29

CPA Practices NAICS: 541211 SIC: 8721 prepared July 10th, 2018

CPA PracticesNAICS: 541211

SIC: 8721

prepared July 10th, 2018

Table of ContentsIndustry Forecast and Structure 3

How Firms Operate 5

Working Capital 6

Capital Financing 8

Bank Product Usage 9

Risks to Watch Out For 11

Industry Trends 13

Quarterly Insight 16

Web Links 22

Business Valuation 23

Just the Numbers 25

© 2017 Vertical IQ, Inc. or its licensors, all rights reserved.

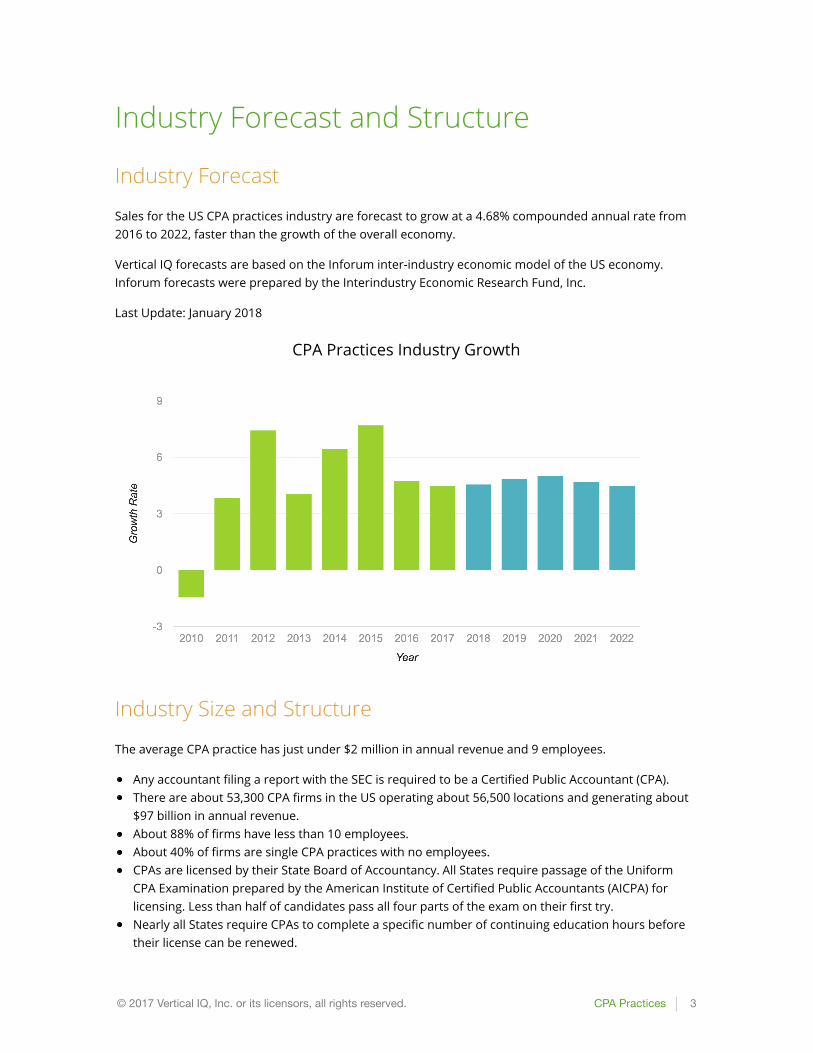

Industry Forecast and Structure

Industry Forecast

Sales for the US CPA practices industry are forecast to grow at a 4.68% compounded annual rate from2016 to 2022, faster than the growth of the overall economy.

Vertical IQ forecasts are based on the Inforum inter-industry economic model of the US economy.Inforum forecasts were prepared by the Interindustry Economic Research Fund, Inc.

Last Update: January 2018

CPA Practices Industry Growth

Industry Size and Structure

The average CPA practice has just under $2 million in annual revenue and 9 employees.

Any accountant filing a report with the SEC is required to be a Certified Public Accountant (CPA).There are about 53,300 CPA firms in the US operating about 56,500 locations and generating about$97 billion in annual revenue.About 88% of firms have less than 10 employees.About 40% of firms are single CPA practices with no employees.CPAs are licensed by their State Board of Accountancy. All States require passage of the UniformCPA Examination prepared by the American Institute of Certified Public Accountants (AICPA) forlicensing. Less than half of candidates pass all four parts of the exam on their first try.Nearly all States require CPAs to complete a specific number of continuing education hours beforetheir license can be renewed.

© 2017 Vertical IQ, Inc. or its licensors, all rights reserved. CPA Practices 3

The business structure of CPA practices is 12% corporations, 55% S-corporations, 17% individualproprietorships, and 15% partnerships.26% of CPA practices are female-owned and 12% are minority-owned.

CPAPractices53,300 practices

SUPPLIERS

Office Supplies

IRS Regulations

FASB Standards

Information Technology

NEWENTRANTSAccounting Graduates

Foreign Outsourcing Firms

SUBSTITUTESTax Preparation Software

Accounting Software

BUYERS

Public Firms

Private Firms

Non-profit Organizations

Individuals

© 2017 Vertical IQ, Inc. or its licensors, all rights reserved. CPA Practices 4

How Firms OperateKEY CPA PRACTICE METRICS: Net Remaining Per Owner: $248,000 Net Client Fees/FTE Professional: $182,000 Utilization Rate: 70% Realization Rate: 86%

Best Practices

Developing expertise in specific vertical markets or services.Training all staff members that marketing is part of their job and making them aware of the firm’sservices and types of clients.Expanding value-added consulting services as a “trusted advisor” to clients.Investing in continuing education to keep staff up-to-speed on changes in regulations.Using information technology to increase staff productivity and client collaboration.Taking advantage of “cloud computing” to save money and eliminate management of servers.Using part-time staff to manage seasonal demand.Reducing work-in process (WIP) through more frequent billing.Accepting credit cards from individuals and small businesses to reduce collection issues.

© 2017 Vertical IQ, Inc. or its licensors, all rights reserved. CPA Practices 5

Working CapitalSell and invoice

New engagements are sold by partners or designated "rainmakers" within the practice. Firms relyheavily on existing clients for referrals and banks for new business. Likewise, CPA practices are anexcellent source of referrals for bankers. On average, firms only spend about 1% of net client fees(revenue) on marketing activities. For auditing or accounting work, firms typically prepare a formalproposal to bid on the project.

CPA firms often have high work-in-process (WIP) - hours worked for a client that are not yet invoiced.Small jobs, such as tax returns, are billed upon completion. Progress payments may be invoiced forlarger jobs. These are tied to specific milestones or percentages of the total estimated hours for thejob. An upfront retainer fee may be requested for certain jobs or clients, particularly if the firm has tohire or contract out for special expertise.

Collect

CPA firms have very little bad debt, but may be forced to lower their billing rates to facilitate clientpayment. Collection periods average 13 to 28 days, though a significant amount of receivables canextend over 90 days. When write-offs occur, they are often caused by clients going out of business.

Manage Cash

CPA practices face seasonal demand for tax services, which accounts for about a third of revenues andpeaks in February, March and April. They build cash reserves during this time. Firms may rely on linesof credit to meet expenses during slow months, such as January and the summer months.

