43. __ (ii) Alternate I (May 2014) of 52.225-3. __ (iii) Alternate II (May 2014) of 52.225-3. __ (iv) Alternate III (May 2014) of 52.225-3. _x_ (48) 52.225-5, Trade Agreements (Oct 2016) (19 U.S.C. 2501, et seq., 19 U.S.C. 3301 note). _x_ (49) 52.225-13, Restrictions on Certain Foreign Purchases (June 2008) (E.O.’s, proclamations, and statutes administered by the Office of Foreign Assets Control of the Department of the Treasury). __ (50) 52.225-26, Contractors Performing Private Security Functions Outside the United States (Oct 2016) (Section 862, as amended, of the National Defense Authorization Act for Fiscal Year 2008; 10 U.S.C. 2302 Note). __ (51) 52.226-4, Notice of Disaster or Emergency Area Set-Aside (Nov 2007) (42 U.S.C. 5150). __ (52) 52.226-5, Restrictions on Subcontracting Outside Disaster or Emergency Area (Nov 2007) (42 U.S.C. 5150). _x_ (53) 52.232-29, Terms for Financing of Purchases of Commercial Items (Feb 2002) (41 U.S.C. 4505, 10 U.S.C. 2307(f)). __ (54) 52.232-30, Installment Payments for Commercial Items (Jan 2017) (41 U.S.C. 4505, 10 U.S.C. 2307(f)). _x_ (55) 52.232-33, Payment by Electronic Funds Transfer.System for Award Management (Jul 2013) (31 U.S.C. 3332). __ (56) 52.232-34, Payment by Electronic Funds Transfer.Other than System for Award Management (Jul 2013) (31 U.S.C. 3332). __ (57) 52.232-36, Payment by Third Party (May 2014) (31 U.S.C. 3332). __ (58) 52.239-1, Privacy or Security Safeguards (Aug 1996) (5 U.S.C. 552a). __ (59) 52.242-5, Payments to Small Business Subcontractors (Jan 2017)(15 U.S.C. 637(d)(12)). __ (60)(i) 52.247-64, Preference for Privately Owned U.S.-Flag Commercial Vessels (Feb 2006) (46 U.S.C. Appx. 1241(b) and 10 U.S.C. 2631). __ (ii) Alternate I (Apr 2003) of 52.247-64. (c) The Contractor shall comply with the FAR clauses in this paragraph (c), applicable to commercial services, that the Contracting Officer has indicated as being incorporated in this contract by reference to implement provisions of law or Executive orders applicable to acquisitions of commercial items: [Contracting Officer check as appropriate.] __ (1) 52.222-17, Nondisplacement of Qualified Workers (May 2014)(E.O. 13495). __ (2) 52.222-41, Service Contract Labor Standards (May 2014) (41 U.S.C. chapter 67). __ (3) 52.222-42, Statement of Equivalent Rates for Federal Hires (May 2014) (29 U.S.C. 206 and 41 U.S.C. chapter 67).

