38

SOURCES OF FUNDING FOR IRISH BUSINESSES MAY 2015

SOURCES OF FUNDING FOR IRISH BUSINESSES MAY 2015

INTRODUCTION TO PEGASUS CAPITAL SECTION I

ABOUT US

• Pegasus Capital is a Dublin-‐based financial advisory firm

• We advise mid-‐market Irish companies on a range of transacRons:

• Raising debt

• Raising quasi-‐equity & equity

• Company disposals, mergers & acquisiRons

• Management buy-‐out & management buy-‐in transacRons

• We typically advise on 8 – 10 transacRons p.a.

• ParRcular experRse in high-‐growth sectors such as technology & lifesciences

Page 3

CHOOSING A SOURCE OF FUNDING SECTION II

OUR GENERAL VIEW ON THE FUNDING ENVIRONMENT

• Debt & equity markets less buoyant than pre-‐Crisis

• Companies that are financially strong have mulRple funding opRons

• Given the size of the market, Ireland is well-‐represented with equity funds

• Funding from internaRonal sources is available in certain circumstances

• InsRtuRonal funds prefer to invest in companies with a strong growth outlook

• High net worth investors have an appeRte for invesRng but decision making is more

arbitrary and quantums are generally low relaRve to insRtuRonal funds

• Most insRtuRonal funds have a preference to invest later in the cycle

• Funding takes Rme to put in place … need to build-‐in appropriate headroom

Page 5

TYPES OF FUNDING

1. DEBT

AMORTISING

BULLET

EQUITY WARRANT

WARRANTLESS

MINORITY STAKE

MAJORITY STAKE

2. QUASI-‐EQUITY

3. EQUITY

HIGHER RISK = H

IGHER CO

ST

Page 6

ü Lower cost

ü Limited loss of control

ü Clear repayment schedule

DEBT EQUITY

ü Strengthens Balance Sheet

ü Increases financial firepower

ü Provides downside protecRon

ü Shareholder de-‐risking

û Typically short-‐term

û Degrees of recourse

û Not always appropriate

û Repaid from cashflow

û Leverage increases

û Expensive

û Difficult to raise

û Dilutes shareholding

û Need to provide an exit

DEBT VS. EQUITY

Page 7

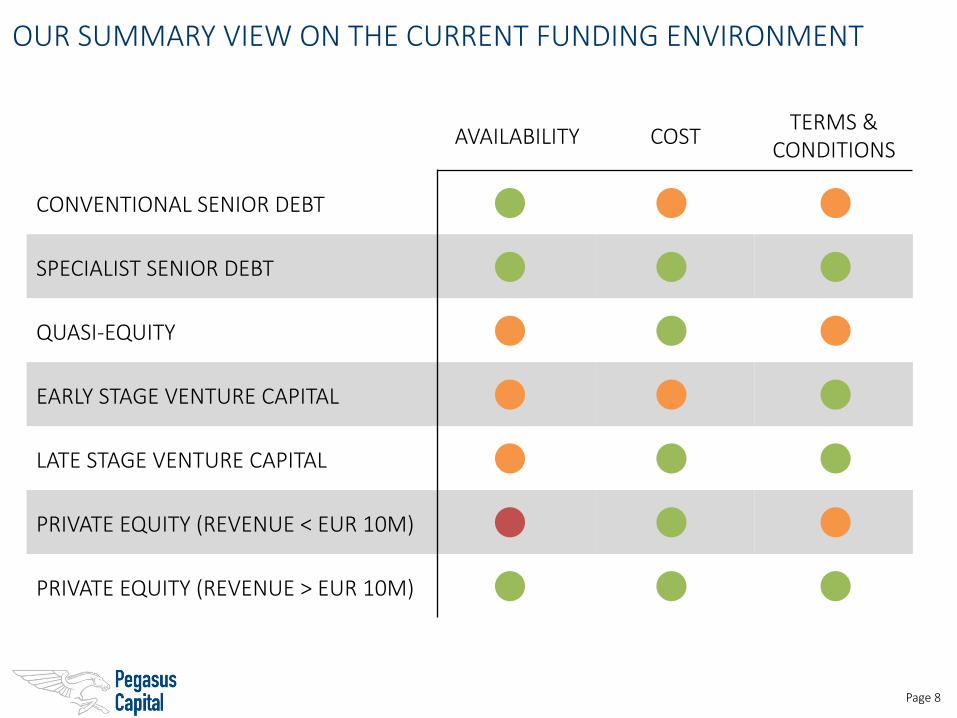

OUR SUMMARY VIEW ON THE CURRENT FUNDING ENVIRONMENT

AVAILABILITY COST TERMS &

CONDITIONS

CONVENTIONAL SENIOR DEBT

