161

2011 Economic, Environmental and Social Report Specialists in creating… sustainable shopping centres

| Date post: | 24-Oct-2014 |

| Category: |

Documents |

| Upload: | csrmediaro-network |

| View: | 242 times |

| Download: | 3 times |

2011Economic, Environmental

and Social Report

Specialists increating… sustainable

shoppingcentres

SONAE SIERRA Economic, Environmental and Social Report 2011

Global Reporting Initiative (GRI)Self-Declaration Statement

For more information about the GRI G3 and G3.1 Sustainability Reporting Guidelines, please see: https://www.globalreporting.org/reporting/reporting-framework-overview/Pages/default.aspx

For more information about the GRI CRESS, please see:https://www.globalreporting.org/reporting/sector-guidance/construction-and-real-estate/Pages/default.aspx

Further reference:

This report provides a comprehensive review of Sonae Sierra’s economic, environmental and social strategy and the Company’s performance in2011. We believe that this report complies with level A of the Global Reporting Initiative (GRI) Sustainability Reporting Guidelines (G3.1:2011),both in terms of the report contents and performance indicators. Our compliance with the GRI Guidelines has been independently verified byDeloitte, whose assurance statement enables us to self-declare to GRI level A+.

Two important developments took place concerning the GRI framework in 2011. In March, the GRI launched the G3.1 Sustainability ReportingGuidelines, which include expanded guidance for reporting on human rights, local community impacts and gender. In September, the GRIlaunched the Construction and Real Estate Sector Supplement (GRI CRESS). The GRI CRESS is a version of the GRI G3.1 Guidelines tailored forthe construction and real estate sector. It encompasses some specific performance indicators and disclosure requirements, as well as generalguidance, so as to ensure that companies in this sector report most effectively on the industry’s key economic, social and environmentalsustainability issues. Sonae Sierra has developed this report in line with the GRI 3.1 guidelines and has also followed the GRI CRESS whereverpossible. We have included a column in our GRI Content Index on pages 109 to 154 to show which of our GRI performance indicators have beenreported in line with the GRI CRESS. However, since these guidelines were only released in September 2011, we have not been able to applythem fully in the 2011 reporting cycle. We aim to do this in time for our next Annual Report, which is scheduled for publication in April 2013.

C C+ B B+ A A+

Mandatory Self declared 3

Optional Third party checked 3

GRI checked

Contents

Corporate Overview

Who We Are… 1

CEO’s Statement 2

The Year at a Glance 4

Our Company 9

Our Business Strategy 15

Economic Performance 29

The Economic Context 30

Operational Performance 32

Consolidated Accounts 39

Environmental Performance 46

Energy and Climate 47

Water 57

Waste 63

Biodiversity and Habitats 68

Social Performance 71

Suppliers 72

Tenants 78

Communities and Visitors 83

Employees 91

Safety and Health 96

Board Members and Executives 104

Global Reporting Initiative 109

Profile Disclosures 110

Economic Aspects 121

Environmental Aspects 123

Labour Practices and Decent Work Aspects 136

Human Rights Aspects 143

Society Aspects 145

Product Responsibility Aspects 150

Independent Auditor’s Review 155

Feedback Form 157

SONAE SIERRA Economic, Environmental and Social Report 2011

Back to main contents

Sonae Sierra is a specialist at the cutting edge of shoppingcentre development, ownership, management and thedelivery of services to third parties in markets as diverseas Europe, South America and North Africa.

Passionate about bringing innovation and excitement to the shopping industry since 1989, Sonae

Sierra has been interpreting trends and spearheading a movement that has defined the shopping

centres of the future focused on the creation of unique shopping experiences. Through our

integrated strategy of investment, development and property management, we have developed

a unique understanding of the business and markets we operate in, and we have earned more

international awards than any other company in our sector.

We have long recognised that environmental and social performance affects our financial results,

and we believe that our long-term business success is dependent on all three dimensions: economic,

environmental and social. We have pioneered the integration of sustainability principles into the

shopping centre business and we are already reaping the benefits of this forward-thinking approach.

This year we have chosen not to publish a stand-alone Corporate Responsibility (CR) Report, but to

develop a fully integrated Economic, Social and Environmental Performance Report. We consider

that this approach provides our stakeholders with a more robust and engaging account of our

current strategy and our performance in 2011, and demonstrates how we encompass all three

dimensions of performance into our day-to-day business activities.

Who We Are…

Centro Colombo, Portugal Manauara Shopping, Brazil Loop5, Germany

CORPORATE OVERVIEW

Who We Are… 1

CEO’s Statement 2

The Year at a Glance 4

Our Company 9

Our Business Strategy 15

1

Fernando Guedes OliveiraChief Executive Officer

“I’M REALLY PROUD OF THE RESULTS WE ARE ABLE TO REPORT FOR THE PAST 12 MONTHS, IN SPITEOF THE CHALLENGING MARKETCONDITIONS. WE INCREASED OUR NET PROFIT IN 2011 BY SUCCESSFULLYSUSTAINING INCOME STREAMS AND REDUCING COSTS.”

A conversation with Fernando Guedes Oliveira,Sonae Sierra CEO

Q: How has Sonae Sierra’s business fared overallduring the past 12 months and has the year turnedout as you expected?

A: I’m really proud of the results we are able to report for the past12 months, in spite of the challenging market conditions. Weincreased our net profit in 2011 by successfully sustaining incomestreams and reducing costs. Overall, global tenant rents are up ona like-for-like basis and our occupancy levels remained above 96%throughout the year – a significant achievement in some marketswhere tenant sales were affected by lower consumer purchasingpower. We have also mitigated some of the market risks outsideour direct control such as rising yields and capital constraints, so I would say we have emerged from a tough year relatively intact.

Q: In the context of continued economic turmoil, whatwould you say have been your greatest achievementsin 2011?

A: Despite the increasing challenges of securing new capital andrefinancing debt in Europe in particular, we have continued tosustain the growth of our business through new developments,with two new centres starting construction; one in Germany andone in Brazil. This has been made possible through our proactivecapital recycling strategy, which in Brazil saw the successful InitialPublic Offering (IPO) of our business generate significant funds,and in Europe included the sale of two shopping centres in Spain.

While the Government austerity measures in some Europeanmarkets have undoubtedly affected consumer purchasing powerand reduced tenant sales, we have succeeded in protecting ourincome streams and maintaining high levels of occupancyamongst our tenants. This has been achieved through theefficiency and attentiveness of our property management, as well as our willingness to work closely with tenants to protecttheir business viability.

Finally, we continue to benefit from international expansion, andour growth in rapidly growing economies like Brazil hedges our riskin other markets where GDP is flatter. In 2011 we established apresence in Morocco and Algeria as a service provider to thirdparties, as well as delivering development services to a client inCroatia. The growth in our third party service provision is anothersuccess factor that has enabled us to retain talent, develop newincome streams, and gain insights into new markets.

Q: What does 2012 look like for Sonae Sierra? Arebusiness prospects likely to get worse before they can return to growth?

A: The last couple of years have required us to focus onmaintaining our financial stability, increasing operationalefficiencies, controlling costs and retaining our core competencies.As a business, we have proven extremely resilient and we shouldemerge from the current financial crisis in a strong position toreturn to growth in the context of a new world reality.

2012 will be a year of recession, decisive for the European Union.There is no doubt that the economic conditions with particularimpact in Portugal, Greece and, to a lesser extent, Spain and Italy,will inevitably affect our operational performance in Europe.

However, we are confident that we will continue to show positiveresults, thanks in part to our geographical spread, which enablesus to be present in countries where economic growth is a reality.For instance in Brazil, we have two inaugurations scheduled for2012: Uberlândia Shopping and Boulevard Londrina Shopping.

In mature markets, we will maintain our efforts to improveoperational efficiency, and we will continue to search for newinvestment opportunities, with a focus on Germany and also Italy,where in March 2012 we will inaugurate Le Terrazze in La Spezia.

2SONAE SIERRA Economic, Environmental and Social Report 2011

CEO’s Statement

Back to main contents

CORPORATE OVERVIEW

Who We Are… 1

CEO’s Statement 2

The Year at a Glance 4

Our Company 9

Our Business Strategy 15

3SONAE SIERRA Economic, Environmental and Social Report 2011

CEO’s Statement continued

Back to main contents

I am privileged to lead an organisation which is highly regarded byour customers, partners, banks and suppliers; an organisation thatacts responsibly towards local communities and the environment,and that is driven by dedicated employees who are always lookingfor better ways of doing business. This is why I am confident thatwe will maintain a good position in 2012 and continue to grow inthe years ahead.

Q: Last year you highlighted a number ofopportunities for expansion into new and emergingmarkets. Have these materialised, and do you plan tocontinue growing the business in new geographies?

a: We believe we have the right combination of skills to tap intothe potential offered by new and emerging markets. We continueto actively explore opportunities to export our business model andhave created a new department for this purpose. Some of the keyprinciples underpinning our growth strategy into new and emergingmarkets include:

• Delivering third party services prior to direct investment, tolearn first-hand about the market characteristics and key risksand opportunities.

• Disposing of some of our operational centres in establishedmarkets, to rebalance the weighting of our portfolio in favour offaster growing economies.

• Entering into partnerships with like-minded shopping centreinvestors/operators, to share skills and capabilities as well asinvestment risks.

Currently, we are actively exploring further opportunities in theMediterranean Basin (Morocco and Algeria) and Colombia.

Q: Can you comment on Sonae Sierra’s overallenvironmental and social performance over the past year? What have been the key highlights andchallenges, and how has CR contributed to your wider business objectives?

a: We are already reaping financial benefits from increased eco-efficiency across our portfolio – for example, we have calculatedthat in 2011 we avoided costs of €7.3 million as a result of theenergy efficiency measures we have implemented since 2002.With regards to social aspects we have also maintained a strongperformance, sustaining levels of tenant and visitor satisfaction,our investment in local communities and reducing accidentsamong our workforce.

For Sonae Sierra, sustainability means the continuous evaluation of our economic, social and environmental performance, seeking toachieve a harmonious balance between all three areas. We continueto be viewed as an international benchmark of sustainabilityexcellence in the shopping centre sector, as proven most recentlyby our funds being ranked as the most sustainable in Europeaccording to the Global Real Estate Sustainability Benchmark.

