SUMMER TRAINING REPORT Shree Cement Limited “Market perception of shree Cement In terms of marketing mix” Submitted in partial fulfillment for the Award of Degree of Master of Business Administration Submitted By :- Submitted To :- SANAT KUMAR NIMBARK MR. MUKESH MACHARA MBA PART- II HEAD OF DEPARTMENT SESSION-2008-10 1

Transcript

SUMMER TRAINING REPORT

Shree Cement Limited

“Market perception of shree Cement In terms of marketing mix”

Submitted in partial fulfillment for theAward of Degree of

Master of Business Administration

Submitted By :- Submitted To :-SANAT KUMAR NIMBARK MR. MUKESH MACHARAMBA PART- II HEAD OF DEPARTMENTSESSION-2008-10

Institute of Information & Management Sciences7-A, RIICO Institutional Complex, Sitapura, Jaipur- 302 022

1

PREFACE

The summer training project of management course plays an important role for a

management student to develop him into a well groomed professional. It provides

him the theoretical concepts and practical exposure in the field of application.

Summer training project also provides him an idea of dynamic and versatile

professional world as well as an exposure to the intricacies and complexities of

the corporate world.

My summer training in SHREE CEMENT LIMITED Jaipur was an eye opening

experience to see the level of customer satisfaction among people of the jaipur

city & local area

During MBA program I was taught about two dozen subjects which if not applied

properly are a simple waste of time. At SHREE CEMENT LMITED I got a

chance to apply management theories to the latest competitive and marketing

oriented environment.

In two months of market exposure, I learned a lot of various aspects of

organizational structure, departments, sales, communication and their impact.

Now I can say one thing that the best way to learn is at work. It was a real

interesting experience and I enjoyed every part of it and hope that it would be

helpful in my future.

2

ACKNOWLEDGEMENTS

Successfully accomplished project work and the completion of this report have

been made possible by the significant contributions of many people.

I would like to express my sincere gratitude towards Mr.Naveen Sharma my

organizational guide for giving me the support and encouragement that I needed,

and providing many valuable suggestions and insights for my work. I would also

like to thank my institutional guide Mr. Mukesh Machra for his support.

Finally, I’m grateful to the entire Shree Cement family, for co-operating with me

during my work here.

