Canaccord Adams is the global capital markets group of Canaccord Capital Inc. (CCI : TSX|AIM) The recommendations and opinions expressed in this Investment Research accurately reflect the Investment Analyst’s personal, independent and objective views about any and all the Designated Investments and Relevant Issuers discussed herein. For important information, please see the Important Disclosures section in the appendix of this document. 5 November 2008 2008-185 J. Frederick Kozak, P.Eng. 1.403.508.3836 [email protected]Timothy Clark 1.403.508.3824 [email protected]INSIDE Summary ..................................................... 2 The Caribbean – An Overview.................... 3 Caribbean Geology ..................................... 4 Trinidad and Tobago................................... 9 Guyana ...................................................... 21 Suriname ................................................... 26 Company Feature Summaries .............. 30 Canadian Superior Energy Inc. ............ 31 CGX Energy Inc...................................... 45 Challenger Energy Corp........................ 61 Petro Andina Resources Inc................. 73 Primera Energy Resources Ltd. ........... 77 Voyager Energy Ltd. .............................. 81 Energy – Oil and Gas, Exploration and Production South American Offshore – The Caribbean Report It’s not just on the beach – there’s oil there The Caribbean is probably best-known as a destination for golden sun and sand, but looking around the Caribbean basin, especially off the northern coast of South America, we find gold of a different colour: black gold, and with it trillions of cubic feet of natural gas. Although this area may not be high on the explorers’ lists of prospect regions, exploration is underway and it is generating results. Mature and not-so-mature Regions of the Caribbean basin, including Barbados and Trinidad and Tobago, are well known for having crude oil – discoveries that were made more than 100 years ago through surface oil seeps and later proven with exploration drilling. While these mature areas are well know, opportunities remain for new and exciting discoveries in these areas. Add to this list the less mature areas where there is exploration potential, hydrocarbons to be produced and not surprisingly money to be made. Focus on the companies We focus on the up-and-coming regional players. In Trinidad and Tobago, the offshore has garnered the most recent interest with continuing large discoveries of natural gas. However, the onshore region is not finished and we look at companies operating in both areas. Further away, with undiscovered resources and a small oil and gas sector, is the Guyana- Suriname Basin, where oil production exists but upcoming exploration activity from large international and smaller, exploration- focused companies is underway. New company initiation reports included As part of our regional study, we are initiating coverage on two Trinidad and Tobago offshore exploration companies and one early-stage exploration company in Guyana. Company Ticker Current Price Rating 12-month target Canadian Superior Energy Inc. SNG : TSX C$1.94 SPECULATIVE BUY C$4.50 CGX Energy Inc. OYL : TSX-V C$0.49 SPECULATIVE BUY C$1.80 Challenger Energy Corp. CHQ : TSX-V C$2.20 SPECULATIVE BUY C$5.25

Transcript

Canaccord Adams is the global capital markets group of Canaccord Capital Inc. (CCI : TSX|AIM)

The recommendations and opinions expressed in this Investment Research accurately reflect the Investment Analyst’s personal, independent and objective views about any and all the Designated Investments and Relevant Issuers discussed herein. For important information, please see the Important Disclosures section in the appendix of this document. 5 November 2008 2008-185

INSIDE Summary ..................................................... 2 The Caribbean – An Overview.................... 3 Caribbean Geology ..................................... 4 Trinidad and Tobago................................... 9 Guyana ......................................................21 Suriname...................................................26

Company Feature Summaries .............. 30 Canadian Superior Energy Inc. ............31 CGX Energy Inc......................................45 Challenger Energy Corp........................61 Petro Andina Resources Inc.................73 Primera Energy Resources Ltd. ...........77 Voyager Energy Ltd. ..............................81

Energy – Oil and Gas, Exploration and Production

South American Offshore – The Caribbean Report It’s not just on the beach – there’s oil there The Caribbean is probably best-known as a destination for golden sun and sand, but looking around the Caribbean basin, especially off the northern coast of South America, we find gold of a different colour: black gold, and with it trillions of cubic feet of natural gas. Although this area may not be high on the explorers’ lists of prospect regions, exploration is underway and it is generating results.

Mature and not-so-mature Regions of the Caribbean basin, including Barbados and Trinidad and Tobago, are well known for having crude oil – discoveries that were made more than 100 years ago through surface oil seeps and later proven with exploration drilling. While these mature areas are well know, opportunities remain for new and exciting discoveries in these areas. Add to this list the less mature areas where there is exploration potential, hydrocarbons to be produced and not surprisingly money to be made.

Focus on the companies We focus on the up-and-coming regional players. In Trinidad and Tobago, the offshore has garnered the most recent interest with continuing large discoveries of natural gas. However, the onshore region is not finished and we look at companies operating in both areas. Further away, with undiscovered resources and a small oil and gas sector, is the Guyana-Suriname Basin, where oil production exists but upcoming exploration activity from large international and smaller, exploration- focused companies is underway.

New company initiation reports included As part of our regional study, we are initiating coverage on two Trinidad and Tobago offshore exploration companies and one early-stage exploration company in Guyana.

Company Ticker Current Price Rating 12-month target Canadian Superior Energy Inc. SNG : TSX C$1.94 SPECULATIVE BUY C$4.50 CGX Energy Inc. OYL : TSX-V C$0.49 SPECULATIVE BUY C$1.80 Challenger Energy Corp. CHQ : TSX-V C$2.20 SPECULATIVE BUY C$5.25

2

South American Offshore 5 November 2008

SUMMARY

In this report we focus on the offshore hydrocarbon potential of the Caribbean adjacent to South America. There are several countries with known hydrocarbon potential and production in the region and other countries that have limited hydrocarbon production but tremendous potential. We have reviewed the region as a whole and, for the purposes of this report, we look at Trinidad and Tobago, Guyana, and Suriname. As part of this review we will also look at companies operating in these areas and highlight new research coverage.

With the popularity of oil and gas in Colombia drawing attention to the South American continent, investors and oil and gas companies alike are looking further afield for investment opportunities. Colombia’s offshore potential is well known, as the country currently produces a majority of its natural gas production from the offshore Caribbean natural gas field at Guajira.

Wrapping around the northern edge of the continent and adjacent to Colombia is the country of Venezuela. Onshore, this country has significant hydrocarbons which appear to extend into tremendous offshore hydrocarbon resource potential. Unfortunately the exploration of this potential is currently limited due to the country’s current political landscape. But extending to just offshore Venezuela is the Caribbean nation of Trinidad and Tobago. This country has long been an area of known oil potential, with surface oil seeps having been used as caulking for ocean-going ships for centuries. There is a long history of oil production from onshore Trinidad, but more recently natural gas production, located offshore Trinidad and Tobago has become the dominant hydrocarbon product of the country. Trinidad and Tobago has become a prime exporter of Liquefied Natural Gas (LNG) to the US and the world through the installation of LNG processing facilities and production. Just 10 years ago production of natural gas was approximately 1.0 Bcf per day – this has now increased to more than 4.0 Bcf/d with the potential to grow further.

As part of our report, we also reviewed companies operating in the Caribbean region. Most notable is the exploration currently underway offshore Trinidad by Canadian Superior and its joint venture group, where as much as 4 trillion cubic feet of natural gas may have been discovered in 2008.

But the known hydrocarbon resources come at a price – the upcoming bidding round for new offshore blocks in Trinidad is expected to be highly contested, given the proximity of the acreage to the new offshore discoveries made by Canadian Superior, et al.

Wrapping further eastward around the northern coast of South America, oil and gas potential still exists. Excluding Venezuela (for now), oil and gas companies are seeing tremendous potential in Guyana and neighbouring Suriname. While no significant recent discoveries have yet been made, the Guyana-Suriname Basin has been identified by the US Geological Service as a very underexplored basin, with potential that could exceed 15 billion barrels of oil with natural gas potential of 42 trillion cubic feet. In this report, we will also examine that area’s potential and operations that are currently underway.

3

5 November 2008 The Caribbean Report

THE CARIBBEAN – AN OVERVIEW

Long considered a hot spot for winter sun seekers from North America and Europe, as well as vacationing sailors, the Caribbean has not been well thought of as a source of oil and gas production. Most people think of Caribbean oil as what’s been spilled on the beach from suntan lotion bottles!

Figure 1: Caribbean region oil production or shows

Source: Google Maps, Canaccord Adams

But think again.

Our specific area of interest is the Caribbean off the coast of South America as shown on the map in Figure 1. The oil and gas potential of South America is well known, given the history of production from Venezuela and Colombia, both located on the northern coast of the continent. However, in addition to extensive oil and gas production (and offshore potential) in these two countries, there has been a long history of oil production from the island of Barbados and the island of Trinidad. (More recently, offshore gas production from Trinidad has been a major new export for the country). In addition to hydrocarbons from the islands, there has been production from onshore Suriname and exploration has also yielded oil and gas shows offshore Suriname and Guyana. While not close to the region in question, explorers have gone further afield and have also found indications of oil and gas in Nicaragua in Central America. While many think of the Caribbean as a holiday destination, it is clear that there is oil and gas potential in the region.

