263

AUSTON G. JOHNSON, CPA UTAH STATE AUDITOR SINGLE AUDIT REPORT FISCAL YEAR ENDED JUNE 30, 2007 Keeping Utah Financially Strong STATE OF UTAH Report No. 07-45

AUSTON G. JOHNSON, CPAUTAH STATE AUDITOR

SINGLE AUDIT REPORT

FISCAL YEAR ENDED JUNE 30, 2007

Keeping UtahFinancially Strong

STATE OF UTAH

Report No. 07-45

OMB Circular A-133 Audit For the Year Ended June 30, 2007

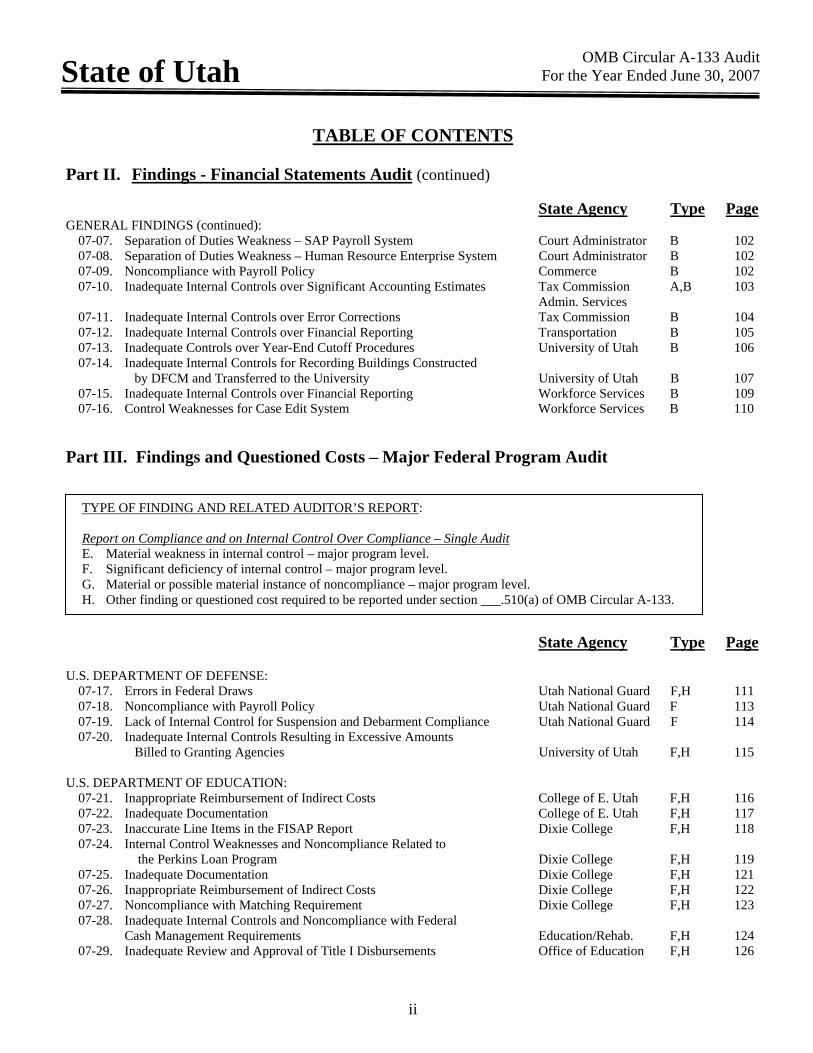

TABLE OF CONTENTS

i

State of Utah

Page INTRODUCTION 1 INDEPENDENT STATE AUDITOR’S REPORT ON INTERNAL CONTROL OVER FINANCIAL REPORTING AND ON COMPLIANCE AND OTHER MATTERS BASED ON AN AUDIT OF FINANCIAL STATEMENTS PERFORMED IN ACCORDANCE WITH GOVERNMENT AUDITING STANDARDS 3 INDEPENDENT STATE AUDITOR’S REPORT IN ACCORDANCE WITH OMB CIRCULAR A-133 ON • COMPLIANCE WITH REQUIREMENTS APPLICABLE TO EACH MAJOR PROGRAM • INTERNAL CONTROL OVER COMPLIANCE • SUPPLEMENTARY SCHEDULE OF EXPENDITURES OF FEDERAL AWARDS 6 SCHEDULE OF EXPENDITURES OF FEDERAL AWARDS Presented by Federal Agency 9 Presented by State Agency 47 NOTES TO THE SCHEDULE OF EXPENDITURES OF FEDERAL AWARDS 86 SCHEDULE OF FINDINGS AND QUESTIONED COSTS: Part I. Summary of Auditor’s Results 96 Part II. Findings - Financial Statements Audit

State Agency Type Page U.S. DEPARTMENT OF HEALTH AND HUMAN SERVICES: 07-01. Incorrect Eligibility Determination and Inadequate Documentation Health A,B,D 98 of Eligibility Workforce Services 07-02. Child Care Internal Control Weaknesses and Noncompliance Workforce Services B,D 98 GENERAL FINDINGS: 07-03. Inadequate Internal Controls over Financial Reporting Admin. Services A,B 99 07-04. FINET Transactions Processed Without Required Approvals Admin. Services B 100 07-05. Inadequate Controls over Statewide Payroll Expenditures Admin. Services B 100 07-06. Inadequate Controls over Capital Asset Additions Admin. Services B 100

TYPE OF FINDING AND RELATED AUDITOR’S REPORT: Report on Compliance and on Internal Control Over Financial Reporting – Government Auditing Standards A. Material Weakness in internal control – basic financial statement level. B. Significant Deficiency of internal control – basic financial statement level. C. Material Noncompliance – basic financial statement level. D. Reportable instance of noncompliance and other matters – fraud or illegal act unless clearly inconsequential,

or significant violations of provisions of contracts or grant agreements and abuse.

OMB Circular A-133 Audit For the Year Ended June 30, 2007

TABLE OF CONTENTS

ii

State of Utah

Part II. Findings - Financial Statements Audit (continued) State Agency Type Page GENERAL FINDINGS (continued): 07-07. Separation of Duties Weakness – SAP Payroll System Court Administrator B 102 07-08. Separation of Duties Weakness – Human Resource Enterprise System Court Administrator B 102 07-09. Noncompliance with Payroll Policy Commerce B 102 07-10. Inadequate Internal Controls over Significant Accounting Estimates Tax Commission A,B 103 Admin. Services 07-11. Inadequate Internal Controls over Error Corrections Tax Commission B 104 07-12. Inadequate Internal Controls over Financial Reporting Transportation B 105 07-13. Inadequate Controls over Year-End Cutoff Procedures University of Utah B 106 07-14. Inadequate Internal Controls for Recording Buildings Constructed by DFCM and Transferred to the University University of Utah B 107 07-15. Inadequate Internal Controls over Financial Reporting Workforce Services B 109 07-16. Control Weaknesses for Case Edit System Workforce Services B 110 Part III. Findings and Questioned Costs – Major Federal Program Audit

State Agency Type Page U.S. DEPARTMENT OF DEFENSE: 07-17. Errors in Federal Draws Utah National Guard F,H 111 07-18. Noncompliance with Payroll Policy Utah National Guard F 113 07-19. Lack of Internal Control for Suspension and Debarment Compliance Utah National Guard F 114 07-20. Inadequate Internal Controls Resulting in Excessive Amounts Billed to Granting Agencies University of Utah F,H 115 U.S. DEPARTMENT OF EDUCATION: 07-21. Inappropriate Reimbursement of Indirect Costs College of E. Utah F,H 116 07-22. Inadequate Documentation College of E. Utah F,H 117 07-23. Inaccurate Line Items in the FISAP Report Dixie College F,H 118 07-24. Internal Control Weaknesses and Noncompliance Related to the Perkins Loan Program Dixie College F,H 119 07-25. Inadequate Documentation Dixie College F,H 121 07-26. Inappropriate Reimbursement of Indirect Costs Dixie College F,H 122 07-27. Noncompliance with Matching Requirement Dixie College F,H 123 07-28. Inadequate Internal Controls and Noncompliance with Federal Cash Management Requirements Education/Rehab. F,H 124 07-29. Inadequate Review and Approval of Title I Disbursements Office of Education F,H 126

TYPE OF FINDING AND RELATED AUDITOR’S REPORT: Report on Compliance and on Internal Control Over Compliance – Single Audit E. Material weakness in internal control – major program level. F. Significant deficiency of internal control – major program level. G. Material or possible material instance of noncompliance – major program level. H. Other finding or questioned cost required to be reported under section ___.510(a) of OMB Circular A-133.

OMB Circular A-133 Audit For the Year Ended June 30, 2007

TABLE OF CONTENTS

iii

State of Utah

Part III. Findings and Questioned Costs – Major Federal Program Audit (continued) State Agency Type Page U.S. DEPARTMENT OF EDUCATION (continued): 07-30. Errors in Federal Financial Reports Office of Education F,H 128 07-31. Inadequate Internal Controls over Indirect Cost Rate Proposal Office of Education F,H 129 07-32. Noncompliance with Davis-Bacon Act Off. of Rehabilitation F,H 130 07-33. Inadequate Controls and Noncompliance with Return of Title IV Funds SL Comm. College F,H 131 07-34. Inadequate Controls for Student Status Changes Reports SL Comm. College F,H 133 07-35. Internal Control Weaknesses and Noncompliance Related to the Perkins Loan Program SL Comm. College F,H 134 07-36. Reporting Errors SL Comm. College F,H 136 07-37. Inappropriate Reimbursement of Indirect Costs Snow College F,H 138 07-38. Inappropriate Reimbursement of Indirect Costs Southern Utah Univ. F,H 139 07-39. Noncompliance with Cash Management Requirements and Payment of Unsupported Expenditure Uintah Basin ATC F,H 140 07-40. Inadequate Separation of Duties Uintah Basin ATC F 141 07-41. Noncompliance with Purchasing Policy Uintah Basin ATC F,H 142 07-42. Missing Certification of Effort for Employees Paid from Federal Funds Uintah Basin ATC F,H 143 07-43. Inadequate Documentation University of Utah F,H 144 07-44. Inadequate Internal Controls Related to Perkins Loans Repayments Utah State University F,H 145 07-45. Internal Control Weaknesses and Noncompliance Related to Perkins Loans Repayments Ut. Valley St. College F,H 146 07-46. Inadequate Documentation Ut. Valley St. College F,H 147 07-47. Inadequate Controls and Noncompliance with Return of Title IV Funds Weber State Univ. F,H 149 07-48. Inadequate Documentation of Loan Disbursement Notifications Weber State Univ. F,H 150 07-49. Reporting Errors Weber State Univ. F,H 151 U.S. DEPARTMENT OF HEALTH AND HUMAN SERVICES: 07-50. Noncompliance with Subgrantee Eligibility Requirements Community & Culture E,F,G,H 155 07-51. Potential Unallowable Political Activities in Subgrantee Contracts Community & Culture F,H 157 07-52. Weaknesses in During-the-Award Monitoring of LIHEAP Subrecipients Community & Culture F,H 160

07-53. LIHEAP Eligibility Determination and Assistance Amount Calculation Errors Community & Culture F,H 161

07-54. Incorrect Eligibility Determination and Inadequate Documentation Health E,F,G,H 163 of Eligibility Workforce Services 07-55. Third Party Liability Information Not Adequately Obtained or Updated Health F,H 167 Workforce Services 07-56. Managed Care Noncompliance Health F,H 170 07-57. Noncompliance with the Medicaid State Plan for Graduate Medical Education Payments Health F,H 172 07-58. Inadequate Claim Review Health F,H 174 07-59. Internal Control Weakness and Inadequate Documentation Health E,F,H 175 Workforce Services 07-60. Internal Control Weaknesses and Noncompliance – Title IV-E Foster Care Human Services F,H 178 07-61. Internal Control Weaknesses and Allegations of Fraud Human Services F,H 181 07-62. Unallowable Expenditures – Title IV-E Foster Care and Adoption Assistance Human Services F,H 182 07-63. Inadequate Internal Controls Resulting in Excessive Amounts Billed to Granting Agencies University of Utah F,H 183

OMB Circular A-133 Audit For the Year Ended June 30, 2007

TABLE OF CONTENTS

iv

State of Utah

Part III. Findings and Questioned Costs – Major Federal Program Audit (continued) State Agency Type Page U.S. DEPARTMENT OF HEALTH AND HUMAN SERVICES (continued): 07-64. Child Care Internal Control Weaknesses and Noncompliance Workforce Services E,F,G,H 185 07-65. TANF Internal Control Weaknesses and Noncompliance Workforce Services E,F,H 190 07-66. Inadequate Controls Over Advances to Subrecipients Workforce Services F,H 193 07-67. Noncompliance with Reporting Requirements Workforce Services F,H 194 U.S. DEPARTMENT OF HOMELAND SECURITY: 07-68. Lack of Supervisor Signature on Timesheet Public Safety F 196 07-69. Inadequate Subrecipient Monitoring Procedures Public Safety F,H 197 U.S. DEPARTMENT OF LABOR: 07-70. WIA Internal Control Weaknesses and Noncompliance Workforce Services E,F,H 199 DEPT. OF TRANSPORTATION: 07-71. Untimely Weekly Certified Payrolls Transportation F,H 207 07-72. Inadequate Subrecipient Monitoring Procedures Transportation F,H 208 GENERAL FINDINGS: 07-73. FINET Transactions Processed Without Required Approvals Admin. Services F 210 07-74. Inadequate Controls over Statewide Payroll Expenditures Admin. Services F 211 07-75. Separation of Duties Weakness – SAP Payroll System Court Administrator F 212 07-76. Separation of Duties Weakness – Human Resource Enterprise System Court Administrator F 213 07-77. Noncompliance with Payroll Policy Commerce F 214 07-78. Reserves in Excess of Federal Guidelines Technology H 215 07-79. Cash Reserves in Excess of Federal Guidelines University of Utah F,H 216 07-80. Untimely Subrecipient Monitoring University of Utah F,H 217 07-81. Inadequate Internal Controls Related to Research and Development Grants Utah State University F,H 218 07-82. Inadequate Controls Over Federal Payroll Compliance Utah State University F,H 220 07-83. Control Weaknesses for Case Edit System Workforce Services E,F 222 SUMMARY SCHEDULE OF PRIOR AUDIT FINDINGS 229