__ (4) 52.222-43, Fair Labor Standards Act and Service Contract Labor Standards-Price Adjustment (Multiple Year and Option Contracts) (May 2014) (29 U.S.C. 206 and 41 U.S.C. chapter 67). __ (5) 52.222-44, Fair Labor Standards Act and Service Contract Labor Standards.Price Adjustment (May 2014) (29 U.S.C. 206 and 41 U.S.C. chapter 67). __ (6) 52.222-51, Exemption from Application of the Service Contract Labor Standards to Contracts for Maintenance, Calibration, or Repair of Certain Equipment.Requirements (May 2014) (41 U.S.C. chapter 67). __ (7) 52.222-53, Exemption from Application of the Service Contract Labor Standards to Contracts for Certain Services.Requirements (May 2014) (41 U.S.C. chapter 67). __ (8) 52.222-55, Minimum Wages Under Executive Order 13658 (Dec 2015). __ (9) 52.222-62, Paid Sick Leave Under Executive Order 13706 (JAN 2017) (E.O. 13706). __ (10) 52.226-6, Promoting Excess Food Donation to Nonprofit Organizations (May 2014) (42 U.S.C. 1792). __ (11) 52.237-11, Accepting and Dispensing of $1 Coin (Sept 2008) (31 U.S.C. 5112(p)(1)). (d) Comptroller General Examination of Record. The Contractor shall comply with the provisions of this paragraph (d) if this contract was awarded using other than sealed bid, is in excess of the simplified acquisition threshold, and does not contain the clause at 52.215-2, Audit and Records.Negotiation. (1) The Comptroller General of the United States, or an authorized representative of the Comptroller General, shall have access to and right to examine any of the Contractor’s directly pertinent records involving transactions related to this contract. (2) The Contractor shall make available at its offices at all reasonable times the records, materials, and other evidence for examination, audit, or reproduction, until 3 years after final payment under this contract or for any shorter period specified in FAR subpart 4.7, Contractor Records Retention, of the other clauses of this contract. If this contract is completely or partially terminated, the records relating to the work terminated shall be made available for 3 years after any resulting final termination settlement. Records relating to appeals under the disputes clause or to litigation or the settlement of claims arising under or relating to this contract shall be made available until such appeals, litigation, or claims are finally resolved. (3) As used in this clause, records include books, documents, accounting procedures and practices, and other data, regardless of type and regardless of form. This does not require the Contractor to create or maintain any record that the Contractor does not maintain in the ordinary course of business or pursuant to a provision of law. (e)(1) Notwithstanding the requirements of the clauses in paragraphs (a), (b), (c), and (d) of this clause, the Contractor is not required to flow down any FAR clause, other than those in this paragraph (e)(1) in a subcontract for commercial items. Unless otherwise indicated below, the extent of the flow down shall be as required by the clause. (i) 52.203-13, Contractor Code of Business Ethics and Conduct (Oct 2015) (41 U.S.C. 3509). (ii) 52.203-19, Prohibition on Requiring Certain Internal Confidentiality Agreements or Statements (Jan 2017) (section 743 of Division E, Title VII, of the Consolidated and Further Continuing Appropriations Act, 2015 (Pub. L. 113-235) and its successor provisions in subsequent appropriations acts (and as extended in continuing resolutions)). (iii) 52.219-8, Utilization of Small Business Concerns (Nov 2016) (15 U.S.C. 637(d)(2) and (3)), in all subcontracts that offer further subcontracting opportunities. If the subcontract (except subcontracts to small business concerns) exceeds $700,000 ($1.5 million for construction of any public facility), the subcontractor must include 52.219-8 in lower tier subcontracts that offer subcontracting opportunities. (iv) 52.222-17, Nondisplacement of Qualified Workers (May 2014) (E.O. 13495). Flow down required in accordance with paragraph (l) of FAR clause 52.222-17. (v) 52.222-21, Prohibition of Segregated Facilities (Apr 2015) (vi) 52.222-26, Equal Opportunity (Sept 2016) (E.O. 11246). (vii) 52.222-35, Equal Opportunity for Veterans (Oct 2015) (38 U.S.C. 4212). (viii) 52.222-36, Equal Opportunity for Workers with Disabilities (Jul 2014) (29 U.S.C. 793).