SPECIALIST SENIOR DEBT

QUASI-‐EQUITY

EARLY STAGE VENTURE CAPITAL

LATE STAGE VENTURE CAPITAL

PRIVATE EQUITY (REVENUE < EUR 10M)

PRIVATE EQUITY (REVENUE > EUR 10M)

Page 8

TARG

ET RETURN

S

RISK

FUNDING PROVIDER RETURNS VS. RISK

Page 9

SENIOR DEBT c. 5%

INFRASTRUCTURE c. 8% -‐ 10%

PROPERTY c. 10 -‐ 12%

DEV. CAP. & MEZZANINE c. 12% +

PRIVATE EQUITY c. 25%

VENTURE CAPITAL 25% +

VENTURE DEBT c. 20%

DEBT & QUASI-‐EQUITY SECTION III

DEBT AS A SOURCE OF FUNDING

• The Irish banking environment has improved but challenges remain:

• Leverage rates remain low

• Interest rates, while reducing, remain above European levels

• Debt tenor remains low with limited appeRte for long-‐term funding

Page 11

DEBT AS A SOURCE OF FUNDING (CONT’D)

• Summary observaRons:

• Debt < 3.5x EBITDA with a focus on profitability

• Key consideraRons:

• Type of funding: term debt vs. invoice discounRng vs. asset finance?

• ConvenRonal bank vs. specialist provider of niche products?

• Debt mulRple … depends on free operaRng cashflow?

• Fixed vs. floaRng interest rate?

• Security & recourse?

• Tenor?

Page 12

QUASI-‐EQUITY AS A SOURCE OF FUNDING

• Quasi-‐equity / mezzanine:

• Sits where equity would otherwise sit

• EffecRvely preferred equity in some cases

• More efficient capital structure … reduces average cost of capital

• Lower availability of convenRonal debt has reduced the risk parameters:

• Overall leverage levels have reduced c. 25% from pre-‐Crisis peak

• Many providers will typically only invest in sponsor-‐led opportuniRes:

1. To remove ‘funder of last resort’ risk, and

2. To provide greater comfort on surety of exit

Page 13

QUASI-‐EQUITY AS A SOURCE OF FUNDING (CONT’D)

• Summary observaRons:

• Investment criteria focused on cashflow

• Reasonably full due diligence requirements

• Fundraising process similar to an equity fundraising process

• (For tech & lifescience companies) may be backed by a specific charge over IP

• Key consideraRons:

• Mezzanine vs. development capital fund?

• Payment in cash vs. payment in kind?

• Timing of funding need and buy-‐back opRon?