We believe that sustainability will increasingly become a decisivefactor in our relationship with our stakeholders. Society isbecoming more and more aware of environmental and socialquestions and is rewarding those companies that have responsibleand resilient business strategies. Legislation reflects this trend,and is progressively more demanding. Finally, through careful costbenefit analysis, we are able to prove that sustainability principlesincorporated in all business areas can result in lower operationalcosts, which in turn lower our service charges for tenants andcontribute to higher occupancy and satisfaction levels.

CORPORatE OvERvIEw

Who We Are… 1

CEO’s Statement 2

The Year at a Glance 4

Our Company 9

Our Business Strategy 15

4SONAE SIERRA Economic, Environmental and Social Report 2011

The Year at a Glance

Back to main contents

Key ActivitiesINVESTMENT

• Successful Initial Public Offering(IPO) of Sonae Sierra Brasil

• Sale of Plaza Éboli and El Rosalshopping centres in Spain to Doughty Hanson for €120 million

• Acquisition of the remaining25% of Plaza Mayor Shopping inSpain on behalf of the SierraFund, making it now the soleowner of the asset

• Successful refinancing ofAlgarveShopping in Portugal

• Completion of the expansionand refurbishment of ShoppingMetrópole and the expansion of Shopping Campo Limpo1

(both in Brazil)

DEVELOPMENT

• Commenced construction of anew project, Passeio das ÁguasShopping, in Goiânia, Brazil

• Announced a joint venture with MAB Development todevelop a shopping centre in Solingen, Germany

• Entered the final stage ofconstruction of Le Terrazze inItaly and Uberlândia Shopping in Brazil

• Proceeded with thedevelopment of BoulevardLondrina Shopping in Brazil

MANAGEMENT

• Proceeded with the letting of Le Terrazze (Italy); UberlândiaShopping and BoulevardLondrina Shopping (Brazil)

• Initiated the letting of Solingenin Germany

SERVICES TO THIRD PARTIES

• Entry into the Moroccan market with a contract toprovide development servicesfor a shopping centre project in Casablanca

• Entered the Algerian marketthrough a joint ventureagreement with Cévital Group to provide development,property management andleasing services for shoppingcentres in this country

• Signed property managementand/or leasing contracts withthird parties for a further nineshopping centres in Europe

• Development managementservice agreement for a new shopping centre in Zagreb, Croatia

Entry into

keygrowthmarkets

CORPORATE OVERVIEW

Who We Are… 1

CEO’s Statement 2

The Year at a Glance 4

Our Company 9

Our Business Strategy 15

1 Since we have a minority position in this shopping centre and the refurbishment process was controlled by the other centres owner, we did not implement our Safety, Health andEnvironment Management System (SHEMS) procedures for development on this project. Therefore, no information regarding this completed project’s energy and waterconsumption; waste recycling rates and safety and health performance is made available in the report. Nevertheless, it is a site managed by Sonae Sierra and we consideradequate reporting on the existence of these works.

AlgarveShopping, Portugal

5SONAE SIERRA Economic, Environmental and Social Report 2011

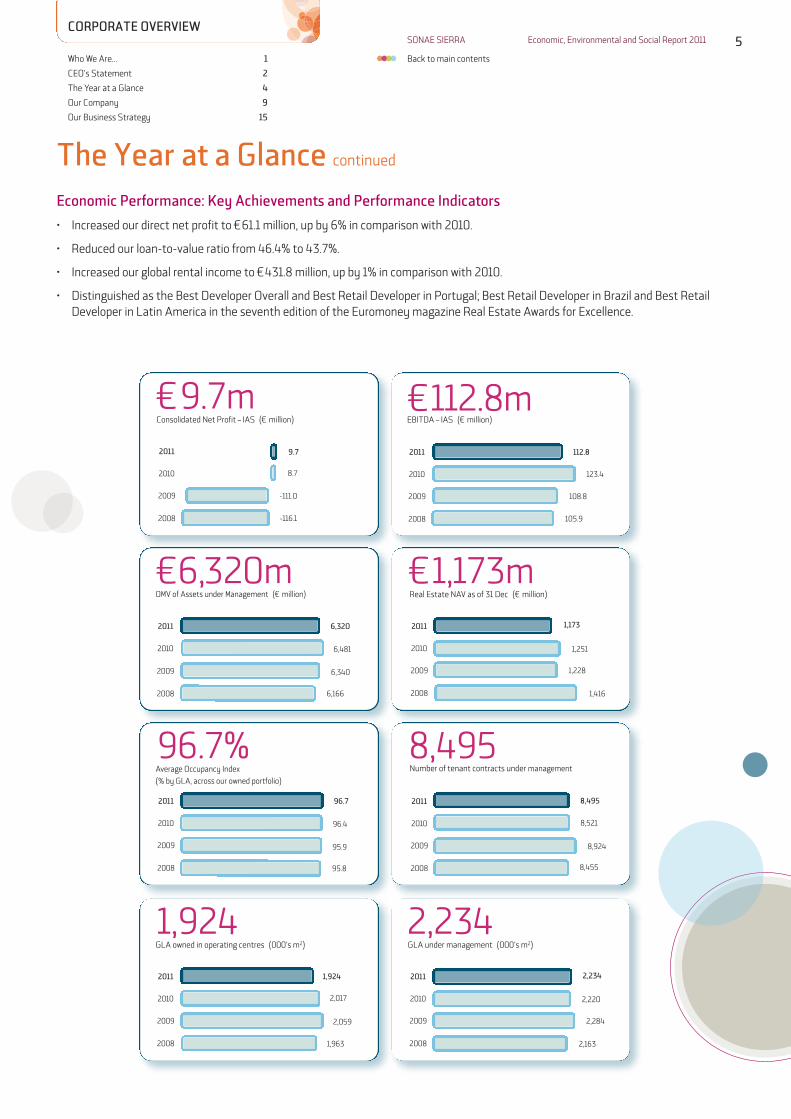

The Year at a Glance continued

Back to main contents

123.42010

112.82011

2008 6,166

6,3402009

6,4812010

6,3202011

€6,320mOMV of Assets under Management (€ million)

2008

2009

€112.8mEBITDA – IAS (€ million)

8,495Number of tenant contracts under management

108.8

105.9

8,495

8,521

8,924

8,455

€1,173mReal Estate NAV as of 31 Dec (€ million)

2,234GLA under management (000’s m2)

1,924GLA owned in operating centres (000’s m2)

1,173

1,251

1,228

1,416

1,924

2,017

2,059

1,963

2,234

2,220

2,284

2,163

CORPORATE OVERVIEW

Who We Are… 1

CEO’s Statement 2

The Year at a Glance 4

Our Company 9

Our Business Strategy 15

Economic Performance: Key Achievements and Performance Indicators

• Increased our direct net profit to €61.1 million, up by 6% in comparison with 2010.

• Reduced our loan-to-value ratio from 46.4% to 43.7%.

• Increased our global rental income to €431.8 million, up by 1% in comparison with 2010.

• Distinguished as the Best Developer Overall and Best Retail Developer in Portugal; Best Retail Developer in Brazil and Best RetailDeveloper in Latin America in the seventh edition of the Euromoney magazine Real Estate Awards for Excellence.

95.8

95.9

96.4

96.7

96.7%Average Occupancy Index

(% by GLA, across our owned portfolio)

2010

2011

2008

2009

2010

2011

2008

2009

2010

2011

2008

2009

2010

2011

2008

2009

2010

2011

2008

2009

-116.1

-111.0

8.7

9.7

€9.7mConsolidated Net Profit – IAS (€ million)

2010

2011

2008

2009

6SONAE SIERRA Economic, Environmental and Social Report 2011

The Year at a Glance continued

Back to main contents

Environmental Performance: Key Achievements and Performance Indicators

• Sonae Sierra property funds ranked as the most sustainable in Europe and third worldwide by the Global Real Estate SustainabilityBenchmark (GRESB), which establishes a ranking of the property funds and companies of the real estate sector that are mostcommitted to the environment.

• Sonae Sierra ranked as the leader of the Corporate Climate Responsibility Index published by ACGE in Portugal for the sixth time.

• ISO 14001 certifications achieved for a further three shopping centres and two construction works. Le Terrazze in Italy was the firstshopping centre in the world to simultaneously achieve ISO 14001 and OHSAS 18001 certifications for the Safety, Health andEnvironment Management System (SHEMS) of its construction works.

Boavista Shopping, Brazil Freccia Rossa, Italy ArrábidaShopping, Portugal

CORPORATE OVERVIEW

Who We Are… 1

CEO’s Statement 2

The Year at a Glance 4

Our Company 9

Our Business Strategy 15

0.028Greenhouse gas (GHG) emissions of our ownedportfolio and corporate offices (tCO2e/m

2 GLA)

0.028

0.034

0.067

0.071

2010

2011

2008

2009

553

527

514

514

514Electricity efficiency (excluding tenants) of ourowned portfolio (kWh/m2 mall and toilet area)

2010

2011

2008

2009

3.7Water efficiency (excluding tenants) of our owned portfolio (litres/visit)

3.7

3.7

3.8

3.6

2010

2011

2008

2009

42

46

51

53

53%Total waste recycled as a proportion of waste produced(% by weight, across our owned portfolio)

2010

2011

2008

2009

7SONAE SIERRA Economic, Environmental and Social Report 2011

Back to main contents

Social Performance: Key achievements and Performance Indicators

• Maintained high levels of satisfaction among our tenants, visitors and our employees.

• Reduced the rate and severity of work accidents in our workforce in comparison with 2010.

• Distinguished at the StrategicRISK European Risk Management Awards in the “Most Innovative Use of IT or other Technology”category for our Safety, Health and Environment Inspections System.

• OHSAS 18001 certifications achieved for a further five shopping centres and two construction works (including Le Terrazze,highlighted on the previous page).

2 In 2011, this indicator included investments in CR made through development projects’ marketing budgets. This data was not included in previous years. It also includes donationscollected from shopping centre visitors.

