38

1 Small Company Reporting Issues Presented by John Selwood

1

Small Company Reporting Issues

Presented by John Selwood

2

Highlights

Changes to the companies

regime

New FREDs and overview

S413 disclosures

Provisions The problem with goodwill

3

Small company draft regulations issued

4

•PC 1 January 2016

•Early adoption from 1 January 2015 permitted

NEW PROPOSALS

Implementation

5

6

• Turnover and short periods

• ‘Balance sheet total’

• Average employees

Size thresholds

7

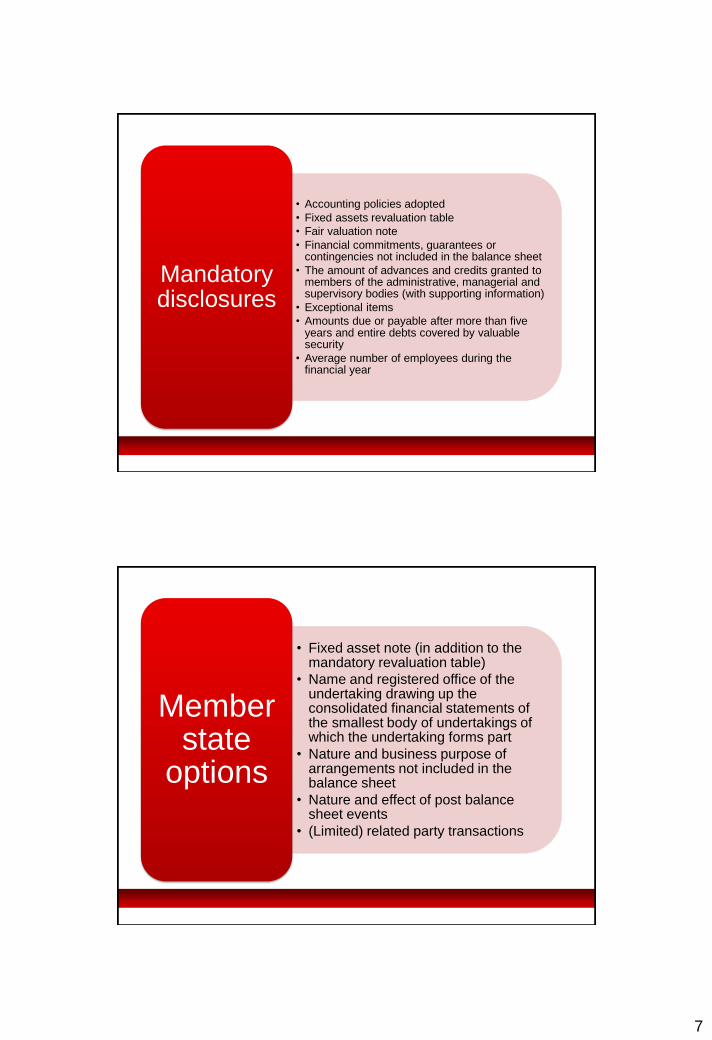

• Accounting policies adopted

• Fixed assets revaluation table

• Fair valuation note

• Financial commitments, guarantees or contingencies not included in the balance sheet

• The amount of advances and credits granted to members of the administrative, managerial and supervisory bodies (with supporting information)

• Exceptional items

• Amounts due or payable after more than five years and entire debts covered by valuable security

• Average number of employees during the financial year

Mandatory disclosures

• Fixed asset note (in addition to the mandatory revaluation table)

• Name and registered office of the undertaking drawing up the consolidated financial statements of the smallest body of undertakings of which the undertaking forms part

