Teacher Name: Stacy Jackson District: _____Randolph ______________________ Class / Subject / Grade: Personal Finance / Business Ed / 11-12 Unit Topic: Investments – Researching different investment options – stocks, bonds, mutual funds, real estate, IRA’s Allocation of Time: 4 days (47-minute class periods) Using Technology with Classroom Instruction That Works skills to be taught and level of proficiency: (double-click in box to ‘check’ it): Identifying Similarities and Differences Summarizing and Note-Taking Non-Linguistic Representation Setting Objectives and Providing Feedback Questions, Cues, and Advance Organizers List Technology Tools used to support the teaching of the above selected “Using Technology with Classroom Instruction that Works” strategies and describe how it will support the strategies: Internet – use reliable online sources to research assigned investment option, Prezi (online presentation software – www.prezi.com ) – used to create a group presentation about an investment tool to present to their classmates. ITLS Standards with grade-level benchmarks OR NETS for Students and level of proficiency: (at least two) (Example: Standard A.8.5: Students will use a graphic organizer program to create a Venn Diagram to compare to stories. Proficiency: 100% accuracy.) A.12.2 Identify and use common media formats A.12.4 Use a computer and communications software to access and transmit information A.12.5: Use media and technology to create and present information B.12.2 Develop information-seeking strategies B.12.5 Record and organize information B.12.6 Interpret and use information to solve the problem or answer the question B.12.7: Communicate the results of research and inquiry in an appropriate format D.12.1: Participate productively in workgroups or other collaborative learning environments

Transcript

Teacher Name: Stacy Jackson District: _____Randolph______________________ Class / Subject / Grade: Personal Finance / Business Ed / 11-12 Unit Topic: Investments – Researching different investment options – stocks, bonds, mutual funds, real estate, IRA’s

Allocation of Time: 4 days (47-minute class periods)

Using Technology with Classroom Instruction That Works skills to be taught and level of proficiency: (double-click in box to ‘check’ it):

Identifying Similarities and Differences Summarizing and Note-Taking

Non-Linguistic Representation Setting Objectives and Providing Feedback

Questions, Cues, and Advance Organizers

List Technology Tools used to support the teaching of the above selected “Using Technology with Classroom Instruction that Works” strategies and describe how it will support the strategies: Internet – use reliable online sources to research assigned investment option, Prezi (online presentation software – www.prezi.com) – used to create a group presentation about an investment tool to present to their classmates. ITLS Standards with grade-level benchmarks OR NETS for Students and level of proficiency: (at least two)

(Example: Standard A.8.5: Students will use a graphic organizer program to create a Venn Diagram to compare to stories. Proficiency: 100% accuracy.)

A.12.2 Identify and use common media formats A.12.4 Use a computer and communications software to access and transmit information A.12.5: Use media and technology to create and present information B.12.2 Develop information-seeking strategies B.12.5 Record and organize information B.12.6 Interpret and use information to solve the problem or answer the question B.12.7: Communicate the results of research and inquiry in an appropriate format D.12.1: Participate productively in workgroups or other collaborative learning environments

Curriculum Content and/or Performance Standards: (at least two) D.12.1.3 Identify and assess various means of building wealth.

D.12.3.1 Understand the role of revenue-generating assets in building wealth (e.g., rental property, small business, etc.).

D.12.3.4 Compare the risk, return, and liquidity of various investment alternatives. Learning Objectives: What students will learn… Students will understand different options in investment types – stocks, bonds, mutual funds, real estate, and IRA’s. Students will understand the characteristics of different investment options. Students will understand the relationship between risk and reward with different investment options. Students will understand how to use Prezi to present their assigned investment option to their classmates.

Step-by-step Unit Plan and Timeline: Activities that will be used to develop understandings… (Please provide enough details that another teacher could ‘pick-up and teach’ the unit.)

1. Notes and discussion on similarities and differences in saving and investing. 2. Students complete self-test of their own risk tolerance level. 3. Discussion regarding how risk relates to reward in saving and investing. 4. Family Economics & Financial Education – Savings Advanced presentation and activities – students complete Savings Advanced

Worksheet. 5. Investment articles from Brass student magazine given to student groups. 6. In the computer lab show students (using a projection of the teacher’s screen) how to create a presentation using Prezi (www.prezi.com).

Topics covered – inserting/formatting text, inserting/formatting pictures, inserting video from youtube, creating brackets to group objects, creating a path to present in a particular order.

Assessments**: Formative and summative assessments that will measure understanding of each learning objective and/or activity… ** Include descriptions or attach copies of all assessment instruments. Formative – Assessment 3-3 (NEFE), Savings Advanced Worksheet (FEFE) Summative – Prezi group presentation, Saving and Investing Test