3 Safety, Health and Environment Preventive Observations (SPOs) are a form of safe behaviour audit undertaken at our shopping centres in operation. For further details, please seepage 102.

passionate about

innovative,sustainableideas for ourindustry

CORPORatE OvERvIEw

Who We Are… 1

CEO’s Statement 2

The Year at a Glance 4

Our Company 9

Our Business Strategy 15

the Year at a Glance continued

4.6Tenant Satisfaction Index(scale of 1 (‘not satisfied’) to 6 (‘very satisfied’))

4.6

4.6

4.6

4.2

2010

2011

2008

2009

€1.484mMarketing investments in CR and othercommunity contributions (€ million)2

1.484

1.219

1.143

2.380

2010

2011

2008

2009

€528Investment in staff training and development(€ per capita)

528

776

1,195

900

2010

2011

2008

2009

7.8Number of non-conformities per hour of reference SPO3

7.8

5.8

5.7

7.9

2010

2011

2008

2009

Click here to view the list of further awards and distinctions which we received in 2011

8SONAE SIERRA Economic, Environmental and Social Report 2011

Back to main contents

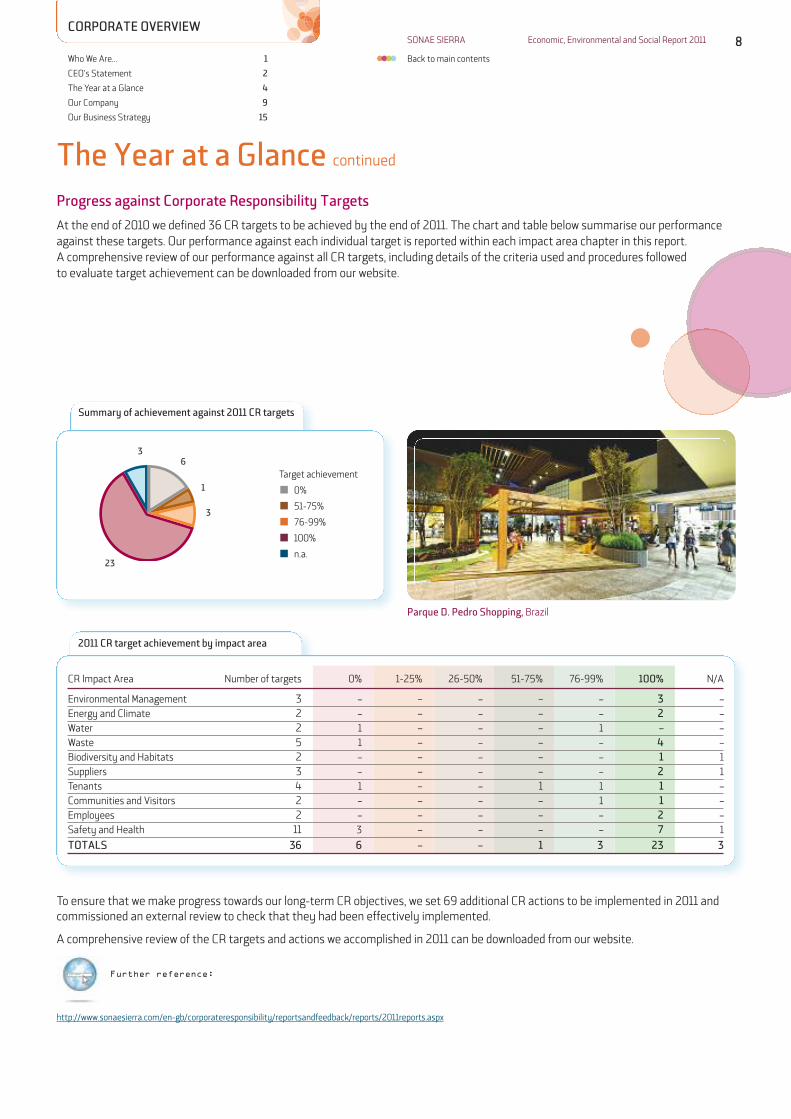

Progress against Corporate Responsibility Targets

At the end of 2010 we defined 36 CR targets to be achieved by the end of 2011. The chart and table below summarise our performanceagainst these targets. Our performance against each individual target is reported within each impact area chapter in this report.A comprehensive review of our performance against all CR targets, including details of the criteria used and procedures followedto evaluate target achievement can be downloaded from our website.

To ensure that we make progress towards our long-term CR objectives, we set 69 additional CR actions to be implemented in 2011 andcommissioned an external review to check that they had been effectively implemented.

A comprehensive review of the CR targets and actions we accomplished in 2011 can be downloaded from our website.

http://www.sonaesierra.com/en-gb/corporateresponsibility/reportsandfeedback/reports/2011reports.aspx

Further reference:

Summary of achievement against 2011 CR targets

Target achievement

0%

51-75%

76-99%

100%

n.a.

2011 CR target achievement by impact area

Parque D. Pedro Shopping, Brazil

23

6

1

3

3

CORPORATE OVERVIEW

Who We Are… 1

CEO’s Statement 2

The Year at a Glance 4

Our Company 9

Our Business Strategy 15

The Year at a Glance continued

CR Impact Area Number of targets 0% 1-25% 26-50% 51-75% 76-99% 100% N/A

Environmental Management 3 – – – – – 3 –Energy and Climate 2 – – – – – 2 –Water 2 1 – – – 1 – –Waste 5 1 – – – – 4 –Biodiversity and Habitats 2 – – – – – 1 1Suppliers 3 – – – – – 2 1Tenants 4 1 – – 1 1 1 –Communities and Visitors 2 – – – – 1 1 –Employees 2 – – – – – 2 –Safety and Health 11 3 – – – – 7 1

TOTALS 36 6 – – 1 3 23 3

9SONAE SIERRA Economic, Environmental and Social Report 2011

Our Company

Back to main contents

Sonae Sierra is the international shopping centre specialist that is passionate about bringing innovation and excitement to theshopping industry. Incorporated in Portugal in 1989, Sonae SGPS(Portugal) and Grosvenor (United Kingdom) each own 50% ofthe Company.

We have an integrated business which encompasses owning,developing and managing shopping centres as well as the provisionof services to third parties in markets as diverse as Europe, SouthAmerica and North Africa.

Our proactive approach to the business ensures that we have thenecessary capital required to maintain and market our shoppingcentres, attract new and innovative tenants and to increase ourcentres’ asset values. This strategy has allowed us to develop aunique know-how and has earned us international recognition forthe development of innovative products and delivery of high-quality property management services. This in turn has enabledus to develop our activity as a service provider to third parties.

On 31 December 2011 we were operating in Portugal, Spain, Italy, Germany, Greece, Romania, Morocco, Algeria, Colombiaand Brazil4. We were also providing services to third parties inCroatia. We owned 49 shopping centres with a total GrossLettable Area (GLA) of 1,924,117m2. We had five projectsunder construction, with a combined total GLA of 237,800m2,and six new projects in different phases of development inPortugal, Italy, Germany, Greece, Romania and Brazil. We alsomanaged and/or leased a further 22 shopping centres and twonew projects on behalf of others.

As a pioneer in the creation of themed shopping centres,Sonae Sierra remains a leader in the development of uniqueconcepts for exceptional shopping centres that offer greatexperiences and turn customers into fans. In 2011 our totalportfolio under management – including shopping centresowned by third parties – welcomed 428 million visits.

49 ownedshoppingcentres inoperation

8,495contracts with tenants

5 shopping centres under construction

operations in

3 continents

and 11 countries

1,090direct employeesworldwide

CORPORatE OvERvIEw

Who We Are… 1

CEO’s Statement 2

The Year at a Glance 4

Our Company 9

Our Business Strategy 15

4 Our countries of operation listed here include those where we have an established presence in the market and/or are actively pursuing new investment opportunities. We differentiate thesefrom those markets where we are merely providing services to third parties with no immediate prospects of direct investment or growth, e.g. Croatia. However, in the environmental andsocial performance sections of this report, we restrict our performance reporting to direct operations only; none of our third party service contracts are included in impact measurements.

22 contracts with thirdparties for the provisionof property managementand/or leasing services

10SONAE SIERRA Economic, Environmental and Social Report 2011

Our Company continued

Back to main contents

Our vision is to be the leading international shopping centre specialist.

Our mission is for Sonae Sierra to be the international shopping centre specialist that providesultimate shopping experiences to customers and creates outstanding value to shareholders,investors, tenants, communities and staff, while contributing to sustainable development.

Our vision and mission are underpinned by a set of core values and principles regarding ourbusiness culture, responsibility towards our staff, the environment and local communities where we operate and independence from political power.

To read about our values and principles see:http://www.sonaesierra.com/en-gb/aboutus/visionmissionandvalues.aspx

Further reference:

Plaza Mayor, SpainGli Orsi, Italy

Alexa, Germany

Centro Colombo, Portugal

CORPORATE OVERVIEW

Who We Are… 1

CEO’s Statement 2

The Year at a Glance 4

Our Company 9

Our Business Strategy 15

Sierra Investments

Sierra Funds

Sierra Developments

Sierra Management

Sonae Sierra Brasil

InvestmentDevelopmentManagement

SONAE SIERRA

Corporate Services

11SONAE SIERRA Economic, Environmental and Social Report 2011

Back to main contents

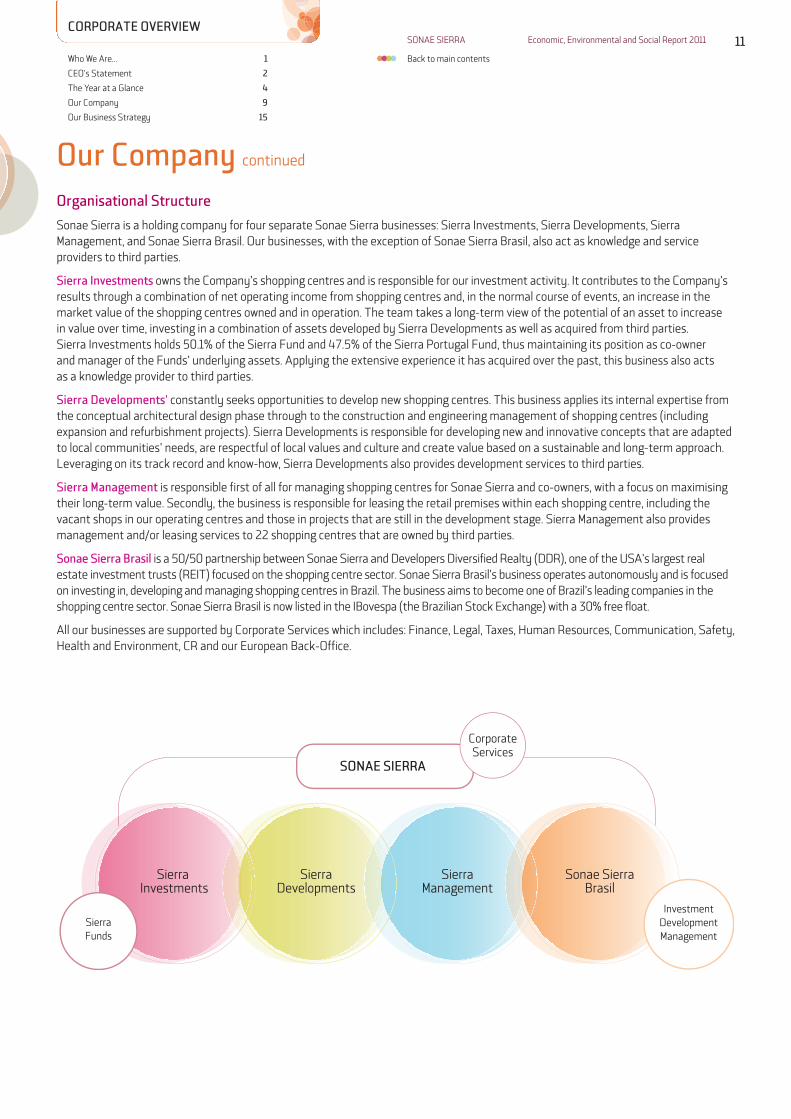

Organisational Structure

Sonae Sierra is a holding company for four separate Sonae Sierra businesses: Sierra Investments, Sierra Developments, SierraManagement, and Sonae Sierra Brasil. Our businesses, with the exception of Sonae Sierra Brasil, also act as knowledge and serviceproviders to third parties.