Pay

The main expenses for CPA practices are payroll and occupancy costs. Salaries for employees average26-28% of revenue. Rent is typically about 4-5% of revenue. Other expenses include computer andphone systems, reference materials on tax laws and accounting standards, and insurance.

Report

CPA firms typically monitor hours and fees charged to clients on a weekly, or even daily, basis. Practicemanagement systems collect staff hours worked by client project and use standard billing rates tocalculate fees. Besides client fees versus plan, firms also track the utilization rates of employees,realization rate, client retention rate, work in progress, accounts receivable, and the staff-to-partnerratio.

Cash Management Challenges

Revenue Seasonality

© 2017 Vertical IQ, Inc. or its licensors, all rights reserved. CPA Practices 6

Demand for CPA services is seasonal, with peaks tied to tax deadlines and year-end reporting. CPAfirms require additional staffing and work long hours during busy seasons, but face cash shortfalls tomeet monthly expenses during slow periods. Firms rely on cash reserves or lines of credit to coverexpenses during these slow months.

Timely Billing

CPA practices typically rely on partners to determine when to bill clients for work performed. Whenpartners are busy, billing can be delayed and work-in-process levels grow. To ensure timely billing,many firms are tracking WIP daily and implementing more frequent billing policies. Some have movedbilling responsibility to the firm’s financial manager.

Billing Disputes

Clients may balk at the amount of fees charged for a project, particularly during a weak economy.Disputes over the hours charged for work delays collection and often results in discounted charges.Doing a better job up-front setting client expectations about fees can help avoid billing disputes.

© 2017 Vertical IQ, Inc. or its licensors, all rights reserved. CPA Practices 7

Capital FinancingCPA practices do not have special equipment needs – capital spending is for information technology,phone systems, and office furnishings. Firms invest in information technology to increase staffproductivity and to improve the consistency and accuracy of the firm’s work. Some firms may also owntheir office space – typically, these are smaller practices that do not have plans to grow their staff.

CPA firms typically spend about 2% of net client fees on computers and information technology. Staffmembers use computers every day to do their work and most have multiple computer screens on theirdesk top. The use of digital documents is making it easier to share information across staff and withclients. Mobile computing increases the productivity of staff working at client sites. Given the sensitivenature of client data, firms are also investing in security solutions and data backup and recovery.

Except for purchase of their office space, CPA practices rarely use loans for capital purchases. They fundpurchases of computers, phone systems, and office furnishings through retained cash or a line ofcredit.

Examples of Equipment Purchases

Practice Management Software$500 - 2,500 per yearSoftware for managing client engagements, preparing proposals, tracking time, andinvoice and billing.

© 2017 Vertical IQ, Inc. or its licensors, all rights reserved. CPA Practices 8

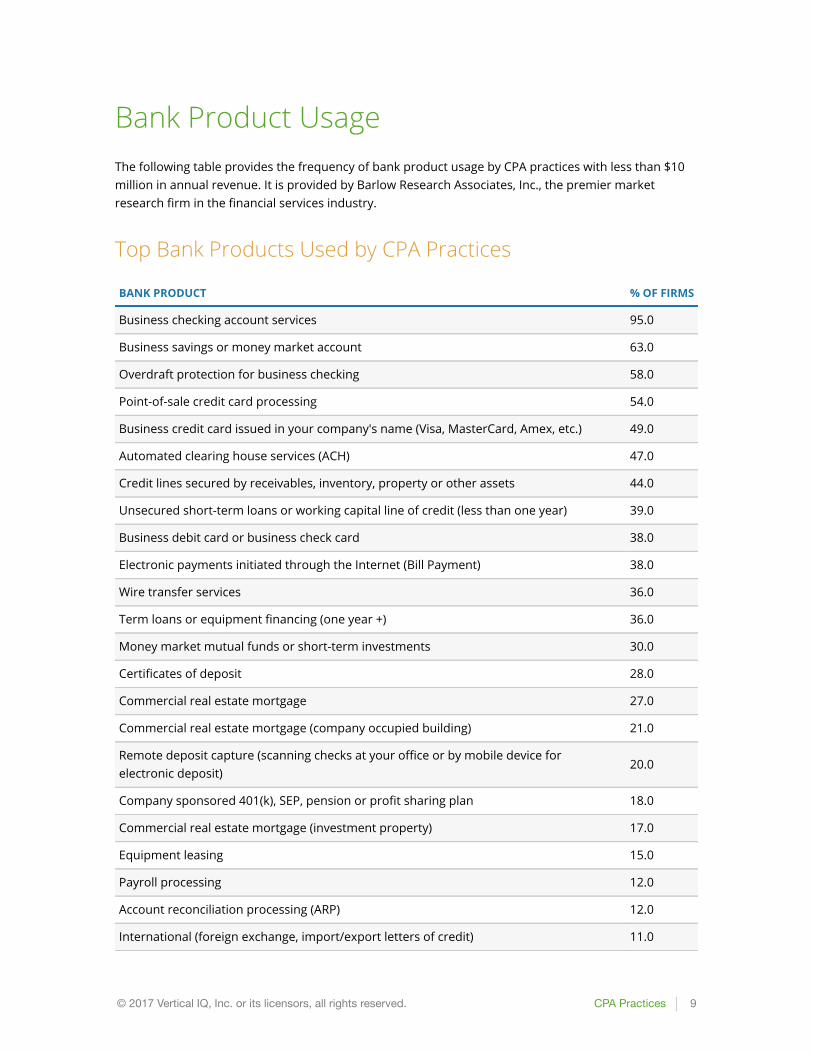

Bank Product UsageThe following table provides the frequency of bank product usage by CPA practices with less than $10million in annual revenue. It is provided by Barlow Research Associates, Inc., the premier marketresearch firm in the financial services industry.

Top Bank Products Used by CPA Practices

BANK PRODUCT % OF FIRMS

Business checking account services 95.0

Business savings or money market account 63.0

Overdraft protection for business checking 58.0

Point-of-sale credit card processing 54.0

Business credit card issued in your company's name (Visa, MasterCard, Amex, etc.) 49.0

Automated clearing house services (ACH) 47.0

Credit lines secured by receivables, inventory, property or other assets 44.0

Unsecured short-term loans or working capital line of credit (less than one year) 39.0

Business debit card or business check card 38.0

Electronic payments initiated through the Internet (Bill Payment) 38.0

Wire transfer services 36.0

Term loans or equipment financing (one year +) 36.0

Money market mutual funds or short-term investments 30.0

Certificates of deposit 28.0

Commercial real estate mortgage 27.0

Commercial real estate mortgage (company occupied building) 21.0

Remote deposit capture (scanning checks at your office or by mobile device forelectronic deposit)

20.0

Company sponsored 401(k), SEP, pension or profit sharing plan 18.0

Commercial real estate mortgage (investment property) 17.0

Equipment leasing 15.0

Payroll processing 12.0

Account reconciliation processing (ARP) 12.0

International (foreign exchange, import/export letters of credit) 11.0

© 2017 Vertical IQ, Inc. or its licensors, all rights reserved. CPA Practices 9

Overnight investment or sweep accounts 11.0

Accounts receivable collection (lockbox) 8.0

SBA loans 7.0

Barlow’s Small Business Banking program is a multi-client research program sponsored by leadingbanks. Each quarter, a stratified random sample of businesses throughout the United States with salesbetween $100,000 to $10 million compiled from an independent list provider are invited to participatein a comprehensive banking survey of over 100 questions. The results measure channel adoption, banksatisfaction, brand power, account management, service quality, business product usage and theselling abilities of leading providers. The results in this chapter are calculated directly from thebusiness product usage section and represent usage for the average small business ($100K-<$10MM).

