Sophisticated Transfer Planning Strategies for Business Owners by Diana S.C. Zeydel Greenberg Traurig, PA | gtlaw.com

What Kinds of Planning Are We Doing Now?

> For less wealthy clients, we need to consider whether transferring wealth during life makes sense

– Is it possible to rely on portability?

– Can you reduce the risks of loss of the DSUE by a subsequent marriage?

– Now that the shelter is portable, it is an asset that can “pass” to a surviving spouse

– How concerned should we be about basis?

1

Sophisticated Transfer Planning Strategies for Business Owners by Diana S.C. Zeydel Greenberg Traurig, PA | gtlaw.com

The Pure Portability Plan and GST

> Cannot avoid the use of trusts and preserve GST planning

– What sorts of trusts should we be using?

Grantor Trust?

QTIP Trust?

Self-Settled Trust?

Credit Shelter Trust?

> How many tax benefits can we obtain without losing control of the assets?

2

Sophisticated Transfer Planning Strategies for Business Owners by Diana S.C. Zeydel Greenberg Traurig, PA | gtlaw.com

Should We Avoid Making Current Taxable Gifts?

> Some suggest that because the shelter is portable it has become a “descendable asset” the use of which requires greater caution

> No longer use it or lose it at death

> Using it on an asset that declines in value seems far worse than it used to be

> But is that really true?

> In case it is, what strategies should we consider?

3

Sophisticated Transfer Planning Strategies for Business Owners by Diana S.C. Zeydel Greenberg Traurig, PA | gtlaw.com

99-Year GRAT

> What’s the Deal?

– It’s a numbers game

Included property of a GRAT is a function of dividing the amount of the annuity by the 7520 rate

The higher the rate, the lower the inclusion

> So the bet is that interest rates will go up

4

Sophisticated Transfer Planning Strategies for Business Owners by Diana S.C. Zeydel Greenberg Traurig, PA | gtlaw.com

