33

Francois Venter July 2018 South Africa and TLD introduction Huge thanks CHAI, Andy Hill, Polly Clayden, BMGF, PEPFAR Pretoria and USAID/CDC DC, Unitaid, SA MRC

Francois Venter

July 2018

South Africa and

TLD introduction

Huge thanks CHAI, Andy Hill, Polly Clayden, BMGF, PEPFAR Pretoria and

USAID/CDC DC, Unitaid, SA MRC

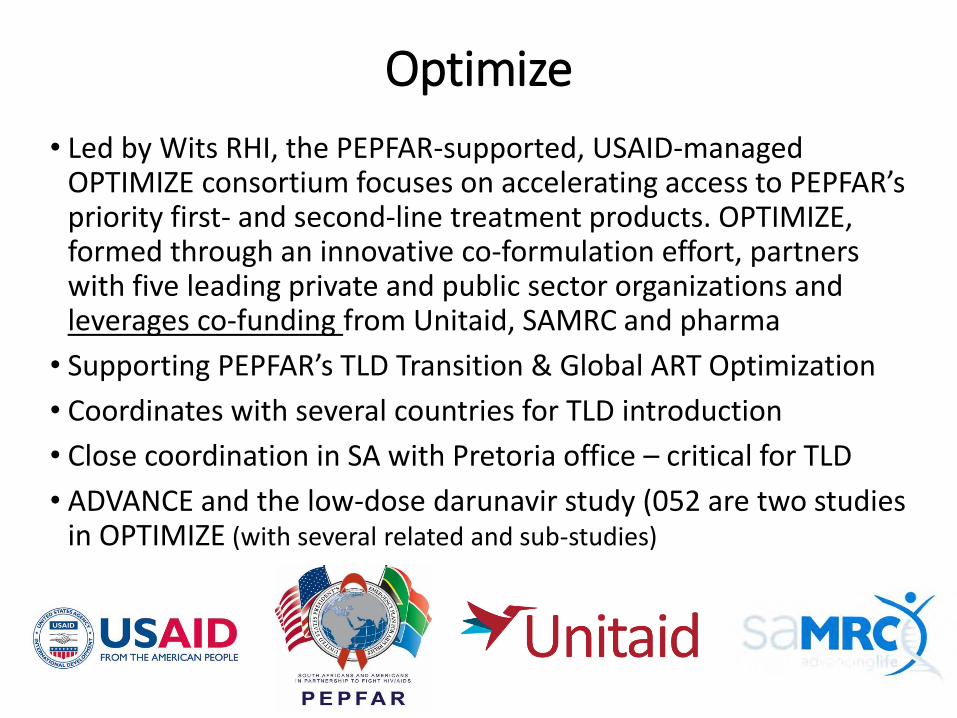

Optimize

• Led by Wits RHI, the PEPFAR-supported, USAID-managed OPTIMIZE consortium focuses on accelerating access to PEPFAR’s priority first- and second-line treatment products. OPTIMIZE, formed through an innovative co-formulation effort, partners with five leading private and public sector organizations and leverages co-funding from Unitaid, SAMRC and pharma

• Supporting PEPFAR’s TLD Transition & Global ART Optimization

• Coordinates with several countries for TLD introduction

• Close coordination in SA with Pretoria office – critical for TLD

• ADVANCE and the low-dose darunavir study (052 are two studies in OPTIMIZE (with several related and sub-studies)

•Almost a fifth of global HIV-positive population

•Almost 5 million people on ART (95% on TEE)

•Procurement giant: SA=PEPFAR=Global Fund for ART generics

•Sustainable programme – mostly funded off SA tax base

•Almost halving of incidence in last 5 years in some demographics – HSRC, July 20128

Why is South Africa important?

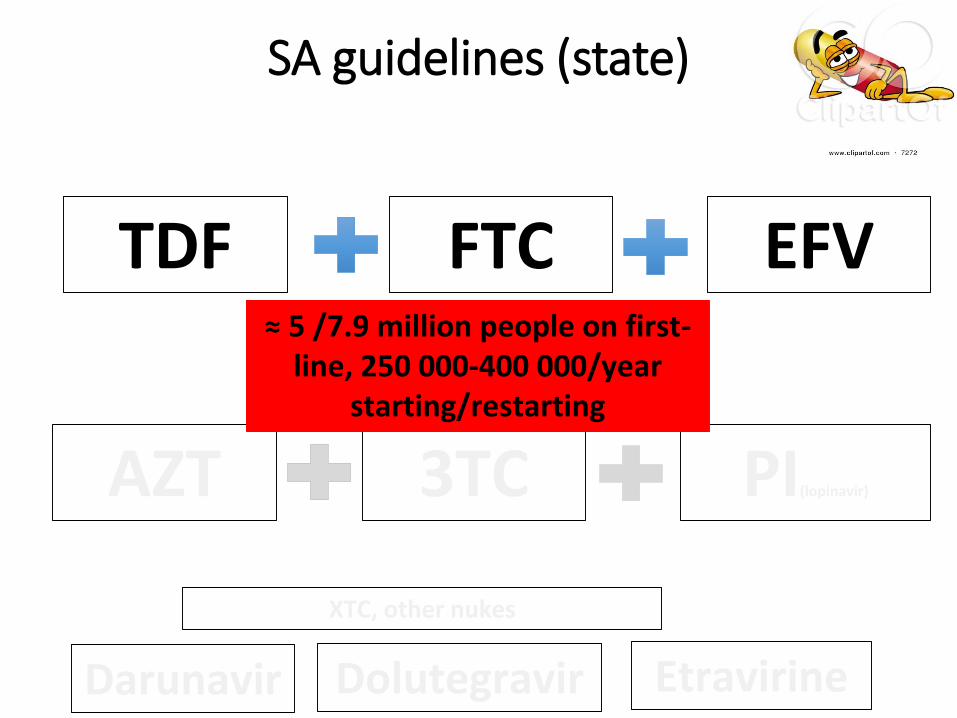

SA guidelines (state)

FTCTDF EFV

XTC, other nukes

3TC PI(lopinavir)AZT

Darunavir Dolutegravir Etravirine

≈ 5 /7.9 million people on first-line, 250 000-400 000/year

starting/restarting

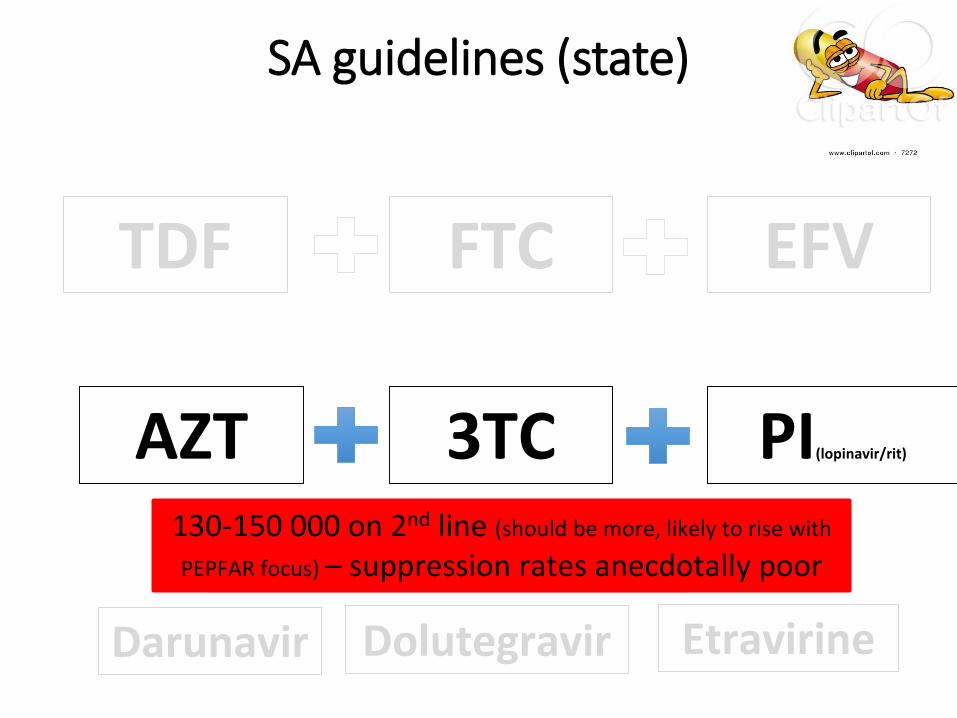

SA guidelines (state)

