45

SILA VIRTUAL CHAPTER 2 ND QUARTER WELCOME! 1

| Date post: | 28-Dec-2015 |

| Category: |

Documents |

| Upload: | edith-daniel |

| View: | 238 times |

| Download: | 0 times |

SILA VIRTUAL CHAPTER2ND QUARTER

WELCOME!

1

Sila virtual chapter2nd quarter

2

• Highlighted Features– SILA National Education Conference– SILA Newsletter - 6/28/2013– SILA Discussion Forum– SILA Digest Service

Workforce Screening-Navigating New Legislation, Compliance and the EEOC

Introduction

WELCOMEWorkforce Screening

Navigating New Legislation, Compliance and the EEOC

Bon IdziakCEO, Applicant Insight, Inc.

Chairman, HR-XML ConsortiumCo-Chair, NAPBS Government Relations

BOD, SAPAA Substance Abuse Program Administrators Assn

4Applicant Insight Inc.-Confidential 2013

Legal Notice

DISCLAIMER

This presentation does not constitute legal advice or guidance.

Consult your own legal counsel regarding any questions of law or how the topics discussed apply to you and the unique needs

within your organization.

5Applicant Insight Inc.-Confidential 2013

Presentation

Presentation Topics

•Consumer Financial Protection Bureau-FCRA

•EEOC Guidance on the Use of Criminal Records

•End User Responsibilities

•Statewide Legislative Efforts

6Applicant Insight Inc.-Confidential 2013

CFPB

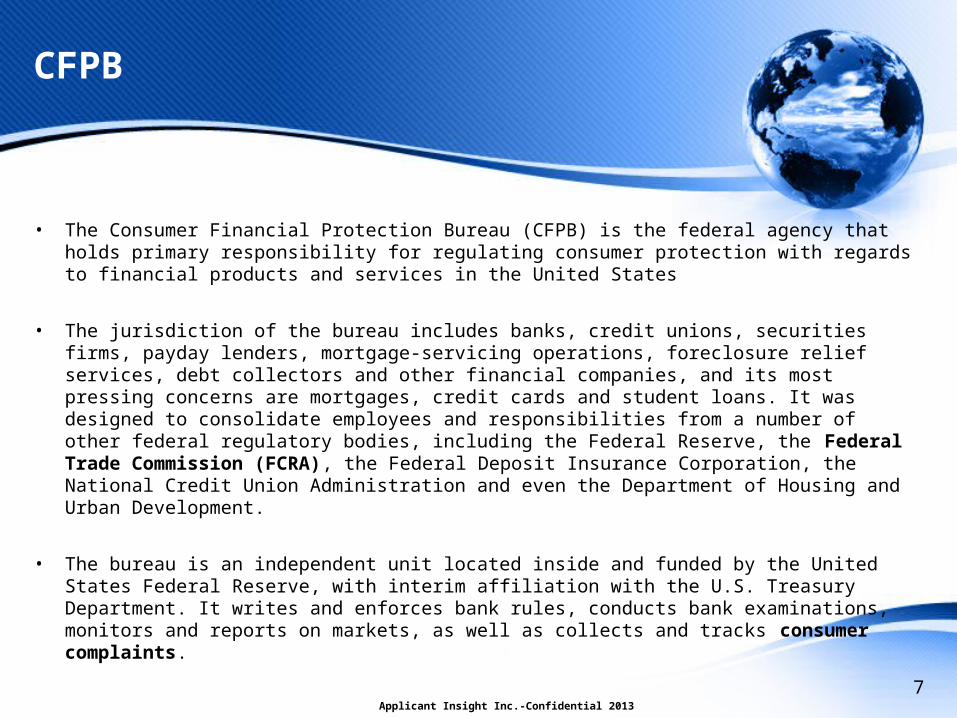

• The Consumer Financial Protection Bureau (CFPB) is the federal agency that holds primary responsibility for regulating consumer protection with regards to financial products and services in the United States

• The jurisdiction of the bureau includes banks, credit unions, securities firms, payday lenders, mortgage-servicing operations, foreclosure relief services, debt collectors and other financial companies, and its most pressing concerns are mortgages, credit cards and student loans. It was designed to consolidate employees and responsibilities from a number of other federal regulatory bodies, including the Federal Reserve, the Federal Trade Commission (FCRA), the Federal Deposit Insurance Corporation, the National Credit Union Administration and even the Department of Housing and Urban Development.

• The bureau is an independent unit located inside and funded by the United States Federal Reserve, with interim affiliation with the U.S. Treasury Department. It writes and enforces bank rules, conducts bank examinations, monitors and reports on markets, as well as collects and tracks consumer complaints.

7Applicant Insight Inc.-Confidential 2013

CFPB

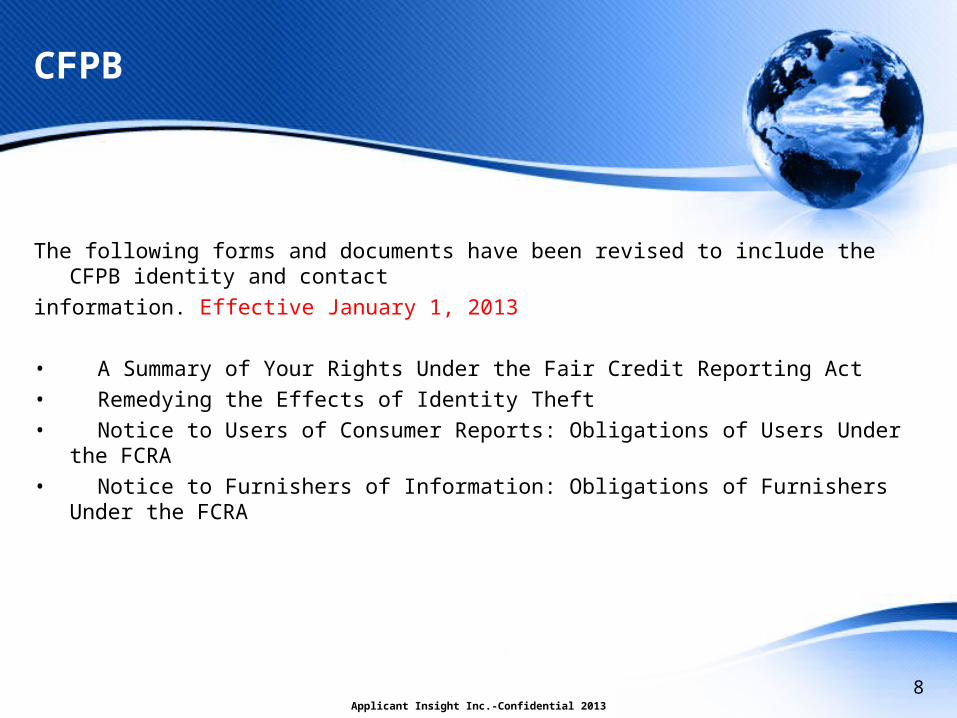

The following forms and documents have been revised to include the CFPB identity and contact information. Effective January 1, 2013

