South African Property Review is the official voice of the South African Property Owners Association, a B2B publication which is also available in print and distributed to a targeted audience of the leading commercial property owners in South Africa

68

SOUTH AFRICAN PROPERTY REVIEW July 2015 South African Property Review Financial and Investments July 2015 NEW KID ON THE BLOCK Newtown Junction takes top honours THE PULSE OF THE BAY Baywest Mall opens its doors FINANCE AND INVESTMENT FOCUS Deconstructing investing in property Ireland: Celtic Tiger rises T h e W O R L D s e r i e s ● O u r m o n t h l y c o u n t r y - b y - c o u nt r y f o c u s ● FURTHERING EDUCATION The SAPOA Bursary Fund’s biggest achievement

Transcript

S O U T H A F R I C A N

PROPERTYR E V I E W

July 2015

South African P

roperty Review

Financial and Investments

July 2015

NEW KID ON THE BLOCKNewtown Junction takes top honours

THE PULSE OF THE BAYBaywest Mall

opens its doors

FINANCE ANDINVESTMENT FOCUS

Deconstructing investingin property

Ireland: Celtic Tiger rises

The

WORLD series ● Our monthly country-by-country focus ●

Cover with Spine_JULY_SUBBED.indd 1 2015/06/15 8:13 AM

40 SOUTH AFRICAN PROPERTY REVIEW

development

Baywest Mall_SUBBED.indd 40 2015/06/19 9:33 AM

S O U T H A F R I C A N

PROPERTYR E V I E W

July 2015

2 From the CEO5 From the Editor’s desk10 Industry news13 Legal update DTI turnaround on Broad Based Empowerment14 Education, training and development18 Planning and development Planning education in South Africa20 Theme leader Deconstructing investing in property24 Eye on the world Ireland28 SAPOA Bursary Fund32 Interview Durban in the hot seat38 Feature The pulse of the bay41 REIT investments42 Eco-mobility breakfast46 Investors to increase acquisitions in 201548 Workshop Collaborating with government50 Inspired over breakfast52 Mingling at the Michelangelo54 Breakfast session at Umhlanga Rocks56 Statistics58 Profi les60 What’s on Upcoming events63 Fun & quirky JT Foxx Q&A64 Off the wall Designing to keep the lights on

ON THE COVERThe R1,4-billion Newtown Junction mixed-use development in the Jo’burg CBD took top honours and scooped multiple awards at the 2015 SAPOA Annual Innovative Excellence in Property Development Awards

Editor in Chief Neil Gopal Editorial Advisor Jane Padayachee Managing Editor Mark Pettipher Copy Editor Ania Rokita Production Manager Dalene van Niekerk

Designers Wade Hunkin, Dirk Knoesen Sales Riëtte Stevens Finance Susan du Toit Contributors Anne Schau� er, Eugenia Makgabo, Lekgolo Mayatula,

Martin Ferguson Photographers Mark Pettipher, Xavier Sauer, Pierre van der Spuy

DISCLAIMER: The publisher and editor of this magazine give no warranties, guarantees or assurances and make no representations regarding any goods or services advertised within this edition. Copyright South African Property Owners’ Association (SAPOA).

All rights reserved. No portion of this publication may be reproduced in any form without prior written consent from SAPOA. The publishers are not responsible for any unsolicited material.

Designed, written and produced for SAPOA by MPDPS (PTY) Ltde: [email protected]

Published by SAPOA, Paddock View, Hunt’s End O� ce Park, 36 Wierda Road West, Wierda Valley, SandtonPO Box 78544, Sandton 2146

Cover with Spine_JULY_SUBBED.indd 1 2015/06/15 8:13 AM

Contents_JULY_SUBBED.indd 1 2015/06/15 11:38 AM

2 SOUTH AFRICAN PROPERTY REVIEW

from the CEO

Commercial property rates and taxes – a comparison

SAPOA CEO Neil Gopal highlights the comparisons regarding commercial property rates and taxes across South Africa’s eight metropolitan municipalities

SAPOA’s comparison of the level of rates and taxes levied in each of the eight

metropolitan municipalities reveals some variance in the cents in the rand rate across the main property types.

The latest rates and taxes research from SAPOA highlights the huge disparity between the country’s major cities in terms of the resources available to deal effectively with ongoing urbanisation, unemployment, poverty and inequality.

Within the context of the National Development Plan’s emphasis on major cities being the engines of economic growth, these disparities and the shortcomings they reveal need to be addressed as a matter of urgency.

The research also confirms that over the last decade, rates and taxes have consistently increased at a rate higher than inflation, with a rates and taxes annualised rate of inflation of +8,2% during the period from 2005 to 2014.

Although prior to this the increase in rates and taxes exceeded inflation, acceleration in growth has been more noticeable since 2005.

From solely a rates randage perspective, for the fiscal year of 2014/2015, the highest level of commercial property rate randage was levied in the eThekwini Municipality, where a rate of 3,053 cents in the rand applied to industrial property. Commercial and business property saw a slightly lower tariff of 2,36 cents in the rand being applied.

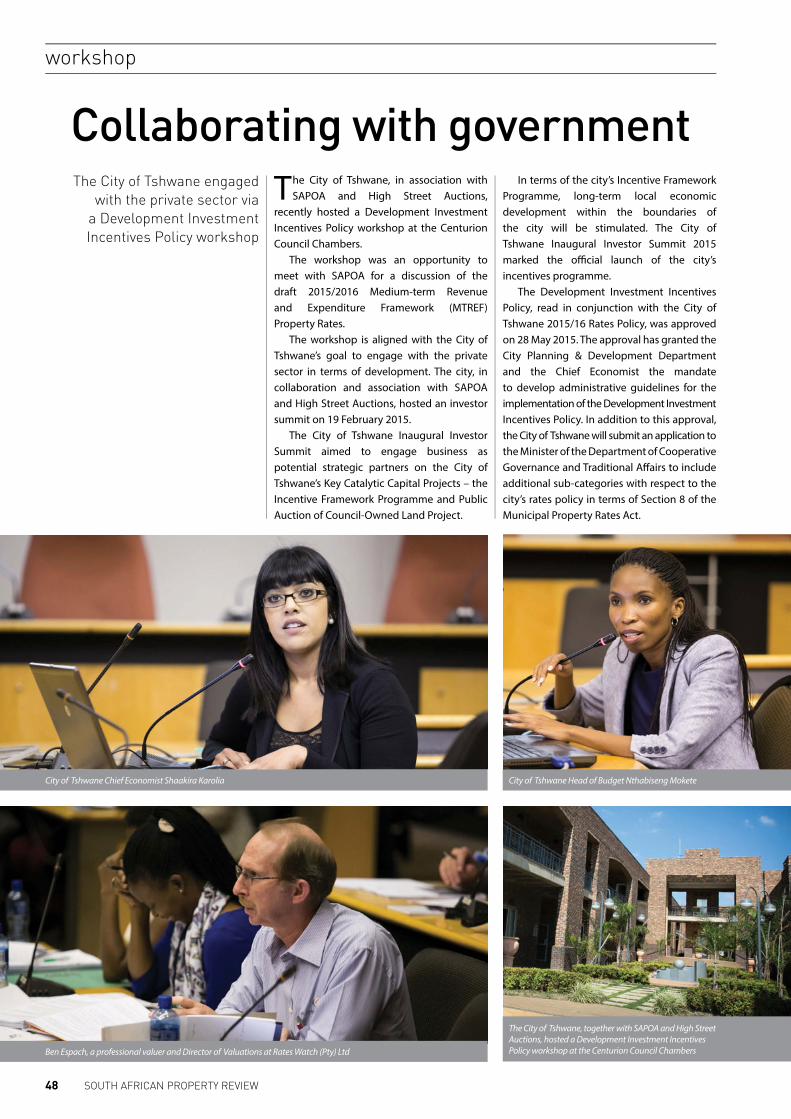

development and job creation. Investments include more than 65 flagship projects across the city, from manufacturing, construction and real estate to tourism, information communication technology, agriculture, maritime and logistics.

The projects are expected to create about 680 000 permanent jobs in the long term and bring in potential revenue of about R9-billion for the city.

The municipality has established a project-management office whose main role is the facilitation of the implementation of catalytic projects such as inner-city renewal in addition to building capacity.