FTCTDF EFV

XTC, other nukes

3TC PI(lopinavir/rit)AZT

Darunavir Dolutegravir Etravirine

130-150 000 on 2nd line (should be more, likely to rise with

PEPFAR focus) – suppression rates anecdotally poor

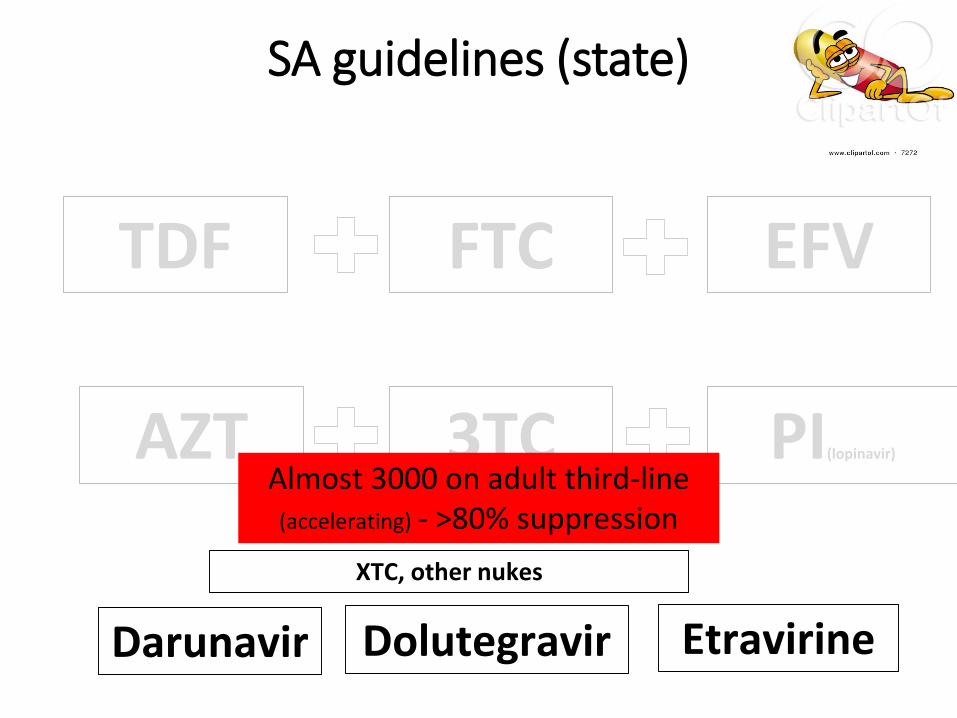

SA guidelines (state)

FTCTDF EFV

XTC, other nukes

3TC PI(lopinavir)AZT

Darunavir Dolutegravir Etravirine

Almost 3000 on adult third-line (accelerating) - >80% suppression

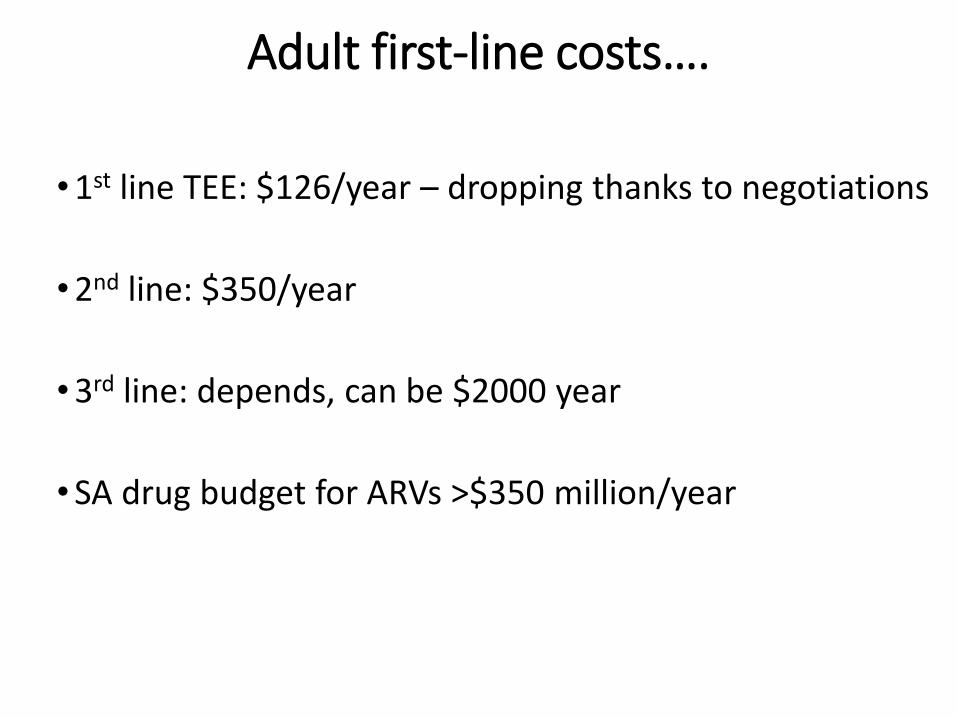

•1st line TEE: $126/year – dropping thanks to negotiations

•2nd line: $350/year

•3rd line: depends, can be $2000 year

•SA drug budget for ARVs >$350 million/year

Adult first-line costs….

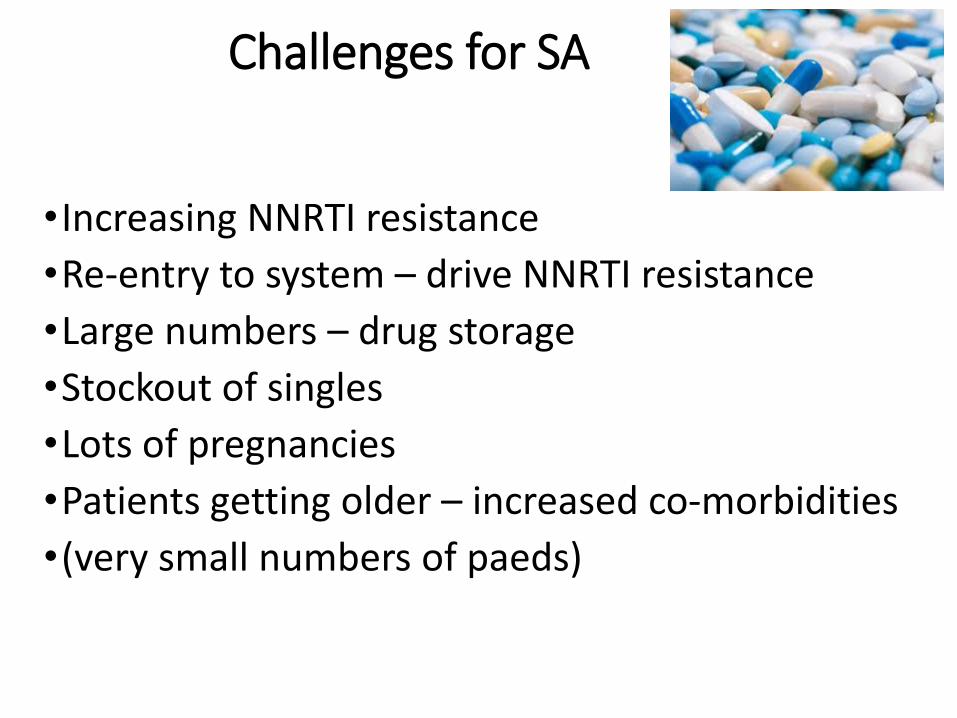

•Increasing NNRTI resistance

•Re-entry to system – drive NNRTI resistance

•Large numbers – drug storage

•Stockout of singles

•Lots of pregnancies

•Patients getting older – increased co-morbidities

•(very small numbers of paeds)

