Report No. 494a-SL Sierra Leone Current Economic Position and Prospects (In Five Volumes) Volume 1: Main Report November 27, 1974 Western Africa Region Not for Public Use D)c urnent of tht International Bank for Reconstruction and Development International Developrmetnt Association This rpot u as prepared tor offitlal LIW only hy the, BRnk ,roL]u[. It may n(lt he pAulflshed, quotetd or t I'd witho t Banhk Croup authorization TheRa Bank Uoup doe,s not ai:r ept rosposmhility tor the .e( Liri(y vor oIrnIplct(ei ls o ti thre report. Public Disclosure Authorized Public Disclosure Authorized Public Disclosure Authorized Public Disclosure Authorized Public Disclosure Authorized Public Disclosure Authorized Public Disclosure Authorized Public Disclosure Authorized

Transcript

Report No. 494a-SL

Sierra LeoneCurrent Economic Position and Prospects(In Five Volumes)

Volume 1: Main ReportNovember 27, 1974

Western Africa Region

Not for Public Use

D)c urnent of tht International Bank for Reconstruction and DevelopmentInternational Developrmetnt Association

This rpot u as prepared tor offitlal LIW only hy the, BRnk ,roL]u[. It may n(lthe pAulflshed, quotetd or t I'd witho t Banhk Croup authorization TheRa Bank Uoup doe,s

not ai:r ept rosposmhility tor the .e( Liri(y vor oIrnIplct(ei ls o ti thre report.

Pub

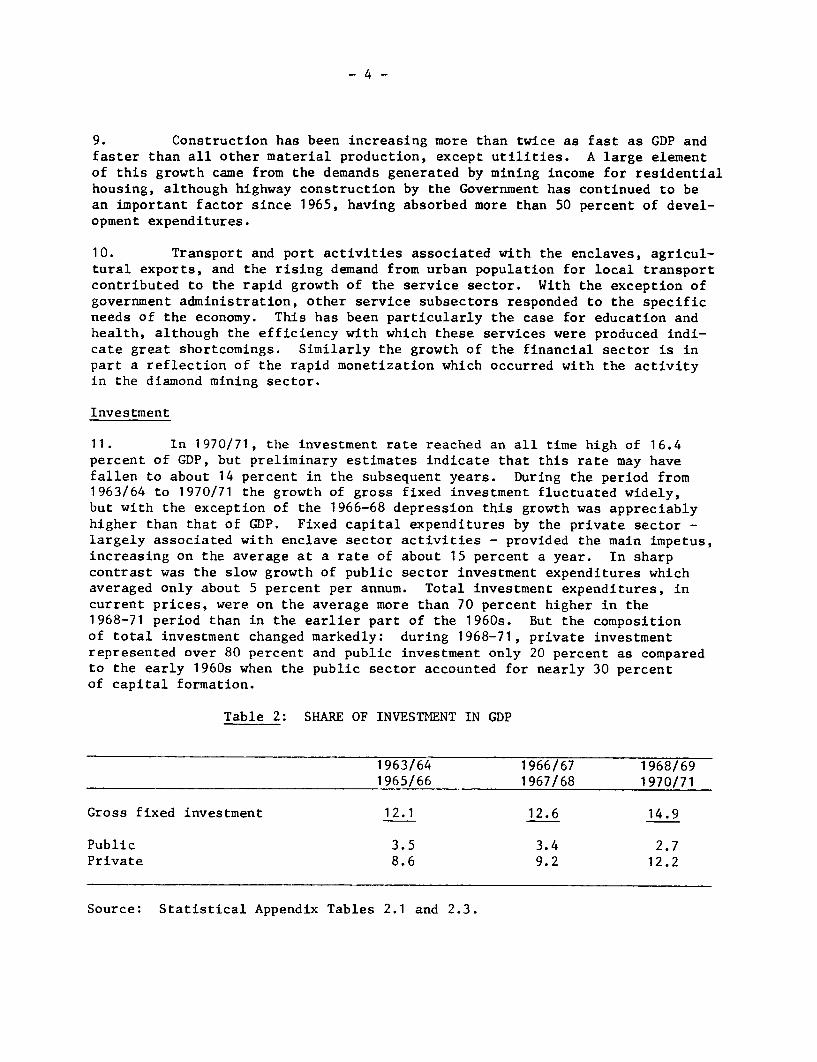

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

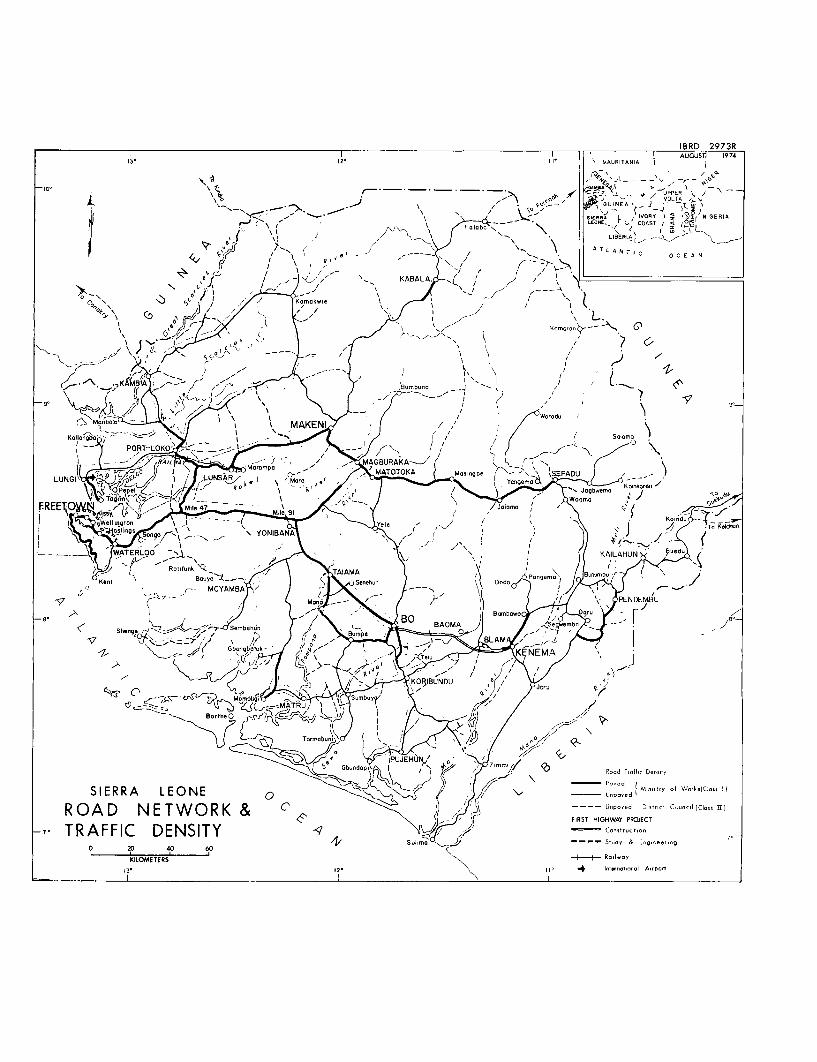

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

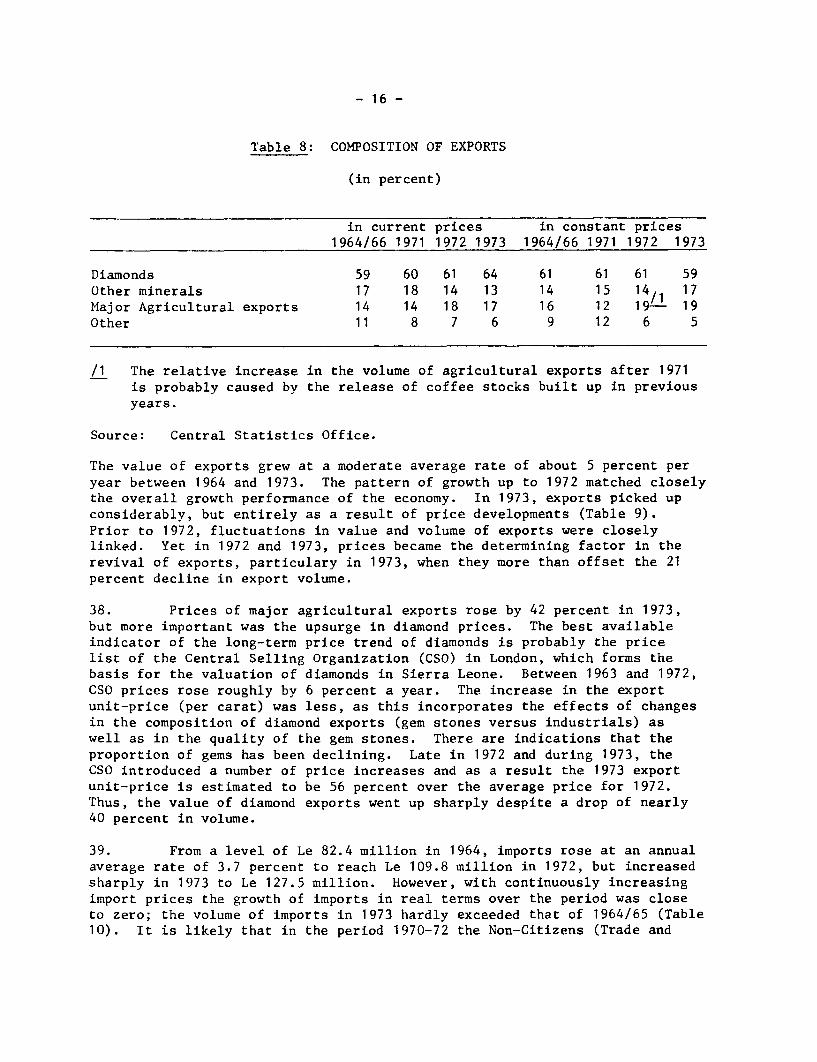

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

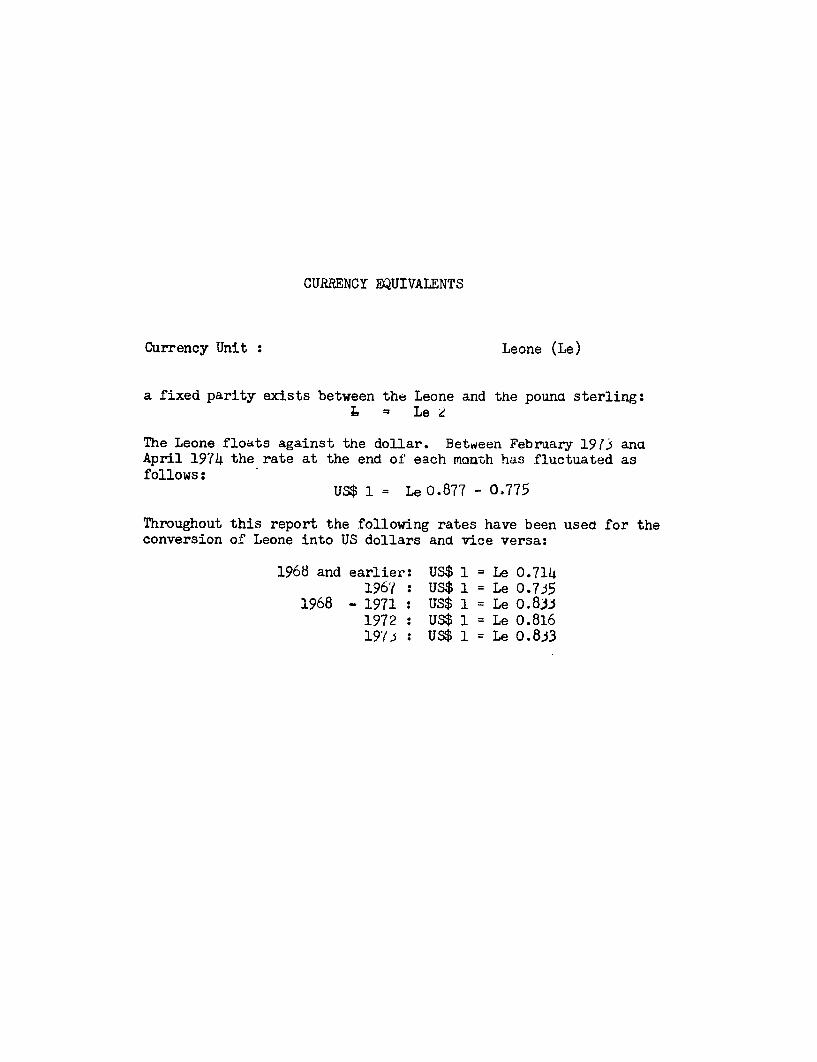

CURRENCY EQUIVALENTS

Currency Unit : Leone (Le)

a fixed parity exists between the Leone and the pouna sterling:L = Le 2

The Leone floats against the dollar. Between Februaary 1913 anaApril 1974 the rate at the end of each month has fluctuated asfollows:

US$ 1 = Leo .877 - 0.775

Throughout this report the following rates have been used for theconversion of Leone into US dollars and vice versa:

1968 and earlier: US$ 1 = Le 0.7141961 : US$ 1 = Le 0.7j5

1968 - 1971 : US$ 1 = Le o.831972 : US$ 1 = Le o.81619(i : US$ 1 = Le 0.8i3

PREFACE

This report is based on the findings of an Economic Missionwhich visited Sierra Leone in November/December 1973. The followingparticipated in the Mission and in the writing of the Report:

Emmerich M. Schebeck - Chief of MissionHendrik T. Koppen - General EconomistRoger S. Suith - Fiscal Economist (IMF)Cornelius P. Cacho - Planning/Administration SpecialistGerald L. Karr - Agricultural Economist (Consultant)Gerhard Gerhardsen - Fishery Specialist (Consultant)Judith A. Edstrom - Education EconomistClaude Delapierre - Transport SpecialistRolf Gusten - Transport EconomistIbrahim Kande - General Economist (ADB)Luz R. Pangilinan - Mission Secretary

Ms. Edstrom and Messrs. Delapierre and Giisten visited Sierra Leonein the spring of 1974.

VOLUME I: THE MAIN REPORT

Table of Contents

Page No.