4

South American Offshore 5 November 2008

CARIBBEAN GEOLOGY

The structural geology of the Caribbean region is surprisingly complex. In the technical readings done to prepare for this report, we noted that even the experts can not fully agree on the full technical development of the region. However, there is enough “big picture” information to explain how the region was formed. With this understanding, it is easy to see how the prospectivity of the region developed and supports the currently known oil and gas potential of the area.

Throughout the Earth’s history, the continents have moved and been joined to one another in some form or fashion. Plate tectonic models have identified the supposed

orientation of the Earth’s crusts as far back as 750 million years ago1.

However, our interest in plate tectonics is only related to the past 250 million years. As shown below, approximately 250 million years ago, the plates of the world were all clustered together as shown below. Note in particular the orientation of North America, South America and Africa.

Figure 2: Plate tectonics – 250 million years ago

Source: Lawver et al; Plates 2002

The significance of this map is not just to the subject of our report. Over time, as the continents started to move apart, major oil and gas regions were formed due to deposition of sediments and faulting. Outside of the Caribbean one most notable impact is the discovery of very significant oil and gas deposits off the eastern coast of South America (Brazil) and the western coast of Africa (Angola).

Starting approximately 170 million years ago (Middle Jurassic), the three continents started moving. Most notable is the movement of North America away from the other two continents. The significance of this event is that it correlated to the formation of the

1 Atlas of Plate Reconstructions, Lawver, Dalziel, Gahagan, Martin and Campbell, 2002

Africa

North America

South America

Caribbean

5

5 November 2008 The Caribbean Report

Atlantic Ocean between North America and Africa and also provided for the formation of reefs and ultimately carbonate formations in the Caribbean area.

Figure 3: Plate tectonics – 170 million years ago

Source: Lawver et al; Plates 2002

Guyana/Suriname potential created by well-understood processes As the Atlantic Ocean was forming, there were changes occurring on all three continents. Specifically, with the movement of the continents away from each other, there occurred uplift of the continents due to the release of geologic stresses and movements of the tectonic plates.

This tectonic movement created the conditions that account for the hydrocarbon potential today. Uplift of the continents (specifically South America) resulted in erosion on the land mass over time. With the erosional process, there was a long period of deposition at the continental margins of thick sedimentary sequences, rich in organic material, well-sorted sandstones and mudstones/claystones and siltstones.

As South America and Africa separated from each other, thick sedimentary sequences from the erosional processes were created in the Caribbean area. Notable was the

creation of large turbidite fan sequences off the coast of northeast South America2. These are now primarily located off the coast of Guyana and Suriname and are identified as the Guyana-Suriname Basin.

2 US Geological Survey World Petroleum Assessment, 2000

6

South American Offshore 5 November 2008

Figure 4: Plate tectonics – 90 million years ago

Source: Lawver et al; Plates 2002

Structural geology drives Trinidad and Tobago Oil and Gas At the same time as the thick sedimentary deposits were being made off the northeast coast of Guyana/Suriname, plate tectonics in the Caribbean were forming this region. In the Late Cretaceous (80 million years ago), the movement of the Caribbean Plate between North and South America commenced.

Figure 5: Movement of the Caribbean Plate (20 million years ago)

Source: Lawver et al; Plates 2002

Starting on the Pacific Ocean side of the continents, the Caribbean plate started moving from west to east as highlighted above in Figure 5. From 80 million to 20 million years ago, the Caribbean Plate continued to move across the top of South America as the continents drifted apart. Further movement of the Caribbean Plate over the past 20 million years has resulted in the structural geological elements of the Caribbean as it stands today.

7

5 November 2008 The Caribbean Report

Figure 6: Caribbean Plate representation

Source: Jackson School of Geosciences, University of Texas at Austin website; Canaccord Adams

This movement of the Caribbean Plate was resisted by both the South American Plate and the North American Plate. As a result, at the margins of the plates, significant faulting and deformation occurred. With the depositional environment providing organic source rock and the geologic environment providing temperature and pressure creating the geologic kitchen, a perfect environment for the formation of hydrocarbons occurred.

Figure 7: Structural areas offshore Trinidad

Source: Leslie J. Wood and Carolyn Roberts “Opportunity in a World-class Hydrocarbon Basin; Trinidad and Tobago’s Eastern Offshore Marine Province” Houston Geological Society Bulletin, June 2001

Caribbean Plate Margin

Trinidad

Large Natural Gas discoveries in this area

8

South American Offshore 5 November 2008

As highlighted above, at the margin of the Caribbean Plate in Trinidad’s offshore waters, large natural gas structures have been discovered in fractured and faulted zones. Most notable are some of the fields highlighted below in Figure 8.

Figure 8: Offshore Trinidad natural gas discoveries

Field Name Discovery Date

Total Recoverable Reserves (Tcf) Partners

East Manzanilla 08 May 1972 0.32 BP* (70.00%), Repsol YPF (30.00%) Juniper 11 Feb 1996 1.91 BP* (70.00%), Repsol YPF (30.00%) Mahogany 13 Sep 1973 2.38 BP* (70.00%), Repsol YPF (30.00%) Manakin 10 May 2000 1.07 BP* (70.00%), Repsol YPF (30.00%) Savonette 18 Dec 2004 2.11 BP* (70.00%), Repsol YPF (30.00%) Dolphin 21 Nov 1976 4.26 BG* (50.00%), Chevron (50.00%) Dolphin Deep 15 Aug 1998 0.50 BG* (50.00%), Chevron (50.00%) Manatee 03 Mar 2005 1.67 Chevron* (50.00%), BG (50.00%) Starfish 30 Nov 1998 0.43 BG* (50.00%), Chevron (50.00%) Toucan 30 Jan 2006 0.70 EOG Resources* (90.00%), CL Financial

(10.00%)

*Operator of the field. Source: Wood Mackenzie

Figure 9 below shows a more detailed interpretation of the prospectivity of this offshore area. At the margin of the Caribbean Plate and the South American Plate, significant anticlinal features have been created. It is in this area that, with a combination of other structural geological elements, the major natural gas fields of Trinidad have been discovered.

GOVERNMENT The country of Trinidad and Tobago (more commonly referred to as “Trinidad”) became a republic in 1976 after gaining its independence in 1962 from the UK. The government system mimics the Westminster (British Parliamentary System) model of government, which values parliamentary democracy. The Executive branch includes the President, Prime Minister, and Cabinet. The Legislative branch includes the bicameral parliament, which consists of 31-seat Senate whom are appointed by the President and a 36-seat House of Representatives whom are elected by popular vote. The judicial branch includes an independent court system and since the country remains a member of the British Commonwealth, the highest court of appeal is London’s Privy Council.

Parliament members elect a President for a five-year term and are instrumental in electing a Prime Minister. The Prime Minister, who is appointed by the President, is generally the Member of Parliament who received the most parliament-member votes. The current President is George Maxwell Richards, who was reelected to a second five-year term on February 11, 2008. Patrick Manning, who holds both the position of Prime Minister and Minister of Finance, has held his positions since December 2001. Currently, the People’s National Movement (PNM), United National Congress (UNC), and the Congress of the People (COP) are the major political parties; these parties are interested in increased foreign investment and pursuing free mark economic policies.

Since gaining its independence in 1962, Trinidad has developed and forged strong relationships with the United States and Europe, both of which are two of the country’s main trading partners. Trinidad has taken a lead role in the Caribbean Community and Common Market (CARICOM), where it was both an advocate and instrumental in strengthening economic conditions and securing political security and integration. Trinidad has many planned, executed, and proposed foreign investment projects. The government wants to increase and expand foreign investment within the country. The history of successful foreign business can be attributed to several factors, including but not limited to: a history of prosperous oil and gas industry, consistent democratic legislation and government, accessible raw materials, and a strong fiscal regime promoting foreign investment. The following chart shows foreign direct investment in Trinidad since 1998.

10

South American Offshore 5 November 2008

Figure 10: Trinidad and Tobago’s historical foreign direct investment

680

835791 808

998940

788

0

200

400

600

800

1,000

1,200

1998 1999 2000 2001 2002 2003 2004

US

$B

Source: Nations Conference on Trade and Development (UNCTAD), World Investment Report 2007

ECONOMY Trinidad has shifted from an oil-based economy to a gas-based economy. The oil and gas industry in Trinidad began with oil exploration and production. During the 1950s, significant gas production began to take place. From 1950 onwards, enormous volumes of natural gas reserves were discovered while exploring for oil. Natural gas boomed in the 1980s and became an integral part of Trinidad’s economy. Starting in the late 1970s natural gas production started a steady growth curve. However, it was not until 2000 when significant Liquefied Natural Gas (LNG) projects commenced that gas production grew significantly. Average natural gas production in Trinidad for 2007 was approximately 3.9 bcf/d. The following graph displays Trinidad’s evolution from an oil-based country to a predominantly natural gas-based country.

11

5 November 2008 The Caribbean Report

Figure 11: Trinidad and Tobago’s crude oil and natural gas average production

0

50

100

150

200

250

300

80 83 86 89 92 95 98 01 04 07

Oil

Prod

uctio

n (m

bls/

d)

0

500

1,000

1,500

2,000

2,500

3,000

3,500

4,000

4,500

Nat

ural

Gas

Pro

duct

ion

(mm

cf/d

)

Oil ProductionNatural Gas Production

*Natural Gas Production for 2007 is based on the CIA Factbook Estimate Source: Energy Information Agency, Canaccord Adams

Trinidad, which has one of the highest GDP growth rates in Latin America, has gained the reputation of being an excellent investment area for international business. The country’s growth can be attributed to oil and gas exploration, LNG, petrochemicals, and steel. GDP in 2007 was $23.8 billion, with oil and gas accounting for approximately 40% of the total. The 2007 GDP breakdown is approximately 0.6% agriculture, 61.9% industry, and 37.5% services. The following graph displays Trinidad’s GDP growth since 2003.