OMB Circular A-133 Audit For the Year Ended June 30, 2007

INTRODUCTION

1

State of Utah

Background The Federal Government requires the State of Utah to have an entity-wide audit of its financial statements and its federal programs as a condition of receiving federal financial assistance. The federally required audit is commonly referred to as the “single audit.” The single audit focuses on testing compliance with laws and regulations and testing related internal control for major programs. The requirements for performing the single audit are stated in the U.S. Office of Management and Budget (OMB) Circular A-133, Audits of States, Local Governments, and Non-Profit Organizations. Scope OMB Circular A-133 requires a risk-based approach to auditing federal programs. Under the risk-based approach, programs are classified as Type A or Type B programs based on a dollar level computed in accordance with Circular A-133. Type A programs for the State are those programs which exceeded $9,300,000 in federal awards expended for the fiscal year ended June 30, 2007. All other programs are classified as Type B. For the year ended June 30, 2007, all “non-low risk” Type A and at least one-half of the “high risk” Type B programs were audited as major programs in accordance with OMB Circular A-133 requirements. Presentation This report includes all required information for the single audit except the State of Utah’s financial statements and our report thereon, which were issued under separate cover. The Schedule of Expenditures of Federal Awards is presented by federal agency as required. An optional Schedule sorted by state agency is also presented. The required summary of our audit results, including a list of the major programs audited is presented on page 96. In addition, management’s corrective action plan is presented with the related finding and questioned cost rather than in a separate section of the report. The type of each finding and the auditor’s report(s) to which it relates is listed in the foregoing Table of Contents. Perspective Federal programs continue to be a significant source of funding for the State. The top graph on the following page shows the relationship of federal award expenditures to total expenditures for State agencies and institutions. The bottom graph on the following page shows the break out of Type A and Type B programs. The State had 37 Type A programs and hundreds of Type B programs in fiscal year 2007.

OMB Circular A-133 Audit For the Year Ended June 30, 2007

INTRODUCTION

2

State of Utah

$433

$2,942

$372

$2,175

$1,217

$399

$118

$506

$280

$577$421

$83 $38 $67$233

$3,687

$0

$500

$1,000

$1,500

$2,000

$2,500

$3,000

$3,500

$4,000

Mill

ions

HIGHERED

USF DOH &DEQ

DHS DOT DWS DCC OTHER

FOR THE FISCAL YEAR ENDED JUNE 30, 2007

FEDERAL vs OTHER FUND EXPENDITURESFOR STATE AGENCIES AND INSTITUTIONS

FEDERAL OTHER

HIGHER ED – Colleges and Universities DOT – Dept. of Transportation USF – Uniform School Fund (Office of Education) DWS – Dept. of Workforce Services DOH & DEQ – Dept. of Health and DCC – Dept. of Community & Culture Dept. of Environmental Quality OTHER – Other state agencies DHS – Dept. of Human Services

TYPE A vs TYPE B PROGRAMS TOTAL FEDERAL ASSISTANCE $5.588 Billion

(includes loan balances & disbursements)

Type B Programs$0.333 Billion

5.95%

Type A Programs$5.255 Billion

94.05%

FOR THE FISCAL YEAR ENDED JUNE 30, 2007

3

Auston G. Johnson, CPA UTAH STATE AUDITOR

STATE OF UTAH

Office of the State Auditor UTAH STATE CAPITOL COMPLEX

EAST OFFICE BUILDING, SUITE E310 P.O. BOX 142310

SALT LAKE CITY, UTAH 84114-2310 (801) 538-1025

FAX (801) 538-1383

DEPUTY STATE AUDITOR: Joe Christensen, CPA FINANCIAL AUDIT DIRECTORS: H. Dean Eborn, CPA Deborah A. Empey, CPA Stan Godfrey, CPA Jon T. Johnson, CPA

INDEPENDENT STATE AUDITOR’S REPORT ON INTERNAL CONTROL OVER FINANCIAL REPORTING AND ON COMPLIANCE AND OTHER MATTERS

BASED ON AN AUDIT OF FINANCIAL STATEMENTS PERFORMED IN ACCORDANCE WITH GOVERNMENT AUDITING STANDARDS

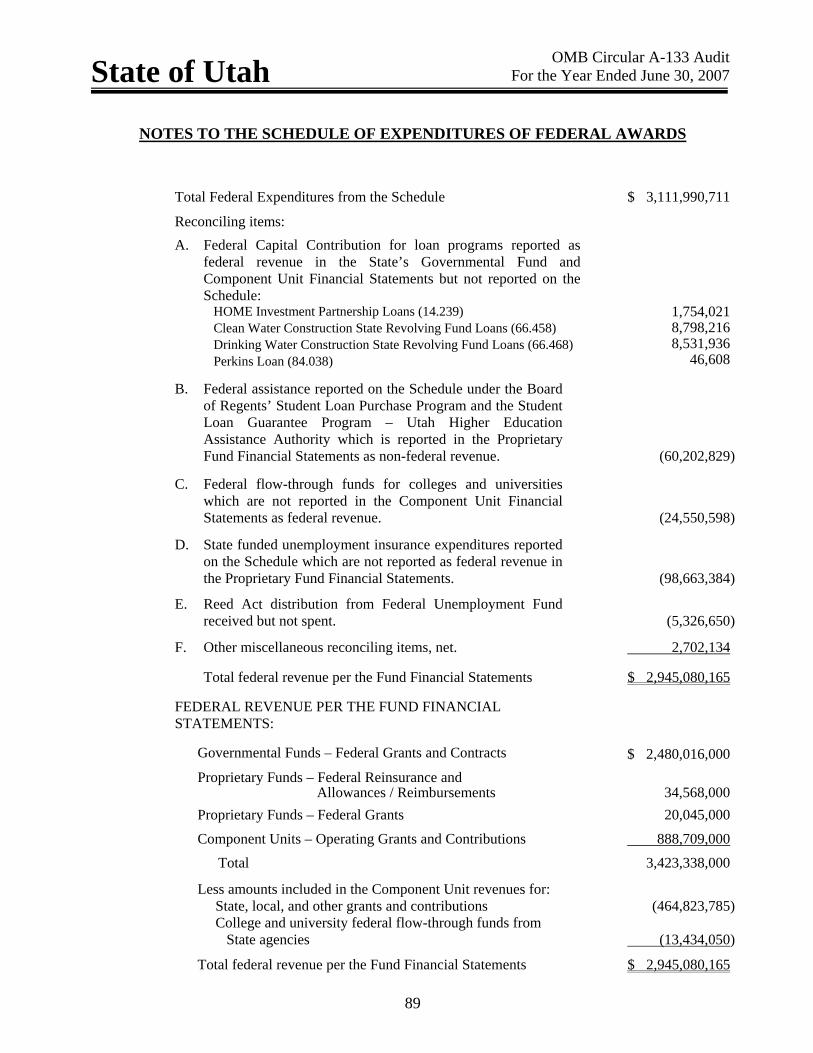

To the Members of the Legislature of the State of Utah and The Honorable Jon Huntsman, Jr. Governor, State of Utah We have audited the financial statements of the governmental activities, the business-type activities, the aggregate discretely presented component units, each major fund, and the aggregate remaining fund information of the State of Utah as of and for the year ended June 30, 2007, which collectively comprise the State’s basic financial statements, and have issued our report thereon dated November 20, 2007. Our report was modified to include a reference to other auditors. We conducted our audit in accordance with auditing standards generally accepted in the United States of America and the standards applicable to financial audits contained in Government Auditing Standards, issued by the Comptroller General of the United States. Other auditors audited the financial statements of Utah Housing Corporation, Utah Public Employees Group Insurance, the University of Utah’s Hospital and component units, the Utah State University Research Foundation, certain other college and university foundations, the Dairy Commission, and the Utah State Retirement Office, as described in our report on Utah’s financial statements. This report includes our consideration of the results of the other auditors’ testing of internal control over financial reporting and compliance and other matters that are reported on separately by those other auditors. However, this report, insofar as it relates to the results of the other auditors, is based solely on the reports of the other auditors. Internal Control Over Financial Reporting In planning and performing our audit, we considered the State of Utah’s internal control over financial reporting as a basis for designing our auditing procedures for the purpose of expressing our opinion on the basic financial statements, but not for the purpose of expressing an opinion on the effectiveness of the State of Utah’s internal control over financial reporting. Accordingly, we do not express an opinion on the effectiveness of the State of Utah’s internal control over financial reporting.

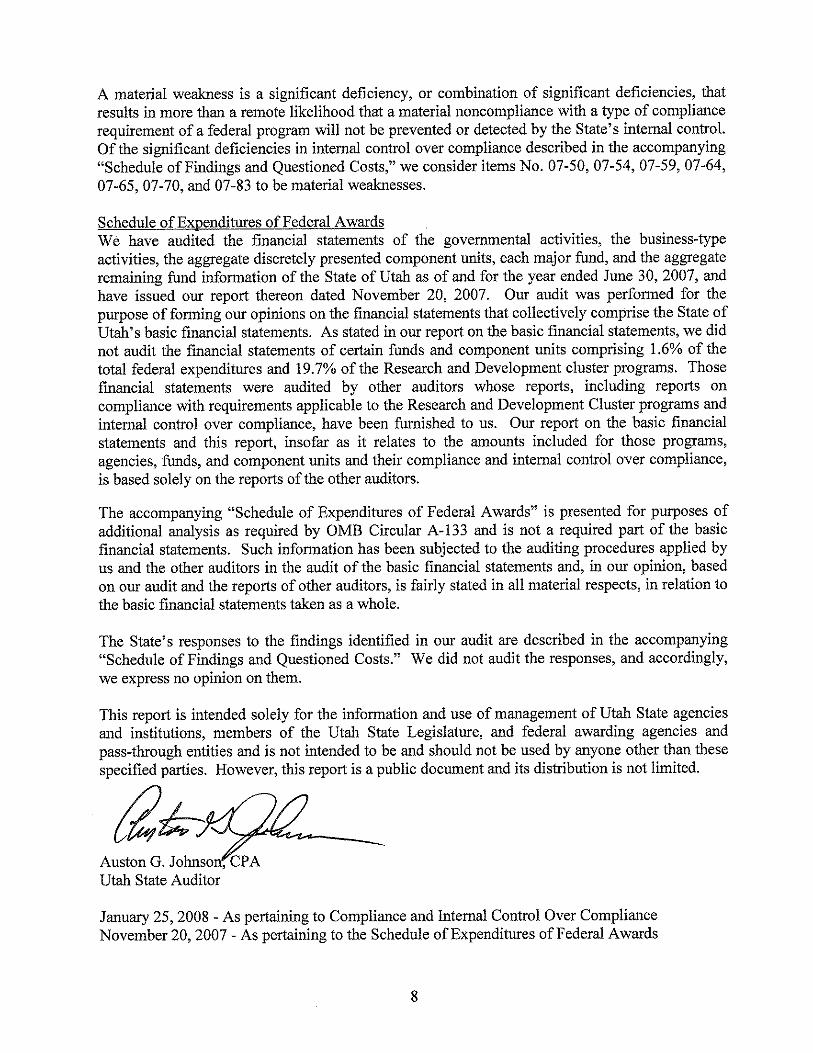

4

Our consideration of the internal control over financial reporting was for the limited purpose described in the preceding paragraph and would not necessarily identify all deficiencies in internal control over financial reporting that might be significant deficiencies or material weaknesses. However, as discussed below, we identified certain deficiencies in internal control over financial reporting that we consider to be significant deficiencies. A control deficiency exists when the design or operation of a control does not allow management or employees, in the normal course of performing their assigned functions, to prevent or detect misstatements on a timely basis. A significant deficiency is a control deficiency, or combination of control deficiencies, that adversely affects the State’s ability to initiate, authorize, record, process, or report financial data reliably in accordance with generally accepted accounting principles such that there is more than a remote likelihood that a misstatement of the basic financial statements that is more than inconsequential will not be prevented or detected by the State’s internal control. We consider the deficiencies described in the accompanying “Schedule of Findings and Questioned Costs” as items No. 07-01 through 07-16 to be significant deficiencies in internal control over financial reporting. A material weakness is a significant deficiency, or combination of significant deficiencies, that results in more than a remote likelihood that a material misstatement of the basic financial statements will not be prevented or detected by the State’s internal control. Our consideration of the internal control over financial reporting was for the limited purpose described in the first paragraph of this section and would not necessarily identify all deficiencies in the internal control that might be significant deficiencies and, accordingly, would not necessarily disclose all significant deficiencies that are also considered to be material weaknesses. However, of the significant deficiencies described above, we consider items No. 07-01, 07-03, and 07-10 to be material weaknesses. Compliance and Other Matters As part of obtaining reasonable assurance about whether the State of Utah’s basic financial statements are free of material misstatement, we performed tests of its compliance with certain provisions of laws, regulations, contracts and grants agreements, noncompliance with which could have a direct and material effect on the determination of financial statement amounts. However, providing an opinion on compliance with those provisions was not an objective of our audit and, accordingly, we do not express such an opinion. The results of our tests disclosed instances of noncompliance or other matters that are required to be reported under Government Auditing Standards and which are described in the accompanying "Schedule of Findings and Questioned Costs" as items No. 07-01 and 07-02. We also noted certain immaterial instances of noncompliance and other matters involving the internal control over financial reporting that we have reported to management of the applicable State agencies and institutions in separate letters. The State’s responses to the findings identified in our audit are described in the accompanying “Schedule of Findings and Questioned Costs.” We did not audit the responses, and accordingly, we express no opinion on them.