COUNTRY DATA

MAPS

SUMMARY AND CONCLUSIONS ...... .......................... i- xi

PART I: THE ECONOMIC STRUCTURE AND RECENT DEVELOPMENTS

I. ECONOMIC TRENDS AND STRUCTURAL FEATURESOF THE ECONOMY ............................. 1

Transport ........ 48Energy ... ............................... 55

IV. SOCIO ECONOMIC NEEDS ............. 59

Education and Training ..... .. -.-........... 59

Health ..... ........... oo-o-o ......... ...... o 63

V. ADMINISTRATION, ABSORPTIVE CAPACITY, PLANNING 65

General Administration .............- ..... 65Projects and Planning ................. 66

Table of Contents (Continued)

PART III: RESOURCES FOR DEVELOPMENT

VI. DOMESTIC RESOURCES - ISSUES AND PROSPECTS ........... 68

Domestic Resources - The Public Sector ........ 70Expenditure Control .................... 70Revenue Measures ........... ........... . 73Allocation of Resources ................... 76

The Fiscal Outlook ....... ........ 78Domestic Resources - The Financial Sector .... 82

VII. BALANCE 'OF PAYMENTS AND EXTERNAL ASSISTANCE . 89

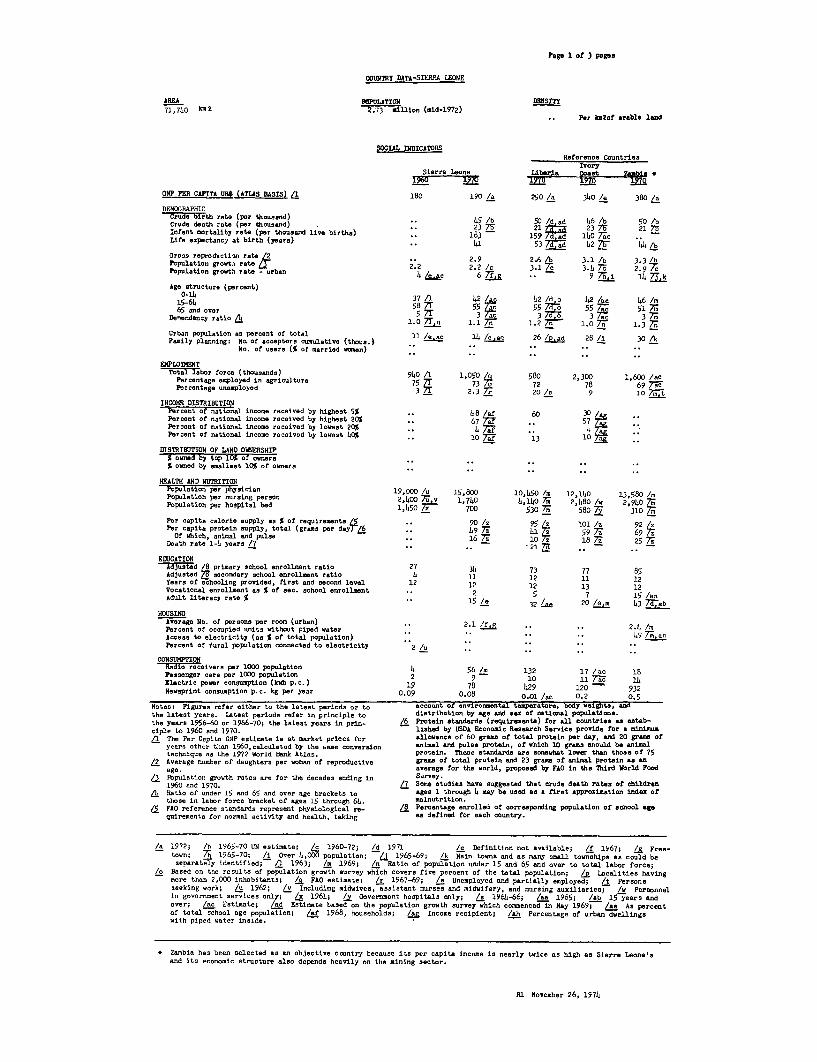

Dse.edency ratio /4/c 37 ~ ~ 3S 37 m10 1.1 7r' . ; L . 1.3 M;

Urban pepil.iti.n as Percent of total 11 I... an 6___d_2_/ 3 Fosily Planning; No. of acceptors cuolative (thnus.)..., 1 eac 2/Uo 28/ 30kNo. of users (% of narried wmoen)

TWLOYMEN?Totaslbor force (thousands) 940A/ 1,050 Ic 580 2,300 1,600 lac

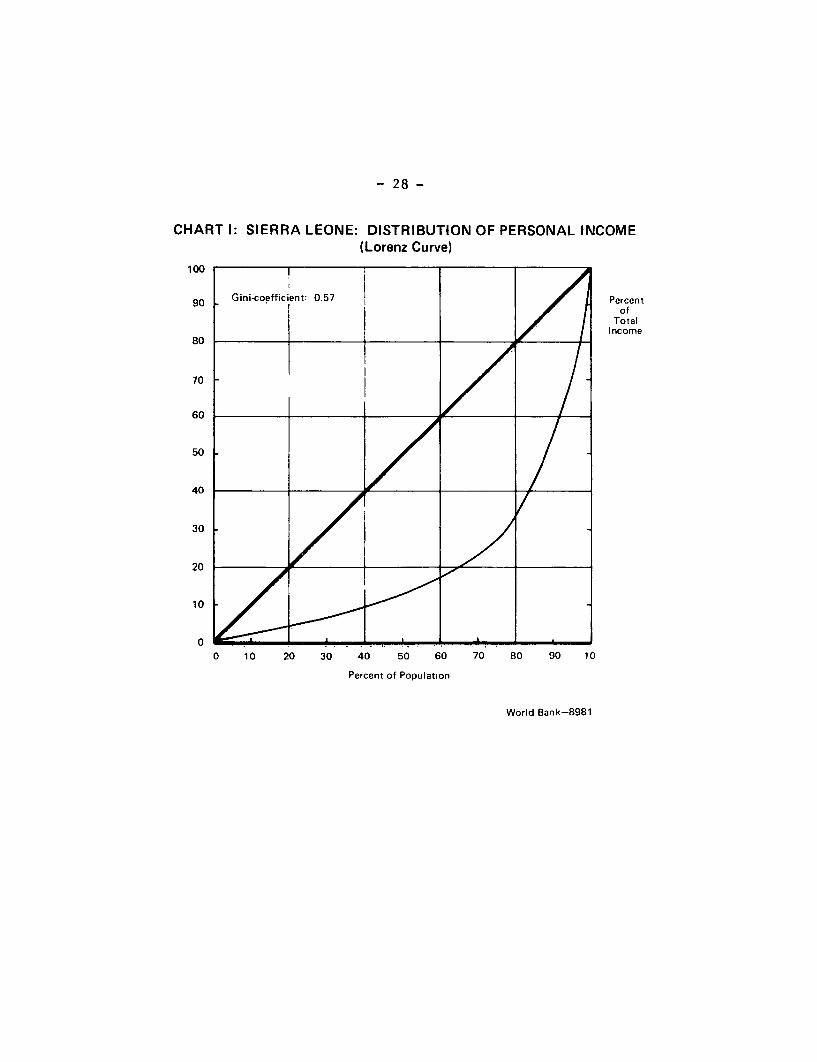

INCOM DISTRIBUTIONPercent of national inceo received by highest 5% ha 1 lxf 60 30IlaPercent nf notinnal income received by highest 20% . 67 72 . 577"Percent of notional income received by lowest 20% 4. I 4 Percent of notional income receivod by lowest 40% . 10 72 13 1

MISTRIBUTION OF LAND OWENSHIP% owned by topll0t of% ownr o-era

HEALTH AND NUTRCTIONPoPulation Per physician 19,000 Ic 15,800 10,160 In 12,140 13,580 /nPopulation per nusing Person 2.0 4 ; 1,740 1,110 7m 2,h80 Is. 2,910oPopulation per hospital hod 1 ,41 5 007r; L"- 700 5307; 68o 7Z 310 7;

Per capita calorie nupply ou % of requirements 5. 90AI 95 In 101iI 92A/Par capita protein supply, total (grams per day,J 6 19 77 41 7 59 77 69 7;

Of which,oanimal and pulse .. 16 77 io7 i 8 7z 25 7;Death rote 1-4s years /7 .. 21 73

EDUCATIONAjuste9d 18 prinery school enroilsent ratin 27317778

Adjasted 79 secondiary school enrollment ratio 4 11 12 U1 12Tears of schooling provided, first and secwnd level 12 12 12 13 12Vocational enrollment as % of sac, school enrollment 2 57 15 la.Adult literacy rate % * 15 /a 32 Le 20 4on 3 77b

HOUSINGAverage No. of persons per rmo (urban) . 2.1 If, .. 2.11 I.Percent of occupied units without piped water 4. 9 7; ohAccens to electricity (an % of total populotion) ..- -Percent of faral population connected to electricity 2 Ic .

CONSUMPTON%_Jo'_eoiver. per 1000 population 4 56 /n 132 17 la 18Passnnger care per 1000 pepulation 2 9 10 11 7/a 21Electric power conSumption (kwh P. c.) 19 78 4,29 120 932Newsprint connsumption p.c. kg per year 0.09 0.08 0.01 Ian 0.2 0.5

Nnten, Figurs refer either to the lotest perlodn or to acnount or environmental temperatre", body .. 1ghta, andthe lateot yearn. latent periods refer in principle to distribution by age and sex of national populations.the yearn 1956-60 or 1966-70; the 1otest years in prin- 6 Protein standards (requiremata) for all countries as estab-ciple in 1960 and 1970. lished by LSUDA Economic Research Service provide for a minioass/jI The Per Copits GNP estimate is at market prices fcr allowance of 60 greamse of total protein par day, arnd 20 grass of

yearn obe- tihn 1960, calculated by the cane onvernion anima and pulse protein, of whIch 1.0 grams enould be animaltechnique as the 1972 World Bank Atlas. protein. Theoe at-adards are somwhat lower than those of 75

12 Average number of daughters per woman of reproductive gramm of total protein and 23 greamse of animal protein a an age. average for the world, proposed by FAO in the Third World Food

/) Population growth roten a- for the decades ending in Suarve.1960 and 1970. l7 one studies have suggested that crude death rates of children

A( Ratio of under 15 and 65 and o-er age brackets t. ~ ages 1 through 4 nay be used as a first apprminiation index ofthose in lahor foree bracket of agen 15 through 64. malnutrition.

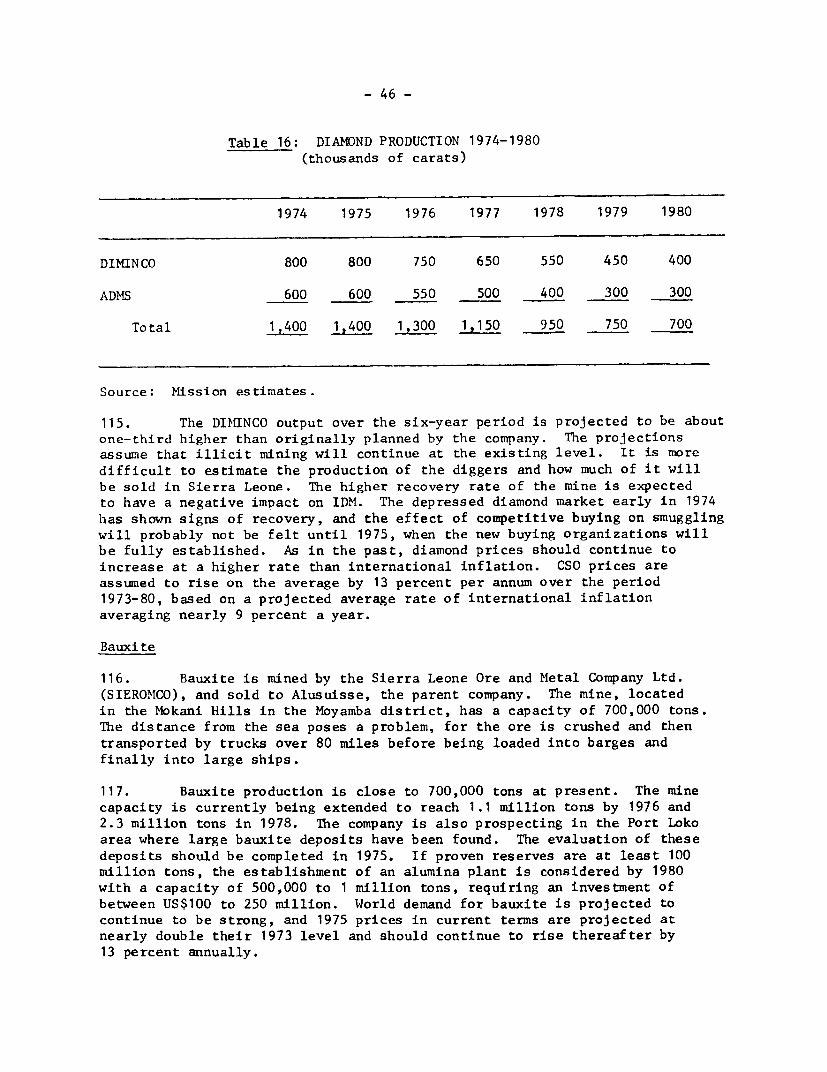

/5 AO reference standards represent physiological re- /8 Pereentage scrolled of correspondting population of school agequir,events for noreal activity and health, taking as defined for each country.

Ia 1972; lb 1965-70 UN estimate; In 1960-72; Id 1971 Ie Definition not available; /-f 1W6; IR Fre-town; 7;h 1965-70; /i Over 1,000 population; -71 1965-69; /k Main ionsn and an many small townshIps an could beneparately identified; /1 1963; /a 1969; In Ratio of popul-ation under 15 and 65 and over to total labor force;

Is Based cc the reoulto of population growth survey which covers five percent of the total population; /P localities havingnore than 2,000 Inhabitants; /I FAO entimate; /r 1967-69; Is Unemployed and partially employed; It Personsseeking sorb; /u 1962; Iv Including midwives, assistant curses and midwifery, and nursing auxiliaries; lw Personnelin govermenet services nuly; Ix 1961; /5 Government hospitals only; Iz 1961-66; l/a 1965; /ab 155yeams andover; Ian Estimate; lad 6otioate based on the population growth ourvey which commencedT in ay 1969-; /ae As percentof total school age populatins; laf 1968, households; I& Income recipient; lah Percentage of urban dwellingswith piped sater Inside.

*Zanbia has been selected as an objective comntr-y because its per capita incene in nearly twice as high as Sierra Leone'sand ito economic structure also depends heavily on the mining sector.