Challenges for SA

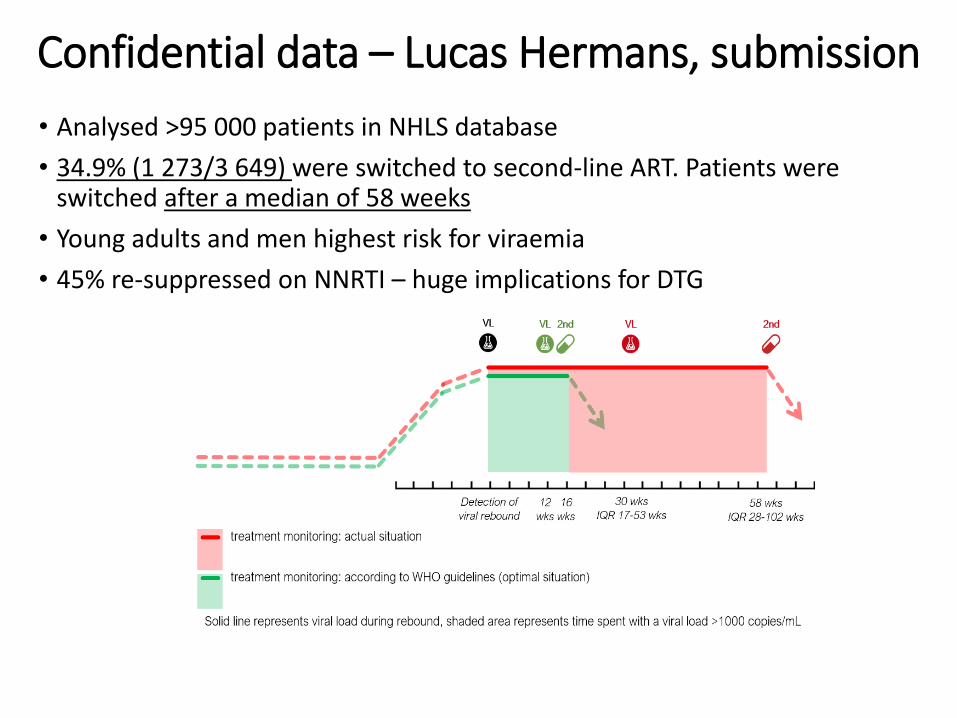

• Analysed >95 000 patients in NHLS database

• 34.9% (1 273/3 649) were switched to second-line ART. Patients were switched after a median of 58 weeks

• Young adults and men highest risk for viraemia

• 45% re-suppressed on NNRTI – huge implications for DTG

Confidential data – Lucas Hermans, submission

“Dolutegravir in first line therapy has by far the highest impact in getting to the last 90 for South Africa”

Professor Gesine Meyer-Rath -Boston University/HE2RO

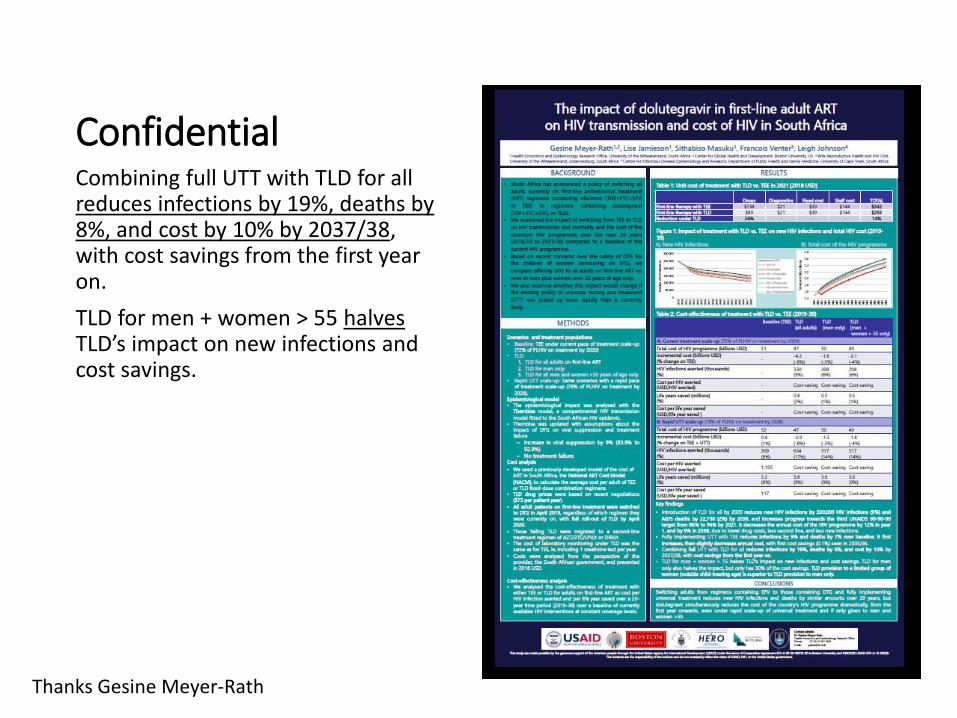

ConfidentialCombining full UTT with TLD for all reduces infections by 19%, deaths by 8%, and cost by 10% by 2037/38, with cost savings from the first year on.

TLD for men + women > 55 halvesTLD’s impact on new infections and cost savings.

Thanks Gesine Meyer-Rath

•Resistance barrier – less second/third-line, simpler adherence message

•Efficacy in context of increasing NNRTI resistance

•Side effects

•Speed of virological control (?PMTCT and sexual transmission benefit)

• Limited drug interactions (especially hormonal contraception)

•Cost

•Size of tablet, packaging

Quick reminder: Benefits of dolutegravir

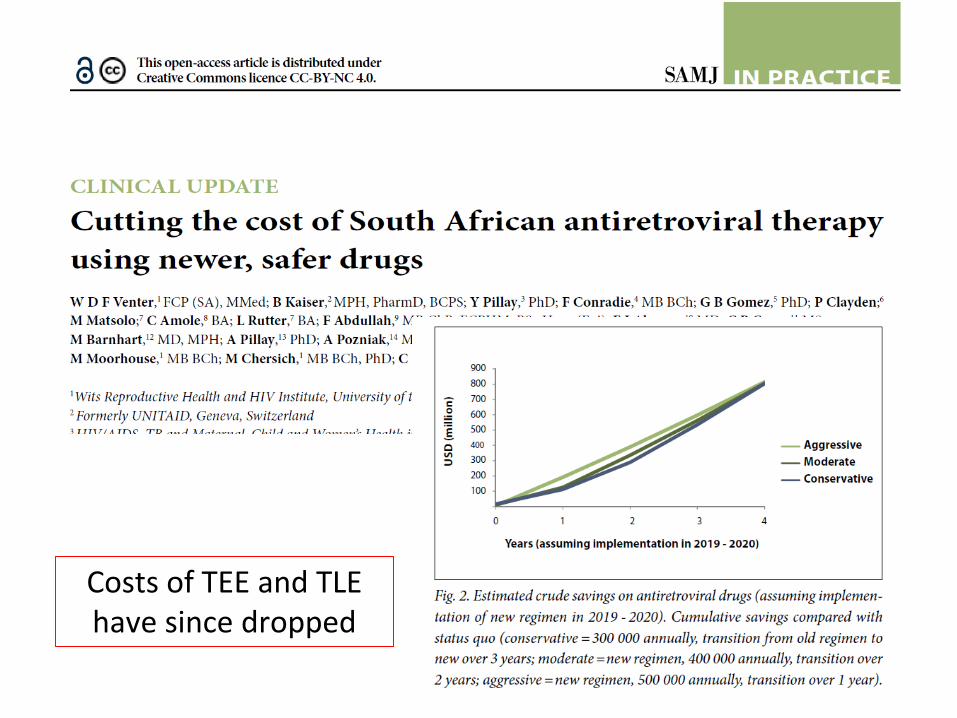

Costs of TEE and TLE have since dropped

Why aren’t these drugs used?

