1 800.851.7789 www.SIIA.org Employee Benefit Captives – The Basics Tuesday, October 2, 2012, 10:15-11:30 am Speakers • Brady Young, Strategic Risk Solutions • Greg Arms, Mercer Marsh Benefits • Andrew Cavenagh, Pareto Captive Services

Transcript

1

800.851.7789www.SIIA.org

Employee Benefit Captives – The BasicsTuesday, October 2, 2012, 10:15-11:30 am

Speakers

• Brady Young, Strategic Risk Solutions

• Greg Arms, Mercer Marsh Benefits

• Andrew Cavenagh, Pareto Captive Services

2

Agenda

• Major Types of Benefit Captives– “Fortune 500” Benefit Captives– Multi-National Benefit Captives– Group Captives for Small to

Medium Sized Employers• Questions & Answers

Regulatory Matrix• States regulate:

– Fully-insured programs (e.g. Blue Cross)– Stop loss policies – MEWAs

• ERISA regulates:– Self-funded programs

• Domicile regulates:– Captives– RRGs

3

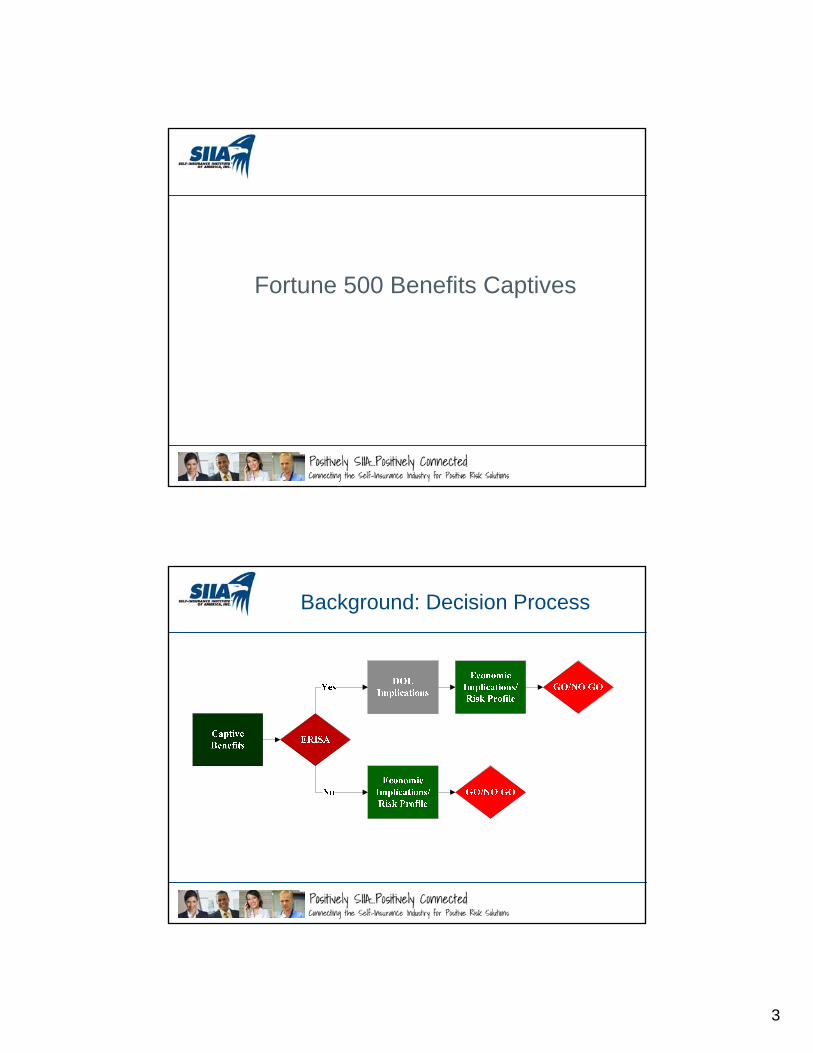

Fortune 500 Benefits Captives

Background: Decision Process

4

Background: Two Approaches

Background: ERISA vs. Non-ERISA

ERISA Non-ERISA

Life Medical Stop‐Loss

AD&D Deferred Compensation

Long-Term Disability Top-Hat Compensation

Short-Term Disability Company Owned Life

Health-Drugs/Other Personal Accident

