18

Investor Presentation February 2008

Investor Presentation

February 2008

1

Disclaimer

This presentation has been prepared by SK Telecom Co., Ltd. (“the Company”). This presentation is being presented solely for your information and is subject to change without notice. No representation or warranty, expressed or implied, is made and no reliance should be placed on the accuracy, fairness or completeness of the information presented. The Company, its affiliates, advisers or representatives accept no liability whatsoever for any losses arising from any information contained in the presentation.

This presentation does not constitute an offer or invitation to purchase or subscribe for any shares of the Company, and no part of this presentation shall form the basis of or be relied upon in connection with any contract or commitment.

The contents of this presentation may not be reproduced, redistributed or passed on, directly or indirectly, to any other person or published, in whole or in part, for any purpose.

2

1. Industry Overview

2. 2007 Operating Results

3. Growth Strategy

4. SK Telecom’s Investment Assets

5. Commitment to Shareholders

Table of ContentsTable of Contents

3

1. Industry Overview

2. 2007 Operating Results

3. Growth Strategy

4. SK Telecom’s Investment Assets

5. Commitment to Shareholders

4

Overview of Korean Wireless MarketOverview of Korean Wireless Market

Mobile Telecommunications Market Trend

67.9%70.1%

75.9%79.4%

83.2% 89.8%

Source: MIC, NSO

Total subscribers Penetration

(000s, %)

Despite the maturing market, wireless data market continues to grow

Wireless Data Market Growth

1,086

1,736

2,424

3,285

3,6853,887

2002 2003 2004 2005 2006 2007

(KRW Bn)

6-yr CAGR : 29.0%

Source: Earnings ReleaseWCDMA subscribers

32,34233,592

36,58638,342

40,19743,498

166

5,700

2002 2003 2004 2005 2006 2007

5,700166

5

2007 Competitive Landscape2007 Competitive Landscape

4,024

1,583

678

SKT KTF LGT

11,286

5,5723,249

SKT KTF LGT

25.3

28.7 29.8

SKT KTF LGT

SK Telecom continues to demonstrate undisputed market leadership

Market Share by Subscribers Revenue

Marketing Expense to Sales EBITDA

(000s, %)

(KRW Bn)(%)

SKT50.5%

LGT18.0%

KTF31.5%

※ As of December 31, 2007

21,968

7,809

13,721

(KRW Bn)

**

* Service revenue(Handset revenue excluded)

6

1. Industry Overview

2. 2007 Operating Results

3. Growth Strategy

4. SK Telecom’s Investment Assets

5. Commitment to Shareholders

7

2007 Results2007 Results

Review of performance in 2007

Revenue

Marketing expense to revenue

Net income

(KRW Bn)

EBITDA (EBITDA Margin)

20072007 YoYYoY 4Q20074Q200720062006

11,286 2,916

1,642 66

4,024(35.7%)

855(29.3%)

25.3% 29.3%

1,855 696

3Q20073Q2007

2,816

777

1,011(35.9%)

25.2%

442

QoQQoQ

4%

-91%

-15%

4.0%p

57%

21,968

10,651

1,447

4,232(39.7%)

20.5%

1,518

20,271 21,968

6%

14%

-5%

4.7%p

22%

8% 21,606 2%

Capital expenditure

Subscribers (000’)

8

1. Industry Overview

2. 2007 Operating Results

3. Growth Strategy

4. SK Telecom’s Investment Assets

5. Commitment to Shareholders

9

WCDMAWCDMA

Enhancing competitiveness in WCDMA market through upgrades of network quality,

extensive handset line-ups and innovative services

� Cutting-edge network

quality/coverage achieved

� Nationwide HSUPA service

by 2009

� WCDMA subscribers 2.5mil.,

exceeding the target of

1.5mil. in 2007

Network

� Wireless-to-wireless, web-to-wireless, fixed-to-wireless visual phone

� Image coloring, image message call

� VU traffic report, VU monitoring

� T-login : Hi-speed Internet access

� Full-browsing: Mobile web browser

� UCC, video messenger, web-like e-mail

Visual

Internet

� GSM / WCDMA covers 80% of the world

� Global roaming alliance with Bridge Alliance*(190mil. subscribers) in Asia and Freemove in Europe

