STATE OF ILLINOIS ILLINOIS COMMERCE COMMISSION Northern Illinois Gas Company ) d/b/a Nicor Gas Company ) ) Petition Pursuant to Rider QIP ) Docket No. 19-0294 of schedule of Rates for Gas Service ) to initiate a Proceeding to Determine ) the Accuracy and Prudence of ) Qualifying Infrastructure Investment ) PUBLIC VERSION DIRECT TESTIMONY OF SEBASTIAN COPPOLA ON BEHALF OF THE PEOPLE OF THE STATE OF ILLINOIS AG Exhibit 1.0 December 13, 2019

Transcript

STATE OF ILLINOIS

ILLINOIS COMMERCE COMMISSION

Northern Illinois Gas Company )

d/b/a Nicor Gas Company )

)

Petition Pursuant to Rider QIP ) Docket No. 19-0294

of schedule of Rates for Gas Service )

to initiate a Proceeding to Determine )

the Accuracy and Prudence of )

Qualifying Infrastructure Investment )

PUBLIC VERSION

DIRECT TESTIMONY OF

SEBASTIAN COPPOLA

ON BEHALF OF

THE PEOPLE OF THE STATE OF ILLINOIS

AG Exhibit 1.0

December 13, 2019

ICC Docket No. 19-0294

Direct Testimony of Sebastian Coppola

AG Exhibit 1.0 PUBLIC

2

TABLE OF CONTENTS

I. Introduction ..............................................................................................................................5

II. Summary Conclusions and Recommendations .....................................................................9

III. Infrastructure Cost Incurred ... ...........................................................................................11

IV. Nicor Gas Attestation of Prudency ... ..................................................................................13

V. Assessment of the 2018 Rider QIP Reconciliation .... .........................................................14

VI. Projects with Large Cost Variances ....................................................................................16

A. Copper Services Replacement ..........................................................................................19

B. Norridge Cast Iron Main Replacement ...........................................................................22

C. Franklin Park Main Replacement ...................................................................................23

D. Glenview Main Replacement ...........................................................................................25

E. Oak Lawn Main Replacement .........................................................................................26

F. Princeton Main Replacement ...........................................................................................28

G. Landscaping and Paving Carryover Costs .....................................................................29

H. Carpentersville Main Replacement .................................................................................30

I. Norridge Cast Iron Services Replacement .......................................................................31

J. Ancona Storage Field Gathering Lines ............................................................................33

K. Horizon Station Odorizer Replacement .........................................................................36

L. Summary ............................................................................................................................37

VII. Project Change Order .........................................................................................................38

A. Railway ROE Approval Issues.........................................................................................39

B. Other Change Order Issues ..............................................................................................44

VIII. Acceptance of Higher Cost Bids ........................................................................................54

A. Aux Sable Pipeline Replacement .....................................................................................55

B. Paving Restoration Zone 2 ...............................................................................................58

C. Paving Restoration Zone 3 ...............................................................................................60

D. Paving Restoration Zone 6 ...............................................................................................62

E. Summary ............................................................................................................................64

IX. Project Not Bid Out ...............................................................................................................65

X. Lack of Contractor Audits ....................................................................................................69

XI. Exclusion of Gas Storage Infrastructure Costs ..................................................................71

XII. Other Observations ..............................................................................................................72

ICC Docket No. 19-0294

Direct Testimony of Sebastian Coppola

AG Exhibit 1.0 PUBLIC

3

EXHIBIT LIST

AG Ex. 1.1 Sebastian Coppola Regulatory Experience and Qualifications 1

AG Ex. 1.2 Nicor Gas Responses to DR AG 3.01, AG 5.01, AG 1.07(Docket 18-1775) 2

AG Ex. 1.3 CONF Nicor Gas Response to DR AG 5.16 with Exhibit 1 CONF 3

AG Ex. 1.4 Nicor Gas Responses to DR MEM 1.03 (Ex. 1), AG 4.10 (Ex. 3), AG 5.15 4

AG Ex. 1.5 Copper Services QIP Cost and Surcharge Adjustment 5

AG Ex. 1.6 Nicor Gas Responses to DR AG 4.25, AG 5.28 6

AG Ex. 1.7 Hudson Compressor Capital Additions Disallowance 7

AG Ex. 1.8 Franklin Park Main QIP Cost and Surcharge Adjustment 8

AG Ex. 1.9 Glenview Main QIP Cost and Surcharge Adjustment 9

AG Ex. 1.10 Oak Lawn Main QIP Cost and Surcharge Adjustment 10

AG Ex. 1.11 Princeton Main QIP Cost and Surcharge Adjustment 11

AG Ex. 1.12 Carryover Restoration Main QIP Cost and Surcharge Adjustment 12

AG Ex. 1.13 Carpentersville Main QIP Cost and Surcharge Adjustment 13

AG Ex. 1.14 Norridge Cast Iron Services QIP Cost and Surcharge Adjustment 14

AG Ex. 1.15 Ancona C & D Gathering Lines QIP Cost and Surcharge Adjustment 15

AG Ex. 1.16 Horizon Station Odorizer Replacement QIP Cost and Surcharge Adjustment 16

AG Ex. 1.17 Nicor Gas Response to DR AG 3.11 17

AG Ex. 1.18 CONF Nicor Gas Response to DR AG 3.11 Exhibit 1A, pages 178-182 18

AG Ex. 1.19 CONF Nicor Gas Response to DR AG 3.11 Exhibit 1A, pages 183-188 19

AG Ex. 1.20 CONF Nicor Gas Response to DR AG 3.11 Exhibit 1A, pages 218-218 20

AG Ex. 1.21 CONF Nicor Gas Response to DR AG 3.11 Exhibit 1A, pages 252-253 21

AG Ex. 1.22 CONF Nicor Gas Response to DR AG 3.11 Exhibit 1B, pages 35-40 22

AG Ex. 1.23 CONF Nicor Gas Response to DR AG 5.04 23

AG Ex. 1.24 Railway ROW Change Orders QIP Cost and Surcharge Adjustment 24

AG Ex. 1.25 CONF Nicor Gas Response to DR AG 3.11 Exhibit 1A, pages 57-58 25

AG Ex. 1.26 CONF Nicor Gas Response to DR AG 3.11 Exhibit 1A, pages 302-303 26

AG Ex. 1.27 CONF Nicor Gas Response to DR AG 3.11 Exhibit 1B, pages 67-68 27

AG Ex. 1.28 CONF Nicor Gas Response to DR AG 3.11 Exhibit 1C, page 159 28

AG Ex. 1.29 CONF Nicor Gas Response to DR AG 3.11 Exhibit 1C, page 303 29

AG Ex. 1.30 CONF Nicor Gas Response to DR AG 3.11 Exhibit 1C, pages 188-189 30

AG Ex. 1.31 CONF Nicor Gas Response to DR AG 3.11 Exhibit 1D, page 31

ICC Docket No. 19-0294

Direct Testimony of Sebastian Coppola

AG Exhibit 1.0 PUBLIC

4

AG Ex. 1.32 Other Change Orders QIP Cost and Surcharge Adjustment 32

AG Ex. 1.33 CONF Nicor Gas Responses to DR AG 4.20 (Ex. 3 CONF and Ex. 4 CONF) 33

AG Ex. 1.34 CONF Nicor Gas Responses to DR AG 5.23 CONF (Ex. 1 CONF) 34

AG Ex. 1.35 CONF Nicor Gas Resp. DR MEM 1.02 (Ex. 13 App. B, p.4), AG 4.22, AG 5.25 35

AG Ex. 1.36 CONF Nicor Gas Resp. DR MEM 1.02 (Ex. 13 App. B, p.5), AG 4.23, AG 5.26 36

AG Ex. 1.37 CONF Nicor Gas Resp. DR MEM 1.02 (Ex. 13 App. B, p.8), AG 4.24, AG 5.27 37

AG Ex. 1.38 Bids Accepted Over Lower Bids QIP Cost and Surcharge Adjustment 38

AG Ex. 1.39 Nicor Gas Response to DR AG 5.06 39

AG Ex. 1.40 Nicor Gas Response to Data Request AG 23.25 from Docket No. 18-1775 40

ICC Docket No. 19-0294

Direct Testimony of Sebastian Coppola

AG Exhibit 1.0 PUBLIC

5

I. INTRODUCTION 41

Q. PLEASE STATE YOUR NAME AND BUSINESS ADDRESS. 42

A. My name is Sebastian Coppola. My business address is 5928 Southgate Rd., Rochester, 43

Michigan 48306. 44

Q. BY WHOM ARE YOU EMPLOYED AND IN WHAT CAPACITY? 45

A. I am President of Corporate Analytics, Inc., a business consulting firm specializing in 46

financial and strategic business issues in the fields of energy and utility regulation. 47

Q. PLEASE SUMMARIZE YOUR PROFESSIONAL QUALIFICATIONS. 48

A. I have more than forty years of experience in public utility and related energy work, both 49

as a consultant and utility company executive. I have been an independent consultant for 50

more than 15 years. Before that, I spent three years as Senior Vice President and Chief 51

Financial Officer of SEMCO Energy, Inc. with responsibility for all financial operations, 52

corporate development and strategic planning for the company’s Michigan and Alaska 53

regulated gas utility operations and non-regulated businesses. During the period at 54

SEMCO Energy, I also had responsibility for certain storage and pipeline operations as 55

President and COO of SEMCO Energy Ventures, Inc. Prior to SEMCO, I was Senior 56

Vice President of Finance for MCN Energy Group, Inc., the parent company of Michigan 57

Consolidated Gas Company. 58

During my 24-year career at MCN and MichCon, I held various analytical, accounting, 59

managerial and executive positions, including Manager of Gas Accounting with 60

ICC Docket No. 19-0294

Direct Testimony of Sebastian Coppola

AG Exhibit 1.0 PUBLIC

6

responsibility for maintaining the accounting records and preparing financial reports for 61

gas purchases and gas production. Over the years, I also held the positions of Treasurer, 62

Director of Investor Relations, Director of Accounting Services, Manager of Corporate 63

Finance, and Manager of Customer Billing. Additionally, I have been responsible for and 64

have managed several new pipeline and construction projects, as well as the 65

implementation of information technology projects. 66

I have testified in several regulatory proceedings before various regulatory commissions. 67

