30

Spokane Region Competitiveness Graham Stone Lu Zhai Albaraa Sultan Shaykhah Almahri BADM 585 Strategy, Competitiveness and Economic Development March 17, 2014

Spokane Region Competitiveness

Graham Stone

Lu Zhai

Albaraa Sultan

Shaykhah Almahri

BADM 585

Strategy, Competitiveness and Economic Development

March 17, 2014

2

Table of Contents

1. Executive Summary ............................................................................................................................... 3

2. Introduction ............................................................................................................................................ 4

2.1 Purpose of the Study .................................................................................................................. 4

2.2 Scope of the Study ..................................................................................................................... 4

3. Literature Review ................................................................................................................................... 5

3.1 Harvard Business School 2012 Competitiveness Survey........................................................... 5

3.2 INSEAD EU Competitiveness Survey ....................................................................................... 7

4. Methodology .......................................................................................................................................... 9

4.1 Overview of Survey ................................................................................................................... 9

4.2 Survey Questionnaire ............................................................................................................... 11

4.3 Sample Design ......................................................................................................................... 11

5. Data Findings ....................................................................................................................................... 12

5.1 The Spokane Region Business Environment ........................................................................... 12

5.2 Actions by Business to Enhance Spokane Region Competitiveness ........................................ 16

5.3 Business Actions Patterns ........................................................................................................ 18

5.4 A Willingness to Do More ....................................................................................................... 19

6. Recommendations ................................................................................................................................ 21

7. Limitation ............................................................................................................................................. 22

8. References ............................................................................................................................................ 23

9. Appendix .............................................................................................................................................. 24

List of Figures

Figure 1: U.S. Competitiveness in Three Years, All Business Leaders in 2…………………..…………......6

Figure 2: Current U.S. Position Compared To Other Advanced Economies, 2011-2012 Movement…….....6

Figure 3: Assessment of Policy Proposals, All Business Leaders………………………………….………...7

Figure 4: European Competitiveness in Three Years, 2013………………………………………….……....8

Figure 5: U.S. and European Business Environments………………………………………………………..8

Figure 6: Position and Trajectory of Elements of Spokane Region Business Environment…………..........12

Figure 7: Elements of The National Business Environment………………………………………….….....13

Figure 8: Comparing Spokane Region Vs. U.S. on Elements of Business Environment…………….....….14

Figure 9: Competitiveness in Three Years………………………………………………………….…..…..15

Figure 10: Portion of Business Leaders Whose Firms Take Specific

Actions in Their Spokane Region Operations……………………………………………….……………...17

Figure 11: Comparing Spokane Region Vs. U.S. on Actions Firms Are Taking

To Affect Business Environment…………………………………………………………………………...17

Figure 12: Portion of Firms Would Be Interested in Each

Action………………………………………………………………………………………………...…….19

Figure 13: Comparing Spokane Region Vs. U.S. on Actions Firms Would Like To

Take……………………………………………………………………………………………..……….…20

List of Tables

Table 1: Metropolitan Areas……………………………………………………..……………………...….9

Table 2: Business Actions That May Enhance Competitiveness……………………………….………....16

Table 3: Correlations Across Business Actions ………………………………………………….…...…..18

3

1. Executive Summary

Competitiveness refers to the ability of firms to compete globally and achieve benefits

from their labor. Harvard Business School ("HBS") conducted a survey on U.S

competitiveness to understand and improve the competitiveness of the United States.

The HBS survey was adapted by the European Competitiveness Initiative to improve

global competitiveness of European-based businesses. This paper discusses adaptation of

the HBS competitiveness survey into an instrument which measures the perceptions of

those in the Spokane region business community regarding the competitiveness of the

Spokane region economy and business environment.

The survey on the Spokane Region competitiveness provides an updated view of Spokane

Region business environment. But it also examines specific actions that business leaders

can take to improve the Spokane Region competitiveness. The survey findings reflect the

perspectives of Eastern Washington University (“EWU”) alumni from different sectors

and members of Greater Spokane Incorporated (“GSI”).

In this survey, most of business leaders in the Spokane Region hold relatively neutral

perceptions on the Spokane business environment, which is different from our

assumption and slightly more positive than perceptions of U.S. competitiveness as a

whole, at least judging from the respondents of this survey. Moreover, even though firms

of the Spokane Region haven’t engaged that much in the business actions to enhance

local competitiveness, they show great interest in taking actions to improve the business

environment.

This paper also discusses some possible conclusions and recommendation that might be

drawn from the data. In particular, it identifies a disconnect between positive perceptions

of higher education and the comparatively low perceptions of skilled labor,

entrepreneurship, and innovation. The authors speculate this may be due to a “brain drain”

caused by Spokane lacking an attractive cultural atmosphere. Other negative perceptions

such as logistical infrastructure and the local political landscape are also briefly discussed.

Finally, the limitations of this survey process are discussed. In particular the potential

impact of the small number of participants and their possible unrepresentative selections

are pointed out as limitations.

4

2. Introduction

Regional competitiveness plays an important role in economic performance. This paper

focuses on understanding the perceptions of Spokane Region firms’ abilities to compete

in the U.S. marketplace. Therefore, the Harvard Business School Competitiveness Survey

was adapted into an instrument to investigate local business leaders’ perceptions of the

Spokane Region business environment and actions firms could take to enhance regional

competitiveness. For the purpose of the survey, the Spokane Region is defined as

Spokane, Spokane Valley, Coeur d’Alene, and adjacent cities and towns. This paper also

compares seventeen dimensions of the Spokane Region’s business environment with

those same dimensions in other similar sized regions, larger sized regions and smaller

sized regions in order to analyze the relative position of Spokane Region in the U.S.

marketplace and come up with data which can be used to make recommendations for

improving the region.

Core sections discuss a literature review which will examine what has already been found

regarding U.S. and European competitiveness. The methodology section will include an

overview of the survey questionnaire and sample design. Then, the findings of the data

will be discussed to draw conclusion regarding the findings found in the study.

Limitations and recommendations for future research will also be included in this study.

Finally, the survey questionnaire is appended at the end of the document.

2.1 Purpose of the Study

The purpose of this project was to adapt HBS competitiveness survey into an instrument

which measured the perceptions of those in the Spokane Region business community

regarding the competitiveness of the Spokane Region economy and business environment

so that recommendations can be made to the local government and business community.

2.2 Scope of the Study

The study compiled responses of business professionals who operate in the Spokane

business environment. These responses contain valuable information on the extent to

which respondents feel that issues such as local education opportunities, work conditions,

the legal system, and labor compensation contribute to shaping the economic landscape

of the Spokane Region.

5

3. Literature Review

The survey instrument used in this research was adapted from Harvard Business School

to better understand and improve the Spokane Region's competitiveness. Since this

questionnaire has been tested and conducted by HBS as well as INSEAD, the reliability

and validity is credible. Moreover, for the purpose of comparing the results of the

Spokane Region with the whole U.S. and even European Union, it was necessary to have

an overview of U.S. and European competitiveness. HBS conducted a U.S.

competitiveness survey on their alumni in 2011 and 2012 respectively. In 2013, INSEAD,

inspired by HBS competitiveness research, also launched the EU competitiveness survey.

