South Asia South Asia – – Regional Cooperation Regional Cooperation on Trade Facilitation: Overview of on Trade Facilitation: Overview of Existing Initiatives Existing Initiatives Prabir Prabir De De RIS RIS Asia Asia – – Pacific Trade Facilitation Forum 2011 Pacific Trade Facilitation Forum 2011 4 4 – – 5 October 2011 5 October 2011 Seoul Seoul

Transcript

South Asia South Asia –– Regional Cooperation Regional Cooperation

on Trade Facilitation: Overview of on Trade Facilitation: Overview of

Existing InitiativesExisting Initiatives

PrabirPrabir DeDe

RISRIS

Asia Asia –– Pacific Trade Facilitation Forum 2011Pacific Trade Facilitation Forum 2011

4 4 –– 5 October 20115 October 2011

SeoulSeoul

South Asia Has High Trade South Asia Has High Trade

Potential, But Largely UnrealizedPotential, But Largely Unrealized�� Regional trade in South Asia is moving below potentialRegional trade in South Asia is moving below potential

�� IntraIntra--regional trade in 2010: US$ 15 billion (approx.)regional trade in 2010: US$ 15 billion (approx.)

�� About 65% of intraAbout 65% of intra--regional trade potential is remained regional trade potential is remained unrealizedunrealized

�� Causes of high underutilization of intraCauses of high underutilization of intra--regional trade are regional trade are mostly economic in nature mostly economic in nature �� High trade barriers High trade barriers –– both visible and invisibleboth visible and invisible

�� Poor transportation links and lack of transitPoor transportation links and lack of transit

�� Lack of supply capabilities of Lack of supply capabilities of LDCsLDCs, among others., among others.

�� Region suffers from high trade costsRegion suffers from high trade costs (e.g. transport (e.g. transport costs outweigh tariffs)costs outweigh tariffs)