Not preferred options in

WHO guidelines

Many drugs are not

registered and no co-

formulations are available

Limited data on use in TB (almost all new drugs)

Limited data on use in

pregnancy (almost all new drugs)

Costs: abacavir, all

integrase inhibitors –

hope for dolutegravir

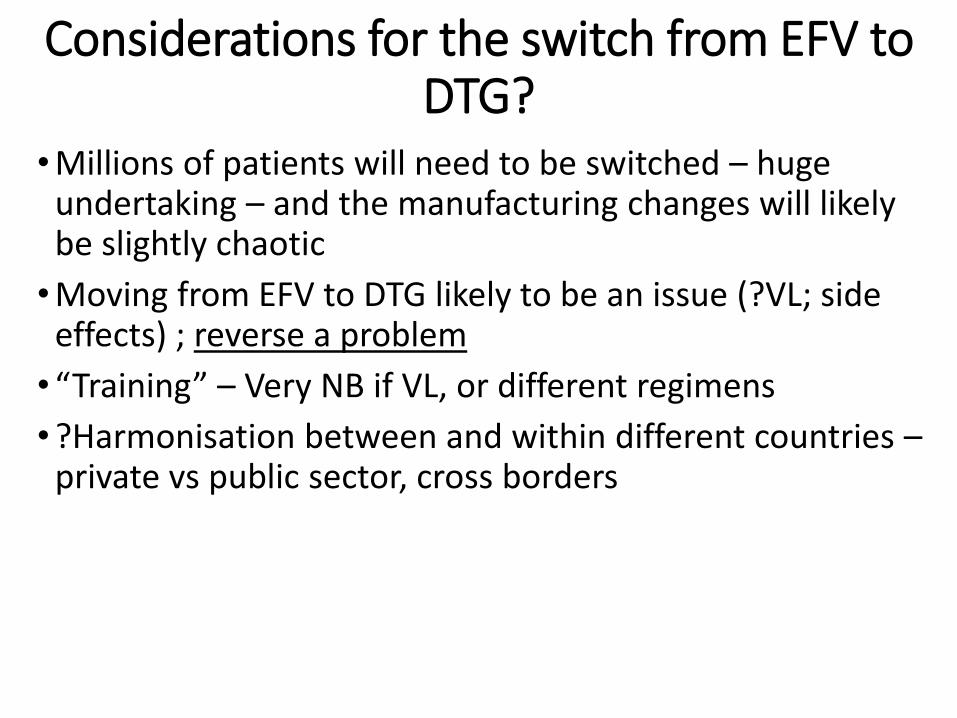

Considerations for the switch from EFV to DTG?

•Millions of patients will need to be switched – huge undertaking – and the manufacturing changes will likely be slightly chaotic

•Moving from EFV to DTG likely to be an issue (?VL; side effects) ; reverse a problem

• “Training” – Very NB if VL, or different regimens

•?Harmonisation between and within different countries –private vs public sector, cross borders

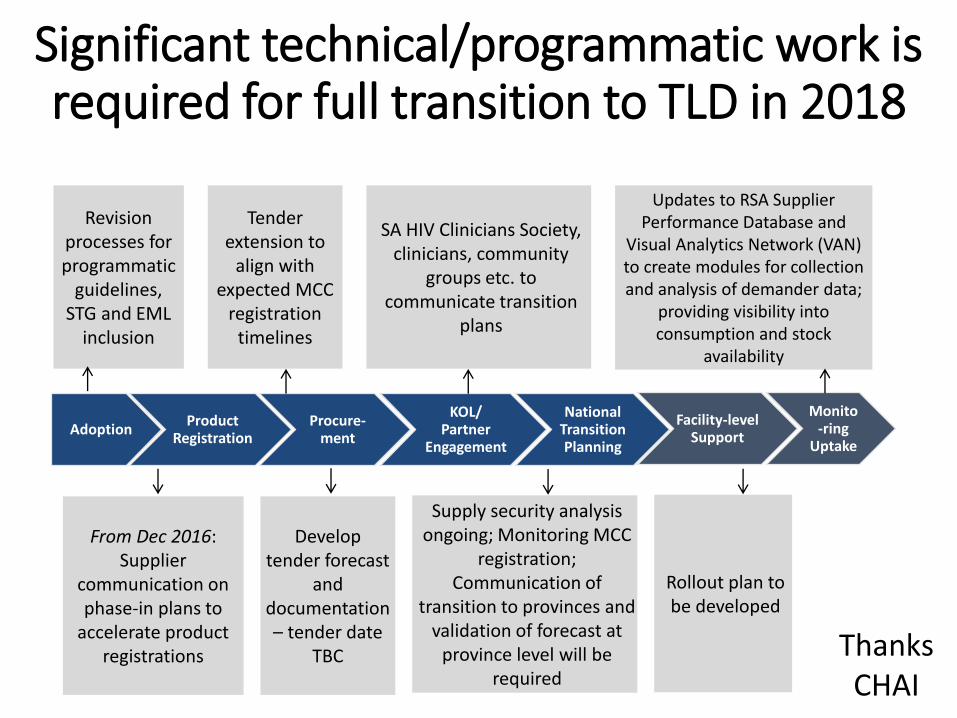

AdoptionProduct

RegistrationProcure-

ment

KOL/Partner

Engagement

National Transition Planning

Facility-level Support

Monito-ring

Uptake

SA HIV Clinicians Society, clinicians, community

groups etc. to communicate transition

plans

Tender extension to

align with expected MCC

registration timelines

Supply security analysis ongoing; Monitoring MCC

registration; Communication of

transition to provinces and validation of forecast at

province level will be required

From Dec 2016: Supplier

communication on phase-in plans to

accelerate product registrations

Revision processes for programmatic

guidelines, STG and EML

inclusion

Develop tender forecast

and documentation – tender date

TBC

Updates to RSA Supplier Performance Database and

Visual Analytics Network (VAN) to create modules for collection and analysis of demander data;

providing visibility into consumption and stock

availability

Rollout plan to be developed

Significant technical/programmatic work is required for full transition to TLD in 2018