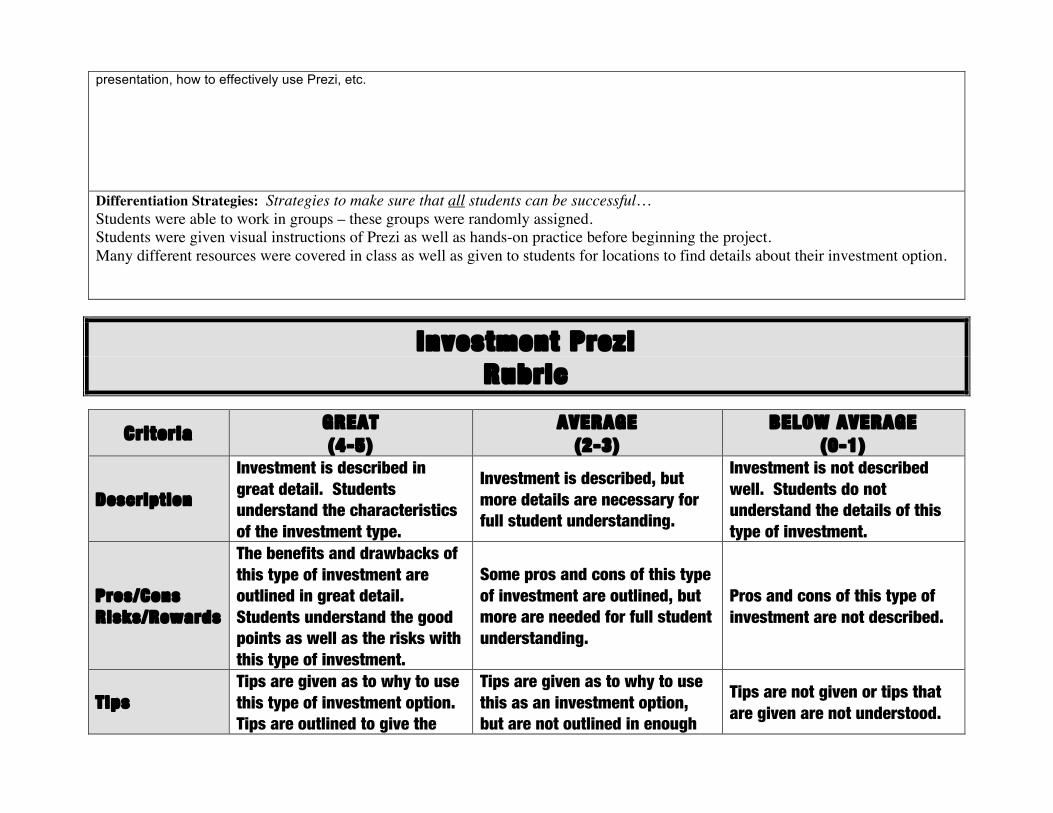

Resources & Technology Tools**: Resources that will be used to develop understanding… ** List resources and attach copies of any handouts created for the unit. Students were given a rubric to aid in creation of their Prezi. We went through many activities comparing savings and investment options – from Family Economics & Financial Education (FEFE) and National Endowment for Financial Education (NEFE). Students were given investment articles from Brass magazine relating to their assigned investment option. The beginning of one class period was spent covering basic concepts in Prezi – inserting text, pictures, and video, formatting the flow of the

presentation, how to effectively use Prezi, etc.

Differentiation Strategies: Strategies to make sure that all students can be successful… Students were able to work in groups – these groups were randomly assigned. Students were given visual instructions of Prezi as well as hands-on practice before beginning the project. Many different resources were covered in class as well as given to students for locations to find details about their investment option.

Investment Prezi Rubric

Criteria GREAT (4-5)

AVERAGE (2-3)

BELOW AVERAGE (0-1)

Description

Investment is described in great detail. Students understand the characteristics of the investment type.

Investment is described, but more details are necessary for full student understanding.

Investment is not described well. Students do not understand the details of this type of investment.

Pros/Cons Risks/Rewards

The benefits and drawbacks of this type of investment are outlined in great detail. Students understand the good points as well as the risks with this type of investment.

Some pros and cons of this type of investment are outlined, but more are needed for full student understanding.

Pros and cons of this type of investment are not described.

Tips Tips are given as to why to use this type of investment option. Tips are outlined to give the

Tips are given as to why to use this as an investment option, but are not outlined in enough

Tips are not given or tips that are given are not understood.

students a full understanding of why someone would choose this as their investment option.

detail. Students cannot get a full grasp as to why people choose this as an investment option.

Text and Pictures

Text is not written in long paragraphs. Short points of text are used and expanded on verbally. Pictures are used successfully to enhance the presentation.

Some long paragraphs/sentences are used in the presentation. Pictures are present, but could be used more successfully to enhance the presentation.

Text is written in long paragraphs. Pictures are not used at all or are not used in a means of enhancing the presentation.

Path

The path created by the students is appropriately done. The information flows in a way that makes sense.

A path is created, but is not done in a way that enhances the flow of the presentation.

No path is created or the path is not successfully created.

GREAT (8-10)

AVERAGE (3-7)

BELOW AVERAGE (0-2)

Presentation

All group members participate in the presentation. Students expand on the concepts in the prezi verbally. Text is not simply read from the screen.

All group members do not share the responsibility of presenting their investment. Some text is read rather than expanded on.

All group members do not participate and text is simply read from the screen – no expansion of concepts.

The Fed, Savings & Investing Test Name_______________________________ 100 pts. In the space provided, write the letter of the savings or investment method the statement represents (each can be used more than once):

a. Bonds b. Certificate of Deposit c. Keogh plan d. Money-market account

e. Mutual funds f. Real estate g. Savings account h. Stocks

1. _____ Penalty is usually charged if money is withdrawn before expiration date. 2. _____ A combination of a checking and savings account. Interest rates, which are based on a

complex structure, vary with the size of your balance. 3. _____ A retirement plan for the self-employed. 4. _____ Professionally managed portfolios made up of stocks, bonds, and other investments. 5. _____ Issuer agrees to pay investors a fixed interest rate for a fixed period of time. 6. _____ Transactions are recorded in a book to keep track of balance. 7. _____ You can only write a limited number of checks each month. 8. _____ Bank pays a fixed amount of interest, on a fixed amount of money, for a fixed amount of

time. 9. _____ This type of investment offers an excellent protection against inflation. 10. _____ You can contribute each year to this tax-deferred account 11. _____ Common type of account where monthly statements are sent to depositor. 12. _____ A way to own a part of a company and share in its profits.

Calculations

13. How long would it take to double your money in an account that paid 8% per year? Show your work. (2 pts.)

14. What interest rate would double your money in 5 years? Show your work. (2 pts.)

15. Alex has $100 to put away. How long will it take him to turn that investment into $200 if he can earn 6% interest? Show your work. (2 pts.)

16. Harold is 18 years old and he needs to double his $10,000 investment. He’s currently earning 4% interest. How old will he be when he has $20,000? Show your work. (2 pts.)

17. Using simple interest rate calculations, how much interest would you earn on $100.00 put in a

savings account for 3 years at 6% interest? Show your work. (2 pts.)

18. Using compound interest rate calculations, how much interest would you earn on $100.00 put in a savings account for 3 years at 6% interest—interest is compounded annually? Show your work. (2 pts.)

19. Using simple interest rate calculations, how much would you have at the end of 4 years if you put $500 in a savings account that earned 4.25% interest? Show your work. (2 pts.)

20. Using compound interest rate calculations (compounded annually), how much would you have at the end of 4 years if you put $500 in a savings account that earned 4.25% interest? Show your work. (2 pts.)

Short Answer

21. What are two factors that determine what type of savings account you should choose? (Not which financial institution – which savings account) (2 pts.)

22. What are two differences between saving and investing? Describe each. (4 pts.)

23. What does it mean that a bank is FDIC Insured? What does this means in terms of per institution per depositor? (2 pts.)

