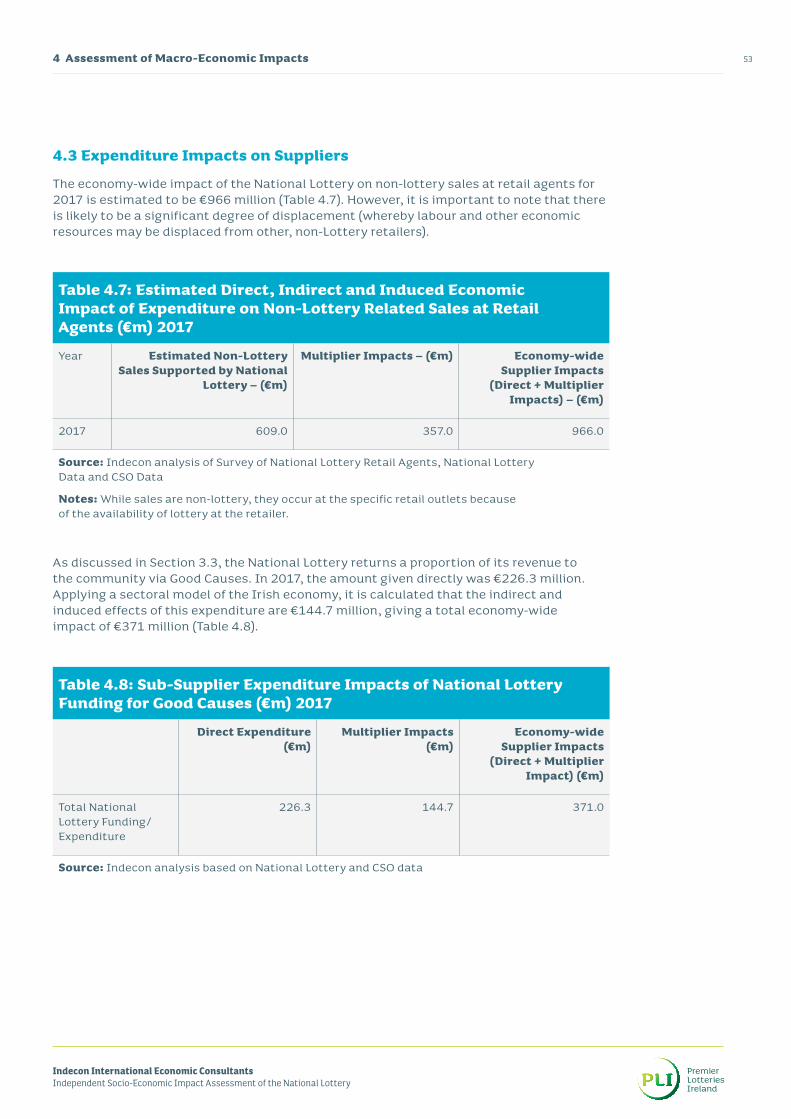

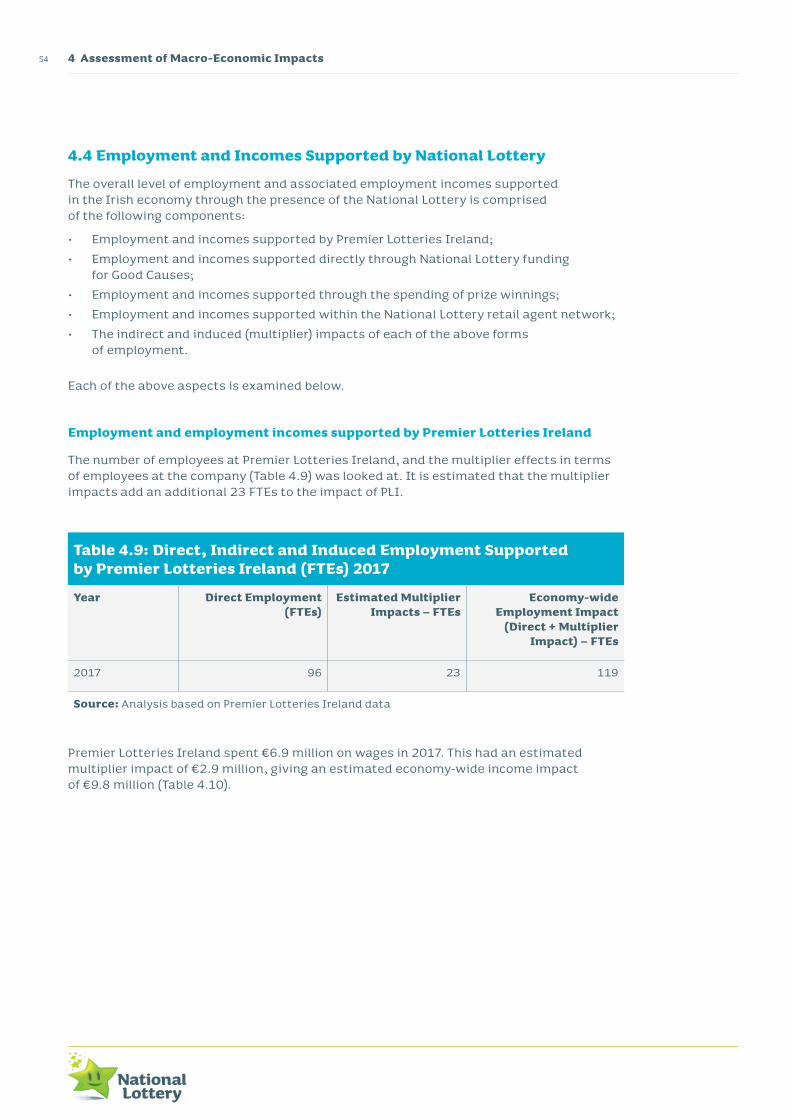

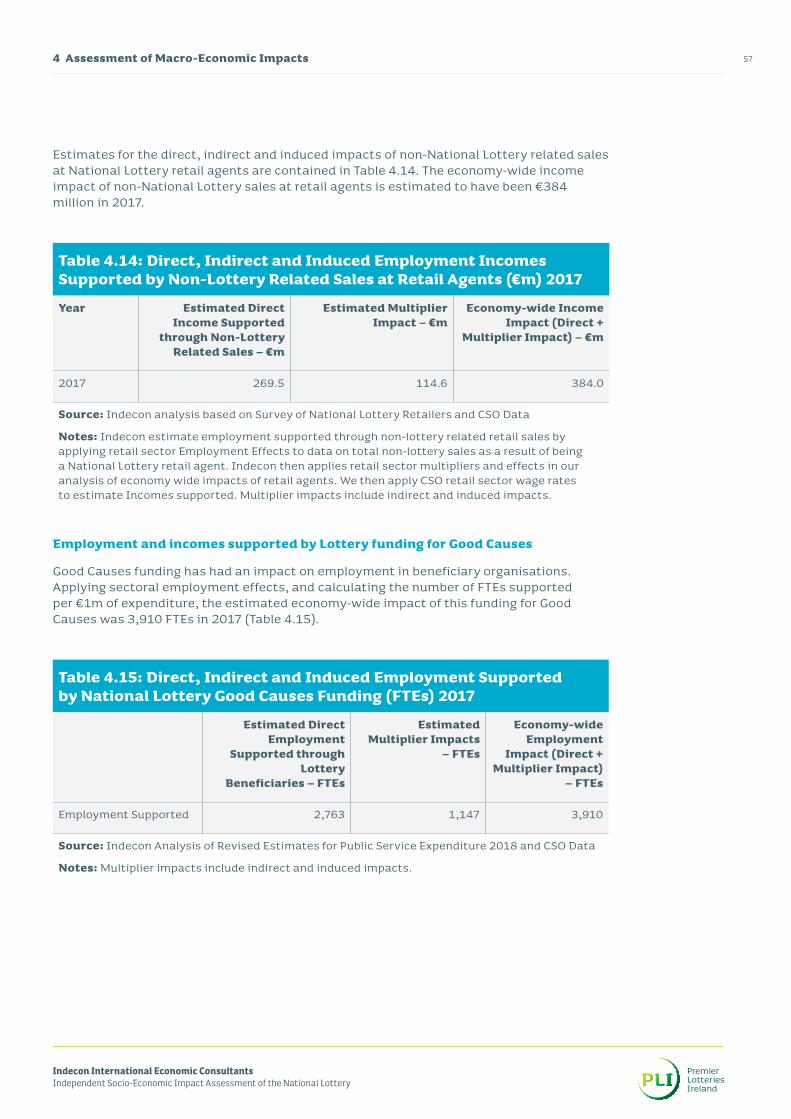

Indecon International Economic Consultants Independent Socio-Economic Impact Assessment of the National Lottery A Executive Summary Socio-Economic Impact of the National Lottery An Independent Assessment Prepared by Indecon Research Economists www.indecon.ie December 2018

Transcript

Indecon International Economic ConsultantsIndependent Socio-Economic Impact Assessment of the National Lottery

AExecutive Summary

Socio-Economic Impact of the National Lottery An Independent Assessment

Prepared by Indecon Research Economists www.indecon.ie

December 2018

Contents

Tables, Figures & Boxes ii

Glossary of Terms and Abbreviations viii

Executive Summary ix

1 Introduction and Methodology 11.1 Introduction 21.2 Methodological Approach 21.3 Report Structure 61.4 Acknowledgements and Disclaimer 6

2 Development of National Lottery in Ireland 72.1 Trends in Lottery Sales 82.2 Innovation and Product Development 92.3 Summary of Key Findings 16

3 Assessment of Micro-Economic and Social Impacts 173.1 Introduction 183.2 Funds raised for Good Causes all over Ireland 183.3 Impact of Funding to Good Causes 213.4 Funds Returned to the Community – Prize Winnings 253.5 Impact on National Lottery Retail Agents 343.6 Summary of Key Findings 44

4 Assessment of Macro-Economic Impacts 454.1 Introduction 464.2 Expenditure/GDP Impacts 484.3 Expenditure Impacts on Suppliers 534.4 Employment and Incomes Supported by National Lottery 544.5 Exchequer Taxation Impacts 624.6 Summary of Key Findings 64

5 Wider Market Developments 655.1 Introduction 665.2 The Gambling Sector in Ireland 665.3 Lottery and Other Forms of Betting 675.4 Comparative International Analysis 765.5 Summary of Key Findings 79

Table 2.1 National Lottery Sales Revenue by Game – Total over Period 1987-2017

10

Table 2.2 National Lottery Sales Revenue by Game – 2017 11

Table 2.3 Main National Lottery Games – 2017 12

Table 2.4 National Lottery Games Available to Play Online 14

Table 2.5 National Lottery Online Sales (€m) – 2009-2017 14

Table 3.1 Total National Lottery Beneficiary Funding – 2006-2017 19

Table 3.2 Expenditure part-funded by the National Lottery by Category, 2017

20

Table 3.3 Impact of National Lottery Funding on Beneficiary Organisations 22

Table 3.4 National Lottery Retail Agents – Importance of Economic and Social Contributions of the National Lottery in Ireland Over the Past 15 Years

24

Table 3.5 Total National Lottery Prizes (€m) – 2007-2017 27

Table 3.6 Breakdown of National Lottery Prize Winnings by Game (%) – 2011-2017

28

Table 3.7 Lotto Prize Winnings over €1m (2015-2017) 30

Table 3.8 EuroMillions Prize Winnings over €1m (2016-2017) 30

Table 3.9 Breakdown of National Lottery Prize Winners by Prize Category and Game – 2017 (Number of Winners)

31

Table 3.10 Comparative Demographic Analysis – National Lottery Players v Population – 2017

32

Table 3.11 Comparative Demographic Analysis – Share of Spend on National Lottery Products

33

Tables, Figures & Boxes Page

ii

Table 3.12 National Lottery Participation by Social Class Indicator 33

Table 3.13 Number of National Lottery Retail Agents – 2006-2017 36

Table 3.14 National Lottery Commissions Paid to Retailers/Agents – 2006-2017 37

Table 3.15 Estimated Total Sales (Lottery and Non-Lottery) of National Lottery Retail Agents – 2017

37

Table 3.16 Estimated Impact on Retail Agents from Non-Lottery Related Retail Sales – 2017

38

Table 3.17 Estimated Employment and Incomes Supported Through Non-Lottery Related Retail Sales – 2017

38

Table 3.18 Summary of Estimated Impacts of National Lottery on Retail Agents – 2017

39

Table 3.19 National Lottery Retail Agents by Region – 2017 39

Table 3.20 National Lottery Revenue at Retail Agents by Region – 2017 40

Table 3.21 National Lottery Retail Agents – Estimated Total Retail Sales at National Lottery Retail Agents

41

Table 3.22 National Lottery Retail Agents – Perceived Estimate of the Extent to Which the Availability Of National Lottery Products Contributes To Additional, Non-Lottery Related Sales

42

Table 3.23 Direct Employment Supported by Non-Lottery Related Sales at Retail Agents (FTEs) – 2017

43

Table 3.24 Direct Incomes Supported by Non-Lottery Related Sales at Retail Agents (FTEs) – 2017

44

Table 4.1 Consumer Expenditure on National Lottery Products (€m) – 2012-2017

48

Table 4.2 Economy-Wide Impacts of Consumer Expenditure on Lottery Products (€m) – 2012-2017

49

Tables, Figures & Boxes Page

Indecon International Economic ConsultantsIndependent Socio-Economic Impact Assessment of the National Lottery

iii

Table 4.3 Scenarios for Consumer Spending Impact of National Lottery Prize Winnings – Indicative Assumptions re % of Prizes Spent by Size Category of Winnings – Estimated 2017 Impact

50

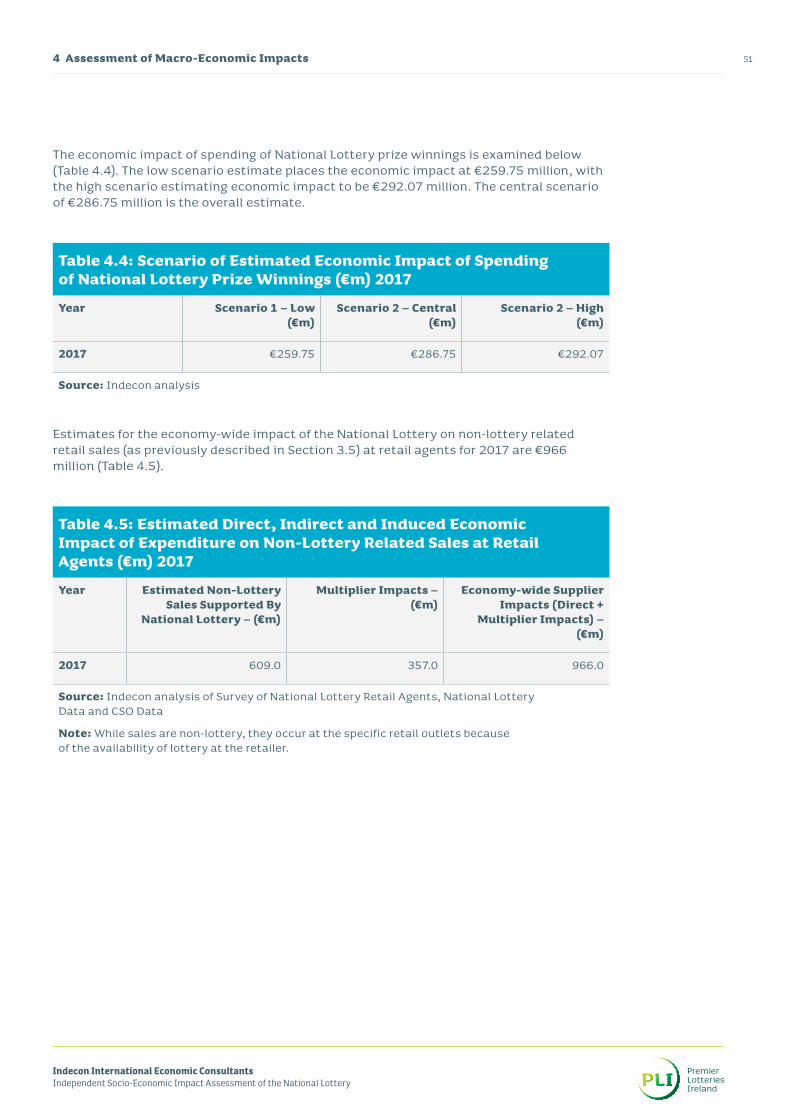

Table 4.4 Scenario of Estimated Economic Impact of Spending of National Lottery Prize Winnings (€m) – 2017

51

Table 4.5 Estimated Direct, Indirect and Induced Economic Impact of Expenditure on Non-Lottery Related Retail Sales at Retail Agents (€m) – 2017

51

Table 4.6 Overall Direct, Indirect and Induced Impact of Consumer Spending on Lottery and Non-Lottery Products (€m) – 2017

52

Table 4.7 Estimated Direct, Indirect and Induced Economic Impact of Expenditure on Non-Lottery Related Retail Sales at Retail Agents (€m) – 2017

53

Table 4.8 Sub-Supplier Expenditure Impacts of National Lottery Beneficiary Funding (€m) – 2017

53

Table 4.9 Direct, Indirect and Induced Employment Supported by Premier Lotteries Ireland (FTEs) – 2017

54

Table 4.10 Direct, Indirect and Induced Impact of Premier Lotteries Ireland Expenditure on Incomes (€m) – 2017

55

Table 4.11 Direct, Indirect and Induced Employment Supported by National Lottery Retail Agents’ Commissions (FTEs) – 2017

55

Table 4.12 Direct, Indirect and Induced Employment Supported by Non-Lottery Related Sales at Retail Agents (FTEs) – 2017

56

Table 4.13 Direct, Indirect and Induced Employment Incomes Supported by National Lottery Sales at Retail Agents (€m) – 2017

56

Table 4.14 Direct, Indirect and Induced Employment Incomes Supported by Non-Lottery Related Sales at Retail Agents (€m) – 2017

57

Table 4.15 Direct, Indirect and Induced Employment Supported by National Lottery Beneficiary Funding (FTEs) – 2017

57

Tables, Figures & Boxes Page

iv

Table 4.16 Direct, Indirect and Induced Employment Incomes Supported by National Lottery Beneficiary Funding (€m) – 2017

