30

STRONG FUNDAMENTALS FUNDAMENTAL STRENGTHS Investor Presentation September 2014

STRONG FUNDAMENTALS

FUNDAMENTALSTRENGTHS

Investor PresentationSeptember 2014

Disclaimer

This presentation contains forward-looking information within the meaning of applicablesecurities laws. The forward-looking information is based on assumptions, estimates andanalysis made in light of the company’s experience and its perception of trends, currentconditions and expected developments, as well as other factors that are believed by thecompany to be reasonable and relevant in the circumstances. Forward-lookinginformation involves known and unknown risks, uncertainties and other factors whichmay cause actual results, performance or achievements to be materially different fromthose predicted, expressed or implied by the forward-looking information. The risks anduncertainties include, among other things, changes in global economic activity andchanges in energy supply and demand which impact on the level of drilling activity andpipeline construction; political, economic and other risks arising from internationaloperations; compliance with environmental, trade and other laws; liability claims;fluctuations in foreign exchange rates and fluctuations in raw material prices, as well asother risks and uncertainties that are more fully described in the company’s currentAnnual Information Form, annual and quarterly reports and in other reports and filingsmade with securities regulatory authorities and available at www.sedar.com.

2

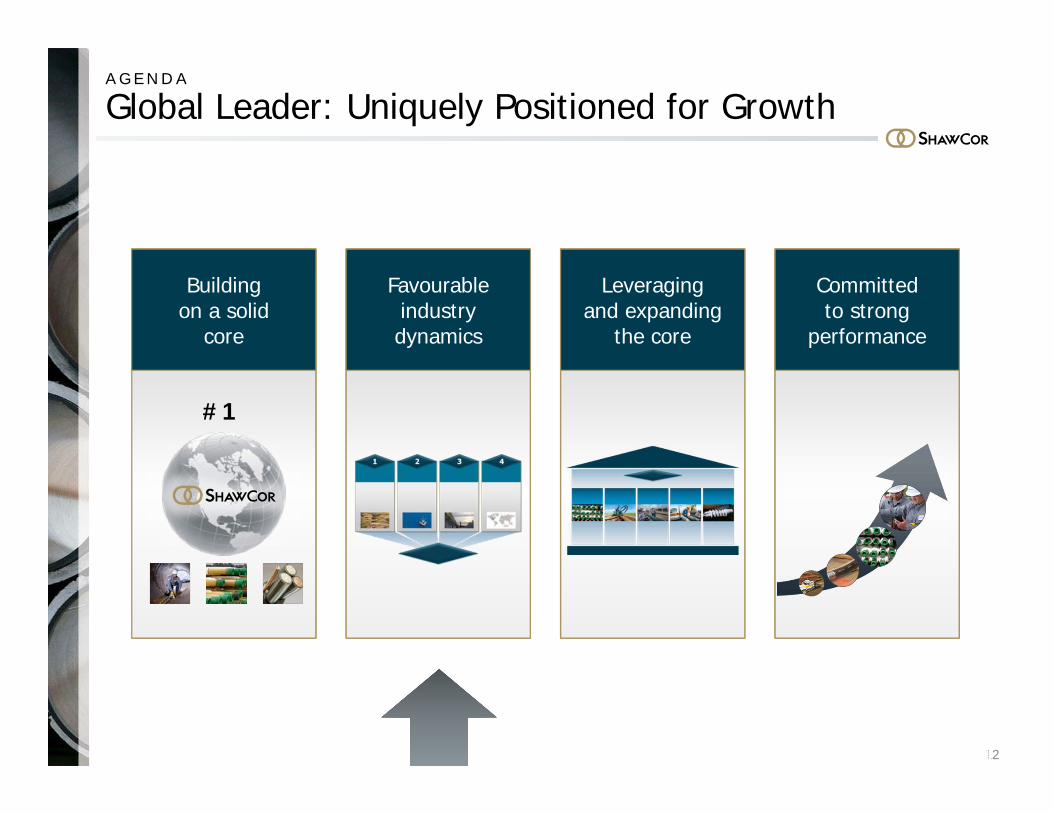

A G E N D A

Global Leader: Uniquely Positioned for Growth

Buildingon a solid

core

Favourable industry dynamics

