13

Snapshot of Telecom Industry Presented by:- Aayushi Garg (109102) Abhimanyu Singh(109103)

| Date post: | 10-Apr-2018 |

| Category: |

Documents |

| Upload: | 9957118230 |

| View: | 220 times |

| Download: | 0 times |

8/8/2019 Snapshot of Telecom Industry 2010

http://slidepdf.com/reader/full/snapshot-of-telecom-industry-2010 1/13

Snapshot of Telecom

Industry

Presented by:-

Aayushi Garg (109102) Abhimanyu Singh(109103)

8/8/2019 Snapshot of Telecom Industry 2010

http://slidepdf.com/reader/full/snapshot-of-telecom-industry-2010 2/13

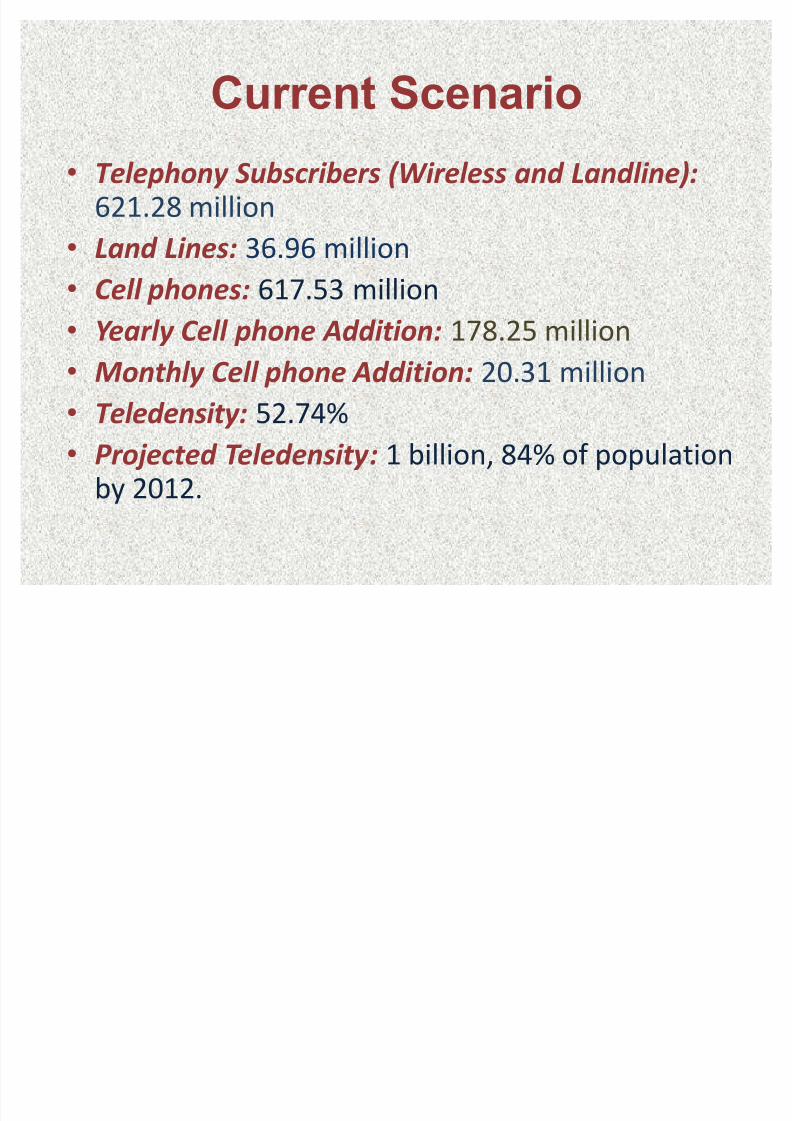

Current Scenario

Telephony Subscribers (Wireless and Landline):621.28 million

Land Lines: 36.96 million

C ell phones: 617.53 million

Y early C ell phone Addition: 178.25 million

Monthly C ell phone Addition: 20.31 million

Teledensity: 52.74% P rojected Teledensity: 1 billion, 84% of population

by 2012.