6

Auston G. Johnson, CPA UTAH STATE AUDITOR

STATE OF UTAH

Office of the State Auditor UTAH STATE CAPITOL COMPLEX

EAST OFFICE BUILDING, SUITE E310 P.O. BOX 142310

SALT LAKE CITY, UTAH 84114-2310 (801) 538-1025

FAX (801) 538-1383

DEPUTY STATE AUDITOR: Joe Christensen, CPA FINANCIAL AUDIT DIRECTORS: H. Dean Eborn, CPA Deborah A. Empey, CPA Stan Godfrey, CPA Jon T. Johnson, CPA

INDEPENDENT STATE AUDITOR’S REPORT IN ACCORDANCE WITH OMB CIRCULAR A-133 ON • COMPLIANCE WITH REQUIREMENTS APPLICABLE TO EACH MAJOR PROGRAM • INTERNAL CONTROL OVER COMPLIANCE • SUPPLEMENTARY SCHEDULE OF EXPENDITURES OF FEDERAL AWARDS To the Members of the Legislature of the State of Utah and The Honorable Jon Huntsman, Jr. Governor, State of Utah Compliance We have audited the compliance of the State of Utah with the types of compliance requirements described in the U. S. Office of Management and Budget (OMB) Circular A-133 Compliance Supplement that are applicable to each of its major federal programs for the year ended June 30, 2007. The State of Utah’s major federal programs are identified in the “Summary of Auditor’s Results” section of the accompanying “Schedule of Findings and Questioned Costs.” Compliance with the requirements of laws, regulations, contracts and grants applicable to each of its major federal programs is the responsibility of the State of Utah’s management. Our responsibility is to express an opinion on the State of Utah’s compliance based on our audit. We conducted our audit of compliance in accordance with auditing standards generally accepted in the United States of America; the standards applicable to financial audits contained in Government Auditing Standards, issued by the Comptroller General of the United States; and OMB Circular A-133, Audits of States, Local Governments, and Non-Profit Organizations. Those standards and OMB Circular A-133 require that we plan and perform the audit to obtain reasonable assurance about whether noncompliance with the types of compliance requirements referred to above that could have a direct and material effect on a major federal program occurred. An audit includes examining, on a test basis, evidence about the State of Utah’s compliance with those requirements and performing such other procedures as we considered necessary in the circumstances. We believe that our audit provides a reasonable basis for our opinion. Our audit does not provide a legal determination on the State of Utah’s compliance with those requirements. As described in items No. 07-50, 07-54, and 07-64 in the accompanying “Schedule of Findings and Questioned Costs,” the State of Utah did not comply with requirements regarding allowable activities, allowable costs/cost principles, and eligibility that are applicable to the U.S. Department of Health and Human Services’ Community Services Block Grant (93.569), Child

7

Care Development Fund cluster (93.575 and 93.596), and Title XIX Medicaid cluster program (93.778). Compliance with such requirements is necessary, in our opinion, for the State of Utah to comply with requirements applicable to those programs. In our opinion, because of the effects of the noncompliance described in the preceding paragraph, the State of Utah did not comply, in all material respects, with the requirements referred to above that are applicable to the U.S. Department of Health and Human Services’ Community Services Block Grant (93.569), Child Care Development Fund cluster (93.575 and 93.596), and Title XIX Medicaid cluster program (93.778). Also, in our opinion, the State of Utah complied, in all material respects, with the requirements referred to above that are applicable to each of its other major federal programs for the year ended June 30, 2007. The results of our auditing procedures also disclosed other instances of noncompliance with those requirements which are required to be reported in accordance with OMB Circular A-133 and which are identified in the accompanying “Table of Contents” on pages ii and iii of this report and described in the “Schedule of Findings and Questioned Costs” section of this report. Internal Control Over Compliance The management of the State of Utah is responsible for establishing and maintaining effective internal control over compliance with the requirements of laws, regulations, contracts and grants applicable to federal programs. In planning and performing our audit, we considered the State of Utah’s internal control over compliance with the requirements that could have a direct and material effect on a major federal program in order to determine our auditing procedures for the purpose of expressing our opinion on compliance, but not for the purpose of expressing an opinion on the effectiveness of internal control over compliance. Accordingly, we do not express an opinion on the effectiveness of the State of Utah’s internal control over compliance. Our consideration of internal control over compliance was for the limited purpose described in the preceding paragraph and would not necessarily identify all deficiencies in the State’s internal control that might be significant deficiencies or material weaknesses as defined below. However, as discussed below, we identified certain deficiencies in internal control over compliance that we consider to be significant deficiencies and other deficiencies that we consider to be material weaknesses. A control deficiency in the State of Utah’s internal control over compliance exists when the design or operation of a control does not allow management or employees, in the normal course of performing their assigned functions, to prevent or detect noncompliance with a type of compliance requirement of a federal program on a timely basis. A significant deficiency is a control deficiency, or combination of control deficiencies, that adversely affects the State’s ability to administer a federal program such that there is more than a remote likelihood that noncompliance with a type of compliance requirement of a federal program that is more than inconsequential will not be prevented or detected by the State’s internal control. We consider the deficiencies in internal control over compliance described in the accompanying “Schedule of Findings and Questioned Costs” as items No. 07-17 through 07-77 and 07-79 through 07-83 to be significant deficiencies.

9

SCHEDULE OF EXPENDITURES

OF FEDERAL AWARDS

BY FEDERAL AGENCY

Federal Federal Pass-State Agency Catalog# Award/Contract # Expenditures Through

AGENCY FOR INTERNATIONAL DEVELOPMENT

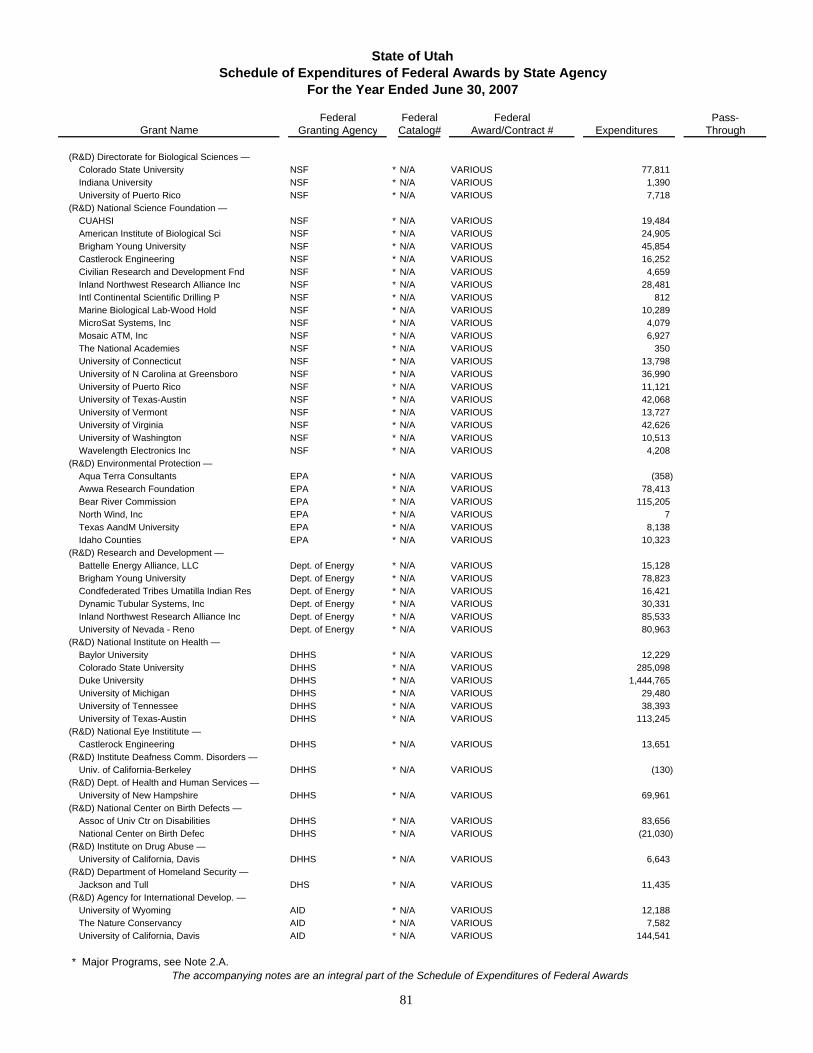

(R&D) Agency for International Development USU * N/A VARIOUS 267,332$ 267,315$ Agency for International Development USU N/A VARIOUS 147,730 417

Pass-Through From Non-State Entities:(R&D) Agency for International Develop. —

University of Wyoming USU * N/A VARIOUS 12,188 The Nature Conservancy USU * N/A VARIOUS 7,582 University of California, Davis USU * N/A VARIOUS 144,541

Agency for International Develop. —Association Liason Office USU N/A VARIOUS 17,761 Academy for Educational Development USU N/A VARIOUS 677

Subtotal – Agency for International Development 597,811 267,732

AGRICULTURE, DEPARTMENT OF

(R&D) AG Research – Basic and Applied Weber State * 10.001 04-CS-11041563-33 & 7,680 06-CS-11041430-013

NONCAPS Inspection Program Agriculture 10.025 05-8588-0587-CA 12,564 Scrapie Program Agriculture 10.025 05-9749-1482-CA 19,211 Avian Influenza Game Birds Agriculture 10.025 06-9749-1588-CA 25,700 NONCAPS Inspection Program Agriculture 10.025 06-8588-0587-CA 34,228 Avian Influenza Surveillance Common Flocks Agriculture 10.025 06-9749-1587-CA 44,980 Animal FAD EMS Agriculture 10.025 05-9749-1446-CA 54,613 CAPS Inspection Program Agriculture 10.025 07-8588-0587-CA 71,670 Johne's Disease Agriculture 10.025 05-979-1370-CA 76,825 National Animal Identification System Agriculture 10.025 05-9749-1404-CA 136,284 Predator Avian Influenza Agriculture 10.025 06-7100-0216-CA 180,000 Chronic Wasting Disease Agriculture 10.025 05-9749-1395-CA 213,561 CAPS Inspection Program Agriculture 10.025 06-8588-0587-CA 227,481 Insect Grant Agriculture 10.025 04-8588-0819-GR 827,341 UDSA School Lunch Agriculture 10.162 12-25-A-3316 2,172 Shell Egg Sureillance Agriculture 10.162 12-25-A-3316 5,386 Bovine Spongiform Encephalophy Agriculture 10.162 223-07-4132 20,000 USDA Poultry Grading Agriculture 10.162 12-25-A-2423 74,145 Specialty Crop Block Grant Agriculture 10.162 12-25-G-0535 103,135 Records Management Agriculture 10.163 12-25-A-3719 28,301 Portereiko Fellowship U OF U 10.206 20043530414931 824 USDA Dairy Grading Agriculture 10.435 12-25-A-3176 15,806 Agriculture Mediation Agriculture 10.435 5200-3087600-0545 17,592 USDA Meat Cooperative Agriculture 10.477 12-37-A-315 7,286 USDA Meat Cooperative Agriculture 10.477 12-37-A-446 116,495 USDA Meat Cooperative Agriculture 10.477 12-37-A-317 979,606 Food Distribution Commodities Education 10.550 VARIOUS 11,924,291 11,924,291 (FSP) Food Stamps SSI Cash Out Workforce Services * 10.551 LOC 4937-2006/7 IS601843 2,157,542 (FSP) Food Stamps Benefits Workforce Services * 10.551 LOC 4942-008006449S6008 132,330,274 (NUT) Nutr. Act School Breakfast Program Education 10.553 VARIOUS 11,766,867 11,766,867 (NUT) Nutr. Act Special Assistance Program Education 10.555 VARIOUS 58,728,377 58,728,377 (NUT) Nutr. Act Special Milk Program Education 10.556 VARIOUS 65,561 65,561 WIC Internal Audit Health * 10.557 3UT700709 31,594 USDA WIC Health * 10.557 3UT700709 31,615,808 9,265,266 Child and Adult Care Food Program Education 10.558 VARIOUS 18,995,026 18,836,035 (NUT) Nutr. Act Summer Food Education 10.559 VARIOUS 2,019,741 1,947,175 Nutr. Act State Administration Education 10.560 VARIOUS 1,399,905 (FSP) Food Stamps State Exchange Workforce Services * 10.561 LOC 4942-2006/7 IS802643 5,490 (FSP) Food Stamps Accuracy Bonus Workforce Services * 10.561 LOC 4942-2005IS251443 39,716 (FSP) Food Stamps Emp/Train 50% Partici. Workforce Services * 10.561 LOC 4942-2006/7 IS252043 96,957 (FSP) Food Stamps Emp/Train 50% Workforce Services * 10.561 LOC 4942-2006/7 IS251943 375,965 (FSP) Food Stamps Emp/Train 100% Workforce Services * 10.561 LOC 4942-2006/7 IE251843 870,757 (FSP) Food Stamps Administration Workforce Services * 10.561 LOC 4942-2006/7 IS251443 19,640,328