(ix) 52.222-37, Employment Reports on Veterans (Feb 2016) (38 U.S.C. 4212) (x) 52.222-40, Notification of Employee Rights Under the National Labor Relations Act (Dec 2010) (E.O. 13496). Flow down required in accordance with paragraph (f) of FAR clause 52.222-40. (xi) 52.222-41, Service Contract Labor Standards (May 2014) (41 U.S.C. chapter 67). (xii) __(A) 52.222-50, Combating Trafficking in Persons (Mar 2015) (22 U.S.C. chapter 78 and E.O 13627). __(B) Alternate I (Mar 2015) of 52.222-50 (22 U.S.C. chapter 78 and E.O 13627). (xiii) 52.222-51, Exemption from Application of the Service Contract Labor Standards to Contracts for Maintenance, Calibration, or Repair of Certain Equipment-Requirements (May 2014) (41 U.S.C. chapter 67). (xiv) 52.222-53, Exemption from Application of the Service Contract Labor Standards to Contracts for Certain Services-Requirements (May 2014) (41 U.S.C. chapter 67). (xv) 52.222-54, Employment Eligibility Verification (Oct 2015) (E.O. 12989). (xvi) 52.222-55, Minimum Wages Under Executive Order 13658 (Dec 2015). (xvii) 52.222-62, Paid Sick Leave Under Executive Order 13706 (Jan 2017) (E.O. 13706). (xviii)(A) 52.224-3, Privacy Training (Jan 2017) (5 U.S.C. 552a). (B) Alternate I (Jan 2017) of 52.224-3. (xix) 52.225-26, Contractors Performing Private Security Functions Outside the United States (Oct 2016) (Section 862, as amended, of the National Defense Authorization Act for Fiscal Year 2008; 10 U.S.C. 2302 Note). (xx) 52.226-6, Promoting Excess Food Donation to Nonprofit Organizations (May 2014) (42 U.S.C. 1792). Flow down required in accordance with paragraph (e) of FAR clause 52.226-6. (xxi) 52.247-64, Preference for Privately Owned U.S.-Flag Commercial Vessels (Feb 2006) (46 U.S.C. Appx. 1241(b) and 10 U.S.C. 2631). Flow down required in accordance with paragraph (d) of FAR clause 52.247-64. (2) While not required, the Contractor may include in its subcontracts for commercial items a minimal number of additional clauses necessary to satisfy its contractual obligations. (End of clause)

Addendum To Contract Clauses FAR And DOSAR Clauses Not Prescribed In Part 12

52.252-2 CLAUSES INCORPORATED BY REFERENCE (FEB 1998)

This contract incorporates one or more clauses by reference, with the same force and effect as if

they were given in full text. Upon request, the Contracting Officer will make their full text

available. Also, the full text of a clause may be accessed electronically at:

(a) The Contracting Officer may designate in writing one or more Government

employees, by name or position title, to take action for the Contracting Officer under this

contract. Each designee shall be identified as a Contracting Officer’s Representative (COR).

Such designation(s) shall specify the scope and limitations of the authority so delegated;

provided, that the designee shall not change the terms or conditions of the contract, unless the

COR is a warranted Contracting Officer and this authority is delegated in the designation.

(b) The COR for this contract is The INL Program Specialist

652.242-73 AUTHORIZATION AND PERFORMANCE (AUG 1999)

(a) The Contractor warrants the following:

(1) That is has obtained authorization to operate and do business in the

country or countries in which this contract will be performed;

(2) That is has obtained all necessary licenses and permits required to perform

this contract; and,

Solicitation 19PE5019Q0062

Page 29 of 50

(3) That it shall comply fully with all laws, decrees, labor standards, and

regulations of said country or countries during the performance of this contract.

(b) If the party actually performing the work will be a subcontractor or joint venture

partner, then such subcontractor or joint venture partner agrees to the requirements of paragraph

(a) of this clause.

652.229-70 EXCISE TAX EXEMPTION STATEMENT FOR CONTRACTORS WITHIN THE UNITED STATES (JUL 1988)

This is to certify that the item(s) covered by this contract is/are for export solely for the use of the U.S. Foreign Service Post identified in the contract schedule.

The Contractor shall use a photocopy of this contract as evidence of intent to export. Final proof

of exportation may be obtained from the agent handling the shipment. Such proof shall be

accepted in lieu of payment of excise tax.

Solicitation 19PE5019Q0062

Page 30 of 50

SECTION 3 - SOLICITATION PROVISIONS

Solicitation Provisions FAR 52.212-1, INSTRUCTIONS TO OFFERORS -- COMMERCIAL ITEMS (OCT 2018) is

incorporated by reference. (See SF-1449, block 27a).

ADDENDUM TO 52.212-1

A. Summary Of Instructions. Each offer must consist of the following:

A.1. A completed solicitation, in which the SF-1449 cover page (blocks 12, 17, 19-24, and 30

as appropriate), and Section 1 has been filled out.

