Datamonitor is a leading business information company specializing in industry analysis.

Through its proprietary databases and wealth of expertise, Datamonitor provides clients with unbiased expert analysis and in depth forecasts for six industry sectors: Healthcare, Technology, Automotive, Energy, Consumer Markets, and Financial Services.

The company also advises clients on the impact that new technology and eCommerce will have on their businesses. Datamonitor maintains its headquarters in London, and regional offices in New York, Frankfurt, and Hong Kong. The company serves the world’s largest 5000 companies.

Datamonitor's premium reports are based on primary research with industry panels and consumers. We gather information on market segmentation, market growth and pricing, competitors and products. Our experts then interpret this data to produce detailed forecasts and actionable recommendations, helping you create new business opportunities and ideas.

Our series of company, industry and country profiles complements our premium products, providing top-level information on 10,000 companies, 2,500 industries and 50 countries. While they do not contain the highly detailed breakdowns found in premium reports, profiles give you the most important qualitative and quantitative summary information you need - including predictions and forecasts.

The sports equipment market consists of equipment for ball sports (baseball, softball, basketball, soccer, football, volleyball, cricket, hockey, etc), adventure sports (camping, hunting and firearms, skin diving and scuba, water ski-ing, surfboarding and sailboarding, etc), fitness (exercise bikes, home gym, rowing machine, hand/wrist/ankle weights, treadmill, jump rope, stepper), golf (clubs, bags, balls, gloves, carts, etc), racket sports (tennis, squash, badminton, etc), winter sports (downhill and cross-country ski-ing, snowboarding, etc), and other sports such as archery, billiards, indoor games, bowling, in-line skating, martial arts, wheel sports, pogo sticks, and fishing equipment. Market values are calculated at retail selling price (RSP). Any currency conversions used in the creation of this report have been calculated using constant annual average 2008 exchange rates.

For the purpose of this report Europe is deemed to comprise of Belgium, the Czech Republic, Denmark, France, Germany, Hungary, Italy, Netherlands, Norway, Poland, Romania, Russia, Spain, Sweden, the Ukraine and the United Kingdom.

1.2 Research Highlights

The French sports equipment market generated total revenues of $4.4 billion in 2008, representing a compound annual growth rate (CAGR) of 1.1% for the period spanning 2004-2008.

The clothing, footwear, sportswear and accessories retailers segment was the market's most lucrative in 2008, generating total revenues of $360.7 million, equivalent to 8.2% of the market's overall value.

The performance of the market is forecast to decelerate, with an anticipated CAGR of 0.9% for the five-year period 2008-2013, which is expected to drive the market to a value of $4.6 billion by the end of 2013.

The French sports equipment market has grown at a fairly steady rate in recent years. Slower growth is expected over the forecast period through to 2013.

The French sports equipment market generated total revenues of $4.4 billion in 2008, representing a compound annual growth rate (CAGR) of 1.1% for the period spanning 2004-2008. In comparison, the German and UK markets grew with CAGRs of 1.2% and 2.4% respectively, over the same period, to reach respective values of $3.3 billion and $4.6 billion in 2008.

The clothing, footwear, sportswear and accessories retailers segment was the market's most lucrative in 2008, generating total revenues of $360.7 million, equivalent to 8.2% of the market's overall value. The hypermarket, supermarket, and discounters segment contributed revenues of $328.7 million in 2008, equating to 7.5% of the market's aggregate revenues.

The performance of the market is forecast to decelerate, with an anticipated CAGR of 0.9% for the five-year period 2008-2013, which is expected to drive the market to a value of $4.6 billion by the end of 2013. Comparatively, the German and UK markets will grow with CAGRs of 1.2% and 3.3% respectively, over the same period, to reach respective values of $3.5 billion and $5.4 billion in 2013.

