Page 1

Page | 174

Slums and Urban Land Prices 6

Urbanization is, however, a development oriented sign of

economic prosperity in any country. The increased level of

urbanization is important for socio-economic development of the

people and is to be encouraged but we require more development

planning to do that. Due to the concentration of number of

industrial units and other service sector activities near the existing

cities, unplanned urbanization and unabated migration and

concentration of poor population from the depressed rural areas

to the urban settlements, numerous problems of complex nature

have emerged. It has created an imbalance situation in the urban

centers especially social and economic conditions. The migration

has strained infrastructure facilities in the cities to the breaking

point. The intermixing various land uses has created confusion

and chaotic conditions. There has been acute shortage of

housing in urban areas with the result that the cities face grim

situation with the fast increasing number of shanty dwellers,

squatters, pavement dwellers and slums in all the metropolitan

and other cities throughout the nation1.

Origin of Slums

Majority of the developed countries, developing countries

and less developed countries are facing this problem of slums

Page 2

Page | 175

and there is no panacea to eradicate the same from the surface of

the earth. Slums are universal in character and no country is able

to get rid of them. Unplanned urbanization with its attendant evils

of negating the fundamental purpose of human society- a secure,

rewarding and happy life- is no doubt a matter of great concern.

Infrastructure facilities like housing, safe drinking water supply,

transport, health care, educational institutions for children, parks,

etc,. have become woefully inadequate and will soon reach a

critical stage threatening the civilized existence itself. As per the

census of India 2001, more than one fourth of urban population

living in slums and squatters, settlements, the future can only be

one of still larger population living in such conditions if public

neglect continues. It is said every second there are two additional

mouths to feed. The overcrowding population, poverty, ignorance,

diseases, mal nutrition, etc, must be eliminated and the society

should seek improvement of living standards and quality of life of

the people.

In the present day world especially in developing countries,

the growth of slums is usually parallel to the growth of

urbanization. In India is no exception to urbanization. In India, one

important reason for the migration of the rural population to the

metropolitan cities, apart from the fact that urban areas offer

better job opportunities appears to be that the development of

rural areas has lagged far behind, with the result that the rural

Page 3

Page | 176

population is attracted to the amenities and entertainment

facilities which are available in the cities.

Housing has, without exception, failed to keep pace with

staggering rate of migration in to the cities and inevitable result

has been unplanned growth of the cities and the consequent

growth of slums. A recent assessment of slums growth as

obtained by the Census of India indicates that more than 25 per

cent of the population of the urban areas is living in slums.

India, a land of colorful contrasts, had a population of about

120 millions at the time of Ashoka (22BC) and the population

remained almost static till the time of Akabar i.e. upto 17th century

AD (during 1901 Census India’s population was 236 million)2. In a

span of one century the population of India increased to 1210

millions in 2011. Planned urbanization is a necessary component

of the infrastructure of economic development as towns provide,

inter alia, a variety of centralized services for the surrounding

area.

Factors Responsible for Creation of Slums

Various factors influence the creation of slums in most of

the developing countries of the world. Some of the major

contributory factors responsible for the growth of slums especially

in Delhi during the early periods can be summarized as follows;

Page 4

Page | 177

1. In the early phase of industrialization, there is large-

scale migration to the cities due to employment

opportunities and other community facilities and

advantages offered by the city, which are absent in

majority of the rural areas of developed countries of

the world.

2. The poverty which means an income level which is

inadequate to maintain a decent standards of living

as judged by the standards of the society and low

paying capacity of the migrants, force them to find

refuge either in low rental areas or to squat on the

unused land located near their work places.

3. There is a housing shortage in urban areas due to

low level of income among the economically weaker

sections of the society, underprivileged sections of

the society, etc,.

4. Proximity of their houses, close to the source of

employment for economic reasons especially due to

the low level of transportation cost.

Page 5

Page | 178

5. Due to the high and fast growth of migration

especially from all rural areas of Indian territory to

the urban centers mainly searching for livelihood,

there is great strain on the existing transport system

and there is absence of cheap and rapid transport,

existing roads are not good for smooth

transportation as per the latest scientific

development of the mechanized vehicles to the work

place.

6. There is often absence of comprehensive

development planning and if it is there, it may not

have taken in to consideration the existing socio

economic conditions and requirements of the ever

growing population belonging to the economically,

politically weaker sections of the society.

7. There is always inadequate and insufficient

municipal civic amenities which increase to the

problems of the slum squatters and cause many

other problems. In addition to the above mentioned

the available municipal civic facilities are not

properly maintained and not functioning at the

appropriate time.

Page 6

Page | 179

8. The high rents accompanied by the evil high rates of

commission (premium required to be paid to secure

possession) in Delhi, have encouraged occupiers or

owners even of average dwelling unit to part with

portion of their buildings. These sub divisions of

small dwelling units have further added to

overcrowding and congestion.

Home is the place where people in general carry out the

basic domestic and personal functions of family life. Physical and

mental health, working efficiently, emotional security and social

status are likely to be influenced by housing conditions. The

dwelling is the oldest branch of building, from man’s first crude

solutions of his most pressing problems, protection from the

elements, wild beasts and human enemies. Acquisition of suitable

home is though, vital to the modern family, but an average family

cannot do so merely on its own initiative. Thus, housing is of

direct significance to the community and the nation.

No country in the world, developed or developing or under

developed is able to provide cheap and adequate accommodation

to the man, which is very essential to eliminate the menace of

slums. However, it will be too simplistic to say that slums owe

their origin to the shortage of houses alone. They emerge,

continue and grow because of serious imbalances in the social

Page 7

Page | 180

and economic set up. To control slums, we have to check these

imbalances otherwise nothing substantial is likely to be achieved.

Like poverty, it may be that slums will always be with us,

however energetic the local authorities may become in eliminating

these. But it must not be forgotten that even the slum landlord of

fiction has rights and owner of the slum or today is often a small

man or woman depending on few rents for a livelihood just above

social security level.

Thus, slums are not a new phenomenon with the

developed or developing or under developed countries. They

have existed, are existing and will remain with us perhaps for

quite a long time. The slums are the result of forces, events and

deficiencies in our socio economic structure. Industrialization and

urbanization especially in the development of secondary and

tertiary sectors during the last three decades in India are equally

responsible for the creation of slums.

Definition of Slums

The term slum is used in a loose sense to designate areas

which are overcrowded dilapidated, faultily laid out and generally

lacking in essential civic services. Slums have been defined as

poverty areas, run-down, overcrowded, inhabited by persons who

are not acceptable in other areas, characterized by unsanitary

Page 8

Page | 181

surroundings, high death rate and high delinquency and crime

rate. As it is generally known, there is no exact definition of the

term slums available and even various writers on the subject differ

on its fundamentals. From the available sources, it can be seen

that a slum has got the characteristics like sub standard housing,

thickly populated squalid part of the city, and overcrowded

neighbourhood inhabited by the poorest people. The Webster

International Dictionary narrates slum as a thickly populated street

or alley, especially one marked by squalor, wretched living

conditions, or degradation of its inhabitants.

Slum problem is not only a problem of shelter; it is a

problem of health and hygiene. A number of widespread epidemic

diseases emanate from the slums. These slums are not only a

nuisance and danger to the slum dwellers but to the rest of the

population. A slum is usually understood to be an area of

overcrowded squalid, closely built and unhygienic housing. Urban

slums rose in great numbers during the growth of industrial cities

and towns in the 19th century.

Thus, slums it appears that they stand for the wretched

socio economic conditions of the city life of the people who are

living in the filthy blight areas. The combination of words of

SLUM appears to have unconsciously acquired the modified form

of existing conditions in the abbreviated form if we take S for

Page 9

Page | 182

Shell, L for Languishing, U for Urban and M for Masses. Thus

the word slum denotes Shell of Languishing Urban Masses.

This clearly narrates the natural condition prevalent in any slum

area of the nation irrespective of developed or developing or

under developed.

Characteristics of Slums

On the basis of observation from slums, we can outline its

major characteristics, which are given below:

1. Appearance:

This may be called a universal mark of the slum; its aspect

of neglect and disorder with respect to building, yards and streets.

The appearance is generally one of dilapidated and old structures

and a declining trend in respect of amenities.

2. Economic Status:

Generally, the people of the lowest income group inhabit a

slum; although there may be occasional buildings of equally run

down appearance inhabited by families that are not so poor.

However, in general, poor people inhabit the slum.

3. Over-crowding:

We may find that the cluster is overcrowded. Most of the

buildings / tenements are crowded with the people. If the slum is

retreating many buildings are unsafe for habitation, but there can

be overcrowding in the building occupied. Uninhabited spaces

are occupied by undesirable occupants and use it as junkyards.

Page 10

Page | 183

4. Population:

In a slum of a heterogeneous occupancy many of the

inhabitants are not welcome in other residential areas, or they

cannot afford to live elsewhere. Thus, it may be a refuge area of

the homeless, socially mal adjusted.

5. Health and Sanitation:

For understandable reasons when compared with

other area of residence, the slum is characterized by low

standards of sanitation. The slum is often most neglected by the

public services for sanitation. For variety of reasons it may also

be an area of high sickness and death rates.

6. Morals:

The slums may be an area of delinquency, crime but this is

more likely to be true of the socially disorganized slum. While

such a slum may not be the habitat of successful criminals, it may

be the habitat of marginal types or the hiding place of fugitive

criminals.

7. Way of Life:

Slums differ widely with respect to the social organization

of their inhabitants. They range from the slums in which the

inhabitants are strangers to one another and wish to be, to the

family slum in which there is wide acquaintance between

inhabitants.

Page 11

Page | 184

8. Social Isolation:

Every residential area within the modern city tends to be

socially isolated from others, partly by choice and partly by

location, the slum is especially so. It is the area of lowest

status inhabited by slum dwellers.