Page 14

DEBT RAISING … INITIAL DOCUMENTATION REQUIREMENTS

1. Proposal overview

2. Financial profile:

• Min. 3 years historic and 1 – 2 years future

• Detailed use of cash

3. Detailed cashflow:

• Cash cover ((operaRng cashflow – tax – working cap – capex) / (capital + interest)) > 1.2x

• Interest cover ((operaRng cashflow – tax – working cap – capex) / (interest)) > 4.0x

• Debt mulRple (net debt / EBITDA) < 3.0x

4. Consider bank security opRons

Page 15

VENTURE CAPITAL SECTION IV

0

5

10

15

20

25

30

35

40

45

50

-‐

1

2

3

4

Q1 09

Q2 09

Q3 09

Q4 09

Q1 10

Q2 10

Q3 10

Q4 10

Q1 11

Q2 11

Q3 11

Q4 11

Q1 12

Q2 12

Q3 12

Q4 12

Q1 13

Q2 13

Q3 13

Q4 13

Q1 14

Q2 14

Q3 14

Q4 14

NO. FUNDRA

ISINGS (RED

) NO. FUNDRA

ISINGS > EU

R 5M

(GRE

EN)

AVER

AGE FU

NDRA

ISING (E

URM

, BLU

E CO

LUMN)

IRISH LIFESCIENCES & TECH EQUITY FUNDRAISINGS (2009 – DATE)

VENTURE CAPITAL FUNDRAISINGS

Page 17

RAISING VENTURE CAPITAL

• Summary comments:

• Raise sufficient capital to fund breakeven based on conservaRve projecRons

• Raising equity overseas is challenging in the absence of reasonable scale

• The majority of acRve funds see the current environment as an “investors” market

• Most VC funds only invest in high-‐growth areas (technology & lifesciences)

• Terms may be opRmised by maximising the number of credible interested parRes

• High availability of seed funding locally over the past number of years

• Consider the availability of follow-‐on funding

• No short-‐term cash / liquidity issues

• Support of exisRng investors

Page 18

EUROPEAN VS. US VENTURE CAPITAL

ü Generally more entrepreneurial

ü ValuaRons frothy in certain segments

ü More focused on generaRng very high exit

values and willing to fund the higher cash burn

required to achieve this

û May require relocaRon to the US

û Less supporRve if the Company underperforms

û Criteria may exclude companies outside US

û Target revenue > US$ 5m for overseas deals

ü Generally more supporRve of unforeseen

challenges

ü Proximity = closer relaRonship

ü Generally give their porzolio companies more

Rme to succeed

û Capacity may be more limited if the investee

company requires significant follow-‐on funds

û Limited value-‐add if customer base is US centric

Page 19

TYPICAL VENTURE CAPITAL TERMS

• Key consideraRons:

• Confidence in projecRons … i.e. trade downside protecRon for greater upside?

• Will the Company require more capital?

• Strategic or financial investor(s)?

• Quantum of funding required?