81 November 26, 1971

Page 2 of 3 pages

ECONOMIC INDICATORS

GROSS NATIONAL PRODUCT IN 197 ANNUAL RATE OF GROWI2H (%, constant prices)

MONEY, CREDIT and PRICES 1968 196 1970 1971 12 1973%Mllion Le outstanding end period)

Money and Quasi Money 38.1 44.4 42.6 47.8 56.o 71.9Bank credit to Public Sector 8.6 4.6 2.5 8.0 9.h 15.1Bank Credit to Private Sector 16.1 16.9 19.4 19.9 21.7 28.2

(Percentages or Index Numbers)

Money and Quasi Money as % of GDP 13.4 13.7 11.5 12.7 ... 1/General Price Index (1963 l 100) 129 134 144 10 1446 154

Annual percentage changes insGeneral Price Index 1.3 3.4 7.6 -2.3 3.9 5.8"Bank credit to Public Sector - 23 -47 -46 320 18 61Bank credit to Private Sector 4 5 15 3 9 30

Note: All conversions to dollars in this table are at the average exchange rate prevailing during the periodcovered.

1/ January - September 1973.not apailable.not applicable

Page 3 of 3 pages

TRADB PAYMS AND CAPITAL FWOIB

BAlANCE OF PAYMENTS MERCHANDISE EXPORTS (AVERAGE 1971 -7'

1971 1972 1973 US $ Mln X(Millions US $)

Diamonds 70 61Exports of Goods, NPS 113.3 129.4 145.2 Other minerals 1/17 15Imports of Goods, NPS 129.8 134.5 171.4 Major sgdcuiural exports- 17 15Resource Gap (deficit 0 -) -i6. ; M s e

-5.1

Interest Payments (net) - 4.6 - 2.9Workers' Remittances _ - - 7.7Other Factor Payments (net) -4.5 - 3.9Net Transfers 5.8 3.0 5.6 All other commodities 10 9Balance on Current Account -19.8 - 9.1 - 28.3 Total 114 lOO,O

Direct Foreign Investment 5.3 3.8 .. EXTERNAL DEBT. DECEMBER 31. 1973Net MLT Borrowing

Disbursements 13.3 11.8 US $ MlnAmortization 7.7 5.7Subtotal 5.6 6.1 17.4 Public Debt, incl. guaranteed 88.7

Capital Grants - - - Non-Guaranteed Private DebtOther Capital (net) 5.7 6.5 8.9 Total outstanding & DisbursedOther items n.e.i 7.1 0.7 0.8 2Increase in Reserves (+) 3.9 8.0 -1.2 DEBT SERVICE RATIO for 197-

SOURCE CENTRAL STATISTICS OFFICE AND IBRD World Bank-9330

SUMMARY AND CONCLUSIONS

Introduction

1. Sierra Leone, with a population of around 2.7 million, has a percapita income of about US$160, comparable to levels in Nigeria and Cameroonor less than in Liberia. The economy is essentially dualistic -- a smallmodern sector co-exists with a large traditional agricultural sector in atribal setting, still generally outside the monetized economy and sustainingthree-quarters of the population. With the resources obtained from mineralexploitation, notably diamonds, Sierra Leone has pursued a development aimedat improving the socio-economic infrastructure. The available data suggestan average of 4.6 percent real growth of GDP in the 1963/64-1970/71 period,an impressive performance by West African standards. The two main sectorsof Sierra Leone's economy -- mining and agriculture -- have developed at verydifferent rates. The exploitation of mineral wealth, which has increasedfairly rapidly because of favorable international prices, has financed inturn a rapid growth in construction and services. In sharp cor.trast, agri-cultural production has more or less stagnated at 1.6 percent per annum, withserious implications, not only in terms of foregone foreign exchange earnings,but also in terms of food production and employment for a populatior. whichincreased at 2.2 percent per annum in the sixties and 2.4 percent since.

2. As elsewhere, accelerating agricultural development has provento be difficult because of firstly, deficiencies in administration, institu-tions and limited absorptive capacity to implement projects and secondly,limited investment resources allocated to the sector. Moreover, attitudes andtherefore investment by farmers were seriously impaired by an unfavorablepricing/ taxing policy for agricultural produce. Real incomes in agriculturerose, therefore, very little, resulting in a pronounced income inequality,more so than generally found in Africa, and widening rural-urban incomedisparities. The poorest 40 percent of the population receive just over 10percent of total income, while the highest 5 percent earn nearly 30 percent.One third of the families lived below a reasonable level of income, earningless than US$12 per month in 1968. Government policies tend to increaserather than reduce disparities and show a clear urban bias: low expendituresfor agricultural development, the Xeavy tax on agricultural exports, the lowprogressivity of income taxation, the exemption of diamond dealers andminers from income taxation, and consumer subsidies for rice, petroleumproducts and electricity.

3. Sierra Leone's development has been as much a problem of resourcemobilization as one of efficient allocation, and the country is now reachinga difficult stage in its development. To date, the resources derived directlyor indirectly from mining have largely taken care of both the domestic and

- ii -

external resource problems. But in the course of the 1970s the country'searnings from diamonds, which currently account for about 60 percent of totalexport receipts, will decline with the depletion of diamond reserves. If therelationship between growth and diamonds is maintained, it will make itdifficult if not impossible to expand national income at a pace sufficient topermit: (i) employment of a fast growing labor force; (ii) the sharing ofall classes in the benefits of development; and (iii) the provision of adequatesocial services. The development of the mining sector will continue to beimportant, since minerals other than diamonds are still insufficientlyexploited. But given Sierra Leone's factor endowments and little opportunityfor establishing an industrial base, agriculture must become the key factorin the country's economic development. It will have to absorb nearly all ofthe net addition to the labor force, provide sufficient food, and become amajor earner of foreign exchange. Moreover, spreading the benefits of develop-ment more widely is only possible through raising rural incomes.

Economic Background

5. The average annual growth of GDP from 1964 to 1971 of 4.6 percentconceals sharp year to year fluctuations, ranging from years of negativegrowth to years of 10 percent real growth. This pattern was, to a greatextent, influenced by vicissitudes of the world diamond market and exacerbatedby periods of political instability and inadequate fiscal management. Forsimilar reasons a recession set in 1971 and the economy has only now shownsigns of picking up.

6. The rise in the level of investment to nearly 16.5 percent of GDPin 1971 was an encouraging sign, even though nearly a quarter of gross fixedinvestment was in private residential housing. The share of public sectorinvestment averaged 20 percent, but the level of public sector investmentactually declined in real terms during the last decade and is now less than3 percent in terms of GDP. The domestic savings performance improved sharplyafter 1967 thereby reducing the reliance on foreign financing of investmentto about 20 percent. Nearly 14 percent of GDP was saved in 1971, and theimplicit marginal savings ratio during the period 1964-71 was an impressive27 percent. The growth of savings originated largely in the private sector.

7. The poor public savings record and a sharp increase in both domesticand external debt indicate a lack of restraint in current expenditure and aninadequate tax effort. The heavy reliance on indirect taxation has resultedin a very inelastic tax system while the rise in current expenditure wasparticularly rapid in recent years. Current government expenditures grew at11.5 percent per annum during the 1970-73 period, while revenues increased byonly 4 percent a year. Despite increased allocation for education, agri-culture, public works and transport, the level of these expenditures is stilllow relative to Sierra Leone's needs. Despite this, the Government's recentexpenditures appear distantly related at best to development needs. The main

- iii -

problem has been rising expenditures on police, defense and external affairs,which are absorbing about 2.5 percent of GDP (equal to nearly 80 percent ofdevelopment (capital) expenditures).

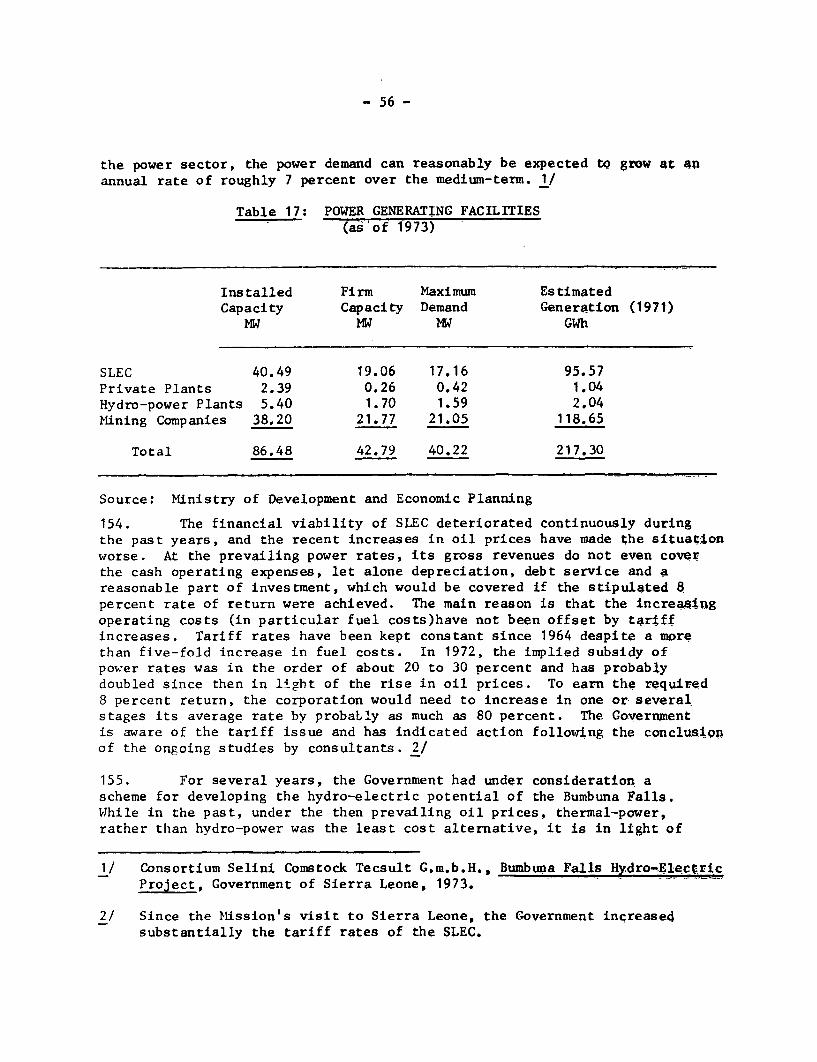

8. For FY 1973/74, current expenditures are estimated at approachingLe 68 million or a record increase of 18 percent over the previous year,attributable mainly to subsidies of rice and petroleum products and interestpayments on debt. Steps were taken belatedly to reduce the rice subsidy andto defer delivery of some of the special imports that had been contracted tomake up for a shortfall in domestic production. Subsidies to consumers ofgasoline, diesel and kerosene have also been somewhat reduced. Nevertheless,the rice and petroleum subsidies together account for as much as 10 percentof total current expenditures in 1973/74 and absorb more than a third of therevenue increase.

9. Foreign exchange reserves have risen steadily since 1967, to alevel of US$50 million or four months imports at the end of 1973, in spiteof regular current account deficits. These deficits reflected the persistentexcess of government expenditures over revenues, coupled with increasingdemand for imported consumer goods (largely induced by incomes in the miningareas). There would have been some improvement in the external trade balanceprior to 1972 but for a deterioration in the terms of trade of more than25 percent. In 1973 the terms of trade improved, but as diamond output fellabruptly, the current account deficit of US$27 million far exceeded that of$9 million in 1972.

10. The total net inflow of external capital over the period 1963-72amounted to US$220 million. The most important source of external financewas private foreign investment, totalling US$93 million. In addition, therewas net inflow of foreign aid of US$39 million and of suppliers' credits ofUS$25 million. Total public debt stood at about Le 114 million (US$136million) at the end of 1973 (US$47 million domestic and US$89 millionexternal debt), and the servicing of external debt amounted to 8.4 percent ofexports. Suppliers' credits were the largest source of external borrowing in1973 when a record of US$20 million was contracted and accounted for one-thirdof external public debt.

11. Development has been hampered as much by limitations of absorptive

capacity as by resource constraints; there has been no systematic effort tochannel resources into investment; and there has been a shortage of concreteprojects. Only if appropriate steps are taken by the Government to overcomethese constraints can the necessary diversification of the economy succeedand its dependence on diamonds be reduced. The establishment of a machineryfor economic planning with the assistance of UNDP in 1971 and the currentwork in preparation of a Five Year Plan are important steps in the desireddirection. 1/ The formulation and implementation of development policies and

1/ In August 1974, the Government finalized the National Development Plan1974/75-1978/79 and a forthcoming Bank mission anticipates to discussthis Plan with government authorities.

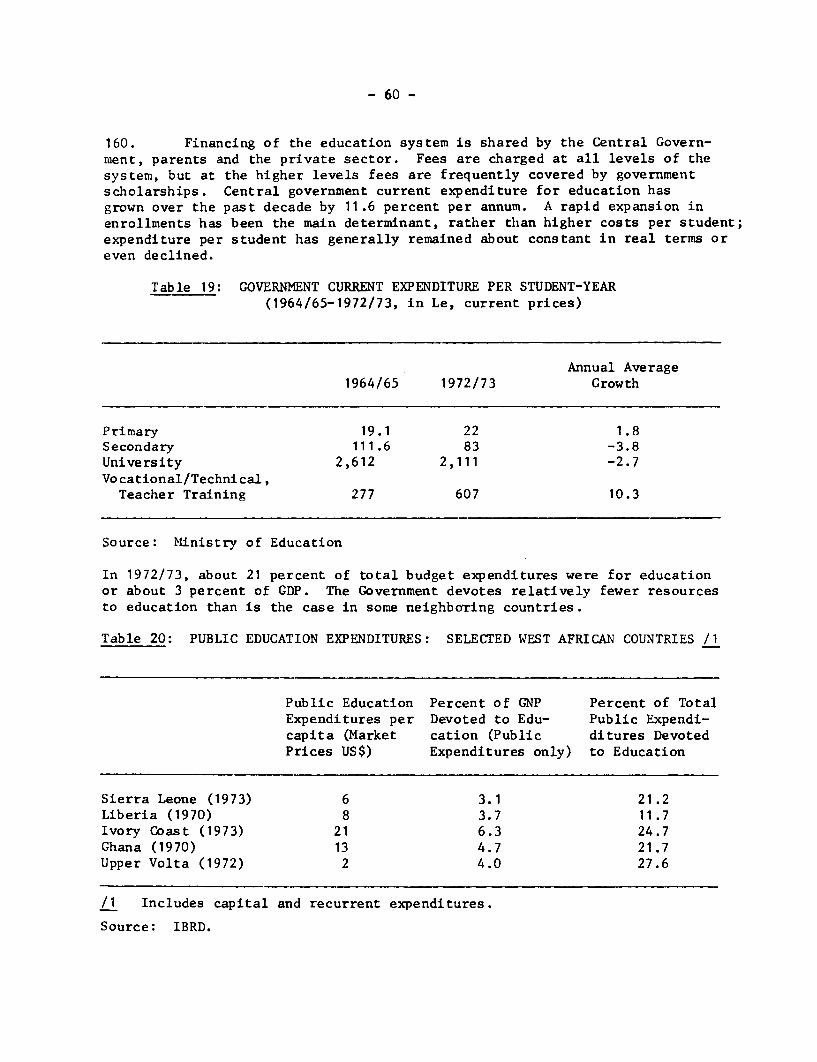

- iv -

investment programs need to be attuned as soon as possible to the new circums-tances if the time lag implicit in achieving economic diversification is notto be unduly long. There is also an urgent need to improve administrativeservices and management and to address the problem of institutional require-ments for plan implementation, including the training of staff.