Figure 12: Trinidad and Tobago’s historical GDP

11.2

12.7

15.1

18.2

20.7

25.0

0%

2%

4%

6%

8%

10%

12%

14%

16%

2003 2004 2005 2006 2007 2008*

Rea

l GD

P G

row

th Y

/Y (%

)

5

10

15

20

25

GD

P (U

S$

BN

)

GDP (US$BN) (current prices)

Real GDP Growth (% change Y/Y)

Source: Australian Department of Foreign Affairs *Estimate for 2008

12

South American Offshore 5 November 2008

The oil and gas industry accounts for approximately 80% of exports and 5% of total employment. Economic growth in 2006 was approximately 12.2% and 5.5% in 2007, fuelled by a growing trade surplus and increasing prices of oil, LNG and petrochemicals. Additionally, during this period the energy sector increased its capacity as foreign investment increased, with a particular focus on oil and gas. Oil and gas plays a vital role in Trinidad’s economy as shown below.

Figure 13: Trinidad and Tobago’s GDP composition

Source: Minister Of Energy And Energy Industries (MEEI) Presentation, 2008

Trinidad exports petroleum and petroleum products, LNG, methanol, ammonia, urea, steel products, beverages, cereal and cereal products, sugar, cocoa, coffee, citrus, fruit, vegetables, and flowers. Additionally, Trinidad is the largest exporter of LNG to the US in the world. Of the total LNG exports in Trinidad, 65% is shipped to the US. The following graph displays Trinidad’s LNG export markets.

Figure 14: Trinidad and Tobago’s LNG exports destinations

Source: BP Statistical Review of World Energy, 2007

13

5 November 2008 The Caribbean Report

Figure 15: Trinidad and Tobago’s LNG exports by country

Source: BP Statistical Review of World Energy, 2007

Figure 16: LNG exporting countries

Source: BP Statistical Review of World Energy, 2007

14

South American Offshore 5 November 2008

OIL AND GAS INDUSTRY In 2007, Trinidad and Tobago’s total crude oil production was 121.4 million barrels a day, with exports of 99 million barrels a day to the US. According to the CIA World Factbook, total crude oil proved reserves are approximately 605.8 million bbl as of January 2007. In 2007, estimated aggregate natural gas production was approximately 1.4 trillion cubic feet,

allowing for natural gas exports of 742.7 billion cubic feet.3 According to Ryder Scott, total natural gas Proven reserves as of year-end 2007 totaled 17.0 trillion cubic feet and Proven plus Probable (2P) reserves were 24.9 trillion cubic feet.

Figure 17: Trinidad and Tobago’s oil and natural gas production

Source: The Natural Gas Company of Trinidad and Tobago Ltd., 2007

Trinidad has a large and increasing domestic demand for gas. The country’s extensive collection of petrochemical plants and infrastructure play a significant role in Trinidad’s domestic demand of approximately 1.58bcfd. According to Wood Mackenzie’s estimates, over the next 15 years (2008-2022) approximately 11.4 tcf of gas will be required to supply existing projects, and over the next 20 years the supply requirement is expected to soar to approximately 15.7 tcf. Trinidad’s domestic demand is expected to increase

29% from 1.58 bcf/d in 2007 to 2.04 bcf/d in 2011.4 The following graph represents Trinidad’s historical natural gas production and consumption.

3 CIA Factbook 4 Wood Mackenzie

15

5 November 2008 The Caribbean Report

Figure 18: Trinidad and Tobago’s natural gas production vs. consumption

Source: CIA World Fact Book - 2007 Estimate, Energy Information Agency (EIA)

Over the next several years, Trinidad needs to discover new natural gas reserves in order to supply existing demand as well as future additional demand. Wood Mackenzie’s demand base case forecast for Trinidad expects that 24.9 tcf of gas will be required over the next 15 years and 33.7 tcf over the next 20 years. These figures are not including proposed new project requirements, which could add an additional 1.7 tcf over 15 years. As mentioned above, current Proven plus Probable reserves according to Ryder Scott are approximately 24.9 tcf. As a result, Trinidad desperately needs to discover new reserves as they fall short, potentially causing the country to be a net importer of natural gas.

The government is attempting to reduce its demand requirements and increase its reserve supply through several means, including:

• Construction of “Train X” (a new LNG processing train) has been postponed until new gas discoveries are made

• The Eastern Caribbean Gas Pipeline, which was a proposed project to build a gas pipeline from Trinidad north to nearby islands including Grenada, Saint Lucia and Barbados.

• Offer better incentives for new exploration. A full review of Trinidad’s upstream fiscal regime is in order, beginning with a review of the PSC terms for new acreage. Trinidad’s 2006 bidding round provoked little interest from businesses, after Trinidad initiated the new “Taxable PSC” terms into the bid rounds.

• The government plans on holding a bid round late in 2008/early 2009 to spur new exploration in Trinidad. The structure of the existing bid round process can take over a year before any contracts are finalized. Expediting this process will help fuel further exploration. (We note that the recent discovery by Canadian Superior et al has likely fueled interest in the upcoming bid round).

16

South American Offshore 5 November 2008

• Potential increase of domestic natural gas prices. The domestic market of Trinidad is paying approximately US$2/mmbtu for gas, compared to LNG, which offers a significantly higher netback in excess of US$5/mmbtu or more. Accounting for the current economic outlook, including rising inflation and the fact that exploration in Trinidad is becoming much more risky and costly, increased domestic gas prices to account for the changing times would reduce domestic consumption and position itself as an economically feasible option compared to LNG.

The following figure highlights Trinidad’s reserve estimates as evaluated by Ryder Scott. Since 2001, the Trinidad government has had six reserve reports prepared. It is clear that over the last three years the country’s overall Proven plus Probable plus Possible (3P) reserves are decreasing.

Figure 19: Trinidad and Tobago’s reserves estimates

17.118.8 17.0

9.07.8 7.9

7.1

6.2 5.9

0

5

10

15

20

25

30

35

40

2004 2006 2007

Trill

ion

Cub

ic F

eet

Proved Probable Possible

Source: Ryder Scott Presentation, July 2008

Production Sharing Contracts (PSC) International oil and gas companies hold a significant stake in the Trinidad and Tobago energy industry. Some of the largest oil and gas companies in the world operate in Trinidad and Tobago. Since 1995, 21 Production Sharing Contracts (PSC) have been awarded to companies such as ConocoPhillips, British Gas, ExxonMobil, BHP Billiton, PetroCanada, and even Enron. However, smaller companies are starting to enter the area such as Canadian Superior Energy, Challenger Energy and EOG Resources. These 21 PSCs awarded since 1995 are reflected in the figure below.

17

5 November 2008 The Caribbean Report

Figure 20: Trinidad and Tobago’s production-sharing contracts history

1995-2002 Blocks Acreage Effective Date Company (main operator) 2(c.) 51,772 April 1996 BHP 2(ab) 133,504 June 1996 BHP Modified U(a) 38,881 July 1996 Enron S11(b) 39,260 November 1996 Elf 5(b) 73,691 January 1997 Amoco NCMA1 93,949 March 1997 British Gas 4(a) 45,743 June 1997 Conoco 4(b) 75,333 June 1997 Conoco 5(a) 40,761 December 1997 British Gas 25(a) 138,811 February 1998 Shell 25(b) 139,076 February 1998 Exxon 26 119,520 February 1998 Exxon 27 117,880 February 1998 Arco 3(a) 614 sq. km. April 2002 BHP Billiton Lower Reverse "L" 364 sq. km April 2002 EOG Resources 2005 Blocks Acreage Effective Date Company (main operator) 1(a) 62,011 July 2005 Petro-Canada/Petrotrin 1(b) 58,591 July 2005 Petro-Canada/Petrotrin 3(b) 64,476 July 2005 Kerr McGee/Primera 4(a) 45,727 July 2005 EOG Resources/Primera 5(c.) 32,392 July 2005 Canadian Superior 22 296,805 July 2005 Petro-Canada

Source: Trinidad and Tobago: Ministry of Energy and Energy Industries website

In January 2006, the Government of Trinidad opened a competitive bidding round for the exploration and production of eleven blocks, including eight onshore/near shore, and three shallow marine blocks. Later in June 2006, the Government furthered its offerings through the tender of one Deep Atlantic Block. The bidding round ultimately attracted eleven companies, resulting in 14 bid proposals for eight blocks and one proposal for the Deep Atlantic block.

The Government of Trinidad plans on hosting an open bidding round late 2008/early 2009. On offer are blocks from the North Coast Marine Area (NCMA), and in the East Coast Marine Area (ECMA). The following blocks are expected to be open for bidding.