Leveragingand expanding

the core

Committedto strong

performance

3

#1

A T A G L A N C E

ShawCor: Profile of a Global Leader

4

>$1.8B

Annual revenue

~$3.4B

Market Cap

> 90 facilities and 18 countries

Global footprint

All global energy players

Established relationships

Strong andgrowing

Barriers to entry

S H A W C O R T O D A Y

A Global Energy Services Company

5

Our Nine Business Units

Broad product and service offering – a powerful competitive advantage

Bredero Shaw

Canusa-CPS

Shaw Pipeline Services

SocothermFlexpipe Systems

Guardian

Desert NDT

DSG-Canusa

ShawFlex

Delivering Leading Solutions to Our Customers Around the World

6

AMERICAS

EMAR

ASIAPACIFIC

PipelinePerformance

CompositeProductionSystems

Integrity Management ConnectivityOilfield Asset

Management

Customers around the world

• Bredero Shaw• Socotherm• Canusa–CPS

• FlexpipeSystems

• Guardian• CSI

• ShawFlex• DSG–Canusa• PFT Systems

& Connectors

• SPS• Desert NDT• Zedi• Vintri

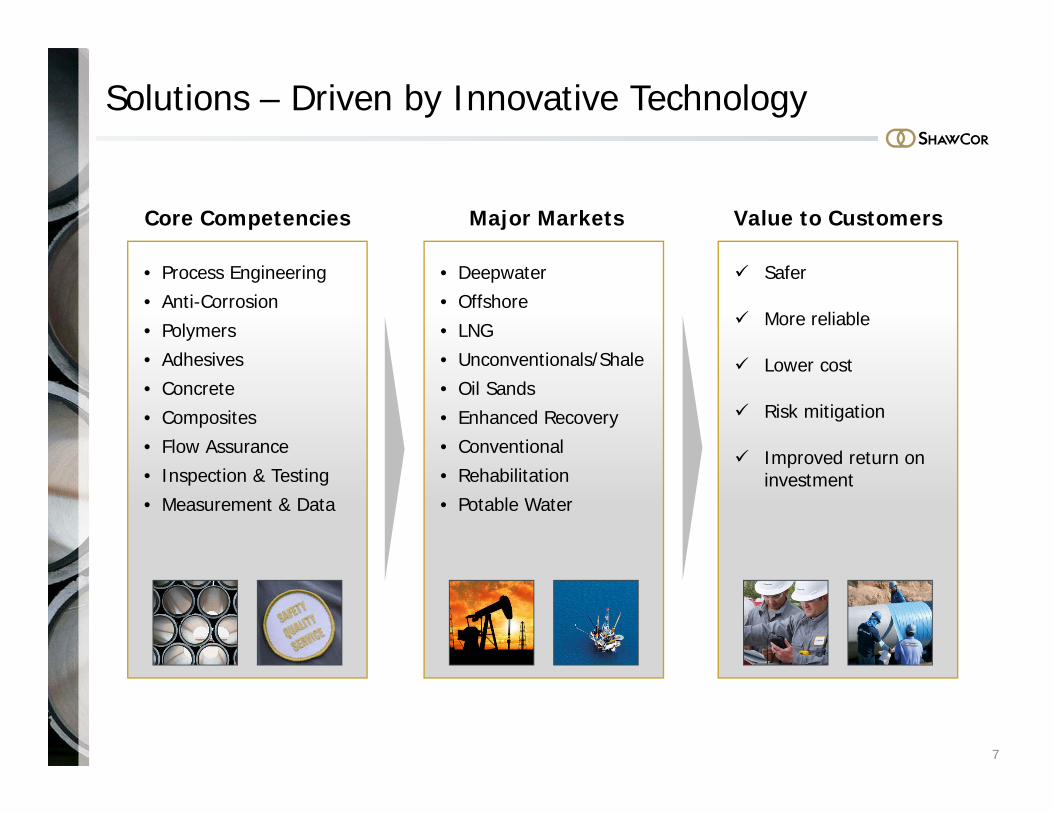

Solutions – Driven by Innovative Technology

7

Core Competencies Major Markets Value to Customers

• Process Engineering• Anti-Corrosion• Polymers• Adhesives• Concrete• Composites• Flow Assurance• Inspection & Testing• Measurement & Data

• Deepwater• Offshore• LNG• Unconventionals/Shale• Oil Sands• Enhanced Recovery• Conventional• Rehabilitation• Potable Water

Safer

More reliable

Lower cost

Risk mitigation

Improved return on investment

Unmatched Scale, Diversity and Global Reach

8

Coating Facility

Other Operating Facility

• 90+ global locations• 7 mobile coating plants• >8,000 employees worldwide• Serving all major basins