Mayor Nxumalo said that in drafting the tariff increases, the city took cognisance of economic conditions, input costs and the affordability of services to ensure the financial sustainability of the city.

Rates and taxes form a significant percentage of overall municipal revenue, with the eight metro municipalities collecting R29-billion in rates and taxes – 17,9% of total revenue.

During the 2013/2014 fiscal cycle, commercial and industrial property rates billings amounted to 54,5% of overall rates revenue in the country’s metropolitan municipalities, with significantly lower levels of arrears than commercial clients.

Of the eight metro municipalities, six reported increases of more than 30% in the value of commercial and industrial properties. Mangaung reported the largest increase, with the valuation of its commercial property almost increasing, while eThekwini reported a municipal valuation increase of 50%. Tshwane and Buffalo City were the only municipalities with a valuation increase close to inflation, with 5,6% and 4,7% respectively.

The increase in rates and taxes comes in a much tougher macroeconomic environment, with economic growth currently at levels of only about half of that during the period between 2004 and 2007. As a result of this tougher trading environment, it is becoming increasingly challenging for landlords to deal with the additional tax burden.

Neil Gopal, CEO

The City of Tshwane reported the second-highest cents in the rand rate, with industrial and business property both taxed at 2,71. The lowest rates applied to the City of Cape Town, with both industrial and commercial property taxed at 1,25 cents in the rand.

The largest municipality in terms of revenue, the City of Johannesburg, applied a rate of 1,73 cents in the rand, while Nelson Mandela Bay, Buffalo City and Mangaung (the three smaller metros) had comparatively high commercial property rate randages.

It must be noted that the rate randages do not necessarily result in higher property rates as this is predominantly affected by the actual property value. The case of the eThekwini Municipality is therefore instructive.

While the eThekwini Municipality’s rate randages come out as the highest, the number of rateable properties is more than 60% less than both Cape Town and Johannesburg, and the value of commercial and industrial properties is more than half that of Johannesburg and nearly half that of Cape Town.

This can be seen with eThekwini having the least quantum of rates revenue of the three major cities. Furthermore, within eThekwini, more than 90% of the total rateable property is residential, resulting in a major challenge for the municipality.

The nett effect is therefore a higher rate randage than in the other major cities but not necessarily higher property rates. Rates revenue is a critical source of revenue within every municipality, and the huge challenges within eThekwini force it to rely heavily on such revenue.

Presenting the highlights of the city’s budget, eThekwini Municipality Mayor James Nxumalo said a large portion of the municipality’s R6,1-billion capital budget will be pumped into low-cost housing and infrastructure development throughout the city, with the aim of creating an enabling environment for new investments and other activities that lead to job creation.

Mayor Nxumalo confirmed the city’s commitment to building a sustainable city for future generations, based on infrastructure-led growth, unlocking investment, economic

CEO_JULY_revised_SUBBED.indd 2 2015/06/15 8:25 AM

3SOUTH AFRICAN PROPERTY REVIEW

from the CEO

CEO_JULY_revised_SUBBED.indd 3 2015/06/15 8:28 AM

4 SOUTH AFRICAN PROPERTY REVIEW

from the Editor’s desk

STRONG RELATIONSHIPS ARE BUILT ON SOLID FOUNDATIONS

We know the importance of relationships.Working together allows us to understandyour needs so we can off er the best realestate solutions for you. With over 152 yearsof banking experience, this is how we’re moving real estate forward.

They call it Africa. We call it home.

www.standardbank.co.za/cib

Authorised financial services and registered credit provider (NCRCP15).The Standard Bank of South Africa Limited (Reg. No. 1962/000738/06). SBSA 204201 – 04/15Moving Forward is a trademark of The Standard Bank of South Africa Limited

204201 Real Estate NIGERIA Portrait SA A4.indd 1 2015/04/02 2:37 PMEd's Letter_JULY_SUBBED.indd 4 2015/06/15 8:33 AM

5SOUTH AFRICAN PROPERTY REVIEW

from the Editor’s desk

In February 2014 I wrote my very � rst editor’s letter for SAPOA’s South African Property Review.

Now, 18 months later, I’m writing my last.I dug up my � rst editor’s letter and

reminisced on what was written. “With a passion for writing and expression and a piqued interest in current a� airs, I always knew I would be involved in the media industry. But I never imagined that I would become the editor of a commercial property magazine – two, in fact.”

The letter continued with, “The South African Property Review and the Property Developer are exceptional titles that have helped to shape my career as a journalist. Property is a fascinating thing. It not only represents our built environment but it de� nes our existence as humans.”

Property still remains fascinating to me and my time as Editor of the South African Property Review has been a phenomenal experience. I have grown and learnt a great deal about the property industry in South Africa, its people and its passions.

I would like to thank Immediate Past President Amelia Beattie for teaching me about the REAL in real estate, SAPOA Chief Executive O� cer Neil Gopal for his leadership, and the SAPOA sta� for their assistance with the publications.

I would also like to extend a warm thanks to the publishing and sales team of SAPOA’s publications – without you, this product wouldn’t be the success that it is.

Lastly, I want to thank all those who play a role in the property industry. Thank you for your guidance, your insight and the wonderful stories that you helped shape for the South African Property Review and Property Developer.

I wish the next editor all the best and hope that they will carry and nurture this baby into the future. My journey has been fun – and it’s de� nitely not the end.

Farewell, Property DeveloperSAPOA Publications will also be bidding a farewell to the quarterly Property Developer. The May 2015 edition was the last stand-alone issue of Property Developer.

But this isn’t goodbye: the publication will be incorporated into the South African Property Review. Once every quarter, the magazine will be beefed up with development content, adding further value to SAPOA’s core monthly publication.

SAPOA would like to thank all clients who have advertised in the Property Developer. Your support has been unrelenting.

Signing offIn her fi nal issue of the South African Property Review, SAPOA Publications Editor Candace King refl ects on her journey

DeveloperPRO

PER

TY

February 2014

Modderfontein metropolisShanghai Zendai’s city plan

Towering feat: a catalyst for investment38

Cornubia: Durban’s mixed-use marvel35

Cover_FEB_SUBBED.indd 1 2014/01/15 10:03 AM

DeveloperPRO

PER

TY

May 2014

Mall of AfricaAtterbury’s retail roll-out: the sky’s the limit

Developing an oceanic fairy tale28

A work in progress

18

Cover_MAY_SUBBED.indd 1 2014/04/08 8:45 AM

DeveloperPRO

PER

TY

May 2015

Introducing Tongaat Hulett

Addressing Africa: RICS Africa Summit 22

Lords View: A green view on things 28

Cover_MAY_SUBBED.indd 1 2015/04/29 10:03 AM

2015/04/02 2:37 PM

from the Editor’s desk

Ed's Letter_JULY_SUBBED.indd 5 2015/06/15 8:50 AM

6 SOUTH AFRICAN PROPERTY REVIEW

from the CEO’s desk

6

The DirectorLand Use and Soil ManagementDepartment of Agriculture, Forestry and FisheriesPrivate Bag X120PRETORIA0001

4 June 2015

SAPOA COMMENTS: DRAFT POLICY AND BILL ON PRESERVATION AND DEVELOPMENT OF AGRICULTURAL LAND FRAMEWORK

INTRODUCTION

1.1. The South African Property Owners Association is the representative body and o� cial voice of the commercial and

industrial property industry in South Africa.1.2. SAPOA was established in 1966 by the leading and large property investment organisations to bring together all

role players in the commercial property � eld and create a powerful platform for property investors.

1.3. SAPOA is recognised as the representative body and o� cial voice of the commercial and industrial property

industry in South Africa, with a combined portfolio in excess of R500 billion. SAPOA members control approximately

90% of all commercial and industrial property in South Africa.

1.4. It is thus clear that SAPOA has a direct and substantial interest in the bill under discussion.

1.5. From what follows it is clear that the structure of the bill with respect to the subdivision and rezoning of agricultural land is

unconstitutional in that it falls foul of the provisions of sections 156(1) and 41(£) of the Constitution as read with schedule

4 Part B, whereby municipalities have executive authority in respect of municipal planning, as explained more fully below.