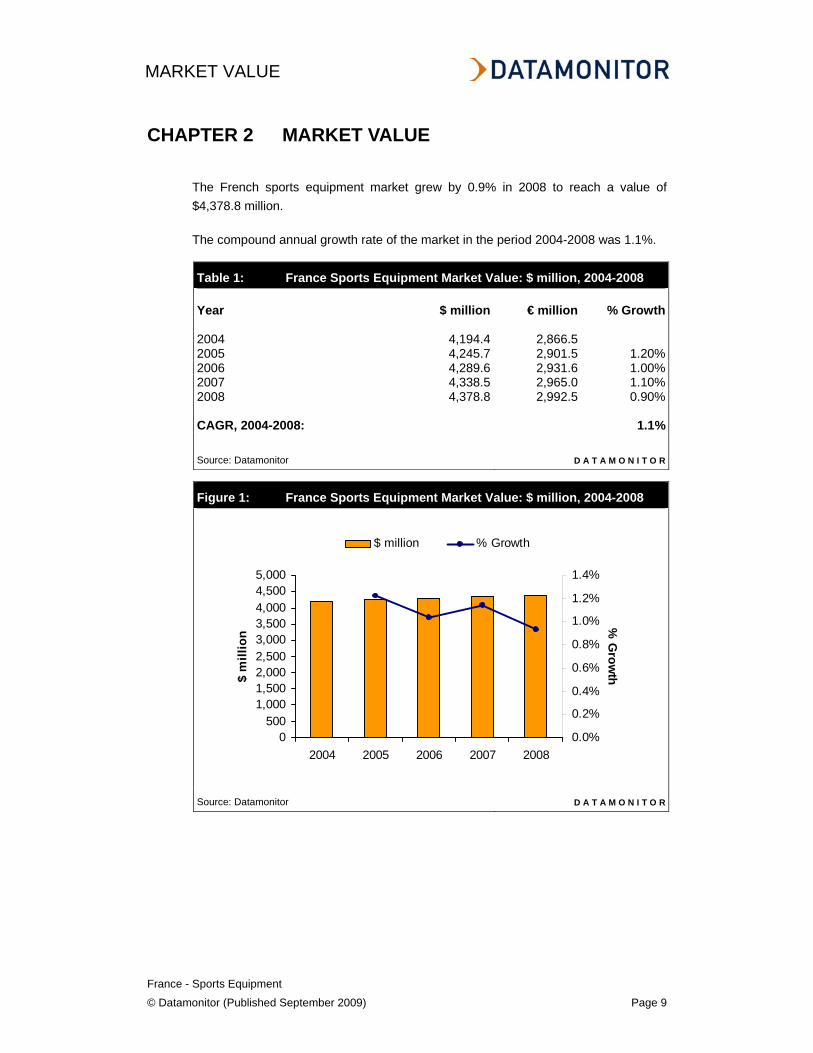

The French sports equipment market grew by 0.9% in 2008 to reach a value of $4,378.8 million.

The compound annual growth rate of the market in the period 2004-2008 was 1.1%.

Table 1: France Sports Equipment Market Value: $ million, 2004-2008 Year $ million € million % Growth 2004 4,194.4 2,866.5 2005 4,245.7 2,901.5 1.20%2006 4,289.6 2,931.6 1.00%2007 4,338.5 2,965.0 1.10%2008 4,378.8 2,992.5 0.90% CAGR, 2004-2008: 1.1% Source: Datamonitor D A T A M O N I T O R

Figure 1: France Sports Equipment Market Value: $ million, 2004-2008

The clothing, footwear, sportswear and accessories retailers segment generated 8.2% of the French sports equipment market's overall revenues.

The hypermarket, supermarket, and discounters segment generated 7.5% of the market's aggregate revenues.

Table 2: France Sports Equipment Market Segmentation I: % Share, by Value, 2008

Category % Share Other Specialists 76.40% Clothing, Footwear, Sportswear and Accessories Retailers 8.20% Hypermarket, Supermarket, and Discounters 7.50% Discount, Variety Store, and General Merchandise Retailers 5.80% Department Stores 1.70% Cash and Carries and Warehouse Clubs 0.40% Total 100.0% Source: Datamonitor D A T A M O N I T O R

Figure 2: France Sports Equipment Market Segmentation I: % Share, by Value, 2008

France accounts for 20.7% of the European sports equipment market's value.