Thus, the overcrowding in the cities, extensive slums,

broken homes, the frustration and despair of poverty, unfavorable

conditions in home and neighborhood, large number of

immigrants, high rate of unemployment, low socio economic

status and physical deterioration are the general characteristics of

the cities and all these have combined to create the situation in

the cities, in which a new inducement for crime and delinquency

have risen11. The common factors contributing to the creation of

slums are manifold like, low wages and poverty preventing people

from paying for decent dwellings; invasion of incompatible

business and commerce in to residential areas leading to neglect

of dwellings, unplanned growth of cities, lack of maintenance and

enforcement of building codes of failure to prosecute for housing

code violations; leniency towards the owners of dilapidated

property in tax assessment, and low standards in remodelling old

dwellings social or other restrictions limiting the location or quality

of housing available to certain group; non adoption and non

enforcement of regulations with respect to satisfaction and safety

by municipal governments and finally human apathy towards

Page 12

Page | 185

menace of slums. Therefore, a slum is characterized by a place

where basic necessities of life i.e. proper shelter, employment,

health, sanitation, education facilities etc are absent. In north

India especially in Delhi slums are often called jhugis, which

usually consists of mud wall and thatched roof. In India majority

of the slum people exist in metro-cities.

Lack of sanitation and inadequate civic basic facilities in

the overcrowded slum areas in majority of our metropolitan cities

help the growth of flies, mosquitoes, bugs, pigs, mice, etc, which

cause scores of diseases such as cholera, typhoid, malaria,

tuberculosis, etc, to which infants and children are easy prey. In

the congested and overcrowded areas people are keeping

rubbing shoulders with each other causing mental tension, which

manifests in social tensions leading to riots and various other

communal problems3. We have been facing the problem of these

due to the existence of large level of slum people in our

metropolitan areas and are obeying and following the rules of high

rich and politically linked people in their surrounding areas4. The

urban population and slum population of India and Delhi during

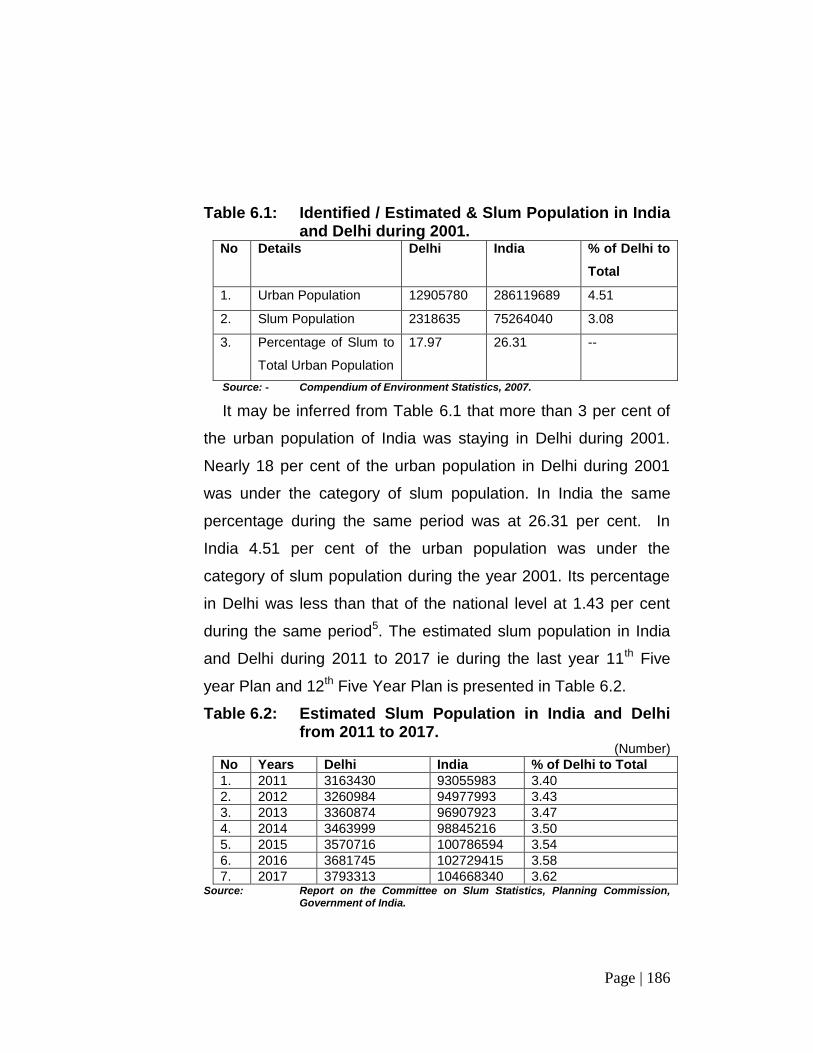

the 2001 is presented in Table 6.1.

Page 13

Page | 186

Table 6.1: Identified / Estimated & Slum Population in India and Delhi during 2001.

No Details Delhi India % of Delhi to

Total

1. Urban Population 12905780 286119689 4.51

2. Slum Population 2318635 75264040 3.08

3. Percentage of Slum to

Total Urban Population

17.97 26.31 --

Source: - Compendium of Environment Statistics, 2007.

It may be inferred from Table 6.1 that more than 3 per cent of

the urban population of India was staying in Delhi during 2001.

Nearly 18 per cent of the urban population in Delhi during 2001

was under the category of slum population. In India the same

percentage during the same period was at 26.31 per cent. In

India 4.51 per cent of the urban population was under the

category of slum population during the year 2001. Its percentage

in Delhi was less than that of the national level at 1.43 per cent

during the same period5. The estimated slum population in India

and Delhi during 2011 to 2017 ie during the last year 11th Five

year Plan and 12th Five Year Plan is presented in Table 6.2.

Table 6.2: Estimated Slum Population in India and Delhi from 2011 to 2017.

(Number)

No Years Delhi India % of Delhi to Total

1. 2011 3163430 93055983 3.40

2. 2012 3260984 94977993 3.43

3. 2013 3360874 96907923 3.47

4. 2014 3463999 98845216 3.50

5. 2015 3570716 100786594 3.54

6. 2016 3681745 102729415 3.58

7. 2017 3793313 104668340 3.62 Source: Report on the Committee on Slum Statistics, Planning Commission,

Government of India.

Page 14

Page | 187

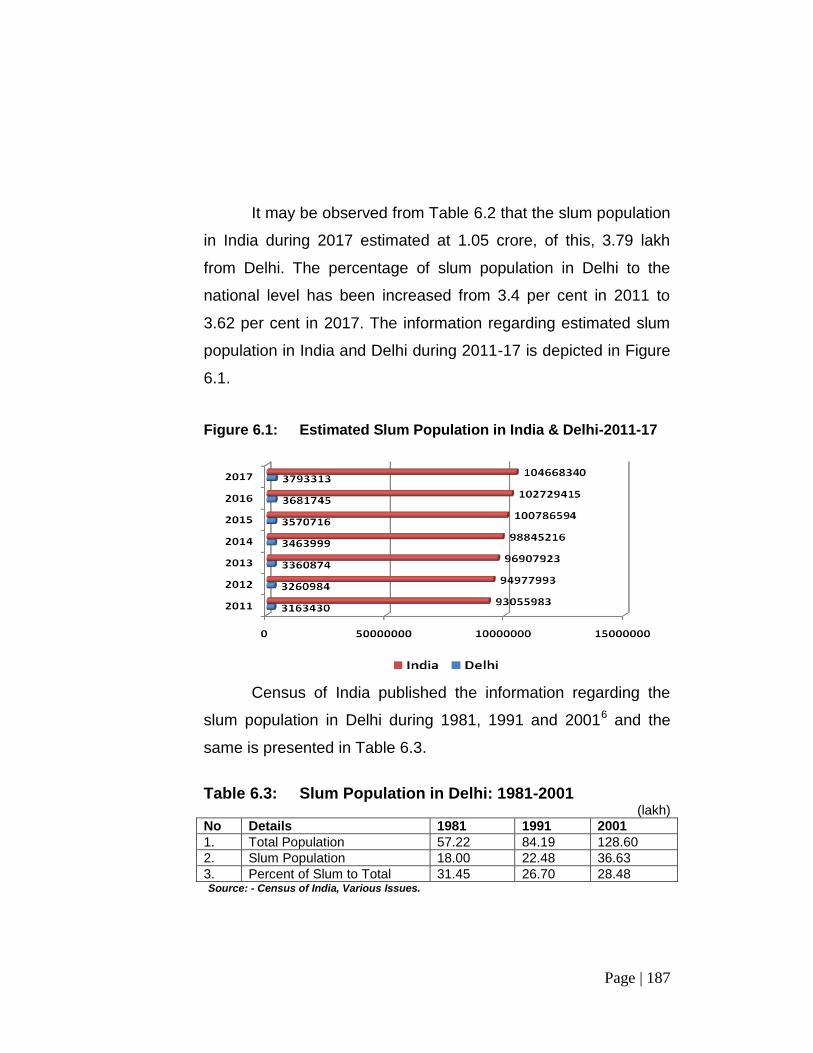

It may be observed from Table 6.2 that the slum population

in India during 2017 estimated at 1.05 crore, of this, 3.79 lakh

from Delhi. The percentage of slum population in Delhi to the

national level has been increased from 3.4 per cent in 2011 to

3.62 per cent in 2017. The information regarding estimated slum

population in India and Delhi during 2011-17 is depicted in Figure

6.1.

Figure 6.1: Estimated Slum Population in India & Delhi-2011-17

Census of India published the information regarding the

slum population in Delhi during 1981, 1991 and 20016 and the

same is presented in Table 6.3.