24. What is one positive and one negative aspect of a money market account? (2 pts.)

25. What are two reasons why people should save? (2 pts.)

26. What are two reasons why people don’t save? (2 pts.) 27. Explain why it is beneficial to start saving at a young age? What key concept applies to this

theory? (2 pts.)

28. Why was the Federal Reserve Act established? What did it establish? (2 pts.)

29. What are 2 of the primary functions of the Federal Reserve System? (2 pts.) 30. What are 2 of the primary functions of the Chicago Fed? (2 pts.)

31. Why did “bank runs” happen? What happened to help end these runs? (2 pts.)

32. With which Federal Reserve Bank do financial institutions in Randolph work? (1 pt.)

33. Explain the reserve requirement that required of banks. Why is this rule set in place? (2 pts.)

34. What are 2 ways that real estate can be used as an investment tool? (2 pts.)

35. Why does a CD usually offer a higher interest rate than that of a savings account? (2 pts.)

36. Explain the concept of liquidity. What is something that is very liquid and why compared to something that is not and why? Think in financial terms. (3 pts.)

37. What is the difference between inflation and recession? Explain each. (2 pts.)

38. What are two items that must be disclosed by financial institutions according to the Truth in Savings Act? (2 pts.)

39. Rank the following cash management tools in terms of liquidity (5 pts.) a. Certificate of Deposit b. Money Market Account c. Checking Account d. Savings bond e. Savings Account

40. What were two tips given in the video “Katrina’s Classroom: Financial Lessons from a Hurricane” on how to be wise with finances in times of disaster? (2 pts.)

41. What is something you learned on the trip to Chicago? (1 pt.)

42. What is one thing you will do to start preparing for your future – financially-speaking? (1 pt.) True/False (each worth 1 pt)

43. _____ A certificate of deposit must be held for a set amount of time such as 6 months or a year. 44. _____ Compound interest refers to money earned from buying a tax-exempt investment. 45. _____ A share of stock represents ownership in a company. 46. _____ A mutual fund is an investment issued by a state or local government agency. 47. _____ Treasury bonds are a safer investment than real estate. 48. _____ A person’s disposable income is their income before taxes and deductions. 49. _____ A 401(k) is a savings plan that is contributed from post-taxed earnings. 50. _____ The Fed was created in 1913. 51. _____ Diversification is the reduction of investment risk by spreading your invested dollars

among several different investments. 52. _____ Because of the time value of money, beginning to save early in life will be more

beneficial than starting to save later in life. 53. _____ A corporate bond is sold by the government to help raise money for government projects

such as the upkeep of our highways. 54. _____ You can open a checking account at the Federal Reserve Bank of Chicago. 55. _____ The Truth in Savings Act requires financial institutions to disclose certain information

about savings accounts 56. _____ Settlement occurs when funds are transferred from a check writer’s account to the

depositor’s account. 57. _____ Inflation occurs when there is less money in circulation and there is decreased demand. 58. _____ The stock market is seen as a short-term investment plan. 59. _____ Corporate bonds are sold by private companies to raise money. 60. _____ The lower risk generally yields a lower return.

Multiple Choice (each worth 1 pt.)

61. _____ The lowest interest rate is usually earned on a: a. money market account b. savings account

c. certificate of deposit d. mutual fund

62. _____ The total interest earned on $100 for two years at 10 percent (compounded annually)

would be: a. $2 b. $21

c. $11 d. $20

63. _____ Based on the rule of 72, money earning 6 percent would take about ___ years to double.

a. 6 b. 8

c. 9 d. 12

64. _____ The investment with the most risk would be: a. a savings account b. U.S. Treasury bonds

c. corporate stocks d. corporate bonds

65. _____ What is the minimum deposit for a savings account?

a. the lowest interest rate available b. the minimum amount of years you must keep the account c. the amount you can withdraw from it each month d. the amount required to start a savings account

66. _____ What is the least risky way to save money?

a. Keep it in your house b. Invest it in a small company

which is just beginning

c. Deposit it in a savings account in a bank d. Invest it in a large, established company

67. _____ Why is buying stocks risky?

a. A company may fail, causing you to lose invested money

b. There is a large tax on buying stocks

c. Stocks undergo faster inflation d. To buy stocks you must invest a

minimum of $2000 Extra Credit

68. Where are the 12 Federal Reserve Districts located? (¼ point for each correct – you can only write down 12.)

68. Who was president when the Federal Reserve Act passed? (1 pt.)

69. What is the approximate value in the bags of “Fed Shreds” that are given as souvenirs at the Chicago Fed? (within $10 – there are two different amounts stated – you have to be within $10 of either one of them)

Name __________________________________________ Date ______________

SM3-1: Dollars and Sense

Purpose: Practice what you have learned about the time value of money by calculating the responses for the following situations.

Directions: After dividing into groups of four to five students, use a financial function calculator, a spreadsheetprogram with time-value-of-money functions, or financial function calculators on the Internet to solve the following time-value-of-money exercises.

1. Diane invests $500 today in an account earning 7%. How much will it be worth in:

5 years? ____________

10 years? ____________

20 years? ____________

2. Same facts as #1, except Diane finds an account earning 10%. How much will it be worth in:

5 years? ____________

10 years? ____________

20 years? ____________

3. Elaine needs to save $4,000 in four years. If she can set aside $1,000 today, what rate of return does

she need on her account? _______________

4. Same facts as in #3, except now Elaine can also set aside $50 per month. What rate of return does

she need on her account? _______________

5. Frank wants to buy a $10,000 car. The car dealer offers him financing of 60 payments at 9% interest.

What will his payments be assuming he pays $0 down? _______________

6. Same facts as #5, except the dealer also offers 48 payments at 8%. Now what will Frank’s payments

be assuming he pays $0 down? _______________

7. Gayle has a credit card with a $500 balance on it and a 19% interest rate. If she wants to pay off her

card in two years, what will her monthly payments be? _______________

How much interest will she pay? _______________

8. Same facts as #7, except now the balance is $2,500.

What will Gayle’s monthly payments be?_______________

How much interest will she pay? _______________

SM3-1: Dollars and Sense pg. 1 of 1

SM3-1: Dollars and Sense (Instructor)

Purpose: Practice what you have learned about the time value of money by calculating the responses for the following situations.

Directions: After dividing into groups of four to five students, use a financial function calculator, a spreadsheetprogram with time-value-of-money functions, or financial function calculators on the Internet to solve the following time-value-of-money exercises.