In comparison, the United Kingdom accounts for a further 21.5% of the regional market's value.

Table 3: France Sports Equipment Market Segmentation II: % Share, by Value, 2008

Geography % Share Rest of Europe 24.60%United Kingdom 21.50%France 20.70%Germany 15.50%Italy 10.90%Spain 6.80% Total 100.0% Source: Datamonitor D A T A M O N I T O R

Figure 3: France Sports Equipment Market Segmentation II: % Share, by Value, 2008

The sports equipment market will be analyzed taking sports equipment retailers as players. The key buyers will be taken as individual consumers, and sports equipment manufacturers as the key suppliers.

5.1 Summary

Figure 4: Forces Driving Competition in the Sports Equipment Market in France, 2008

0

1

2

3

4

5Buyer Pow er

Supplier Pow er

New EntrantsThreat of Substitutes

Degree of Rivalry

Score for each force is mean of scores for its drivers. Total area & color indicates intensity of competition overall. Source: Datamonitor D A T A M O N I T O R

The French market for sports equipment is fragmented despite the presence of some larger players. The wide range of products available, the existence of a large number of retailers and the fact that some large sports equipment companies have integrated forwards into retail all mean that buyer power is prevented from becoming disproportionately strong in this market.

The manufacture of sports equipment offers few economies of scale and it is therefore possible to enter the market on a modest scale by producing, for example, small quantities of custom-made golf clubs, although uninspiring revenue growth in recent years makes entering this market a less attractive prospect for newcomers. Many companies in this market also manufacture sports apparel and footwear, which reduces their reliance on sales of sports equipment and rivalry, is weakened further by the policy of many large corporations to outsource manufacturing.

Figure 5: Drivers of Buyer Power in the Sports Equipment Market in France, 2008

01

23

4

5Buyer size

Oligopsony threat

Low -cost sw itching

Undifferentiated product

Tendency to sw itch

Price sensitivity

Financial muscle

Backw ards integration

Buyer independence

Product dispensability

Scores: 1= weak driver...5=strong driver Source: Datamonitor D A T A M O N I T O R

The French sports equipment market will be analyzed by considering manufacturers of sports equipment as players with retailers as buyers, since these constitute the predominant distribution channel for sports equipment. The sports equipment market may be characterized by three main themes: research & development, innovation and adoption of new materials.

Previously distinct lines between sportswear and casual wear are becoming increasingly blurred. Although the focus of this report is on sporting equipment and not garments the markets cross over potential cannot be denied. Fast expanding sectors, like snowboard, mountain bike and cycling, are rather atomized and innovate much more on new product and materials.

In areas such as these equipment and lifestyle go hand in hand, given the developing nature of extreme/adrenaline sports the potential for growth cannot be ignored. This leads to the potential for equipment products to be stocked alongside sports garments in populist retail outlets such as super/hypermarkets. In most countries, these retailers include multiples such as The Sports Authority and JJB Sports; numerous independents; club stores; department stores and e-commerce operations.

Department stores and hypermarkets are also important as these have the space to stock and display large pieces of equipment such as home gyms. Switching costs are low for buyers, which strengthens buyer power. Manufacturers of sports equipment can differentiate their products strongly, not only by the overall function (tennis racket or golf club, for example) but also by design, target market, technological innovation, and so on.

Some sports equipment companies, such as Nike, have integrated forwards into selling directly to the consumer through company-owned retail outlets and a number of smaller companies take advantage of the internet to sell directly to consumers via company websites. Both of these strategies diminish sports equipment manufacturers’ reliance on third-party retailers, thereby weakening buyer power. Buyer power is therefore assessed as moderate overall.