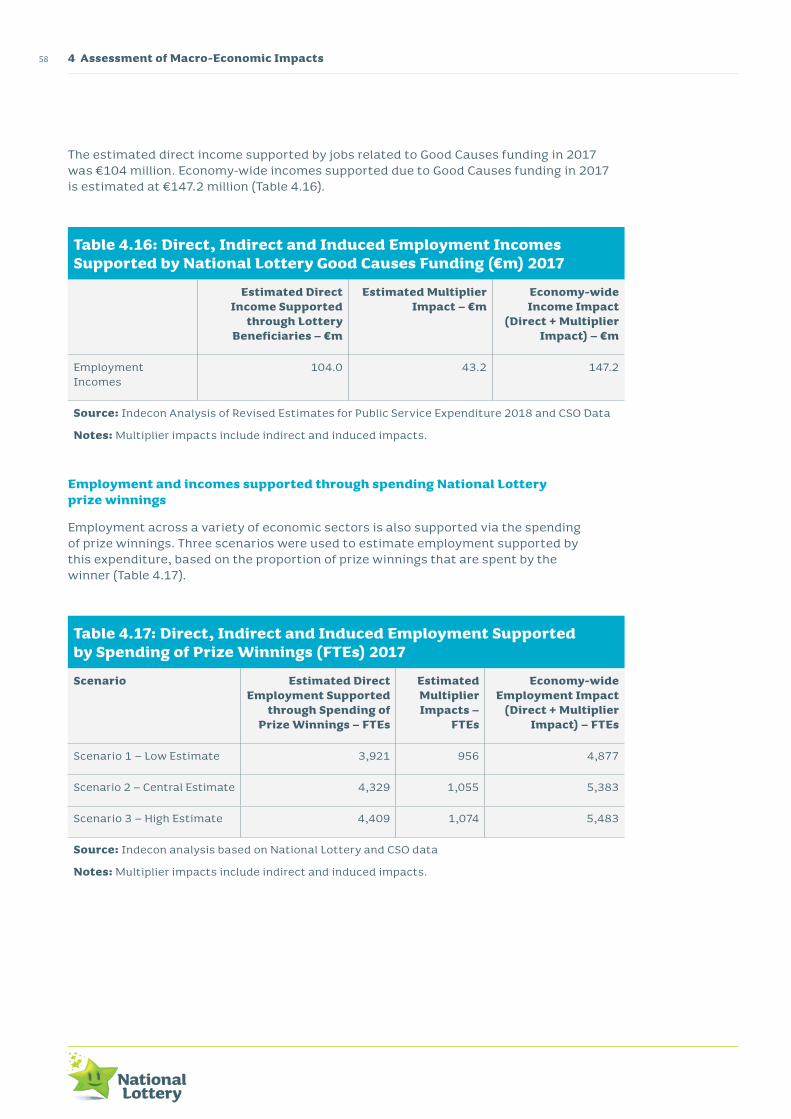

58

Table 4.17 Direct, Indirect and Induced Employment Supported by Spending of Prize Winnings (FTEs) – 2017

58

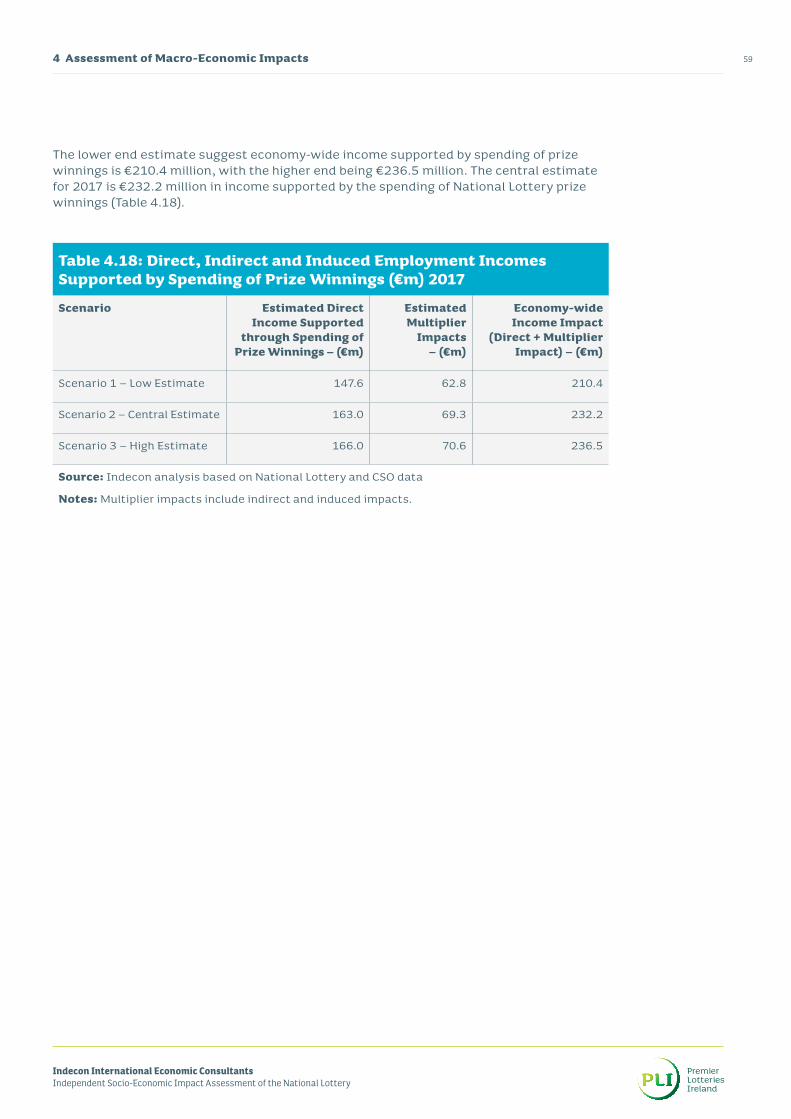

Table 4.18 Direct, Indirect and Induced Employment Incomes Supported by Spending of Prize Winnings (€m) – 2017

59

Table 4.19 Breakdown of Overall Employment Supported by the National Lottery (FTEs) – 2017

60

Table 4.20 Estimated Direct, Indirect and Induced Income Impacts Supported by National Lottery (€m) – 2017

61

Table 4.21 Estimated Taxation Paid to the Exchequer by National Lottery Employees 2017 – (€)

62

Table 4.22 Estimated Taxation Paid to the Exchequer by National Lottery Beneficiary Funding 2017 – (€)

62

Table 4.23 Estimated Taxation Paid to the Exchequer by Retail Agent Employees 2017 – (€)

63

Table 4.24 Estimated Taxation Paid to the Exchequer by Retail Agent Employees Supported by Non-National Lottery Sales in 2017 – (€)

63

Table 4.25 Estimated Taxation Paid to the Exchequer by Employees Supported by the Respending of National Lottery Prize Winnings – (€)

64

Table 4.26 Estimated Exchequer Impacts Supported by National Lottery (€m) – 2017

64

Table 5.1 Revenue Commissioner Data on Betting Receipts (€ Million) – 2011-2016

66

Table 5.2 Indicative Estimate of Size of Gambling Sector in Ireland – 2016 67

Table 5.3 Awareness of the Concept of Bet-On-Lottery Websites 71

Tables, Figures & Boxes Page

Indecon International Economic ConsultantsIndependent Socio-Economic Impact Assessment of the National Lottery

v

Table 5.4 Awareness of Bet-On-Lottery Websites in Ireland 71

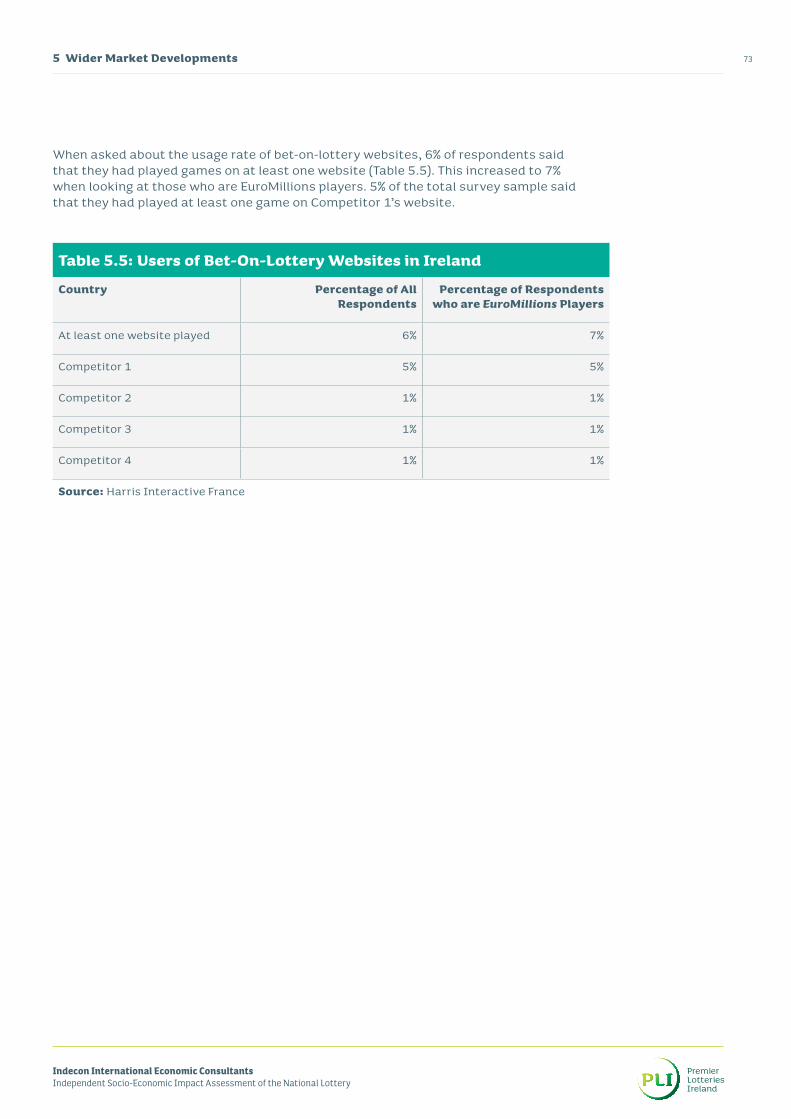

Table 5.5 Users of Bet-On-Lottery Websites in Ireland 73

Table 5.6 EuroMillions Sales Per Capita – € (2015-2016) 76

Table 5.7 Number of Residents per Retailer 77

Table 5.8 Per Capita Total Sales 77

Table 5.9 Per Capita Lottery Sales 78

Table 5.10 Per Capita Scratch Card Sales 78

Table 5.11 Sales Per Capita (2015-2016) (Countries/States with Pop Between 3-5 Million)

79

Figure 1.1 Overview of Indecon’s Methodological Approach to Assessment 03

Figure 1.2 Framework Used to Assess Economic and Social Impacts of National Lottery

05

Figure 2.1 Development of National Lottery Sales – Overall Sales, € Million 08

Figure 2.2 Timeline of National Lottery Products 09

Figure 2.3 National Lottery Products – % of Sales by Game – 1990 vs. 2017 13

Figure 3.1 Breakdown of Total Public Expenditure on Activities which are Part-funded by the National Lottery – 2017 – %

21

Figure 3.2 National Lottery Funding Beneficiaries – Perceived Significance of Economic and Social Contribution of the National Lottery in Ireland over the Past 15 Years

23

Figure 3.3 Historical Development of National Lottery Prize Winnings (1987-2017)

25

Tables, Figures & Boxes Page

vi

Figure 3.4 Prize Winnings as % National Lottery Sales – 1987-2017 26

Figure 3.5 Breakdown of National Lottery Prize Pay-Out by Game – 2017 – % 29

Figure 3.6 Weekly Retail Sales (DBC & SC) and Number of Authorised Agents, 2014-2017

34

Figure 3.7 National Lottery Sales Per Retail Agent Excl. Select Agents (Draw Based Games v Scratch Cards)

35

Figure 4.1 Components of Macro-Economic Impacts of the National Lottery 46

Figure 4.2 Composition of National Lottery Net Consumption Impact on GDP 47

Figure 5.1 Frequency of Gambling (UK) – 2013-2016 68

Figure 5.2 Type of Gambling Activity (UK – In Person) – 2016 69

Figure 5.3 Type of Gambling Activity (UK – Online) – 2016 70

Figure 5.4 Awareness of National Lottery Competitor 1 (Aug 2016-May 2017) 72

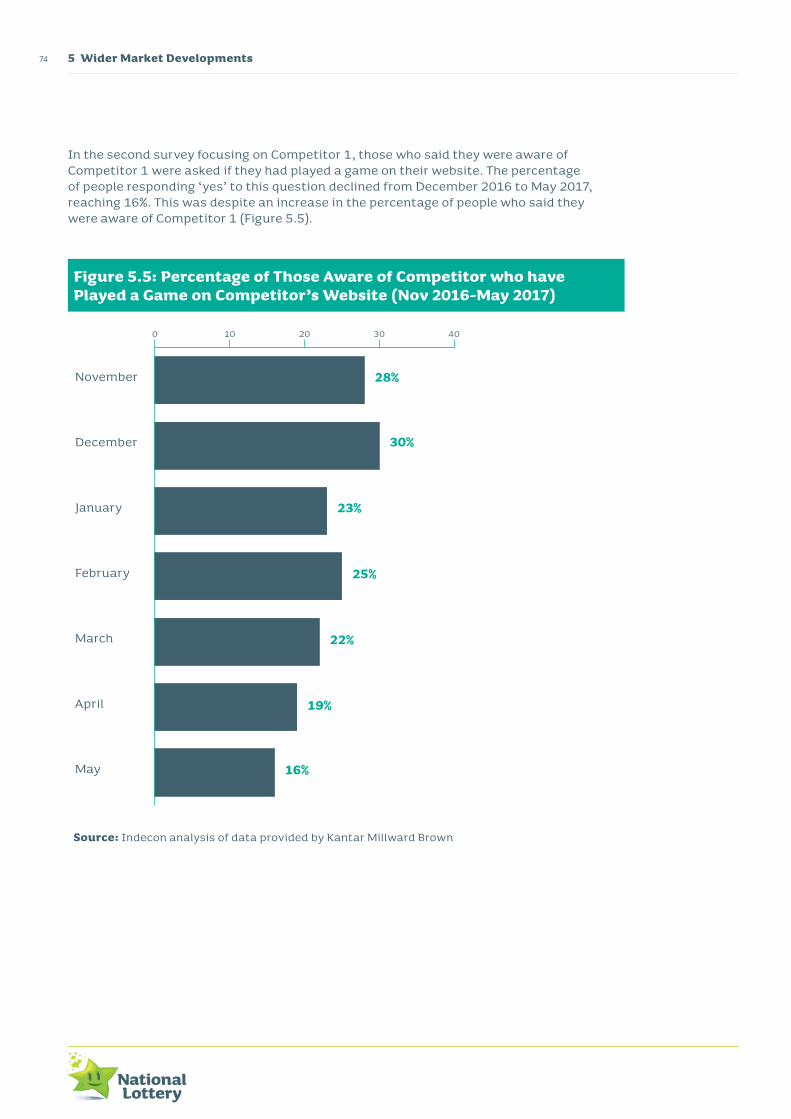

Figure 5.5 Percentage of Those Aware of Competitor who have Played a Game on Competitor’s Website (Nov 2016-May 2017)

74

Tables, Figures & Boxes Page

Indecon International Economic ConsultantsIndependent Socio-Economic Impact Assessment of the National Lottery

vii

Executive Summaryviii

Glossary of Terms and Abbreviations

Good Causes An organisation in receipt of National Lottery Good Causes funding.

Consumer Surplus This is the difference between what a consumer is willing to pay for a good or service and what they actually pay for the good or service.

CSO Central Statistics Office

DBG Draw Based Games

FTE Full-Time Equivalent – The unit which indicates the time worked by one employee on a full-time basis. It is used to convert the hours worked by part-time employees into the hours worked by full-time employees.

GDP Gross Domestic Product

Indirect Effects Indirect impacts include the knock-on business activity that is supported through direct economic activity, e.g., the positive economic impacts of upstream suppliers.

Induced Effects Induced effects are concerned with the knock-on impact of household consumption due to direct economic activity. This will include the impact of additional employment wages directly supported by the National Lottery.

IWG Digital Instant Win Games

NLF National Lottery Fund

NUTS Nomenclature of Territorial Units for Statistics. A classification system for dividing up territory of countries in the EU for the purpose of socio-economic analyses of these regions. There are eight NUTS 3 level regions in Ireland, which is the level covered in this report.

Select Channel Select channel is a channel that utilises the infrastructure of a third party payment provider to deliver a limited range of National Lottery Services.

Core Agents Our core agents form the primary sales network that provide full range of National Lottery services using proprietary National Lottery telecommunications and terminal hardware.

Executive Summary

Introduction and key findingsThis independent assessment of the socio-economic impact and contribution of the National Lottery in Ireland was undertaken by Indecon International Research Economists on behalf of Premier Lotteries Ireland, operator of the National Lottery. The National Lottery was established in 1987 under the National Lottery Act 1986 with the purpose of raising funds to support Good Causes in the areas of youth, sports, recreation, health, arts, culture, national heritage and the Irish language.

The report examines the National Lottery’s impact in its contribution to GDP, employment and to Good Causes. A rigorous and empirical approach was used to assess the evidence based on Irish and international datasets; new primary research and econometric modelling.

Indecon International Economic ConsultantsIndependent Socio-Economic Impact Assessment of the National Lottery

ixExecutive Summary

Executive Summaryx

Macro-Economic Impacts

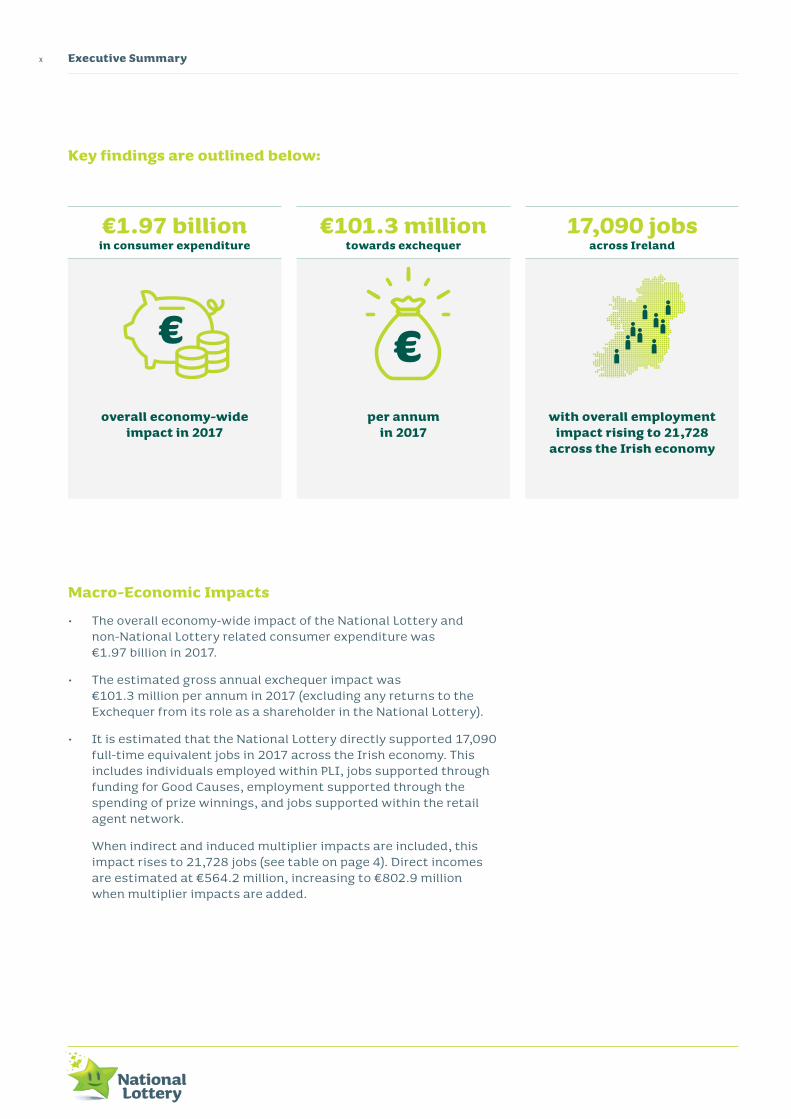

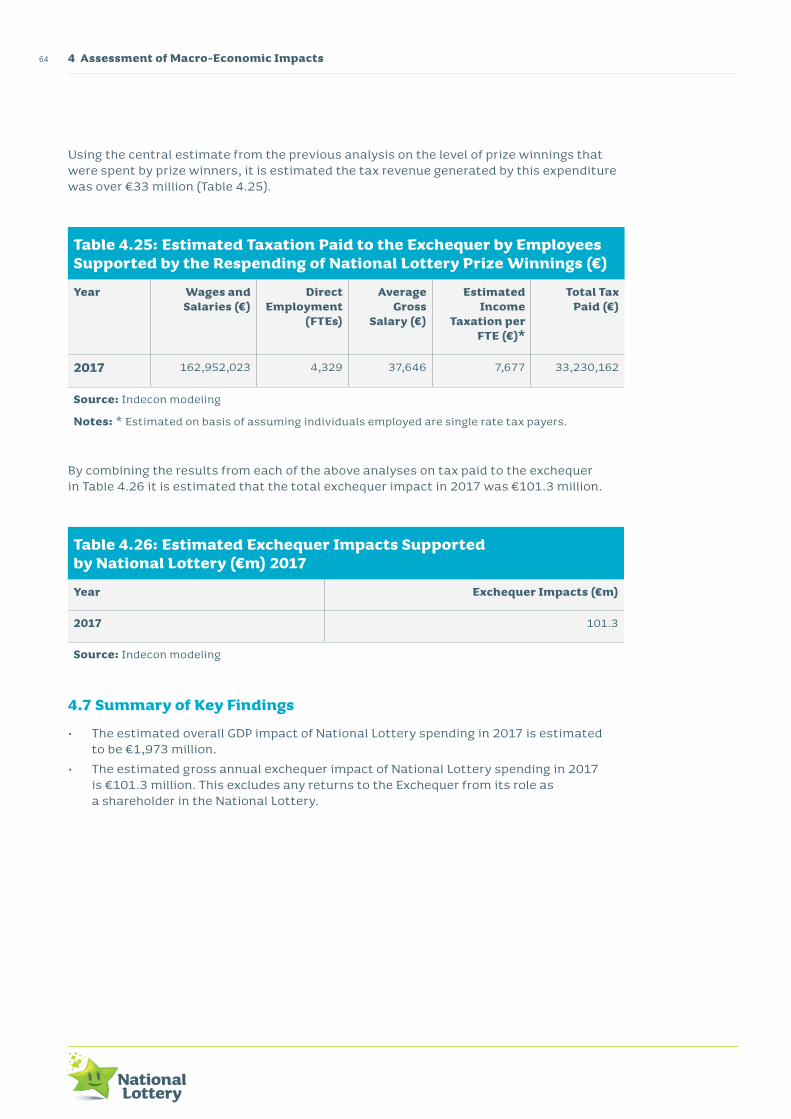

• The overall economy-wide impact of the National Lottery and non-National Lottery related consumer expenditure was €1.97 billion in 2017.