1. Diane invests $500 today in an account earning 7%. How much will it be worth in:

5 years? ____________

10 years? ____________

20 years? ____________

2 Same facts as #1, except Diane finds an account earning 10%. How much will it be worth in:

5 years? ____________

10 years? ____________

20 years? ____________

3. Elaine needs to save $4,000 in four years. If she can set aside $1,000 today, what rate of return does

she need on her account? _______________

4. Same facts as in #3, except now Elaine can also set aside $50 per month. What rate of return does

she need on her account? _______________

5. Frank wants to buy a $10,000 car. The car dealer offers him financing of 60 payments at 9% interest.

What will his payments be assuming he pays $0 down? _______________

6. Same facts as #5, except the dealer also offers 48 payments at 8%. Now what will Frank’s payments

be assuming he pays $0 down? _______________

7. Gayle has a credit card with a $500 balance on it and a 19% interest rate. If she wants to pay off her

card in two years, what will her monthly payments be? _______________

How much interest will she pay? ___________ ($25.20 x 24 = $604.80, less the $500 original balance = $104.80)

8. Same facts as #7, except now the balance is $2,500.

What will Gayle’s monthly payments be?_______________

How much interest will she pay? _________ ($126.02 x 24 = $3,024.48, less the $2,500 original balance = $524.48)

After students have completed the activity, lead a discussion with the following questions:

1. Did any of the answers to these problems surprise you? Which ones and why?

2. How does solving problems in a group differ from doing it on your own?

3. How would you feel about teaching someone else how to solve a time-value-of-money problem?

$701

$984

$1,935

$805

$1,297

$3,364

41%

24%

$208

$224

$25.20

$104.80

$126.02

$524.48

SM3-1: Dollars and Sense (Instructor) pg. 1 of 1

Name __________________________________________ Date ______________

SM3-2: Are You a Risk-Taker?

Purpose: Assess your personal risk level by completing the questionnaire.

Directions, Part I: Take the following quiz to find out if you are a conservative, average, or aggressive investor.Mark your choice in Column B.

Column APoint(s)

Column BChoice

1. When it comes to making the best choice, my luck has been:a. Rottenb. Averagec. Better than averaged. Terrific

2. Most of the good things that have happened to me have been because:a. I planned themb. I was able to exploit opportunities that arosec. I was in the right place at the right timed. Someone looks out for me

3. If a stock doubled in price five months after I bought it, I would:a. Sell all my stockb. Sell half my stockc. Sit tightd. Buy more shares

4. Making decisions about saving and investing on my own is something that I:

a. Never dob. Occasionally doc. Often dod. Almost always do

5. If my boss were to tell me to do something at work that I know is a bad idea, I would:

a. Say directly that it was a mistakeb. Get co-workers to join me in opposing the ideac. Do nothing unless the boss brings it up againd. Do it anyway

6. For me to put 10% of all of my savings and belongings into a new venture that has a 75% chance of success, the potential profit would have to be at least:

a. The same as the amount I had risked in investing in the ventureb Three times the amountc. Five times the amountd. No amount would be worth the risk

7. When I see people involved in sports such as hang gliding or bungee jumping, I:

a. Think they are idiotsb. Admire them but would never participatec. Wish I could try such sports just once to see what they are liked. Think seriously about participating myself

SM3-2: Are You a Risk-Taker? pg. 1 of 2

SM3-2: Are You a Risk-Taker? continued

Directions, Part II: For each question, write the points in Column A according to the following scales.

For questions 5 and 7: No matter what you chose, do not give yourself any points. Moral courage and physicalbravery are not associated with your tolerance for investment risk.

For question 10: Count up the number of items you circled. Subtract that number from 5, and this is the score youreceive for this question.

What your score means:

8 to 16 points Conservative investor; you are willing to take few risks

17 to 24 points Average investor; you are willing to take average risks

25 to 32 points Aggressive investor; you are willing to take greater-than-average risks

Adapted and reprinted with permission from University of Idaho Extension

For questions 1, 3, and 4:a. = 1 pointb. = 2 pointsc. = 3 pointsd. = 4 points

For questions 2, 6, 8, and 9:a. = 4 pointsb. = 3 pointsc. = 2 pointsd. = 1 point

Column APoint(s)

Column BChoice

8. If I held a finalist ticket in a lottery with a 1 in 5 chance of winning the $50,000 prize, the smallest amount I would consider selling my ticket for before the lottery drawing would be:

a. $30,000b. $17,000c. $13,000d. $10,000

9. In the past, I have spent $10 on one or more of the following activities: bet on my own recreational activities such as golf or poker, or bet on professional sports. (Choose the one that best applies.)

a. I have done two or more of these in the past yearb. I have done one of these in the past yearc. I have done one of these a few timesd. I have never done any of these

10. If I had to make a critical decision involving a large amount of money, I would probably do one or more of the following things: (Circle all that apply.)

a. Delay the decisionb. Have someone else make the decision for mec. Ask others to share in the decisiond. Plan strategies that would minimize any loss

Total Points

SM3-2: Are You a Risk-Taker? pg. 2 of 2

SM3-3: Assessment 3-2 Evaluation pg. 1 of 4

Assessment 3-2: Evaluation

Multiple Choice (10 pts.): Read each item carefully; then select the best answer. Each answer is worth 1 pt.

____ 1. The Rule of 72 is useful in calculating the a. interest an investor needs to earn to reach a goal.b. age of money.c. time required to double an investment.d. fluctuations of the stock market.

____ 2. The basic rule of a risk-to-return relationship is that the a. lower the risk, the higher the return rate.b. higher the risk, the higher the return rate.c. higher the risk, the lower the return rate.d. two are not related.

