Page 1

NC WARN

Duke Environmental Law and Policy Clinic

The Climate Times

Chapel Hill, North Carolina

March 29, 2016

J. David HughesPost Carbon Institute

Global Sustainability Research Inc.

Shale Gas: Myths and RealitiesLong-term Sustainability and Implications for Future

Energy Security

Page 2

Points to be covered:

- SHALE GAS – A look at the fundamentals with examples from

major U.S. plays

-The SHALE REVOLUTION and

CONVENTIONAL WISDOM

- IMPLICATIONS for long term energy sustainability

2

Page 3

Conventional Wisdom

• The United States is on the verge of Energy Independence thanks

to the “SHALE REVOLUTION”.

• Shale Gas production will continue to grow for the foreseeable

future (2040 at least) and prices will remain low.

• The way is clear for U.S. LNG exports to monetize the shale gas

bounty.

• Shale gas production, although temporarily in decline, can be

turned around very quickly with a slight increase in prices. The sky

is the limit when it comes to increasing production.

© Hughes GSR Inc, 2016

3

Page 5

0

2

4

6

8

10

12

0

5

10

15

20

25

30

35

40

2012 2015 2018 2021 2024 2027 2030 2033 2036 2039

Price

$2

01

3 p

er M

Mb

tuTr

illi

on

Cu

bic

Fe

et

pe

r Ye

ar

Year

LNG Imports Canada Imports

Shale Gas Alaska

Coalbed Methane Tight Gas

Conventional Offshore

Domestic Demand Price (Henry Hub)

U.S. Natural Gas Supply Projection by Source, 2012-2040,

EIA Reference Case 2015

Shale Gas

(+93% 2012-2040)

55% of 2040

Production

47% increase in

production by 2040

Tight Gas

Conventional/Other

Offshore

Alaska

U.S. domestic consumption

(data from EIA Annual Energy Outlook 2015, Tables 13 and 14, http://www.eia.gov/forecasts/aeo/er/excel/yearbyyear.xlsx)© Hughes GSR Inc, 2015

5

Price

Page 6

0

10

20

30

40

50

60

70

2000 2005 2010 2015 2020 2025 2030 2035 2040

Gas P

rod

ucti

on

(B

illi

on

cu

bic

feet

per

day)