• Nature and business purpose of arrangements not included in the balance sheet

• Nature and effect of post balance sheet events

• (Limited) related party transactions

Member state

options

8

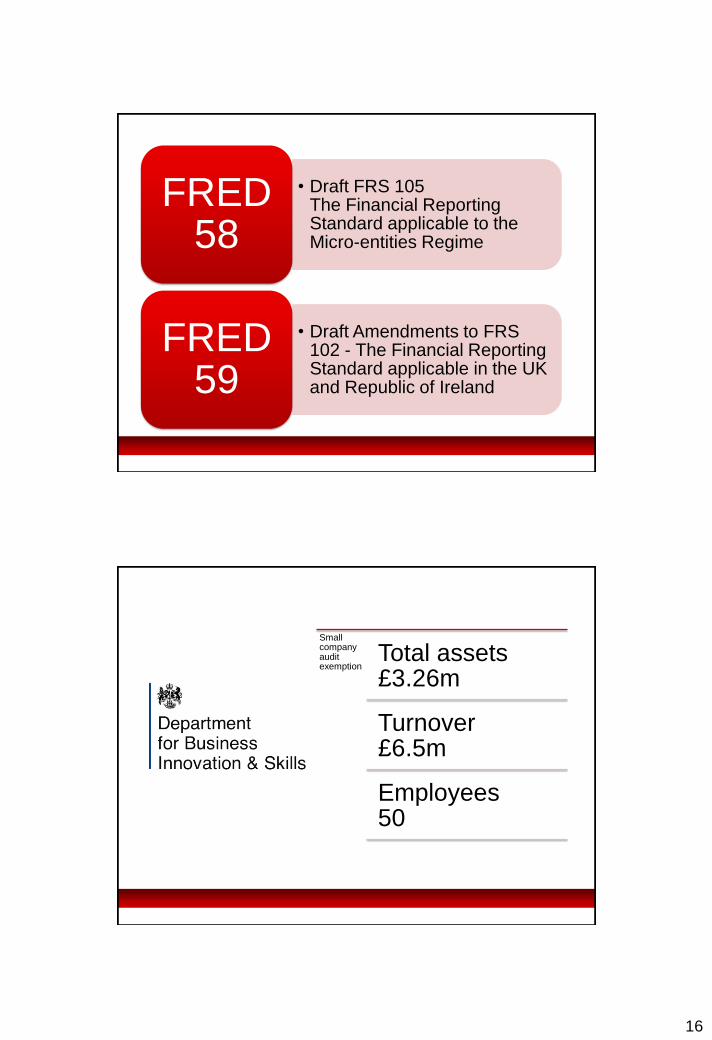

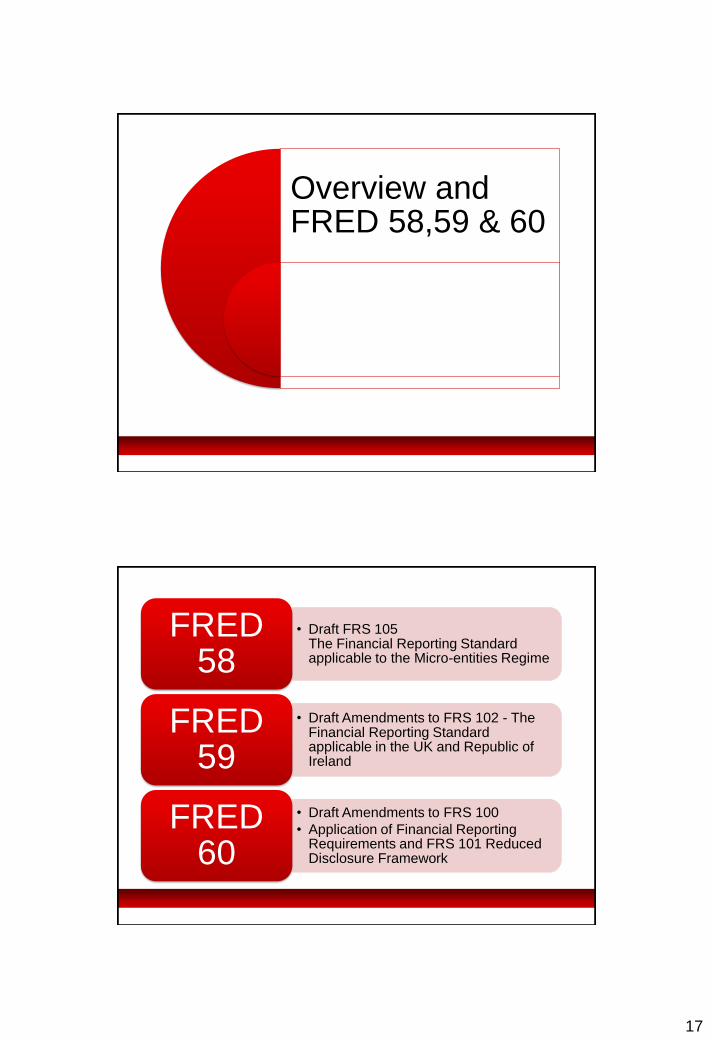

• Draft FRS 105 The Financial Reporting Standard applicable to the Micro-entities Regime

FRED 58

• Draft Amendments to FRS 102 - The Financial Reporting Standard applicable in the UK and Republic of Ireland

FRED 59

9

10

True & Fair view!