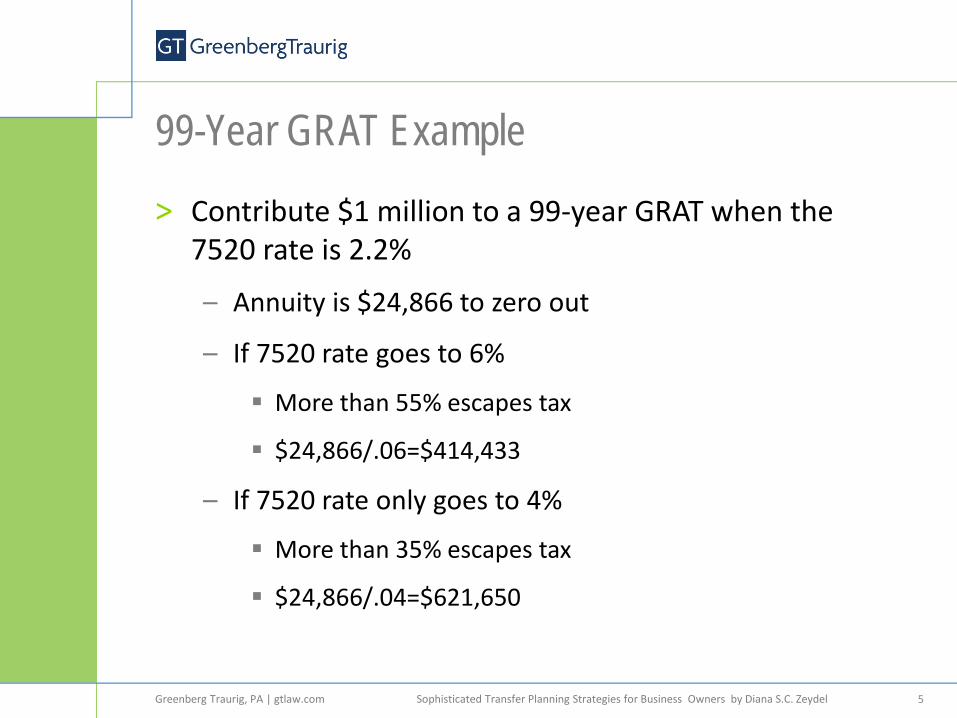

99-Year GRAT Example

> Contribute $1 million to a 99-year GRAT when the 7520 rate is 2.2%

– Annuity is $24,866 to zero out

– If 7520 rate goes to 6%

More than 55% escapes tax

$24,866/.06=$414,433

– If 7520 rate only goes to 4%

More than 35% escapes tax

$24,866/.04=$621,650

5

Sophisticated Transfer Planning Strategies for Business Owners by Diana S.C. Zeydel Greenberg Traurig, PA | gtlaw.com

Leveraged GRATs

> Purpose

– More valuation protection than with a traditional installment sale

> Method

– Perform the sale with an entity that is owned by the seller or a wholly grantor trust owned by the seller for income tax purposes that is an incomplete gift trust

6

Sophisticated Transfer Planning Strategies for Business Owners by Diana S.C. Zeydel Greenberg Traurig, PA | gtlaw.com

Leveraged GRAT

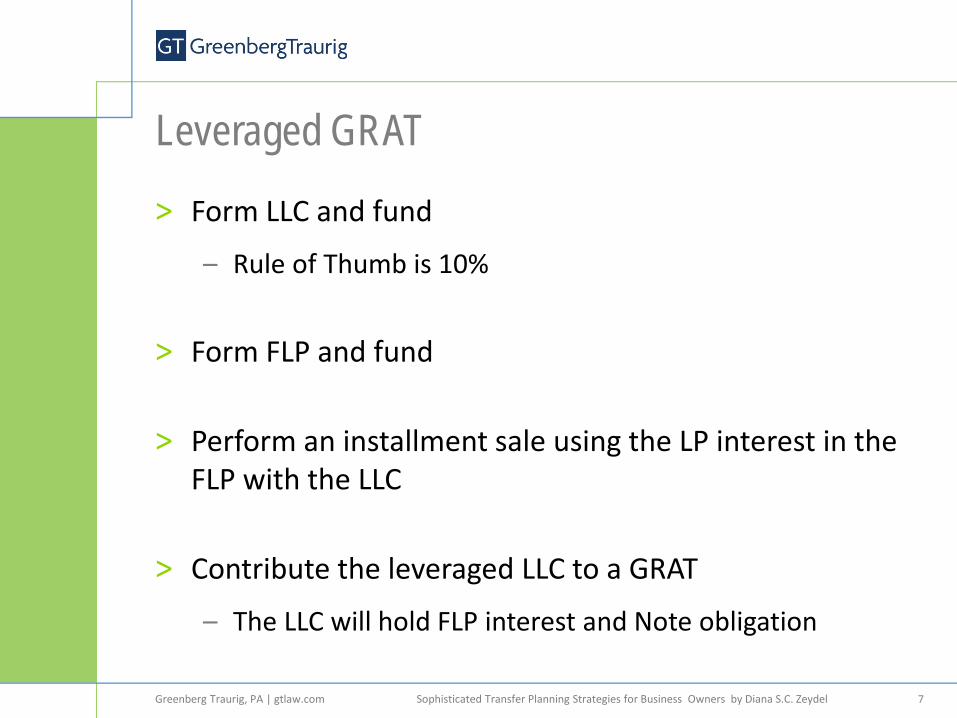

> Form LLC and fund

– Rule of Thumb is 10%

> Form FLP and fund

> Perform an installment sale using the LP interest in the FLP with the LLC

> Contribute the leveraged LLC to a GRAT

– The LLC will hold FLP interest and Note obligation

7

Sophisticated Transfer Planning Strategies for Business Owners by Diana S.C. Zeydel Greenberg Traurig, PA | gtlaw.com