Year

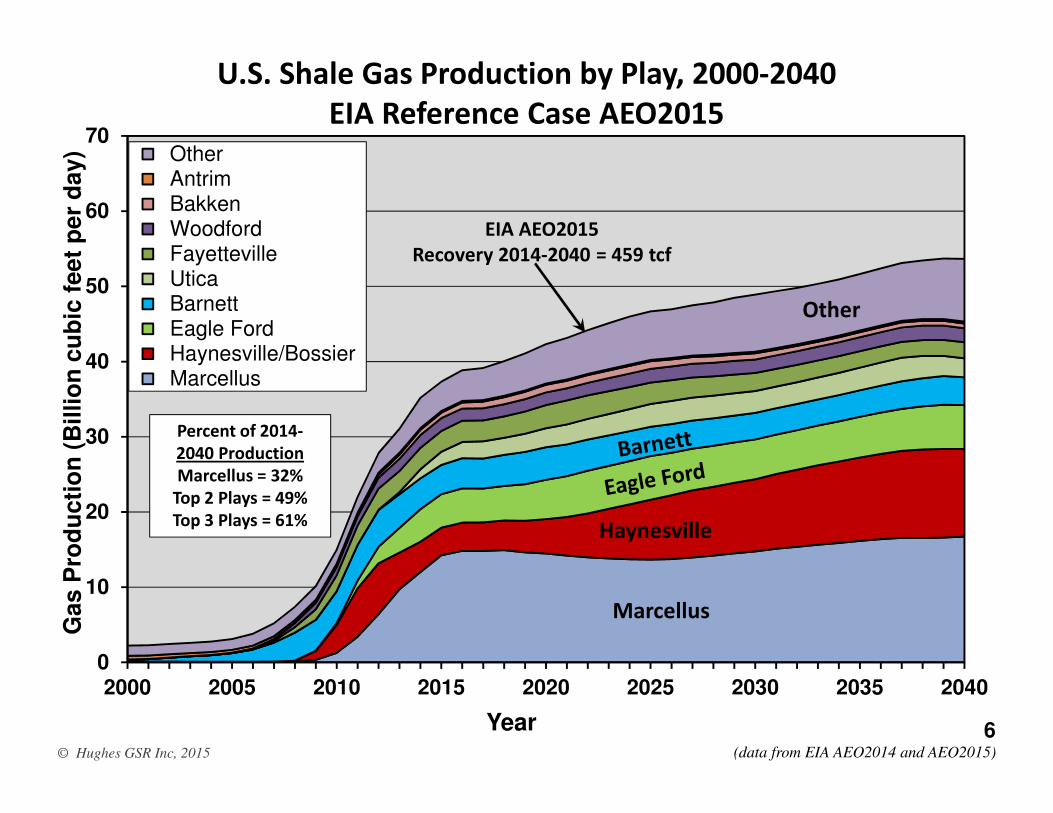

Other Antrim Bakken Woodford Fayetteville Utica Barnett Eagle Ford Haynesville/Bossier Marcellus

U.S. Shale Gas Production by Play, 2000-2040

EIA Reference Case AEO2015

© Hughes GSR Inc, 2015 (data from EIA AEO2014 and AEO2015)

Haynesville

Marcellus

Percent of 2014-

2040 Production

Marcellus = 32%

Top 2 Plays = 49%

Top 3 Plays = 61%

Other

EIA AEO2015

Recovery 2014-2040 = 459 tcf

6

Page 7

0

5

10

15

20

25

30

35

40

45

2000 2002 2004 2006 2008 2010 2012 2014

Gas P

rod

ucti

on

(B

illi

on

cu

bic

feet

per

day)

Year

Rest of US

Utica

Woodford

Marcellus

Eagle Ford

Antrim

Bakken

Fayetteville

Barnett

Haynesville

U.S. Shale Gas Production by Play, 2000-2016

© Hughes GSR Inc, 2016 (data from EIA Natural Gas Weekly Update, March, 2016 )

Barnett

Haynesville

Marcellus

Current Production

Top Play = 37%

Top 2 Plays = 48%

Top 6 Plays = 78%

5 Legacy Plays

Collectively Peaked in

August 2012 and

are down 32%

as of January 2016

Peak October 2015

Eagle Ford

7

Page 8

The Shale Play Life Cycle

• Discovery followed by leasing frenzy.

• Drilling boom follows to meet “held-by-production” lease requirements.

• Sweet spots identified, targeted and drilled off. Companies always drill

their best locations first.

• Production rises rapidly and is maintained for cash-flow despite

potentially uneconomic full-cycle costs.

• Sweet spots become saturated and well quality and field production

decline.

• Plays like the Haynesville become middle aged after just five years.

© Hughes GSR Inc, 2014 8

Page 9

0

500

1000

1500

2000

2500

3000

3500

4000

0

1

2

3

4

5

6

7

8

2007 2008 2009 2010 2011 2012 2013 2014 2015

Nu

mb

er o

f Pro

du

cin

g W

ells

Gas P

rod

ucti

on

(B

illi

on

cu

bic

feet

per

day)

Year

Gas Production

Number of Wells

SHALE PLAY LIFE CYCLE - Haynesville Gas Production and Number of

Producing Wells, 2007-2015

© Hughes GSR Inc, 2016 (data from Drillinginfo, March, 2016)

Peak November 2011

Production

Down 50%

Discovery

Leasing Boom

Drilling Boom

Decline

9

Page 10

© Hughes GSR Inc, 2016 (map by John Van Hoesen based on data from Drillinginfo, August, 2014)

Haynesville Play – Well Quality by Initial Gas Production

10

Page 11

0

1000

2000

3000

4000

5000

6000

7000

8000

1 6 11 16 21 26 31 36 41 46

Ga

s P

rod

uct

ion

(T

ho

usa

nd

cu

bic

fe

et

/da

y)

Months on Production

Haynesville Average Gas Well Decline Curve

3-Year Decline = 89%

First Year = 59%

Second Year = 54%

Third Year = 39%

Fourth Year = 23%

© Hughes GSR Inc, 2016 (data from Drillinginfo, March, 2016)

11

Page 12

0

500

1000

1500

2000

2500

3000

3500

4000

0

1

2

3

4

5

6

7

8

2010 2011 2012 2013 2014 2015

Nu

mb

er o

f Pro

du

cin

g W

ells

Gas P

rod

ucti

on

(B

illi

on

cu

bic

feet/

day)

