23

So Much To Do, So Little Time! Tangible Capital Assets LGAA Annual Conference Red Deer, Alberta March 13, 2008

| Date post: | 14-Dec-2015 |

| Category: |

Documents |

| Upload: | christiana-rice |

| View: | 218 times |

| Download: | 0 times |

So Much To Do, So Little Time!

Tangible Capital Assets

LGAA Annual Conference

Red Deer, Alberta

March 13, 2008

Provide tools and training

Raise awareness

Mitigate the cost

AMAH Project Goals

2

What is required

Legislative impact

Implementation update

Challenges

Session Overview

3

angible – can be touched

Definition

4

apital – lasts over time

sset – has measurable value

Major Asset Classifications

5

Land

Land improvements

Buildings

Engineered structures

Machinery & equipment

Vehicles

Cultural & historical

Global View

6

Australia1998

New Zealand1990

USA2006

Canada & Provinces 2000-2003

Canadian Municipalities2009

Why?

7

Budget and

Reporting Requirements

Long Term Decisions by Short Term Councils

Not New

and Exciting

Aging Infrastructure

Property Tax Rate Sensitivity

Awareness

Out of Sight /

Out of Mind

Outside Contributions

8

Provincial grants Federal grants

Developers

Constructed assets funded from third parties require replacement

Meeting the Standard

9

CICA - PSAB 3150

Timeline

10

Planning and Policy Development

Resource Identification and Acquisition

Inventory Listing

Valuation & Amortization

Reporting & Presentation

AssetManagement

2009

Step 1

Step 4

Step 2

Step 3

Capital Asset Policy

11

1. Purpose & Scope2. Asset Definitions & Classification3. Asset Recording & Valuation4. Amortization Methods and Rates5. Review & Write-downs6. Maintaining Records7. Asset Disposal8. Systems9. Reporting & Budgeting

Toolkit

12

www.MEnet.ab.ca

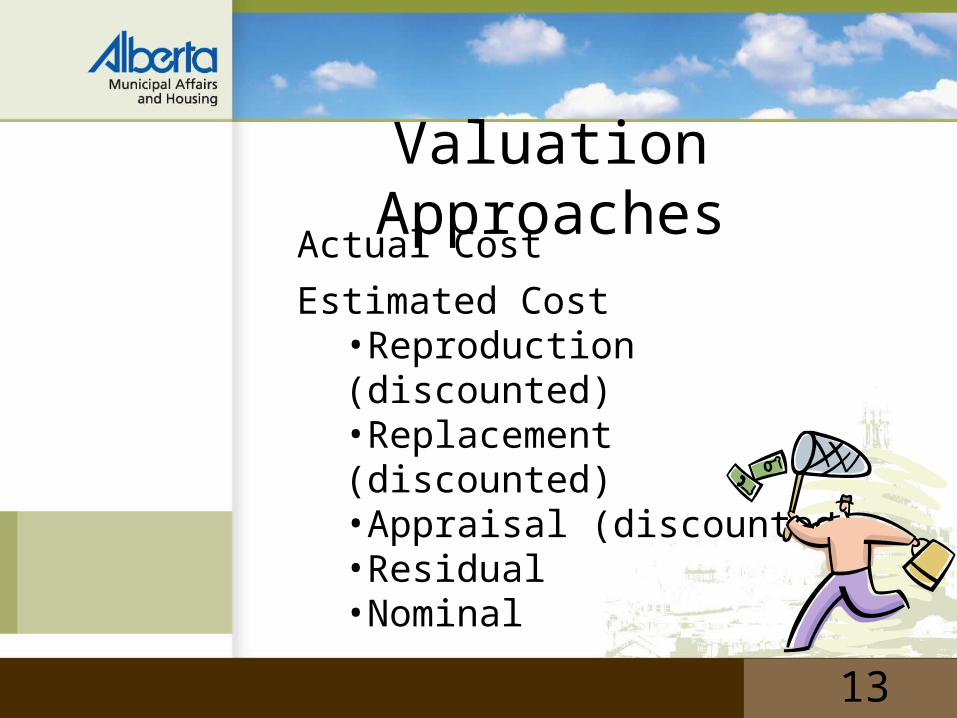

Actual Cost

Estimated Cost•Reproduction (discounted)•Replacement (discounted)•Appraisal (discounted)•Residual•Nominal

