24

State of Global Retailing A Closer Look at Russia Artem Bektemirov, CEO Pharmacy Chain 36.6 NRF Annual Meeting 16 January 2005

| Date post: | 30-Dec-2015 |

| Category: |

Documents |

| Upload: | darrel-buckley |

| View: | 36 times |

| Download: | 0 times |

State of Global RetailingState of Global Retailing

A Closer Look at Russia

Artem Bektemirov, CEOPharmacy Chain 36.6NRF Annual Meeting

16 January 2005

2

Soviet-Style

Retailing

3

Retailing

Today

4

Shopping at

Apteka 36.6

5

RUSSIA: #1 EMERGING RETAIL GROWTH MARKETRUSSIA: #1 EMERGING RETAIL GROWTH MARKET

Ranking CountryCountry

RiskMarket

AttractivenessMarket

SaturationTime

Pressure Score

1 Russia 56 56 77 100 100

2 India 62 34 92 72 88

3 China 71 42 62 90 86

A.T. Kearney’s 2004 Global Retail Development Index

6

Market Growth: 10% annual growth in the next 5 years. Already one of the 10 largest retail markets in the world.

Strong Economy: Driven by strong trade balance, growth in productivity and investment, and fiscal responsibility.

Market Opportunities: With rising incomes, consumers seek greater quality and choice offered by modern formats.

Government Support: Relatively liberal policies in consumer economy balance traditional hurdles.

Strong Local Players Emerging: Russia retailers now emerging with operating efficiencies comparable to international benchmarks.