I have prepared and/or filed testimony in general rate case proceedings, revenue 68

decoupling reconciliations, gas conservation programs, gas cost and power supply cost 69

recovery reconciliation mechanisms, and pipeline and meter infrastructure replacement 70

cases. 71

In recent years, I have filed testimony in several infrastructure replacement cases on 72

behalf of the Illinois Attorney General and the Citizens Utility Board before the Illinois 73

Commerce Commission (“the Commission” or “ICC”) pertaining to Peoples Gas and 74

Coke’s accelerate main replacement program and Rider QIP reconciliations. I also 75

submitted testimony in the last Nicor Gas rate case, ICC Docket 18-1775. 76

AG Exhibit 1.1 describes my regulated-energy qualifications in more detail and a list of 77

cases in which I have testified in different jurisdictions. 78

Q. WHAT IS THE PURPOSE OF YOUR TESTIMONY IN THIS CASE? 79

A. On November 9, 2018, Northern Illinois Gas Company, d/b/a Nicor Gas Company, 80

(“Nicor Gas, or “Company”) filed a petition under Docket No. 19-0294 before the Illinois 81

ICC Docket No. 19-0294

Direct Testimony of Sebastian Coppola

AG Exhibit 1.0 PUBLIC

7

Commerce Commission (“the Commission” or “ICC”) to initiate an annual reconciliation 82

proceeding, pursuant to Rider QIP of its Schedule of Rates for Gas Service (“Rider QIP”), 83

in order to determine the accuracy and the prudence of the qualifying infrastructure plant 84

investments for the calendar year 2018. 85

I have been asked by the Office of the Attorney General, on behalf of the People of the 86

State of Illinois (“AG”), to provide an independent analysis of the prudency and 87

reasonableness of the qualifying infrastructure costs incurred in 2018, and present related 88

recommendations for adjustments to costs, the Rider QIP Tariff, and management 89

practices. 90

Q. WHAT TOPICS ARE YOU ADDRESSING IN YOUR TESTIMONY? 91

A. My review is mainly limited to the larger QIP capital expenditures incurred by Nicor Gas 92

during 2018, and the processes and practices applied by the Company in planning and 93

completing the construction of various projects. 94

Specifically, I will address the following topics in this case: 95

1. Company witness Patrick Whiteside’s attestation about the reasonableness and 96

prudency of the 2018 QIP costs; 97

2. Cost disallowances related to certain projects with significant cost overruns, or 98

inadequate evidence to support the actual expenditures; 99

3. Cost disallowances related to imprudent approval of contractor change orders; 100

4. Acceptance of higher project bids above the lowest acceptable bid; 101

5. Poor project bidding practices; 102

ICC Docket No. 19-0294

Direct Testimony of Sebastian Coppola

AG Exhibit 1.0 PUBLIC

8

6. Lack of contractor audits of billed costs and lack of transparency on contractors’ 103

work performance; and 104

7. Inclusion of non-qualified infrastructure plant projects within the Rider QIP 105

Tariff. 106

The absence of a discussion of other matters in my testimony should not be taken as an 107

indication that I agree with those aspects of Nicor Gas’s QIP filing. My testimony is, 108

instead, a consequence of focusing on priority issues within the resources available to me. 109

Other AG witnesses may identify other proposed disallowances that may be additive to the 110

recommendations made in this testimony. 111

Q. DO YOU HAVE ANY EXHIBITS SUPPORTING YOUR TESTIMONY? 112

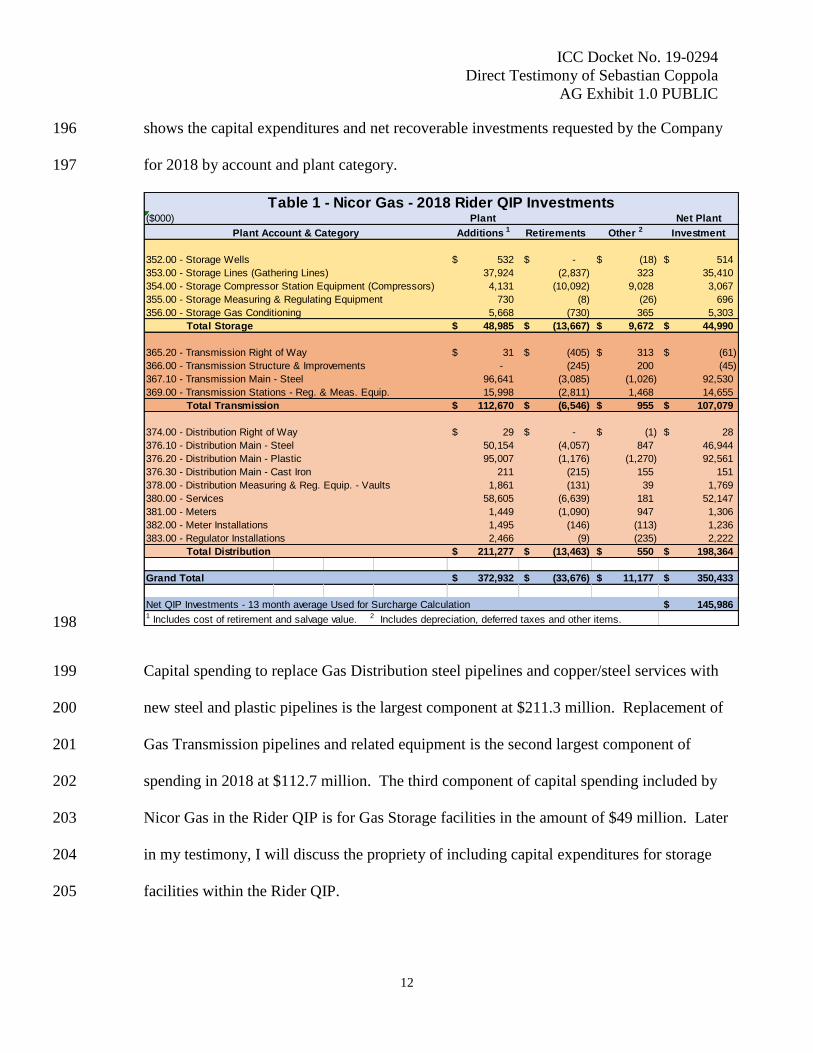

A. Yes. I am sponsoring AG Exhibits 1.1 through 1.40. 113

Q. WHAT INFORMATION HAVE YOU RELIED UPON IN FORMULATING YOUR 114

RECOMMENDATIONS? 115

A. I have relied on Nicor Gas’s testimony, exhibits, and data request responses provided in 116

this docket. I have also relied on pertinent information from the Company’s last general 117

rate case in Docket No. 18-1775 and other select information from Nicor’s prior Rider 118

QIP reconciliation case filings. 119

In addition, I have read, and I am familiar with, the Rider QIP tariff filed by the Company 120

with the Commission, and Section 9-220.3 of the Public Utilities Act that authorized the 121

Commission to establish the Rider QIP tariff surcharge, including the transcript1 of the 122

1 Available at: https://www.icc.illinois.gov/downloads/public/edocket/366197.pdf (approved by ICC

January 7, 2014).

ICC Docket No. 19-0294

Direct Testimony of Sebastian Coppola

AG Exhibit 1.0 PUBLIC

9

deliberations of the Illinois House of Representatives in passing legislation in May 2013 123

authorizing the establishment of the Rider QIP. 124

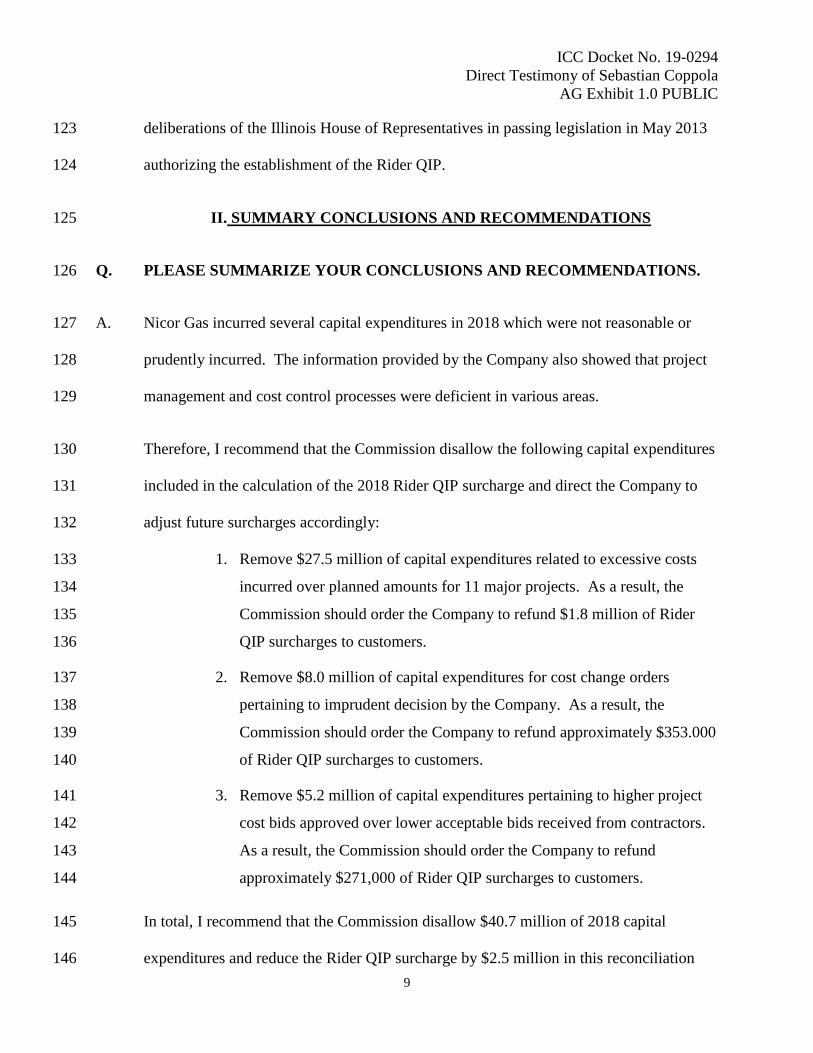

II. SUMMARY CONCLUSIONS AND RECOMMENDATIONS 125

Q. PLEASE SUMMARIZE YOUR CONCLUSIONS AND RECOMMENDATIONS. 126

A. Nicor Gas incurred several capital expenditures in 2018 which were not reasonable or 127

prudently incurred. The information provided by the Company also showed that project 128

management and cost control processes were deficient in various areas. 129

Therefore, I recommend that the Commission disallow the following capital expenditures 130

included in the calculation of the 2018 Rider QIP surcharge and direct the Company to 131

adjust future surcharges accordingly: 132

1. Remove $27.5 million of capital expenditures related to excessive costs 133

incurred over planned amounts for 11 major projects. As a result, the 134

Commission should order the Company to refund $1.8 million of Rider 135

QIP surcharges to customers. 136

2. Remove $8.0 million of capital expenditures for cost change orders 137

pertaining to imprudent decision by the Company. As a result, the 138

Commission should order the Company to refund approximately $353.000 139

of Rider QIP surcharges to customers. 140

3. Remove $5.2 million of capital expenditures pertaining to higher project 141

cost bids approved over lower acceptable bids received from contractors. 142

As a result, the Commission should order the Company to refund 143

approximately $271,000 of Rider QIP surcharges to customers. 144

In total, I recommend that the Commission disallow $40.7 million of 2018 capital 145

expenditures and reduce the Rider QIP surcharge by $2.5 million in this reconciliation 146