SANAT KUMAR NIMBARKMBA, Session of 2008-2010

Institute of information & management sciences

Jaipur

3

-: CONTENTS :-1 Industry overview 9

1.1 Cement industry in India 9

1.2 Major Players in Indian Cement Industry 10

1.3 Process Technology 11

1.3.1 Raw Materials for Cement Production 11

1.4 Process 11

1.4.1 Stages of Cement Production 12

1.5 Types of Cement 15

1.6 Scale of Operations 17

1.6.1 Industrial production 17

1.7 Exports 20

1.8 Policy Initiatives 22

1.9 Future Outlook 22

1.10 Significant Consolidations 22

1.11 Competitor & Environment Analysis 24

PART-2

2 Company Overview – Shree Cement Limited 25

2.1 Introduction 25

2.2 Vision of SCL 26

2.3 Philosophy of SCL 26

2.4 Mission of SCL 27

2.5 SCL manufacturing units 27

2.6 Business & Managerial Challenges for SCL 30

2.7 Market of SCL 31

2.8 SCL’s Brands & Products 32

2.9 Strengths of SCL 32

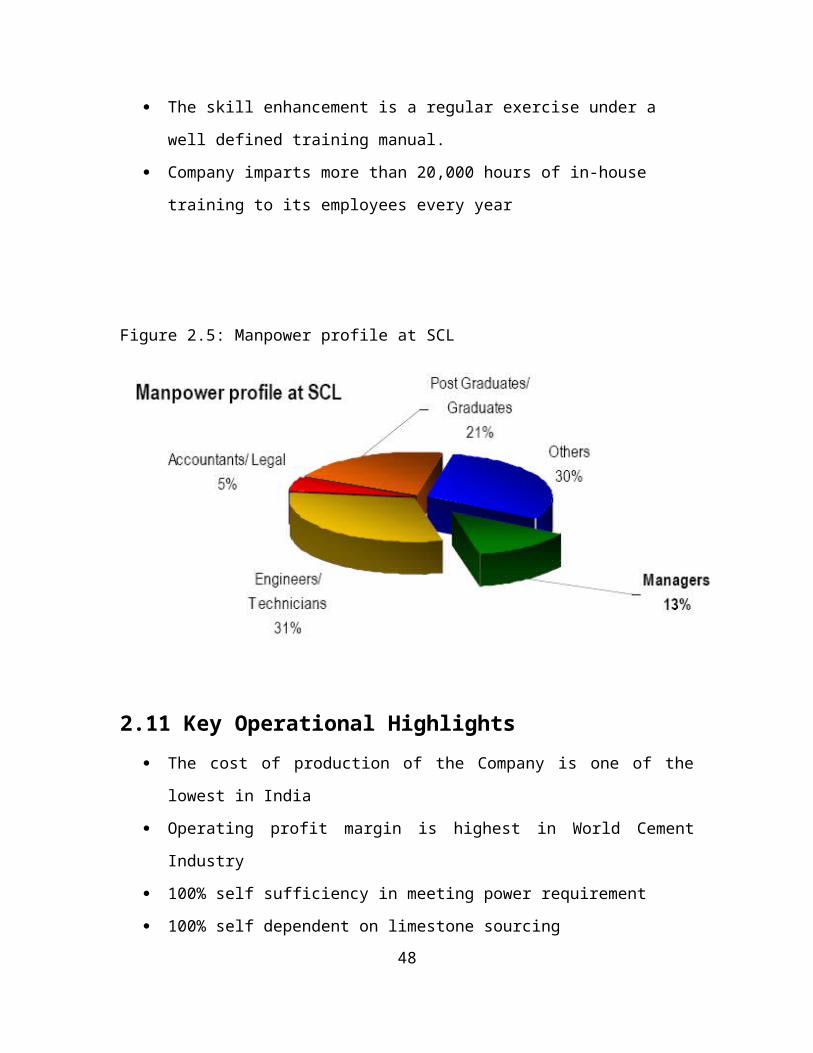

2.10 SCL’s Manpower profile 35

4

2.11 Key Operational Highlights 36

2.12 Recognition and Awards 42

2.13 SCL vis-à-vis Competitors 42

2.14 Information Technology at SCL 46

2.15 Bangur Cement – SCL’s Premium Brand 48

2.16 Comparison between various cement brands 50

PART-3

3 Marketing research 53

3.1 Classification marketing research 54

3.1.1 Process of marketing research 55

3.2 Research methodology 56

3.2.1 Data collection 57

3.2.2 Area covered 59

3.2.3 Data analysis 60

3.2.4 Findings 69

PART-4

4 Questionnaire 70

Performa of Questionnaire 71

Dealer /sub dealer report 72

PART-5

5.1 Conclusion 78

5.2 Recommendation 79

5.3 Bibliography & webliography 81

List of tables

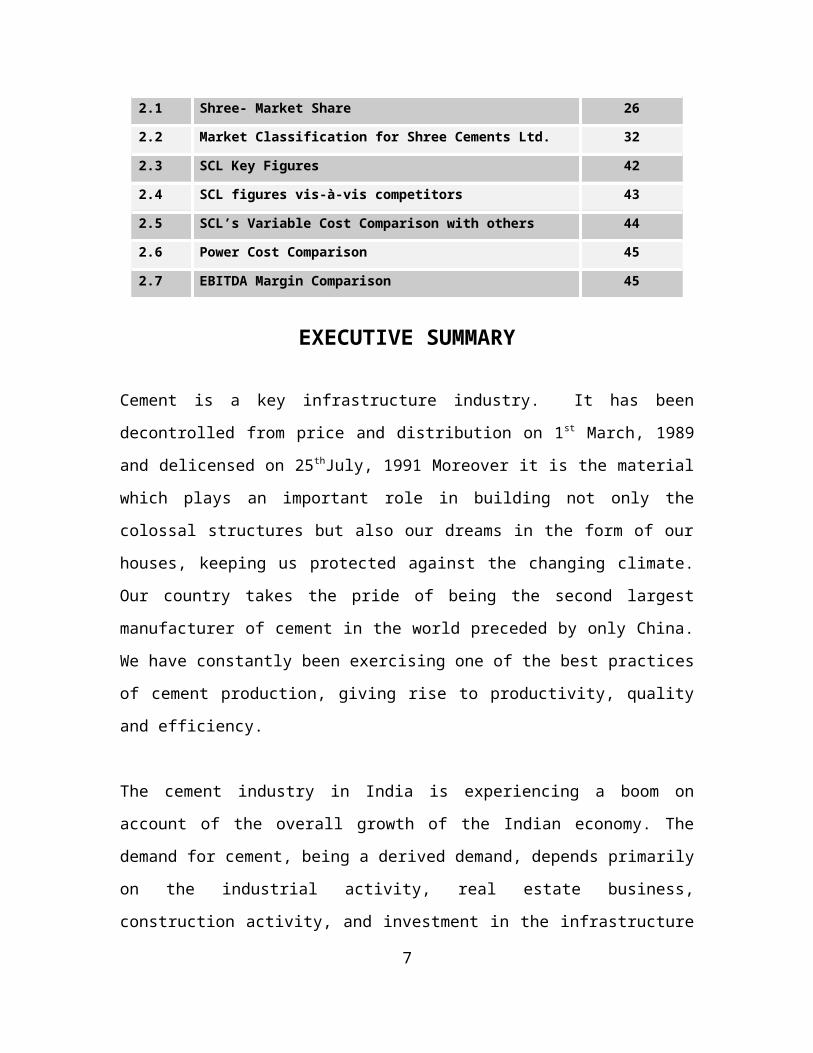

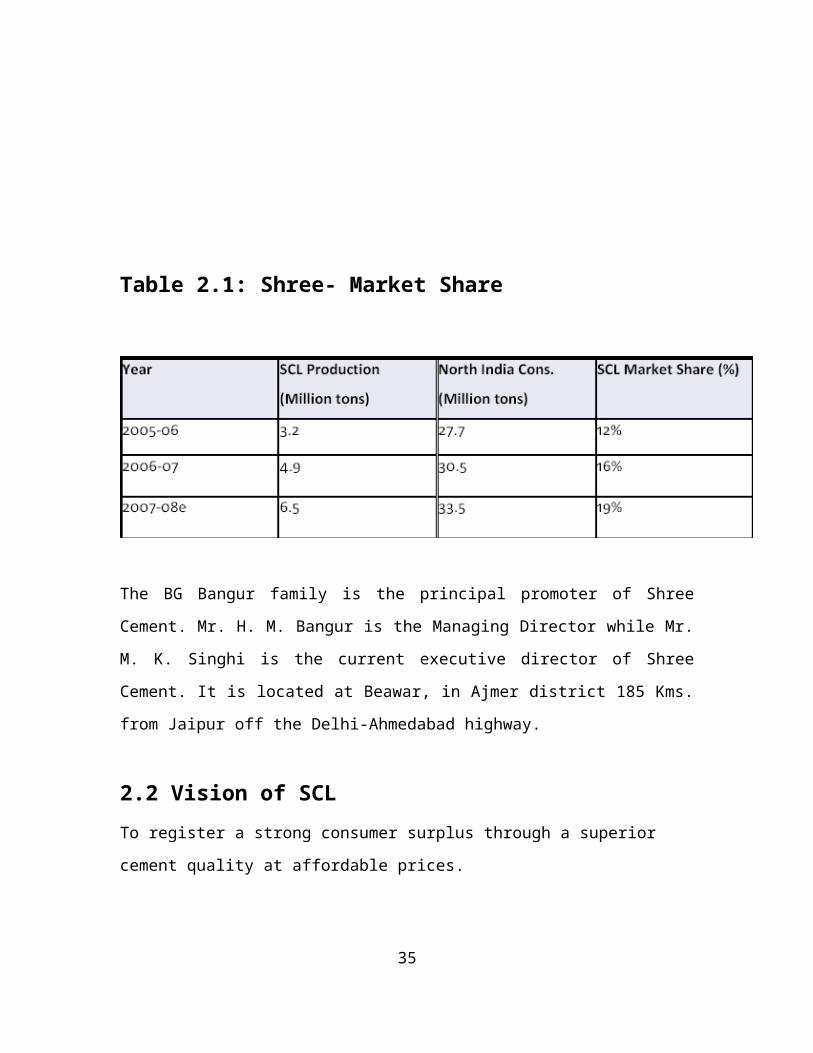

2.1 Shree- Market Share 26

2.2 Market Classification for Shree Cements Ltd. 32

2.3 SCL Key Figures 42

2.4 SCL figures vis-à-vis competitors 43

2.5 SCL’s Variable Cost Comparison with others 44

2.6 Power Cost Comparison 45

2.7 EBITDA Margin Comparison 45

5

EXECUTIVE SUMMARY

Cement is a key infrastructure industry. It has been decontrolled from price and

distribution on 1st March, 1989 and delicensed on 25thJuly, 1991 Moreover it is

the material which plays an important role in building not only the colossal

structures but also our dreams in the form of our houses, keeping us protected

against the changing climate. Our country takes the pride of being the second

largest manufacturer of cement in the world preceded by only China. We have

constantly been exercising one of the best practices of cement production, giving

rise to productivity, quality and efficiency.

The cement industry in India is experiencing a boom on account of the overall

growth of the Indian economy. The demand for cement, being a derived demand,

depends primarily on the industrial activity, real estate business, construction

activity, and investment in the infrastructure sector. India is experiencing growth

on all these fronts and hence the cement market is flourishing like never before.

Indian cement industry is globally competitive because the industry has

witnessed healthy trends such as cost control and continuous technology up

gradation. It is believed that cement demand in India is expected to grow at 10%

annually in the medium term buoyed by housing, infrastructure and corporate

capital expenditures.

As mentioned above, the Indian cement industry is the second largest producer

of quality cement, which meets global standards. The cement industry comprises

more than 50 cement companies with 130 large cement plants with an installed

capacity of 156.26 million tonnes and more than 300 mini cement plants with an

estimated capacity of 11.10 million tonnes making a total installed capacity of

167.36 million tonnes.

6

Continuous technological upgradation and assimilation of latest technology has

been going on in the cement industry. Indian cement industry is modern and

uses the latest technology. India is also producing different varieties of cement

like Ordinary Portland cement (OPC), Portland Pozzolana cement (PPC),

Portland Blast furnace Slag Cement (PBFS), Oil Well Cement, Sulphate

Resisting Portland Cement, White Cement, etc.

Future growth of the industry is belief to be driven by expected GDP growth of

more than 8 percent, growth of the housing sector and the development of roads,

ports, airports and other infrastructure.

This project is pertaining to explore the market perception of Shree cement’s

brand vis-à-vis competitors by taking care of all the components of marketing

mix. Keeping main objective of the study in mind the survey has been done in

jaipur city & local area

The methodology of the study contains interacting with distributors and dealers,

questioning them around the various attributes of the market to collect the facts

about the market scenario of the region and eventually exploring their role in

marketing of company’s brand

For past two months, I have been working as a summer trainee on this project

assigned to me . The idea was to study the importance and role of various

factors of the marketing mix in the cement industry in terms of Quality (Product),

Price, Promotional activities, Services to the dealer and Dealers profitability.

The report also throws light on dealer’s opinions and preferences when it comes

to discounts and benefits offered to them and promotional support provided by

company to help dealers. This information is vital to the company in forming its

strategy and schemes to increase its market share.

7

To start with an attempt was made to understand and diagnose the prevailing

situation of Shree’s cement. Carrying out the industry analysis, competitor’s

analysis, channel analysis and SWOT analysis did it. To get the real market

scenario, a survey of dealers was conducted to get their perception about the

prevailing situation and to find their expectations.

According to dealer’s feedback Quality, Availability and Profit margin are the

factors on which Bangur is rated high.

A positive relationship was seen between Brand image and Quality of the

cement. Along with this there was no significant relationship between the Profit

margin and the sales.

Survey results confirm that SCL has been able to make a mark in market and

perceived to have good quality and also there is a great demand of cement in

market. But survey results also shows that despite of above mentioned positive

factors it has not been able to make a breakthrough in building its brand name

the reason come out to be its low brand awareness (lack of dealer motivation/

meetings/ advertising) and cut-throat in-house brand competition.

To increase the brand awareness aggressive promotion need to be carried out

ensuring its effectiveness in making a mark, also as survey results confirm that

it’s the dealer/mason/contractor who is the ultimate decision maker in choosing a

brand so efforts need to be made to build long term relationship with all these

people. Meetings, gifts, and kit distribution are the best tool to ensure masons

understanding and satisfaction. As dealer play a prominent role in sale of a brand

every possible effort (like training/ plant visit/ additional margin/ sufficient POP

material distribution/ grace period of three days for payment) need to be made a

strong dealer network.

8

PART 1INDUSTRY OVERVIEW

1.1 CEMENT INDUSTRY IN INDIA

Cement industry is a capital intensive and cyclical industry. The demand for

cement is linked to economic activity, can be categorized into two segments,

household construction and infrastructure creation.

The Indian Cement Industry today is the second largest in capacity and

production with an installed capacity of around 157 mtpa after China. The Indian

Industry charted a fast track growth of around 10% per year on an average

during the last decade. Demand has shown an upward surge in recent times

buoyed by housing sector, infrastructure development, and increase in capital

expenditure by corporate and growing retail sector. The cement demand in the

country is expected to grow at an annual rate of 8% for the next five years.

The Indian cement industry is a mixture of mini and large capacity cement plants,

ranging in unit capacity per kiln as low as 10 tonnes per day (tpd) to as high as

7500 tpd. Majority of the production of cement in the country (94%) is by large

plants, which are defined as plants having capacity of more than 600 tpd.

The Industry faces several bottlenecks in high cost of inputs like fuel and power,

high taxes and duties and transportation cost. More than 70% of the input cost in

cement manufacture is beyond the control of the industry and is administered by

regulatory authorities. These include royalties and cess on limestone, tariff for

coal, rail transport and power, duties on finished goods, namely, central excise,

local sales tax, octroi, etc.9

The only areas where industry can induce cost controls and economy are

reduction in consumption of inputs like fuel and power through energy efficiency,

improved productivity through planned maintenance and reduction of stoppages,

etc. The continuous efforts by the industry in these areas have brought in good

results. It is noteworthy that the energy consumption by the most efficient cement

plants in India at the level of 665 Kcal per kg of clinker and 69 kWh per tonne of

cement are comparable with the best achieved in the world.

