52

Social Security Its Vital Role for Workers & Their Families

| Date post: | 14-Dec-2015 |

| Category: |

Documents |

| Upload: | shaylee-burnell |

| View: | 216 times |

| Download: | 3 times |

Social Security

Its Vital Role for Workers & Their

Families

Social Security 54.2 million people receive Social

Security benefits But more than a retirement program More than one-third all monthly

checks for non-retired individuals Social Security = social & family

insurance

May 2011 Consortium for Citizens with Disabilities 2

May 2011Consortium for Citizens with

Disabilities 3

Social & Family Insurance

Workers share risk of common life events

Each worker’s record provides benefits for different family generations, even young workers

Guaranteed monthly payment

May 2011 Consortium for Citizens with Disabilities 4

Social Security Insurance

Retirement - insures against poverty after worker retires

Survivors - insures dependents after worker dies or retires

Disability - insures against loss of ability to work due to disability

May 2011Consortium for Citizens with

Disabilities 5

Current Design: The Positives

Fixed monthly payment Ability to move among 3 programs:

work history, age & eligibility category

Pays multiple family members based on one worker’s earnings

Adjusted annually for inflation (generally)

Social Security & The Deficit

National groups examining ways to reduce deficit, including Social Security changes

Social Security did NOT cause the deficit Cutting benefits will NOT solve budget

crisis Cutting benefits will deepen financial crisis

for many people with disabilities May 2011

Consortium for Citizens with Disabilities 6

Social Security & The Deficit

Social Security did NOT cause the deficit: It is self-funded By law, it can only spend money

dedicated to the program No borrowing authority

May 2011 Consortium for Citizens with Disabilities 7

May 2011Consortium for Citizens with

Disabilities 8

How Does Social Security Benefit

People with Disabilities & Their

Families?

May 2011 Consortium for Citizens with Disabilities 9

How to Earn Social Security

Insurance Coverage

Payroll Tax: Workers & employers pay FICA (Federal Insurance Contributions Act) taxes

Workers earn “credits” to become insured Multiple generations receive benefits

from wage earner’s record when worker becomes disabled, retires or dies

May 2011Consortium for Citizens with

Disabilities 10

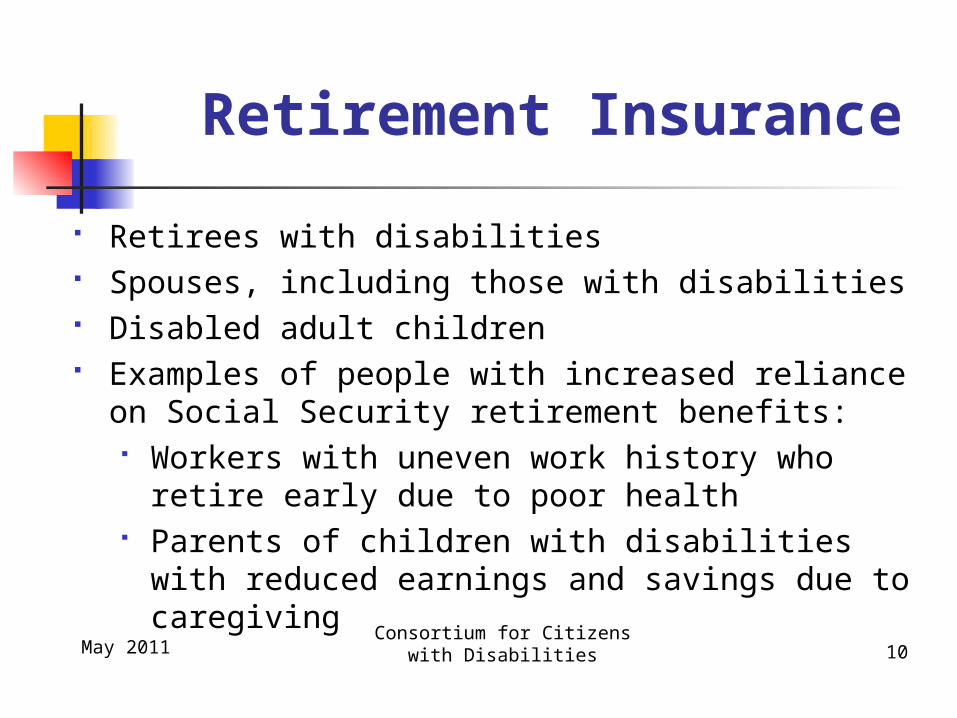

Retirement Insurance

Retirees with disabilities Spouses, including those with disabilities Disabled adult children Examples of people with increased reliance on

