19

State & Local Digital Economy and More www.pwc.com/il Alon Sherer, Senior Tax Manager, PwC Israel November 2018

State & LocalDigital Economy and More

www.pwc.com/il

Alon Sherer, Senior Tax Manager, PwC Israel

November 2018

2PwC Israel

Agenda

Sales Tax – Wayfair ruling

1. General Overview

2. States Action

3. What should Companies Do

Qualified opportunity funds - tax incentives for investors

1. General Overview

3PwC Israel

Sales Tax – Wayfair ruling

4PwC Israel

Sales tax: quick overview

• Sales Tax Nexus - allows a state to exercise its taxing authority over a company.

• Pre-Wayfair federal law required some sort of physical presence.

• The Supreme Court first held in the 1960s that only businesses with a physical presence had to collect Sales Tax. This view was ratified by its decision in Quill vs North Dakota (1992)

5PwC Israel

Sales tax: quick overview

• The internet age – e-commerce sales revenue

• Since 2008, various nexus expansion legislation by state:

Click-Through Nexus

Affiliate Nexus

Economic Nexus

Marketplace Nexus

Use Tax Notice and Reporting Requirements

6PwC Israel

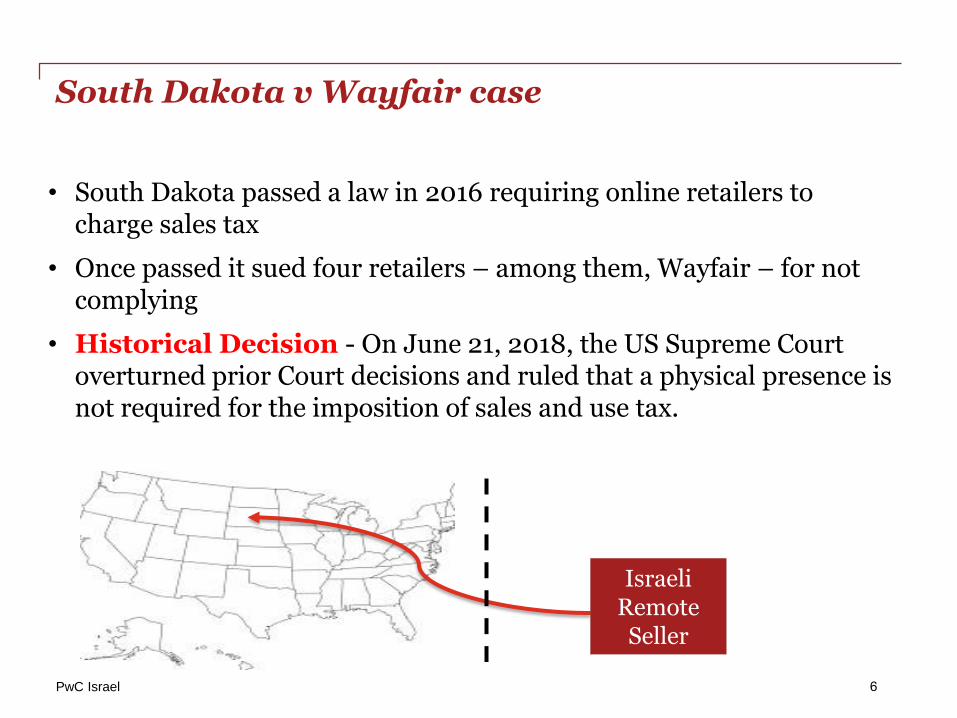

South Dakota v Wayfair case

• South Dakota passed a law in 2016 requiring online retailers to charge sales tax

• Once passed it sued four retailers – among them, Wayfair – for not complying

• Historical Decision - On June 21, 2018, the US Supreme Court overturned prior Court decisions and ruled that a physical presence is not required for the imposition of sales and use tax.