Table 6.3: Slum Population in Delhi: 1981-2001

(lakh)

No Details 1981 1991 2001

1. Total Population 57.22 84.19 128.60

2. Slum Population 18.00 22.48 36.63

3. Percent of Slum to Total 31.45 26.70 28.48 Source: - Census of India, Various Issues.

Page 15

Page | 188

It may be inferred from Table 6.3 that the slum population

in Delhi increased from 18 lakh in 1981 to 36.63 lakh in 2001

recorded an annual growth rate at 5.18 per cent. During the same

period the population growth rate outweighs the slum population

by 1.06 per cent per annum. Census of India also published the

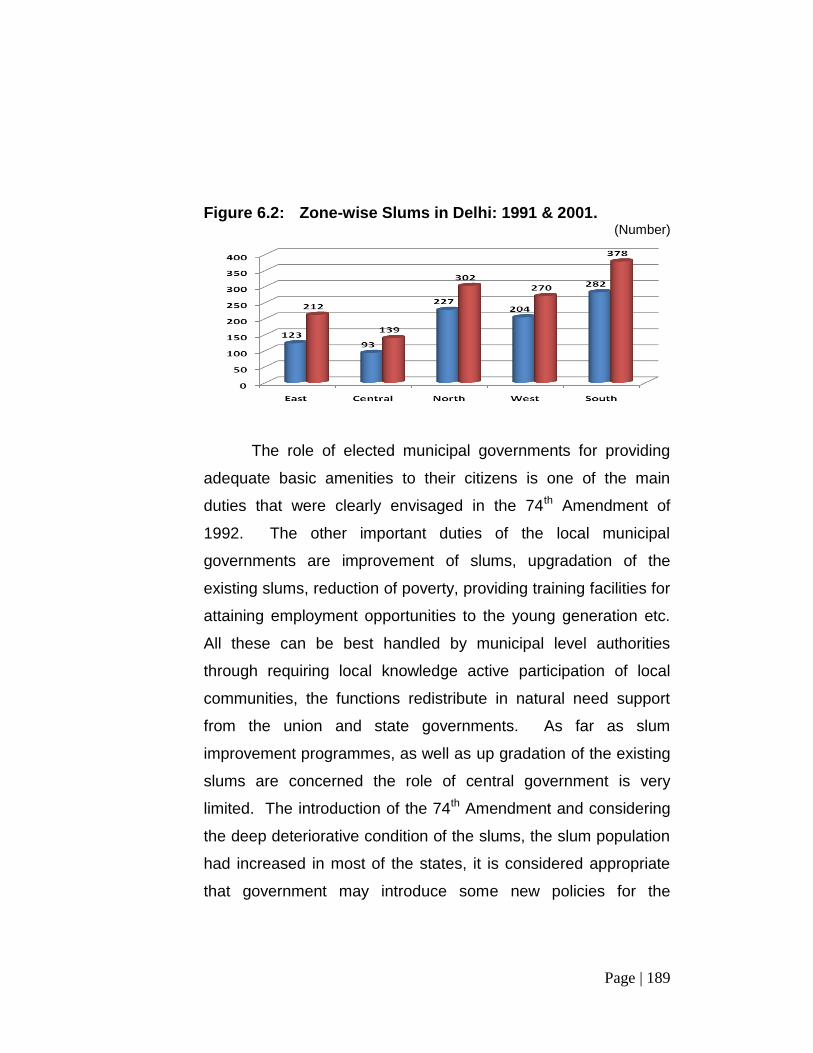

information regarding zone-wise number slums in Delhi7 during

1991 and 2001 and the same is presented in Table 6.4.

Table 6.4: Zone-wise Distribution of Slums in Delhi:

1991&2001.

(Number)

No Zones 1991 2001

No % No %

1 East 123 13.24 212 16.29

2 Central 93 10.01 139 10.68

3. North 227 24.40 302 23.21

4. West 204 22.00 270 20.75

5. South 282 30.35 378 29.05

Total 929 100.00 1301 100.00 Source: - Census of India.

It may be inferred from Table 6.4 that the number of slums

in south zone was higher during 1991 & 2001. During the same

period number of slums in Delhi increased from 929 in 1991 to

1301 in 2001. The zone-wise number of slums in Delhi is depicted

in Figure 6.2.

Page 16

Page | 189

Figure 6.2: Zone-wise Slums in Delhi: 1991 & 2001. (Number)

The role of elected municipal governments for providing

adequate basic amenities to their citizens is one of the main

duties that were clearly envisaged in the 74th Amendment of

1992. The other important duties of the local municipal

governments are improvement of slums, upgradation of the

existing slums, reduction of poverty, providing training facilities for

attaining employment opportunities to the young generation etc.

All these can be best handled by municipal level authorities

through requiring local knowledge active participation of local

communities, the functions redistribute in natural need support

from the union and state governments. As far as slum

improvement programmes, as well as up gradation of the existing

slums are concerned the role of central government is very

limited. The introduction of the 74th Amendment and considering

the deep deteriorative condition of the slums, the slum population

had increased in most of the states, it is considered appropriate

that government may introduce some new policies for the

Page 17

Page | 190

development of slums. he main factors behind the high rate of

growth of slums in cities are low wage level, poverty, unplanned

city growth and its planning, lack of all basic facilities, lack of

maintenance of existing facilities at the appropriate time, misuse

of existing facilities by a limited group of persons etc. These in

turn will create number of problems such as environmental

problems, especially pollution in air and water, various social

disorders, unhygienic living conditions etc.

In 2008-09, 65th Round of National Sample Survey

Organization under the Ministry of Statistics and Programme

Implementation conducted a survey regarding urban slums in

Delhi. The survey estimated that the number of urban slums in

Delhi during 2008-09 was at 43908. The following table clearly

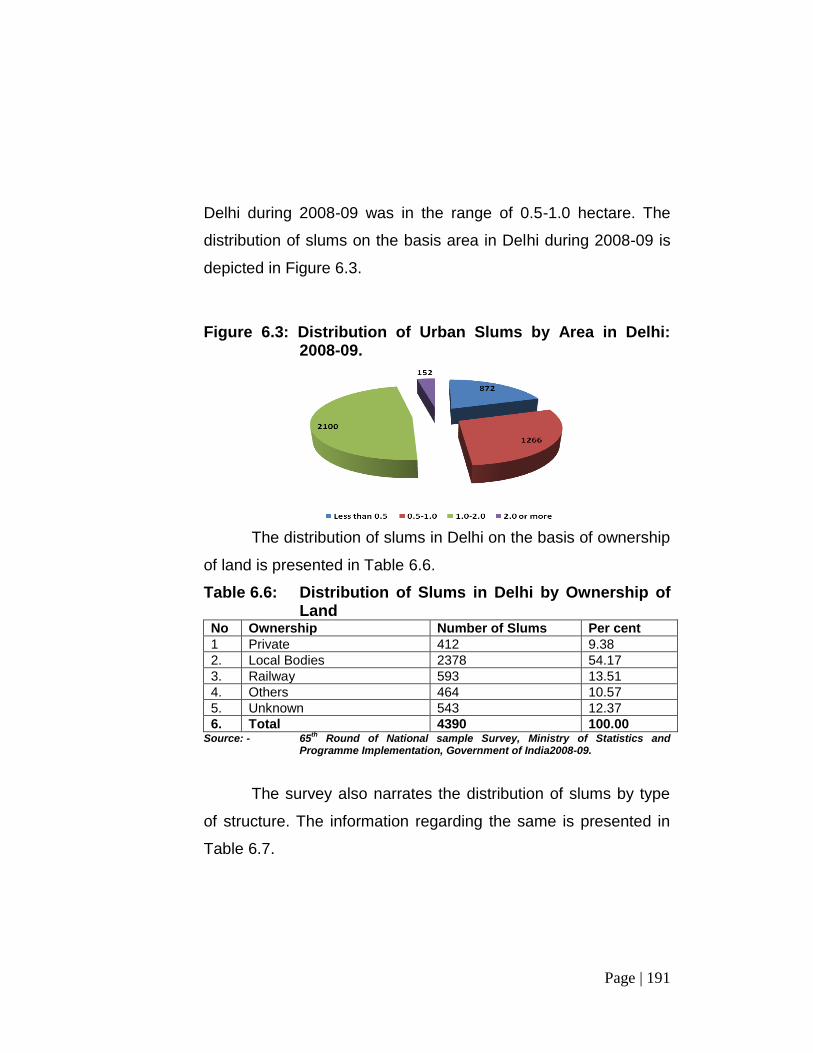

narrates the distribution of urban slums in Delhi during 2008-09.

Table 6.5: Distribution of Urban Slums by Area in Delhi:

2008-09 No Area (Hectare) No. of Slums Per cent

1 Less than 0.5 872 19.86

2. 0.5-1.0 1266 28.84

3. 1.0-2.0 2100 47.84

4. 2.0 or more 152 3.46

5. Total 4390 100.00 Source: - 65

th Round of National sample Survey, Ministry of Statistics and

Programme Implementation, Government of India2008-09.

It may be observed from Table 6.5 that near about one half

of the total urban slums area was in between one and two

hectares. While more than 28 per cent of the urban slums area in

Page 18

Page | 191

Delhi during 2008-09 was in the range of 0.5-1.0 hectare. The

distribution of slums on the basis area in Delhi during 2008-09 is

depicted in Figure 6.3.

Figure 6.3: Distribution of Urban Slums by Area in Delhi:

2008-09.

The distribution of slums in Delhi on the basis of ownership

of land is presented in Table 6.6.

Table 6.6: Distribution of Slums in Delhi by Ownership of Land

No Ownership Number of Slums Per cent

1 Private 412 9.38

2. Local Bodies 2378 54.17

3. Railway 593 13.51

4. Others 464 10.57

5. Unknown 543 12.37

6. Total 4390 100.00 Source: - 65

th Round of National sample Survey, Ministry of Statistics and

Programme Implementation, Government of India2008-09.