1.6. It furthermore falls foul of section 155(7) of the Constitution whereby national government and the legislative and

executive authority are to see to the e� ective performance by municipalities of their functions in respect of inter alia

schedule 4 by regulating the exercise by municipalities of their executive authority, already alluded to above. The

bill does not do so but seeks to disempower the municipalities with respect to their executive function in respect of

municipal planning and to vest the power to do so in the Minister responsible for agriculture, the MEC responsible for

agriculture and bodies created in the bill.1.7. Furthermore, the bill does not profess to be a section 44(2) statute in that section 44(2) of the Constitution applies

only to functional areas listed in schedule 5; indeed, in terms of section 44(3) of the Constitution, the bill will have to

be regarded as regulating a matter that is reasonably necessary for or incidental to the e� ective exercise of a power

concerning a matter listed in schedule 4, and will to that extent be unconstitutional for the aforegoing reasons.

1.8. It further falls foul of the provisions of section 25(3) of the Constitution in that it seeks to provide for expropriation of

agricultural land in certain circumstances at less than just and equitable compensation at a lower price than would be paid

for similar land in the same geographical area which is used optimally for agricultural purposes (clause 54(3)(c) and 151 (a)).

1.9. Furthermore the Spatial Planning and Land Use Management Act 16 of2013 is completely ignored by the Bill.

This act has been assented to by the President and is awaiting � nal promulgation. The bill, if legislated in its

present form, deals largely with the same subject matter, but substitutes the processes described in the act

with new processes and new decision makers. In many respects, the bill duplicates town planning processes but

within the context of the supremacy of agricultural use of land over any other land uses. If the bill is legislated in

its present form, the question arises whether the legislator intends to amend the SPLUMA statute, because the

two statutes cannot exist side by side with di� erent decision makers granting applications in respect of the very

same land uses and matters.

LOBBIES FOR

YOU

Neil's Letters July.indd 6 2015/06/15 8:37 AM

7SOUTH AFRICAN PROPERTY REVIEW

from the CEO’s desk

7SOUTH AFRICAN PROPERTY REVIEW

LOBBIES FOR

YOU

THE CONSTITUTIONAL DIMENSIONS OF DECISION MAKING WITH RESPECT TO THE FUNCTIONAL AREA

OF MUNICIPAL PLANNING

2.1. In Johannesburg Municipality v Gauteng Tribunal1 the Constitutional Court had to decide on the meaning of

municipal planning as used in part B of schedule 4 of the Constitution. It decided that the term municipal planning

is a term which assumed a particular, well established meaning which includes the zoning of land and the

establishment of townships. In that context, the term is commonly used to de� ne the control and regulation of the

use of land. It decided that there is nothing in the Constitution where the word carries a meaning other than its

common meaning, which includes the control and regulation of the use of land.2

2.2. Section 41(f ) of the Constitution con� rms the autonomy of each sphere of government by stipulating that one

sphere may not assume any power or function of the other except those conferred on them in terms of the

Constitution. The limited scope for intervention by one sphere in the a� airs of another is the context in which the

powers conferred on each sphere must be construed. While the national and provincial spheres enjoy concurrent

legislative authority over matters listed in part B of schedule 4, neither of them can by legislation give itself the

power to exercise executive municipal powers or the right to administer municipal a� airs.3

2.3. Chapters V and VI ofthe Development Facilitation Act 67 of 1995 were thus declared inconsistent with section 156

of the Constitution read with part B of schedule 4 in that it granted powers to the DFA Tribunal to grant rezoning

and decide and grant applications for establishment of townships.

2.4. The bill under discussion follows the same structure as the impugned chapters V and VI of the Development

Facilitation Act 67 of 1995 divesting the municipalities of their exclusive executive power to control and regulate the

use of land, the zoning of land and the establishment of townships, and may I add in this context, the subdivision

of land. It falls foul of section 41(f ) of the Constitution by having the Minister responsible for agriculture as well as

the MEC responsible for agriculture clothed with the powers or functions of municipalities whilst those powers and

functions were not conferred on them in terms of the Constitution.

2.5. It must be realised that all land within the Republic of South Africa fall within the jurisdictional area of some

municipality and the e� ect of the bill will be that the exclusive executive authority and administration conferred

upon municipalities with respect to agricultural land within their municipal areas will not only be interfered with,

but will become subject to decisions by the national government and the provincial government.

ASSUMPTION OF MUNICIPAL PLANNING POWERS IN THE BILL

3.1. The very object of the bill illustrates the unconstitutionality thereof. Clause 2 provides for the object to regulate the

subdivision, rezoning and protection of agricultural land whilst the object expressed in clause 2(b)(ii) is inter alia to

prohibit land uses unrelated to agriculture from taking place on agricultural land including urban and other non-

agricultural developments that are likely to create con� ict with the established or proposed protected agricultural

areas and to prohibit the subdivision and rezoning of agricultural land that results in fragmentation of farming

systems, reduced agricultural productivity and land degradation.

3.2. Clause 2(e) has the object to ensure the sustainable use of natural agricultural resources and maintain the agricultural

landscape through the prohibition or discouragement of land use changes from agriculture to other forms of development.

3.3. Clause 3(1) then declares agricultural land to be the common heritage of all the people of South Africa and the

department as custodian thereof for the bene� t of all South Africans. This declaration seems to be modelled on the

Mineral and Petroleum Resources Development Act, 2002 as well as the National Water Act, 1998. However, the

“custodianship” expressed in those acts derive from international law and the Declaration on Permanent Sovereignty

over Natural Resources adopted by the United Nations in 1962. No such instrument exists with respect to agricultural

land and the expression of custodianship in this section is a rather convoluted way of stating that the Department is

entitled to regulate agricultural land; however, as pointed out above, the kind of regulation with respect to municipal

planning as set out in the bill does not fall within the power of either the department or the national government.

3.4. Therefore clause 3(2) which states that as custodian of the nation’s agricultural land, the department’s power

to approve, reject, control, administer and manage any rezoning or subdivision of agricultural land, is simply

unconstitutional. at par 57 p 203

Neil's Letters July.indd 7 2015/06/15 8:37 AM

8 SOUTH AFRICAN PROPERTY REVIEW

from the CEO’s desk

8 SOUTH AFRICAN PROPERTY REVIEW

LOBBIES FOR

YOU See Johannesburg Municipality v Gauteng Development Tribunal supra at par 43-44 and 49 pp 199E, 200 A-B and 204 D-D

3.5. Chapter 2 of the bill sets about to regulate on national level, high potential cropping land, and on provincial level

medium potential agricultural land.4 In both instances the subdivision of the relevant land is prohibited, unless

approved by the minister and/or the MEC, as the case may be. Again, the rezoning with associated subdivision, if

required, is prohibited unless approved by the inter-governmental committee. A similar structure is created with

respect to medium potential agricultural land in clauses 31 to 52.

3.6. In all of this the ultimate decision is not taken by a municipality and the high water mark of the municipality’s

involvement is the right to comment upon applications.3.7. However, the bill goes further by prescribing what municipalities should take into account in formulating their IDP’s

and SDF’s.3.8. All these provisions, read in conjunction, make the Department of Agriculture, the minister, the MEC’s and the

structures created in terms of the bill, the ultimate decision makers who may prescribe to the municipalities

how their planning must be done, all of which are unconstitutional.

4 See with respect to high potential cropping land clauses 5 to 40 and with respect to medium potential land, clauses 31 to 52

MISUSE OF POWER TO EXPROPRIATE

4.1. A power to expropriate may be created in legislation, but that power to expropriate has to be exercised according

to the procedures set out in the Expropriation Act 63 of 19755 and it must in general conform with the requirements

of section 25 of the Constitution.4.2. The power to expropriate ought to be closely circumscribed and deviations from section 25(3) as far as just and

equitable compensation is concerned, will be unconstitutional. The only space which exists to supplement the

provisions of section 23(3) of the Constitution lies in factors which have to be taken into account in order to arrive

at just and equitable compensation. However, legislation which seek to grant less compensation than would

otherwise have been payable in terms of section 25(3) of the Constitution, will be completely unconstitutional.

4.3. In clauses 34(3) and 15l(a) there is a strange notion that the compensation norm is to be at a price lower than

market value, apparently as a sanction for not using agricultural land optimally for that purpose or heeding a

directive issued in terms of clause 151.64.4. On the other hand clause 65(3) provides that the amount of compensation and the time and manner of payment must

be determined in accordance with section 25(3) of the Constitution. The other sections are therefore contradicted.