• A Summary of Your Rights Under the Fair Credit Reporting Act • Remedying the Effects of Identity Theft• Notice to Users of Consumer Reports: Obligations of Users Under the FCRA• Notice to Furnishers of Information: Obligations of Furnishers Under the FCRA

8Applicant Insight Inc.-Confidential 2013

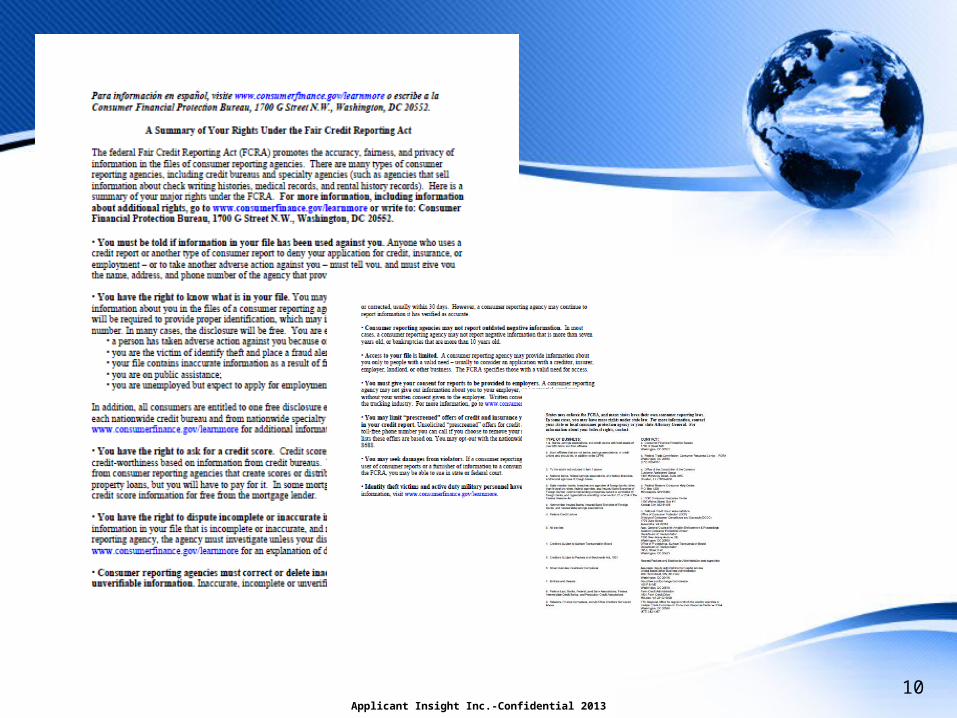

CFPB

A Summary of Your Rights Under the Fair Credit Reporting Act

• Provided to Consumers as a component of the Disclosure Notice, Acknowledgement and Authorization for Consumer Reports, and in the event of Adverse Action

• Details the “Rights” of a Consumer as afforded by the Fair Credit Reporting Act • Provided by End-User and/or Consumer Reporting Agency acting on behalf of End-User

9Applicant Insight Inc.-Confidential 2013

Applicant Insight Inc.-Confidential 2013

10

CFPB

Remedying the Effects of Identity Theft

• Provided to Consumers who claim to be a victim of Identity Theft • Details the “Rights” of a Consumer as afforded by the Fair Credit Reporting Act • Provided by Consumer Reporting Agency and/or End-User

11Applicant Insight Inc.-Confidential 2013

Applicant Insight Inc.-Confidential 2013

12

CFPB

Notice to Users of Consumer Reports: Obligations of Users Under the FCRA

• Provided to End-Users who utilize Consumer Reports • Details the “Legal Obligations” of an End-User as outlined in the Fair Credit Reporting Act • Provided by Consumer Reporting Agency

13Applicant Insight Inc.-Confidential 2013

Applicant Insight Inc.-Confidential 2013

14

CFPB

Notice to Furnishers of Information: Obligations of Furnishers Under the FCRA

• Provided to Furnishers of Information to Consumer Reporting Agencies• Details the “Responsibilities” of a Furnisher of Information as outlined in the Fair Credit Reporting Act• Provided by Consumer Reporting Agency

15Applicant Insight Inc.-Confidential 2013

Applicant Insight Inc.-Confidential 2013

16

Equal Employment Opportunity Commission

The Equal Employment Opportunity Commission's (EEOC) new Enforcement Guidance on Consideration of Arrest and Conviction Records in Employment Decisions Under Title VII of the Civil Rights Act of 1964 passed by a 4-1 vote of the EEOC’s Commissioners on April 25, 2012.

http://www.eeoc.gov/eeoc/newsroom/index.cfm

Commissioners Chair Berrien Commissioner LipnicCommissioner FeldblumCommissioner BarkerCommissioner Ishimaru -left commission after vote. Now is Commissioner Yang.

17Applicant Insight Inc.-Confidential 2013

EEOC: What is Title VII?

The EEOC enforces Title VII of the Civil Rights Act of 1964 which prohibits employment discrimination based on race, color, religion, sex or national origin. The Guidance is issued as part of the Commission’s efforts to eliminate unlawful discrimination in employment screening, for hiring or retention, by entities covered by Title VII, including private employers as well as federal, state, and local governments.

18Applicant Insight Inc.-Confidential 2013

E-RaceThis new guidance is part of the EEOC’s E-Race (Eradicating Racism and Colorism in Employment) Initiative which addresses the “21st century manifestations of discrimination” under Title VII of the Civil Rights Act of 1964.

In 2011 alone, 50,060 charges of discrimination alleging race/color/national origin-based discrimination were filed with the EEOC, which accounted for 50% of the charges filed that year.

http://www.eeoc.gov/eeoc/statistics/enforcement/charges.cfm

• Disparate Impact & Discrimination Concerns“Arrests and incarceration rates are particularly high for African American and Hispanic men. African Americans and Hispanics are arrested at a rate that is 2 to 3 times their proportion of the general population. Assuming that current incarceration rates remain unchanged, about 1 in 17 White men are expected to serve time in prison during their lifetime; by contrast, this rate climbs to 1 in 6 for Hispanic men; and to 1 in 3 for African American men.”

EEOC: E-Race

19Applicant Insight Inc.-Confidential 2013

EEOC: The Guidance

Ban the Box As a best practice, the EEOC recommends employers not ask about convictions on applications. If made, they should be job-related.

Arrest Records The fact of an arrest does not establish that criminal conduct has occurred, and an exclusion based on an arrest, in itself, is not job related and consistent with business necessity. However, an employer may make an employment decision based on the conduct underlying an arrest if the conduct makes the individual unfit for the position.

Pending Cases The Guidance does not contemplate the difference between arrest records and pending cases.

20Applicant Insight Inc.-Confidential 2013

Criminal Histories The new Guidance takes a deeper dive into the factors originally set forth in the EEOC Policy Statement on the Issue of Conviction Records Under Title VII and adds some additional elements to be considered.

