62

Skanska Commercial Property Development Stockholm New, Sweden

Skanska Commercial Property Development

Stockholm New, Sweden

Agenda

Time Subject Speaker

08:30-09:00 Commercial Property Development in the Group Claes Larsson

09:00-10:00Commercial Development Nordic

Commercial Development Europe

Jan Odelstam

Nicklas Lindberg

10:00-10:30 Commercial Development USA Mats Johansson

10:30-11:00 Break

11:00-11:30 LeasingArkadiusz Rudzki

Caroline Arehult

11:30-12:00 TransactionsFredrik Bergenstråhle

Adrian Karczewicz

12:00-12:30 Q&A and info regarding site visit

12:30-13:15 Lunch

13:15-13:45 Transportation to site visit

13:45-15:15 Presentation of Stockholm New and site visitMarkus Dangré

Daniel Dahlqvist

Ca 15:30-16:00 Transportation back to Skanska HQ

2

Stockholm New, Sweden

Skanska Commercial Property Development

Claes LarssonExecutive Vice President

3

4

Agenda

1) Background/history/overview

2) Value creation

3) Financial performance

and allocation

4) The future

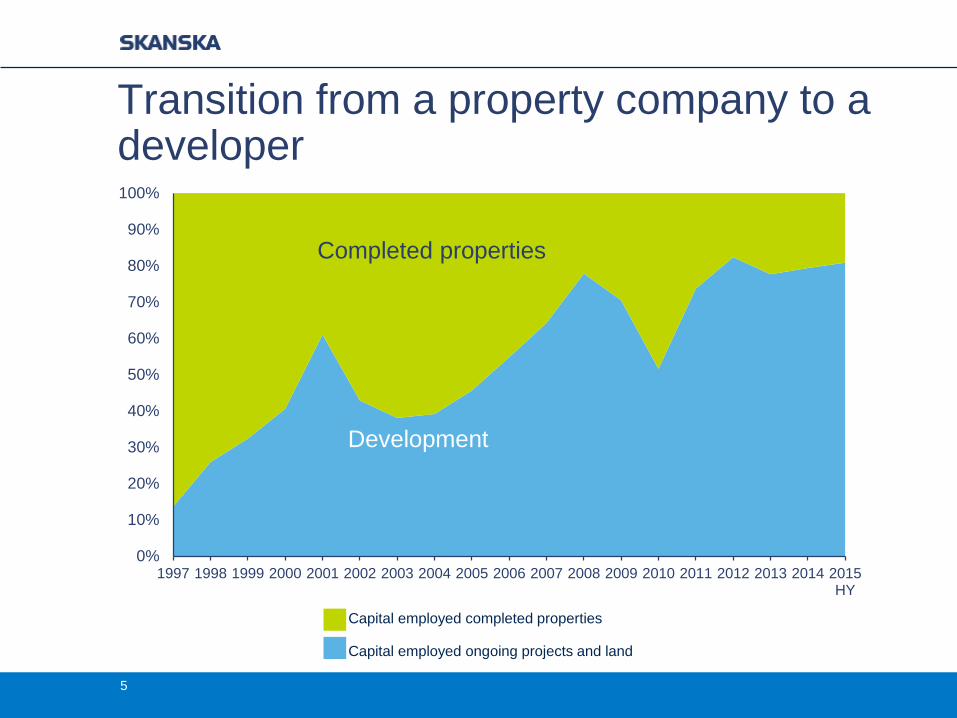

Transition from a property company to a developer

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

1997 1998 1999 2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015HY

Development

Completed properties

Capital employed completed properties

Capital employed ongoing projects and land

5

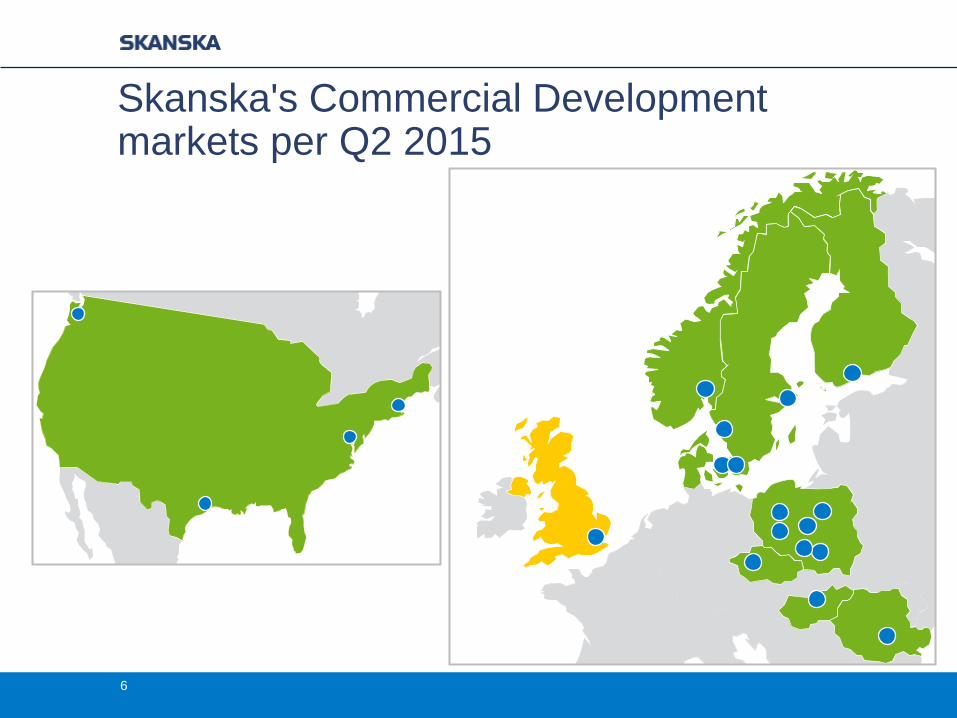

Skanska's Commercial Development markets per Q2 2015

6

Products

− Office

− In selected markets

− Retail

− Rental residential

− Industrials

7

8

Agenda

1) Background/history/overview

2) Value creation

‒ The value chain

‒ Key functions

‒ Risk management

3) Financial performance

and allocation

4) The future

Complete value chain

9

Permitting

Planning

Design

Investment in

land bank

Project

idea

Leasing

Construction

Property Mgmt

Exit

Key functions in house

10

Property management Property transactions

Leasing Project management

Risks

− Zoning risks

− Permit risks

− Construction cost risks

− Leasing risks

− Exit risks

Risk exposure:

Full investment

Risk exposure: Land investment

11

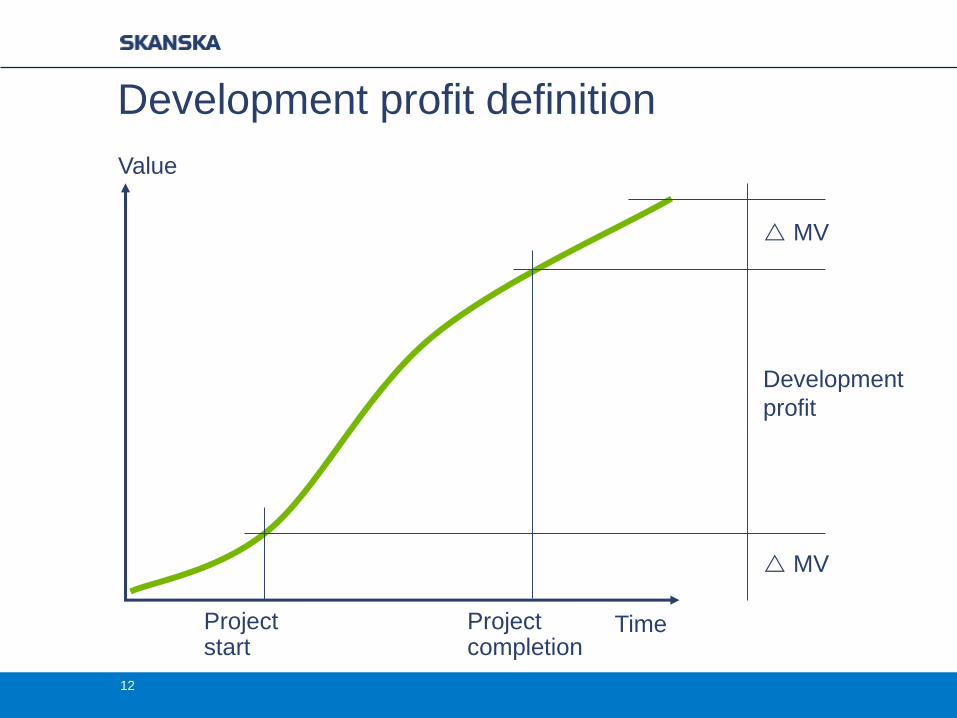

Development profit definition

MV

MV

Development

profit

Value

TimeProject start

Project completion

12

13

Agenda

1) Background/history/overview

2) Value creation

3) Financial performance

and allocation

4) The future

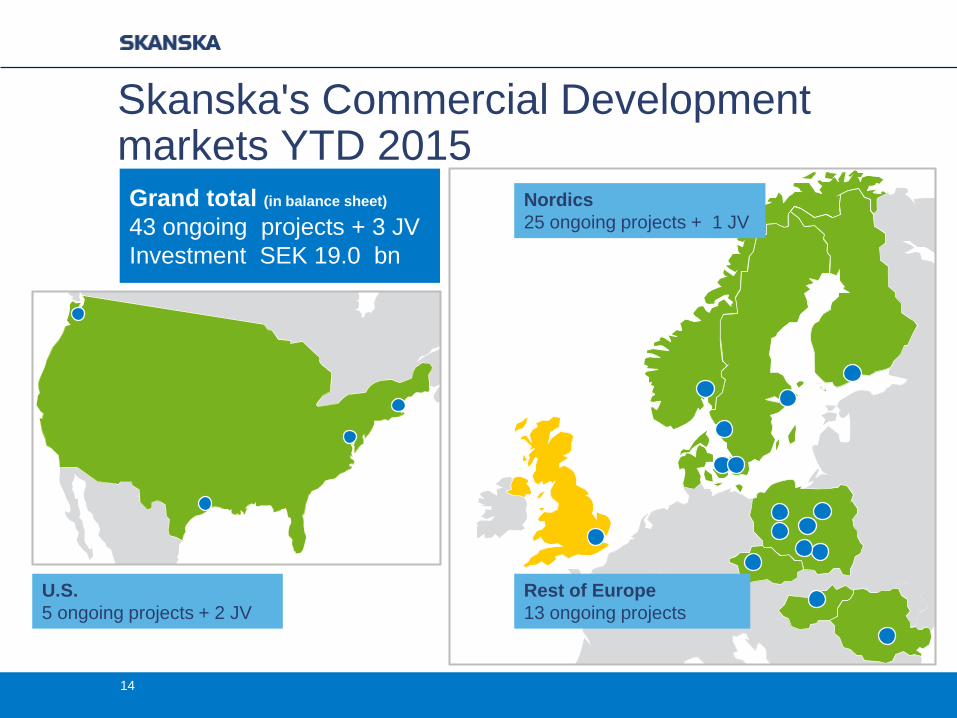

Grand total (in balance sheet)

43 ongoing projects + 3 JV

Investment SEK 19.0 bn

Skanska's Commercial Development markets YTD 2015

14

U.S.