The survey also narrates the distribution of slums by type

of structure. The information regarding the same is presented in

Table 6.7.

Page 19

Page | 192

Table 6.7: Distribution of Slums in Delhi by Type of Structure.

No Type of Structure Number of Slums Per cent

1 Pucca 2184 49.75

2. Semi Pucca 1834 41.78

3. Serviceable Kutcha 372 8.47

4 Total 4390 100.00 Source- 65

th Round of National sample Survey, Ministry of Statistics and

Programme Implementation, Government of India2008-09.

The survey also mentioned that the basic facilities in the

urban households covering, safe drinking water, latrine facility,

electricity, etc. the information regarding the basic amenities

available to the urban slums in Delhi during 2008-09 is presented

in Table 5.8.

Delhi is one of the fast growing urbanized states in the

Indian union. The concentration of economic activities especially

in service sector attract the people from different parts of the

nation to the urbanized areas for employment, livelihood etc.

Delhi Urban Shelter Improvement Board is earmarked for the

development of slums and its activities in Delhi.

Delhi Urban Shelter Improvement Board (DUSIB) has

come in existence under Delhi Urban Shelter Improvement Board

Act, 2010 which has been passed by the Legislative Assembly of

the National Capital Territory of Delhi on the 01st April, 2010 and

has come in force by the orders of Hon'ble Lt. Governor of Delhi

on 1st July, 2010.

Page 20

Page | 193

Table 6.8: Basic Amenities Available in Urban Slums of Delhi.

No Details Number of Slums Per cent

1. Safe Drinking Water

a. Tap 3847 87.63

b. Hand Pump/ Tube Well 391 8.91

c. Others 152 3.46

d. Total 4390 100.00

2.

Latrine Facility

a. Owned 344 7.84

i. Septic Tank 344 7.84

b. Shared 270 6.15

i. Septic Tank 121 2.76

ii. Pit 74 1.68

iii. Service 75 1.71

c. Public/ Community 2901 66.08

i. Septic Tank 2294 52.26

ii. Pit 32 0.73

iii. Service 575 13.10

d. No Latrine 875 19.93

e. Total 4390 100.00

3. Electricity

a. Street Light & Household Use 2093 47.68

b. Household Use only 1284 29.25

c. Street Light Only 866 19.73

d. No Electricity 147 3.35

e. Total 4390 100.00 Source: - 65

th Round of National sample Survey, Ministry of Statistics and

Programme Implementation, Government of India2008-09.

DUSIB is primarily responsible for the qualitative

improvement of slum settlements and providing various kinds of

services for slum dwellers in the city9. It also undertakes works

relating to provision of shelters to the urban poor / slum dwellers

under the policy for relocation of slum and JJ dwellers, including

the provisions of built up flats under exceptional circumstances,

when the properties / katras become dangerous / unfit for human

Page 21

Page | 194

habitation. The main thrust is to provide minimal civic

infrastructural facilities like toilets, bathrooms and Basti Vikas

Kendras (Community Centres) in JJ Clusters.

The broad activities of DUSIB are as follows;

Construction, Management and Maintenance of Night Shelters.

Construction of low cost Housing under EWS for Slum dwellers under Jawahar Lal Nehru National Urban Renewal Mission(JNNURM)

Relocation of squatters.

In-situ up-gradation.

Environmental Improvement in Urban Slums.

Construction of Pay and Use Jansuvidha (Toilet) Complexes.

Construction of Basti Vikas Kendras / Community Halls.

Structural Improvement and Rehabilitation of Katras.

Containing the size of Jhuggi Clusters and Development of Shishu Vatikas.

Study and Preparation of Perspective Plans for Delhi Slums

Government of Delhi started a Plan Scheme in 1997-98 for

providing minimum civic services i.e construction of road,

roadside drain and filling up of low lying area so as to maintain

hygienic conditions in slum areas. Government of NCT of Delhi

has established a special fund for development of unauthorized

colonies with an outlay of Rs. 2800 crore10 for the Eleventh Five

Year Plan Period (2007-12) to meet the expense on provision of

water supply, sewerage, roads, drains, sanitation, street lighting

and electrification etc,.

Page 22

Page | 195

Delhi Government has provided plan funds of Rs 185.00

crore during 2010-11 under this plan scheme and an amount of

Rs. 128.77 crore have been spent up to March 2011. These

colonies now proposed to be regularized and a Board for

Unauthorized Colonies has been constituted under the

chairmanship of Hon’ble Chief Minister of Delhi, which will advise

Government of NCT of Delhi on the process of regularization of

these unauthorized colonies. A total 1639 applications were

received and provisional regularization certificates have been

issued to 1218 unauthorized colonies in, 2008.

Government of India recently announced a new scheme

called Rajiv Awas Yojana (RAY)11 under JNNURM for the slum

dwellers and the urban poor people envisages a ‘Slum-free city’

through the active participation of States/Union Territories to

tackle the problem of slums in cities. An amount of Rs.9.78 crore

has been received from the Government of India. The main

objectives are;

Bringing existing slums within the formal system and

enabling them to avail of the same level of basic

amenities as the rest of the town.

Redressing the failures of the formal system that lie

behind the creation of slums and

Tackling the shortages of urban land and housing that

keep shelter out of reach of the urban poor and force

Page 23

Page | 196

them to resort to extra-legal solutions in a bid to retain

their sources of livelihood and employment.

Under this scheme States/Union Territories have to

undertake preparatory activities of conducting slum survey,

mapping of slums, developing slum information system,

undertaking community mobilization, preparation of Slum-free

City/State Slum-free Plans before seeking support under Rajiv

Awas Yojana. The Government of NCT of Delhi has already

submitted a detailed proposal to the Government of India for

under taking slum survey, mapping of slums, developing slum

information system, undertaking community mobilization etc.,

The inception of slums or jhuggi jhopri clusters started with

the development of cities. In Delhi the formation of slums

observed even before Independence. The main reason behind

the formation of slum clusters was due to various factors such as

flow of migrants from neighboring states for livelihood and

employment. The condition was manageable before 1970 and

most of slums were resettled. After 1970, the high pace of

development of Delhi and slow development in other cities in

northern India automatically speeding up the flow of migration of

Delhi with a massive increase in slum clusters.

Page 24

Page | 197

The exact number of JJ Clusters was enumerated in a

survey conducted by Government of Delhi in 199012. The survey

report mentioned that there were 929 slum clusters and around

2.59 lakh households in Delhi. Delhi Urban Shelter Improvement

Board estimated the number of jhuggi jhopri clusters and slum

population of Delhi. The same was mentioned that around 643

slum clusters with 4 lakh households having a population of 20

lakh in Delhi. The Census 2001 also indicated about 20 lakh

persons residing in JJ Clusters of Delhi.

The Sub Mission II of the Jawaharlal Nehru National Urban

Renewal Mission (JNNURM) involves Basic Services to the Urban

Poor (BSUP) including the integrated housing and slum

development programme. The basic objectives are;

Focused attention to integrated development of

Basic Services to the Urban Poor in cities covered

under the mission.

Provision of Basic Services to Urban Poor including

security of tenure at affordable prices, improved

housing, water supply, sanitation and ensuring

delivery through convergence of other already

existing universal services of the Government for

education, health and social security. Care will be

Page 25

Page | 198

taken to see that the urban poor are provided

housing near their place of occupation.

Secure effective linkages between asset creation

and asset management so that the Basic Services

to the Urban Poor created in the cities are not only

maintained efficiently but also become self-

sustaining over time.

Ensure adequate investment of funds to fulfil

deficiencies in the Basic Services to the urban poor.

Scale up delivery of civic amenities and provision of

utilities with emphasis on universal access to urban

poor.

Under Sub Mission-II Basic Services to the Urban Poor

(BSUIP) of JNNURM, Government of India has so far approved

15 Projects in Delhi (10 Projects of DSIIDC, 1 Project of DDA and

4 Projects of Slum Wing of MCD) with an estimated cost of

Rs.1814.51 crore. Till 31st March 2011, 13528 flats have been

completed and 35768 flats are under construction stage. The

Delhi Urban Shelter Improvement Board has been established

and nominated as nodal agency for the implementation of scheme

of relocation/rehabilitation of jhuggi jhopri clusters in Delhi like

improvement of environment, relocation and in-situ development

of slums in Delhi. The Board has allotted 85 flats to the eligible

slum dwellers of 2 JJ clusters.

Page 26

Page | 199

Policy on Slums

1. The slums located in congested unhygienic areas of the

urban areas wherein equitable distribution of space is

not feasible shall be cleared and tenement schemes put

up.

2. Wherever in-situ development is feasible, such slums

be identified and taken up for in-situ improvement for

the provision of basic facilities to make the areas

habitable.

3. Wherever neither tenement scheme nor in-situ

development is feasible, rehabilitation & resettlement in

tenements in nearby locations be followed.

The urban poor have become an inevitable concomitant of

the development path of many countries including India, have

chosen or have been forced to choose. The poor in urban areas

not only prop up the economy, but they also help the city

governments make services economical because the poor offer

their labour at a very nominal rate. Imagine the city without the

poor malnourished loader, the scavenger and the conservancy

labour. Economically speaking, the urban poor make the city

living affordable and less costly than it would be. But seldom do

the not so poor care to help them to make their living affordable.

In order to be more meaningful, objectives and goals must be

translated into day-to-day practice in conjunction with the people

Page 27

Page | 200

facing problems. That requires both dedication and sacrifice on

the part of city government and its staff and of the non-

governmental organizations, self help groups and volunteers and

whose support is so essential in any effort to reach the un-

reached.