� Wireless financial services via USIM

-Credit card transactions, mobile banking and payment services, membership cards, mobile gift cards, etc

Global

Convenience

� Strengthen WCDMA competitiveness through reinforcement of handset line-ups

- 14 models in 2007(30% of total line-ups introduced in 2007)

- Introduce 28~35 models in 2008 (60% of new models planned in 2008)

� Plans to introduce handsets by global manufacturers in 2008

Device

Service

* A partnership of eleven leading mobile operators in Asia Pacific region including Bharti Airtel, Telkomsel, AIS,

Globe Telecom, Optus, SingTel, etc.

10

Acquisition of Hanaro TelecomAcquisition of Hanaro Telecom

Solidify sustainable growth trajectory and create customer value in wired/wireless

convergence environment

Bundled

Products

Overview of Hanaro TelecomOverview of Hanaro Telecom Expected SynergiesExpected Synergies

IPTV

• IPTV to provide growth momentum for

SKT’s content business

• Strengthen HanaTV’s content competitiveness

through SKT’s diverse content universe

• Reinforce product competitiveness through

bundled products and services

- Combine SKT’s mobile services with

Hanaro Telecom’s fixed line services

Convergence

BM

• Realize sustainable growth through

development of new convergence business

model

• 2nd largest fixed line operator with 3.6mil. broadband and 2.0mil. telephony subscribers (Dec. 07)

• KRW 1,868Bn sales in 2007

• 807,000 subscribers (Dec. 07)

• Competitive edge from its rich contents relative to peers

Broadband Market Share (%)

Hanaro

Telecom

25.3

Sales Composition (%)

* As of September 31, 2007

Others

0.4%KT 44.7

Others

19.2

LG

Dacom

10.9

Broadband

59.8

Voice

27.8

Leased

line 6.3%

※ SKT decided to acquire an additional 38.89% stake in December 2007 and will become

the largest shareholder of Hanaro Telecom with a 43.59% stake after government approval