5 ongoing projects + 2 JV

Nordics

25 ongoing projects + 1 JV

Rest of Europe

13 ongoing projects

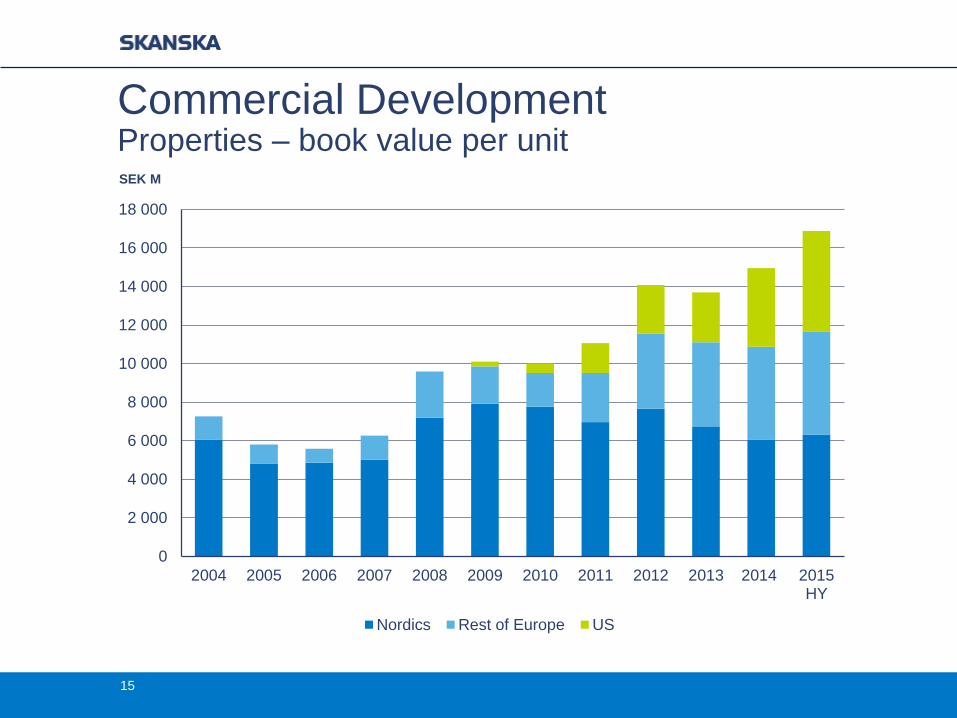

Commercial DevelopmentProperties – book value per unit

0

2 000

4 000

6 000

8 000

10 000

12 000

14 000

16 000

18 000

2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015HY

Nordics Rest of Europe US

15

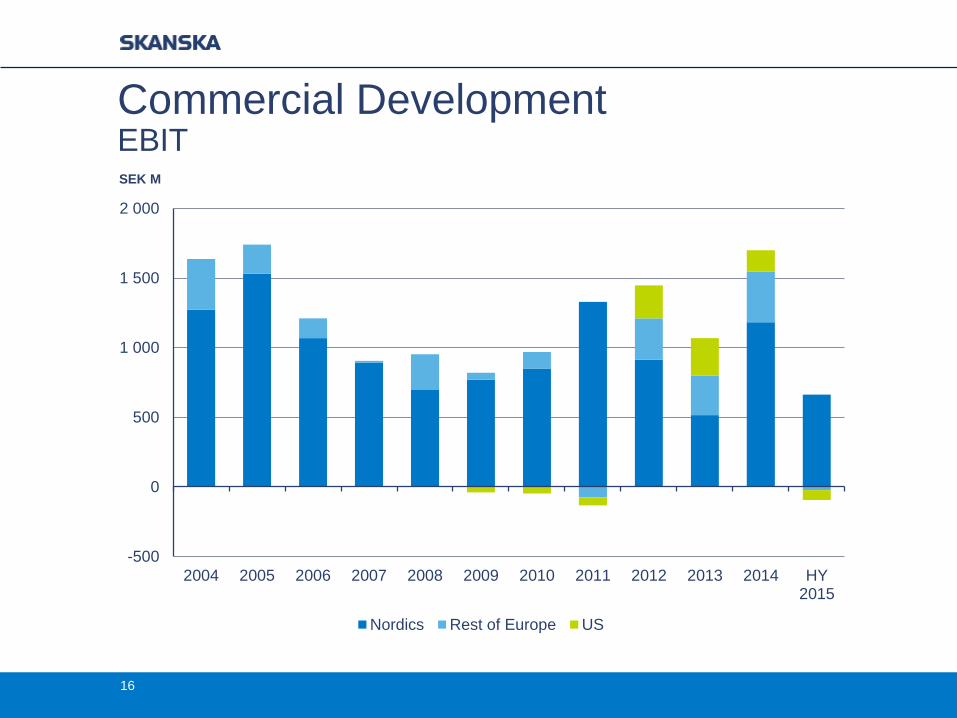

SEK M

Commercial Development EBIT

-500

0

500

1 000

1 500

2 000

2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 HY2015

Nordics Rest of Europe US

16

SEK M

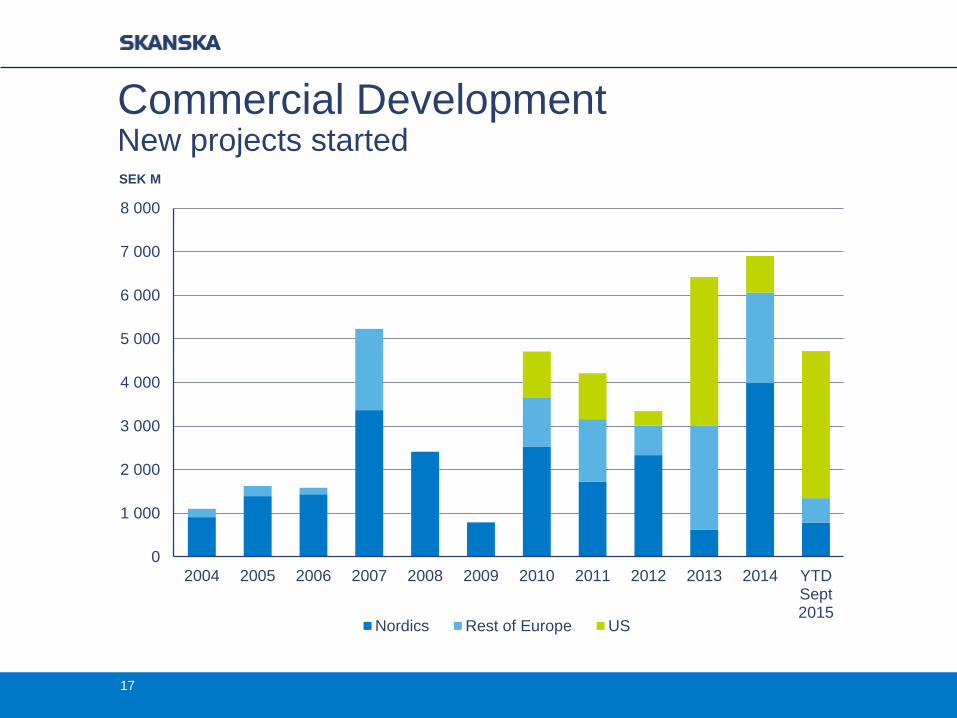

Commercial DevelopmentNew projects started

0

1 000

2 000

3 000

4 000

5 000

6 000

7 000

8 000

2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 YTDSept2015

Nordics Rest of Europe US

17

SEK M

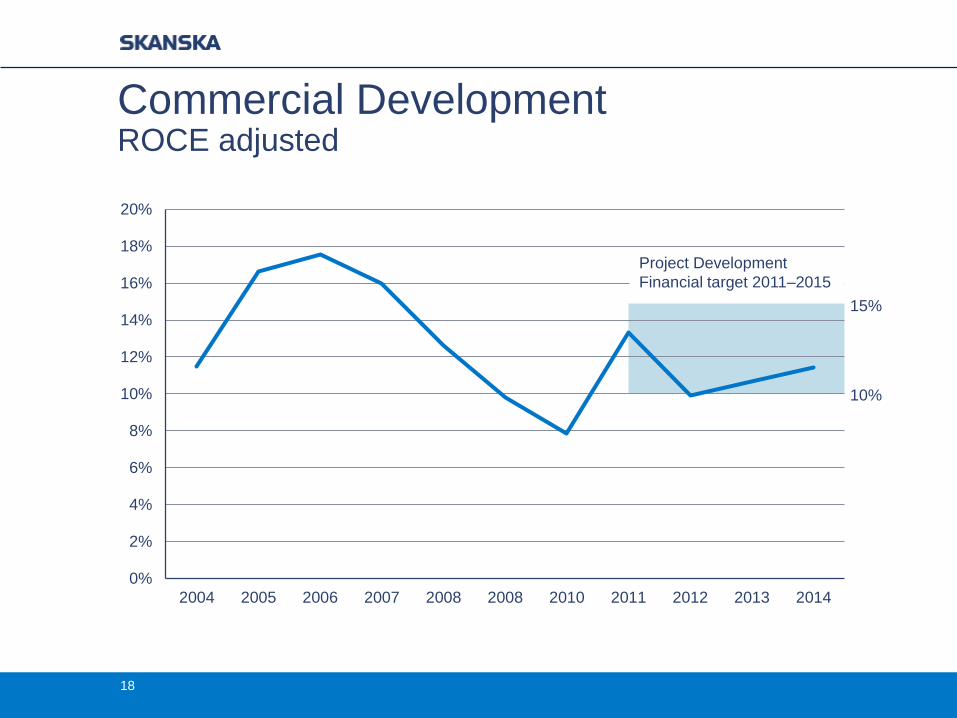

Commercial Development ROCE adjusted

0%

2%

4%

6%

8%

10%

12%

14%

16%

18%

20%

2004 2005 2006 2007 2008 2008 2010 2011 2012 2013 2014

15%

10%

18

Project Development

Financial target 2011–2015

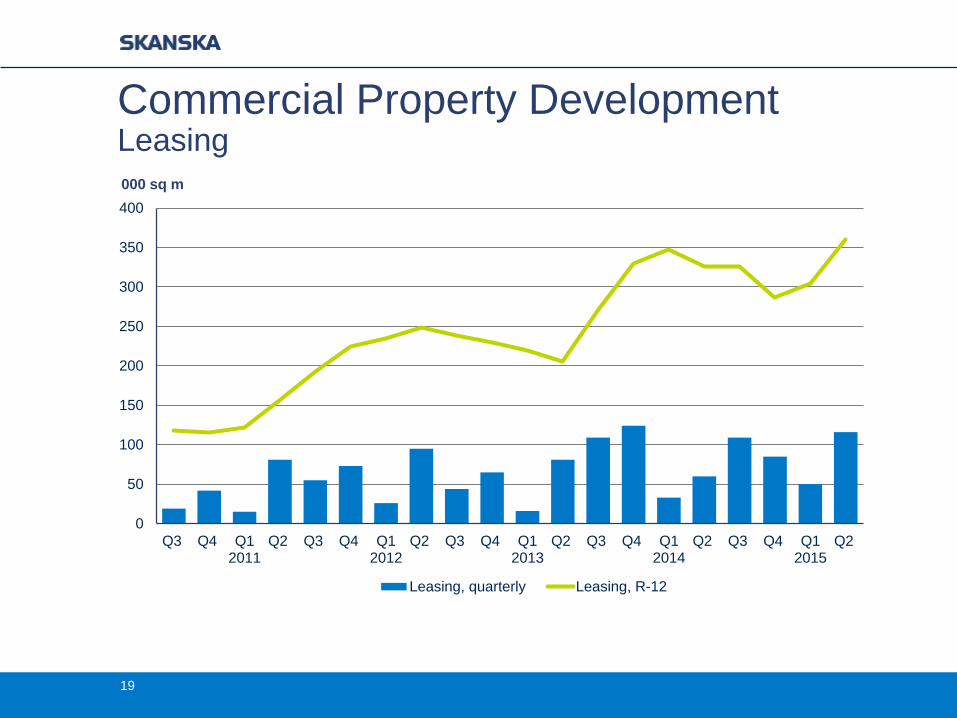

0

50

100

150

200

250

300

350

400

Q3 Q4 Q12011

Q2 Q3 Q4 Q12012

Q2 Q3 Q4 Q12013

Q2 Q3 Q4 Q12014

Q2 Q3 Q4 Q12015

Q2

Leasing, quarterly Leasing, R-12

000 sq m

Commercial Property Development Leasing

19

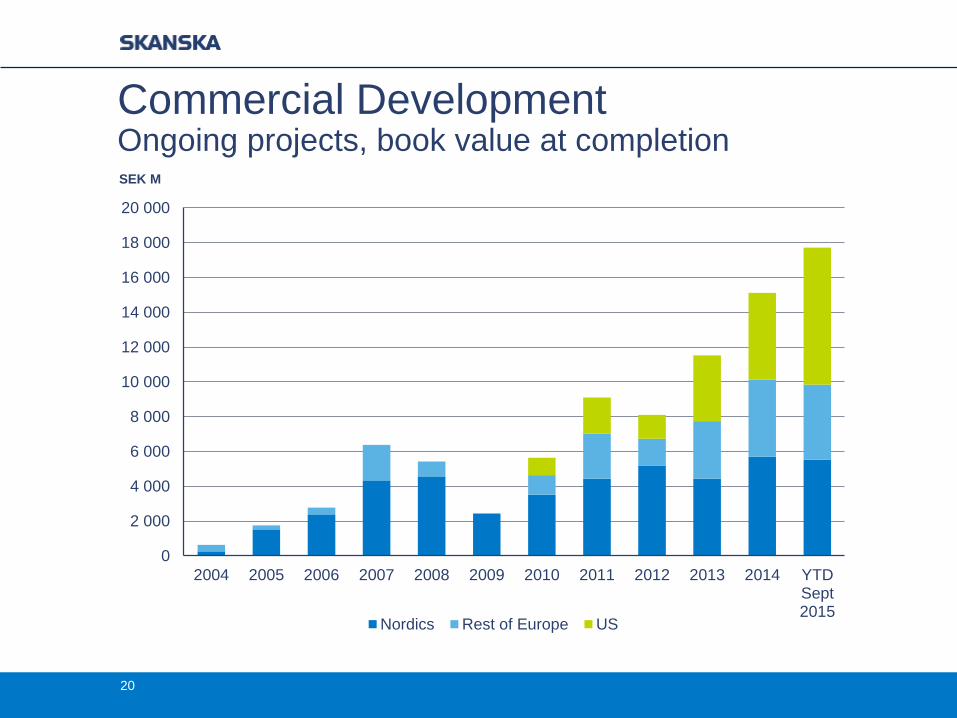

Commercial DevelopmentOngoing projects, book value at completion

0

2 000

4 000

6 000

8 000

10 000

12 000

14 000

16 000

18 000

20 000

2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 YTDSept2015

Nordics Rest of Europe US

20

SEK M

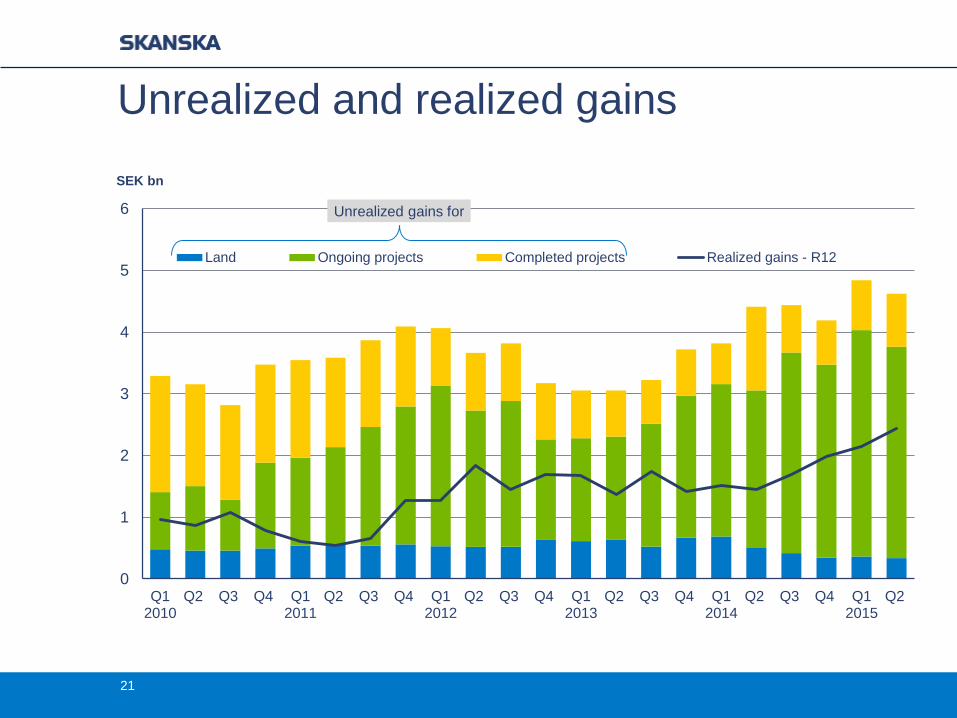

Unrealized and realized gains

21

0

1

2

3

4

5

6

Q12010

Q2 Q3 Q4 Q12011

Q2 Q3 Q4 Q12012

Q2 Q3 Q4 Q12013

Q2 Q3 Q4 Q12014

Q2 Q3 Q4 Q12015

Q2

Land Ongoing projects Completed projects Realized gains - R12

SEK bn

Unrealized gains for

Timing is crucial

22

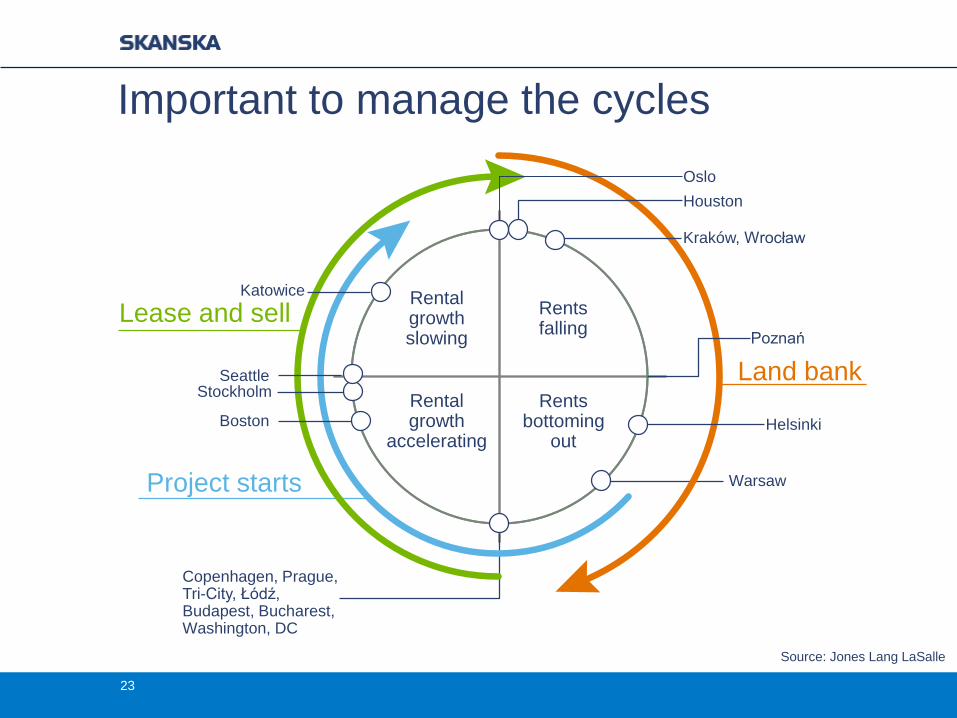

Important to manage the cycles

Rentsfalling

Rental growth slowing

Rentsbottoming

out

Rentalgrowth

accelerating