Dental

Vision

5

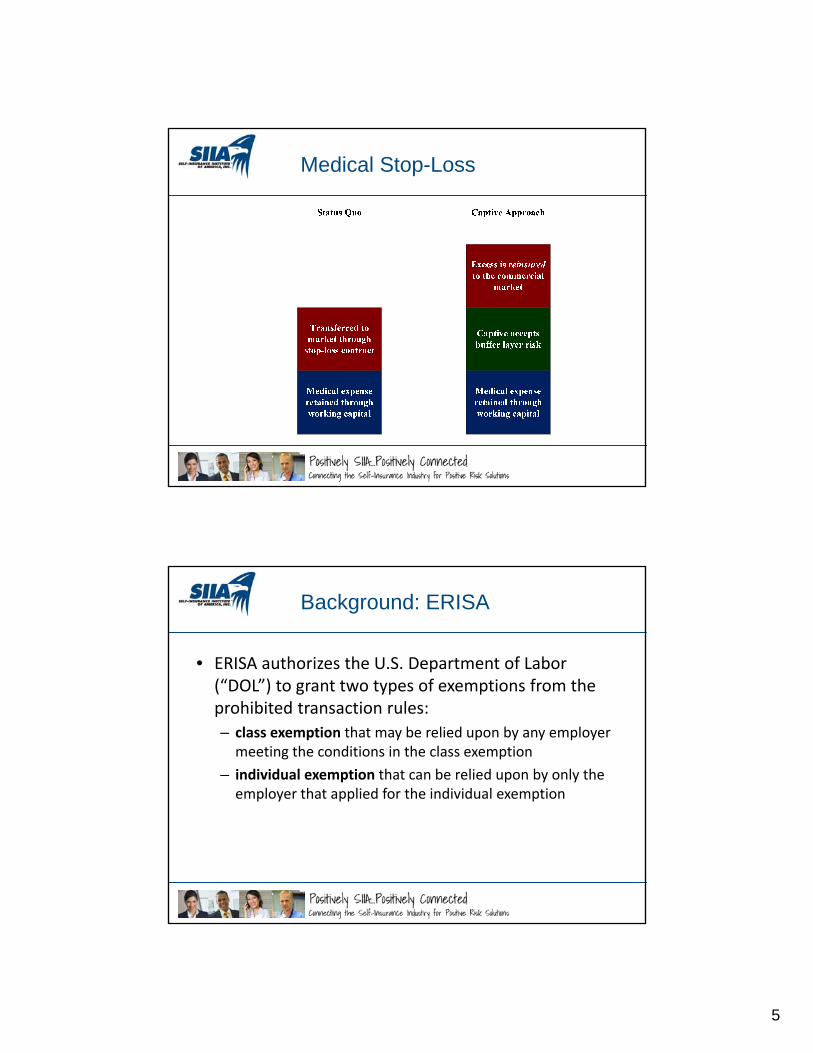

Medical Stop-Loss

Background: ERISA

• ERISA authorizes the U.S. Department of Labor (“DOL”) to grant two types of exemptions from the prohibited transaction rules: – class exemption that may be relied upon by any employer meeting the conditions in the class exemption

– individual exemption that can be relied upon by only the employer that applied for the individual exemption

6

Background: Regulatory History

• The DOL had granted a class exemption allowing an employer to use its captive to insure or reinsure employee benefits plans if the captive derives no more than 50% of its annual premiums from related business

• The Columbia Energy ruling PTE 2000‐48 was a landmark individual exemption ruling that allowed an employer to use a captive for employee benefits with less than 50% unrelated risk

Background: Regulatory History

• Archer Daniels Midland (“ADM”) PTE 2003‐07 followed the Columbia Energy path to gain an individual exemption allowing for life insurance benefits in a Vermont Captive

• The significance of the ADM ruling was the triggering of “EXPRO” or expedited processing of the request leading to approval in 75‐90 days