Thanks CHAI

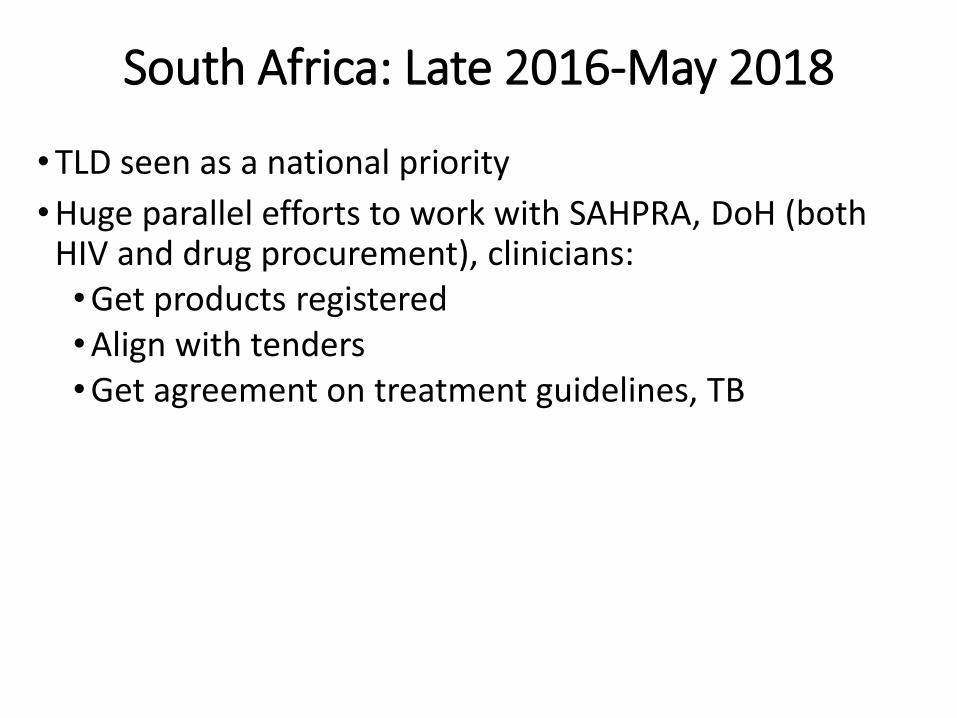

South Africa: Late 2016-May 2018

•TLD seen as a national priority

•Huge parallel efforts to work with SAHPRA, DoH (both HIV and drug procurement), clinicians:•Get products registered•Align with tenders•Get agreement on treatment guidelines, TB

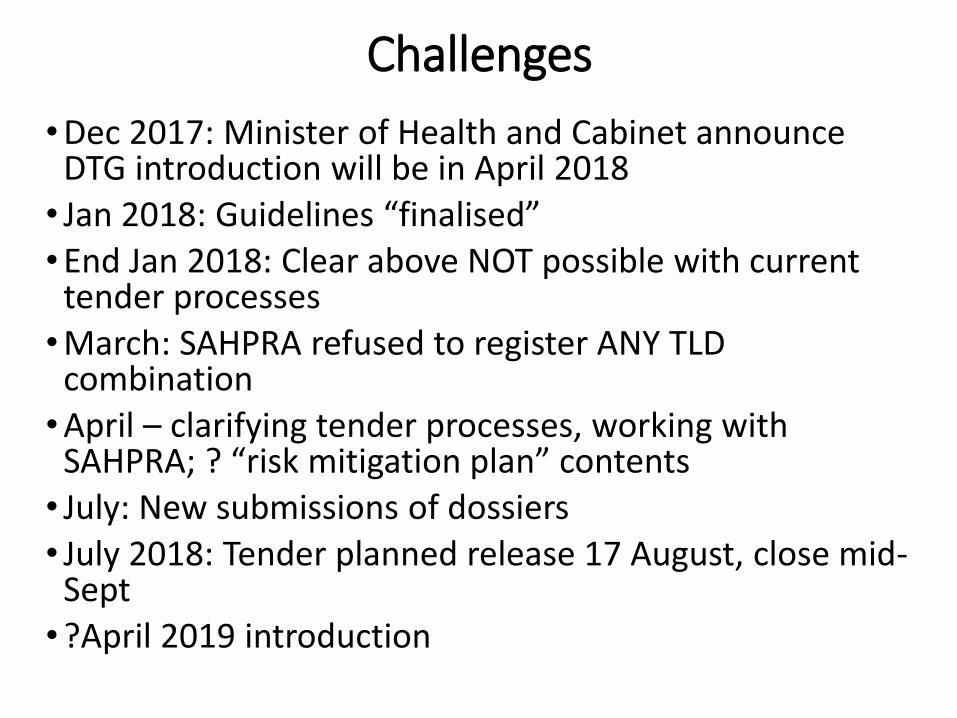

Challenges

•Dec 2017: Minister of Health and Cabinet announce DTG introduction will be in April 2018• Jan 2018: Guidelines “finalised”•End Jan 2018: Clear above NOT possible with current

tender processes•March: SAHPRA refused to register ANY TLD

combination•April – clarifying tender processes, working with

SAHPRA; ? “risk mitigation plan” contents• July: New submissions of dossiers• July 2018: Tender planned release 17 August, close mid-

Sept•?April 2019 introduction

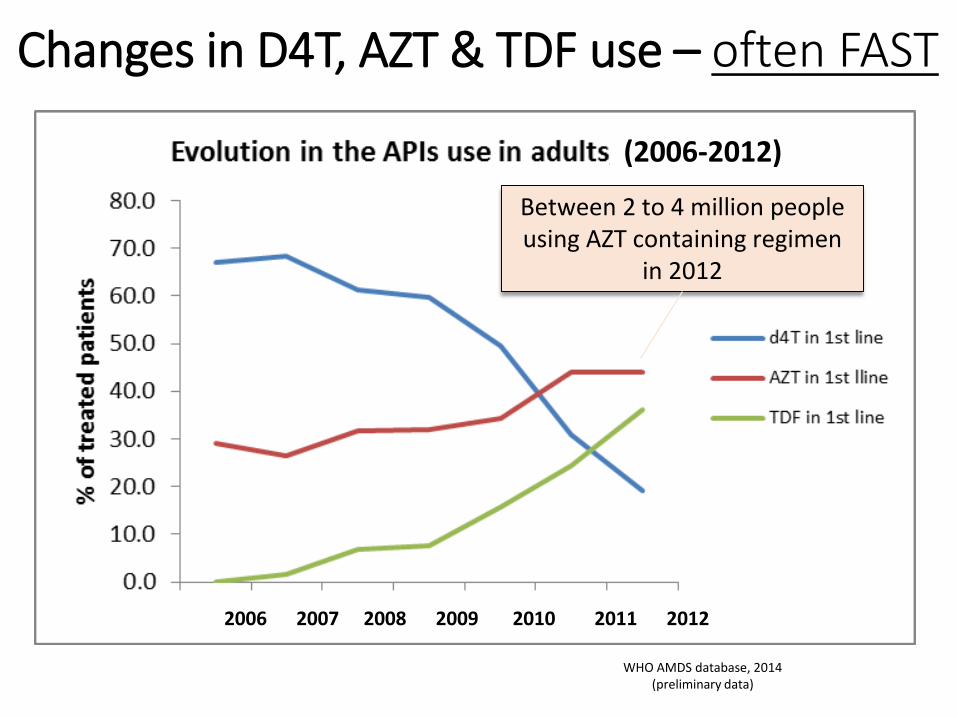

Changes in D4T, AZT & TDF use – often FAST

Between 2 to 4 million people using AZT containing regimen

in 2012

2006 2007 2008 2009 2010 2011 2012

(2006-2012)

WHO AMDS database, 2014 (preliminary data)