Thus, slum clusters huge number of squatters deal in

collecting and trading of inflammable items, which may cause a

fire hazard thus affecting the safety of the inhabitants and

neighborhood population especially during summer period. The

area is prone to mishap during the monsoon season when the

storm water mixed with over flow of sewer may cause spread of

epidemic, pollution of water and spread of disease keeping in

view the slums squatters in question. It is quite apparent that the

in situ up gradation is not feasible at the existing sites due to their

high density and locational hazards. The only course left to the

land owning agency is to relocate them to safer areas with

adequate physical and social infrastructure.

The dominant discourse portrayed the slum population

mainly as a problem and not as a resource for environmental

management and city development. The concerns of the slum

dwellers, their poverty and livelihood problems were excluded

from the center stages of the discourse, except in political

rhetoric. Few government efforts reached the slum dwellers in a

Page 28

Page | 201

positive manner. Strategies for slum development were made to

correspond to a generalized image of the slums and their role in

the city development, while aspects of the slums, which did not

correspond to this stereotype image or other sub discourse, were

suppressed. The diversity and dynamics of the evolving slum

societies were underplayed and neglected.

If accepted that the stereotype and dominant image of

slum dwellers characterized in this chapter reflected the real

nature of local dynamics nor captured well the causes and effects

of urban environmental degradation, more empirical research

would be needed to understand who the slum dwellers really are,

what diversity of interests and capacity they possess, and how

they could become engaged in formulating alternative urban

strategies. Through recent public consultations organized by

some research institutions, NGOs in collaboration with the

government bodies, new empirical findings have been brought to

the attention of a variety of stakeholders, finding that provide a

more diverse, realistic and positive image of the slum dwellers.

Such changes in images are today increasingly reflected in

more positive attitude to slum rehabilitation. By the local

government accepting to take responsibility for slum upgrading,

more positive attitude are likely to emerge since the aim would

now be to build on whatever capacity the slum dwellers have and

Page 29

Page | 202

what the local resources are available. The new agenda for urban

politics, as promoted by civil society groups and critical

researchers, it is precisely to move issue of poverty

empowerment of slum dwellers and partnerships between city

government and the people to the center stage of urban politics –

and thereby create a new dominant discourse.

Public debate is essential for effective transformation of the

slums discourse and adoption of alternatives and more fruitful

perspective by the parties concerned. A combination of research,

advocacy and public reform might be needed to promote greater

pluralism in the discourse. Empirical research and along these

lines would require more than a simple analysis of the discourse –

understood as an analysis of the confrontation between

constructed ideas and images. It would require an understanding

of the variety of social and institutional stakeholders concerned,

their views, interest and influence, and specific outcome of their

interaction with each other and the government. It would require

a focus on historical events and processes, open public debate –

informed by empirical research - is a necessary condition for the

emergence of good government policies and practice based, less

on ideology constructed myths and more on empirical realities.

Page 30

Page | 203

Trends in Land Prices

Research on urban land price changes in developing

nations involves a variety of data from different sources.

Generally, there is a lack of uniformity in the data sources and as

such comparability of data from various sources is difficult. It is

observed that the availability of data from different sources

formed basis for a particular methodology applied in land price

research. Hence the need is to examine more closely the relative

utility of major data sources available for taking up research in

changing land price scenario. Exploratory analysis and diagnosis

of each data source facilitate to rule out or accept certain data

points in urban land price study. Without this, one takes a

common platform where one can globally compare the findings of

one study with others. This leads to assertions and wide scale

generalizations such as that land prices are increasing at a rapid

rate or sky rocketing. Anecdotal assertions based on isolated on

highly selective cases may not be corroborated once analyzed

empirically.

A meaningful analysis of the land registration information is

required immediately, especially at a time when international

agencies and multi-national agencies like United Nation’s

Development Programme (UNDP), World Bank, International

Monitory Fund and various other organizations show a

considerable concern to extend tools for land and housing market

Page 31

Page | 204

management in developing nations in the world. In view of the

above World Bank stresses the desirability of developing nations

considering land price information as surrogates for land prices in

order that governments can then recoup service provisions, host

by ploughing back a proportion of land price change. Here in

India, data questions the applicability of associating registered

land prices with notional land price13.

The main advantage of collecting land price information is

to have information about land price changes also that occur at a

city wide level rather than simply explaining prices for very recent

deviations at the outskirts of the city. Land price information is

available through out the city in most of the developing nations in

the world. It is an important data but the need is to analyse the

data in a comprehensive manner to explore its potential.

Nature of Land Price Information

In India the land price data are available at the Tehsil office

(land registration office) with a breakup to the level of colonies,

mohallas, (The term mohalla is normally used for old settlements

that are mainly located in older areas of the city.) and villages

located within the city limits. There are usually two main data

sources at the land registration office or tehsil office level that

provide the land price information. The first main source

comprises confidential records of what can be termed as first level

Page 32

Page | 205

data. These are unpublished and contain basic details of

individual property transactions that have taken place in the city

over a period of time. These records have information on each

type of property transaction, ie. house and land (plot) and are

used by the state and private individuals for completing property

searches in order to ascertain plot or house ownership. One must

be careful with these data sources because of listings of the

house and land transactions are unsorted in the records.

Moreover there are many types of registrations for land and

house transactions. Types of registrations recorded in the

confidential records at the first level are numerous. For example,

registrations include gift deed, partition deed, errata, cancellation

of sale deed, surrender deed, re-conveyance deed, mortgage,

return of mortgage, rent deed, receipt, assignment deed,

agreement deed, sale deed, etc. With these records, what should

concern the researcher is the data for the plot sale, which have

been registered as a sale deed or agreement. These are the only

types of registration under which land is actually sold. In this

respect the data reflect land transactions that include;

(i) Plot size,

(ii) Declared price of the plot (also known as registered

price or the consideration money)

(iii) Valuation price as assessed by the officials of the

revenue department,

Page 33

Page | 206

(iv) Date of presentation of registry papers in the land

registration office/ tehsil office (i.e. the date the

transaction occurs)

(v) The date of registration in the land registration /

tehsil office

(vi) Name of the seller and buyer and

(vii) Location of the Plot in the colony.

For research purposes, access to this first level of

information can be obtained easily in a reasonable time14.

The tehsil /land registration office in India also collects the

information confidentially at the so called second level. These

contain explanatory details of each property transaction as cited

in the confidential report of the earlier mentioned first level. The

second level records are extremely voluminous and are

unpublished. Keeping in mind the time limits of the research it

may not be wise to opt for a data collection from the second level

over the confidential records of the first level. In addition, access

to the confidential report of the second level is less assured.

When the purpose of collecting land price information is partly met

by the confidential report of the first level, there seems little

practical gain in investing huge amount of time with the

confidential records of the second level.

Page 34

Page | 207

The third data source consists of open / public records.

This information is unambiguously in the public domain. It is

published data sources and contains city wide estimated land

prices. The main purpose of this information is to minimize the

under valuation of landed property in the registration office / tehsil

office and to raise the revenues. The fixing of these prices at city

level is largely contingent upon changes in land and revenue

policies over a period of time. Since these policies vary from

state to state; comparability of the price with the rate prices

remaining in other state is not straight forward or more

complicated or difficult or impossible. The rate is the minimum

market price of land expressed in terms of Rupees per unit of

land. It is determined on the basis of a sub set of example land

prices as informed by the property developers, colonizers, open

market sale deed and rates of urban development and housing

authorities in the state sector. Even knowing that the actual

market prices are always higher than the prescribed rate, the

latter are city wide kept to the minimum level. The government

has taken the conscious decision to maintain minimum price in

order not to discourage land registration at the concerned office.

Thus, given priority to extend registration rather than technical

accuracy of the land price value. In this way, it is expected that

revenue will be maximized and not lost through the failure to

register land by selling plots on a Power of Attorney basis.

Power of Attorney includes any instruments (not chargeable with

Page 35

Page | 208

a fee under the law relating to court fees for the time being in

force) empowering a specified person to act for and in the name

of person executing it.

Limitations of Land Price Information

The Information of Land Price available from the

confidential records of the Land Registration Office / tehsil office

is rarely intact or complete for every year. It is generally

maintained in hand written basis that are often found by the

researchers to be in a damaged form or illegible condition. It

depends upon the use to which these books / register have been

put, and that is normally contingent upon the number and the

frequency of the transaction of property in a year. It is a general

practice for lawyers, individuals and property developers to

enquire about the basic information of the property before

conveyance.

It is unlikely that the valuation price of each plot will be

shown throughout the confidential records of the first level.

Therefore, the information on the Registrar’s assessment value as

noted in the registers may not always be available. However,

even if sufficient registers were available, the comparability of the

assessment values would be weak in two aspects. The first is that

valuation prices determined before the stipulation of the circle

rates might be inconsistent since these were decided by the Chief

Page 36

Page | 209

Registrar under the Indian Stamp Act Rules. Though the rules are

quite clear for the plot valuation, actual plot valuation in the land

registration office is often quite arbitrary and idiosyncratic. It may

be adjusted so as to provide benefits to all concerned- the valuer,

the appropriator and the buyer. Underassessment of prices in the

land registration office records is almost universal. It is likely to

occur whenever taxation on land transaction is stringent and

particularly where it is high. Underassessment is not common for

the transactions of the state institutions or state based money.

The second reason for a lack of comparability in the data

sources is the addition of one –off statutory reassessments.

These reassessments are rarely applied evenly across the city

and thus affect a small subset of plots in colonies. They do

however, account for significant difference in the circle rates

among colonies, as some include the additional assessments

while others do not. Without an intimate knowledge of the city and

significant amounts of cross checking, it is difficult to control for

plots that have been subject to this assessment.