For more information on Barlow's banking research, go to http://www.barlowresearch.com/

© 2017 Vertical IQ, Inc. or its licensors, all rights reserved. CPA Practices 10

Risks to Watch Out For

Business Failure and Merger Rate

CPA Practices Fail or Merge more frequently

The business failure and merger rate for cpa practices from the end of 2016 to the end of 2017 was16.54%, higher than than the average for all US businesses, according to data from Bizminer. "Business failures and mergers" include those firms that ceased operations during the time period, aswell as firms that ceased being independent entities due to merger or acquisition.

Industry Risks

Client Retention

As the economy improves, CPA firms are focusing on attracting new clients, but client retentionremains a concern for many practices. Clients experiencing financial difficulties may cut back ondiscretionary projects, shop around for lower fees, or go out of business. Even though retaining anexisting client usually costs less than acquiring a new client, many CPA firms have difficulty not billingfor time spent with existing clients, since performance measures are often tied to utilization rates. As aresult, they may under-invest in providing services that could help clients recover and that couldstrengthen their long-term relationship with clients.

Competition for Talent

Demand for hiring accountants and auditors is expected to grow 10% between 2016 and 2026. Hiringwill be driven by growth in the number of businesses, changing regulations, greater financial scrutinyof companies, and a surge in retiring CPAs. Firms are looking for graduates with advanced degrees at atime when schools are struggling with tight budgets and constraints on their capacity to teach largeclasses. The result may be a limited pool of talent with advanced degrees, which could push wages upfor new accountants.

Changing Tax Laws and Accounting Standards

Keeping up with changes in complex tax laws and accounting rules is a major challenge for CPApractices, particularly smaller ones. Regulations to increase financial reporting transparency areaffecting CPA practices, and the adoption of IFRS has driven further changes. The Tax Cuts and JobsAct of 2018 makes significant changes to tax reporting and deductions for individuals and businesses.Difficulty in keeping up with change can cause firms to specialize in particular industries or services tolimit the breadth of knowledge they must maintain.

Competition from Large Firms

Local CPA practices compete for clients with the “Big 4” national accounting firms, as well as largeregional firms. Large firms sell the wide range of expertise available in-house across all their offices, butgenerally have more overhead and higher billing rates than local practices. However, the Big 4 are

© 2017 Vertical IQ, Inc. or its licensors, all rights reserved. CPA Practices 11

opening offices in India, giving them access to low-cost labor for outsourcing and tax preparationservices.

Liability Exposure

Difficult economic times can cause business owners to blame their advisors for financial difficulties. CPApractices may face lawsuits from small business owners over tax liabilities and investors in publiccompanies over audit opinions. CPA practices carry liability insurance to reduce their financialexposure, but lawsuits still take time and attention away from revenue-generating activities.

Company Risks

Lack of Succession Planning

Most CPA practices are highly dependent on the sales skills and client relationships of a few keypartners, yet less than half of firms have a succession plan in place if these partners are disabled or die.About 44% of CPA practices have a practice continuation agreement in place to cover the death ordisability of a partner. About 84% of firms expect succession planning to be a significant issue in thenext 10 years.

High Staff Turnover

Annual turnover rates at CPA firms average 8-14%, with higher rates at larger firms. Firms with highstaff turnover risk losing needed expertise, lowering client satisfaction, and incurring higher recruitingcosts. High staff turnover can also be a sign of poor morale and management practices.

Client Concentration

CPA firms may become highly dependent on one or several clients for a large portion of their revenue.If they lose these clients, they will have difficulty making up the shortfall in revenue. CPA firms may loseclients if they go public, are acquired by another firm, change CFOs, or are offered cost savings by acompetitive CPA practice.

© 2017 Vertical IQ, Inc. or its licensors, all rights reserved. CPA Practices 12

Industry TrendsModest Revenue Growth

CPA practices have seen modest growth in net client fees in recent years. Fee increases averaged 5-10% in 2016, according to the 2016 National Management of an Accounting Practice (MAP) Surveyconducted by the AICPA. The increase in fees continued the trend reported in the 2012 and 2014 MAPSurveys. The 2016 survey also found that more CPA practices are experiencing revenue growth andmaking strategic investments for the future.

Increased M&A Activity

Increased M&A activity is driven by firms looking to grow, the need for external succession as a largenumber of partners reach retirement age, and the demands of clients for greater breadth and depth ofservices as they compete on a global basis. Over the next decade, the supply of CPA firms for salecould exceed M&A demand, which may negatively affect their value. About 19% of firms acquired acompetitor in 2016.

Niche Marketing

To compete more effectively and grow revenues, many CPA practices are focusing on either specificvertical markets (such as healthcare professionals) or specific services (such as business valuation). Aniche marketing approach can help differentiate the practice, particularly for a smaller firm facingchallenges from larger competitors, and result in higher profit margins.

Computer Automation

The widespread use of accounting and tax preparation software packages has eliminated much of thetedious “number-crunching” tasks that CPAs used to perform. While automation of routine accountingreporting is a potential threat to the billable hours charged by CPA practices, it frees CPAs to focus onhigher-value analysis and has created new opportunities for consulting on the implementation and useof computer systems. CPA practices are also implementing information technology, such as knowledgesystems and mobile computing, to improve the productivity of their employees.

Status as Trusted Business Advisor

In the face of increased computer automation and a weak economy, CPA practices are seeking tobecome “trusted business advisors,” providing additional consulting and planning services to clients. Bymoving away from low-value transaction services and after-the-fact reporting to proactive consultingand financial planning services, CPA practices can deepen client relationships and increase firmprofitability.

Stricter Auditing Requirements

The accounting scandals at Enron and Worldcom spurred an increased emphasis on accountability andtransparency in financial reporting. New regulations have led to increased controls and scrutiny byexternal auditors, driving up demand for CPA services. Demand has also grown for forensic accounting

© 2017 Vertical IQ, Inc. or its licensors, all rights reserved. CPA Practices 13

services to investigate white-collar crimes, such as securities fraud and embezzlement.

Global Standard Convergence

In 2014, the US Financial Standards Accounting Board (FASB) and the International AccountingStandards Board (IASB) converged on a common set of International Financial Reporting Standards(IFRS). The new standards took effect in December 2016 for public firms using US GAAP, in January2017 for firms using IFRS, and in December 2017 for US private companies and organizations.

