29

SPECIALTY MENTAL HEALTH AUDITS “Preparing for an audit” Presented by DHCS-Specialty Mental Health Audits Section Shirley Castaneda, MPA Jiayu Kelly Zhang

SPECIALTY MENTAL

HEALTH AUDITS

“Preparing for an audit”Presented by DHCS-Specialty Mental Health Audits

Section

Shirley Castaneda, MPA

Jiayu Kelly Zhang

A. PURPOSE OF PRESENTATION

The purpose of this presentation is to provide a high

level overview on how to better prepare for a successful

audit. During this presentation we will talk about who

we audit, what we audit (cost reports), the requirements

to conduct audits, why we audit cost reports, and brief

overview of the documentation requirements in an

audit.

B. SMH COST REPORTSCounty Mental Health Plans are required to submit cost reports to the

Department on an annual basis in accordance with the following W&I

Code Section requirements:

W&I Code Section 5651(a) (3) states, in pertinent part the following:

• “5651. The County Performance Contract

• The proposed annual county mental health services performance contract shall include all of the following:

• “(3) That the county shall comply with all requirements necessary for Medi-Cal reimbursement for mental health treatment services and case management programs provided to Medi-Cal eligible individuals, including, but not limited to, the provisions set forth in Chapter 3 (commencing with Section 5700), and that the county shall submit cost reportsand other data to the department in the form and manner determined by the department.” (Emphasis added)

W&I Code Section 5664 states:

• “5664. The County Performance Contract

• In consultation with the County Behavioral

Health Directors Association of

California, the State Department of Health

Care Services, the Mental Health Services

Oversight and Accountability Commission,

the California Behavioral Health Planning

Council, and the California Health and

Human Services Agency, county

behavioral health systems shall provide

reports and data to meet the information

needs of the state, as necessary.

C. AMENDED COST REPORTS –

SD/MC RECONCILIATION

• SD/MC Reconciliation Process

• Annually, the Department submits a letter to each county Mental Health Plan outlining the submission and reporting for the fiscal year. Among other things, the letter includes a section entitled: SD/MC Reconciliation. Following is the complete text of that letter taken from Department of Mental Health (DMH) Policy Letter No. 12-07 that states:

• “The SD/MC reconciliation process allows counties to add or reduce Medi-Cal units of service and revenue that have changed subsequent to the cost report submission for each legal entity.”

• This process is extremely important to the audit function since this reconciliation almost always results in an amended cost report thereby initiating a new starting point for the statute of limitations for conducting audits according to Section 14170 of the W&I Code.

The cost report is an all-inclusive document that contains information about a

number of programs that are subject to audit by the Department such as: the

Medi-Cal program, Mental Health Services Act (MHSA) , MAA Programs,

CALWORKS, Therapeutic Behavioral Services (TBS) and the Federal Block

Grant programs.

W&I Code Section 5718(c) states, in pertinent part the following:

“5718. Services to persons eligible for Medi-Cal:

With regard to county operated facilities, clinics, or programs for which claims are submitted to the department for Medi-Cal reimbursement for mental health services to Medi-Cal eligible individuals, the county shall ensure that all requirements necessary for Medi-Cal reimbursement for these services are complied with, including, but not limited to, utilization review and the submission of year-end cost reports by December 31 following the close of the fiscal year” (Emphasis added)

D. TYPES OF PROGRAM

• SHORT-DOYLE MEDI-CAL PROGRAM

• EARLY AND PERIODIC SCREENING, DIAGNOSTIC & TREATMENT

• FEE FOR SERVICE MEDI-CAL PROGRAM (INDIVIDUAL & GROUP)

• CALIFORNIA WORK OPPORTUNITY AND RESPONSIBILITY TO KIDS (CALWORKS)

• MEDI-CAL ADMINISTRATIVE ACTIVITIES (MAA) PROGRAM

• HEALTHY FAMILIES PROGRAM

• THERAPEUTIC BEHAVIORAL SERVICES PROGRAM (TBS)

• MENTAL HEALTH SERVICES ACT (MHSA) PROGRAM

E.REQUIREMENT TO CONDUCT

AUDITS

• Section 5717(b) of the W&I Code states:

“The director may make investigations and audits of expenditures the director may deem necessary.”