ICC Docket No. 19-0294

Direct Testimony of Sebastian Coppola

AG Exhibit 1.0 PUBLIC

10

through the O Factor adjustment. In addition, I recommend that the Commission instruct 147

the Company to remove the disallowed capital expenditures from the calculation of future 148

Rider QIP surcharges and from the Company’s rate base when filing changes to its 149

distribution base rates in the next general rate case. 150

By removing the disallowed capital expenditures from rate base for imprudence, consumers 151

will not be required to pay the principal amount of capital expenditures, which in this case 152

is approximately $40.7 million. In addition, the Company forfeits the return on the 153

disallowed capital expenditures over the depreciable life of those capital additions. 154

Furthermore, the Commission should: 155

a. Direct the Company that in future Rider QIP reconciliations it will identify all 156

capital projects that were competitively bid, the bids considered and selected, 157

and if capital projects of at least $250,000 in value were not competitively bid 158

individually, or combined with other projects, explain and justify why not. 159

b. Direct the Company to perform annual audits of the amounts billed by any 160

contractor who bills the Company at least $5 million for work performed 161

during the annual QIP program. The absence of such audits in future Rider 162

QIP reconciliations should be considered a failure to attest as to the 163

reasonableness and prudency of the costs included in the QIP program. 164

c. Direct the Company to exclude gas storage related plant additions and 165

retirements from future Rider QIP plans and reconciliations. My conclusion is 166

that storage-related capital expenditures were never intended to be included in 167

the Rider QIP program and the Company has expanded the definition of 168

Qualifying Infrastructure Plant beyond its actual and intended purpose. 169

d. Direct the Company that in future Rider QIP reconciliation filings include 170

testimony and other exhibits to provide through explanations of (1) the major 171

projects completed during the Rider QIP reconciliation year; (2) any 172

ICC Docket No. 19-0294

Direct Testimony of Sebastian Coppola

AG Exhibit 1.0 PUBLIC

11

significant variance of 10% or greater in the cost of the major projects 173

completed during the year in comparison to the plan filed with the 174

Commission; (3) QIP projects that had been planned for the year, but were 175

later deferred and not completed, as well as new projects added that were not 176

initially planned; (4) the number and amount of change orders affecting 177

capital expenditures for QIP projects and an explanation of the more 178

significant cost change orders exceeding $250,000; (5) how the Company 179

prioritized the projects for public safety and reliability; and (6) other useful 180

information that justify undertaking the QIP projects completed during the 181

reconciliation year. 182

The remainder of my testimony provides further details and support to these summary 183

conclusions and recommendations. 184

III. INFRASTRUCTURE COSTS INCURRED 185

Q. PLEASE BRIEFLY SUMMARIZE THE 2018 QIP RIDER RECONCILIATION 186

FILING MADE BY NICOR GAS. 187

A. Nicor Gas filed the testimony and exhibits of Matthew Kim and Patrick Whiteside to 188

provide an accounting of the infrastructure capital costs incurred in 2018 and explanations 189

of how in their opinion they conform to the Rider QIP statute and rate tariff. The Company 190

also filed affidavits and attestations required under the Rider QIP rate tariff. 191

According to the filing, in 2018 the Company incurred capital spending costs of 192

approximately $350.4 million net of retirements, disposal costs and deferred taxes, as 193

shown in Nicor Gas Ex. 1.1. The amount of gross plant additions, including cost of 194

removal and salvage value, for the 2018 Rider QIP was $372.9 million. Table 1 below 195

ICC Docket No. 19-0294

Direct Testimony of Sebastian Coppola

AG Exhibit 1.0 PUBLIC

12

shows the capital expenditures and net recoverable investments requested by the Company 196

for 2018 by account and plant category. 197

198

Capital spending to replace Gas Distribution steel pipelines and copper/steel services with 199

new steel and plastic pipelines is the largest component at $211.3 million. Replacement of 200

Gas Transmission pipelines and related equipment is the second largest component of 201

spending in 2018 at $112.7 million. The third component of capital spending included by 202

Nicor Gas in the Rider QIP is for Gas Storage facilities in the amount of $49 million. Later 203

in my testimony, I will discuss the propriety of including capital expenditures for storage 204

Total Distribution 211,277$ (13,463)$ 550$ 198,364$

Grand Total 372,932$ (33,676)$ 11,177$ 350,433$

Net QIP Investments - 13 month average Used for Surcharge Calculation 145,986$ 1 Includes cost of retirement and salvage value. 2 Includes depreciation, deferred taxes and other items.

Table 1 - Nicor Gas - 2018 Rider QIP Investments

Plant Account & Category

ICC Docket No. 19-0294

Direct Testimony of Sebastian Coppola

AG Exhibit 1.0 PUBLIC

13

Based on the net 2018 Rider QIP plant investments of $350.4 million, the average cost base 206

on which the Company could earn a return was approximately $146 million, as shown on 207

page 9 of Nicor Gas Ex. 1.1, and also on line 1, column A, of page 1 of Nicor Gas Ex. 1.6. 208

The return on this cost base is $17.3 million as reported by the Company.2 209

AG witness Mary Selvaggio presents the impact of my adjustments to the 2018 recoverable 210

QIP costs in AG Ex. 2.1, along with other adjustments she has identified. 211

IV. NICOR GAS ATTESTATION OF PRUDENCY 212

Q. PLEASE PROVIDE YOUR ASSESSMENT OF THE ATTESTATION BY 213

COMPANY WITNESS WHITESIDE THAT THE RIDER QIP CAPITAL 214

EXPENDITURES WERE PRUDENTLY INCURRED. 215

A. On page 1 of his direct testimony. Mr. Whiteside states that he is responsible for the 216

Company’s top line growth and for the customer development teams focused on improving 217

gas utilization and streamlining customer additions to the Nicor Gas system. Additionally, 218

he stated that he is responsible for leading the Company’s planning and execution of 219

investment in qualifying infrastructure plant, workforce development, strategic capital asset 220

portfolio design, strategic operational projects and the energy efficiency program.3 221

On page 2 of his direct testimony, he “conclude[s] that the costs of the Rider QIP 222

infrastructure investments for the 2018 reconciliation period were prudently incurred.” 223

2 Nicor Gas Ex. 1.6, page 1.

3 Nicor Gas Ex. 2.0, page 1.

ICC Docket No. 19-0294

Direct Testimony of Sebastian Coppola

AG Exhibit 1.0 PUBLIC

14

In the subsequent pages of his seven pages of direct testimony, Mr. Whiteside provides a 224

summary of the categories of qualifying plant additions allowed under the Rider QIP tariff, 225

plus a summary of the number of units installed or replaced, and a summary statement on 226

the prioritization approach taken to select projects for the Rider QIP program. The rest of 227

his testimony addresses the number of jobs attributable to the Rider QIP program. 228

Nowhere in his testimony does Mr. Whiteside explain what direct involvement he has with 229

the Rider QIP program or on what basis he can attest that the costs incurred in 2018 were 230

reasonable and prudently incurred. In fact, in response to a data request, the Company 231

shows that Mr. Whiteside is not a member of the Project Management Group responsible to 232

manage and direct the execution of the QIP projects. 233

His involvement with the QIP program appears to be so significantly removed from the 234

operation of the program that it renders his attestation of the prudency and reasonableness 235

of the costs incurred in 2018 meaningless. Therefore, I recommend that the Commission 236

disregard the attestation by Mr. Whiteside that all the QIP costs incurred by the Company 237

were reasonable or prudently incurred. Instead, based on my testimony, the Commission 238

should find that certain costs were not prudently incurred and should be removed from the 239

recoverable base on which the Rider QIP surcharges during 2018 were calculated. 240

V. ASSESSMENT OF THE 2018 RIDER QIP RECONCILIATION 241

Q. PLEASE PROVIDE YOUR OVERALL ASSESSMENT OF THE PRUDENCY AND 242

REASONABLENESS OF THE COSTS INCLUDED IN THE 2018 RIDER QIP 243

RECONCILIATION. 244

ICC Docket No. 19-0294

Direct Testimony of Sebastian Coppola

AG Exhibit 1.0 PUBLIC

15

A. In 2018, the Company continued to significantly ramp up its QIP capital expenditures, 245

taking advantage of the cost recovery mechanism permitted by the enactment of the Rider 246

QIP beginning in 2014. As stated earlier, the Company spent approximately $372.9 million 247

on QIP projects in 2018. In comparison, in 2017 it spent $327.2 million. Although the 248

capital spending increased in 2018, the number of miles of pipe replaced decreased. In 249

2017, the Company replaced 84 miles of vintage plastic, vintage steel and bare steel 250

pipelines. In 2018, the number of miles of pipe replaced declined to 70 miles.4 251

Similarly, Nicor Gas replaced 15,847 service lines in 2018, which was a lower number than 252

the 16,346 services replaced in 2017.5 Therefore, with regard to gas distribution projects, 253

the increase in capital spending from 2017 to 2018 does not track with the number of miles 254

of mains and services replaced. 255

It is also concerning that the Company had planned to replace 106 miles of vintage plastic, 256

vintage steel, and bare steel pipe in 2018. However, it actually replaced only 70 miles, or 257

66% of the planned miles, while still increasing 2018 capital expenditures over the prior 258

year. AG Exhibit 1.2 includes the Company’s responses to data request AG 1.07 (Docket 259

No. 18-1775), AG 3.01 and AG 5.01 showing this information. 260

In my review of the Company’s capital expenditures on various QIP projects, I have 261

identified several issues with the level of capital spending, cost change order requests, poor 262

bidding acceptance practices, and other problems with the Company’s actions and practices. 263

4 In Nicor Gas Ex. 2.2 in Docket Nos. 19-0294 and 18-0621, the Company reports 161.2 miles of vintage

and bare steel main replaced/installed in 2018 and 139.3 miles in 2017. Although the number of miles

installed can differ somewhat from the miles retired, it is not clear why these quantities differ significantly

from the Company’s response to data requests AG 1.07 (Docket No. 18-1775) and AG 5.01 included in AG

Ex. 1.2. 5 Nicor Gas Ex. 2.2 in Docket Nos. 19-0294 and 18-0621.