• The estimated gross annual exchequer impact was €101.3 million per annum in 2017 (excluding any returns to the Exchequer from its role as a shareholder in the National Lottery).

• It is estimated that the National Lottery directly supported 17,090 full-time equivalent jobs in 2017 across the Irish economy. This includes individuals employed within PLI, jobs supported through funding for Good Causes, employment supported through the spending of prize winnings, and jobs supported within the retail agent network.

When indirect and induced multiplier impacts are included, this impact rises to 21,728 jobs (see table on page 4). Direct incomes are estimated at €564.2 million, increasing to €802.9 million when multiplier impacts are added.

Key findings are outlined below:

overall economy-wide impact in 2017

per annum in 2017

with overall employment impact rising to 21,728

across the Irish economy

€1.97 billion in consumer expenditure

€101.3 million towards exchequer

17,090 jobs across Ireland

xi

Indecon International Economic ConsultantsIndependent Socio-Economic Impact Assessment of the National Lottery

Executive Summary

Breakdown of Overall Employment Supported by the National Lottery (FTEs) – 2017

Direct Employment Supported – FTEs

Indirect and Induced Employment*

Total Employment**

Employment in PLI/National Lottery

96 23 119

Employment supported by non-Lottery sales in retail agent network

9,192 2,240 11,433

Employment supported by retail agent commissions

709 173 882

Employment supported by National Lottery funding to Good Causes organisations

2,763 1,147 3,910

Employment supported by spending of National Lottery prize winnings

4,329 1,055 5,383

Total Employment Impact 17,090 4,638 21,728

Source: Indecon analysis* Indirect and Induced Employment: Multiplier Impacts – Additional Indirect and Induced Employment

Supported across Irish Economy – FTEs** Total Employment: Supported Across Irish Economy (incl. Multiplier Impacts) – FTEs

Executive Summaryxii

from 1987 to the end of 2017

€5.1 billion raised for Good Causes

by National Lottery participants in 2017

an estimated €620,000 was raised every day

Impact of National Lottery Funding on Good Causes organisations

• More than €5.1 billion has been raised for Good Causes between the establishment of the National Lottery in 1987 and the end of 2017. The total sum raised for Good Causes in 2017 was €226.3 million.

• It is estimated that 2,763 full-time equivalent jobs were supported in Good Causes beneficiary organisations in 2017. This increases to 3,910 jobs when multiplier impacts are included.

• The number of volunteers in organisations supported by National Lottery funding is estimated at 177,000. Total number of hours volunteered in 2017 is estimated to have an economic value amounting to €79.7 million.

• A high percentage of Good Causes state that the National Lottery has made a “very significant” or “significant” contribution to youth and recreation activities and organisations.

¤The estimated number of

volunteers in organisations supported by National Lottery

Good Causes funding

177,000 volunteers in organisations

xiii

Indecon International Economic ConsultantsIndependent Socio-Economic Impact Assessment of the National Lottery

Executive Summary

Impact of National Lottery on Retailers

• Direct employment within National Lottery retail agents supported by sales of non-Lottery products, added to employment supported by the retail agent commissions, was estimated to be 9,902 full-time equivalent jobs in 2017.

• Retail agents’ commissions combined with the sale of non-National Lottery products in shops which are National Lottery agents was estimated at €609 million in 2017.

Wider Market Developments

• There has been a rise in online gaming and the growth in competitors offering bets on lottery games.

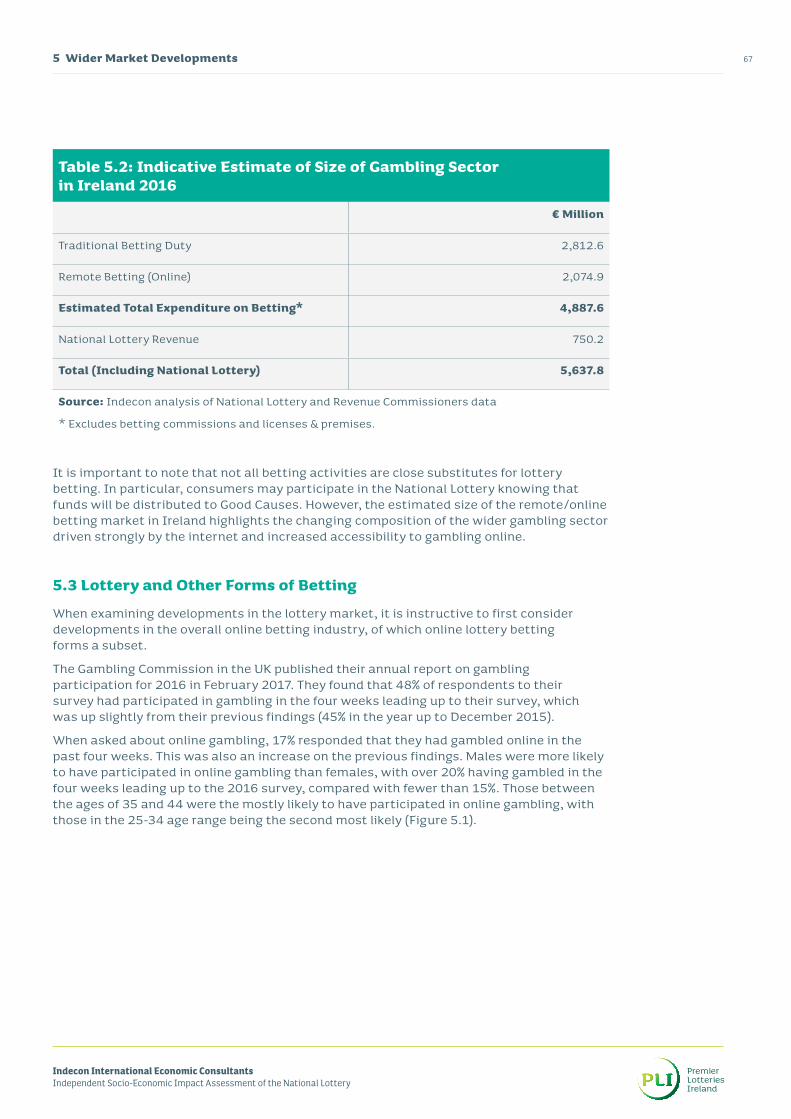

• Indecon estimates that the total size of the betting and lotteries sector in Ireland was €5.6 billion. National Lottery’s sales represented 13% of this market.

• One of the key differences between the National Lottery and its competitors is that the National Lottery is mandated to raise funds for Good Causes. Approximately 91% of revenue generated by the National Lottery is returned to the community in prizes, retail commissions and Good Causes.

Non-National Lottery sales at retail agents supported

by the presence of National Lottery in 2017

National Lottery’s sales represented 13% of this market in 2017

€5.6 billion size of betting and lottery sector

in the form of prize winnings, funding for Good Causes and

retailer commissions

91% of generated revenue goes back into the community

€609 million sales at retail agents

13%

91%

Executive Summaryxiv

€53

€47

€69

€98

€104 €1

13 €122

€128

€128 €1

36

€141 €1

59

€163 €1

76

€173 €1

91

€187 €2

03 €218

€245

€268

€263

€244

€232

€226

€188

€213

€206

Micro-economic and social impacts

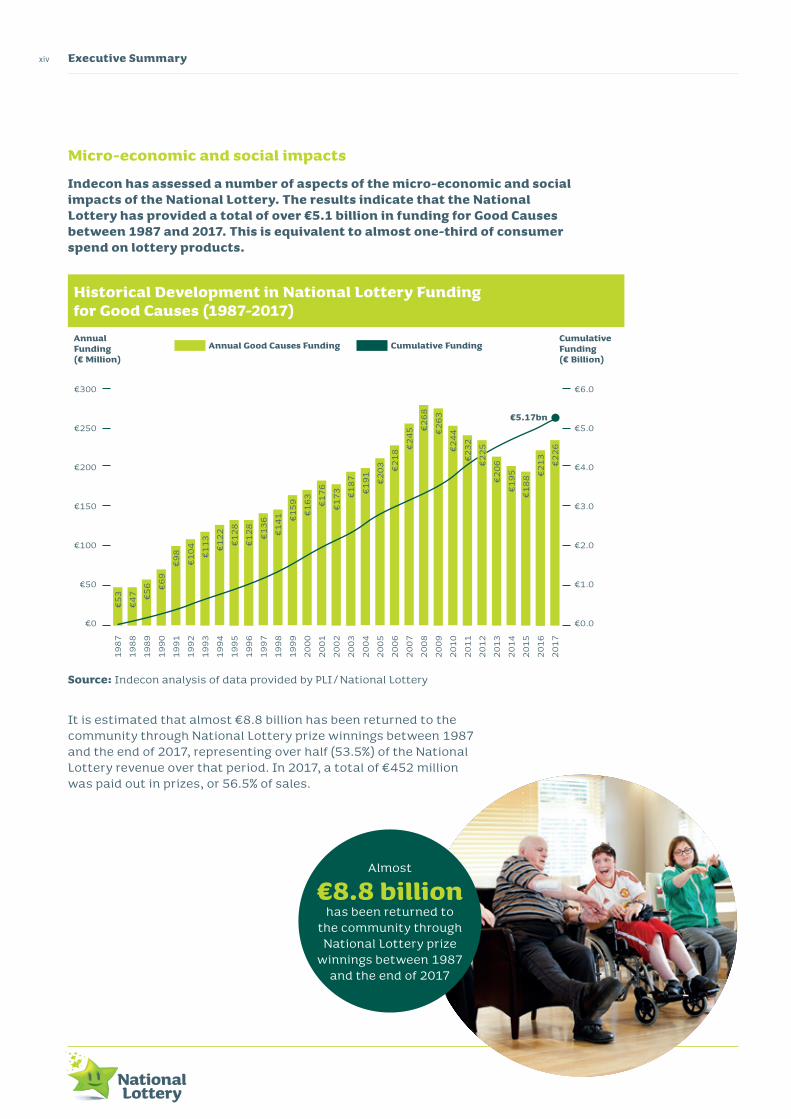

Indecon has assessed a number of aspects of the micro-economic and social impacts of the National Lottery. The results indicate that the National Lottery has provided a total of over €5.1 billion in funding for Good Causes between 1987 and 2017. This is equivalent to almost one-third of consumer spend on lottery products.

It is estimated that almost €8.8 billion has been returned to the community through National Lottery prize winnings between 1987 and the end of 2017, representing over half (53.5%) of the National Lottery revenue over that period. In 2017, a total of €452 million was paid out in prizes, or 56.5% of sales.

Almost

€8.8 billionhas been returned to

the community through National Lottery prize

winnings between 1987 and the end of 2017

Source: Indecon analysis of data provided by PLI/National Lottery

Historical Development in National Lottery Funding for Good Causes (1987-2017)Annual Funding (€ Million)

€5.17bn

Cumulative Funding (€ Billion)

€300

€250

€200

€150

€100

€50

€0

€6.0

€5.0

€4.0

€3.0

€2.0

€1.0

€0.0

1987

1988

1989

1990

1991

1992

1993

1994

1995

1996

1997

1998

1999

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

2011

2012

2013

2014

2015

2016

2017

€56

Annual Good Causes Funding Cumulative Funding

€225

€195

xv

Indecon International Economic ConsultantsIndependent Socio-Economic Impact Assessment of the National Lottery

Executive Summary

Estimated Economic Impacts of National Lottery on Retail Agent Network

2017

Retail Agent Commissions (€m) €47.0 m

Non-lottery sales supported by presence of National Lottery agency (€m)

€609.0 m

Employment supported within National Lottery retail agent network*

9,902 FTEs

Source: Indecon analysis and modelling

* Includes Direct employment within National Lottery retail agents supported by sales of non-Lottery products, in addition to employment supported by the retail agent commissions

The income of National Lottery retail agents around the country is boosted with retail commissions and non-lottery sales. Because of high opportunity and displacement costs, these gains are likely to be at a cost to non-Lottery retailers. National Lottery funding may, however, help smaller retailers and post offices to remain economically viable.

Executive Summaryxvi

Contribution of lottery funding to Good CausesOur survey of Good Causes organisations demonstrates that recipients of National Lottery funding believe it has made a very significant or significant economic and social contribution to youth and recreation activities, sporting activities, local communities, and arts, culture and heritage (see table below).

Provision of funding for social enterprises

Support for Irish language activities and organisations

Provision for funding for charitable organisations

Provision for funding for community health and welfare facilities in Ireland

Contribution to exchequer taxation

42.1%

44.4%

48.6%

55%

68.9%

75%

76.3%

78%

82.1%

Support for local Communities

Support for arts, culture and heritage organisations and activites

Provision for funding for sporting activities and organisations

Provision for funding for youth and recreation activities and organisations

Source: Indecon analysis

0% 10% 20% 30% 40% 50% 60% 70% 80% 90% 100%

xvii

Indecon International Economic ConsultantsIndependent Socio-Economic Impact Assessment of the National Lottery

Executive Summary

The economic value of volunteering activity

in Good Causes beneficiary organisations is estimated

at over

€79.7 million

per annum

Research shows that Good Causes beneficiaries considered that National Lottery funding has made a “very significant” or “significant” economic and social contribution, especially in the areas of youth and recreation, sport, local communities, arts, culture and heritage.

Empirical evidence from the survey of Good Causes organisations and published accounts suggests that on average 13% of overall funding came from the National Lottery Good Causes Fund, up to 90% in some cases. 2,763 full-time equivalent jobs are supported in Good Causes beneficiary organisations which have over 177,000 volunteers. The economic value is estimated at over €79.7 million per annum.

Employment and volunteering activity in Good Causes organisations indicate that 2,763 full-time equivalent jobs are supported by National Lottery funding. These organisations have over 177,000 volunteers and the economic value is estimated at over €79.7 million per annum.

Impact of National Lottery Funding on Good Causes organisations

Lottery funding as % of total organisation funding base 13.05%

Estimated Total Employment in Good Causes organisations which is directly supported by National Lottery Funding (FTEs)

2,763

Estimated Total Number of Volunteers in Good Causes organisations (Persons)

177,293

Estimated Total Annual Volunteer Hours 8,615,273

Estimated Total Economic Value of Volunteering in Good Causes organisations

€79.7 million

Source: Indecon analysis based on research among selected National Lottery funding Good Causes organisations, survey of Good Causes organisations and data from CSO

On average

13% of overall Good Causes

beneficiaries funding was provided by the National

Lottery

Executive Summaryxviii

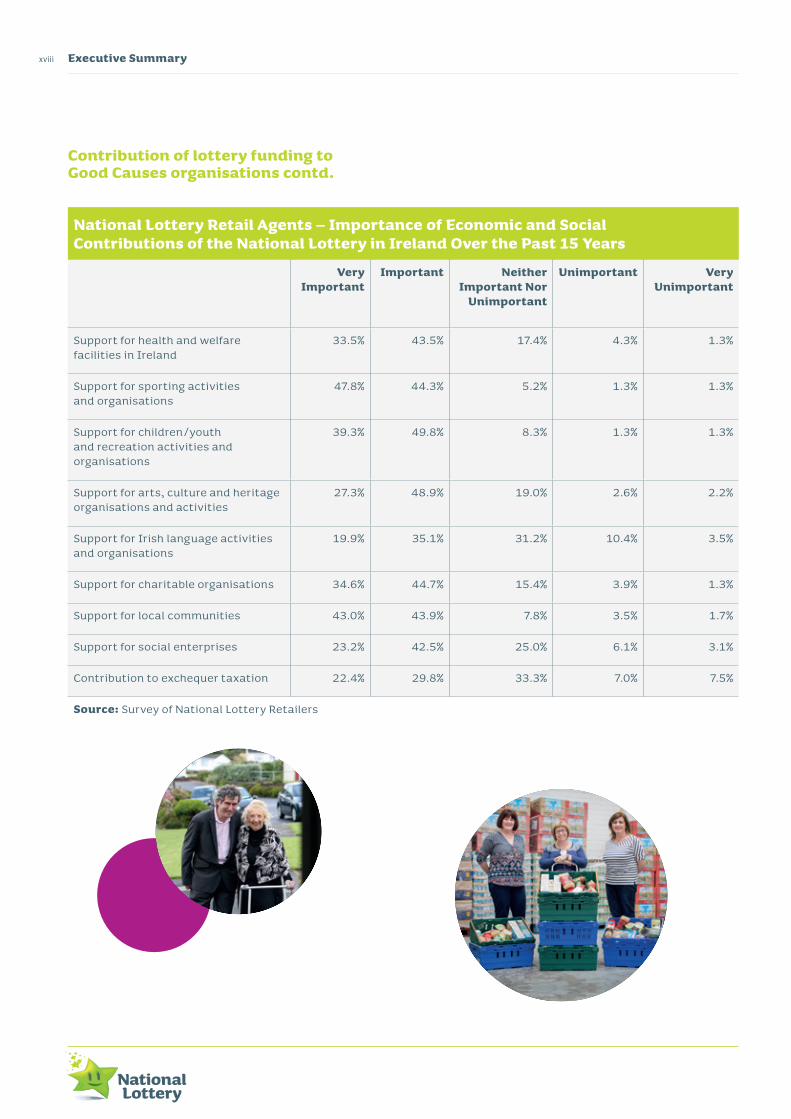

National Lottery Retail Agents – Importance of Economic and Social Contributions of the National Lottery in Ireland Over the Past 15 Years

Very Important

Important Neither Important Nor

Unimportant

Unimportant Very Unimportant

Support for health and welfare facilities in Ireland

33.5% 43.5% 17.4% 4.3% 1.3%

Support for sporting activities and organisations

47.8% 44.3% 5.2% 1.3% 1.3%

Support for children/youth and recreation activities and organisations

39.3% 49.8% 8.3% 1.3% 1.3%

Support for arts, culture and heritage organisations and activities

27.3% 48.9% 19.0% 2.6% 2.2%

Support for Irish language activities and organisations

19.9% 35.1% 31.2% 10.4% 3.5%

Support for charitable organisations 34.6% 44.7% 15.4% 3.9% 1.3%

Support for local communities 43.0% 43.9% 7.8% 3.5% 1.7%

Support for social enterprises 23.2% 42.5% 25.0% 6.1% 3.1%

Contribution to exchequer taxation 22.4% 29.8% 33.3% 7.0% 7.5%

Source: Survey of National Lottery Retailers

Contribution of lottery funding to Good Causes organisations contd.

xix

Indecon International Economic ConsultantsIndependent Socio-Economic Impact Assessment of the National Lottery

Executive Summary

Macro-economic impactsIn assessing the wider, macro-economic impacts of the National Lottery, Indecon examined the:

• employment and employment incomes and associated consumer expenditure; and,

• contribution to the Exchequer from income tax as a result of this employment.

