29

Society of Trust and Estate Practitioners September 9, 2014 Presented by Karl J. Feitelberg and Gary R. Lee Sterling Resources, LTD Solving the UNI Quagmire

| Date post: | 03-May-2018 |

| Category: |

Documents |

| Upload: | hoangtuyen |

| View: | 219 times |

| Download: | 2 times |

Society of Trust and Estate Practitioners September 9, 2014

Presented by

Karl J. Feitelberg and Gary R. Lee

Sterling Resources, LTD

Solving the UNI Quagmire

1. A Non-grantor Foreign Trust with a U.S. Beneficiary

accumulates income over time (UNI)

Non-Grantor Foreign Trust

2. In later years, the Trust makes a distribution to the U.S. Beneficiary in excess of current year

Distributable Net Income (DNI)

Solving the UNI Quagmire (Undistributed Net Income)

3. The U.S. taxes the distribution under the ‘Throwback Rules’ which are intended to impose the tax that would have been paid if the Trust had made distributions in the years the

income was earned…plus interest…capping the amount at 100% of the distribution

9/1/2014 SRL© 2014

1

Definitions

Foreign Trust – Court and Control Test U.S. court exercises primary supervision over trust administration U.S. persons control all substantial trust decisions Non-Grantor Foreign Trust Grantor retains right to revoke the trust, or Only permissible lifetime distributions are to the Grantor/Grantor’s spouse Distributable Net Income (DNI) In general, taxable income (includes capital gains for foreign trusts) Maximum amount deductible for distributions to Beneficiary Undistributed Net Income (UNI) Income retained by the trust from a year in which all current DNI was not distributed Accumulation Distribution When the trust has a UNI balance and distributions for the year exceed current DNI/accounting income

U.S. Trust

Grantor

Trust

9/1/2014 SRL© 2014

2

UNI

A/D

DNI

UNI

Distribution to Beneficiary retains its tax character

Accumulation Distribution to the Beneficiary UNI is taxed as ordinary income with

interest charges

Year X Distribute less than current year

DNI to Beneficiary

Year Y Distribute more than current

year DNI to Beneficiary when there is UNI in the Trust

DNI

Excess DNI not distributed is retained by the Trust as UNI

Distribution to Beneficiary retains its tax character

The UNI “Cycle”

9/1/2014 SRL© 2014

3

Income/Estate Tax

Current Year Income

Original Gift to Trust

UNI

Ordinary Income/ Capital Gains

Non-Taxable

Ordinary Income plus

Interest Charge

Income Tax Upon Distribution

Inclusion in Taxable Estate

Depends on Terms of Trust

Assumed Taxable If Distributed

To Beneficiary and Retained Until Death

Foreign Non-Grantor Trust

9/1/2014 SRL© 2014

4

The Case

Scenario An Italian grandfather established an offshore trust for the benefit of his heirs The grandfather died in 1991 at which time the trust became a Non-Grantor Foreign Trust The current beneficiary of the trust is the grandfather’s granddaughter The granddaughter moved to the U.S. prior to 1991 She is now 50 years old and is reviewing her distribution options The Trust The Trust had a balance of $10,000,000 in 1991 at the time of the grandfather’s death Currently, the Trust has a balance of approximately $30,000,000

9/1/2014 SRL© 2014

5

UNI Options

Alternative Planning Options Continue to Accumulate Current Income Distribute All Assets/Terminate the Foreign Trust Decant the Trust to a U.S. Trust * Domesticate the Foreign Trust to a U.S. Trust Distribute Current Income Annually to a U.S. Beneficiary/U.S. Trust Default Method for distributions to a U.S. Beneficiary/U.S. Trust