ICC Docket No. 19-0294

Direct Testimony of Sebastian Coppola

AG Exhibit 1.0 PUBLIC

16

These occurrences warrant several cost disallowances from the amount of capital 264

expenditures and related costs that the Company seeks to recover in this reconciliation case. 265

In the following pages of my testimony, I describe the most egregious cases and identify 266

recommended cost disallowances and adjustments to the Rider QIP surcharge billings. 267

Table 2 below identifies my summary assessment of the capital expenditures that should be 268

disallowed for 2018 and the related adjustments to the surcharge billings. 269

270

In total, I have identified approximately $40.7 million of capital expenditure disallowances 271

in the reconciliation of the 2018 Rider QIP. Approximately $27.5 million relate to large 272

cost variances between planned costs and actual costs for 11 construction projects. An 273

additional $8 million of disallowed capital expenditures pertains to change orders where 274

imprudent decisions were made by the Company. The other $5.2 million of capital 275

disallowances pertain to projects where the Company accepted higher cost bids than the 276

lower acceptable bid from contractors. 277

Capital Surcharge

Expenditures Revenue

Large Cost Variance Projects 27,489,988$ 1,836,372$

Project Change Orders 7,995,208 353,090

Bid Amounts Over Lowest Bid 5,219,618 270,707

Total Disallowance 40,704,814$ 2,460,169$

1 Source: AG Witness Coppola Testimony and Exhibits.

Table 2

2018 Nicor Gas Rider QIP Disallowances 1

ICC Docket No. 19-0294

Direct Testimony of Sebastian Coppola

AG Exhibit 1.0 PUBLIC

17

The proposed disallowances for each of these categories are explained in the following 278

pages of my testimony. 279

VI. PROJECTS WITH LARGE COST VARIANCES 280

Q. PLEASE EXPLAIN YOUR FINDINGS FROM REVIEWING MAJOR PROJECTS 281

WITH LARGE COST VARIANCES. 282

A. In discovery, the Company was asked to provide a reconciliation of the projects and costs 283

proposed in the 2018 QIP plan update, filed with the Commission under Section J of the 284

Rider 32 QIP tariff, against the actual costs incurred for the projects completed in 2018. 285

The Company also was asked to provide a comparison of actual costs incurred and units 286

installed in 2018 versus prior years for major project categories. 287

In response to several data requests, the Company provided a report of 189 major projects 288

with planned costs, actual costs, cost variances, units planned and installed, and 289

explanations for cost variances. AG Exhibit 1.3 CONF includes a copy of the report 290

provided in response to data request AG 5.16 along with the confidential exhibit. 291

The 189 major projects planned for 2018 had a total projected cost of $338.9 million. 292

During the year, the Company decided to defer 28 projects to future years. The capital cost 293

of these projects totals $32.7 million. Thus, the remaining 161 projects completed in 2018 294

had a total projected cost of $306.2 million. In comparison, the Company incurred actual 295

capital expenditures of $359.5 million for the remaining 161 projects. Therefore, actual 296

costs for the 161 projects exceeded the projected cost by $53.3 million, an overall variance 297

of 17% over the projected cost. 298

ICC Docket No. 19-0294

Direct Testimony of Sebastian Coppola

AG Exhibit 1.0 PUBLIC

18

Q. DID YOU IDENTIFY LARGE VARIANCES BETWEEN PLANNED AND ACTUAL 299

EXPENDITURES IN CERTAIN PROJECTS THAT RAISE CONCERNS ABOUT 300

THE REASONABLENESS AND PRUDENCY OF THE COST INCURRED FOR 301

THOSE PROJECTS? 302

A. Yes. Of the 161 projects completed in 2018, 134 had variances of 10% or greater. Of the 303

134 projects with variances of 10% or greater, 78 had positive variances (actual costs above 304

planned costs) with 39 of them having variances of greater than 50% above the planned cost 305

amount. The remaining 56 projects of the 134 projects with variances of 10% or greater had 306

negative variances of varying degrees with some exceeding 50%. AG Exhibit 1.3 CONF 307

provides the full list of projects and related cost variances. 308

The explanations provided by the Company for the larger variances are generally attributed 309

to project estimates not being final when the QIP plan was developed. The Company also 310

attributes the increase in costs to higher installation and restoration costs, permit delays, 311

difficult ground conditions, prior year carryover costs, etc. The large variances raise 312

concerns about the adequacy of the Company’s project planning practices, the accuracy of 313

forecasted costs provided to the Commission, and the adequacy of project management cost 314

controls. 315

Based on my review of the information provided by the Company, I have identified 11 316

projects where the explanations and justifications are inadequate or not credible, and a 317

disallowance of a portion of the project actual capital expenditures is warranted. The total 318

capital expenditures disallowance amount for the 11 projects is $27.5 million. The Rider 319

QIP surcharge adjustment refundable to customer from the capital expenditures 320

ICC Docket No. 19-0294

Direct Testimony of Sebastian Coppola

AG Exhibit 1.0 PUBLIC

19

disallowance is $1.8 million. I will discuss each of the disallowances in my testimony 321

below. 322

A. Copper Services 323

Q. PLEASE EXPLAIN YOUR FINDINGS AND DISALLOWANCE OF CAPITAL 324

EXPENDITURES FOR COPPER SERVICES. 325

A. In response to data request AG 4.10, the Company provided the actual cost incurred to 326

complete replacement of 4,630 copper services during 2018 at $23,015,860, or $4,971 per 327

service line. In the plan filed with the Commission, the Company had projected that it 328

would replace 5,500 services in 2018 at a cost of $20,139,000, or cost per unit of $3,662. 329

The Company spent approximately $2.9 million more to replace 870 fewer services at a 330

higher unit cost. 331

The information provided by the Company in response to Staff data request MEM 1.03 332

(Exhibit 1) shows that the unit cost to replace copper service in 2017 was $3,557 and in 333

2016 it was $2,182. In discovery, the Company was asked to explain the cost increase 334

experienced in 2018 over prior years. In response to data request AG 4.10(b), the Company 335

stated that the cost increase was due to completion of more copper service replacements by 336

outside contractor crews than by Company crews. 337

Asked to explain why copper service line replacement costs by contractor crews is more 338

costly than using Company employees, the Company stated that contractor crew sizes are 339

larger than Company crews. The Company also provided service line installation cost data 340

ICC Docket No. 19-0294

Direct Testimony of Sebastian Coppola

AG Exhibit 1.0 PUBLIC

20

that shows Company crews are able to complete an average service line installation for 341

$3,026, while the contractor charges $7,246, or 2.4 times more. 342

The Company was also asked to explain why it did not hire and use more employees to 343

perform service line replacement given the large cost difference. In response, the Company 344

stated that it had limited internal resources to replace copper services, and in an effort to 345

replace copper service by the end of 2019 additional outside resources were required. 346

Instead of hiring additional full-time employees for work that was not sustainable, the 347

Company decided to utilize resources. Although on the surface these reasons appear 348

plausible, they are not credible when reviewing the Company’s practices in prior years. 349

In 2018, Company employees replaced 54% of the total copper services replaced that year. 350

In 2017, they replaced 71% of all copper service replaced that year. The percentage 351

replaced by Company employees reached 88% in 2016. While in 2015, only 59% of the 352

copper services were replaced by Company employees. Therefore, the Company had 353

staffed for and dedicated more Company crews to complete copper service line 354

replacements in 2016 and 2017, and could have kept those internal crews into 2018 to 355

complete more copper service replacements at a much lower cost. 356

AG Exhibit 1.4 and 1.6 include the information provided by the Company in response to 357

several data requests discussed above. 358

Q. DID THE COMPANY BID OUT THE SPECIFIC SERVICE LINE REPLACEMENT 359

PROJECTS TO MULTIPLE CONTRACTORS TO ENSURE THE WORK WAS 360

COMPLETED AT THE LOWEST COMPETITIVE COST? 361

ICC Docket No. 19-0294

Direct Testimony of Sebastian Coppola

AG Exhibit 1.0 PUBLIC

21

A. No. It does not appear that the Company competitively bid out the specific projects either 362

as a total group or by sub-groups in specific areas to multiple contractors in order to 363

determine that the work would be completed at the lowest cost within the applicable 364

standards. In response to a data request, the Company stated that it performs service line 365

replacement under blanket contracts which are not bid out annually.6 The lack of 366

competitive bids likely was a contributing factor to the excessive cost billed by the 367

contractors above the cost per service line incurred through installations by Company 368

employees. Later in my testimony, I will discuss in more detail my concerns with the 369

Company’s contractor work bidding practices. 370

Q. DID YOU CALCULATE THE INCREMENTAL AVOIDABLE COST OF USING 371

MORE COMPANY CREWS INSTEAD OF CONTRACTOR CREWS TO 372

COMPLETE THE COPPER SERVICE LINE REPLACEMENTS IN 2018? 373

A. Yes. I have determined that if the Company had maintained the same average mix of 374

service line replacement with Company crews as it did in 2017 and 2016, it could have 375

reduced capital expenditures in 2018 by approximately $9.7 million. 376

I determined this amount by taking the average cost to replace copper services in 2017 and 377

2016 of $2,870 per service line7 and multiplied it by the 4,630 services completed in 2018 in 378

order to calculate a total cost of $13.3 million. The difference between the $13.3 million 379

and the actual cost of $23.0 million incurred by the Company in 2018 is $9.7 million. This 380

6 Nicor Gas response to DR AG 5.06 included in AG Ex. 1.39 7 In response to data request Staff MEM 1.03 Exhibit 1, the Company reported that it installed 7,232 copper

services at a cost of $25,727,021, or $3,557 per service. It also reported that in 2016 it installed 10,032

copper services at a cost of 21,894,501, or $2,182 per service. The average cost for the two years is $2,870

per copper service installed. AG Exhibit 1.4 includes this information.