Agriculture

12. There are good opportunities for accelerating the growth of agri-cultural output to about 3.5 percent per year in the medium to long run.Land and labor are relatively abundant; there is ample scope for introductionof improved technology in rice and tree crop production; and internationaland domestic demand for the country's agricultural produce should continueto expand. But realizing this potential will require a concerted governmenteffort to attack the constraints impeding development and to ensure greaterresources for agriculture, involving an estimated investment program of aboutLe 70 million over the next five years. Agricultural services are inadequate,credit and farm inputs are not available, fertilizer is used by 3 percent ofthe farmers, and one-fifth of the farmers growing cash crops or rice useonly the most primitive tools. The extension field staff is limited, andthe ratio of extension staff to farm families is 1:1,470.

13. Until the Government's development machinery improves, agriculturaldevelopment will have to depend largely on private initiative and a greatershare of agricultural value added should remain within the sector for privatereinvestment. While government revenue receipts would fall, in the medium tolong-run the revenues generated by a prospering agricultural sector shouldbe much larger than those forgone presently by an export tax reduction.Pricing policy is the single most important tool available to the Governmentfor stimulating agricultural production. Although farm gate prices increasedsomewhat in 1973/74, little of the current boom in world commodity prices hasbeen passed on to producers. In 1972, the farmers' share of the export price(f.o.b.) was about 70 percent for palm kernels and between 40 to 50 percentfor coffee and cocoa, while the support price for rice is presently aboutUS$120 per ton less than import prices. A revision in the export taxationof farm produce would be essential, and as an initial step a 50 percentreduction in taxes on cuik'.e and cocoa at current world prices and a 30percent reduction in palm kernel taxation should be considered.

14. More adequate farm inputs, credit and marketing and extension servicesare also essential, but far more complex to implement. A reorganization ofthe Marketing Board (SLPMB) and the Rice Corporation into a marketing-storage-input supply organization and the development of a minimum package programgeared to reach a large number of farmers could ease some of these constraints.

15. Production targets should continue to stress rice production inswamps, but greater emphasis must be placed on upland cultivation whichaffords the best possibility for accelerating production in the short run.Attention should also be concentrated on raising the output of export crops,notably cocoa and coffee with possible diversification into coconuts, rubber,cashew nuts and groundnuts.

- v -

16. The Government has opted for a regional approach to agriculturaldevelopment, which has been supported by IDA through its financing of anintegrated agricultural project in the Eastern Province. A similar projectfor the Northern Province is now being planned. Since development ought toextend beyond these Provinces, the Government should focus its limitedresources upon establishing key production centers in chiefdoms outside theEastern and Northern Provinces. By seeking chiefdom support, a maximuminvolvement of local leaders and of farm population will be insured. Thismay assist the Ministry of Agriculture in partly overcoming the absorptivecapacity constraint, provided the reorganization of the Market'ng Board iscarried out.

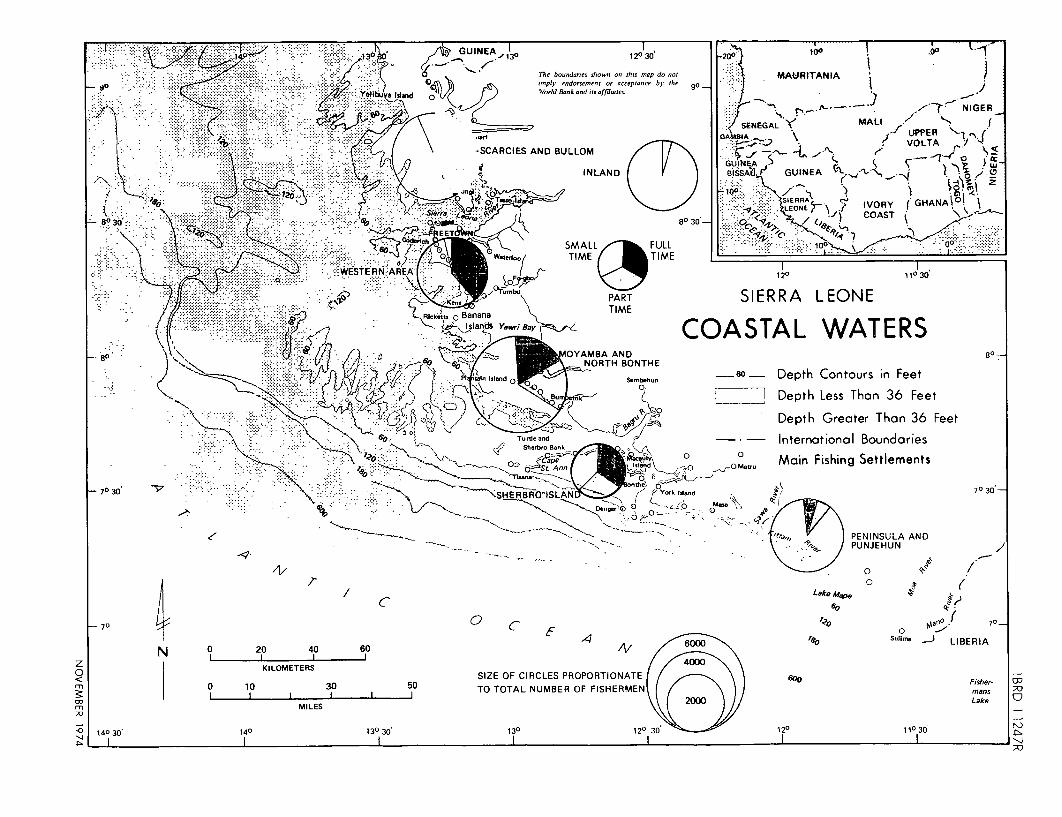

Fishery

17. The fish resources in Sierra Leonean waters could support a consider-able expansion in the indigenous fisheries industry and possibly make thecountry a net exporter. Provided that the organizational problems and thelow level of technology can be overcome and action is taken to graduallywithdraw permits of foreign boats operating in territorial waters, the fishcatch might be more than doubled over the next five years to a level of around100,000 tons a year. A basic issue of government policy concerns the balanceto be established between indigenous artisanal and industrial fishing onthe one hand and fishing by foreign vessels on the other hand. Action isalso needed to improve domestic processing and marketing, to provide betterinfrastructure, such as harbors and to strengthen government services to theindustry, particularly with regard to research, education and training andinstitutional credit.

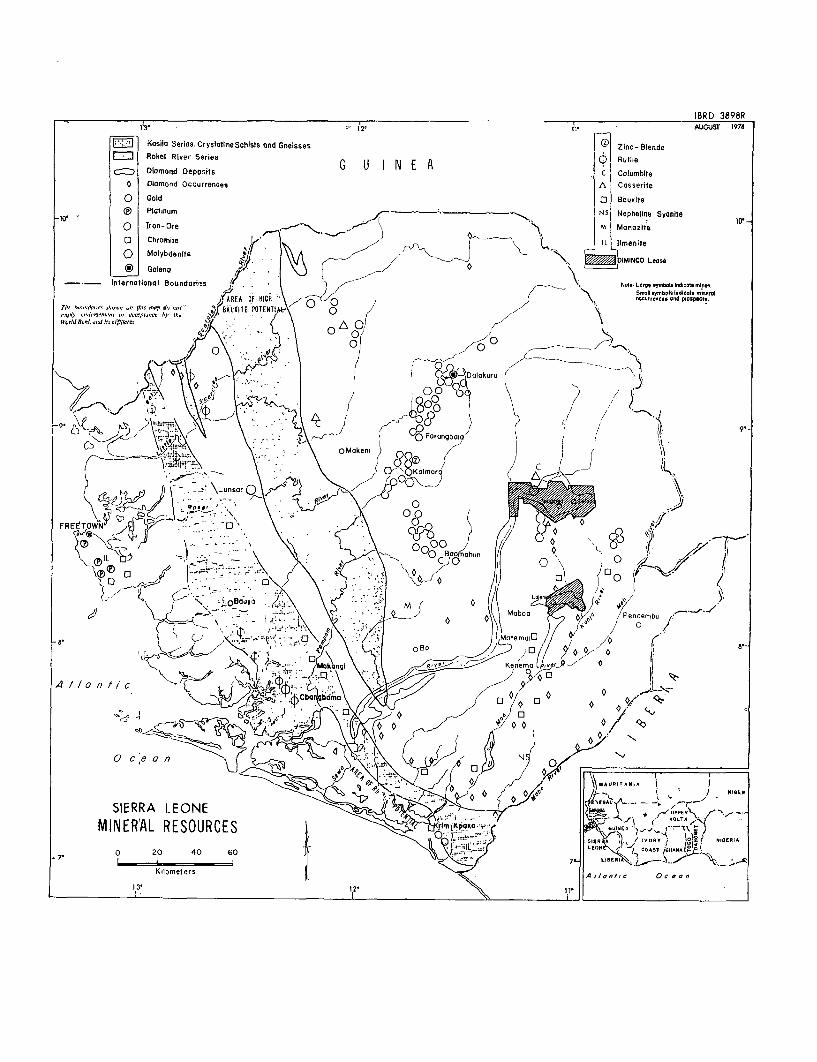

Mining

18. In recent years a bleak picture has been painted of the prospectfor diamond mining in Sierra Leone, as a result of the projected depletionof reserves. Recently, however, the recovery rate of DIMINCO increased by30 percent; the steep rise in diamond prices in 1973 makes it economicallyfeasible to mine deposits of lower grade and at a deeper level; and the newsystem of competitive buying is expected to reduce smuggling. Nevertheless,exports are expected to drop from around 1.4 million carats in 1974 to 700,000carats in 1980.

19. Prospecting which was halted in 1970 is unlikely to resume unlessillicit mining is controlled. Since this may not be feasible without offeringan alternative to diggers, consideration should be given to: (i) providingdiggers with technical and financial assistance on a larger scale than atpresent in order to achieve a higher recovery rate; (ii) increasing Govern-ment's own prospecting operations outside the DIMINCO lease; and (iii) allow-ing diggers to work small deposits within the lease that are at present un-economical for the company to mine.

- vi -

20. Other minerals - iron ore, bauxite and rutile - contribute around13 percent to total exports. Prospects for expansion of bauxite and rutilemining are favorable, with bauxite production expected to reach 2.3 milliontons and rutile output 150,000 tons by 1978. While a number of factors haveconsiderably increased the cost of operation of the iron ore mine, notablyhigher oil prices, its output can probably be maintained at the present level.As a result of these expected developments the share of these other mineralsin exports would rise to 46 percent by 1980. There is a need to assess thelong-existing concession agreements governing bauxite and rutile mining todetermine whether Sierra Leone receives a fair share of their profits,particularly now when the world market is very strong.

Social and Economic Infrastructure

21. Education. Since independence the Government has made an effortto increase access to education and to improve its quality. Despite theseimprovements 85 percent of the population is still illiterate, and onlyabout a third of primary school age children receive schooling. The Govern-ment is aware of the shortcomings of the education system and in 1973 itundertook an Education Review to formulate reform proposals. Total publicexpenditures on education amounted to over 20 percent of total budget expen-ditures in 1972/73 or about 3 percent of GDP. Some increase in budgetaryallocations appears to be desirable. But if Sierra Leone is to succeed inexpanding education's coverage and maintaining or improving its quality,some costs of the education system will have to be reduced. Curriculumchanges will be necessary to reorient primary and secondary education towardthe rural environment, and manpower requirements. Given the shortage oftechnically trained manpower, vocational and technical education and sub-degree programs at universities should be developed and expanded in suchareas as agriculture, management and health.

22. The health situation is unsatisfactory: life expectancy is around40 years, the rate of infant mortality is 183 per 1,000 -- one of the highestin the world -- about 28 percent of all deaths are among one-year infantsand complications of pregnancy and childbirth claim 20 percent of all deathsof females. The primary emphases of future programs should be on: (i) expand-ing health facilities in rural areas; (ii) improving the services for preand post-natal care and maternity care and introducing a family planningprogram; (iii) emphasizing preventive services, such as free distributionof anti-malarial drugs and provision of protected water supply; and (iv)increasing training of physicians and para-medical personnel.

23. Transport. Most of the public sector investment has been forimprovements of infrastructure, and the network of modern roads has consider-ably expanded over the past few years. True, many more roads are needed andthe temptation to over expand investments in roads, an area where absorptivecapacity does exist, is great. But with limited resources available, theemphasis on the transport sector has to be reduced if investments in thosesectors wich can produce the needed foreign exchange earnings and/or savings

- vii -

are to be implemented. W4hile some basic sections of the national highwaysystem remain to be constructed, there is a more urgent need for maintenanceand rehabilitation of existing roads and construction of feeder roads, link-ing the production centers with the main highways and markets.

24. Energy. The energy crisis has made the development of SierraLeone's hydroelectric potential - conservatively estimated at 1,150 MW ofinstalled capacity - economically viable. This adds a significant dimensionto Sierra Leone's ability to overcome the economic adjustment problem createdby the oil crisis. A feasibility study of the Bumbuna Falls scheme has beencarried out. Consideration should be given to an alternative constructionsequence than earlier proposed which is more consistent with both the anti-cipated growth in demand and the overall resource constraint. Meanwhile, anyprogram for the development of the power sector must encompass improvementsof the electricity corporation (SLEC) and a revision of tariff rates whichhave been kept constant since 1964. 1/

Development Prospects and the Resource Problem

25. Severe constraints on growth are imposed by the lack of skilledmanpower and the shortage of external finances, the latter aggravated byrecent changes in commodity prices, the poor outlook for diamond exports andinternational inflation. It is for these reasons tbat the medium-term growthprojections by the Mission of 3.5 percent real GDP a year until 1980 are farless optimistic than the preliminary growth target envisaged for the FiveYear Plan. This growth would essentially occur in agriculture and throughan expansion of bauxite and a renewal of rutile mining, marking the beginningof the necessary diversification of the economy. The following table summari-zes a projection of Sierra Leone's potential development toward the end ofthe decade:

1/ Since the Mission's visit to Sierra Leone, the tariff rates of the SLECwere increased by an average of 60 percent.