Individualized Assessment The EEOC recommends that an “individualized assessment” could help employers avoid Title VII liability.

− Further, as stated by Commissioner Lipnic in her opening remarks at The Hearing, “when particular criminal history will be so manifestly relevant to the position in question that an employer can lawfully screen out an applicant without further inquiry…”

EEOC: The Guidance

21Applicant Insight Inc.-Confidential 2013

Three Point Consideration

The nature and gravity of the offense or offenses Evaluating the harm caused, the legal elements of the crime, and the classification, i.e., misdemeanor or felony.

The time that has passed since the conviction and/or completion of the sentence Looking at particular facts and circumstances and evaluating studies of recidivism.

The nature of the job held or sought Requires more than examining just the job title, but also specific duties, essential functions, and environment.

22Applicant Insight Inc.-Confidential 2013

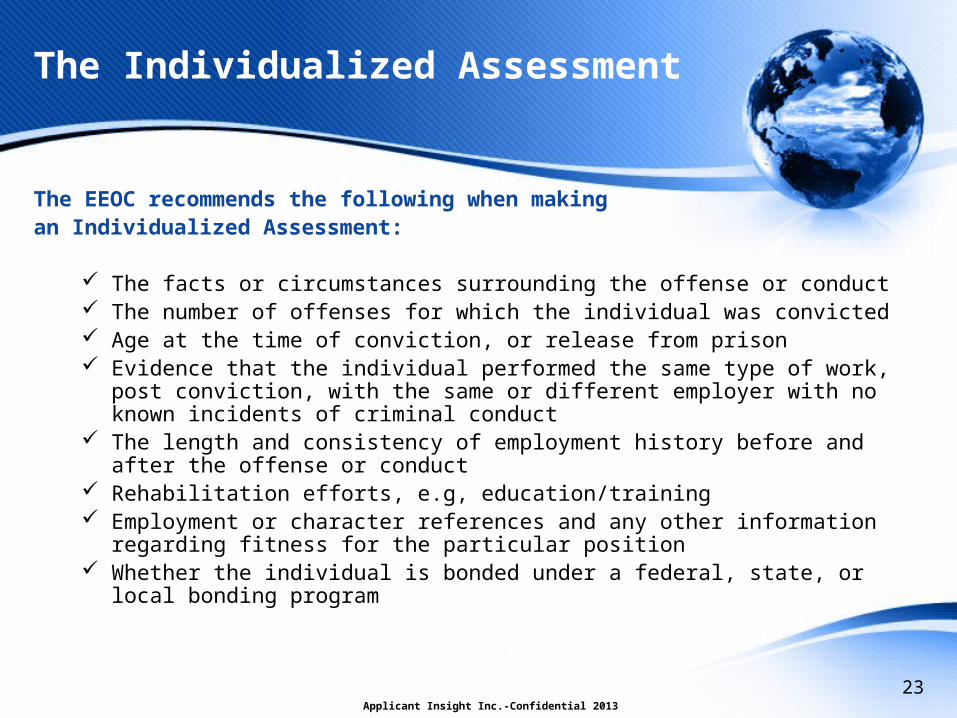

The EEOC recommends the following when making an Individualized Assessment:

The facts or circumstances surrounding the offense or conduct The number of offenses for which the individual was convicted Age at the time of conviction, or release from prison Evidence that the individual performed the same type of work, post conviction, with

the same or different employer with no known incidents of criminal conduct The length and consistency of employment history before and after the offense or

conduct Rehabilitation efforts, e.g, education/training Employment or character references and any other information regarding fitness for

the particular position Whether the individual is bonded under a federal, state, or local bonding program

The Individualized Assessment

23Applicant Insight Inc.-Confidential 2013

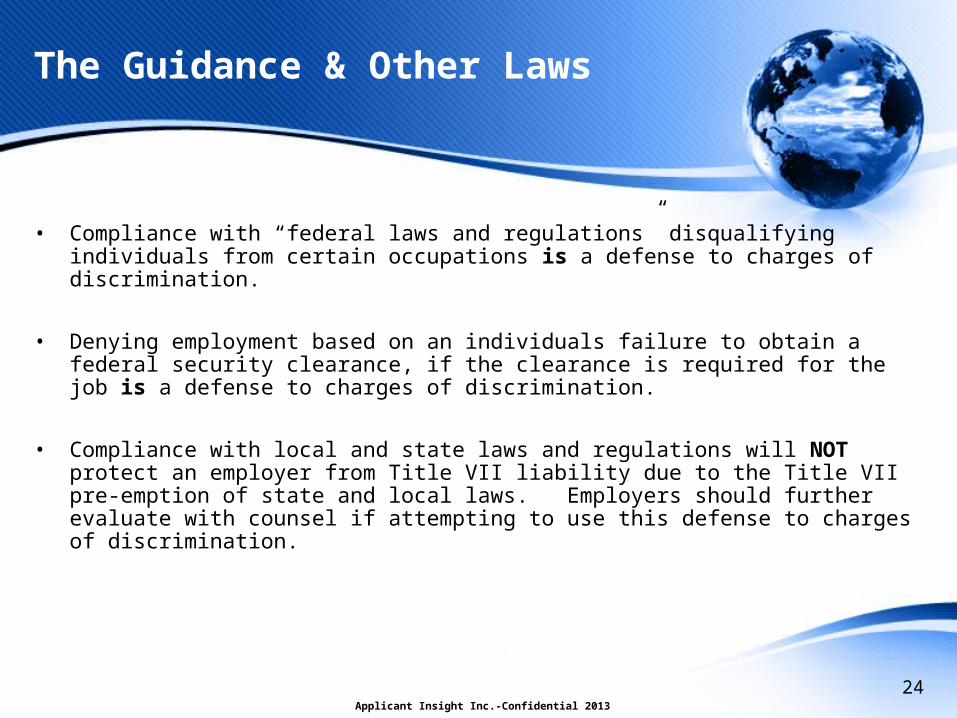

The Guidance & Other Laws

• Compliance with “federal laws and regulations” disqualifying individuals from certain occupations is a defense to charges of discrimination.

• Denying employment based on an individuals failure to obtain a federal security clearance, if the clearance is required for the job is a defense to charges of discrimination.

• Compliance with local and state laws and regulations will NOT protect an employer from Title VII liability due to the Title VII pre-emption of state and local laws. Employers should further evaluate with counsel if attempting to use this defense to charges of discrimination.

24Applicant Insight Inc.-Confidential 2013

Non-Legal Opinions

• End-Users should develop a narrowly tailored policy and conduct a thorough review of their practices relative to the use of criminal records in hiring and/or retention

• End-Users should evaluate their application packages and relationships with CRA’s to ensure compliance with The Guidance

• End-Users should provide formal training to personnel using criminal records specific to the job relatedness and individualized assessment components of The Guidance

• Systems Integrators should evaluate their integrations and raise a red flag to any “blanket” disqualifications (“fail”) currently being utilized between End-Users and CRA’s.

