Standing for trust and integrity 19 th XBRL International Conference Paris, June 22-25 2009 Status FEE XBRL Task Force, what is happening around Europe Philip Johnson FEE Deputy President Chairman FEE Auditing Working Party and FEE XBRL Task Force

Transcript

Standing for trust and integrity

19th XBRL International Conference

Paris, June 22-25 2009

Status FEE XBRL Task Force,what is happening around Europe

Philip JohnsonFEE Deputy President

Chairman FEE Auditing Working Party and FEE XBRL Task Force

2 Standing for trust and integrity

Federating Member Bodies

43 professional institutes of accountants 32 European countries, including all 27 EU > 500.000 professional accountants

3 Standing for trust and integrity

Agenda

Why should auditors in Europe be interested in XBRL?

Will auditors be asked to provide additional levels of assurance on XBRL information?

What has FEE done to consider the matter? Where are IASB in the debate? What is IAASB doing? What are some of the other issues for auditors

surrounding XBRL?

4 Standing for trust and integrity

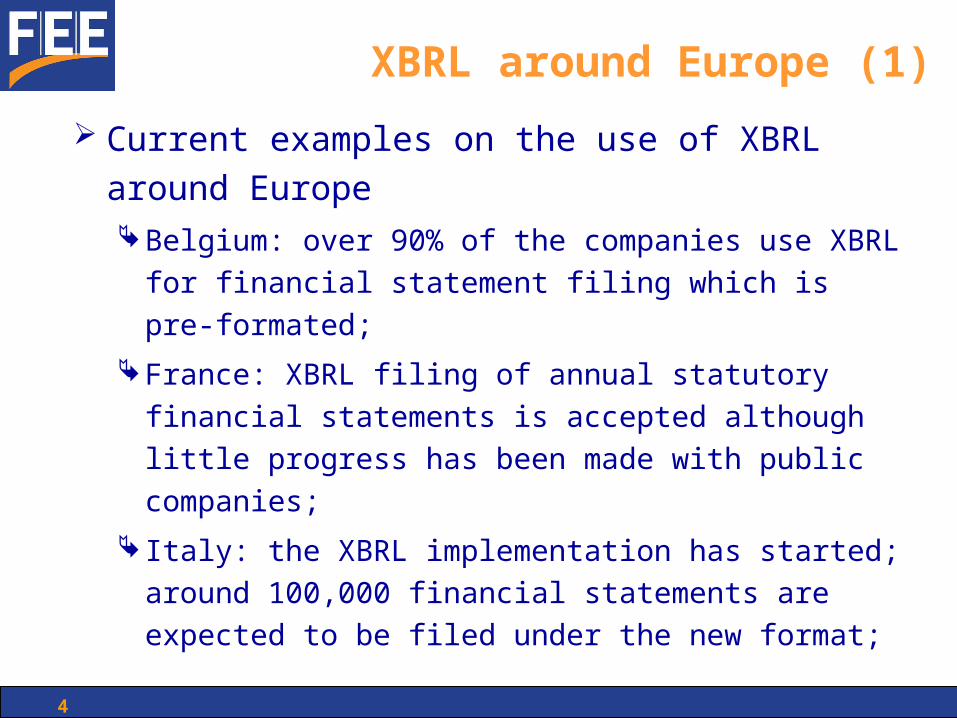

XBRL around Europe (1)

Current examples on the use of XBRL around

EuropeBelgium: over 90% of the companies use XBRL for

financial statement filing which is pre-formated;

France: XBRL filing of annual statutory financial

statements is accepted although little progress has

been made with public companies;

Italy: the XBRL implementation has started; around

100,000 financial statements are expected to be filed

under the new format;

5 Standing for trust and integrity

XBRL around Europe (2)

Netherlands: XBRL information prepared in agreement

with the tax authorities will be accepted for tax purposes;

banks have developed an extension of the Dutch

taxonomy and are ready to start using it;

Spain: the use of XBRL has been approved by the

authorities to file accounts;

Sweden: since 2006 electronic filing has been permitted by

the legislator. For the year 2008, 60 fully electronic XBRL

tagged annual reports have been submitted via the official

internet service provided;

UK: there is a limited use of XBRL. Parallel projects are

taking place, for audit exempt companies, abbreviated

accounts can be filed in XBRL.