- viii -

Current Projected Growth GrowthLevel Level Rate Rate

Debt Service Ratio toGovernment Revenue 16.0 17.4 15.0

* - Leading to 4.5 percent in 1980-1982 and 5 percent in 1982-1985 periods.

26. To achieve a 3.5 percent growth of GDP, investment requirementsare projected to reach about 18 percent of GDP by 1980. Public sector invest-ment is projected to grow from about 3.5 percent of GDP at present to 7.5percent in 1980. The projected public sector investment program would amountto Le 280 million over the period 1974/75 to 1979/80. These are ambitioustargets, but the urgent need for economic diversification justifies a policyof maximizing savings and investments in the short run.

Domestic Resources

27. Substantial efforts to mobilize both public and private savingswill be essential if the public sector development program is to expandat the pace indicated above and if the resource gap is not to widen. On theGovernment side, a substantially greater savings effort is feasible anddesirable, depending very much on controlling the growth of current expendi-tures. While in the past tax revenues have been rising, the impact this hashad on aggregate national savings has been largely, if not entirely, neutral-ized by the behavior of current expenditure. Possible measures which couldbe taken include: a restraint on personnel expenditures, maintaining expendi-tures for defense, police and external affairs at current levels and a gradualphasing out of subsidies for rice 1/ and petroleum products. In order to ease

1/ Since the Mission's visit to Sierra Leone, the rice subsidy to consumerswas abolished in May, 1974 and the producer price for paddy has beenraised to Le 5 per bushel (equivalent to about US$222/ton of milled rice).

- ix -

the debt burden on the budget, supplier credit finance must be limited. Stepsshould also be taken to establish a budget bureau in order to ensure themuch needed coordination between the recurrent and development budget andimprove the internal control mechanism needed to force ministries andagencies to stay within their budgetary appropriations.

28. There is also a need to increase the tax contribution of the non-agricultural sector, particularly that of the concessions. Direct taxationaccounts for less than 20 percent of total taxes, which is low relative totax efforts in other developing countries. Indirect taxes are the mainrevenue source, and this has severely restricted the elasticity of the taxsystem. This could partly be overcome by implementing the relevant aspectsof the IMF "Report on Tax Reform in Sierra Leone". Additional measureswhich should be sought include: higher taxation for incomes between Le 400and Le 3,000; a system of standard assessments; and income taxation oflicensed diamond dealers. Beyond this, continued efforts are required toimprove tax administration and enforcement. Greater benefits could be derivedfrom the concessions through a tightening of exemptions on corporate taxes,a renegotiation of the concession terms in order to obtain more favorableexport prices, and the introduction of stumpage fees on log exports. Ageneral tariff revision plus a simplification of tariffs by changing thespecific import duties to an ad valorem basis are measures which should alsobe contemplated. Further, as public corporations have become a drain on thebudget, actions are needed now to review their pricing policies. Timelyimplementation of these measures should compensate to a great extent forthe likely fall in government revenues due to reduced diamond productionafter 1976/77.

29. The potential for private savings in financial assets could belarge if positive real interest rates were offered. A more efficient alloca-tion of resources by financial institutions could also be achieved were itnot for the presently distorted interest rate structure. Lending policiesand reserve requirements of commercial banks require reorientation to pro-vide the needed real resources for the agricultural sector which has prac-tically no access to institutional finance at present. Since the creationof a wholly new institution for agricultural credit would not appear to bejustified at present and commercial banks may not risk to lend directly toagriculture, they should be encouraged to lend indirectly, by channellingfunds either through the National Development Bank, the Marketing Board orthrough regional project entities.

External Resources

30. Recent changes in commodity prices will severely restrict foreignexchange availability in the next few years. The increases in oil and riceprices alone will cause an estimated loss of Le 27 million (US$32 million)a year on average between 1974 and 1980. Rice imports are not expected tofall below 37,000 tons a year until 1980, nor will possible substitution of

-x -

hydropower for petroleum take place before then. More serious, however, isthe gradual depletion of diamond reserves, even though there is uncertaintyabout the rate of decline. With a modest export performance, and rice and oilimports already imposing a strain on the balance of payments, other imports,particularly of consumer goods, will have to be restrained if the resourcegap is to remain manageable even with a growth of only 3.5 percent a year.Reducing the elasticity of "other" imports to 0.75 should be possible throughrestrictions on construction of luxury housing and a revision of import dutiesaffecting non-essential consumer goods. A favorable factor affecting thetrade balance is the projected improvement in the terms of trade, which couldbe of the order of 30 percent between 1974 and 1980.

31. As a consequence of these developments, deficits on the resourcebalance during the 1974-80 period are projected to amount to about Le 190million (US$230 million). With rising factor payments abroad by the miningsector the cummulative deficit on the current account.balance may reachLe 273 million (US$328 million) during the period. The gross capital inflowrequired is projected to be Le 371 million (US$446 million), or an averageof Le 53 million (US$64 million) a year. Undoubtedly, inflows of suchquantities would be unlikely should Sierra Leone not succeed in obtainingsubstantial amounts of foreign aid. A gross aid inflow of about Le 120 mil-lion (US$144 million) is projected until the end of the decade. Althoughthis foreign assistance is within present and anticipated lending programsof the agencies involved, it will be contingent upon a satisfactory perform-ance on the part of Sierra Leone both in overall terms and also with respectto the ability to carry out the projects involved.

32. Heavy reliance on suppliers' credits cannot continue since it wouldlead to an unmanageable debt service burden, particularly in terms of govern-ment revenues. Suppliers' credits amounting to about Le 4 million (US$4.8million) of new commitments a year could, however, be usefully absorbed andwould be within the limits of prudent debt management. Taking into consider-ation an inflow of private foreign investment of Le 74 million (US$89 million)as well as private short-term capital, SDR allocations and a drawing of twocredit tranches with the IMF, Sierra Leone would still have an uncovered gapof Le 77 million (US$92 million). To fill the gap the Government couldexercise various options. It could seek assistance from the IMF oil facility,the development funds of Arab nations and the European Development Fund, orborrow modest amounts from export credit agencies and commercial banks. Iffinancing is obtained along these lines, and most importantly, if Le 120million of foreign aid is available on concessionary terms, the debt serviceratio should not rise above the current 8.3 percent by 1980.

33. With some restraint on imports and a concerted effort to obtainexternal finance as outlined above, Sierra Leone should be able to managethe foreign exchange situation despite the combined impact of a depletion ofdiamond reserves and of high oil and rice prices, and achieve a 3.5 percent

- xi -

growth of GDP until 1980. Long-term projections are particularly difficultin view of the uncertain future of diamonds. However, a satisfactory growthperformance of 5 percent real GDP could be obtained by 1985, provided anumber of policies are adopted in order to: (i) improve fiscal policy andresource utilization; (ii) improve project preparation; (iii) insure that adeepening of the development process, particularly in agriculture, goes handin hand with appropriate policies, foremost pricing policies; and (iv) obtainexternal capital on suitable terms, limiting its use to high priority projects.

PART I

THE ECONOMIC STRUCTURE AND RECENT DEVELOPMENTS

Page No.

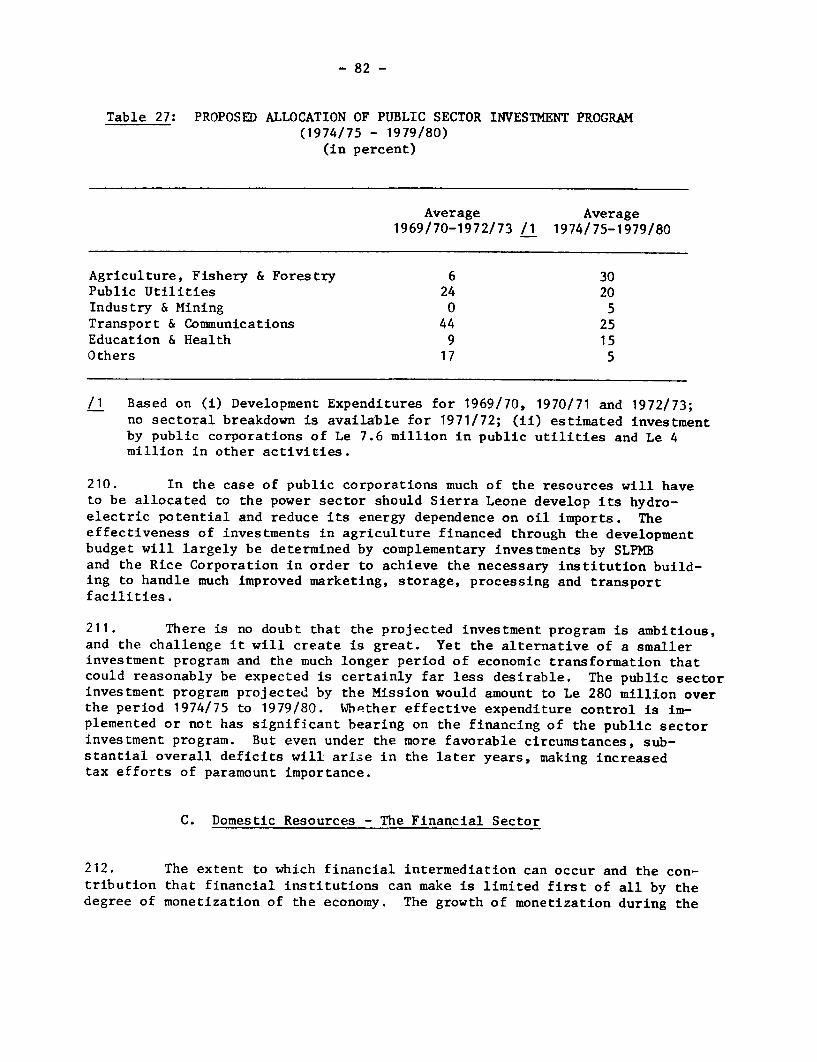

I. ECONOMIC TRENDS AND STRUCTURAL FEATURES OF THEECONOMY 1

II. POPULATION, EMPLOYMENT AND INCOME DISTRIBUTION 21

CHAPTER I

ECONOMIC TRENDS AND STRUCTURAL FEATURES OF THE ECONOMY

Overall Growth

1. Sierra Leone's growth performance was impressive by West Africanstandards: an average annual rate of 4.6 percent of GDP in real terms between1963/64 and 1970/71. As factor payments abroad declined over this period, realGNP grew on the average by 4.8 percent a year. With a population growth rateestimated at 2.2 percent, it appears that real GNP per capita rose on theaverage by 2.6 percent a year. The national accounts, available only for theperiod 1963/64 to 1970/71, do not necessarily present a perfect picture ofevents, but there is no reason to question their basic indications.

2. Since independence in 1961, Sierra Leone's economic development andthe sharp year to year fluctuations in its growth performance were to a greatextent affected by and interrelated with (i) the vicissitudes of the worldmarket for diamonds, the country's major export earner, (ii) periods of poli-tical instability and (iii) weak fiscal and debt management policies. From1963/64 to 1965/66 Sierra Leone experienced a real growth of 6.1 percent ofGDP per annum which was sharply interrupted by two years of depression whichbrought negative growth rates of 2.1 percent. Domestic factors were thebasic causes of this crisis: a sharp fall in agricultural exports (causedby a near collapse of the marketing board in 1966) and a drop of recordeddiamond exports (resulting from increased export duties and income taxes im-posed on diamond dealers) was exacerbated by weak fiscal performance (lack ofexpenditure control leading to excessive reliance on suppliers' credits anddomestic borrowing) and political instability. A strong recovery followed in1968/69 and 1969/70 with annual growth at 10 percent, induced by a rise indiamond exports and guided by an IMF stabilization program. Yet in 1970/71economic activity again slowed down for essentially the same reasons as duringthe 1966 crisis, resulting in a comparative absence of growth. There are nonational account statistics for 1971/72 and 1972/73, but on the basis ofavailable indicators, it appears that the tempo of economic activity startedto pick-up in 1973. Real growth in income was probably in the order of 2 to3 percent and came largely as a result of a marked increase in world pricesfor Sierra Leone's major exports, rather than through an expansion of output.

3. The level of GNP per capita in current prices based on officialnational account data was estimated at Le 136.2 ($163) in 1970/71. Followingthe low growth of the economy since 1970/71 and a population growth estimatedto have reached 2.3 percent, tentative mission estimates indicate that thelevel may have fallen to approximately Le 134 ($161) by 1973. This is almostequivalent to levels in Nigeria and Cameroon or less than in Liberia.

4. Yet, in an economy as strongly dependent on foreign trade as SierraLeone, the concepts of per capita GNP or GDP would be misleading indicatorsof improvements in real income since they do not take account of the incomeeffects of changes in the terms of trade. Despite the impressive growth ofvalue added in goods and services, a progressive deterioration in the terms

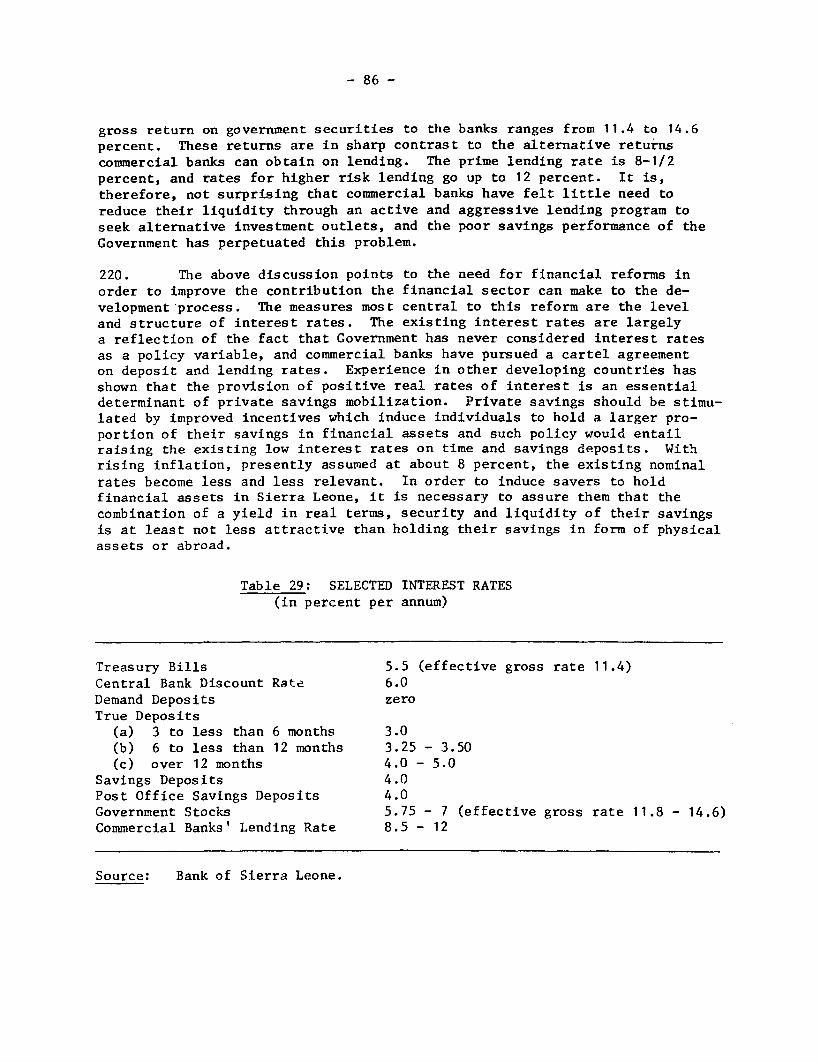

- 2 -

of trade since 1963/64 led both to lower earnings of those goods and servicesin terms of imports that could be purchased for a given volume of exports andto a reduced growth of gross domestic income (GDY is defined as GDP adjustedfor the income effect of terms of trade). As discussed later (para. 37), theterms of trade deteriorated by as much as 27 percent from 1963/64 to 1970/71.As a consequence of these adverse effects, real GDY rose on the average byonly 3.5 percent a year, thus bringing about only a moderate improvement interms of per capita income.