25Applicant Insight Inc.-Confidential 2013

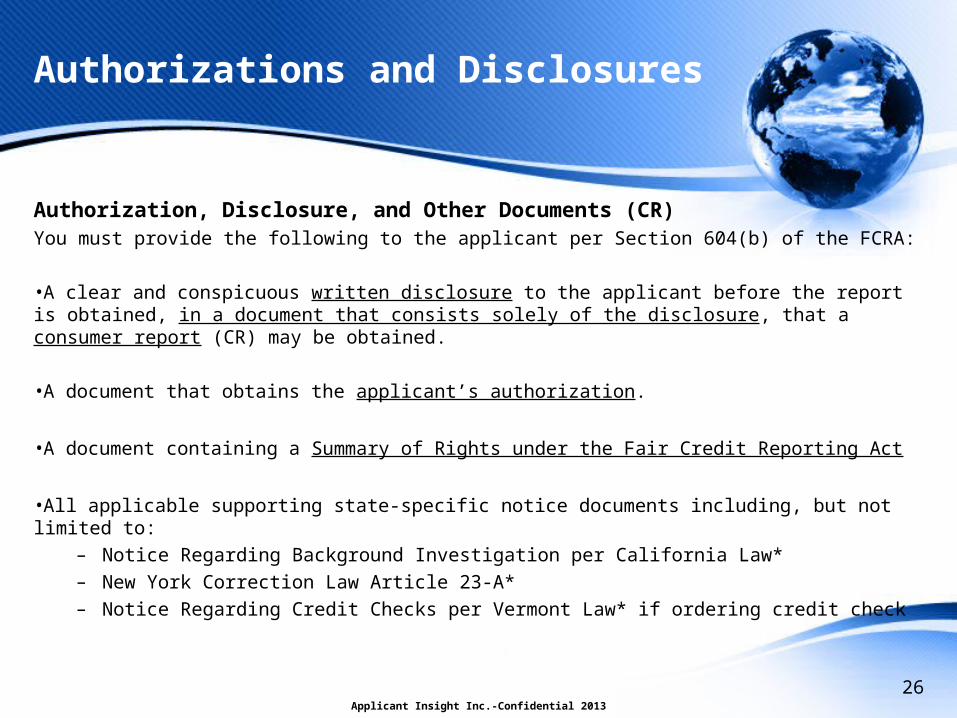

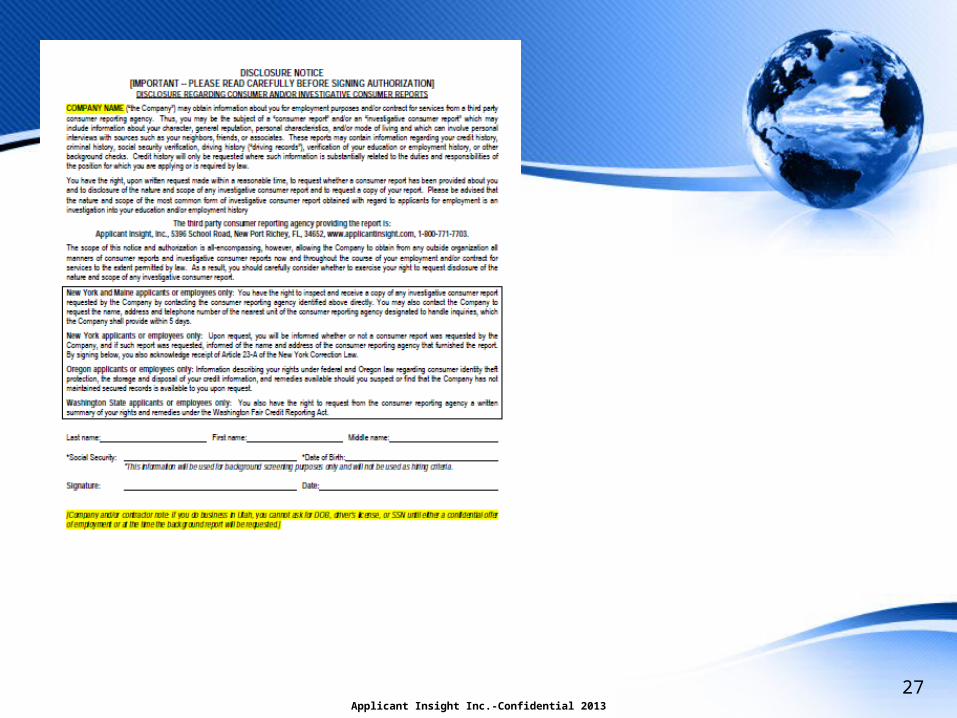

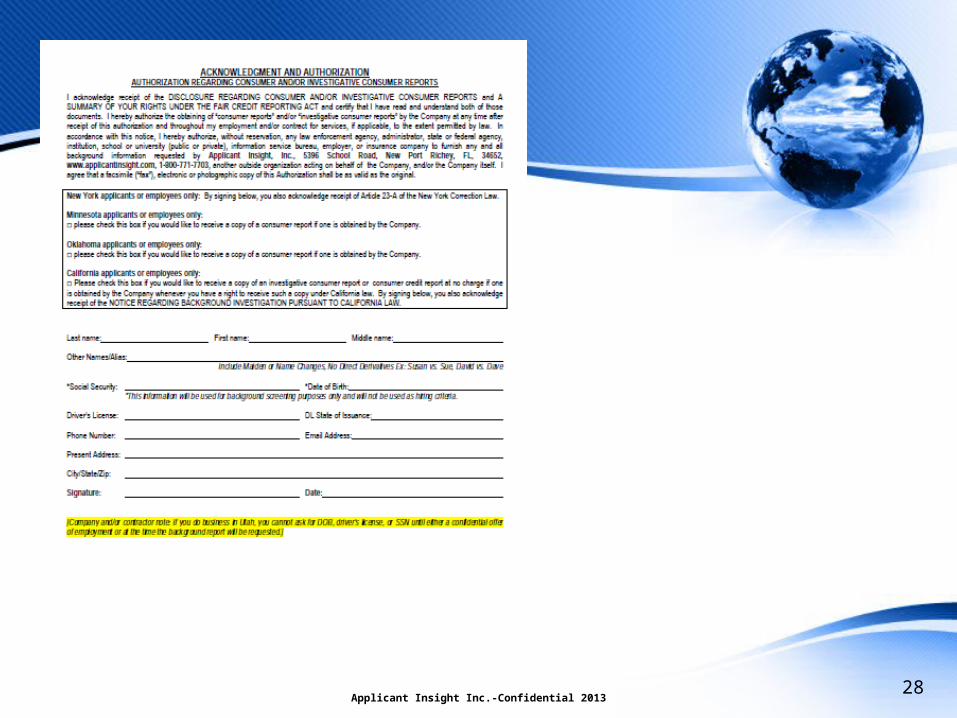

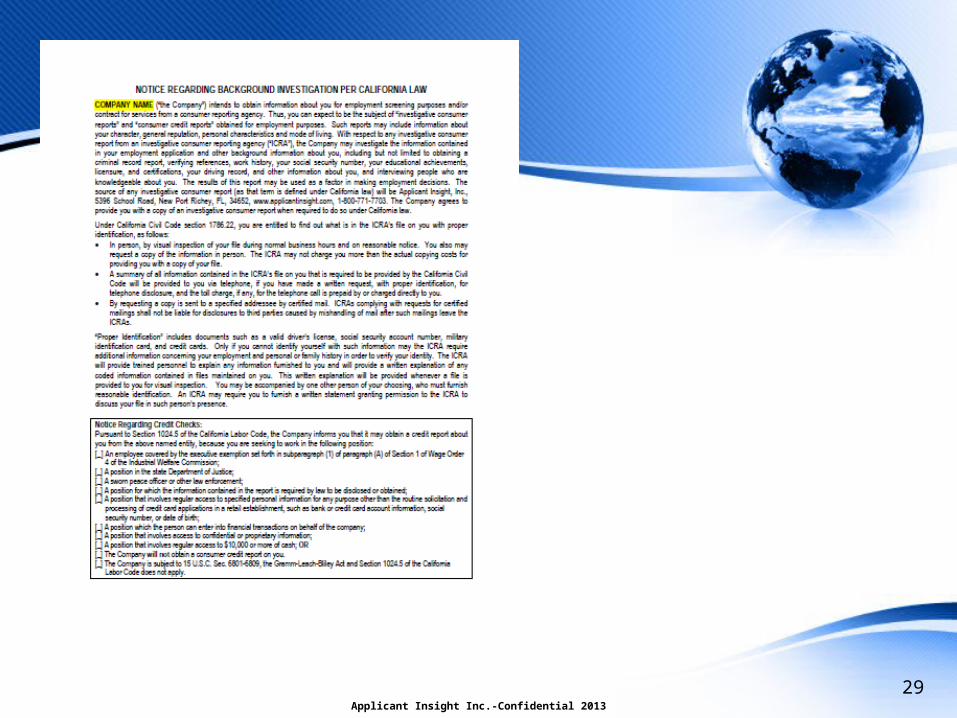

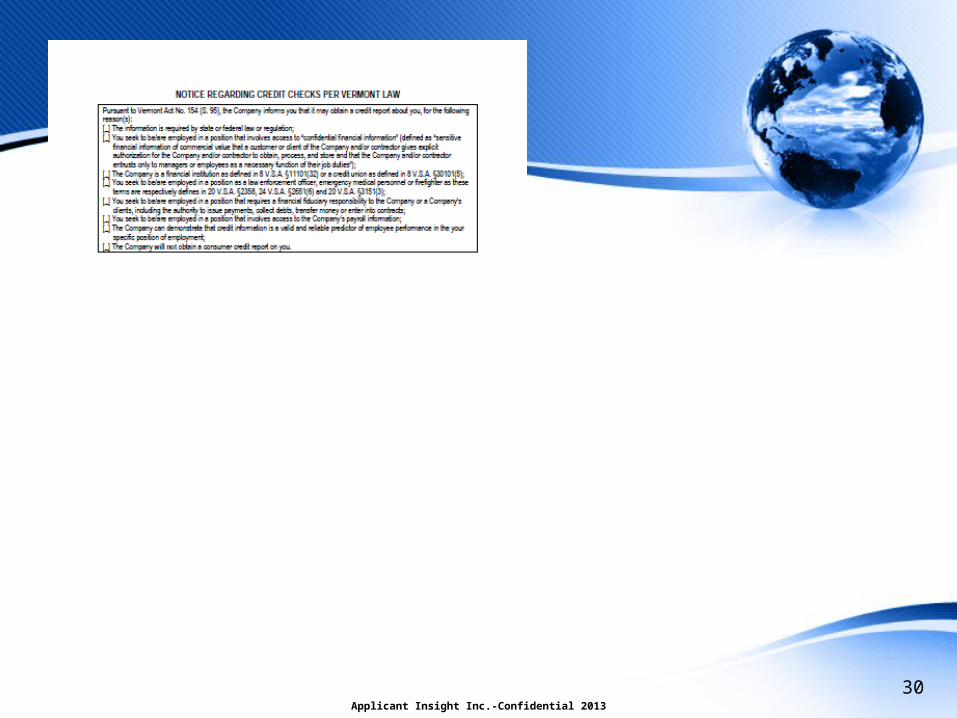

Authorizations and Disclosures

Authorization, Disclosure, and Other Documents (CR)You must provide the following to the applicant per Section 604(b) of the FCRA:

•A clear and conspicuous written disclosure to the applicant before the report is obtained, in a document that consists solely of the disclosure, that a consumer report (CR) may be obtained.

•A document that obtains the applicant’s authorization.