A Track Record of Successful Project Execution

9

Darwin

Ichthys LNG Project

• Longest offshore gas pipeline in southern hemisphere

• Coatings for >1,000 km of offshore pipelines

• Value >$500M

Ichthys

Gas pipelineGas field

Trinidad Project• Concrete weight coatings for

offshore Dragon Cigma gas field• Executed with 2 mobile plants in

Trinidad• Value >$100M

North America Gathering Lines

• > 22,000 km of Flexpipe composite linepipe installed

• > 1.5 million welds inspected per year by Desert NDT

Dragon Cigma

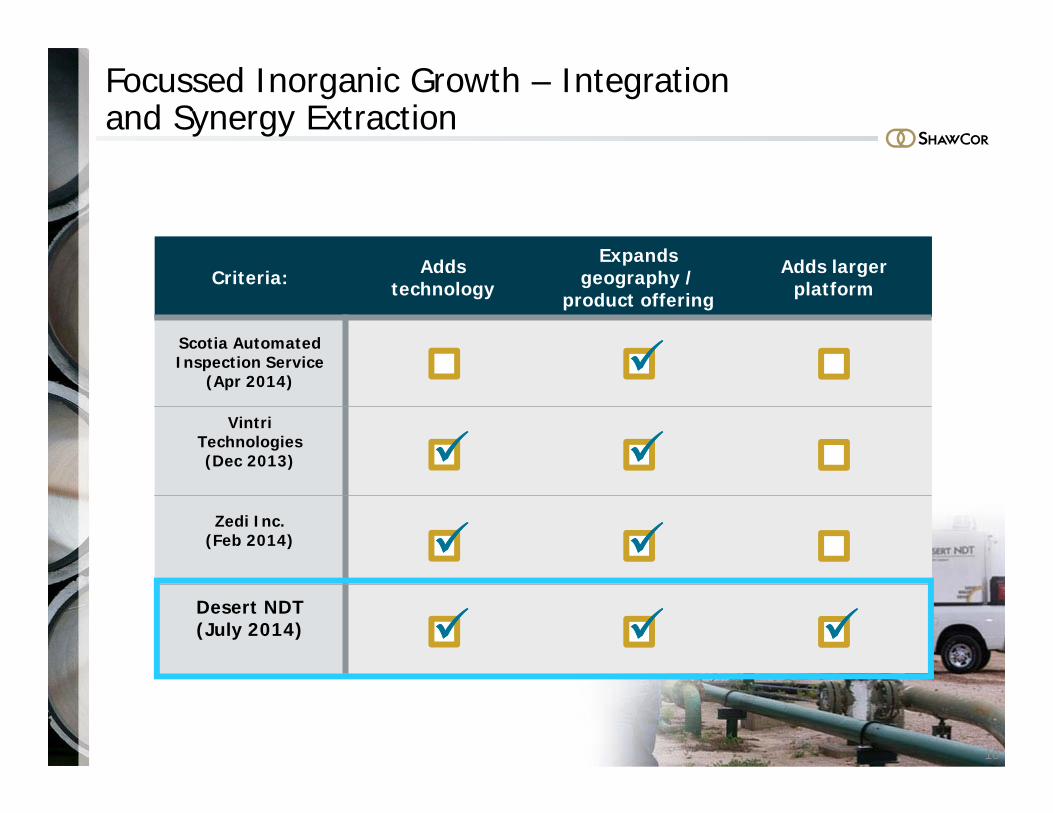

Focussed Inorganic Growth – Integration and Synergy Extraction

10

Criteria: Addstechnology

Expands geography /

product offering

Adds larger platform

Scotia Automated Inspection Service

(Apr 2014)

VintriTechnologies(Dec 2013)

Zedi Inc. (Feb 2014)

Desert NDT(July 2014)