Social Security retirement benefits: Workers with uneven work history who retire

early due to poor health Parents of children with disabilities with reduced

earnings and savings due to caregiving

May 2011Consortium for Citizens with

Disabilities 11

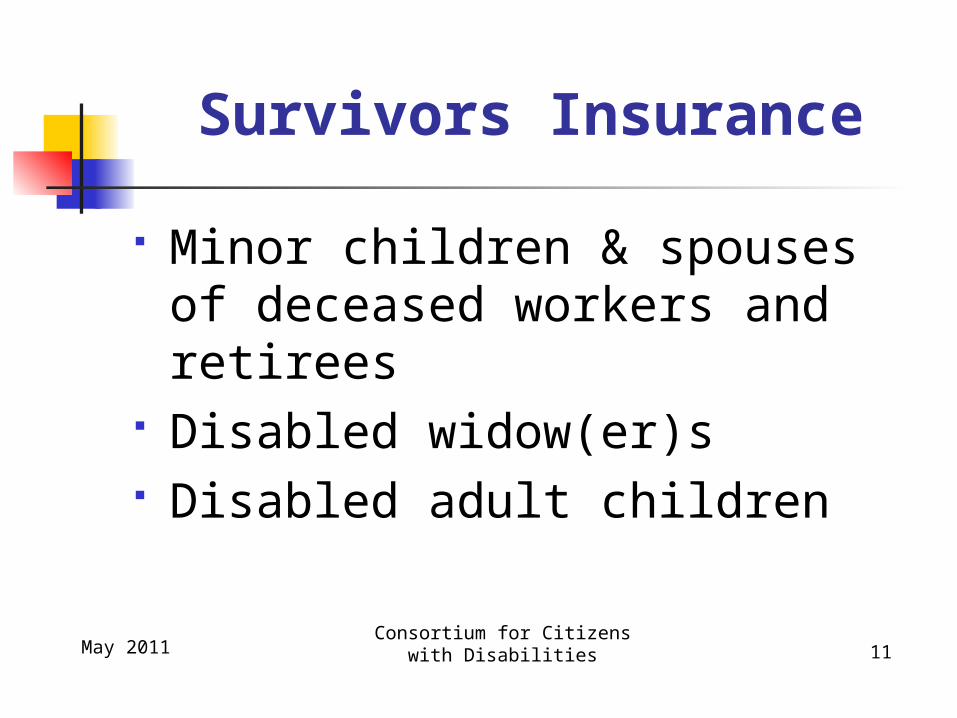

Survivors Insurance

Minor children & spouses of deceased workers and retirees

Disabled widow(er)s Disabled adult children

May 2011Consortium for Citizens with

Disabilities 12

Disability Insurance

Disabled workers, their children & spouses

Disabled adult children

May 2011 Consortium for Citizens with Disabilities 13

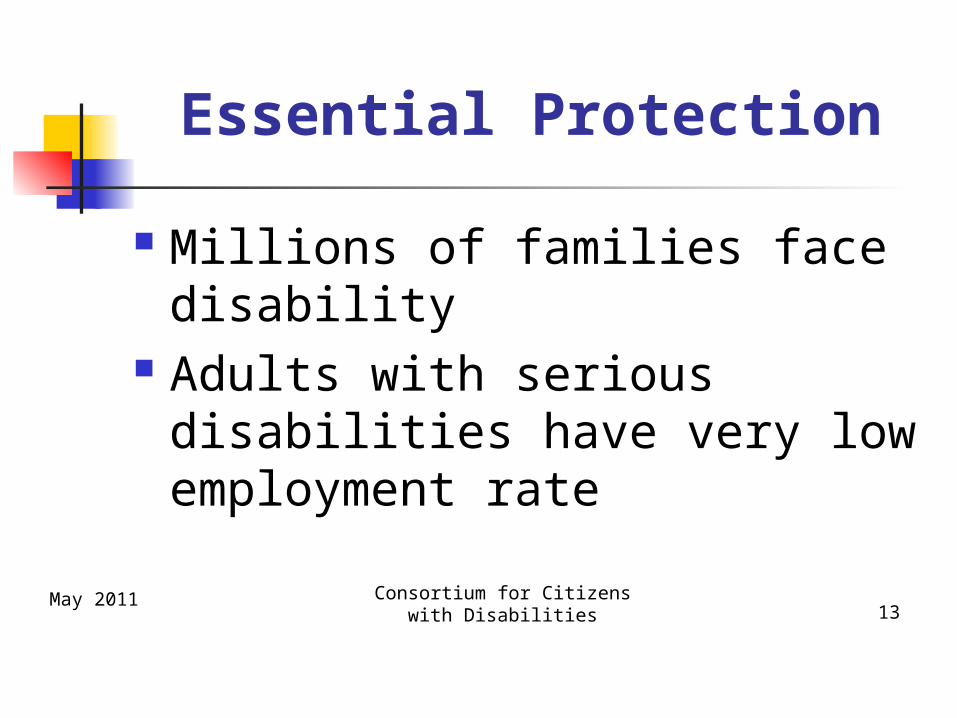

Essential Protection

Millions of families face disability

Adults with serious disabilities have very low employment rate

May 2011Consortium for Citizens with

Disabilities 14

Disability & Poverty

Poverty rates among workers with disabilities: twice as high as others who get Social Security