•A document containing a Summary of Rights under the Fair Credit Reporting Act

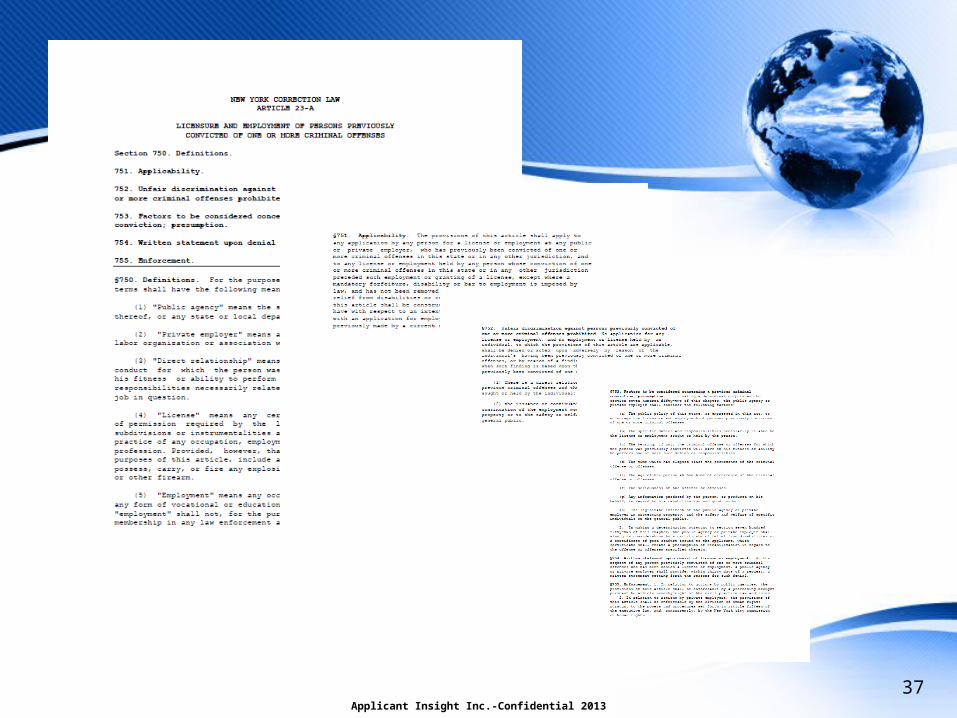

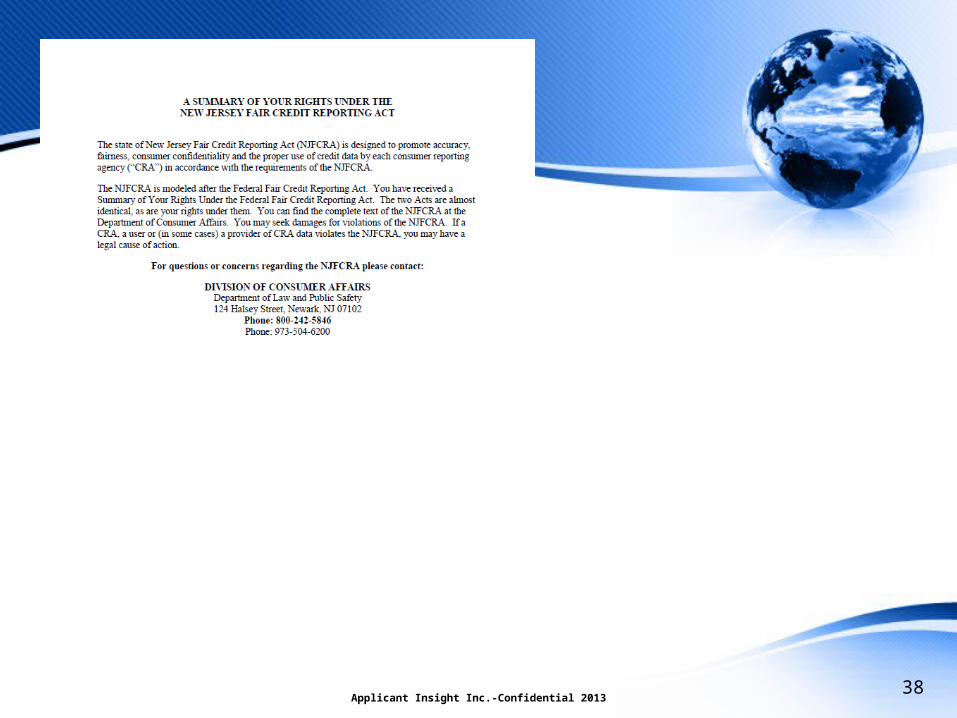

•All applicable supporting state-specific notice documents including, but not limited to:– Notice Regarding Background Investigation per California Law* – New York Correction Law Article 23-A* – Notice Regarding Credit Checks per Vermont Law* if ordering credit check

26Applicant Insight Inc.-Confidential 2013

Applicant Insight Inc.-Confidential 2013

27

Applicant Insight Inc.-Confidential 201328

Applicant Insight Inc.-Confidential 2013

29

Applicant Insight Inc.-Confidential 2013

30

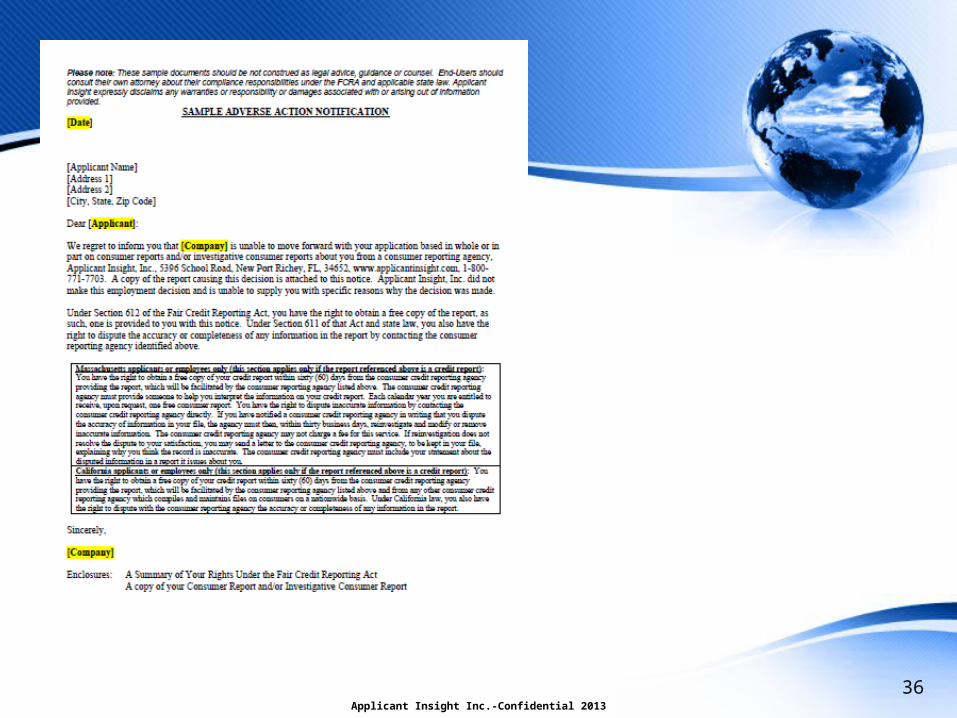

You Must Notify Consumers When Adverse Actions Are Taken

The term "adverse action" is defined very broadly by Section 603. "Adverse actions" include all employment actions affecting consumers that can be considered to have a negative impact as defined by Section 603(k) of the FCRA – such as denying employment or promotion.

If you take any type of adverse action as defined by the FCRA that is based in whole or in part on information contained in a consumer report provided by a CRA Section 615(a) requires the user to notify the consumer.

Under the FCRA, no adverse actions can be taken by an employer against an applicant or employee until the pre-adverse process and dispute notification time period has passed.