WHY RUSSIA IS #1 RETAIL GROWTH MARKETWHY RUSSIA IS #1 RETAIL GROWTH MARKET

7

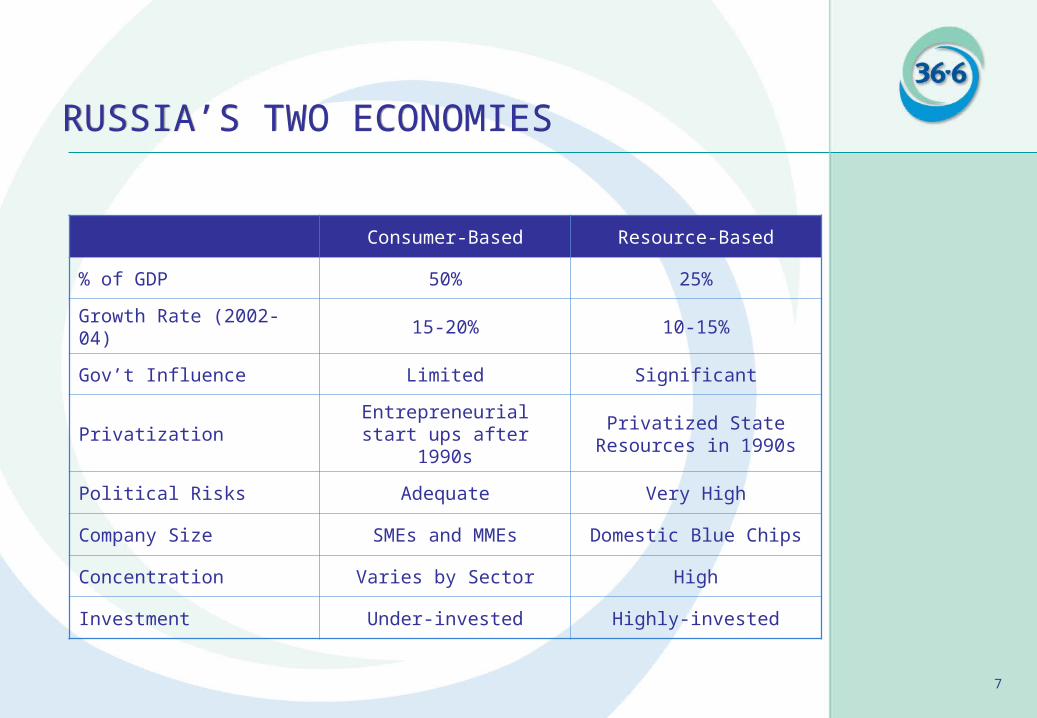

RUSSIA’S TWO ECONOMIESRUSSIA’S TWO ECONOMIES

Consumer-Based Resource-Based

% of GDP 50% 25%

Growth Rate (2002-04) 15-20% 10-15%

Gov’t Influence Limited Significant

PrivatizationEntrepreneurial start ups

after 1990sPrivatized State Resources

in 1990s

Political Risks Adequate Very High

Company Size SMEs and MMEs Domestic Blue Chips

Concentration Varies by Sector High

Investment Under-invested Highly-invested

8

Real growth of consumer income and retail turnover % y-o-y

11.9

8.5 8.9

14.6

10.2

9.09.0

10.9

9.2

8.0

9.28.5

0.0

2.0

4.0

6.0

8.0

10.0

12.0

14.0

16.0

2000 2001 2002 2003 2004F 2005F

Income Retail turnover

Source: State statistic committee, IRG estimations

6-Year Annual

Average:

Retail:

9.1%

Income:

10.3%

RUSSIA’S RETAIL MARKET:$170 BILLION AND GROWINGRUSSIA’S RETAIL MARKET:$170 BILLION AND GROWING

9

Source: GKS, UFG, Euromonitor

RETAIL MARKET SEGMENTSRETAIL MARKET SEGMENTSAnnual

Forecast Growth 2004-2010*

Electronics 15%

DIY 14%

Food 12%

Cosmetics 11%

Pharmaceuticals 9%

*nominal USD, CAGR

Apparel13%

Other19%

Food47% Furniture

7%

Consumer electronics

4%Cosmetics & toiletries

4%2%

DIY4%

Pharmaceuticals

10

5%Food

36%Electronics

9%DIY

6%Pharmaceuticals

Source: UFG Research

Top-5 Players’ Marketshare

RUSSIAN RETAIL MARKETREMAINS FRAGMENTEDRUSSIAN RETAIL MARKETREMAINS FRAGMENTED

Food:

Metro

Electronics:

Eldorado

Pharmaceuticals:

36.6

DIY:

Starik Hottabych

Top Russian

Retailers

11

Sales per Square Meter (2002)

15500

14080

16500

9400

5600

4900

22000Tesco

Sainsbury

Safeway

Morrisons

Pyaterochka

Perekrestok

Sedmoy Kontinent

USD

FOOD RETAIL: RUSSIA vs. INTERNATIONALFOOD RETAIL: RUSSIA vs. INTERNATIONAL

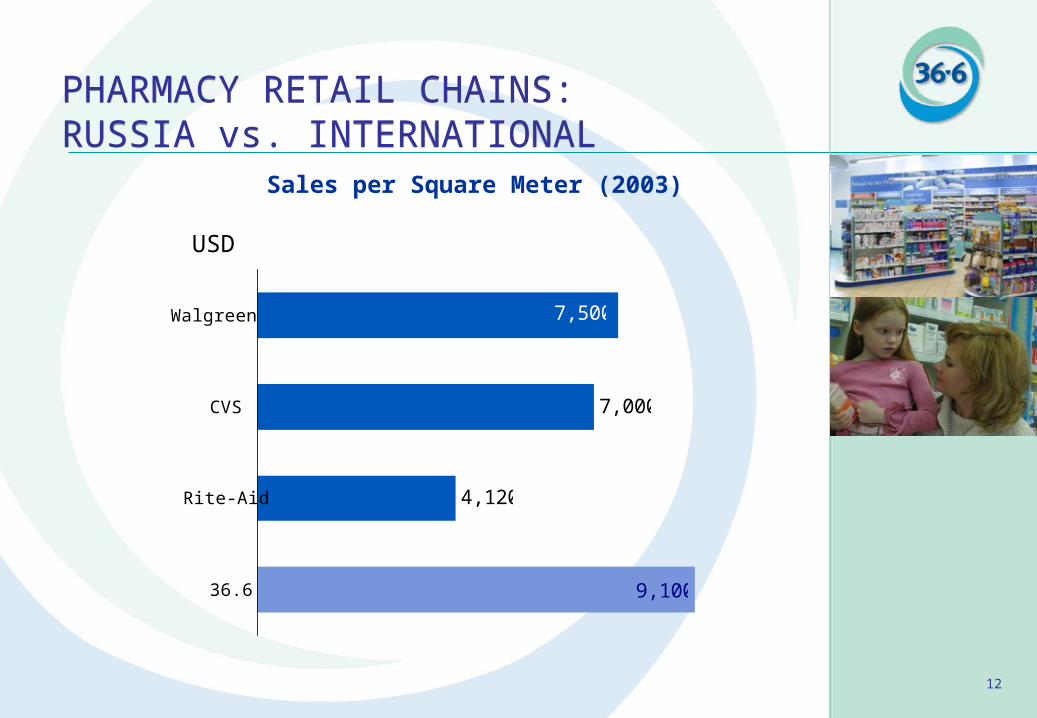

12

Sales per Square Meter (2003)