Significant funding for sporting activities, children

and youth recreation and wider impact on local

communities

Almost €8.8 billion was been returned to the community through

National Lottery prize winnings between 1987

and the end of 2017

¤

Executive Summaryxx

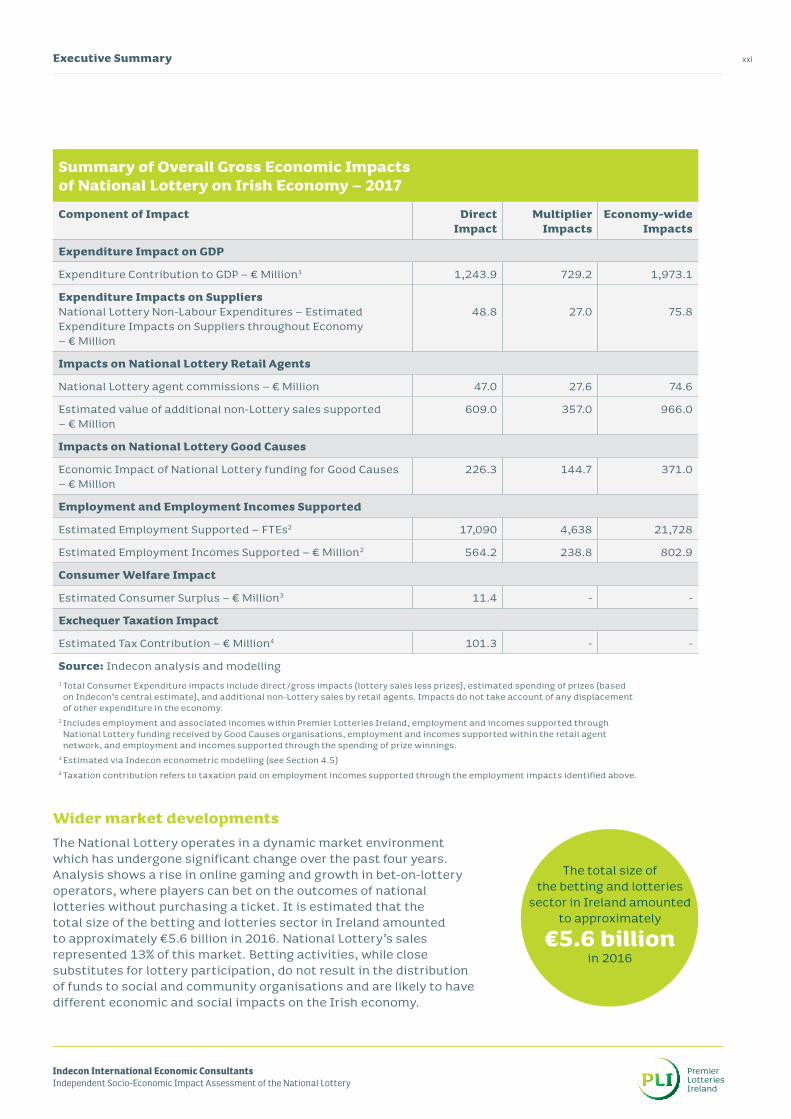

Summary of Components of Overall Economic Impact of National LotteryThe overall economic impact of the National Lottery in 2017 are summarised in the table on page 14. Overall GDP impact of lottery spending is estimated to be €1.973 billion, and tax to the exchequer of €101.3 million (excluding any returns to the Exchequer from its role as a shareholder in the National Lottery). Estimates are based on conservative assumptions and recognise that all economic sectors have inter-relationships with other parts of the economy.

overall GDP impact of lottery spending in 2017

estimated

€1.973 billion

per annum in 2017

€101.3 million towards exchequer

National Lottery funding for Good Causes in 2017

€226.3 million

¤

xxi

Indecon International Economic ConsultantsIndependent Socio-Economic Impact Assessment of the National Lottery

Executive Summary

Wider market developmentsThe National Lottery operates in a dynamic market environment which has undergone significant change over the past four years. Analysis shows a rise in online gaming and growth in bet-on-lottery operators, where players can bet on the outcomes of national lotteries without purchasing a ticket. It is estimated that the total size of the betting and lotteries sector in Ireland amounted to approximately €5.6 billion in 2016. National Lottery’s sales represented 13% of this market. Betting activities, while close substitutes for lottery participation, do not result in the distribution of funds to social and community organisations and are likely to have different economic and social impacts on the Irish economy.

Summary of Overall Gross Economic Impacts of National Lottery on Irish Economy – 2017

Component of Impact Direct Impact

Multiplier Impacts

Economy-wide Impacts

Expenditure Impact on GDP

Expenditure Contribution to GDP – € Million1 1,243.9 729.2 1,973.1

Expenditure Impacts on Suppliers National Lottery Non-Labour Expenditures – Estimated Expenditure Impacts on Suppliers throughout Economy – € Million

48.8

27.0

75.8

Impacts on National Lottery Retail Agents

National Lottery agent commissions – € Million 47.0 27.6 74.6

Estimated value of additional non-Lottery sales supported – € Million

609.0 357.0 966.0

Impacts on National Lottery Good Causes

Economic Impact of National Lottery funding for Good Causes – € Million

Source: Indecon analysis and modelling1 Total Consumer Expenditure impacts include direct/gross impacts (lottery sales less prizes), estimated spending of prizes (based

on Indecon’s central estimate), and additional non-Lottery sales by retail agents. Impacts do not take account of any displacement of other expenditure in the economy.

2 Includes employment and associated incomes within Premier Lotteries Ireland, employment and incomes supported through National Lottery funding received by Good Causes organisations, employment and incomes supported within the retail agent network, and employment and incomes supported through the spending of prize winnings.

3 Estimated via Indecon econometric modelling (see Section 4.5)4 Taxation contribution refers to taxation paid on employment incomes supported through the employment impacts identified above.

The total size of the betting and lotteries

sector in Ireland amounted to approximately

€5.6 billion in 2016

Executive Summaryxxii

Conclusion

This report shows that the National Lottery has had a significant impact on the Irish economy, including contributing to GDP and employment. This is evident from the independent estimates presented. In addition a key social impact of the National Lottery has been the provision of funds.

1 Introduction and Methodology

Indecon International Economic ConsultantsIndependent Socio-Economic Impact Assessment of the National Lottery

1 Introduction and Methodology2

1 Introduction and Methodology1.1 Introduction

This independent assessment of the socio-economic impact and contribution of the National Lottery in Ireland was undertaken by Indecon Research Economists on behalf of Premier Lotteries Ireland DAC (operators of the National Lottery). The National Lottery was established in 1987 under the National Lottery Act 1986 for the benefit of Good Causes. Since its launch 31 years ago (in 1987), the National Lottery has raised more than €5.3 billion for Good Causes in the areas of youth, sport, recreation, amenities, health, welfare, arts, culture, national heritage and the Irish language.

Initially operated by An Post, the Government (under the National Lottery Act 2013) launched a competitive tender process to operate the National Lottery. In November 2014 a 20-year licence to run the National Lottery was awarded to Premier Lotteries Ireland (PLI).

This report examines a number of key aspects of the National Lottery including:

• The micro-economic and social impacts; • The macro-economic impacts of the lottery on the Irish economy, including

its contribution to Gross Domestic Product (GDP), employment and its impacts on suppliers;

• Exchequer impacts from additional taxation and the estimated value of consumer surplus.

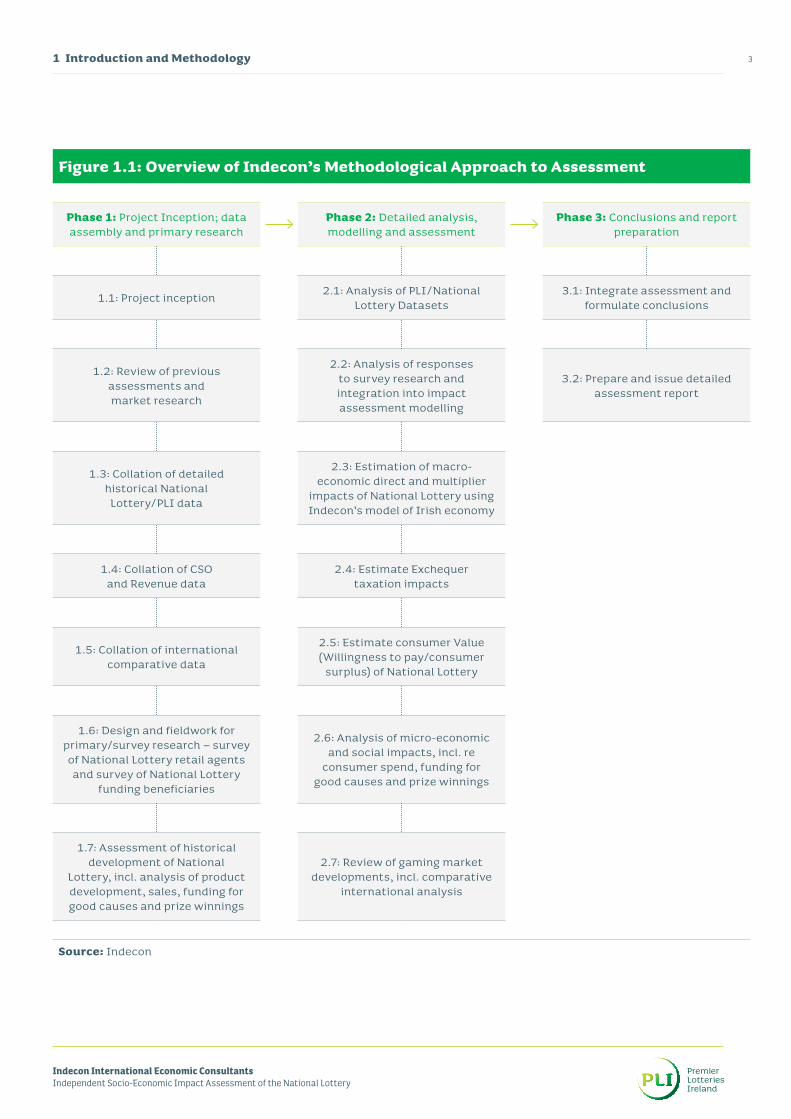

1.2 Methodological Approach

A schematic description of the rigorous methodology used is presented below (Figure 1.1)

3

Indecon International Economic ConsultantsIndependent Socio-Economic Impact Assessment of the National Lottery

1 Introduction and Methodology

Figure 1.1: Overview of Indecon’s Methodological Approach to Assessment

Phase 1: Project Inception; data assembly and primary research

Phase 2: Detailed analysis, modelling and assessment

Phase 3: Conclusions and report preparation

1.1: Project inception 2.1: Analysis of PLI/National Lottery Datasets

3.1: Integrate assessment and formulate conclusions

1.2: Review of previous assessments and market research

2.2: Analysis of responses to survey research and integration into impact assessment modelling

3.2: Prepare and issue detailed assessment report

1.3: Collation of detailed historical National Lottery/PLI data

2.3: Estimation of macro-economic direct and multiplier

impacts of National Lottery using Indecon’s model of Irish economy

1.4: Collation of CSO and Revenue data

2.4: Estimate Exchequer taxation impacts

1.5: Collation of international comparative data

2.5: Estimate consumer Value (Willingness to pay/consumer

surplus) of National Lottery

1.6: Design and fieldwork for primary/survey research – survey of National Lottery retail agents and survey of National Lottery

funding beneficiaries

2.6: Analysis of micro-economic and social impacts, incl. re

consumer spend, funding for good causes and prize winnings

1.7: Assessment of historical development of National

Lottery, incl. analysis of product development, sales, funding for good causes and prize winnings

2.7: Review of gaming market developments, incl. comparative

international analysis

Source: Indecon

1 Introduction and Methodology4

1.2.1 Framework for assessment of impacts

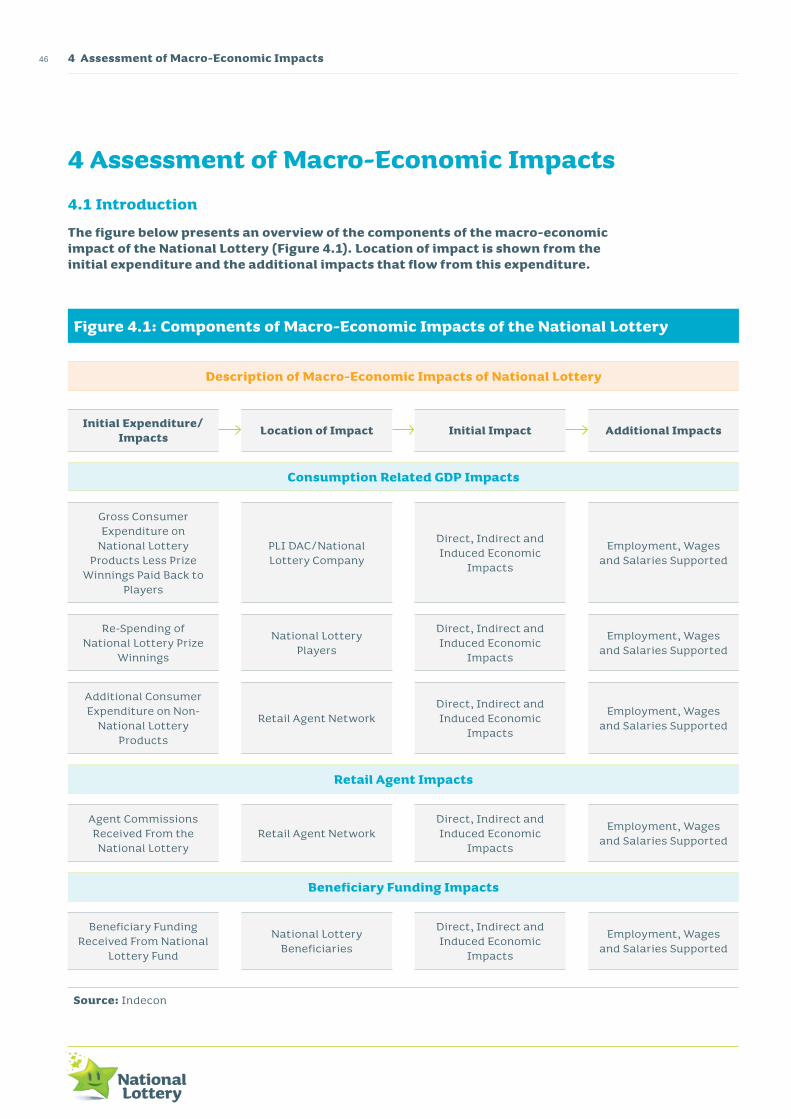

This assessment builds on Indecon’s previous research into the impact of the National Lottery and examines a diverse set of economic and social impacts associated with the National Lottery. A schematic description of the conceptual framework was applied in completing the assessment is set out in the figure below (Figure 1.2).

5

Indecon International Economic ConsultantsIndependent Socio-Economic Impact Assessment of the National Lottery

1 Introduction and Methodology

Figure 1.2: Framework Used to Assess Economic and Social Impacts of National Lottery

National Lottery Company

Direct Consumer Expenditure Impact

(Lottery Sales less Prizes Paid Out

Lottery Consumer Expenditure

Impact on GDPPrize Winners Prize Winnings

Impact of Re-Expenditure

of Prize Winnings

Lottery Retail AgentsAdditional

Non-Lottery Sales within Retail Agents

National Lottery Company

National Lottery Company Expenditures

Expenditures on Sub-Supply Inputs

Expenditure Impacts on Sub-SuppliersRetail Agents

Lottery Funding Beneficiaries

Funding for Good Causes Prize Winnings

National Lottery Company

Employment and Incomes Supported

and Exchequer Taxation Contribution

Employment and Incomes Supported

and Taxation ImpactsRetail Agents

Lottery Funding Beneficiaries

Multiplier Impacts

(a) Consumer Expenditure (b) Expenditure on Sub-Suppliers

(c) Employment and Incomes

Consumer Value/Consumer Surplus Economy-wide Impacts of National Lottery

Source: Indecon

1 Introduction and Methodology6

This detailed assessment uses data from a wide range of sources:

• Detailed financial data on National Lottery provided by Premier Lotteries Ireland, including: • Lottery sales data by product/game by County;• Good Causes funding data;• Prize winnings by game and amount;• National Lottery retail agents, number by County;• Lottery online sales;• Product development and innovations.

• Market research, including tracking surveys on National Lottery players;• Comparative international data, including data from La Fleurs World Lottery Almanac,

the UK Gambling Commission, and Company Service aux Lotteries en Europe (SLE); • Department of Public Expenditure and Reform, Revised Estimates (various years);• Revenue Commissioners data on receipts from betting taxation;• Central Statistics Office (CSO) datasets, including Quarterly National Household

Survey (QNHS) and Household Budget Survey.

This assessment was supported by extensive new primary research, including:

• Survey of National Lottery retail agents; • Survey of National Lottery Good Causes beneficiary organisations.

This research was used to achieve a deeper understanding of the economic and social impacts of the National Lottery and to inform the analysis. Qualitative inputs were obtained from organisations in receipt of funding for Good Causes, and the implications for National lottery retailers was assessed.

1.3 Report Structure

The remainder of this report is structured as follows:

• Section 2 contains a discussion of the development of the National Lottery;• Section 3 assesses the micro-economic and social impacts of the National Lottery;• Section 4 examines the macro-economic impacts of the lottery on Irish economy

as a whole; • Section 5 presents an overview of under market developments.

1.4 Acknowledgements and Disclaimer

Indecon would like to express our gratitude to management and staff at Premier Lotteries Ireland, including Dermot Griffin, Miriam Donohoe, Carol-Anne Bergin, Dorothy Donohoe, Robert Magee, George Canavan, Sile Rooney, Jenny Fisher and Maurice Nolan, for their valuable assistance throughout the process of completing this study.

Particular thanks are due to organisations that received National Lottery funding and National Lottery retail agents who provided valuable inputs.

The usual disclaimer applies and the analysis and findings in this independent report are the sole responsibility of Indecon Research Economists.