The Offeror shall include Defense Base Act (DBA) insurance premium costs covering

employees. The offeror may obtain DBA insurance directly from any Department of Labor

approved providers at the DOL website at http://www.dol.gov/owcp/dlhwc/lscarrier.htm ]

A.2. Documented information demonstrating the offeror’s/quoter’s ability to perform,

including:

(1) The professional qualifications of the certifying auditors;

(2) Identification of auditing standards, methods and techniques employed to execute

the financial audit;

(3) Evidence that the offeror/quoter operates an established business with a

permanent address and telephone listing;

(4) List of clients over the past ____8_____ years, demonstrating prior experience

with relevant past performance information and references (provide dates of contracts, places of

performance, value of contracts, contact names, telephone and fax numbers and email addresses).

If the offeror has not performed comparable services in _Lima_ then the offeror shall provide its

international experience. Offerors are advised that the past performance information requested

above may be discussed with the client’s contact person. In addition, the client’s contact person

may be asked to comment on the offeror’s:

Quality of services provided under the contract;

Compliance with contract terms and conditions;

Effectiveness of management;

Willingness to cooperate with and assist the customer in routine matters, and when

confronted by unexpected difficulties; and

Business integrity / business conduct.

The Government will use past performance information primarily to assess an offeror’s capability to meet the solicitation performance requirements, including the relevance and successful performance of the offeror’s work experience. The Government may also use this data to evaluate the credibility of the offeror’s proposal. In addition, the Contracting Officer may use past performance information in making a determination of responsibility.

(5) Evidence that the offeror/quoter can provide the necessary personnel, equipment, and

financial resources needed to perform the work; (6) The offeror shall address its plan to obtain all licenses and permits required by local

law (see DOSAR 652.242-73 in Section 2). If offeror already possesses the locally required

licenses and permits, a copy shall be provided with the volume II.

(7) The offeror’s strategic plan for _the monthly and annual financial audit __ to include

but not limited to:

(a) A work plan in the form of a narrative and Gantt Chart taking into account all

work elements in Section 1, Performance Work Statement.

(b) Identify types and quantities of equipment, supplies and materials required for

performance of services under this contract. Identify if the offeror already possesses the

listed items and their condition for suitability and if not already possessed or inadequate

for use how and when the items will be obtained;

(c) Plan of ensuring quality of services including but not limited to contract

administration and oversight; and

(d) (1) Copy of the Certificate of Insurance(s), or (2) a statement that the Contractor

will get the required insurance, and the name of the insurance provider to be used.

(e) (1) Copy of the Auditing Firms World Wide Certification representation.

No information concerning this RFQ shall be provided in response to telephone calls. All such requests shall be submitted in writing to the Procurement Specialist. Written questions relating to this RFQ shall be accepted through 12:00 P.M. (local Lima time) Friday, March 22, 2019. Any communications in reference to this RFQ shall cite the reference section title and page number, and directed to the following individual: Name: Saul Espinoza, [email protected], answers will be provided by Tuesday, March 26, 2019 in writing.

Offerors are warned against contacting any INL personnel other than the procurement specialist prior to award of the Contract resulting from this RFQ. If such a contact occurs and found to be prejudicial to competing vendors, the vendor making such a contact may be excluded from award consideration.

FAR AND DOSAR PROVISIONS NOT PRESCRIBED IN PART 12

52.252-1 SOLICITATION PROVISIONS INCORPORATED BY REFERENCE

(FEB 1998)

This solicitation incorporates one or more solicitation provisions by reference, with the

same force and effect as if they were given in full text. Upon request, the Contracting Officer

will make their full text available. Also, the full text of a clause may be accessed electronically

at: http://acquisition.gov/far/index.html/ or http://farsite.hill.af.mil/search.htm

These addresses are subject to change. If the Federal Acquisition Regulation (FAR) is not

available at the locations indicated above, use the Department of State Acquisition website at

http://www.statebuy.state.gov/ to see the links to the FAR. You may also use an Internet “search

engine” (such as Google, Yahoo, Excite, etc.) to obtain the latest location of the most current

FAR.