Grant Name

State of UtahSchedule of Expenditures of Federal Awards by Federal Agency

For the Year Ended June 30, 2007

* Major Programs, see Note 2.A. The accompanying notes are an integral part of the Schedule of Expenditures of Federal Awards

10

Federal Federal Pass-State Agency Catalog# Award/Contract # Expenditures ThroughGrant Name

State of UtahSchedule of Expenditures of Federal Awards by Federal Agency

For the Year Ended June 30, 2007

(EFA) TEFAP Administration Education 10.568 6UT400013 291,294 291,294 Fresh Fruit and Vegetable Education 10.582 VARIOUS 775,094 775,094 Joint Fire Science Program U OF U 10.652 06CA11046000612JSFP063131 20,505 Gypsy Moth Agriculture 10.664 07CA-11046000-065 8,958 Gypsy Moth Agriculture 10.664 06CA-11046000-065 22,798 Cooperative Weed Management Agriculture 10.664 04-DG-11010000-022 28,579 Forest Legacy - Cedar Project #3 (Adams/Meeks) Natural Resources 10.664 06-DG-11046000-602 1,667 Hazardous Fuel Reduction (Stevens Money) Natural Resources 10.664 06-DG-11046000-610 19,375 Forest Legacy - Administration Natural Resources 10.664 06-DG-11046000-600 27,765 Consolidated Grant - All Programs Natural Resources 10.664 03-DG-11046000-027 39,825 6,940 Forest Legacy - Administration Natural Resources 10.664 05-DG-11046000-073 44,304 Hazardous Fuel Reduction (Stevens Money) Natural Resources 10.664 04-DG-11046000-029 67,963 Hazardous Fuel Reduction (Stevens Money) Natural Resources 10.664 05-DG-11046000-064 83,471 Consolidated Grant - All Programs Natural Resources 10.664 04-DG-11046000-026 244,683 56,203 Consolidated Grant - All Programs Natural Resources 10.664 06-DG-11046000-608 619,335 52,284 Consolidated Grant - All Programs Natural Resources 10.664 01-DG-11046000-021 757,638 Consolidated Grant - All Programs Natural Resources 10.664 05-DG-11046000-050 935,246 157,887 Forest Legacy - Virgin River Headwaters Natural Resources 10.664 07-DG-11046000-601 939,750 Cooperative Forestry Assistance Natural Resources 10.664 VARIOUS 169,900 Economic Action - 4 Corners Natural Resources 10.670 03-DG-11046000-036 5,250 Economic Action - 4 Corners Natural Resources 10.670 03-DG-11046000-025 9,737 Economic Action - Economic Recovery Program (ERPNatural Resources 10.670 01-DG-11046000-053 46,512 Rural Development Council SUU 10.672 VARIOUS 150,145 Forest Land Enhancement Program (FLEP) Natural Resources 10.677 03-DG-11046000-050 25,226 SCD Education Project Agriculture 10.902 65-8D43-5-70 7,913 GIP Grazing Training & Scholarships Agriculture 10.902 68-8-D43-6-06 22,379 GIP Conservation Projects Agriculture 10.902 69-8-D43-6-10 42,008 (R&D) Marine Fungi U OF U * 10.961 5831487040 2,032 (R&D) Marine Invertebrate Symbionts U OF U * 10.962 5831484038 3,138 (R&D) Food Safety and Inspection Service USU * N/A VARIOUS 14,021 (R&D) Valles Caldera Trust USU * N/A VARIOUS 23,577 (R&D) Foreign Agriculture Service USU * N/A VARIOUS 35,420 22,325 (R&D) Department of Agriculture U OF U * N/A VARIOUS 59,655 (192) (R&D) Rural Development USU * N/A VARIOUS 79,211 (R&D) Forest Service USU * N/A 06-JV-11221667-213 (070043) 100,097 (R&D) Forest Service USU * N/A 06-VT-11041930-057 (070198) 107,130 (R&D) Cooperative State Research Svc. USU * N/A 2004-51130-03121 (041753) 120,579 (R&D) Cooperative State Research Svc. USU * N/A 2001-52103-11215 (011310) 126,862 (R&D) Research and Development USU * N/A VARIOUS 134,244 112,497 (R&D) Animal & Plant Health Inspection Svc USU * N/A 07-7449-0042(070272) 141,980 (R&D) Cooperative State Research Svc. USU * N/A 2006-34371-17033 (061713) 142,601 (R&D) Agriculture Research Services USU * N/A 59-5428-4-351(041449) 148,630 (R&D) Animal & Plant Health Inspection Svc USU * N/A VARIOUS 157,845 (R&D) Cooperative State Research Svc. USU * N/A 2006-34530-17329 (070091) 173,329 (R&D) Research and Development USU * N/A 2005-35205-15431(041703) 176,969 (R&D) Cooperative State Research Svc. USU * N/A F061100 187,862 (R&D) Cooperative State Research Svc. USU * N/A 2006-34552-17561 (061775) 192,614 (R&D) National Resources Conservation Svc USU * N/A VARIOUS 208,869 (9,392) (R&D) Cooperative State Research Svc. USU * N/A F072000 210,475 (R&D) Cooperative State Research Svc. USU * N/A 2003-38640-13140 (035135) 225,366 (R&D) Cooperative State Research Svc. USU * N/A F061000 226,839 (R&D) Animal & Plant Health Inspection Svc USU * N/A 07-7400-0470(CA)(070239) 227,738 (R&D) Cooperative State Research Svc. USU * N/A 2005-34552-15828 (051629) 292,651 (R&D) National Resources Conservation Svc USU * N/A 69-8D43-6-05 (070087) 328,514 (R&D) Cooperative State Research Svc. USU * N/A 2006-34570-17134 (061668) 370,568 (R&D) Cooperative State Research Svc. USU * N/A 2005-38640-15900 (051687) 372,393 (R&D) Agriculture Research Services USU * N/A VARIOUS 439,525 (R&D) Cooperative State Research Svc. USU * N/A 2004-38640-14398 (041535) 456,234 (R&D) Forest Service USU * N/A VARIOUS 518,486 40,911 (R&D) Cooperative State Research Svc. USU * N/A F071100 590,852 (R&D) Cooperative State Research Svc. USU * N/A 2006-34526-17001 (061686) 647,011 (R&D) Agriculture Research Services USU * N/A 58-3625-4-121 675,558

* Major Programs, see Note 2.A. The accompanying notes are an integral part of the Schedule of Expenditures of Federal Awards

11

Federal Federal Pass-State Agency Catalog# Award/Contract # Expenditures ThroughGrant Name

State of UtahSchedule of Expenditures of Federal Awards by Federal Agency

For the Year Ended June 30, 2007

(R&D) Cooperative State Research Svc. USU * N/A 2006-38880-03509 (061631) 783,434 (R&D) Cooperative State Research Svc. USU * N/A F071000 848,071 (R&D) Cooperative State Research Svc. USU * N/A VARIOUS 2,142,774 1,241,679 USDA Wool Payment SUU N/A 748D434A637 269 Virgin River Fish Surveys Natural Resources N/A CD-98870602 3,372 EOTC Curation Services Natural Resources N/A 43-8499-2-0022 4,489 Research Joint Venture - Community Wildfire Protecti Natural Resources N/A 05-JV-11231300-050 7,800 Deer/Elk Chronic Wasting Disease Natural Resources N/A 53-8D43-6-01 7,941 Organics Agriculture N/A 12-25-A-4185/4579 10,970 National Resources Conservation Service USU N/A VARIOUS 33,642 Avian Influenza Natural Resources N/A 05-9749-1396-CA 40,069 Department of Agiculture U OF U N/A VARIOUS 40,115 Animal & Plant Health Inspection Service USU N/A VARIOUS 60,402 Forest Service USU N/A VARIOUS 62,206 Farm Bill Biologists Natural Resources N/A CD-98870601 82,195 Research and Development USU N/A VARIOUS 89,816 Risk Management Agency USU N/A 06-IE-0833-0183-E (061770) 105,799 Cooperative State Research Service USU N/A 2005-47001-03205 (051688) 112,465 Rural Development Council SUU N/A 05-DG-1046000-055 113,656 Cooperative State Research Service USU N/A F075000 120,100 Cooperative State Research Service USU N/A 2002-38640-11763 (024264) 127,241 Cooperative State Research Service USU N/A 2002-41590-01384 (024220) 137,644 Risk Management Agency USU N/A VARIOUS 147,106 Animal & Plant Health Inspection Service USU N/A 06-7400-0600(CA)(061141) 184,805 Foreign Agricultural Service USU N/A VARIOUS 191,705 Cooperative State Research Service USU N/A 41100 (F064000) 206,964 Cooperative State Research Service USU N/A 2006-51150-03477 (061653) 212,833 Cooperative State Research Service USU N/A F077000 239,837 Cooperative State Research Service USU N/A 2005-51150-02301 (051620) 243,196 Chronic Wasting Disease Natural Resources N/A 72-8D43-1-43 250,000 Water Quality Manure Management Agriculture N/A 68-8D43-1-198 250,789 Watershed Restoration Natural Resources N/A 04-9749-1229-CA 620,628 Cooperative State Research Service USU N/A F074000 1,240,995 Cooperative State Research Service USU N/A VARIOUS 1,425,617 619,074

Pass-Through From Non-State Entities:(R&D) National Resources Conservation Svc

Farm Pilot Project Coord., Inc. USU * N/A VARIOUS 66,631 (R&D) Animal & Plant Health Inspection Svc —

Mississippi State University USU * N/A VARIOUS 9,039 (R&D) Research and Development —

Dairy Management Inc USU * N/A VARIOUS 13,247 North Dakota State University USU * N/A VARIOUS 4,853 Oregon State University USU * N/A VARIOUS 22,457

(R&D) Cooperative State Research Svc. —Colorado State University USU * N/A VARIOUS 55,394 Dee's Incorporated USU * N/A VARIOUS 3 Hansen Energy & Environmental LLC USU * N/A VARIOUS (296) Michigan State University USU * N/A VARIOUS 14,026 Ohio State University USU * N/A VARIOUS 40,489 Oregon State University USU * N/A VARIOUS (1,727) Purdue University USU * N/A VARIOUS 8,911 The Welding Research Council, Inc USU * N/A VARIOUS 16,218 University of California-Davis USU * N/A VARIOUS 66,379 University of Minnesota USU * N/A VARIOUS 10,850 University of Nevada - Reno USU * N/A VARIOUS 72,674 Washington State University USU * N/A VARIOUS 8,216

Food Safety and Inspection Service —Association of Food & Drug Officials USU N/A VARIOUS 5,514

* Major Programs, see Note 2.A. The accompanying notes are an integral part of the Schedule of Expenditures of Federal Awards

12

Federal Federal Pass-State Agency Catalog# Award/Contract # Expenditures ThroughGrant Name

State of UtahSchedule of Expenditures of Federal Awards by Federal Agency

For the Year Ended June 30, 2007

Cooperative State Research Service —Auburn University USU N/A VARIOUS 104,583 Colorado State University USU N/A VARIOUS 62,618 Kansas Institutions of Higher Educatn USU N/A VARIOUS 16,438 Kansas State University USU N/A VARIOUS 8,808 University of California-Davis USU N/A VARIOUS 1,116 University of Wyoming USU N/A VARIOUS 7,525 Washington State University USU N/A VARIOUS 28,617

Agriculture Research Services —Colorado State University USU N/A VARIOUS 38

Animal & Plant Health Inspection Svc —Colorado State University USU N/A VARIOUS 4,359 Mississippi State University USU N/A VARIOUS 35,839 Montana State University USU N/A VARIOUS 14,627 South Dakota State University USU N/A VARIOUS 9,743

Research and Development —Kansas State University USU N/A VARIOUS 8,005 Texas AandM University USU N/A VARIOUS 75,330