* Treated as a distribution for UNI purposes

ACCUMULATE UNI

DISTRIBUTE UNI

“FREEZE” UNI

9/1/2014 SRL© 2014

6

Current Income Retained by Trust

UNI Increases over time

Accumulation Distribution Taxes/interest could equal 100%

of the distribution

Estate Tax May not apply

Net to Heirs Reduced over time

Accumulate UNI

Continue to Accumulate UNI

Taxes and Interest Due Upon Ultimate

Distribution

Taxes and Interest Capped at 100% of

the Distribution

Accumulation Distribution

Accumulation Distribution

9/1/2014 SRL© 2014

7

NON-UNI INVESTMENT ACCOUNT Balance BOY Earnings Taxes Net Investment Account Earnings CURRENT DISTRIBUTION FROM TRUST Income Taxes Net Current Distribution ACCUMULATION DISTRIBUTION Accumulation Distribution Tax on Accumulation Distribution Interest on Accumulation Distribution Net Accumulation Distribution CAPITAL DISTRIBUTION TOTAL AVAILABLE FUNDS ESTATE TAX Assets Included in Taxable Estate Estate Tax Rate Estate Tax Due NET TO HEIRS

2050 0 0 0 0 8,300,000 3,500,000 4,800,000 157,800,000 68,500,000 89,300,000 0 10,000,000 14,800,000 - 40% - 14,800,000

2015 0 0 0 0 0 0 0 0 0 0 0 0 0 - 40% - 0

Accumulate UNI

*

*

Assumes distribution outside taxable estate

*

9/1/2014 SRL© 2014

8

Current Income Remaining assets reinvested by

U.S. Beneficiary/U.S. Trust

Accumulation Distribution UNI taxed with interest upon

distribution

Estate Tax Assets held in Beneficiary

account subject to estate tax

Net to Heirs Reduced, but larger than

“Accumulate” option

Distribute UNI

If held by Beneficiary at death, account balance included in taxable estate further reducing net to heirs

Investment account growth is reduced

Tax and Interest on UNI paid immediately reduces

investment account

Accumulation Distribution

9/1/2014 SRL© 2014

9

NON-UNI INVESTMENT ACCOUNT Balance BOY Earnings Taxes Net Investment Account Earnings CURRENT DISTRIBUTION FROM TRUST Income Taxes Net Current Distribution ACCUMULATION DISTRIBUTION Accumulation Distribution Tax on Accumulation Distribution Interest on Accumulation Distribution Net Accumulation Distribution CAPITAL DISTRIBUTION TOTAL AVAILABLE FUNDS ESTATE TAX Assets Included in Taxable Estate Estate Tax Rate Estate Tax Due NET TO HEIRS

2050 53,700,000 2,600.000 1,000,000 55,300,000 0 0 0 0 0 0 0 0 55,300,000 55,300,000 40% 22,100,000 33,200,000

2015 0 0 0 0 1,500,000 600,000 900,000 20,900,000 7,900,000 4,700,000 8,300,000 10,000,000 19,200,000 - 40% - 0

Distribute UNI

9/1/2014 SRL© 2014

10

Current Income Current income taxed;

reinvested outside UNI umbrella

UNI Tax is “Frozen” since current

income is distributed annually

Accumulation Distribution Taxed with interest when

ultimately distributed

Estate Tax Assets held in Beneficiary

account subject to estate tax

Net to Heirs Enhanced over other options

“Freeze” UNI

Net after-tax income accumulated outside of the

UNI environment

Accumulation Distribution

“Frozen”

Tax and Interest on UNI Could reach 100% of the

“Frozen” UNI amount

Accumulation Distribution

Accumulation Distribution

9/1/2014 SRL© 2014

11

INVESTMENT ACCOUNT Balance BOY Earnings Taxes Net Investment Account Earnings CURRENT DISTRIBUTION FROM TRUST Income Taxes Net Current Distribution ACCUMULATION DISTRIBUTION Accumulation Distribution Tax on Accumulation Distribution Interest on Accumulation Distribution Net Accumulation Distribution CAPITAL DISTRIBUTION TOTAL AVAILABLE FUNDS ESTATE TAX Assets Included in Taxable Estate Estate Tax Rate Estate Tax Due NET TO HEIRS