Employment and Wage Trends

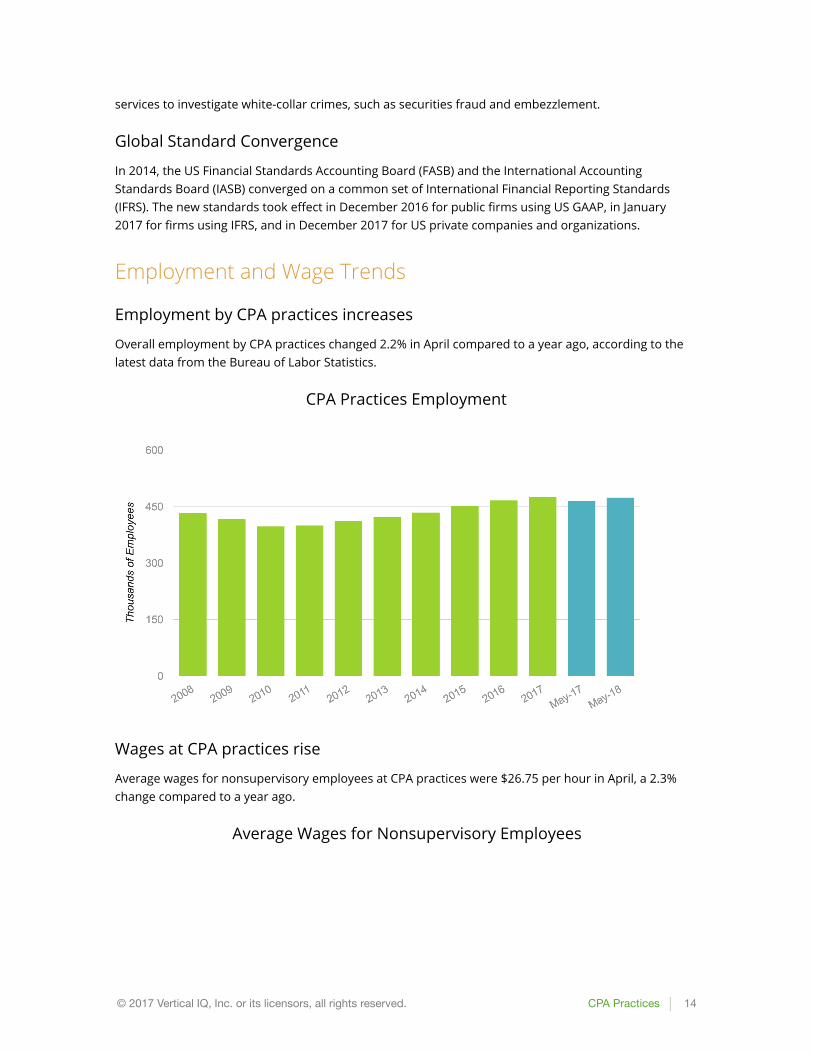

Employment by CPA practices increases

Overall employment by CPA practices changed 2.2% in April compared to a year ago, according to thelatest data from the Bureau of Labor Statistics.

CPA Practices Employment

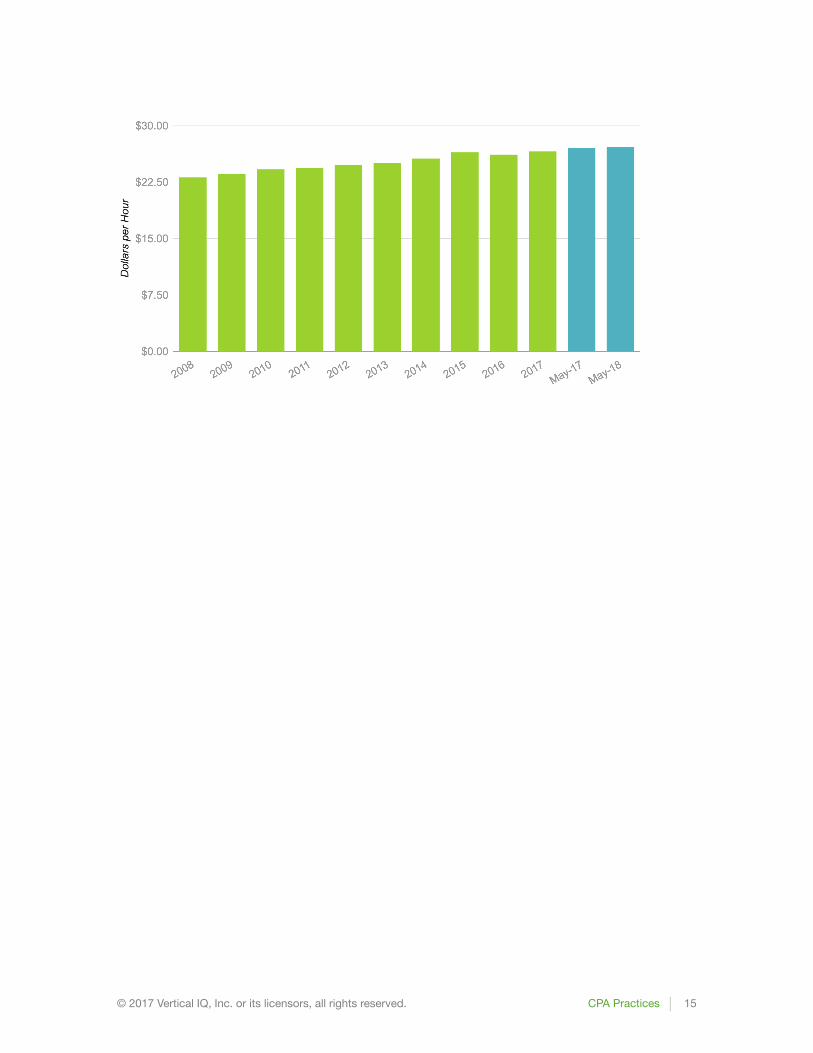

Wages at CPA practices rise

Average wages for nonsupervisory employees at CPA practices were $26.75 per hour in April, a 2.3%change compared to a year ago.

Average Wages for Nonsupervisory Employees

© 2017 Vertical IQ, Inc. or its licensors, all rights reserved. CPA Practices 14

© 2017 Vertical IQ, Inc. or its licensors, all rights reserved. CPA Practices 15

Quarterly Insight

Second Quarter 2018

Banking Oversight Changes Advance to US Senate

The US House of Representatives has approved the most significant overhaul of banking oversight tobecome law since Dodd-Frank was enacted in 2010. Many industry experts say the legislation is theproduct of years of financial-industry lobbying to soften post-2008 financial crisis rules so local banksand credit unions can focus more on lending and less on burdensome and costly regulation. Theoverhaul, if passed is expected to result in more and bigger banking deals because the threshold forfederal oversight will be raised from banks with $50 billion in assets to banks with $250 billion. CPApractices may benefit from an increase in large, complex banking deals. Opponents of the legislationhave called it a gift to lobbyists and a massive giveaway to Wall Street.

First Quarter 2018

Extensions for Storm Victims

The IRS granted many businesses affected by severe winter storms additional time to request a six-month extension to file their 2017 federal income tax returns. The extension helps victims and taxprofessionals affected by Winter Storm Quinn and Winter Storm Skylar that primarily hit portions ofthe Northeast and Mid-Atlantic regions. In the wake of the back-to-back storms, many businesses wentwithout power and phone service for days, even weeks.

Fourth Quarter 2017

HOUSE AND SENATE REPUBLICANS PASS TAX REFORM

House and Senate Republicans both passed bills to cut taxes on businesses and individuals, setting thestage for potential passage of a final bill by year end. While difference still need to be worked out inconference, both bills chop the corporate tax rate to 20% from 35% and make other changes aimed atmaking businesses more competitive. The bills also reduce individual tax brackets, limit state and localdeductions and the mortgage interest deduction, eliminate the personal exemption and nearly doublethe standard deduction.