Structural Change and Sectoral Development

5. Table 1 shows sector growth rates, distribution of GDP by economicactivity between 1963/64 and 1970/71 and underlines the structural problem ofthe economy: an average annual growth of material production of only 2.8 per-cent, whereas the service sector and government expanded at 6.9 and 5.6 percentrespectively. The growth of material production reflects the low growth of theagricultural sector while the fast growing sectors, such as utilities and con-struction were initiated from a base too low to change the picture significantlyThe resulting structural transformation brought a decline in the share of mat-erial production from 65 percent to about 59 percent and led to an increasingimport dependency over the period.

Table 1: SECTORAL DISTRIBUTION OF GDP AND GROWTH RATES

Average annual growth inShares real terms over period

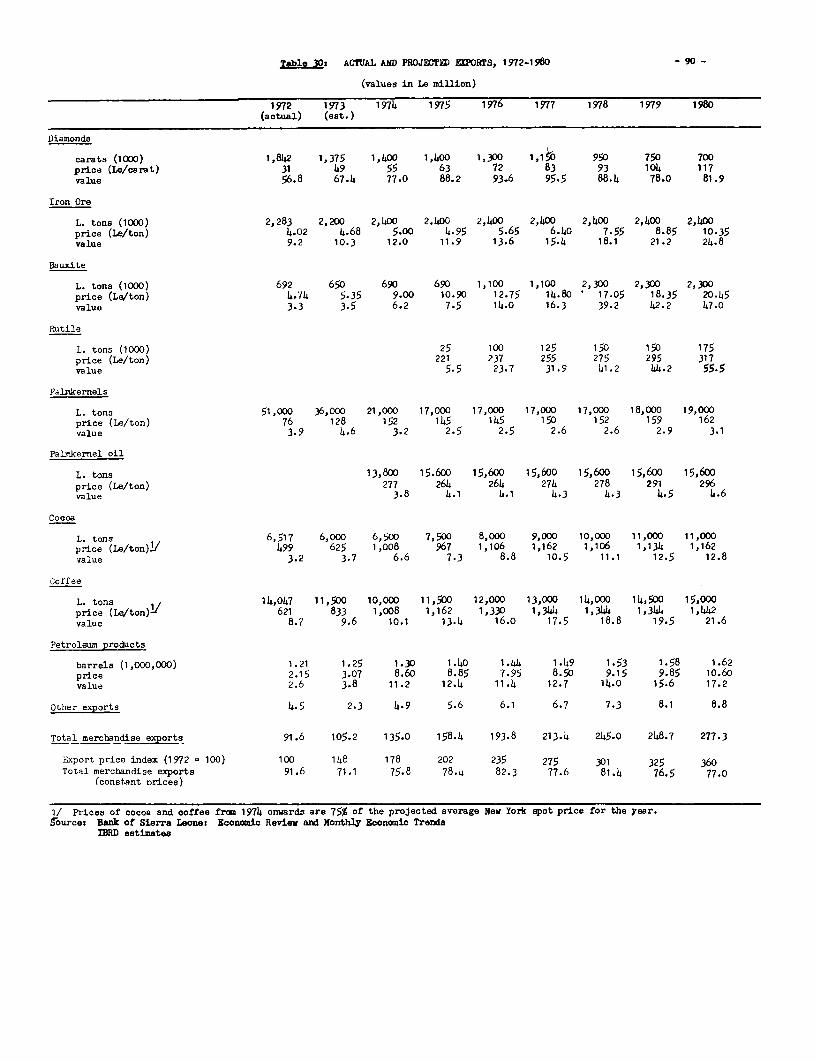

Government and Social Services 8.4 9.4 5.6 4.5 3.2 8.0

GDP (constant market prices) 100.0 100.0 4.6 6.1 -2.0 7.4

Source: National Accounts of Sierra Leone 1964/65 to 1970/71, C.S.O., 1972.

- 3 -

6. Agriculture, which sustains about 75 percent of the population, hadthe lowest sectoral growth - a mere 1.6 percent per annum over the 1963/64-1970/71 period. Looking only at the period 1967/68 to 1970/71 shows someacceleration of growth to 2.5 percent a year. Nevertheless, the repercussionsof low agricultural growth were serious, not only in terms of foregone foreignexchange earnings but also in terms of providing food and employment for apopulation increasing at a rate of 2.2 percent per annum. Of course, therewas no reason for agriculture to grow faster, given the low support it received.Although agricultural investment expenditures have increased from 4 percent ofdevelopment expenditures in 1963/64 to about 25 percent in 1973/74, they stillaccount for less than 1 percent of GDP. Moreover, the little investment under-taken had, with some few exceptions, only a minimal impact at the farm level.Similarly inadequate was the financing of supporting services: they accountedon the average for less than 5 percent of the current budget and benefited onlya small segment of farms. Probably the most depressing effect on growth ofagriculture was exerted by the pricing policy pursued which heavily taxesagricultural output and thereby deprives farmers not only of adequate incomesbut also of proper price signals and price incentives.

7. Value added in mining, originated primarily from diamonds and toa lesser extent from iron ore, bauxite and rutile, increased at an averageannual rate of 3.3 percent over the period 1963/64 to 1970/71, while for1967/68 to 1970/71 the sectoral growth rate averaged 7 percent a year.Yet the importance of this sector cannot be measured by its contributionto GDP alone, nor is it fully measured by the foreign exchange earnings.It contributes on the average 12 percent of government revenues (as muchas 30 percent in 1972/73) and two-thirds of export earnings, and throughmultiplier effects it also induces other demands, notably on imports andresidential construction. This over-dependence on depleting diamonddeposits is, however, one of the basic weaknesses of the economy. Afterhaving reached its peak in 1969, diamond output declined gradually in thefollowing years, but it was only in 1973 when output fell by as much as25 percent that the depletion of reserves became markedly evident.

8. Growth of the manufacturing sector has been limited partly bythe small size of the market for import substitutes. Small-scale estab-lishments predominate, although some factory-type enterprises exist, notablyin the food and beverage industries and an oil refinery was established re-cently. Most of the industries established in the 1960s were foreign-owned,capital intensive, relying mainly on imported raw and semi-finished materialsand dependent upon a high degree of effective protection. Their contributionin terms of value added is therefore low. Indications suggest that the ben-efits to the economy, either in terms of employment or in terms of foreignexchange saving derived from the Government's import substitution policy ofthe 1960s, was more than offset by the costs to the economy in the form ofhigher prices and foregone tax revenues through lavish tax concessions andprofit remittances.

- 4 -

9. Construction has been increasing more than twice as fast as GDP andfaster than all other material production, except utilities. A large elementof this growth came from the demands generated by mining income for residentialhousing, although highway construction by the Government has continued to bean important factor since 1965, having absorbed more than 50 percent of devel-opment expenditures.

10. Transport and port activities associated with the enclaves, agricul-tural exports, and the rising demand from urban population for local transportcontributed to the rapid growth of the service sector. With the exception ofgovernment administration, other service subsectors responded to the specificneeds of the economy. This has been particularly the case for education andhealth, although the efficiency with which these services were produced indi-cate great shortcomings. Similarly the growth of the financial sector is inpart a reflection of the rapid monetization which occurred with the activityin the diamond mining sector.

Investment

11. In 1970/71, the investment rate reached an all time high of 16.4percent of GDP, but preliminary estimates indicate that this rate may havefallen to about 14 percent in the subsequent years. During the period from1963/64 to 1970/71 the growth of gross fixed investment fluctuated widely,but with the exception of the 1966-68 depression this growth was appreciablyhigher than that of GDP. Fixed capital expenditures by the private sector -largely associated with enclave sector activities - provided the main impetus,increasing on the average at a rate of about 15 percent a year. In sharpcontrast was the slow growth of public sector investment expenditures whichaveraged only about 5 percent per annum. Total investment expenditures, incurrent prices, were on the average more than 70 percent higher in the1968-71 period than in the earlier part of the 1960s. But the compositionof total investment changed markedly: during 1968-71, private investmentrepresented over 80 percent and public investment only 20 percent as comparedto the early 1960s when the public sector accounted for nearly 30 percentof capital formation.

Table 2: SHARE OF INVESTMENT IN GDP

1963/64 1966/67 1968/691965/66 1967/68 1970/71

Gross fixed investment 12.1 12.6 14.9

Public 3.5 3.4 2.7Private 8.6 9.2 12.2

Source: Statistical Appendix Tables 2.1 and 2.3.

Table 3: GROSS FIXED CAPITAL FORMATION

(a) Annual average growth rates, in constant prices

Public 4.8 28.0 -23.0 18.7Private 15.2 25.0 3.5 17.5

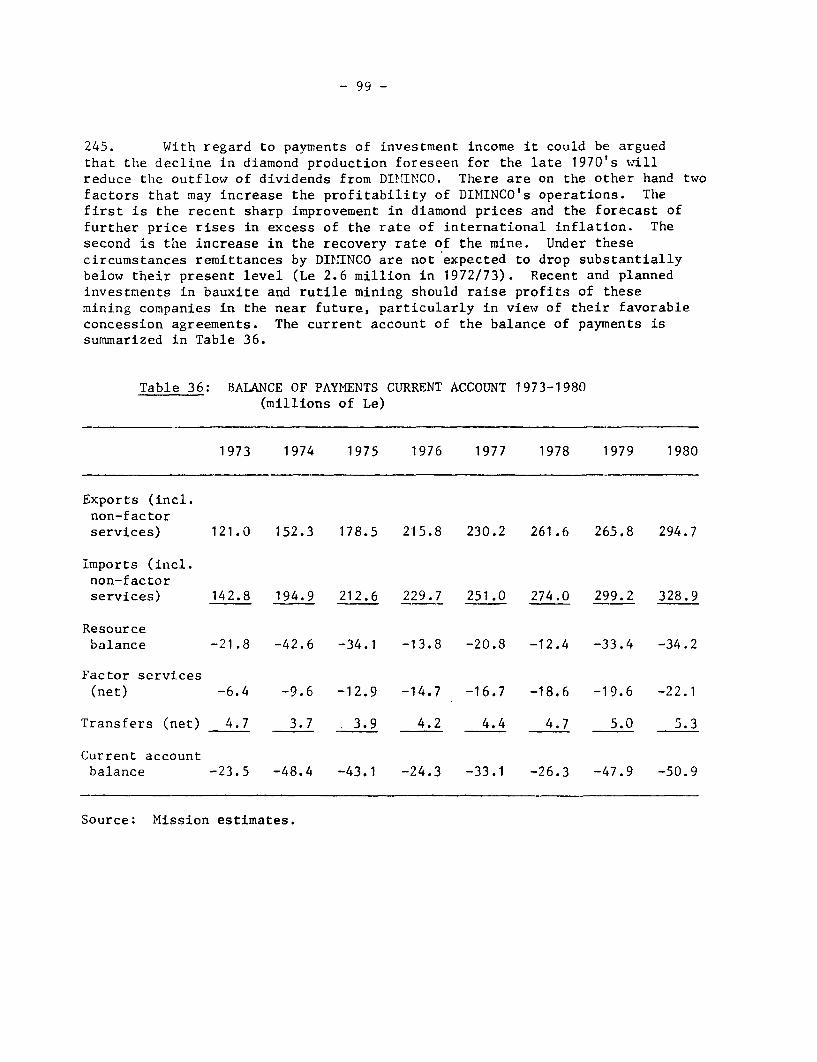

(b) Annual averages, in current Le million

1963/64- 1966/67- 1968/69-1965/66 1967/68 1970/71

Gross Fixed Investment 31 36 53

Public 9 10 10Private 22 26 43

Source:Statistical Appendix Tables 2.3, 2.10 and 2.11.

12. For the 1963-71 period the gross incremental capital output ratio(ICOR) was approximately 3.0 which appears to have been reasonable givenSierra Leone's stage of development. However, the extreme wide fluctuationsin the implicit ICOR raise the general question of the relationship betweenoutput growth and investment expenditure. Moreover, the gross ICOR is theresult of the particular composition of capital formation during the period.About one-half of total investment took place in construction, mostly resi-dential buildings. Most of the remainder was accounted for by other highlycapital intensive activities, such as mining and oil refining, which havegrown far less than GDP. Services, the growth sector contributing about 50percent to total growth, received relatively little additional capital. Allthis indicates firstly, the difficulty of drawing conclusions or derivingfuture projections from the ICOR, because changes in the structure of invest-ment will probably lead to a completely different ICOR. Secondly, it pointsalso to the importance of elements other than capital as factors of growth.There are signs that much of the non-residential investment has not given areturn as it should, largely as a result of inadequate planning and projectpreparation.