“Freeze” UNI

2015 0 0 0 0 1,500,000 600,000 900,000 0 0 0 0 0 900,000 - 40% - 0

2050 57,000,000 2,900,000 1,100,000 58,800,000 1,500,000 600,000 900,000 20,900,000 9,100,000 11,800,000 0 10,000,000 69,700,000 59,700,000 40% 23,900,000 45,800,000

* Assumes distribution outside taxable estate

9/1/2014 SRL© 2014

12

Prior Year 1

$ Distribution

Prior Year 2

$ Distribution

Prior Year 3

$ Distribution

Sum of Prior 3 Years Distributions Times 1.25

Divided by 3

Average Distribution Increased by 25%

Treated as a Distribution of Current Income

without UNI Charges

|

Balance of Distribution Taxed as an Accumulation Distribution

The Default Method – A Hybrid “Freeze” Approach

The “Cost” of the Election All income taxed at ordinary rates Once elected, can not be changed

9/1/2014 SRL© 2014

13

Summary – Highlighted Concerns

Current Income Retained by Trust

UNI Increases over time

Accumulation Distribution Taxes/interest could equal 100%

of the distribution

Estate Tax May not apply

Net to Heirs Reduced over time

Current Income Remaining assets reinvested by

U.S. Beneficiary/U.S. Trust

Accumulation Distribution UNI taxed with interest upon

distribution

Estate Tax Assets held in Beneficiary

account subject to estate tax

Net to Heirs Reduced, but larger than

“Accumulate” option

Current Income Current income taxed;

reinvested outside UNI umbrella

UNI Tax is “Frozen” since income is

distributed annually

Accumulation Distribution Taxed with interest when

ultimately distributed

Estate Tax Assets held in Beneficiary

account subject to estate tax

Net to Heirs Enhanced over other options

Accumulate UNI Distribute UNI “Freeze” UNI

9/1/2014 SRL© 2014

14

The Spreadsheet Analysis

Approached by an attorney with a UNI issue who wondered if life insurance might offer a solution given the tax-free build up of cash value and income tax-free receipt of death benefit… …however, life insurance proceeds received inside a foreign trust do not escape UNI treatment for subsequent trust distributions We took a different approach, accepting the UNI toll charge and using life insurance to recreate the trust corpus in a more tax advantageous environment, making this the generation to “solve the problem” The goal of the analysis was to compare UNI distribution alternatives to see which was stronger in terms of maximizing the net amount passed to heirs under three scenarios No Life Insurance $30,000,000 Life Insurance on the Beneficiary’s life (current Trust balance) $99,000,000 Life Insurance on the Beneficiary’s life (premium based on Trust net cash flow)

9/1/2014 SRL© 2014

15

-

20,000,000

40,000,000

60,000,000

80,000,000

100,000,000

120,000,000

140,000,000

160,000,000

180,000,000

200,000,000

220,000,000

Net to Heirs - Death at Age 85 1991 Trust for a Beneficiary Insurance Age 50

No Insurance

30.9m Insurance

99.0m Insurance *

9/1/2014 SRL© 2014

16

Accumulate Distribute Decant Domesticate Income to Bene Income to Trust Default to Bene Default to Trust MEC

No Insurance 14,800,000 33,200,000 53,500,000 69,700,000 45,800,000 69,700,000 38,000,000 63,400,000 -

DB - Trust Bal

DB - Net Income

-

20,000,000

40,000,000

60,000,000

80,000,000

100,000,000

120,000,000

140,000,000

160,000,000

180,000,000

200,000,000

220,000,000

Net to Heirs - Death at Age 85 1991 Trust for a Beneficiary Insurance Age 50

No Insurance

30.9m Insurance

99.0m Insurance *

9/1/2014 SRL© 2014

17

Accumulate Distribute Decant Domesticate Income to Bene Income to Trust Default to Bene Default to Trust MEC

No Insurance 14,800,000 33,200,000 53,500,000 69,700,000 45,800,000 69,700,000 38,000,000 63,400,000 -