See Section 26( 1)See clause 151(9), 34(3)

SALE OF A PORTION OF AGRICULTURAL LAND

5.1. The use of the word “portion” is ambiguous. When an original farm has already been subdivided into portions, each

existing as a separate cadastral unit, those cadastral units are also described as portions ofthe farm. It should be

made clear that what is intended, is an undivided portion of a cadastral unit.

5.2. Section 58 does not strike at the sale of a portion of agricultural land for agricultural purposes. Was that the intention?

Will the sale of an un subdivided portion of agricultural land for agricultural purposes now be unregulated?

5.3. Does clause 59(1) also strike at existing undivided shares in high potential cropping land? Previously no consent

was necessary where existing undivided shares were bought, sold or registered. As formulated in clause 59(1)(c)

the registration of transfer of existing undivided shares in the name of another, will also need the relevant consent.

5.4. In this context the question also arises why consolidation of two or more portions of land need the consent of the

minister in terms of clause 61.5.5. As with other consents, there is no indication in clause 61 of what the criteria would be on which the minister or the MEC

Neil's Letters July.indd 8 2015/06/15 8:40 AM

9SOUTH AFRICAN PROPERTY REVIEW

from the CEO’s desk

9SOUTH AFRICAN PROPERTY REVIEW

LOBBIES FOR

YOU

must grant consent or must consider an application. In that sense this section is overbroad and grants an absolute discretion

with respect thereto. This is against the rule of law and is unconstitutional in terms of section 2 of the Constitution.

5.6. The same di� culty which existed with respect to the di� erentiation between a right in land and a servitude which

existed in the Subdivision of Agricultural Land Act is continued by clause 68 as read with clause 59 of the bill. For

example, a habitatio as mentioned in clause 59(1)(d) is indeed a personal servitude, while servitudes are separately

dealt with in clause 68. Are these provisions cumulative? The authorities which have to grant consent are di� erent

or may in speci� c instances be di� erent.

VIOLATION OF THE RULE OF LAW

6.1. There is a further constitutional dimension which needs comment.

6.2. In all the provisions concerning applications for rezoning, subdivision, consolidation and the like, the relevant

o� cial or body representing the national government or the MEC representing the relevant province, is granted

absolute discretions in respect to the granting or dismissing of applications.

6.3. No criteria are laid down in the bill which prescribes what the relevant factors are which the decision maker

has to take into account. Furthermore there is no indication of the circumstances and criteria applicable which

would oblige the decision maker to grant the applications.6.4. In this regard the bill is thus overbroad and leaves the applicant in a position where the law with respect to the granting

or refusal of applications is so vague that the decision maker can handle the matter according to his own whims.

6.5. In order to comply with the rule of law, the law must be certain and the exercise of discretions must be circumscribed.

6.6. In this respect the bill is contrary to the rule of law and in contravention of section 2 of the Constitution.

THE POWER TO ENFORCE OPTIMAL AGRICULTURAL USE OF AGRICULTURAL LAND

7.1. In part IV of chapter 2 from clause 54 onwards the bill seeks to enforce the active use of development of agricultural

land and the optimal utilisation thereof on pains of expropriation of the land.

7.2. The members of SAPOA, after having bought land with development potential, even with the consent of the

minister, will thus be in a position that they will have to conduct farming operations optimally on such land or face

the possibility of being expropriation until such land has been developed.

7.3. This illustrates how the bill does not take into account the highest and best use of land and simply accepts that the

highest and best economic use of land would be for farming purposes.

7.4. That would be the position even if the land is demarcated for future development in the spatial development

framework of the relevant municipality.

MISCELLANEOUS REMARKS

8.1. There are various formulation problems and other practical problems arising from the bill which are not dealt with

in this comment, such as the agricultural land register which is impractical and will in practice take years to compile.

8.2. Broadly speaking, the bill is structurally unconstitutional and once the unconstitutional aspects thereof are excised

there remains very little.8.3. The bill should be withdrawn and reformulated on those aspects which fall within the functional area of

the Department.

Yours faithfully

Neil Gopal Chief Executive O� cerSAPOA The South African Property Owners Association

Neil's Letters July.indd 9 2015/06/15 8:40 AM

10 SOUTH AFRICAN PROPERTY REVIEW

industry news

Atterbury Property Developments’ new R1,4-billion Newtown Junction mixed-

use development in the Jo’burg CBD took top honours and scooped many awards at the 2015 SAPOA Annual Innovative Excellence in Property Development Awards. Newtown Junction was declared the overall winner at the coveted awards, after also receiving accolades for best mixed-use development and the overall transformation award.

Atterbury was the big winner at this year’s SAPOA Excellence Awards with another two Atterbury developments – the West Hills Mall in Ghana and the Westcon Offices and Warehouse development at Waterfall Industrial Park – winning the international development award and the industrial development award respectively.

“We are delighted to secure multiple awards, including the main overall title at the 2015 SAPOA Innovative Excellence in Property Development Awards for our Newtown Junction development,” says Cobus van Heerden, Director of Retail Developments at Atterbury.

Newtown Junction – an 85 000m² mixed-use shopping, leisure and office development in Jo’burg’s trendy Newtown precinct – was opened in September 2014. It was developed by Atterbury Property Developments for

Atterbury Property Holdings and JSE-listed Attacq Limited. Newtown Junction includes a 38 000m² retail component, about 39 000m² of prime office space, basement parking for 2 400 cars and a new City Lodge Hotel, which is under development.

“These awards are regarded as the Oscars of South Africa’s property industry, so we are truly proud that our Newtown Junction project has been recognised as the overall best property development in the country,” says Van Heerden. “This is a great achievement for a great development, which is transforming the Jo’burg CBD’s historic Newtown precinct into a vibrant mixed-use shopping and leisure destination with prime office space.”

Newtown Junction’s development represents the first significant injection in the Jo’burg CBD in 40 years and is part of a key urban regeneration initiative in the Newtown node. The office component of Newtown Junction is largely taken up by Nedbank in a landmark building that has achieved a 4-Star Green Star SA rating from the Green Building Council of South Africa. Newtown Junction has to date created about 2 700 jobs during the construction phase of which 850 were jobs for local unemployed people. It is estimated

that about 4 800 people will be working at Newtown Junction when it’s fully operational on the retail, office and hotel components.

“Newtown Junction is anchored by its retail component, which includes more than 70 stores and restaurants, a Ster-Kinekor cinema complex and a gym,” says Lucille Louw, Managing Director of Atterbury Asset Managers. “Atterbury is committed to the success of the Newtown node and urban regeneration within the Jo’burg CBD. The Newtown Junction mixed-use development offers shoppers, office workers, residents and visitors a first-rate, trendy and safe shopping and leisure destination in the Jo’burg CBD. With the introduction of FATTi, Atterbury’s new shopping centre analytics and technology solutions service, in Newtown since December 2014, we can accurately say that the current footfall at Newtown Junction is nearing 500 000 per month.”

“Winning the SAPOA international development award for the 27 700m² West Hills Mall project is another feather in the cap of Atterbury,” says Van Heerden. “Atterbury is a leading developer of prime and world-class property projects not just in South Africa but also in other parts of the continent.” +27 (0)12 471 1600, Atterbury.co.za

Atterbury wins big as Newtown Junction takes top honours

News Review_JULY_SUBBED.indd 10 2015/06/15 8:43 AM

11SOUTH AFRICAN PROPERTY REVIEW

industry news

Nedbank makes R323-million commitment to the Cape’s retail sector

Newmark Hotels scoops multiple awards

Nedbank Property Finance has granted R323-million to

FPG Group for the purchase of the Cape Gate Lifestyle precinct from Hyprop, Africa’s leading specialist shopping centre real estate investment trust (REIT).

The acquisition comprises 30 000m2 GLA, which includes a lifestyle and decor centre, an Engen service station, drive-thru Steers and KFC, and a Toyota dealership. The six properties are located along Okavango Road in Durbanville, Cape Town, adjacent to the Cape Gate regional mall and in close proximity to the successful Makro development, which is partly owned by Nedbank. Tenants of the lifestyle and decor centres include Super Spar, Virgin Active, Build-It Hardware, Cash Converters, Pure Plastics, Postnet and Tafelberg Furniture.

Richard Thomas, Nedbank Property Finance’s Regional Executive for the Western Cape, says the bank was enthusiastic about funding the development not only because of its long-term relationship with the FPG Group, but also because the properties are well located and tenanted by quality national tenants on long-term leases.