18

South American Offshore 5 November 2008

Figure 21: Trinidad and Tobago’s available concessions

Source: Trinidad and Tobago: Ministry of Energy and Energy Industries website

Figure 22: Trinidad and Tobago’s bidding round 2008/2009

2008 Bidding Round – Q4 2008 North Coast Marine Area Blocks Acreage Water Depth (ft) NCMA 3 2100 km² 100-300 NCMA 4 1800 km² 200-400 NCMA 5 2300 km² 100-350

2009 Bidding Round - Deep Atlantic Area East Coast Marine Area Blocks Acreage Water Depth (ft) Block 4(b) 750 km² 1300-2700 Block 5(d) 700 km² 1400-2700

Source: Trinidad and Tobago: Ministry of Energy and Energy Industries website

Fiscal regime The Petroleum Act (1969), Petroleum Regulations (1970), and the Petroleum Taxes Act (1974) govern the petroleum industry in Trinidad. The Petroleum Act created a structure for the grant of licences and contracts for petroleum operations in the area, including both onshore and offshore activities. The Act established the areas to be allowed for petroleum operations. Additionally, a land right to explore and produce petroleum from these given areas is decided through competitive bidding. Once bidding has taken place, the following types of licences/contracts can be offered:

• Exploration Licence: allows the licensee(s) the right to conduct operations, with terms according to the licence, in the given area.

• Exploration and Production Licence: allows the licensee(s) the sole right, with rules according to the licence, to explore and produce all petroleum opportunities within the given area.

19

5 November 2008 The Caribbean Report

• Exploration and Production (Private Petroleum Rights) Licence.

• Production Sharing Contract (PSC): an agreement where the licensee(s) have an agreement with the host government. According to the agreement, which varies between contracts, the contractors carry all exploration and development risks in order to be granted a share of the potential production.

The current energy taxation/fiscal regime is a two-tier system including a production based tax, which includes a Royalty, Production Levy, and a Supplemental Petroleum Tax (S.P.T.). The second-tier is a profits based tax, which has a Petroleum Profits Tax and an Unemployment Levy. The government has added incentives to attract business investments. The following table outlines the fiscal regime.

Figure 23: Trinidad’s fiscal regime

Production-Based Tax Royalty Tax 12.5% of all hydrocarbon production. Production Tax Value ranges.

Maximum of 3% of gross income earned from crude oil production. Rate is unique to each project.

S.P.T. Charged on production of crude oil. Rate is defined by oil price sensitivities. Ranges from 0% to 35% for crude in excess of US$49.50/bbl.

S.P.T. Allowable Deductions 50% of geological/geophysical costs. 100% of drilling exploration wells direct costs. 40% of direct intangible drilling costs. 40% of tangible development costs. Royalty payments.

Profits-Based Tax P.P.T. 50% of gross revenue less deductible

expenses/allowances Unemployment Levy 5% with eligible deductions.

Including: Operating/Administrative Expenses. Royalty Tax. Production Tax. S.P.T. Payments. Capital Allowances. Heavy Oil Allowance.

Source: Trinidad and Tobago: Ministry of Energy and Energy Industries website

Infrastructure Trinidad relies heavily on LNG plants to facilitate the transportation of natural gas between their country and other countries. An LNG plant uses “trains” to properly convert and process the LNG, where the gas passes through a compression area, propane condenser area, and methane and ethane areas before being liquefied. The process of bringing LNG to market takes several steps, including:

• Producing the natural gas (15% of cost);

• Liquefying the natural gas through LNG plants (trains) (40% of cost);

• Shipping the LNG (25% of cost);

• Re-gasification—turning the LNG back into a gas (20% of cost);

• Bring the natural gas to market.

20

South American Offshore 5 November 2008

The Atlantic LNG Company of Trinidad, with operations in Point Fortin, Trinidad, currently operates four LNG trains. The trains are owned by various companies, including: BG, BP, Repsol YPF, NGC Trinidad LNG, and Suez. These are the only LNG trains operated in Trinidad. The four trains have a combined production capacity of approximately 15.3 million metric tones per annum. LNG trains account for a significant portion of domestic demand for gas (approximately 59%). Currently, all four trains are at full capacity and require approximately 2.5 billion cubic feet a day of natural gas to run the trains. Wood Mackenzie believes that feedstock requirements will increase to 13.5 tcf over the next 15 year period (2008 to 2022) and 18.0 tcf over the next 20-year period (2008-2027).

A fifth train, or “Train X,” has been proposed; however, the project has been put on hold until further discoveries or new production becomes available. The following figure displays information regarding the four current trains in Trinidad.

Figure 24: Atlantic LNG liquefaction trains information

Source: BG Trinidad and Tobago Limited

21

5 November 2008 The Caribbean Report

GUYANA

GOVERNMENT The government of Guyana is run under a semi-presidential representative democratic republic system, where the President of Guyana heads both the government and multi-party system. This system is basically a hybrid of the Westminster (British Parliamentary System) style democracy and the Philadelphia (Presidential) system. Executive power is exercised by the government, but legislative power is vested in both the government and National Assembly of Guyana, which is the country’s parliament. The judicial system is independent from executive and legislative powers.

Currently, there are two main political parties in Guyana: the Peoples’ Progressive Party or PPP, and the Peoples National Congress or PNC. Parties are elected every five years; the PPP currently forms the government. The government system considerably lowers the risk to foreign investment compared to its neighbor Venezuela.

Guyana’s government is inclined to attracting more foreign investment. Both public and private business leaders have declared their openness and willingness to foreign investment. This approach is confirmed with Guyana’s conduct towards foreign investors, who are treated the same as domestic investors. In addition, there are many attractive incentives to doing business in Guyana. Incentives include a flat tax rate, tax holidays, export tax allowances and waivers of custom duties. Specifically, custom duties waivers cover plant, machinery and equipment imports (with the permission of the Commissioner General). Due to the amicable relations between Guyana and the U.S., Guyana offers the same high quality and reliable low cost goods as the U.S. Additionally, many Guyanese importers favor U.S. suppliers. The following chart shows foreign direct investment in Guyana since 2003. Foreign Direct Investment from 2004 to 2006 has increase significantly due to improved investment climate in the country. Specifically, the increase is a result in the government’s aim to maintain infrastructure needed to maintain growth and development, such as roads, bridges, sea defense, drainage and irrigation, and schools. Moreover, the government is also allocating funds for

improvement in agriculture, housing and water, and national security.5

5 US State Department

22

South American Offshore 5 November 2008

Figure 25: Guyana’s historical foreign direct investment

67

56

44

2630

77

102

0

10

20

30

40

50

60

70

80

90

100

110

2000 2001 2002 2003 2004 2005 2006

FDI (

In U

S$M

M)

DFI Flow (US$MM)

Source: Nations Conference on Trade and Development (UNCTAD), World Investment Report 2007

Natural resources in Guyana are vast and include mineral deposits of gold, bauxite, diamonds and potentially large reservoirs of oil and gas in the minimally explored Guyana-Suriname Basin and Takatu Basin. Although the country is known primarily for its rice and sugar production capabilities, its agricultural industry includes fresh fruits and processed vegetables. Another potentially lucrative resource is Guyana’s forestry, which is only beginning to be exploited. The U.S. Commercial Service from the Department of Commerce lists the sectors with the best prospects in Guyana as Agricultural Machinery/Equipment, Telecommunications Equipment, Mining Industry Equipment, Computers/Peripherals, Automotive Parts, Construction Equipment, and Architectural/Construction/Engineering Services.

A major block of foreign investment into the country’s oil and gas industry resulted from an offshore border dispute between Guyana and Suriname. The dispute had flared up in June 2000, when CGX Energy was drilling for oil under a Guyanese concession and was forced to cease operations by Surinamese military gunboats. After several failed attempts at negotiation, in 2004 Guyana took the dispute to the UN Law of the Sea tribunal, which unanimously determined that the vast majority of the area in contention belonged to Guyana. The resolution of the dispute is expected to very positive for Guyana's economy in

the long term, as the seabed is estimated to contain approximately 15 billion barrels of oil.6

6 US State Department

23

5 November 2008 The Caribbean Report

Figure 26: Guyana’s export partners

Canada

U.S.

U.K.

Portugal

Trinidad and Tobago

France Netherlands

Jamaica

0%

2%

4%

6%

8%

10%

12%

14%

16%

18%

20%

Perc

enta

ge o

f Tot

al E

xpor

ts

Source: CIA World Factbook

Although the oil and gas industry has not historically been an important part of Guyana’s economy, the potential is there. Depending on exploration results and Guyana’s ability to attract more foreign exploration and production companies, oil and gas could be a lucrative opportunity to boost Guyana’s economy. With the end of Guyana and Suriname’s border dispute, the biggest block against foreign investment has been resolved. The U.S. Geological Survey estimates there are potentially 15 billion barrels of oil and 42 trillion cubic feet of gas lying off the shores of Guyana and Suriname. Until a bidding process is created, Guyana will continue to award licences and concessions on a first-come first-served basis. The Petroleum Division of the Guyana Geology and Mines Commission is in charge of negotiating the exploration contracts. Guyana had no oil and gas production in 2007.

Guyana has two basins of interest, the Guyana-Suriname Basin which is located both onshore and offshore, and the onshore Takatu basin. The Guyana-Suriname Basin is a classic passive margin basin associated with the opening of the Central Atlantic. Its stratigraphic and sedimentation framework is comparable to the Espirito Santo and Campos basins, especially in terms of the shelf and basin stratigraphy. The difficulty in this basin for petroleum exploration is finding prospective traps of oil from the migration path of the source rock. The Takatu basin origins from a failed rift associated with the opening of the Central Atlantic. However, both basins have not been explored enough to be completely understood.