7,000

4,120

7,500

9,100

Walgreen

CVS

Rite-Aid

36.6

USD

PHARMACY RETAIL CHAINS: RUSSIA vs. INTERNATIONALPHARMACY RETAIL CHAINS: RUSSIA vs. INTERNATIONAL

13

RUSSIAN RETAIL: FUTURE TRENDSRUSSIAN RETAIL: FUTURE TRENDS

New Formats: New and different formats (DIY, convenience stores).

Consolidation: Small chains bought by larger retailers.

Regional Expansion: Cities with population +1 million.

Foreign Retailers: Continued expansion over next 2 - 3 years.

Large Format Retail: Trade centers and hypermarkets.

14

RUSSIAN RETAIL: MAIN BARRIERSRUSSIAN RETAIL: MAIN BARRIERS

Capital: Lack of investments for domestic retail chain development.

Consumer Income: Low income of Russian population outside Moscow.

Real Estate Shortage/Prices: Lack of space and high rental and purchase prices.

Competition: Particularly with unorganized trade and open markets.

Bureaucracy & Red Tape.

15

Source: Pharmexpert, RMBC, DSM, 36.6

617 660 706 749 786 826 867

3,0543,378

3,7364,137

4,5884,979

5,402

2003 2004F 2005F 2006F 2007F 2008F 2009F

Moscow

Regions

Russia 3,6714,038

4,4424,886

5,3755,805

6,269

2003-2009 CAGR*

Russia

9.3%

Regions

10%

Moscow

5.8%

*Compound Annual Growth Rate

USD Millions

PHARMACEUTICAL MARKET FORECASTPHARMACEUTICAL MARKET FORECAST

16

*Includes medical devices (blood pressure meters, thermometers, glucometers, etc.), first aid (adhesive bandages, wound care materials, etc.), patient care products, specialty hosiery and support products.