Sierra Investments owns the Company’s shopping centres and is responsible for our investment activity. It contributes to the Company’sresults through a combination of net operating income from shopping centres and, in the normal course of events, an increase in themarket value of the shopping centres owned and in operation. The team takes a long-term view of the potential of an asset to increasein value over time, investing in a combination of assets developed by Sierra Developments as well as acquired from third parties.Sierra Investments holds 50.1% of the Sierra Fund and 47.5% of the Sierra Portugal Fund, thus maintaining its position as co-ownerand manager of the Funds’ underlying assets. Applying the extensive experience it has acquired over the past, this business also actsas a knowledge provider to third parties.

Sierra Developments’ constantly seeks opportunities to develop new shopping centres. This business applies its internal expertise fromthe conceptual architectural design phase through to the construction and engineering management of shopping centres (includingexpansion and refurbishment projects). Sierra Developments is responsible for developing new and innovative concepts that are adaptedto local communities’ needs, are respectful of local values and culture and create value based on a sustainable and long-term approach.Leveraging on its track record and know-how, Sierra Developments also provides development services to third parties.

Sierra Management is responsible first of all for managing shopping centres for Sonae Sierra and co-owners, with a focus on maximisingtheir long-term value. Secondly, the business is responsible for leasing the retail premises within each shopping centre, including thevacant shops in our operating centres and those in projects that are still in the development stage. Sierra Management also providesmanagement and/or leasing services to 22 shopping centres that are owned by third parties.

Sonae Sierra Brasil is a 50/50 partnership between Sonae Sierra and Developers Diversified Realty (DDR), one of the USA’s largest realestate investment trusts (REIT) focused on the shopping centre sector. Sonae Sierra Brasil’s business operates autonomously and is focusedon investing in, developing and managing shopping centres in Brazil. The business aims to become one of Brazil’s leading companies in theshopping centre sector. Sonae Sierra Brasil is now listed in the IBovespa (the Brazilian Stock Exchange) with a 30% free float.

All our businesses are supported by Corporate Services which includes: Finance, Legal, Taxes, Human Resources, Communication, Safety,Health and Environment, CR and our European Back-Office.

CORPORatE OvERvIEw

Our Company continued

Who We Are… 1

CEO’s Statement 2

The Year at a Glance 4

Our Company 9

Our Business Strategy 15

Key facts by country(as on 31 December 2011)

12SONAE SIERRA Economic, Environmental and Social Report 2011

Back to main contents

Where We Operate

Our strong partnership policy, both with international investors and local partners, provides the financial backing and market intelligencenecessary to successfully develop new business in new geographies. Currently we are present in Portugal, Spain, Italy, Germany, Greece,Romania, Morocco, Algeria, Brazil and Colombia. We are also providing services to third-parties in Croatia.

Italy

Germany

Romania

Croatia

Greece

Algeria

Brazil

Spain

Portugal

MoroccoColombia

Portugal Spain Italy Germany Greece Romania Brazil Total

Number of shopping centres owned5 21 9 4 3 1 1 10 49

GLA of owned shopping centres (m2)6 806,841 415,650 146,308 149,289 21,058 11,555 373,416 1,924,117

Number of shopping centres managed 12 4 1 2 – 1 – 20on behalf of other owners

GLA of shopping centres managed 126,830 130,810 21,765 26,506 – 3,634 – 309,545on behalf of other owners (m2)

Visits to owned shopping centres (millions) 176.0 61.6 18.9 32.6 1.6 3.2 102.5 396.3

Visits to all shopping centres 184.9 73.9 22.1 38.1 1.6 4.8 102.5 428.0under management (millions)7

Rents received at all shopping centres 191.9 64.9 25.5 46.2 1.6 1.6 102.1 433.8under management (€ million)8

Tenant sales at owned 2,010.1 676.3 284.9 480.4 14.7 10.3 1,709.3 5,186.0shopping centres (€ million)9

Tenant sales at all shopping centres 2,170.9 839.6 309.6 501.0 14.8 16.8 1,709.3 5,562.0under management (€ million)

Costs by country (€ million)10 95.6 18.9 13.5 12.1 6.7 1.7 18.4 170.6

Number of direct employees11 409 111 55 50 17 30 413 1,090

CORPORATE OVERVIEW

Our Company continued

Who We Are… 1

CEO’s Statement 2

The Year at a Glance 4

Our Company 9

Our Business Strategy 15

Key

Countries where we are present

Other countries where we areproviding services to third parties

5 These figures cover shopping centres that are 100% and co-owned by Sonae Sierra.6 GLA figures are periodically confirmed by technical specialists, sometimes leading to adjustments of these figures with respect to individual shopping centres.7 These figures cover the total number of visits welcomed by all Sonae Sierra owned shopping centres and shopping centres managed on behalf of other owners.8 Rents have been calculated based on account performance between 1 January 2011 and 31 December 2011.9 These figures do not include sales achieved by tenant owners (those who own individual units in our centres). These figures have been calculated based on account performance

between 1 January 2011 and 31 December 2011.10 Costs by country include costs associated with external suppliers and services, costs with common charges, buy out costs and other operating expenses. The Netherlands is not

included as a ‘country’ in this table, although it is within the value of total costs. Costs by country have been calculated based on account performance between 1 January 2011 and31 December 2011.

11 Sonae Sierra also has three employees based in The Netherlands, one employee based in Colombia and one employee based in Algeria. These five employees are included in thetotal number of employees reported in the end column of this table.

13SONAE SIERRA Economic, Environmental and Social Report 2011

Our Company continued

Back to main contents

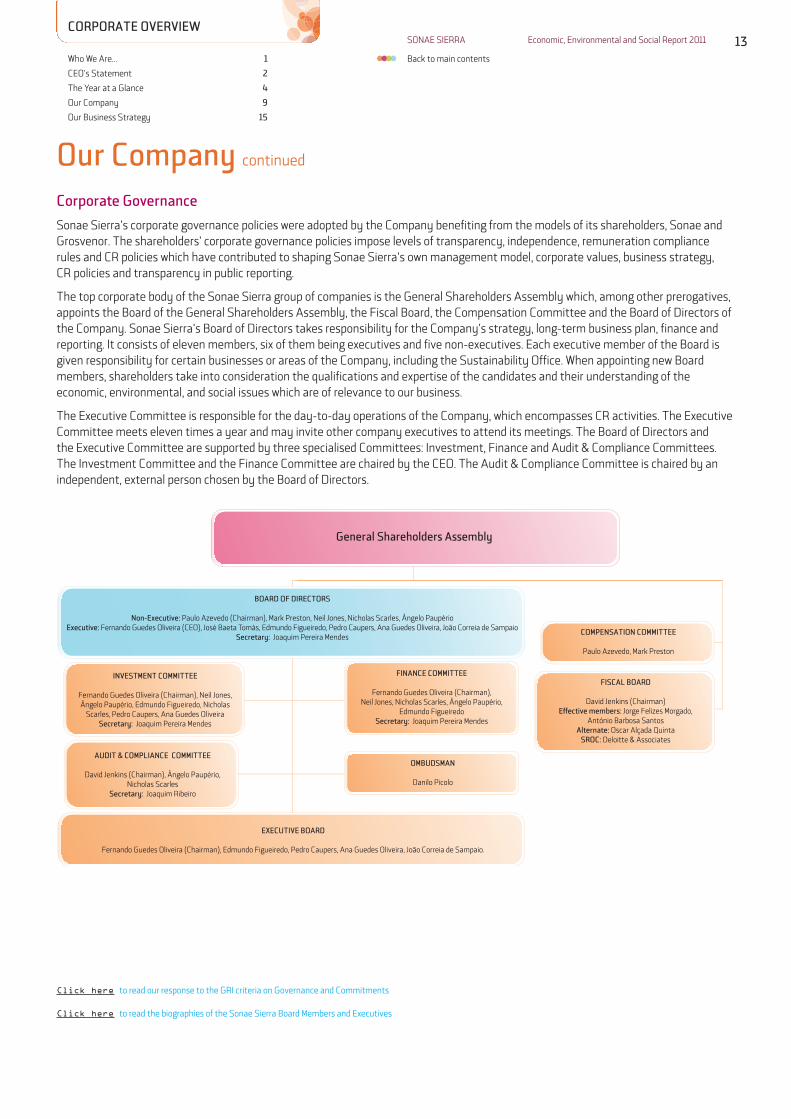

Corporate Governance

Sonae Sierra’s corporate governance policies were adopted by the Company benefiting from the models of its shareholders, Sonae andGrosvenor. The shareholders’ corporate governance policies impose levels of transparency, independence, remuneration compliancerules and CR policies which have contributed to shaping Sonae Sierra’s own management model, corporate values, business strategy, CR policies and transparency in public reporting.

The top corporate body of the Sonae Sierra group of companies is the General Shareholders Assembly which, among other prerogatives,appoints the Board of the General Shareholders Assembly, the Fiscal Board, the Compensation Committee and the Board of Directors ofthe Company. Sonae Sierra’s Board of Directors takes responsibility for the Company’s strategy, long-term business plan, finance andreporting. It consists of eleven members, six of them being executives and five non-executives. Each executive member of the Board isgiven responsibility for certain businesses or areas of the Company, including the Sustainability Office. When appointing new Boardmembers, shareholders take into consideration the qualifications and expertise of the candidates and their understanding of theeconomic, environmental, and social issues which are of relevance to our business.