IDC &

Solution 5.6%

11

12

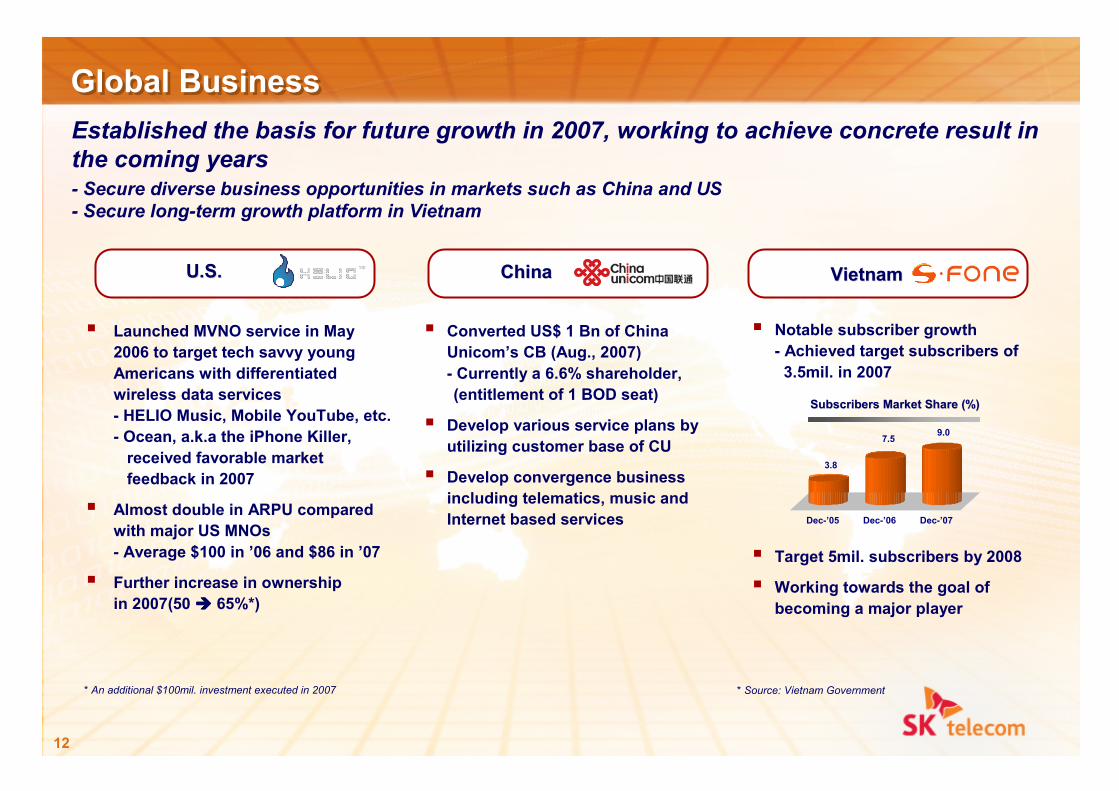

Global Business Global Business

Established the basis for future growth in 2007, working to achieve concrete result in

the coming years- Secure diverse business opportunities in markets such as China and US

- Secure long-term growth platform in Vietnam

� Converted US$ 1 Bn of China

Unicom’s CB (Aug., 2007)

- Currently a 6.6% shareholder,

(entitlement of 1 BOD seat)

� Develop various service plans by

utilizing customer base of CU

� Develop convergence business

including telematics, music and

Internet based services

ChinaChina

* Source: Vietnam Government

� Notable subscriber growth

- Achieved target subscribers of

3.5mil. in 2007

� Target 5mil. subscribers by 2008

� Working towards the goal of

becoming a major player

VietnamVietnam

Subscribers Market Share (%)Subscribers Market Share (%)

� Launched MVNO service in May

2006 to target tech savvy young

Americans with differentiated

wireless data services

- HELIO Music, Mobile YouTube, etc.

- Ocean, a.k.a the iPhone Killer,

received favorable market

feedback in 2007

� Almost double in ARPU compared

with major US MNOs

- Average $100 in ’06 and $86 in ’07

� Further increase in ownership

in 2007(50 ���� 65%*)

U.S.U.S.