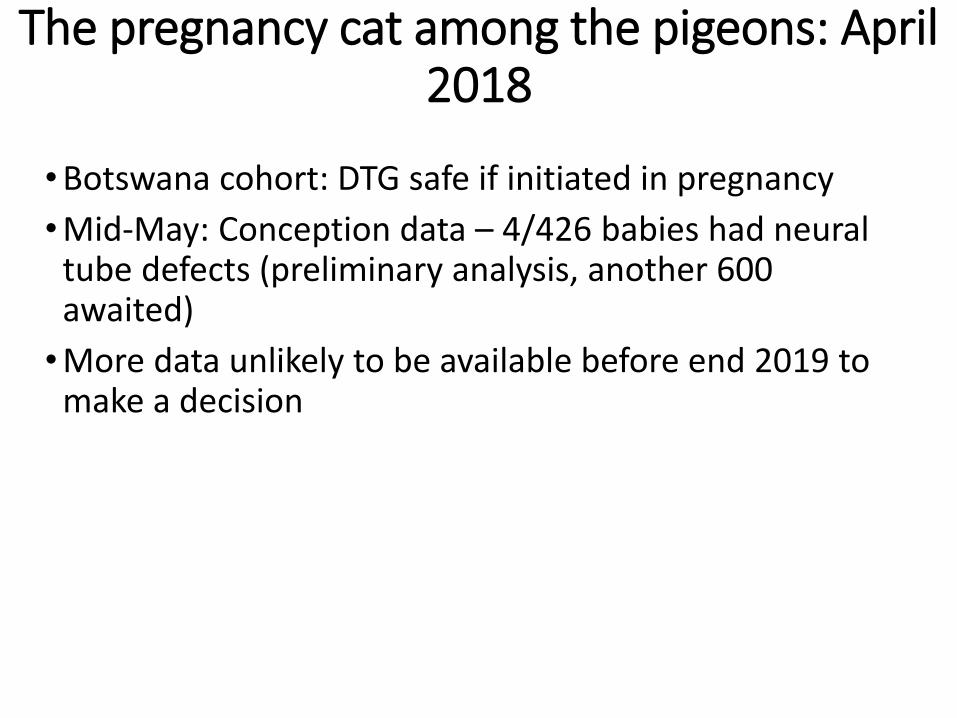

The pregnancy cat among the pigeons: April 2018

•Botswana cohort: DTG safe if initiated in pregnancy

•Mid-May: Conception data – 4/426 babies had neural tube defects (preliminary analysis, another 600 awaited)

•More data unlikely to be available before end 2019 to make a decision

SAHPRA: willing to register TLD if:

•Provided with scientific rationale by OPTIMIZE and WHO

CheckBox1

SAHPRA: willing to register products if:

•Provided with scientific rationale by OPTIMIZE and WHO

• Immediate access to early ADVANCE data, with subsequent access to the data till 96 weeks

CheckBox1

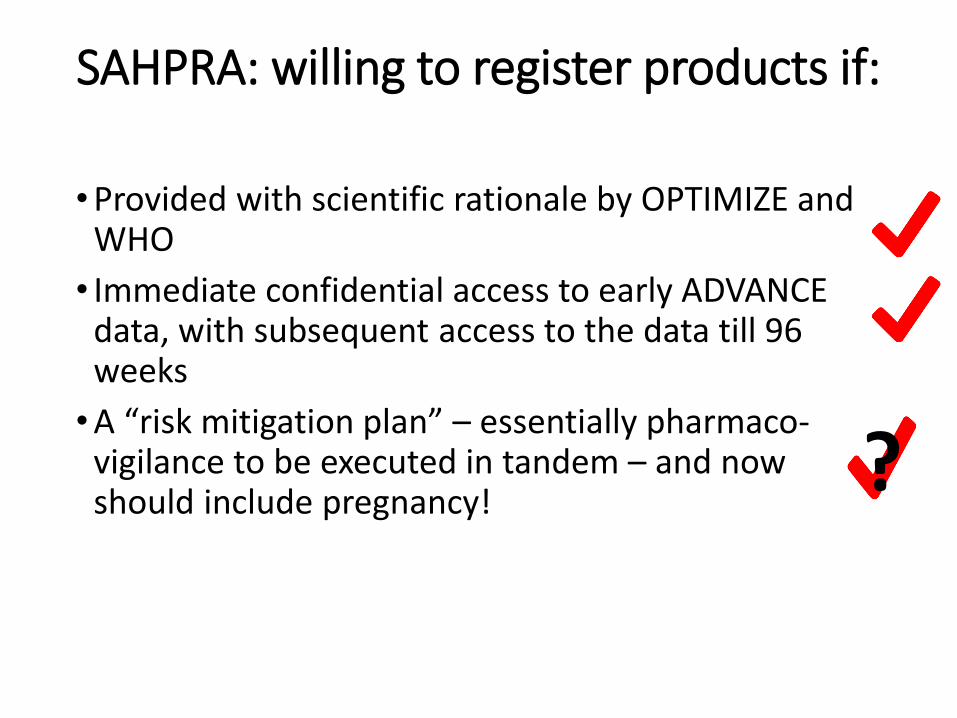

SAHPRA: willing to register products if:

•Provided with scientific rationale by OPTIMIZE and WHO

• Immediate confidential access to early ADVANCE data, with subsequent access to the data till 96 weeks

•A “risk mitigation plan” – essentially pharmaco-vigilance to be executed in tandem – and now should include pregnancy!

?

CheckBox1

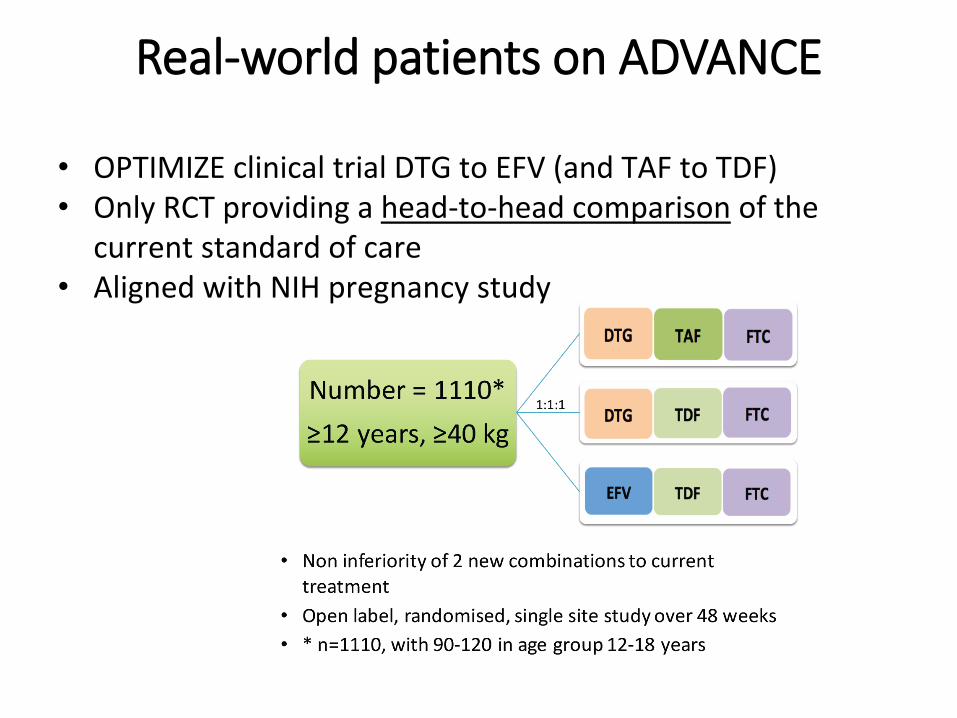

Real-world patients on ADVANCE

• OPTIMIZE clinical trial DTG to EFV (and TAF to TDF)• Only RCT providing a head-to-head comparison of the