Leveraged GRAT

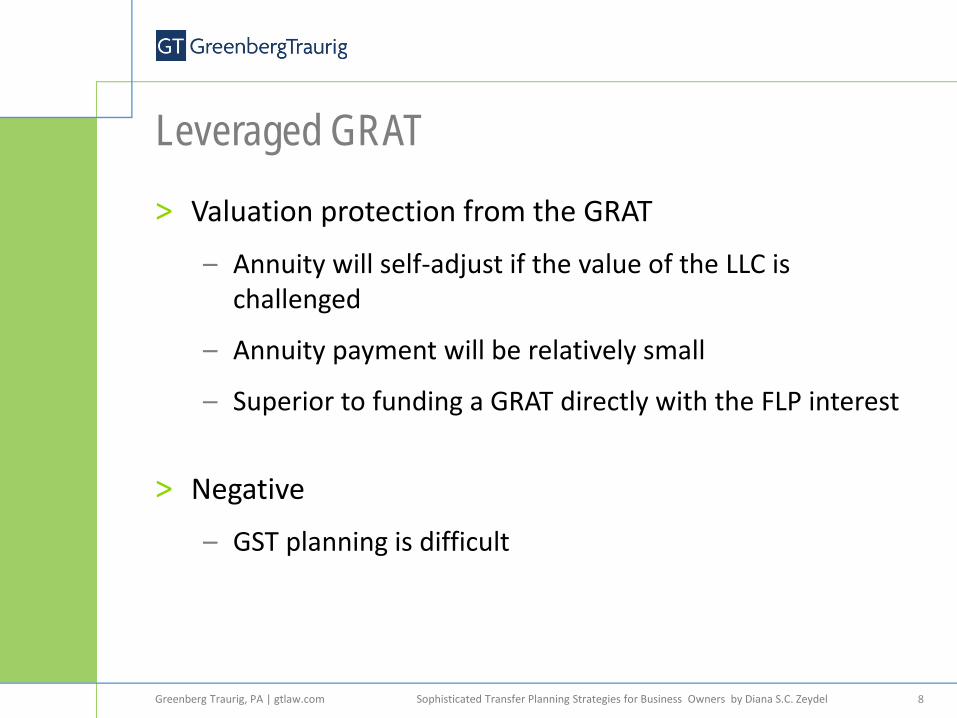

> Valuation protection from the GRAT

– Annuity will self-adjust if the value of the LLC is challenged

– Annuity payment will be relatively small

– Superior to funding a GRAT directly with the FLP interest

> Negative

– GST planning is difficult

8

Sophisticated Transfer Planning Strategies for Business Owners by Diana S.C. Zeydel Greenberg Traurig, PA | gtlaw.com

