12

CAC.5050 (08.16) Protective ProPayer ® Income Annuity Single Premium Immediate Annuity Overview

CAC.5050 (08.16)

Protective ProPayer® Income AnnuitySingle Premium Immediate Annuity Overview

www.protective.com

Protective and Protective Life refer to Protective Life Insurance Company (PLICO) and its affiliates, including Protective Life & Annuity Insurance Company (PLAICO). Annuities are issued by PLICO in all states except New York and in New York by PLAICO. Both companies are located in Birmingham, AL. Each company is solely responsible for the financial obligations accruing under the products it issues. Product guarantees are backed by the financial strength and claims paying ability of the issuing company.

Single premium immediate annuity contracts issued under policy form series IPD-2112 (PLICO) and AF-2112 (PLAICO). Policy form numbers, product availability and product features may vary by state.

CAC.5050 (08.16)

Protect Tomorrow. Embrace Today.TM

No matter how you intend to experience your retirement,

you will essentially need to fund a comfortable lifestyle

and protect your loved ones. You’ll also need income for

as long as you live. Proper planning and perseverance

are key, especially as you navigate the market’s ups and

downs and anticipate rising inflation. It’s important to

have adequate flexibility to structure your retirement

cash flow.

An immediate annuity provides the assurance of a

series of payments guaranteed to last for as long as you

choose—even for as long as you live. The information

contained in this brochure, along with the guidance of

your financial professional, can help you learn more

about how an immediate annuity may be used as part of

a customized financial strategy to protect your financial

goals for tomorrow so that you can embrace today.

1

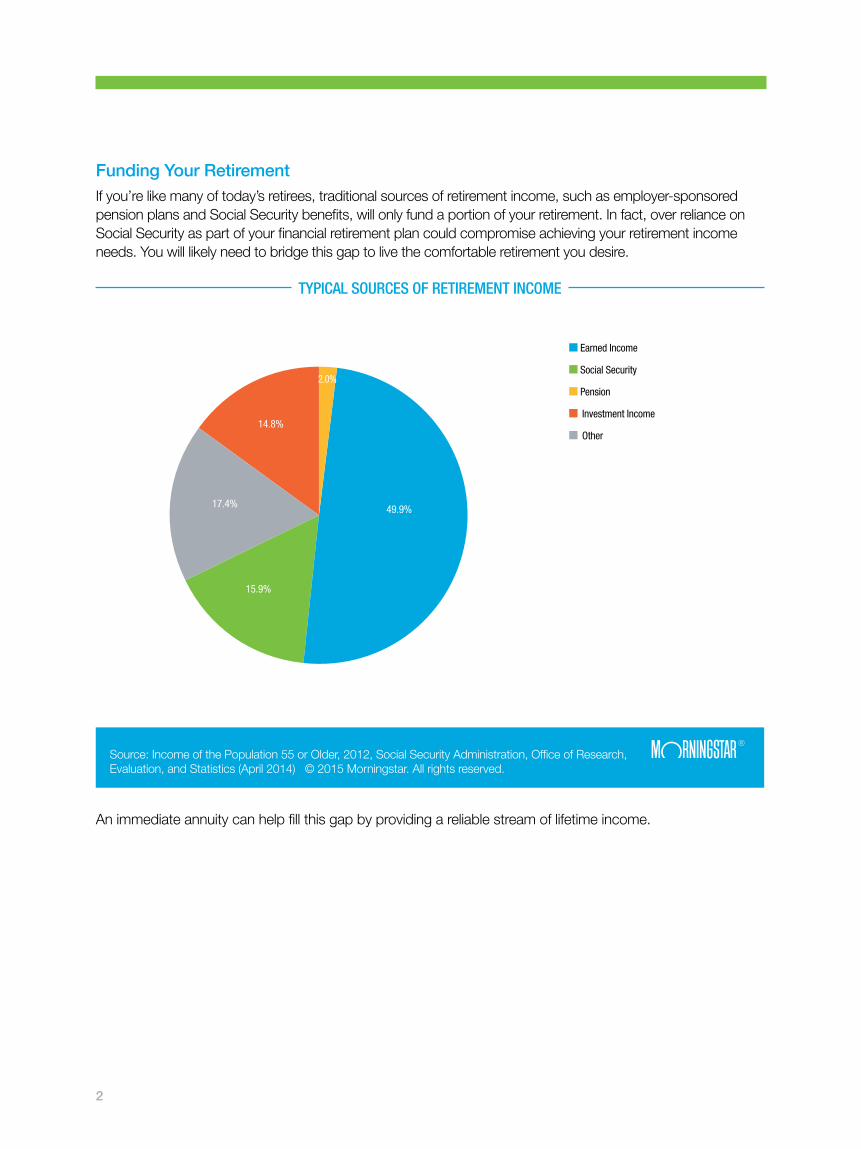

Funding Your RetirementIf you’re like many of today’s retirees, traditional sources of retirement income, such as employer-sponsored pension plans and Social Security benefits, will only fund a portion of your retirement. In fact, over reliance on Social Security as part of your financial retirement plan could compromise achieving your retirement income needs. You will likely need to bridge this gap to live the comfortable retirement you desire.