The Executive Committee is responsible for the day-to-day operations of the Company, which encompasses CR activities. The ExecutiveCommittee meets eleven times a year and may invite other company executives to attend its meetings. The Board of Directors and the Executive Committee are supported by three specialised Committees: Investment, Finance and Audit & Compliance Committees.The Investment Committee and the Finance Committee are chaired by the CEO. The Audit & Compliance Committee is chaired by anindependent, external person chosen by the Board of Directors.

CORPORatE OvERvIEw

Who We Are… 1

CEO’s Statement 2

The Year at a Glance 4

Our Company 9

Our Business Strategy 15

General Shareholders Assembly

AUDIT & COMPLIANCE COMMITTEE

David Jenkins (Chairman), Ângelo Paupério, Nicholas Scarles

Secretary: Joaquim Ribeiro

BOARD OF DIRECTORS

Non-Executive: Paulo Azevedo (Chairman), Mark Preston, Neil Jones, Nicholas Scarles, Ângelo PaupérioExecutive: Fernando Guedes Oliveira (CEO), José Baeta Tomás, Edmundo Figueiredo, Pedro Caupers, Ana Guedes Oliveira, João Correia de Sampaio

Secretary: Joaquim Pereira Mendes

INVESTMENT COMMITTEE

Fernando Guedes Oliveira (Chairman), Neil Jones, Ângelo Paupério, Edmundo Figueiredo, Nicholas

Scarles, Pedro Caupers, Ana Guedes OliveiraSecretary: Joaquim Pereira Mendes

OMBUDSMAN

Danilo Picolo

FINANCE COMMITTEE

Fernando Guedes Oliveira (Chairman),Neil Jones, Nicholas Scarles, Ângelo Paupério,

Edmundo FigueiredoSecretary: Joaquim Pereira Mendes

EXECUTIVE BOARD

Fernando Guedes Oliveira (Chairman), Edmundo Figueiredo, Pedro Caupers, Ana Guedes Oliveira, João Correia de Sampaio.

FISCAL BOARD

David Jenkins (Chairman)Effective members: Jorge Felizes Morgado,

António Barbosa SantosAlternate: Oscar Alçada Quinta

SROC: Deloitte & Associates

COMPENSATION COMMITTEE

Paulo Azevedo, Mark Preston

Click here to read our response to the GRI criteria on Governance and Commitments

Click here to read the biographies of the Sonae Sierra Board Members and Executives

14SONAE SIERRA Economic, Environmental and Social Report 2011

Our Company continued

Back to main contents

CORPORatE OvERvIEw

Who We Are… 1

CEO’s Statement 2

The Year at a Glance 4

Our Company 9

Our Business Strategy 15

Corporate Governance (continued)

Our Code of Conduct includes a set of ethical principles which apply to everything we do and outline our commitment to success whilstoperating with integrity, openness and honesty. The Code also promotes ethical and responsible decision-making by providing guidanceon dealing with issues such as bribery, corruption, legal compliance, equality and human rights. Whilst the Executive Committee isultimately responsible for managing these issues, ethical conduct is a personal responsibility and every employee is held accountable forhis or her behaviour. The Sierra Ombudsman promotes compliance with our Code of Conduct and encourages behaviour aligned with ourethical principles. The Ombudsman is an independent facilitator to whom all stakeholders can present their complaints with assurancethat they will be processed, investigated, and responded to in a timely and sensitive manner.

Click here to read our response to the GRI criteria on Corruption, Anti-Competitive Behaviour and Compliance

Click here to read our response to the GRI criteria on Human Rights

our code of conduct includes a set of ethicalprinciples which apply to everything we do andoutline our commitment to success whilst operating

with integrity,

opennessand honesty

15SONAE SIERRA Economic, Environmental and Social Report 2011

Our Business Strategy

Back to main contents

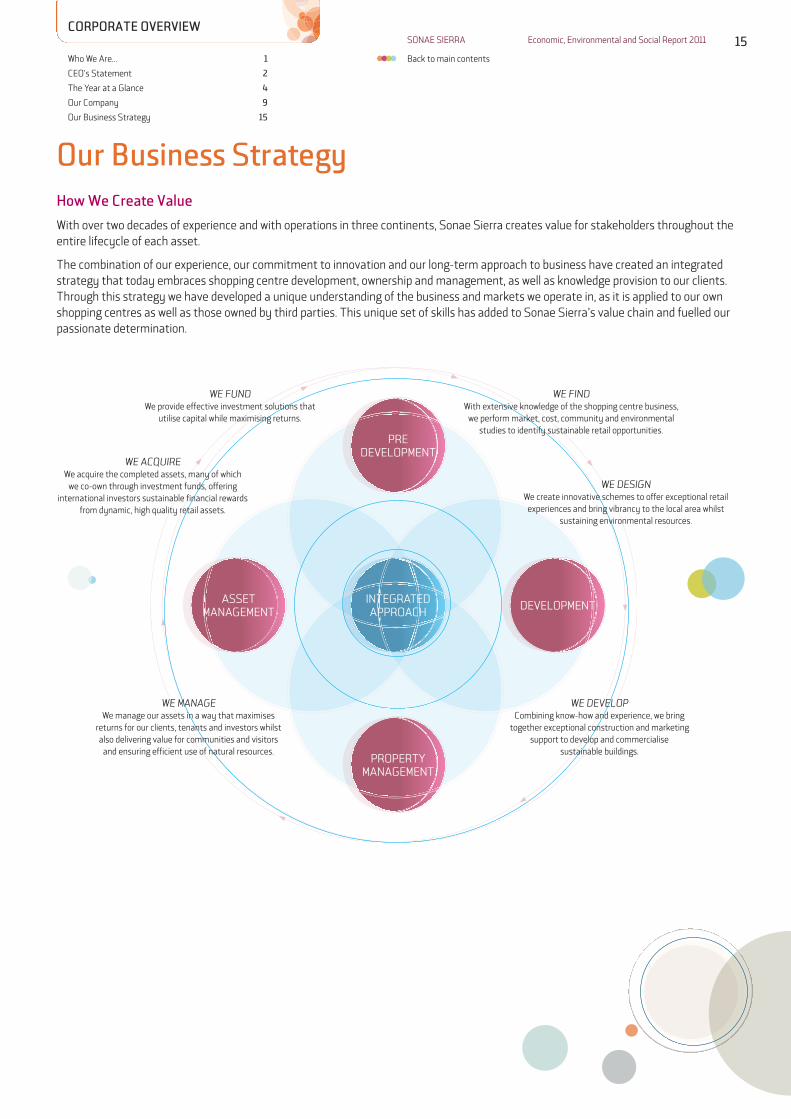

How we Create value

With over two decades of experience and with operations in three continents, Sonae Sierra creates value for stakeholders throughout theentire lifecycle of each asset.

The combination of our experience, our commitment to innovation and our long-term approach to business have created an integratedstrategy that today embraces shopping centre development, ownership and management, as well as knowledge provision to our clients.Through this strategy we have developed a unique understanding of the business and markets we operate in, as it is applied to our ownshopping centres as well as those owned by third parties. This unique set of skills has added to Sonae Sierra’s value chain and fuelled ourpassionate determination.

CORPORatE OvERvIEw

Who We Are… 1

CEO’s Statement 2

The Year at a Glance 4

Our Company 9

Our Business Strategy 15

INTEGRATED APPROACH DEVELOPMENT

PROPERTY MANAGEMENT

ASSETMANAGEMENT

PRE DEVELOPMENT

wE mANAgEWe manage our assets in a way that maximises

returns for our clients, tenants and investors whilstalso delivering value for communities and visitors

and ensuring efficient use of natural resources.

wE AcQuIREWe acquire the completed assets, many of which

we co-own through investment funds, offeringinternational investors sustainable financial rewards

from dynamic, high quality retail assets.

wE fuNdWe provide effective investment solutions that

utilise capital while maximising returns.

wE fINdWith extensive knowledge of the shopping centre business,

we perform market, cost, community and environmentalstudies to identify sustainable retail opportunities.

wE dESIgNWe create innovative schemes to offer exceptional retail

experiences and bring vibrancy to the local area whilstsustaining environmental resources.

wE dEvElopCombining know-how and experience, we bring

together exceptional construction and marketingsupport to develop and commercialise

sustainable buildings.

16SONAE SIERRA Economic, Environmental and Social Report 2011

Our Business Strategy continued

Back to main contents

Our RelationshipsOur stakeholders

We believe that conducting our activities in a way that is sensitive and responsive to our stakeholders’ needs and concerns is vital for thelong-term success of our business. We employ a range of stakeholder engagement techniques and receive valuable feedback from ourinvestors, tenants, clients, visitors, employees, suppliers and from local community members which can help us to refine our approach ata corporate level as well as allow us to identify and implement improvements on individual sites. The diagram below highlights our mainstakeholder groups and examples of engagement and/or feedback received in 2011.

Click here to read about the stakeholder engagement techniques we employed in 2011 and key feedback received

More detailed commentary on feedback received from stakeholders in 2011 and the ways in which we responded to this feedback can befound in the Suppliers, Tenants, Communities and Visitors and Employees chapters of this report.

CORPORATE OVERVIEW

Who We Are… 1

CEO’s Statement 2

The Year at a Glance 4

Our Company 9

Our Business Strategy 15

CLIENTSINVESTORS

&FINANCIERS

THE MEDIA

SHOPPING CENTRE

VISITORS

LOCAL AUTHORITIES EMPLOYEES

LOCAL COMMUNITY

MEMBERSSUPPLIERS

TENANTS

OUR STAKEHOLDERS

98% of our shopping centres achieved a tenant satisfaction

rating of 4 or above on ascale of 1 (‘not satisfied’)

to 6 (‘very satisfied’)

We have received some

positive feedback from our property

management services’ clients

12% of visitors say that a company’s

environmental and social track record influences which shopping centre

they visit and 23% say it influences what they buy

83% of staff responding to our Employee

satisfaction survey agreed

that Sonae Sierra is a good company

to work for

Property management suppliers’ audits

showed good team work

and organisation but knowledge of

our safety procedures could be improved

CommunityAdvisory Panels were held across

29 of our shoppingcentres and new projects in 2011, giving us useful

insights on community perspectives

We engaged with local authorities

during the shopping centre

planning, development and operations phases

We received 5,082 cases of press coverage

covering economic, environmental and

social aspects ofour performance,

96% were positive or neutral

We were invited by one investor to

participate in the Global Real Estate

Sustainability Benchmark (GRESB),

and as a result our funds were ranked

as the most sustainable in Europe

17SONAE SIERRA Economic, Environmental and Social Report 2011

Our Business Strategy continued

Back to main contents

Our Partnerships & Clients – past and present

When it comes to shopping centres, we’re the partner of choice. Our business, quite simply, would not be what it is today without ourpartners ( ) and services clients ( ). With their backing, we can ensure we have financial strength, and also the ability to quickly gain anin-depth knowledge of markets, and create new opportunities.