• All subsequent approvals have followed the EXPRO

7

Background: EXPRO Timetable

Submit application to Department of Labor on

EXPRO format basis

Department of Labor acknowledges receipt of

application

Period of "Tentative Authorization" -45 days to

elapse

After "Tentative Authorization" period expires, Notice of

Distribution can commence is sent by first class mail is

deemed to be completed 3 days after started

25 day Comment Period after completion of Notice of

Distribution

Final Authorization - expiration of 5 day waiting period after lapsing of Comment Period

Captive can commence underwriting ERISA governed

reinsurance coverageTotal time = 75-90 days

Background: EXPRO Approvals

Parent Approval Date Coverage Line

Columbia Energy 10/2000 LTD

ADM 5/2003 Life Insurance

International Paper 11/2003 Life Insurance

SCA 7/2004 LTD, Life, A&D

Alcon Laboratories 8/2004 LTD, Life

Alcoa 1/2005 Life Insurance

Sun Microsytems 10/2005 Life Insurance

Astra Zeneca 1/2006 LTD, AD&D

AGL Resources 5/2006 LTD, AD&D

H. J. Heinz 9/2006 and 5/2008 Life, LTD, AD&D

Wells Fargo 1/2007 LTD, Life Insurance

8

Background: EXPRO Approvals

Parent Approval Date Coverage Line

NiSource 3/2007 Life Insurance

Cephalon 5/2008 LTD, Life, AD&D

YKK 6/2008 Basic Life and LTD

United Technologies 12/2008 LTD

Deutsche Post/DHL 12/2008 LTD

ConAgra 10/2008 Life, AD&D

Sloan-Kettering 3/2009 LTD, Life

Banner Health 7/2009 Life

Dow Corning 10/2009 LTD, Life

Microsoft 11/2009 LTD

BB&T 10/2010 LTD, Life, AD&D

Coca-Cola 2010-11 Retiree Health

Deutsche Bank 8/2011 LTD

800.851.7789www.SIIA.org

Economic Aspects/Risk Profile

9

Sample Structure

• The structures developed to date exhibit the need for partnership and risk sharing between the captive and the fronting carrier

• Deal components include:– Quota Share Loss Agreement– Sunset Clause in Long‐Term Disability Claims

• To avoid 20+ year payout

– Funds Withheld vs. Transferred Approach• Captive receives guaranteed investment return in funds withheld structure

Sample Structure

10

Sample Structure

Carrier 50% quota share to 125% expected

Captive 50% quota share to 125% expected

AggStop

Case Study: Large US Corporate

• Originally purchased guaranteed cost• Placed LTD in their captive after feasibility review• LTD performance had never been measured and managed