Third Quarter 2017

TECHNOLOGY A TOP CONCERN

Technology and related issues are top concerns in the accounting industry and pushing firms to stayahead of the curve. An informal survey of the top executives cited a wide range of implications foraccountants, from dangers posed by automation and hackers to new services through data analytics,

© 2017 Vertical IQ, Inc. or its licensors, all rights reserved. CPA Practices 16

according to Accounting Today. Disruptive technologies like data automation, Blockchain and artificialintelligence are expected to change the nature of the services accountants offer. Automationtechnologies are a positive disruption, but require accountants to rethink their processes and the waythey deploy technologies within their firms. Blockchain and artificial intelligence, though not ubiquitousat this point, have the potential to displace thousands of jobs within the accounting profession,especially for cyclical services like bookkeeping, audit and tax preparation.

Second Quarter 2017

CPA PRACTICES HIRING

The market outlook for accountants remains strong, and firms are looking to grow their workforces.During the 2Q 2017, industry employment is projected to grow 1.8%, according to the AICPA’s Business& Industry Economic Outlook Survey, the same level as the 1Q 2017 and the highest since a 2.1%growth forecast in the 4Q of 2014. The plan-to-hire percentage has risen five consecutive quarters andincreased from 15% to almost 25% between the 1Q and 2Q of 2016. With wage and employee costsrising, firms are focusing on retention and placing increased emphasis on training and development.

First Quarter 2017

ETHICS FALL SHORT

CPAs that work in industry and government rate their ethical environment as inferior to publicaccounting firms, according to a study in Behavioral Research in Accounting, published by the AmericanAccounting Association. CPAs in government and industry gave their environment scores of 64 and 67(on a 100-point scale), compared to CPAs in public accounting and Big Four firms, which gave theirenvironment a score of 73 and 76, respectively. The higher ethics scores among the Big Four came as asurprise, given recent well-publicized problems. Low scores among government CPAs was especiallyconcerning and reflected a diminished trust in government seen in other public surveys.

Fourth Quarter 2016

IRS ANNOUNCES CHANGES

The IRS announced changes to income tax deductions, credits, and other tax benefits for 2017. Thechanges provide adjustments for inflation for more than 50 tax provisions. The most significantchanges include an increase in the standard deduction, a phase out for the personal exemption startingat an adjusted gross income of $261,500 ($313,800 for married couples filing jointly), and an increase inthe level of income for the highest tax rate (39.6%). There is also a limit for itemized deductions forindividuals with incomes of $287,650 or more ($313,800 for married couples filing jointly). The ever-changing tax code is a driver of business for CPA firms.

Third Quarter 2016

© 2017 Vertical IQ, Inc. or its licensors, all rights reserved. CPA Practices 17

MILLENNIALS, LOVE, AND MONEY

Millennials are more money-savvy than they appear, and discuss money matters as they developrelationships with each other. Almost 75% of Millennials discuss money weekly and almost half whoused online dating services discussed finances before the first date (compared to 36% across allgenerations), according to the TD Bank Love & Money survey. Millennials were less likely to have sharedcredit card accounts and all generations expressed concern over dating someone with significant creditcard debt. While Millennials were twice as likely to end a relationship if they discovered a financialsecret, they were also twice as likely to keep one, such as a secret bank account, major credit card debt,or a bad credit score.

Second Quarter 2016

Restatements Drop

After six years of relative stability, the number of financial restatements dropped to its lowest levelsince 2002. The total number of restatements decreased by almost 15% between 2014 and 2015,according to Audit Analytics. The number of reissuance restatements has fallen over the last nine yearsand reached its lowest level since 2004. Revision restatements accounted for the same percentage ofrestatements disclosed by 10-K filers (about 75%) and the number of accelerated filers that disclosedstatements dropped from 353 companies to 264 companies between 2014 and 2015.

Fourth Quarter 2015

"Retired-CPA" Status Proposed

The American Institute of CPAs (AICPA) and the National Association of State Boards of Accountancy(NASBA) have proposed creating a uniform status for retired CPAs who want to offer their services forfree without fulfilling the continuing professional education requirements. Demand for the designationhas risen as the Baby Boomer generation enters retirement. Currently, states are taking on thechallenge of creating their own status for retired CPAs, but rules are not uniform and are creatinginconsistency in the status. Retired-CPA services would be limited in scope and uncompensated. Theactive CPA industry could benefit from retired CPAs mentoring businesses and organizations.

Third Quarter 2015

CPAs Delay FASB Revenue Recognition Standards

After hearing concerns from the industry, FASB has pushed the deadline to December 2017 forimplementation of new revenue recognition standards for business entities, some non-profits andcertain employee benefit plans. CPAs' clients may choose to be early adopters and file annual andinterim financial standards according to the new standards beginning in December 2016. Other entitieswill have until Dec 2018. The International Accounting Standards Board (IASB) is also proposing a one-year delay to coincide with FASB and make the process easier for CPAs with international clients. Theindustry asked for the delay due in part to a lack of available IT solutions, difficulty in implementinginternal controls, and the timing of the changes. Some CPAs are concerned that staggered

© 2017 Vertical IQ, Inc. or its licensors, all rights reserved. CPA Practices 18

implementation will make financial statements hard for investors to compare.

Second Quarter 2015

Pricing Customers, Not Services

Some CPAs are shifting away from the traditional billable hour to tailored pricing based on the client'sneeds and work required. To effectively provide value-based pricing, a CPA should understand thevalue drivers for their customers and then create and communicate their value. Clients can betterjustify the cost if they understand the value of the CPA's services. This communication before workbegins allows CPAs to properly set expectations in clients' minds, uncover potential future work withthe client, and reduce conflict with clients over the price at the end of service.

First Quarter 2015

Hiring and Salary Forecast

On average, accountants are expected to see a 3.5% increase in their salaries in 2015, according toRobert Half. As accounting firms and other businesses gain back clients and increase revenues, theyare hiring additional staff to alleviate pressure on existing employees and take on new roles that havebeen created. The challenge in hiring new accountants is that the unemployment rate for theprofession is very low at 2.4%. Firms may encounter difficulty attracting the limited number ofapplicants and may need to up their incentives to capture top notch accountants. Compounding thelabor issue is the large number of Baby Boomers that are retiring from the industry.

Fourth Quarter 2014

Online Content Best Practices

The accounting industry is high-touch in terms of managing relationships with clients, but it also reliesheavily on technology and online communications. To improve their online content, firms areencouraged by the top accounting marketers to tailor their content to a variety of devices - i.e. design awebsite and mobile app that is optimized for the devices they are viewed on. Online content shouldlead viewers through the site and tell them what to do next - click a link for more info, join a chat, signup for emails, schedule a consultation. Videos, blogs and emotional content should be used to create amore dynamic and authentic appearance for users. Firms should track results and modify systems toboost prospecting. Accounting firms can also use LinkedIn and search engine optimization (SEO) todrive customers to their websites and boost lead generation.

Third Quarter 2014

Proactive Services in Demand

A recent survey of small and medium businesses found that 76% of owners think their CPAs aren'tproactive enough, and some have changed their CPA in an effort to gain more proactive services.