Year

Pre-2014 Production

Total Production

Number of pre-2014 Wells

Total Number of Wells

First Year Field Decline = 41%

Haynesville Field Decline – Gas Production from all Wells Drilled

Prior to 2014

© Hughes GSR Inc, 2016 (data from Drillinginfo, March, 2016)

12

Page 13

0

200

400

600

800

1000

1200

-12000

-10000

-8000

-6000

-4000

-2000

0

2000

4000

6000

2008 2009 2010 2011 2012 2013 2014 2015

Drillin

g R

ate

(Wells

per Y

ear)

An

nu

al

Gas P

rod

ucti

on

Ad

ded

per

Well

(Th

ou

san

d c

ub

ic f

eet

per

day)

Year

Field Production Added per New Well

Wells Added in prior 12 months

Haynesville Annual Gas Production Added per New Well, 2008-2015

© Hughes GSR Inc, 2014 (data from Drillinginfo, February, 2014, three month trailing moving average)

Drilling Rate peaks @ 1100 wells/year

700 Wells per Year @ 7 bcf/day

@$9M/Well = $6.3 Billion/year

Production will fall to

3bcf/day with 200 wells/year

@$9M/Well = $1.8 Billion/yearGROWTH

DECLINE

13

Page 14

4000

4500

5000

5500

6000

6500

7000

2011 2012 2013 2014 2015

Avera

ge F

irst

Six

Mo

nth

Pro

du

cti

on

(T

ho

usan

d c

ub

ic f

eet/

day)

Year

Haynesville Average

Haynesville Well Productivity – Average Production Rate over First

Six Months, 2011-2015

(data from Drillinginfo, March, 2016)

Peak well productivity 2014

© Hughes GSR Inc, 2016

Down 4% from 2014 peak

Sweet Spot exhaustion?

Increase a result both of

better technology and

Sweet Spot focus

14

Page 15

Haynesville Sweetspot Well Footprint

1 Mile

© Hughes GSR Inc, 2016 (data from Drillinginfo, March, 2016)

15

Page 16

Haynesville Sweetspot Well Footprint

1 Mile

© Hughes GSR Inc, 2016 (data from Drillinginfo, March, 2016)

16

4-5 acre multi-well pads

Page 17

0

2000

4000

6000

8000

10000

12000

14000

16000

0

1

2

3

4

5

6

7

8

9

2000 2004 2008 2012 2016 2020 2024 2028 2032 2036 2040

Nu

mb

er o

f Pro

du

cin

g W

ells

Gas P

rod

ucti

on

(B

illi

on

cu

bic

feet

per

day)

Year

Most likely Production

High drilling rate Production

Low drilling rate Production

Most likely Wells - 300/y

High drilling rate Wells 500/y declining to 300/y

Low drilling rate Wells - current rate 200/y

Haynesville Gas Production Forecast in various Drilling Rate

Scenarios through 2040

© Hughes GSR Inc, 2014 (data from Drillinginfo, August, 2014,

Peak 2011

Recovery to date 11.7 tcf

Recovery by 2040

30-50 tcf

17

Page 18

0

2000

4000

6000

8000

10000

12000

0

2

4

6

8

10

12

14

2000 2004 2008 2012 2016 2020 2024 2028 2032 2036 2040

Nu

mb

er o

f Pro

du

cin

g W

ells

Gas P

rod

ucti

on

(B

illi

on

cu

bic

feet

per

day)

Year

EIA AEO2015 excess

Most likely Production

EIA AEO2015

Most likely Wells

Haynesville Gas Production in Most Likely Rate Scenario through

2040 compared to EIA 2015 Projection

© Hughes GSR Inc, 2015 (data from Drilling Deeper, 2014;EIA AEO2015 Reference Case Projection)

EIA AEO2015

Recovery 2014-2040 = 79 tcf

An Extra 50 tcf (174%)

Recovery 2014-2040 = 29 tcf

Peak 2011

18

Page 19

© Hughes GSR Inc, 2015 (data from EIA, 2015)

Distribution and elevation of Marcellus (feet)

19

Page 20

0

2000

4000

6000

8000

10000

12000

0

2

4

6

8

10

12

14

16

18

2007 2008 2009 2010 2011 2012 2013 2014 2015

Nu

mb

er o

f Pro

du

cin

g W

ells

Gas P

rod

ucti

on

(B

illi

on

cu

bic

feet

per

day)

Year

WV Production

PA Production

EIA Weekly

Number of Wells

Marcellus Gas Production and Number of

Producing Wells, 2007-2015

© Hughes GSR Inc, 2016

(data from Drillinginfo, March, 2016; PA 6-month trailing moving average;