1.2 Major Players in Indian Cement Industry:

Domestic players:1.) ACC Limited

2.) Ambuja Cements Limited

3.) Birla Corporation Limited

4.) UltraTech Cement

5.) Binani Cement

6.) Shree Cements Limited

7.) India Cements

8.) J K Cement

9.) Grasim

10.) Jaypee Group

11.) Madras Cements

12.) Century Textiles

Major foreign players: 1.) Holcim

2.) Lafarge

3.) Italcementi

10

1.3 PROCESS TECHNOLOGY

1.3.1 Raw Materials for Cement ProductionCement is usually used in mortar or concrete. Here it is mixed with inert material

(called aggregate), like sand and coarse rock. Portland cement consists of

compounds of lime mixed with oxides like silica, alumina and iron oxide.

There are three major raw materials for cement:

1.) LimestoneLimestone is the main raw material and is the source of calcium carbonate.

Calcium carbonate is burnt to obtain calcium oxide (CaO). The other sources of

calcium carbonate are marl, chalk, seashell and coral reef. Limestone is the most

abundant source of CaO. The other user industries for limestone are iron & steel,

fertilizer and chemicals. Cement is the biggest limestone user in

India accounting for over 75-80% of limestone produced in India. The

composition of limestone used by the various sectors varies. For cement, the

CaO content of limestone should be a minimum of 44%. Typically, 1.4-1.5 tonnes

of limestone are required per tonne of clinker. Thus, for a 1 million tonne cement

plant, assured availability of cement grade limestone reserves of the order of 50-

60 mt in the close vicinity is important.

2.) GypsumGypsum is used as a retarding agent. Ground clinker, on contact with water,

tends to set instantaneously because of the very fast reaction between tri-

calcium aluminates and water. In the presence of gypsum, the desired setting

time can be achieved. Gypsum is added to the extent of 5% during the clinker

grinding stage. Gypsum is naturally available in abundance in Rajasthan, Gujarat

and Tamilnadu.11

3.) Granulated Blast Furnace Slag (GBFS) and Fly AshThe other raw materials that are also used in the manufacture of cement are

blast furnace slag (a waste product obtained from iron-smelting furnaces) and fly

ash (leftover ash from a thermal power station). Limestone contains about 52%

of lime and about 80% of this lime is lost during ignition of the raw materials.

Similarly, Clay contributes about 57% silica of which about 25% is lost during

ignition. GBFS is obtained by granulation of slag obtained as a by-product during

the manufacture of steel. It is a complex calcium aluminium silicate and has

latent hydraulic properties. That is why it is used in the manufacture of Portland

blast furnace slag cement.

1.4 PROCESS

1.4.1 Stag es of Cement Production

There are seven stages of cement production at a cement plant:

1. Procurement of raw materials2. Raw Milling - preparation of raw materials for the pyroprocessing system3. Pyroprocessing - pyroprocessing raw materials to form cement clinker4. Cooling of cement clinker5. Storage of cement clinker6. Finish Milling7. Packing and loading

12

Figure 1.1: Cement manufacturing from the quarrying of limestone to the bagging

of cement

While adding fresh capacities, the cement manufacturers are very conscious of

the technology used. In cement production, raw materials preparation involves

primary and secondary crushing of the quarried material, drying the material (for

use in the dry process) or undertaking a further raw grinding through either wet or

dry processes, and blending the materials.

Clinker production is the most energy-intensive step, accounting for about 80% of

the energy used in cement production. Produced by burning a mixture of

materials, mainly limestone, silicon oxides, aluminium, and iron oxides, clinker is

made by one of two production processes: wet or dry; these terms refer to the

grinding processes although other configurations and mixed forms (semi-wet,

semi-dry) exist for both types.

In the dry process, the raw materials are ground, mixed, and fed into the kiln in

their dry state.

In the wet process, the crushed and proportioned materials are ground with

water, mixed, and fed into the kiln in the form of slurry.13

The choice among different processes is dictated by the characteristics and

availability of raw materials. For example, a wet process may be necessary for

raw materials with high moisture content (greater than 15%) or for certain chalks

and alloys that can best be processed as a slurry. The dry process is the more

modern and energy-efficient configuration. In general, the dry process is much

more energy efficient than the wet process, and the semi-wet somewhat more

energy efficient than the semi-dry process. The semi-dry process has never

played an important role in Indian cement production and accounts for less than

0.2% of total production.

In 1960, around 94% of the cement plants in India used wet process kilns. These

kilns have been phased out over the past 46 years and at present, 96.3% of the

kilns are dry process, 3% are wet, and only 1% are semidry process. Dry process

kilns are typically larger, with capacities in India ranging from 300- 8,000 tonnes

per day or tpd (average of 2,880 tpd). While capacities in semi-dry kilns do range

from 600-1,200 tpd (average 521 tpd), capacities in wet process kilns range from

200-750 tpd (average 425 tpd).

Over the last decade, increased preference is being given to the energy efficient

dry process technology so as to obtain a cost advantage in a competitive market.

Moreover, since the initiation of the decontrol process, many manufactures have

switched over from the wet technology to the dry technology by making suitable

modifications in their plants. Due to new, even more efficient technologies, the

wet process is expected to be completely phased out in the near future. Due to

the dominant use of carbon intensive fuels such as coal in clinker making, the

cement industry has been a major source of carbon dioxide (CO2) emissions.

Besides energy consumption, the clinker making process also emits CO2 due to

the calcining process.

14

1.5 TYPES OF CEMENT

There are different varieties of cement based on different compositions according

to specific end uses, namely, Ordinary Portland Cement, Portland Pozzolana

Cement, White Cement, Portland Blast Furnace Slag Cement and Specialised

Cement.

The basic difference lies in the percentage of clinker used.

1.) Ordinary Portland Cement (OPC):OPC, popularly known as grey cement, has 95 per cent clinker and 5 per cent

gypsum and other materials. It accounts for 70 per cent of the total consumption.

2.) Portland Pozzolana Cement (PPC):PPC has 80 per cent clinker, 15 per cent Pozzolana and 5 per cent gypsum and

accounts for 18 per cent of the total cement consumption. It is manufactured

because it uses fly ash/burnt clay/coal waste as the main ingredient.

3.) White Cement:White cement is basically OPC - clinker using fuel oil (instead of coal) with iron

oxide content below 0.4 per cent to ensure whiteness. A special cooling

technique is used in its production. It is used to enhance aesthetic value in tiles

and flooring. White cement is much more expensive than grey cement.

4.) Portland Blast Furnace Slag Cement (PBFSC):PBFSC consists of 45 per cent clinker, 50 per cent blast furnace slag and 5 per

cent gypsum and accounts for 10 per cent of the total cement consumed. It has a

heat of hydration even lower than PPC and is generally used in the construction

of dams and similar massive constructions.

15

5.) Specialised Cement:Oil Well Cement is made from clinker with special additives to prevent any

porosity.

6.) Rapid Hardening Portland cement:Rapid Hardening Portland Cement is similar to OPC, except that it is ground

much finer, so that on casting, the compressible strength increases rapidly.

7.) Water Proof Cement:Water Proof Cement is similar to OPC, with a small portion of calcium stearate or

non- saponifiable oil to impart waterproofing properties.

In India, the different types of cement are manufactured using dry, semi-dry, and

wet processes. In the production of Clinker Cement, a lot of energy is required. It

is produced by using materials such as limestone, iron oxides, aluminium, and

silicon oxides. Among the different kinds of cement produced in India, Portland

Pozzolana Cement, Ordinary Portland Cement, and Portland Blast Furnace Slag

Cement are the most important because they account for around 99% of the total

cement production in India.

The Portland variety of cement is the most common one among the types of

cement in India and is produced from gypsum and clinker. The Ordinary Portland

cement and Portland Blast Furnace Slag Cement are used mostly in the

construction of airports and bridges. The production of white cement in the

country is very less for it is very expensive in comparison to grey cement. In

India, while cement is usually utilized for decorative purposes, marble foundation

work, and to fill up the gaps between tiles of ceramic and marble.

The different types of cement in India have registered an increase in production

in the last few years. Efforts must be made by the cement industry in India and

the government of India to ensure that the cement industry continues innovation

and research to come up with more and more varieties in the near future.

16

1.6 SCALE OF OPERATIONS

The cement industry has witnessed a significant change in the scale of

operations. In 1961, the largest kiln in operation had a capacity of 750 tpd. In

1970, of the total 119 kilns, 1 had over 1,000 tpd capacity, with 55 having less

than 400 tpd capacity. In 1980, 11 of the total 141 kilns were over the 1000 tpd

mark, with 1 kiln having a capacity larger than 3,000 tpd (roughly 1 mtpa). The

1990s saw still higher capacity 4500-5000 tpd (or 1.5 mtpa) kilns. The recent

practice for a large size plant is to have 6,500-7,000 tpd (or 2.5 mtpa) capacity.