DB - Trust Bal

DB - Net Income

Accumulate Distribute ‘Freeze’

-

20,000,000

40,000,000

60,000,000

80,000,000

100,000,000

120,000,000

140,000,000

160,000,000

180,000,000

200,000,000

220,000,000

Net to Heirs - Death at Age 85 1991 Trust for a Beneficiary Insurance Age 50

No Insurance

30.9m Insurance

99.0m Insurance *

9/1/2014 SRL© 2014

18

Taxable in the Estate

Not subject to Estate Tax

Taxable in the Estate

Not subject to Estate Tax

Taxable in the Estate

Not subject to Estate Tax

Accumulate Distribute Decant Domesticate Income to Bene Income to Trust Default to Bene Default to Trust MEC

No Insurance 14,800,000 33,200,000 53,500,000 69,700,000 45,800,000 69,700,000 38,000,000 63,400,000 -

DB - Trust Bal

DB - Net Income

Accumulate Distribute ‘Freeze’

-

20,000,000

40,000,000

60,000,000

80,000,000

100,000,000

120,000,000

140,000,000

160,000,000

180,000,000

200,000,000

220,000,000

Net to Heirs - Death at Age 85 1991 Trust for a Beneficiary Insurance Age 50

No Insurance

30.9m Insurance

99.0m Insurance *

9/1/2014 SRL© 2014

19

Income to Trust Domesticate Default

to Trust

Accumulate Distribute Decant Domesticate Income to Bene Income to Trust Default to Bene Default to Trust MEC

No Insurance 14,800,000 33,200,000 53,500,000 69,700,000 45,800,000 69,700,000 38,000,000 63,400,000 -

DB - Trust Bal

DB - Net Income

Accumulate Distribute ‘Freeze’

-

20,000,000

40,000,000

60,000,000

80,000,000

100,000,000

120,000,000

140,000,000

160,000,000

180,000,000

200,000,000

220,000,000

Net to Heirs - Death at Age 85 1991 Trust for a Beneficiary Insurance Age 50

No Insurance

30.9m Insurance

99.0m Insurance *

Income to Trust Domesticate Default

to Trust

Accumulate Distribute Decant Domesticate Income to Bene Income to Trust Default to Bene Default to Trust MEC

No Insurance 14,800,000 33,200,000 53,500,000 69,700,000 45,800,000 69,700,000 38,000,000 63,400,000 -

DB - Trust Bal 37,800,000 52,900,000 71,100,000 87,300,000 65,600,000 87,300,000 57,700,000 81,000,000

DB - Net Income

9/1/2014 SRL© 2014

20 Accumulate Distribute ‘Freeze’

-

20,000,000

40,000,000

60,000,000

80,000,000

100,000,000

120,000,000

140,000,000

160,000,000

180,000,000

200,000,000

220,000,000

Net to Heirs - Death at Age 85 1991 Trust for a Beneficiary Insurance Age 50

No Insurance

30.9m Insurance

99.0m Insurance *

Income to Trust Domesticate Default to

Trust

MEC

Accumulate Distribute Decant Domesticate Income to Bene Income to Trust Default to Bene Default to Trust MEC

No Insurance 14,800,000 33,200,000 53,500,000 69,700,000 45,800,000 69,700,000 38,000,000 63,400,000 -

DB - Trust Bal 37,800,000 52,900,000 71,100,000 87,300,000 65,600,000 87,300,000 57,700,000 81,000,000

DB - Net Income 88,400,000 84,500,000 109,800,000 126,100,000 109,000,000 126,100,000 96,500,000 119,700,000 202,400,000

9/1/2014 SRL© 2014

21 Accumulate Distribute ‘Freeze’

* (202m net)