3.1 Harvard Business School 2012 Competitiveness Survey

The HBS 2012 competiveness survey aimed at finding the perspectives of business

leaders and the general public regarding the competitiveness of the U.S. compared with

other advanced economies.

The HBS survey participants include 70,000 alumni, some of which also took part in a

similar survey in 2011, and 1,025 members of the general public. Questions about the

U.S. business environment have been asked of some participants twice; once in October

2011 and again in September 2012, allowing a longitudinal perspective about U.S.

competitiveness. The different opinions from the two results reflect the changing

impressions of the alumni on U.S. competitiveness over time. But one thing should be

kept in mind: that respondents can be easily influenced by the political climate of the

time. The 2011 survey was administered in October 2011, soon after the July-August

congressional standoff over the federal debt ceiling and Standard & Poor’s downgrading

of the federal government’s credit rating. The 2012 survey was administered in

September 2012, as the U.S. presidential election campaign approached its climax and

after a year of anxiety about the potential breakup of the Euro zone (Porter, Rivkin, and

Kanter, R., 2013).

The HBS 2012 survey focused on three parts of competitiveness topics: the U.S. business

environment, federal policy priorities, and business actions which may enhance U.S.

competitiveness (Porter, Rivkin, and Kanter, R., 2013).

The result showed that business leaders were not positive about the U.S. business

environment, even though they were less pessimistic in 2012 than the previous year.

Figure 1 shows that fifty-eight percent of business leaders thought that U.S.

competitiveness was getting worse; firms would be less competitive in the global market

and less able to pay high wages. Meanwhile, only twenty-five percent held a positive

perspective of increased U.S. competitiveness and increasing wages.

6

FIGURE 1: U.S. COMPETITIVENESS IN THREE YEARS, ALL BUSINESS LEADERS IN 2012

Will firms in the U.S. be more or less able to compete in the global economy?

LESS

NEITHER

LESS NOR

MORE MORE

LESS 28% 17% 7%

NEITHER

LESS NOR

MORE 5% 17% 7%

MORE 1% 5% 14%

Percentages in boxes may not sum to total because of rounding. Source: Harvard Business School Survey on U.S. Competitiveness.

As shown in figure 2, business leaders perceived modest improvement in most elements

of the U.S. business environment between 2011 and 2012. However, perceptions of the

tax code, the K–12 education system, regulation, and the availability of skilled labor

remained stubbornly negative (Porter, Rivkin, and Kanter, R., 2013).

FIGURE 2: CURRENT U.S. POSITION COMPARED TO OTHER ADVANCED ECONOMIES,

2011-2012 MOVEMENT

Source: Harvard Business School Survey on U.S. Competitiveness.

The last part of HBS survey investigated the actions firms could take or did take to

improve business competitiveness. The general actions consisted of internal training

programs, regional initiatives, research collaboration, business-wide lobbying, startup

Will firms in the U.S. be more

or less able to pay high wages

and benefits?

Red, or falling

competitiveness: 58%

in total

Green, or rising

competitiveness: 25%

in total

7

incubation, apprenticeships, local sourcing and cluster initiatives. More than 30% of

respondents stated that their firms took those actions in their U.S. operations to improve

business competitiveness. Figure 3 displays the specific portion of business leaders

whose firms take specific actions in their U.S. operations.

FIGURE 3: ASSESSMENT OF POLICY PROPOSALS, ALL BUSINESS LEADERS

Source: Harvard Business School Survey on U.S. Competitiveness.

The results also showed that the manufacturing sector made the most contributions to U.S.

competitiveness, followed by education and healthcare sectors. Financial services and

construction & real estate took fewer actions to benefit U.S. competitiveness.

3.2 INSEAD EU Competitiveness Survey

INSEAD is one of the leading business schools in the world and has three campuses in

France, Singapore, and Abu Dhabi. The INSEAD European Competitiveness Initiative

(IECI) was inspired by Harvard Business School (HBS) and its U.S. Competitiveness

Project. The main goal of this project is “to impact on improving global competitiveness

of Europe-based businesses” (Gimeno, 2013, p. 3). The alumni survey was one of the

most important activities done by the INSEAD European Competitiveness Initiative in

2013 because it sought to track the evolution of competitiveness. They essentially

focused on Europe; the 27 countries of the European Union (EU 27) and the European

Free Trade Association (EFTA 4) which includes Iceland, Liechtenstein, Norway and

Switzerland as well as micro-states.

The findings were the result of an analysis of the responses to the main two questions: 1)

In three years, will firms in Europe be more or less able to compete in the global

economy? 2) In three years, will firms be more or less able to pay high wages and

benefits?

As shown in Figure 4, the study found that the majority of business leaders, seventy-five

percent, expected European competitiveness to deteriorate, with firms less able to

compete, less able to pay well, or both. Another eleven percent were neutral, anticipating

8

no change on either dimension. Only fourteen percent were optimistic, expecting one or

both dimensions of European competitiveness to improve and neither to decline.

FIGURE 4: EUROPEAN COMPETITIVENESS IN THREE YEARS, 2013

Will firms in Europe be more or less able to compete in the global economy?

LESS

NEITHER

LESS NOR

MORE MORE

LESS 44% 17% 8%

NEITHER

LESS NOR

MORE 5% 11% 4%

MORE 1% 3% 7%

Percentages in boxes may not sum to total because of rounding. Source: INSEAD European Competitiveness Survey: Implementation and Findings.

In addition, Figure 5 shows that twenty-one percent of European business leaders believe

that the current European position is better compared to the business environment of

other advanced economies, whereas sixty-four percent of U.S. business leaders responded

that the current U.S. position is better when compared to the business environment of

other advanced economies (Gimeno, 2013).

FIGURE 5: U.S. AND EUROPEAN BUSINESS ENVIRONMENTS

Source: INSEAD European Competitiveness Survey: Implementation and Findings.

Will firms in Europe be more

or less able to pay high wages

and benefits?

Red, or falling

competitiveness: 75%

in total

Green, or rising

competitiveness: 14%

in total

9

4. Methodology

The methodology section will provide a brief overview of the survey and will discuss the

core sections; the survey questionnaire and the sample design.

4.1 Overview of Survey

Because perception of competitiveness is by its nature a comparison, a scope of

comparison was determined. One possibility was to have participants rate the

competitiveness of Spokane versus that of the world at large, including such advanced

economies as Western Europe, Japan, and the United States. While this comparison

could be made, the scale of comparison between Spokane and such large entities made

the comparison less meaningful. The possibility of limiting the comparison to similar

sized economies in the rest of the world was considered, but that would add another layer

of unnecessary conjecture on the part of the participants, who may not be familiar with

other similar sized economies around the world. It is also taken into consideration that

the previous studies already drew comparisons to the world at large.