• Section 14170(a) (1) of the W&I Code states, in pertinent part the following:

“Amounts paid for services to Medi-Cal beneficiaries shall be audited by the department in the manner and form prescribed by the department…”

• Section 20202 of Title 22 of the California Code of Regulationsstates, in pertinent part the following:

“All contract entered into with the department shall be subject to audit.”

F. STATUTE OF LIMITATIONS FOR

CONDUCTING AUDITS OR REVIEWS OF

COST REPORTS

• Section 14170 (a) (1) of the W&I Code states, in pertinent part the following about limitations for conducting audits of cost reports and other data:

• “…Moreover the cost reports and other data for cost reporting periods beginning on January 1, 1972, and thereafter shall be considered true and correct unless audited or reviewed within three years after the close of the period covered by the report, or after the date of submission of the original or amended report by the provider, whichever is later.”

• Note: Above regulation is incorporated and elaborated upon in the County’s Mental Health Plan contract agreement with the State.

G. TYPE OF AUDIT – FINANCIAL AND

COMPLIANCE

• Audits conducted by the Specialty Mental Health Audits Section are primarily financial and compliance in nature. That is to say that the audits are financial in as much as the auditors look at various documents retained by the provider to support entries entered onto the cost report resulting in a financial outcome. The audits are in compliance in as much as the entries in the cost reports are checked for compliance with various federal and State laws, regulations.

H. TYPES OF AUDIT

FIELD AUDITS DESK AUDITS

• Field audits are audits in which the auditor visits the organization to be audited and either remains on site for the duration of the audit or gathers supporting documentation for use in completing the audit in the auditor’s headquarters office. Audits are selected based on a risk analysis using a set of criteria including performance by the provider during the last audit.

• Desk audits are usually limited to documents in possession of the Department such as the cost report, approved claims information and cost report settlement documents. However, a desk audit could also include a request for certain specific documents or other information from the provider to facilitate the audit. Cost reports selected for a desk audit usually pose less risk than those reports selected for a field audit either due to the magnitude of the costs involved or the known practices of the provider.

I. Entrance Conference

• The purpose of the entrance conference is to:

• Introduce auditors to organization representatives

• Explain the purpose and scope of the audit

• Review the requested list of items needed in the audit (The list is typically sent at least thirty days before the entrance conference.)

• Note: Providing the documentation at the entrance conference and during the audit can save on time and headaches towards the end of the audit (and afterwards).

J. ADEQUATE COST DATA &

COST FINDING

• Providers receiving payment based on reimbursable cost must provide adequate cost data based on financial and statistical records which can be verified by the auditors. The data must be based on an approved method of cost finding and accrual based method of accounting. Those who operate on cash basis of accounting, cost data on this basis is acceptable subject to treatment of capital expenditures.