current standard of care• Aligned with NIH pregnancy study

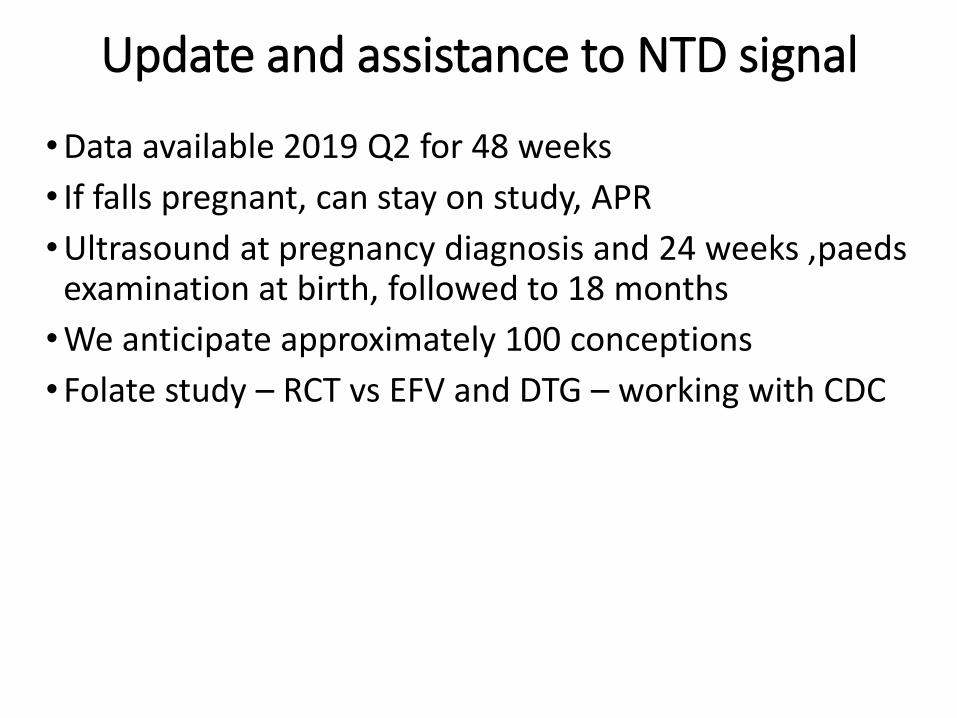

Update and assistance to NTD signal

•Data available 2019 Q2 for 48 weeks

• If falls pregnant, can stay on study, APR

•Ultrasound at pregnancy diagnosis and 24 weeks ,paedsexamination at birth, followed to 18 months

•We anticipate approximately 100 conceptions

•Folate study – RCT vs EFV and DTG – working with CDC

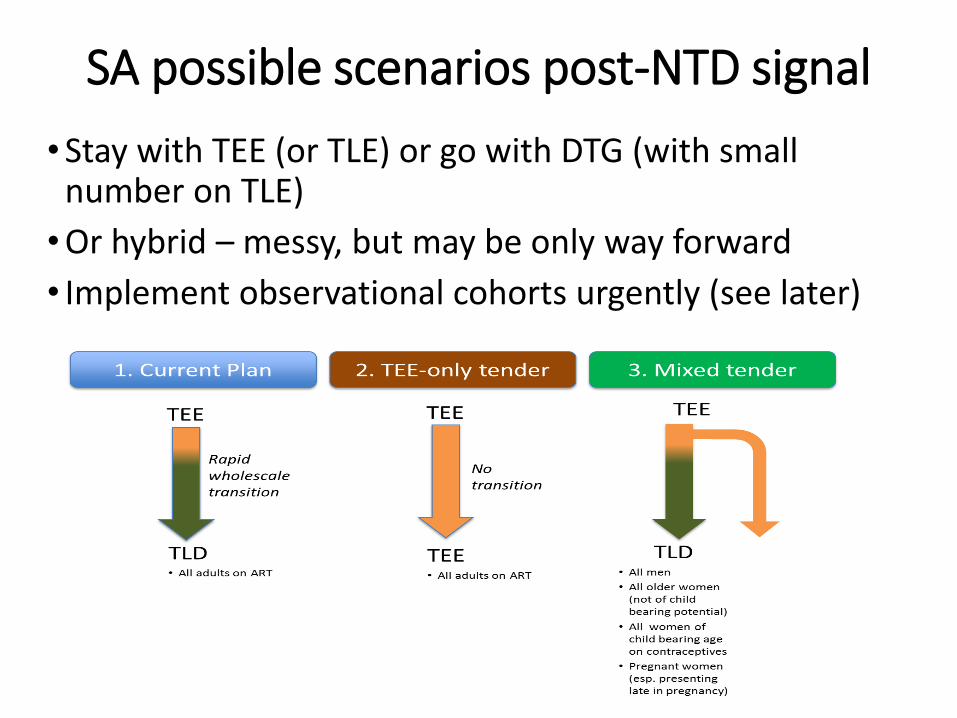

SA possible scenarios post-NTD signal

•Stay with TEE (or TLE) or go with DTG (with small number on TLE)

•Or hybrid – messy, but may be only way forward

• Implement observational cohorts urgently (see later)

Second-line patients in DTG era?

• Lots of concern that DTG not as powerful as PI-based regimens – possibly:•AZT/3TC/DTG if failing TLE/TEE•AZT/3TC/PI if failing TLD (will be rare!)•Suppressed on PI (and never failed d4T/AZT)

What about TAF?

•10-15% saving (manufacturing cost, packaging). ?safety benefit, tablet much small

•Paucity of data – addressed with ADVANCE (TAF arm) partially, TB

•Pregnancy and breastfeeding a concern – 7-8x increase in intracellular tenofovir levels vs conventional TDF

•?2021 introduction – same issues for SAHPRA?

What about darunavir/ritonavir?

•Will be SOME need for second-line

•Current 800/100 or 400/100mg dose can be dose reduced with nanotechnology – big cost saving, potential FDC

•This conference: 400/100mg works as a switch

What about 400mg efavirenz?

•Probably will be recommended as replacing the 600mg dose

•Caution: NAMSAL data due

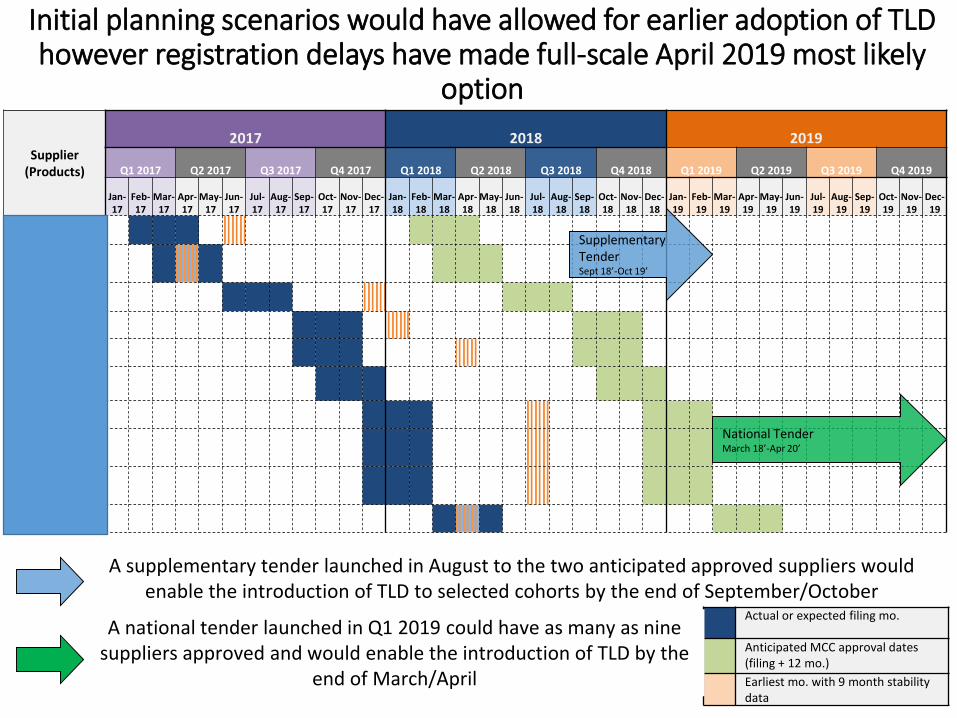

Supplier (Products)