24

South American Offshore 5 November 2008

Figure 27: Guyana-Suriname Basin

Source: www.economist.com

The fiscal regime in Guyana consists of two licences, one for exploration and the other for production. The Petroleum Prospecting Licence includes a waiver of duty for imports of petroleum equipment, reduction of duty to nominal levels on fuel for exploration operations and exemption for the contractor from certain provisions of the Corporate Tax Act. For both exploration and production, there are no tax obligations and a 10% reduction on all fuel costs. The government has a minimum discretionary position to profit from the split of oil production with the contractor; contractors can make a maximum of 50%. The Petroleum Prospecting Licence is for an initial period of four years with provision for two further renewal periods with each period lasting no more than three years. The renewal period is at the option of the licensee. The Petroleum Production Licence has an initial period of 20 years, potentially followed by one renewal period up to 10 years, which is also at the option of the licensee. CGX Energy, a Canadian exploration and production company with interests in Guyana, estimates that using full-cycle economics, the licensee’s share of gross revenue is 63%.

Figure 28: Guyana’s exploration licences

Area/Block/Licence Acreage (MM) Company (main operator) Corentyne Licence 3.8 CGX Energy Georgetown Licence 2.8 CGX Energy and Repsol YPF Pomeroon Licence 2.8 CGX Energy Exxon Licence 17.0 ExxonMobil Takatu Basin Area 2.7 Groundstar Resources

Source: CGX Energy Corporate Website, Groundstar Resources Corporate Website

25

5 November 2008 The Caribbean Report

Figure 29: Guyana’s offshore exploration licences

Source: CGX Energy Corporate Website

Exploration and production companies operating in Guyana include Exxon-Mobil, Century Oil, CGX Energy, Repsol YPF, Maersk Oil, and Groundstar Resources.

26

South American Offshore 5 November 2008

SURINAME

GOVERNMENT Suriname’s government is a constitutional democracy, consisting of a 51 member National Assembly. The President must be chosen by a minimum of 2/3 of all votes of the National Assembly or else a People’s Assembly will be formed. If a President is elected, he or she appoints a 16 member cabinet. The President also selects 10 commissioners, one for each administrative district of Suriname.

ECONOMY Suriname’s economy is highly dependent on mining and petroleum exploration, with 85% of exports coming from aluminum, gold and oil. Although aluminum accounted for 46.2% of all exports in 2006, government revenue from oil is now higher than that of both bauxite and aluminum. At present time, Suriname is doing relatively well when compared with its history. In 2000, when the government of Ronald Venetiaan came into power, inflation was over 100% and the fiscal deficit was growing. In 2006, inflation had fallen to a more manageable 5.6%. Real GDP annual growth for 2006 was 5.8% and 2007 GDP was US$ 2.23 billion. Canada is an important part of Suriname’s trade, purchasing approximately 24.5% of Suriname’s exports. The Venetiaan government has also been successful at managing its fiscal debt; a ceiling of 60% debt to GDP was put in place during 2002.

Figure 30: Suriname’s export partners

Canada

Norway

Belgium U.S.U.A.E.

France

Venezuela

0%

5%

10%

15%

20%

25%

Perc

enta

ge o

f Tot

al E

xpor

ts

Source: CIA World Factbook

Each investment project is individually negotiated by Suriname’s government. Keeping good business relations with the U.S. is crucial to Suriname due to various U.S. firms

27

5 November 2008 The Caribbean Report

operating in the country, including Suralco, Exxon-Mobil, Texaco, IBM and Alico. Additionally, Suriname is highly dependent on its relations with the Dutch government.

OIL AND GAS INDUSTRY The country has a state owned petroleum firm called Staatsolie. Many of the foreign companies operating in Suriname are doing so through production sharing contracts with Staatsolie, including Repsol YPF, Noble Energy, Maersk Oil, Teikoku, Murphy Oil and Tullow Oil. In addition, Staatsolie also has a 100% subsidiary called Paradise Oil. In 2007, Staatsolie contributed US$150 million to the government’s budget. ROE was 54% on a net profit of US$ 225 million. Total crude oil production for Suriname in 2007 was 13,500 bbl/d.

Figure 31: Suriname’s historical oil production

8

9

10

11

12

13

14

2000 2001 2002 2003 2004 2005 2006 2007

Thou

sand

s of

bar

rels

a d

ay

Source: Energy Information Agency (EIA)

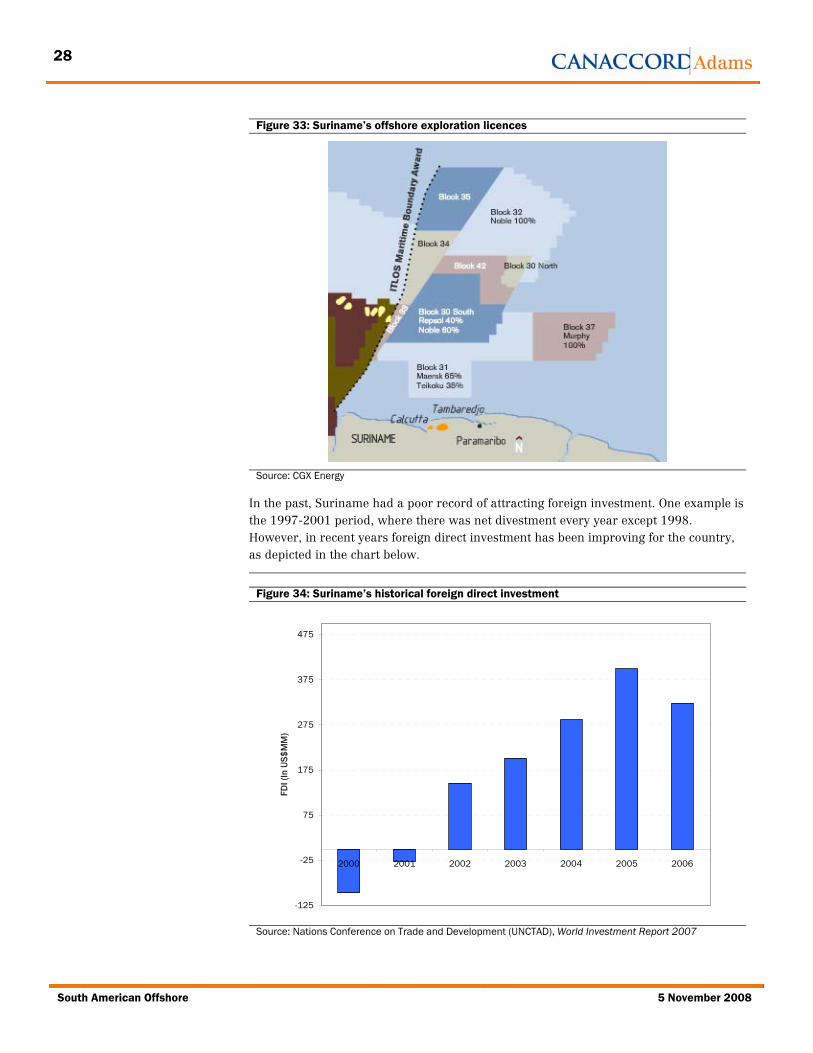

The table below summarizes oil and gas exploration areas in Suriname:

In the past, Suriname had a poor record of attracting foreign investment. One example is the 1997-2001 period, where there was net divestment every year except 1998. However, in recent years foreign direct investment has been improving for the country, as depicted in the chart below.

Figure 34: Suriname’s historical foreign direct investment

-125

-25

75

175

275

375

475

2000 2001 2002 2003 2004 2005 2006

FDI (

In U

S$M

M)

Source: Nations Conference on Trade and Development (UNCTAD), World Investment Report 2007

29

5 November 2008 The Caribbean Report

Historically, oil and gas has not played an important role in Suriname’s economy. Going forward, exploration and production activity could be a significant contributor to the country’s prosperity. This would be dependent on exploration results as onshore and offshore exploration has been limited. However, with the resolution of the border dispute with Guyana, there is more certainty to the offshore land position which could generate further offshore activity.

30

South American Offshore 5 November 2008

COMPANY FEATURE SUMMARIES

In the following section, we highlight a number of oil and gas companies that have operations in the Caribbean. We have included five public companies and one private company which are all headquartered in Canada. Within our company features we have three companies of particular interest that we have initiated research coverage on. These companies are Canadian Superior Energy, Challenger Energy, and CGX Energy.