• CMS Pub. 15-2 Chapter 23

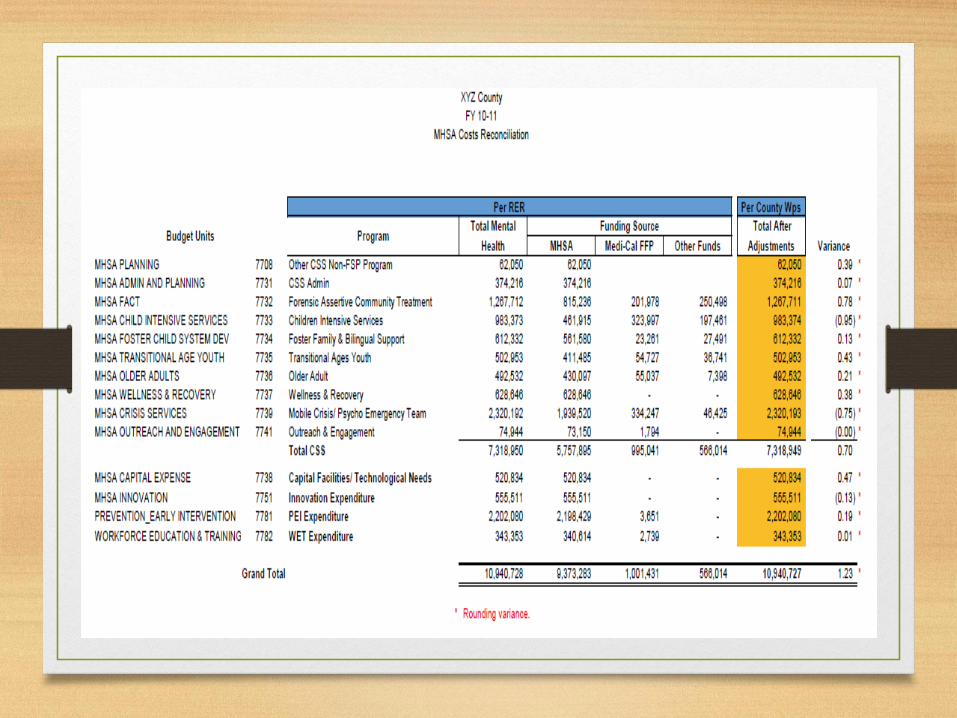

County SD/MC Workpaper

MHSA Budget Units

Amount ties to RER

Amount ties to MH 1960

Continued…

Amount ties to MH 1960

BeforeAmendment

AfterAmendment

AfterAmendment

BeforeAmendment

AfterAmendment

BeforeAmendment

AfterAmendment

BeforeAmendment

RER Innovation

K. Allocation of Expenditures

Allowable Methods of Allocating Administrative Costs:

• Percentage of program beneficiaries in the population served by the county (AKA: Unduplicated Client Count)

• Relative values based on the units and published charges

• Gross costs of each program

When allocating administrative costs using the percentage of program beneficiaries, Administrative Costs should be allocated to non-treatment services first using gross cost of each program. Note: Most County’s billing system do not track client statistics in non-treatment modes such as Modes 45, 55 and 60.

• Chart Review (For Utilization Review)

Gross Cost Method Example

L. Indirect Costs Examples

• Compensation of county mental health employees for time not devoted and identified specifically with the delivery of a reimbursable activity, performance of a specific administrative activity, or performance of a specific utilization review/quality assurance activity.

• Legal services

• Personnel administration

• Procurement

• Depreciation expense

Refer to DMH Letter No. 11-01

M. EXIT CONFERENCE

Following is an excerpt from Section 51016 (a) (6) of Title 22 of the California Code of Regulations (CCR) defining an exit conference:

“Exit conference” means an informal meeting, between the provider and those Department representatives responsible for the audit or examination, at which the preliminary findings of the audit or examination are discussed.”

• The exit conference affords the Department an opportunity to explain the audit findings by presenting documentation of the findings including code or regulatory citations. A good exit conference in many cases reduces the likelihood that the provider will file an appeal of the audit findings.

N. REGULATION

Section 51021 (b) of Title 22 CCR states that:

“The provider must make available to the Department

any records which were identified as unavailable for

review or missing within 15 calendar days of the exit

conference to be included in the Audit Report.”

O. CONCLUSION

• We have provided a lot of information for you today.

Some of that information will be new to many of

you and you may need further clarification in the

future. A successful audit is when reported figures

are supported by adequate documentation, helps

ensure program integrity, avoids unnecessary appeals

and ensures compliance with federal and state

requirements supporting the basis for the funding

sources.

P. QUESTIONS

THANK YOU FOR YOUR

PARTICIPATION