2 Development of National Lottery in Ireland

Indecon International Economic ConsultantsIndependent Socio-Economic Impact Assessment of the National Lottery

2 Development of National Lottery in Ireland8

2 Development of National Lottery in Ireland

This section contains an overview of the National Lottery, focusing on developments since its establishment in 1987.

2.1 Trends in Lottery Sales

Total National Lottery Sales since its inception in 1987 are shown below (Figure 2.1). There was a steady increase in sales between 1987 and 2008. However, sales fell from a peak of €840 million in 2008 to €670 million in 2015. This is likely to reflect the economic recession as well as developments in the market environment, including the growth in alternative forms of gaming and of substitute products. There was a return to growth in 2016 with sales of €750 million recorded. Sales in 2017 reached over €800 million for the first time since 2009.

Figure 2.1: Development of National Lottery Sales – € Million

130.0140.2

178.3214.0

300.3320.4

344.4370.0

385.0390.9

411.8427.6

479.2495.4

538.1533.1

559.2578.3

616.4679.1

778.5840.1

815.1772.0

761.4735.1

685.2687.7

670.4750.2

800.2

0 100 200 300 400 500 600 700 800 900

Total National Lottery Sales (€ Million)

1987

1988

1989

1990

2017

1990

1991

1992

1993

1994

1995

1996

1997

1998

1999

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

2011

2012

2013

2014

2015

2016

Source: Indecon analysis of data provided by PLI/National Lottery

Indecon International Economic ConsultantsIndependent Socio-Economic Impact Assessment of the National Lottery

92 Development of National Lottery in Ireland

2.2 Innovation and Product Development

The chart below shows how the product offering of the National Lottery has developed since its establishment in 1987 (Figure 2.2). The first products offered were scratch cards, followed by the Lotto in 1988. The next game launched in 1997 was Lotto 5-4-3-2-1, with Telly Bingo and Lotto Plus introduced over the following years. Phone Play (which was part of Winning Streak) started in 2003 but was discontinued in 2007. EuroMillions was introduced in 2004, followed by EuroMillions Plus in 2007. New games offered in 2008 and 2009 were: Monday Million, the Millionaire Raffle, All or Nothing. Online play was also introduced in 2009. Monday Million (as well as Monday Million Plus) and All or Nothing were discontinued after 2012. Daily Millions and Daily Millions Plus commenced in 2012 and remain part of the National Lottery’s offering. The development of these games over the last two decades highlights the product innovation implemented by the National Lottery.

Figure 2.2: Timeline of National Lottery Products

1987

1988

1989

199

019

9119

9219

9319

9419

9519

9619

9719

9819

9920

00

2001

2002

2003

200

420

0520

06

2007

2008

2009

2010

2011

2012

2013

2014

2015

2016

2017

Daily Millions Plus

Daily Millions

Monday Million Plus

Digital Channel

All or Nothing

Millionaire Raffle

Monday Million

EuroMillions Plus

EuroMillions

Phone Play

Lotto Plus

Telly Bingo

Lotto 5-4-3-2-1

Lotto

Scratch Cards (Instant Win)

Source: Indecon analysis of data provided by PLI/National Lottery

2 Development of National Lottery in Ireland10

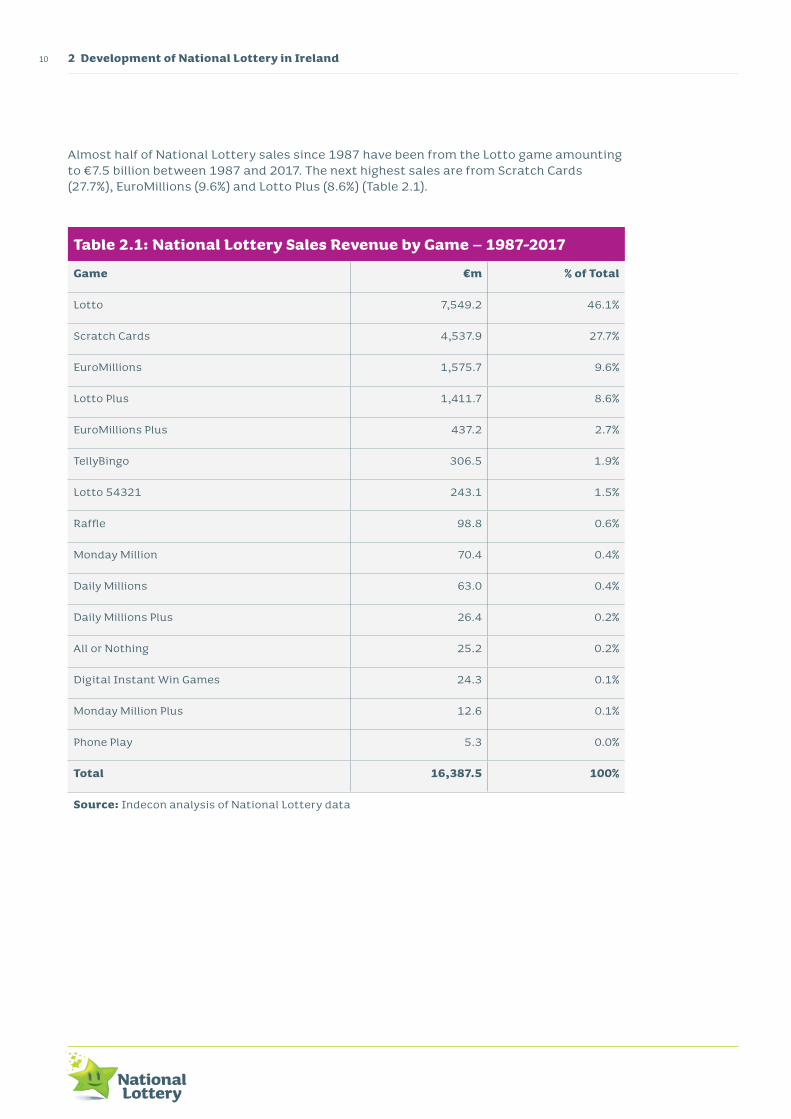

Almost half of National Lottery sales since 1987 have been from the Lotto game amounting to €7.5 billion between 1987 and 2017. The next highest sales are from Scratch Cards (27.7%), EuroMillions (9.6%) and Lotto Plus (8.6%) (Table 2.1).

Table 2.1: National Lottery Sales Revenue by Game – 1987-2017

Game €m % of Total

Lotto 7,549.2 46.1%

Scratch Cards 4,537.9 27.7%

EuroMillions 1,575.7 9.6%

Lotto Plus 1,411.7 8.6%

EuroMillions Plus 437.2 2.7%

TellyBingo 306.5 1.9%

Lotto 54321 243.1 1.5%

Raffle 98.8 0.6%

Monday Million 70.4 0.4%

Daily Millions 63.0 0.4%

Daily Millions Plus 26.4 0.2%

All or Nothing 25.2 0.2%

Digital Instant Win Games 24.3 0.1%

Monday Million Plus 12.6 0.1%

Phone Play 5.3 0.0%

Total 16,387.5 100%

Source: Indecon analysis of National Lottery data

Indecon International Economic ConsultantsIndependent Socio-Economic Impact Assessment of the National Lottery

112 Development of National Lottery in Ireland

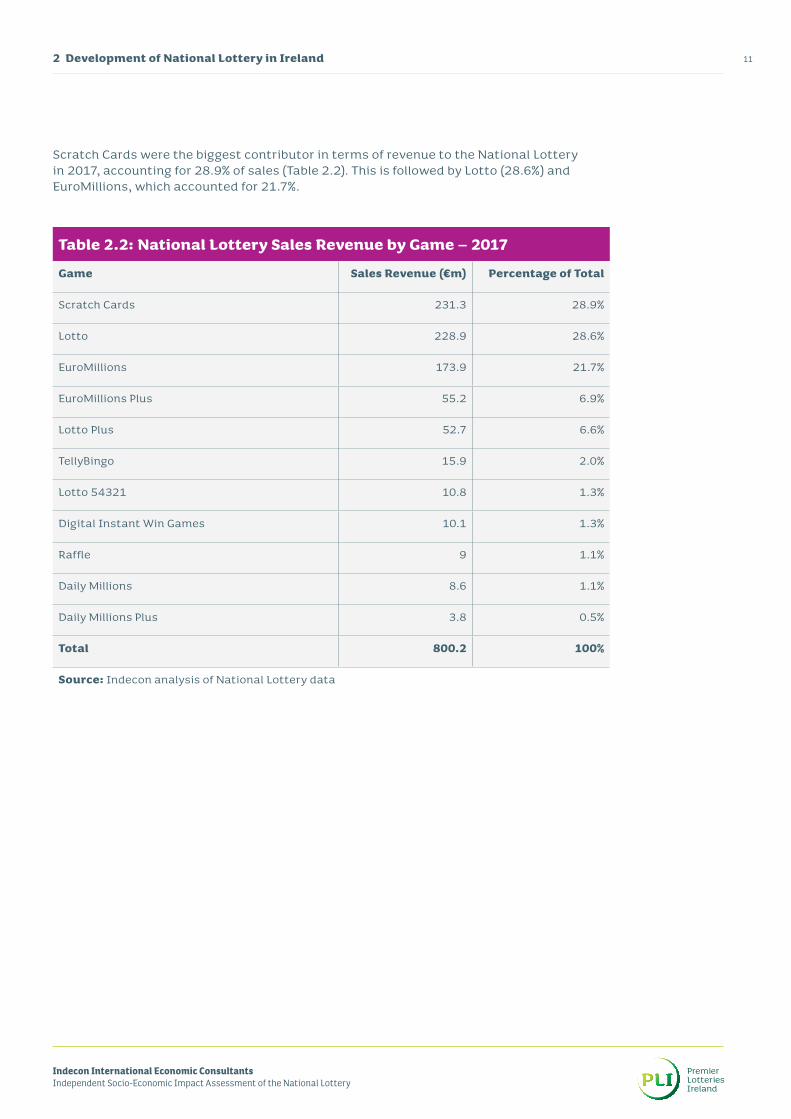

Scratch Cards were the biggest contributor in terms of revenue to the National Lottery in 2017, accounting for 28.9% of sales (Table 2.2). This is followed by Lotto (28.6%) and EuroMillions, which accounted for 21.7%.

Table 2.2: National Lottery Sales Revenue by Game – 2017

Game Sales Revenue (€m) Percentage of Total

Scratch Cards 231.3 28.9%

Lotto 228.9 28.6%

EuroMillions 173.9 21.7%

EuroMillions Plus 55.2 6.9%

Lotto Plus 52.7 6.6%

TellyBingo 15.9 2.0%

Lotto 54321 10.8 1.3%

Digital Instant Win Games 10.1 1.3%

Raffle 9 1.1%

Daily Millions 8.6 1.1%

Daily Millions Plus 3.8 0.5%

Total 800.2 100%

Source: Indecon analysis of National Lottery data

2 Development of National Lottery in Ireland12

The main games in the National Lottery's portfolio, as of 2017 are as follow:

Table 2.3: Main National Lottery Games – 2017

Games

Scratch Cards

Lotto

Lotto Plus

Lotto 5-4-3-2-1

Telly Bingo

EuroMillions

EuroMillions Plus

Millionaire Raffle

Digital Instant Win Games

Daily Millions

Daily Millions Plus

Source: Indecon analysis of data provided by PLI/National Lottery

Indecon International Economic ConsultantsIndependent Socio-Economic Impact Assessment of the National Lottery

132 Development of National Lottery in Ireland

The significance of product innovation can be seen by comparing the percentage of sales by game in 2017 compared to 1990. Scratch Cards and Lotto accounted for under 30% of sales in 2017.

Figure 2.3: % of Sales by Game – 1990 vs. 2017

Lotto65%

EuroMillions22%

2.3

EuroMillions Plus7%

Raffle 1%

Source: Indecon analysis of data provided by PLI/National Lottery

Daily Million Plus0%

Daily Million 1%

Digital IWG1%

Lotto29%

Lotto Plus7%

Lotto 543211%

TellyBingo2%

Scratch Cards35%

Instant WinScratch Cards29%

1990 2017

Source: Indecon analysis of data provided by PLI/National Lottery

2 Development of National Lottery in Ireland14

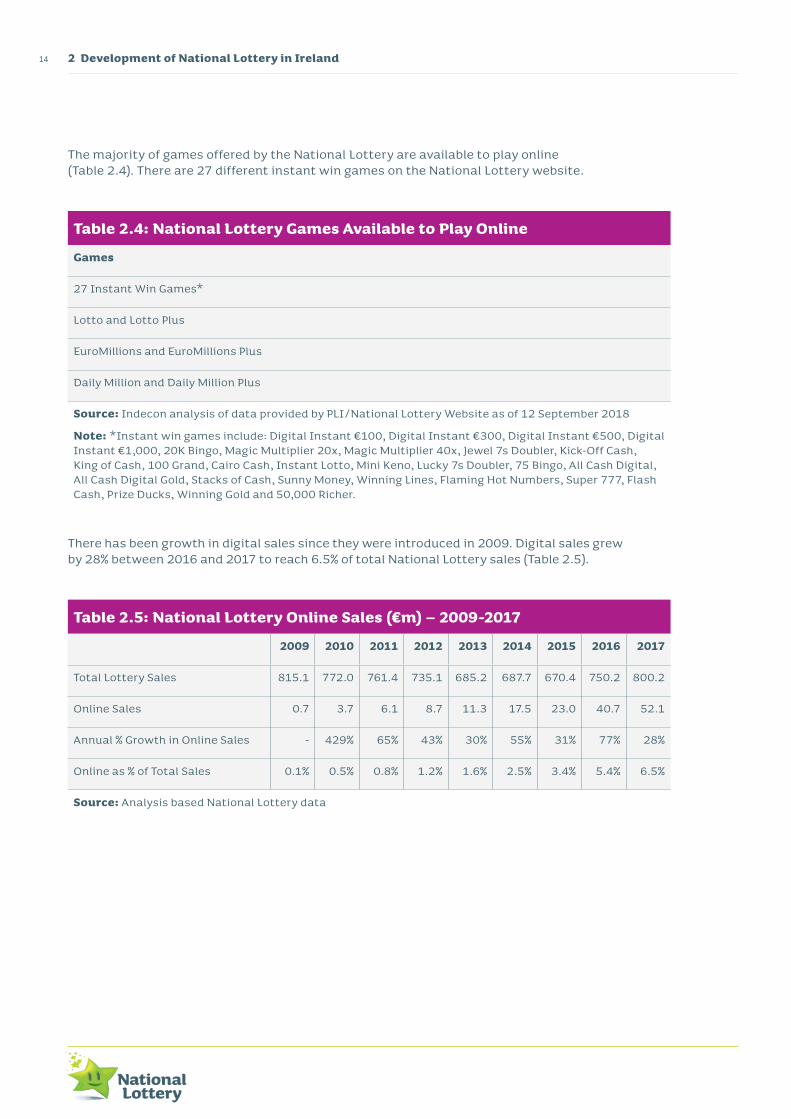

The majority of games offered by the National Lottery are available to play online (Table 2.4). There are 27 different instant win games on the National Lottery website.

Table 2.4: National Lottery Games Available to Play Online

Games

27 Instant Win Games*

Lotto and Lotto Plus

EuroMillions and EuroMillions Plus

Daily Million and Daily Million Plus

Source: Indecon analysis of data provided by PLI/National Lottery Website as of 12 September 2018

Note: *Instant win games include: Digital Instant €100, Digital Instant €300, Digital Instant €500, Digital Instant €1,000, 20K Bingo, Magic Multiplier 20x, Magic Multiplier 40x, Jewel 7s Doubler, Kick-Off Cash, King of Cash, 100 Grand, Cairo Cash, Instant Lotto, Mini Keno, Lucky 7s Doubler, 75 Bingo, All Cash Digital, All Cash Digital Gold, Stacks of Cash, Sunny Money, Winning Lines, Flaming Hot Numbers, Super 777, Flash Cash, Prize Ducks, Winning Gold and 50,000 Richer.

There has been growth in digital sales since they were introduced in 2009. Digital sales grew by 28% between 2016 and 2017 to reach 6.5% of total National Lottery sales (Table 2.5).

Table 2.5: National Lottery Online Sales (€m) – 2009-2017

Online as % of Total Sales 0.1% 0.5% 0.8% 1.2% 1.6% 2.5% 3.4% 5.4% 6.5%

Source: Analysis based National Lottery data

Indecon International Economic ConsultantsIndependent Socio-Economic Impact Assessment of the National Lottery

152 Development of National Lottery in Ireland

The growth in online sales reached €52.1 million in 2017, compared to €0.7 million in 2009 (Figure 2.4). Most of the sales were from draw-based games such as Lotto or EuroMillions.

Figure 2.4: National Lottery Digital Sales (€m) – 2009-2017

0 10 20 30 40 50 60

0.72009

3.72010

6.12011

8.72012

11.32013

17.52014

23.02015

40.72016

52.12017

Internet Sales (€ Million)

Source: Analysis based PLI/National Lottery data

2 Development of National Lottery in Ireland16

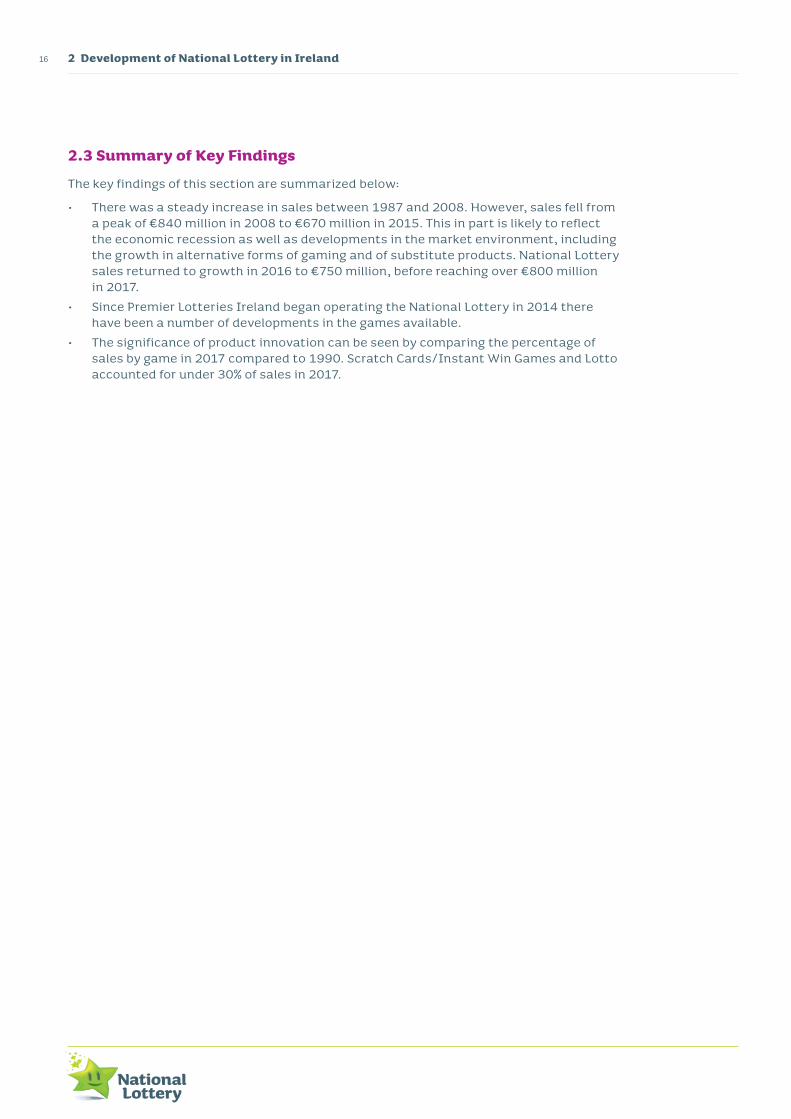

2.3 Summary of Key Findings

The key findings of this section are summarized below:

• There was a steady increase in sales between 1987 and 2008. However, sales fell from a peak of €840 million in 2008 to €670 million in 2015. This in part is likely to reflect the economic recession as well as developments in the market environment, including the growth in alternative forms of gaming and of substitute products. National Lottery sales returned to growth in 2016 to €750 million, before reaching over €800 million in 2017.