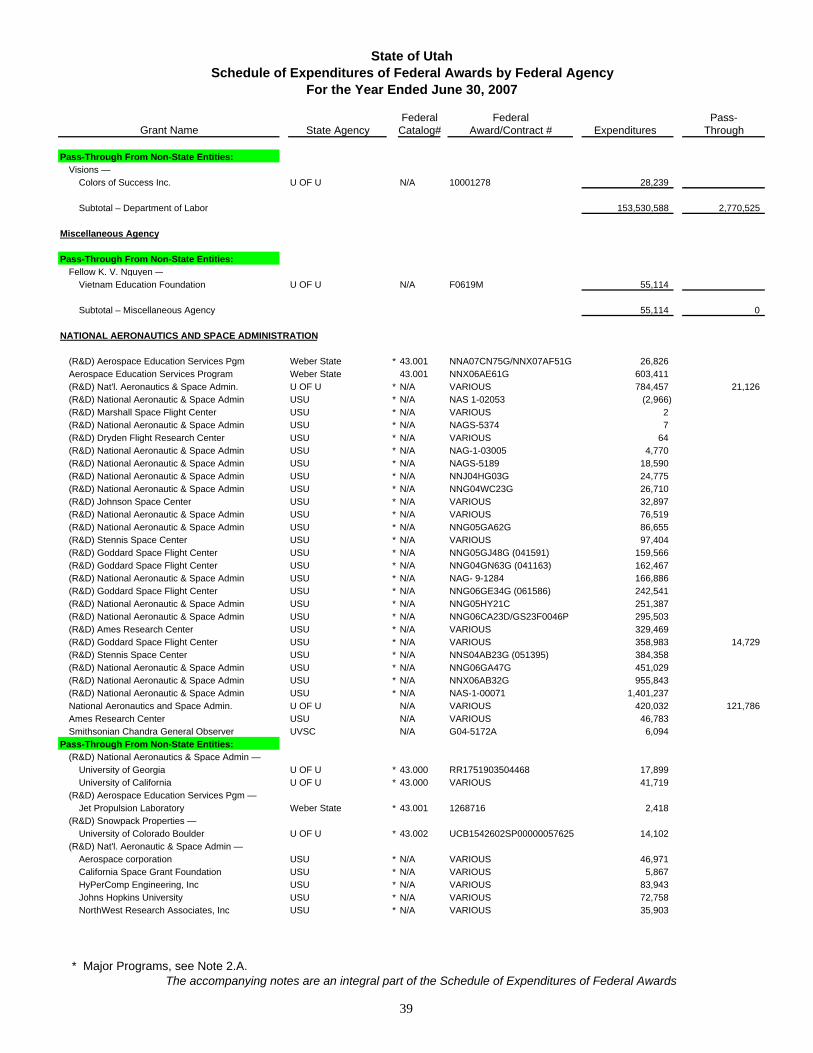

Subtotal – Department of Agriculture 319,632,749 115,900,176

COMMERCE, DEPARTMENT OF

(R&D) NCEP Regional Reanalysis U OF U * 11.431 NA040AR4310077 74,380 PTFP U OF U 11.550 VARIOUS 607,759 Acute Burn Care Telemedicine U OF U 11.552 4960104009 52,107 National Inst. of Standards & Technology UVSC 11.611 70NANB5H1142 813,283 (R&D) Department of Commerce U OF U * N/A VARIOUS 440,982 800 Visualizing History U OF U N/A AB133F06SE5815 1,720 (R&D) Natl. Oceanic and Atmospheric Admin. USU * N/A VARIOUS 4,678 (R&D) Air Force Research Laboratory (NM) USU * N/A VARIOUS 37,445 (R&D) Natl. Oceanic and Atmospheric Admin. USU * N/A 50-SPNA-1-00037 137,393 (R&D) Natl. Oceanic and Atmospheric Admin. USU * N/A DG133E06CQ0079 T0002 244,643 (R&D) National Institute of Standards & Tech. USU * N/A 70NANB6H6145 359,766 (R&D) Natl. Oceanic and Atmospheric Admin. USU * N/A DG133E06CQ0079 T0001 393,061 Economic Development Administration USU N/A 05-01-04089 ('035359) 174,893

Pass-Through From Non-State Entities:(R&D) Coastal Zone Management Admin. —

University of New Hampshire U OF U * 11.419 VARIOUS 80,846 (R&D) High Density Mesonet Obs —

Univ. Corp. Atmospheric Research U OF U * 11.467 S0444697 1,181 (R&D) Natl. Institute of Standards & Tech. —

KT Consulting, Inc. USU * N/A VARIOUS 21,711 Natl. Oceanic and Atmospheric Admin.

Chesapeake Research Consortium USU N/A VARIOUS 6,094

Subtotal – Department of Commerce 3,451,942 800

CORPORATION FOR NATIONAL SERVICE

NCS Americorps Subgrantees DCC 94.003 04CAHUT001 195,207 NCS Americorps Subgrantees DCC 94.003 06ACHUT001 636,848 636,848 NCS Americorps Subgrantees DCC 94.003 03ACHUT001 871,806 871,806 Service Learning Education 94.004 03/05/06KSPUT001 227,147 194,631 School and Community Based Programs SLCC 94.004 03LHHUT001 7,211 NCS Americorps Subgrantees DCC 94.006 06AFHUT001 66,292 66,292 NCS Americorps Subgrantees DCC 94.006 03AFHUT001 381,803 381,803 AmeriCorps Education Award Davis ATC 94.006 VARIOUS 196 NCS Americorps Subgrantees DCC 94.007 04CDHUT001 23,436 23,436 Planning and Program Development SLCC 94.007 VARIOUS 74,395 NCS Americorps Subgrantees DCC 94.009 07VSPUT001 2,393

* Major Programs, see Note 2.A. The accompanying notes are an integral part of the Schedule of Expenditures of Federal Awards

13

Federal Federal Pass-State Agency Catalog# Award/Contract # Expenditures ThroughGrant Name

State of UtahSchedule of Expenditures of Federal Awards by Federal Agency

For the Year Ended June 30, 2007

NCS Americorps Subgrantees DCC 94.009 05PTHUT001 94,743 Natl. Assoc. of Service & Conservation Corps USU N/A VARIOUS 15,040

Pass-Through From Non-State Entities:Planning and Program Development —

Denver Options, Inc. SLCC 94.007 VARIOUS 10,696

Subtotal – Corporation for National Service 2,607,213 2,174,816

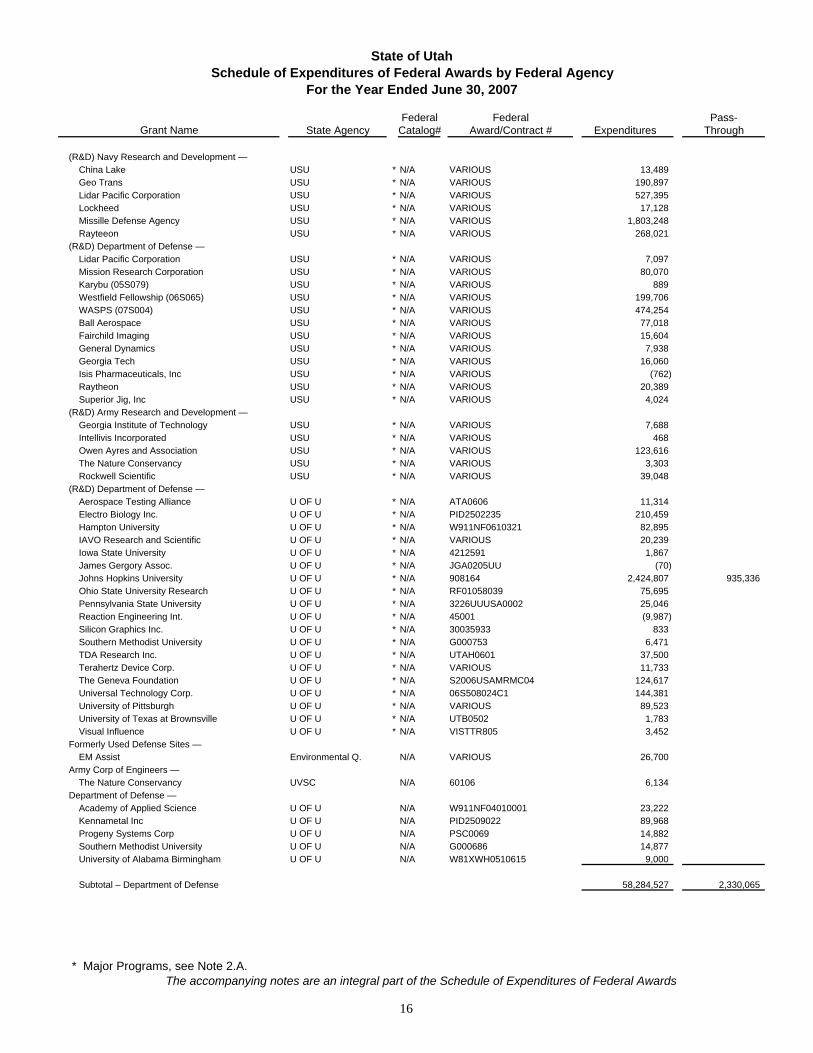

DEFENSE, DEPARTMENT OF

Defence Logistics Agency Governor's Office 12.002 SP4800-03-2-0305,MOD2 300,000 (R&D) Basic and Applied Scientific Res. U OF U * 12.300 VARIOUS 422,315 Military Construction National Guard 12.400 DAHA42-1001A 2,771,469 Military Operations and Maintenance National Guard * 12.401 DAHA42-1040 60,127 Military Operations and Maintenance National Guard * 12.401 DAHA42-1001C 201,314 Military Operations and Maintenance National Guard * 12.401 DAHA42-1015 249,338 Military Operations and Maintenance National Guard * 12.401 DAHA42-1007 273,961 Military Operations and Maintenance National Guard * 12.401 DAHA42-1004 325,649 Military Operations and Maintenance National Guard * 12.401 DAHA42-1023 556,984 Military Operations and Maintenance National Guard * 12.401 DAHA42-1024 883,890 Military Operations and Maintenance National Guard * 12.401 DAHA42-1005 1,578,371 Military Operations and Maintenance National Guard * 12.401 DAHA42-1021 1,798,773 Environmental Resource Management National Guard * 12.401 DAHA42-1002 1,942,362 Military Operations and Maintenance National Guard * 12.401 DAHA42-1001B 1,963,411 Military Operations and Maintenance National Guard * 12.401 DAHA42-1003 2,006,364 Military Operations and Maintenance National Guard * 12.401 DAHA42-1001A 6,855,206 Military Operations and Maintenance National Guard * 12.401 DAHA42-1041 14,738 (R&D) Military Medical Research & Develop. U OF U * 12.420 VARIOUS 227,173 NF Site U OF U 12.420 W81XWH0610030 11,116 (R&D) Basic and Scientific Research U OF U * 12.431 VARIOUS 152,971 38,777 (R&D) Air Force Defense Research Sci. U OF U * 12.800 VARIOUS 331,238 (R&D) Navy Research and Development USU * N/A N66001-00-1-8909 (20,256) (R&D) Missile Defense Agency USU * N/A HQ0006-00-D-0006 D.O. 7 (13,581) (R&D) Missile Defense Agency USU * N/A HQ0006-00-D-0006 D.O. 12 (1,420) (R&D) Missile Defense Agency USU * N/A HQ0006-02-2-0001-0006 (1,329) (R&D) Missile Defense Agency USU * N/A HQ0006-02-2-0001-0007 (153) (R&D) Navy Research and Development USU * N/A N00173-02-D-2003 D3O.0002 5 (R&D) Navy Research and Development USU * N/A N00173-3-01-G014 20,275 (R&D) Missile Defense Agency USU * N/A HQ0006-032-2-0001-0011 24,020 (R&D) Missile Defense Agency USU * N/A HQ0006-05-D-0005-0012 26,086 (R&D) Missile Defense Agency USU * N/A HQ0006-05-D-0005-0011 33,156 (R&D) Missile Defense Agency USU * N/A HQ0006-02-2-0001-0007 39,718 (R&D) Navy Research and Development USU * N/A VARIOUS 39,903 (R&D) Navy Research and Development USU * N/A GS04T05DBP020/ GS-23F-0046 43,894 (R&D) Navy Research and Development USU * N/A N00173-05-P-2019 51,289 (R&D) National Geospatial-Intelligence Agency USU * N/A VARIOUS 52,154 (R&D) Department of Defense USU * N/A VARIOUS 74,563 2,324 (R&D) Navy Research and Development USU * N/A N00014-06-1-0820 (061707) 78,826 (R&D) Army Research and Development USU * N/A VARIOUS 80,479 (R&D) AF Research and Development USU * N/A FA9550-05-1-0482 129,564 (R&D) Missile Defense Agency USU * N/A HQ0006-05-D-0005-0006 152,783 (R&D) Navy Research and Development USU * N/A N00014-07-1-0053 (070108) 168,019 (R&D) AF Research and Development USU * N/A FA9550-06-1-0217 (061442) 172,770 (R&D) AF Research and Development USU * N/A VARIOUS 265,318 27,029 (R&D) Missile Defense Agency USU * N/A HQ0006-05-D-0005-0001 324,054 (R&D) Navy Research and Development USU * N/A N00173-02-D-2003 D.O.003 348,051 (R&D) AF Research and Development USU * N/A FA8819-06-C-0003 380,721 (R&D) AF Research and Development USU * N/A F19628-03-C-0058 406,332 (R&D) Missile Defense Agency USU * N/A HQ0006-05-D-0005-0010 447,363 (R&D) AF Research and Development USU * N/A FA8718-06-C-0001 545,468 (R&D) Missile Defense Agency USU * N/A HQ0006-00-D-0006 D.O. 19 613,734

* Major Programs, see Note 2.A. The accompanying notes are an integral part of the Schedule of Expenditures of Federal Awards

14

Federal Federal Pass-State Agency Catalog# Award/Contract # Expenditures ThroughGrant Name