Canadian Superior Energy Inc. (SNG : TSX : C$1.94 | SPECULATIVE BUY, C$4.50 12-month target).........................31

CGX Energy Inc. (OYL : TSX-V : C$0.49 | SPECULATIVE BUY, C$1.80 12-month target) ............................................45

COMPANY STATISTICS: Forecast Return %: 132% 52-week Range: C$1.27–5.01 Avg. Daily Vol. (000s): 147.8 Shares Out (M) basic: 157.6 Shares Out (M) fd: 179.1 Market Cap (M): C$305.8 Net Debt (2008E) (M): C$60.9 Enterprise Value (M): C$366.7 EARNINGS SUMMARY: FYE 2007A 2008E 2009E Oil & NGL (b/d): 594 750 750 Natural Gas (mmcf/d): 13.5 18.0 20.0 Total (boe/d): 2,843 3,750 4,083 EPS (fd) $(0.07) $0.19 $0.11 CFPS (fd): $0.09 $0.25 $0.29 Commodity Prices 2007A 2008E 2009E WTI (US$/b): $72.29 $104.97 $80.00 NYMEX Gas (US$/mmbtu): $6.97 $9.25 $8.75 SHARE PRICE PERFORMANCE:

COMPANY SUMMARY: Canadian Superior Energy is a Calgary-based oil and gas exploration and production company with operations in Western Canada, offshore Trinidad & Tobago, and Offshore Nova Scotia. All amounts in C$ unless otherwise noted.

Energy – Oil and Gas, Exploration and Production

PUSHING BEYOND CANADIAN BOUNDARIES Initiating research coverage We are initiating coverage on Canadian Superior Energy Inc. with a SPECULATIVE BUY recommendation and a 12-month target price of C$4.50. Our target price is based on a risked net asset valuation of the company’s development projects in Canada and Trinidad and Tobago.

Overview Canadian Superior Energy is a Calgary-based oil and gas exploration and production company with operations in western Canada, offshore Nova Scotia, offshore Trinidad and Tobago and a recently awarded block in Libya in north Africa.

The company has a sizeable presence in Trinidad and Tobago with interests in Block 5(c) and the Mayaro/Guayaguayare (M/G) project, accounting for gross undeveloped holdings of 135,041 acres. The company has a 45% working interest in Block 5(c), which has estimated reserves of 4 tcf. Block 5(c) has three separate potential hydrocarbon basins: Victory, Bounty and Endeavour. Exploration wells on the Victory and Bounty discoveries have potential initial production rates of approximately 100 and 200 mmcf/d respectfully. Additionally, the company has a 100% working interest on the M/G Block, which has estimated reserves of 10-30 million barrels of oil. Canadian Superior expects to drill two exploration wells on the licence by the end of the first quarter of 2009

32

South American Offshore 5 November 2008

RECOMMENDATION

We are initiating coverage on Canadian Superior Energy Inc. with a SPECULATIVE BUY recommendation and a 12-month target price of C$4.50. Our target price is based on a risked net asset valuation of the company’s development projects in Canada and Trinidad and Tobago.

CORPORATE PROFILE

COMPANY HISTORY Canadian Superior Energy was previously known as Kapalua Gold Mines Ltd. when it was founded in 1983. During 1993, the company changed its name to Prize Energy Inc. before finally changing its name to Canadian Superior Energy in 2000. The company has offices in Calgary, Halifax, Jersey City (NY) and Port of Spain, Trinidad, with total staff (including direct contract) of approximately 70.

The company was founded by Mr. Greg Noval, the current Chairman of Canadian Superior Energy, who also founded 88 Energy Corp., a company that he grew to a market cap worth over $500 million. Unfortunately, 88 Energy Corp. eventually ran into trouble with an unsuccessful exploration program and oil price volatility. This resulted in Mr. Noval coming to an agreement with the board of directors at 88 Energy Corp. to form a new entity called Canadian Superior. The new company was formed with the divestiture of certain assets and properties from 88 Energy Corp. to shareholders. Canadian Superior made one of its first major acquisitions on January 13, 2003, by purchasing the Drumheller, Alberta, area of the Canadian plains assets from El Paso, a multi-billion-dollar company that had become overburdened with debt.

Canadian Superior’s major holdings now include offshore properties in Trinidad and Tobago and 2.59 million gross acres located in offshore Nova Scotia. Other areas with interests include Libya and Tunisia, and Windfall and Boundary Lake in western Canada. The company also has a 50/50 LNG joint venture called Liberty Natural Gas with Excalibur Energy USA. The project proposes to bring LNG to the Greater New York City area in the United States.

BUSINESS STRATEGY Canadian Superior’s business focus is on international high-impact growth paired with production growth in western Canada, while also exploring in offshore in eastern Canada. At the same time, the company will strive to maintain financial discipline; one of Canadian Superior’s short-term goals is to be debt-free by the end of 2008. Additionally, the firm will mitigate risk where it can but will still attempt to take bold new business steps.

MANAGEMENT AND DIRECTORS The management group and board of directors consist of professionals with considerable international oil and gas industry experience.

33

5 November 2008 Caribbean Report

• Greg Noval, Chairman. Mr. Noval was recently Chairman of Challenger Energy (CHQ : TSX-V : C$2.20 | SPEC BUY, C$5.25 target) but recently resigned his position. Mr. Noval is also an owner of many private firms involved in real estate development, aviation and farming and ranching. He has over 20 years’ experience in the Canadian energy industry. Mr. Noval founded Canadian 88 Energy Corp., which converted into Esprit Energy Trust, before being acquired by Pengrowth Corporation. He holds a BComm and BA in economics from the University of Alberta and also a Bachelor of Law degree from the University of Saskatchewan.

• Craig McKenzie, Chief Executive Officer and Director. Mr. McKenzie was previously President of BG Trinidad & Tobago, one of BG’s largest and most profitable divisions. He has 21 years of international exploration and production experience in diverse segments including LNG, commercial and corporate operations and large-scale business transformations. Mr. McKenzie has also worked with BP plc and Amoco Corporation in various senior management positions. He holds an MBA from Kellogg School of Management at Northwestern University and a BS, petroleum engineering, from Louisiana State University.

• Michael Coolen, President and Chief Operational Officer. Mr. Coolen has worked for Canadian Superior since mid-2001. Prior to joining the company he was employed for over 20 years at Mobil Oil Canada and ExxonMobil. His last assignment at ExxonMobil was as senior manager for the Sable Offshore Energy project, which was the first offshore natural gas production project in offshore Nova Scotia. Mr. Coolen holds Bachelor of Science and Bachelor of Engineering degrees.

• Robb Thompson, Chief Financial Officer. Mr. Thompson was formerly the CFO and VP Finance at Berkana Energy Corp. He has over 25 years of experience, including technical, financial and operational expertise. He is a Chartered Accountant who has worked with KPMG LLP where he was an audit partner in the energy sector.

• Leif Snethun, VP, Western Canada. Mr. Snethun was a founder and President and CEO of Seeker Petroleum Ltd. He is a Professional Geologist and a member of the Association of Professional Engineers, Geologists and Geophysicists of Alberta. He holds a Bachelor of Science in geology from the University of Calgary and has 25 years of oil and gas experience within various senior geological, geotechnical and managerial positions.

The board of directors consists of Greg Noval, Craig McKenzie, Michael Coolen, Alex Squires (Managing Director of Brant Securities Ltd.), Charles Dallas, T.J. (Jake) Harp, Kaare (Kory) Idland and Richard (Rick) Watkins.

CAPITALIZATION Canadian Superior’s capital structure is designed to support a growth-oriented model. The most recent equity issue closed on September 4, 2008, and raised total gross proceeds of US$35 million at a price of $4.00 per share through the issue of approximately 8.8 million shares. The firm also completed a financing on November 16, 2007, raising gross proceeds of $22.7 million at a price of $3.50 per share through the issue of 6.5 million shares. The company currently has 157.7 million common shares outstanding and approximately 21.4 million dilutive securities. The 21.4 million in dilutive securities consist of 17.1 million options with an exercise price of $2.39 per

34

South American Offshore 5 November 2008

share and 4.4 million warrants with an exercise price of $4.00 per share. Additionally, the company has drawn $40.8 million against a revolving credit facility of $45 million.

Institutional investors own approximately 36% of the issued and outstanding shares of Canadian Superior. According to Thomson Financial, the major institutional shareholders of Canadian Superior include: Steelhead Partners, LLC (16.2 million shares), Palo Alto Investors, LLC (16.1 million shares), Blackrock Financial Management Inc. (9.4 million shares) and West Coast Asset Management Inc. (8.4 million shares).

Canadian Superior’s directors and management team own approximately 1.2% of the issued and outstanding shares of the company.

35

5 November 2008 Caribbean Report

OPERATIONS

BLOCK 5(C) – OFFSHORE TRINIDAD This block is located approximately 86 kilometres off the east coast of Trinidad, where the water depths range from approximately 500 to 1,500 feet. All wells drilled on this block to date have been drilled with a semi-submersible drilling rig. The company is paying 26.3% of the block’s exploration costs as a result of farming out to other parties to maintain a 45% working interest.