• Transfer to captive increased transparency, measurement and management of risk

• Witnessed direct correlation to managing STD and its benefit on LTD

11

Case Study: LTD Premium Rate

1.7671.707

1.3881.275

1.1550.955 0.955

Period 1 Period 2 Period 3 Period 4 Period 5 Period 6 Period 7

LTD Rate

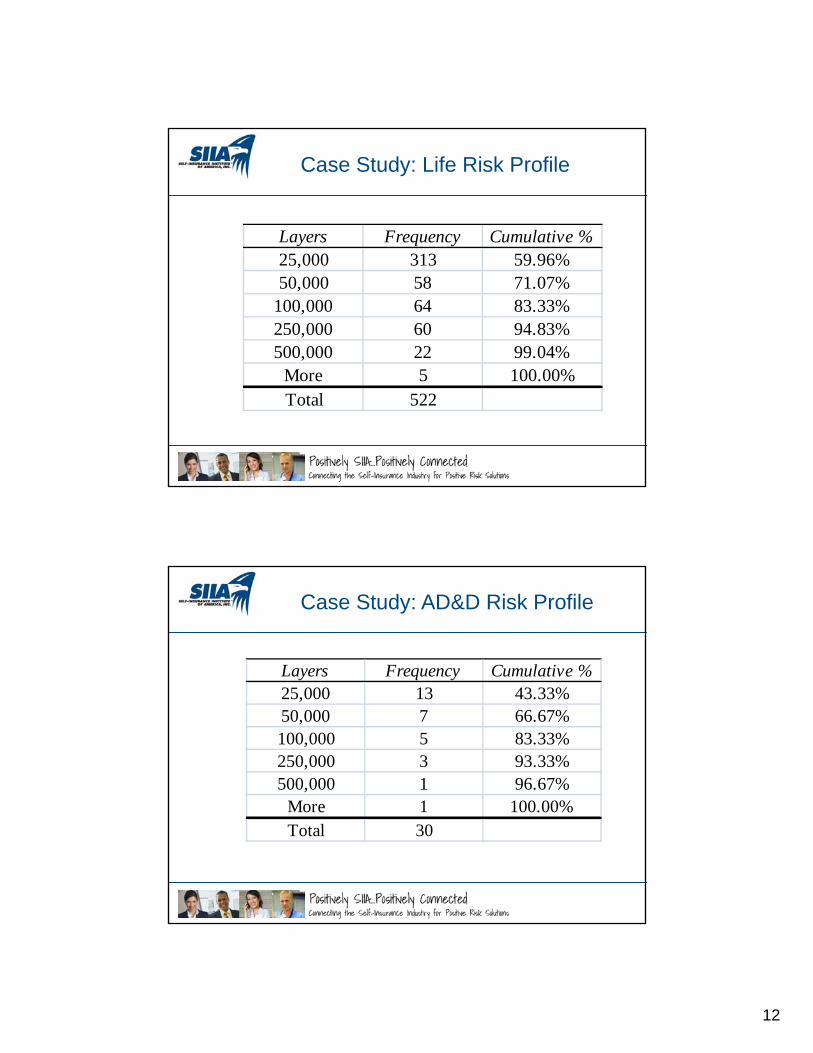

Case Study: LTD Risk Profile

Layers Frequency Cumulative %25,000 197 54.12%50,000 72 73.90%

• Cost Savings/Stability– Retain more risk– Reduce risk charges– Lower fixed costs– Retain investment income

14

Benefit Captive Considerations

• Control– Gain greater understanding of risk– Increase management and measurement of risk– Improved coordination with Integrated Disability Management (“IDM”)

– Expand use of existing captive surplus– Moderating current captive claims volatility through addition of uncorrelated risk

Captive Prospect/Coverage Profile

• At least 3,000 employees• A sizeable benefit program of $1,000,000 or more annually

• Purchases “guaranteed cost” insurance • These are rules of thumb and there are exceptions to all of these suggested targets

15

Summary

• Companies that have implemented benefits in captives have found:– Current benefit procurement process can be inefficient– Program experience is not being measured and monitored– Claims are being mishandled e.g. placed in disability instead of workers compensation

– Focus on benefit programs is positive, with or without the implementation of a captive and results in direct savings on benefit programs

Multi-National Benefits Captives

16

800.851.7789www.SIIA.org

Multinational Pooling Historical Overview

1953

2012

The industry’s first multinational benefits pool by AIG for Chase Manhattan covering three countries for $17k group life / medical premiums. The pool has since grown both geographically and financially over the years

1,500 companies have over 3,000 pools with a global premium of around $6 billion and an estimated 20 million covered lives

There are now 8 pooling networks active in 170 countriesversus 11 networks just several years ago

1962Swiss Life created the first pool in a tariff based country that included pensions. Today, the Swiss Life Network is a leading international network of more than 60 local insurers

Multinational Pooling Spectrum of Risk

Where are you now?Low Risk Increased Risk

LocalMarket

NaturalPool

TraditionalPooling

ActiveManagement

Reinsureto Captives

Directto Captives

Increased cash flow and potential for

cost savings

17

• How many international benefits captive clients do you have?

Pooling Networks In‐Force Captives

5

28

6

1

0

15

1

5

Benefits Captives / Multinational PoolingPulse Survey September 2011

60+captives

with benefits

• Where do you see new product innovation and new services being added to the multinational pooling spectrum of solutions?

“We see some room for product innovation in the alternative solutions space, in particular for

global underwriting programs.”