Since the Spokane Region is itself made up not only of the City of Spokane, but also

Coeur d'Alene, Post Falls, and Airway Heights, a more meaningful comparison could be

drawn with other metropolitan areas that are similar in population. Because the previous

studies already offered perceptions of the U.S. versus the rest of the world, a study that

focused on the perceptions of Spokane versus other similar sized U.S. metropolitan areas

could then be used to extrapolate perceptions of Spokane vis-a-vis the world. For this

reason, the comparison was focused on other similar sized metropolitan areas. Other

metropolitan areas which would be useful as a comparison to the size of the Spokane

Region were determined by using the Metropolitan Statistical Areas (“MSA”) established

by the U.S. census, which ranked them according to size. Areas such as Salt Lake City

(UT), Colorado Springs (CO), Reno (NV), Jackson (MS), and Des Moines (IA) were

found to be similar to, though somewhat varied from, the Spokane region.

TABLE 1: METROPOLITAN AREAS

MSA Population Median Income GDP Export ( USD)

New York–Northern New Jersey 21,199,865 $57,799 $1,358,416 $102,298,029,869

Seattle–Tacoma–Bellevue, Washington 3,554,760 50,733 258,819 50,301,690,645

Salt Lake City–Ogden, Utah 1,333,914 48,594 72,072 15,989,999,420

Spokane, Washington 417,939 19,233 20,352 873,470,610

Colorado Springs ,Colorado 516,929 46,844 28,029 1,044,574,535

Boise City, Idaho 432,345 20,280 27,455 4,088,209,242

Jackson, Mississippi 440,801 38,887 5,318 942,848,736

Des Moines, Iowa 456,022 46,651 42,129 1,183,201,634

Yakima, Washington 339,486 45,815 20,400 2,018,999,123

Santa Crus, California 264,298 67,769 9,451 838,042,424

Reno ,Nevada 222,581 34,828 8,108 1,181,158,276

Waco, Texas 213,517 33,560 9,691 398,046,200

Bellingham, Washington 166,814 40,005 9,888 1,642,712,278

10

Table 1 shows the variability of prosperity indicators of similar sized metropolitan areas

such as median income, exports, and GDP. The table includes thirteen MSAs with

population figures which can be divided into three categories based on population: high

population (above 1 million), moderate population (between 300,000 and 1,000,000), and

low population (less than 300,000). As illustrated by table1, the Spokane Region is

ranked seventh among the selected MSAs in population but ranked ninth in terms of

export volume and median income. However, the goal of this project is to measure the

perceptions of business leaders regarding the competitiveness of the Spokane Region,

rather than compare actual indicators. These figures are provided only as a reference for

the reader.

The perceptions of Spokane Region competitiveness were measured in a way as close to

the original survey as possible in order to decrease the possibility that differing results

were due to differences in the underlying instrument. In adapting the survey, minimal

changes were made to existing survey questions. The only questions which were removed

were those which could not be adapted since they inquired about topics that would be

irrelevant to the scope of comparison.

In particular, references to perceptions of the U.S. were changed to perceptions of the

Spokane Region, which was defined in the introduction of the survey instrument. In

addition to that, comparisons to major world economies were changed to comparisons to

similar-sized U.S. metropolitan areas and some examples of similar regions were

included. For example, a section that previously read "For each element, please rate the

U.S. compared to other advanced economies like Western Europe, Japan, and Canada.",

would now read as "For each element, please rate the Spokane area compared to other

similar sized regions in the U.S." These changes customized the scope of the instrument

to the needs of this study; competitiveness of the Spokane compared to that of other

similar size regions in the U.S.

The end result of the adaptation review is a streamlined yet very similar survey

instrument. The only question added was to inquire about the size of the firm the

participant represents. This instrument retains the strengths of the original and can be

used as a parallel study to the previous studies which each have a larger scope of

comparison.

11

4.2 Survey Questionnaire

National competitiveness is “The ability of firms operating in the U.S. to compete

successfully in the global economy while supporting high and rising living standards for

Americans” (Porter, Rivkin, and Kanter, R., 2013, p.1 ). In this study, this concept was

applied to investigate the perceptions of managers of local firms regarding the local

business environment and its ability to support high wages.

This survey consists of four sections including business environment, firm performance,

actions firms do or could take to improve the business environment, and basic

information about the firm. The first set of questions concern the state and trajectory of

seventeen elements that affect how well firms in the Spokane region can compete in the

U.S. market. The second section asks whether firms operating in the Spokane region can

support rising wages and benefits. The third section asks business managers about steps

that their own firm is taking or might take to improve local competitiveness. Finally, the

last section asks basic information about respondents’ firms such as number of employees

and area of business.

4.3 Sample Design

The Spokane Region Competitiveness Survey was designed to include EWU alumni with

known email addresses and members of Greater Spokane Incorporated (GSI). Its design

excludes alumni without email addresses. Alumni with invalid email addresses were also

excluded. GSI and alumni with an email address were considered to be eligible for the

survey.

Each respondent can only respond once to the survey; this requirement exists throughout

the study. Potential participants will receive an introduction email inviting them to

participate in the survey, and a link to the survey itself. The survey was placed online

such that participants could click on their responses for each section before moving on to

the next. Once completed, the website compiled the responses in a form that made

analysis of each question easier.

The survey was sent to 134 business leaders as well as GSI through EWU faculty. The

response rate was 35% for the direct emails to the 134 businesses, plus 12 more responses

from GSI participants with an unknown response rate. Seven respondents started but did

not complete the survey. The respondents are part of organizations of a variety of sizes.

Most of the respondents were employed by private sector, for profit organizations. The

job titles held by respondents were President, CEO, Owner, Financial Specialist,

Financial Analyst and Director of Finance. The main sectors that respondents work in

were professional, financial services, other manufacturing, utilities and other services.

These primary data were collected and analyzed to draw final conclusions of the findings

compared to the previous results of HBS and INSEAD studies.