11

12

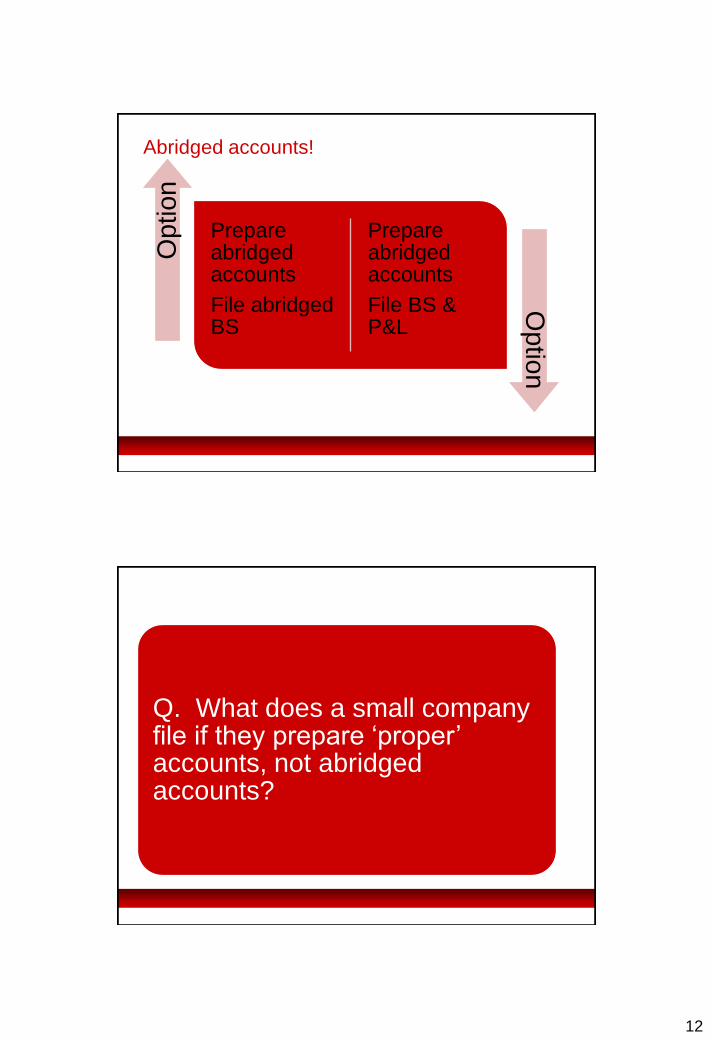

Prepare abridged accounts

File abridged BS

Prepare abridged accounts

File BS & P&L

Op

tio

n

Op

tion

Abridged accounts!

Q. What does a small company file if they prepare ‘proper’ accounts, not abridged accounts?

13

….the Regulations require the consent of ALL members when it comes to drawing up the abridged accounts.

… and deliver to the Registrar a statement that all the members have consented to the abridgement .

• If an abridged P&L is filed, the audit report is filed with it

• If just the abridged balance sheet is filed, do not file the audit report but the directors make disclosures instead

What if a small

company is

audited?

14

PIEs PLCs

Useful economic

life?

20

10 5

15

• the nature of the business purpose

• the financial impact of the

• small only discloses first item.

Off balance sheet

arrangements

• all companies disclose average number of employees

• small companies do not analyse by function

• directors rem disclosure unchanged

Employee numbers

• additional disclosure:

• any amounts written off

• any amounts waived

S413 Advances, credits &

guarantees

Directors’ report abolished for micros!

16

• Draft FRS 105 The Financial Reporting Standard applicable to the Micro-entities Regime

FRED 58

• Draft Amendments to FRS 102 - The Financial Reporting Standard applicable in the UK and Republic of Ireland

FRED 59

Small company audit exemption

Total assets £3.26m

Turnover £6.5m

Employees 50

17

Overview and FRED 58,59 & 60

• Draft FRS 105 The Financial Reporting Standard applicable to the Micro-entities Regime

FRED 58

• Draft Amendments to FRS 102 - The Financial Reporting Standard applicable in the UK and Republic of Ireland

FRED 59

• Draft Amendments to FRS 100

• Application of Financial Reporting Requirements and FRS 101 Reduced Disclosure Framework