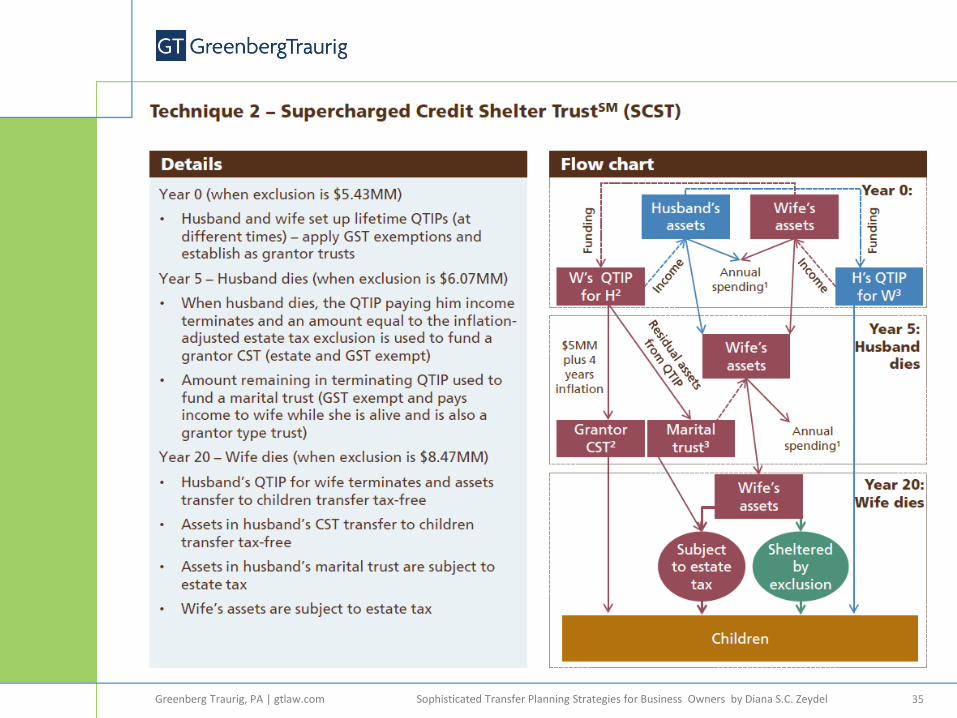

The Benefits of Supercharging a Credit Shelter Trust

> Goal: Make the CST a grantor trust as to surviving spouse

> Section 678 and power of withdraw triggers section 2041

> Each spouse creates reverse lifetime QTIP trust included under section 2044 and which becomes a credit shelter trust (and perhaps a QTIP trust with excess) for survivor who created the lifetime QTIP trust

> Despite estate tax inclusion, it remains a grantor trust as to the surviving spouse

> Benefits: Earlier allocation of GST exemption, tax free growth of CST and opportunity for simulated step-up at survivor’s death

9

Sophisticated Transfer Planning Strategies for Business Owners by Diana S.C. Zeydel Greenberg Traurig, PA | gtlaw.com

Supercharged CSTSM

> Why does 678 not work?

– It does not appear that withdrawal for HEMS is sufficient to make a credit shelter trust a grantor trust with respect to the surviving spouse

– A greater power of withdrawal would make the trust estate tax includible under Section 2041

10

Sophisticated Transfer Planning Strategies for Business Owners by Diana S.C. Zeydel Greenberg Traurig, PA | gtlaw.com