ICC Docket No. 19-0294

Direct Testimony of Sebastian Coppola

AG Exhibit 1.0 PUBLIC

22

incremental cost is not reasonable and was not prudently incurred. Therefore, I recommend 381

that the Commission remove $9.7 million from the 2018 QIP capital investments. 382

Assuming the capital expenditures were incurred evenly throughout 2018, the adjustment to 383

the QIP surcharge is $718,301, as calculated in AG Exhibit 1.5 using the Company financial 384

model shown in Nicor Gas Ex. 1.1. 385

B. Norridge-Chicago #119620 Cast Iron Main Replacement 386

Q. PLEASE EXPLAIN YOUR FINDINGS AND DISALLOWANCE OF CAPITAL 387

EXPENDITURES FOR THE NORRIDGE-CHICAGO CAST IRON MAIN 388

REPLACEMENT. 389

A. In data request AG 4.25, the Company was asked to explain why it spent $6.7 million to 390

retire and replace 1.4 miles of cast iron main in 2018 at a cost of $4.8 million per mile, when 391

in 2017 and 2016 it spent $968,000 and $809,000 per mile, respectively. In its initial 392

response, the Company stated that the main drivers for the cost increase per mile were 393

carryover costs for landscape and paving from the prior year with no associated miles of 394

pipe replaced in 2018. In addition, the Company stated that the last 1.4 miles of cast iron 395

main replaced in the Norridge-Chicago area involved road openings and tight city 396

coordination, which increased the average cost per mile. 397

In a follow up data request, the Company was asked to explain in more detail the amount of 398

carryover costs, the categories of costs where the higher costs were incurred and specifically 399

why. In response to data request AG 5.28, the Company stated that carryover costs were 400

$1.6 million of the $6.7 million, leaving still $5.1 million of costs in 2018 for 1.4 miles of 401

main. The Company also explained that the Norridge-Chicago main replacement required 402

ICC Docket No. 19-0294

Direct Testimony of Sebastian Coppola

AG Exhibit 1.0 PUBLIC

23

$1.5 million in incremental landscaping and paving costs due to City of Chicago permit 403

requirements. After adjusting for this incremental cost, the remaining amount is $3.6 404

million. AG Exhibit 1.6 includes the Company response to data requests AG 4.25 and AG 405

5.28. 406

If we use the cost per mile of cast iron main replaced in 2017 of $968,000 and multiply it by 407

the 1.4 miles replaced in 2018, the expected cost is approximately $1.4 million. Comparing 408

this amount to the $3.6 million of remaining costs from the actual amount spent in 2018 409

leaves $2.2 million of costs incurred in 2018 that the Company has not justified. 410

It is also noteworthy to point out that in the QIP plan filed with the Commission, the 411

Company has projected that it would incur $4.9 million in 2018 to complete this project, 412

including carryover costs. Actual costs exceeded this amount by more than $1.8 million. 413

This is a further indication that the $2.2 million of incremental costs incurred in 2018 for 414

this project are not reasonable, and do not appear to have been prudently incurred. 415

Therefore, I recommend that the Commission remove $2.2 million from the 2018 Rider QIP 416

capital expenditures. Assuming the capital expenditures were incurred evenly throughout 417

2018, the adjustment to the QIP surcharge is $115,331, as calculated in AG Exhibit 1.7 418

using the Company financial model. 419

C. Franklin Park #119662 Main Replacement 420

Q. PLEASE EXPLAIN YOUR FINDINGS AND DISALLOWANCE OF CAPITAL 421

EXPENDITURES FOR THE FRANKLIN PARK MAIN REPLACEMENT 422

PROJECT. 423

ICC Docket No. 19-0294

Direct Testimony of Sebastian Coppola

AG Exhibit 1.0 PUBLIC

24

A. On line 34 of Exhibit 1 CONF to data request AG 5.16 (AG Ex. 1.3 CONF), the Company 424

reported that it planned to retire and replace 8,287 feet of steel main at a cumulative cost of 425

[BEGIN CONFIDENTIAL] 426

427

428

429

. [END CONFIDENTIAL] 430

Although the installation of additional feet of pipe explains part of the increase in cost, it 431

does not explain the entire increase. Using the planned cost of [BEGIN CONFIDENTIAL] 432

433

. [END CONFIDENTIAL] This leaves $684,739 of higher actual costs due to 434

other reasons. In Exhibit 1 CONF to DR AG 5.16, the Company explained that the 435

additional increase in costs was due to higher restoration costs due to permit delays which 436

required the Company to temporarily backfill and restore areas, and later return to redo 437

some of this work.8 438

Having timely permits is a basic task of scheduling work so that work can be completed in 439

the most cost-efficient manner. It is the responsibility of the Company to ensure it has the 440

necessary work permits to complete the work timely and without the need to redo the same 441

work and incur additional costs. Customers should not pay for imprudently incurred costs. 442

Therefore, I recommend that the Commission remove the $684,739 of higher costs incurred 443

by the Company for this project from the total 2018 QIP capital expenditures. Assuming 444

8 See line 34 of Exhibit 1 CONF to the response to data request AG 5.16.

ICC Docket No. 19-0294

Direct Testimony of Sebastian Coppola

AG Exhibit 1.0 PUBLIC

25

that this incremental cost was incurred evenly throughout the year, the applicable reduction 445

in billed Rider QIP surcharge is $35,888, as calculated in AG Exhibit 1.8 using the 446

Company financial model. 447

D. Glenview #120043 Main Replacement 448

Q. PLEASE EXPLAIN YOUR FINDINGS AND DISALLOWANCE OF CAPITAL 449

EXPENDITURES FOR THE GLENVIEW MAIN REPLACEMENT PROJECT. 450

A. On line 36 of Exhibit 1 CONF to data request AG 5.16 (AG Ex. 1.3 CONF), the Company 451

reported that it planned to retire and replace 9,462 feet of steel main at a cost of [BEGIN 452

CONFIDENTIAL] 453

454

455

. 456

[END CONFIDENTIAL] 457

The only explanation provided by the Company was that the main installation and 458

restoration costs were higher than the QIP plan.9 This explanation is inadequate and 459

provides no evidence to justify the significant increase in actual cost over the planned 460

amount. Using the planned cost per mile of [BEGIN CONFIDENTIAL] 461

. [END CONFIDENTIAL] The 462

remaining amount of $1,456,186 is unsupported and unjustified. I recommend that the 463

Commission remove this amount from the total 2018 QIP capital expenditures. Assuming 464

9 See line 36 of Exhibit 1 CONF to the response to data request AG 5.16.

ICC Docket No. 19-0294

Direct Testimony of Sebastian Coppola

AG Exhibit 1.0 PUBLIC

26

that this incremental cost was incurred evenly throughout the year, the applicable reduction 465

in billed Rider QIP surcharge is $76,332, as calculated in AG Exhibit 1.9 using the 466

Company financial model. 467

E. Oak Lawn #120058 Main Replacement 468

Q. PLEASE EXPLAIN YOUR FINDINGS AND DISALLOWANCE OF CAPITAL 469

EXPENDITURES FOR THE OAK LAWN MAIN REPLACEMENT PROJECT. 470

A. On line 58 of Exhibit 1 CONF to data request AG 5.16 (AG Ex. 1.3 CONF), the Company 471

reported that it planned to retire and replace 25,675 feet of steel main at a cost of [BEGIN 472

CONFIDENTIAL] 473

474

475

476

[END CONFIDENTIAL] 477

Although the installation of additional feet of pipe explains part of the increase in cost, it 478

does not explain the entire increase. Using the planned cost of [BEGIN CONFIDENTIAL] 479

480

[END CONFIDENTIAL] This leaves $1,514,406 of higher actual costs due to 481

other reasons. In Exhibit 1 CONF to DR AG 5.16, the Company explained that facilities of 482

other utilities encountered in the right of way increased the difficulty of the pipe installation 483

and increased costs.10 484

10 See line 58 of Exhibit 1 CONF to the response to data request AG 5.16.

ICC Docket No. 19-0294

Direct Testimony of Sebastian Coppola

AG Exhibit 1.0 PUBLIC

27

Performing appropriate due diligence upfront about the conditions of the project, including 485

other utilities’ facilities in the common right-of-way, is a basic step at the time the project is 486

designed and before it is let out for construction work to begin. Also, providing all pertinent 487

information in the request for cost bids allows the contractors to provide accurate cost 488

proposals so the Company can properly select the lowest cost bid that meets all other 489

applicable requirements. This avoids subsequent project cost change orders that increase 490

the cost of the project without an appropriate competitive bidding process. 491

From the information provided by the Company, it appears that it did not do sufficient 492

research and due diligence work up-front to establish the true cost of the project. 493

Information about the location of facilities installed by other utilities in the common right-494

of-way should have been readily available to the Company at the time the project was 495

designed by working collaboratively with the city and other utilities. The failure to 496

determine the existence of those facilities and any additional difficulties that would be 497

encountered in the installation of the main rises to the level of imprudence on the part of the 498

Company. The lack of proper planning for the project should not be rewarded by allowing 499

the Company to recover the large incremental costs incurred for this project. 500

Therefore, I recommend that the Commission remove the $1,514,406 of higher costs 501

incurred by the Company for this project from the total 2018 QIP capital expenditures. 502