á QUANTUM OF FUNDING

á VALUATION

DRAG ALONG â

ANTI-‐DILUTION â

LIQUIDATION PREFERENCE â

Page 20

HIGH

SEED

LOW APPETITE FOR IRISH DEALS

DEVELOPMENT CAPITAL

STAG

E OF INVE

STMEN

T

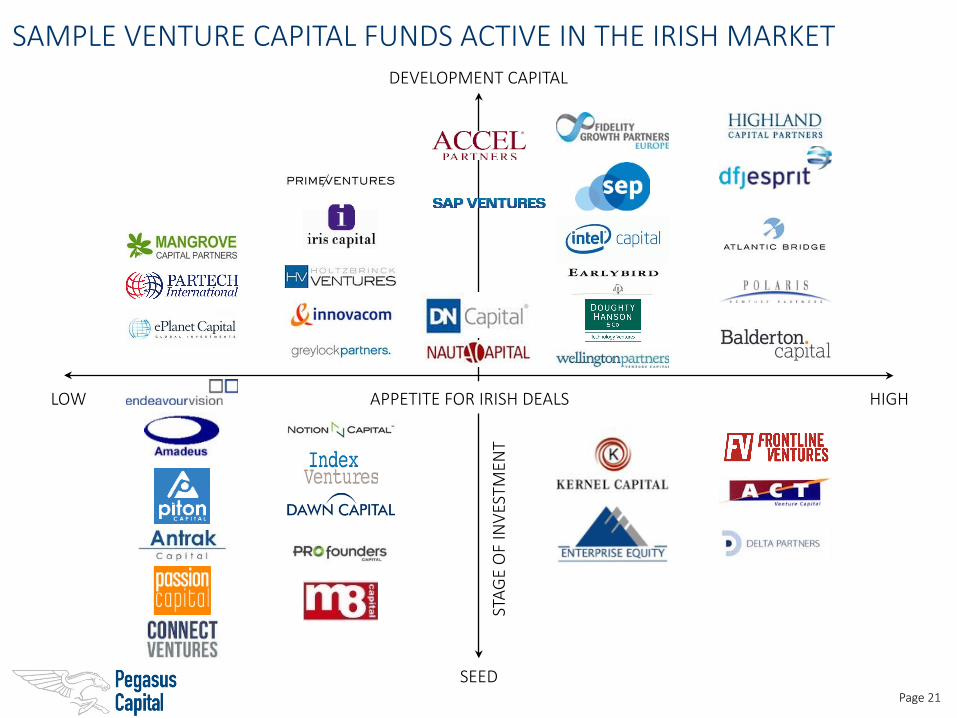

SAMPLE VENTURE CAPITAL FUNDS ACTIVE IN THE IRISH MARKET

Page 21

NO. OF PROPOSALS TIMEFRAME COMMENTS

Annual investment proposals

5 mins. 20 -‐ 25% disregarded immediately … not in the area of focus

1 hr. AddiRonal 20 -‐ 25% disregarded a{er an iniRal ‘sense-‐check’