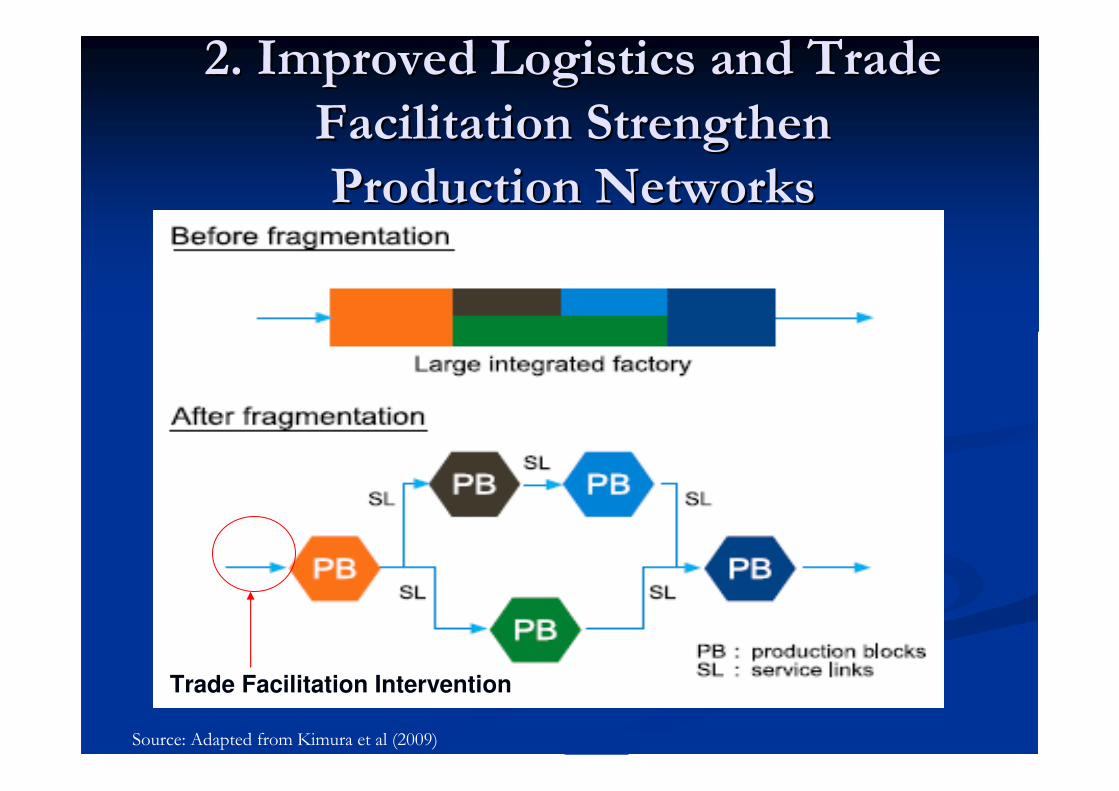

Trade Facilitation Measures in Trade Facilitation Measures in

Forefront of Regional AgreementsForefront of Regional Agreements

NoNoNoYesNoBIMSTEC

YesYesNoYesYesSAARC

NoNoNoYesNoINDIA-THAI

YesYesYesYesYesEU

YesYesYesYesYesNAFTA

YesYesNoYesYesASEAN

NoNoNoNoNoINDIA-LANKA

NoNoNoNoNo

INDIA-

AFGHAN

NoYesNoYesNoCHINA-PAK

NoNoNoYesNoASEAN-INDIA

NoNoNoNoNoAPTA

Cooperation in

Trade

Facilitation

E-Commerce

/Paperless

Trade

Trade

Regulations

Publication

Customs

Valuation

Customs

ProceduresAgreement

Source: APTIAD, UNESCAP

Regional Trade and Regional Trade and

Transport Facilitation: Transport Facilitation:

Progress so FarProgress so Far

Some Encouraging Developments in Some Encouraging Developments in

Physical ConnectivityPhysical Connectivity� Negotiation of Regional Transport and Transit Agreement, and a Regional Motor Vehicle’s

Agreement (ongoing).� SAARC Expert Group finalized the text of the Regional Agreement on Railways in August 2011.

� Launch of feasibility studies of pilot projects:� Birganj and Kathmandu (160 km) completed in October 2008 – negotiation ongoing

� Kathmandu-Birgunj-Kolkata/Haldia – rail corridor� Birgunj-Katihar-Singhabad-Rohanpur-Chittagong with links to Jogbani, Biratnagar and Agartala –

rail corridor

� Agartala-Akhaura-Chittagong – rail corridor

� Construction between Agartala and Akhaura (14 km) is about to commence.

� Phuntsholing and Hashimara – road corridor

� Ferry link - between Colombo and Tuticorin (started already) and Colombo and Cochin

� Air link - Malé-New Delhi and Islamabad-New Delhi;

� Establishment of modern border crossing facility at Phuntsholing.

� On-going projects: � Feasibility study for India - Bhutan rail link

� Construction of railway line from Jiribam-Tupui (near to Imphal, India) has commenced

� Construction of Kaladan Multimodal Transport project has started in December 2010

� Railway infrastructure improvement projects in Sri Lanka� Intermodal connectivity – Air Services Agreement (single ticket to fly between South Asian

nations)

� Demonstration run of container train involving Bangladesh, India and Nepal

Progress in Modernizing and Progress in Modernizing and

Opening of Land Customs Stations Opening of Land Customs Stations

� India’s Integrated Check Post (ICPs)

project

� Opening of Banglabandha – Fulbari land

port for trade

� Opening of border haat in Baliamari

(Bangladesh) – Kalaichar (India)

� Few more border haats (e.g. between India

and Bangladesh) coming up

Progress in Customs CooperationProgress in Customs Cooperation� SAARC Agreement on Mutual Administrative Assistance in

Customs Matter, signed in 2005� The Seventh Meeting of the Sub-Group on Customs Cooperation

(11-12 February 2010) made following recommendations with a view to facilitating trade in goods in SAARC. � Building infrastructure including roads and railways networks near the LCSs.� Customs clearance procedures at LCSs need to be smoothened;� Customs Administrations may consider a system of customs facilitation in

which export documentation of one Member State could be considered by the Customs Administration in the importing country for the purposes of assessing and clearing the consignment.

� Need for developing an Electronic Data Exchange System within the region, including at LCSs, with a view to ensure better facilitation of trade in goods among the SAARC countries including improved compliance.

� SAARC Secretariat to develop a regional/sub-regional project to set up automated customs clearing mechanism at the designated LCSs.

� Harmonisation of 8-digit tariff lines is needed, and in order to make this task easier, all Member States would further provide upto only 100 8-digit tariff lines with a trade potential of 75% (in value terms) in the region.

Regional Transit Regional Transit –– Benefits to Smaller Benefits to Smaller

CountriesCountries� Bangladesh can earn hefty

revenue (over US$ 1 billion per annum) as transit fees from Indian vehicles plying to and from India’s North Eastern Region (NER) to rest of India using Bangladeshi soil.

� Similarly, transit arrangement between India, Pakistan and Afghanistan will fetch a hefty royalty to Pakistan for movement of vehicles between India and Afghanistan using Pakistani soil.

� There are also huge gains associated with energy conservation due to transit and efficient use of resources.