State of UtahSchedule of Expenditures of Federal Awards by Federal Agency

For the Year Ended June 30, 2007

(R&D) Army Research and Development USU * N/A W911W6-06-C-0008 660,302 (R&D) AF Research and Development USU * N/A FA8819-06-C-0004 744,326 (R&D) Department of Defense U OF U * N/A VARIOUS 1,513,714 419,486 (R&D) Missile Defense Agency USU * N/A HQ0006-05-D-0005-0008 2,159,297 (R&D) Navy Research and Development USU * N/A N00173-02-D-2003 D3O.0005 2,670,827 (R&D) Navy Research and Development USU * N/A N00173-02-D-2003 D3O.0006 8,411,836 Neotropical Migratory Bird Natural Resources N/A CD-98870604-0 (1,398) Database Update Natural Resources N/A VARIOUS 845 Army Research and Development USU N/A VARIOUS 1,353 Bat Database Natural Resources N/A DE-RE013-02GJ67277 7,877 Ogden Defense Depot Environmental Q. N/A CerclaSctn120 17,409 Air Force Research and Development USU N/A VARIOUS 17,658 Hill Air Force Base Environmental Q. N/A CerclaSctn120 141,030 DSMOA Environmental Q. N/A W9128F-04-2-0149 422,644 Department of Defense U OF U N/A VARIOUS 1,480,532 907,113

Pass-Through From Non-State Entities:(R&D) Basic Scientific Reserach —

University of California U OF U * 12.431 KK4100 79,245 University of Pittsburgh U OF U * 12.431 4030864 410,890

(R&D) Air Force Defense Research Sciences—Colorado Schools of Mines U OF U * 12.800 00001040 31,652 Ohio State University U OF U * 12.800 P0RF00960594 (3,468)

(R&D) COLD —Idaho State University U OF U * 12.910 06348A 112,000

(R&D) Military Medical Research & Devlop. —University of Minnesota U OF U * 12.420 M6636393101 43,173 University of Texas, Houston U OF U * 12.420 5DAMD170310222 4,895

(R&D) Basic and Applied Scientific Research —Ohio State University U OF U * 12.300 P0RF00921713 (8,785) University of CA Los Angeles U OF U * 12.300 P0190GBC15808 56,859

Procurement Technical Asst. for Business — SubK-05-Weber State-BearingPoint Inc. Weber State 12.002 FA8601-05-F-0106-826 563,940

(R&D) AF Research and Development —Aerospace Engineering Spectrum USU * N/A VARIOUS 17,782 CH2M HILL USU * N/A VARIOUS 3,418 EarthTech USU * N/A VARIOUS (187) Micro Stat Systems, Inc USU * N/A VARIOUS 21,068 Multimedia Data Services Corporation USU * N/A VARIOUS 991 Northrop Grumman USU * N/A VARIOUS 10,481 Science Application International Corp USU * N/A VARIOUS 25,898 Select Engineering Services USU * N/A VARIOUS 13,314 State University of New York USU * N/A VARIOUS 153 SVT Associates Inc USU * N/A VARIOUS 24,682 Taitech, Inc USU * N/A VARIOUS 4,699 URS Corporation USU * N/A VARIOUS 4,644 The Aerospace Corporation USU * N/A VARIOUS (333) Ball Aerospace USU * N/A VARIOUS 58,025 CRAFT Technology USU * N/A VARIOUS 7,865 Fairchild Imaging USU * N/A VARIOUS 39,204 L-3 Communications USU * N/A VARIOUS 114,924 Lockheed USU * N/A VARIOUS 1,961,834 MicroSat Systems USU * N/A VARIOUS 34,913 Missile Defense Agency USU * N/A VARIOUS 290,613 MRC USU * N/A VARIOUS 181,094 Northrop Grumman USU * N/A VARIOUS 271,846 Phillips Lab USU * N/A VARIOUS 399,758 Raytheon USU * N/A VARIOUS 30,360 Sensing Strategies, Inc USU * N/A VARIOUS 267,316 Spectral Sciences, Inc. USU * N/A VARIOUS 209,007

* Major Programs, see Note 2.A. The accompanying notes are an integral part of the Schedule of Expenditures of Federal Awards

15

Federal Federal Pass-State Agency Catalog# Award/Contract # Expenditures ThroughGrant Name

State of UtahSchedule of Expenditures of Federal Awards by Federal Agency

For the Year Ended June 30, 2007

(R&D) Navy Research and Development —China Lake USU * N/A VARIOUS 13,489 Geo Trans USU * N/A VARIOUS 190,897 Lidar Pacific Corporation USU * N/A VARIOUS 527,395 Lockheed USU * N/A VARIOUS 17,128 Missille Defense Agency USU * N/A VARIOUS 1,803,248 Rayteeon USU * N/A VARIOUS 268,021

(R&D) Department of Defense —Lidar Pacific Corporation USU * N/A VARIOUS 7,097 Mission Research Corporation USU * N/A VARIOUS 80,070 Karybu (05S079) USU * N/A VARIOUS 889 Westfield Fellowship (06S065) USU * N/A VARIOUS 199,706 WASPS (07S004) USU * N/A VARIOUS 474,254 Ball Aerospace USU * N/A VARIOUS 77,018 Fairchild Imaging USU * N/A VARIOUS 15,604 General Dynamics USU * N/A VARIOUS 7,938 Georgia Tech USU * N/A VARIOUS 16,060 Isis Pharmaceuticals, Inc USU * N/A VARIOUS (762) Raytheon USU * N/A VARIOUS 20,389 Superior Jig, Inc USU * N/A VARIOUS 4,024

(R&D) Army Research and Development —Georgia Institute of Technology USU * N/A VARIOUS 7,688 Intellivis Incorporated USU * N/A VARIOUS 468 Owen Ayres and Association USU * N/A VARIOUS 123,616 The Nature Conservancy USU * N/A VARIOUS 3,303 Rockwell Scientific USU * N/A VARIOUS 39,048

(R&D) Department of Defense —Aerospace Testing Alliance U OF U * N/A ATA0606 11,314 Electro Biology Inc. U OF U * N/A PID2502235 210,459 Hampton University U OF U * N/A W911NF0610321 82,895 IAVO Research and Scientific U OF U * N/A VARIOUS 20,239 Iowa State University U OF U * N/A 4212591 1,867 James Gergory Assoc. U OF U * N/A JGA0205UU (70) Johns Hopkins University U OF U * N/A 908164 2,424,807 935,336 Ohio State University Research U OF U * N/A RF01058039 75,695 Pennsylvania State University U OF U * N/A 3226UUUSA0002 25,046 Reaction Engineering Int. U OF U * N/A 45001 (9,987) Silicon Graphics Inc. U OF U * N/A 30035933 833 Southern Methodist University U OF U * N/A G000753 6,471 TDA Research Inc. U OF U * N/A UTAH0601 37,500 Terahertz Device Corp. U OF U * N/A VARIOUS 11,733 The Geneva Foundation U OF U * N/A S2006USAMRMC04 124,617 Universal Technology Corp. U OF U * N/A 06S508024C1 144,381 University of Pittsburgh U OF U * N/A VARIOUS 89,523 University of Texas at Brownsville U OF U * N/A UTB0502 1,783 Visual Influence U OF U * N/A VISTTR805 3,452

Formerly Used Defense Sites —EM Assist Environmental Q. N/A VARIOUS 26,700

Army Corp of Engineers —The Nature Conservancy UVSC N/A 60106 6,134

Department of Defense —Academy of Applied Science U OF U N/A W911NF04010001 23,222 Kennametal Inc U OF U N/A PID2509022 89,968 Progeny Systems Corp U OF U N/A PSC0069 14,882 Southern Methodist University U OF U N/A G000686 14,877 University of Alabama Birmingham U OF U N/A W81XWH0510615 9,000

Subtotal – Department of Defense 58,284,527 2,330,065

* Major Programs, see Note 2.A. The accompanying notes are an integral part of the Schedule of Expenditures of Federal Awards

16

Federal Federal Pass-State Agency Catalog# Award/Contract # Expenditures ThroughGrant Name

State of UtahSchedule of Expenditures of Federal Awards by Federal Agency

For the Year Ended June 30, 2007

EDUCATION, DEPARTMENT OF

Adult Education Act Education 84.002 V002A04/05/060044 3,331,749 2,701,694 (SFA) Supp. Educ. Opportunity Grants Davis ATC * 84.007 P007A067112 41,516 (SFA) Supp. Educ. Opportunity Grants Ogden/Weber ATC * 84.007 P007A066314 91,152 (SFA) Supp. Educ. Opportunity Grants Dixie College * 84.007 P007A064194 107,937 (SFA) Supp. Educ. Opportunity Grants CEU * 84.007 P007A064192 69,660 (SFA) Supp. Educ. Opportunity Grants SLCC * 84.007 P007A064220 286,322 (SFA) Supp. Educ. Opportunity Grants Snow College * 84.007 P007A064212 82,143 (SFA) Supp. Educ. Opportunity Grants SUU * 84.007 P007A064213 166,045 (SFA) Supp. Educ. Opportunity Grants U OF U * 84.007 P007A054217/064217 614,712 (SFA) Supp. Educ. Opportunity Grants USU * 84.007 VARIOUS 636,442 (SFA) Supp. Educ. Opportunity Grants UVSC * 84.007 P007A064219 984,451 (SFA) Supp. Educ. Opportunity Grants Weber State * 84.007 P007A064221 461,583 Title I Grants to Local Education Agencies Education * 84.010 S010A04/05/060044 52,156,842 51,222,982 Title I Migrant Education Education 84.011 S011A04/05/060045 2,071,408 1,849,684 Title I Neglected & Delinquent Children Education 84.013 A013A04/05/060044 670,571 584,612 NRC Fellowships Program U OF U 84.015 VARIOUS 460,983 International Studies Global and Local U OF U 84.016 P016A040007 31,608 International Studies and Foreign Language USU 84.016 VARIOUS 94,153 (SE) IDEA Special Education Education 84.027 H027A04/05/060059 100,879,127 96,918,888 (SE) Special Education Grants to States USU 84.027 VARIOUS 22,932 22,932 Scholarship Endowment, Federal Expend. CEU 84.031 VARIOUS 161,324 Title III CEU 84.031 P031A030080 355,921 Title III Student Success Retention UVSC 84.031 PO31A060252 370,738 1988 Scholarship Endowment Grant UVSC 84.031 PO31G80105 17,346 1990 Scholarship Endowment Grant UVSC 84.031 PO31G00018 93,862 Special Allowance Payments Board of Regents * 84.032 VARIOUS 45,968,433 Federal Interest Subsidy Payments Board of Regents * 84.032 VARIOUS 15,550,136 Federal Reinsurance Received on Defaulted Loan Claims Paid 33,730,882 Less Collection on Defaulted Loans Remitted to Department of Education 6,043,149 Net Federal Reinsurance Received on Defaulted Loan Claims Paid Board of Regents * 84.032 VARIOUS 27,687,733 Default Adversion Fee Board of Regents * 84.032 VARIOUS 584,367 Account Maintenance Fee Board of Regents * 84.032 VARIOUS 2,954,851 Loan Processing and Issuance Fee Board of Regents * 84.032 VARIOUS 1,188,309 (SFA) College Work-Study Program Davis ATC * 84.033 P033A067112 21,446 (SFA) College Work-Study Program Ogden/Weber ATC * 84.033 P033A066314 72,595 (SFA) College Work-Study Program Dixie College * 84.033 P033A064194 204,296 (SFA) College Work-Study Program CEU * 84.033 P033A064192 43,378 (SFA) College Work-Study Program SLCC * 84.033 P033A064220 321,472 (SFA) College Work-Study Program Snow College * 84.033 P033A064212 95,441 (SFA) College Work-Study Program SUU * 84.033 P033A064213 241,695 (SFA)(R&D) College Work-Study Program U OF U * 84.033 P033A064217 293,455 (SFA) College Work-Study Program U OF U * 84.033 P033A054217/064217 916,813 (SFA) College Work-Study Program USU * 84.033 VARIOUS 534,987 (SFA) College Work-Study Program UVSC * 84.033 P033A064219 1,227,593 (SFA) College Work-Study Program Weber State * 84.033 P033A054221 / 064221 727,497 (SFA) Perkins Loan Program CEU * 84.038 P038A064192 42,094 (SFA) Perkins Loan Program SLCC * 84.038 VARIOUS 109,173 (SFA) Perkins Loan Program Snow College * 84.038 P038A064212 4,685 (SFA) Perkins Loan Program SUU * 84.038 P038A064213 22,784 (SFA) Perkins Loan Program U OF U * 84.038 P033A064217 393,972 (SFA) Perkins Loan Program USU * 84.038 P038A064218 107,198 (SFA) Perkins Loan Program UVSC * 84.038 P037Y054219 30,582 (SFA) Perkins Loan Program Weber State * 84.038 P038A044221 35,857 (TRIO) Student Support Services Dixie College * 84.042 P042A050119 314,191 (TRIO) Student Support Services CEU * 84.042 P042A050297 223,540 (TRIO) Student Support Services CEU * 84.042 P042A020583/060026 327,833 (TRIO) Student Support Services SLCC * 84.042 P042A020427/060409 315,995

* Major Programs, see Note 2.A. The accompanying notes are an integral part of the Schedule of Expenditures of Federal Awards

17

Federal Federal Pass-State Agency Catalog# Award/Contract # Expenditures ThroughGrant Name