1 hr. Post desktop review c. ⅓ of applicaRons given consideraRon

1 hr. Conf. call with Target to assess opportunity

+ 2 wks. Internal desk-‐top & industry research

30 mins. Sponsor-‐led investment commi}ee review

+ 3 -‐ 4 wks. Review Business Plan and internal due diligence

IndicaRve Heads of Terms

variable Full due diligence

CompleRon

c. 1,000

4 -‐ 5

c. 750

c. 500

c. 333

c. 100

c. 50

TYPICAL VC INVESTMENT PROCESS

20 -‐ 25

Page 22

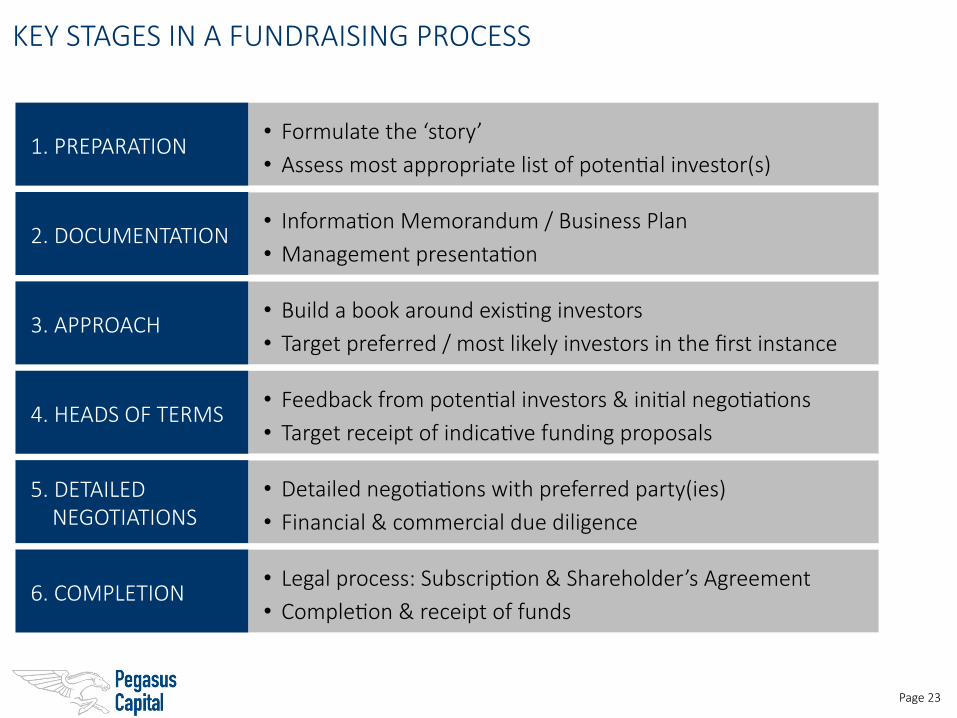

KEY STAGES IN A FUNDRAISING PROCESS

• Formulate the ‘story’ • Assess most appropriate list of potenRal investor(s)

• Build a book around exisRng investors • Target preferred / most likely investors in the first instance

• InformaRon Memorandum / Business Plan • Management presentaRon

• Feedback from potenRal investors & iniRal negoRaRons • Target receipt of indicaRve funding proposals

• Detailed negoRaRons with preferred party(ies) • Financial & commercial due diligence

• Legal process: SubscripRon & Shareholder’s Agreement • CompleRon & receipt of funds

1. PREPARATION

3. APPROACH

2. DOCUMENTATION

4. HEADS OF TERMS

5. DETAILED NEGOTIATIONS

6. COMPLETION

Page 23

PRIVATE EQUITY SECTION V

PRIVATE EQUITY AS A SOURCE OF FUNDING

• Private equity is most suitable for:

1. Funding an acquisiRon (or merger)

2. Funding a management buy-‐out or buy-‐in

3. The outright (or majority) purchase of a company

4. Business expansion … e.g. purchase of a new producRon facility

5. Debt pay-‐down (i.e. de-‐leveraging) … replacing exisRng debt with new equity

6. Internal recapitalisaRon or other minority stake investment … only a limited

number of private equity funds will be content with a minority stake

7. Other Balance Sheet restructuring

Page 25

PRIVATE EQUITY AS A SOURCE OF FUNDING (CONT’D)

• Choosing a private equity fund:

• Personal fit?

• Fund vintage, sectoral focus & experRse?

• Profile of the Fund’s precedent investments?

• Investment track record (i.e. performance) of the Fund?

• Key transacRon consideraRons:

• ValuaRon?

• Exit rights / influence / Rmeframe?

• PotenRal for addiRonal future diluRon?

• Investment instrument (i.e. equity, loan-‐note etc.)?

• InsRtuRonal vs. private investors (vs. combinaRon)?