Assuming that this incremental cost was incurred evenly throughout the year, the applicable 503

reduction in billed Rider QIP surcharge is $79,392, as calculated in AG Exhibit 1.10 using 504

the Company financial model. 505

ICC Docket No. 19-0294

Direct Testimony of Sebastian Coppola

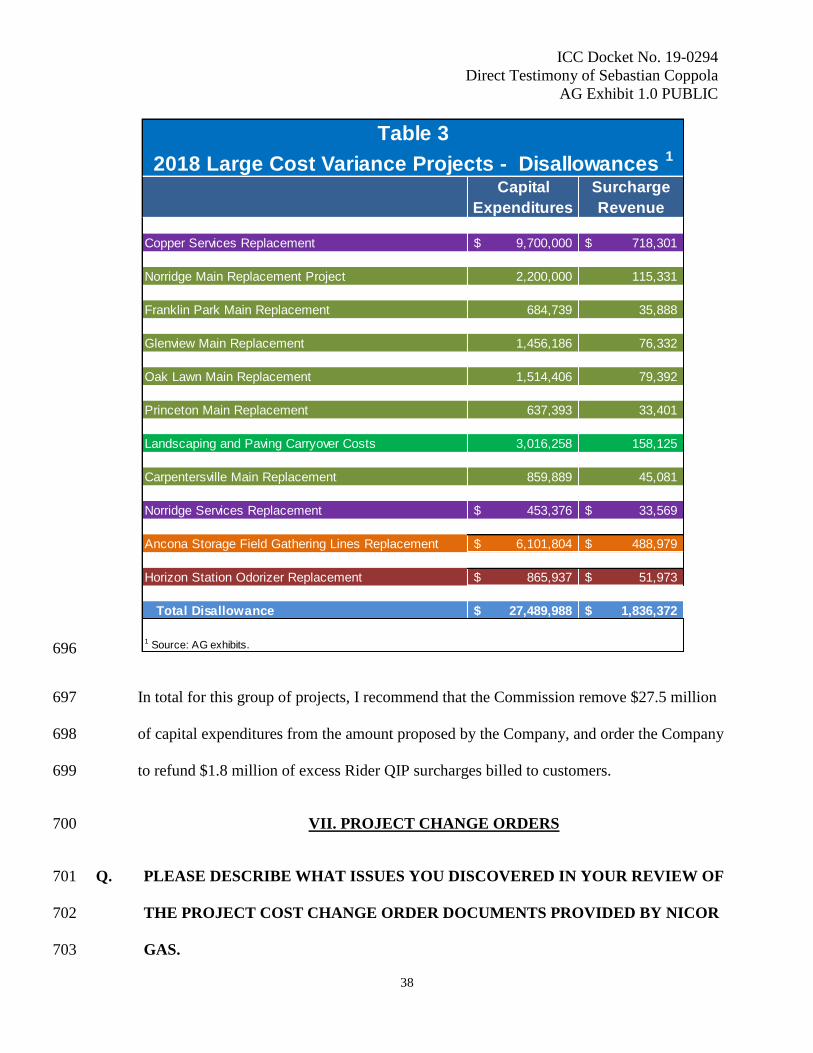

AG Exhibit 1.0 PUBLIC

28

F. Princeton #128621 Main Replacement 506

Q. PLEASE EXPLAIN YOUR FINDINGS AND DISALLOWANCE OF CAPITAL 507

EXPENDITURES FOR THE PRINCETON MAIN REPLACEMENT PROJECT. 508

A. On line 70 of Exhibit 1 CONF to data request AG 5.16 (AG Ex. 1.3 CONF), the Company 509

reported that it planned to retire and replace 11,903 feet of steel main for a cost of [BEGIN 510

CONFIDENTIAL] 511

512

0 513

514

[END CONFIDENTIAL] 515

The only explanation that the Company provided to justify this cost increase was that the 516

main installation and retirement costs were higher than the QIP plan.11 This explanation is 517

inadequate and provides no evidence to justify the significant increase in actual cost over the 518

planned amount. Given that the 10,289 feet of new pipe actually installed was lower than 519

the 11,903 feet planned, the entire amount of cost variance of $637,393 between the actual 520

and planned amounts is unsupported and unjustified. 521

I recommend that the Commission remove this amount from the total 2018 QIP capital 522

expenditures. Assuming that this incremental cost of $637,393 was incurred evenly 523

throughout the year, the applicable reduction in billed Rider QIP surcharge is $33,401, as 524

calculated in AG Exhibit 1.11 using the Company financial model. 525

11 See line 70 of Exhibit 1 CONF to the response to data request AG 5.16.

ICC Docket No. 19-0294

Direct Testimony of Sebastian Coppola

AG Exhibit 1.0 PUBLIC

29

G. Landscaping and Paving Carryover Costs 526

Q. PLEASE EXPLAIN YOUR FINDINGS AND DISALLOWANCE OF CAPITAL 527

EXPENDITURES FOR CARRYOVER LANDSCAPING AND PAVING COSTS 528

PERTAINING TO PRIOR YEAR MAIN REPLACEMENT PROJECTS. 529

A. On line 112 of Exhibit 1 CONF to data request AG 5.16 (AG Ex. 1.3 CONF), the Company 530

reported that it planned to incur [BEGIN CONFIDENTIAL] [END 531

CONFIDENTIAL] during 2018 for landscaping, paving and retirement costs pertaining to 532

various projects completed or undertaken in the prior year. The Company also reported that 533

the actual carryover costs incurred during 2018 were [BEGIN CONFIDENTIAL] 534

[END 535

CONFIDENTIAL] 536

The only explanation that the Company provided was that carryover costs for restoration 537

and retirement were higher than the QIP plan.12 This explanation states the obvious and is 538

inadequate. It provides no evidence to justify the significant increase in actual costs over 539

the planned amount. I recommend that the Commission remove the unexplained and 540

unjustified cost variance of $3,016,258 from the total 2018 QIP capital expenditures. 541

Assuming that this incremental cost was incurred evenly throughout the year, the applicable 542

reduction in billed Rider QIP surcharge is $158,125, as calculated in AG Exhibit 1.12 using 543

the Company financial model. 544

12 See line 112 of Exhibit 1 CONF to the response to data request AG 5.16.

ICC Docket No. 19-0294

Direct Testimony of Sebastian Coppola

AG Exhibit 1.0 PUBLIC

30

H. Carpentersville #128737 Main Replacement 545

Q. PLEASE EXPLAIN YOUR FINDINGS AND DISALLOWANCE OF CAPITAL 546

EXPENDITURES FOR THE CARPENTERSVILLE MAIN REPLACEMENT 547

PROJECT. 548

A. On line 119 of Exhibit 1 CONF to data request AG 5.16 (AG Ex. 1.3 CONF), the Company 549

reported that it planned to retire and replace 2,810 feet of main at a cost of [BEGIN 550

CONFIDENTIAL] 551

552

r 553

554

[END CONFIDENTIAL] 555

The only explanation that the Company provided was that the main installation and 556

retirement costs were higher than the QIP plan.13 This explanation states the obvious and is 557

inadequate. It provides no evidence to justify the significant increase in actual costs over 558

the planned amount. Although the installation of additional feet of pipe explains part of the 559

increase in cost, it does not explain the entire increase. Using the planned cost of [BEGIN 560

CONFIDENTIAL] 561

. [END CONFIDENTIAL] This leaves $859,889 of actual costs 562

due to other reasons, which the Company has not identified, explained, or justified. 563

13 See line 119 of Exhibit 1 CONF to the response to data request AG 5.16.

ICC Docket No. 19-0294

Direct Testimony of Sebastian Coppola

AG Exhibit 1.0 PUBLIC

31

Therefore, I recommend that the Commission remove this amount from the total 2018 QIP 564

capital expenditures. Assuming that this incremental cost was incurred evenly throughout 565

the year, the applicable reduction in billed Rider QIP surcharge is $45,081, as calculated in 566

AG Exhibit 1.13 using the Company financial model. 567

I. Norridge Cast Iron Services Replacement 568

Q. PLEASE EXPLAIN YOUR FINDINGS AND DISALLOWANCE OF CAPITAL 569

EXPENDITURES FOR THE NORRIDGE CAST IRON SERVICES 570

REPLACEMENT PROJECT. 571

A. On line 123 of Exhibit 1 CONF to data request AG 5.16 (AG Ex. 1.3 CONF), the Company 572

reported that it planned to retire and replace 285 cast iron services at a cost of [BEGIN 573

CONFIDENTIAL] 574

575

576

. 577

[END CONFIDENTIAL] 578

The first explanation for the higher cost provided by the Company was that 150 of the 579

services were located under pavement which increased the replacement unit cost for those 580

services.14 In a subsequent response to a follow up data request, the Company explained 581

that when replacing the cast iron services in the City of Chicago – Norridge area all long 582

14 See the response to data request AG 4.10(b), second bulleted item, included in AG Ex. 1.4.

ICC Docket No. 19-0294

Direct Testimony of Sebastian Coppola

AG Exhibit 1.0 PUBLIC

32

side services had to be open cut as part of the permit requirements. Outside the City of 583

Chicago, the Company replaces service lines by directional boring, not open cut.15 584

Performing appropriate due diligence upfront about the conditions of the project, including 585

determining the site conditions of services being located under pavement, as well as the 586

permit requirements of the City of Chicago about replacement of service lines by open cut, 587

are basic steps that should be taken and understood at the time the project is designed and 588

before it is let out for construction work to begin. 589

Additionally, providing all pertinent information in the request for cost bids allows the 590

contractors to provide accurate cost proposals from which the Company can select the 591

lowest cost bid that meets all other applicable requirements. This avoids subsequent project 592

cost change orders that increase the cost of the project without an appropriate competitive 593

bidding process. 594

From the information provided by the Company, it appears that it did not do sufficient 595

research and due diligence work up-front to establish the basic requirements and true cost of 596

the project. Information about the placement of the services below pavement can be 597

readily determined by performing a site visit to the project before or during the design 598

phase. The Company knows the location of its services because it must mark those 599

locations under the JULIE system before customers and other contractors undertake 600

construction work near those service lines. Also, with a portion of its service area in the 601