Israeli Remote Seller

7PwC Israel

Sales Tax Post Wayfair

• Foreign / US remote seller and E-commerce

• 45 states with sales tax - Approximately 30 states impose some form of economic nexus– the rest are likely to follow

• Economic Threshold – most of the states have adopted economic thresholds equal to or higher than South Dakota’s (100K annual sale of good or service or 200 transaction), but NOT ALL

• Anticipated enforcement actions – Watch out for Audits

• After Wayfair, states may seek to enforce economic nexus provisions for income taxes

8PwC Israel

201920182017Jurisdiction10/1/2018Alabama

12/1/2018Colorado

12/1/2018Connecticut

1/1/2019Georgia

7/1/2018Hawaii

10/1/2018Illinois

10/1/2018Indiana

1/1/2019Iowa

10/1/2018Kentucky

1/1/2019Louisiana

7/1/2018Maine

10/1/2018Maryland

10/1/2017Massachusetts

10/1/2018Michigan

10/1/2018Minnesota

9/1/2018Mississippi

1/1/2019Nebraska

10/1/2018New Jersey

11/1/2018North Carolina

10/1/2018North Dakota

1/1/2018Ohio

7/1/2018Oklahoma

3/1/2018Pennsylvania

8/17/2017Rhode Island

11/1/2018South Carolina

11/1/2018South Dakota

1/1/2019Utah

7/1/2018Vermont

10/1/2018Washington

10/1/2018Wisconsin

Sales Tax Economic Nexus Effective Date

9PwC Israel

Considerations for foreign sellers

• Nothing in Wayfair decision limits holding to domestic US companies

• Income tax treaties do not protect foreign companies from sales tax collection responsibilities in any U.S. state.

• At the same time, there is also currently no treaty between any foreign country and the U.S. to collect sales tax based on a state judgment. (“Revenue Rule”).

• Enforcement of online sellers of digital products with no physical presence in the US?

• Possible state actions –

- Warrants, liens, credit rating, M&A hurdles, U.S. bank accounts

- Reputational considerations, publicity and public relations

• Federal enforcement? Congress – potential foreign transactions provision

10PwC Israel

What should companies do?

There will be more of everything!

• Filing - review the physical and economic footprint in each jurisdictions

• Taxability - determine product/service taxability or exemption

• System & Process - computer system or outsourcing

• Continuing Monitoring - state guidance varies and still developing

• Financials – evaluate ASC 450 (sales tax reserve) positions

• Foreign sellers – compliance is a complex issue- should move forward to evaluate its action.

Slide 10

11PwC Israel

State Income Tax Considerations

• Wayfair implication to state corporate tax should not overlooked

• Economic income tax nexus and factor presence tests. Approximately 30 states already impose some form of economic income tax threshold

• Market-based sourcing – 27 states ( CO & NJ effective 2019)

• Federal Public Law 86-272 – protect remote sales of tangible personal property - Will it apply to foreign retailers?

• ASC 740 implication - Wells Fargo – reported $481 million income tax expense because its affiliated entities may now face income tax assessments for jurisdictions where they do business but have no physical presence.