Supercharged CSTSM

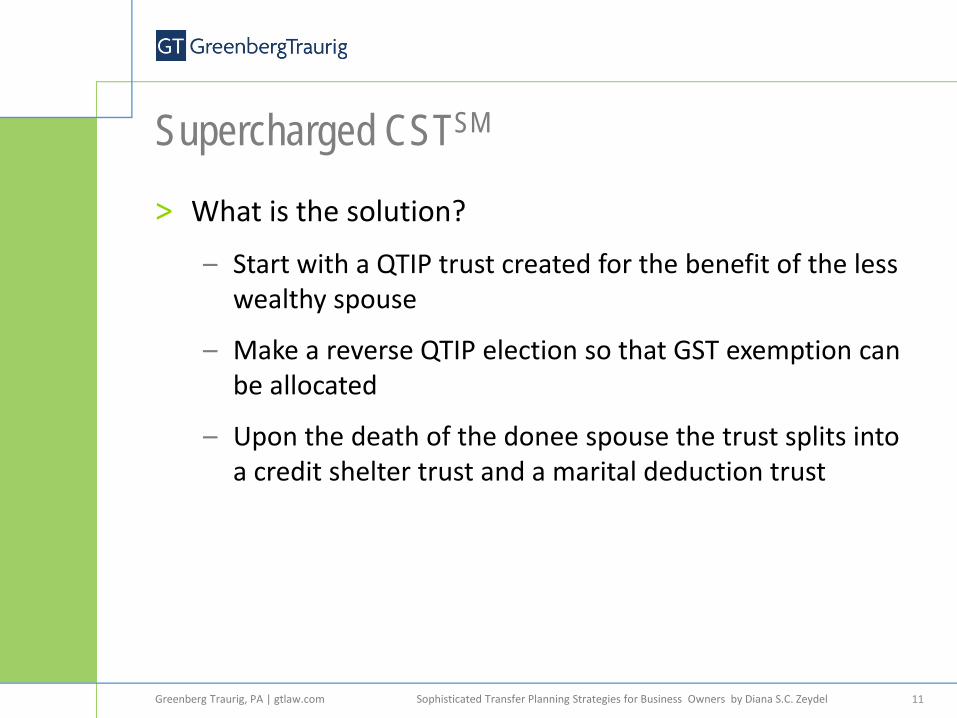

> What is the solution?

– Start with a QTIP trust created for the benefit of the less wealthy spouse

– Make a reverse QTIP election so that GST exemption can be allocated

– Upon the death of the donee spouse the trust splits into a credit shelter trust and a marital deduction trust

11

Sophisticated Transfer Planning Strategies for Business Owners by Diana S.C. Zeydel Greenberg Traurig, PA | gtlaw.com

Supercharged CSTSM

> What about estate tax inclusion for the donor spouse? – Protected from inclusion under the QTIP regs with

respect to Sections 2036 and 2038 Example 11, Treas. Reg. 25.2523(f)-1(f)

> Need to avoid creditor’s rights – How do you do that?

Use a self-settled asset protection trust jurisdiction

Or use a jurisdiction such as FL that specifically says a marital deduction trust is not available to the creditors of the settlor

12

Sophisticated Transfer Planning Strategies for Business Owners by Diana S.C. Zeydel Greenberg Traurig, PA | gtlaw.com

Authority for the Supercharged CSTSM > Treas. Reg. §1.671-2(e) provides that a gratuitous transfer is

any transfer other than a transfer for fair market value. “A transfer of property to a trust may be considered a gratuitous transfer without regard to whether the transfer is treated as a gift for gift tax purposes.”

> A grantor includes any person who creates or makes a gratuitous transfer to a trust.

> However a person who creates a trust but makes no gratuitous transfer is not an owner.

13

Sophisticated Transfer Planning Strategies for Business Owners by Diana S.C. Zeydel Greenberg Traurig, PA | gtlaw.com

Only the Exercise of a GPOA shifts the identity of the Grantor for Income Tax Purposes > Treas. Reg. §1.671-2(e)(5). “If a trust makes a

gratuitous transfer of property to another trust, the grantor of the transferor trust is generally treated as the grantor of the transferee trust. However, if a person with a general power of appointment over the transferor trust exercises that power in favor of another trust, then such person will be treated as the grantor of the transferee trust even if the grantor of the transferor trust is treated as the owner of the transferor trust [under the grantor trust rules].”

> The above rule is consistent with creditor’s rights.

14

Sophisticated Transfer Planning Strategies for Business Owners by Diana S.C. Zeydel Greenberg Traurig, PA | gtlaw.com

Supercharged CSTSM

> The leverage of GST exemption is powerful

> Grantor trust status creates additional leverage

– ADDED BONUS

Spouses can retain an income interest in the trusts

Yes, you must navigate the reciprocal trust doctrine

BUT maybe not as scary because the trusts are already estate tax includible

15

Sophisticated Transfer Planning Strategies for Business Owners by Diana S.C. Zeydel Greenberg Traurig, PA | gtlaw.com

Structuring an Installment Sale > Woelbing cases

– It appears that a defined value formula was used, NEVERTHELESS: The agent asserted that § 2702 applies resulting in a

transfer without a qualified retained interest

The note would be assigned a zero value in the estate

In the alternative, the arrangement is a transfer with a retained interest implicating §§ 2036 and 2038

– Transaction appears carefully and properly planned

– $20 million of the $59 million note was repaid within 3 years (evidence of debt)

16

Sophisticated Transfer Planning Strategies for Business Owners by Diana S.C. Zeydel Greenberg Traurig, PA | gtlaw.com

Can Analysis of Trombetta Help?