The following Federal Acquisition Regulation solicitation provision(s) is/are incorporated by

reference:

PROVISIONS TITLE AND DATE

52.204-7 SYSTEM FOR AWARD MANAGEMENT (OCT 2018)

52.204-16 COMMERCIAL AND GOVERNMENT ENTITY CODE REPORTING

(JUL 2016)

52.214-34 SUBMISSION OF OFFERS IN THE ENGLISH LANGUAGE (APR 1991)

The following DOSAR provision is provided in full text: 652.206-70 ADVOCATE FOR COMPETITION/OMBUDSMAN (FEB 2015) (a) The Department of State’s Advocate for Competition is responsible for assisting industry in removing restrictive requirements from Department of State solicitations and removing barriers to full and open competition and use of commercial items. If such a solicitation is considered competitively restrictive or does not appear properly conducive to competition and commercial practices, potential offerors are encouraged first to contact the contracting office for the solicitation. If concerns remain unresolved, contact:

(1) For solicitations issued by the Office of Acquisition Management (A/LM/AQM) or

a Regional Procurement Support Office, the A/LM/AQM Advocate for Competition, at

(b) The Department of State’s Acquisition Ombudsman has been appointed to hear concerns from potential offerors and contractors during the pre-award and post-award phases of this acquisition. The role of the ombudsman is not to diminish the authority of the contracting officer, the Technical Evaluation Panel or Source Evaluation Board, or the selection official. The purpose of the ombudsman is to facilitate the communication of concerns, issues, disagreements, and recommendations of interested parties to the appropriate Government personnel, and work to resolve them. When requested and appropriate, the ombudsman will maintain strict confidentiality as to the source of the concern. The ombudsman does not participate in the evaluation of proposals, the source selection process, or the adjudication of formal contract disputes. Interested parties are invited to contact the contracting activity ombudsman, [insert name] , at ___[insert telephone and fax numbers] . For an American Embassy or overseas post, refer to the numbers below for the Department Acquisition Ombudsman. Concerns, issues, disagreements, and recommendations which cannot be resolved at a contracting activity level may be referred to the Department of State Acquisition Ombudsman at (703) 516-1696 or write to: Department of State, Acquisition Ombudsman, Office of the Procurement Executive (A/OPE), Suite 1060, SA-15, Washington, DC 20520.

(End of provision)

Solicitation 19PE5019Q0062

Page 34 of 50

SECTION 4 - EVALUATION FACTORS

Evaluation Factors The Government intends to award a contract resulting from this solicitation to the lowest priced,

technically acceptable offeror/quoter who is a responsible Contractor. The evaluation process

shall include the following:

(a) COMPLIANCE REVIEW. The Government will perform an initial review of

proposals/quotations received to determine compliance with the terms of the solicitation. The

Government may reject as unacceptable proposals/quotations that do not conform to the

solicitation.

(b) TECHNICAL ACCEPTABILITY. Technical acceptability will include a review of past

performance and experience as defined in Section 3, along with any technical information

provided by the offeror with its proposal/quotation.

(c) PRICE EVALUATION. The lowest price will be determined by multiplying the offered

prices times the estimated quantities in “Prices - Continuation of SF-1449, block 23”, and

arriving at a grand total, including all options. The Government reserves the right to reject

proposals that are unreasonably low or high in price.

(d) RESPONSIBILITY DETERMINATION. The Government will determine Contractor

responsibility by analyzing whether the apparent successful offeror complies with the

requirements of FAR 9.1, including:

adequate financial resources or the ability to obtain them;

ability to comply with the required performance period, taking into consideration

all existing commercial and governmental business commitments;

satisfactory record of integrity and business ethics;

necessary organization, experience, and skills or the ability to obtain them;

necessary equipment and facilities or the ability to obtain them; and

otherwise qualified and eligible to receive an award under applicable laws and

regulations.

Solicitation 19PE5019Q0062

Page 35 of 50

Addendum to Evaluation Factors FAR and DOSAR Provision(s) not Prescribed in Part 12

The following FAR provisions are provided in full text:

FAR 52.225-17 EVALUATION OF FOREIGN CURRENCY OFFERS (FEB 2000):

If the Government receives offers in more than one currency, the Government will

evaluate offers by converting the foreign currency to United States currency using the exchange

rate used by the Embassy in effect as follows:

(a) For acquisitions conducted using sealed bidding procedures, on the date of bid opening.

(b) For acquisitions conducted using negotiation procedures—