Premature Death Lack of investment time

Fewer premium payments Impact of UNI rules Consistent pattern

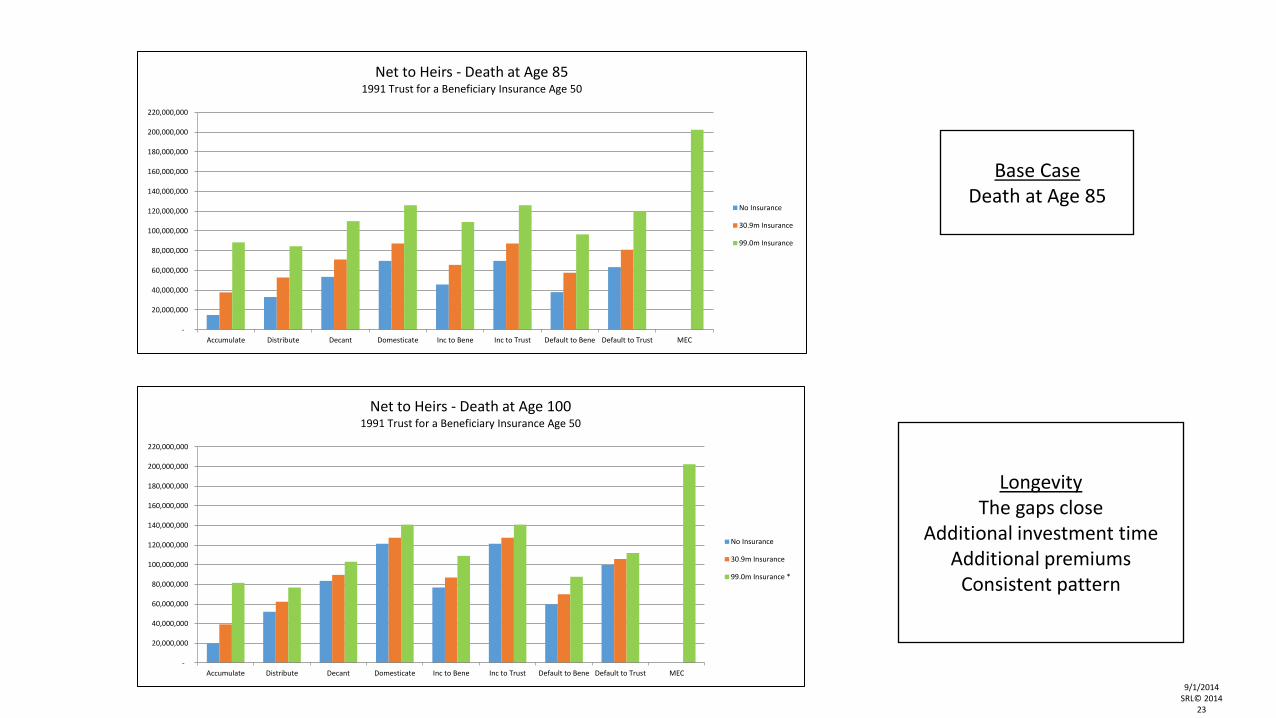

Base Case Death at Age 85

-

20,000,000

40,000,000

60,000,000

80,000,000

100,000,000

120,000,000

140,000,000

160,000,000

180,000,000

200,000,000

220,000,000

Accumulate Distribute Decant Domesticate Inc to Bene Inc to Trust Default to Bene Default to Trust MEC

Net to Heirs - Death at Age 85 1991 Trust for a Beneficiary Insurance Age 50

No Insurance

30.9m Insurance

99.0m Insurance

-

20,000,000

40,000,000

60,000,000

80,000,000

100,000,000

120,000,000

140,000,000

160,000,000

180,000,000

200,000,000

220,000,000

Accumulate Distribute Decant Domesticate Inc to Bene Inc to Trust Default to Bene Default to Trust MEC

Net to Heirs - Death at Age 70 1991 Trust for a Beneficiary Insurance Age 50

No Insurance

30.9m Insurance

99.0m Insurance *

9/1/2014 SRL© 2014

22

Longevity The gaps close

Additional investment time Additional premiums

Consistent pattern

Base Case Death at Age 85

-

20,000,000

40,000,000

60,000,000

80,000,000

100,000,000

120,000,000

140,000,000

160,000,000

180,000,000

200,000,000

220,000,000

Accumulate Distribute Decant Domesticate Inc to Bene Inc to Trust Default to Bene Default to Trust MEC