Proven Track Record – 2008 to 2013

11

* 5 year compound annual growth rate

Revenuegrowth

6.0%*

EBITDAgrowth

8.0%*

EPSgrowth

10.9%*

AverageROIC

16.2%

#1

A G E N D A

Global Leader: Uniquely Positioned for Growth

12

Buildingon a solid

core

Favourable industry dynamics

Leveragingand expanding

the core

Committedto strong

performance

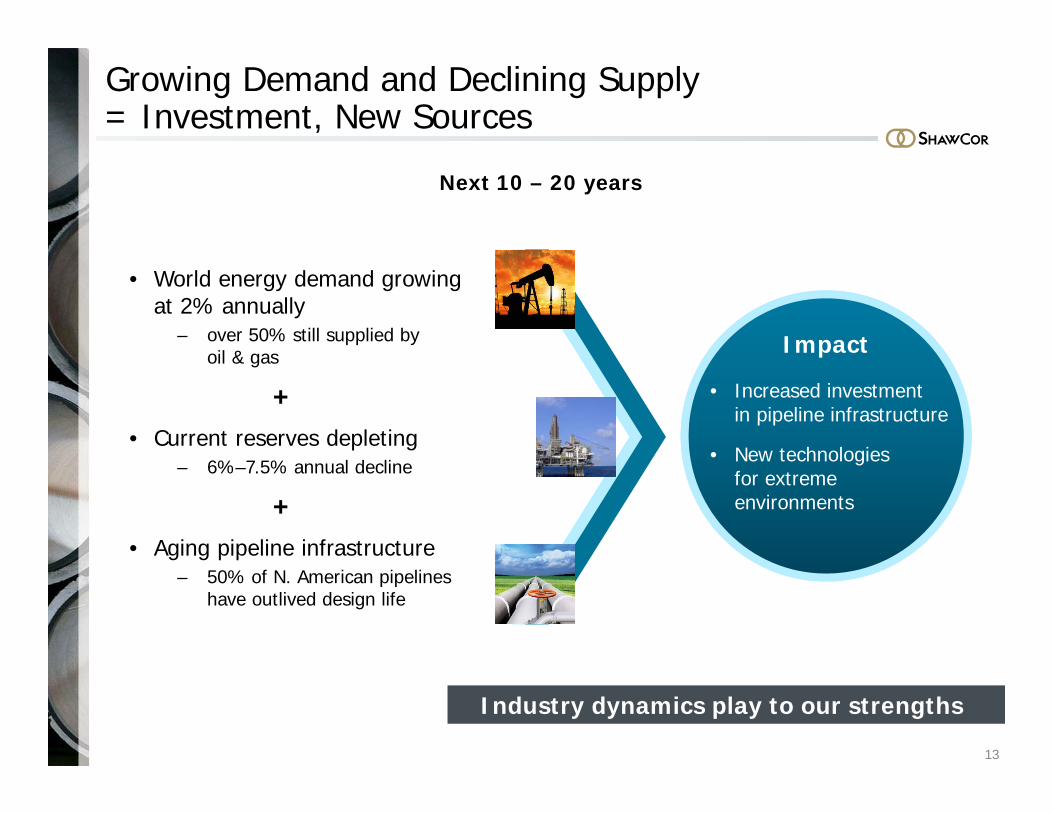

Growing Demand and Declining Supply = Investment, New Sources

13

Next 10 – 20 years

• World energy demand growing at 2% annually

– over 50% still supplied by oil & gas

+• Current reserves depleting

– 6%–7.5% annual decline

+• Aging pipeline infrastructure

– 50% of N. American pipelines have outlived design life

Impact

• Increased investment in pipeline infrastructure

• New technologies for extreme environments

Industry dynamics play to our strengths

Growing Gap Between Energy Supply and Demand

14

Growing demand distant from supply driving new pipeline infrastructure

Source: EIA International Energy Outlook 2013

Oil Supply

Oil Demand

Gas Supply

Gas DemandGapGap

GapGap

GapGapGapGap

Africa

Middle East

Europe & EurasiaNorth America

Central & South America

Asia Pacific

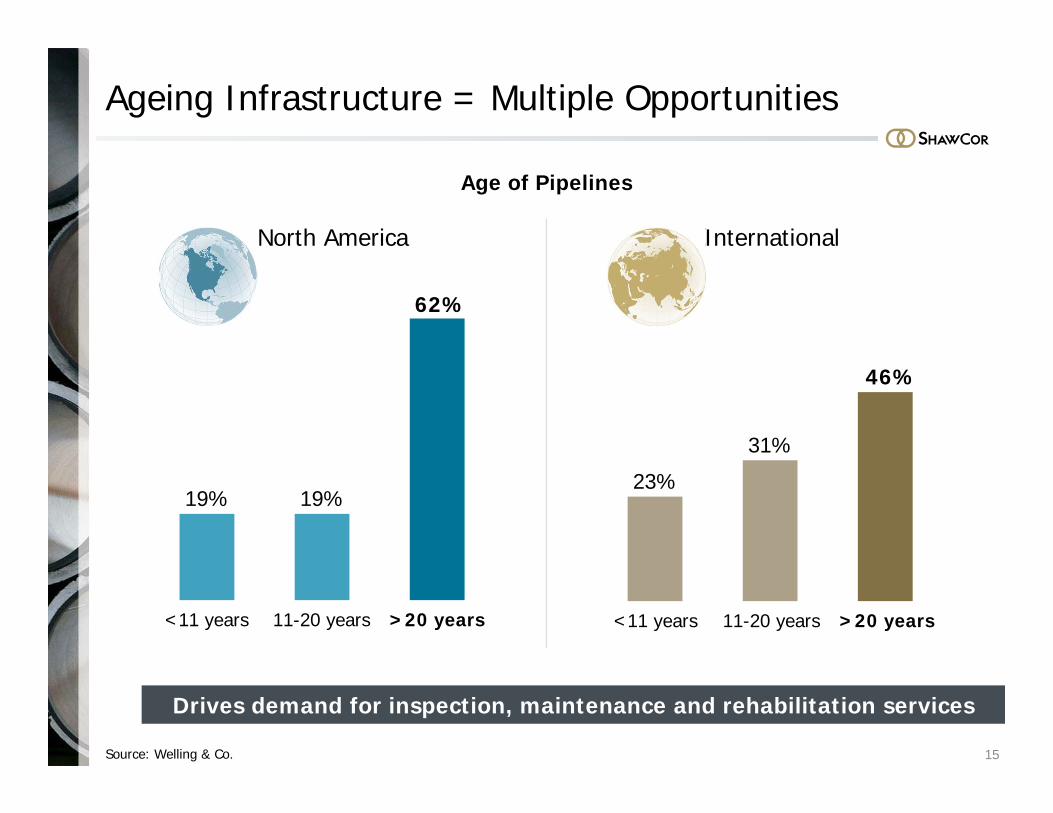

Ageing Infrastructure = Multiple Opportunities

15Source: Welling & Co.