Social Security equals half/more of TOTAL family income for about half of disabled worker beneficiaries

May 2011Consortium for Citizens with

Disabilities 15

Better Than Private Insurance

Adjusted for inflation Covers children of disabled

workers Available to workers with

disabilities & chronic health problems

May 2011Consortium for Citizens with

Disabilities 16

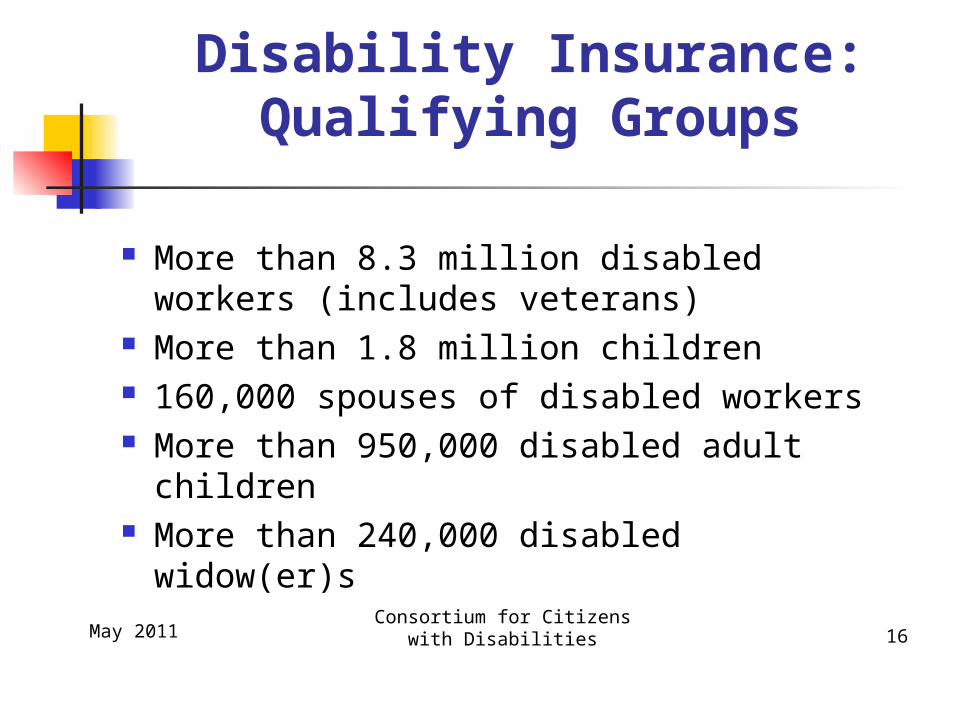

Disability Insurance:Qualifying Groups

More than 8.3 million disabled workers (includes veterans)

More than 1.8 million children 160,000 spouses of disabled workers More than 950,000 disabled adult