> Trombetta was a sale in exchange for a private annuity worth less than the value of the property transferred

> Was determined to be a transfer with a retained interest within § 2036

> Can you avoid this construction?

17

Sophisticated Transfer Planning Strategies for Business Owners by Diana S.C. Zeydel Greenberg Traurig, PA | gtlaw.com

Gans and Blattmachr Analysis > Fidelity-Philadelphia (U.S. Supreme Court) identifies three

factors that avoid the application of § 2036 – The obligation to make payments to the decedent is not

chargeable to the transferred property – The transferee is personally obligated to make payments – Payments are not dependent upon the income from the

transferred property

> Gans and Blattmachr believe satisfying these three factors should – Result in a bona fide sale for purposes of § 2036 – Avoid § 2702

18

Sophisticated Transfer Planning Strategies for Business Owners by Diana S.C. Zeydel Greenberg Traurig, PA | gtlaw.com

Trombetta

> How do you satisfy the Fidelity-Philadelphia factors?

– Seed capital independent of the sale transaction

– Avoid a part sale/part gift (also true for purposes of designing a formula that avoids Procter)

– Time between the contribution (gift) and the sale should help

– Note that guarantees were not persuasive either in Trombetta or Woelbing – primarily because they were never enforced

19

Sophisticated Transfer Planning Strategies for Business Owners by Diana S.C. Zeydel Greenberg Traurig, PA | gtlaw.com

Use of a Formula

> Generally, seems superior to use a formula allocation clause, rather than a pure Wandry clause

> John Porter favors charity and GRATs to receive the excess, but a marital trust or even a self-settled trust may work

> Even if a formula is used, consider a purchase price adjustment clause as well

20

Sophisticated Transfer Planning Strategies for Business Owners by Diana S.C. Zeydel Greenberg Traurig, PA | gtlaw.com

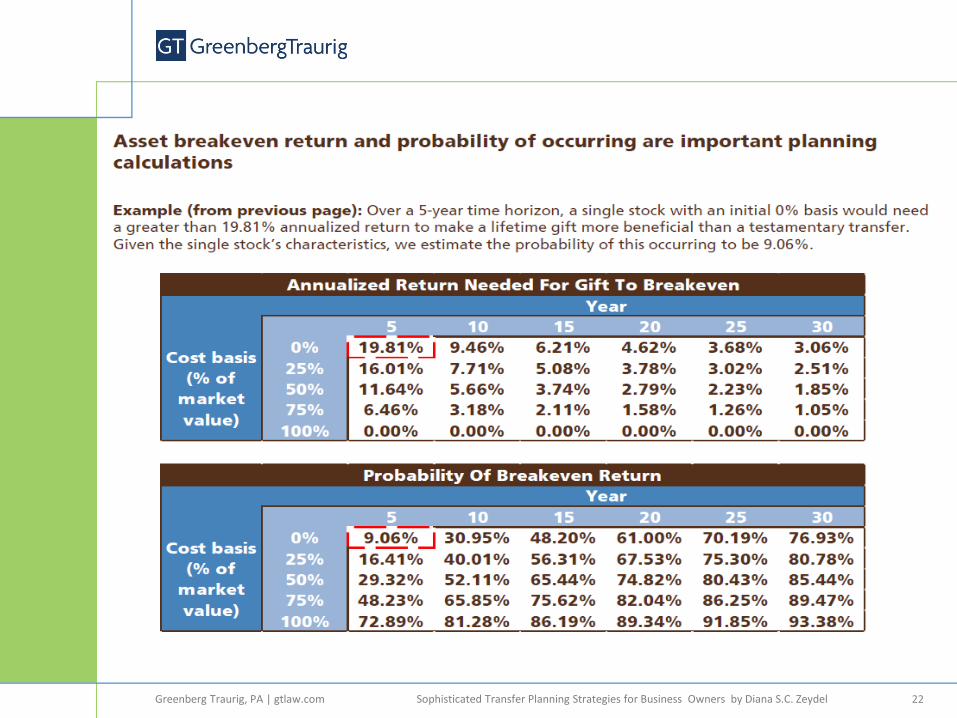

What About Basis?