P C

CORPORATE OVERVIEW

Who We Are… 1

CEO’s Statement 2

The Year at a Glance 4

Our Company 9

Our Business Strategy 15

PORTUGALEstevão NevesBensaude GroupSonae DistribuiçãoEstação ShoppingCGD

P

P

P

P

P

BRAZILMultiplanTivoli EPEnplanta EngenhariaMarco ZeroCredit Suisse HG

P

P

P

P

P

UNITED KINGDOMGrosvenor Fund ManagementMiller DevelopmentsRockspringCastle CitySchroders Investment ManagementAberdeen Property InvestorsScottish Widows

P

P

P

P

P

P

C

FRANCECNP AssuranceCDCFoncière Euris

P

P

P

THE NETHERLANDSING Real EstateING DevelopmentsAPG InvestmentsMAB Development

P

P

P

P

GERMANYDekaUnion InvestmentCommerzbankBalsa

P

P

C

C

SPAINLAR GroupMall GroupIberdrolaEroski GroupBanco Santander

P

P

P

C

P

USAAIGTIAA-CREFDDR

P

P

P

GREECECharagionis GroupLamda Development

P

P

MOROCCOMarjaneFonciere Chellah (CDG Group)AUDA – Agence d’urbanisation etde Developpement d’Auda

C

C

C

ITALYCoimpredilP

FINLANDKEVAIlmarinen

P

P

ALGERIACévital GroupP

COLOMBIACentral ControlP

GREECE / CROATIA Bluehouse CapitalC

18SONAE SIERRA Economic, Environmental and Social Report 2011

Back to main contents

CORPORatE OvERvIEw

Our Medium- to Long-term Strategy

Research into social, consumer and technological trends suggests that we are likely to see a rapid transformation in the global retailindustry over the next decade brought about by the fast-growing use of mobile internet devices, demographic changes; shiftingconsumer behaviour and preferences and growing segmentation between different customer groups. To succeed in this new era of retail,we will need to continue focusing on the ultimate experience of retail customers, and we aim to improve this by offering premium spaceand unique shopping centre concepts which remain a destination of choice for visitors.

Our business strategy to achieve this is very clear. We continue to focus our attention on the five strategic axes that we identified aspriorities in 2010.

• Maintain and enhance our shopping centre specialism, continuing to integrate our investment, development and propertymanagement business, and focusing on the highest quality product available in any given market. As part of this we will continue topursue the delivery of property management services to third parties.

• Continue to pursue international growth and to enter new and emerging markets where the retail industry is still evolving andconsumer purchasing power is increasing. We expect to see further growth in our operations in the Mediterranean Basin and LatinAmerica and to expand further in other emerging markets, based on third party services.

• Improve our capital intelligence, by further developing our capital raising capabilities and pursuing our capital light approach. Thisincludes the delivery of third party services and taking minority shareholding positions in new joint venture partnerships. We alsoanticipate reducing our capital involvement, and in some cases disposing of non-core operational centres in established markets, tofree up capital to finance our development pipeline in growth markets.

• Create the ultimate shopping centre experience by developing innovative shopping centre concepts that bring together the righttenant mix, architecture, ambience, services and customer experience. Our ultimate aim is to become the destination of choice and toprovide customers with a venue where their needs, aspirations, desires and expectations come together. For us, each one of ourcentres is more than a building: it is a living space in continuous evolution. As a company we will continue to focus progressively onprime assets and team up with key tenants and selected partners from other industries to develop new and exciting customerexperiences, in line with consumer trends.

• Undertake dynamic portfolio management allowing us to shift the weighting of our portfolio. For mature markets, this means we arelikely to see the sale of more properties and a reduction in our fund stakes; whilst emerging markets and geographical areas withgrowth potential will gain weight in Sonae Sierra’s portfolio.

We are aware that the negative economic cycle we are presently experiencing brings with it important challenges, but we are confident inour ability to execute the defined strategy and, with rigour, efficiency and determination, to overcome those challenges.

Our Business Strategy continued

Who We Are… 1

CEO’s Statement 2

The Year at a Glance 4

Our Company 9

Our Business Strategy 15

19SONAE SIERRA Economic, Environmental and Social Report 2011

Back to main contents

CORPORatE OvERvIEw

Our Business Strategy continued

Who We Are… 1

CEO’s Statement 2

The Year at a Glance 4

Our Company 9

Our Business Strategy 15

Risk Management

We operate a Risk Management Working Group to serve as facilitator and promoter of risk management best practices in all parts of theCompany. The Working Group gathers information and reports on the risks that the Company is facing or may face in the future andreports, via the CFO, to the Audit and Compliance Committee of the Company. In this context, the Risk Management Working Group mayfoster initiatives to improve the Company’s risk management information systems.

In 2011 we reviewed our risk matrix and added two new risks (environmental and services provision risks) whilst the emphasis on someindividual risks has changed due to the wider economic context. The Working Group analysed three risks in detail (sovereign and politicalrisks, contract integrity and rents sustainability) and established a policy, monitoring procedures and mitigation actions for each one.Other activities included the development of a policy for Medium-term Liquidity Management and the commencement of the BEST12

training programme for Sonae Sierra employees on the Anti-Corruption Policy. Our Risk Management targets for 2012 are to update andapprove the Sonae Sierra Risk Matrix and to deliver training on the Company's anti-corruption policy.

The table below presents a summary of our key controllable and non-controllable financial risks and mitigation strategies.

12 BEST stands for ‘Behaviour with Ethics Sierra Training’.

Key controllable risks

Risks

tenant Default Risk: The trading environment has been toughfor tenants in Portugal, Spain and Greece and it has beenincreasingly difficult for us to collect rents in some areas inthese countries. There are also potential risks in Italy.

vacancy Risk: With many tenants facing financial challenges in some markets, we are at risk of having higher vacancy rates.

Mitigation strategy

Our approach to property management has always involved closescrutiny of our tenants’ business performance. Over the past twoyears we have increased the efficiency of our property managementin order to reduce service charges and have negotiated temporaryrental discounts with some tenants. We have also intensified ourefforts to increase footfall in shopping centres through ourmarketing and events programmes. Our geographical spread, and inparticular our current presence in the Brazilian market reduces theimpact that individual tenant default can have on our business.

Key non-controllable risks

Risks

Property valuations Risk: Property valuations are affected bythe prevailing conditions in the property investment marketand the macro economic climate in general, and this impactson our indirect results. Increased yields in many Europeanmarkets have been adversely impacting on property values.

Liquidity Risk: The lack of availability of bank debt in Europeat present constrains our ability to finance new developmentsand refinance loans which are maturing.

Interest Rate Risk: Interest charged on borrowings canconstitute a significant cost for our business.

Exchange Rate Risk: Brazil is the main market where SonaeSierra is exposed to exchange rate risk.

Mitigation strategy

As a counter-measure to mitigate the adverse effects of yield shiftson asset value, we have focused on increasing the operationalefficiency of our shopping centres and introducing tighter assetmanagement controls.

Our capital recycling approach helps us to offset the lack ofavailable bank debt, the intention being to dispose of or refinanceassets in mature markets so as to fund new development activityin rapidly growing economies. We maintain our loan to value ratioat prudent levels (below 43.7%).

Our debt is quite long-term, relatively evenly spread throughout theyears with almost 60% of it being repayable after 2015 only.

We have mitigated exchange rate risk in Brazil through two actions:the Initial Public Offering (IPO) of Sonae Sierra Brasil and using localdebt to finance not only our developments but also some of ouroperational shopping centres in this country. Sonae Sierra Brasil isa 50/50 joint venture with DDR, and this partnership arrangementalso decreases our share of this risk.

20SONAE SIERRA Economic, Environmental and Social Report 2011

Our Business Strategy continued

Back to main contents

CORPORatE OvERvIEw

Who We Are… 1

CEO’s Statement 2

The Year at a Glance 4

Our Company 9

Our Business Strategy 15

Risk Management (continued)

As a separate but related exercise, Sonae Sierra continues to review the relative materiality of individual environmental and socialimpact areas in terms of both the risk and opportunity that they might represent to the business. We have used a standard riskmanagement framework to evaluate environmental and social issues according to their likelihood/frequency of occurrence and the scaleof impact should the issue arise13. The findings of our latest assessment conducted in 2011 are summarised in the table below. The mainimpact areas identified through this assessment form the basis of our CR strategy and are focused on in detail in the Environmental andSocial Performance chapters of this report.

13 In 2009 and in 2010, a single score from 1 to 5 (very low to high) was allocated to each issue based on an assessment of its likelihood/frequency of occurrence, with reference tolikelihood/ frequency categories used by standard risk management frameworks. The ‘impact’ of each issue was assessed using a weighted average score of five factors which were based on AccountAbility’s five materiality tests established in ‘The Materiality Report – Aligning Strategy, Performance & Reporting’; Maya Forstater, Simon Zadek et al.,AccountAbility, BT Group plc & LRQA, 2006. The CR risk matrix which was developed as a result of this analysis is presented on page 110.

14 According to a pilot study commissioned on two of our assets in Portugal. See page 56 for further details.

l Energy and Climate – Greenhouse gas emissions minimisation; efficient energyuse; sustainable energy supply; climate change adaptation

Risks

• Non-compliance with more stringent regulations which haveemerged under the European Union’s (EU) Energy Performanceof Buildings Directive.

• Increased demand for energy and anticipated increase in energycosts could reduce profitability by 2% - 5% maximum in 203014.

Opportunities

• Avoid costs and reduce environmental impact (€7.3 million costsavoided in 2011 due to energy efficiency measures implemented inshopping centres between 2002 and 2011).