Source: Jones Lang LaSalle

Katowice

Warsaw

Copenhagen, Prague, Tri-City, Łódź, Budapest, Bucharest, Washington, DC

Project starts

Lease and sell

Land bank

Helsinki

Seattle

Boston

Houston

Stockholm

Kraków, Wrocław

Poznań

Oslo

23

Occu

pa

ncy r

ate

, %

Completion rate, %

0%

20%

40%

60%

80%

100%

0% 20% 40% 60% 80% 100%

PC < = 200

200 = < PC < = 500

PC > 500

CDE Projects

CDN Projects

CDUS Projects

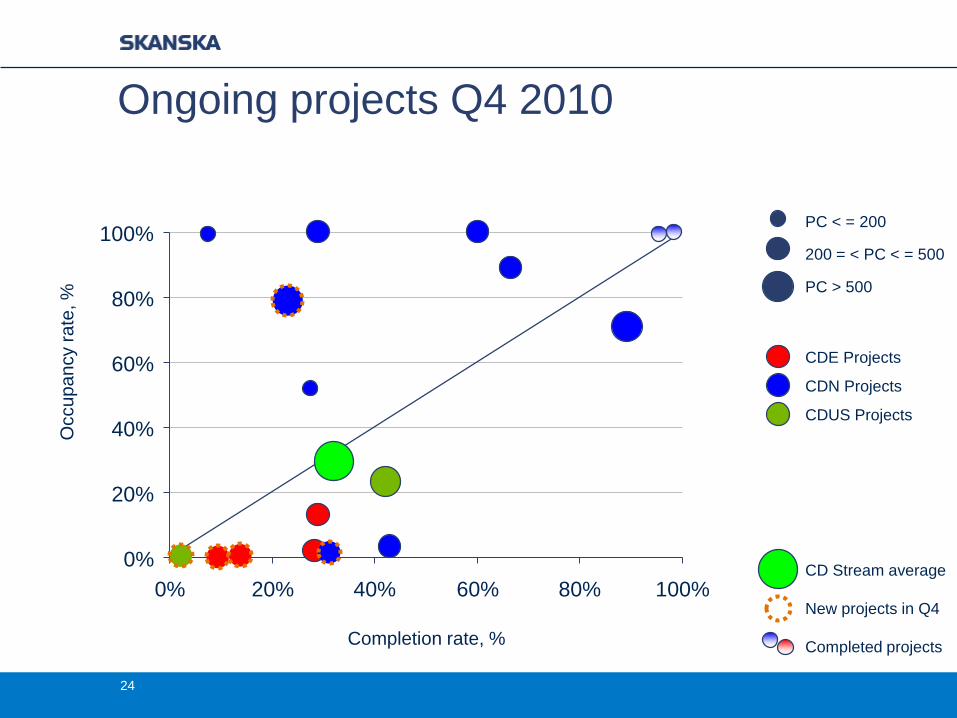

Ongoing projects Q4 2010

CD Stream average

New projects in Q4

Completed projects

24

Occu

pa

ncy r

ate

, %

Completion rate, %

0%

20%

40%

60%

80%

100%

0% 20% 40% 60% 80% 100%

PC < = 200

200 = < PC < = 500

PC > 500

CDE Projects

CDN Projects

CDUS Projects

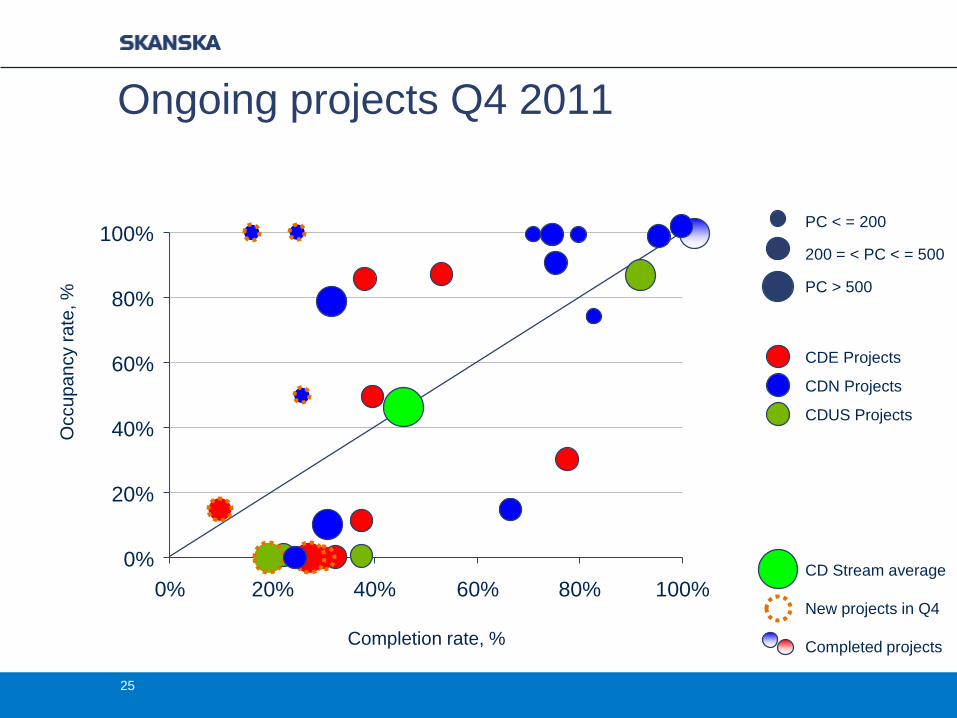

Ongoing projects Q4 2011

CD Stream average

New projects in Q4

Completed projects

25

Occu

pa

ncy r

ate

, %

Completion rate, %

0%

20%

40%

60%

80%

100%

0% 20% 40% 60% 80% 100%

PC < = 200

200 = < PC < = 500

PC > 500

CDE Projects

CDN Projects

CDUS Projects

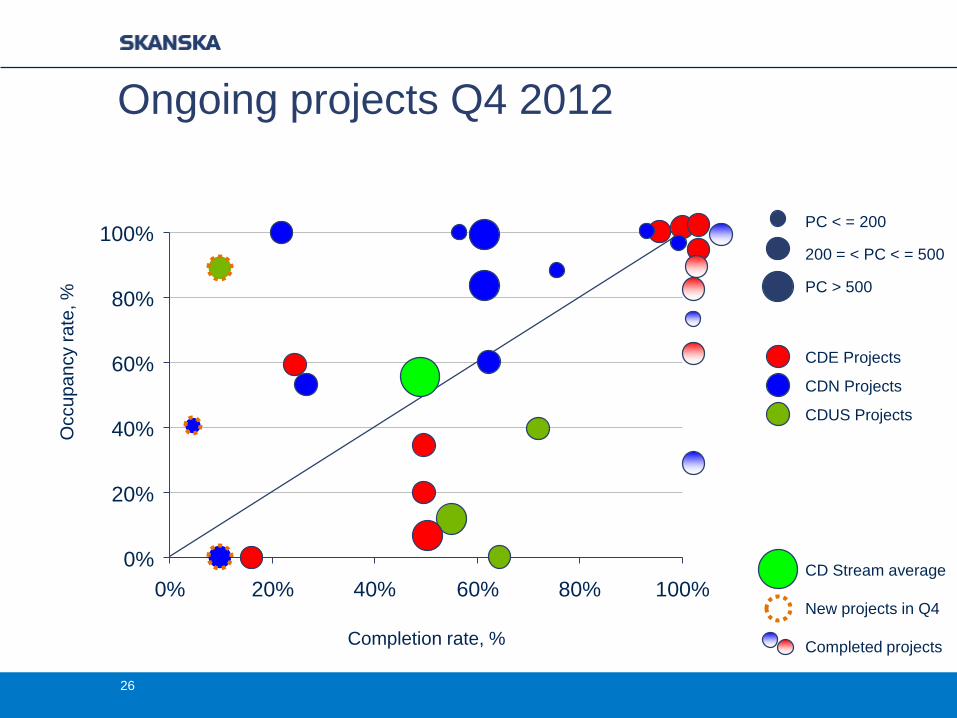

Ongoing projects Q4 2012

CD Stream average

New projects in Q4

Completed projects

26

Occu

pa

ncy r

ate

, %

Completion rate, %

0%

20%

40%

60%

80%

100%

0% 20% 40% 60% 80% 100%

PC < = 200

200 = < PC < = 500

PC > 500

CDE Projects

CDN Projects

CDUS Projects

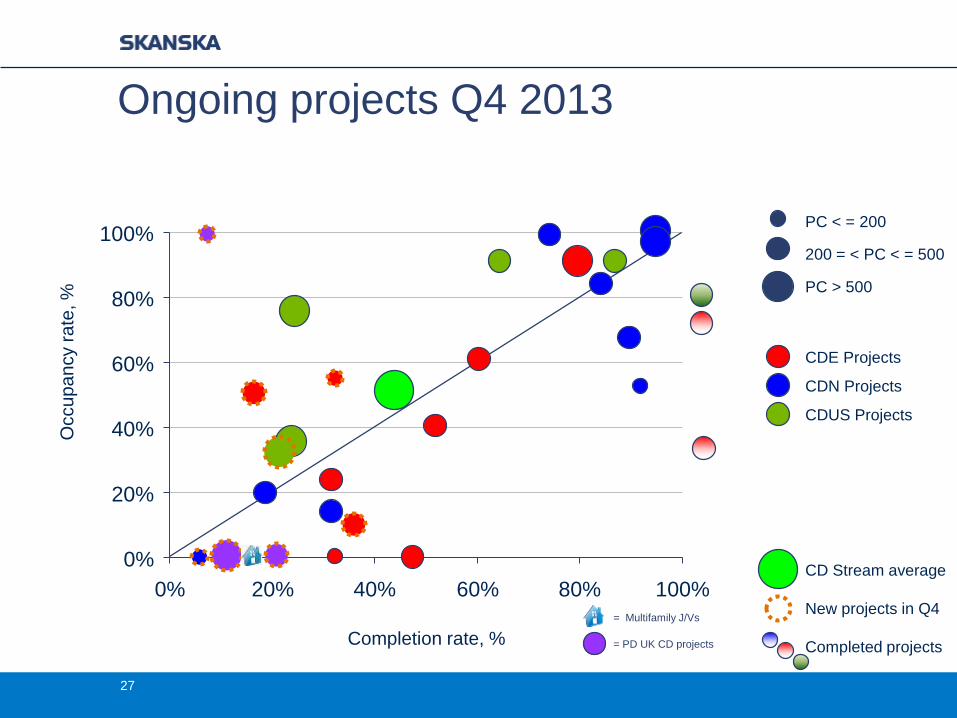

Ongoing projects Q4 2013

= Multifamily J/Vs

= PD UK CD projects

CD Stream average

New projects in Q4

Completed projects

27

Occu

pa

ncy r

ate

, %

Completion rate, %

0%

20%

40%

60%

80%

100%

0% 20% 40% 60% 80% 100%

PC < = 200

200 = < PC < = 500

PC > 500

CDE Projects

CDN Projects

CDUS Projects

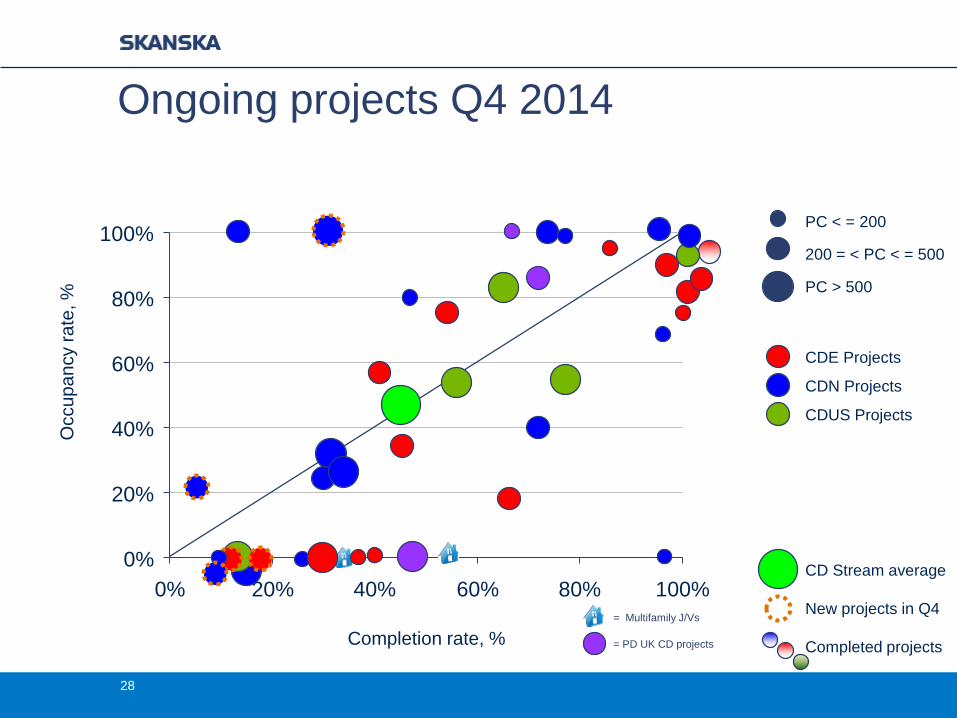

Ongoing projects Q4 2014

= PD UK CD projects

= Multifamily J/Vs

CD Stream average

New projects in Q4

Completed projects

28

Occu

pa

ncy r

ate

, %

Completion rate, %

0%

20%

40%

60%

80%

100%

0% 20% 40% 60% 80% 100%

PC < = 200

200 = < PC < = 500

PC > 500

CDE Projects

CDN Projects

CDUS Projects