12

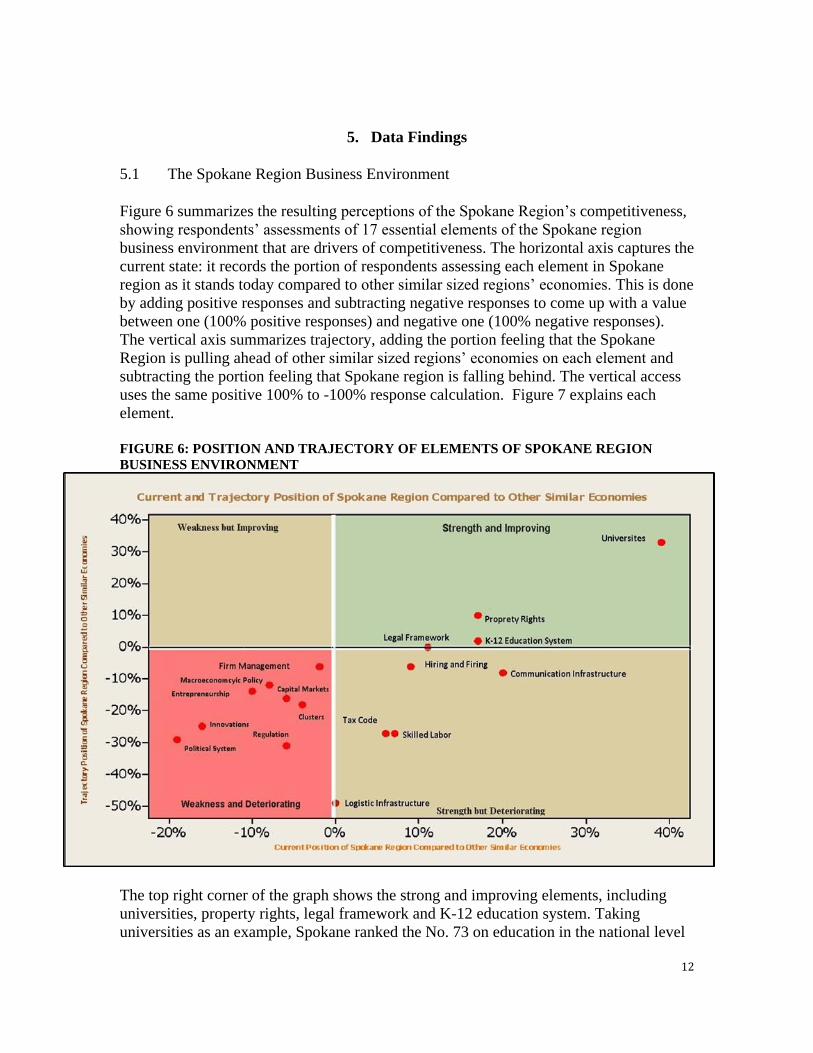

5. Data Findings

5.1 The Spokane Region Business Environment

Figure 6 summarizes the resulting perceptions of the Spokane Region’s competitiveness,

showing respondents’ assessments of 17 essential elements of the Spokane region

business environment that are drivers of competitiveness. The horizontal axis captures the

current state: it records the portion of respondents assessing each element in Spokane

region as it stands today compared to other similar sized regions’ economies. This is done

by adding positive responses and subtracting negative responses to come up with a value

between one (100% positive responses) and negative one (100% negative responses).

The vertical axis summarizes trajectory, adding the portion feeling that the Spokane

Region is pulling ahead of other similar sized regions’ economies on each element and

subtracting the portion feeling that Spokane region is falling behind. The vertical access

uses the same positive 100% to -100% response calculation. Figure 7 explains each

element.

FIGURE 6: POSITION AND TRAJECTORY OF ELEMENTS OF SPOKANE REGION

BUSINESS ENVIRONMENT

The top right corner of the graph shows the strong and improving elements, including

universities, property rights, legal framework and K-12 education system. Taking

universities as an example, Spokane ranked the No. 73 on education in the national level

13

(Forbes, 2013). According to U.S. News & World Report’s 2012 college rankings,

Gonzaga University is the No. 3 best university in the West. Whitworth University was

recognized No. 2 on the best values list in 2012. In U.S. News’ 2010 America’s Best

Colleges guidebook, Spokane is one of only four cities in the U.S. with more than one

school in the top 10 of both the best schools and best values rankings (Greater Spokane

Incorporated, 2014).

However, political system, regulation, innovation, entrepreneurship, clusters, capital

markets, macroeconomic policy and firm management are falling at the left bottom,

which means they are perceived as worse than other similar regions and falling behind

overtime. Some elements like logistics infrastructure, even though respondents value it

average level regarding its current situation, about half of business leaders thought it was

deteriorating overtime. As we all know, there are highways, railroads, and a major airport

in Spokane, but these assets are perceived as falling behind other regions.

FIGURE 7: ELEMENTS OF THE NATIONAL BUSINESS ENVIRONMENT

Source: Harvard Business School Survey on U.S. Competitiveness.

Figure 8 compares perceptions of the Spokane Region and U.S. business leaders on

essential elements of their respective business environments. Data points that fall on the

diagonal line mean that both groups hold the same perception on that aspect of their

business environments, like regulation; which both see as somewhat negative.

Perceptions of the Spokane Region business environment surpassed perceptions of the

U.S business environment in three elements found in the lower right: legal framework,

tax code and k-12 education system. The lower left portion of the figure reflects that

14

perceptions of both the U.S and the Spokane Region are low with respect to political

system and macroeconomic policy.

The upper right area shows that perceptions of both U.S. and Spokane Region

universities, property rights, hiring and firing, communication infrastructure, skilled labor,

and logistic infrastructure, are generally positive. The upper left shows there is a

difference of perception on clusters, capital markets, innovations and entrepreneurship;

which is seen as more negative in the Spokane Region but more positive in the U.S. as a

whole. There is an especially large difference of perception in the areas of innovations,

entrepreneurship, capital markets, and firm management. These areas in particular

deserve additional attention in order to catch up with U.S. perceptions.

FIGURE 8: COMPARING SPOKANE REGION VS. U.S. ON ELEMENTS OF BUSINESS

ENVIRONMENT

Most business leaders in the Spokane Region hold neutral perceptions of the Spokane

Region’s competitiveness, which is slightly positive compared to perceptions of U.S.

competitiveness as a whole. Remember, competitiveness is measured both in the abilities

of firms to compete and the ability to sustain high wages. In this sense, 46% of Spokane

business leaders expected the Spokane Region competitiveness to deteriorate, with firms

either less able to pay high wages or less competitive, or both. 32% were optimistic

(green boxes), expecting one or both dimensions of competitiveness to increase without a

drop in the other dimension.

15

Wil

l fi

rms

in t

he

U.S

. be

more

or

less

able

to

pay

hig

h w

ages

an

d b

enef

its?

Comparing the Spokane Region’s results with that of the U.S., we find more pessimism

in U.S. perceptions. 58% perceived one or both dimensions as weaker versus only 46% in

the Spokane Region. Only 26% perceived the U.S. as positive in one or both categories

without being negative in the other compared to 32% in the Spokane Region. Both

results show that respondents are more doubtful about the future of worker payment than

about the future of firms’ marketplace success. However, business leaders in Spokane

Region cast more doubt on worker pay, while seeming more confident to maintain firms

operating ability.