“We have been the FPG Group’s financier of choice

for more than five years and we are proud to partner with them once again in this transaction,” he says. “The Group is an experienced retail operator and we feel sure it will add value to this key property in Cape Town’s northern suburbs.”

The FPG Group – then known as Foodprop – was established in 1989 as a wholly owned subsidiary of the Foodworld Group, which was then the largest independent retail group in the Western Cape, consisting of 13 supermarkets and four wholesale outlets, which was sold to Shoprite. Foodprop was created to build a property-owning entity to source new sites for its retail division, and

to build a diverse property portfolio to include the industrial and office sectors.

In 2006, the Group concluded its largest single property development – the R300-million The Claremont, which consisted of 322 apartments. In 2013, the Group rebranded to become the FPG Group to reflect the broader focus across all property sectors, and made its first international property acquisition in the UK. Today FPG Properties has grown to include 38 properties, primarily in the retail sector, with limited exposure in the office, industrial and residential sectors.

The portfolio comprises a GLA of more than 160 000m²

and more than 70% of this space is occupied by national tenants. “With the latest IPD results confirming that the retail sector has held its ground, Nedbank Property Finance continues its ongoing commitment to the sector by providing agile and relevant financial solutions that realise opportunities for quality retail property clients such as the FPG Group,” says Thomas. “This, coupled with our strong partnership approach, is a strong proposition that ensures we remain the market leader in the commercial property finance sector.” +27 (0)11 295 8045, Nedbank.co.za

Boutique hotel group Newmark Hotels, Reserves

& Lodges has scooped a total of 10 TripAdvisor Certificates of Excellence and one sought-after Hall of Fame award. TripAdvisor’s Certificate of Excellence awards are based on consumer reviews and take into account the quality, quantity and most recent reviews and opinions submitted by travellers over a 12-month period.

The 10 Newmark properties awarded are The Dock House

Boutique Hotel & Spa, the Victoria & Alfred Hotel and the Queen Victoria Hotel in the heart of the V&A Waterfront in Cape Town; and, also at the Waterfront, Dash restaurant at the Queen Victoria Hotel and Oyo restaurant at the Victoria & Alfred Hotel; Nkomazi Game Reserve in Mpumalanga; The Five-Star Drostdy Hotel in Graaff-Reinet; Motswari Private Game Reserve in the Timbavati – part of the greater Kruger National Park; The Nyungwe

Forest Lodge in Rwanda; and Coral Lodge 15.41 in Northern Mozambique.

Another coup is that Newmark’s Victoria & Alfred Hotel has been included in the TripAdvisor Hall of Fame, which is a new award for properties that have won the Certificate of Excellence for five years consecutively. This is some achievement because only nine percent of total winners qualify for the Certificate of Excellence

Hall of Fame by consistently doing well over five years.

“Our hotels and lodges appeal to travellers – we give them the service and the overall good experience they are looking for,” says Newmark Hotel’s Managing Director Neil Markovitz. “TripAdvisor keeps us on our toes – the public doesn’t lie – so these 10 awards confirm we’re determined to get it right on every level. We’re delighted.” +27 (0)21 427 5900, Newmarkhotels.com

News Review_JULY_SUBBED.indd 11 2015/06/15 8:45 AM

12 SOUTH AFRICAN PROPERTY REVIEW

industry news

The iconic V&A Waterfront has contributed about

R227-billion towards the GDP of South Africa’s Western Cape province between 2002 and 2014, with forecasts revealing that this growth will continue for the next 10 years. Despite the perception that the V&A is predominately a retail and tourism hub, the residential property component is a significant contributor towards GDP growth.

According to David Rebe, Chief Executive Officer of Sandak-Lewin Property Trust, in the recent past the V&A has become a thriving residential area, providing residents with convenient and vibrant accommodation. While in the past residential property within the V&A has been perceived as only catering to the ultra-luxurious high-end market, the area now offers career-driven entry-to-high-level professionals vibrant urban residences at reasonable prices.

An example is the recently completed long-term residential rental complex, the Ports Edge, which is the first of its kind in the area. This is the first residential building wholly owned by the V&A that is being offered for rental. With easy access to the city centre, highways and MyCiti bus stops, the residential complex is ideal for professionals who want to live and breathe the buzz of the city.

Rebe says that apartments across the V&A Waterfront, CBD, Green Point and Sea Point remain

in huge demand because of the central and scenic location – and the lack of affordable, reasonably priced accommodation in the region means developments such as Ports Edge are fast gaining popularity, with the building’s occupancy rate at almost 100%. “Areas such as the V&A Waterfront remain attractive because of the vibrant lifestyle that residents can enjoy,” he says. “Perks of being situated in the area include easy access to the city, limited traffic congestion and amenities such as live

entertainment and an assortment of restaurants, cafés, bars, local and international retail outlets, as well as safe running tracks and bicycle lanes for residents to enjoy.”

He adds that the R50-million development of the Watershed – which is situated next to the Ports Edge, offering arts and craft workmanship exhibited by local artists – provides residents with an opportunity to indulge in the creative landscape at their own leisure. In addition, the Watershed features Workshop17, a collaborative shared working space.

“Other than the sought- after living experience at the V&A, residents are also attracted to the rental aspect of the accommodation as they prefer not to be tied down with a mortgage,” says Rebe. “Moreover, residents are able to enjoy the urban and vibrant environment knowing that they have 24-hour security.”+27 (0)21 408 7500, Waterfront.co.za

Despite the current economic environment characterised

in part by muted growth, subdued business and consumer confidence, reduced disposable income and ongoing energy constraints, South Africa’s housing market continues to demonstrate noteworthy stamina and resilience across all segments in the face of these challenges, says Dr Andrew Golding, Chief Executive of the Pam Golding Property Group.

“With rising inflation a growing concern, the decision by the Monetary Policy Committee (MPC) to keep the repo rate steady was positive news, although it is likely that the increasing fuel price and proposed further hike in electricity tariffs may bring pressure to bear on the MPC’s future stance,” he says.

Property market resilience can be demonstrated in a number of ways. One example is that of first-time buyers who continue to exhibit an increasing appetite to transact, and as a result enjoy a long-term benefit of investing in their future through home ownership. “In addition, we remain confident that in the coming months we will begin to see the positive impact of the 2015 National Budget announcement that no transfer duties are payable on property transactions below R750 000 (as opposed to the former R600 000 threshold),” says Golding. “The lending climate and affordability of a deposit and bond repayments play a significant role in the first- time home-buyer segment of the market. Also encouraging is what

is generally perceived as a more favourable lending environment, with mortgage originator Ooba reporting higher approval rates (76% in April 2015) and more competitive rate concessions by financial institutions. These are critical factors in supporting growth in this sector of the market.

“Despite socioeconomic and political challenges, confidence in real estate as an investment prevails across all sectors of the market, with some clear trends evident. These include a desire to reside in economic nodes and transport corridors with easy access to the workplace and schools; a growing demand for convenient apartment living, both in terms of sales and rental accommodation; and a shift towards secure estate living in integrated communities where there is a strong emphasis on sustainability and self-sufficiency. The latter undoubtedly reflects a direct response to rising energy, water and other municipal costs as well as a growing environmental awareness.” +27 (0)21 710 1700, Pamgolding.co.za

V&A Waterfront rental accommodation offers affordable and vibrant luxury living

Stable interest rates provide affirmation for home buyers

Dr Andrew Golding, Chief Executive of the Pam Golding Property Group

News Review_JULY_SUBBED.indd 12 2015/06/15 11:42 AM

13SOUTH AFRICAN PROPERTY REVIEW

legal update

The Department of Trade and Industry caused widespread

uncertainty and confusion in its Notice 396 in the Government Gazette of 5 May 2015, which stated that black participants in broad-based and employee share ownership schemes could only contribute a maximum of three points (out of the total available 25 BBBEE ownership points) to a firm’s BBBEE score in terms of the Codes of Good Practice issued under the Broad Based Black Empowerment Act.

On 8 May, the Department issued a statement that BBBEE transactions concluded before 1 May 2015 would not be affected and that the Department would appoint a technical task team to explore the “appropriate balance between active (direct) and passive (broad based schemes) ownership”, and report to the Minister within 30 days.

On 12 May 2015 in a radio interview, the Minister of Trade and Industry Rob Davies clearly and unequivocally announced that the DTI will withdraw paragraph (d) of the clarification notice, and as such dispense with the three-point cap on broad-based empowerment schemes and employee share ownership schemes.