12PwC Israel

Qualified opportunity funds - tax incentives for investors

13PwC Israel

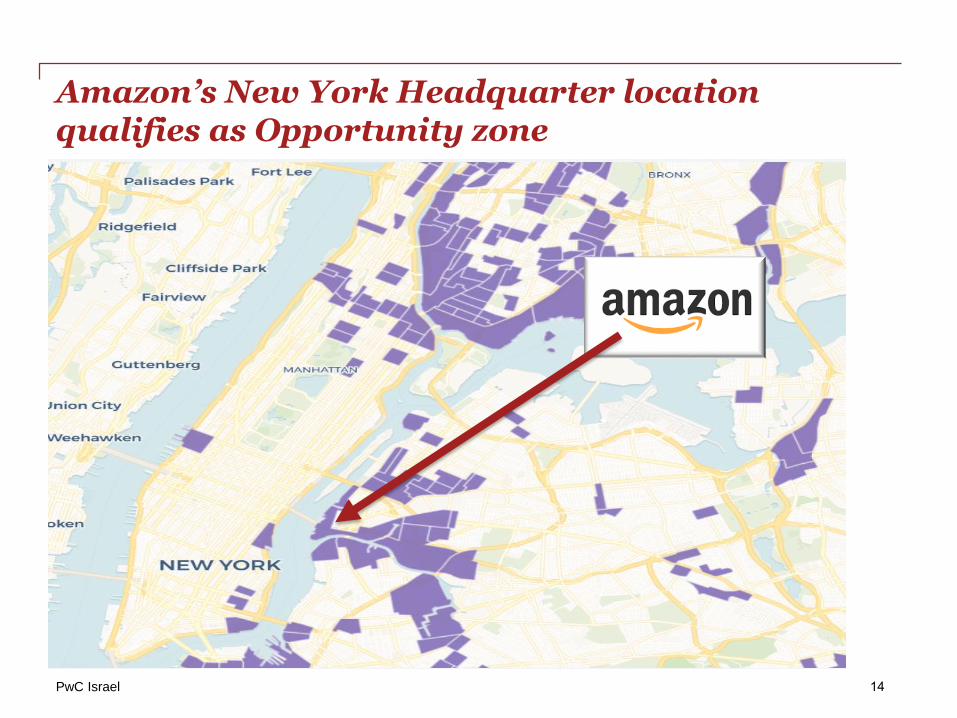

Qualified Opportunity Zones (“QOZ”)

• The 2017 Tax Act, includes a new tax incentive program, Internal Revenue Code Subchapter Z – Opportunity Zones. IRS released proposed regulation on October 19,2018

• Promote investments in certain economically distressed communities

• An QOZ is a community nominated by the state and certified by the Treasury Department as qualifying for this program. List of opportunity zones is found in Notice 2018-48

• Over 8,700 QOZ in the US (all 50 states)

14PwC Israel

Amazon’s New York Headquarter location qualifies as Opportunity zone

15PwC Israel

California - Bay Area - Opportunity zones

16PwC Israel

Opportunity Zones – Tax Benefit

Taxpayers with capital gain are given the opportunity to defer and possibly reduce the tax on recognized capital gains.

Temporary deferral of Tax

Elimination of up to 15% of the deferred

gain

Potential exclusion of

tax gain of the appreciated investment

17PwC Israel

How Does This Program Work?

• Taxpayer – Individual, corporation, partnership & other pass-through entities.

• Eligible capital gains - Taxable for federal income tax, not arising from sale or exchange with related person

• Taxpayer has 180 days from date of sale to invest in QOZ

• QOZ Fund must be organized as a domestic corporation or a partnership (“Entity Test”).

• Hold on the investment to defer tax and increase in basis. Mandatory deferred gain recognition in year 8.

18PwC Israel

Opportunity Zones – Tax Benefit example

Fact: Taxpayer sells stock with a realized gain of $1M. On 12/1/18 he invests in QZF (within 180 days). If Taxpayer sells interest in QOF:

• Prior to 12/1/2023 – recognize gain on the $1M.• After 12/1/23 and before 12/1/25 recognize gain on $900k.• After 12/1/25 and before 12/31/26 recognize gain on $850k.• After 12/31/26 and before 12/1/28 recognize gain if exceed $1M.• After 12/2/28 Tax free withdrawal (FMV election)

August 1,2018 –Capital gain

December 1,2018 – Fund Investment

5 years

December 1,2023 –10% basis increase

2 years

December 1,2025 –5% basis increase

December 31,2026 – mandatory recognition of deferred gain

3 years

December 2,2028 –Tax free withdrawal

©2018 Kesselman& Kesselman. All rights reserved.

In this document, “PwC Israel” refers to Kesselman & Kesselman, which is a member firm of PricewaterhouseCoopers International Limited, each

member firm of which is a separate legal entity. Please see www.pwc.com/structure for further details.

PwC Israel helps organisations and individuals create the value they’re looking for. We’re a member of the PwC network of firms with 250,000 people in

more than 157 countries. We’re committed to delivering quality in assurance, tax and advisory services. Tell us what matters to you and find out more by

visiting us at www.pwc.com/il

Thank You!

Alon Sherer, Senior Tax Manager, PwC [email protected]

Larry Croock, Senior Tax Manager, PwC [email protected]