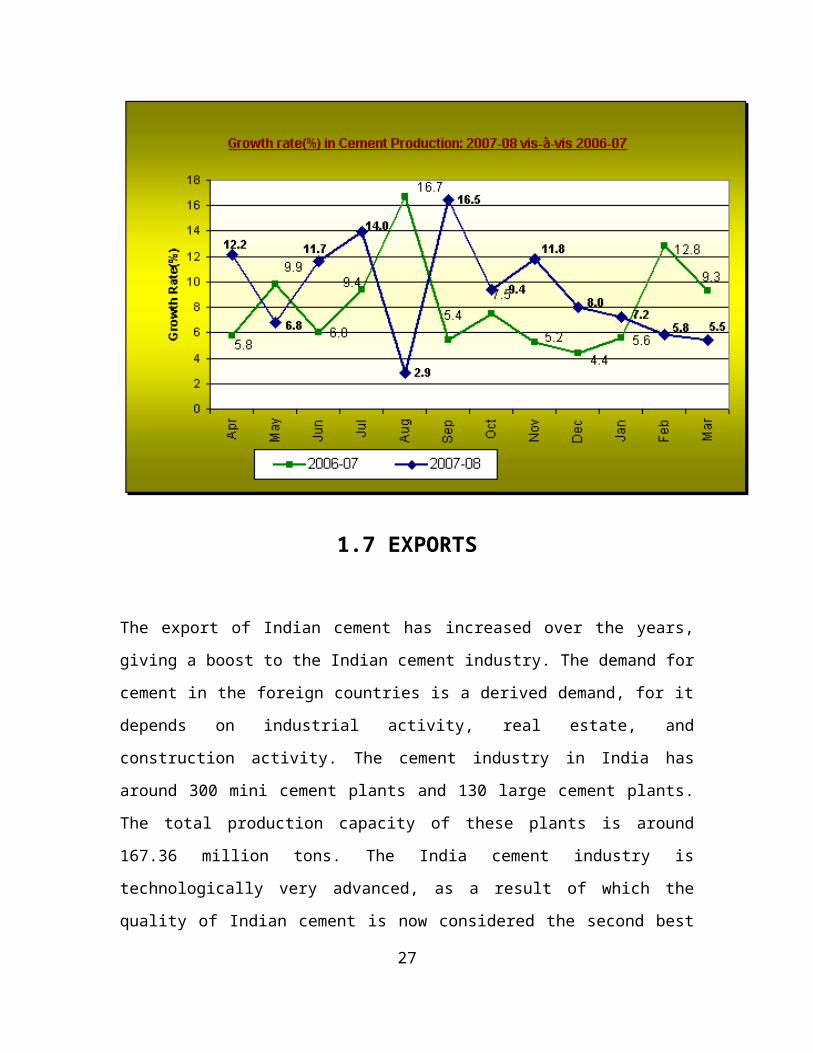

1.6.1 Industrial production:

The cement industry is enhancing its production levels as new homes and offices

are being built, and in keeping with the economy’s annual growth rate. According

to the Cement Manufacturers Association, the overall cement production rose by

8.11 per cent during 2007-08 to 168.29 million tonnes (mt) as against 155.66 mt

and Shree Ultra Ordinary Portland Cement have high consumer recall.

New super premium brand Tuff Cemento produced with German

technology has a lot of expectations.

37

Initiatives for global warming reduction

Pioneered in the application of innovative Electro static precipitator technology in Dg power generation to save fuel and combat pollution, and replaced HSD by LDO.

Achieved unity power factor

… In electrical distribution system to reduce maximum demand, and transmission / distribution losses

Partial utilization of waste heat

… For 3 MW power generation.

Initiator in the use of pet coke for power generation in India

36 MW captive thermal power plant under commissioning to generate quality power for the plant, avoid transmission and distribution losses, and provide surplus power to Rajas than.

SAVINGS: Rs 496.46 Million pa

Development of DD conesIn house development of deduiling cones cyclones resulting in reduction in pressure drop, higher outputs and lower energy consumption.

Single roller press for tow Ball Mills

Capacity enhancement & utilization of CM –2 Roller press for capacity increase and energy saving increase CM –1, Energy saving –2.02 KWH / The

Objective, CSI (Cement sustainability initiative)

1. The purpose of the Cement Sustainability Initiative is to:2. Explore what sustainable development means for the participating

companies and the cement industry.

38

3. Identify and facilitate actions that companies can take as a group and individually to accelerate the move towards sustainable development.

4. Provide a framework through which other cement companies can participate, and

5. Provide a framework for engaging external stakeholders.

Agenda, CSI

The 10 companies involved in the CSI have chosen to develop an agenda for three reasons:To prepare for a sustainable future by making a more efficient use of natural resources and energy, and engaging with lock issues increase emerging market

To meet the expectations of stakeholders and maintain their ‘license to operate’ increase communities across the world through a greater transparency of operations effective engagement with society and initiating action, which lead to sustained positive changes, and

To individually understand and build new market opportunities through process innovation, which achieve greater resource/ energy efficiency and long – term coos savings; product and service innovation to reduce environment impacts and work with other industries on novel uses of – product and waste material in cement production.

The companies have identified six key areas where they believe that the CSI can make a significant contribution towards a more sustainable society:

Climate protection.

Fuels and raw materials.

Employee health and safety.

Emissions reduction.

Local impacts.

Internal business processes.

Productivity39

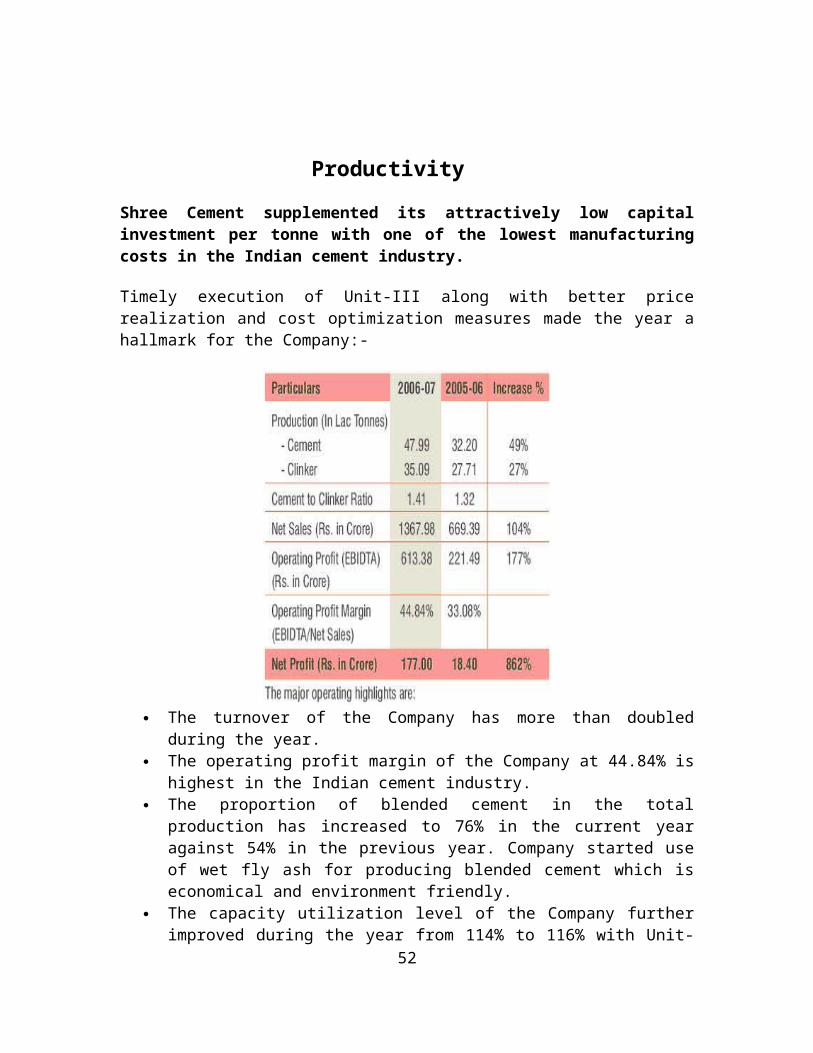

Shree Cement supplemented its attractively low capital investment per tonne with one of the lowest manufacturing costs in the Indian cement industry.

Timely execution of Unit-III along with better price realization and cost optimization measures made the year a hallmark for the Company:-

The turnover of the Company has more than doubled during the year. The operating profit margin of the Company at 44.84% is highest in the

Indian cement industry. The proportion of blended cement in the total production has increased to

76% in the current year against 54% in the previous year. Company started use of wet fly ash for producing blended cement which is economical and environment friendly.

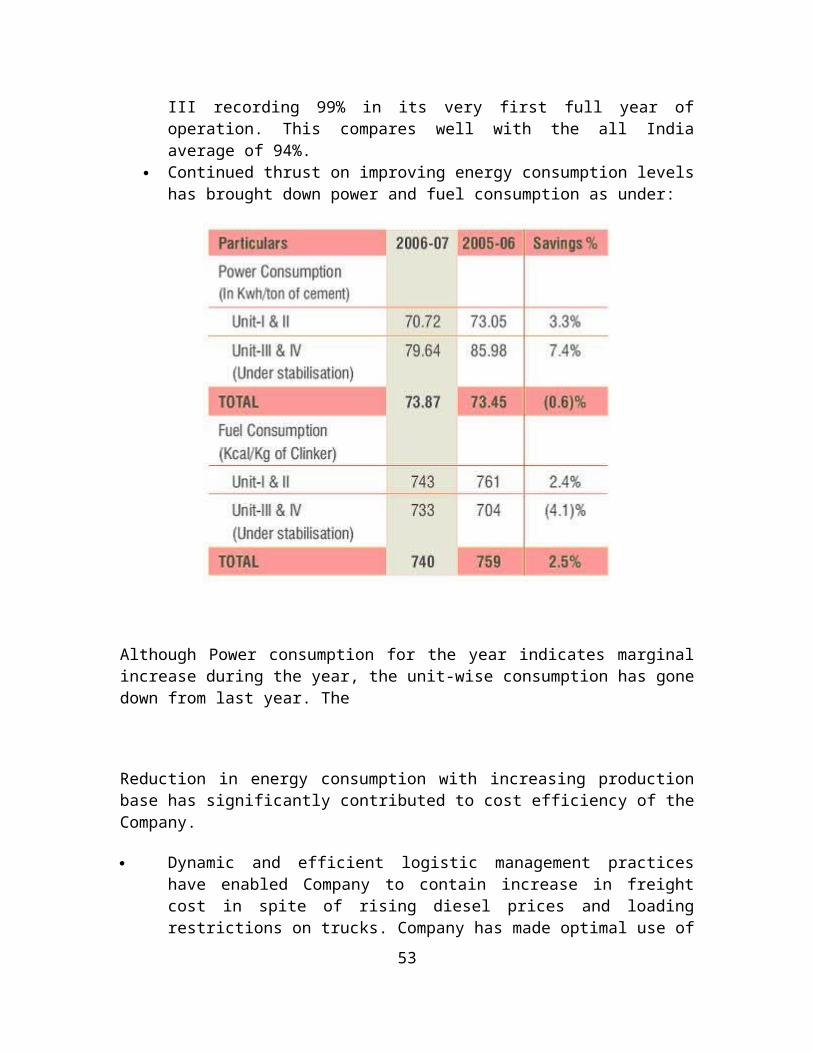

The capacity utilization level of the Company further improved during the year from 114% to 116% with Unit-III recording 99% in its very first full year of operation. This compares well with the all India average of 94%.