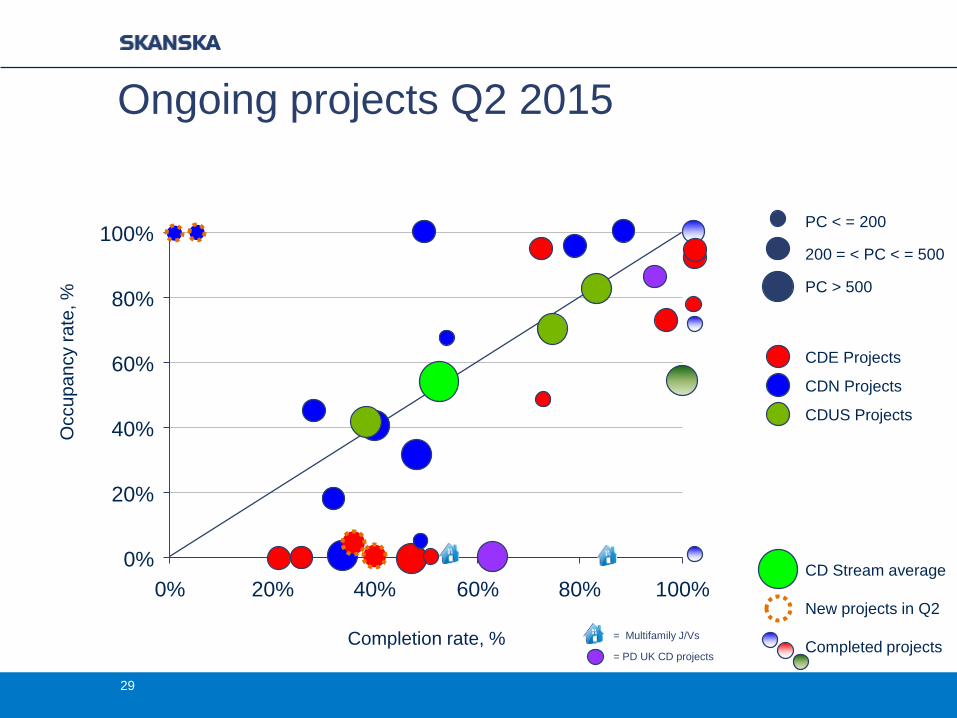

Ongoing projects Q2 2015

= Multifamily J/Vs

= PD UK CD projects

CD Stream average

New projects in Q2

Completed projects

29

30

Agenda

1) Background/history/overview

2) Value creation

3) Financial performance

and allocation

4) The future

The future for Commercial Development

− Transfer/rotation and development

of key people

− Keep proven business model

− Evaluate new markets

− Land bank focus to backfill pipeline

− Market orientation

− Key client management

− Cost efficiency

− Manage the cycles

31

Commercial DevelopmentNordic

Jan Odelstam

Business Unit President

Stockholm New, Sweden

32

Skanska Commercial Development Nordic

33

− 108 employees

− Headquartered in Stockholm

2006–2015 Q2

− 1.2 million sqm leased

− 95 projects developed

− Investments SEK 20.3 billion

− Divestments SEK 27.3 billion

HelsinkiStockholm

MalmöCopenhagen

Gothenburg

Oslo

Business concept

− Invest in self developed

properties

− Create value in the whole value

chain

− Prime products for institutional

investors

− High turnover in project portfolio

− Long term land banking

34

Malmö Live, Sweden

Permitting

Planning

Design

Investment in

land bank

Project

idea

Leasing

Construction

Property Mgmt

Exit

Products & Markets

35

Office Stockholm

Gothenburg

Malmö

Oslo

Copenhagen

Helsinki

Logistic

facilitiesSweden

Rental

Residential

Copenhagen

36

Stockholm

− 12 M sqm

− Growth 120,000 sqm / year

Gothenburg

− 3 M sqm

− Growth 40,000 sqm / year

Oslo

− 8 M sqm

− Growth 80,000 sqm / year

Helsinki

− 9 M sqm

− Growth 50,000 sqm / year

Copenhagen

− 12 M sqm

− Growth 120,000 sqm / year

Skanska Commercial DevelopmentNordic

Malmö

− 2 M sqm

− Growth 30,000 sqm / year

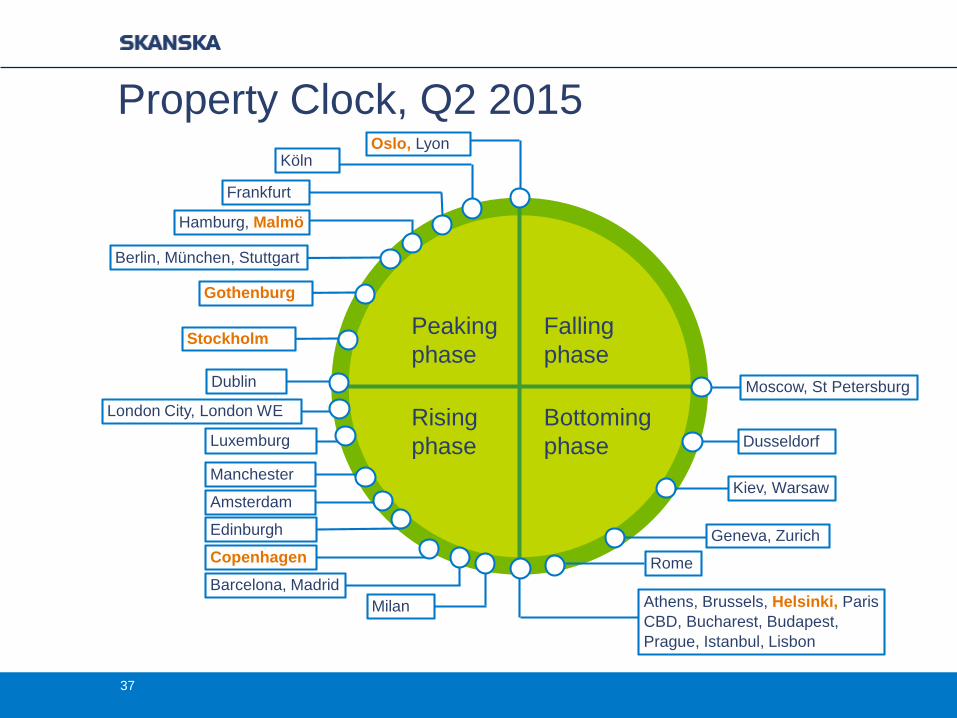

Property Clock, Q2 2015

37

Peaking

phase

Falling

phase

Rising

phase

Bottoming

phase

Edinburgh

Copenhagen

Milan Athens, Brussels, Helsinki, Paris

CBD, Bucharest, Budapest,

Prague, Istanbul, Lisbon

Frankfurt

Oslo, Lyon

Hamburg, Malmö

Berlin, München, Stuttgart