An immediate annuity can help fill this gap by providing a reliable stream of lifetime income.

TYPICAL SOURCES OF RETIREMENT INCOME

Source: Income of the Population 55 or Older, 2012, Social Security Administration, Office of Research, Evaluation, and Statistics (April 2014) © 2015 Morningstar. All rights reserved.

n Earned Income

n Social Security

n Pension

n Investment Income

n Other

Sources of Retirement Income

Source: Income of the Population 55 or Older, 2012, Social Security Administration, Office of Research, Evaluation, and Statistics (April 2014)

• Earned income• Social Security• Pension• Investment income• Other

15.9%

17.7%

14.8%

2.0%

49.9%

© 2015 Morningstar. All rights reserved.

49.9%

15.9%

17.4%

14.8%

2.0%

2

What is an Immediate Annuity?In simple terms, an immediate annuity is a contract between you and a life insurance company and is intended to help replace income during retirement. You purchase an immediate annuity contract by making a single payment to the insurance company, after which you receive an immediate and continuing stream of annuity income payments for a duration tailored to meet your specific needs. The amount of your payment is based on how much you invest in the annuity and your calculated life expectancy. Generally, your health status is not a consideration.

There are certainly many alternatives to an immediate annuity that may offer higher rates of return—along with higher elements of risk. Unlike most equity investments, however, the value of immediate fixed annuities does not move with the ups and downs of the market. Furthermore, even the most conservative fixed interest investments do not ensure a stream of payments that will last your lifetime.