Figure 6: Drivers of Supplier Power in the Sports Equipment Market in France, 2008

012345

Supplier size

Oligopoly threat

Sw itching costs

Player independence

Player dispensabilityNo substitute inputs

Importance of quality/cost

Differentiated input

Forw ard integration

Scores: 1= weak driver...5=strong driver Source: Datamonitor D A T A M O N I T O R

The main raw materials used in the production of sports equipment are steel, various plastic products, resins, carbon fibre, rubber and leather. The production of some inputs, such as plastics, is by nature a large-scale operation and relatively few companies may be able to supply a specific grade of material. It is rare for sports equipment companies to integrate backwards into the production of raw material, which also strengthens supplier power.

Suppliers are not usually solely dependent on sports equipment companies for their revenues and can often find alternative markets. Carbon fibre, for example, is increasingly being used by the aviation industry to create a new generation of lighter, more fuel-efficient planes, and is also growing in popularity among manufacturers of military aircraft. Consequently, the price of this commodity has roughly doubled since 2003: a situation over which sports equipment companies have little control. Steel, too, has a variety of industrial applications aside from the production of sports equipment.

Raw material quality can be highly important in this business: end products such as professional golf clubs are strongly influenced by the nature of the inputs used in their production. However, forward integration among raw material suppliers into the production of sports equipment is highly unlikely as they often operate in distinctly different businesses.

The suppliers of some of the aforementioned inputs, such as rubber, include small factories and operate in a fragmented up-stream landscape, which also weakens supplier power. Outsourcing is a prominent feature of this market. Large corporations such as Nike often design their products in places like the US and then sub-contract manufacturers in countries like South Korea, India, China and Indonesia for the actual production of the goods.

A significant proportion of Adidas products, for example, are produced at outsourced manufacturing locations around the world. The large number of relatively low-cost factory options available to these large corporations combined with the financial muscle of these sports equipment companies considerably weakens the power held by these suppliers. Overall, supplier power is assessed as moderate.

Figure 7: Factors Influencing the Likelihood of New Entrants in the Sports Equipment Market in France, 2008

012345

Low -cost sw itching

Undifferentiated product

Scale unimportant

Low fixed costs

Little regulation

Incumbents acquiescentDistribution accessible

Suppliers accessible

Little IP involved

Weak brands

Market grow th

Scores: 1= weak driver...5=strong driver Source: Datamonitor D A T A M O N I T O R

Entry to the French sports equipment market may be achieved by starting up a new company or by diversifying an existing company's operations into the manufacture of sports equipment. Although some brands of sports equipment are used across more than one sport (e.g. Slazenger, Wilson, Head), a considerable proportion is produced by specialists. As a consequence of this, it is possible to enter this market on a small scale without the need to invest in large production plants. Custom-made sports equipment, a good example of this is Balabushka pool cues. George Balabushka developed, made and sold his own pool cues at higher prices than any initial investment in raw materials, production equipment, etc and recouped by adding a good margin to the price of the end-product due to the quality care are sort-after nature of his creations, many innovations of his are now industry standard.

However, there is a degree of proprietary knowledge within the industry, with many sports equipment companies closely guarding detailed information concerning new products designs. Depending on the type of equipment in question, companies wishing to enter this market must also take account of the regulations imposed by the ruling professional sporting body. The International Tennis Federation stipulates, amongst other things, that tennis rackets must not exceed 29 in (74 cm) in length. Similarly, the rules of golf in Europe, including golf club regulations, are established by the R&A of St Andrews in Scotland. An additional entry barrier is the need to access good distribution channels.

Although some large sports equipment companies may be able to open their own retail outlets, this strategy often proves too costly for smaller manufactures. This means that the latter must persuade hypermarkets, specialist stores and other businesses to stock their products. Market revenue growth over recent years has been unexciting, which also makes the market less attractive to new companies. Overall, there is a moderate likelihood of new entrants.

Figure 8: Factors Influencing the Threat of Substitutes in the Sports Equipment Market in France, 2008

012345

Low -cost sw itching

Cheap alternativeBeneficial alternative

Scores: 1= weak driver...5=strong driver Source: Datamonitor D A T A M O N I T O R

Substitutes to sports equipment may include any products purchased for the purpose of enhancing/passing leisure time as generally sport is a recreational activity. This is certainly the feeling from a retailers’ point of view, who deem substitutes for sports equipment to include other leisure products such as books, board games, music and computer games.