6 Standing for trust and integrity

FEE and XBRL

FEE has an XBRL Task Force combining

financial reporting and auditingFirst meeting in October 2008 brainstormed on

possible FEE actions and considered types of

assurance which may be requested;

Second meeting in March 2009 considered

developing a project proposal;

A Policy Statement to educate the accountancy

profession and stakeholders is being drafted.

7 Standing for trust and integrity

Assurance from auditors

What type of assurance should be given:Reasonable assurance

Limited assurance

Agreed upon procedures

To whom:Management

Shareholders

Third Parties

And when?

8 Standing for trust and integrity

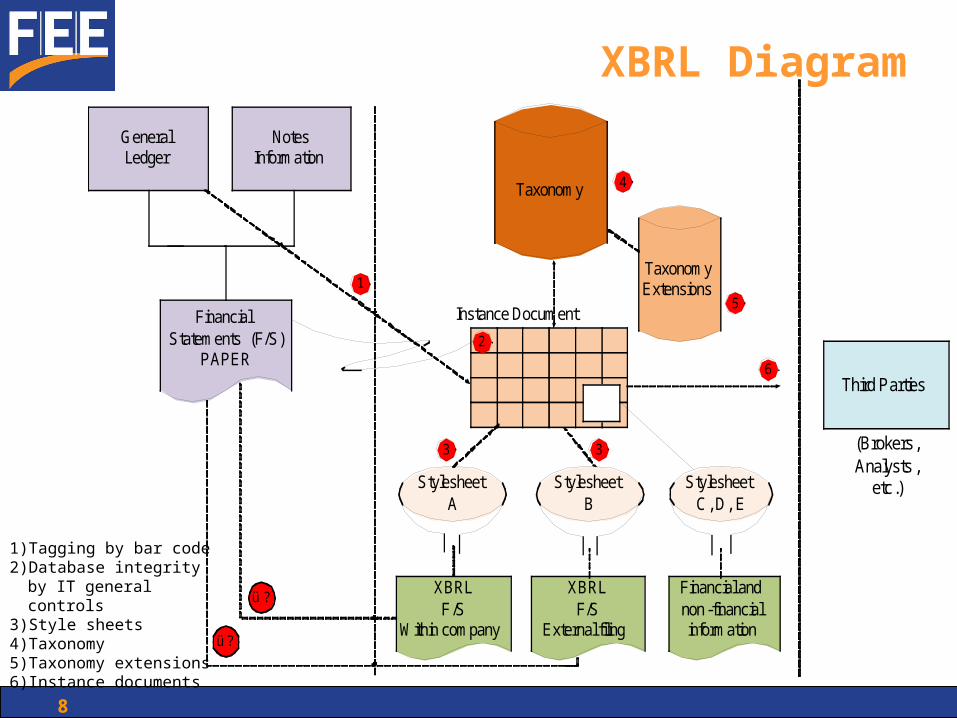

XBRL Diagram

XBRLF/S

Within company

XBRLF/S

External filing

Financial andnon-financial information

GeneralLedger

NotesInformation

StylesheetC, D, E

Taxonomy Extensions

Taxonomy

Financial Statements (F/S)

PAPER

StylesheetA

StylesheetB

Instance Document

1

4

2

3 3

ü ?

ü?

5

6

1) Tagging by bar code2) Database integrity by IT

general controls3) Style sheets4) Taxonomy5) Taxonomy extensions6) Instance documents

Third Parties

(Brokers, Analysts ,

etc.)

(Brokers, Analysts ,

etc.)

9 Standing for trust and integrity

FEE Policy Statement on XBRL (1)

FEE Policy Statement on XBRL main aim is to

increase awareness in and outside the

professionWhat is XBRL?