FIGURE 9: COMPETITIVENESS IN THREE YEARS

5.2

LESS

NEITHER

LESS NOR

MORE MORE

LESS 28% 17% 7%

NEITHER

LESS NOR

MORE 5% 17% 7%

MORE 1% 5% 14%

LESS

NEITHER

LESS NOR

MORE MORE

LESS 8% 30% 6%

NEITHER

LESS NOR

MORE 2% 25% 11%

MORE 0% 8% 13%

Red, or falling

competitiveness:

45% in total

Green, or rising

competitiveness:

30% in total

Red, or falling

competitiveness: 58%

in total

Green, or rising

competitiveness: 25%

in total

Wil

l fi

rms

in t

he

Spokan

e R

egio

n b

e m

ore

or

less

able

to p

ay h

igh w

ages

an

d b

enef

its?

Will firms in the Spokane Region be

more or less able to compete in the

U.S. economy?

Will firms in the U.S. be more or less

able to compete in the global

economy?

Percentages in boxes may not sum to total because of rounding.

Percentages in boxes may not sum to total because of rounding.

16

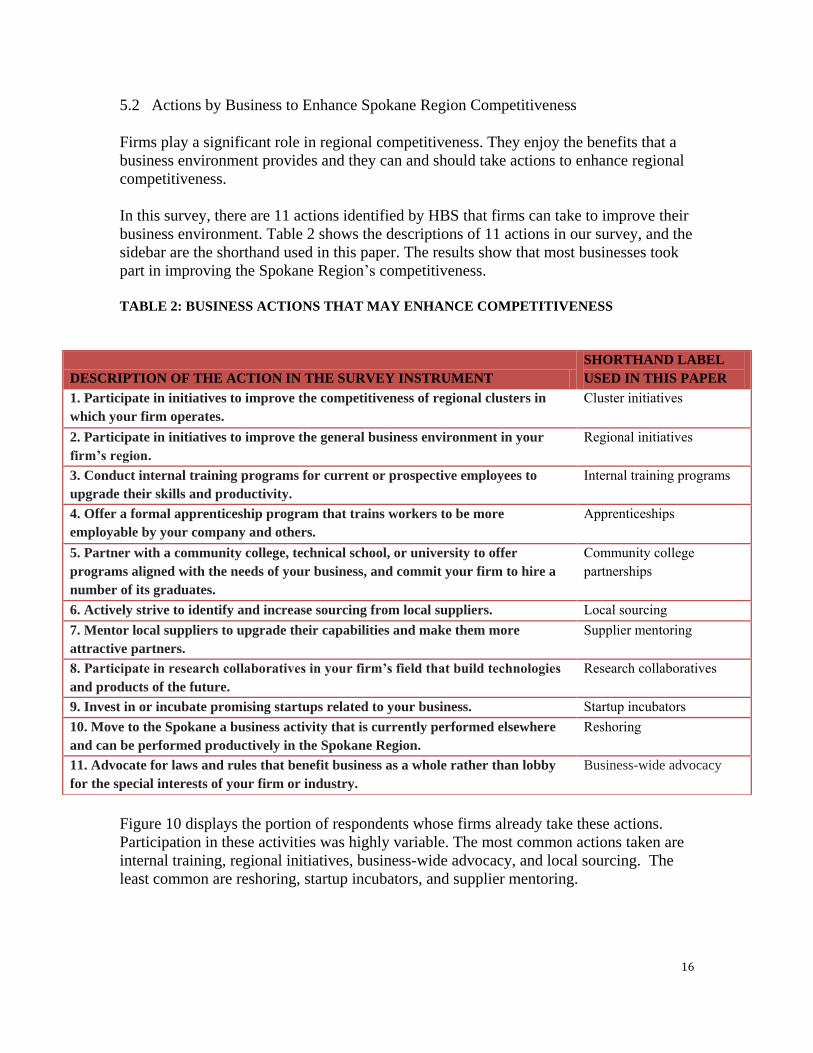

5.2 Actions by Business to Enhance Spokane Region Competitiveness

Firms play a significant role in regional competitiveness. They enjoy the benefits that a

business environment provides and they can and should take actions to enhance regional

competitiveness.

In this survey, there are 11 actions identified by HBS that firms can take to improve their

business environment. Table 2 shows the descriptions of 11 actions in our survey, and the

sidebar are the shorthand used in this paper. The results show that most businesses took

part in improving the Spokane Region’s competitiveness.

TABLE 2: BUSINESS ACTIONS THAT MAY ENHANCE COMPETITIVENESS

Figure 10 displays the portion of respondents whose firms already take these actions.

Participation in these activities was highly variable. The most common actions taken are

internal training, regional initiatives, business-wide advocacy, and local sourcing. The

least common are reshoring, startup incubators, and supplier mentoring.

DESCRIPTION OF THE ACTION IN THE SURVEY INSTRUMENT

SHORTHAND LABEL

USED IN THIS PAPER

1. Participate in initiatives to improve the competitiveness of regional clusters in

which your firm operates.

Cluster initiatives

2. Participate in initiatives to improve the general business environment in your

firm’s region.

Regional initiatives

3. Conduct internal training programs for current or prospective employees to

upgrade their skills and productivity.

Internal training programs

4. Offer a formal apprenticeship program that trains workers to be more

employable by your company and others.

Apprenticeships

5. Partner with a community college, technical school, or university to offer

programs aligned with the needs of your business, and commit your firm to hire a

number of its graduates.

Community college

partnerships

6. Actively strive to identify and increase sourcing from local suppliers. Local sourcing

7. Mentor local suppliers to upgrade their capabilities and make them more

attractive partners.

Supplier mentoring

8. Participate in research collaboratives in your firm’s field that build technologies

and products of the future.

Research collaboratives

9. Invest in or incubate promising startups related to your business. Startup incubators

10. Move to the Spokane a business activity that is currently performed elsewhere

and can be performed productively in the Spokane Region.

Reshoring

11. Advocate for laws and rules that benefit business as a whole rather than lobby

for the special interests of your firm or industry.

Business-wide advocacy

17

FIGURE 10: PORTION OF BUSINESS LEADERS WHOSE FIRMS TAKE SPECIFIC

ACTIONS IN THEIR SPOKANE REGION OPERATIONS

FIGURE 11: COMPARING SPOKANE REGION VS. U.S. ON ACTIONS FIRMS ARE

TAKING TO AFFECT BUSINESS ENVIRONMENT

In figure 11, internal training was the most common action taken by firms at 69%.

Because we have many medium and small sized firms in the Spokane Region, local

sourcing seems like play an important role, almost 20% higher than the national level.

Furthermore, because there are so many education resources here in the Spokane Region,

0% 20% 40% 60% 80% 100%

Reshoring

Startup incubators

Supplier mentoring

Research collaboratives

Cluster initiatives

Apprenticeships

Community college partnerships

Local sourcing

Business-wide advocacy

Regional initiatives

Internal training programs

Yes No Not Applicable Don't know

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

Spokane Region

U.S.

18

the amount of firms that partner with a community college, technical school, or university

to offer programs is also high. Advocating for laws and rules that benefit business as a

whole also seems like a special character of regional economy. Comparing with national

wide business actions, we still lag behind in research collaboratives and startup

incubators, which are strong factors for an innovation-driven economy.