These substitutes pose little threat to specialist equipment retailers, whose customers usually visit the store with the express purpose of buying sports equipment. However, in the case of department stores, which need to offer a wide range of both sports equipment and other leisure items in order to meet consumer demand, the threat presented by these substitutes is much greater. The threat from substitutes is therefore assessed as strong overall.

Figure 9: Drivers of Degree of Rivalry in the Sports Equipment Market in France, 2008

012345

Competitor size

Number of players

Low -cost sw itching

Undifferentiated product

Low fixed costs

Easy to expandHard to exit

Lack of diversity

Similarity of players

Storage costs

Zero-sum game?

Scores: 1= weak driver...5=strong driver Source: Datamonitor D A T A M O N I T O R

The French market for sports equipment is fairly fragmented and is served by a diverse range of specialist companies in addition to large multi-nationals like Adidas. It is possible to differentiate these products very effectively and some manufacturers of sports equipment have developed strong brands. Players in the sports equipment market are often less reliant on mass-marketed goods than manufacturers in many other consumer product markets, which tends to weaken rivalry.

A number of companies in this market also manufacture sports apparel, footwear and other sports accessories. These products often represent a significant segment of manufacturers’ revenues, which makes them less reliant on the sports equipment market and also decreases rivalry somewhat. Large corporations’ strategy of outsourcing sports equipment manufacture means that they have relatively low fixed costs and little invested in the physical plants. Retaliation by existing players, such as the launch of a price war, is a possibility, especially where a new entrant moves into a more concentrated segment. The brand strength of the major chains is considerable, which may negate much of the effect of low switching costs. Leaving the industry however would, at most, entail the divesting of some lightweight fabrication equipment and these low exit costs serve to weaken rivalry in this market. However, purchasers have a fairly wide range of products to choose from, with low switching costs, and unexciting market revenue growth in recent years tends further to strengthen rivalry, which is assessed as moderate overall.

Table 4: Key Facts: Amer Sports Corporation Address: Makelankatu 91, 00610 Helsinki, FIN Telephone: 358 9 7257 800 Fax: 358 9 7257 8200 Website: www.amersports.com Financial Year-End: December Ticker: AMEAS Stock Exchange: Taiwan Source: Company Website D A T A M O N I T O R

Amer Sports Corporation (Amer Sports) is a Finland based company that develops, manufactures and sells sports equipment. The company and its subsidiaries operate in 34 countries and their primary markets are the US and Europe.

Amer Sports operates through three business segments: winter and outdoor, ball sports, and fitness.

Amer Sports, through its winter and outdoor segment, offers winter sports equipment under the brand names Salomon, Atomic and Bonfire; apparel and footwear under Salomon and Arc'teryx brands;cycling systems under Mavic brand; and sports instruments under Suunto brand.

The company offers advanced equipment under the brand name Wilson through its ball sports segment. Wilson's core categories include baseball, football, basketball, softball, bats, volleyball, soccer, youth sports, apparel, golf products and footwear. It also offers tennis, racquetball, squash, badminton and platform tennis products under racquet sports category.

The fitness segment of Amer Sports offers fitness equipment for commercial and home markets under the brand name Precor. Its main products include aerobic exercise equipment, strength-training systems and entertainment systems. Precor is one the world's leading manufacturers of elliptical crosstrainers.

The company also offers sporting equipment under various brands including Cliche for skateboards; Dynamic for alpine skis; Volant for high-segment skis; Oxygen for snowboarding; DeMarini for high-performance bats; ATEC for athletic training equipment; Cardio Theater for full line exercise entertainment' systems; ClubCom for private media networks; Recta for compasses, altimeters and accessories; and Bare for diving, water sports and wading.

In addition, the company manufactures air drive computers under the brand Suunto.