> Portability permits a couple to receive a basis step-up (adjustment) on the first death and on the second death while preserving the use of the estate tax shelter of the first spouse to die

> What is the likelihood that making a gift of a low basis asset would be beneficial?

21

Sophisticated Transfer Planning Strategies for Business Owners by Diana S.C. Zeydel Greenberg Traurig, PA | gtlaw.com

22

Sophisticated Transfer Planning Strategies for Business Owners by Diana S.C. Zeydel Greenberg Traurig, PA | gtlaw.com

Examples

> $5 million asset is gifted and appreciates to $6 million

– Estate tax savings is $400,000

– Capital gains tax cost is $1,428,000

> $5 million asset is gifted and appreciates to $10 million

– Estate tax savings is $2 million

– Capital gains tax cost is $2,380,000

> $5 million asset is gifted and appreciates to $15 million

– Estate tax savings is $4 million

– Capital gains tax cost is $3,570,000

23

Sophisticated Transfer Planning Strategies for Business Owners by Diana S.C. Zeydel Greenberg Traurig, PA | gtlaw.com

Can you make a gift and still get a basis adjustment?

> You can if the trust is a grantor trust and the client has the ability to substitute assets

> How would you set this up?

– Make sure all assets, even cash, are held in entities

– This allows you to effectuate a substitution without moving the assets from one account to another

> Is a grantor trust really a big deal?

24

Sophisticated Transfer Planning Strategies for Business Owners by Diana S.C. Zeydel Greenberg Traurig, PA | gtlaw.com 25

Sophisticated Transfer Planning Strategies for Business Owners by Diana S.C. Zeydel Greenberg Traurig, PA | gtlaw.com

Portability and Grantor Trusts > Grantor Trusts: Rev. Rul. 85-13 and Rev. Rul. 2004-64

> Surviving spouse puts the DSUE amount into a grantor trust: tax-free compounding and substitution before death

> Cost: Potentially give up a beneficial interest and control at death

> Could use a self-settled trust – PLR 200944002 and Huber

26

Sophisticated Transfer Planning Strategies for Business Owners by Diana S.C. Zeydel Greenberg Traurig, PA | gtlaw.com

Portability and Grantor Trusts (cont’d) > A Better Plan: Have survivor use his or her own assets to

create a grantor trust and have DSUE amount pass into a credit shelter trust for survivor and descendants?

> Another Possible Plan: Have the first spouse to die create a reverse QTIP to use GST exemption and have the surviving spouse create two grantor trusts, one using the DSUE amount and one using his or her own gift and GST exemptions

> Have spouses use their gift and GST exemptions as early in life as possible (using grantor trusts)

27

Sophisticated Transfer Planning Strategies for Business Owners by Diana S.C. Zeydel Greenberg Traurig, PA | gtlaw.com

Trusts Created By Entities

> How can a non-grantor trust make a charitable contribution?

– If there is UBI, contribution limitations are the same as applicable to an individual

> Can a partnership owned by a trust make a charitable contribution for which the trust obtains a section 642(c) deduction?

– Must the contribution be from gross income?

> Is it possible for a partnership to create a split-interest trust?