____ 3. Which one of the following types of investments has the lowest risk and lowest rate of return? a. Savings bondsb. Stocksc. Collectiblesd. Real estate

____ 4. Which one of the following types of investments has the highest risk and the highest potential rate of return? a. Money market mutual fundb. Stocksc. Government bondsd. Savings bonds

____ 5. Which statement below is true about mutual funds? a. All mutual funds buy stocksb. Mutual funds offer guaranteed returnsc. Mutual funds are convenient and professionally managedd. You can choose which stock to include in your mutual funds

____ 6. The time value of money can best be explained using which one of the following concepts? a. The “pay yourself first” philosophyb. The risk-to-return relationshipc. The dynamics of compoundingd. The Rule of 72

____ 7. What approximate interest rate would an investor need to earn in order to double the value of an investment in six years? a. 6%b. 10%c. 12%d. 72%

____ 8. If an investor can earn 9 percent on an investment, approximately how long will it take to double in value? a. 72 monthsb. 8 yearsc. 9 yearsd. 12 years

Score ________/50 Name __________________________________________ Date ______________

____ 9. In the future, a dollar will be worth a. Less than a dollar todayb. More than a dollar todayc. The same as a dollar today

____ 10. Monica adds $500 to her mutual fund every year for the next 10 years. Mason decides to wait 10 years when he knows he will have a lump sum of $5,000 to invest in a mutual fund. If both Monica and Mason earn on average a 7 percent rate of return, who will have the larger mutual fund balance in 20 years? a. Monica b. Mason c. They will have the same balance amount because they each invested the same amount at the

same rated. There is not enough information presented to make a prediction

Ranking (16 pts.) (Each question is worth 8 pts.): Use what you learned in this unit and consider current trendsto rank the investment options listed below.

11. In the left column, rank the investments highest (#1) to lowest (#8) to show how they compare according to the opportunity for reward.

12. In the left column, rank the investments highest (#1) to lowest (#8) to compare the risk of the investments.

Matching (5 pts.): Read each statement carefully. Select the term that best matches the statement by writingthe letter of the matching term.

____ 13. Used to determine how long it takes for your money to double

____ 14. One type of income investment

____ 15. The mathematical relationship between time, money, a rate of return,

and earnings growth

____ 16. The process of earning interest on interest

____ 17. Spreading your money among different savings and investments

Short Answer (4 pts.): Read each item carefully; then write an answer based on what you learned about savingand investing in Unit 2. Each question is worth 2 pts.

18. What is the difference between saving and investing?

20. In this unit, you have considered ways to use investments to help you meet financial goals. Use what you have learned to outline your investment plan for the near future.

a. State your top three choices of investment options you will use in the next 10 years. b. Summarize your plan for how much, how often, and when you will invest.c. Justify why you have selected each option and how the option relates to your financial goals.

.

SM3-3: Assessment 3-2 Evaluation pg. 4 of 4

Investment A:

Approximate Amount

$_________________

Plan for when/how often:

Investment B:

Approximate Amount

$_________________

Plan for when/how often:

Investment C:

Approximate Amount

$_________________

Plan for when/how often:

How this option relates to my intermediate- and long-term financial goals

Why I selected this investment

How this option relates to my intermediate- and long-term financial goals

Why I selected this investment

How this option relates to my intermediate- and long-term financial goals

Why I selected this investment

SM3-3: Assessment 3-2 Evaluation (Instructor) pg. 1 of 2

Assessment 3-2: Evaluation Answer Key

Multiple Choice (10 pts.): Each answer is worth 1 pt.

1. c. time required to double an investment [Objective B, p. 32]

2. b. higher the risk, the higher the return rate [Objective D, p. 33–34]

3. a. Savings bonds [Objective D, p. 33]

4. b. Stocks [Objective D, p. 33]

5. c. Mutual funds are convenient and professionally managed [Objectives C, D; p. 37]

6. c. The dynamics of compounding [Objective B, p. 30]

7. c. 12% [Objective B, p. 32]

8. b. 8 years [Objective B, p. 32]

9. a. Less than a dollar today [Objective B, p. 30]

10. a. Monica [she started investing early and has the advantage of compounding interest][Objective B, pp. 29–30]

SM3-3: Assessment 3-2 Evaluation (Instructor) pg. 2 of 2

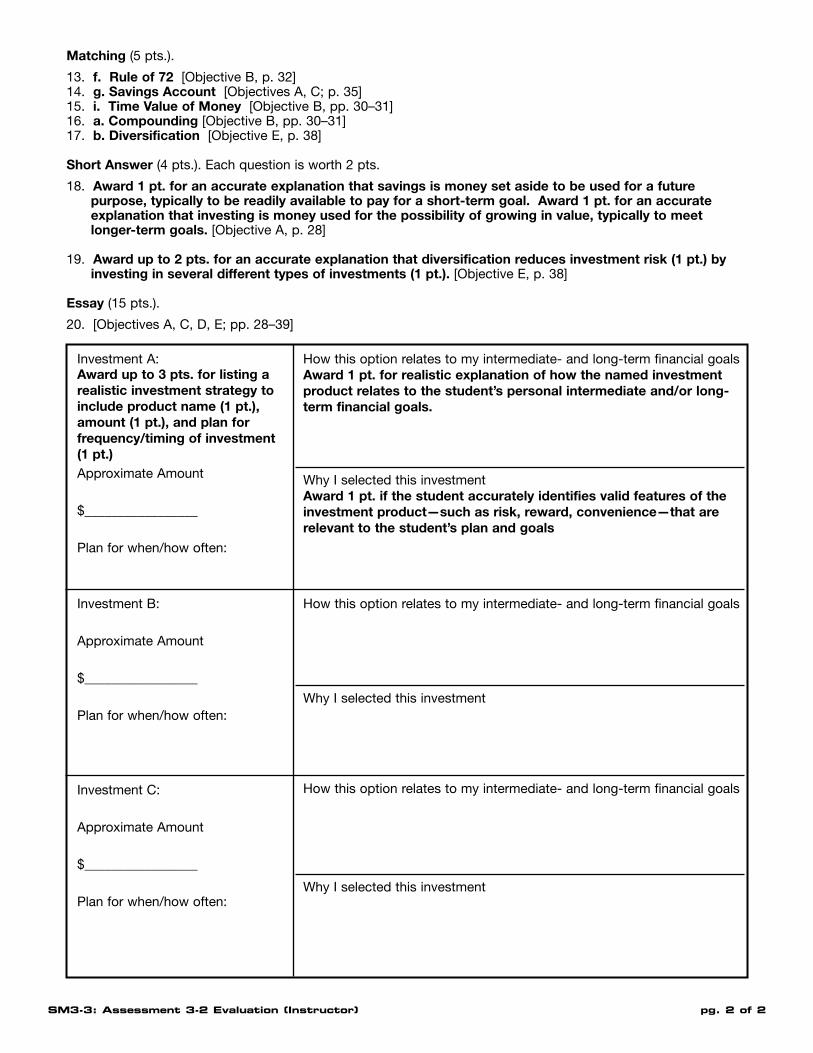

Matching (5 pts.).