© 2017 Vertical IQ, Inc. or its licensors, all rights reserved. CPA Practices 19

Business owners are looking for more business planning and strategic advice (57%), more tax planning(30%) and better analytics (21%), according to The Sleeter Group. Businesses also want their CPAs to beproactive with technology (85%), but only 13% feel that their CPAs are tech savvy. Providing moreproactive services and technology solutions may help CPAs build better relations and retain moreclients.

Second Quarter 2014

Growth through Client Assessment

CPA firms can expand their revenues by conducting client assessments and determining how familiarclients are with the range of services offered. A recent study by Hinge Marketing found that 44% ofCPA clients want to know more about the additional services that their accounting firms provide. Firmsthat can educate their clients on the full range of service and how they could benefit the client arebetter able to expand the number of services their clients receive. Clients overwhelmingly prefer tolearn about additional services via a personal call or visit from their CPA (50%); far more than throughemail (13%) or direct mail (4%). Targeted assessments help clients see their strengths, weaknesses, andopportunities and which CPA service will help them improve or move toward their goals.

First Quarter 2014

Merger Activity Remains Strong

Mergers among CPA firms are expected to continue at a brisk pace in 2014, according to the AmericanInstitute of CPAs. Activity is expected to be greatest among small and midsized regional firms. Driversinclude succession planning as retiring professionals leave the industry, and the opportunity tobroaden the firms' scope of work and market share. Organic growth has been difficult, since theindustry has a low unemployment rate and small firms often have difficulty hiring additionalaccountants to expand their businesses. Roadblocks to merger negotiations include inaccuratelyassessing the firm’s value or succession plans, a mismatch of clients and firm strengths, weakinvestment in technology, and a lack of developing specialty practices or niche service areas.

Fourth Quarter 2013

Crowdfunding Creates Opportunities for CPAs

New rules proposed by the SEC regarding businesses' use of crowdfunding to sell securities and raisecapital will create opportunities for CPAs to offer their services. The rules have been developed tocomply with the Jumpstart Our Business Startups (JOBS) Act of 2012, which was created to make capitaleasier to access for small businesses. CPAs can benefit by offering to review financial statements or byproviding audit services. A CPA review of financial statements would be required for offerings rangingfrom $100,000 to $500,000, and an audit would be required for offerings over $500,000.

Third Quarter 2013

© 2017 Vertical IQ, Inc. or its licensors, all rights reserved. CPA Practices 20

Record Hiring

CPA firms are hiring a record number of accounting graduates and the pace is not expected to stop.Firms hired 40,350 graduates in 2012 and almost 90% expect to hire the same or more in 2013,according to a report by the American Institute of CPAs (AICPA). Firms are picking from a large pool ofgraduates, over 82,000 accounting degrees were awarded during the 2011-2012 school year.Undergraduate and graduate accounting degrees are at the highest level in the 40 years that AICPAhas been tracking. Also, a record number of students are currently enrolled in accounting programsacross the nations, which means the pool of applicants will remain large.

Second Quarter 2013

CPA Exam Results

The National Association of State Boards of Accountancy has issued results from the 2012 CPA examsittings with some interesting results. Last year, 92,839 candidates took the exam, up 2% from theprevious year, but down 7% from the historic high set in 2010. The exam is divided into four sectionsthat can be taken individually; 245,193 sections were taken in 2012, up about 4% from a year earlier.The passing rate was slightly less than half. The gender gap in CPA candidates has shifted over the pastfew years; from 2005 to 2010, more women were taking the exam, but in 2011 the ratio evened, and in2012 more men sat for the exam. States with the highest passing rates included Utah (61.2%), Missouri(57.7%), and Wisconsin (56.8%).

First Quarter 2013

Metrics Measure Performance

As CPA firms are planning for their busiest time of year, the tax season, they are measuring theirsuccess in 2012 using some key metrics. Metrics may be client-centered, sales- and marketing-based, oroperation- and revenue-focused. Client-centered metrics include the lifetime value of a client, the costto acquire new clients, and retention rates. Sales and market-based metrics relate to the quantity andquality of interactions with clients, number of services per client and cross-selling opportunities, andthe size of the prospective client pipeline and conversions. Operational metrics include staff responseand utilization rates, professional development hours, staff-to-partner ratio, and revenue growth.Measuring metrics allows CPA firms to make adjustments to services, time, staffing, sales, andmarketing that can improve revenue, the client experience, staff satisfaction and advancement, andoptimize operations.

© 2017 Vertical IQ, Inc. or its licensors, all rights reserved. CPA Practices 21

Web Links

American Institute of CPAs

News, policies, white papers, and education.

Accounting Today

News, white papers, and issues

CPANet

News and resources for CPAs

CPA Practice Advisor

Latest information technology for CPA practices

© 2017 Vertical IQ, Inc. or its licensors, all rights reserved. CPA Practices 22

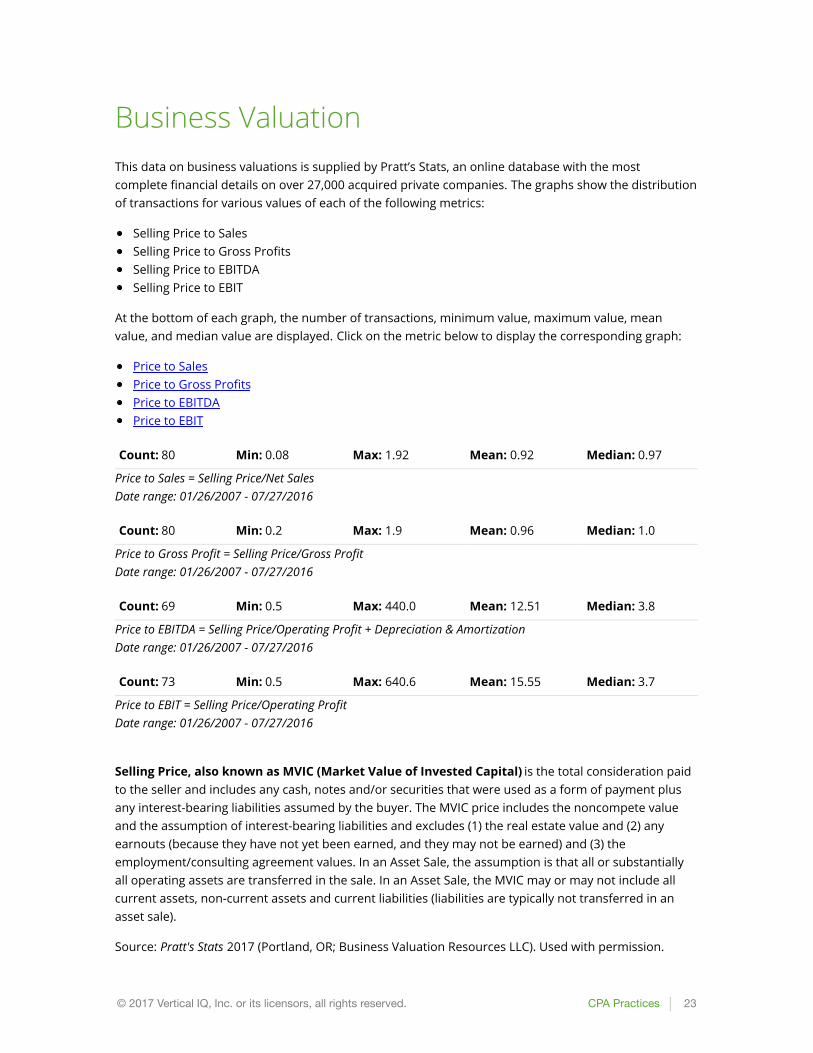

Business ValuationThis data on business valuations is supplied by Pratt’s Stats, an online database with the mostcomplete financial details on over 27,000 acquired private companies. The graphs show the distributionof transactions for various values of each of the following metrics:

Selling Price to SalesSelling Price to Gross ProfitsSelling Price to EBITDASelling Price to EBIT

At the bottom of each graph, the number of transactions, minimum value, maximum value, meanvalue, and median value are displayed. Click on the metric below to display the corresponding graph:

Price to SalesPrice to Gross ProfitsPrice to EBITDAPrice to EBIT

Count: 80 Min: 0.08 Max: 1.92 Mean: 0.92 Median: 0.97

Price to Sales = Selling Price/Net SalesDate range: 01/26/2007 - 07/27/2016

Count: 80 Min: 0.2 Max: 1.9 Mean: 0.96 Median: 1.0

Price to Gross Profit = Selling Price/Gross ProfitDate range: 01/26/2007 - 07/27/2016

Count: 69 Min: 0.5 Max: 440.0 Mean: 12.51 Median: 3.8

Price to EBITDA = Selling Price/Operating Profit + Depreciation & AmortizationDate range: 01/26/2007 - 07/27/2016

Count: 73 Min: 0.5 Max: 640.6 Mean: 15.55 Median: 3.7

Price to EBIT = Selling Price/Operating ProfitDate range: 01/26/2007 - 07/27/2016

Selling Price, also known as MVIC (Market Value of Invested Capital) is the total consideration paidto the seller and includes any cash, notes and/or securities that were used as a form of payment plusany interest-bearing liabilities assumed by the buyer. The MVIC price includes the noncompete valueand the assumption of interest-bearing liabilities and excludes (1) the real estate value and (2) anyearnouts (because they have not yet been earned, and they may not be earned) and (3) theemployment/consulting agreement values. In an Asset Sale, the assumption is that all or substantiallyall operating assets are transferred in the sale. In an Asset Sale, the MVIC may or may not include allcurrent assets, non-current assets and current liabilities (liabilities are typically not transferred in anasset sale).

Source: Pratt's Stats 2017 (Portland, OR; Business Valuation Resources LLC). Used with permission.

© 2017 Vertical IQ, Inc. or its licensors, all rights reserved. CPA Practices 23

Pratt's Stats is available at http://www.bvresources.com/prattsstats

© 2017 Vertical IQ, Inc. or its licensors, all rights reserved. CPA Practices 24

Just the Numbers

Financial Summary

Cash IntensityInventory IntensityLabor IntensityProfitabilityCapital Intensity

Cash Intensity

20.38% Cash to Total Assets (%)

1st quartile

Inventory Intensity

0.38 Days Inventory

4th quartile

Labor Intensity

25.87% Salaries/Wages to Sales (%)

1st quartile

Profitability

8.06% Operating Income to Sales (%)

2nd quartile

Capital Intensity

22.06% Net Fixed Assets to Total Assets (%)

3rd quartile

Industry Financial Benchmarks

Here are typical financial statements for CPA practices.

This data is supplied by BizMiner, a leading supplier of industry analytical statistics to the financial sector,accounting and business valuation communities. BizMiner content includes financial and market reports onmore than 9000 industry segments at national and local levels. Learn more about BizMiner products orreview BizMiner data sources.

© 2017 Vertical IQ, Inc. or its licensors, all rights reserved. CPA Practices 25

Need more detailed financial benchmark data for your client or prospect? BizMiner can breakdown this industry data by specific industry segments, size of business, or geographic market. Thesemore detailed reports are available for as little as $79. To learn more or order a report, click here.