• Since Premier Lotteries Ireland began operating the National Lottery in 2014 there have been a number of developments in the games available.

• The significance of product innovation can be seen by comparing the percentage of sales by game in 2017 compared to 1990. Scratch Cards/Instant Win Games and Lotto accounted for under 30% of sales in 2017.

3 Assessment of Micro-Economic and Social Impacts

Indecon International Economic ConsultantsIndependent Socio-Economic Impact Assessment of the National Lottery

3 Assessment of Micro-Economic and Social Impacts18

3 Assessment of Micro-Economic and Social Impacts

3.1 Introduction

This section examines three key areas:

• Funds for Good Causes beneficiaries;• Funds returned to the community via prize winnings; • The impact on National Lottery retail agents.

3.2 Funds for Good Causes beneficiaries

The National Lottery Fund (NLF) was set up under the National Lottery Act, with a portion of the revenue from the sales of National Lottery products being paid into the NLF. This fund supports activities in the following:1

• Sport and recreation;• National culture and heritage (including the Irish language);• The Arts (within the meaning of the Arts Act 2003);• Health of the community;• Youth, welfare and amenities;• Natural environment; and,• Such other objectives (if any) as the Government may determine from time to time.

The amount given in funding to beneficiaries is outlined in Table 3.1. Beneficiary funding in 2017 amounted to over €226 million.

1 National Lottery Act 2013, Op. Cit.

193 Assessment of Micro-Economic and Social Impacts

Indecon International Economic ConsultantsIndependent Socio-Economic Impact Assessment of the National Lottery

Table 3.1: Total National Lottery Funding for Good Causes – 2006-2017

Year € Million

2006 218.0

2007 245.5

2008 267.8

2009 263.5

2010 243.7

2011 231.9

2012 225.3

2013 205.9

2014 194.6

2015 188.0

2016 213.0

2017 226.3

Source: Analysis based on National Lottery data

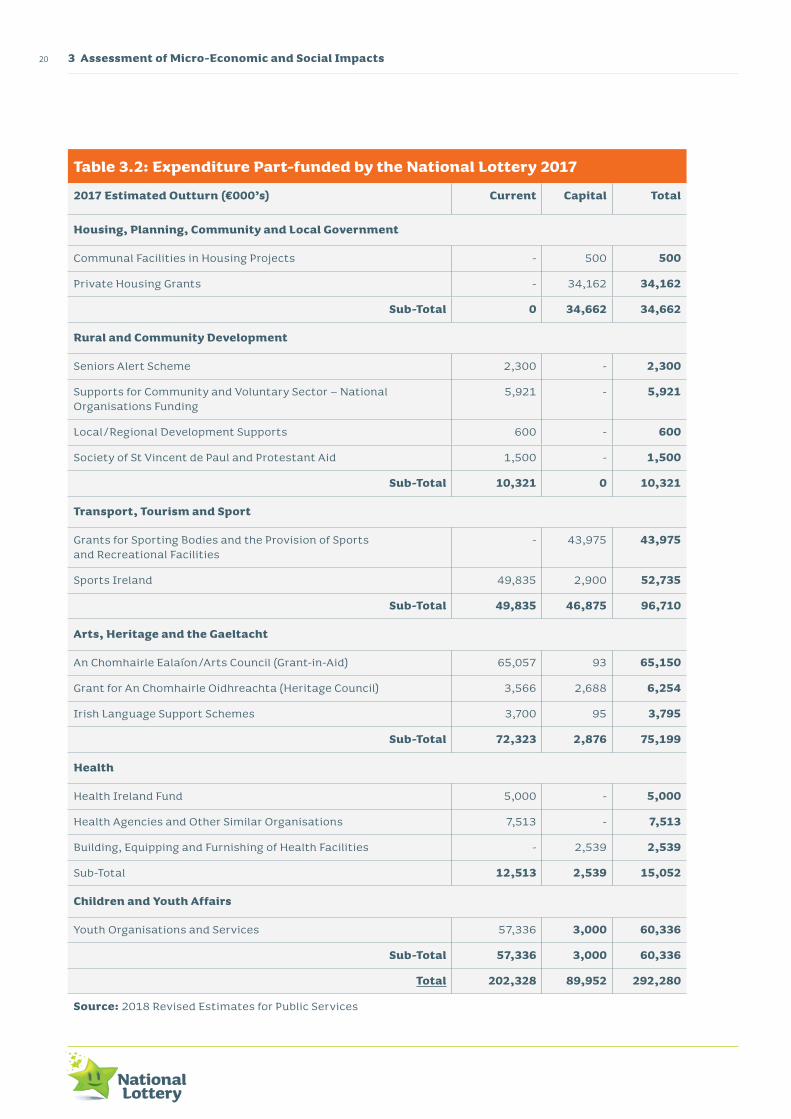

Table 3.2 shows the estimated expenditure supported by National Lottery Good Causes funds.

3 Assessment of Micro-Economic and Social Impacts20

Table 3.2: Expenditure Part-funded by the National Lottery 2017

2017 Estimated Outturn (€000’s) Current Capital Total

Housing, Planning, Community and Local Government

Communal Facilities in Housing Projects - 500 500

Private Housing Grants - 34,162 34,162

Sub-Total 0 34,662 34,662

Rural and Community Development

Seniors Alert Scheme 2,300 - 2,300

Supports for Community and Voluntary Sector – National Organisations Funding

5,921 - 5,921

Local/Regional Development Supports 600 - 600

Society of St Vincent de Paul and Protestant Aid 1,500 - 1,500

Sub-Total 10,321 0 10,321

Transport, Tourism and Sport

Grants for Sporting Bodies and the Provision of Sports and Recreational Facilities

- 43,975 43,975

Sports Ireland 49,835 2,900 52,735

Sub-Total 49,835 46,875 96,710

Arts, Heritage and the Gaeltacht

An Chomhairle Ealaíon/Arts Council (Grant-in-Aid) 65,057 93 65,150

Grant for An Chomhairle Oidhreachta (Heritage Council) 3,566 2,688 6,254

Irish Language Support Schemes 3,700 95 3,795

Sub-Total 72,323 2,876 75,199

Health

Health Ireland Fund 5,000 - 5,000

Health Agencies and Other Similar Organisations 7,513 - 7,513

Building, Equipping and Furnishing of Health Facilities - 2,539 2,539

Sub-Total 12,513 2,539 15,052

Children and Youth Affairs

Youth Organisations and Services 57,336 3,000 60,336

Sub-Total 57,336 3,000 60,336

Total 202,328 89,952 292,280

Source: 2018 Revised Estimates for Public Services

213 Assessment of Micro-Economic and Social Impacts

Indecon International Economic ConsultantsIndependent Socio-Economic Impact Assessment of the National Lottery

Funding for Transport, Tourism and Sport was one of the most important expenditure areas, part funded by the National Lottery by 33%. This is followed by Arts, Heritage and the Gaeltacht (26%), and Children and Youth Affairs (Figure 3.1).

Figure 3.1: Breakdown of Total Public Expenditure on Activities which are Part-funded by the National Lottery – 2017 – %

Housing, Planning,Community and LocalGovernment 12%

Rural and CommunityDevelopment 3%Health 5%

Children and Youth Affairs 21%

Arts, Heritage and the Gaeltacht 26%

Transport, Tourismand Sport 33%

Source: Indecon analysis of 2018 Revised Estimates for Public Service Expenditure

3.3 Impact of Good Causes funding

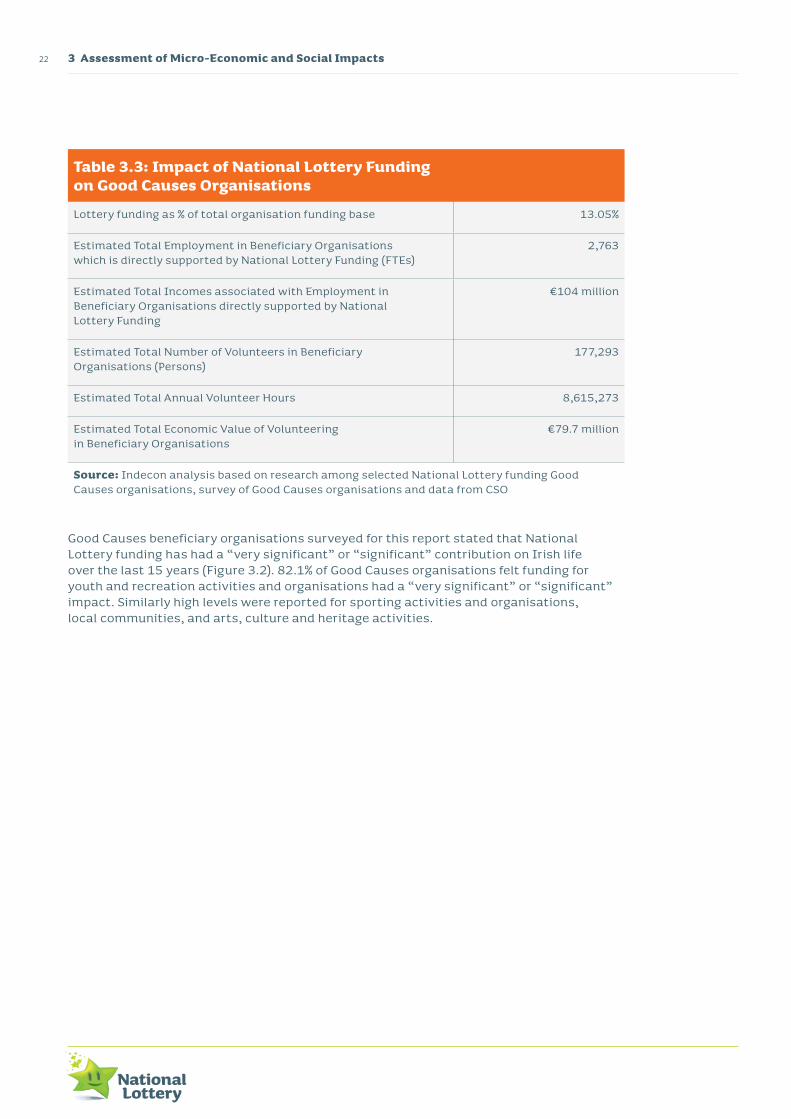

An important impact of National Lottery Good Causes funding is the employment it supports directly in beneficiary organisations. Estimates suggest that 2,763 full-time equivalent jobs (FTEs) were supported directly through National Lottery funding in 2017. (These organisations are estimated to have 15,285 full-time equivalent employees in total). Estimates based on this report’s modelling indicate that approximately €104 million in employment incomes are supported directly through the contribution made by National Lottery funding to these organisations. In addition, there are over 177,000 volunteers working in Good Causes organisations. The value to the economy of this volunteering is estimated at over €79.7 million per annum (Table 3.3).

3 Assessment of Micro-Economic and Social Impacts22

Table 3.3: Impact of National Lottery Funding on Good Causes Organisations

Lottery funding as % of total organisation funding base 13.05%

Estimated Total Employment in Beneficiary Organisations which is directly supported by National Lottery Funding (FTEs)

2,763

Estimated Total Incomes associated with Employment in Beneficiary Organisations directly supported by National Lottery Funding

€104 million

Estimated Total Number of Volunteers in Beneficiary Organisations (Persons)

177,293

Estimated Total Annual Volunteer Hours 8,615,273

Estimated Total Economic Value of Volunteering in Beneficiary Organisations

€79.7 million

Source: Indecon analysis based on research among selected National Lottery funding Good Causes organisations, survey of Good Causes organisations and data from CSO

Good Causes beneficiary organisations surveyed for this report stated that National Lottery funding has had a “very significant” or “significant” contribution on Irish life over the last 15 years (Figure 3.2). 82.1% of Good Causes organisations felt funding for youth and recreation activities and organisations had a “very significant” or “significant” impact. Similarly high levels were reported for sporting activities and organisations, local communities, and arts, culture and heritage activities.

233 Assessment of Micro-Economic and Social Impacts

Indecon International Economic ConsultantsIndependent Socio-Economic Impact Assessment of the National Lottery

Figure 3.2: National Lottery Good Causes Beneficiaries – Perceived Socio-economic Impact of the National Lottery in Ireland over the Past 15 Years

0 10 20 30 40 50 60 70 80 90 100

Provision of funding for Youth and Recreation Activities and Organisations

Provision of funding for Sporting Activities and Organisations

Support for Arts, Culture and Heritage Organisations and Activities

Support for Local Communities

Provision for funding for Community Health and Welfare facilities in Ireland

Provision for funding for Charitable Organisations

Support for Irish Language Activities and Organisations

Contribution to Exchequer Taxation

Provision of funding for Social Enterprises

82.1%

78.0%

76.3%

75.0%

68.9%

55.0%

48.6%

44.4%

42.1%

Source: Indecon Confidential Survey of National Lottery Funding Beneficiaries

3 Assessment of Micro-Economic and Social Impacts24

A surveys of retail agents found:

• 92.1% believed National Lottery funding had a “very” or “important” impact on support for sporting activities and organisations.

• Support for children/youth organisations was also viewed as important.• 86.9% suggested National Lottery funding had a very important or important

impact on local communities.

Table 3.4: National Lottery Retail Agents – Importance of Socio-Economic Impact of the National Lottery in Ireland Over the Past 15 Years

Very Important

Important Neither Important

Nor Unimportant

Unimportant Very Unimportant

Support for Health and Welfare facilities in Ireland

33.5% 43.5% 17.4% 4.3% 1.3%

Support for Sporting Activities and Organisations

47.8% 44.3% 5.2% 1.3% 1.3%

Support for Children/Youth and Recreation Activities and Organisations

39.3% 49.8% 8.3% 1.3% 1.3%

Support for Arts, Culture and Heritage Organisations and Activities

27.3% 48.9% 19.0% 2.6% 2.2%

Support for Irish Language Activities and Organisations

19.9% 35.1% 31.2% 10.4% 3.5%

Support for Charitable organisations

34.6% 44.7% 15.4% 3.9% 1.3%

Support for Local Communities

43.0% 43.9% 7.8% 3.5% 1.7%

Support for Social Enterprises

23.2% 42.5% 25.0% 6.1% 3.1%

Contribution to Exchequer Taxation

22.4% 29.8% 33.3% 7.0% 7.5%

Source: Confidential Survey of National Lottery Retailers

253 Assessment of Micro-Economic and Social Impacts

Indecon International Economic ConsultantsIndependent Socio-Economic Impact Assessment of the National Lottery

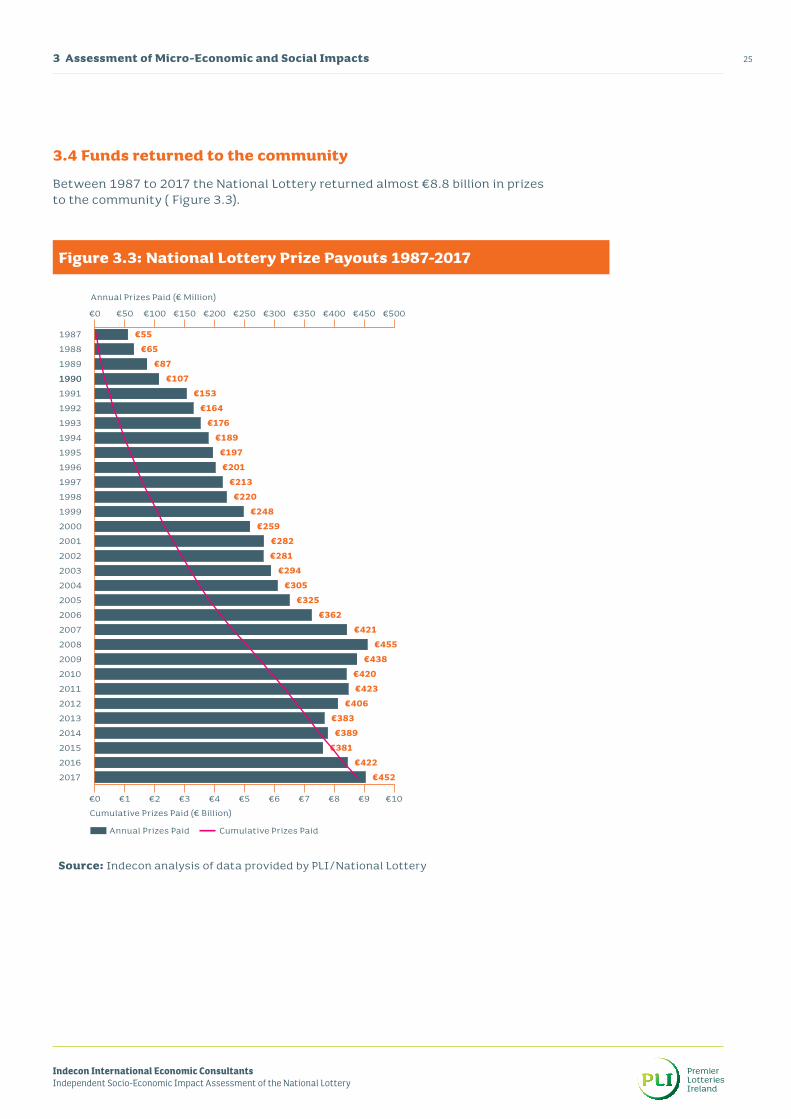

3.4 Funds returned to the community

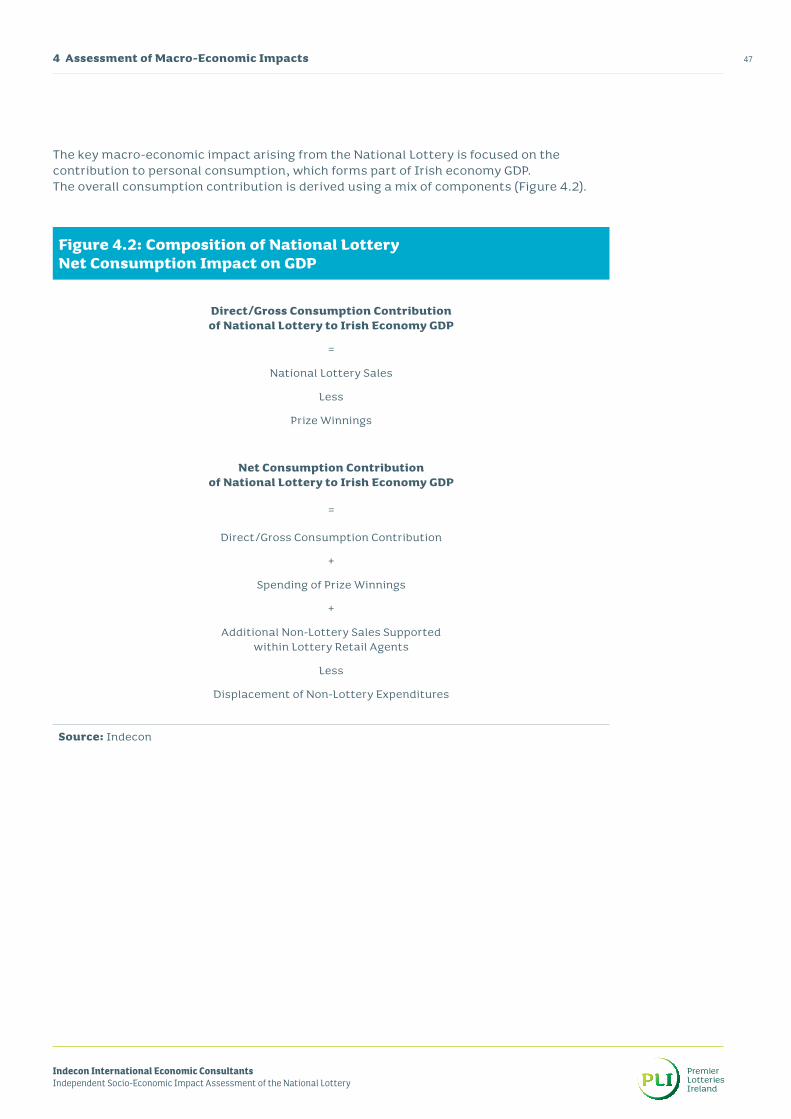

Between 1987 to 2017 the National Lottery returned almost €8.8 billion in prizes to the community ( Figure 3.3).