The records of the first level do not show the proper

address of the seller or buyer of the plot sold. They tell us about

the plot number and the situation on two sides of the plot. Since

the address of the plot owner is not recorded in the first level, it is

hardly possible to cross check the land prices of one plot (as

Page 37

Page | 210

recorded in the first level) to the same plot through a household

survey. Of course, an address can be obtained from the second

level records, but one has to overcome two problems; first, get

access through the officials, and second, the enormous amount of

time required in reviewing these records. Another complication is

that in most cases the plot number does not correspond to the

present house number, ie. Subdivisions are made on different

numbers, and once house are built, the local authorities often

assigns different numbers to the individual houses.

Factors Influencing Land Prices

The following factors determine the land price of urban

area of any country. They are:

a. Locational Advantage: - Whether the particular

land is adjacent to the main road or other important

roads, near to the public utility places constructed by

the urban local bodies/ development authorities /

Municipal corporations at the government cost of the

public exchequer.

b. Land use:- The value of the land significantly

increases as the land use assigned to a piece of

land in the plan changes from low importance to a

higher importance like from public street or park and

open space to a institutional or commercial or

official, etc,. The land owners thus benefit or suffer

Page 38

Page | 211

from the somewhat artificially determined and

externally imposed factors by which they are bound

even without there will.

c. Amenities: - The cost of the land changes from the

provision of infrastructural facilities by the urban

local bodies/ urban developmental authorities or

other service providing agencies in terms of facilities

like road, transport, communication, water supply,

sanitation, electricity, power, etc,.

d. Inherent Value: - It is related to the buildability on

building potential of the land in an urban area.

e. Floor Area Ratio (FAR):- It is an important factor

determining the market value of any land. For

example, if the planning authority increases the

FAR, the market value of the land almost doubles; if

it is increased three times, the market value also

trebles and so on. The owners of the land have no

contribution, whatsoever, that would justify their

appropriating all the benefits arising from the

enhancement of FAR for them.

f. Speculation: - Generally it is called scarcity value.

Whenever the demand is higher than the supply,

speculation arises. The fast rate of growth of

population and the development in urban areas

leads to a migratory movement of the people from

Page 39

Page | 212

rural areas to the cities; the demand for serviced

land perpetually outstrips its supply leading to ever

rising price of land. Whenever there is a scarcity,

there is a speculation and therefore, it would not be

incorrect to conclude that urban land prices include

high degrees of speculative factor.

g. Black market: - There is no secret that black market

value of any piece of land is far more than its value

in the legal market, mainly for exemption of stamp

duty, income, wealth and other taxes. There is thus,

a significant black market component attached to

the market value of urban land, as specified in the

documents in the records of sale transaction.

h. Changes in Interest Rate: - Decline in the interest

rate in the formal banking system is also another

important factor for changes in the price of land. It is

an inverse relation, that is, decline in the interest

rate in the banking system leads to enhancement of

investment in real estates and which in turn

increases the price of land and vice-versa.

i. Recent Developments of Service Sector: - The rapid

growth of Information Technology (IT), Information

Technology Enabled Services (ITES), Business

process Outsourcing (BPO), Special Economic

Zones (SEZ)15, Industrial Parks (IP), Foreign Direct

Page 40

Page | 213

Investment (FDI) and other service industries

handled by the multinational companies require lot

of space in the urban area. These companies are

purchasing the land at a higher rate than the market

forces of demand and supply of land16. This in turn

leads to increase in the price of land.

Thus, number of factors influences the price of urban land

whether it is for residential or commercial or industrial use. In

order to understand the causes as well as providing land for

residential purposes or residence mainly to economically and

socially weaker sections of the society, the policy makers,

academicians, researchers, social scientists, etc, need to know

the average price of land in particular city or area. In this

connection, the Research Scholar has undertaken a study on the

basis of random sample survey, supported by series of

discussions and interactions with the officials at the centre,

Government of National Capital Territory of Delhi, New Delhi

Municipal Council, Municipal Corporation of Delhi, Delhi

Cantonment Board, researchers, academicians, non-

governmental organizations, self help groups, consultants,

property dealers/developers, real estate agents, etc,.

Page 41

Page | 214

The information mentioned in this thesis narrates both

maximum and minimum land prices with the prevailing market

trend. The maximum and minimum land prices have been culled

out on the basis of locational advantage mainly the accessibilities

of various infrastructure facilities and other disadvantages of the

particular locality. The market value of land in Delhi was collected

from the well known real estate agents, their associations and

property dealers with the active co-operation of the Government

of NCT of Delhi, Delhi Development Authority and the like. The

whole area of Delhi was categorized into five zones namely

Central, North, South, East and West zones respectively. The

information regarding study of urban residential land has been

collected from 250 localities spread over five different zones in the

city and in each zone fifty localities covered for the purpose. It

covers both the minimum and maximum land prices of residential

land for six years from 2005 to 2010.

The information regarding the urban residential land price

of Delhi was derived in the units of Rupees per square ft. The

average residential land price of Delhi during 2005-2010 is

presented in Table 6.9.

Page 42

Page | 215

Table 6.9: Market Price of Residential Land in Delhi 2005-2010.

No Years Land Price (Rs./Sq. Mtr)

Minimum Maximum Average

1 2005 114608 139972 127290

2 2006 136588 165112 150850

3 2007 163110 199992 181550

4 2008 165828 200972 183400

5 2009 152080 180948 166514

6 2010 160028 191588 175808

Source: - Field Survey 2010.

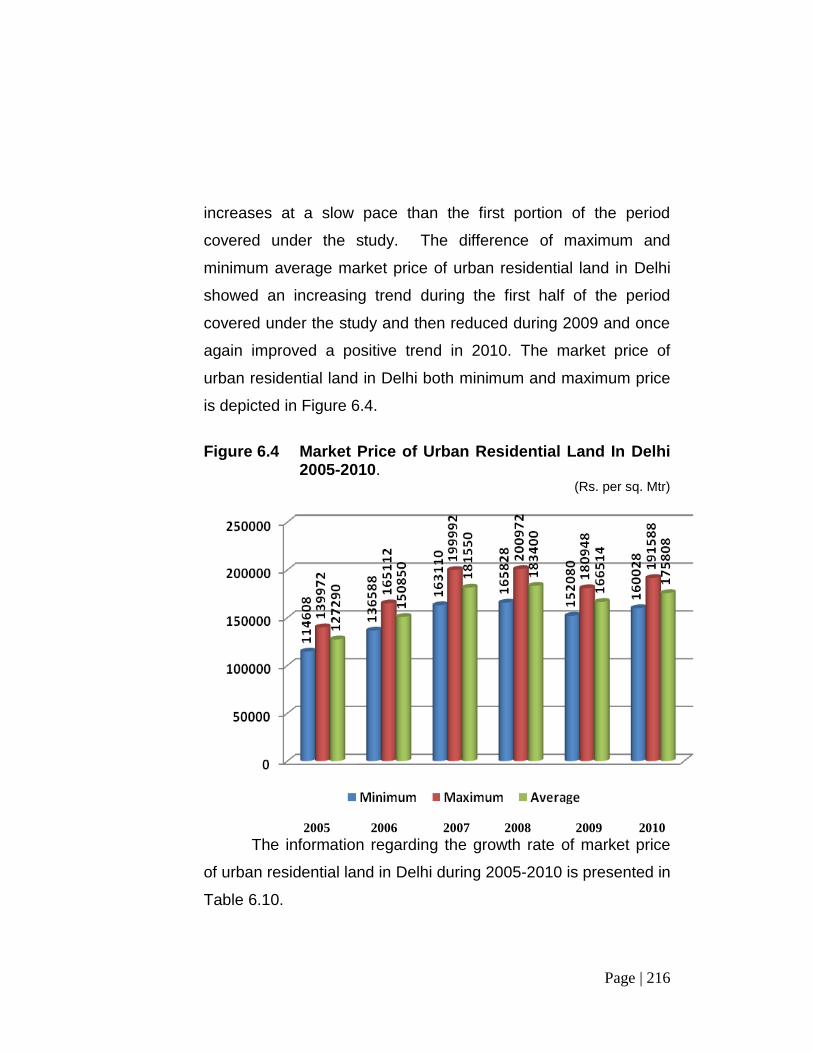

It may be observed from Table 6.9 that the average market

price of urban residential land increased from Rs. 127290 per sq.

mtr. in 2005 to Rs. 175808 per sq. mtr in 2010 recording an

annual growth rate of 6.35 per cent. During the same period the

minimum average market price of urban residential land

increased from Rs. 114608 per sq. mtr to Rs. 160028 per sq. mtr

recording an annual growth rate of 6.61 per cent. In the case of

the maximum average market price of residential land annual

growth rate is 6.15 per cent. The market price of urban residential

land in Delhi recorded highest during 2008. Due to economic

slowdown in the world economy, inflationary tendencies and

increase tendencies of prices of yellow metals in the world the

real estate prices showed a declining trend in during 2009. But

the timely intervention of Government and hopes for profit for

investing in real estate sector the prices of residential land

Page 43

Page | 216

increases at a slow pace than the first portion of the period

covered under the study. The difference of maximum and

minimum average market price of urban residential land in Delhi

showed an increasing trend during the first half of the period

covered under the study and then reduced during 2009 and once

again improved a positive trend in 2010. The market price of

urban residential land in Delhi both minimum and maximum price

is depicted in Figure 6.4.

Figure 6.4 Market Price of Urban Residential Land In Delhi

2005-2010. (Rs. per sq. Mtr)

2005 2006 2007 2008 2009 2010

The information regarding the growth rate of market price

of urban residential land in Delhi during 2005-2010 is presented in

Table 6.10.

Page 44

Page | 217

Table 6.10 Growth Rates of Market Price of Residential Land in Delhi.