US$ 110 - 180

MILLION

AGATALA (INDIA)/ AKHAURA

(BANGLADESH),

BENAPOLE /

PETRAPOLE

INDIA &

BANGLADESH

AGARTALA –AKHAURA –

DHAKA –

KOLKATA (478

KMS)

US$ 660 - 1060

MILLION

DAWKI (INDIA)

/TAMABIL

(BANGLADESH),

BENAPOLE

(BANGLADESH) /

PETRAPOLE (INDIA)

INDIA &

BANGLADESH

SHILLONG –

SYLHET –

DHAKA –

KOLKATA (721

KMS)

REVENUE OF

BANGLADESH FROM

TRANSIT (US$)*

BORDER CROSSINGSCOUNTRIESCORRIDOR

Note:* Average during the period 2007 to 2010. Several assumptions applied.

Source: Author

Estimated Transit Revenue of Bangladesh for

India – Bangladesh Trade

Encouraging Progress in TransitEncouraging Progress in Transit

� All SAARC countries have in-principally agreed to regional regional transittransit.

� Motor Vehicle Agreement is being negotiated.

� SAARC Expert Group finalized the text of the Regional Agreement on Railways in August 2011.

� Sub-regional transit has been agreed between India, Nepal, Bhutan and Bangladesh.

� Bilateral document between India and Bangladesh signed during the state visit of Indian PM to Bangladesh in September 2011 to facilitate overland transit traffic between Bangladesh and India

� Demonstration run of container train between Bangladesh, India and Nepal is getting ready.

� Huge trade opportunities if Afghanistan – Pakistan Transit Agreement covers Western South Asia subregion.

Three Important Developments on Three Important Developments on

Regional Connectivity Regional Connectivity

(Strong Impact on Trade Flow)(Strong Impact on Trade Flow)

1. Transit for traffic between India, Bangladesh,

Nepal, and Bhutan.

2. Integrated check post (ICP) in Moreh in

Manipur and Petrapole in West Bengal (India)

3. India – ASEAN connectivity projects

Deepening South Deepening South

Asian Integration Asian Integration

The Renewed VisionThe Renewed Vision

1. With SAFTA, South Asia has entered into the second era of regional integration

2. Vision is to achieve Common (Single) Marketthrough Customs Union and then Economic Union

Milestones to CrossMilestones to Cross

Harmonized &

integrated road

and railway

network

Maritime &

waterways

network

Aviation

policy

One

‘Customs’

Transit Competition

Policy

EU (10)✓ ✓ ✓ ✓ ✓ ✓

ASEAN � ✓ ✓ ✓ ✓ �

NAFTA �*✓ ✓ ✓

✓*✓

SAARC � � � � � �

SAARC Integration Next Stages:

Customs Union (2015) => Economic Union (2020)