Page 26

Page 27

SAMPLE PRIVATE EQUITY FUNDS ACTIVE IN IRELAND

+ non-‐insRtuRonal sources

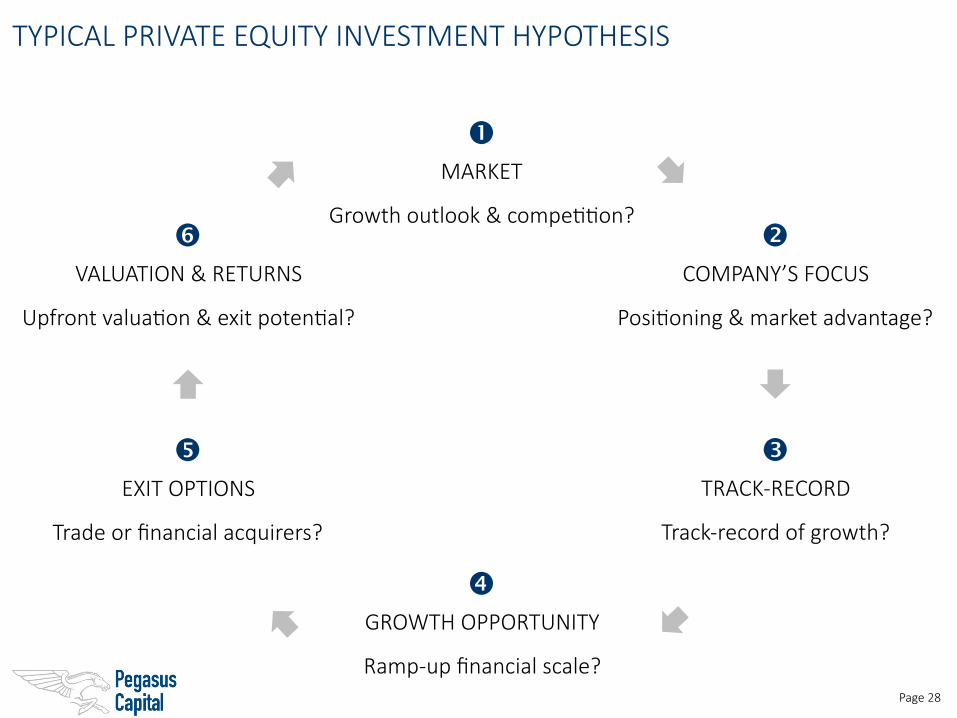

TYPICAL PRIVATE EQUITY INVESTMENT HYPOTHESIS

Page 28

� GROWTH OPPORTUNITY

Ramp-‐up financial scale?

� MARKET

Growth outlook & compeRRon? �

COMPANY’S FOCUS

PosiRoning & market advantage?

� TRACK-‐RECORD

Track-‐record of growth?

� EXIT OPTIONS

Trade or financial acquirers?

� VALUATION & RETURNS

Upfront valuaRon & exit potenRal?

TYPICAL FUND STRUCTURE

• Limited Partners (investors) + General Partners (fund managers)

• Investors include pension funds, endowments, Sovereign funds, fund-‐of-‐funds, etc.

• Management fees are typically ~ 1.5% -‐ 2.0% of overall funds raised

• 80% : 20% split in ‘profits’ (in favour of LP’s) subject to a ~ 8% LP hurdle rate

• Typical terms:

• Fund life typically 7 -‐ 10 years

• No single investment > 10% of the fund

• Aim to have 75% of fund invested by year 5

• 20% -‐ 30% of funds held in reserve for follow-‐on investment

• Will typically raise a new fund when 75% of ‘old’ fund is invested

Page 29

T&C’S OF PRIVATE EQUITY INVESTMENT

• Ordinary equity vs. loan note combinaRon

• Minority vs. controlling stake:

• Control by veto / consent ma}ers

• Management vs. investor rights & responsibiliRes

• InformaRon rights, Board representaRon & voRng rights

• Availability of follow-‐on funding?

• Pre-‐empRon & anR-‐diluRon rights

• Agreement in principle on exit (Rming etc.):

• Drag & tag along rights

• RecapitalisaRon opRons (incl. valuaRon mulRples)

Page 30

GENERAL COMMENTS ON RAISING EQUITY

• Shareholder’s Agreement only likely to be important in the event of a future

breakdown in relaRonships … at which Rme it will be very important

• Other key consideraRons:

• Venture capital or private equity firms will not give warranRes in an exit

• Future fundraising(s) should not be through different investment instruments

• Timing of investment process?

• Due diligence vs. exclusivity

• Investors will require full clarity on:

• Use of proceeds & future funding requirements?

• Exit opRons?