2017 2018 2019

Q1 2017 Q2 2017 Q3 2017 Q4 2017 Q1 2018 Q2 2018 Q3 2018 Q4 2018 Q1 2019 Q2 2019 Q3 2019 Q4 2019

Jan-17

Feb-17

Mar-17

Apr-17

May-17

Jun-17

Jul-17

Aug-17

Sep-17

Oct-17

Nov-17

Dec-17

Jan-18

Feb-18

Mar-18

Apr-18

May-18

Jun-18

Jul-18

Aug-18

Sep-18

Oct-18

Nov-18

Dec-18

Jan-19

Feb-19

Mar-19

Apr-19

May-19

Jun-19

Jul-19

Aug-19

Sep-19

Oct-19

Nov-19

Dec-19

Filing Filing Filing 9 Month Stability Approval Approval Approval

Filing Both Filing and Stability Filing Approval Approval Approval

Filing Filing Filing 9 Month Stability Approval Approval Approval

Filing Filing Filing 9 Month Stability Approval Approval Approval

Filing Filing Filing 9 Month Stability Approval Approval Approval

Filing Filing Filing Approval Approval Approval

Filing Filing Filing 9 Month Stability Approval Approval Approval

Filing Filing Filing 9 Month Stability Approval Approval Approval

Filing Filing Filing 9 Month Stability Approval Approval Approval

Filing Both Filing and Stability Filing Approval Approval Approval

As we stand now, only 2-4 TLD suppliers could possibly be registered

Actual or expected filing mo.

Anticipated MCC approval dates (filing + 12 mo.)

Earliest mo. with 9 month stability data

A supplementary tender launched in August to the two anticipated approved suppliers would enable the introduction of TLD to selected cohorts by the end of September/October

SupplementaryTenderSept 18’-Oct 19’

National TenderMarch 18’-Apr 20’

A national tender launched in Q1 2019 could have as many as nine suppliers approved and would enable the introduction of TLD by the

end of March/April

Initial planning scenarios would have allowed for earlier adoption of TLD however registration delays have made full-scale April 2019 most likely option

Initial planning scenarios would have allowed for earlier adoption of TLD however registration delays have made full-scale April 2019 most likely

option

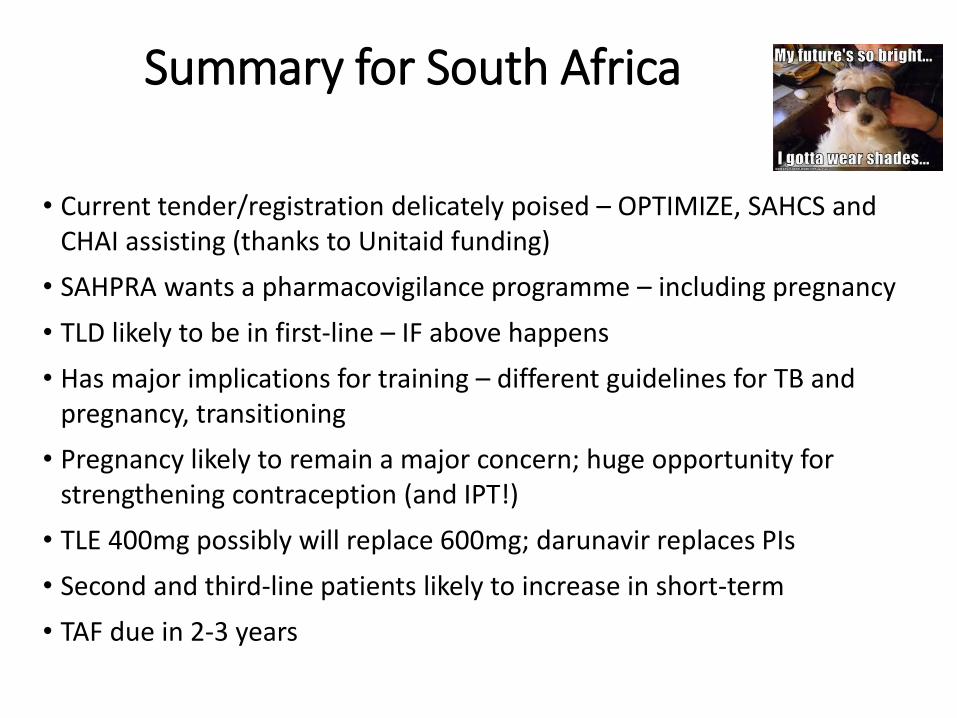

Summary for South Africa

• Current tender/registration delicately poised – OPTIMIZE, SAHCS and CHAI assisting (thanks to Unitaid funding)

• SAHPRA wants a pharmacovigilance programme – including pregnancy

• TLD likely to be in first-line – IF above happens

• Has major implications for training – different guidelines for TB and pregnancy, transitioning

• Pregnancy likely to remain a major concern; huge opportunity for strengthening contraception (and IPT!)

• TLE 400mg possibly will replace 600mg; darunavir replaces PIs

• Second and third-line patients likely to increase in short-term

• TAF due in 2-3 years

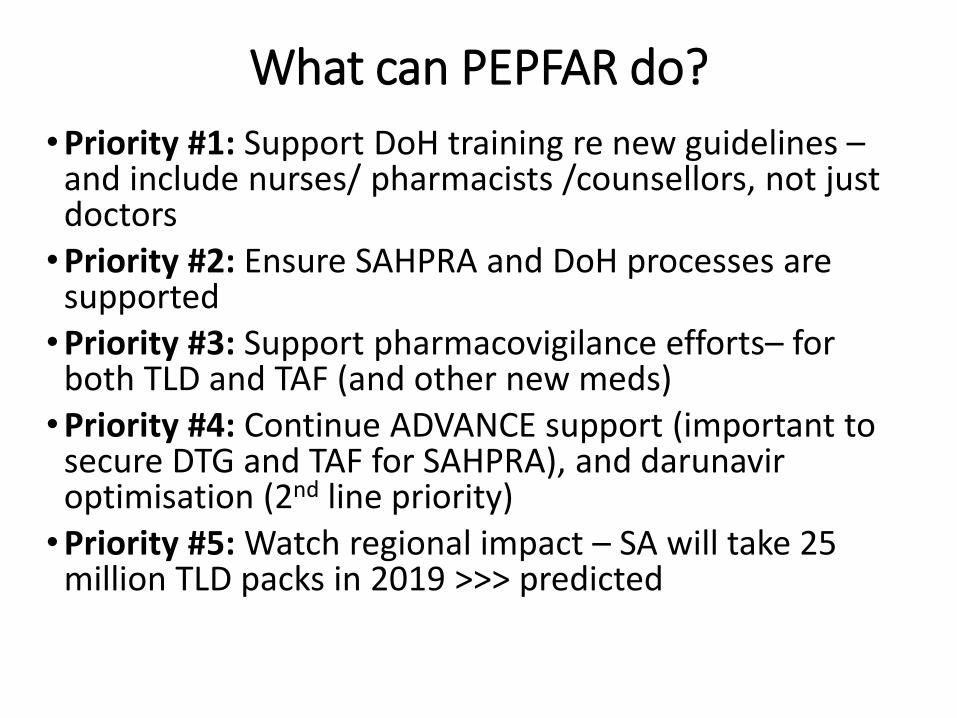

What can PEPFAR do?

•Priority #1: Support DoH training re new guidelines –and include nurses/ pharmacists /counsellors, not just doctors•Priority #2: Ensure SAHPRA and DoH processes are

supported•Priority #3: Support pharmacovigilance efforts– for

both TLD and TAF (and other new meds)•Priority #4: Continue ADVANCE support (important to

secure DTG and TAF for SAHPRA), and darunaviroptimisation (2nd line priority)•Priority #5: Watch regional impact – SA will take 25

million TLD packs in 2019 >>> predicted