State of UtahSchedule of Expenditures of Federal Awards by Federal Agency

For the Year Ended June 30, 2007

(TRIO) Student Support Services Snow College * 84.042 P042A050435 319,248 (TRIO) Student Support Services SUU * 84.042 P042A050878 277,351 (TRIO) Student Support Services U OF U * 84.042 P042A010889/050797 304,404 (TRIO) – Student Support Services USU * 84.042 P042A020890(011102) 262,608 (TRIO) Student Support Services UVSC * 84.042 P042A050863 219,687 (TRIO) Student Support Services Weber State * 84.042 P042A050608 383,370 (TRIO) Talent Search Dixie College * 84.044 P044A020614 353,644 (TRIO) Talent Search CEU * 84.044 P044A020606/060589 367,407 (TRIO) Talent Search SLCC * 84.044 P044A020845 207,058 (TRIO) Talent Search Snow College * 84.044 P044A020785 421,520 (TRIO) Talent Search SUU * 84.044 P044A020377/060385 265,872 (TRIO) Talent Search UVSC * 84.044 P044A020762 258,963 (TRIO) Talent Search Weber State * 84.044 P044A060394 152,892 (TRIO) Upward Bound Dixie College * 84.047 P047A040666 326,831 (TRIO) Upward Bound CEU * 84.047 P047A050427 472,097 (TRIO) Upward Bound Snow College * 84.047 P047A030734 359,770 (TRIO) Upward Bound Program SUU * 84.047 P047A030982 454,464 (TRIO) Upward Bound U OF U * 84.047 P047A030332/070615 400,111 (TRIO) Upward Bound UVSC * 84.047 P047A031157 319,242 (TRIO) Upward Bound Weber State * 84.047 P047A040876 / 030623 692,546 Voc. Ed. Programs Carl Perkins Education * 84.048 V048A06/05/040044 11,713,207 6,034,178 (SFA) Pell Grant Program Bridgerland ATC * 84.063 P063P063761 378,296 (SFA) Pell Grant Program Davis ATC * 84.063 P063P063839 336,709 (SFA) Pell Grant Program Mountainland ATC * 84.063 P063P065818 7,797 (SFA) Pell Grant Program Ogden/Weber ATC * 84.063 P063P064239 448,933 (SFA) Pell Grant Program Uintah Basin ATC * 84.063 VARIOUS 68,305 (SFA) Pell Grant Program Dixie College * 84.063 VARIOUS 3,864,329 (SFA) Pell Grant Program CEU * 84.063 P063P062350 1,562,879 (SFA) Pell Grant Program SLCC * 84.063 VARIOUS 11,291,022 (SFA) Pell Grant Program Snow College * 84.063 P063P062353 2,250,817 (SFA) Pell Grant Program SUU * 84.063 P063P062352 5,961,928 (SFA) Pell Grant Program U OF U * 84.063 VARIOUS 12,888,014 (SFA) Pell Grant Program USU * 84.063 P063P052351(051519) 56,989 (SFA) Pell Grant Program USU * 84.063 P063P062351(061617) 14,241,802 (SFA) Pell Grant Program UVSC * 84.063 VARIOUS 16,408,305 (SFA) Pell Grant Program Weber State * 84.063 VARIOUS 10,679,214 (TRIO) Educational Opportunity Center UVSC * 84.066 P066A020251 225,681 Leveraging Educational Assist. Partnership Board of Regents 84.069 VARIOUS 597,423 597,423 State Student Initiative Grants USU 84.069 VARIOUS 318,000 Improvement of Postsecondary Education USU 84.116 VARIOUS 94,303 Improvement of Postsecondary Education USU 84.116 P116B041212 (041516) 130,981 FIPSE Directed Grants–County Jail Project UVSC 84.116 P116Z050285 22,409 FIPSE Directed Grants–Turning Point UVSC 84.116 P116Z040168 36,244 FIPSE Directed Grants–Single Parent Pgrms UVSC 84.116 P116Z040166 84,509 Voc. Rehab. Basic Title 1 Section Education * 84.126 H126A07/06/050066 23,337,830 205,041 Rehab Service – Migrant and Seasonal Education 84.128 H128G020009 162,839 Rehabilitation Long-Term Training USU 84.129 H129B050003 (051633) 109,227 Rehabilitation Long-Term Training USU 84.129 H129B040005 (041165) 143,586 Rehabilitation Long-Term Training USU 84.129 H129W050002 (051657) 175,048 (R&D) Natl. Institute on Disability & Rehab USU * 84.133 VARIOUS 51,059 Migrant Education Coordination Education 84.144 S144F04/05/060045 125,831 13,137 Independent Living Services Education 84.169 H169A04/05/060065 293,562 293,562 (SE) Preschool Grant Education 84.173 H173S03/04/050092 3,444,851 3,331,969 Independent Living for Older Blind Persons Education 84.177 H177B04/05/060044 227,188 191,838 H/C Infant and Todlers Health 84.181 H181A050111 5,608,124 234,795 Drug Free State Data Education 84.184 Q184R040014 401,485 Byrd Honors Scholarships Education 84.185 P185A040040/050046 360,750 Safe and Drug Free Education 84.186 Q186A03/04/050046 1,806,605 1,650,542 Safe And Drug Free Schools Human Services 84.186 S186B030047 541,417 541,417 Title VI Supported Employment Education 84.187 H187A04/05/060067 362,107 Bilingual Education, Professional Devlop. Weber State 84.195 T195N020048 382,276 332,888 Homeless Child Education Education 84.196 S196A04/05/060046 218,392 164,320

* Major Programs, see Note 2.A. The accompanying notes are an integral part of the Schedule of Expenditures of Federal Awards

18

Federal Federal Pass-State Agency Catalog# Award/Contract # Expenditures ThroughGrant Name

State of UtahSchedule of Expenditures of Federal Awards by Federal Agency

For the Year Ended June 30, 2007

Graduate Assist. in Areas of National Need USU 84.200 VARIOUS 186,081 950 Education Statistics System Education 84.201 VARIOUS 164,230 Even Start Family Literacy Education 84.213 S213C04/05/060045 610,229 576,350 FIE Earmark Programs Education 84.215 VARIOUS 641,679 500,525 Improvement of Education SLCC 84.215 U215K050626 5,584 Fund for the Imporvement of Education U OF U 84.215 VARIOUS 224,806 Ciber U OF U 84.220 VARIOUS 292 (R&D) State Grants for Assistive Technology USU * 84.224 VARIOUS 62,796 State Grants for Assistive Technology USU 84.224 VARIOUS 122,106 State Grants for Assistive Technology USU 84.224 H224A060044 (061407) 336,217 Projects with Industry SLCC 84.234 VARIOUS 299,478 Projects with Industry UVSC 84.234 H234R050178 206,451 Voc. Educ. Technical Preparation Education 84.243 VARIOUS 1,257,239 336,865 Voc. Rehab. In-Service Training Education 84.265 H265A000029 36,511 Rehabilitation Training General Training USU 84.275 H129B050003 (051849) 334,719 Public Charter Schools Facilities Education 84.282 U282D040006 1,753,492 1,753,492 Public Charter Schools Education 84.282 VARIOUS 3,938,551 3,706,918 After School Learning 21st Century Education 84.287 S287C04/05/060045 4,888,098 4,765,781 Innovative Education Program Strategies Education 84.298 VARIOUS 1,347,340 1,000,942 Indian Education – Special Programs U OF U 84.299 VARIOUS 898,380 (R&D) Ed Research, Develop & Dissemination USU * 84.305 R305M050003(051368) 257,770 (1,559) Technology Literacy Challenge Education 84.318 S318X04/05/060044 2,418,357 2,259,178 State Improvement Grant IDEA Education 84.323 H323A040016 1,283,103 1,283,103 Spec. Ed–Research Children w Disabilities U OF U 84.324 VARIOUS 83,194 Research in Special Education USU 84.324 VARIOUS 238 Career Award USDB 84.324 H324N040044 74,377 Spec. Ed–Personnel Children w Disabilities U OF U 84.325 VARIOUS 862,272 107,693 (R&D) Special Ed–Personnel Preparation USU * 84.325 VARIOUS 1,542 (R&D) Special Ed–Personnel Preparation USU * 84.325 H325D040065 (041553) 145,439 Special Ed–Personnel Preparation USU 84.325 H325N020079-04 (021160) 107,511 Special Ed–Personnel Preparation USU 84.325 VARIOUS 138,359 Deaf and Blind Centers Education 84.326 H326C030012 37,500 8,357 Special Ed – Technical Assit. and Dissmin. USU 84.326 H326X040039 (051073) 187,863 Special Ed – Technical Assit. and Dissmin. USU 84.326 H326R040006 (041579) 1,147,985 Deaf and Blind Centers USDB 84.326 H326C030012 107,357 (R&D) Special Ed–Tech & Media Services USU * 84.327 VARIOUS 1,692 1,505 Special Ed–Tech & Media Services USU 84.327 H327A040096 (041584) 129,247 Special Ed–Tech & Media Services USU 84.327 H327A050088 (051721) 222,241 Advanced Placement Program Test Fees Education 84.330 U330B060014 3,692 Advanced Placement Program Education 84.330 U330C030086 666,261 316,137 Training Incarcerated Youth Education 84.331 Q331A04/05/060046 44,746 Comphensive School Reform Education 84.332 A332A03/04/050046 1,533,130 1,509,088 (R&D) Demo Project to Ensure Students with Disabilities Receive Higher Ed USU * 84.333 VARIOUS 66,055 Gear-Up UVSC 84.334 P334S050019 1,397,319 Child Care Access Means Parents in School U OF U 84.335 P335A050094 135,582 Child Care Access Means Parents in School UVSC 84.335 P335A050435 189,703 Career Resource Network Education 84.346 V346A000049/49-04 42,381 40,640 Transition to Teaching Education 84.350 S350B02033-03/04/05 173,801 Reading First Education 84.357 S357A04/05/060046 6,066,297 4,641,975 English Language Acquisition Education 84.365 T365A04/05/060044 2,527,895 2,447,114 Math and Science Partnership Education 84.366 S366B04/05/060045 697,605 232,684 Improving Teacher Quality Education 84.367 S367A04/05/060042 18,908,353 18,362,767 No Child Left Behind Board of Regents 84.367 S367B040039A 434,889 State Assessments Education 84.369 S369A04/05/060046 5,146,370 144,859 (SFA) Academic Competitiveness Grant Dixie College * 84.375 P375A062346 46,450 (SFA) Academic Competitiveness Grant SLCC * 84.375 P375A062605 17,550 (SFA) Academic Competitiveness Grant Snow College * 84.375 P375A062353 1,500 (SFA) Academic Competitiveness Grant SUU * 84.375 P375A062352 20,700 (SFA) Academic Competitiveness Grant U OF U * 84.375 P375A062349 86,425

* Major Programs, see Note 2.A. The accompanying notes are an integral part of the Schedule of Expenditures of Federal Awards

19

Federal Federal Pass-State Agency Catalog# Award/Contract # Expenditures ThroughGrant Name

State of UtahSchedule of Expenditures of Federal Awards by Federal Agency

For the Year Ended June 30, 2007

(SFA) Academic Competitiveness Grant USU * 84.375 P375A062351 107,684 (SFA) Academic Competitiveness Grant UVSC * 84.375 P375A062493 66,325 (SFA) Academic Competitiveness Grant Weber State * 84.375 P375A062354 13,508 (SFA) National SMART Grant Dixie College * 84.376 P376S062346 134,467 (SFA) National SMART Grant SUU * 84.376 P376S062352 445,882 (SFA) National SMART Grant U OF U * 84.376 P376A062349 1,470,235 (SFA) National SMART Grant USU * 84.376 P376S062351 1,999,235 (SFA) National SMART Grant UVSC * 84.376 P376S5062493 1,126,446 (SFA) National SMART Grant Weber State * 84.376 P376S062354 299,088 National Writing Project USU 84.928 VARIOUS 37,641 ESEA Hurricane Relief Education 84.938 S938C060033 542,250 542,250

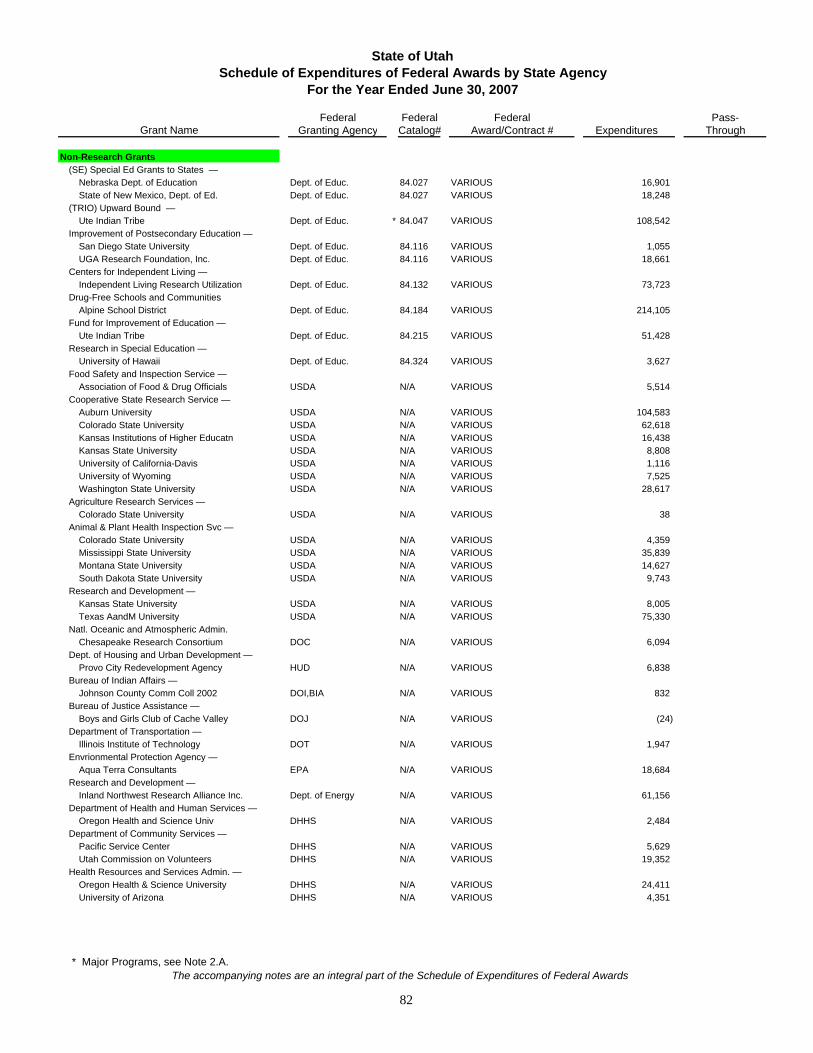

Pass-Through From Non-State Entities:(SE) Special Ed Grants to States —

Nebraska Dept. of Education USU 84.027 VARIOUS 16,901 State of New Mexico, Dept. of Ed. USU 84.027 VARIOUS 18,248