15 See the response to data request AG 5.15(g) included in AG Ex. 1.4.

ICC Docket No. 19-0294

Direct Testimony of Sebastian Coppola

AG Exhibit 1.0 PUBLIC

33

City of Chicago, the Company knows, or should know, what the permitting requirements are 602

for replacing service lines in the city. 603

The failure to determine the existence of those requirements and difficulties during the 604

design phase of the project rises to the level of imprudence on the part of the Company. The 605

lack of proper planning for the project should not be rewarded by allowing the Company to 606

recover the large incremental costs incurred for this project. 607

Given that the 252 services actually installed were lower than the 285 services planned, the 608

entire amount of cost variance of $453,376 between the actual and planned amount should 609

be removed as unreasonable and imprudently incurred. I recommend that the Commission 610

remove this amount from the total 2018 QIP capital expenditures. Assuming that this 611

incremental cost was incurred evenly throughout the year, the applicable reduction in billed 612

Rider QIP surcharge is $33,569, as calculated in AG Exhibit 1.14 using the Company 613

financial model. 614

J. Ancona Storage Field Gathering Lines (“SFGL”) Replacement 615

Q. PLEASE EXPLAIN YOUR FINDINGS AND DISALLOWANCE OF CAPITAL 616

EXPENDITURES FOR THE ANCONA LINE D AND C STORAGE FIELD 617

GATHERING LINES REPLACEMENT PROJECTS. 618

A. On lines 147 and 148 of Exhibit 1 CONF to data request AG 5.16 (AG Ex. 1.3 CONF), the 619

Company reported that in 2018 it planned to replace 475 feet of the Ancona “D” line 620

gathering system at a cost of [BEGIN CONFIDENTIAL] 621

622

ICC Docket No. 19-0294

Direct Testimony of Sebastian Coppola

AG Exhibit 1.0 PUBLIC

34

623

624

625

. [END 626

CONFIDENTIAL] 627

In its initial explanation the Company stated that the higher cost was attributed to 628

unforeseen site conditions that required more pipe to be installed than had been planned.16 629

In a subsequent response to a follow up data request, the Company explained that the 630

original design and construction plan was to open cut the two 16” gathering lines crossing 631

the Moon Creek. As the projects moved into the construction phase, the Company 632

determined that it would not be possible to properly and safely control the volume of water 633

present in the Moon Creek. Instead, the Company decided to utilize directional drilling to 634

cross the creek with new lines. According to the Company, due to the close proximity of 635

the Moon Creek to IL Route 17, the contour of the land, and the deflection of the pipe, the 636

directional drilling required more pipe than planned with the original open cut approach.17 637

Q. WHAT IS YOUR ASSESSMENT OF THE PROJECT PLANNING WORK AND 638

THE RESULTING INCREASE IN PROJECT COSTS. 639

A. There are at least four main issues that arise from the Company’s explanations about the 640

reason for the tripling in the actual costs to $9.3 million for these two projects from the 641

planned amount of $3.2 million. First, it is difficult to understand why the Company would 642

16 See the response to data request AG 4.10(b), page 2, fifth bulleted item from the top of the page, included

in AG Ex. 1.4. 17 See the response to data request AG 5.15(h) included in AG Ex. 1.4.

ICC Docket No. 19-0294

Direct Testimony of Sebastian Coppola

AG Exhibit 1.0 PUBLIC

35

plan to open cut a trench across a creek with a significant running water stream. Diverting 643

the water stream, in order to cut a trench to remove the old pipe and then install new pipe 644

over a period of multiple weeks is not an easy task. Additionally, when cutting an open 645

trench, there is the risk of environmental damage to the creek bed and contamination of the 646

water stream. From my experience working at two gas utilities and reviewing dozens of 647

construction projects proposed by other utilities in several rate cases, utilities perform such 648

crossings usually through directional drilling under the creek or river bed to avoid the 649

problems described above. 650

Second, installation of a 16” pipeline through directional drilling under a river bed can be a 651

lower cost option than cutting an open trench given the challenges and risks discussed 652

above. The Company has often stated this lower cost preference for directional drilling with 653

other pipeline projects. It is difficult to understand why replacing the pipelines through an 654

open cut trench would have been the preferred option with this project. 655

Third, it is also difficult to understand why directional drilling would require between four 656

and five times more pipe than the open trench approach. Unless the Company was making 657

some wide loops of nearly a half mile past the original pipeline crossing area, the increase in 658

the number of feet of pipe from 475 to 2,031 for the D Line and from 528 to 2,609 feet for 659

the C line seems exceptionally high and likely unnecessary. 660

Fourth, this is another case where a simple site inspection and critical assessment of the two 661

projects up-front should have led to the reasonable conclusion that crossing the creek and 662

replacing the existing pipelines through an open cut trench would not be a workable option. 663

ICC Docket No. 19-0294

Direct Testimony of Sebastian Coppola

AG Exhibit 1.0 PUBLIC

36

In conclusion, it seems clear that the Company did not plan the project in a reasonable and 664

prudent manner. The result was a tripling of the cost of the project for an incremental 665

amount of $6,101,804. The lack of proper planning should not be rewarded by allowing the 666

Company to recover the large incremental costs incurred for the two projects. 667

Therefore, I recommend that the Commission remove the $6,101,804 from the total 2018 668

QIP capital expenditures. Assuming that this incremental cost was incurred evenly 669

throughout the year, the applicable reduction in billed Rider QIP surcharge is $488,979, as 670

calculated in AG Exhibit 1.15 using the Company financial model. 671

K. Horizon Station 125 Odorizer Replacement 672

Q. PLEASE EXPLAIN YOUR FINDINGS AND DISALLOWANCE OF CAPITAL 673

EXPENDITURES FOR THE HORIZON STATION ODORIZER REPLACEMENT 674

PROJECT. 675

A. On line 169 of Exhibit 1 CONF to data request AG 5.16 (AG Ex. 1.3 CONF), the Company 676

reported that it planned to replace the odorizer equipment at the Horizon station at a cost of 677

[BEGIN CONFIDENTIAL] 678

[END CONFIDENTIAL] 679

which is an increase of $865,937 or 156.2% over the planned amount. 680

The only explanation that the Company provided was that the construction costs were 681

higher than the QIP plan.18 This explanation states the obvious and is inadequate. It 682

18 See line 169 of Exhibit 1 CONF to the response to data request AG 5.16.

ICC Docket No. 19-0294

Direct Testimony of Sebastian Coppola

AG Exhibit 1.0 PUBLIC

37

provides no evidence to justify the significant increase in actual costs over the planned 683

amount. This leaves the $865,937 cost variance unexplained and unjustified. 684

Therefore, I recommend that the Commission remove this amount from the total 2018 QIP 685

capital expenditures. Assuming that this incremental cost was incurred evenly throughout 686

the year, the applicable reduction in billed Rider QIP surcharge is $51,973, as calculated in 687

AG Exhibit 1.16 using the Company financial model. 688

L. Summary 689

Q. PLEASE SUMMARIZE THE QIP CAPITAL EXPENDITURES AND RIDER QIP 690

SURCHARGE REVENUE ADJUSTMENTS THAT YOU RECOMMEND. 691

A. The following table summarizes the capital expenditure amounts that I recommend the 692

Commission should remove from the 2018 QIP capital expenditures for the Projects with 693

Large Variances, and the related surcharge revenue that should be refunded to customers for 694

the 2018 Rider QIP reconciliation. 695

ICC Docket No. 19-0294

Direct Testimony of Sebastian Coppola

AG Exhibit 1.0 PUBLIC

38

696

In total for this group of projects, I recommend that the Commission remove $27.5 million 697

of capital expenditures from the amount proposed by the Company, and order the Company 698

to refund $1.8 million of excess Rider QIP surcharges billed to customers. 699

VII. PROJECT CHANGE ORDERS 700

Q. PLEASE DESCRIBE WHAT ISSUES YOU DISCOVERED IN YOUR REVIEW OF 701

THE PROJECT COST CHANGE ORDER DOCUMENTS PROVIDED BY NICOR 702

GAS. 703

Capital Surcharge

Expenditures Revenue

Copper Services Replacement 9,700,000$ 718,301$

Norridge Main Replacement Project 2,200,000 115,331

Franklin Park Main Replacement 684,739 35,888

Glenview Main Replacement 1,456,186 76,332

Oak Lawn Main Replacement 1,514,406 79,392

Princeton Main Replacement 637,393 33,401

Landscaping and Paving Carryover Costs 3,016,258 158,125

Carpentersville Main Replacement 859,889 45,081

Norridge Services Replacement 453,376$ 33,569$

Ancona Storage Field Gathering Lines Replacement 6,101,804$ 488,979$

Horizon Station Odorizer Replacement 865,937$ 51,973$

Total Disallowance 27,489,988$ 1,836,372$

1 Source: AG exhibits.

Table 3

2018 Large Cost Variance Projects - Disallowances 1

ICC Docket No. 19-0294

Direct Testimony of Sebastian Coppola

AG Exhibit 1.0 PUBLIC

39

A. In response to data request AG 3.11, the Company provided several documents pertaining 704

to approximately 60 change orders entered into between Nicor Gas and its construction 705

contractors for QIP projects completed during 2018.19 In my review of the change orders 706

provided by the Company, I discovered 12 situations where the change order was the result 707

of an imprudent action or decision by Nicor Gas which unnecessarily increased the 708

construction cost of the project. The total incremental construction cost from these 12 709

change orders is $7,995,208. These costs were imprudently incurred and should be 710

removed from the QIP capital expenditures included by the Company in this reconciliation 711

case. 712

Five of the change orders pertain to Railway Right-of-Way (“ROW”) approval issues. The 713

remaining seven change orders are for other specific projects. 714

A. Railway ROW Approval Issues 715

Q. PLEASE DESCRIBE THE RAILWAY ROW ISSUES THAT YOU DISCOVERED 716

IN YOUR REVIEW OF THE CHANGE ORDERS. 717

A. In my review, I discovered five change orders where contractors encountered difficulties in 718

completing the project as initially agreed with Nicor Gas. The difficulties arose from the 719

contractor’s inability to complete the work in a railway ROW. In each of these cases, the 720

contractors requested a project cost increase allowance through a change order, which the 721

Company approved. The total incremental cost of the five change orders included in 2018 722

QIP capital expenditures is $5,556,274. I will describe each of them separately. 723