Stockholm

Dublin

Manchester

Amsterdam

Barcelona, Madrid

Geneva, Zurich

Kiev, Warsaw

Dusseldorf

Moscow, St Petersburg

Rome

Luxemburg

London City, London WE

Gothenburg

Köln

The Nordic Real Estate Market– Office Trends

38

− Shared services for global

companies will continue to relocate

outside the Nordics

− Location will be no 1 with access to

public communications

− New ways of working puts

sqm/person out of play

− Green still important but not a

differentiator

Result 2011 – 2015 Q2

39

-3 000

-2 000

-1 000

0

1 000

2 000

3 000

4 000

5 000

2011 2012 2013 2014 2015 Q2YTDDivestments Investments

0

20

40

60

80

100

120

2011 2012 2013 2014 2015Q2

Number of employees

0

20

40

60

80

100

120

2011 2012 2013 2014 2015Q2 YTD

Leasing, thousand square meters

0

200

400

600

800

1 000

1 200

1 400

2011 2012 2013 2014 2015 Q2YTD

EBIT, SEK M

0,0%

2,0%

4,0%

6,0%

8,0%

10,0%

12,0%

14,0%

16,0%

0

1 000

2 000

3 000

4 000

5 000

6 000

7 000

2011 2012 2013 2014 2015 Q2

Capital employed and ROCE

Capital Employed Adjusted ROCE

Investment and divestments

SEK 2,068 M

2012

SEK 4,555 M

2011

SEK 2,167 M

2013

4,360 MSEK

2014

Sold Projects

2011–2015

SEK 15 bn

40

SEK 1,907 M

2015

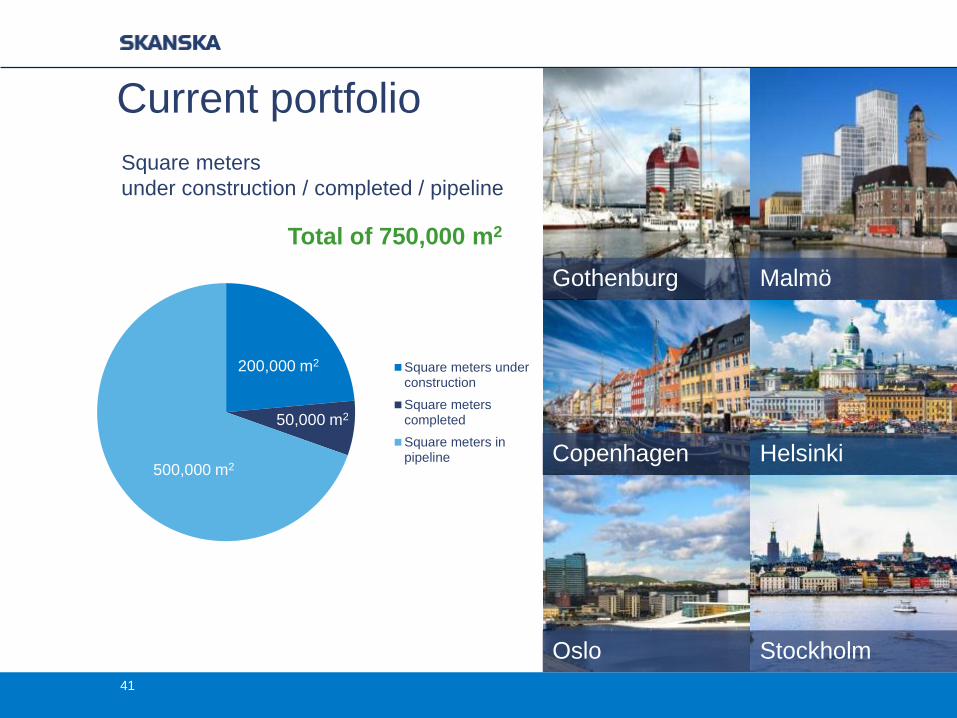

Current portfolio

41

Square meters

under construction / completed / pipeline

Total of 750,000 m2

Copenhagen Helsinki

Oslo Stockholm

MalmöGothenburg

Square meters underconstruction

Square meterscompleted

Square meters inpipeline

500,000 m2

200,000 m2

50,000 m2

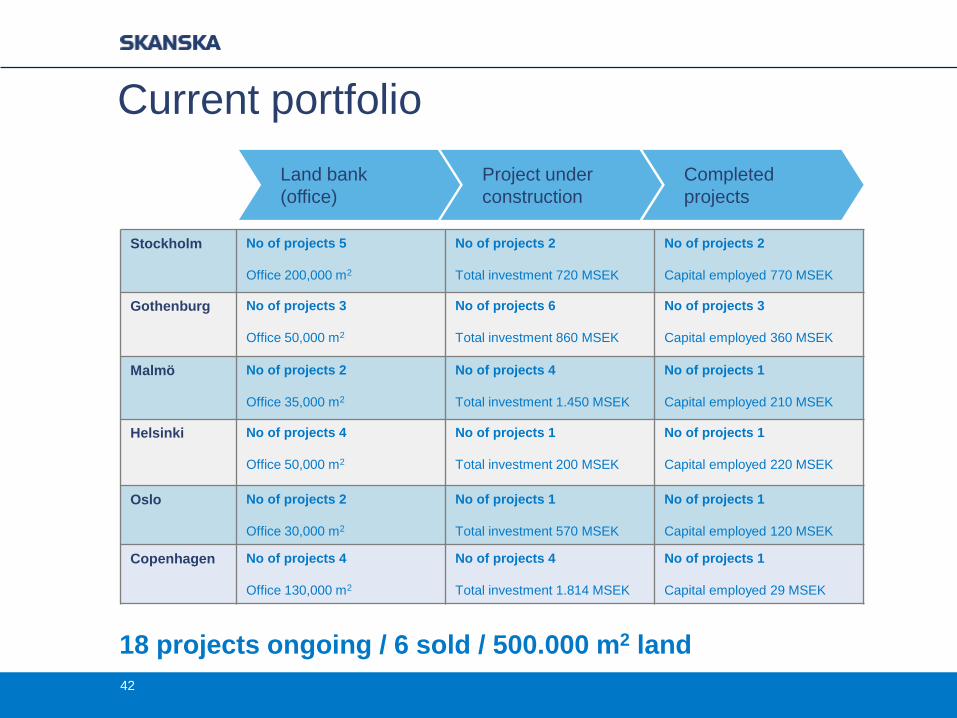

Current portfolio

42

Stockholm No of projects 5

Office 200,000 m2

No of projects 2

Total investment 720 MSEK

No of projects 2

Capital employed 770 MSEK

Gothenburg No of projects 3

Office 50,000 m2

No of projects 6

Total investment 860 MSEK

No of projects 3

Capital employed 360 MSEK

Malmö No of projects 2

Office 35,000 m2

No of projects 4

Total investment 1.450 MSEK

No of projects 1

Capital employed 210 MSEK

Helsinki No of projects 4

Office 50,000 m2

No of projects 1