5.3 Business Actions Patterns

TABLE 3: CORRELATIONS ACROSS BUSINESS ACTIONS

A company’s effort to boost competitiveness is defined not just by the number of

individual actions it takes but also by the way it combines and aligns its actions (Porter,

Rivkin, and Kanter, R., 2013). Table 3 shows the correlation in adoption across each pair

of actions, reflecting how often a firm that adopted one action also pursued another. This

statistical analysis revealed some set of patterns. Firms combined certain kinds of actions

to enhance the business environment and local situation.

Instead of isolated actions, firms sometimes take a set of measures to reinforce actions

effectively and efficiently. For instance, community college partnerships often

accompanied Apprenticeships (correlation index 0.63) as well as internal training

programs. Companies that stressed local sourcing were likely to mentor suppliers

(correlation index 0.51). Startup incubator was commonly employed alongside research

collaboratives (correlation index 0.59).

Cluster Regional Internal Training

Apprenticeships

Community College Local Supplier Research Startup Reshoring

Initiatives Initiative Program Partnerships Sourcing Mentoring Collabora

tive Incubation

Regional initiatives 0.22

Internal training programs 0.17 0.41

Apprenticeships 0.07 0.08 0.43 Community

college+ partnerships 0.10 0.29 0.56 0.63

Local sourcing 0.54 0.15 0.05 -0.01 0.05 Supplier

mentoring 0.47 0.09 0.08 -0.01 0.16 0.51 Research

collaboratives 0.14 0.04 0.39 0.33 0.47 0.14 0.29 Startup

incubation 0.32 0.08 0.36 0.36 0.37 0.32 0.27 0.59 Reshoring -0.07 0.03 0.10 0.16 0.11 0.21 0.18 0.20 0.30

Business-wide lobbying 0.36 0.31 0.23 0.08 0.14 0.44 0.18 0.20 0.32 0.00

19

5.4 A Willingness to Do More

We asked respondents about their firms’ willingness to consider actions that they are not

currently taking. Up to 57% indicated that they might be interested in doing so, with 7-23%

indicating that they would definitely be interested in particular actions as shown in figure

12. Spokane Region business leaders expressed greater interest in taking actions

compared with survey participants at the national level. Internal training programs and

business-wide advocacy attracted the most interest among them, followed by regional

initiatives, local sourcing and cluster initiatives.

FIGURE 12: PORTION OF FIRMS WOULD BE INTERESTED IN EACH ACTION

0% 20% 40% 60% 80% 100%

Cluster initiatives

Regional initiatives

Internal training programs

Apprenticeships

Community college partnerships

Local sourcing

Supplier mentoring

Research collaboratives

Reshoring

Startup incubators

Business-wide advocacy

Portion of firms would be interested in each action

Definitely not interested Probably not interested May or may not be interested

20

FIGURE 13: COMPARING SPOKANE REGION VS. U.S. ON ACTIONS FIRMS WOULD

LIKE TO TAKE

It can be clearly seen from figure 13 that Spokane Region business leaders, compared

with the U.S. as a whole, have more interest in taking business actions to enhance

regional competitiveness. This seems especially true for local sourcing and supplier

mentoring, since most of the respondents work for small and medium sized private

companies, it is reasonable for them to want to cooperate with nearby companies and

build strong relationships with suppliers. Moreover, from a long-term point of view, it

will help companies to cut down costs and control quality with local sourcing.

21

6. Recommendations

While the data does not offer a crystal ball into the problems or solutions of the Spokane

Region economy, it raises some informative points that could guide further study. One of

the Spokane Region’s clearest strengths is in its higher education. This bears out both in

official rankings of schools as well as local perception of them. Not only are our

institutions of higher learning well-perceived now, but participants also predict they will

get better with time. Added to this, many firms report that they take part in activities

such as community college partnerships and apprenticeships. One might think that a

highly rated education system would then translate into a skilled work force, but

perceptions on that point were only mildly positive as to Spokane’s current state of

having a skilled workforce and it is widely perceived that it will get worse.

Possible explanations of this disconnect may be that while we may have the ability to

produce a skilled workforce, Spokane does not retain these workers, who instead move to

other areas. Anecdotally, it seems to be a common complaint that Spokane is “ugly” or

otherwise lacks that certain cultural something that makes it a desirable place to live year

round. Developments such as Kindle Yards may add more recreation space and

attractions, while others such as developing Tubbs Hill (a popular outdoor recreation site

in the middle of civilization) may detract from Spokane’s attractiveness. A focused plan

to improve the collective attractiveness of Spokane as a city to live in may help stymie

this perceived brain drain.

A similar disconnect of perception is that innovation and entrepreneurship are poorly

perceived in both current state and future prospects despite glowing reviews of higher

education. Again, this may be linked to talent moving out of the area.

Linked to Spokane’s attractiveness is another factor that received tepid review: logistical

infrastructure. This factor received middling scores on perceptions of current status, but

was overwhelmingly seen as deteriorating in the future. This could be due to lack of

upkeep on current infrastructure, the snail’s pace of infrastructure improvements such as

the North/South corridor, and or urban sprawl; especially to the North. It may also be

that existing infrastructure, such as the airport, bus system, freeways, and rail systems are

perceived as less convenient or effective than they could be, with no perceived plans to

improve.

By far the lowest perceptions in both current status and future outlook belonged to the

political system. It is no secret that Spokane does no re-elect mayors, which may lead to

a perception of a revolving door of leadership where nothing lasting gets done. Perhaps

if leadership addressed other longstanding points with clear vision for the future, the

residents may be more inclined to keep that leadership in office.

22

7. Limitations

The primary limitations of the survey are the sample population and the sample size.

Since the majority of participants were drawn from the contacts of EWU faculty, the

sample may not be representative of business leaders in the Spokane Region. The sample

is likely to over-represent EWU alumni and others closely related to EWU. Also, despite

the high response rate, the overall sample size is fairly low, which could potentially make

the sample statistically unreliable in representing the greater population. It is possible

that others view Spokane competitiveness significantly differently than our sample

population.

It is also possible that our sample has a higher view of regional education than a less

biased sample that included fewer alumni, which would undermine one of the stronger

findings: that higher education is well-perceived.

23

8. References

Forbes (2013). Best Places For Business And Careers.

Gimeno, J. (2013). INSEAD European competitiveness survey: Implementation and

findings. 2013 INSEAD Faculty Workshop.

Greater Spokane Incorporated (2014). Education.

Porter, M , J Rivkin and R Kanter (2013). Competitiveness at a crossroads. Boston:

Harvard Business School.

The United States Census Bureau (2012). Metropolitan Statistical Areas Rank by

Population.

24

9. Appendix

Spokane Region Competitiveness Survey

Thank you for taking the Spokane Region Competitiveness Survey. The goal of the survey is to

measure the perceptions the Spokane region's economic competitiveness compared to other similar

regions in the U.S. The survey will take approximately 10 minutes and consists of four sections. Many

people find the questions very interesting. Participation in this survey is entirely voluntary and you can

stop at any time. Your responses to the survey are confidential.