On 15 May 2015, the department issued a further notice in the Government Gazette, which withdrew Notice 396. It accordingly now appears that the status quo has been restored and that broad-based and employee share ownership schemes are again eligible to contribute to all (and not just three) of the 25 available BBBEE ownership points in the Codes.

It would thus appear that the task team that was to be created in this respect would no longer be necessary.

The Revised Notice of Clarification has, however, retained the following:

● The Amended Codes of Good Practice came into effect on 1 May 2015.

● All BBBEE verifications conducted using the financial year ending before 30 April 2015 can still be verified using the old Codes of Good Practice, and all BBBEE verifications conducted using the financial year ending after 1 May 2015 must be verified using the amended Codes, with the exception of the Sector Codes. This is a welcome clarification, as companies with a financial year end in 2014 or prior to 30 April 2015 may still be rated under the old Codes.

● The transitional period for the alignment of Sector Codes has been extended to the end of October 2015. From 1 November 2015, Sector Codes that are aligned shall be effective in accordance with the 1 May 2015 effective date. A consideration shall be made for Sector Codes not aligned by the end of October 2015 to be repealed.

● All valid BBBEE certificates issued under the old Codes as well as the relevant Sector Codes should remain valid, accepted and treated as empowering suppliers.

● All EME (Exempted Micro Enterprises) certificates issued without Empowering Supplier Status will be automatically recognised as Empowering Suppliers.

Eugenia Makgabo is an Admitted Attorney of the High Court and Legal Manager at SAPOA

DTI turnaround on Broad Based EmpowermentIn light of the recent uncertainty regarding the DTI’s Broad Based Empowerment notice, the department has made some revisions

20 SOUTH AFRICAN PROPERTY REVIEW

legal update

Eugenia Makgabo is an Admitted Attorney of the High Court and Legal Manager at SAPOA

Don’t be left in the darkLandlords are cautioned to heed against the cutting off of tenant’s electricity

Landlords are constantly faced with frustration when tenants

do not fulfil their contractual obligations. This leaves the landlord in a situation where they could potentially be left out of pocket. A scenario that is popular is the non-payment of electricity by tenants.

In the Anva Properties CC v End Street Entertainment

Enterprises CC case (hereinafter referred to as the case), there is evidence of the above-mentioned conduct by a tenant.

Anva Properties CC (hereinafter referred to as the applicant) sought an order authorising it to terminate the electricity supply to premises in a building situated at 34-36 Riebeeck Street, Cape Town. The applicant owns the building and

End Street Entertainment CC (hereinafter referred to as the respondent) was one of the tenants occupying it.

The applicant pays electricity to the City of Cape Town and recovers that cost from the tenants. The respondent occupied the basement of the building since 2012, from where it conducted business as a bar and nightclub.

The respondent used electricity for its air-conditioning, refrigeration and lighting facilities, which were the primary requirements for the business to be functional. It was established that the tenant had not paid its electricity bill since September 2014; and that it is in arrears in excess of R300 000.

ConsiderationsThe respondent raised two defences. The first related to the validity of the lease and the second to the right to bring an action by the landlord.

● Firstly, it was contended that on the applicant’s own showing, the respondent was finally deregistered in 1998, long before it purportedly entered into a lease agreement with the applicant on 7 May 2012 to hire the premises. Secondly, the applicant has no locus standi to claim payment of any debt from the respondent because it has ceded all its rights to Nedbank Limited. Consequently it has no right to recover any amount under the ceded debt.

● It is settled law that deregistration puts an end to the existence of a corporate entity. No steps have been taken to restore the respondent to register

of close corporations, and even if these had been taken, the restoration of a close corporation under the Close Corporations Act No. 69 of 1984,

read with the Companies Act No. 71 of 2008, does not necessarily mean that all of its activities during the period when it was deregistered are automatically validated.

● Given the above-mentioned established facts it was recognised that no valid lease agreement was entered into between the parties, and that the applicant’s claim for the relief based on a lease purportedly entered into between the parties cannot succeed.

● Further, given that the respondent has been deregistered and that the lease agreement purportedly concluded is invalid, it is unnecessary to deal with respondent’s second defence.

Landlords are constantly faced with frustration when tenants do not fulfil their contractual obligations. This leaves the landlord in a situation where they could potentially be left out of pocket. A scenario that is popular is the non-payment of electricity by tenants

The only defences available to the landlord would be that the tenant failed to prove one of the two essential spoliation requirements, namely possession or dispossession, which would be a mammoth task

This legal opinion is only a guide and should not be copied with the expectation that it will serve each party’s individual circumstances. Most of these recommendations have not been tested in our courts. SAPOA cannot guarantee any success in any court if any of these recommendations are put to use.

It accordingly now appears that the status quo has been restored and that broad-based and employee share ownership schemes are again eligible to contribute to all (and not just three) of the 25 available BBBEE ownership points in the Codes

The Spatial Planning and Land Use Management Act (Act No. 16 of 2013) is now in effect.

Dear Members, please note that the Spatial Planning and Land Use Management Act (Act No. 16 of 2013) came into effect on 1 July 2015.

In terms of Section 61 of the Spatial Planning and Land Use Management Act (Act No. 16 of 2013) (“the Act”), South African President Jacob Zuma determined 1 July 2015 as the date on which the Act shall come into operation.

SPLUMA proclaimed

Legal Review_JULY_SUBBED.indd 13 2015/06/15 10:40 AM

14 SOUTH AFRICAN PROPERTY REVIEW

education, training and development

The purpose of the property valuation and management

programme at the University of Johannesburg is to prepare students to be well-rounded prospective employees once they enter the property industry.

To achieve this, property valuation and management modules were introduced as electives in the BCom Finance degree. After a generic first year, students can register for property valuation and management modules in the second and third year of their undergrad studies.

The primary purpose of the BCom Finance degree is to provide students with applied competencies in the mastering, analysis, interpretation and application of financial and investment management, financial planning, accounting principles and property valuation and management in preparation for a career in the property industry as well as to provide a basis for further learning.

Consistent exposure to real- world situations provides students with opportunities to reflect on their ability to apply financial, investment, financial planning, accounting and property valuation and management decisions, and to assess the effect thereof in the holistic context of the property industry.

Exposure to the different disciplines provides a sturdy foundation to support the multidisciplinary nature of the property industry. After successful completion of the BCom Finance degree, students can specialise in one of four honours degrees: Financial Management, Investment Management, Financial Planning, or Property Valuation and Management.

Martin Ferguson is SAPOA’s HR, Education, Training and Development Manager

Property programmes at UJ

The purpose of the BCom Honours in Property Valuation and Management degree is to strengthen students’ knowledge and comprehension of the disciplines of property valuation and management.

The programme consists of a broad-based curriculum to prepare the postgraduate student for a wide range of property-related specialities. The curriculum topics range from property valuation and property law to property finance and property management.

The programme emphasises application, analysis and evaluation within each topic area, and the application of integrity and ethics in a professional environment. Mastering the curriculum will provide students with the skills to synthesise complex valuation, management, financial and legal principles in order to add value to the entities that employ them.

Although the BCom Finance degree with property valuation and management modules is the preferred route of entry into BCom Honours in Property Valuation and Management, there are other routes for prospective students who completed other qualifications.

One such route is the Bridging Programme in Finance, intended for prospective students with any bachelor’s degree, related BTech degree or a related national diploma, excluding the National Diploma: Real Estate, who intend enrolling for BCom Honours in Property Valuation and Management.

The learning material repeats the core topics and outcomes covered in the second and third year of Financial Management, Financial Planning, Investment Management, and Property

Valuation and Management modules. The content of these modules provides students with the foundation necessary for the successful completion of honours studies in the field property valuation and management.

The Advanced Diploma: Property Valuation and Management offers progression for National Diploma: Real Estate students to NQF Level 7. Successful completion of this programme will provide students with property valuation and management knowledge and may lead to articulation into the BCom Honours Property Valuation and Management programme.

The formal qualifications described above were all accredited by the South African Council for the Property Valuers Profession in 2014. Students who successfully complete any one of these qualifications will be able to register as candidate valuers, and those who complete the BCom Honours in Property Valuation and Management as professional valuers.