Figure 3.3: National Lottery Prize Payouts 1987-2017

Source: Indecon analysis of data provided by PLI/National Lottery

3 Assessment of Micro-Economic and Social Impacts26

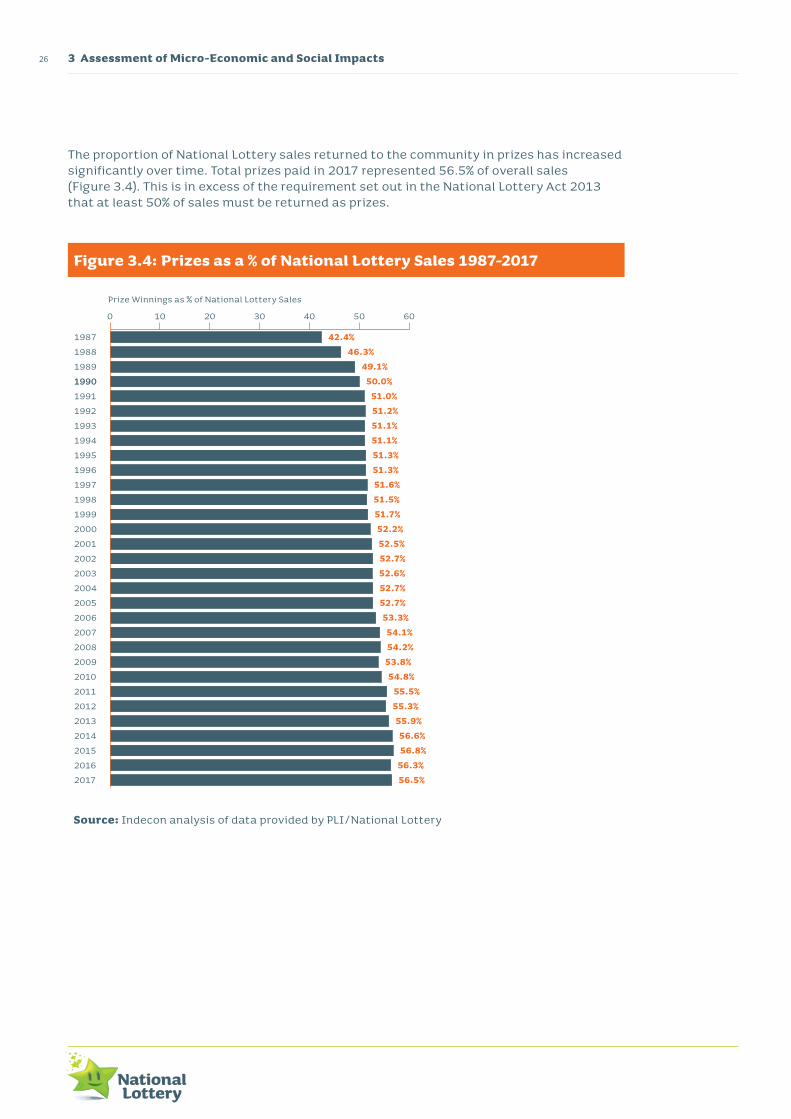

The proportion of National Lottery sales returned to the community in prizes has increased significantly over time. Total prizes paid in 2017 represented 56.5% of overall sales (Figure 3.4). This is in excess of the requirement set out in the National Lottery Act 2013 that at least 50% of sales must be returned as prizes.

Figure 3.4: Prizes as a % of National Lottery Sales 1987-2017

Source: Indecon analysis of data provided by PLI/National Lottery

273 Assessment of Micro-Economic and Social Impacts

Indecon International Economic ConsultantsIndependent Socio-Economic Impact Assessment of the National Lottery

The amount paid in prizes in 2017 was €452 million, its highest level since 2008 (Table 3.5).

Table 3.5: Total National Lottery Prizes (€m) 2007-2017

Year Prize Winnings (€ Million) Prizes as a % Total Sales

2007 420.9 54.1

2008 455.0 54.2

2009 438.3 53.8

2010 419.9 54.4

2011 422.5 55.5

2012 406.4 55.3

2013 382.7 55.9

2014 389.4 56.4

2015 381.1 56.8

2016 422.0 56.3

2017 452.0 56.5

Total 2007-2017 4,590.3 55.3

Source: Indecon analysis of National Lottery data

3 Assessment of Micro-Economic and Social Impacts28

In 2017 the three games that paid out most in prizes were Scratch Cards (34.3%), Lotto (26.3%) and EuroMillions (19.2%). Scratch Cards paid out most in prizes in 2014, compared to the previous three years when Lotto paid the most in prizes (Table 3.6).

Table 3.6: Breakdown of National Lottery Prizes by Game (%) 2011-2017

EuroMillions Plus 5.5% 6.0% 5.8% 6.3% 6.1% 6.2% 6.6%

Lotto Plus 9.4% 8.7% 8.5% 8.0% 7.4% 6.0% 5.5%

TellyBingo 3.1% 3.2% 3.5% 3.5% 3.1% 2.8% 2.6%

Instant Win Games 0.1% 0.2% 0.2% 0.4% 0.1% 1.2% 1.5%

Lotto 54321 2.2% 2.1% 2.3% 2.1% 2.0% 1.6% 1.5%

Daily Million 0.0% 1.0% 2.2% 2.3% 1.4% 1.3% 1.0%

Raffle 1.1% 1.6% 1.3% 0.5% 0.8% 0.8% 1.0%

Daily Million Plus 0.0% 0.4% 1.0% 0.0% 0.6% 0.6% 0.5%

Monday Million 1.8% 1.1% 0.0% 0.0% 0.0% 0.0% 0.0%

All or Nothing 1.1% 0.6% 0.0% 0.0% 0.0% 0.0% 0.0%

Monday Million Plus 0.8% 0.5% 0.0% 0.0% 0.0% 0.0% 0.0%

Source: Indecon analysis of National Lottery data

293 Assessment of Micro-Economic and Social Impacts

Indecon International Economic ConsultantsIndependent Socio-Economic Impact Assessment of the National Lottery

In 2017 over 79% of prizes were paid in Scratch Cards, Lotto and EuroMillions (Figure 3.5). EuroMillions Plus accounted for 6.6%.

Figure 3.5: Breakdown of National Lottery Prizes by Game 2017

EuroMillions Plus6.6%

Lotto Plus5.5%

TellyBingo2.6%

IWGs1.5%

Lotto 543211.5%

Daily Million Plus0.5%

Daily Million 1.0%

Raffle1.0%

EuroMillions19.2%

Lotto26.3%

Scratch Cards34.3%

Source: Indecon analysis of data provided by PLI/National Lottery

3 Assessment of Micro-Economic and Social Impacts30

There were 12-15 Lotto prize winners of over €1 million 2015, 2016 and 2017. The average size of these prizes was around €6m in 2017.

Table 3.7: Lotto Prizes over €1m (2015-2017)

Year Winners Amount Won

(€ Million)

% of Total Amount

Won

Average win size

(€ Million)

Jackpots Hit

Average Jackpot Size

When Hit (€ Million)

2015 15 70.0 63.3% 4.7 13 5.4

2016 13 80.2 62.8% 6.2 11 7.3

2017 12 71.8 61.4% 6.0 11 6.5

Total 40 222.0 62.5% 5.6 35 6.3

Source: Indecon analysis of National Lottery data

There were four winners of over €1 million in 2017 for the EuroMillions and the average size win was almost €40 million (Table 3.8).

Table 3.8: EuroMillions Prizes over €1m (2016-2017)

Year Winners Amount Won (€ Million)

% of Total Amount Won in that Year

Average win size (€ Million)

2016 3 91.1 70.4% 30.4

2017 4 157.5 80.0% 39.4

Source: Indecon analysis of National Lottery data

313 Assessment of Micro-Economic and Social Impacts

Indecon International Economic ConsultantsIndependent Socio-Economic Impact Assessment of the National Lottery

The majority of winners won prizes of less than €1,000 (Table 3.9). There was one prize worth between €500,000 and €999,999, whilst there were 18 winners of prizes of €1 million or above. The majority were won on Lotto, with the others winning on EuroMillions, Daily Million and the Millionaire Raffle.

Table 3.9: Breakdown of Non-Digital National Lottery Prizes 2017 (Number of Winners)

Up to €1,000

€1,001-€10,000

€10,001-€50,000

€50,001-€100,000

€100,001-€500,000

€500,001-€999,999

€1m and over

Total

EuroMillions 5,405,029 117 14 2 9 0 4 5,405,175

Lotto 3,979,158 2,114 23 20 19 1 12 3,981,347

Lotto Plus 2,531,707 119 0 0 23 0 0 2,531,849

TV Bingo 1,310,704 205 14 9 0 0 0 1,310,932

EuroMillions Plus

261,299 5,999 0 0 31 0 0 267,329

Daily Million 74,837 3 0 0 0 0 1 74,841

Daily Million Plus

65,732 9 0 0 1 0 0 65,742

L54321 58,437 65 0 0 0 0 0 58,502

L54321 Plus 1

29,893 39 0 0 0 0 0 29,932

L54321 Plus 2

27,622 32 0 0 0 0 0 27,654

Millionaire Raffle

5,015 35 0 4 1 0 1 5,056

EuroMillions Ireland Only Raffle

0 1,040 0 0 0 0 0 1,040

Total 13,749,433 9,777 51 35 84 1 18 13,759,399

Source: Indecon analysis of National Lottery data

3 Assessment of Micro-Economic and Social Impacts32

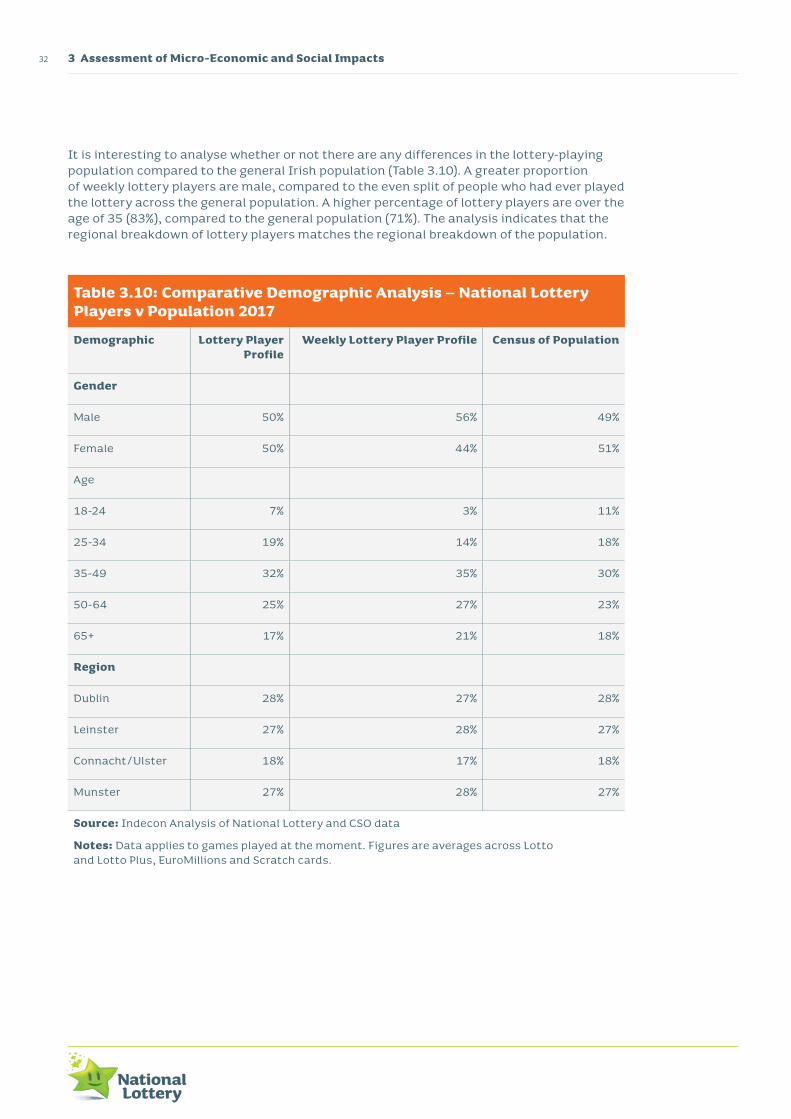

It is interesting to analyse whether or not there are any differences in the lottery-playing population compared to the general Irish population (Table 3.10). A greater proportion of weekly lottery players are male, compared to the even split of people who had ever played the lottery across the general population. A higher percentage of lottery players are over the age of 35 (83%), compared to the general population (71%). The analysis indicates that the regional breakdown of lottery players matches the regional breakdown of the population.

Table 3.10: Comparative Demographic Analysis – National Lottery Players v Population 2017

Demographic Lottery Player Profile

Weekly Lottery Player Profile Census of Population

Gender

Male 50% 56% 49%

Female 50% 44% 51%

Age

18-24 7% 3% 11%

25-34 19% 14% 18%

35-49 32% 35% 30%

50-64 25% 27% 23%

65+ 17% 21% 18%

Region

Dublin 28% 27% 28%

Leinster 27% 28% 27%

Connacht/Ulster 18% 17% 18%

Munster 27% 28% 27%

Source: Indecon Analysis of National Lottery and CSO data

Notes: Data applies to games played at the moment. Figures are averages across Lotto and Lotto Plus, EuroMillions and Scratch cards.

333 Assessment of Micro-Economic and Social Impacts

Indecon International Economic ConsultantsIndependent Socio-Economic Impact Assessment of the National Lottery

The survey into spend on different Lottery games shows that older men spend more on Lotto and EuroMillions (Table 3.11). When it comes to online Instant Win Games young men have the highest percentage of spend (27%). Spending on Scratch Cards is more evenly split.

Table 3.11: Share of Spend on National Lottery Products

Lotto EuroMillions Scratch Cards Online Instant Win Games

Young Men 8% 11% 19% 27%

Young Women 7% 9% 17% 20%

Middle Men 19% 21% 15% 21%

Middle Women 13% 14% 15% 15%

Older Men 30% 28% 16% 7%

Older Women 23% 17% 19% 11%

Total 100% 100% 100% 100%

Source: Indecon analysis of data provided by PLI/National Lottery data

The social class breakdown of National Lottery players is similar to that of the overall population (Table 3.12). While there are some variations it is, however, clear that all socio-economic groups actively play the lottery.

Table 3.12: National Lottery Participation by Social Class

Social Class Indicator Population Ever Played the Lottery Weekly Lottery Player

AB 13% 13% 12%

C1 28% 27% 27%

C2 20% 21% 23%

DE 32% 32% 32%

F 6% 7% 7%

Source: Indecon analysis of data provided by PLI/National Lottery data

Notes: Data applies to games currently offered, AB includes: Upper Middle Class and Middle Class, C1 includes Lower Middle Class, C2 includes: Skilled Working Class, DE includes: Working Class and Casual or Lower Grade Workers, F applies to Agricultural workers

3 Assessment of Micro-Economic and Social Impacts34

3.5 Impact of National Lottery on retail agents

The sales data for the National Lottery’s core retail network is broken down by draw based games and Scratch Cards on a per agent basis (Figure 3.6). Average draw based game sales per agent have remained constant despite the increase in core agencies from 2014 to 2017. When analysed organically, sales have increased slightly over the period. Scratch Card sales have seen a steady increase on a per agent weekly average basis over the same period. Larger fluctuations are due to larger jackpots in some weeks. This is also the case for ‘select’ agents, following their introduction in 2016.

Figure 3.6: Weekly Retail Sales (DBC & SC) and Number of Authorised Agents 2014-2017

€0 €5m €10m €15m €20m €25m

#Retail ex Select Agents (LHS) Retail ex Select Sales (RHS)# Linear (Retail ex Select Agents (RHS) )

Source: Indecon analysis of data provided by PLI/National Lottery Data

353 Assessment of Micro-Economic and Social Impacts

Indecon International Economic ConsultantsIndependent Socio-Economic Impact Assessment of the National Lottery

The significant increase in the number of retail agents in 2016/17 is largely due to the introduction of the Select Channel to complement the Lottery’s existing core network (Figure 3.7). Weekly sales figures fluctuated between €10 million to €15 million between 2014 and 2017.

Figure 3.7: National Lottery Sales Per Retail Agent Excl. Select Agents (Draw Based Games v Scratch Cards)

0 1000 2000 3000 4000 5000

0 1000 2000 3000 4000 5000

2017 Wk 52

2017 Wk 45

2017 Wk 38

2017 Wk 31

2017 Wk 24

2017 Wk 17

2017 Wk 10

2017 Wk 3

2016 Wk 49

2016 Wk 42

2016 Wk 35

2016 Wk 28

2016 Wk 21

2016 Wk 14

2016 Wk 7

2015 Wk 53

2015 Wk 46

2015 Wk 39

2015 Wk 32

2015 Wk 25

2015 Wk 18

2015 Wk 11

2015 Wk 4

2014 Wk 50

2014 Wk 43

2014 Wk 36

2014 Wk 29

2014 Wk 22

2014 Wk 15

2014 Wk 8

2014 Wk 1

Sales per Agent (DBG - Retail ex Select) Sales per Agent (SC - Retail ex Select)Linear (Sales per Agent (SC - Retail ex Select))Linear (Sales per Agent (DBG - Retail ex Select))

DBG SCLinear (SC) Linear (DBG)

€0 €2m €4m €6m €8m €10m €12m €14m €16m

€0 €2m €4m €6m €8m €10m €12m €14m €16m

2016_38

2016_32

2016_26

2016_20

2016_14

2017_9

2017_3

2016_50

2017_27

2017_30

2017_33

2017_42

2017_51

2017_48

2017_21

2017_15

2016_44

2016_8

2016_2

2015_49

2015_43

2015_37

2015_31

2015_25

2015_19

2015_13

2015_7

2015_1

Source: Indecon analysis of data provided by PLI/National Lottery Data

3 Assessment of Micro-Economic and Social Impacts36

The National Lottery supports a large network of retail agents, totalling 5,780 in 2017. This has expanded by over 50% since 2006 with the greatest increase in 2016/17 because of Select Channel. This saw the retail estate grow from 4002 at the end of 2015 to 5,780 by 2017. Lottery Select allowed for the sale of a limited range of Lottery products through Payzone & PostPoint agents and all Post Offices nationwide using an integrated point of sale solution.