13. f. Rule of 72 [Objective B, p. 32]14. g. Savings Account [Objectives A, C; p. 35]15. i. Time Value of Money [Objective B, pp. 30–31] 16. a. Compounding [Objective B, pp. 30–31] 17. b. Diversification [Objective E, p. 38]

Short Answer (4 pts.). Each question is worth 2 pts.

18. Award 1 pt. for an accurate explanation that savings is money set aside to be used for a future purpose, typically to be readily available to pay for a short-term goal. Award 1 pt. for an accurate explanation that investing is money used for the possibility of growing in value, typically to meet longer-term goals. [Objective A, p. 28]

19. Award up to 2 pts. for an accurate explanation that diversification reduces investment risk (1 pt.) by investing in several different types of investments (1 pt.). [Objective E, p. 38]

Essay (15 pts.).

20. [Objectives A, C, D, E; pp. 28–39]

Investment A:Award up to 3 pts. for listing arealistic investment strategy toinclude product name (1 pt.),amount (1 pt.), and plan for frequency/timing of investment(1 pt.)Approximate Amount

$_________________

Plan for when/how often:

Investment B:

Approximate Amount

$_________________

Plan for when/how often:

Investment C:

Approximate Amount

$_________________

Plan for when/how often:

How this option relates to my intermediate- and long-term financial goalsAward 1 pt. for realistic explanation of how the named investmentproduct relates to the student’s personal intermediate and/or long-term financial goals.

Why I selected this investmentAward 1 pt. if the student accurately identifies valid features of theinvestment product—such as risk, reward, convenience—that arerelevant to the student’s plan and goals

How this option relates to my intermediate- and long-term financial goals

Why I selected this investment

How this option relates to my intermediate- and long-term financial goals

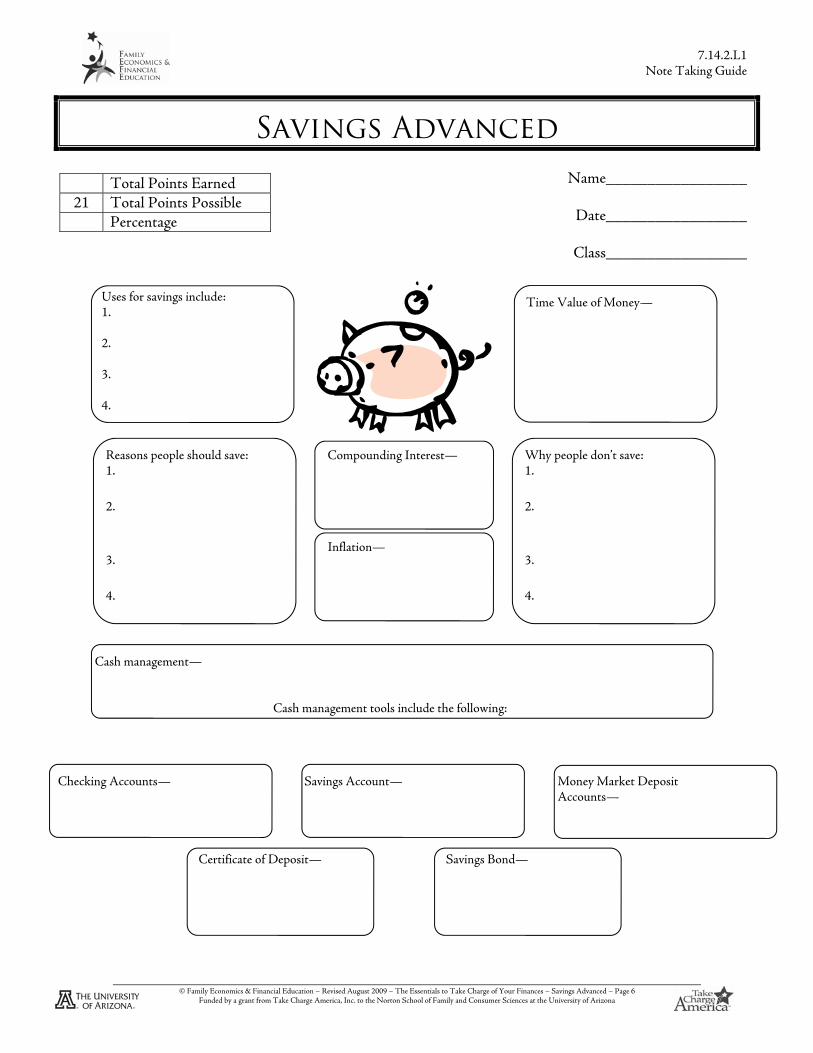

Time to complete: 60 minutes Objectives Upon completion of this workshop, participants will be able to:

Understand the time value of money. Explore the value of saving. Understand how interest works. Describe different saving methods.

FEFE Lesson Plan Resources Time Value of Money lesson plan 1.14.5 Introduction to Savings lesson plan 1.14.1 Managing Your Cash lesson plan 1.14.2 Introduction Saving is difficult for many people because it involves decreasing current consumption and investing in a future standard of living. The future is an unknown risk and without developing a savings and investing plan individuals will not have the financial means to meet future financial goals such as purchasing homes, cars and saving for retirement. Savings is the portion of current income not spent on consumption. Financial experts recommend individuals keep a minimum of three to six months of salary in a savings account. One of the most important concepts about saving and investing is the time value of money. This means money paid out or received in the future is not equivalent to money paid out or received today. There are three factors affecting how much an investment will grow: time, money and interest rate. The earlier an individual invests, the more time their investment has to compound interest and increase in value. For example: At 10% interest rate Sally Saver started investing $3,000 per year into an Individual Retirement Account at age 22 and invested a total of $30,000.00. Ed Uninformed began investing $3,000 per year into an Individual Retirement Account earning a 10% interest rate at age 28 and invested a total of $117,000.00. At age 65, when Ed and Sally would like to retire Sally has earned $1,239,564.00 from her $30,000 investment. Ed has earned $1,102,331.00 from his $117,000.00 investment. The interest rate refers to the percentage rate paid on the money saved or invested. The higher the interest rate, the more money an individual will earn. One important consideration regarding interest rates is ensuring the interest rate is higher than the rate of inflation. Inflation is the steady rise in the general level of prices. If an individual has money invested at 4%, and the inflation rate is 4%, the individual’s wealth will not increase. The following is an illustration of how interest rates affect the total return on $1,000.00:

$1,000 Invested Compounded Monthly Interest Rate 1 Year 5 Years 10 Years 4% $1,040.74 $1,221.00 $1,490.83 6% $1,061.68 $1,348.85 $1,819.40 8% $1,083.00 $1,489.85 $2,219.64 10% $1,104.71 $1,645.31 $2,707.04

As a person’s income increases, he/she will have more cash to manage. This requires a person to have an idea about how much cash he/she would like to keep on hand and in what type of cash management tools. Cash management is the daily routine of handling money to take care of an individual’s or family’s needs by keeping enough available for living expenses, emergencies, savings, and investing while maximizing interest earnings. A cash management tool is a financial account used to assist with daily cash management. Cash management can be performed through different types of cash management tools and cash on hand. A person must effectively manage these monetary assets. A checking account is a tool used to transfer funds deposited into the account to make a cash purchase. Unlimited access to funds can be through checks, ATMs, debit cards, telephone, or internet. It reduces the need to carry large amounts of cash. Checking accounts are the most liquid and have the lowest interest rate. A savings account is an account to hold money not spent for daily living expenses. They have a low interest rate, although higher than a checking account, and often require a minimum balance. There is also a limit placed on the number of withdrawals from a savings account. A money market deposit account is a government insured account offered at most depository institutions. These accounts have a minimum balance requirement with tiered interest rates. Tiered interest rates mean the amount of interest earned depends on the account balance. For example, a balance of $10,000 will earn a higher interest rate than a balance of $2,500. Accounts are limited to a certain number of transactions each month. Customers usually have to deposit a minimum amount to open the account ($1,000). Money market deposit accounts have a higher average rate of return than checking and savings accounts. A savings bond is a discount bond purchased for 50% of the face value from the U.S. Government. U.S. savings bonds are for conservative, low-risk savers who like government secured savings instruments. For a $100.00 bond, a person would invest $50.00. The bond can be redeemed when the investment doubles to reach $100.00. Any interest earned is exempt from being taxed until the bond is redeemed. If the bond is used to pay for college, it is tax exempt when redeemed. A certificate of deposit (CD) is an insured interest earning savings instrument with restricted access to the funds. The length of time for a CD usually ranges from seven days to eight years. If the funds are withdrawn before the expiration date, penalties are assessed. The longer the length of a CD, the higher the interest rate will be. Liquidity is how quickly and easily an asset can be converted into cash. If an individual were to have an emergency, cash needs to be easily accessible. Wise financial managers place money in both liquid and non-liquid tools to be able to cover everyday needs and to still earn interest. In this lesson, participants discuss the importance of savings and the different tools that can aid in the process. They will learn the significance of the time value of money and that it is best to start saving early. Participants also evaluate recommended savings guidelines and develop a savings goal for themselves. Body 5 minutes

1. Provide each participant with $100.00 in play money. a. Ask each participant what they would do with the money.

i. Record their answers on the board if possible. 2. Pass out a Savings Advanced note taking guide 7.14.2.L1 or the Savings Advanced Information Sheet

7.14.2.F1 to each participant and instruct them to complete it during the Savings Advanced PowerPoint presentation 7.14.2.G1.

3. Present Saving Advanced PowerPoint presentation 7.14.2.G1 a. Slide 1: Introduction b. Slide 2: Savings Basics

i. Ask the participants what it means to save. ii. Ask participants to discuss what the last item they saved for was.

c. Slide 3: Uses for Saving i. Ask participants to brainstorm reasons why people may want to save money.

ii. Add to their ideas by discussing the four listed on the slide. d. Slide 4: Reasons People Should Save

i. Emergencies – It is recommended individuals have a minimum of three to six months of salary in savings accounts for emergencies. Examples of emergencies can include illness, losing a job, or immediate need to replace a large item such as a washing machine.

ii. Expenses – Savings accounts can be used as a budgeting tool to manage monthly expenses. iii. Future purchases – Money can be used to meet future goals such as a college education, new

car, down payment on a home, or a new stereo. iv. Investing – After an individual has established a savings account, money should be invested

monthly for future income. e. Slide 5: Reasons People Don’t Save

i. Brainstorm with participants reasons why people do not begin a savings plan. 1. People are not having their current consumption needs and wants met. 2. People do not know how much they need to be saving or investing for future goals. 3. Money in savings accounts earns such poor interest rates. It barely (if at all) keeps

up with inflation. a. Investing usually gains higher interest rates.

4. Individuals justify not needing money for emergencies because they have credit easily available.

5. People feel they have adequate insurance and job security; therefore, they feel they do not need money for emergencies.

f. Slide 6: Time Value of Money g. Slide 7: Interest Rates

i. Ask participants to brainstorm where they have heard the term interest rates used before. ii. Identify that interest rates can be helpful when saving and negative in credit.

h. Slide 8: Compounding Interest i. Compounding interest is earning interest on interest.

ii. This means if a person has $1,000 earning 10% interest compounded annually he/she will earn $104.71 in interest. Therefore, in year two, it will become $1,104.71 earning 10% interest for a total of $1,220.39.

iii. Compounding interest is different than simple interest. Simple interest takes the amount invested multiplied by the annual interest rate multiplied by the number of years.

i. Slide 9: A little goes a long way i. Have the participants recognize and report the differences between Sally and Ed.

ii. Discuss why starting at an earlier age is better. iii. Discuss why starting at an earlier age may be more difficult.

j. Slide 10: The costs add up i. Discuss why it is important to track even small expenditures throughout the day.

ii. Have participants identify sources of money they can save. k. Slide 11: Inflation

i. Inflation is the steady rise in the general level of prices. If the interest rate for the savings or investment is not higher than inflation, a person will be losing money on an investment after taxes

l. Slide 12: Cash Management m. Slide 13: Cash Management Tools

i. Ask participants why individuals want to manage their cash. 1. Answers should include the reasons from slide 2 of why people save money.

n. Slide 14: Checking Account i. Remind participants that in order to use an ATM they must also know their Personal

Identification Number (PIN). o. Slide 15: Savings Accounts

i. Discuss with participants that often consumers will use the same depository institution for both their checking and savings accounts.

p. Slide 16: Money Market Deposit Accounts i. Discuss with participants that interest is the price paid or gained for money. In this case

using a money market account will be money that is gained. q. Slide 17: Certificate of Deposit r. Slide 18: Savings Bond s. Slide 19: Cash management tools comparison chart t. Slides 20-21: Liquidity

i. Explain to participants that assets are items that can be exchanged for value. 1. Instruct participants to give examples of assets. Examples may include:

a. Home b. Car c. Investments

u. Slides 22-24: Dominoes v. Slide 25: Conclusion

Conclusion 20 minutes

Use the Dominoes Questions and Answers 7.14.2.K1 to play Dominoes 7.14.2.H1. Refer to 7.14.2.J1 for detailed instructions.