* An additional $100mil. investment executed in 2007

3.8

7.59.0

Dec-’05 Dec-’06 Dec-’07

13

1. Industry Overview

2. 2007 Operating Results

3. Growth Strategy

4. SK Telecom’s Investment Assets

5. Commitment to Shareholders

14

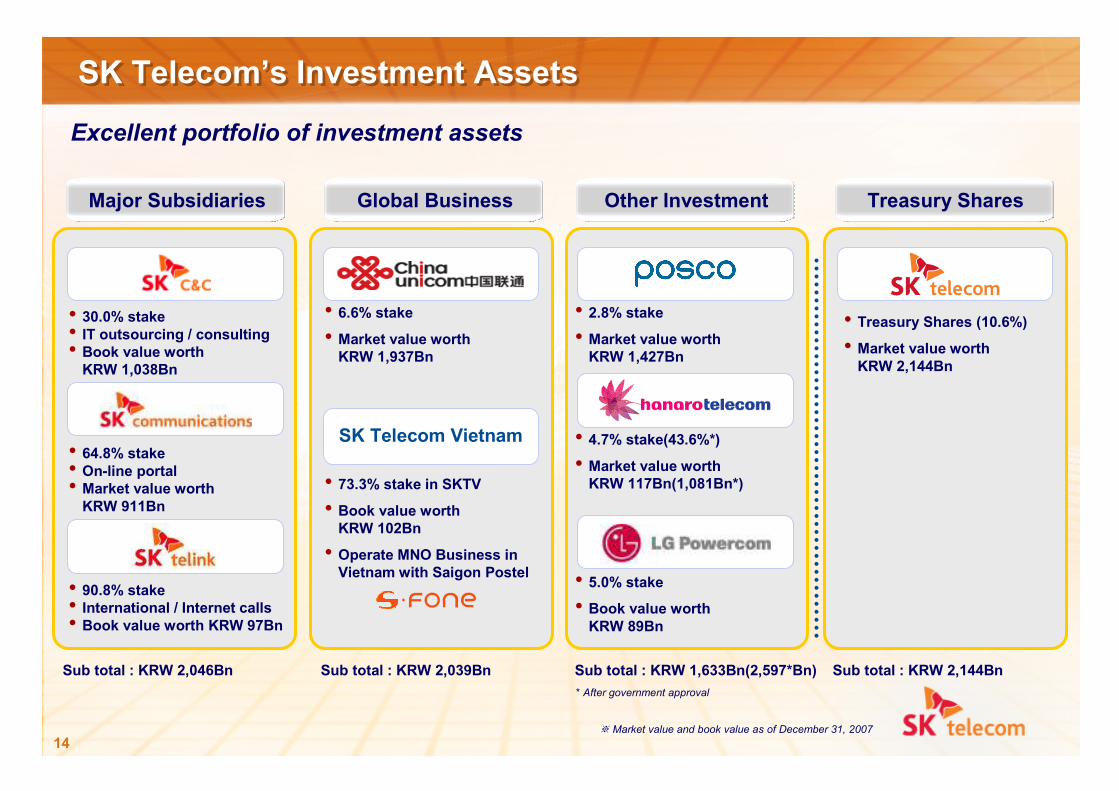

SK Telecom’s Investment AssetsSK Telecom’s Investment Assets

※ Market value and book value as of December 31, 2007

Excellent portfolio of investment assets

• 30.0% stake• IT outsourcing / consulting• Book value worth KRW 1,038Bn

• 64.8% stake• On-line portal• Market value worthKRW 911Bn

• 90.8% stake• International / Internet calls• Book value worth KRW 97Bn

SK Telecom Vietnam

• 6.6% stake• Market value worth KRW 1,937Bn

• 73.3% stake in SKTV• Book value worth KRW 102Bn

• Operate MNO Business in Vietnam with Saigon Postel

• 2.8% stake• Market value worth KRW 1,427Bn

• 4.7% stake(43.6%*) • Market value worth KRW 117Bn(1,081Bn*)

• 5.0% stake• Book value worth KRW 89Bn

• Treasury Shares (10.6%)• Market value worth KRW 2,144Bn

Major Subsidiaries Global Business Other Investment Treasury Shares

Sub total : KRW 2,046Bn Sub total : KRW 2,039Bn Sub total : KRW 1,633Bn(2,597*Bn) Sub total : KRW 2,144Bn

* After government approval

15

1. Industry Overview

2. 2007 Operating Results

3. Growth Strategy

4. SK Telecom’s Investment Assets

5. Commitment to Shareholders

16

Improving Shareholder ValueImproving Shareholder Value

10%21% 25%

35% 40% KRW 8,000

2002 2003 2004 2005 2006 2007

SK Telecom is committed to enhancing shareholder value

Payout ratio DPS* Overall amount is expected tobe similar to 2007

Special Dividends : Approx. KRW 300 Bn for 2004

Special Dividends : KRW 1,400 per shareSpecial Dividends : KRW 1,400 per share for 2007for 2007

Stock Buyback : KRW 100 Bn for 2007Stock Buyback : KRW 100 Bn for 2007

Stock Buyback : KRW 200 Bn for 2006

2008E

17

THANK YOUTHANK YOUTHANK YOU