WV 3-month trailing moving average with 2015 estimated; EIA Weekly = natural gas weekly report March 13, 2016)

20

Peak April 2015

Pennsylvania

WV

Page 21

Marcellus Shale Gas Play, All Wells, 2005-2014

© Hughes GSR Inc, 2014 (data from Drillinginfo, September, 2014)21

Page 22

0

1

2

3

4

Tril

lio

n C

ub

ic F

ee

t

County

Marcellus Cumulative Gas Production by County December, 2015

© Hughes GSR Inc, 2015 (data from Drillinginfo; PA current to December, 2015; WV current to December, 2014)

Top 2 counties = 39% of production

Top 5 counties = 68% of production

Top 8 counties = 81% of production

22

Page 23

0

1000

2000

3000

4000

5000

6000

7000

8000

1 6 11 16 21 26 31 36 41 46

Ga

s P

rod

uct

ion

(T

ho

usa

nd

cu

bic

fe

et

/da

y)

Months on Production

Susquehanna

Bradford

Lycoming

Washington

Next 4 counties

Other counties

Marcellus Average Gas Well Decline Curves by County

3-Year Decline

Susquehanna = 81%

Bradford = 72%

Lycoming = 77%

Washington = 81%

Next 4 counties = 85%

Other counties = 84%

© Hughes GSR Inc, 2016 (data from Drillinginfo, March, 2016)

23

Page 24

0

1

2

3

4

5

6

7

8

Susquehanna Bradford Lycoming Washington Next 4Counties

OtherCounties

Bil

lio

n C

ub

ic F

eet

County

Next 21 Years

First Four Years

Estimated Ultimate Recoverable Gas per Well By County

© Hughes GSR Inc, 2016 (data from Drillinginfo, March, 2016)

10

17

We

lls

10

46

We

lls

74

5 W

ell

s

11

36

We

lls

42

38

We

lls

16

85

We

lls

64% to 71% is Recovered

in first 4 Years

7.29

5.77

4.43

3.43

4.52

2.60

24

Page 25

0

1000

2000

3000

4000

5000

6000

7000

8000

2011 2012 2013 2014 2015

Av

era

ge F

irst

12

Mo

nth

s o

f P

rod

uct

ion

(Th

ou

san

d c

ub

ic f

ee

t /d

ay

)

Months on Production

Susquehanna

Bradford

Lycoming

Washington

Next 4 counties

Marcellus Average Well

First 12 Months of Production by County

© Hughes GSR Inc, 2016 (data from Drillinginfo, March, 2016)

Susquehanna

Technology hits limit

Other counties

Bradford

25

Page 26

Marcellus Northeast Pennsylvania Sweetspot Well Footprint

10 Miles

© Hughes GSR Inc, 2016 (data from Drillinginfo, March, 2016)

26

Page 27

Marcellus Northeast Pennsylvania Sweetspot Well Footprint

1 Mile

© Hughes GSR Inc, 2016 (data from Drillinginfo, March, 2016)

27

Page 28

Marcellus Northeast Pennsylvania Sweetspot Well Footprint

1 Mile

© Hughes GSR Inc, 2016 (data from Drillinginfo, March, 2016)

28

Page 29

0

5000

10000

15000

20000

25000

30000

35000

40000

45000

50000

0

2

4

6

8

10

12

14

16

18

2000 2004 2008 2012 2016 2020 2024 2028 2032 2036 2040

Nu

mb

er o

f Pro

du

cin

g W

ells

Gas P

rod

ucti

on

(B

illi

on

cu

bic

feet

per

day)

Year

West Virginia Production

Pennsylvania Production

Most Likely Rate 1320 Wells/year declining to 920

Marcellus Gas Production Forecast by State in Most Likely Drilling

Rate Scenario through 2040

© Hughes GSR Inc, 2016 (data from Drillinginfo, September, 2014)

Peak 2018

Recovery to date 17.3 tcf

Ultimate Recovery

129 tcf by 2040

Pennsylvania

West Virginia

29

Page 30

0

5000

10000

15000

20000

25000

30000

35000

40000

0

2

4

6

8

10

12

14

16

18

2000 2004 2008 2012 2016 2020 2024 2028 2032 2036 2040

Nu

mb

er o

f Pro

du

cin

g W

ells

Gas P

rod

ucti

on

(B

illi

on

cu

bic

feet

per

day)