No Years Growth Rates (Per Cent)

Minimum Maximum Average

1. 2005-06 19.18 17.96 18.51

2. 2006-07 19.42 21.13 20.35

3. 2007-08 1.67 0.50 1.02

4. 2008-09 -8.29 -9.96 -9.21

5. 2009-10 5.23 5.88 5.58

6. 2005-10 39.63 36.88 38.12

Source: - Field Survey 2010.

It may be observed from Table 6.10 that the growth rate of

average market price of residential land in Delhi during 2005-10

was recorded at 37.84 per cent. While the growth rate of average

maximum and minimum market price of residential land in Delhi

were at 36.88 per cent and 39.63 per cent respectively. In

minimum as well as maximum market price of urban residential

land in Delhi the growth in 2008-09 was lowest and recorded

negative growth as compared with the price of urban residential

land during the previous year covered under the study. Analysis

showed the growth of minimum market price of residential land

was the highest in 2006-07 but later on it increased at a lesser

rate and become negative in 2008-09 and once again increased

at a slow pace. Growth rate of maximum market price of

residential land in Delhi was the highest during 2006-07 which

witnessed reducing trend during the later period covered under

Page 45

Page | 218

the study including a negative growth during 2008-09. On an

average market price of residential land in Delhi showed an

increasing trend during 2005-2010; at an average growth rate of

6.35 per cent per annum.

The information regarding the growth of average market

price of urban residential land in Delhi including both minimum

and maximum prices during 2005-10 is depicted in Figure 6.5.

Figure 6.5: Growth of Urban Residential Land in Delhi during 2005-10

(Per Cent)

Page 46

Page | 219

Information regarding the market price of land is vital and is

one of the basic resources. Like any other resources, the

information on market price of land is also available in various

forms. Some people are in possession of it or have access to it

and others need it but do not have it. Those who have it can use

it, waste it, market it or else give it away. But it is useful and

hence its value will remain the same however much it is used; yet

it cannot be destroyed or corrupted. It can be transformed, yet it

remains with the transfer. It is indivisible, yet it can be

accumulated. It has tremendous importance both from the social

and cultural point of view but, on its own, it has been very material

use- its value is tangible only when the information on land prices

in the particular city is used for productive purposes like as a

module for policy formulation, valuation, implementation and

monitoring and evaluation of various policies introduced by the

government from time to time or we can say with other tangible

products. The policy makers, town planners, social scientists,

academicians and researchers dealt with the land price

information on various matters. Thus the information regarding

the land price is major information. There is a wide hierarchy of

needs for such information on land from the point of view of

sovereignty, defence, public safety, protecting the welfare of all

sections of the society.

.

Page 47

Page | 220

Table 6.11 Zone-wise Urban Residential Land Price in

Delhi: 2005-10.

(Rs. Per sq. Mtr)

No Years Central North South East West Total

1 2005

i. Min 238600 61400 153800 48140 71100 114608

ii. Max 278000 84100 182100 61460 94200 139972

iii. Av 258300 72250 167950 54800 82650 127290

2 2006

i. Min 271000 83500 183800 57840 86800 136588

ii. Max 311800 107700 218100 76060 111900 165112

iii. Av 291400 95600 200950 66950 99350 150850

3 2007

i. Min 317300 106100 214900 72140 105110 163110

ii. Max 365500 150600 251400 93360 139100 199992

iii. Av 341400 128350 233150 82750 122100 181550

4 2008

i. Min 319740 106900 225200 69400 107900 165828

ii. Max 370700 145200 261700 88460 138800 200972

iii. Av 345220 126050 243450 78930 123350 183400

5 2009

i. Min 292700 95100 210400 64700 97500 152080

ii. Max 335000 127400 242200 79540 120600 180948

iii. Av 313850 111250 226300 72120 109050 166514

6 2010

i. Min 313540 98220 215880 68700 103800 160028

ii. Max 365920 131860 247920 84540 127700 191588

iii. Av 339730 115040 231900 76620 115750 175808

Source: - Field Survey 2010.

Page 48

Page | 221

As already mentioned Delhi is divided into five zones for

the analysis of market value of land price in the city namely

central, north, east and west zones respectively. The information

regarding the market price of urban residential land in the above

mentioned zones in Delhi during the years 2005-10 is presented

in Table 6.11

It may be observed from Table 6.11 that the highest

average market price of urban residential land in Delhi during the

year 2010 was in Central Zone at Rs.339730 per Sq. Mtr. The

highest minimum and maximum market price of urban residential

land during 2010 was also observed in the same Central zone of

the city at Rs.313540 per sq. Mtr and Rs. 365920 per sq. mtr.

respectively. While the lowest average, minimum and maximum

market price of urban residential land in Delhi during the same

period covered under the study was observed in East Zone of

Delhi at Rs. 76620 per sq. mtr, Rs. 68700 per sq. mtr and

Rs.84540 per sq. mtr. respectively. The lowest and highest

average market price of urban residential land in Delhi during the

initial period covered under the study was also observed in

Central Zone and West Zone at Rs.258300 per sq. mtr and Rs.

54800 per sq. mtr. respectively. The minimum and maximum

market price of urban residential land in Central Zone during 2005

was observed at Rs.238600 per sq. mtr. and Rs. 278000 per sq.

Page 49

Page | 222

mtr. respectively. The minimum and maximum market price of

urban residential land in East Zone during 2005 was observed at

Rs.48140 per sq. mtr and Rs. 61460 per sq. mtr respectively. This

clearly indicates the fact that the development process, all other

basic facilities in East Zone was comparatively lesser and the

future scope for increasing the development activities in this zone

was gloomy. On the contrary the highest market price of urban

residential land in all the period covered under the study showed

highest in Central Zone of Delhi; which in turn implies that the

highest level of infrastructure facilities in the Indian Union. All the

basic facilities are available within in the Central Zone itself. In

addition this zone is the nerve of Indian system; occupies

residences or offices of India’s top political, economic,

representatives of foreign dignitaries, etc. While other zones of

Delhi are having high potential for the growth and development as

compared with other parts of India and the residential prices are

also showed the indicator for the speedy development in these

zones.

The information regarding zone-wise ie. Central, North,

South, East and West Zones growth rates of market price of

urban residential land in Delhi during 2005-b 10n is presented in

Table 6.12.

Page 50

Page | 223

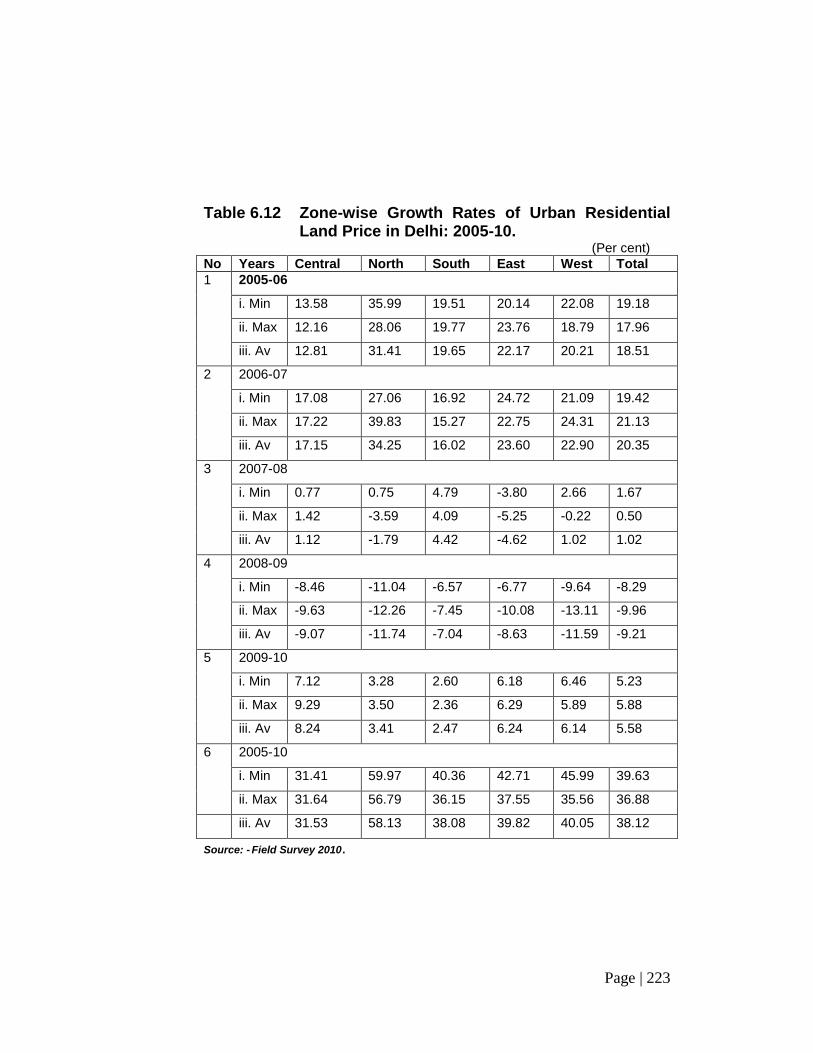

Table 6.12 Zone-wise Growth Rates of Urban Residential Land Price in Delhi: 2005-10.