Figure 36: Joint venture partner working interest on Block 5(c)

Exploration Program Production Sharing Capital Commitment Contract Interest Canadian Superior 27% 45% British Gas 40% 30% Challenger 33% 25% 100% 100%

Source: Company reports

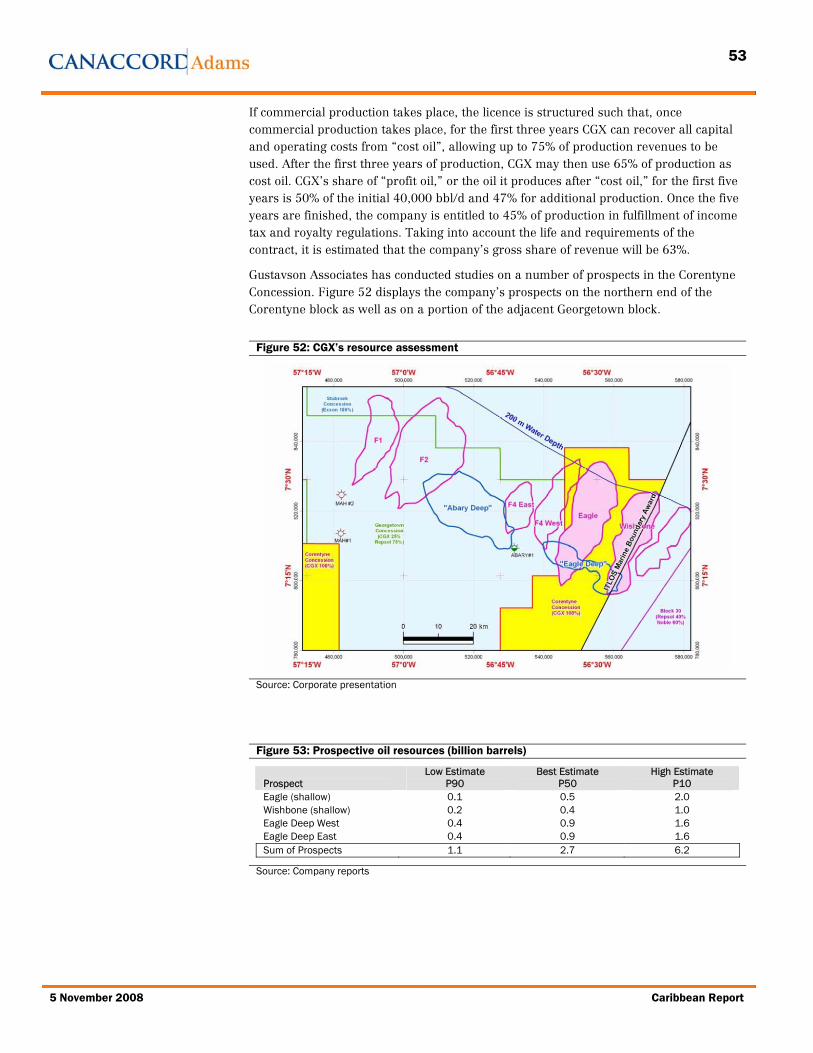

Over the last several years the company determined three large separate potential hydrocarbon structures on the block: named the Victory, Bounty, and Endeavour prospects. Canadian Superior drilled the Victory and Bounty prospects this year, and both were very successful. The third prospect, Endeavour, is currently being drilled with total depth expected to be reached in November 2008. The block is adjacent to several large gas fields including British Gas’ Dolphin and Dolphin Deep natural gas fields (see Figure 37).

Figure 37: Canadian Superior’s Block 5(c) operations

Source: Company reports

36

South American Offshore 5 November 2008

In early 2008, the company drilled the first well on the block at the Victory prospect. The well tested natural gas in two formations with the first zone being condensate rich. The first zone tested natural gas at pressure rates averaging between 40 mmcf/d and 45 mmcf/d and the second tested at rates averaging 30 mmcf/d. The two zones combined could produce gas at rates of approximately 100 mmcf/d. Reserves for the prospect are estimated to be between 0.6 and 1 tcf. The company believes that the Victory discovery well has an expected initial sales rate of 195 mmcf/d plus 6,000 bbl/d of condensate.

In July 2008, the company completed drilling the Bounty prospect to a total depth of 17,360 feet, which is located 2.2 miles from the Victory well. The well encountered gas-bearing zones with the main targeted zone encountering approximately 200 feet of pay. The well’s flow test indicated productive capability in excess of 200 mmcf/d of natural gas from this main targeted zone. Canadian Superior believes it has up to 2.6 Tcf of natural gas from this tested structure.

The company is now in the process of drilling the third prospect on Block 5(c). The Endeavour prospect is an independent prospect to the formerly drilled two prospects. It is expected that drilling will be completed in November 2008, with testing results due in the early first quarter of 2009. Despite the discoveries at Bounty and Victory, the chance of success on Endeavour is rated to be only 30%.

Regardless of the current and future success of these three prospects, the company still has the problem of bringing the Block 5(c) gas onstream. Canadian Superior and its partners are considering two options. The first one is to build a pipeline from Block 5(c) to the mainland. From there a fifth LNG train must be constructed to accommodate the new gas as the other four existing trains are already at capacity. A fifth train in the area has been proposed. However, the Trinidad government has yet to make a decision until a “new substantial gas discovery” can be made to justify the construction. Canadian Superior’s management believes a discovery over 4.5 tcf of natural gas should be sufficient to justify the construction of a fifth train. The second option is to liquefy the gas offshore and then transport the LNG to a sales point. Management has stated that both options have roughly the same economics and the decision depends on agreement from other stakeholders and joint venture partners, as well as the success of Endeavour well.

M/G BLOCK The company is a joint venture partner (100% working interest) with the Petroleum Company of Trinidad and Tobago (Petrotrin) in the near-shore Mayaro/Guayaguayare (M/G) Block. The block is off the east coast of Trinidad and consists of 58,080 gross acres. Reserves are estimated to be approximately 10-30 million barrels. Additionally, the block is in close proximity to several large onshore and offshore oil and natural gas discoveries. It is located 1.5 miles from the Navette field, which has produced over 60 million barrels of oil. Also nearby is its neighbour, the Angostura field, which has estimated reserves of approximately 1.75 tcf of natural gas and 450 million barrels of oil.

The company is currently in the process of receiving permits for the drilling of two locations on the block. Canadian Superior plans to drill both in the first quarter of 2009 pending approval from the government. The wells are expected to cost approximately $12-14 million assuming a 100% interest to the company. If the exploration wells are successful the company will follow up with additional 3D seismic in the area to determine a full field development plan.

37

5 November 2008 Caribbean Report

Figure 38: Canadian Superior’s M/G operations

Note: Corporate website

OTHER OPERATIONS

Libya and Tunisia The company recently announced its entry into North Africa, which it calls its Oasis project. On August 27, 2008, the company signed the formal Exploration and Production Sharing Agreement for the offshore Libya/Tunisia block called the 7th of November Block. The block comprises approximately 1,200 square miles (750,000 acres) of exploration property located 75 miles offshore North Africa in the Mediterranean Gulf of Gabes. Water depths in this area range from 250 to 375 feet. Nearly equal portions of the block fall in Tunisian and Libyan waters.

In close proximity to the7th of November Block is the El Bouri (Libya) and Ashtart (Tunisia) oil fields, which are estimated to have produced over 750 million barrels of oil and 250 million barrels of oil, respectively. Canadian Superior’s management team believes that its newly acquired block lies on productive trends established by these two fields. The company will be the operator of the block but has not yet disclosed its working interest.

38

South American Offshore 5 November 2008

Figure 39: 7th of November Block located on the border of Tunisia and Libya

Source: Company Reports, Canaccord Adams

Western Canada The company’s production currently resides in its western Canadian properties. Essentially, the Canadian assets are used to finance the larger and riskier projects for the company. Management has stated that, owing to future capital requirements for the development drilling of the Trinidad Block 5(c) prospects, these assets may be put up for sale as soon as this winter.

Figure 40: Western Canadian assets

Source: Company Reports, Canaccord Adams.

39

5 November 2008 Caribbean Report

Offshore eastern Canada Canadian Superior Energy is the largest offshore exploration acreage holder in offshore Nova Scotia, with approximately 1.2 million net acres residing in five exploration licences. The company holds a 100% interest in these five licences. The first exploration well (I-85) in the area was drilled in March 2004 on the Mariner prospect. The well encountered non-commercial quantities of natural gas pay. However, the well provided insight into the geology of the prospect. The company has a preliminary plan to drill a second offset exploration well at Mariner in March 2009. The company has identified possible potential unrisked reserves of as much as 2.5 trillion cubic feet.

Ideally, Canadian Superior would like to decrease the risk and cost of this well by bringing in some private investors for 50% of the interest. The company has not finalized any farm-out arrangements as of yet, but recently signed an agreement whereby the Tunisian/Libyan Joint Exploration, Production, and Petroleum Services Company (Joint Oil) was awarded an overriding royalty interest and optional participating interest to Joint Oil, in Canadian Superior’s Mariner Block.

Figure 41: Canadian Superior offshore eastern Canada blocks

Source: Company reports

Liberty Natural Gas Canadian Superior is also in a 50/50 LNG joint venture project with Excalibur Energy USA Inc. called Liberty Natural Gas. The proposed project will provide LNG to the largest and highest price yielding area in the United States – the greater New York City area. The project is unique in that it provides LNG to the city without being an eye sore to the residents and is safe from terrorist threats since it is submerged below the ocean surface. Canadian Superior’s management team believes it has the government onside for the project and feels comfortable that it can finance the project, since many institutional investors have approached the company already. If completed, the project would have a payback period of approximately one year and would generate about $600-700 million in cash flow each year.