Valuation Approaches

13

Valuation Tools

14

Linear

•Roads

•Drainage

•Water & Wastewater

Bridges

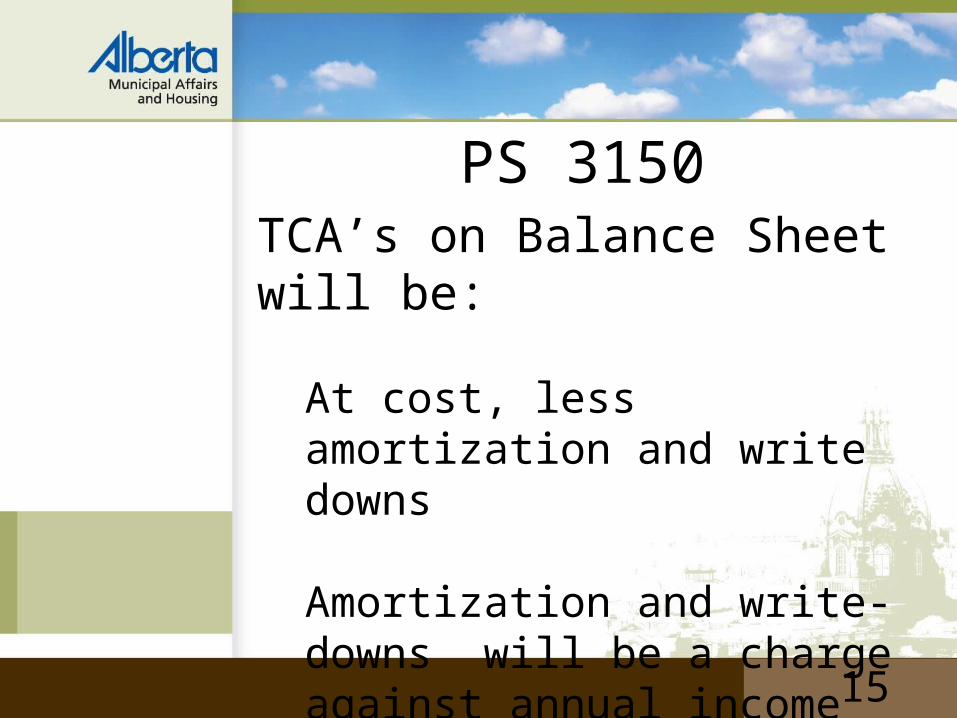

TCA’s on Balance Sheet will be:

At cost, less amortization and write downs

Amortization and write-downs will be a charge against annual income

PS 3150

15

Brings a non-cash dimension to financial reporting and

budgeting

Full Accrual Accounting

This change does not require a change in behavior, but it may cause you to change because there will be more information

available

Impact of Recording TCA’s

16

Municipalities will not be required to

fund amortization

Legislative Impact

17

All TCA to be recorded in 2009Amortized over useful lifeAnnual amortization expensed;

could result in deficienciesPS 3150 does not mandate funding amortization

PS 3150 Requirements

18

Operating, capital and reserve fund statements replaced with one statement

Future Changes to Financial Reporting – PS

1200

19

Statement of Financial Position

‘Accumulated Surplus’ is one amount; includes ‘Equity in ‘TCA

Future Changes to Financial Reporting – PS

1200

20

Focus on net financial assets/net debt; not annual results

Statement of OperationsAnnual budget will replace operating and capital budgets

Future Changes to Financial Reporting – PS

1200

21

Capital purchases, debt proceeds and debt principal retirements excluded

Summary

22

Next Steps• Replacement cost reassessment• Status of reserve fund levels• Asset Management

Benefits• Awareness of problem and magnitude• Better internal information for decision makers • Significant step towards good asset management

Resources• Considerable work is required to implement this change• Resources and expertise will be required •Involve auditors, engineers and facility management personnel early on!

Questions?

23