Key Metrics

Amer Sports Corporation generated revenues of $2,306.1 million in the financial year ended December 2008, a decrease of 4.6% compared to the previous year. The company's net income totaled $49.8 million in fiscal 2008, an increase of 83.8% compared with 2007.

Table 5: Key Facts: Adidas AG Address: Adi Dassler Platz 1 2, 91074 Herzogenaurach, DEU Telephone: 49 9132 840 Fax: 49 9132 84 2241 Website: www.adidas-group.com Financial Year-End: December Ticker: ADS Stock Exchange: Frankfurt Source: Company Website D A T A M O N I T O R

Adidas is one of the largest companies in the sporting goods industry. The group has divided its operating activities by major brand into three divisions: Adidas, Reebok and TaylorMade-adidas Golf. The group operates through more than 150 subsidiaries in Europe, the US and Asia, each focusing on a particular market or part of the manufacturing process.

The focus of the Adidas brand is on sports. The Adidas brand offers footwear, apparel and hardware in three divisions, including sport performance, sport heritage and sport style. The sport performance division develops sports products, focused on running, football, basketball, tennis and training. The sport heritage division concentrates on sports lifestyle and casual wear. The sport style division is focused on fashion-conscious consumers and includes collections like the 'Y-3' designed by Yohji Yamamoto.

The focus of Reebok brand, meanwhile, is more on style. It offers sports, fitness and casual footwear, apparel and equipment under the Reebok brand. The TaylorMade-adidas Golf brand offers a range of golf clubs, accessories, footwear and apparel. It also includes Maxfli brand, which designs and develops golf balls.

Most of the group's products are manufactured by third party independent manufacturers. During 2007, the group sourced products from 377 independent manufacturing partners, of which 71% were located in Asia, 17% were located in Europe, and 12% in Americas.

The group undertakes research and development activities on a global scale. Research and development activities within the Adidas group are decentralized, with each brand having its own research, design and development operations across several countries. The group markets its products through an extensive distribution channel. The group has 542 concept stores, 317 factory outlets and 142 concession corners worldwide.

Adidas has concluded several endorsement contracts with several sportsmen and women. Sportsmen under contract include David Beckham (soccer), Kevin Garnett and Tim Duncan (basketball), Ian Thorpe (swimming), Maurice Greene and Haile Gebreselassie (athletics) and Sergio Garcia (golf). It also provides the team kit wear for the French football team and clubs such as Real Madrid, AC Milan, Bayern Munich and the New York Yankees.

Key Metrics

Adidas AG generated revenues of $15,801.6 million in the financial year ended December 2008, an increase of 4.9% compared to the previous year. The company's net income totaled $939.4 million in fiscal 2008, an increase of 16.5% compared with 2007.

Table 7: Key Facts: Head N V Address: Rokin 55, 1012 KK Amsterdam, NLD Telephone: 31 20 6251291 Fax: 31 20 6250956 Website: www.head.com Financial Year-End: December Ticker: HEAD Stock Exchange: Vienna Source: Company Website D A T A M O N I T O R

Head is a manufacturer and marketer of branded sports equipment. It sells its products under the Head, Penn, Tyrolia and Mares/Dacor brands. The group operates in Europe, North America and Asia. The group offers its products under four categories: winter sports, racquet sports, diving and licensing.

Head's winter sports products include alpine skis, ski boots and bindings, snowboard equipment, and protection equipment. The group's racquet sports products include tennis, squash, badminton and racquetball racquets; tennis and racquetball balls; and accessories and footwear. The group's diving products include diving equipment, wetsuits, dry suits and diving accessories.

The group grants rights to its brand for other product categories such as apparel, bags, bicycles, eyewear, footwear, gloves, golf, headwear and accessories, skates, socks, toiletries, watches, underwear, balls, and fitness equipment. In addition, Head licenses the Penn brand name to approximately 10 licensees worldwide, primarily for apparel, footwear and golf products.