This survey is adapted from the Harvard Business School ("HBS") U.S. Competitiveness Survey.

HBS developed this survey to better understand and improve the competitiveness of the United States.

HBS originally conducted its version of this study in 2011 and 2012 and results have been shared

through media such as the Economist. This study has sparked further study through the federal

government on how to improve the competitiveness of the U.S.

Eastern Washington University ("EWU") is part of the Microeconomics of Competitiveness

("MOC") network which is based at Harvard. EWU learned about the Harvard survey through this

network. As part of this MOC network, EWU teaches a course on Strategy, Competitiveness and

Economic Development, instructed by Dr. Harm-Jan Steenhuis. One of the goals of this course is

understanding and improving the competitiveness of the Spokane region. The survey instrument from

HBS was adapted as a project for this course in order to better understand and improve the

competitiveness of the Spokane region, as well as to compare results obtained from respondents in

Spokane with the national HBS survey. The aggregate results of this survey will be shared with HBS and

used for further research.

If you have any questions about this survey, please contact:

Eastern Washington University

Dr. Harm-Jan Steenhuis

Professor of Management and MOC member

Phone: 509-828-1202

E-mail: [email protected]

NOTE: For the purpose of the survey, the Spokane Region is defined as Spokane, Spokane Valley,

Coeur d’Alene, and adjacent cities and towns.

25

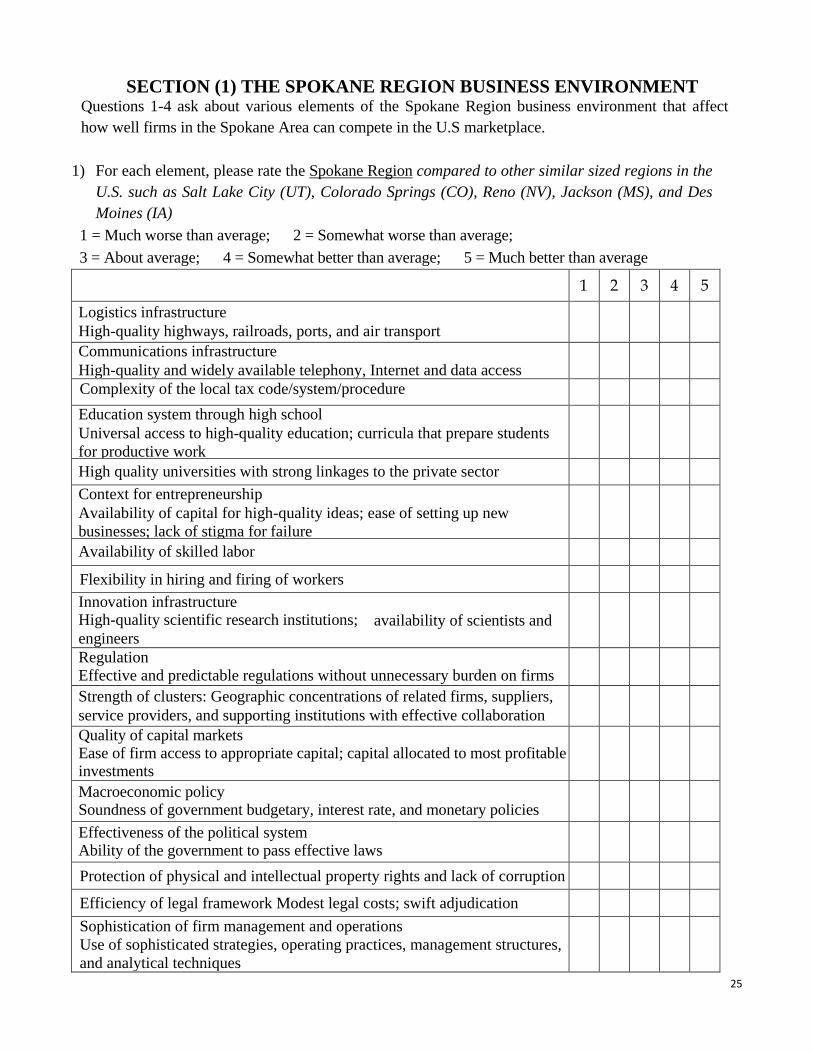

SECTION (1) THE SPOKANE REGION BUSINESS ENVIRONMENT Questions 1-4 ask about various elements of the Spokane Region business environment that affect

how well firms in the Spokane Area can compete in the U.S marketplace.

1) For each element, please rate the Spokane Region compared to other similar sized regions in the

U.S. such as Salt Lake City (UT), Colorado Springs (CO), Reno (NV), Jackson (MS), and Des

Moines (IA)

1 = Much worse than average; 2 = Somewhat worse than average;

3 = About average; 4 = Somewhat better than average; 5 = Much better than average

1 2 3 4 5

Logistics infrastructure

High-quality highways, railroads, ports, and air transport

Communications infrastructure

High-quality and widely available telephony, Internet and data access

Complexity of the local tax code/system/procedure

Education system through high school

Universal access to high-quality education; curricula that prepare students

for productive work

High quality universities with strong linkages to the private sector

Context for entrepreneurship

Availability of capital for high-quality ideas; ease of setting up new

businesses; lack of stigma for failure

Availability of skilled labor

Flexibility in hiring and firing of workers

Innovation infrastructure High-quality scientific research institutions; availability of scientists and engineers

Regulation Effective and predictable regulations without unnecessary burden on firms

Strength of clusters: Geographic concentrations of related firms, suppliers,

service providers, and supporting institutions with effective collaboration

Quality of capital markets Ease of firm access to appropriate capital; capital allocated to most profitable investments

Macroeconomic policy Soundness of government budgetary, interest rate, and monetary policies

Effectiveness of the political system Ability of the government to pass effective laws

Protection of physical and intellectual property rights and lack of corruption

Efficiency of legal framework Modest legal costs; swift adjudication

Sophistication of firm management and operations

Use of sophisticated strategies, operating practices, management structures,

and analytical techniques

26

2) Compared to other similar sized regions, would you say that the Spokane Region business

environment, overall, is…

A. Much worse than average

B. Somewhat worse than average

C. About average

D. Somewhat better than average

E. Much better than average

3) Over time, is each element of the Spokane Region business environment falling behind, keeping pace

with, or pulling ahead of the same element in similar sized regions?