Continued thrust on improving energy consumption levels has brought down power and fuel consumption as under:

40

Although Power consumption for the year indicates marginal increase during the year, the unit-wise consumption has gone down from last year. The

Reduction in energy consumption with increasing production base has significantly contributed to cost efficiency of the Company.

Dynamic and efficient logistic management practices have enabled Company to contain increase in freight cost in spite of rising diesel prices and loading restrictions on trucks. Company has made optimal use of its in-house railway sidings facility with appropriate route plan to limit freight cost.

The Company's marketing strategy of maintaining multiple brands competing with each other with a view to garner increased market share has yield good returns. As a result,

Company has retained market leadership status in Rajasthan and Delhi.

41

“Jung Rodhak” brand has further strengthened its presence in its segment in the North India market.

“Bangur Cement” launched last year in the premium quality segment, has been well received in the market and has been improving its market share. Its marketing strategy of appointment of Business associates and Business partners has enabled the Company to keep its debtors levels at zero and minimizing the Working Capital requirement.

Company has introduced another premium quality brand “Tuff Cemento 3556”. The new brand has started attracting customer’s attention and is getting good response.

The proportion of trade sale to total sale increased during the year from 66% to 74% showing higher customer recall and satisfaction.

The Company continued with its highest credit rating of PR1+ for its short-term debt and AA for its long-term debt enabling containment of its cost of funds despite large borrowing requirements for its capital expenditure programme

The interest cost has been kept at a low level in the rising interest rate environment through optimal utilization of funds and judicious mix of rupee and fully hedged foreign currency borrowings.

Timely execution of projects is a hallmark of the Company. The 1.5 MTPA capacity expansion with captive power plant of 18 x 3 MW completed in Feb 08 has been achieved well within the targets both time and budget.

During the year Company has undertaken implementation of an “Enterprise Resource Planning” (ERP) Project with Oracle E-Business Suite to manage its expanding business operations. ERP Project shall help it in improving its business matrices by process optimization, improving logistics and integration across disciplines. The project is expected to be operational in FY 2008-09.

42

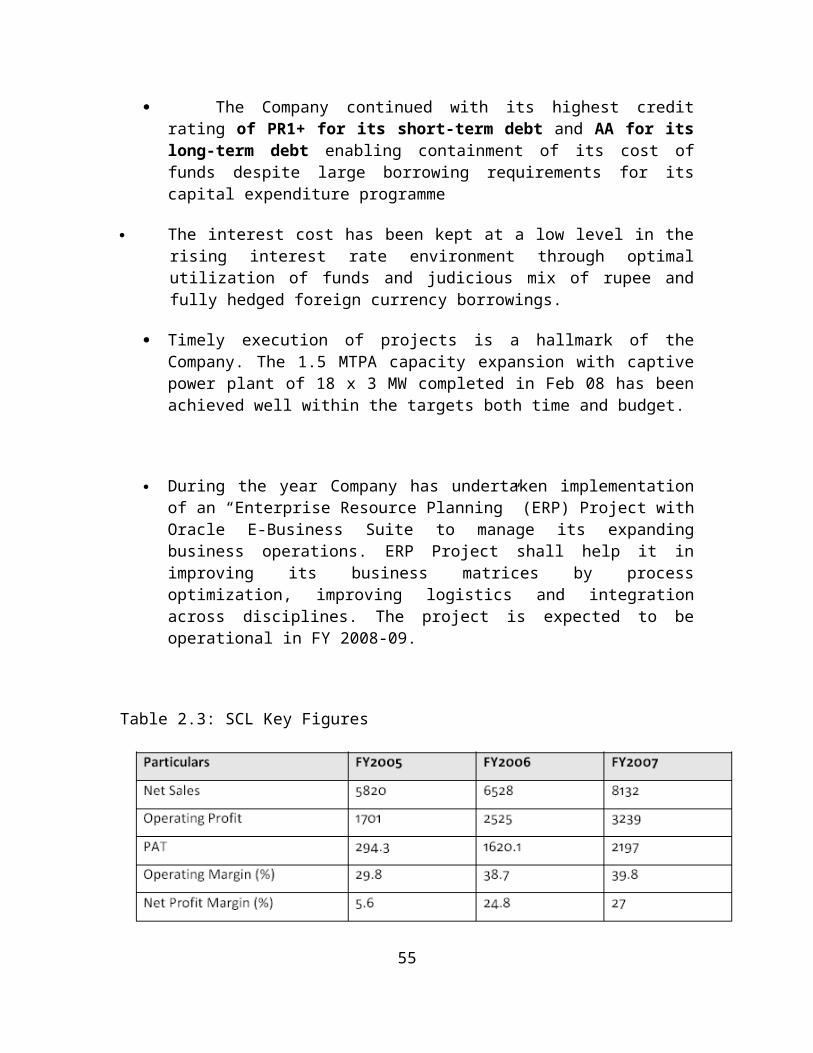

Table 2.3: SCL Key Figures

2.12 Recognition and Awards• Whitehopleman UK - International Cement Consultants have consistently

maintained 4 star rating for Shree since 2000 (No one in the world has been

assigned a 5 star rating!!)

• Excellence in Energy Management Award 2006 from Confederation of Indian

Industry for the second time

• National Awards for Energy Conservation and Best Thermal and Electrical

Energy from

Ministry of Power, Govt of India

• National Safety Awards by Ministry of Labour, Govt. of India

• ICWAI National award 2005 for excellence in cost management

• Golden Peacock Award-2006 &2008 in recognition of its excellent Environment

Management practices

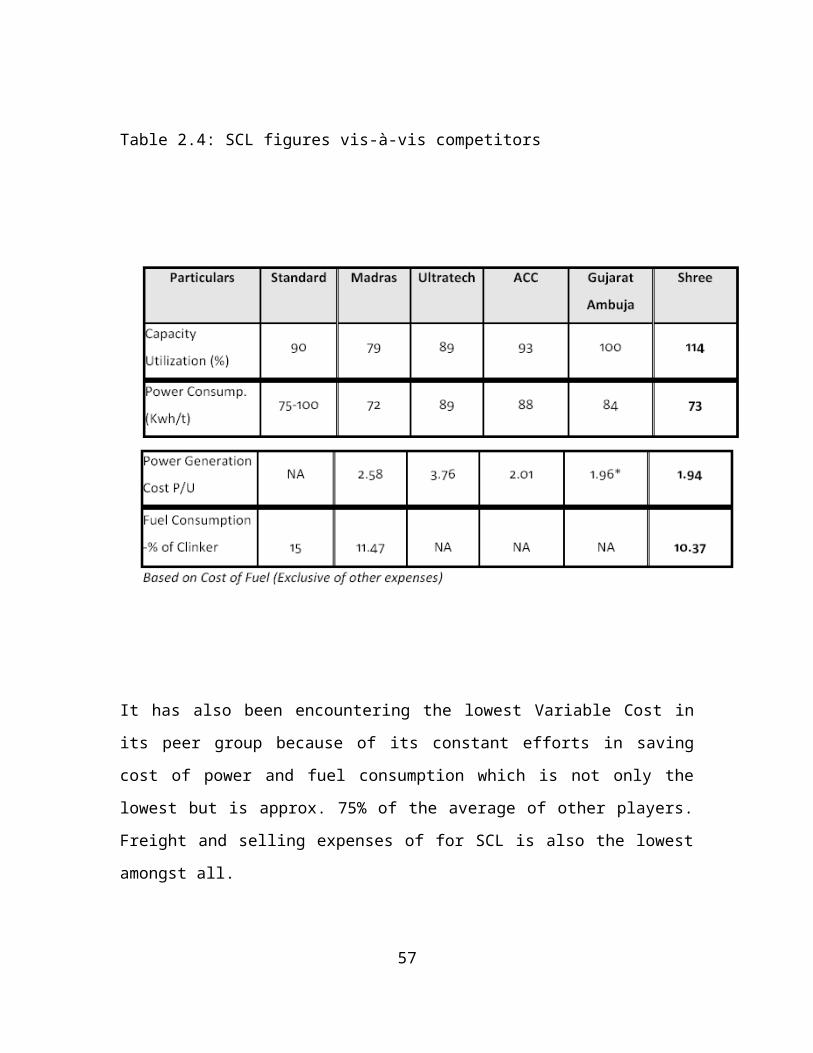

2.13 SCL vis-à-vis CompetitorsSCL has been omnipresent in the performance with various achievements within

a short period of time. Following figures suggests that it has been doing the best

job among its peers in terms of high capacity utilization, low power consumption,

low power generation cost, and low fuel consumption ratio.