FRED 60

18

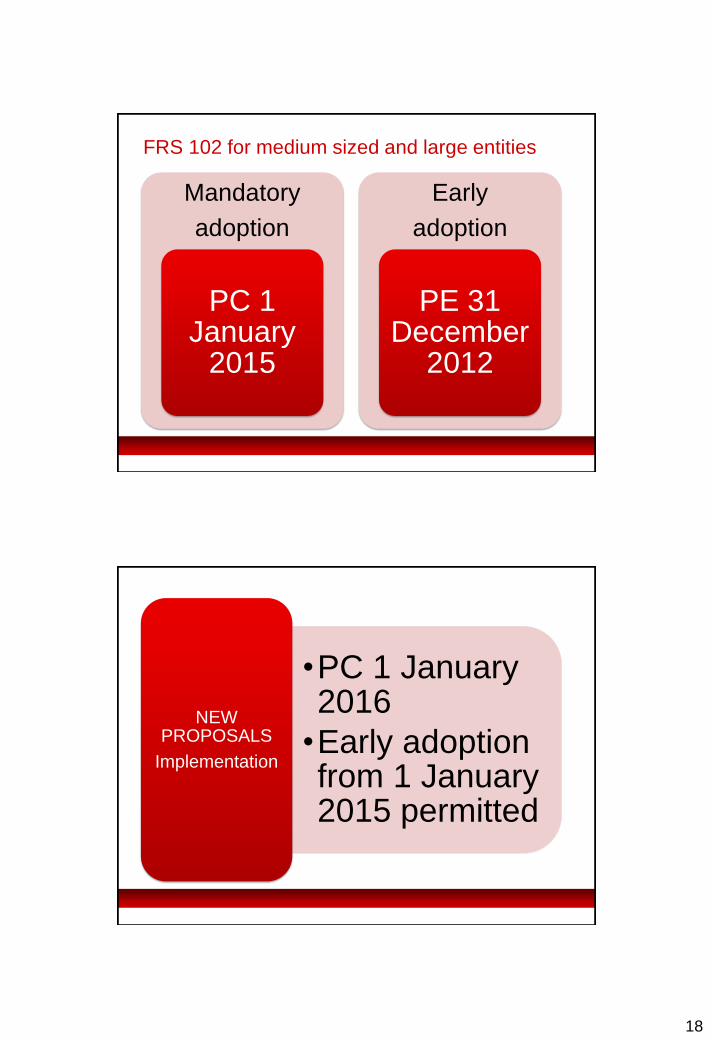

Mandatory

adoption

PC 1 January

2015

Early

adoption

PE 31 December

2012

FRS 102 for medium sized and large entities

•PC 1 January 2016

•Early adoption from 1 January 2015 permitted

NEW PROPOSALS

Implementation

19

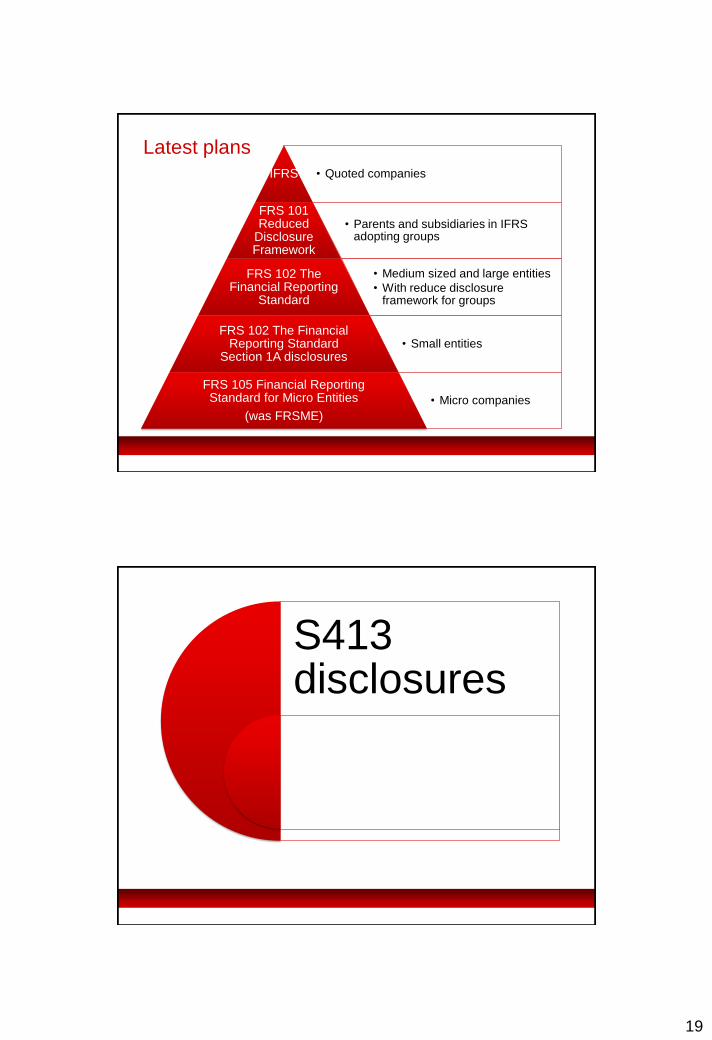

• Quoted companies IFRS

• Parents and subsidiaries in IFRS adopting groups

FRS 101 Reduced

Disclosure Framework

• Medium sized and large entities

• With reduce disclosure framework for groups

FRS 102 The Financial Reporting

Standard

• Small entities FRS 102 The Financial

Reporting Standard Section 1A disclosures

• Micro companies

FRS 105 Financial Reporting Standard for Micro Entities

(was FRSME)

Latest plans

S413 disclosures

20

Micro company regime

• 30th Sept 2013 YE

• Accounts file after Dec 2013 When?