3

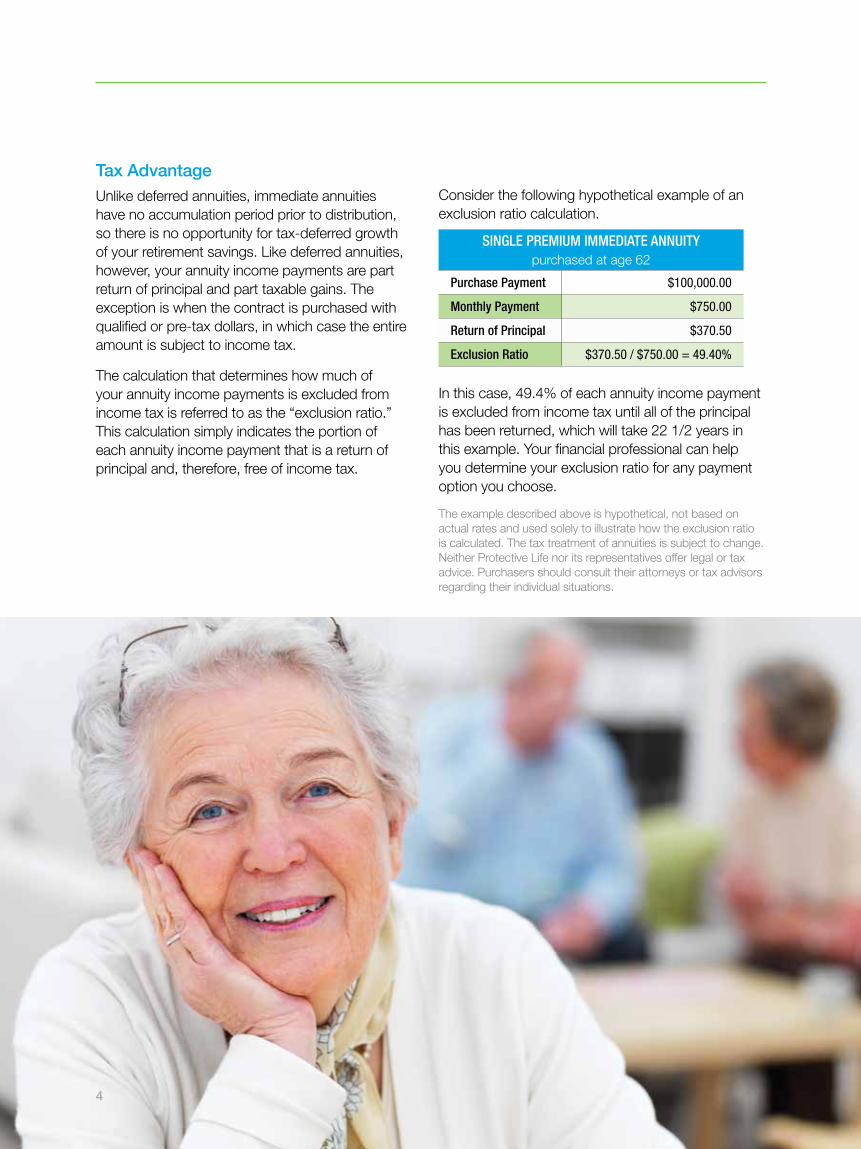

Tax AdvantageUnlike deferred annuities, immediate annuities have no accumulation period prior to distribution, so there is no opportunity for tax-deferred growth of your retirement savings. Like deferred annuities, however, your annuity income payments are part return of principal and part taxable gains. The exception is when the contract is purchased with qualified or pre-tax dollars, in which case the entire amount is subject to income tax.

The calculation that determines how much of your annuity income payments is excluded from income tax is referred to as the “exclusion ratio.” This calculation simply indicates the portion of each annuity income payment that is a return of principal and, therefore, free of income tax.

SINGLE PREMIUM IMMEDIATE ANNUITY purchased at age 62

Purchase Payment $100,000.00

Monthly Payment $750.00

Return of Principal $370.50

Exclusion Ratio $370.50 / $750.00 = 49.40%

Consider the following hypothetical example of an exclusion ratio calculation.

In this case, 49.4% of each annuity income payment is excluded from income tax until all of the principal has been returned, which will take 22 1/2 years in this example. Your financial professional can help you determine your exclusion ratio for any payment option you choose.

The example described above is hypothetical, not based on actual rates and used solely to illustrate how the exclusion ratio is calculated. The tax treatment of annuities is subject to change. Neither Protective Life nor its representatives offer legal or tax advice. Purchasers should consult their attorneys or tax advisors regarding their individual situations.

4

Designing Your Retirement IncomeThe primary benefit of using an immediate annuity as part of your retirement strategy is creating a reliable stream of payments. Available annuity income payment options vary by insurance company and product type. In general, your options will include the following, and the descriptions assume you are the owner and annuitant.

• Payments for a Certain Period: Payments are made for a certain number of years. When this period has ended, all payments stop. Should you die during the specified period, your beneficiary will receive the remaining payments.

• Payments for Life with Certain Period: Payments are made for a certain number of years or for your lifetime, whichever is longer. If you die during the specified period, the remaining payments are made to your beneficiary.

• Payments for Life with an Installment Refund: Payments are made for as long as you live. Should you die before your entire investment has been paid out, payments will continue to your beneficiary until the full purchase amount has been paid out.

• Payments for Life with a Cash Refund: Payments are made for as long as you live. Should you die before your entire investment has been paid out, the remaining balance is paid out in a lump sum to your beneficiary.

Most annuity issuers also offer options to base payments on two lives. This can include:

• Joint and Survivor Payments for Life with Certain Period: Payments are made for a certain number of years, or for the lifetimes of you and your joint annuitant, whichever is longer. If one of the annuitants dies before the certain period has ended, payments will continue to the other for the remainder of the certain period. Depending on the particular annuity contract, payments may be reduced upon the death of the first annuitant or at the end of the certain period. These payments will continue until the death of the second annuitant.

For non-qualified annuities, a portion of each annuity payment generally is considered to be a return of your investment, which is not taxed. The remaining portion of the payment consists of earnings and is taxable as ordinary income. After you have recovered your investment, all of your annuity payments will be taxable.

Access to Your MoneyMost immediate annuity contracts do not offer any liquidity or “surrender value.” This means that with these contracts, you will be limited to receiving payments only as provided under the annuity income payment schedule you choose at the time of your annuity purchase.

In recent years, some insurance companies have developed new annuity products and features that do provide for liquidity in certain situations. Your financial professional can tell you more about these products and help you select an immediate annuity contract that is appropriate for your needs.

Mitigate InflationSome insurance companies offer payment options that provide automatic increases in payment amounts. These increases may be a fixed percentage (e.g., +3% each year) or may be tied to an outside index, such as the Consumer Price Index. Features like this vary greatly, so ask your financial professional for more information about products that may provide increasing payment options to help mitigate the effects of inflation.

5

We are Protective LifeWhen you purchase a single premium immediate annuity for retirement, you begin a long-standing relationship with the issuing life insurance company. For more than 100 years, our mission has remained boldly alive in our name. We are Protective Life.