Total investment 200 MSEK

No of projects 1

Capital employed 220 MSEK

Oslo No of projects 2

Office 30,000 m2

No of projects 1

Total investment 570 MSEK

No of projects 1

Capital employed 120 MSEK

Copenhagen No of projects 4

Office 130,000 m2

No of projects 4

Total investment 1.814 MSEK

No of projects 1

Capital employed 29 MSEK

Land bank

(office)

Project under

construction

Completed

projects

18 projects ongoing / 6 sold / 500.000 m2 land

− Office

− 21.000 m2

− Completion: Q4 2016

− Office

− 30,000 m2

− Completion: Q1 2017

− Residential

− 42,000 m2

− Completion: Q2 2018

− Office

− 16,000 m2

− Completion: Q4 2016

Example Prime Ongoing Projects

43

STUDIOMalmö

SeasideStockholm

SundtkvartaletOslo

Öresund StrandparkCopenhagen

− Office

− 9,000 m2

− Project Start: 2016

− Office

− 20.000 m2

− Project Start: 2017

− Office

− 40,000 m2

− Project Start: 2016

44

− Office

− 25.000 m2

− Project Start: 2016

TalismanHelsinki

Gothenburg City GateGothenburg

Stockholm NewStockholm

Copenhagen HighlineCopenhagen

Prime Future Projects

45

Challenges

− High turnover in project

portfolio

− New zoning plans

− Market conditions

Opportunities

− Strong organization

− Land bank

− Leasing and investor market

46

In summary

− Strong track record

− Solid organization

− Competitive land bank

− Keep market shares in

Sweden

− Increase market shares

in Oslo and Helsinki

Stockholm New, Sweden

Commercial Development Europe

Nicklas Lindberg

Business Unit President

47

1Strong market

2BPO/SSC

leadership

3Drive for

innovation

− Lot of liquidity on the market

− Healthy demand from tenants

− Poland and Czech Republic perceived as mature markets

− Romania & Hungary picking up quickly

− Key change from back office to middle office

− Strong inflow of operations from banks / financial institutions

− Well-established partnerships in the sector

− We are on the rapid journey and we need keep with the market

− Innovation & work smarter is our idea for the future growth

− One Skanska enabling functions

Why Central Europe?