8/8/2019 Snapshot of Telecom Industry 2010

http://slidepdf.com/reader/full/snapshot-of-telecom-industry-2010 3/13

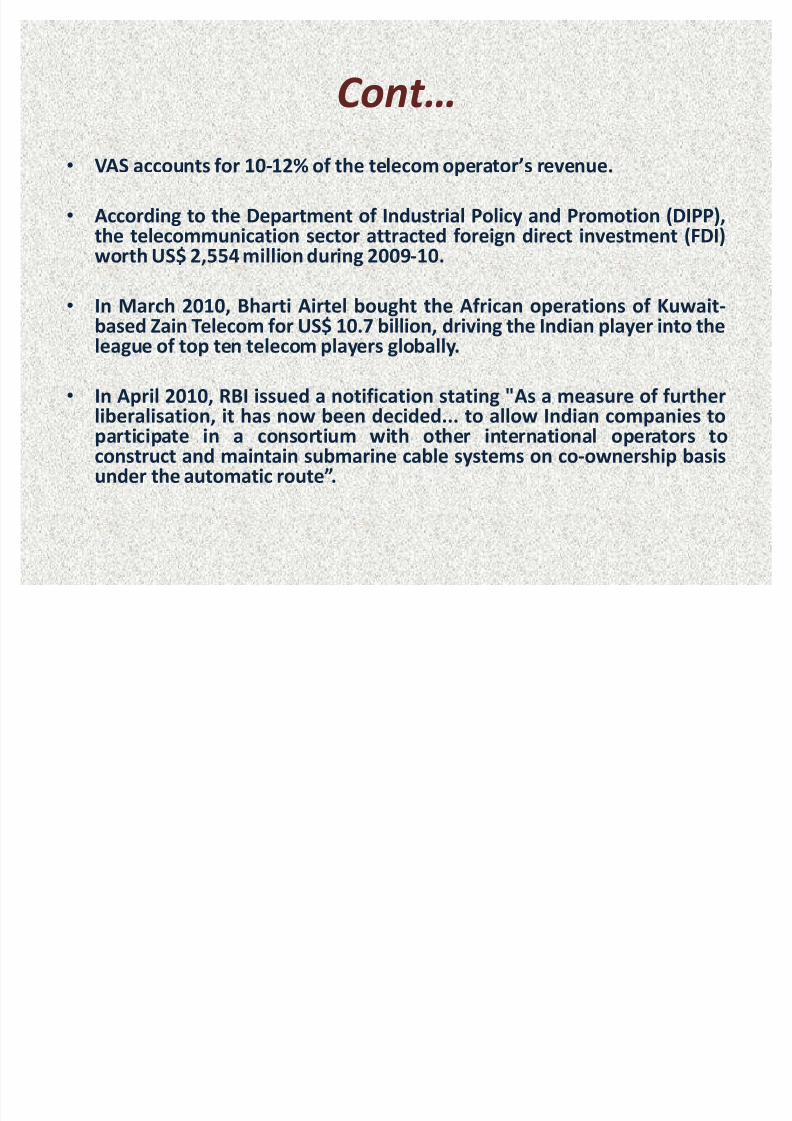

C ont

VAS accounts for 10-12% of the telecom operators revenue.

According to the Department of Industrial Policy and Promotion (DIPP),the telecommunication sector attracted foreign direct investment (FDI)worth US$ 2,554 million during 2009-10.

In March 2010, Bharti Airtel bought the African operations of Kuwait-based Zain Telecom for US$ 10.7 billion, driving the Indian player into theleague of top ten telecom players globally.

In April 2010, RBI issued a notification stating "As a measure of further

liberalisation, it has now been decided... to allow Indian companies toparticipate in a consortium with other international operators toconstruct and maintain submarine cable systems on co-ownership basisunder the automatic route.

8/8/2019 Snapshot of Telecom Industry 2010

http://slidepdf.com/reader/full/snapshot-of-telecom-industry-2010 4/13

C ont.

Remote treatment and diagnosis of patients throughmobile phones would become a reality in the nearfuture..

According to the Economic Survey 2009-10, the

production of telecom equipment in value terms hasincreased from US$ 9 billion in 2007-08 to US$ 10.53billion in 2008-09 and is expected to be US$ 12.4billion in 2009-10.

It is proposed to achieve rural tele-density of 25 per

cent by means of 200 million rural connections by theend of the Eleventh Five Year Plan.

8/8/2019 Snapshot of Telecom Industry 2010

http://slidepdf.com/reader/full/snapshot-of-telecom-industry-2010 5/13

Trends in Telephone subscribers and

Teledensity in India

8/8/2019 Snapshot of Telecom Industry 2010

http://slidepdf.com/reader/full/snapshot-of-telecom-industry-2010 6/13

Wireless Segment:-

Service Provider wise Market Share as

on 30-6-2010

8/8/2019 Snapshot of Telecom Industry 2010

http://slidepdf.com/reader/full/snapshot-of-telecom-industry-2010 7/13

Wireline Segment:-

Service Provider wise Market Share as

on 30-6-2010

8/8/2019 Snapshot of Telecom Industry 2010

http://slidepdf.com/reader/full/snapshot-of-telecom-industry-2010 8/13

Porters Five Forces Model

8/8/2019 Snapshot of Telecom Industry 2010

http://slidepdf.com/reader/full/snapshot-of-telecom-industry-2010 9/13

8/8/2019 Snapshot of Telecom Industry 2010

http://slidepdf.com/reader/full/snapshot-of-telecom-industry-2010 10/13

Porters five force model

Rivalry among existing companies

There are three types of players in telecom service:

State owned companies.

Private Indian owned companies.

Foreign invested companies.

8/8/2019 Snapshot of Telecom Industry 2010

http://slidepdf.com/reader/full/snapshot-of-telecom-industry-2010 11/13

Bargaining power of supplier

Service based industry which is intangible.

Mobile handset supliers

Other suppliers like opticle fiber suppliers,aluminium

suppliers and softwares.

threat of new entry

New entrance may alter the competitive

environment. barriers of entry.

8/8/2019 Snapshot of Telecom Industry 2010

http://slidepdf.com/reader/full/snapshot-of-telecom-industry-2010 12/13

Substitues to product

Off ers wide range of service in india,such as

wireless,CDMA mobile,internet,broadband,VOIP etc.

substitutes most focused are:

which tends to improving their performance trade

off with the industrial products.

product which are produced by high profit earning

industies.

8/8/2019 Snapshot of Telecom Industry 2010

http://slidepdf.com/reader/full/snapshot-of-telecom-industry-2010 13/13