19 AG Ex. 1.17.

ICC Docket No. 19-0294

Direct Testimony of Sebastian Coppola

AG Exhibit 1.0 PUBLIC

40

1. Aux Sable Phase 6 – Project 143642, Change Order 17, Dated 4/12/18: 724

In this change order, the contractor, Precision Pipeline, requested a cost increase allowance 725

of [BEGIN CONFIDENTIAL] 726

727

728

729

[END CONFIDENTIAL]. The 730

full text of the change order and cost is included in AG Ex. 1.18 CONF. The Company 731

approved the change order on April 17, 2018. According to the Company’s response to 732

data request AG 5.04, the actual incremental cost due to the change order included in 2018 733

QIP capital expenditures was $1,639,278.20 734

2. Aux Sable Phase 6 – Project 143642, Change Order 18, Dated 4/12/18: 735

In this change order, the contractor, Precision Pipeline, requested a cost increase allowance 736

of [BEGIN CONFIDENTIAL] 737

738

739

740

[END CONFIDENTIAL]. The 741

full text of the change order and cost is included in AG Ex. 1.19 CONF. The Company 742

approved the change order on April 17, 2018. The actual incremental cost due to the 743

change order included in 2018 QIP capital expenditures was $1,906,471.21 744

20 AG Ex. 1.23 21 AG Ex. 1.23.

ICC Docket No. 19-0294

Direct Testimony of Sebastian Coppola

AG Exhibit 1.0 PUBLIC

41

3. Aux Sable Phase 6 – Project 143642, Change Order 21, Dated 4/21/18: 745

In this change order, the contractor, Precision Pipeline, requested a cost increase allowance 746

of [BEGIN CONFIDENTIAL] 747

748

[END 749

CONFIDENTIAL]. The full text of the change order and cost is included in AG Ex. 1.20 750

CONF. The Company approved the change order on June 12, 2018. The actual 751

incremental cost due to the change order included in 2018 QIP capital expenditures was 752

$265,114.22 753

4. Aux Sable Phase 6 – Project 143642, Change Order 24, Dated 6/25/18: 754

In this change order, the contractor, Precision Pipeline, requested a cost increase allowance 755

of [BEGIN CONFIDENTIAL] 756

757

758

759

e 760

[END CONFIDENTIAL] The full text of the change order and cost is 761

included in AG Ex. 1.21 CONF. The Company approved the change order on June 25, 762

2018. The actual incremental cost due to the change order included in 2018 QIP capital 763

expenditures was $137,196.23 764

22 Id. 23 Id.

ICC Docket No. 19-0294

Direct Testimony of Sebastian Coppola

AG Exhibit 1.0 PUBLIC

42

5. Aux Sable Phase 7 – Project 143645, Change Order 19, Dated 4/12/18: 765

In this change order, the contractor, Precision Pipeline, requested a cost increase allowance 766

of [BEGIN CONFIDENTIAL] 767

768

769

770

[END 771

CONFIDENTIAL] The full text of the change order and cost is included in AG Ex. 1.22 772

CONF. The Company approved the change order on April 17, 2018. The actual 773

incremental cost included in 2018 QIP capital expenditures was $1,608,215.24 774

Q. WHAT IS YOUR ASSESSMENT OF THE FIVE CHANGE ORDERS DESCRIBED 775

ABOVE? 776

A. It appears that the Company ran into difficulties in obtaining permission from CN to cross 777

the railway and to work in the railway ROW as early as September 2017. The Company 778

knew since September 2017 following the CN train derailment that CN had notified Nicor 779

Gas to cease any work in the railroad ROW. AG Ex. 1.40 includes the Company’s response 780

to data request AG-23.25 from Docket No. 18-1775 detailing the sequence of events leading 781

to the cease and desist request by CN. 782

24 Id.

ICC Docket No. 19-0294

Direct Testimony of Sebastian Coppola

AG Exhibit 1.0 PUBLIC

43

Nevertheless, the Company proceeded to schedule the contractor to perform work in an area 783

for which it had no permission to do work, resulting in the contractor incurring additional 784

costs which the Company now wants to recover in this rate case. 785

The change orders indicate that the Company released work to its construction contractors 786

before Nicor Gas had obtained permits or permission to do work in the railway ROW. 787

Such a practice is unusual, and can be risky and very costly, as demonstrated by the cost 788

change orders. The Company should not have released the contractors to begin work on 789

the projects before obtaining the necessary permits or permission for the contractors to 790

work in the railway ROW. 791

By proceeding with the projects without the necessary permits or permission, Nicor Gas 792

incurred cost increases through change orders for a total amount exceeding $5.5 million. 793

This happened on multiple occasions in the construction of the Aux Sable pipeline 794

replacement project during 2018. The number of occurrences clearly shows a pattern of 795

imprudent decisions and actions by Nicor Gas. The incremental costs of $5,556,274 796

incurred for the five change orders are not reasonable and should not be included in the 797

2018 QIP capital expenditures. 798

Q. WHAT IS YOUR RECOMMENDATION? 799

A. I recommend that the Commission disallow the $5,556,274 pertaining to the five change 800

orders for the railway ROW problems from the calculation of the Rider QIP surcharge in 801

this reconciliation case. Based on the information provided by the Company in response to 802

data request AG 5.04(j) (AG Ex. 1.23) and the months when the incremental costs were 803

incurred, I have calculated a Rider QIP surcharge adjustment of $256,949. The calculation 804

ICC Docket No. 19-0294

Direct Testimony of Sebastian Coppola

AG Exhibit 1.0 PUBLIC

44

of the surcharge adjustment was determined using the Company’s financial model and is 805

shown in AG Ex. 1.24. 806

B. Other Change Order Issues 807

Q. PLEASE DESCRIBE WHAT OTHER ISSUES YOU DISCOVERED DURING 808

YOUR REVIEW OF THE CHANGE ORDERS PROVIDED BY NICOR GAS. 809

A. During my review, I discovered 7 additional change orders where the Company incurred 810

excessive cost overruns in certain projects or approved change orders for incremental costs 811

caused by its own imprudent action or lack of action. 812

The total incremental cost of the 7 change orders is $2,438,934 I will describe each of the 813

cost change orders separately. 814

1. Aux Sable Phase 6 – Project 143642, Change Order 11, Dated 5/10/18: 815

In this change order, the contractor, Precision Pipeline, requested a cost increase allowance 816

of [BEGIN CONFIDENTIAL] 817

818

819

820

821

822

823

824

[END CONFIDENTIAL] 825

AG Ex. 1.25 CONF includes the full text of the change order and the related cost. From 826

the information shown in the change order, it appears that the Company did not deliver 827

ICC Docket No. 19-0294

Direct Testimony of Sebastian Coppola

AG Exhibit 1.0 PUBLIC

45

sufficient pipe of the appropriate wall thickness. This failure caused the contractor to incur 828

additional costs for which it requested reimbursement under the change order. 829

Nicor Gas is responsible for providing the contractor with the correct materials at the 830

scheduled time. With this project, it seems clear that the Company failed to deliver the 831

correct material. The result of the imprudent action or inaction on the part of Nicor Gas 832

was an additional cost of [BEGIN CONFIDENTIAL] [END CONFIDENTIAL] 833

to complete the project. Customers should not pay for the Company’s errors in completing 834

a project within the specified design and cost parameters. The additional cost is 835

unreasonable, and the Commission should disallow it from the 2018 QIP capital 836

expenditures in this reconciliation case. 837

2. Aux Sable Phase 6 – Project 143642, Change Order 041, Dated 9/14/18: 838

In this change order, the contractor, Precision Pipeline, requested a cost increase allowance 839

of [BEGIN CONFIDENTIAL] 840

841

842

843

844

845

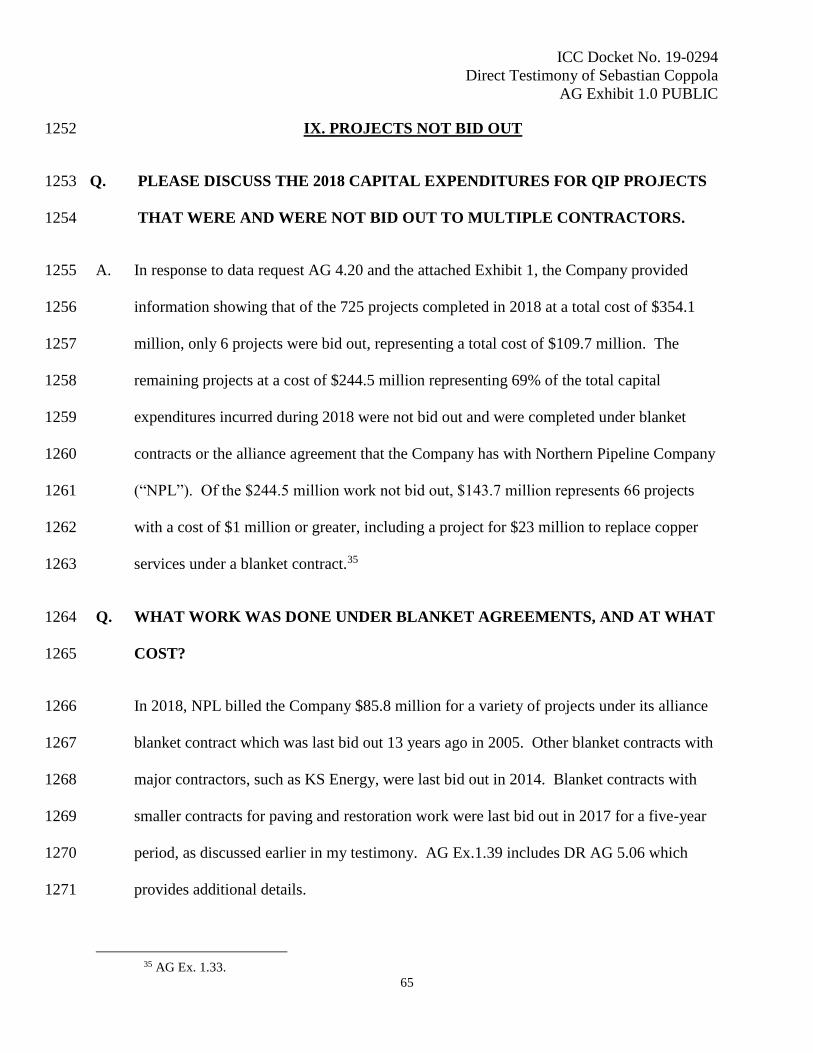

[END CONFIDENTIAL] 846