43

Table 2.4: SCL figures vis-à-vis competitors

It has also been encountering the lowest Variable Cost in its peer group because

of its constant efforts in saving cost of power and fuel consumption which is not

only the lowest but is approx. 75% of the average of other players. Freight and

selling expenses of for SCL is also the lowest amongst all.

44

Table 2.5: SCL’s Variable Cost Comparison with others

SCL’s ability to produce cement with lowest power consumption and other low

costs of production and raw material procurement has resulted into the top

EBITDA Margin figures for SCL amongst all its competitors.

45

Figure 2.6: Power Cost Comparison

Figure 2.7: EBITDA Margin Comparison

46

2.14 Information Technology at SCLSCL has embraced Information Technology in a big manner and made

investments to establish strong IT infrastructure:

• IT Policy & Quality Standards: SCL has clearly defined IT policy. Backup and

Disaster

Recovery Policy, SCL Internet/Network Access Policy and Business Continuity

Plans have been endorsed and religiously implemented.

• ‘SUMriddhi’ - Shree Enterprise Resource Planning: The Shree ERP

programme, christened ‘SUMriddhi’, was developed deploying Oracle 9i RDBMS

and Developer 2000 platform. A comprehensive ERP program was designed to

integrate all functional modules, namely Financial Accounting & Costing (FA),

Material Management (MM), Personnel and Payroll (PP), Laboratory and Quality

Control, Integrated Management System (IMS) and Raw Material Procurement

(RMP) with the objective to make operations online. The company expects to

implement ERP ‘live’ across the organisation in 2004-05.

• Online operations of Sales and Distribution: Company successfully

implemented the computerization of its sales and distribution functions by

integrating all branches/dealers through a secured connectivity with the plant for

online order processing. In the second phase, necessary enhancements will

make the system work in a centralized manner using dedicated and secure

Virtual Private Network (VPN) across its branch/dealer network.

• SCL’s IT Infrastructure: The Company has a scalable, state-of-the-art IT

network infrastructure, with optic fibre cable-based gigabit backbone, high-end

layer 3 switches, Cisco routers and IBM corporate-computing servers. Shree has

a secure network across its corporate and site locations with e-trust firewall

supplemented with intrusion detection system and Active Virus Defense Solution

47

from Network Associates. The organisation is provided with the latest computing

tools in hardware and software.

• SCL’s corporate website: The Company launched its content-exhaustive

corporate website shreecement.com on 1 August 2003. The portal is dynamic,

informative and user-friendly with a menu-driven interface. The website contains

the latest information about the company with news flashes and a photo gallery.

The website is e-commerce enabled, which provides access to customers on

their latest account statement and vendors/ suppliers on order positions for the e-

procurement program.

• E-Procurement: Shree implemented an e-procurement programme to facilitate

purchases through the reverse auction process to maximize price benefits and

transparency.

• Paperless office: Shree is moving towards the ultimate goal of achieving a

paperless office environment through a widespread use of e-mails and instant

messaging for daily communication across all its offices. A program was

undertaken for storing and cataloguing the huge archive of blueprints of technical

drawings in a digitised form for instant accessibility.

• Raw material procurement: The entire raw material procurement operation

was integrated with ‘SUMriddhi’ - Shree ERP, to increase efficiency and control.

• Training: Shree is committed to enhance the IT skills of not only employees

across all functions but their family members as well. As a result, training is an

ongoing process and more than 200 personnel were imparted training across

departments.

• Online Knowledge management: Shree has launched a platform for sharing

knowledge across the enterprise. A knowledge management tool was developed

48

and implemented through which people across all levels can contribute and

share achievements, domain expertise, social and cultural ideas. This also

provides a ‘public folder’ for up-to-date information on the cement industry and

the company.

• Network Security: SCL network is protected by the high end e-Trust Firewall

from Computer Associates and Network Associates Intrusion Detection System

(IDS). SCL has implemented Network Associates Active Virus Defence for virus

protection and SPAM control. All network resources are protected by adopting

strong password policies. SCL has enforced three-layer security for all data and

information systems.

2.15 Bangur Cement – SCL’s Premium Brand

Bangur cement started with a vision to be the most effective and efficient cement

brand of the country. As in Bangur cement, SCL aimed at providing the best

quality cement that ensures customer satisfaction. The Bangur cement is

advertised with a tagline saying “The best, not inexpensive”.

To serve the fast growing National Capital Region (NCR) with immediate and

prompt services, Bangur cement is establishing a grinding capacity at Khuskhera

in Alwar District of Rajasthan, which is just 80 kms away from the capital.

Excelling in the quality, price, availability and packaging of the product, SCL

aspires to be the first choice of the consumers. The Bangur cement plant is one

of the most modern and sophisticated plants in the India equipped with state-of-

the-art German Technology.

49

Following factors makes Bangur cement, the SCL’s premium brand:

Best Quality of Lime Stone: The Ras belt is among the finest quality

limestone deposits in India. Importantly, it is a single source of limestone

belt where all necessary ingredients of cement are available in limestone

and there is no dependency on outside sources, thus enabling

consistency in quality.

Better Quality Control, Clinkerisation and superior cement grinding

makes the quality of the brand one of the best in the industry. State-of-the-art technology: The plant has been set up in the technical

collaboration with internationally acclaimed German cement manufacturer.

In line with its marketing strategy, Bangur cement realized sales predominantly in

the trade segment. The brand contribution to more then 40% of the trade sale of

the company, registering 14.20 Lac MT sales out of the total of 35.92 Lac MT .In

fact , trade sales accounted for 95% of total sales of BANGUR CEMENT while

non trade sales was just 5%. BANGUR CEMENT registered its 55% sales of its

total sales in its home market, Rajasthan. By selling within a smaller radius, the

company was able to notch higher net realization because of lower logistics.