What are XBRL “Taxonomies”?

What are “Extensions” of a Taxonomy and why are

they used?

What is “tagging”?

What is an “Instance Document”?

What is a “Style sheet”?

10 Standing for trust and integrity

FEE Policy Statement on XBRL (2)

The Policy Statement also deals with:Use of XBRL

How does XBRL change the preparation of financial

statements

Implications of XBRL for statutory auditors

IAASB project on XBRL

XBRL Advantages and Disadvantages

Implications of XBRL for third parties

Practical implications

11 Standing for trust and integrity

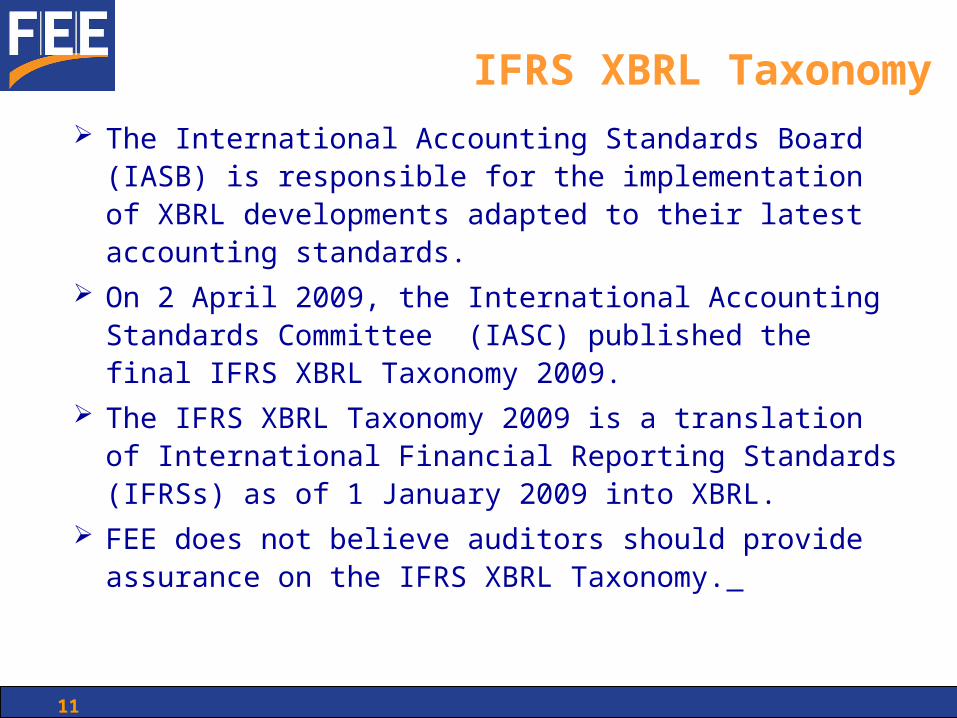

IFRS XBRL Taxonomy The International Accounting Standards Board (IASB) is

responsible for the implementation of XBRL developments adapted to their latest accounting standards.

On 2 April 2009, the International Accounting Standards Committee (IASC) published the final IFRS XBRL Taxonomy 2009.

The IFRS XBRL Taxonomy 2009 is a translation of International Financial Reporting Standards (IFRSs) as of 1 January 2009 into XBRL.

FEE does not believe auditors should provide assurance on the IFRS XBRL Taxonomy.

12 Standing for trust and integrity

IAASB XBRL Project

The International Auditing and Assurance Standards Board (IAASB) approved a project that includes:

1. Consultation to obtain views about the IAASB’s plans to develop a pronouncement to address the performance and reporting expectations of the auditor in connection with audited financial statements that are accompanied by XBRL data (Phase 1 by March 2010); and

2. Subject to no indication to the contrary in the public interest arising from Phase 1, the development of a pronouncement on the responsibilities of the auditor in an audit of financial statements when audited financial statements are accompanied by XBRL data (Phase 2 by December 2011).

No new (non-audit) assurance or related services standard would be developed.