• Achieved recognition through awards, rankings and indices.

• Increase competitiveness and sustain assets’ value by increasingenergy efficiency and/or generating energy on site.

s water – Sustainable water supply; water efficiency and avoiding water pollution

Risks

• Fines can be incurred for non-compliance with local wastewaterregulations.

• Increase in water costs could reduce profitability by between0.15% and 2% maximum in 2030.

Opportunities

• Avoid costs and reduce environmental impact (€0.8 million costs avoided in 2011 due to water efficiency measures implemented inshopping centres between 2003 and 2011).

• Contribute to the recognition of Sonae Sierra as a ‘responsible’ company.

• Increase competitiveness and sustain assets’ value by increasing waterefficiency and/or reusing water on site.

t waste – Increasing recycling and reducing waste sent to landfill

Risks

• Non-compliance with waste management regulations, includingon construction sites.

Opportunities

• Avoid costs and reduce environmental impact (€0.6 million costs saved in 2011 due to the increase in the proportion of waste recycled at shopping centres between 2002 and 2011).

• Contribute to the recognition of Sonae Sierra as a ‘responsible’ company.

• Be prepared for more stringent regulations which could be introduced in the future.

n Biodiversity and Habitats – Reducing negative impacts on biodiversity and enhancing it where possible

Risks

• Non-compliance with EU and local legislation on biodiversity.

Opportunities

• Integrate biodiversity on sites (such as green features that providenatural habitats) to demonstrate commitment; this also may result invisitors staying longer.

• Biodiversity impacts in the supply chain could lead to commodity priceincreases, e.g., impact of deforestation on timber prices in China.

21SONAE SIERRA Economic, Environmental and Social Report 2011

Back to main contents

Our Business Strategy continued

CORPORATE OVERVIEW

Who We Are… 1

CEO’s Statement 2

The Year at a Glance 4

Our Company 9

Our Business Strategy 15

l Suppliers – Environmental and social practices along our supply chain

Risks

• Fines/ reputational damage if contractors do not comply withregulations.

• Ineffective delivery of suppliers’ services in shopping centrescan reduce tenant and visitor satisfaction.

• Some supplier businesses may be impacted by commodityprice increases.

Opportunities

• Reduce costs through greater efficiencies in the supply chain.

n Tenants – Increasing tenant satisfaction; engaging with tenants on CR issues

Risks

• Higher void rates leading to lower profitability.

• Not meeting tenants’ expectations in the long-term if/when CR issues become more important.

Opportunities

• Maintain tenant satisfaction (68% of our tenants say CR is animportant factor that contributes to their overall satisfaction).

• Maintain high occupancy rates and rental income.

l Communities and Visitors – Impact on local communities; community engagement and visitor satisfaction

Risks

• Inability to obtain planning permission if cannot demonstrateadded value to local communities.

• Lack of buy-in from local community could reduce footfall.

• Lack of attentiveness to visitors’ needs in the long-termdecreases appeal and competitiveness of the centre.

Opportunities

• Maintain good community relations; this is likely to result in higherfootfall and sales.

• Enhance our brand through projects that demonstrate 'corporatecitizenship' (e.g., Volunteering Day, CR campaigns, educational projects).

• Contribute to sustaining high footfall and sales by being attentive tochanging visitor preferences.

l Employees – Employee satisfaction and retention; equal opportunities and diversity; talent management

Risks

• Non-compliance with regulations on gender equality and non-discrimination.

• Costs associated with employee turnover.

Opportunities

• Increase staff motivation and retention through progressive policiessuch as offering flexible work arrangements.

• Increase competitiveness by retaining talented employees (theestimated value of innovations implemented by Sonae Sierra as aresult of employees’ suggestions is €6.9 million).

l Safety and Health – Safety and health of the workforce; construction site and shopping centre safety

Risks

• Non-compliance with EU and national S&H regulations.

• Fines associated with accidents; delays on construction projects.

• Strong stakeholder expectations in relation to this issue, as seriousaccidents/ fatalities on sites can damage reputation.

Opportunities

• Reduce insurance costs.

• Future-proof assets (buildings need to comply with ever-tighteningS&H regulations).

• Enhance reputation through awards and recognition by stakeholdersfor proactive attitude.

More detailed information about how we manage our environmental and social risks and maximise value generating opportunities isprovided in the Environmental and Social sections of this report.

Risk Management (continued)

22SONAE SIERRA Economic, Environmental and Social Report 2011

Back to main contents

Our Business Strategy continued

CORPORatE OvERvIEw

Who We Are… 1

CEO’s Statement 2

The Year at a Glance 4

Our Company 9

Our Business Strategy 15

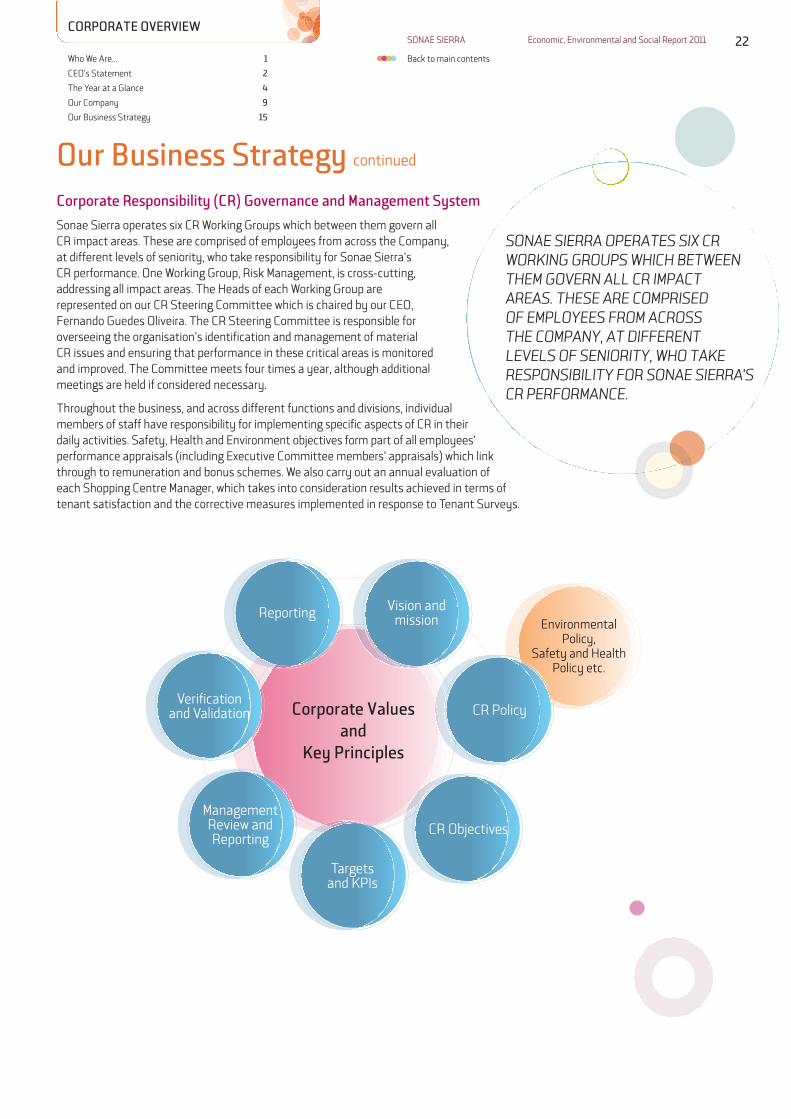

Corporate Responsibility (CR) Governance and Management System

Sonae Sierra operates six CR Working Groups which between them govern allCR impact areas. These are comprised of employees from across the Company,at different levels of seniority, who take responsibility for Sonae Sierra’sCR performance. One Working Group, Risk Management, is cross-cutting,addressing all impact areas. The Heads of each Working Group arerepresented on our CR Steering Committee which is chaired by our CEO,Fernando Guedes Oliveira. The CR Steering Committee is responsible foroverseeing the organisation’s identification and management of materialCR issues and ensuring that performance in these critical areas is monitoredand improved. The Committee meets four times a year, although additionalmeetings are held if considered necessary.

Throughout the business, and across different functions and divisions, individualmembers of staff have responsibility for implementing specific aspects of CR in theirdaily activities. Safety, Health and Environment objectives form part of all employees’performance appraisals (including Executive Committee members’ appraisals) which linkthrough to remuneration and bonus schemes. We also carry out an annual evaluation ofeach Shopping Centre Manager, which takes into consideration results achieved in terms oftenant satisfaction and the corrective measures implemented in response to Tenant Surveys.

EnvironmentalPolicy,

Safety and HealthPolicy etc.

Corporate Values and

Key Principles

Verification and Validation

Reporting Vision andmission

CR Policy

Targetsand KPIs

ManagementReview andReporting

CR Objectives

SoNAE SIERRA opERAtES SIx cRwoRkINg gRoupS whIch bEtwEENthEm govERN All cR ImpActAREAS. thESE ARE compRISEdof EmployEES fRom AcRoSSthE compANy, At dIffERENtlEvElS of SENIoRIty, who tAkERESpoNSIbIlIty foR SoNAE SIERRA’ScR pERfoRmANcE.

Our Business Strategy continued

CORPORatE OvERvIEw

Who We Are… 1

CEO’s Statement 2

The Year at a Glance 4

Our Company 9

Our Business Strategy 15

Corporate Responsibility (CR) Governance and Management System (continued)

We operate a CR Management System in order to monitor our performance and improve it on an on-going basis across all the identifiedimpact areas. The values and principles embodied in our vision are developed into policies and strategies which allow us to translate ourcommitments into practical actions. We track and evaluate our progress against key performance indicators and targets on an annualbasis to ensure that we achieve our long-term objectives.