• Turnover is not more than £632,000

• Gross assets is not more than £316,000

• Employees does not exceed 10 Who?

• Abridged P&L and BS – no notes

• S413 and o/s obligations disclosure

• S444 accounts filed with Registrar What?

21

Vo

tin

g

Yes

No

In practice do you disclose these transactions in

the abbreviated accounts?

22

23

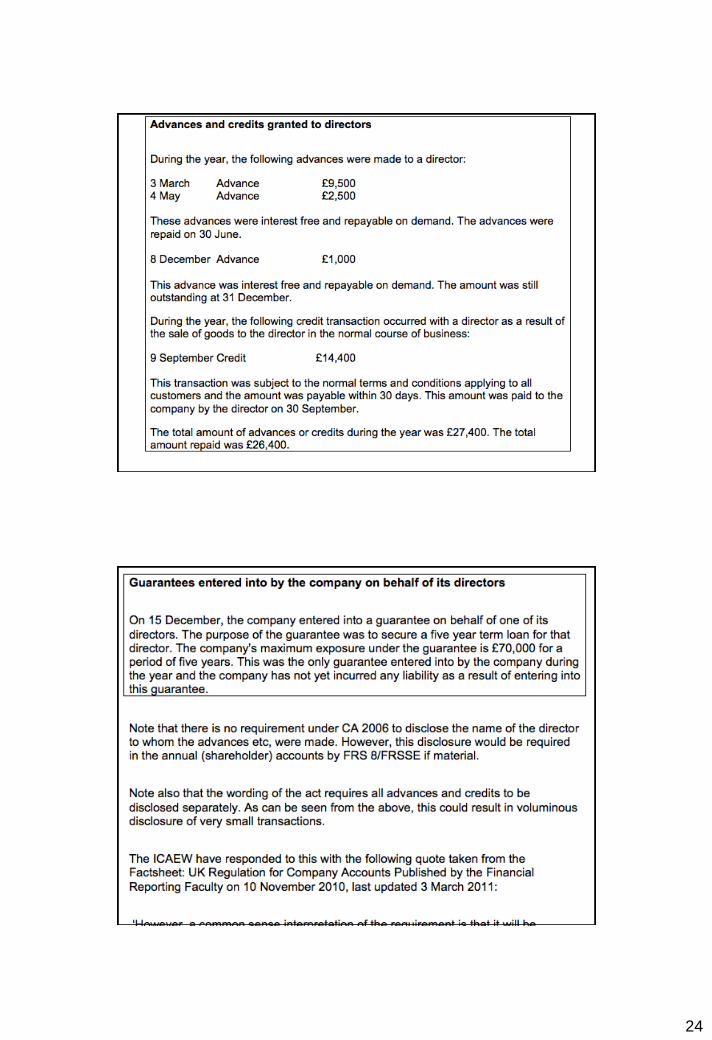

s413 Disclosure requirements

• its amount,

• an indication of the interest rate,

• its main conditions, and

• any amounts repaid.

Credits and advances

• its main terms,

• the amount of the maximum liability that may be incurred by the company (or its subsidiary), and

• any amount paid and any liability incurred by the company (or its subsidiary) for the purpose of fulfilling the guarantee (including any loss incurred by reason of enforcement of the guarantee).

Guarantees

24

25

Vo

tin

g

Yes

No

In practice do you aggregate S413 disclosure?