48

Country by countryKey facts:

Poland:

− Warsaw – business hub for CEE, Wroclaw & Kraków has reached

momentum, Poznan, Katowice & Lodz constantly growing

− Growth of the public sector and modern services drives leasing

performance

Czech Republic:

− HQ offices (moderately sized leases) for local or CEE-based companies

− Once the building is leased, it’s highly likely to find a buyer

Hungary & Romania:

− Coming up from low levels but are gaining momentum now as there is

an increasing BPO/SSC demand

49

Prague:

− Headquaters of small and

medium CEE businesses

− Attractive for investors

Warsaw:

− Biggest market in the

region (over 4,5 mln sqm)

− Public sector growth

Prime markets

Budapest:

− Gaining up from low

levels

− Front office IT outsourcing

Bucharest:

− Young, growing market

− Huge demand for modern,

A-class offices

50

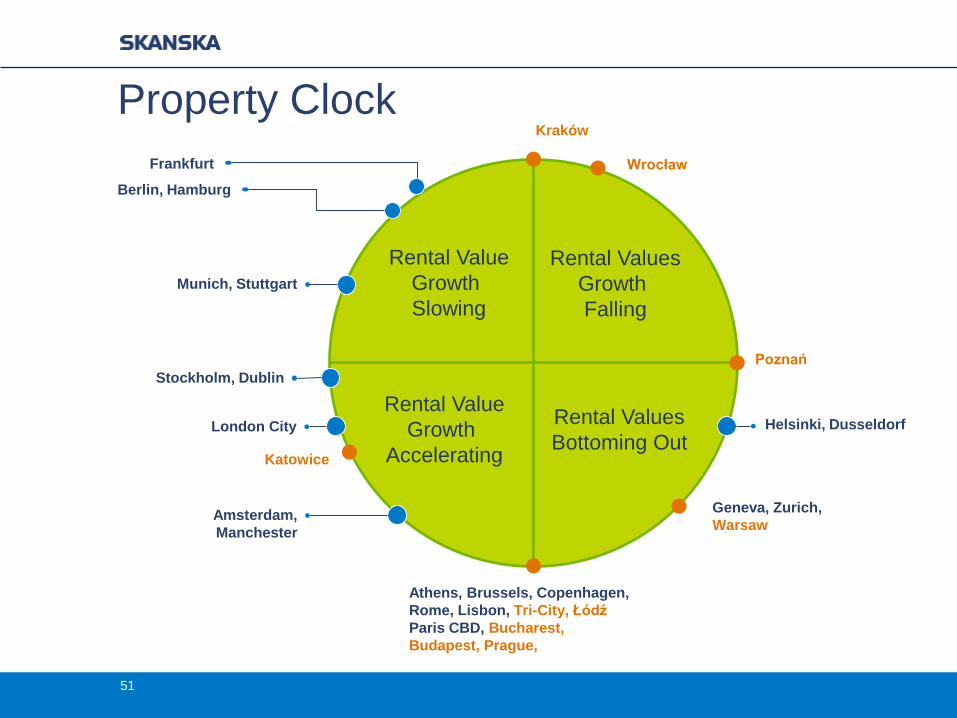

Property Clock

Rental Value

Growth

Slowing

Rental Values

Growth

Falling

Rental Value

Growth

Accelerating

Rental Values

Bottoming Out

Kraków

Wrocław

Poznań

Katowice

Athens, Brussels, Copenhagen,

Rome, Lisbon, Tri-City, Łódź

Paris CBD, Bucharest,

Budapest, Prague,

Berlin, Hamburg

London City

Munich, Stuttgart

Geneva, Zurich,

WarsawAmsterdam,

Manchester

Stockholm, Dublin

Helsinki, Dusseldorf

Frankfurt

51

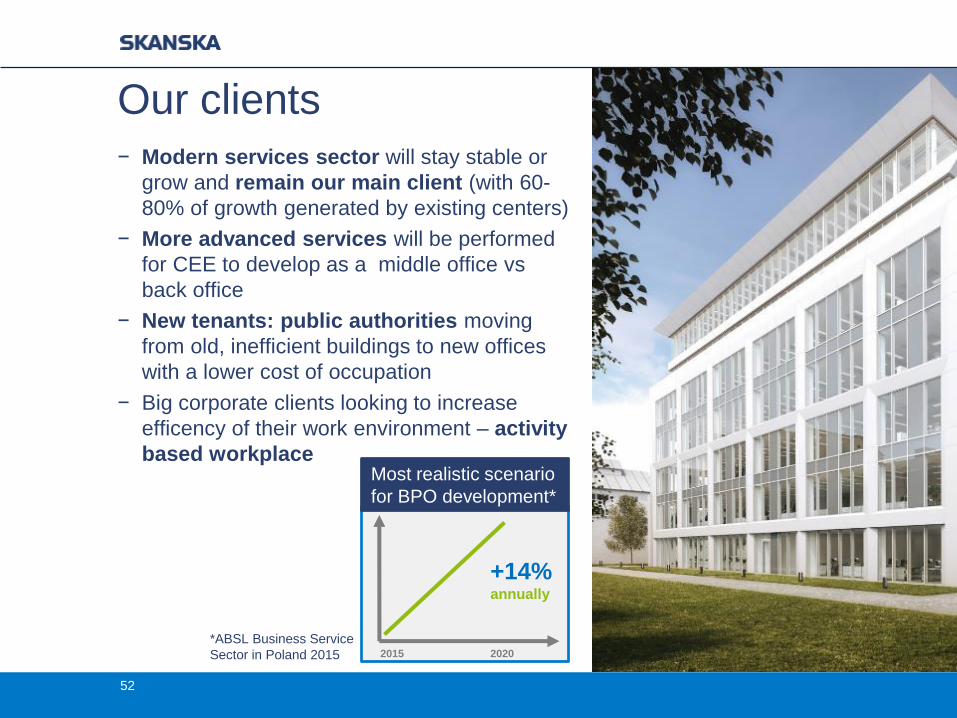

*ABSL Business Service

Sector in Poland 2015

Our clients

− Modern services sector will stay stable or

grow and remain our main client (with 60-

80% of growth generated by existing centers)

− More advanced services will be performed

for CEE to develop as a middle office vs

back office

− New tenants: public authorities moving

from old, inefficient buildings to new offices

with a lower cost of occupation

− Big corporate clients looking to increase

efficency of their work environment – activity

based workplace

+14%annually

2015 2020

Most realistic scenario

for BPO development*

52

Acquiring & retaining great people is key

53

Risks and challenges:

− Keep the company culture in a growing organization

− Getting people ready to deliver and understand what creates value

− Process management balanced with creativity, innovation and flexible

approach

− How to retain best people – more independent generations, more

competitive labor market and mobility

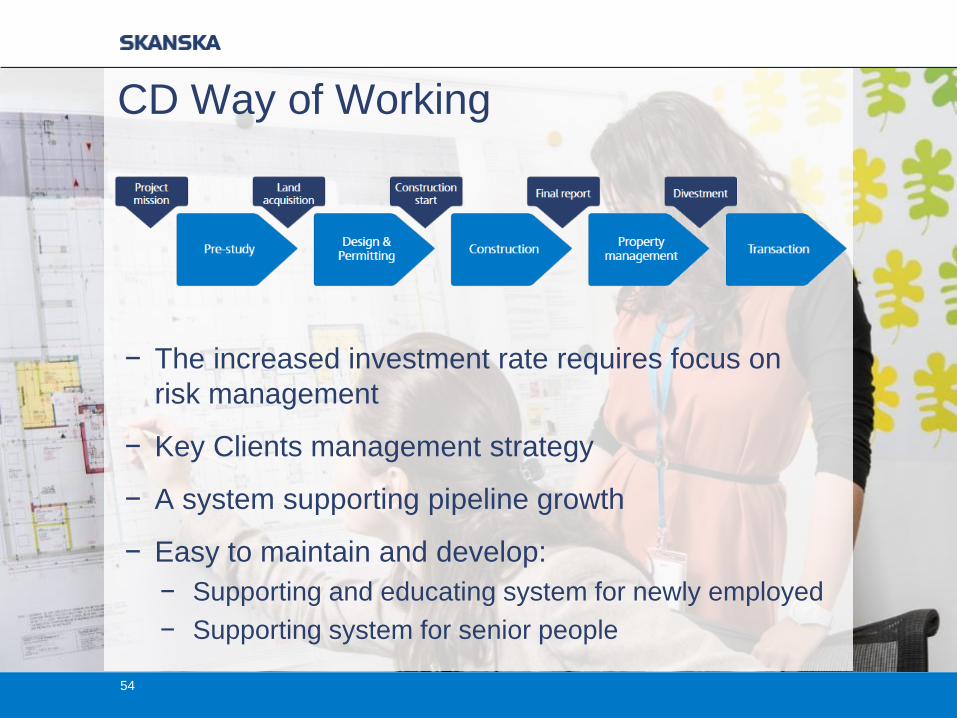

54

− The increased investment rate requires focus on

risk management

− Key Clients management strategy

− A system supporting pipeline growth

− Easy to maintain and develop:

− Supporting and educating system for newly employed

− Supporting system for senior people

CD Way of Working

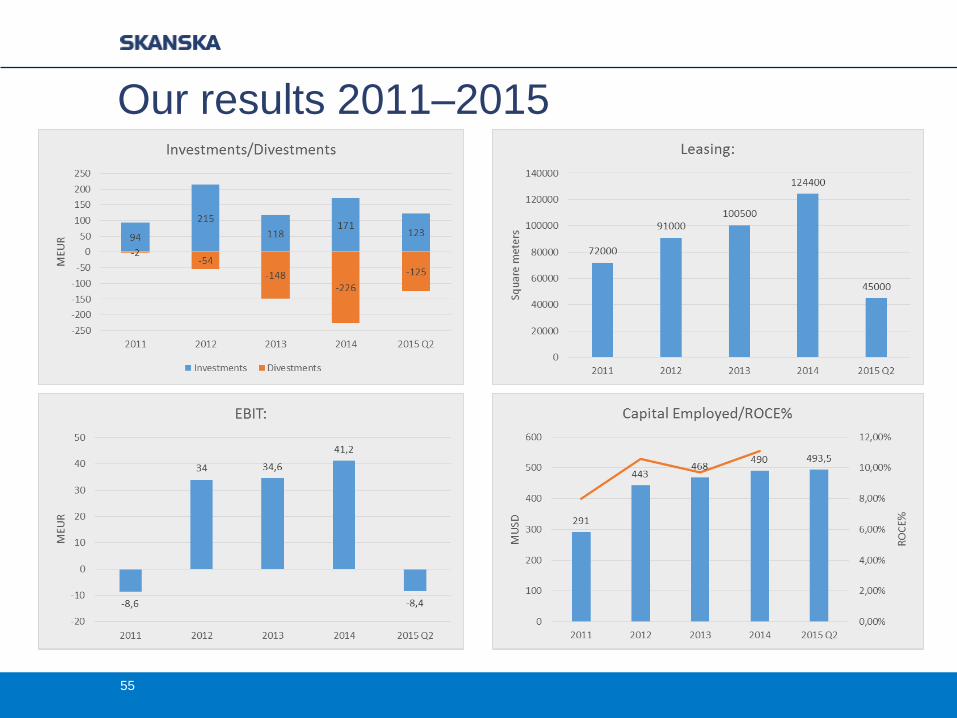

Our results 2011–2015

55

530 000 sqm

170 000 sqm

320 000 sqm

delivered

ongoing

planned

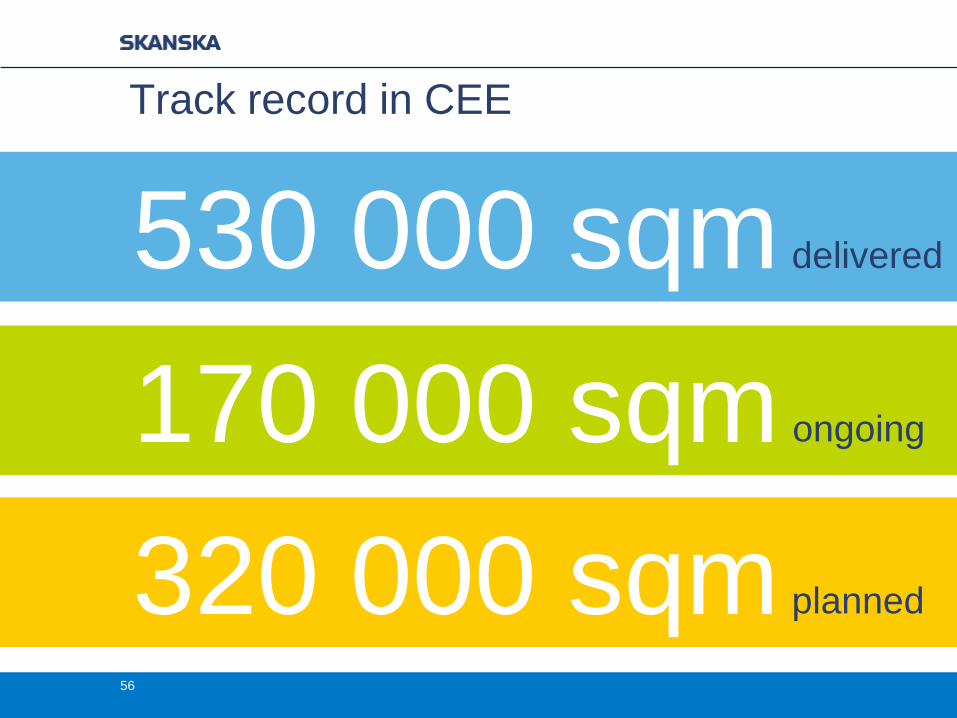

Track record in CEE

56

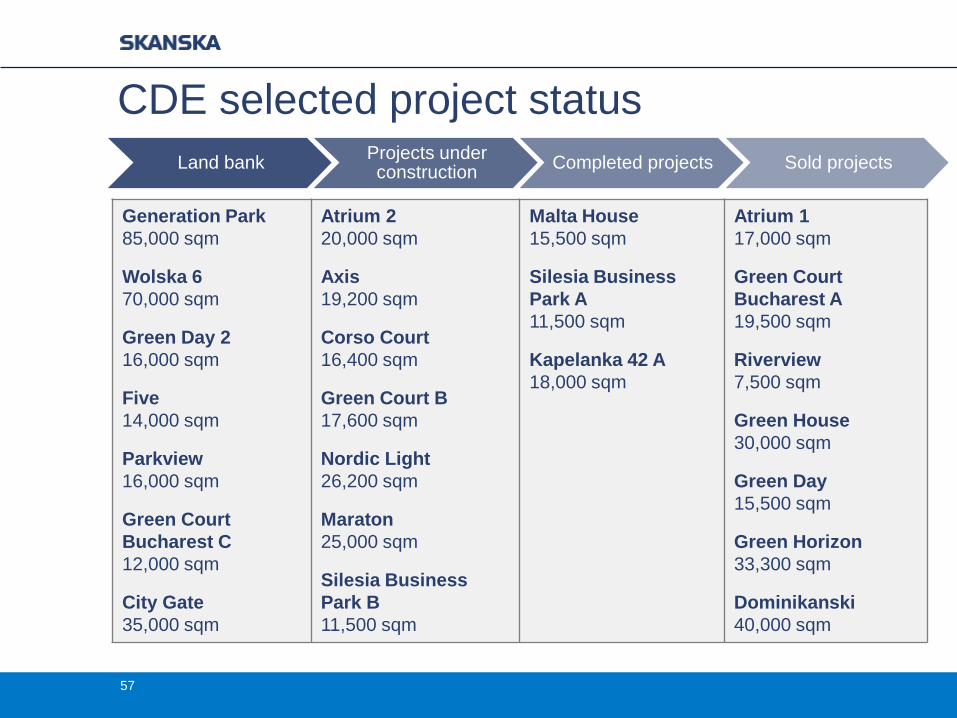

Generation Park

85,000 sqm

Wolska 6

70,000 sqm

Green Day 2

16,000 sqm

Five

14,000 sqm

Parkview

16,000 sqm

Green Court

Bucharest C

12,000 sqm

City Gate

35,000 sqm

Atrium 2

20,000 sqm

Axis

19,200 sqm

Corso Court

16,400 sqm

Green Court B

17,600 sqm

Nordic Light

26,200 sqm

Maraton

25,000 sqm

Silesia Business

Park B

11,500 sqm

Malta House

15,500 sqm

Silesia Business

Park A

11,500 sqm

Kapelanka 42 A

18,000 sqm

Atrium 1

17,000 sqm

Green Court

Bucharest A

19,500 sqm

Riverview

7,500 sqm

Green House

30,000 sqm

Green Day

15,500 sqm

Green Horizon

33,300 sqm

Dominikanski

40,000 sqm

Land bankProjects under construction

Completed projects Sold projects

CDE selected project status

57

Total transaction volume in 2014exceeded EUR 330 M & 125 000 sqm

58

Atrium 2Poland, Warsaw

Q1 2016

20,000 sqm

OngoingCDE Projects Total: 170,000 sqm

MaratonPoland, Poznań

Q4 2016

25,000 sqm

Green Court

BucharestRomania, Bucharest

Q4 2016

52,000 sqm

Nordic Light

Hungary, Budapest

Q3 2016

26,200 sqm

Dominikański

Poland, Wrocław

Q3 2015

38,000 sqm

Axis

Poland, Kraków

Q3 2016

20,000 sqm

59

Corso

CourtCzech Republic, Prague

Q3 2015

17,000 sqm

Silesia

Business ParkPoland, Katowice

Q3 2015

48,000 sqm

City GatePoland, Łódź

2018-19

32,000 sqm

Prime Future Projects More than300,000 sqm

Generation

ParkPoland, Warsaw

2018-2020

84,000 sqm

PawiaPoland, Kraków

2018-2022

70,000 sqm

Nordic Light 2Hungary, Budapest

2016

25,200 sqm

FiveCzech

Republic,

Prague

2018

15,000 sqm

60

61

Challenges

− Future land bank, lack of

easy plots on the market

− Easy money on the market-

competition catching up

Opportunities

− Macro economical stability

in the region

− Strong inflows of foreign

capital

− Domestic investment funds

becoming active

62

− Stable macroeconomic

situation and market growth

− Favorable market conditions

and prospect tenants

segments bring continued

opportunities

− Well-established structures

within the region, all countries

delivering

Summary