1 = Falling behind; 2 = Keeping pace; 3 = Pulling ahead

1 2 3

Logistics infrastructure

High-quality highways, railroads, ports, and air transport

Communications infrastructure

High-quality and widely available telephony, Internet and data access

Complexity of the local tax code/system/procedure

Education system through high school

Universal access to high-quality education; curricula that prepare students for

productive work

High quality universities with strong linkages to the private sector

Context for entrepreneurship

Availability of capital for high-quality ideas; ease of setting up new

businesses; lack of stigma for failure

Availability of skilled labor

Flexibility in hiring and firing of workers

Innovation infrastructure High-quality scientific research institutions; availability of scientists and engineers

Regulation Effective and predictable regulations without unnecessary burden on firms

Strength of clusters: Geographic concentrations of related firms, suppliers,

service providers, and supporting institutions with effective collaboration

Quality of capital markets Ease of firm access to appropriate capital; capital allocated to most profitable investments

Macroeconomic policy Soundness of government budgetary, interest rate, and monetary policies

Effectiveness of the political system Ability of the government to pass effective laws

Protection of physical and intellectual property rights and lack of corruption

Efficiency of legal framework Modest legal costs; swift adjudication

Sophistication of firm management and operations

Use of sophisticated strategies, operating practices, management structures, and

analytical techniques

24

4) Over time is the overall Spokane Region business environment falling behind, keeping pace with, or

pulling ahead of the business environments in…

Falling

behind

Keeping

pace

Pulling

ahead

Other similar sized regions in the U.S. such as Salt Lake City (UT), Colorado Springs (CO), Reno (NV), Jackson (MS), and Des

Moines (IA)

Other larger regions in the U.S. such as New York-Newark-Jersey City, and Seattle-Tacoma (WA)

Other smaller regions in the U.S. such as Waco (TX), Bellingham (WA), Santa Cruz (CA)

SECTION (2) SPOKANE REGION FIRM’S PERFORMANCE The next set of questions (5-8) asks about the performance of firms from the Spokane Region.

5) Think about firms operating in the Spokane Region. Overall, how successful are these firms at

competing in the U.S. marketplace against firms operating in other similar sized regions in the U.S.

such as Salt Lake City (UT), Colorado Springs (CO), Reno (NV), Jackson (MS), and Des Moines

(IA)?

A. Not at all successful

B. Not very successful

C. Somewhat successful D. Very successful

E. Extremely successful

6) Three years from now, do you expect the ability of firms operating in the Spokane Region to

compete successfully against firms from similar sized regions in the U.S. to be…

A. Much worse than today

B. Somewhat worse

C. The same

D. Somewhat better

E. Much better than today

7) Three years from now, do you expect firms operating in the Spokane Region to be…

A. Much less able to support high wages and benefits

B. Somewhat less able to support high wages and benefits

C. Neither less nor more able to support high wages and benefits

D. Somewhat more able to support high wages and benefits

E. Much more able to support high wages and benefits

8) Can your firm’s Spokane Region operations compete successfully in the U.S. marketplace and

maintain current employment levels…

A. While supporting rising wages and benefits for an average employee

B. While supporting stable wages and benefits

C. Only with declining wages and benefits for an average employee

D. Your firm does not compete in the whole U.S. marketplace

25

SECTION (3) ACTIONS OF FIRMS

The next two questions ask about actions your firm is taking or might take in the future. 9) To the best of your knowledge, does your firm or organization currently take any of the following

actions in its Spokane Region based operations?

Yes No

Not

Appli-

cable

Don’t

know

Participate in initiatives to improve the competitiveness

of regional clusters in which your firm operates

Clusters are geographic concentrations of related firms,

suppliers, service providers, and supporting institutions

with effective collaboration

Participate in initiatives to improve the general business

environment in your firm’s region

Conduct internal training programs for current or

prospective employees to upgrade their skills and

productivity

Offer a formal apprenticeship program that trains

workers to be more employable by your firm and others

Partner with a community college, technical school, or

university to offer programs aligned with the needs of

your business, and commit your firm to hire a number of

its graduates

Actively strive to identify and increase sourcing from

local suppliers

Mentor local suppliers to upgrade their capabilities and

make them more attractive partners

Participate in research collaboratives in your firm’s field

that build technologies and products of the future

Invest in or incubate promising startups related to your

business

Move to the Spokane Region a business activity that is

currently performed elsewhere and can be performed

productively in the Spokane Region

Advocate for laws and rules that benefit business as a

whole rather than lobby for the special interests of your

firm or industry

26

10) Among the actions your firm does not currently take, would your firm be interested in undertaking

each of the following in its Spokane Region operations?

1 = Definitely not interested; 2 = Probably not interested; 3 = May or may not be interested

4 = Probably interested; 5 = Definitely interested; 6= Not applicable.

1

2

3

4

5

NA

Join or establish initiatives to improve the competitiveness of regional clusters in which your firm operates Clusters are geographic concentrations of related firms, suppliers, service providers, and supporting institutions with collaboration

Join or establish initiatives to improve the general business environment in your firm’s region.

Establish an internal program for current or prospective employees to upgrade their skills and productivity.

Create an apprenticeship program that trains Spokane Region workers to be more employable by your firm and others.

Enter into a partnership with a community college, technical school, or university to offer programs aligned with the needs of your business, and commit your firm to hire a number of its graduates.

Identify and increase sourcing from local suppliers.

Mentor local suppliers to upgrade their capabilities and make them more attractive partners.

Join or establish research collaboratives in your firm’s field that build technologies and products of the future.

Invest in or incubate promising startups related to your business.

Move to the Spokane Region a business activity that is currently performed elsewhere and can be performed productively in the Spokane Region.

Invest in or incubate promising startups related to your business.

Advocate for laws and rules that benefit business as a whole rather than lobby for the special interests of your firm or industry.

27

SECTION (4) YOUR FIRM’s INFORMATION

Questions 11-17 request information about your firm.

11) What is the size of your firm?

A. 0-20 employees B. 21-50 employees C. 51-100 employees D. 101-200 employees

E. 201-500 employees F. 501-1000 employees G >1000 employees

12) What is your current job title? ____________________________________________

13) Does your firm have any business activities outside the Spokane Region?

A. Yes B. No

14) Is your firm exposed to international competition?

A. Yes B. No

15) Does your firm do any international business?

A. Yes B. No

16) Are you employed by a…

A. Private sector, for-profit organization

B. Nonprofit organization C. Public sector or government organization

17) In what sector do you work?

Insurance Construction Accommodation and

Food Services

Financial Services

Real Estate

Health Care and Social

Assistance

Accounting

Wholesale and Retail Trade

Arts, Entertainment,

and Recreation

Professional Services Manufacturing: Food and

Beverage

Transportation and

Logistics

Scientific Services Manufacturing: Textile and

Apparel

Mining and Oil & Gas

Extraction

Technical Services Manufacturing: Wood,

Paper, and Printing Utilities

Media: Broadcast, Film,

and Multimedia

Manufacturing: Petroleum,

Chemicals, and Plastics

Agriculture, Forestry,

and Fishing

Media: Print and

Publishing

Manufacturing: Metal and

Machinery Educational Services

Telecommunications

Manufacturing: Computer,

Electrical, and Appliance Other Services

Data Processing Other Manufacturing Public Administration

THANK YOU FOR YOUR PARTICIPATION