Our mission is to help customers find the financial security they so desperately need, enabling them to protect tomorrow and embrace today. It’s a liberating feeling – one experienced when focus is allowed to return to those things that enrich our lives the most.

At the heart of our Company’s business philosophy are four adopted values. Each equally shapes our identity and guides us in all that we do.

Do the Right Thing: Character is doing the right thing, even when no one is looking. We have a collective responsibility to do what’s right by our customers to ensure their financial needs are met today and tomorrow.

Serve People: To help our customers protect tomorrow and embrace today, we must put their financial needs first and take the time to truly understand the challenges they face in life.

Build Trust: Hard won but easily lost, earning the trust of our customers is just as imperative as keeping it for a lifetime. Do the right thing and serve people, and do it with sincerity and transparency.

Simplify Everything: From product design to choice and delivery to service support, our goal is to make doing business easier by making it as simple as possible. We educate customers using relatable concepts and terms to address their specific financial needs. It’s our belief that an informed customer is an empowered one.

1907 Governor William Dorsey Jelks founds Protective Life Insurance Company, as Theodore Roosevelt begins his seventh year as U.S. President.

1909 Protective Life pays its first death claim.

1932 Protective Life celebrates its Silver Anniversary, with over $65 million of insurance in force.

1957 Protective Life celebrates 50 years, with insurance in force approaching $1 billion.

1983 Acquires Protective Life and Annuity Insurance Company.

1997 West Coast Life is acquired, solidifying Protective’s national presence.

2002 John D. Johns becomes CEO of Protective Life.

2006 Chase Insurance Group is acquired, representing Protective’s largest acquisition to date.

2007 Protective Life celebrates its 100th Anniversary. Insurance in force surpasses $252 billion.

2009 Protective achieves record consolidated statutory capital level in a historically challenging financial environment.

2011 The combined United Investors Life and Liberty Life acquisitions increase policies in force by 50%.

2013 Protective Life completes the acquisition of MONY Life Insurance Company.

2015 Protective Life is acquired by The Dai-ichi Life Insurance Company, Limited, becoming part of the 13th largest global life insurer in terms of total assets.*

*based on financials as of 12/31/13.

6

The Strength of Our PromiseWe take comfort in our strengths. We rely on more than a century’s worth of experience to fulfill the obligations and uphold the promises made to our customers. The strength of our promise is backed by the financial stability and long-term performance of our Company. Protective Life carries high ratings from independent rating organizations who assign ratings measuring financial strength or claims-paying abilities. They consider factors such as overall operating performance, asset quality, financial flexibility, and capitalization.

Our tradition of financial strength and strong growth has allowed us to touch so many lives and help protect tomorrow. We continually strive to provide innovative, valuable, affordable products that are simple to understand and easy to acquire. We serve with integrity and honesty, treating each of our customers the way we would like to be treated.

We offer more than just products. We offer solutions—solutions to help meet the many financial challenges we all face in life. Simplified products, valuable educational resources and over 100 years of service experience empower our customers to take charge of their lives and embrace all that the day has to offer.

PROTECTIVE LIFE HAS INSURER FINANCIAL STRENGTH RATINGS

A+ (Superior, 2nd highest of 15 ratings) from A.M. Best

AA- (Very Strong, 4th highest of 21 ratings) from Standard & Poor’s

A+ (Strong, 5th highest of 22 ratings) from Fitch

Ratings do not reflect the investment experience or financial strength of any sub account. These ratings are current as of August 1, 2016, are subject to change and do not apply to products or their performance. Please visit www.protective.com for more current information.

7

Protect Tomorrow. Embrace Today.TM

As you prepare for your retirement, it’s important

to ensure that you have the options needed to

customize a personal financial plan and meet your

individual needs—along with assurance that the

companies you work with will be there to see you

through your entire retirement. Talk to your financial

professional today to learn more about how you

can utilize a Protective Life immediate annuity to

tailor your unique retirement solution.

8

CAC.5050 (08.16)

Protective ProPayer® Income AnnuitySingle Premium Immediate Annuity Overview

www.protective.com

Protective and Protective Life refer to Protective Life Insurance Company (PLICO) and its affiliates, including Protective Life & Annuity Insurance Company (PLAICO). Annuities are issued by PLICO in all states except New York and in New York by PLAICO. Both companies are located in Birmingham, AL. Each company is solely responsible for the financial obligations accruing under the products it issues. Product guarantees are backed by the financial strength and claims paying ability of the issuing company.

Single premium immediate annuity contracts issued under policy form series IPD-2112 (PLICO) and AF-2112 (PLAICO). Policy form numbers, product availability and product features may vary by state.

CAC.5050 (08.16)