The group's subsidiaries include Head Holding Unternehmensbeteiligung, HTM Sport- und Freizeitgerate, Head Sport, Head International, Head Technology, Tyrolia Technology, Head Austria, Head Canada, Head Sport, HTM Sport, HTM Bulgaria, Head France, Head Germany, Head UK, Mares, HTM Sports Japan, Head Spain, Head Switzerland, HTM USA Holdings, Head USA, Head Sports, Penn Racquet Sports, Mares Asia Pacific, Power Ahead Holding, and Head Sports (Hui Zhou), among others.

Key Metrics

Head N V generated revenues of $491.2 million in the financial year ended December 2008, an increase of 4.6% compared to the previous year. The company reported a net loss of $14.2 million in fiscal 2008 compared to a net loss of $16.4 million the previous year.

In 2013, the French sports equipment market is forecast to have a value of $4,570 million, an increase of 4.4% since 2008.

The compound annual growth rate of the market in the period 2008-2013 is predicted to be 0.9%.

Table 8: France Sports Equipment Market Value Forecast: $ million, 2008-2013

Year $ million € million % Growth 2008 4,378.8 2,992.5 0.90%2009 4,416.8 3,018.5 0.90%2010 4,458.8 3,047.2 1.00%2011 4,493.9 3,071.2 0.80%2012 4,529.0 3,095.2 0.80%2013 4,570.0 3,123.2 0.90% CAGR, 2008-2013: 0.9% Source: Datamonitor D A T A M O N I T O R

Figure 11: France Sports Equipment Market Value Forecast: $ million, 2008-2013

Table 9: France Size of Population (million) , 2004-2008 Year Population (million) % Growth 2004 62.62005 62.9 0.60%2006 63.3 0.60%2007 63.7 0.60%2008 64.1 0.60% Source: Datamonitor D A T A M O N I T O R

Table 10: France GDP (Constant 2000 Prices, $ billion), 2004-2008

Year Constant 2000

Prices, $ billion % Growth 2004 1414.92005 1436.1 1.50%2006 1465.1 2.00%2007 1492.9 1.90%2008 1506.4 0.90% Source: Datamonitor D A T A M O N I T O R

Table 11: France Inflation, 2004-2008 Year Inflation Rate (%) % Growth 2004 2.12005 1.8 -17.00%2006 1.7 -4.80%2007 1.5 -11.50%2008 3.3 122.00% Source: Datamonitor D A T A M O N I T O R

Table 12: France Exchange Rate, 2004-2008 Year Exchange Rate ($/€) 2004 1.242082005 1.242962006 1.254662007 1.369862008 1.46325 Source: Datamonitor D A T A M O N I T O R

Datamonitor Industry Profiles draw on extensive primary and secondary research, all aggregated, analyzed, and cross-checked and presented in a consistent and accessible style.

Review of in-house databases – Created using 250,000+ industry interviews and consumer surveys and supported by analysis from industry experts using highly complex modeling & forecasting tools, Datamonitor’s in-house databases provide the foundation for all related industry profiles

Preparatory research – We also maintain extensive in-house databases of news, analyst commentary, company profiles and macroeconomic & demographic information, which enable our researchers to build an accurate market overview

Definitions – Market definitions are standardized to allow comparison from country to country. The parameters of each definition are carefully reviewed at the start of the research process to ensure they match the requirements of both the market and our clients

Extensive secondary research activities ensure we are always fully up-to-date with the latest industry events and trends

Datamonitor aggregates and analyzes a number of secondary information sources, including:

- National/Governmental statistics - International data (official international sources) - National and International trade associations - Broker and analyst reports - Company Annual Reports - Business information libraries and databases

Modeling & forecasting tools – Datamonitor has developed powerful tools that allow quantitative and qualitative data to be combined with related macroeconomic and demographic drivers to create market models and forecasts, which can then be refined according to specific competitive, regulatory and demand-related factors

Continuous quality control ensures that our processes and profiles remain focused, accurate and up-to-date

FPS (Fédération Professionnelle des Entreprises du Sport et des Loisirs) 124 Haussmann, 75008, Paris Tel: 33 1 44 70 77 90 Fax: 33 1 44 70 77 91 www.filieresport.com/