28

Sophisticated Transfer Planning Strategies for Business Owners by Diana S.C. Zeydel Greenberg Traurig, PA | gtlaw.com 29

Sophisticated Transfer Planning Strategies for Business Owners by Diana S.C. Zeydel Greenberg Traurig, PA | gtlaw.com 30

Sophisticated Transfer Planning Strategies for Business Owners by Diana S.C. Zeydel Greenberg Traurig, PA | gtlaw.com 31

Sophisticated Transfer Planning Strategies for Business Owners by Diana S.C. Zeydel Greenberg Traurig, PA | gtlaw.com 32

Sophisticated Transfer Planning Strategies for Business Owners by Diana S.C. Zeydel Greenberg Traurig, PA | gtlaw.com 33

Sophisticated Transfer Planning Strategies for Business Owners by Diana S.C. Zeydel Greenberg Traurig, PA | gtlaw.com 34

Sophisticated Transfer Planning Strategies for Business Owners by Diana S.C. Zeydel Greenberg Traurig, PA | gtlaw.com 35

Sophisticated Transfer Planning Strategies for Business Owners by Diana S.C. Zeydel Greenberg Traurig, PA | gtlaw.com 36

Sophisticated Transfer Planning Strategies for Business Owners by Diana S.C. Zeydel Greenberg Traurig, PA | gtlaw.com 37

Sophisticated Transfer Planning Strategies for Business Owners by Diana S.C. Zeydel Greenberg Traurig, PA | gtlaw.com 38

Sophisticated Transfer Planning Strategies for Business Owners by Diana S.C. Zeydel Greenberg Traurig, PA | gtlaw.com 39

Sophisticated Transfer Planning Strategies for Business Owners by Diana S.C. Zeydel Greenberg Traurig, PA | gtlaw.com

40

Sophisticated Transfer Planning Strategies for Business Owners by Diana S.C. Zeydel Greenberg Traurig, PA | gtlaw.com 41

Sophisticated Transfer Planning Strategies for Business Owners by Diana S.C. Zeydel Greenberg Traurig, PA | gtlaw.com 42

Sophisticated Transfer Planning Strategies for Business Owners by Diana S.C. Zeydel Greenberg Traurig, PA | gtlaw.com 43

Sophisticated Transfer Planning Strategies for Business Owners by Diana S.C. Zeydel Greenberg Traurig, PA | gtlaw.com 44

Sophisticated Transfer Planning Strategies for Business Owners by Diana S.C. Zeydel Greenberg Traurig, PA | gtlaw.com 45

Sophisticated Transfer Planning Strategies for Business Owners by Diana S.C. Zeydel Greenberg Traurig, PA | gtlaw.com 46

Sophisticated Transfer Planning Strategies for Business Owners by Diana S.C. Zeydel Greenberg Traurig, PA | gtlaw.com 47

Sophisticated Transfer Planning Strategies for Business Owners by Diana S.C. Zeydel Greenberg Traurig, PA | gtlaw.com 48

Sophisticated Transfer Planning Strategies for Business Owners by Diana S.C. Zeydel Greenberg Traurig, PA | gtlaw.com 49

Sophisticated Transfer Planning Strategies for Business Owners by Diana S.C. Zeydel Greenberg Traurig, PA | gtlaw.com 50

Sophisticated Transfer Planning Strategies for Business Owners by Diana S.C. Zeydel Greenberg Traurig, PA | gtlaw.com 51

Sophisticated Transfer Planning Strategies for Business Owners by Diana S.C. Zeydel Greenberg Traurig, PA | gtlaw.com 52

Sophisticated Transfer Planning Strategies for Business Owners by Diana S.C. Zeydel Greenberg Traurig, PA | gtlaw.com 53

Sophisticated Transfer Planning Strategies for Business Owners by Diana S.C. Zeydel Greenberg Traurig, PA | gtlaw.com

54

Sophisticated Transfer Planning Strategies for Business Owners by Diana S.C. Zeydel Greenberg Traurig, PA | gtlaw.com 55

Sophisticated Transfer Planning Strategies for Business Owners by Diana S.C. Zeydel Greenberg Traurig, PA | gtlaw.com 56

Sophisticated Transfer Planning Strategies for Business Owners by Diana S.C. Zeydel Greenberg Traurig, PA | gtlaw.com 57