Source: Euromonitor, Pharmexpert, Supplier data, Internal estimates

163 199 237 278 322 368 413180

200240

288

346

415

498

2002 2003 2004F 2005F 2006F 2007F 2008F

Dietary supplements

Other*

Total PPh 343399

477

566

667

783

911

2003-2009 CAGR

Total PPh

18%

Other

20%

Supplements

15.8%

USD Millions

PARA-PHARMACEUTICAL MARKET FORECASTPARA-PHARMACEUTICAL MARKET FORECAST

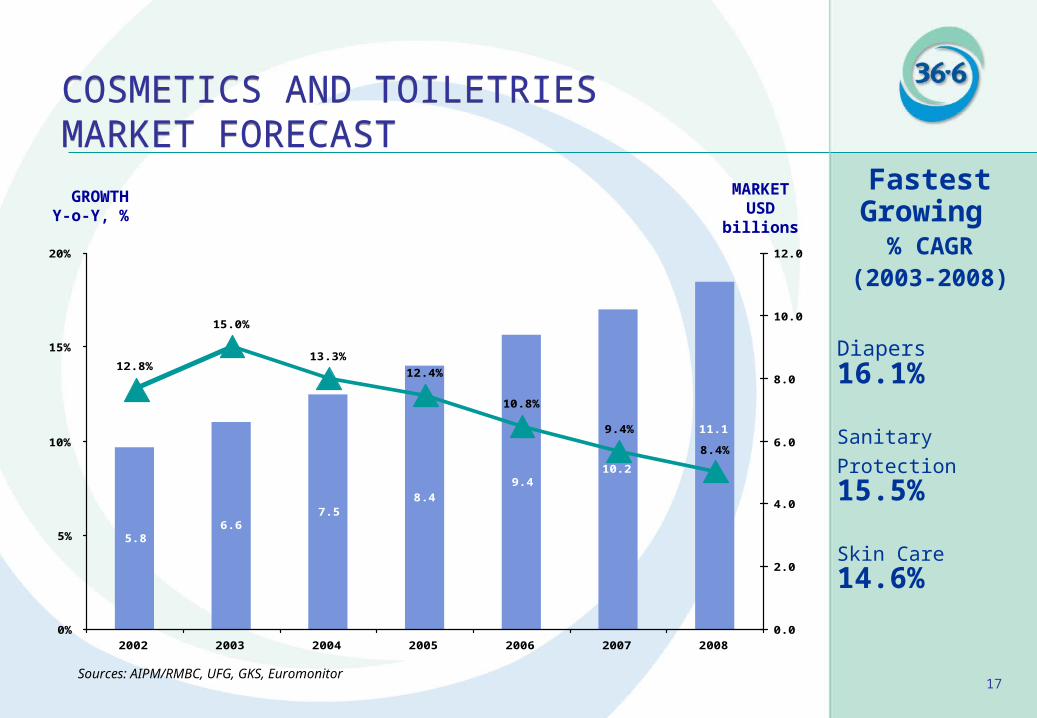

17

5.86.6

7.58.4

9.410.2

11.1

12.8%

15.0%

13.3%

12.4%

10.8%

9.4%

8.4%

0%

5%

10%

15%

20%

2002 2003 2004 2005 2006 2007 20080.0

2.0

4.0

6.0

8.0

10.0

12.0

Sources: AIPM/RMBC, UFG, GKS, Euromonitor

GROWTHY-o-Y, %

MARKETUSD billions

COSMETICS AND TOILETRIES MARKET FORECASTCOSMETICS AND TOILETRIES MARKET FORECAST

Diapers 16.1%

SanitaryProtection 15.5%

Skin Care 14.6%

Fastest Growing

% CAGR(2003-2008)

Pharmacy Chain 36.6

Russia’s Leading Health and Beauty Retailer

19

sales in 2003. EBITDA was 9.3% in 2003.

market capitalization. 20% of shares placedin 2003 IPO.

topline annual growth: 30% in retail, 20% inmanufacturing.

in 7 Russian regions.

purchases in 4th quarter 2004.

in the generic portfolio of Veropharm.

skilled personnel and experiencedmanagement team.