Age of Pipelines

Drives demand for inspection, maintenance and rehabilitation services

19% 19%

62%

North America International

23%

31%

46%

<11 years 11-20 years >20 years <11 years 11-20 years >20 years

Increasing Public and Regulatory Scrutiny…

16

…is driving need for increased traceability and operator confidence

RISK

What This All Means: Multiple Opportunities for ShawCor

17

Growth inUnconventionals

Growth in Deepwater Reserves

Ageing Infrastructure and IncreasingPublic Scrutiny

Transportation for Mismatch of Supply

– Demand

• Large regional plays i.e. Bakken, Eagle Ford, Vaca Muerta

• Factory approach to achieve economics

• Technical extremes

• Component and system reliability

• Execution critical

• Operational continuity and effectiveness

• Recurring revenues from pipeline operating expenditures

• Gas mobility through pipeline and LNG

• Production infrastructure to feed exports

Four Key Opportunities

1 2 3 4

#1

A G E N D A

Global Leader: Uniquely Positioned for Growth

Buildingon a solid

core

Favourable industry dynamics

Leveragingand expanding

the core

Committedto strong

performance

18

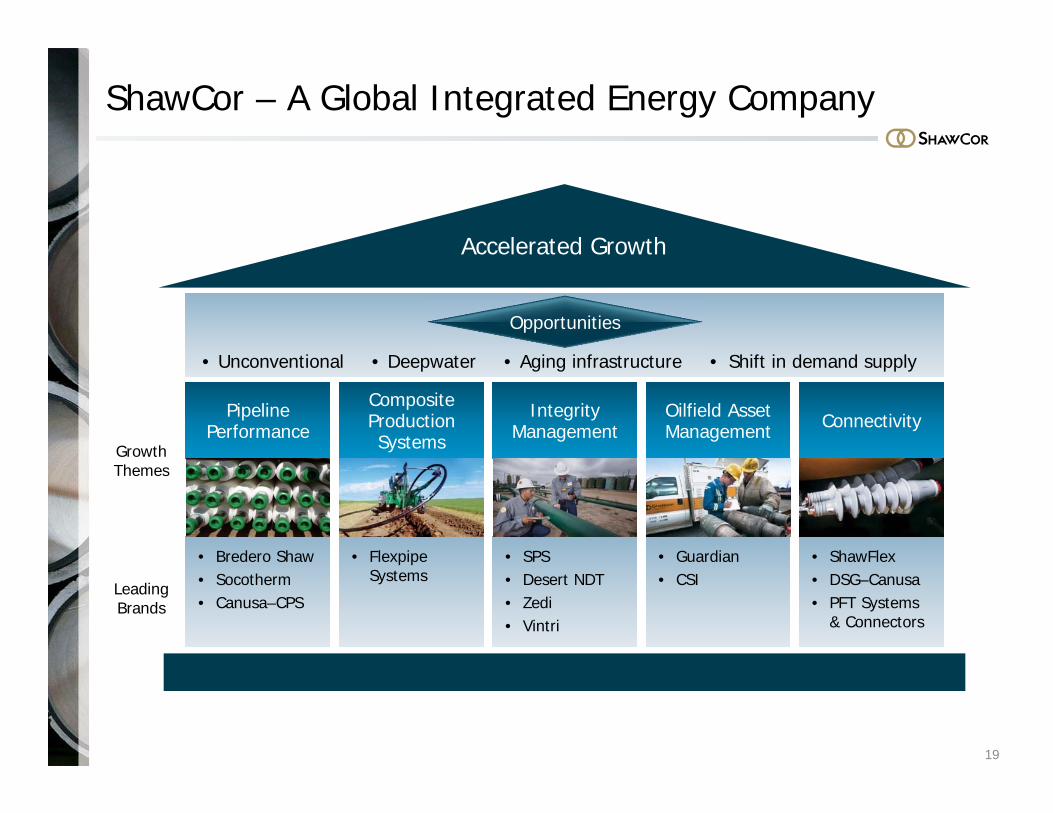

ShawCor – A Global Integrated Energy Company

19

• Bredero Shaw• Socotherm• Canusa–CPS

• FlexpipeSystems

• Guardian• CSI

• ShawFlex• DSG–Canusa• PFT Systems

& Connectors

CompositeProductionSystems

Integrity Management ConnectivityOilfield Asset

Management

Accelerated Growth

PipelinePerformance

• Deepwater• Unconventional • Aging infrastructure • Shift in demand supply

GrowthThemes

LeadingBrands

Opportunities

• SPS• Desert NDT• Zedi• Vintri

Why ShawCor?Value to Customer

G R O W T H T H E M E # 1

Pipeline Performance

20

The OpportunityLeverage our leading pipe coating products, services and systems into innovative solutions that extend the life of pipeline assets and/or expand operating envelopes

• Extend life of pipeline assets

• Expand operating envelopes (increased production)

• Reduced risk (HSE and execution)