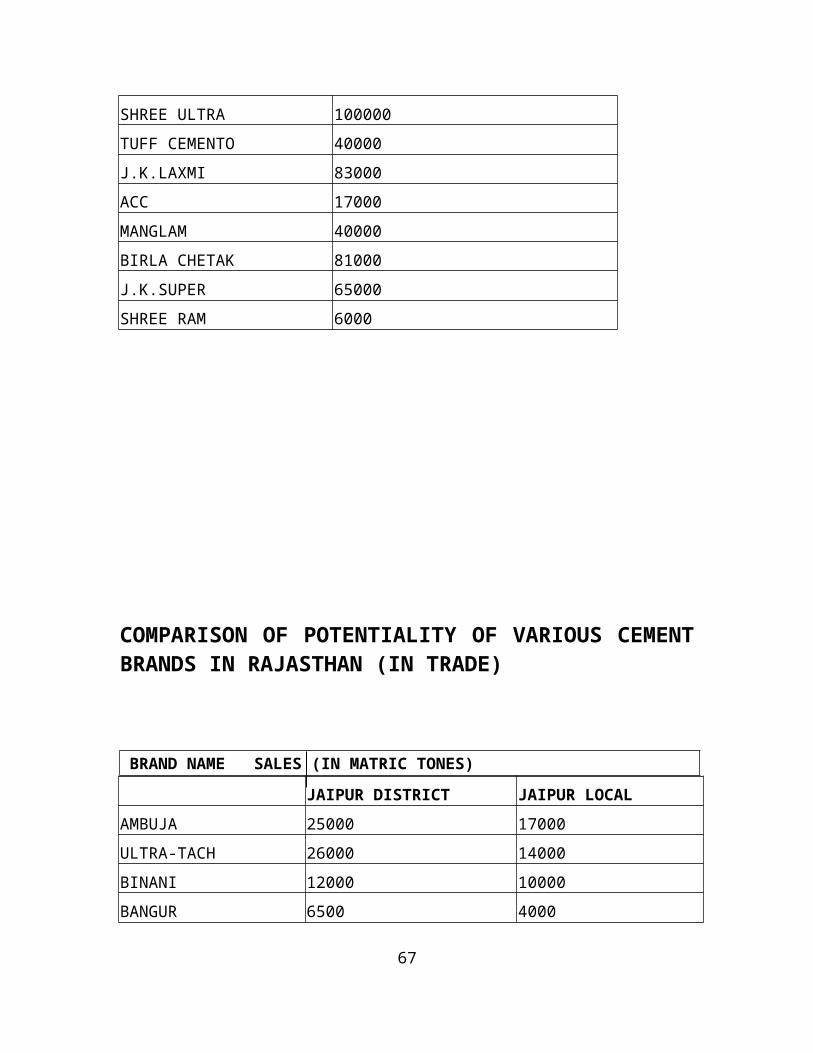

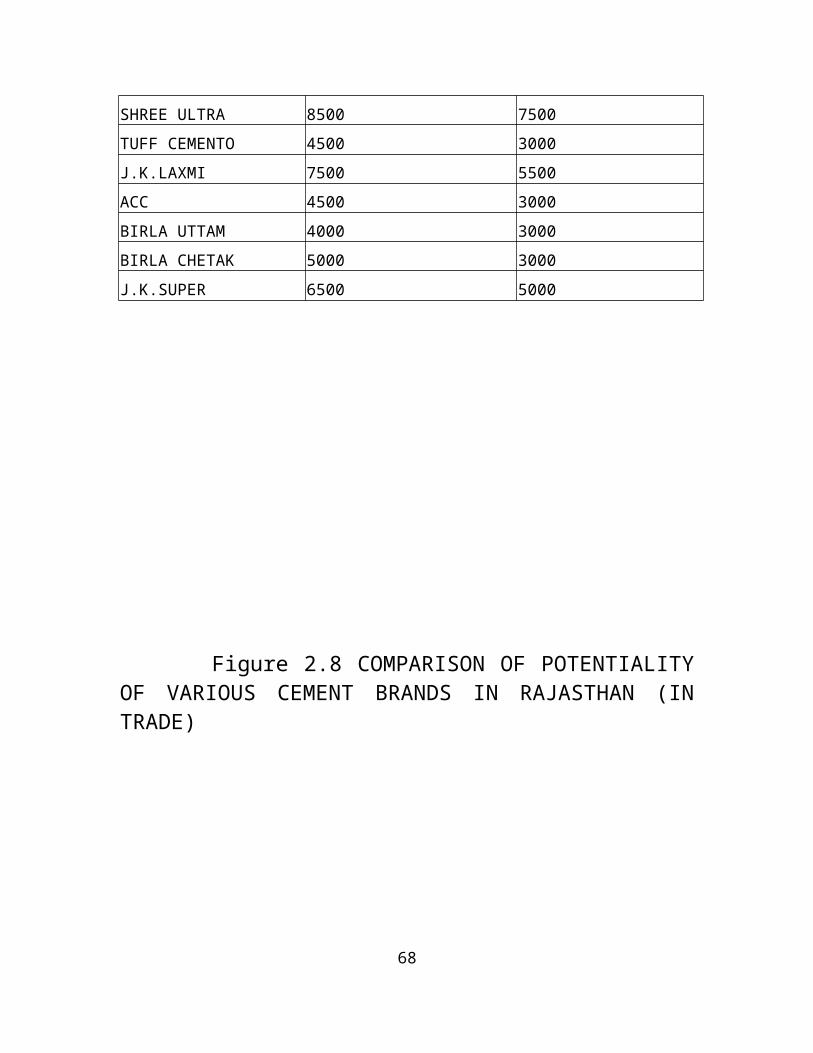

2.16 COMPARISON OF POTENTIALITYOF VARIOUS CEMENT BRANDS

COMPARISON OF POTENTIALITY OF VARIOUS CEMENT BRANDS IN RAJASTHAN

BRAND NAME SALES (IN MATRIC TONES)

AMBUJA 121000

ULTRA-TACH 145000

BINANI 103000

BANGUR 55000

SHREE ULTRA 100000

TUFF CEMENTO 40000

J.K.LAXMI 83000

ACC 17000

MANGLAM 40000

BIRLA CHETAK 81000

J.K.SUPER 65000

SHREE RAM 6000

51

COMPARISON OF POTENTIALITY OF VARIOUS CEMENT BRANDS IN RAJASTHAN (IN TRADE)

BRAND NAME SALES (IN MATRIC TONES)

JAIPUR DISTRICT JAIPUR LOCAL

AMBUJA 25000 17000

ULTRA-TACH 26000 14000

BINANI 12000 10000

BANGUR 6500 4000

SHREE ULTRA 8500 7500

TUFF CEMENTO 4500 3000

J.K.LAXMI 7500 5500

ACC 4500 3000

BIRLA UTTAM 4000 3000

BIRLA CHETAK 5000 3000

J.K.SUPER 6500 5000

52

Figure 2.8 COMPARISON OF POTENTIALITY OF VARIOUS CEMENT BRANDS IN RAJASTHAN (IN TRADE)

53

PART-3

MARKET RESEARCH

3 MARKETING RESEARCH

Marketing research in the systematic gathering, recording and analyzing of data about problems connected with the market place i.e. H.P’s in order to find justified solutions for the problem.

IMPORTANCE

Consumer oriented marketing.

Effective managerial decision.

Identification of opportunities.

Reduces risk.

Stimulates sales.

Assessment of real image of company.

Integrating the company and consumer interest.

54

3.1 CLASSIFICATION OF MARKETING REASEARCH

1. Research on consumer

Studying consumer tastes, reactions and brand preference. Customer satisfaction study.

2. Research on market

Study on market size / potential / market growth.

Study on market segment.

Detailed market surveys.

3. Research on distribution:

Measuring dealer reaction to the company and its products and services.

Distribution cost Analysis.

4. Research on advertising effectiveness.

Studies on advertising effectiveness.

Studies on media.

Assessing and effectiveness and ad impact.

Studies on sales promotion effectiveness.

55

3.1.1 PROCESS OF MARKETING RESEARCH

PROBLEM FORMULATION

DETERMINATION OF RESEARCH OBJECTIVE

PLANNING AND CONDUCTFORMAL INVESTIGATION

COLLECTION OF PRIMARY DATA

DATA PROCESSING ANALYSIS AND INTERPRETATION

REPORT WRITING

FOLLOW UP

56

3.2 RESEARCH METHODOLOGY

3.2 RESEARCH METHODOLOGY

Research definition:

Research is a process of systematic and in – depth study or search for any particular topic, subject by collection, compilation, presentation and interpretation of relevant details or data.

Research refers to a search of knowledge. It is a scientific and systematic search for pertinent information on a specific topic.

It is an art of scientific investigation.

Movement from known to unknown.

Voyage of discovery.

Original contribution to the existing socks of knowledge making for its advancement.

The main aim of the project was to find out the market share of SCL and it’s customers with respect to Jaipur (Rajasthan). The opinions of the customers were taken by visiting various places and information was collected from the customers.

57

3.2.1 DATA COLLECTION:

Data collection is the heart of all marketing research.It is an elaborate process through which the researcher makes a planned search for all relevant data and gathers the entire data required for the assignment.

Primary data source:

1. Observation

2. Interview: -

3. Questionnaire:

The project was started from the questionnaire. The questions are asked to respondents about their experiences towards SCL’S Brands and other competitors. The survey was conducted to know the market potential and market share for two-wheeler segment. Questionnaire contains both open ended and close-ended question.

Secondary data source:

1. Internet:For this purpose different web sites have been used some of those are: -

www.google.com www.shreecement.com

2. Newspapers

3. Reference book-

58

Sampling method: -

1. Probability / random sampling method

2. Non-probability sampling method

For research purpose of project researcher selected the probability sampling. The population for our project was very large; it was not possible to meet every one so researcher select simple random sampling. Researcher had covered the Jaipur city.

Sample size: -

As considering the coverage of researcher takes the sample size as about 150 dealers and divided this sample in equal strength to give same weight age for all area

Statistical technique used: -

Here I have used Bar chart & pie chart

Scaling technique used: -

For this purpose I have used different response of the customers like – excellent, satisfied, Not Satisfied. Other response is Good, Poor, Can’t say.

Excellent

Very Good

Good

59

Poor

3.2.2 AREAS COVERED

Any study that is conducted has a scope. The scope here signifies the geographical limits within which the study will be carried discrepancies in the study due to a large number of extraneous variables in the area.

The market survey was conducted on the dealers, sub-dealers of cement brands to measure the most potential brand in jaipur territory.

The study was under SCL’S BRANDS jaipur. The geographical scope of my study was limited to the area of jaipur territory where by different area were covered.

Mansarovar

Jagatpura

Pratap Nagar

Prithviraj Nagar

C-scheme

Vidhyadhar Nagar

Sirsi road

60

3.2.3 DATA ANALYSIS

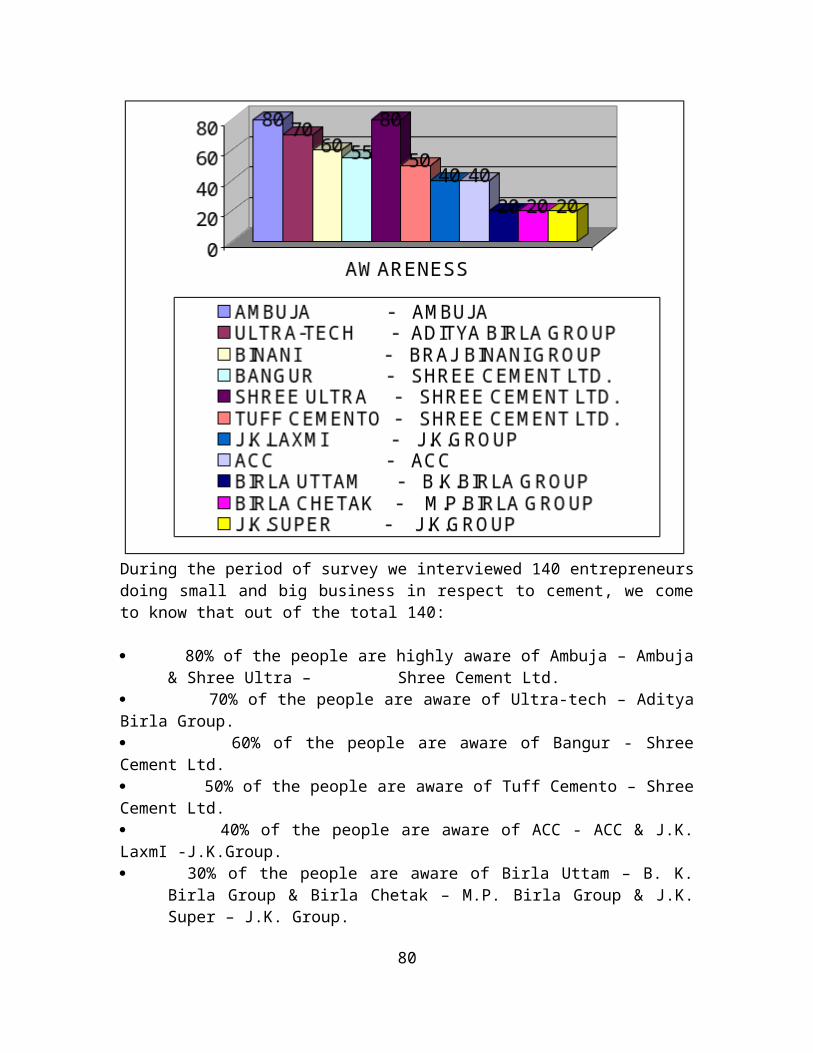

Q.1 Name the current cement brands you are aware of?