children More than 240,000 disabled widow(er)s

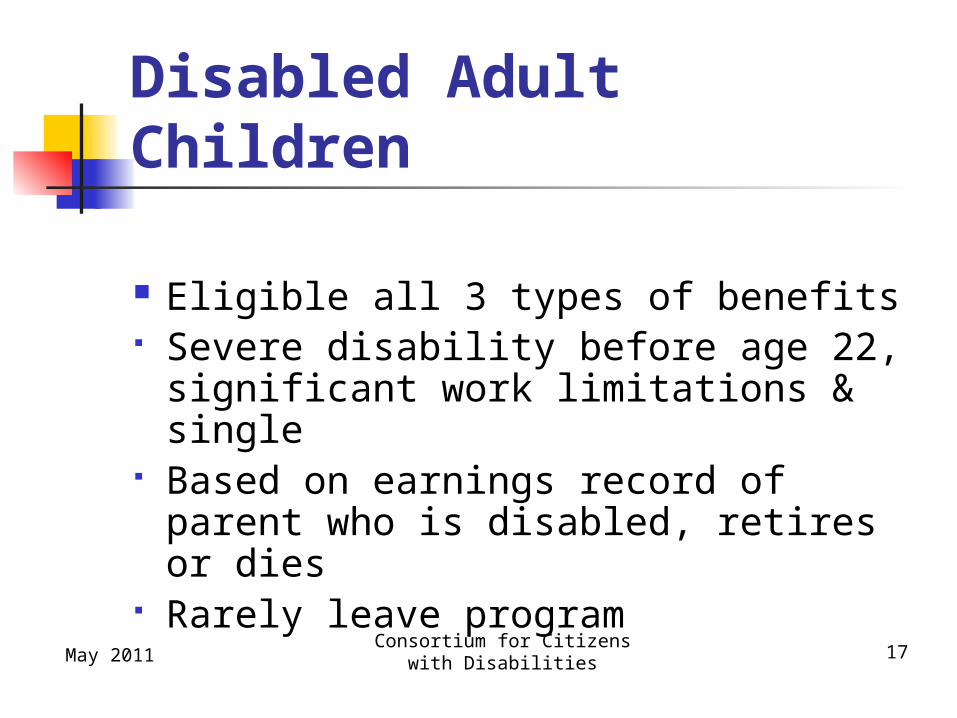

Disabled Adult Children

Eligible all 3 types of benefits Severe disability before age 22,

significant work limitations & single

Based on earnings record of parent who is disabled, retires or dies

Rarely leave programMay 2011

Consortium for Citizens with Disabilities 17

Social Security Helps Young Workers and Their

Families

Disability or death can happen at any time to people of all ages

Disability & survivors benefits provide guaranteed income for spouse & children

May 2011Consortium for Citizens with

Disabilities 18

May 2011 Consortium for Citizens with Disabilities 19

Younger Workers: Eligibility

Need fewer “credits” than older workers to qualify

Disability: Must prove significant work limitations

Benefit amount depends on worker’s previous earnings

Families of Younger Workers

Benefits for spouse & children as dependents of disabled worker or survivors of deceased worker

Survivors: Benefit amount based on what worker would have received if had reached full retirement age

May 2011Consortium for Citizens with

Disabilities 20

May 2011Consortium for Citizens with

Disabilities 21

Value of Social Security

Young workers with spouse and 2 children – approximate value

“Life” insurance = $476,000 Disability = $ 465,000

May 2011Consortium for Citizens with

Disabilities 22

How are Social Security & SSI Different?

May 2011Consortium for Citizens with

Disabilities 23

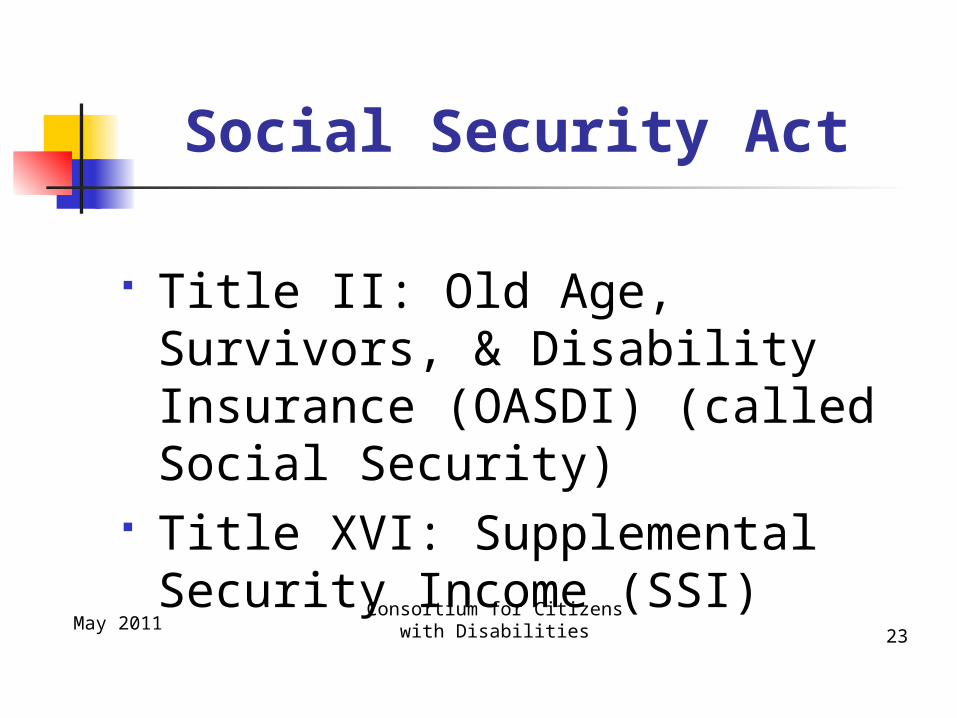

Social Security Act

Title II: Old Age, Survivors, & Disability Insurance (OASDI) (called Social Security)

Title XVI: Supplemental Security Income (SSI)

May 2011 Consortium for Citizens with Disabilities 24

Different Programs: Title II & Title XVI

Title II: OASDI Social Security

payroll taxes Workers Other

beneficiaries: spouses & children

Medicare

Title XVI: SSI General revenues

from federal budget

Aged & blind and disabled adults & children

Needs-based Medicaid

May 2011 Consortium for Citizens with Disabilities

25

You Can Receive Both Social Security and SSI

May get Social Security disability & SSI at same time – must have VERY limited income & resources (for SSI)

May get one benefit now & another later

Beneficiaries may work, but rules about allowable earnings (“work incentives”) differ for each program

May 2011 Consortium for Citizens with Disabilities 26

How is Social Security Funded?

May 2011Consortium for Citizens with

Disabilities 27

Is There Enough Money?