Show data for: Industry-wide

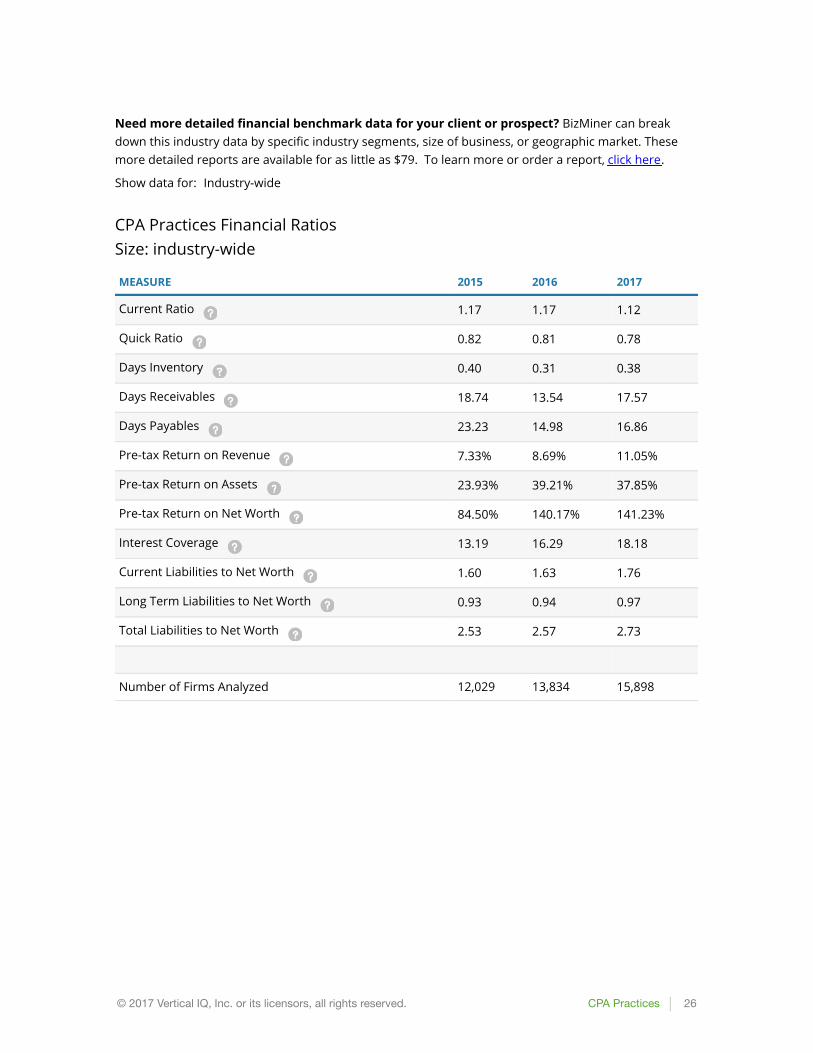

CPA Practices Financial RatiosSize: industry-wide

MEASURE 2015 2016 2017

Current Ratio 1.17 1.17 1.12

Quick Ratio 0.82 0.81 0.78

Days Inventory 0.40 0.31 0.38

Days Receivables 18.74 13.54 17.57

Days Payables 23.23 14.98 16.86

Pre-tax Return on Revenue 7.33% 8.69% 11.05%

Pre-tax Return on Assets 23.93% 39.21% 37.85%

Pre-tax Return on Net Worth 84.50% 140.17% 141.23%

Interest Coverage 13.19 16.29 18.18

Current Liabilities to Net Worth 1.60 1.63 1.76

Long Term Liabilities to Net Worth 0.93 0.94 0.97

Total Liabilities to Net Worth 2.53 2.57 2.73

Number of Firms Analyzed 12,029 13,834 15,898

© 2017 Vertical IQ, Inc. or its licensors, all rights reserved. CPA Practices 26

CPA Practices Income StatementSize: industry-wide

ITEM 2015 2016 2017

Revenue 100% 100% 100%

Cost of Sales 20.22% 20.27% 19.85%

Gross Margin 79.78% 79.73% 80.15%

Officers Compensation 14.63% 14.48% 14.31%

Salaries-Wages 27.30% 26.64% 25.87%

Rent 4.48% 4.35% 4.22%

Taxes Paid 4.36% 4.21% 4.08%

Advertising 0.93% 0.89% 0.86%

Benefits-Pensions 3.91% 3.81% 3.71%

Repairs 0.43% 0.42% 0.41%

Bad Debt 0.06% 0.05% 0.05%

Other SG&A Expenses 15.65% 15.41% 14.88%

EBITDA 8.03% 9.47% 11.76%

Amortization-Depreciation 1.49% 1.41% 1.34%

Operating Expenses 73.24% 71.67% 69.73%

Operating Income 6.54% 8.06% 10.42%

Interest Income 0.16% 0.15% 0.16%

Interest Expense 0.61% 0.58% 0.65%

Other Income 1.23% 1.06% 1.11%

Pre-tax Net Profit 7.32% 8.69% 11.04%

Income Tax 1.65% 2.33% 3.29%

After Tax Net Profit 5.67% 6.36% 7.75%

Number of Firms Analyzed 12,029 13,834 15,898

© 2017 Vertical IQ, Inc. or its licensors, all rights reserved. CPA Practices 27

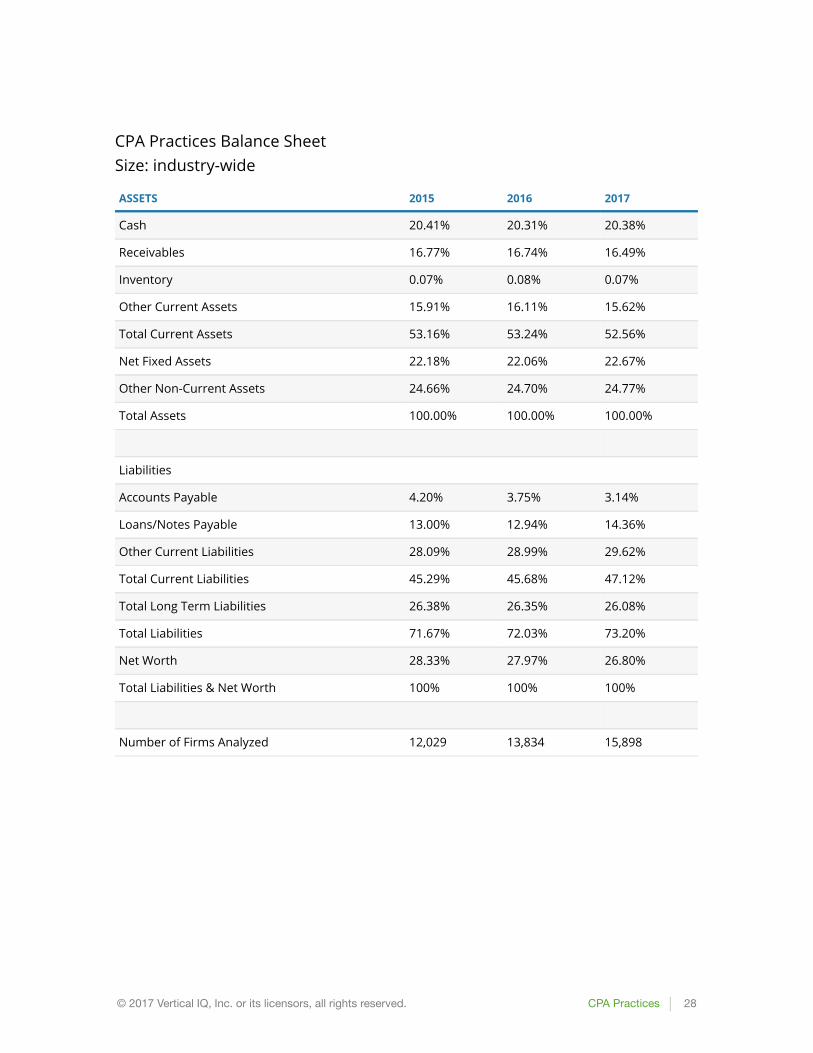

CPA Practices Balance SheetSize: industry-wide

ASSETS 2015 2016 2017

Cash 20.41% 20.31% 20.38%

Receivables 16.77% 16.74% 16.49%

Inventory 0.07% 0.08% 0.07%

Other Current Assets 15.91% 16.11% 15.62%

Total Current Assets 53.16% 53.24% 52.56%

Net Fixed Assets 22.18% 22.06% 22.67%

Other Non-Current Assets 24.66% 24.70% 24.77%

Total Assets 100.00% 100.00% 100.00%

Liabilities

Accounts Payable 4.20% 3.75% 3.14%

Loans/Notes Payable 13.00% 12.94% 14.36%

Other Current Liabilities 28.09% 28.99% 29.62%

Total Current Liabilities 45.29% 45.68% 47.12%

Total Long Term Liabilities 26.38% 26.35% 26.08%

Total Liabilities 71.67% 72.03% 73.20%

Net Worth 28.33% 27.97% 26.80%

Total Liabilities & Net Worth 100% 100% 100%

Number of Firms Analyzed 12,029 13,834 15,898

© 2017 Vertical IQ, Inc. or its licensors, all rights reserved. CPA Practices 28

_______________________ All contents of this “Report”, including without limitation the data, information, statistics, charts,diagrams, graphics and other material contained herein, are copyright © 2017 Vertical IQ, Inc. or itslicensors, all rights reserved. Use of this Report is subject to the Terms of Use accepted upon purchaseof a license to this Report, and this Report is intended solely for the purchaser’s internal businesspurposes as further described in the Terms of Use. Except as expressly authorized in the Terms of Use(which permits the purchaser to provide a single printed copy of this Report to its bona fide clients atno charge), this Report may not be, directly or indirectly: shared, resold, transferred, brokered,published, reproduced, displayed publicly, used to create any derivative works or otherwise distributed.The purchaser assumes sole responsibility for use of this Report and conclusions drawn therefrom.EXCEPT AS SPECIFICALLY SET FORTH IN THE TERMS OF USE, VERTICAL IQ, INC. MAKES NOREPRESENTATIONS OR WARRANTIES, EXPRESS OR IMPLIED, REGARDING THE CONTENTS OF THISREPORT, OR USE OF OR RELIANCE ON THIS REPORT, AND THIS REPORT IS PROVIDED “AS IS”. If youhave received a copy of this Report in electronic format and you did not purchase a license to thisReport directly from Vertical IQ, Inc., please destroy all electronic copies of this Report and contact us [email protected] to report a potential violation of the Terms of Use for this Report.

© 2017 Vertical IQ, Inc. or its licensors, all rights reserved. CPA Practices 29