AWARENESS

During the period of survey we interviewed 140 entrepreneurs doing small and big business in respect to cement, we come to know that out of the total 140:

90% of the people are highly aware of Ambuja. 85% of the people are aware of Ultra-tech & Binani. 80% of the people are aware of Bangur & Shree Ultra. 65% of the people are aware of Tuff Cemento. 40% of the people are aware of ACC & J.K.Laxmi. 30% of the people are aware of Birla Uttam & Birla Chetak & J.K.Super.

61

Q.2 Name of the company of the brand you are aware of?

During the period of survey we interviewed 140 entrepreneurs doing small and big business in respect to cement, we come to know that out of the total 140:

80% of the people are highly aware of Ambuja – Ambuja & Shree Ultra – Shree Cement Ltd.

70% of the people are aware of Ultra-tech – Aditya Birla Group. 60% of the people are aware of Bangur - Shree Cement Ltd. 50% of the people are aware of Tuff Cemento – Shree Cement Ltd. 40% of the people are aware of ACC - ACC & J.K. LaxmI -J.K.Group. 30% of the people are aware of Birla Uttam – B. K. Birla Group & Birla

Chetak – M.P. Birla Group & J.K. Super – J.K. Group.

62

Q.3 Name the brands you deal with?

DEALING

In respect of dealing with cement brand, we found that out of the total 140 respondents: - 50%of the people are dealing with ultra-tech. 40%of the people are dealing with Ambuja & Binani 30%of the people are dealing with Bangur. 20%of the people are dealing with Shree Ultra 10%of the people are dealing with Tuff cemento & J.K. Laxmi. 5%of the people are dealing with ACC, Birla Uttam, and Birla Chetak,

J.K. super.

63

Q.4 You are authorized dealer of ?

AUTHORISED DEALER

From the following 140 respondents, it was analyzed that authorized dealer pertaining to various cement brands have been distributed as follows: - 25 Authorized dealer of Ultra-tech. 15 Authorized dealers of Ambuja & Binani. 10 Authorized dealer of Shree Ultra & Tuff Cemento. 5 Authorized dealer of Bangur & J.K. Laxmi. 4 Authorized dealer of ACC. 2 Authorized dealer of Birla Uttam, Birla Chetak & J.K. Supers.

64

Q.5 Rank the following brands in quality terms:

TWO CATEGERY IN THE QWALITY (A & B)

CATEGEY (A)

Also. In respect of quality of products it was observed that: According to 55% people, of Ambuja is excellent. Around 45% People told that quality of Ultra-tech & Binani is very good. Around 20% of people told that quality of Bangur is very good. 10% people told that quality of Shree Ultra & Tuff Cemento is good. 5&4% J.K. Laxmi, ACC, Birla Uttam, Birla Chetak & J.K. Super is average.

65

CATEGORY (B)

Also. In respect of Second quality of products it was observed that:

According to 30% people, of Ambuja & Ultra-tech is second-class quality.

Around 50% People told that quality of Binani & Bangur is second-class quality.

Around 40% of people told that quality of Shree Ultra, Tuff Cemento & J.K. Laxmi is Second class quality.

10% J.K. Laxmi, ACC, Birla Uttam, Birla Chetak & J.K. Super is average quality of this product.

66

Q.6 Have you seen the TV advertisement of cement brand’s?

TV ADVERTISMENT

90% of the people had seen the TV advertisement of Ambuja. 70% of the people had seen the TV advertisement of Ultra-tech. 45% of the people had seen the TV advertisement of Bangur & Binani. 20% of the people had seen the TV advertisement of Shree Ultra & J.K.

Laxmi. 30% of the people had seen the TV advertisement of Tuff Cemento. 5% of the people had seen the TV advertisement of Birla Uttam & Birla

Chetak, J.K.Super & ACC.

67

Q.7 Rank the following brands in price terms:

Two category ‘A’ & ‘B’

CATEGORY ‘A’

Also. In respect of PRICE of products it was observed that: According to 70% people told that price of Ambuja is very high price than

other brands.

Around 35% People told that price of Ultra-tech & Binani is very high.

Around 7% of people told that price of Bangur Shree Ultra & Tuff Cemento, J.K. Laxmi is high.

2% of the people told that price of ACC, Birla Uttam, and Birla Chetak & J.K. Super is high.

68

CATEGORY ‘B’

Also. In respect of PRICE of products (in ‘B’ Category) it was observed that: According to 60% people told that price of Binani & Bangur are include in

second price than other brands.

Around 45% People told that price of Ultra-tech & Shree Ultra & Tuff Cemento price are normal than other brand’s.

Around 30% of people told that price of Ambuja, J.K. Laxmi is average.

10% of the people told that price of ACC, Birla Uttam, Birla Chetak & J.K. Super price are low.

3.2.4 FINDINGSAWARENESS

69

Ambuja, Ultra-Tech, Binani, Bangur & Shree Ultra are highly aware brand in jaipur city.

Tuff Cemento, J.K. Laxmi, Birla Uttam Birla chetak, J.K. Super & ACC are also reasonable awared.

AWARENESS OF COMPANY WITH BRANDS

Ambuja, Ultra-Tech, Binani, Bangur & Shree Ultra & Tuff Cemento are highly aware of brand with company in jaipur city.

J.K. Laxmi, Birla Uttam Birla chetak, J.K. Super & ACC are also reasonable awared.

DEALING

Maximum dealers are dealing with Ambuja, Ultra-Tech, and Binani & Bangur.

Mainly dealers are dealing with multiple brands.

Retailers having good sale are authorized dealer of a company.

QUALITY

Ambuja, Ultra-Tech & Binani are considered to be best quality product.

Shree Ultra, Bangur, Tuff Cemento, J.K. Laxmi, Birla Uttam Birla chetak, J.K. Super & ACC are also among good perception about quality.

PRICE

Ambuja, Ultra-Tech & Binani are considered to be best price product in the market (higher price than other product).

Shree Ultra, Bangur, Tuff Cemento, J.K. Laxmi, Birla Uttam Birla chetak, J.K. Super & ACC are also normal price in the market.

PART-4 QUESTIONNAIRE

70

QUESTIONNAIRE

Name of shop _____________________________

Owner of Shop ____________________________

Address ______________________________

Dealership _______________________________

Q.1 Name the current cement brands you are aware of?(A) Ambuja (B) Ultra-tech(C) Binani (D) Bangur(E) Shree Ultra (F) Tuff Cemento(G) J.K.Laxmi (H) ACC (I) Birla Uttam

Q.2 Name of the company of the brand you are aware of?(A) Ambuja (Ambuja)(B) Aditya Birla Group (Ultra-tech)(C) Barj Binani Group (Binani)(D) Shree Cement Ltd (Bangur)(E) Shree Cement Ltd (Shree Ultra)(F) Shree Cement Ltd (Tuff Cemento)(G) J.K. Group (J.K.Laxmi)(H) ACC (ACC)(I) B.K. Birla Group (Birla Uttam)(J) M.P. Birla Group (Birla Chetak)(K) J.K. Group (J.K. Super)

Q.3 Name the brands you deal with?(A) Ambuja (B) Ultra-tech(C) Binani (D) Bangur(E) Shree Ultra (F) Tuff Cemento(G) J.K.Laxmi (H) ACC(I) Birla Uttam

Q.5 Rank the following brands in quality terms:Two category ‘A’ & ‘B’(A) Ambuja (B) Ultra-tech(C) Binani (D) Bangur(E) Shree Ultra (F) Tuff Cemento(G) J.K.Laxmi (H) ACC (I) Birla Uttam (J) Birla Chetak(K) J.K.Super

Q.6 Have you seen the TV advertisement of cement brand’s? (A) Ambuja (B) Ultra-tech(C) Binani (D) Bangur(E) Shree Ultra (F) Tuff Cemento(G) J.K.Laxmi (H) ACC(I) Birla Uttam (J) Birla Chetak(K) J.K.Super

Q.7 Rank the following brands in price terms:Two Category ‘A’ & ‘B’(A) Ambuja (B) Ultra-tech(C) Binani (D) Bangur(E) Shree Ultra (F) Tuff Cemento(G) J.K.Laxmi (H) ACC(I) Birla Uttam (J) Birla Chetak(K) J.K.Super

DEALERS / SUBDEALERS REPORT

72

S NO.

NAME OF FIRM WITH ADDRESS

NAME OF OWNER

DEALER /SUBDEALE

R

SALE (P/M) BRAND

1 MAIHTA BUILDING MATERIAL & SUPPLAIR

(SHIRSHI ROAD)

MAHESH JI SUBDEALER 2000BAGE TUFF CEMENTO & JK LAXMI

2 RAKESH BUILDING MATERIAL & SUPPLAIR (MEENA WALA SHIRSHI