(TRIO) Upward Bound —Ute Indian Tribe USU * 84.047 VARIOUS 108,542

Improvement of Postsecondary Education —Gadsden State Community College SLCC 84.116 VARIOUS 6,387

Improvement of Postsecondary Education —San Diego State University USU 84.116 VARIOUS 1,055 UGA Research Foundation, Inc. USU 84.116 VARIOUS 18,661

Improvement of Postsecondary Education —Coastline Community College UVSC 84.116 U-7819.9.00.8860 42,297

Centers for Independent Living —Independent Living Research Utilization USU 84.132 VARIOUS 73,723

Early Intervention —State of Arizona Health 84.181 1804012 229,548

Drug-Free Schools and CommunitiesAlpine School District USU 84.184 VARIOUS 214,105

Even Start State Educational Agencies —Ogden City School District Weber State 84.214 VARIOUS 16,666

New Jersey Caring Schools Incl. —Rutgers University U OF U 84.215 3062 3,155

Fund for Improvement of Education —Ute Indian Tribe USU 84.215 VARIOUS 51,428

(R&D) Ed Research, Devlp & Dissemination —University of Toledo USU * 84.305 VARIOUS 61,019

(R&D) Research in Special Education —Arc of the United States USU * 84.324 VARIOUS 7,769

Research in Special Education —University of Hawaii USU 84.324 VARIOUS 3,627

Leadership Preparation —Oregon State University U OF U 84.325 ED068AA 25,131

(R&D) Special Ed–Tech. Asst. & Dissem. —University of Oregon USU * 84.326 VARIOUS 60,974

Gear Up —Granite School District U OF U 84.334 04009 38,917

National Writing Project —National Writing Project Corporation Weber State 84.928 07-UT02 5,958

Department of Education —Centro De La Familia De Utah U OF U N/A PID2403012 11,798 Mathematica U OF U N/A 613604069 46,515

Subtotal – Department of Education 473,094,501 211,429,516

* Major Programs, see Note 2.A. The accompanying notes are an integral part of the Schedule of Expenditures of Federal Awards

20

Federal Federal Pass-State Agency Catalog# Award/Contract # Expenditures ThroughGrant Name

State of UtahSchedule of Expenditures of Federal Awards by Federal Agency

For the Year Ended June 30, 2007

ELECTION ASSISTANCE COMMISSION

Help America Vote Act Requirements Pmts. Governor's Office 90.401 VARIOUS 5,753,812 (R&D) Counting and Recounting Procedures U OF U * N/A E4019683EAC0552 50,048

Subtotal – Election Assistance Commission 5,803,860 0

ENERGY, DEPARTMENT OF

Formula Grant- Working Group (UWG1) Natural Resources 81.041 DE-FG26-04R806611 11,433 11,433 Formula Grant-Schools K-12 (UK12) Natural Resources 81.041 DE-FC48-00R04511 12,000 12,000 Formula Grant- Clean Cities (UCCC) Natural Resources 81.041 E4R4DM4141 19,717 19,717 Sep Special Projects (UCDS) Natural Resources 81.041 DE-FG48-02R830111 23,692 22,741 Sep Special Projects (UCS2) Natural Resources 81.041 DE-FG48-02R830111 36,100 36,100 Formula Grant- Renewable (UBLD) Natural Resources 81.041 DE-FC48-05R807011 39,862 28,223 Geothermal Outreach (UHT3) Natural Resources 81.041 DE-FG36-04R806711 51,504 Formula Grant- Renewable (UANM) Natural Resources 81.041 X7-97820101 54,350 11,218 Formula Grant- Renewable (UPUB) Natural Resources 81.041 DE-FG48-02R830111 58,310 15,000 Sep Special Projects (UBUS) Natural Resources 81.041 DE-FG48-02R830111 180,000 180,000 Formula Grant-Adm (UADM) Natural Resources 81.041 DE-FG48-02R805611 208,378 Weatherization Assistance DCC 81.042 DE-FG48-03R830011-A006 2,240,268 2,004,649 (R&D) Science Financial Assistance Prgm. U OF U * 81.049 VARIOUS 633,775 (R&D) Bed Black Liquor Reformer U OF U * 81.079 DEFG2602NT41490 50,775 8,206 (R&D) Renewable Energy Research & Develop. U OF U * 81.087 VARIOUS 21,293 32,741 Paradox III (UPX3) Natural Resources 81.089 DE-FG48-02R830111 17,153 17,153 (R&D) Fossil Energy Research & Develop. U OF U * 81.089 VARIOUS 200,680 Monticello DOE Environmental Q. 81.092 DE-FG01-89ID12849 49,011 Doe Pump II (UPUM) Natural Resources 81.107 DE-FG26-03NT41901 6,633 (R&D) Reactor Infrastructure and Ed. Support U OF U * 81.114 VARIOUS 70,193 Sep Special Projects (UIT2) Natural Resources 81.119 DE-FC26-03NT15424 8,671 8,630 Sep Special Projects (UWD4) Natural Resources 81.119 DE-FC48-04R821112 10,000 Sep Special Projects (UIT3) Natural Resources 81.119 DE-FC26-02NT15133 12,363 12,363 Sep Special Projects (URB2) Natural Resources 81.119 DE-FC26-04R821115 32,441 32,441 VITRO Environmental Q. 81.502 DE-FC01-99GJ79483 132 Green River DOE Environmental Q. 81.502 DE-FC01-99GJ79483 2,067 (R&D) Department of Energy U OF U * N/A VARIOUS 6,165,183 234,468 (R&D) Department of Energy USU * N/A DE-FC02-04ER54798 (041511) 108,019 (R&D) Sandia National Laboratory USU * N/A VARIOUS 150,703 (R&D) Department of Energy USU * N/A DE-FC07-05ID14670 (041760) 182,654 (R&D) Department of Energy USU * N/A DE-FG48-05R810736 (051650) 196,971 (R&D) Department of Energy USU * N/A VARIOUS 255,801 22,980 Air Monitoring Device Natural Resources N/A VARIOUS (53) Department of Energy U OF U N/A VARIOUS 149,268

Pass-Through From Non-State Entities:(R&D) SOFC Generator —

Versa Power U OF U * 81.069 PID2308086 135,408 (R&D) Conservation Research and Develop. —

Brigham Young University U OF U * 81.086 020097 11,798 Ohio State University U OF U * 81.086 P0RF00905447 53,502

(R&D) Proton Conductors —Clemson University U OF U * 81.087 104975582192095335 138,655

(R&D) Fossil Energy Research & Develop. —New Mexico Institute of Mininig U OF U * 81.089 DSRP20 103,722 University of Kentucky U OF U * 81.089 VARIOUS 274,540 University of North Dakota U OF U * 81.089 567 (6,702) University of Arizona U OF U * 81.089 Y431394 107,824 Virginia Polytech Inst. U OF U * 81.089 VARIOUS 179,858 12,441

(R&D) WNSA —Oregon State University U OF U * 81.114 G0070AG 25,733

(R&D) Active Learning Exercises —Brigham Young University U OF U * 81.116 050143 3,016

* Major Programs, see Note 2.A. The accompanying notes are an integral part of the Schedule of Expenditures of Federal Awards

21

Federal Federal Pass-State Agency Catalog# Award/Contract # Expenditures ThroughGrant Name

State of UtahSchedule of Expenditures of Federal Awards by Federal Agency

For the Year Ended June 30, 2007

(R&D) Research and Development —Battelle Energy Alliance, LLC USU * N/A VARIOUS 15,128 Brigham Young University USU * N/A VARIOUS 78,823 Condfederated Tribes Umatilla Indian Res USU * N/A VARIOUS 16,421 Dynamic Tubular Systems, Inc USU * N/A VARIOUS 30,331 Inland Northwest Research Alliance Inc USU * N/A VARIOUS 85,533 University of Nevada - Reno USU * N/A VARIOUS 80,963

(R&D) Department of Energy —American Iron and Steel Institute U OF U * N/A TRP99530403C 139,431 Automotive Composites Consortium U OF U * N/A 061619 34,364 Battelle Science & Technology U OF U * N/A VARIOUS 139,562 FERMI National Accelerator Labs U OF U * N/A 563065 224 Lawrence Berkely National Lab U OF U * N/A VARIOUS 207,546 Lawrence Livermore National Lab U OF U * N/A VARIOUS 3,895,167 130,679 Los Alamos National Lab U OF U * N/A VARIOUS 113,218 National Renewable Engergy Lab U OF U * N/A XXL54420509 197,371 138,880 Pacific NW National Lab U OF U * N/A 1066518938 10,718 Sandia National Labs U OF U * N/A VARIOUS 32,518 ERIEZ Manufacturing Company U OF U * N/A PID2404100 11,138 Esmerelda Energy Company U OF U * N/A PID2406087 (6,429) ETC Group U OF U * N/A PID2509024 3,343 Golder Associates U OF U * N/A DEFG2602NT154514 1,377 Materials and Systems Research U OF U * N/A VARIOUS 74,722 New Mexico State University U OF U * N/A 707582874H 95,031 Purevision Technology Inc. U OF U * N/A VARIOUS 29,058 Reaction Engineering Int. U OF U * N/A 2404004 56,882 Therochem Recovery International U OF U * N/A 100001540 41,983 US Automotive Materials Partnership U OF U * N/A 061470 89,489 Washington Savannah River Company U OF U * N/A AC493990 255,781 97,625

Waste Isolation Pilot Plant — Western Governors Association Environmental Q. N/A 30-310-0608 114,087 Research and Development —

Inland Northwest Research Alliance Inc. USU N/A VARIOUS 61,156 Department of Energy —

Sandia National Laboratories U OF U N/A VARIOUS 42,868

Subtotal – Department of Energy 18,234,505 3,089,688

ENVIRONMENTAL PROTECTION AGENCY

Air Pollution Control Program Support Weber State 66.001 EP06B000224 15,000 Air Monitoring Network PM 2.5 Environmental Q. 66.006 PM99878902 466,994 Urban Air Toxics Monitoring 103 Environmental Q. 66.034 XA-98871301 45,055 (R&D) SCERP U OF U * 66.034 VARIOUS 442,639 381,905 EPA FFY 07 Underground Injection Control Natural Resources 66.433 GR008426-07 48,440 EPA FFY 06 Underground Injection Control Natural Resources 66.433 GR008426-06 52,031 Biological Data - RGI Environmental Q. 66.436 X7988821-01 30,000 UWCC Headwater Initiative Environmental Q. 66.436 X7978079-01 59,548 Permit Compliance System Environmental Q. 66.436 X7987074-01 79,946 Upper Sevier Watershed Environmental Q. 66.439 WS97850401 23,321 Water Quality Management Planning Environmental Q. 66.454 C6008567-05 39,481 Water Quality Management Planning Environmental Q. 66.454 C6008567-07 68,342 Clean Water Capitalization Grant SRF Environmental Q. 66.458 CS490001-05 148,226 NPS Projects 98 Environmental Q. 66.460 C9998187-98 4,272 NPS Projects 00 Environmental Q. 66.460 C9998187-00 31,191 15,024 NPS Projects 06 Environmental Q. 66.460 C9998187-06 37,344 17,149 NPS Projects 01 Environmental Q. 66.460 C9998187-01 167,323 143,851 NPS Projects 02 Environmental Q. 66.460 C9998187-02 179,464 139,452 NPS Projects 05 Environmental Q. 66.460 C9998187-05 259,719 71,916 NPS Projects 04 Environmental Q. 66.460 C9998187-94 415,494 340,753 NPS Projects 03 Environmental Q. 66.460 C9998187-03 473,221 47,429

* Major Programs, see Note 2.A. The accompanying notes are an integral part of the Schedule of Expenditures of Federal Awards

22

Federal Federal Pass-State Agency Catalog# Award/Contract # Expenditures ThroughGrant Name

State of UtahSchedule of Expenditures of Federal Awards by Federal Agency

For the Year Ended June 30, 2007