Question everyone asks! Solvency = ability to pay legal

obligations Facts support no immediate crisis

May 2011 Consortium for Citizens with Disabilities 28

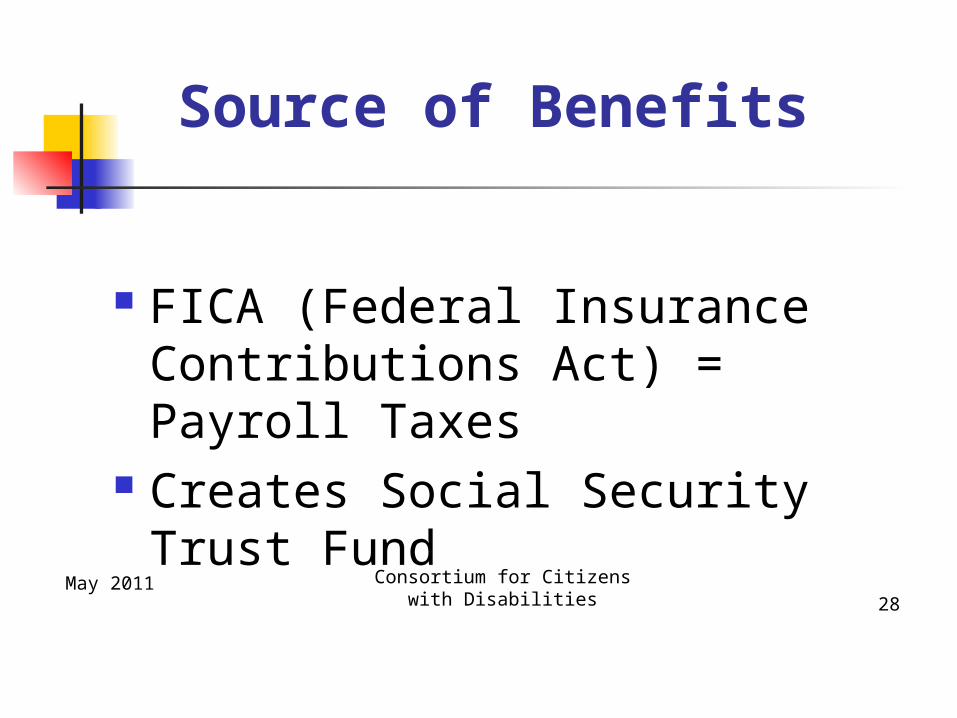

Source of Benefits

FICA (Federal Insurance Contributions Act) = Payroll Taxes

Creates Social Security Trust Fund

May 2011Consortium for Citizens with

Disabilities 29

What Are the Trust Funds?

Technically 2 trust funds: Old Age and Survivors Insurance Disability Insurance

People with disabilities get benefits from both

Policymakers treat as one fund

May 2011 Consortium for Citizens with Disabilities 30

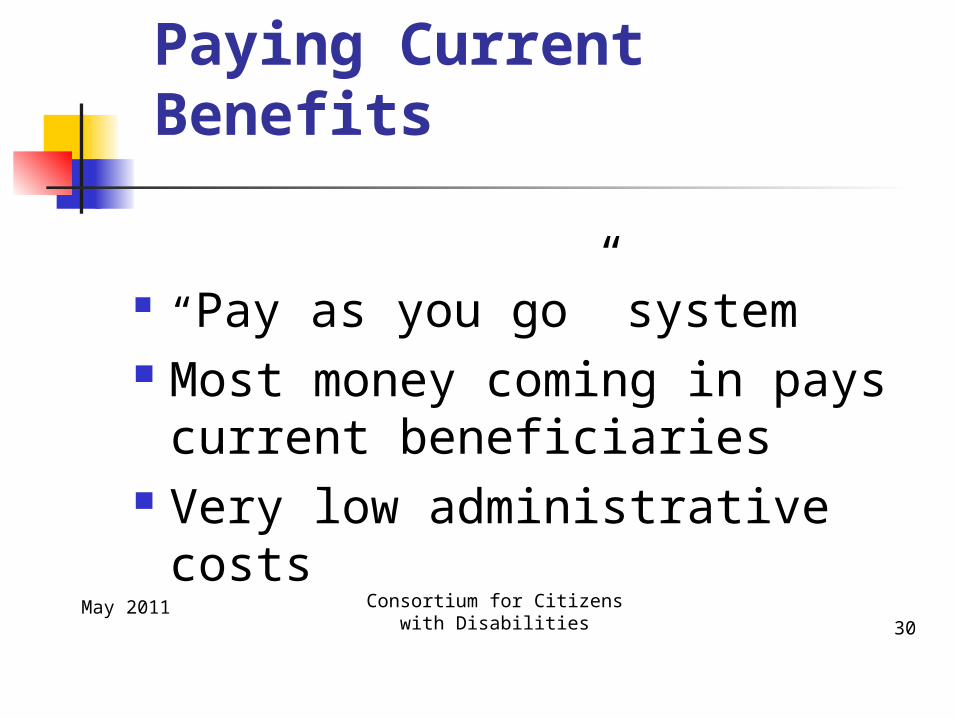

Paying Current Benefits

“Pay as you go” system Most money coming in pays

current beneficiaries Very low administrative costs

May 2011Consortium for Citizens with

Disabilities 31

Paying Future Benefits

Collect more now than need: build surplus (reserve) for future benefits

Use surplus to buy U.S. Treasury bonds

Put bond interest in Trust Fund Redeem bonds later when not

enough incoming payroll taxes to pay full benefits

May 2011Consortium for Citizens with

Disabilities 32

Investing Surplus

U.S. Treasury bonds = safest investment in world

Not invested in stock market U.S. government bears risk,

not individuals Program will NOT go bankrupt!