“Some pools will be established for information purposes only and clients

will be willing to pay a fee for this information monitoring service.”

“Increasing demand towards utilization and trends reports on the

health business.”

“Global service standards – real time access.”

“More on-line services and reporting through web based client lock-boxes.”

“Corporate wellness solutions with group medical insurance are actively promoted.”

Benefits Captives / Multinational PoolingPulse Survey September 2011

18

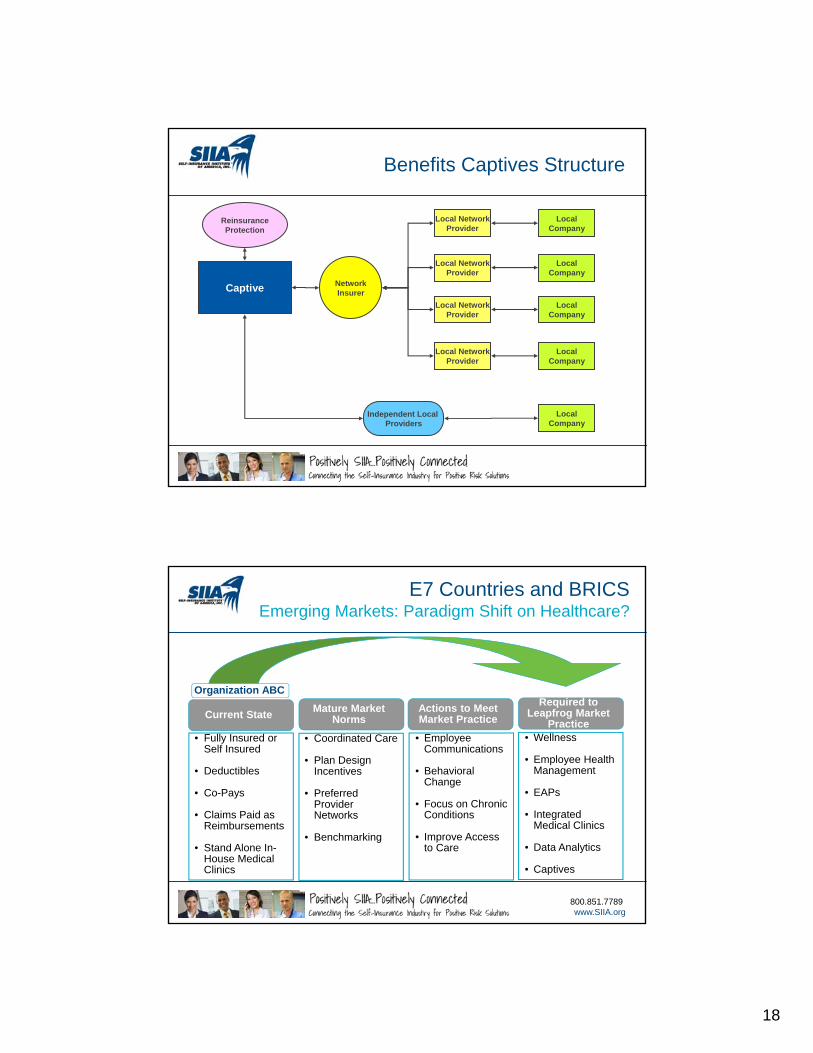

Benefits Captives Structure

ReinsuranceProtection

Captive NetworkInsurer

Local NetworkProvider

Local NetworkProvider

Local NetworkProvider

Local NetworkProvider

LocalCompany

LocalCompany

LocalCompany

LocalCompany

Independent Local Providers

LocalCompany

800.851.7789www.SIIA.org

Required to Leapfrog Market

PracticeActions to Meet Market Practice

Mature Market NormsCurrent State

Organization ABC

• Fully Insured or Self Insured

• Deductibles

• Co-Pays

• Claims Paid as Reimbursements

• Stand Alone In-House Medical Clinics

• Coordinated Care

• Plan Design Incentives

• Preferred Provider Networks

• Benchmarking

• Employee Communications

• Behavioral Change

• Focus on Chronic Conditions

• Improve Access to Care

• Wellness

• Employee Health Management

• EAPs

• Integrated Medical Clinics

• Data Analytics

• Captives

E7 Countries and BRICSEmerging Markets: Paradigm Shift on Healthcare?

