25

NIMISHA AGARWAL 2013173 CREDIT RISK ANALYSIS- A CASE STUDY APPROACH

| Date post: | 19-Aug-2015 |

| Category: |

Documents |

| Upload: | nimisha-agarwal |

| View: | 104 times |

| Download: | 0 times |

NIMISHA AGARWAL2013173

CREDIT RISK ANALYSIS- A CASE STUDY APPROACH

INTRODUCTION

Established in 1985Indian bank and financial service firm

BASEL II

THREE PILLARS

MINIMUM CAPITAL

REQUIREMENTS

• Credit risk • Operational

risk• Market risk

SUPERVISORY REVIEW

• Principles of internal control• Corporate governance practices• Risk

management framework

MARKET DISCIPLINE

• Capital adequacy• Risk

assessment methods• Promote

stability in the financial system

CREDIT APPRAISAL

While appraising a borrower, the following questions need to be answered:

Is the borrower credit worthy?What should be the overall exposure to the borrower?Whether the borrower should be extended short term

facilities or long term facilities based on his requirement?

What security or other credit enhancement measures should be stipulated to safeguard our facilities in case of default?

What should be the key monitor able parameters to identify any deterioration in credit profile of the borrower subsequent to our disbursement?

LEGAL DOCUMENTS

Application/ request letter for the facilityAccepted sanction letterConstitutional documentsMaster facility agreement and the relevant

product schedulesDemand Promissory Note (DPN)Letter of continuing securityFacility/ product specific documents

CREDIT RISK

The inability or unwillingness of a borrower to repay his liability on due date

Lack of churn in the working capital account for a period of more than 90 days or shortfall in drawing power or occurrence of events of default as per contractual terms.

CREDIT RISK ASSESSMENT

INDUSTRY RISK

FINANCIAL RISK

BUSINESS RISK

MANAGEMENT RISK

CASE STUDY

Name of the Company: Prestige Industries Limited (PILT)

Group: Amba GroupLocation: New DelhiYear of incorporation: 1945Constitution: Public Limited CompanyIndustry & Activity: Paper & wood

(Manufacturer of paper & paper products)Banking Arrangement: Multiple Banking

ArrangementProposal for: Renewal of credit facilities

ABOUT THE COMPANY

Operates in five segments: Coated wood free paper Uncoated hi-bright paper(maplitho) Business stationary Copier paper and specially fine paper Rayon grade pulp3 manufacturing facilities at Haryana, Orissa and

MaharashtraAcquisition of SFI, Malaysia in 2007 i.e. First

overseas acquisition by an Indian paper company

BUSINESS MODEL

RISKSIndustry outlook is

weak High input costsDeclining profitability

of the rayon grade pulp segment

High group leverage and impacted profitability of the major group companies

STRENGTHSBrand Retail: Market

leader in Indian writing and printing paper industry

Wide distribution network

Geographic diversification

FINANCIAL STATEMENT

Microsoft Office Excel 97-2003 Worksheet

CREDIT RISK ASSESSEMENT

INDUSTRY RISK

In 2012, Raw material price increases partly driven by rupee depreciation

Pricing pressures due to low demand and excess capacity

As per industry estimates, the domestic demand growth slowed down to about 4% in 2012 from 6% in 2011

Increase in power costs due to erratic domestic coal supplies

Significant borrowings for capex to keep credit metrics stretched

BUSINESS RISK

Market leader in writing and printing paperRestructuring in manufacturing assets Merging CPPs of Amba group in PILT and PGPPLThree basic risk: a) Digitisation but penetration rate in primary

markets of PILT is lowb) Production based on wood and risk of

unavailability of right raw material due to depletion of forest resources

c) Expanded capacity (30-40%) builds pressure to penetrate markets with products in order to absorb over supply

FINANCIAL RISK

Turnover stagnant over the last 2-3 years. PBDIT margin fell due to high power cost Profitability expected to improve due to incoming of

more profitable AP unitTNW fell due to dividend payment from reservesRequired to pay Rs. 115 crores to PGPPL and Rs.17

crores to APIL. Group debt of Rs. 16753 crores as per info availableHigh capital expenditure lead to negative impact on

free operating cash flowsLow repayment capacity depicted by Total debt/ Cash

Profit of 7.71 as on June 30, 2012. DSCR below 1.