40

South American Offshore 5 November 2008

VALUATION

We value Canadian Superior using a sum-of-the-parts valuation methodology. Within our valuation we have taken into account the company’s Canadian asset value as well as an estimated value of the company’s Block 5(c) assets. We have assumed no value from the company’s exploration prospects on the M/G Block, in the frontier offshore blocks held in eastern Canada, and in the offshore block on the border of Libya and Tunisia. We also note that, due to the uncertainty around final approval of the Liberty Gas project, we have not included any value for this asset. This results in what we view as a very conservative value for the company which is appropriate in today’s current capital markets.

Currently all of Canadian Superior’s production resides in Canada. As mentioned, this asset provides the company with cash flow to fund a portion its operations in Trinidad. The reserves for the Canadian assets have been determined by independent third-party engineering at December 31, 2007, for proven plus probable reserves along with the associated values. We note that these reserves estimates themselves are likely conservative given the different commodity prices as well as any reserve additions or adjustments that may be made as a result of the company’s 2008 drilling program. Including estimated company debt, the net asset value of the company’s Canadian assets is outlined in the figure below.

Figure 42: Canadian net asset value

NPV 10% Before Tax ($mm) Proven Reserves 103.8 Probable Reserves 44.5 Total Proved plus Probable 148.4 Estimated net debt (4.7) Total Value 143.7 NAV: $/ basic share 0.91 NAV: $/FD share 1.13

Source: Canaccord Adams, company reports

Additionally, Canadian Superior has a 45% interest in Block 5(c) offshore Trinidad, which has two confirmed discoveries on the block and a highly prospective third discovery currently drilling. As such, we present a potential value grid by which we have run various development scenarios related to reserve size, production and gas price. Our economics assume generic LNG costs for the offshore development and assume a cost-recovery/tariff model for the new pipeline from the block to Trinidad as well as for the construction and operation of a fifth LNG processing train.

Our assumptions for the economic analysis are reflected in the figure below. We have assumed gross capital expenditures to develop the three Block 5(c) prospects to be US$1.2 billion. Included in this capital are development drilling capital and a production platform. We have also assumed two different sets of operating costs that are dependent on the final destination of the LNG. We have assumed operating costs of US$3.25/mcf if the LNG is transported to North America and US$4.25/mcf if the LNG is transported to an international destination.

41

5 November 2008 Caribbean Report

Figure 43: Assumptions for discounted cash flow evaluation of Block 5(c)

Gross Capital Expenditures (US$M) 1,160 Operating Costs - North America Freight ($US/mcf) 3.25 Operating Costs - International Freight ($US/mcf) 4.25 Commencement of Production July 2014

* Includes all three exploration prospects on Block 5(c) to the combined total gross recoverable reserves ** The values in the areas of grey shading assumes gas delivery to North America only Source: Canaccord Adams

Figure 45: Valuation Grid for Block 5(c) – per share (in Canadian dollars)

NPV After-Tax @ 10% per Basic Share Outstanding (C$) Long-term Natural Gas Price (US$/mmbtu) Gross Recoverable

* Includes all three exploration prospects on Block 5(c) to the combined total gross recoverable reserves ** The values in the areas of grey shading assumes gas delivery to North America only Source: Canaccord Adams

Clearly, the valuation of Block 5(c) is a function of resources discovered and sales price. Even with double-digit natural gas prices available in North America, the smallest recoverable reserve size is only marginally economic based on the capital expenditures required to develop the resource. Given the world’s demand for energy and current LNG markets, it is our view that the successful development of the discoveries made on Block 5(c) will be sold to LNG buyers around the world. This would argue for a value based on natural gas prices of better than US$10.00/mmbtu.

The next component of the valuation relates to the total size of the discoveries on the block. To date, the first discovery at Victory is estimated to be 0.6-1.1 Tcf in size. The second discovery at Bounty is estimated to have a potential size of up to 2.6 Tcf of natural gas. Therefore, the resource potential identified so far could be as high as 3.7 Tcf of natural gas.

42

South American Offshore 5 November 2008

Given the history of production and resource size from the area, we have a degree of comfort in the potential resources discovered to date and are not risking the size of the prize, but have instead risked the development costs and assumptions,

Combining the value of the Canadian assets with the value attributable to Trinidad, we have set a 12-month target price of C$4.50. For the Trinidad assets, we assume a contribution of C$3.65 per share. We base this on the assumption that the recoverable resources will prove to be at the low end of the range shown above and ultimately sold for a gas price in the range of $10.00-15.00/mmbtu. However, we note that the upside value from this level in terms of reserves and price likely makes this target price conservative.

43

5 November 2008 Caribbean Report

Figure 46: Summary of estimates

CANADIAN SUPERIOR ENERGY INC. SNGRecommendation SPEC BUY Current price C$1.9412-month target price C$4.50 Total projected return* 132%November 3, 2008 * includes dividends payable

Share Information Current Market Multiples 2006A 2007A 2008E 2009E 2010EMarket cap ($M) $305.8 Discretionary cash flow multiple 13.1x 21.4x 7.8x 6.8x 7.2xShares O/S – basic (M) 157.6 Debt-adjusted multiple 12.1x 15.9x 8.8x 10.1x 12.5xShares O/S – float (M) 94.0 Earnings multiple NA NA 10.3x 17.1x 18.1xShares O/S – f.d. (M) 179.1 Target multiple 26.8x 45.6x 15.4x 15.7x 16.6x52-week range C$1.27 C$5.01 Debt-adjusted target multiple 27.1x 36.7x 18.4x 18.5x 20.9x Avg Daily Trading Volume (year) 147,777Valuation Current Net Income 2006A 2007A 2008E 2009E 2010ENet asset value (CCI estimate) $4.56 Net income ($M) NA ($9.9) $29.4 $17.9 $16.9Price/NAV 43% EPS (basic) ($0.09) ($0.07) $0.19 $0.11 $0.11Enterprise value ($M) $366.7 EPS (f.d.) ($0.10) ($0.07) $0.19 $0.11 $0.11EV/proven reserves ($/boe) $70.11

1.2% 1.5% 0.6% 0.5% 0.6%Reserves - 6:1 (at December 31, 2007) +/- C$0.10/mcf Gas $0.00 $0.00 $0.00 $0.00 $0.00Equivalent reserves (mmboe) Oil Gas Total 2.0% 3.2% 1.3% 1.2% 1.5%Proven 1.0 4.2 5.2Proven + probable 1.9 6.5 8.5 Management Team % Proven producing 96% 77% 80% Craig McKenzie, CEO British Gas % Proven 52% 65% 62% Michael Coolen, President and COO Mobil Oil, ExxonMobil % Crude oil & liquids 19% Robb Thompson, CFO Berkana Energy, KPMG Reserve life – proven (yrs) 4.3 4.5 4.5

1 Year 3 Year Reservoir Engineer BankerProven F&D costs ($/boe) 0.00 6.17 GLJ Associates Ltd. Canadian Western BankP+P F&D costs ($/boe) 0.00 4.76 Auditor Bank Lines - Q2/08 2008E 2009E 2010EProven reserve replacement ratio 1.0x 1.1x Meyers Norris Penny LLP $45 135% 335% 540%

Analyst: J. Frederick Kozak, P.Eng. (403) 508-3836Associate: Timothy Clark (403) 508-3824

Source: Canaccord Adams

44

South American Offshore 5 November 2008

Investment risks Risks to our investment thesis include:

• An investment in the company’s securities would be speculative due to the nature of the company’s involvement in the exploration, development and production of oil and natural gas and its present stage of development.

• Capital requirements and liquidity risks associated with the development and production of natural gas from the company’s Block 5(c) property as well as future projects.

• Commodity price swings in crude oil and natural gas could impact Canadian Superior’s profitability.

• Adverse changes to government regulations and fiscal terms. Any adverse changes could impact Canadian Superior’s execution and profitability.

• A left-leaning government that is less business friendly could affect the profitability of the company’s operations.

COMPANY STATISTICS: Forecast Return %: 267% 52-week Range: C$0.42–4.60 Avg. Daily Vol. (000s): 203.4 Shares Out (M) basic: 125.6 Shares Out (M) fd: 135.2 Market Cap (M): C$60.9 Net Debt (2008E) (M): C$(23.3) Enterprise Value (M): C$37.6 EARNINGS SUMMARY: FYE 2007A 2008E 2009E Oil & NGL (b/d): NA NA NA Natural Gas (mmcf/d): NA NA NA Total (boe/d): NA NA NA EPS (fd) ($0.04) ($0.14) ($0.02) CFPS (fd): ($0.02) ($0.02) ($0.03) Commodity Prices 2007A 2008E 2009E WTI (US$/b): $72.29 $104.97 $80.00 NYMEX Gas (US$/mmbtu): $6.97 $9.25 $8.75 SHARE PRICE PERFORMANCE:

COMPANY SUMMARY: CGX Energy is a Canadian-based oil and gas company focused on offshore and onshore oil exploration in the Guyana-Suriname basin. All amounts in $US unless otherwise noted.

Energy – Oil and Gas, Exploration and Development

SWINGING FOR THE FENCES Initiating research coverage Our 12-month target price of C$1.80 is based on the assumption that the company is able to develop successfully a 50 million barrel offshore discovery from offshore Guyana with internal expertise and capital resources. We note that independent third party evaluation of the best prospects on the company's landholdings put the resource potential at 1.1 billion barrels on a low estimate basis, implying that this prospect has an approximate 5 percent chance of success. We rate CGX Energy SPECULATIVE BUY.