In addition to the formal qualifications, the University of Johannesburg also offers a number of extracurricular qualifications, which include well-known SAPOA courses such as the Introduction to Commercial Property Programme (ICPP), the Essential Commercial Property Programme (ECPP), the Property Management Programme (PMP), and the Property Financial Programme at basic, intermediate and advanced levels.

The PMP programme with UJ is run over two separate week- long block sessions (total of 10 contact days), followed by an examination.

For more information, please contact:

Martin FergusonHuman Resources, Education, Training and Development Managert: +27 (0)11 883 0679 e: [email protected]

A look at property valuation and management qualifications available at the University of Johannesburg

HR_JULY_SUBBED.indd 14 2015/06/15 9:32 AM

15SOUTH AFRICAN PROPERTY REVIEW

education, training and development

Partnering with UJ

SAPOA Valuations Workshop series for 2015

University of Johannesburg Annual Prize Giving Breakfast in the spotlight

SAPOA in partnership with the University of Pretoria is planning a series of Valuations Workshops for 2015

SAPOA has a close relationship with the University of

Johannesburg, especially the Department of Finance & Investment Management, under which the Property Valuation and Management qualifications and the SAPOA Educational Short Learning Programmes fall.

On 23 April, the Department of Finance & Investment Management honoured its top-performing students for the 2014 academic year at the Johannesburg Country Club.

Various associations – including the South African Council for Valuers, SAPOA and the South African Institute of Chartered Accountants, and others that are involved in the allocation and sponsoring of bursaries, providing internships and graduation programmes, serving on the Department of Finance & Investment Management advisory committees, and sponsoring top performance awards – were present.

For the Property Valuation and Management qualifications, Martin Ferguson from SAPOA and Andrè Kruger from the Property Division of the Department of Finance & Investment Management were invited to present the award to

the Top Performing Student, Nichole Leigh Maroun, who achieved the highest marks in Property Valuation and Management 2 during the 2014 academic year.

We wish Nichole all the best with her future studies and trust

that she will be rewarded again next year for her 2015 academic achievements. We congratulate the Department of Finance & Investment Management on this great initiative and wonderful event in honour of their top achievers.

The Valuation Workshops will be offered monthly for the

remainder of the year. They will be full one-day workshops and will deal with the following topics on the indicated dates. Venues will be confirmed and will either be at the University of Pretoria or in Midrand:

● 3 July 2015: Advanced income capitalisation valuations

● 21 August 2015: Commercial property economics

● 18 September 2015: Principles of discounted cash flow valuations

● 23 October 2015: Highest and best use valuations

● 13 November 2015: Valuation of properties under construction

● 4 December 2015: Principles of feasibility studies

The workshop fees for SAPOA members will be R2 150 per workshop (including VAT).

The workshop fees for non-members will be R2 500 per workshop (including VAT). If delegates register and pay for all workshops before commencement of the first workshop, they will receive a 10% discount per workshop.

The workshops have been vetted by the Engineering Council of South Africa and SA Council for the Property Valuers Profession, and CPD credits will be allocated. See Sapoa.org.za for more details.

To register or for enquiries, please contact: Banele SenatlaCourse Coordinator t: +27 (0)012 434 2630 e: [email protected]

FROM LEFT Martin Ferguson, Nichole Leigh Maroun and Andrè Kruger

HR_JULY_SUBBED.indd 15 2015/06/15 9:32 AM

16 SOUTH AFRICAN PROPERTY REVIEW

education, training and development

3087 SAPOA Courses AD (21-08-2014).indd 1HR_JULY_SUBBED.indd 16 2015/06/15 9:40 AM

17SOUTH AFRICAN PROPERTY REVIEW

education, training and development

2014/08/26 12:45 PMHR_JULY_SUBBED.indd 17 2015/06/15 9:40 AM

18 SOUTH AFRICAN PROPERTY REVIEW

planning and development

The South African Council for Planners (SACPLAN) is

the statutory council responsible for regulating the planning profession in terms of the Planning Profession Act No. 36 of 2002 (the Act). In addition to the typical functions of a statutory professional council, this includes the setting of standards and the accreditation of planning schools for ensuring and promoting a high standard of education and training in planning.

As a result of ongoing transformation since 1994 and the implications of the need for planning to be “reinvented”, in 2009 SACPLAN commissioned a consortium to undertake research into the process of preparing new competencies and standards for the planning profession.

SACPLAN has identified the need to re-evaluate the current planning competencies to ensure that the competencies enable registered planners to meet the challenges they face. What is clear is that the definition of planning in South Africa has evolved over time.

Planning was widely viewed as a technical activity concerned mainly with layouts, infrastructure design and control of land use and the built form. This was followed by a period during which planners needed conceptual and technical skills to enable them to operate effectively in an increasingly complex world where change is less predictable than in the past.

The formulation of competencies and standards for the planning profession needed

Planning education in South Africa

to be informed by four contextual factors. The first is recognising the diversity of local needs and choices: how planning can improve people’s lives while taking cognisance of diversity of cultural, gender and rural-urban relationships as well as the formality-informality continuum.

The second is the need for planning to promote sustainable patterns of development. Sustainability can be broadly understood to mean social, economic and environmental sustainability. The role of planning is to harmonise the three dimensions of economic efficiency, social equity and environmental sustainability.

The third relates to the high level of economic inequality in the country. How can planning reinvent itself and become a catalyst for providing economic and livelihood opportunities? Different forms of investment need to reflect local needs and choices, and not only represent the dominant public and private drivers of investment. This not only requires a substantial understanding of the dynamics of land markets and regulatory instruments used to influence the forces at play in those markets but also an understanding of the nature of the economies at local and community levels.

The fourth relates to the complexity of our rural history and land use practices. Planning education needs to ensure that planners are mindful of the rich history of traditional land practices and that they incorporate these into planning approaches in a way that builds on and supports indigenous practices while also

recognising the role formal and informal land markets and planning practices play in a global economy.

To achieve the above, three inter-related sets of competencies have been identified for the planning profession. These are generic, core and functional competencies.

Generic competencies are the essential skills, attributes and behaviours that are seen as important for all planners, regardless of their function or level. Generic competencies are the basic competencies common in all the built and natural environment disciplines.

Core competencies, on the other hand, include the specific knowledge, skills, abilities and experience that a planner must possess to successfully perform the work and activities central to professional planning practice. This is the set of competencies that distinguishes planning from the other professions with which it interfaces.

Functional competencies are the basic skills and behaviours needed to do a job successfully. These are competencies that relate to the “how to do” aspects of planning.

Accredited qualifications must cover the competencies at either a diploma level (NQF Level 6), a three-year bachelor’s degree level (NQF Level 7), or a four-year professional bachelor’s degree level, honours degree level or master’s degree level (NQF Level 8 or 9).

A professional planner (a person who holds a qualification on NQF Level 8 or 9 with at least 24 months of post-qualification

The South African Council for Planners places education in the spotlight

SACPLAN has identified the need to re-evaluate the current planning competencies to

ensure that the competencies

enable registered planners to meet

the challenges they face. What is clear is that the definition of

planning in South Africa has evolved

over time

By Martin Lewis

Sources SACPLAN Consolidated Report on Competencies and Standards: December 2014; SACPLAN Guidelines for Competencies and Standards for Curricula Development: December 2014

Lekgolo Mayatula is SAPOA’s Planning and Development Manager

Town Planning_JULY_SUBBED.indd 18 2015/06/15 9:55 AM

19SOUTH AFRICAN PROPERTY REVIEW

planning and development

Martin Lewis is the Chief Executive Officer of the South African Council for Planners

experience) must demonstrate a good conceptual grasp of the field of urban and regional planning as practised in South Africa and an ability to assess a situation that requires planning intervention and formulate appropriate responses; provide leadership to fellow professional planners, professionals in related fields, communities and other stakeholders in the planning processes; and possess some specialist planning knowledge or skills.