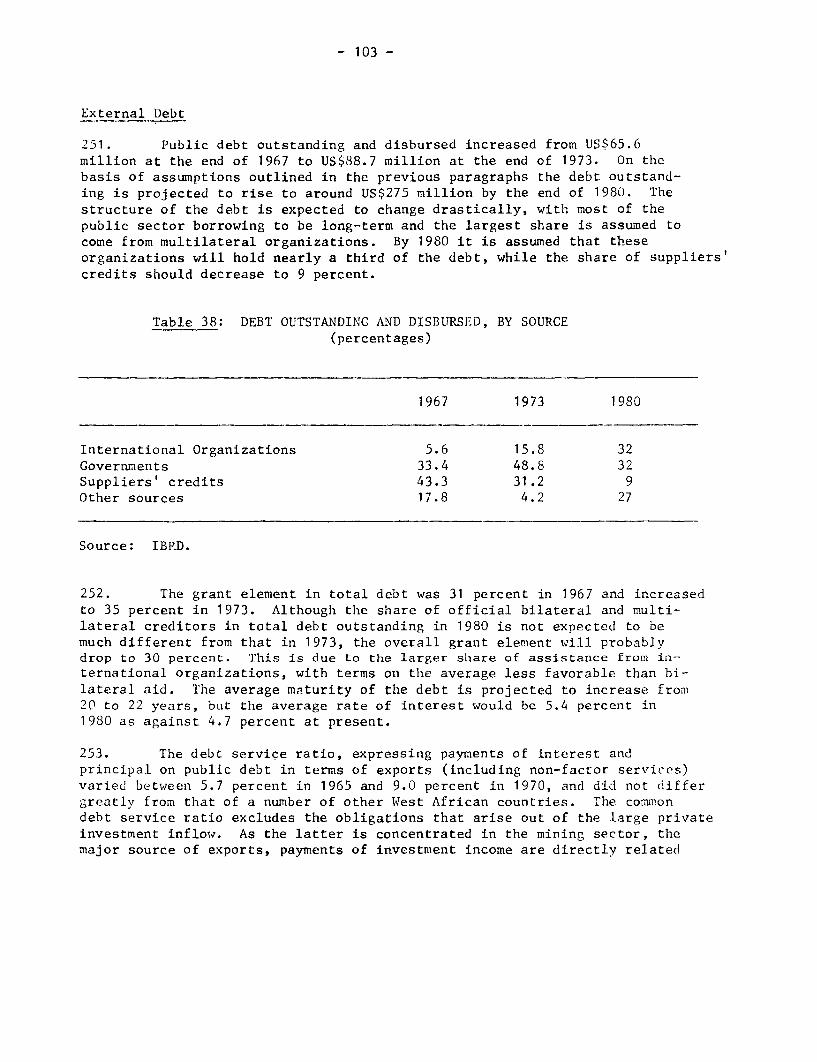

Investment and Savings

13. Table 4 below summarizes the investment-savings gap for the period1963/64 to 1970/71. As the overall savings performance improved continuouslythroughout the period, thus financing an increasing share of capital formation

-6-

in GDP, the investment-savings gap has steadily declined since the early 1960sto reach 3.7 percent of GDP in 1970/71. Except for the years 1968/69 and1969/70, the public sector has saved less than it has invested and the privatesector has a chronic savings deficit.

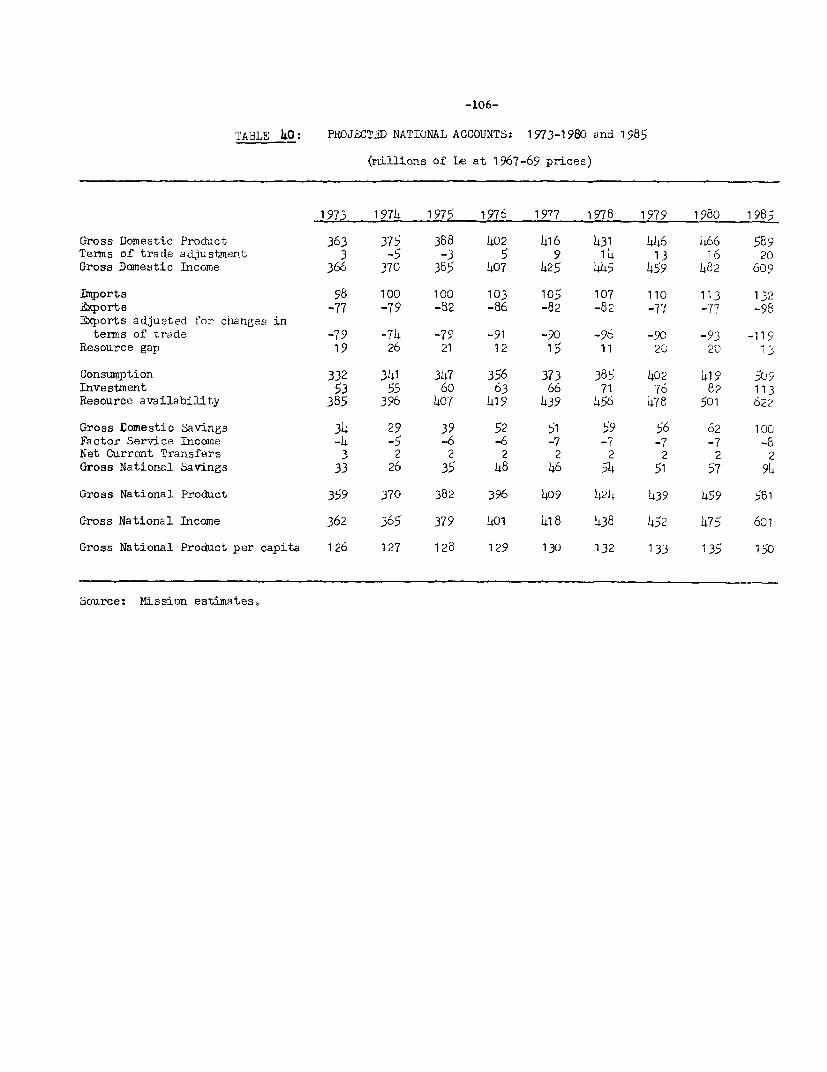

Table 4: PRIVATE AND PUBLIC SECTOR INVESTMENT-SAVINGS GAP

/1 Gross domestic investment minus gross domestic savings.

Source: Statistical Appendix, Section 2.

14. Savings performance in Sierra Leone has shown an encouraging trend:from 1964, the share of gross domestic savings in GDP increased from 5.3 per-cent to 13.8 percent by 1971, although the relative stagnant nature of theeconomy since 1971 would suggest that savings have improved little since then.In terms of gross national savings the average savings rate amounted to 13percent of GDP in 1971. The implicit marginal savings rate during the periodwas an impressive 27 percent. Sierra Leone's savings performance by 1971 was,therefore, not substantially at variance with the results of a cross-sectionanalysis of 70 countries, undertaken by IBRD, which shows that the predictedaverage propensity to save out of a per capita GNP of US$190 is estimated at13 percent. 1/ Most of the increase in savings originated in the privatesector, sharply in contrast to the public sector whose savings performancehas been generally poor. Private zavings generated close to 80 percent oftotal savings in 1971. As seen from Table 5, the upward trend in privatesavings has been distinct, induced greatly by export growth, and by a loweffective level of taxation of personal incomes in the urban sector and ofbusiness profits, notably from diamonds.

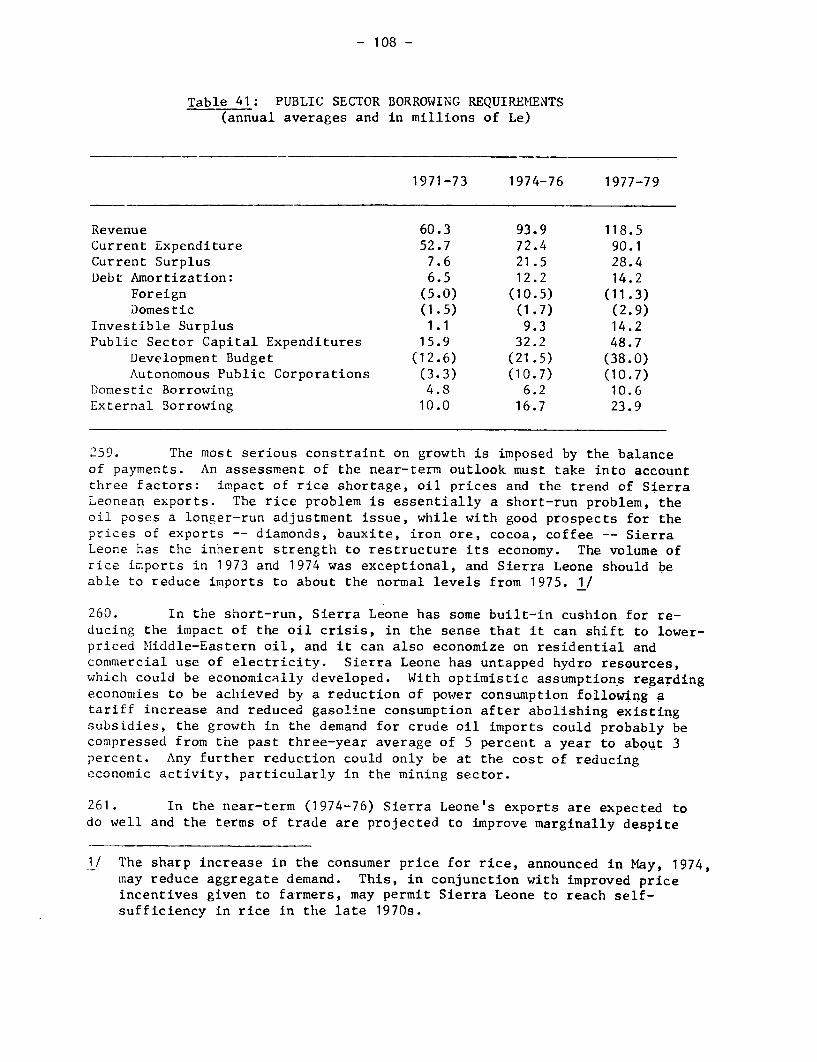

1/ IBRD "The Determinants of Aggregate Savings", Economic Staff Working PaperNo. 127, March 1972.

- 7-

15. Table 5 gives an illustration of the financing of gross fixed invest-ment derived from national accounts and balance of payments data. Throughoutboth the pre-depression and depression periods, with its fiscal and balanceof payments difficulties, investment levels could only be maintained by heavyreliance upon foreign savings and by drawing on external reserves. Duringthis period external finance accounted for between half to three-fourths oftotal investment expenditures and in 1964/65 it reached a record high of 77percent. The period since 1967/68 shows a drastic reduction in the relativeimportance of external financing of investment expenditures to a level ofabout 20 percent, although the share of capital formation in GDP continuedto expand.

16. Private direct investment from abroad was of relatively great im-

portance during the early 1960s when large mining investments took place andagain in 1969, with the expansion of bauxite mining and the start of the oilrefinery. During these years foreign investment ranged between Le 4.6 and13.5 million, accounting for between 1.6 and 4.7 percent of GDP. After 1969,the absolute level of foreign investment has fallen sharply to about Le 3.1million in 1972 or less than one percent of GDP.

Note: Figures do not add-up because national account data relate tofiscal years and balance of payments data to calendar years.

Source: Statistical Appendix, Sections 2 and 8.

17. Sierra Leone has no up-to-date economic indicators since 1970/71.It is, however, fairly generally accepted that the economy is depressed inpart because of an apparent decline in capital investment since 1970/71. Itappears that nearly all of this decline occurred in the private sector andwas largely associated with the completion of various investment programsin the mining sector. On the other hand, public sector investment seems onlyto have increased slightly faster than increased project costs arising out ofinternational price movements, thus the share of public investment in GDP hasprobably remained at about 3 percent. Part of the explanation for this devel-opment is attributable to the lack of absorptive capacity and to the fact thatthe current budget became far more expansionary than would have been warrantedby the increase in revenues. Also there appears to have been little or noimprovement in the savings performance of the private sector beyond its ownneeds. Moreover, private savings are largely held in form of physical assetsand the flow of such savings into financial assets has been small in recentyears. Thus an increased proportion of public investment had to be financedthrough credit creation.

Fiscal Development

18. Sierra Leone's fiscal performance during most of the period sinceindependence has imposed a serious constraint on public investment. The re-sulting resource problem was as much if not more a problem of expenditurepolicy and resource utilization as one of tax policy. The inadequate effortsby the Government in mobilizing resources on the one hand and restraininggovernment spending on the other, is evidenced by the low level of publicsavings and the sharp increase in both domestic and external debt with itsheavy reliance on suppliers' credits as means of financing budgetary expendi-tures.

19. There are indications that the taxable capacity has not been fullyutilized. While the tax effort has shown some improvement since the early1960s - in terms of GDP tax revenues rose from 12 percent in 1963/64 to 16percent in 1968/69 and reached about 14 percent in 1971/72 - it is stillsubstantially below the average tax effort of similar developing countries. 1/The buoyancy of the tax system which measures the percentage change in taxrevenues relative to percentage changes in GDP was relatively high, havinga coefficient of 1.5. Yet, the overall elasticity of the system, which refersto the revenue response of the existing tax system relative to changes in GDPand excludes the effect of tax system changes, has been extremely low, showinga coefficient of 0.7. As a result, revenue growth could only be maintained byfrequent adjustments in the tax system. Rough estimates indicate that about60 percent of the overall tax revenue increase was due to changes in the taxsystem, whereas about 40 percent of the total increase resulted from growthin GDP.

1/ See Annex 1, Fiscal Trends and Prospects, Chapter IV, which presents thedetails of a comparative analysis of the tax effort in 49 developingcountries.

- 9 -

20. The heavy reliance on indirect taxes (export taxes and import duties)which have provided between 60 and 80 percent of tax revenues in the past, isthe primary reason for the very inelastic tax system. This situation is,furthermore, exacerbated by the dependency on diamond production and on worldprices of Sierra Leone's exports. What improvement in the tax effort did occursince 1963/64, has therefore been nearly entirely associated with the growthof exports and imports. Illustrative of the structural problem of the taxsystem is the fact that the relative importance of indirect taxes is presentlygreater than a decade ago. Without improvements in the efficiency of collectionand the progressivity of direct taxation not only revenue growth was inhibitedbut also an increase in the elasticity of the tax system. The yield of directtaxation has increased by about 60 percent since 1963/64, but in terms of GDPdirect taxation changed very little, and in 1970/71 it amounted to about4 percent of GDP.

21. Recurrent expenditure growth during the last decade has been at anannual rate of about 7 percent. Yet without effective control recurrent ex-penditures increased sharply at a rate of about 11.5 percent a year during the1970-73 period, rising from 11.3 percent to 15.4 percent of GDP. This devel-opment had its inevitable repercussion on public savings since revenues grewonly 4 percent per annum: the recurrent surplus having reached Le 15 millionin 1969/70 fell to about Le 6 million in 1972/73. The sharp rise in non-productive expenditures for police, defense and external affairs was one ofthe main factors for the rapid expenditure growth. They rose from 12 percentof total current expenditures in 1963/64 to 17 percent in 1972/73 when thesize of these expenditures equalled nearly 80 percent of the development bud-get and about 2.5 percent of GDP. Rising education expenditures and an upwardadjustment in the civil service salary scale in 1971 also contributed signi-ficantly to the growth of recurrent expenditures.