Current & Future Surplus

Surplus = invested assets or Trust Fund reserves

$2.6 trillion by end 2010 Will continue to grow 2011-2022 Projected to reach $3.7 trillion by

2022 May 2011

Consortium for Citizens with Disabilities 33

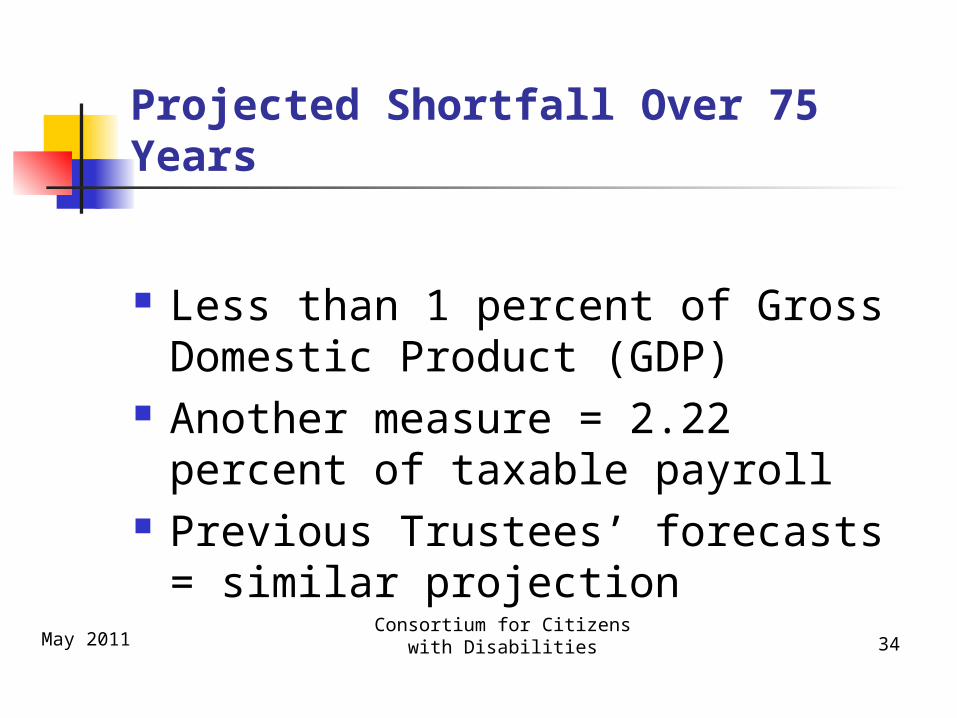

Projected Shortfall Over 75 Years

Less than 1 percent of Gross Domestic Product (GDP)

Another measure = 2.22 percent of taxable payroll

Previous Trustees’ forecasts = similar projection

May 2011Consortium for Citizens with

Disabilities 34

May 2011Consortium for Citizens with

Disabilities 35

No Immediate Problem

Long term planning = 75 years

Social Security Trustees project future benefits based on payroll tax income & reserves

Need to start addressing problem, but no need to change basic program design

May 2011Consortium for Citizens with

Disabilities 36

Future Projections

Pay 100% of scheduled benefits 2011 Trustees Report: until 2036

Pay reduced benefits (if no action taken) 2011 Trustees Report: 77% of

scheduled benefits starting 2037

Future Projections – DI Trust Fund

2011 Trustees Report: DI Trust Fund exhausted in 2018

Solution: Reallocation of payroll tax rate between OASI and DI Trust Funds Reallocation has occurred before

May 2011 Consortium for Citizens with Disabilities 37

May 2011 Consortium for Citizens with Disabilities 38

Future Challenges

What will it take to fix system’s long term funding shortfall? Wide range of options to phase in gradually