As indicated, SACPLAN is mandated to accredit planning schools with the aim of ensuring and promoting a high standard of education and training in planning. There are eleven institutions of higher education that offer planning at NQF Level 6 or higher. SACPLAN has accredited qualifications of the following institutions:

● Cape Peninsula University of Technology (National Diploma: Town and Regional Planning (ND TRP) and Bachelor of Technology: Town and Regional Planning (BTech TRP));

● Durban University of Technology (National Diploma: Town and Regional Planning (ND TRP) and Bachelor of Technology: Town and Regional Planning (BTech TRP));

● North-West University (Bachelor of Arts ET Science (Planning));

● University of Cape Town (Master in City and Regional Planning (MCRP));

● University of the Free State (Master in Urban and Regional Planning (MURP));

● University of Johannesburg (National Diploma: Town and Regional Planning (ND TRP) and Bachelor of Technology: Town and Regional Planning (BTech TRP));

● University of KwaZulu- Natal (Master of Town and Regional Planning (MTRP));

● University of Pretoria (Bachelor of Town and Regional Planning (BTRP) and Master of Town and Regional Planning (by coursework) (MTRP));

● University of Venda (Bachelor of Urban and Regional Planning (BURP)); and

● University of the Witwatersrand (Bachelor of Science Honours in Urban and Regional Planning (BSc Hons (URP), Bachelor of Science in Town and Regional (BSc TRP), and Master of Science in Development Planning (MSc (DP)).

Property developers who wish to appoint an urban and regional planner must ensure that such a planner is registered with SACPLAN. Registration with SACPLAN as a professional or technical planner validates a person’s professional knowledge, experience and commitment to working to highest standards, and indicates that the person is a responsible member of the planning profession, working under a Code of Ethics and Professional Conduct.

If a planner is successfully registered with SACPLAN,

property developers can expect that person to have a knowledge of urban spatial structure or physical design and the way in which cities work; an ability to analyse demographic information to discern trends in population, employment and health; a knowledge of plan-making and project evaluation; an understanding of local, regional and national government programmes and processes; an understanding of the social and environmental impact of planning decisions on communities; an ability to work with the public and articulate planning issues to a wide variety of audiences; an ability to function as a mediator or facilitator when community interest conflict; an understanding of the legal foundation for land use regulation; an understanding of the interaction between the economy, transportation, health and human services and land-use regulation; an ability to solve problems using a balance of technical competence, creativity and pragmatism; and an ability to envision alternatives to the physical and social environments in which we live.

Registration with SACPLAN as a professional or technical planner validates a person’s professional knowledge, experience and commitment to working to the highest standards, and indicates that the person is a responsible member of the planning profession, working under a Code of Ethics and Professional Conduct

For more information, please contact: Martin Lewis Pr. Pln, MRTPI, CEO South African Council for Planners t: +27 (0)11 318 0460/0437 e: [email protected] w: Sacplan.co.za

Town Planning_JULY_SUBBED.indd 19 2015/06/15 11:44 AM

20 SOUTH AFRICAN PROPERTY REVIEW

theme leadertheme leader

20 SOUTH AFRICAN PROPERTY REVIEW20 SOUTH AFRICAN PROPERTY REVIEW

theme leader

Theme Leader_JULY_SUBBED.indd 20 2015/06/15 10:20 AM

theme leader

21SOUTH AFRICAN PROPERTY REVIEW

theme leader

21SOUTH AFRICAN PROPERTY REVIEW

theme leader

21SOUTH AFRICAN PROPERTY REVIEW

Deconstructing investing in property

The South African property sector has been a huge winner over the last decade, returning 22% per year compared with 18% for the FTSE/JSE All Share Index (ALSI). Allan Gray discusses how the sector has

managed to perform so well, why this performance is unlikely to be repeated, and why property companies may be more risky than they appear at fi rst glance

By Allan Gray Associate Portfolio Manager Jacques Plaut and Investment Analyst Yusuf Mowlana

The past decade has been a very good one for property investors. Those investors,

ourselves included, who were underweight in the sector, lost out.

Looking back, we underestimated the extent to which interest rates would decline and stay low under a very accommodative monetary policy in developed countries, and we underestimated the ability of some management teams to add value to their portfolios.

On top of this, the resulting tailwind to valuations allowed listed property companies to bene� t from earnings-enhancing acquisitions in South Africa and overseas.

While this past decade’s performance has been fantastic, it is unlikely to be repeated. Investors who buy into the sector today are only getting a 5,1% initial dividend yield. This might not seem so much more expensive than the 8,7% yield they would have received in 2005, but it equates to a 70% price increase.

The sector’s eight percent growth over the last 10 years is better than in� ation, which has averaged six percent, but worse than the average JSE-listed company, which has grown dividends at about 16% per year over the same period. Even this relatively modest eight percent is an overstatement of underlying growth because it has been boosted by acquisitions and by property companies paying less interest on their debt.

More generally, the upside of owning a property share is limited compared to other businesses. Some companies can reinvest earnings at a 30%-plus return on equity; property companies tend to do single digits.

This is probably partly the result of the di� erent competitive position. Despite location advantages, most malls and o� ces can be replicated, but it is harder to compete with an established brand such as Cartier or the technology and commercial innovation expertise at work in Tencent.

In the last � ve years, there have been 29 new property listings, more than in any other sector. These have been driven not only by favourable valuations but also by recent changes to regulations that now favour listed property over unlisted property.

Large new o� ces are under construction in Sandton, Johannesburg, despite already-high vacancies, generally low levels of net space uptake and a trend towards more e� cient use of space. In most industries, high levels of investment coupled with more competition equal lower returns for existing players. With capacity expanding ahead of demand growth, certainly one should expect lower growth in dividends for the next part of the industry cycle.

Lastly, re-valuation has added six percent to overall returns over the past 10 years but this may not be the case over the next 10. Because interest rates are currently zero in many countries, investors are paying high prices for risky assets such as shares, junk bonds and property. This has bene� ted South African property companies, which are currently trading at record-high valuations.

The large South African property companies in the sector currently trade at a premium to the 10-year rolling bond yield, which was previously only surpassed in 2007 during the last decade.

Theme Leader_JULY_SUBBED.indd 21 2015/06/15 10:26 AM

22 SOUTH AFRICAN PROPERTY REVIEW

theme leader

Investors appear to be pricing in future growth, which is higher relative to history. The risk is that the growth disappoints. One could argue that this will continue but on a balance of probabilities, we think it is more likely to reverse and turn into a headwind.

Risks in the sectorOne explanation for the sector’s high valuation could be that investors see very low risk to current earnings. We think this view is optimistic.

Many companies use debt to boost their returns. There is nothing wrong with this, but the extent to which it happens in the property sector can be somewhat disquieting. Some property companies have a debt balance that is seven times larger than annual income. To put this another way, if a company in such a position applied all its income to paying o� debt – and paid no dividends – it would take seven years to pay o� all the debt.

The only other sector that is more geared than this is the banking sector. It is no coincidence that both sectors have long-term contracts with their clients and relatively stable income. But in times of stress, the large debt balances will become more prominent in investors’ minds.

Economically stressed tenants can’t always meet their commitments nor easily renew their leases. If debt holders suddenly required higher interest rates or safer covenants, equity holders would be in trouble.

If property valuers became more conservative, the ratio of debt to property value would increase, and property companies would have to raise more money from shareholders. We saw this all happen to a dramatic extent in Australia in 2008.

Property companies do not account for the replacement cost of assets like other companies do: there is no depreciation charge on the income statement. In this respect, long-term earnings are overstated, and property companies normally need to issue debt or shares to be able to pay for capital expenditure.

Take Growthpoint Properties Ltd, the largest South African property stock, as a typical example. It is clear that capital expenditure – some of which was for growth, and some of which was for replacing or upgrading of old buildings – has been paid for by borrowing money and by issuing shares. It is striking that the company has raised R7-billion more from shareholders than it has paid to the shareholders. As a result, Growthpoint Properties Ltd’s shares in issue have increased by 14% per year over this period.

To a large extent, these shares have been issued to make acquisitions – and, mostly, Growthpoint Properties Ltd has bought companies trading on a higher dividend yield than itself – in other words, companies that the market has placed on a cheaper valuation than Growthpoint Properties Ltd itself.

This operation has the e� ect of boosting earnings per share even when there is no actual organic improvement. We believe Growthpoint Properties Ltd has added real value by issuing all those shares in order to make acquisitions; however, we don’t think this is something it will be able to repeat given its current size.

Beware of paying a premiumIn hindsight, there were times in the past 10 years when we should have been more positive on property. But right now, we think that investors are paying a premium multiple for property stocks that is not justi� ed by the fundamental prospects.

The re-valuation tailwind is not likely to repeat, and may even reverse. Dividend growth has been boosted by acquisitions. We think the market does not fully appreciate all of the risks in the sector, especially the high level of gearing.