26

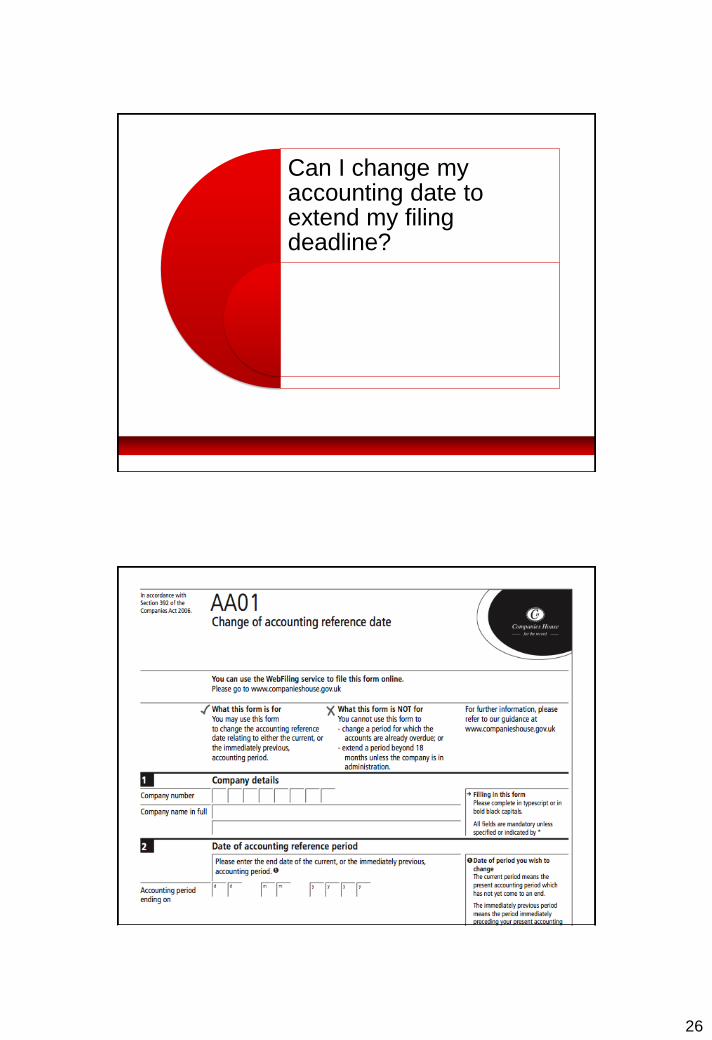

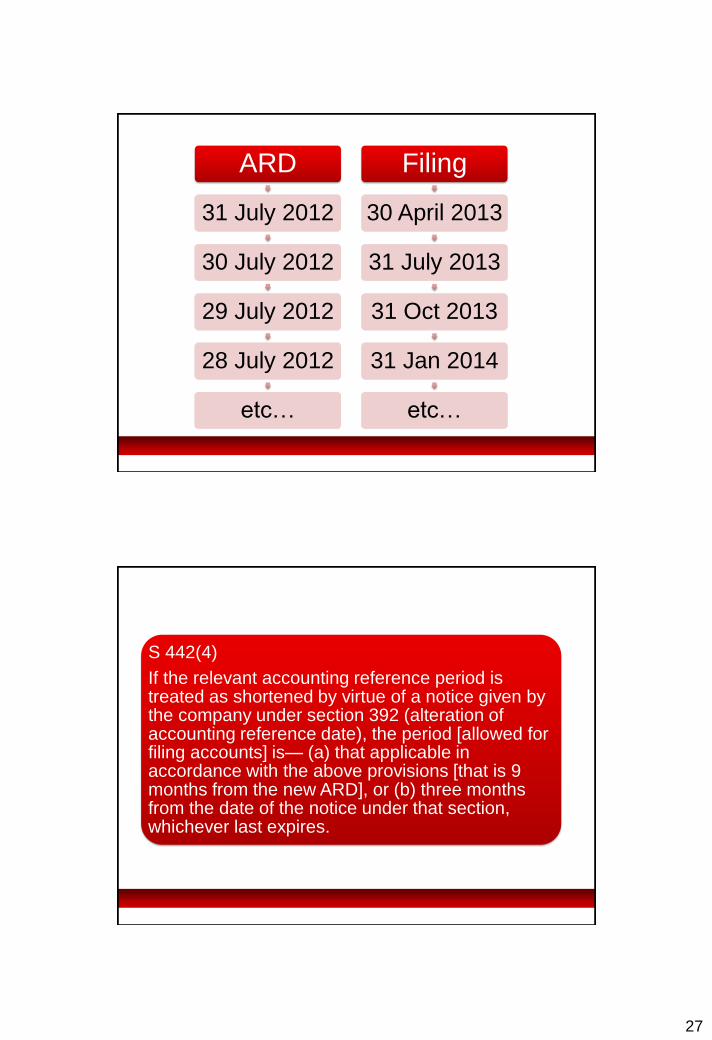

Can I change my accounting date to extend my filing deadline?