Has Congress ever stepped in to strengthen Social Security’s financial future? YES. In 1983 to plan for retirement of “baby

boomers” which helped create current surplus

May 2011 Consortium for Citizens with Disabilities 39

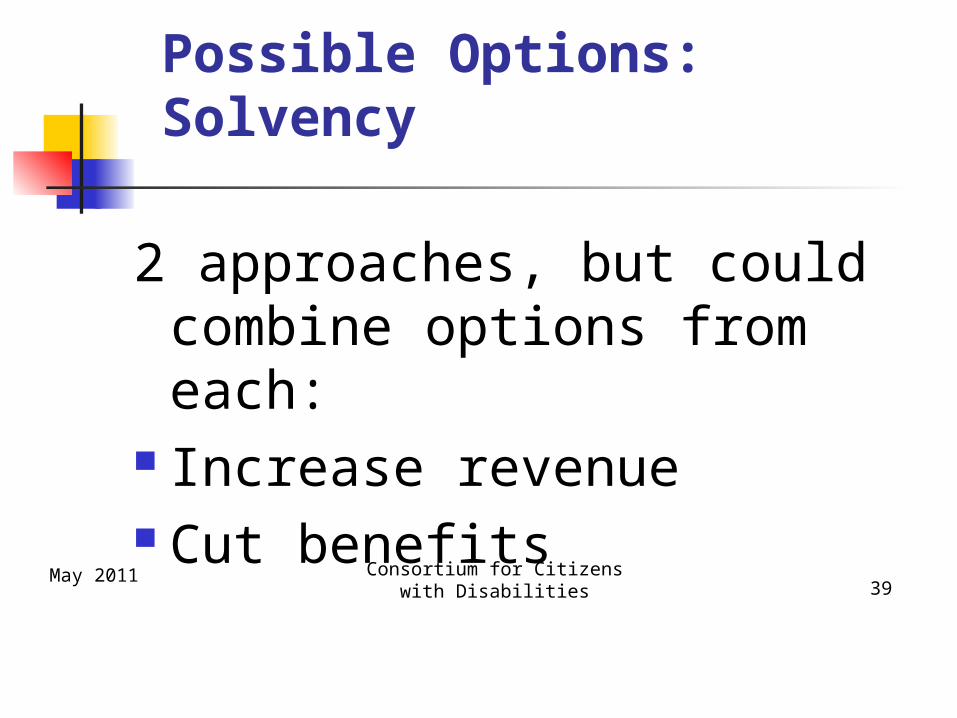

Possible Options: Solvency

2 approaches, but could combine options from each:

Increase revenue Cut benefits

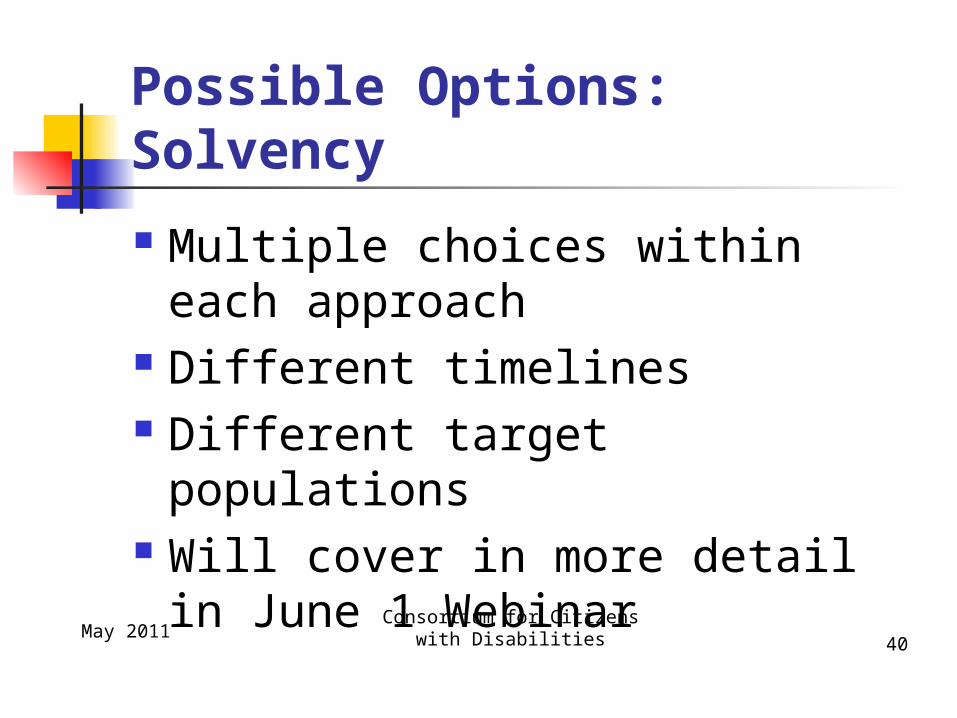

Possible Options: Solvency

Multiple choices within each approach

Different timelines Different target populations Will cover in more detail in

June 1 WebinarMay 2011

Consortium for Citizens with Disabilities 40

Increase Revenue: Some Options

Increase payroll tax for employers & employees Raise limit on maximum taxable income (2011:

$106,800) Tax earnings above taxable maximum Extend covered employees (e.g. state & local

now excluded) Earmark specific taxes for new funding stream Diversify investments beyond U.S. Treasury

bondsMay 2011

Consortium for Citizens with Disabilities 41

Cut Benefits: Some Options Modify cost of living adjustment: reduce

annually OR adopt new measure Raise normal and/or early retirement

age Lengthen time period used to set level

of insurance benefits Reduce payments for new beneficiaries

May 2011 Consortium for Citizens with Disabilities 42

May 2011Consortium for Citizens with

Disabilities 43

What Lies Ahead?