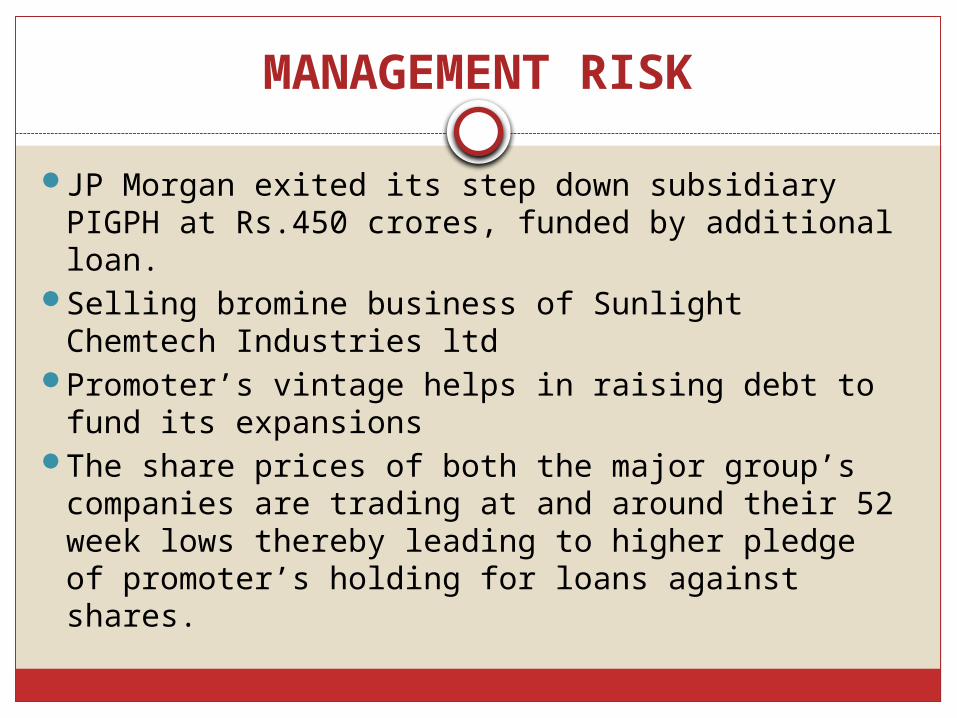

MANAGEMENT RISK

JP Morgan exited its step down subsidiary PIGPH at Rs.450 crores, funded by additional loan.

Selling bromine business of Sunlight Chemtech Industries ltd

Promoter’s vintage helps in raising debt to fund its expansions

The share prices of both the major group’s companies are trading at and around their 52 week lows thereby leading to higher pledge of promoter’s holding for loans against shares.