19

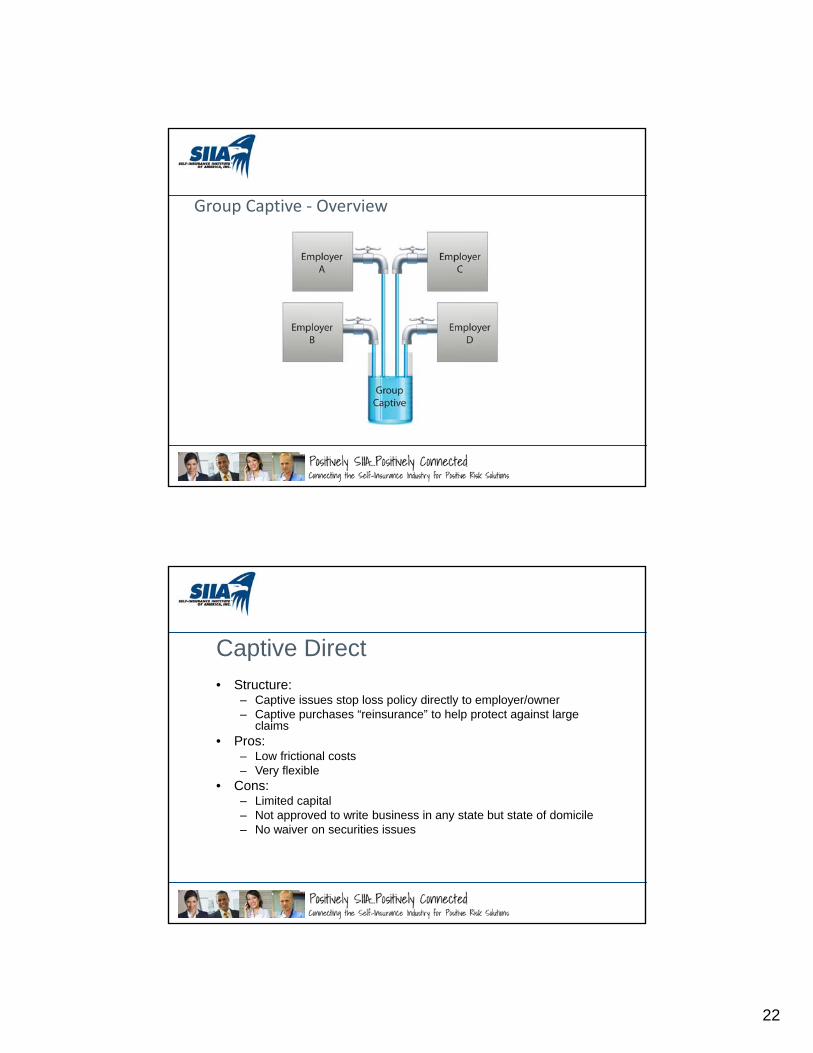

Benefits Captives for Small and Medium Sized Employers

Employee Benefit Group Captives• Built on a self‐funded platform• Typically designed for small to medium employers (25 to 500 employees)

• Medical and pharmacy most common lines• Typically doesn’t required DOL approval• Approximately 50 programs in existence• Growing rapidly

20

800.851.7789www.SIIA.org

Average Annual Health Insurance Premiums and Worker Contributions for Family Coverage, 2005-

2010

$8,167$9,773

$2,713

$3,997

2005 2010

Worker Contribution

Employer Contribution

$10,880

$13,770

47%

20%

27%

Motivations

• Control• Reduce costs• Receive data• Reduce or manage risk

21

What’s Driving Costs?• CDC estimates that 70% of costs are driven by:

– Stroke– Heart disease– Cancer– Diabetes– COPD

• These items can be controlled through exercise, diet, and treatments

• Employers’ views are moving past the next 12 months

Three Major Structures

• Almost all are actually stop loss captives not “employee benefit captives”