27

ARD

31 July 2012

30 July 2012

29 July 2012

28 July 2012

etc…

Filing

30 April 2013

31 July 2013

31 Oct 2013

31 Jan 2014

etc…

S 442(4)

If the relevant accounting reference period is treated as shortened by virtue of a notice given by the company under section 392 (alteration of accounting reference date), the period [allowed for filing accounts] is— (a) that applicable in accordance with the above provisions [that is 9 months from the new ARD], or (b) three months from the date of the notice under that section, whichever last expires.

28

S 392(4)

A notice under this section may not be given in respect of a previous accounting reference period if the period for filing accounts and reports for the financial year determined by reference to that accounting reference period has already expired.

ARD

31 July 2012

30 July 2012

29 July 2012

xxxxxxxxxx

Filing

30 April 2013

31 July 2013

xxxxxxxxx

xxxxxxxxx

29

Notes:

However, I am not a lawyer, and it may well be argued that your client’s interpretation follows the letter of the law. So I cannot provide a definitive answer to your question. However, I am sure that the government never intended that a company could extend its year end indefinitely and therefore my belief is that, as chartered accountants, we should not be wasting our time with such schemes.

Vo

tin

g

Yes

No

Have you ever seen the extension applied

twice?

30

Provisions

• an entity has a present obligation (legal or constructive) as a result of a past event,

• it is probable that a transfer of economic benefits will be required to settle the obligation and

• a reliable estimate can be made of the amount of the obligation.

FRS 12 – A provision

is recognised

when

31

Example 1: An entity A has been operating for many years in a

country which has no environmental legislation. At 31 December

2011 it is virtually certain that a draft law will be enacted shortly

after the year-end which will require entities to clean-up land they

have already contaminated. Should A make provision for the

estimated cost of cleaning up past contamination?

Vo

tin

g

Yes

No

Should you provide?

32

• an entity has a present obligation (legal or constructive) as a result of a past event,

• it is probable that a transfer of economic benefits will be required to settle the obligation and

• a reliable estimate can be made of the amount of the obligation.

FRS 12 – A provision

is recognised

when

Example 2: An entity B has just begun operating in a country which

has no environmental legislation. However, B has published its

environmental policy in which it undertakes to clean up all

contamination that it causes. B has honoured this pledge in other

countries in the past. Should B make provision for the estimated

cost of cleaning up contamination in this country?

33

Vo

tin

g

Yes

No

Should you provide?

• an entity has a present obligation (legal or constructive) as a result of a past event,

• it is probable that a transfer of economic benefits will be required to settle the obligation and

• a reliable estimate can be made of the amount of the obligation.

FRS 12 – A provision

is recognised

when

34

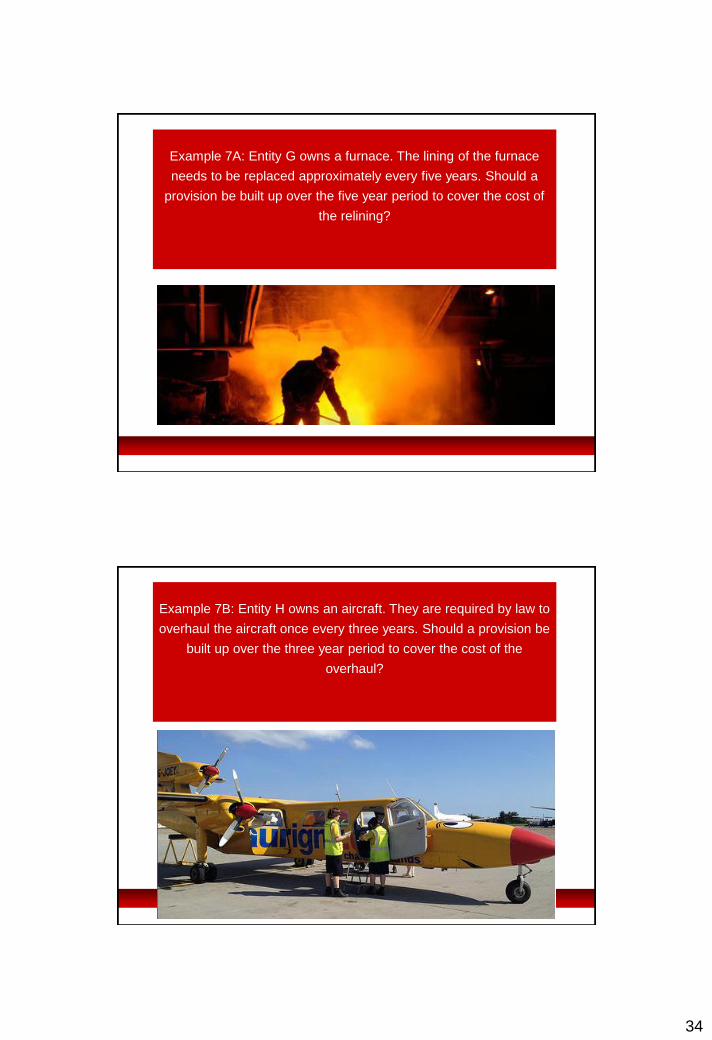

Example 7A: Entity G owns a furnace. The lining of the furnace

needs to be replaced approximately every five years. Should a

provision be built up over the five year period to cover the cost of

the relining?