• Proven track record

• Proven technology

• Global presence

Note: ShawCor market share based on 2014 Revenue on a proforma basis

Market Size

• Global market $5 Billion, ShawCor share ~25%

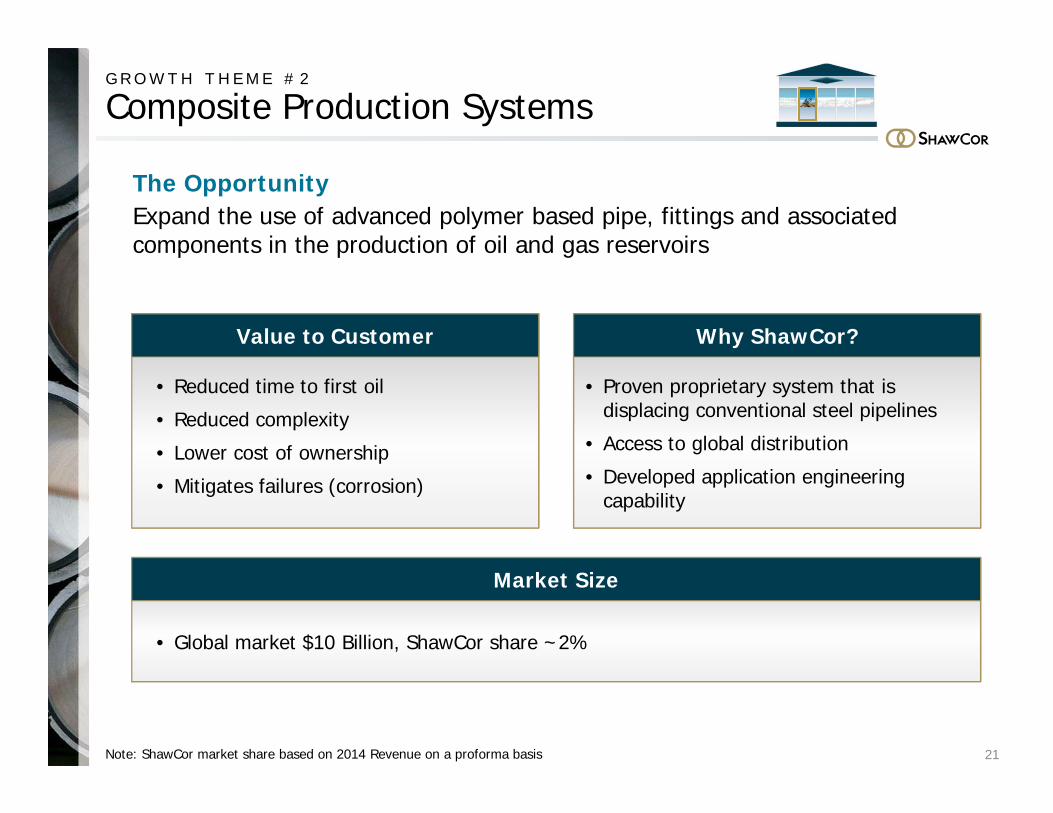

G R O W T H T H E M E # 2

Composite Production Systems

21

The OpportunityExpand the use of advanced polymer based pipe, fittings and associated components in the production of oil and gas reservoirs

Note: ShawCor market share based on 2014 Revenue on a proforma basis

Value to Customer Why ShawCor?

Market Size

• Reduced time to first oil

• Reduced complexity

• Lower cost of ownership

• Mitigates failures (corrosion)

• Proven proprietary system that is displacing conventional steel pipelines

• Access to global distribution

• Developed application engineering capability

• Global market $10 Billion, ShawCor share ~2%

Value to Customer

G R O W T H T H E M E # 3

Integrity Management

22

The OpportunityDevelop measurement and data technology and systems to enhance the operational continuity and efficiency of oil and gas infrastructure assets

• Mitigation of failures

• Quality control

• Reduce costs

• Reliable traceability

Note: ShawCor market share based on 2014 Revenue on a proforma basis

Why ShawCor?

• North American leader in pipeline weld inspection

• Established global presence

• Proprietary measurement technology

• Access to Zedi remote data monitoring and Vintri tracking capabilities

Market Size

• North America market $3.5 Billion, ShawCor share ~8%

Value to Customer

G R O W T H T H E M E # 4

Oilfield Asset Management

23

The OpportunityImprove customer’s oilfield asset utilization, especially in unconventional production, by providing asset management, inspection and repair services

• Improved return on capital employed

• Increased confidence in operational performance and asset uptime

• Cost reduction

• One-stop shop (inspection, repair, asset tracking)

Note: ShawCor market share based on 2014 Revenue on a proforma basis

Why ShawCor?