31Applicant Insight Inc.-Confidential 2013

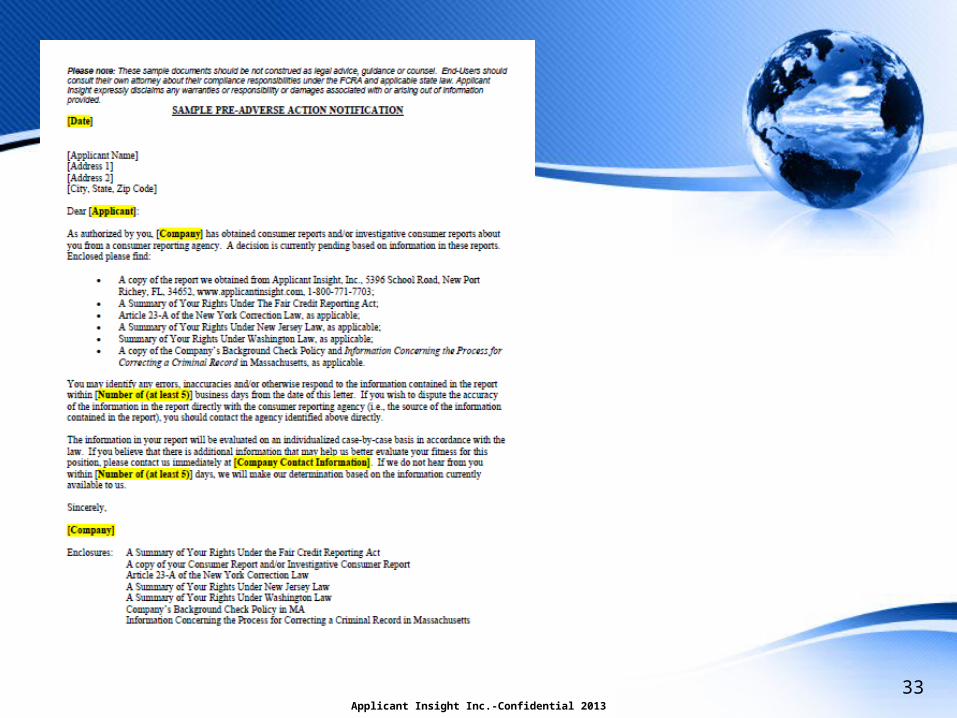

Adverse Action Requirements

Pursuant to section 604(b)(3) of the FCRA, before taking an adverse action, you must send or initiate a Pre-Adverse Action Notice to the applicant including:

•A pre-adverse action notice letter including CRA contact information and website •A statement that CRA is not involved in making the potential adverse decision and is not able to explain why the decision was made•An opportunity to engage the Consumer in the EEOC’s recommended “Individualized Assessment”•A statement setting forth the applicant’s right to dispute directly with CRA the accuracy or completeness of any information provided by CRA•A copy of the report •A copy of the applicant’s Summary of Rights under the Fair Credit Reporting Act•All applicable supporting state-specific notice documents including, but not limited to:

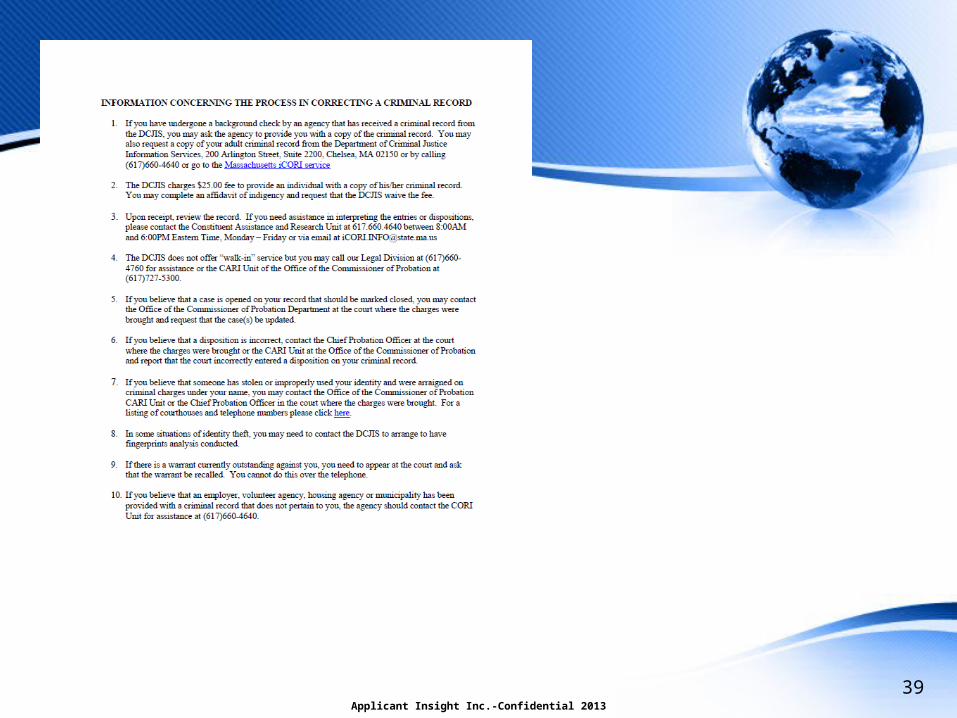

– Notice Regarding Background Investigation per California Law* – Notice Regarding Credit Checks per Vermont Law* if ordering credit check – New York Correction Law Article 23-A* - only if there is a NY criminal record – A Summary of Your Rights Under New Jersey Law* – Your Background Check Policy for MA* - only necessary if there is a criminal record in MA

• Information concerning the Process for Correcting A Criminal Record in MA 32

Applicant Insight Inc.-Confidential 2013

Pre-Adverse Action

Applicant Insight Inc.-Confidential 2013

33

Pre-Adverse Action: Dispute

Re-Investigation Under Pre-Adverse Action

As part of Pre-Adverse Action, the applicant has the right to dispute directly with CRA the accuracy of any information contained in the Consumer Report (CR) or Investigative Consumer Report (ICR) pursuant to section 611(a)(1)(A) of the FCRA.

•The dispute and reinvestigation process is contingent upon a consumer contacting CRA directly within a “reasonable” period time (undefined, but commonly interpreted as 5-10 business days). Generally, the re-investigation must be resolved within 30 days of notification, with 1 minor exception regarding an extension allowance for applicant-provided information. The most common resolutions are (1) verification of original results, (2) an edit or correction of the original result, and (3) removal of the item altogether if unverifiable. The re-investigation is conducted free of charge, and upon resolution, multiple notification requirements must be satisfied by CRA pursuant to the FCRA. Based on the results of the re-investigation, the employer must make the decision to proceed with the hiring process or to initiate final Adverse Action.

•If the applicant does not file a dispute in response to the Pre-Adverse Notice within a “reasonable” period time (see above), Adverse Action can be initiated and the proper notices can be sent.

Applicant Insight Inc.-Confidential 2013

34

35Applicant Insight Inc.-Confidential 2013

A Section 615(a) Adverse Action Notice should be sent only after the pre-adverse action is taken and after allowing “a reasonable opportunity to dispute with the CRA any information on which the employer relied” (interpreted as 5-10 business days). The notification must be done in writing and must include the following:

•An adverse action notice letter including CRA contact information and website •A statement that CRA did not make the adverse decision and is not able to explain why the decision was made•A statement setting forth the applicant’s right to obtain a free disclosure of the applicant/consumer's file from CRA if the applicant makes a request within 60 days •A copy of the report •A copy of the applicant’s Summary of Rights under the Fair Credit Reporting Act•All applicable supporting state-specific notice documents including but not limited to:

• Notice Regarding Background Investigation per California Law* • Notice Regarding Credit Checks per Vermont Law* if ordering credit check • New York Correction Law Article 23-A* - only if there is a NY criminal record • A Summary of Your Rights Under New Jersey Law* • Your Background Check Policy for MA* - only necessary if there is a criminal record in MA

• Information concerning the Process for Correcting A Criminal Record in MA

Adverse Action

Applicant Insight Inc.-Confidential 2013

36

Applicant Insight Inc.-Confidential 2013

37

Applicant Insight Inc.-Confidential 201338

Applicant Insight Inc.-Confidential 2013

39

Additional documents to provide upon applicant request:

• Remedying the Effects of Identity Theft

• A Summary of Rights Under Oregon Law*

• A Summary of Your Rights Under Washington Law*

* Please note the laws and regulations in some states are unclear pertaining to whether or not the applicant resides in the state, the company is headquartered in the state, or if the company is conducting business within the state. The suggested best practice is to provide all documents above to all applicants, each time. This should be your company’s individual determination. If you decide to provide or have your CRA provide forms on only certain occasions (when a resident of a particular state, etc.), guidelines will have to be established to set the ground rules for this process and we recommend you consult your Legal Counsel for further guidance.