Example 7B: Entity H owns an aircraft. They are required by law to

overhaul the aircraft once every three years. Should a provision be

built up over the three year period to cover the cost of the

overhaul?

35

The goodwill problem

Useful economic

life?

20

10 5

36

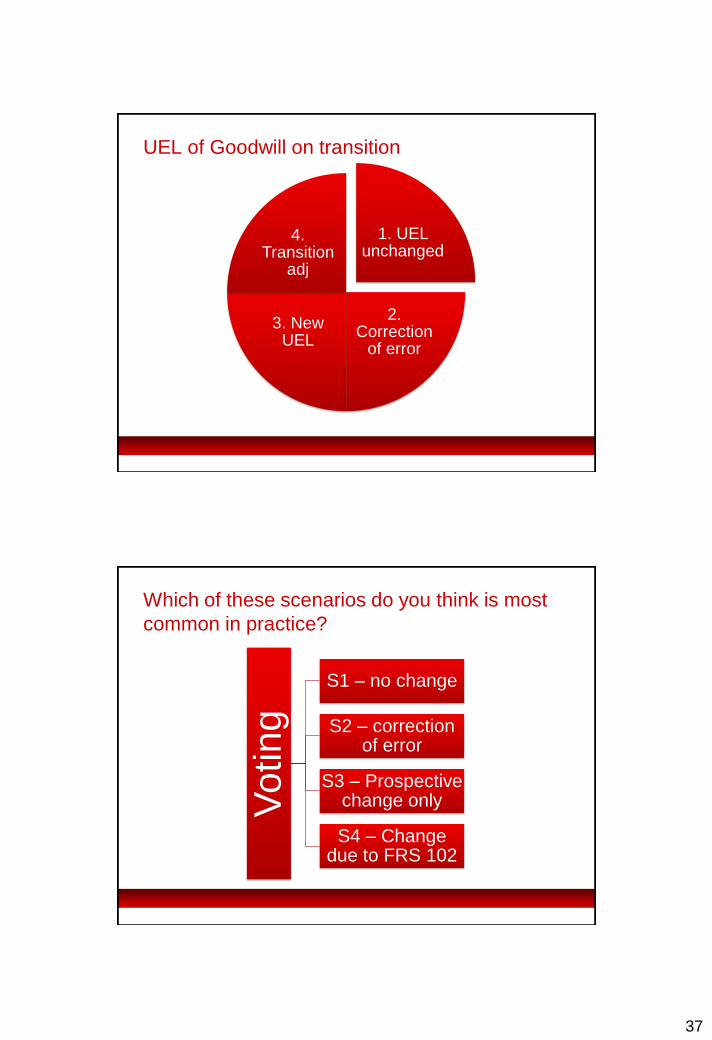

• 20 years remains the appropriate UEL and there is sufficient evidence to support it

Scenario 1

• The 20 year life is unsupported and on closer inspection is unsupportable

Scenario 2

• There was sufficient information to support the 20 year life on acquisition but circumstances have changed since then and a shorter life is now thought to be more appropriate

Scenario 3

• There was sufficient information to support the 20 year life on acquisition and circumstances have not changed since then but the evidence to support the 20 year UEL is insufficient so the FRS 102, 5 year maximum applies

Scenario 4

37

1. UEL unchanged

2. Correction

of error

3. New UEL

4. Transition

adj

UEL of Goodwill on transition

Vo

tin

g

S1 – no change

S2 – correction of error

S3 – Prospective change only

S4 – Change due to FRS 102

Which of these scenarios do you think is most

common in practice?

38

Vo

tin

g Yes

No

I don’t know

Do you think scenario 4 is a possibility?

![Le Château Inc....Deficit (57,367) (33,394) Total shareholders’ equity 200 23,860 123,035 144,939 Contingencies, commitments and guarantees [notes 11, 18 and 24] See accompanying](https://static.documents.pub/doc/80x56/5fb8b7b4de8d3c606b627dd0/le-chteau-inc-deficit-57367-33394-total-shareholdersa-equity-200.jpg)