• Proven asset management systems

• Proven repair capability

• Leading market position in Canada

• Established position in large U.S. and growing Mexico markets

Market Size

• North America market $2 Billion, ShawCor share ~ 4%

Value to Customer

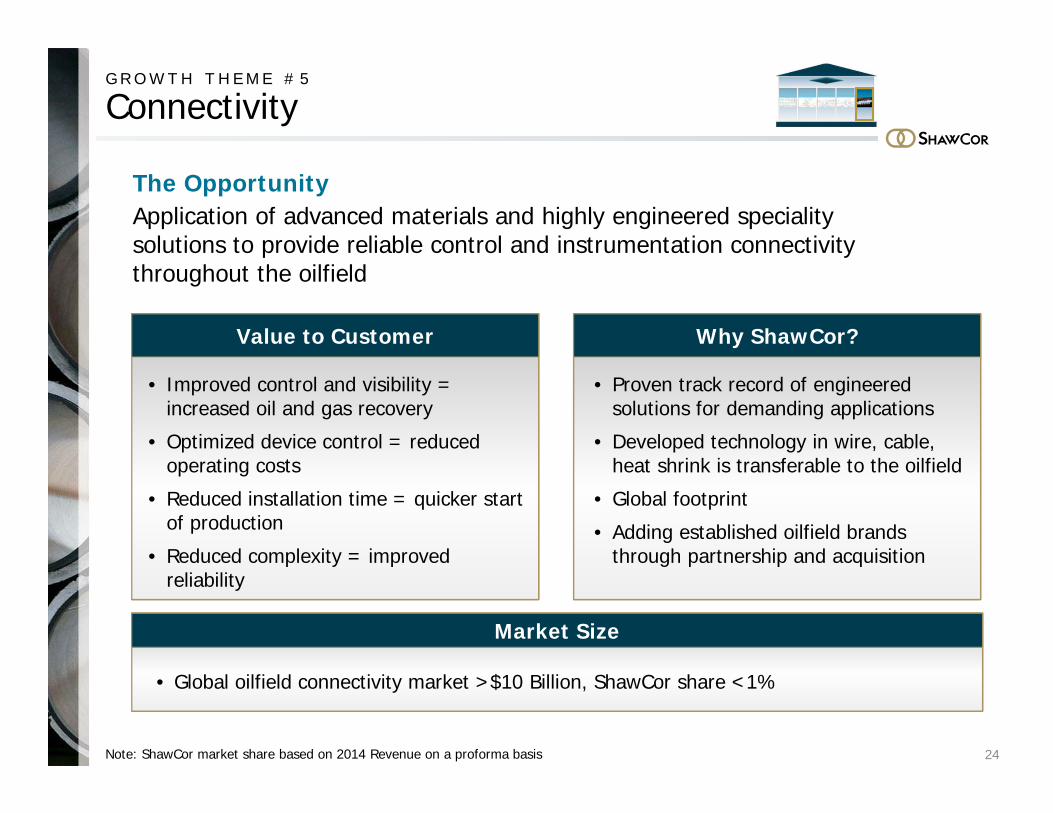

G R O W T H T H E M E # 5

Connectivity

24Note: ShawCor market share based on 2014 Revenue on a proforma basis

The OpportunityApplication of advanced materials and highly engineered speciality solutions to provide reliable control and instrumentation connectivity throughout the oilfield

• Improved control and visibility = increased oil and gas recovery

• Optimized device control = reduced operating costs

• Reduced installation time = quicker start of production

• Reduced complexity = improved reliability

Why ShawCor?

• Proven track record of engineered solutions for demanding applications

• Developed technology in wire, cable, heat shrink is transferable to the oilfield