40

Applicant Insight Inc.-Confidential 2013

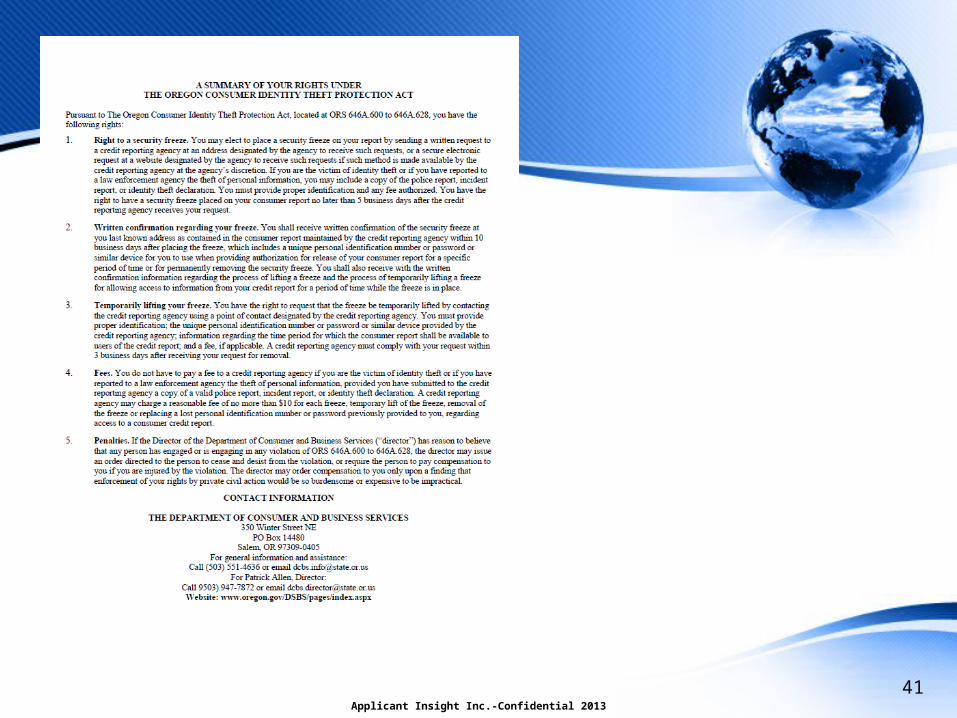

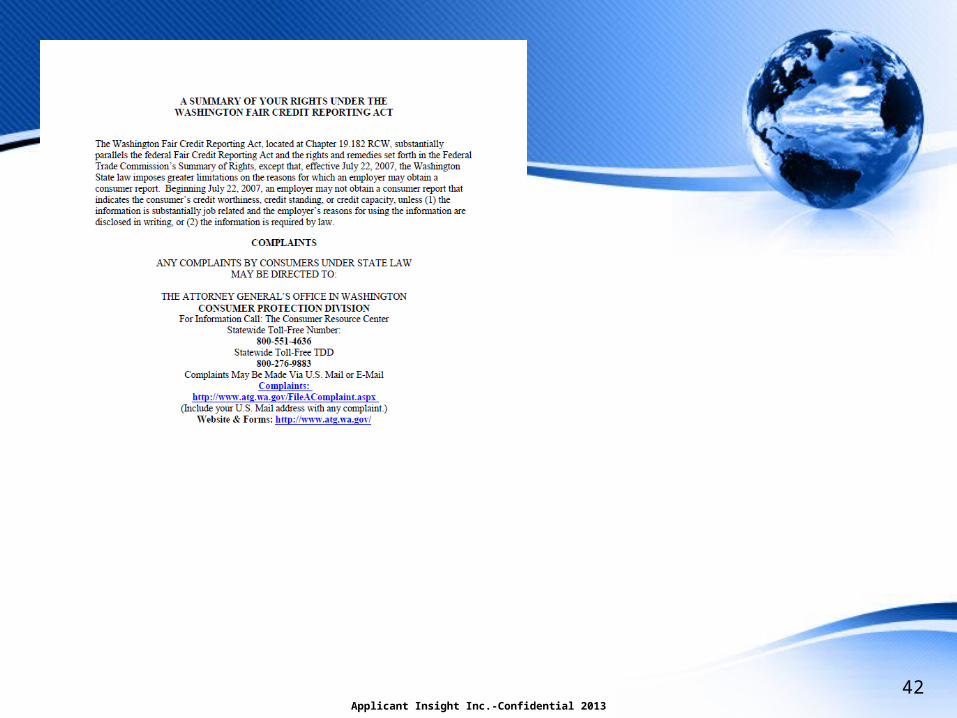

Adverse Action: Other

Applicant Insight Inc.-Confidential 2013

41

Applicant Insight Inc.-Confidential 2013

42

Restrictions on the Use of Credit Reports

Current Restrictions•In the last few years, 8 states have passed laws which, subject to few exceptions, regulate and/or ban employers' ability to use credit information in making employment decisions. The states are:

o CA, CT, HI, IL, MD, OR, VT, WA

•Colorado becomes the ninth after signing the “Employment Opportunity Act,” Colo. Rev. St 8-2-126, which goes into effect on July 1, 2013.

•Nevada will become the tenth after signing SB 127, an amendment to Chapter 613: Employment Practices of the Nevada Revised Statutes. This law goes into effect on October 1, 2013

•Additionally, 13 states are currently considering legislation that would limit the use of credit reports when making employment decisions. Those states are:

o FL, GA, IN, KY, MI, MO, MT, NE, NJ, NM, OH, PA, TX

•There are also 2 additional states that have recommended guidance on record:o LA, MN

•That leaves only 25 states and the District of Columbia without active or pending credit report use legislation or guidance 43

Applicant Insight Inc.-Confidential

This informational webinar has been provided to members of the Securities & Insurance Licensing Association.

This document remains the property of Applicant Insight, Inc. and is provided for reference and the convenience of SILA

Members and should be treated confidentially.

Applicant Insight Inc.-Confidential 201344

Bon Idziak (800) 771.7703

Thank you for Attending!

45Applicant Insight Inc.-Confidential 2013