Assessment Have participants complete the Savings Advanced worksheet 7.14.2.A1 Or Have participants take the Savings Pre/Post Test 7.14.2.M1 Materials Saving Advanced Worksheet – 7.14.2.A1 Savings Advanced PowerPoint presentation – 7.14.2.G1 Domino activity instructions – 7.14.2.J1 Domino activity questions and answers – 7.14.2.K1 Savings Advanced note taking guide – 7.14.2.L1 Computer Projector Dominoes® – approximately one Activity per 2 to 4 participants (optional – paper dominoes 7.14.1.H1)

Nontransparent bag Workshop Alternatives 1. Show the importance of interest rates overhead 1.14.5.D3 from the Time Value of Money lesson plan 1.14.5.

a. This will help participants to recognize the importance of interest rates. 2. Display A Little Goes a Long Way poster 4.19.1.

a. This poster will work as a good review and discussion point of the importance of putting money away at a young age.

3. Hand out one Savings information sheet 1.14.1. F1 to each participant. a. The information sheet will supplement the lesson being taught in the workshop.

Class_________________ Directions: Complete the following questions by placing the letter of the term next to its correct definition. (Each is worth 1 point)

1. _______ A government insured account with tiered interest

rates offered at most depository institutions. 2. _______ Money to be paid out or received in the future is not

equivalent to money paid out or received today. 3. _______ Tool used to transfer funds deposited into an

account to make a cash purchase. 4. _______ An insured, interest earning savings instrument with

restricted access to the funds. 5. _______ The portion of current income not spent on

consumption. 6. _______ Earning interest on interest. 7. _______ Discount bond purchased for 50% of the face value

from the U.S. Government. 8. _______ How quickly and easily an asset can be converted

into cash. 9. _______ Account to hold money not spent on consumption. 10. _______ The steady rise in the general level of prices.

A) Certificate of Deposit B) Savings Bond C) Inflation D) Checking Account E) Liquidity F) Money Market Deposit Account G) Compounding interest H) Savings I) Time Value of Money J) Savings Account

Directions: Complete the following questions. 11. The daily routine of handling money to take care of individual or family needs is called

. (1 point)

12. Define a cash management tool. (1 point) 13. Name three ways to access funds in a checking account. (3 points) 14. A savings account is meant to hold what kind of money? (1 point)

15. Describe two features of a savings account. (2 points) 16. Name and define the type of interest rate used for a money market deposit account. (2 points) 17. What are two features of a certificate of deposit? (2 points) 18. For what amount can a savings bond be purchased? (1 point) 19. Investors should invest in both and tools. (2 points) 20. Complete the chart below by listing the most liquid cash management tool to the least. (5 points)

Cash Management Tool Most liquid 1. 2. 3. 4. Least liquid 5.

• Bone is the name given to a domino. • Doublet is a bone whose two ends are alike. • Blanks are dominoes without a numeric value. • Block game is one of the many ways to play dominoes.

1. Prepare to play activity

a. Divide participants into groups of three to four. b. Designate one person in the group as the facilitator. c. The facilitator will be the score keeper and inform the other participants if questions have been

answered correctly. d. Shuffle bones and place face down in the center of the group, take care to not turn any bone face

up in doing so. e. Each player draws their bones and places them so he/she can view them but the rest of the

group cannot. i. Two players: each draws seven bones

ii. Three or four: each draws five bones 2. Play the activity

a. The player holding the highest doublet set lays it down as the first play. b. The player then pulls a question from the bag and attempts to answer it correctly. c. The facilitator in the group will tell the person if the answer is correct. d. If the answer is correct

i. The person receives points equal to the face value on the domino and receives another turn.

e. If the answer is wrong i. The question then moves to the player on the left who has a chance to earn the points.

ii. The question moves around the group until it is answered correctly or the question has moved around the entire group once and never answered.

1. The person who eventually answers the question then places one of his/her bones down on one of the wide sides of the doublet, the bone they place must have the same value as one side of the doublet.

2. In the case that a correct answer is not given by anyone in the group, the play moves to the left and no one scores.

f. Special notes about the activity i. The play always moves to the left.

ii. Players will have two options to place their bones, one on either of the “open ends” of the layout.

iii. The dominoes are placed end to end with like numbers touching, unless a doublet is put down; doublets are customarily placed perpendicular to the other dominoes, but this still only offers one open end. Below is a picture of how bones are put down.

iv. If a player cannot play in turn, that is, he/she does not have a bone with a like number for either of the open ends, he/she passes.

g. Concluding the Activity i. The Activity ends when a player gets rid of his hand or when no player is able to add to

the layout. ii. Variation: Before beginning, the group can decide on a certain point value, such as first

one to 50 points wins. h. Choosing a winner

i. The winner of the Activity is the player who reaches the agreed upon points or has the most points when the Activity is over, this player may or may not be the player who ran out of bones first.

3. Discussion a. After participants have finished the Activity, hold a class discussion reviewing the major

1. What is the definition of Compounding Interest? Earning interest on interest

2. What is a fixed interest rate?

The rate will not change for the lifetime of the investment

3. What is the definition of inflation? The steady rise in the general level of prices

4. What is the definition of financial institutions?

Business which offer multiple services in banking and finance 5. Does a person want a higher or lower interest rate on an investment?

An individual wants a higher interest rate. The higher the interest rate the more money that is earned

6. What is the definition of Time value of money? Money to be paid out or received in the future is not equivalent to money paid out or received today

7. What services may be included with financial institutions?

Savings and checking accounts, loans, investments, and financial counseling

8. What are the four types of financial institutions? Commercial Bank, Savings and Loan Association, Credit Union, and Brokerage Firm

9. Identify two cash management tools

Savings account, money market deposit account, certificate of deposit, and savings bond 10. An account to hold money not spent on consumption is what type of account.

Savings account

11. A government insured account offered at most depository institutions is a what Money Market Deposit Account

12. An insured, interest earning savings instrument with restricted access to funds is called a what Certificate of Deposit