22. During the past decade, allocations for development expenditureswere low, and though there was some fluctuation, they remained at a level of3 percent in terms of GDP. Domestic resource availability was certainly themost important constraint on development expenditure, followed by a limitedabsorptive capacity, and the lack of both concrete projects and a systematic-ally organized developmental effort. Largely because of these constraints de-velopment expenditures fell in several years short of their relatively lowbudgeted levels, notably in 1972/73 when development expenditures were 17percent below the previous year's level. The establishment of a planningmachinery in 1971 with the assistance of UNDP and the ongoing preparation ofa Five Year Plan should go a long way in removing part of these constraints.

23. Over the past years the Government has increasingly relied on bothdomestic and external borrowing. Debt statistics are only available since1968. In the following period total public debt has grown at an annual aver-age rate of 9.8 percent and amounted to about Le 114 million (US$136 million)at the end of 1973 (Le 40.1 million domestic and Le 73.9 million externaldebt). A large part of budget deficits were financed through expansion of

1/ The 1965/66 budget ran for 15 months. For ease of comparison all figures in this column are actual figures for 15 months reduced by 20 per cent.2/ Excluding debt amortization and transfers to the development budget. Interest payments on debt are staff estimates.3/ Includes Le 0.6 million resulting from a once-and-for-all direct tax receipt of Le 5 million associated with the sale of diamond stocks held bv

SLST at the time of formation of DOMINCO, minus government lending of Le 4.1 million to DOMINCO for working capital and Le 0.3 million to the RoadTransport Corporation.4/ Staff estimates.Sources Sierra Leone authorities, Economic Review and Economic Trends published by the Bank of Sierra Leone, Est,matas of Revenue and Expenditures,

and debt statements from the Auditor General.

- 11 -

domestic debt which more than doubled from 1968 to 1973. At the end of 1973,over one-third of outstanding internal public debt was held by the privatesector of which commercial banks were the single largest holder.

24. External debt (outstanding and disbursed) which expanded by 6 percenta year between 1968 and 1972, rose 10 percent in 1973. But including the un-disbursed portion, external debt was 19 percent higher in 1973 than in 1972.Suppliers' credits were the largest source of external borrowing in 1973 whena record of US$20 million new suppliers' credits was contracted. At the endof December, 1973, outstanding and disbursed suppliers' credits accounted forone-third of external public debt, and the servicing of external debt amountedto 8.4 percent of exports (goods and non-factor services).

Prices and Wages

25. Available indicators on price changes in Sierra Leone are not com-prehensive. The implicit GDP deflator has great limitations, and the priceindices for low-income groups in Freetown and in the mining area in theEastern Province give only some rough indication of changes in the pricelevel. 1/ The indices show considerable seasonality, with the price of foodincreasing in the rainy season as the supply of domestic foodstuffs reachingthe market dwindles. Between 1961 and 1972 the Freetown consumer price indexrose by 46 percent or at an average annual rate of 3.5 percent. Inflationarypressures were most severe in 1964 (11.5 percent, largely induced by a 22percent rise in housing costs) and in 1970, when they reached 7.6 percentfollowing a poor rice harvest. Over the 1961-72 period the changes in theconsumer price index were largely determined by a two-fold increase in thehousing price index, a 30 percent rise in food items and a 20 percent in-crease in clothing. The explanation for the sharp rate of inflation inthe housing item (including rents, fuel, light, furniture, etc.) is attri-butable mainly to migration and the scarcity of low cost housing in Freetown.A poor rice harvest again exerted strong inflationary pressures in 1973. Bythe second quarter of 1973, the Freetown consumer price index had increasedby 7.3 percent as compared with the second quarter of 1972, while the rateof inflation of food items accelerated at 15 percent over the same period.

26. Compared to Freetown, the rate of price change was considerablyless in the mining area, reaching only 2.8 percent a year during the 1961-72

1/ Both indices are based on budgetary surveys held in 1961 which onlycovered low income groups with household earnings of less than Le 40per month. Domestically produced food items have a heavy weighting andvery few imported items are included in the indices. Import prices haverisen more rapidly than those of domestic goods, both because of inflationin supplier countries and the depreciation of the Leone resulting fromits being pegged to the pound sterling. Hence the indices do not reflectthe effects of one of the major causes of domestic price increases.

- 12 -

period. Because of subsidies provided by the mining companies, the housingitems rose less than the overall price index. However, similar subsidieson rice could not prevent the food index from increasing at 3.7 percent ayear, slightly faster than the 2.7 percent annual increase of food pricesin Freetown.

27. Wages have been quite stable in monetary terms thus decliningsecularly in real terms. There is, therefore, little indication which wouldsuggest a link between inflation and wage legislation in Sierra Leone. Bydeveloping country standards industrial wages are low compared to agricul-tural wages, showing a ratio of less than 2:1. Civil service wages arehigh, however, compared to other wages in the economy.

28. Following several years when wages in the private sector didnot change, a round of wage negotiations took place between 1969 and 1970during which the then-prevailing wage rates were established as minimumrates. The rates for manual labor vary between Le 0.85 to Le 1.55 a day, andfor non-manual workers between Le 26.85 to 53.50 per month. To review civilservice salaries, which have not been increased since 1957, the Hugh ClarkCommission was appointed in 1969, and based on its recommendations, civilservice salaries were raised in September, 1971. A 10 percent raise was grantedto employees with an income of Le 500 per annum or less, while those earningmore than Le 4,700 per year received no increase.

29. In September, 1971, the Regulation of Wages and Industrial RelationsAct established a Joint National Negotiating Board to determine minimum wages,public holidays and maximum hours of work for employees below the supervisorylevel. The Act also provides for the establishment of trade group negotiat-ing councils to determine wages and conditions of service for employees ofparticular trades. Previously wages and other conditions of service weredetermined through a system of joint industrial councils and wage boards onwhich trade unions and employers were represented. So far four agreementshave been concluded under this Act, covering workers in industry, construction,commerce and mining. In the mining industry, the basic wage was raised toLe 1.00 per day, while for industrial workers the basic daily wage was es-tablished at Le 0.90 (US$1.08). Most establishments in the modern sector whoare regular employers adhere to the legal minimum wage, but in the rural areas,where this would result in a substantial increase in labor costs, actual wagesare often very much lower. The average farm wage in Sierra Leone is onlyLe 0.63 (US$0.75) per day including food valued at Le 0.18.

Monetary Developments

30. Only since 1968 has Sierra Leone's financial system experienced anexpansion. In the period 1964 through 1967, total liquidity (money supplyplus quasi-money) changed very little in nominal terms, and the real sizeof the financial system declined, with total liquid assets to GDP fallingto 11.8 percent in 1967. After 1967, the first year of the IMF stabilizationprogram and with increased investment and output, the size of the financialsystem showed a sharp recovery. By 1971, the ratio of total liquidity to

- 13 -

GDP rose to 13.5 percent and regained its 1964 level. The growth of totalliquidity accelerated sharply to 16 percent in 1972 and to as high as 27percent in 1973. No national income data is available beyond 1971, butgiven the relatively sluggish economy since then the real size of the fi-nancial system in terms of GDP must have increased markedly. Yet despitethe rapid expansion of the financial system, it was not accompanied by anychange in the asset composition, and the share of quasi-money in totalliquidity remained at about one-third.

31. The absence of both an effective interest rate policy and of asavings strategy, which could have reinforced fiscal policy measures byfinancial policies in order to channel private savings into financial assets,accounts for this lack of development. Interest rates for time and savingsdeposits ranged between 2 to 4 percent during the past decade and at thatlevel they offered only a negative real return on savings in financial assets.

32. From 1964 to 1966, domestic credit expansion of Le 6 million wasentirely on account of the public sector. It resulted only in a minor increasein the money supply because of the rise in quasi-money and other assets. Insharp contrast was the 1966-1972 period when total domestic credit grew byonly Le 7.6 million with nearly three-fourths on account of the private sector.The expansion of money supply of Le 16 million originated primarily from amore than four-fold increase in foreign assets reaching a level of Le 36 mil-lion at the end of 1972. Yet the period June, 1972 to June, 1973 showed asudden explosion of credit to the public sector: it more than doubled duringthis fiscal year, reaching a level of Le 15.6 million. At the same time com-mercial banks had difficulty in finding suitable lending outlets in the privatesector although their liquidity was rising rapidly in line with the build-upof foreign assets.

- 14 -

Table 7: CHANGES IN MONEY SUPPLY AND QUASI-MONEY AND FACTORS AFFECTING CHANGES

(in millions of Le)

1964-1966 1966-1968 1968-1971 1972 1973(at the end of December) June Dec. June Dec.

/1 Includes non-monetary liabilities of the banking system.

Source: DMF, International Financial Statistics, Bank of Sierra Leone,Economic Review, 1972.

33. During the second half of 1973, credit to the public sector continuedits sharp expansion and was only halted in December, 1973 following a suddenimprovement in the financial position of the Government with the banking sys-tem resulting from record profits from the National Diamond Mining Company(DIMINCO). The minimal credit expansion to the private sector during FY1972/73was largely a reflection of the commercial sector to sluggish consumerdemand which brought reduced import orders and a depletion of inventories.This situation changed drastically in the second half of 1973, leading toan increase in the credit need of the private sector. At the end of 1973,private sector credit had increased by 32 percent over the previous year.The rapid growth in money supply during 1973, taking largely the form ofincreased currency in circulation has not yet resulted in extreme infla-tionary pressures, but this may very well be only a matter of a 6 to 8 monthstime lag. The other explanation for this peculiarity seems to be related to(i) the continuing willingness of the public, notably in the diamond miningareas, to increase their cash balances at times of buoyant diamond activities,since purchases of diamonds are made exclusively in cash, and (ii) the factthat most credit creation was in conjunction with food imports.

- 15 -

Balance of Payments

34. Sierra Leone is very dependent on foreign trade. With year to yearfluctuations, exports have averaged 25 percent of GDP at market prices andimports close to 30 percent since 1964. The Government has found it advantage-ous to pursue liberal policies essential for an open economy. Sierra Leone is,therefore, among the few West African countries which do not have restrictionson trade or capital movements and its exchange rate policy is one of floatingthe Leone in line with the pound sterling.

35. Although a number of trade restrictions exist most commodities maybe imported freely. To protect local production some goods are subject toquantitative restrictions. Capital movements are subject to exchange controlbut the restrictions actually imposed are few and investments by non-residentsand profits may be freely repatriated. The imposition of import and exportduties provided 55 percent of budget revenue in recent years, about 85 percentof this on account of import duties alone. Since 1970, the actual nominaltariff rate is around 20 percent - a substantial reduction from the rate ofabout 30 percent prevailing during the 1966-68 period. It is difficult,however, to ascertain to what extent this reduction is a result of liberaliza-tion measures or of higher government imports which are duty exempt. Thetariff structure is unnecessarily complex, consisting too often of specificand ad valorem rates on the same goods and its wide range reflects the factthat tariff policy is regarded predominantly as a revenue device. Tariffsnave been modified from time to time in response to revenue requirementswithout due regard to other economic implications. As a consequence, manyequipments and inputs for agriculture and fishery are heavily taxed. Aslong as Sierra Leone is still in its pre-industrial development stage, re-venue generation as the primary aim of a tariff schedule is an alternativeto sales and excise taxation.

36. The leone is linked to sterling at the rate of Le 1 = h 0.50. Thelink was maintained when in June, 1972 the U.K. Government decided to floatthe pound. At the currency realignment in December, 1971 the exchange ratefor the leone was fixed at Le 1 = SDR 1.20 or US$1.30. Since the floatingstarted this rate has dropped to its present level of close to US$1.20.

37. Exports are dominated by diamonds, which contribute consistentlyaround 60 percent to merchandise exports. Other exports consist of variousminerals - iron ore, bauxite, rutile - and agriculture produce (palm kernels,cocoa, coffee). The composition of exports did- not undergo drastic changesduring this period either in terms of value or in terms of volume (Table 8).

- 16 -

Table 8: COMPOSITION OF EXPORTS

(in percent)

in current prices in constant prices1964/66 1971 1972 1973 1964/66 1971 1972 1973

/1 The relative increase in the volume of agricultural exports after 1971is probably caused by the release of coffee stocks built up in previousyears.

Source: Central Statistics Office.

The value of exports grew at a moderate average rate of about 5 percent peryear between 1964 and 1973. The pattern of growth up to 1972 matched closelythe overall growth performance of the economy. In 1973, exports picked upconsiderably, but entirely as a result of price developments (Table 9).Prior to 1972, fluctuations in value and volume of exports were closelylinked. Yet in 1972 and 1973, prices became the determining factor in therevival of exports, particulary in 1973, when they more than offset the 21percent decline in export volume.

38. Prices of major agricultural exports rose by 42 percent in 1973,but more important was the upsurge in diamond prices. The best availableindicator of the long-term price trend of diamonds is probably the pricelist of the Central Selling Organization (CSO) in London, which forms thebasis for the valuation of diamonds in Sierra Leone. Between 1963 and 1972,CSO prices rose roughly by 6 percent a year. The increase in the exportunit-price (per carat) was less, as this incorporates the effects of changesin the composition of diamond exports (gem stones versus industrials) aswell as in the quality of the gem stones. There are indications that theproportion of gems has been declining. Late in 1972 and during 1973, theCSO introduced a number of price increases and as a result the 1973 exportunit-price is estimated to be 56 percent over the average price for 1972.Thus, the value of diamond exports went up sharply despite a drop of nearly40 percent in volume.

39. From a level of Le 82.4 million in 1964, imports rose at an annualaverage rate of 3.7 percent to reach Le 109.8 million in 1972, but increasedsharply in 1973 to Le 127.5 million. However, with continuously increasingimport prices the growth of imports in real terms over the period was closeto zero; the volume of imports in 1973 hardly exceeded that of 1964/65 (Table10). It is likely that in the period 1970-72 the Non-Citizens (Trade and

- 17 -

Business) Act and currency uncertainties had a depressing influence on trade.The effect of import substitution can only have been minor, considering thatthe manufacturing sector was unable to maintain even its low share in GDPbetween 1963/64 and 1970/71.

Table 9: INDICES OF EXPORT PERFORMANCE(1967-69 = 100)

Value of merchandise imports 105 119 115 119 154Volume of merchandise imports 106 110 101 99 106Import prices 99 108 114 121 145

/1 The indices of import values are based on data expressed in currentUS$. The import price index is the average of the export priceindices of the four major supplying countries.

Source: Central Statistics Office, Freetown.