* Except US and Mexico

The ChallengesThe Challenges

Source: World Bank

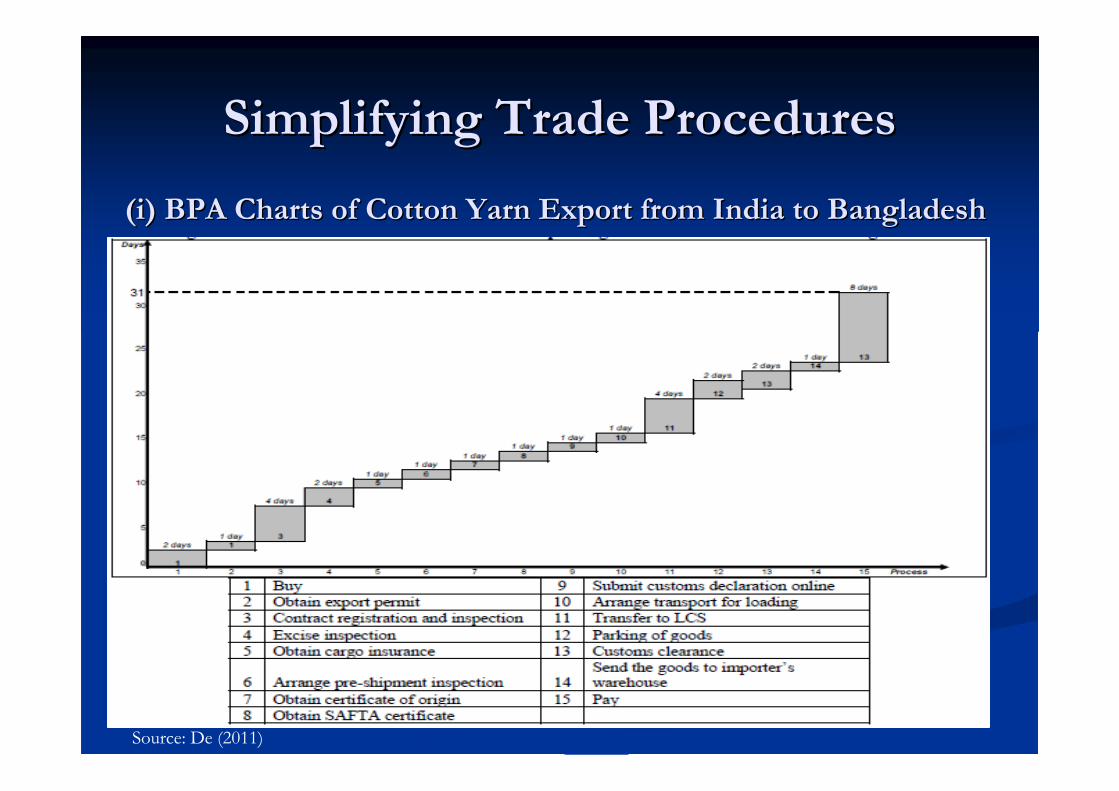

Making Trade Friendly Land BordersMaking Trade Friendly Land Borders

Unplanned and informal market

Long queue of trucks

3.6

0

hrs

5.0

0

hrs

78

.40

h

rs10

.00

h

rs

Loading at

Kolkata

Kolkata to

Petrapole

Time at

Petrapole

Unloading at Benapole

5.1

0

hrsCrossing border

returning from

Benapole

International

border

Total Time = 102.10 hrs.

(≈≈≈≈ 4 days)

Kolkata

Ban

gla

desh

Ind

ia

Case of India (Petrapole) and Bangladesh (Benapole)

3.6

0

hrs

5.0

0

hrs

78

.40

h

rs10

.00

h

rs

Loading at

Kolkata

Kolkata to

Petrapole

Time at

Petrapole

Unloading at Benapole

5.1

0

hrsCrossing border

returning from

Benapole

International

border

Total Time = 102.10 hrs.

(≈≈≈≈ 4 days)

Kolkata

Ban

gla

desh

Ind

ia3.6

0

hrs

5.0

0

hrs

78

.40

h

rs10

.00

h

rs

Loading at

Kolkata

Kolkata to

Petrapole

Time at

Petrapole

Unloading at Benapole

5.1

0

hrsCrossing border

returning from

Benapole

International

border

Total Time = 102.10 hrs.

(≈≈≈≈ 4 days)

Kolkata

Ban

gla

desh

Ind

ia3.6

0

hrs

5.0

0

hrs

78

.40

h

rs10

.00

h

rs

Loading at

Kolkata

Kolkata to

Petrapole

Time at

Petrapole

Unloading at Benapole

5.1

0

hrsCrossing border

returning from

Benapole

International

border

Total Time = 102.10 hrs.

(≈≈≈≈ 4 days)

Kolkata

Ban

gla

desh

Ind

ia3.6

0

hrs

5.0

0

hrs

78

.40

h

rs10

.00

h

rs

Loading at

Kolkata

Kolkata to

Petrapole

Time at

Petrapole

Unloading at Benapole

5.1

0

hrsCrossing border

returning from

Benapole

International

border

Total Time = 102.10 hrs.

(≈ 4 days)

Kolkata

Ban

gla

desh

Ind

ia3.60

hrs

5.00

hrs

78.40

hrs

10.00

hrs

Loading at

Kolkata

Kolkata to

Petrapole

Time at

Petrapole

Unloading at

Benapole

5.10 hrsCrossing border

returning from

Benapole

International

border

Total Time = 102.10 hrs. (Total Time = 102.10 hrs. (≈≈≈≈≈≈≈≈

Sri LankaPakistanNepalMaldivesIndiaBhutanBangladeshAfghanistanConvention

Some Specific RecommendationsSome Specific Recommendations1.1. Accept Accept subregionalsubregional and subsequently regional and subsequently regional transittransit

2. Fast track lane and priority of goods in transit to cross the border

3. Set-up SAARC Single Window (Customs) (pilot run of authorized economic operator, AEO; and mutual recognition agreement)

4. Simplification and harmonization of trade procedures, more particularly at border.

5.5. Strengthen Strengthen crosscross--border infrastructureborder infrastructure (move from road corridors to (move from road corridors to economic corridors)economic corridors)

6.6. Introduce Introduce modern corridor management techniquesmodern corridor management techniques in selected in selected corridorscorridors

7.7. Promote Promote multimodal transportationmultimodal transportation (with rail transit, regular (with rail transit, regular container train in the region)container train in the region)

8.8. Improve the Improve the efficiency of border corridorsefficiency of border corridors (both side of border (both side of border improvement in ICP project in parallel)improvement in ICP project in parallel)

9.9. Effective Effective project coordinationproject coordination among government stakeholdersamong government stakeholders

10. Stronger institution (publicinstitution (public--private interface)private interface) for trade facilitation is for trade facilitation is urgently needed. urgently needed.