Table 3.13: Number of National Lottery Retail Agents 2006-2017

Year No. Of Agents (Core Network) No. of Agents (Select Channel) Total Agents

2006 3,489 0 3,489

2007 3,623 0 3,623

2008 3,675 0 3,675

2009 3,794 0 3,794

2010 3,813 0 3,813

2011 3,780 0 3,780

2012 3,744 0 3,744

2013 3,745 0 3,745

2014 3,700 0 3,700

2015 4,002 0 4,002

2016 4,008 1,282 5,290

2017 3,969 1,811 5,780

Source: Indecon analysis of data provided by PLI/National Lottery data

Commission paid to retail agents increased between 2016 and 2017 from €40.6 million to €47 million, reversing a decline between 2014 and 2015 (Table 3.14).

373 Assessment of Micro-Economic and Social Impacts

Indecon International Economic ConsultantsIndependent Socio-Economic Impact Assessment of the National Lottery

Table 3.14: National Lottery Commissions Paid to Retailers 2006-2017

Year Retail Agent Commissions Paid by National Lottery – € Million

2006 42.1

2007 49.0

2008 52.3

2009 50.9

2010 47.9

2011 47.1

2012 45.4

2013 42.1

2014 42.2

2015 40.6

2016 44.5

2017 47.0

Source: Indecon analysis of data provided by PLI/National Lottery data

Using the level of National Lottery sales through retail agents, and responses from our survey of retailers, it is estimated that, on average, National Lottery sales amount to 6.44% of total sales (Table 3.15).

Table 3.15: Estimated Total Sales (Lottery and Non-Lottery) of National Lottery Retail Agents 2017

Metric Details

Total National Lottery Sales through Retail Agents (€m) (A) €748.1 m

% of Total Retail Agent Sales from Lottery Products (B) 6.44%

Total Sales (Lottery and Non-Lottery) of National Lottery Retail Agents (€m) (A/B) €11,610.8 m

Source: Indecon analysis

Notes: Sales through retail agents equates to total sales less online sales. (A) is taken from analysis based on data provided to Indecon by the National Lottery. (B) is derived from Indecon’s Confidential Survey of National Lottery Retail Agents.

3 Assessment of Micro-Economic and Social Impacts38

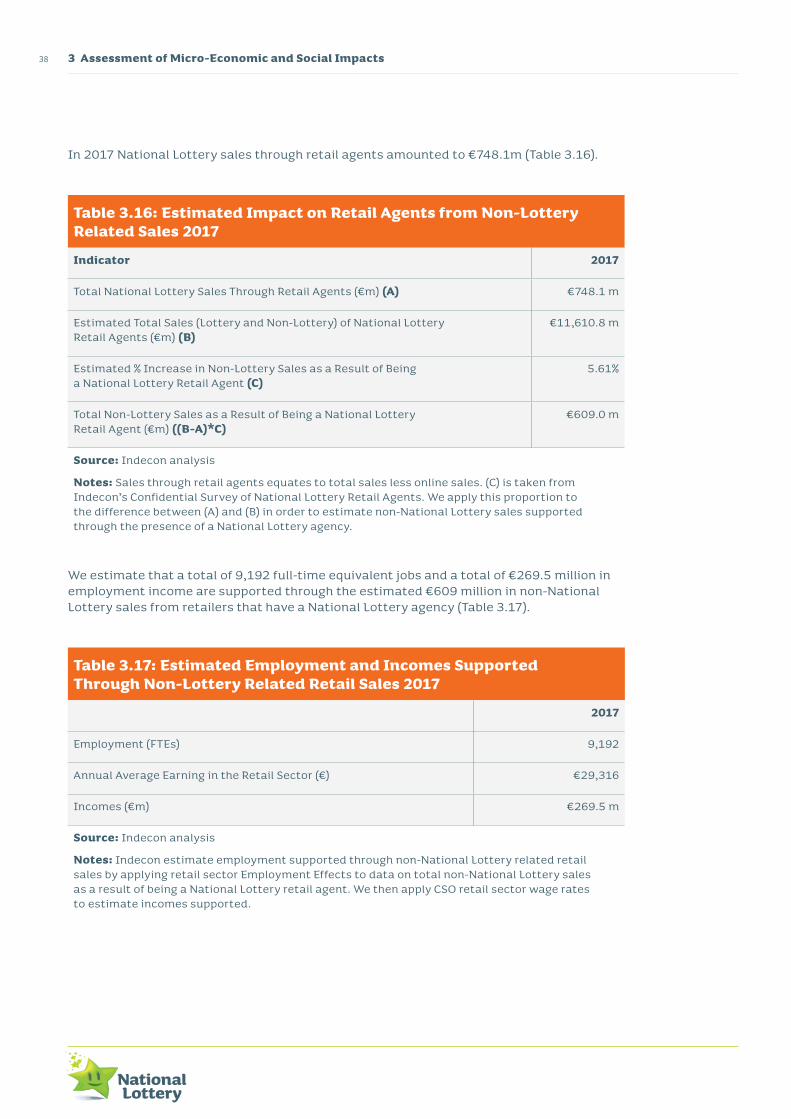

In 2017 National Lottery sales through retail agents amounted to €748.1m (Table 3.16).

Table 3.16: Estimated Impact on Retail Agents from Non-Lottery Related Sales 2017

Indicator 2017

Total National Lottery Sales Through Retail Agents (€m) (A) €748.1 m

Estimated Total Sales (Lottery and Non-Lottery) of National Lottery Retail Agents (€m) (B)

€11,610.8 m

Estimated % Increase in Non-Lottery Sales as a Result of Being a National Lottery Retail Agent (C)

5.61%

Total Non-Lottery Sales as a Result of Being a National Lottery Retail Agent (€m) ((B-A)*C)

€609.0 m

Source: Indecon analysis

Notes: Sales through retail agents equates to total sales less online sales. (C) is taken from Indecon’s Confidential Survey of National Lottery Retail Agents. We apply this proportion to the difference between (A) and (B) in order to estimate non-National Lottery sales supported through the presence of a National Lottery agency.

We estimate that a total of 9,192 full-time equivalent jobs and a total of €269.5 million in employment income are supported through the estimated €609 million in non-National Lottery sales from retailers that have a National Lottery agency (Table 3.17).

Table 3.17: Estimated Employment and Incomes Supported Through Non-Lottery Related Retail Sales 2017

2017

Employment (FTEs) 9,192

Annual Average Earning in the Retail Sector (€) €29,316

Incomes (€m) €269.5 m

Source: Indecon analysis

Notes: Indecon estimate employment supported through non-National Lottery related retail sales by applying retail sector Employment Effects to data on total non-National Lottery sales as a result of being a National Lottery retail agent. We then apply CSO retail sector wage rates to estimate incomes supported.

393 Assessment of Micro-Economic and Social Impacts

Indecon International Economic ConsultantsIndependent Socio-Economic Impact Assessment of the National Lottery

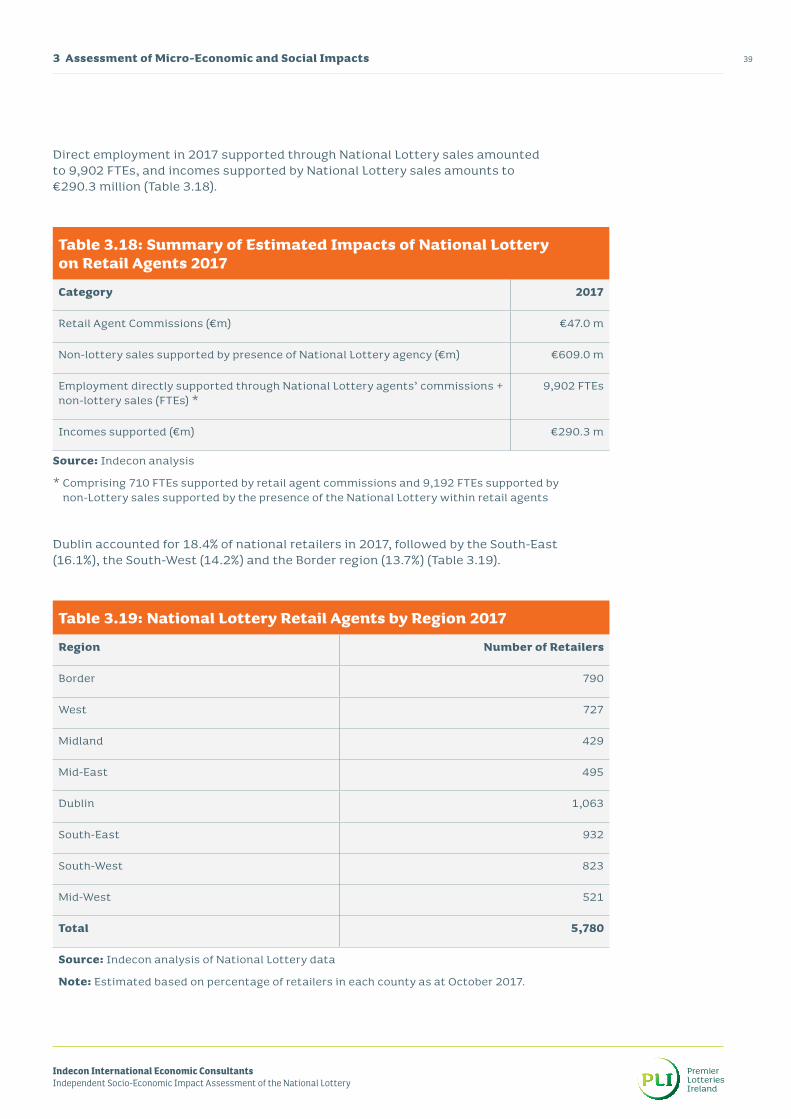

Direct employment in 2017 supported through National Lottery sales amounted to 9,902 FTEs, and incomes supported by National Lottery sales amounts to €290.3 million (Table 3.18).

Table 3.18: Summary of Estimated Impacts of National Lottery on Retail Agents 2017

Category 2017

Retail Agent Commissions (€m) €47.0 m

Non-lottery sales supported by presence of National Lottery agency (€m) €609.0 m

Employment directly supported through National Lottery agents’ commissions + non-lottery sales (FTEs) *

9,902 FTEs

Incomes supported (€m) €290.3 m

Source: Indecon analysis

* Comprising 710 FTEs supported by retail agent commissions and 9,192 FTEs supported by non-Lottery sales supported by the presence of the National Lottery within retail agents

Dublin accounted for 18.4% of national retailers in 2017, followed by the South-East (16.1%), the South-West (14.2%) and the Border region (13.7%) (Table 3.19).

Table 3.19: National Lottery Retail Agents by Region 2017

Region Number of Retailers

Border 790

West 727

Midland 429

Mid-East 495

Dublin 1,063

South-East 932

South-West 823

Mid-West 521

Total 5,780

Source: Indecon analysis of National Lottery data

Note: Estimated based on percentage of retailers in each county as at October 2017.

3 Assessment of Micro-Economic and Social Impacts40

Dublin accounted for a quarter of total National Lottery revenue through retail agents in 2017 (Table 3.20). The South-West region had National Lottery sales of €101.1 million in 2017, making the second highest contribution to the national total.

Table 3.20: National Lottery Revenue at Retail Agents by Region 2017

Region National Lottery Revenue (€ Million)

Border 93.9

West 75.7

Midland 51.6

Mid-East 76.2

Dublin 190.0

South-East 96.9

South-West 101.1

Mid-West 62.7

Total 748.1

Source: Indecon analysis of National Lottery data

Note: Estimated based on percentage of retailers in each county as at October 2017.

413 Assessment of Micro-Economic and Social Impacts

Indecon International Economic ConsultantsIndependent Socio-Economic Impact Assessment of the National Lottery

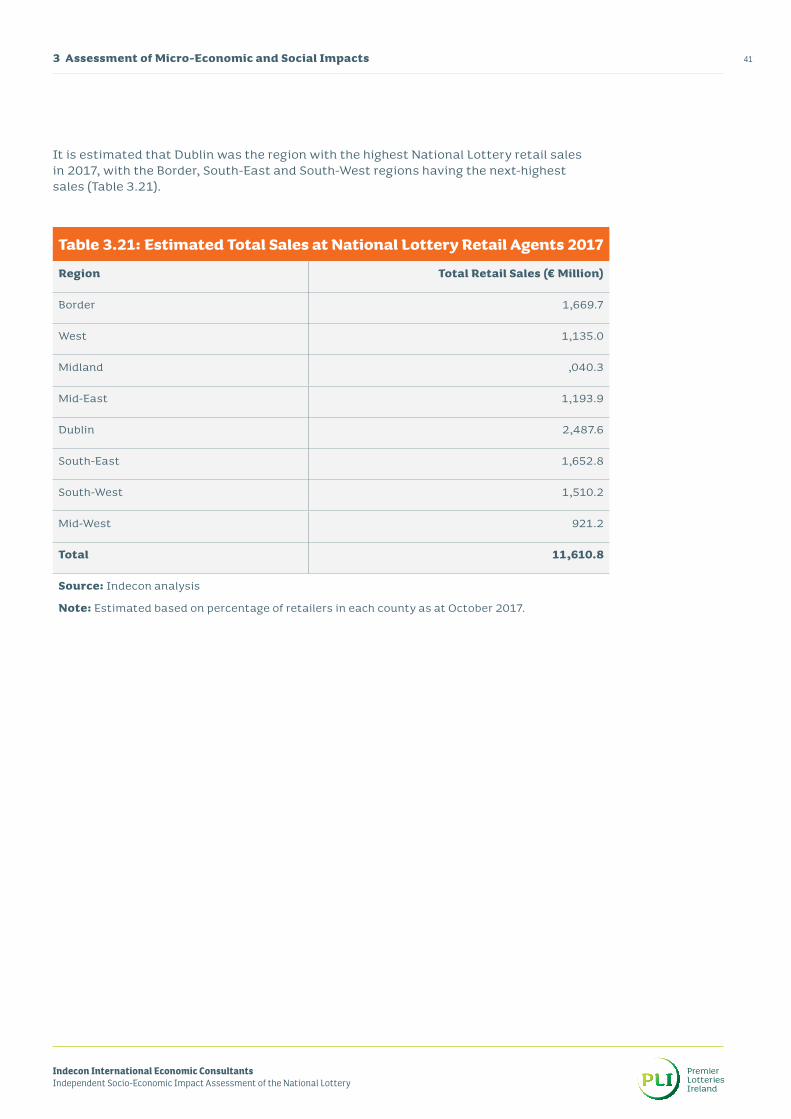

It is estimated that Dublin was the region with the highest National Lottery retail sales in 2017, with the Border, South-East and South-West regions having the next-highest sales (Table 3.21).

Table 3.21: Estimated Total Sales at National Lottery Retail Agents 2017

Region Total Retail Sales (€ Million)

Border 1,669.7

West 1,135.0

Midland ,040.3

Mid-East 1,193.9

Dublin 2,487.6

South-East 1,652.8

South-West 1,510.2

Mid-West 921.2

Total 11,610.8

Source: Indecon analysis

Note: Estimated based on percentage of retailers in each county as at October 2017.

3 Assessment of Micro-Economic and Social Impacts42

An estimated €131 million of non-National Lottery sales in Dublin in 2017 were due to retailers having National Lottery games. The South-East has the next highest figure, €96.7 million, followed by the Mid-East, €79.4 million, and the Border region, €75 million (Table 3.22).

Table 3.22: Perceived Estimate of Impact of Availability of National Lottery Games to Non-Lottery Sales

Region Non-Lottery Sales as a Result of Being a National Lottery Retail Agent (€ Million)

Border 75.0

West 48.1

Midland 55.8

Mid-East 79.4

Dublin 131.4

South-East 96.7

South-West 70.1

Mid-West 52.6

Total 609.0

Source: Indecon analysis

Note: Estimated based on percentage of retailers in each county as at October 2017.

433 Assessment of Micro-Economic and Social Impacts

Indecon International Economic ConsultantsIndependent Socio-Economic Impact Assessment of the National Lottery

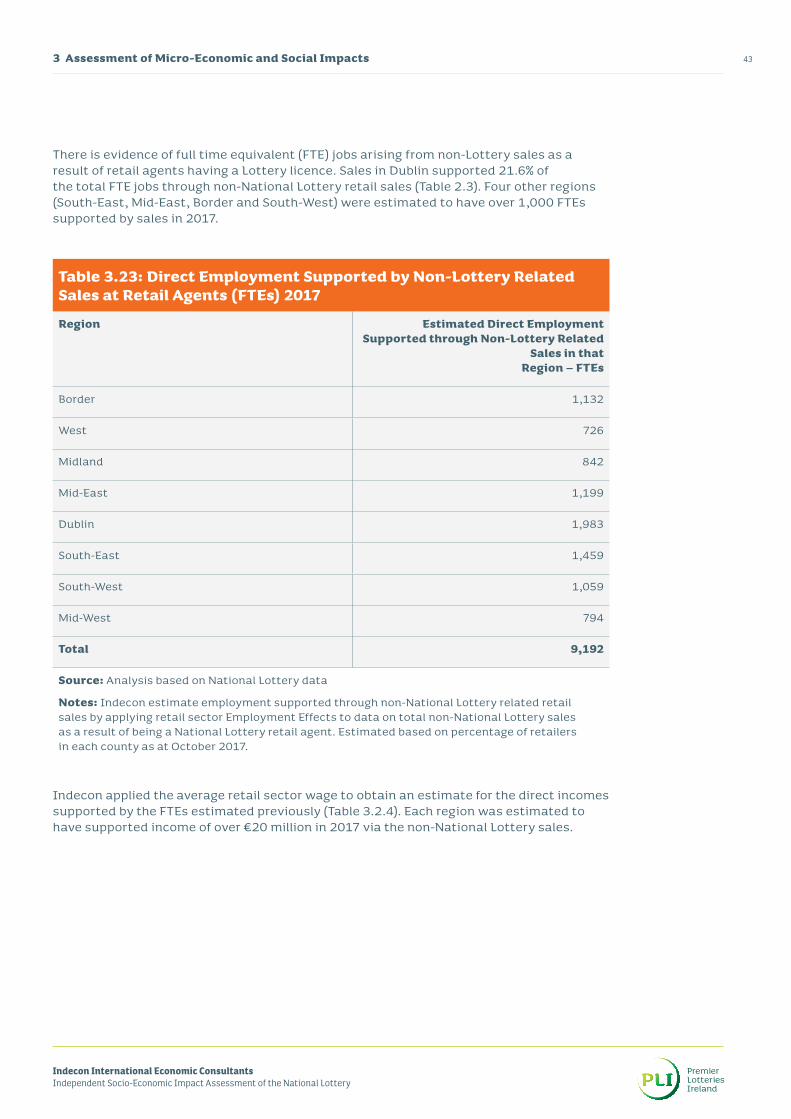

There is evidence of full time equivalent (FTE) jobs arising from non-Lottery sales as a result of retail agents having a Lottery licence. Sales in Dublin supported 21.6% of the total FTE jobs through non-National Lottery retail sales (Table 2.3). Four other regions (South-East, Mid-East, Border and South-West) were estimated to have over 1,000 FTEs supported by sales in 2017.

Table 3.23: Direct Employment Supported by Non-Lottery Related Sales at Retail Agents (FTEs) 2017

Region Estimated Direct Employment Supported through Non-Lottery Related

Sales in that Region – FTEs

Border 1,132

West 726

Midland 842

Mid-East 1,199

Dublin 1,983

South-East 1,459

South-West 1,059

Mid-West 794

Total 9,192

Source: Analysis based on National Lottery data