Each potential change affects Social Security’s future

No immediate crisis Possible to meet long term

needs with modest adjustments over next 20-30 years

May 2011Consortium for Citizens with

Disabilities 44

A Checklist for People with Disabilities &

Their Families

May 2011Consortium for Citizens with

Disabilities 45

Our Principles

Do not change basic design based on payroll taxes

Preserve as social insurance for disability, survivors & retirement

Guarantee monthly benefits adjusted for inflation

Preserve current & future benefits Restore program’s long term funding

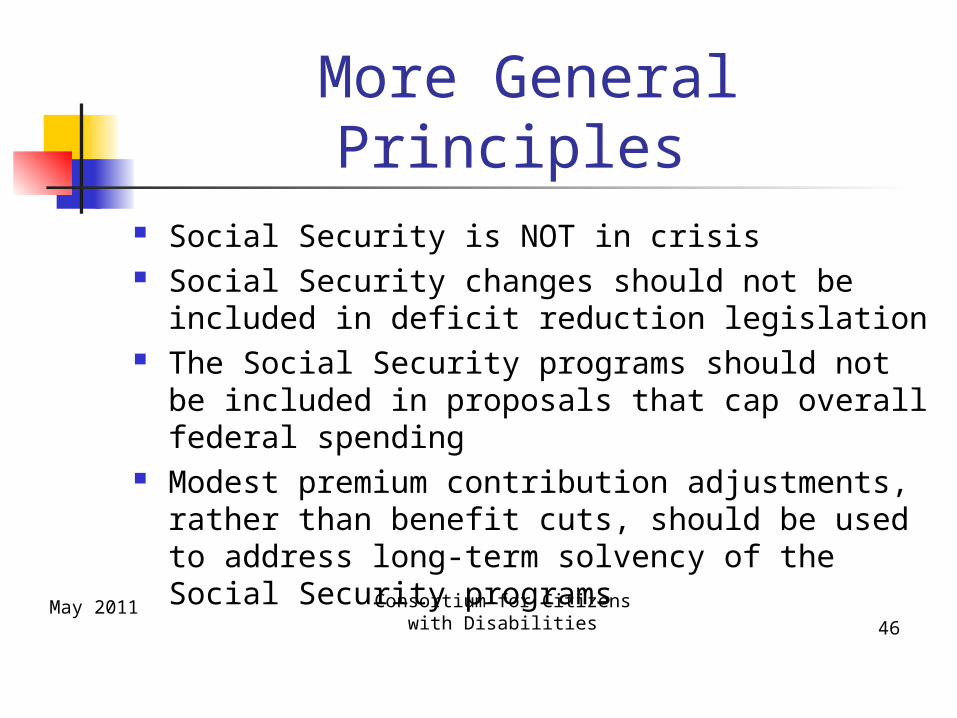

More General Principles Social Security is NOT in crisis Social Security changes should not be included

in deficit reduction legislation The Social Security programs should not be

included in proposals that cap overall federal spending

Modest premium contribution adjustments, rather than benefit cuts, should be used to address long-term solvency of the Social Security programsMay 2011 Consortium for Citizens with

Disabilities 46

May 2011Consortium for Citizens with

Disabilities 47

Our Questions

Do proposals: Change benefit formula? Change cost-of-living adjustments? Switch from “wage” to “price” index? Provide benefits for family members? Raise retirement age?

May 2011 Consortium for Citizens with Disabilities 48

Our Message

Some change is necessary, but nothing drastic now or later

Protect basic design Require beneficiary impact

statement for each proposal

May 2011Consortium for Citizens with

Disabilities 49

Beneficiary Impact

Statement

Analyze impact for each type of beneficiary Disabled workers/their dependents Retirees/their dependents Disabled adult children –

dependents of parents who retire, die or become disabled

Disabled widow(er)s

For More Information

To find fact sheets regarding Social Security and disability, links to helpful resources, or to access a recording of this webinar, please visit

www.disabilityandsocialsecurity.org

May 2011

Consortium for Citizens with Disabilities

50

Join us for our next webinar

Current Social Security Reform Proposals: How Would They Affect People with DisabilitiesWednesday June 1, 2011 1:00 – 3:00 p.m. EDT email [email protected] with questions

May 2011Consortium for Citizens with

Disabilities 51

Webinar Sponsors

This webinar has been sponsored by the Consortium for Citizens with Disabilities. Funding was provided through a grant administered by the National Academy of Social Insurance and provided by the Ford Foundation.

May 2011 Consortium for Citizens with Disabilities 52