FACILITIES ASSESSMENT

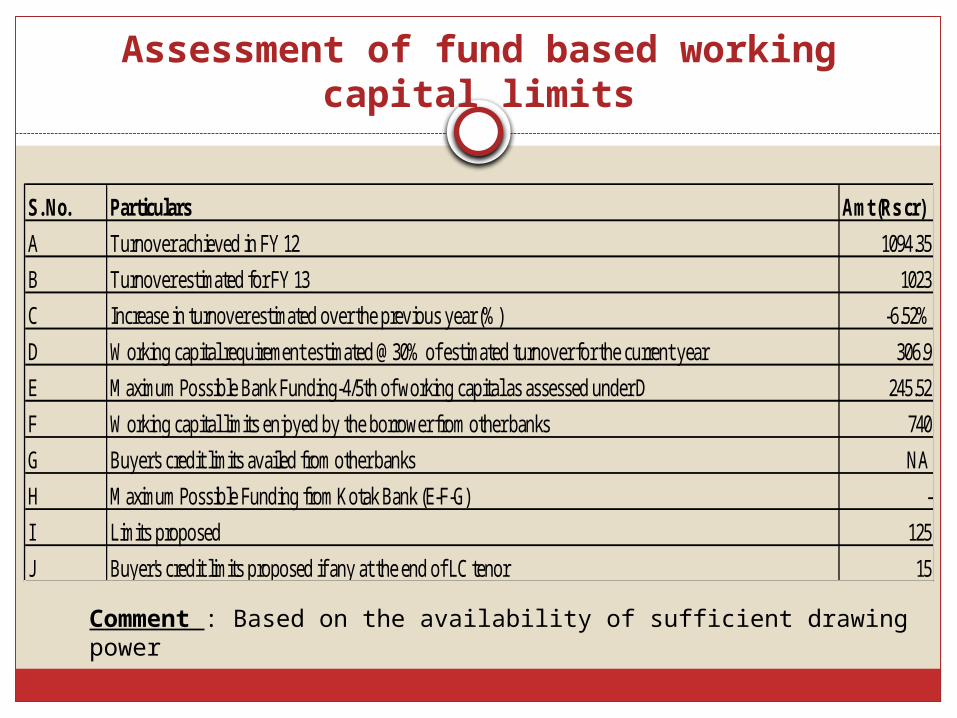

Assessment of fund based working capital limits

S. No. Particulars Amt (Rs cr)

A Turnover achieved in FY 12 1094.35

B Turnover estimated for FY 13 1023

C Increase in turnover estimated over the previous year (%) -6.52%

D Working capital requirement estimated @30% of estimated turnover for the current year 306.9

E Maximum Possible Bank Funding-4/5th of working capital as assessed under D 245.52

F Working capital limits enjoyed by the borrower from other banks 740

G Buyer's credit limits availed from other banks NA

H Maximum Possible Funding from Kotak Bank (E-F-G) -

I Limits proposed 125

J Buyer's credit limits proposed if any at the end of LC tenor 15

Comment : Based on the availability of sufficient drawing power

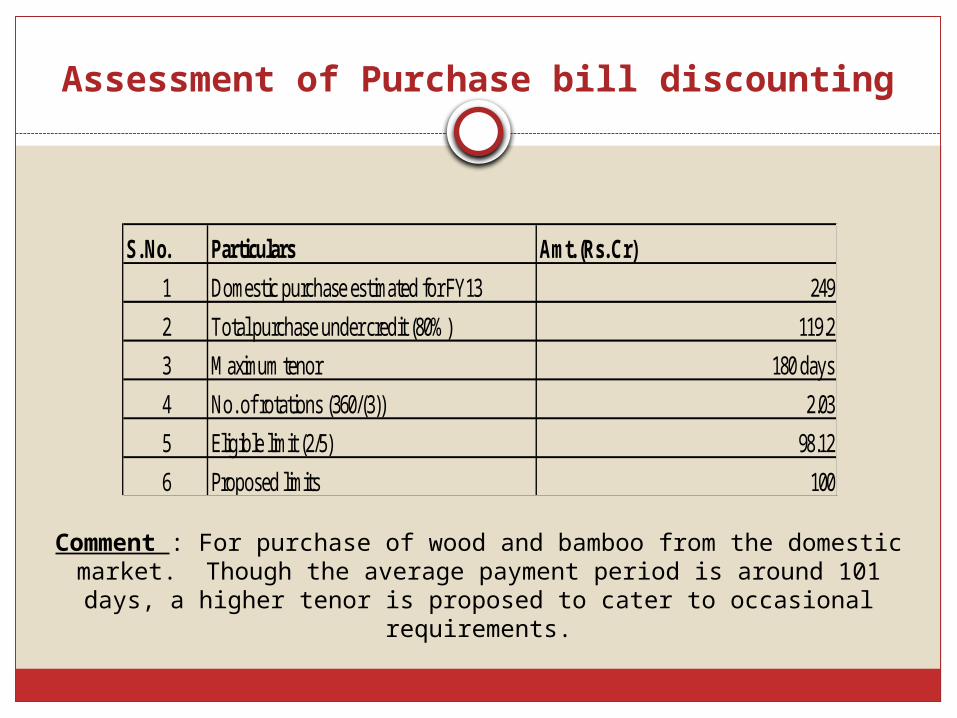

Assessment of Purchase bill discounting

S. No. Particulars Amt. (Rs. Cr)

1 Domestic purchase estimated for FY13 249

2 Total purchase under credit (80%) 119.2

3 Maximum tenor 180 days

4 No. of rotations (360/(3)) 2.03

5 Eligible limit (2/5) 98.12

6 Proposed limits 100

Comment : For purchase of wood and bamboo from the domestic market. Though the average payment period is around 101 days, a

higher tenor is proposed to cater to occasional requirements.