Page 31

EQUITY RAISING … INITIAL DOCUMENTATION REQUIREMENTS

1. TransacRon drivers

2. Company overview:

• Landscape & posiRoning

• Short-‐term growth outlook

• Shareholder & capital structure

3. Financial profile:

• Min. 3 years historic and 3 – 5 years future

• Sales analysis & pipeline

• Profit bridge

4. PotenRal exit opRons

Page 32

FUNDING CASE STUDIES SECTION VI

CASE STUDY 1

• Scenario:

• EUR 5.2m acquisiRon

• Target company is export-‐focused

• Target company profitability of EUR 1.0m … with > 80% of this converRng to cash

• Funding opRons:

1. Bank debt available up to EUR 3.2m (local bank @ 5.0% over 3 years)

2. Outside investor (loan note @ 15% or ordinary equity)

3. Vendor financing

Page 34

CASE STUDY 2

• Scenario:

• Irish manufacturing company with a EUR 13m funding need (to fund an MBO)

• EBITDA c. EUR 2.5m, ex-‐growth but strong cash generaRon

Bank # 1:

• Dublin-‐based bank

• Specialist sector focus

• Standard senior debt:

• Higher equity requirement (EUR 5.5m)

• 3.0x EBITDA debt

• Margin of 3%

Bank # 2:

• London-‐based bank

• Unitranche debt:

• Lower equity (EUR < 3m)

• c. 4x EBITDA debt faciliRes

• Accelerated repayment opRon

• Margin of 6%

• Extended term

• Warrant

Page 35

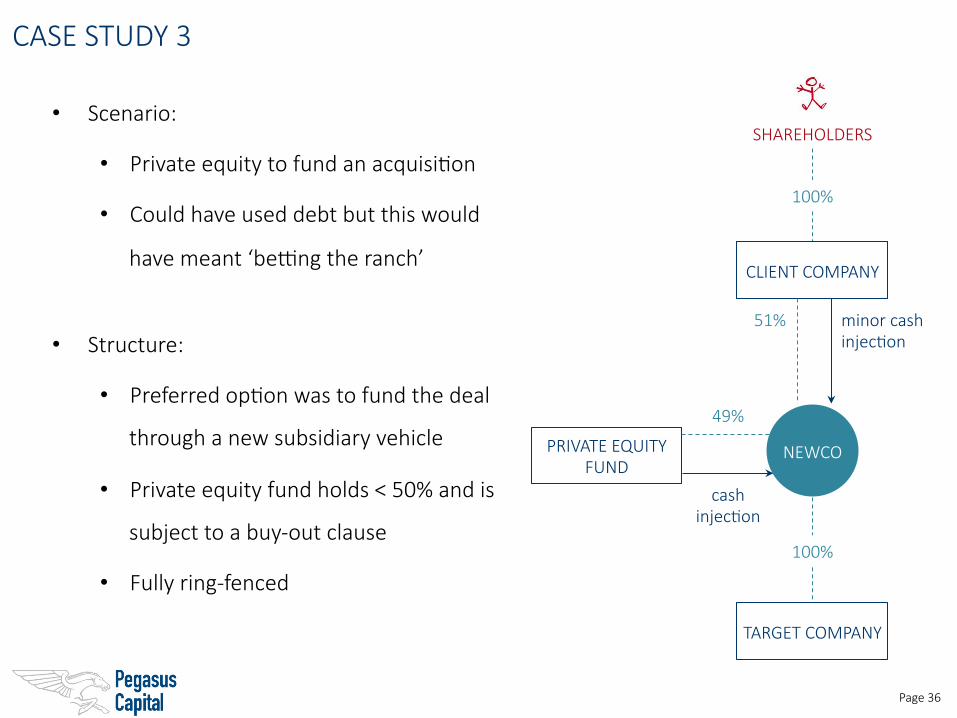

CASE STUDY 3

• Scenario:

• Private equity to fund an acquisiRon

• Could have used debt but this would

have meant ‘be�ng the ranch’

• Structure:

• Preferred opRon was to fund the deal

through a new subsidiary vehicle

• Private equity fund holds < 50% and is

subject to a buy-‐out clause

• Fully ring-‐fenced

NEWCO

CLIENT COMPANY

TARGET COMPANY

100%

SHAREHOLDERS

100%

51% minor cash injecRon

PRIVATE EQUITY FUND

49%

cash injecRon

Page 36

THANK YOU