250pharmacies

145million

25%

290products

6000employees

147.8million

7.3million

36.6 AT A GLANCE36.6 AT A GLANCE

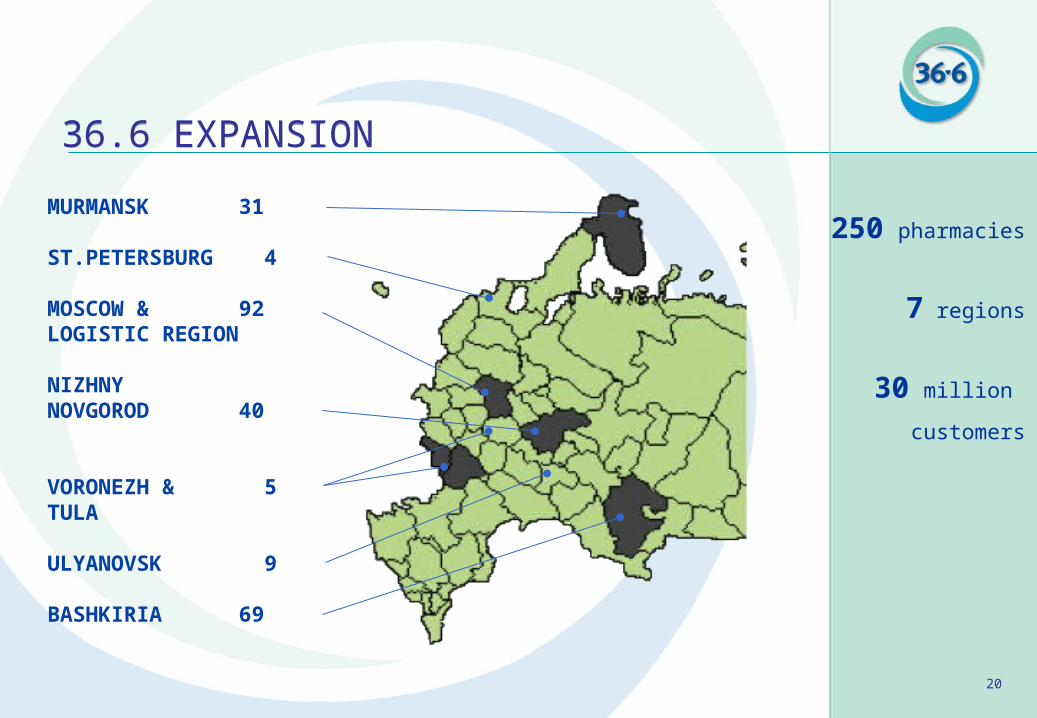

20

250 pharmacies

7 regions

30 million

customers

MURMANSK 31

ST.PETERSBURG 4

MOSCOW & 92LOGISTIC REGION

NIZHNYNOVGOROD 40

VORONEZH & 5TULA

ULYANOVSK 9

BASHKIRIA 69

36.6 EXPANSION36.6 EXPANSION

21

72.4%

67.2%

63.2%

63.0%

62.6%

58.9%

56.2%

56.2%

52.3%

51.2%

36.6

GUM

TsUM

IKEA

Detsky Mir

Starik Khottabych

Technosila

M.Video

Okhotny Ryad

Mir

Source: Gallup Media Survey, 2003

Also leads in:

attendance 49%purchases 40%

36.6 IS RUSSIA’S MOST RECOGNIZABLE BRAND36.6 IS RUSSIA’S MOST RECOGNIZABLE BRAND

22

We strive to increase the value of the company by providing our customers with a reason to come back.

CUSTOMER VALUE PROPOSITIONCUSTOMER VALUE PROPOSITION

Convenient locations.

Reliable quality products.

Excellent shopping experience.

Wide assortment.

Competitive prices.

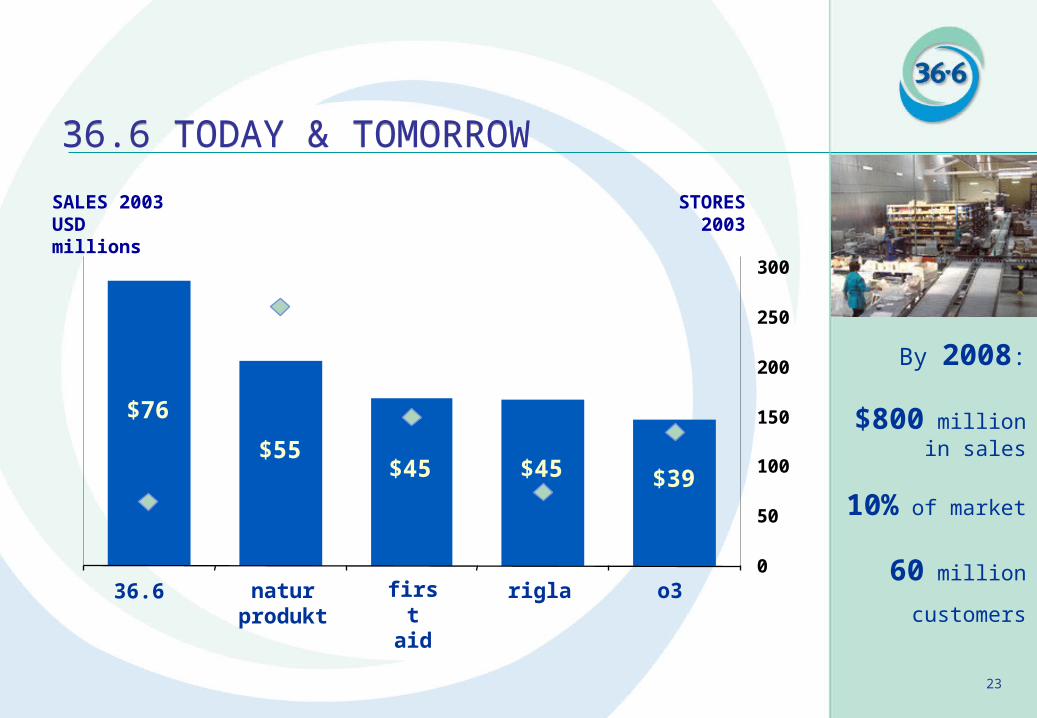

23

By 2008:

$800 million in sales

10% of market

60 million

customers

36.6 TODAY & TOMORROW36.6 TODAY & TOMORROW

0

50

100

150

200

250

300

$55

$76

$45 $45 $39

STORES2003

SALES 2003USD millions

36.6 o3riglafirst aid

natur produkt

24

Address: 105082 Moscow,36 Bolshaya Pochtovaya str.

Tel.: +7 (095) 792-5207Fax: +7 (095) 792-5206E-mail: [email protected]

www.pharmacychain366.com