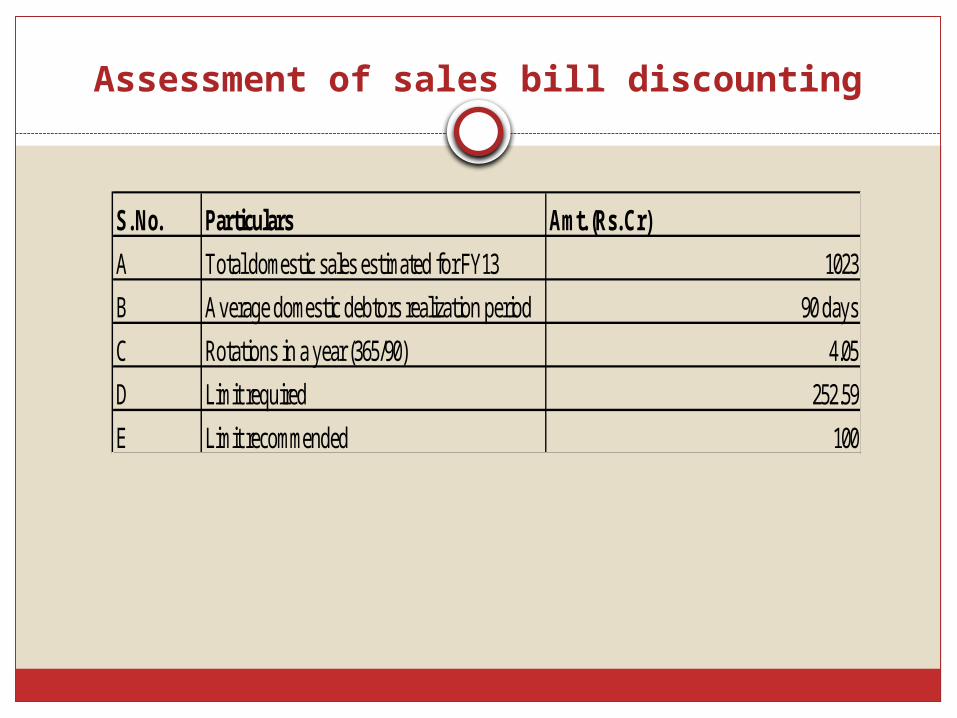

Assessment of sales bill discounting

S. No. Particulars Amt. (Rs. Cr)

A Total domestic sales estimated for FY13 1023

B Average domestic debtors realization period 90 days

C Rotations in a year (365/90) 4.05

D Limit required 252.59

E Limit recommended 100

Assessment of Non Fund based facilities

Letter of Credit Forex

S. No. Particulars Amt(Rs. Cr)

1 Imports estimated for FY13 53.06

2 Maximum usance period 180 days

3 Average Lead Time 30 days

4 No. of rotations (365/(2+3)) 1.74

5 Eligible limit (1/4) 30.49

6 Proposed limits (renewal) 15

S. No. Particulars Amt(Rs. Cr)

1 Imports projected for FY13 50

2 Forex loan as on 30.06.12 111.21

3 Total 161.21

4 LEV 15%5 Eligible limit (3*4) 24.18

6 Proposed limits- renewal 5

ACCOUNT MONITORING

PBDIT/ Net sales shall be at a minimum of 16% verifiable at quarterly intervals

Reduction of shareholding of promoter group below 30%. The same should be verified annual intervals

TOL/TNW not to exceed 2 times. The ratio be checked at annual intervals

SECURITY/ COMFORTS

Post dated cheque for disbursed WCDL/ STL and PBD facility (beyond Rs.25 cr). UDC for OD and disputed BG.

RECOMMENDATIONS

Integration of pulp within house mills coming up in MFI and Maharashtra unit, the consolidated profitability is expected to improve in the coming years.

Renewal of the existing facilities in view of the promoter’s vintage

Satisfactory account conduct with the bank (group relationship since 2004)

FB facilities are disbursed based on the company’s DP availability

Submission of quarterly stock statement