• Global footprint

• Adding established oilfield brands through partnership and acquisition

Market Size

• Global oilfield connectivity market >$10 Billion, ShawCor share <1%

#1

A G E N D A

Global Leader: Uniquely Positioned for Growth

25

Buildingon a solid

core

Favourable industry dynamics

Leveragingand expanding

the core

Committedto strong

performance

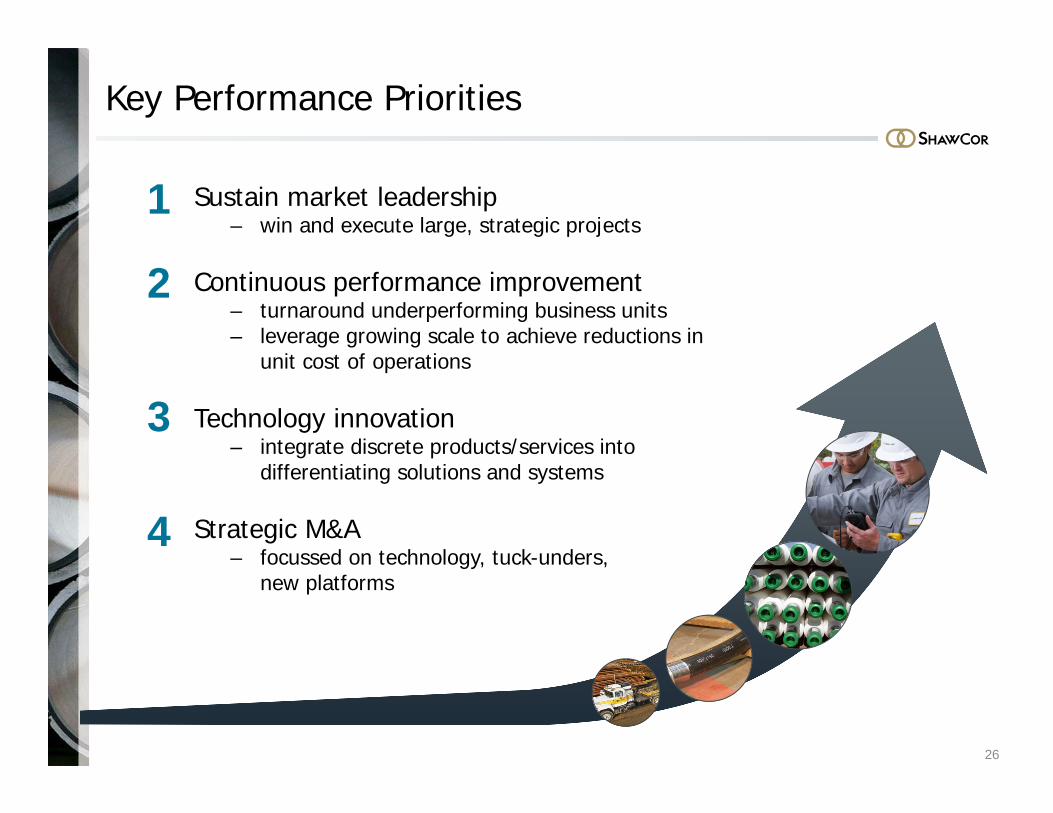

Key Performance Priorities

26

1 Sustain market leadership – win and execute large, strategic projects

2

3

4

Continuous performance improvement– turnaround underperforming business units – leverage growing scale to achieve reductions in

unit cost of operations

Technology innovation– integrate discrete products/services into

differentiating solutions and systems

Strategic M&A– focussed on technology, tuck-unders,

new platforms

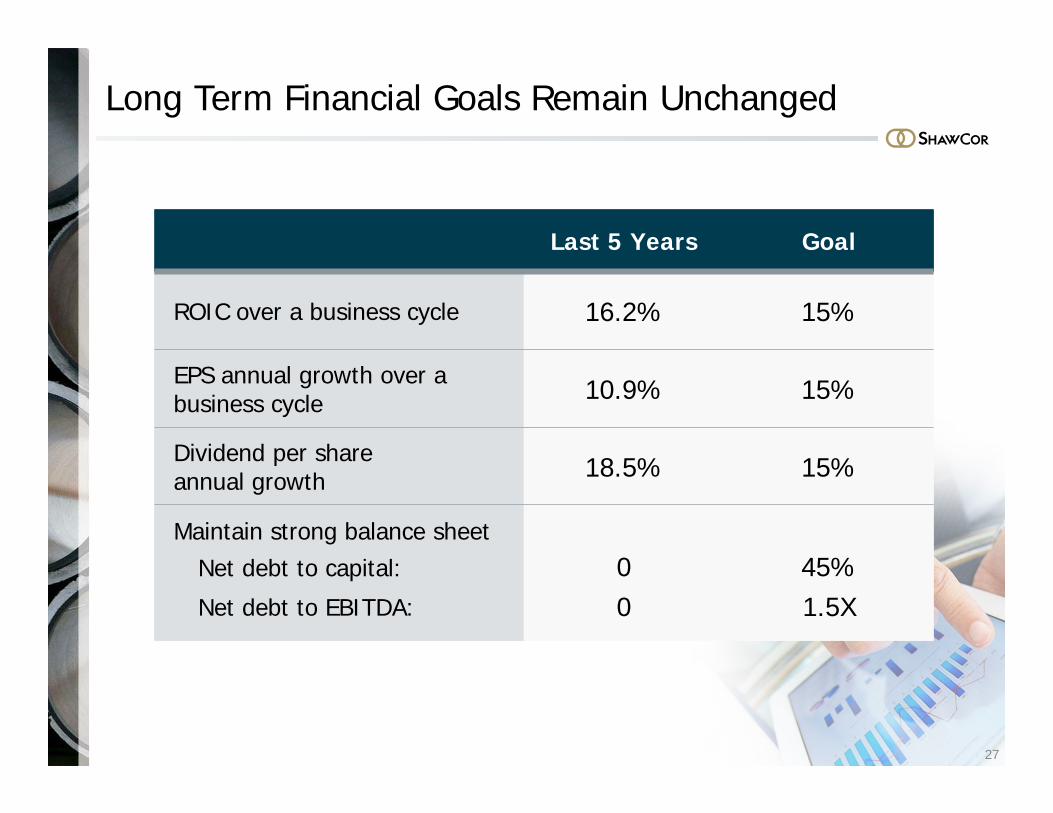

Long Term Financial Goals Remain Unchanged

27

Last 5 Years Goal

ROIC over a business cycle 16.2% 15%

EPS annual growth over a business cycle 10.9% 15%

Dividend per share annual growth 18.5% 15%

Maintain strong balance sheetNet debt to capital:

Net debt to EBITDA:

00

45%1.5X

S H A W C O R V I S I O N

A Global Integrated Energy Services Company

• Revenue in excess of $4 Billion

• Leading market positions in >$30 Billion available market

• Platform of 5 focussed businesses, each >$300M

• Reduced financial performance variability through recurring revenues >85%

28

I N S U M M A R Y

Global Leader: Uniquely Positioned for Growth

29

• 10.9% EPSgrowth 2008-13

• Growing demand, depleting supply

• Vision of $4 Billion, clear performance drivers

• Capitalizing on five growth themes

#1

Buildingon a solid

core

Favourable industry dynamics

Leveragingand expanding

the core

Committedto strong

performance

STRONG FUNDAMENTALS

FUNDAMENTALSTRENGTHS

Investor PresentationSeptember 2014

30