23SONAE SIERRA Economic, Environmental and Social Report 2011

Back to main contents

EnvironmentWorking Group

Energy and Climate

EmployeesWorking Group

Employees

Communities and Visitors

Working Group

Communitiesand Visitors

Safety and Health Working Group

Safety and Health

Water

Business Chain Working Group

Suppliers

Tenants

Waste

Biodiversityand Habitats

Risk Management

All NINE IMPACT AREAS

EXECUTIVE COMMITTEE OF SONAE SIERRA

CORPORATE RESPONSIBILITY STEERING COMMITTEE

24SONAE SIERRA Economic, Environmental and Social Report 2011

Back to main contents

Our Business Strategy continued

CORPORatE OvERvIEw

Who We Are… 1

CEO’s Statement 2

The Year at a Glance 4

Our Company 9

Our Business Strategy 15

Safety, Health and Environment Management System

Our Company first developed an Environmental Management System (EMS) in 1999 and in 2005 we were the first company in our sectorin Europe to obtain ISO 14001 certification for our corporate EMS, which covered all our business activities. In 2004, we launched ourSafety and Health (S&H) Policy and in 2008 became the first company in Europe to achieve OHSAS 18001 certification for our corporateS&H Management System. In 2010, we began working on the integration of these two management systems with an aim to exploit thesynergies between them and increase our operational efficiency. In 2011 our integrated Safety, Health and Environment ManagementSystem (SHEMS) became fully operational. It is based on the international standards ISO 14001:2004 and OHSAS 18001:2007 and wasrecertified by Lloyds Quality Register Assurance according to both of these standards in 2011. The SHEMS covers all of our businessactivities (development, investment and property management) and all assets which we own or occupy (shopping centres in developmentand in operation and our corporate offices), in all the countries where we operate.

During the New Business phase of our projects, Environmental Due Diligence andan Environmental Impact Study are developed so that we can understand thepotential environmental liabilities that sites may contain (such as contaminatedland or materials) and therefore guarantee sufficient budget in our InvestmentPlans to adequately deal with these issues. Environmental Due Diligence isalso implemented upon the acquisition of existing shopping centres. It isreinforced by the execution of S&H Due Diligence, which complements theTechnical Due Diligence recommendations and provides Sonae Sierra withinformation on the capability of the existing shopping centre’s systemsto perform according to Sonae Sierra’s expectations.

Policy: S&H, EnvironmentReview by the Management

Checking and Corrective Actions

• Monitoring and measurement• Conformity evaluation• Incident investigation• Non conformities, Corrective and Preventive Actions• Records control• Internal Audits

Planning

• Assessment and control of S&H Risks and Environmental Impacts• Legal requirements and others • Objectives and Targets Program

Continuous Improvement

Implementing and Operating

• Resources, Roles, Responsibility, Accountability and Authority• Competence, training and awareness• Communication, Participation and Consultation• Documents control• Operational control• Emergency Preparedness and response

IN 2011 ouR INtEgRAtEd SAfEty,hEAlth ANd ENvIRoNmENtmANAgEmENt SyStEm (ShEmS) bEcAmEfully opERAtIoNAl. It IS bASEd oNthE INtERNAtIoNAl StANdARdSISo 14001:2004 ANd ohSAS 18001:2007ANd wAS REcERtIfIEd by lloydSQuAlIty REgIStER ASSuRANcEAccoRdINg to both of thESEStANdARdS IN 2011.

25SONAE SIERRA Economic, Environmental and Social Report 2011

Back to main contents

Our Business Strategy continued

CORPORatE OvERvIEw

Who We Are… 1

CEO’s Statement 2

The Year at a Glance 4

Our Company 9

Our Business Strategy 15

Safety, Health and Environment Management System (continued)

During the design stage, we have introduced a ‘sustainable shopping centre’ concept, which is achieved through the implementation ofour Safety, Health and Environment Development Standards (SHEDS). The SHEDS consist of 179 standards based on our experience,best available techniques and certification schemes such as LEED® and BREEAM as well as international safety standards. The SHEDSencompass the environmental standards which were previously known as the ESRD (Environmental Standards for Retail Development)prior to the integration of our Environmental and S&H Management Systems. The issues addressed by the SHEDS include:

• Energy • Health and well-being • Site safety conditions

• Water • Land and ecology • Emergency response

• Waste • Fire prevention • Hazardous products

• Transport • Electrical risks • Security

The SHEDS are revised periodically to ensure that they are kept up to date. All new development projects, major expansions andrefurbishments15 are required to achieve 100% compliance with the ‘critical’ SHEDS standards, a threshold which would allow them toachieve a BREEAM ‘Good’ certification. Shopping Metrópole, the expansion project which we inaugurated in Brazil in 2011, introducedmeasures such as minimising the power of lighting in the mall, food-court and car park areas and controlling these areas remotelythrough a Building Management System (BMS), as well as installing energy efficient conveyors and escalators.

Each of our projects under development and all of our operational shopping centres are required to have a specific SHEMS manual inplace to ensure that risks and characteristics unique to each site are managed adequately16. As of 31 December 2011, ISO 14001certifications had been achieved in 90% of our shopping centres in operation and OHSAS 18001 certification had been achieved in 55%.With regards to the development of new shopping centres, since 2004, 23 Sonae Sierra construction sites have achieved ISO 14001certification and four have achieved OHSAS 18001 certification, the most recent being Le Terrazze in Italy, which became the firstshopping centre in the world to achieve joint ISO 14001 and OHSAS 18001 certifications for the SHEMS of its construction works, andUberlândia Shopping in Brazil, which was the second shopping centre to achieve both certifications.

We recognise that creating sustainable buildings does not end once the development has been completed. We monitor the performanceof new shopping centres with respect to energy; water; waste and safety, and identify further improvements that need to be made tooptimise the buildings’ performance and reduce S&H risks. Across our operational portfolio, we have been measuring, monitoring andtargeting energy use and waste management since the year 2000 and water use since 2003. Our energy and water metering strategy is designed to ensure effective sub-metering with connection to each centre’s BMS, which allows us to have a better control of theseutilities’ use. Data collection and monitoring for energy, water and waste is managed through a centralised online database which allowseach of our shopping centre management teams to input environmental performance data and generate reports that can be used tocompare performance across Sonae Sierra's portfolio. This information is also used to set annual targets to improve performance andincrease staff and tenant awareness of all three issues. We monitor and evaluate safety and health performance on a regular basis usingtools such as SHE Preventive Observations (SPO), emergency drills and SHE inspections (covering safety-related equipment andinstallations in tenant units and technical areas). Furthermore, the annual capital expenditure budget allocated to each of our shoppingcentres includes investments to improve the centres’ SHE performance.

We deliver SHE training to our staff and other key stakeholders on an on-going basis, and in 2011 we delivered a total of 147,037 manhours of training (including meetings) on SHE to staff, suppliers and tenants across our shopping centres, development projects and inour corporate offices.

15 Sonae Sierra specifies three types of construction works interventions that may occur: (1) New shopping centres, which are managed by a Development Manager; (2) Expansion orrefurbishment of existing centres, which may be managed by a Development Manager or Asset Manager, and (3) Small works, which may be managed by any person belonging toSierra Developments, Sierra Asset or Sierra Property Management. Since each of these varies considerably in terms of environmental impact, S&H risks and intervention costs,criteria have been set to establish the most appropriate scheme for each case. All new shopping centres and expansions, refurbishments and other works with a construction costover €10 million or a construction cost of more than 10% of the centre’s Open Market Value (OMV) must apply the standard SHEDS procedure. Expansions, refurbishments and otherworks with a construction cost of over €2.5 million but under €10 million or with a construction cost of less than 10% of the centre’s OMV should apply a simplified SHEDS procedure.Finally, expansions, refurbishments and other works with a construction cost of less than €2.5 million should instead apply the ‘Small Works’ procedure defined within our SHEMS.As explained before in Campo refurbishment SHEDS were not implemented.

16 With reference to the three types of construction interventions described in the note above, all new shopping centres must apply the construction works SHEMS. All expansions,refurbishments and other works with a construction cost of more than €2.5 million must apply a Safety, Health and Environment Management Plan (SHEMP). Finally, expansions,refurbishments and other works with a construction cost of less than €2.5 million should instead apply the ‘Small Works’ procedure defined within our SHEMS. One exception tothese procedures in 2011 was the expansion project of Shopping Campo Limpo: since we have a minority position in this shopping centre, we were not able to implement the entiretyof our SHEMS procedures for development on this project. See page 4 for further details.

wE hAvE dEfINEd loNg-tERm objEctIvES INRElAtIoN to EAch ofouR mAtERIAl cR ImpActAREAS. thESE INcludEouR objEctIvESRElAtINg to ShE.

Energy and Climate

water

26SONAE SIERRA Economic, Environmental and Social Report 2011

Back to main contents

Our Business Strategy continued

CORPORatE OvERvIEw

Who We Are… 1

CEO’s Statement 2

The Year at a Glance 4

Our Company 9

Our Business Strategy 15

Safety, Health and Environment Management System (continued)

In 2011 we also developed a new online management system, called the SHE Portal. This tool, which is expected to be fully operational in2012, will allow us to streamline our SHE management processes and improve the accuracy of data and information reported by holdingall data in one central platform which is accessible to all our staff. We performed audits across our entire portfolio in order to improve theaccuracy and reliability of data reported through the SHEMS, and we delivered training to shopping centre management teams,development teams and staff in corporate offices on how to use the new SHE Portal.

Our CR Objectives

We have defined long-term objectives in relation to each of our material CR impact areas. These include our objectives relating to SHE.These are shown in the table below. Unless otherwise stated, our objectives cover all Sonae Sierra owned shopping centres.

• Achieve a 70% reduction in GHG emissions per m2 of GLA, by 2020, compared to the 2005 level (GHG Protocol scopes 1 and 2, plusbusiness air travel; also includes corporate offices).

• Attain a maximum electricity consumption of 400kWh per m2 of mall and toilet area per year, by 2020.

• Develop and implement a long-term Climate Change Adaptation strategy covering investment, development, management andcorporate activities, by 2020.

• Attain a level of water consumption at or below three litres per visit, by 2020.

• At least 10% of total water consumed to be reused greywater or harvested rainwater by 2020.

• Develop and implement a long-term strategy to ensure a secure water supply, with a particular focus on locations that are vulnerableto water shortages, by 2020.

• Ensure that all discharges to local water courses comply with Sonae Sierra’s wastewater quality standards and pollutant limits, by 2020

taRGEtS FOR 2012

• Ensure that all projects applying the SHEDS (former ESRD version) achieve at least 45% of the available points for applicableLeadership Standards.

• Ensure that all new shopping centre development projects have a valid ISO 14001 and OHSAS 18001 certificate upon opening.

• Achieve ISO 14001 certifications for the SHEMS of one further shopping centre in operation and OHSAS 18001 for a furtherthree shopping centres in operation.

Biodiversity and Habitats

Suppliers

tenants

Communities and visitors

27SONAE SIERRA Economic, Environmental and Social Report 2011

Back to main contents

Our Business Strategy continued

CORPORatE OvERvIEw

Who We Are… 1