Year

EIA AEO2015 excess

Most likely Production

EIA AEO2015

Most likely Wells

Marcellus Gas Production in Most Likely Rate Scenario through

2040 compared to EIA AEO 2015

© Hughes GSR Inc, 2015 (data from Drilling Deeper, 2014; EIA AEO2014 and EIA AEO2015)

Peak 2018

EIA AEO2015

Recovery 2014-2040 = 147 tcf

An Extra 27 tcf (22%)

Recovery 2014-2040 = 120 tcf

30

Page 31

0

2000

4000

6000

8000

10000

12000

Bakken Barnett Eagle Ford FayettevilleHaynesville Marcellus Woodford

Avera

ge W

ell

Pro

du

cti

on

(m

cf/

day)

County

Average

Sweet Spot

© Hughes GSR Inc, 2014 (data from Drillinginfo, October, 2014)

Major Shale Play Well Quality in 2013

Average and Sweet Spots – First 12 month Production Rate

31

Page 32

0

20000

40000

60000

80000

100000

120000

140000

160000

180000

200000

0

5

10

15

20

25

30

35

40

45

2000 2004 2008 2012 2016 2020 2024 2028 2032 2036 2040

Nu

mb

er o

f Pro

du

cin

g W

ells

Gas P

rod

ucti

on

(B

ilio

ncu

bic

feet/

per

day)

Year

Marcellus

Haynesville

Eagle Ford

Bakken

Woodford

Fayetteville

Barnett

Most likely Wells

Most Likely Drilling Rate Gas Production from Major Shale Plays

through 2040 (88% of 2014 Production)

© Hughes GSR Inc, 2014 (data from Drillinginfo, September, 2014,

Peak 2017

Marcellus

Recovery to

date 59 tcf

Remaining

232 tcf 2015-

2040

Barnett

Eagle Ford

Haynesville

32

Page 33

0

5

10

15

20

25

30

35

40

45

2000 2004 2008 2012 2016 2020 2024 2028 2032 2036 2040

Gas P

rod

ucti

on

(B

ilio

ncu

bic

feet/

per

day)

Year

EIA 2015 AdditionalMarcellusHaynesvilleEagle FordBakkenWoodfordFayettevilleBarnett

Most Likely Gas Production from Major Shale Plays through 2040

Compared to EIA AEO 2015 Projection

© Hughes GSR Inc, 2016 (data from Drillinginfo, September, 2014; EIA AEO2015)

Peak 2017

Recovery to

date 59 tcf

Remaining

232 tcf 2015-

2040

Marcellus

EIA 2015 Additional

125 tcf 2015-2040

or 54% more

20

40

EIA

Pro

du

ction

17

0%

Hig

he

er

Haynesville

Eagle Ford

Barnett

33

Page 34

0

10

20

30

40

50

60

2000 2004 2008 2012 2016 2020 2024 2028 2032 2036 2040

Gas P

rod

ucti

on

(B

ilio

ncu

bic

feet/

per

day)

Year

EIA 2015 Other PlaysEIA 2015 AdditionalMarcellusHaynesvilleEagle FordBakkenWoodfordFayettevilleBarnett

Most Likely Gas Production from Major Shale Plays through 2040

with EIA AEO 2015 Additions

© Hughes GSR Inc, 2016 (data from Drillinginfo, September, 2014; EIA AEO2015)

Recovery to

date 59 tcf

Remaining

232 tcf 2015-

2040

Marcellus

EIA 2015 Additional

From Major Plays

125 tcf 2015-2040

or 54% more

Haynesville

34

Page 35

- Shale has been a game-changer in the short-term, but projections

of long-term sustainability at low prices are highly questionable.

Summary and Implications

- Assuming long term sustainability of production at low prices is folly for energy policy. The shale revolution is a temporary windfall and

should be viewed as such.

- High quality shale plays are not ubiquitous – and plays are not

uniform. Sweet spots are exploited early in the development process.

The best parts of major plays are being drilled NOW.

35

- High well decline rates require a drilling treadmill and high capital

inputs to sustain production and offset field declines, along with

associated environmental impacts.

Page 36

Summary and Implications

- U.S. “Energy Independence” with the forecast energy trajectory is highly unlikely, barring a radical reduction in consumption and a major ramp up of renewable energy.

- A sustainable energy future requires a vision beyond the

next couple of quarters or the next election. In the absence of

a coherent plan, investments assuming cheap oil and gas in

the long term are

very likely to end badly.

36