(Per cent)

No Years Central North South East West Total

1 2005-06

i. Min 13.58 35.99 19.51 20.14 22.08 19.18

ii. Max 12.16 28.06 19.77 23.76 18.79 17.96

iii. Av 12.81 31.41 19.65 22.17 20.21 18.51

2 2006-07

i. Min 17.08 27.06 16.92 24.72 21.09 19.42

ii. Max 17.22 39.83 15.27 22.75 24.31 21.13

iii. Av 17.15 34.25 16.02 23.60 22.90 20.35

3 2007-08

i. Min 0.77 0.75 4.79 -3.80 2.66 1.67

ii. Max 1.42 -3.59 4.09 -5.25 -0.22 0.50

iii. Av 1.12 -1.79 4.42 -4.62 1.02 1.02

4 2008-09

i. Min -8.46 -11.04 -6.57 -6.77 -9.64 -8.29

ii. Max -9.63 -12.26 -7.45 -10.08 -13.11 -9.96

iii. Av -9.07 -11.74 -7.04 -8.63 -11.59 -9.21

5 2009-10

i. Min 7.12 3.28 2.60 6.18 6.46 5.23

ii. Max 9.29 3.50 2.36 6.29 5.89 5.88

iii. Av 8.24 3.41 2.47 6.24 6.14 5.58

6 2005-10

i. Min 31.41 59.97 40.36 42.71 45.99 39.63

ii. Max 31.64 56.79 36.15 37.55 35.56 36.88

iii. Av 31.53 58.13 38.08 39.82 40.05 38.12

Source: - Field Survey 2010.

Page 51

Page | 224

It may be observed from Table 6.12 that the highest growth

rates of market price of urban residential land in Delhi during the

period covered under the study was observed in north zone of

Delhi at 9.69 per cent per annum. The reason behind the fast

growth rates in this zone was due to various reasons such as fast

development during the last decade, opening up of metro

corridors, high level of infrastructure facilities, initiating various

developmental activities such as SEZs, industrial parks etc,.

While the lowest growth rates of market price of urban residential

land in Delhi during the period covered under the study was

observed in central zone at 5.26 per cent per annum. This zone

has already reached the saturated level and the availability of

land in this zone is rare. In addition the cost of land in central

zone of Delhi was comparatively higher than in all other zones in

Delhi and a good percentage of buyers compelled to purchase

the land from other zones. The second, third and fourth positions

of growth of market price of urban residential land in Delhi was

observed in west, east and south zones respectively at 6.68 per

cent, 6.64 per cent and 6.35 per cent per annum respectively

during the period covered under the study.

The highest average market price of urban residential land

in Delhi during the year 2010 was observed in CP Barakhamba

Road and Teen Murti of central zone of Delhi at Rs. 515000 per

sq. mtr. The highest minimum market price of urban residential

Page 52

Page | 225

land in Delhi during the same period was observed in CP

Barakhamba Road of Central Zone of Delhi at Rs. 500000 per Sq.

mtr and highest maximum urban residential land was observed in

Teen Murti of central Zone of Delhi at Rs. 540000 per Sq. mtr.

respectively. On the contrary, the lowest minimum, maximum and

average market price of urban residential land in Delhi during

2010 was recorded in Ghonda of east Zone of Delhi at Rs.18000

per sq. mtr, Rs.32000 per sq. mtr and Rs. 25000 per Sq. mtr

respectively. This clearly indicates the fact that there was a wide

gap of price of urban residential land both minimum and

maximum in Delhi during the period covered under the study. This

may be due to various reasons such as availability of various

infrastructure facilities, speculation of the people for future

development, introduction of metro corridors, state intervention

especially in the introduction of special economic zones, industrial

parks, export oriented units, institutes of high excellence, etc,.

In central zone of Delhi the highest maximum market price

of urban residential land was observed in Teen Murti area at Rs.

540000 per sq. mtr. during the year 2010 while the highest

minimum market price of urban residential land was observed in

CP Barakhamba Road at Rs. 500000 per sq. mtr. The lowest

minimum market price of urban residential land in central zone of

Delhi during 2010 recorded in Yamuna Bazar at Rs. 132000 per

sq. mtr. and lowest maximum market price of urban residential

Page 53

Page | 226

land in Delhi during the same period recorded at Rs. 180000 per

Sq. mtr. in three localities namely Mori Gate, Mandir Marg and

Yamuna Bazar respectively. The lowest average market price of

urban residential land in central zone of Delhi during 2010 was

observed in Yamuna Bazar at Rs. 165000 per sq. mtr.

In north zone of Delhi, the highest maximum market price

of urban residential land during the year 2010 was observed in

Ashok Vihar and Kamala Nagar at Rs. 205000 per sq. mtr and

lowest at Rs.45000 per sq. mtr. in Gandhi Vihar. The highest and

lowest minimum market prices at Rs. 155000 per sq. ft and Rs.

22000 per sq. mtr were observed in Ashok Vihar and Sant Nagar

Burari localities respectively. The highest difference between the

maximum and minimum market price of urban residential land in

northern zone of Delhi was observed in GTB Nagar locality and

lowest at Nirankari Colony during the same period covered under

the study.

In south zone of Delhi, the highest maximum, minimum

and average market price of urban residential land was observed

in Khan Market/ Lodi Colony during the year 2010 at Rs. 452000

per sq. mtr, Rs. 425000 per sq. mtr and Rs. 438500 per sq. mtr.

respectively. The lowest maximum, minimum and average market

price urban residential land in south zone of Delhi was recorded in

Methapur locality at Rs. 55000 per sq. mtr, Rs.45000 per sq.mtr.

Page 54

Page | 227

and Rs.50000 per sq. mtr. respectively during the same period

covered under the study. The highest difference between the

maximum and minimum market price of urban residential land in

this zone was observed in Vasant Vihar at Rs. 105000 per sq.

mtr. and lowest of Rs. 5000 per sq. mtr at Tara Apartment

respectively.

The highest maximum, minimum and average market price

of urban residential land in east zone of Delhi during the year

2010 was observed in Preet Vihat at Rs. 255000 per sq. mtr, Rs.

215000 per sq.mtr and Rs. 235000 per sq. mtr. respectively. On

the other hand the lowest minimum, maximum and average

market price of urban residential land was recorded at Rs. 18000

per sq. mtr, Rs. 32000 per sq.mtr. and Rs. 25000 per sq.mtr. in

Ghonda locality and this is lowest recorded market price of urban

residential land in entire Delhi. The difference between the

maximum and minimum market price of urban residential land

recorded highest in Karkardumma at Rs. 43000 per sq. mtr. and

lowest in three localities namely Pandav Nagar, Shasthri Nagar

and Wazirabd at Rs. 5000 per sq. mtr.

The information regarding the market price of urban

residential land both minimum and maximum price of 250

selected localities during 2005- 2010 is presented in Annexure 1.

The information regarding the price range-wise market price of

Page 55

Page | 228

urban residential land in Delhi during the year 2010 is presented

in Table 6.13.

Table 6.13: Price Range-wise Distribution of Localities in

Delhi during 2010. No Price Range(Rs. Per sq.mtr) No. of Localities

Minimum Maximum

1. Up to 74999 52 (20.80) 31 (12.40)

2. 75000-149999 98 (39.20) 86 (34.40)

3. 150000-224999 32 (12.80) 49 (19.60)

4. 225000-299999 29 (11.60) 26 (10.40)

5. 300000+ 39 (15.60) 58 (23.20)

Total 250 (100.00) 250(100.00)

Source: - Field Survey 2010. Note: Figures in parenthesis relate to percentage to total.

It may be observed from Table 6.13 that three fifth of the

localities, the minimum price was up to Rs. 149999 per sq. mtr.

during the last period covered under the study .ie. in 2010. While

the remaining three price range-wise classification, the highest

number of localities lies in the range of above Rs. 3 lakh per sq.

mtr. at 15.6 per cent. The other two ranges contribute 12.8 per

cent and 11.6 per cent of the price of localities. On the other hand

the maximum price, the highest percentage of localities land price

was in the Near about one fourth of the localities maximum

market price of urban residential land was in the highest price

range of Rs. 3 lakh per sq. mtr. or more. Like-wise the lowest

price range category had less number of localities in maximum

land price and this constituted on 12.40 per cent of the total

Page 56

Page | 229

localities covered under the study. The information regarding the

distribution of land price of Delhi on the basis of price-range

during 2010 is depicted in Figure 6.6

Figure 6.6: Price Range-wise Distribution of Localities in Delhi during 2010.

The information regarding the distribution of land price of

Delhi on the basis of price-range during 2005-2010 is presented

in Table 6.14.

Page 57

Page | 230

Table 6.14: Price Range-wise Distribution of Localities in Delhi during 2005-2010.

No Years No. of Localities/ Price Range (Rs. Per sq. mtr.) Upto 74999

74999-149999

150000- 224999

225000- 299999

300000+ Total

1. 2005

Min 116 (46.40)

68 (27.20)

33 13.20)

12 (4.80)

21 (8.40)

250 (100.00)

Max 69 (27.60)

92 (36.80)

40 (16.00)

19 (7.60)

30 (12.00)

250 (100.00)

2. 2006

Min 74 (29.60)

84 (33.60)

40 (16.00)

24 (9.60)

28 (11.20)

250 (100.00)

Max 40 (16.00)

99 (39.60)

43 (17.20)

28 (11.20)

40 (16.00)

250 (100.00)

3. 2007

Min 50 (20.00)

88 (35.20)

52 (20.80)

24 (9.60)

36 (14.40)

250 (100.00)

Max 26 (10.40)

81 (32.40)

59 (23.60)

30 (12.00)

54 (21.60)

250 (100.00)

4. 2008

Min 49 19.60)

92 (36.80)

38 (15.20)

32 (12.80)

39 (15.60)

250 (100.00)

Max 26 (10.40)

76 (30.40)

62 (24.8)

19 (7.60)

67 (26.80)

250 (100.00)

5. 2009

Min 60 (24.00)

92 (36.80)

38 (15.20)

28 (11.20)

32 (12.80)

250 (100.00)

Max 38 (15.20)

80 (32.00)

54 (21.60)

30 (12.00)

48 (19.20)

250 (100.00)

6. 2010

Min 52 (20.80)