Net to Heirs - Death at Age 85 1991 Trust for a Beneficiary Insurance Age 50

No Insurance

30.9m Insurance

99.0m Insurance

-

20,000,000

40,000,000

60,000,000

80,000,000

100,000,000

120,000,000

140,000,000

160,000,000

180,000,000

200,000,000

220,000,000

Accumulate Distribute Decant Domesticate Inc to Bene Inc to Trust Default to Bene Default to Trust MEC

Net to Heirs - Death at Age 100 1991 Trust for a Beneficiary Insurance Age 50

No Insurance

30.9m Insurance

99.0m Insurance *

9/1/2014 SRL© 2014

23

Base Case $250,000 Annual

Distribution to Beneficiary

Base Case Maximize

Distribution to Heirs

-

20,000,000

40,000,000

60,000,000

80,000,000

100,000,000

120,000,000

140,000,000

160,000,000

180,000,000

200,000,000

220,000,000

Accumulate Distribute Decant Domesticate Inc to Bene Inc to Trust Default to Bene Default to Trust MEC

Net to Heirs - Death at Age 85 1991 Trust for a Beneficiary Insurance Age 50

No Insurance

30.9m Insurance

99.0m Insurance

(40,000,000)

(20,000,000)

-

20,000,000

40,000,000

60,000,000

80,000,000

100,000,000

120,000,000

140,000,000

160,000,000

180,000,000

200,000,000

220,000,000

Accumulate Distribute Decant Domesticate Inc to Bene Inc to Trust Default to Bene Default to Trust MEC

Net to Heirs - Death at Age 85 1991 Trust for a Beneficiary Insurance Age 50

No Insurance

30.9m Insurance

99.0m Insurance *

9/1/2014 SRL© 2014

24

“The” Solution to the UNI Quagmire…

Alternative Approaches Monitor Income Distributions Manage trust accounting income through use of a trust owned LLC Alternate between Foreign and U.S. Beneficiary distributions Distribute Capital Gain Property at Basis Subsequent taxation upon sale by Beneficiary Continue Trust in Place with Distributions of Income “Forever” Rule Against Perpetuities may force an ultimate distribution No early access to corpus for business/investment reasons Use Life Insurance to Replicate the Trust Corpus in a More Advantageous Tax Environment To maximize net to heirs To include an annual distribution to the current beneficiary

9/1/2014 SRL© 2014

25

-

20,000,000

40,000,000

60,000,000

80,000,000

100,000,000

120,000,000

140,000,000

160,000,000

180,000,000

200,000,000

220,000,000

Net to Heirs - Death at Age 85 1991 Trust for a Beneficiary Insurance Age 50

No Insurance

30.9m Insurance

99.0m Insurance *

Accumulate Distribute Decant Domesticate Income to Bene Income to Trust Default to Bene Default to Trust MEC

No Insurance 14,800,000 33,200,000 53,500,000 69,700,000 45,800,000 69,700,000 38,000,000 63,400,000 -

DB - Trust Bal 37,800,000 52,900,000 71,100,000 87,300,000 65,600,000 87,300,000 57,700,000 81,000,000

DB - Net Income 88,400,000 84,500,000 109,800,000 126,100,000 109,000,000 126,100,000 96,500,000 119,700,000 202,400,000

* (202m net) 9/1/2014

SRL© 2014 26

Sterling Resources, Ltd 175 Derby Street, Suite 33

Hingham, MA 02043 781-749-1533

Karl J. Feitelberg Gary R. Lee 617-645-3598 617-692-0279

Society of Trust and Estate Practitioners September 9, 2014

Presented by

Karl J. Feitelberg and Gary R. Lee

Sterling Resources, LTD

Solving the UNI Quagmire