36

STATE REVENUE RECEIPT – CASE STUDY S. GUNASEKERAN Workshop on State Revenue Report at NAAA, Simla

| Date post: | 23-Dec-2015 |

| Category: |

Documents |

| Upload: | amy-hancock |

| View: | 220 times |

| Download: | 3 times |

STATE REVENUE RECEIPT – CASE STUDY

S. GUNASEKERAN

Workshop on State Revenue Report at NAAA, Simla

Evolution of VATThe concept VAT first conceived by Dr.

Wilhelm von Siemens (Germany) in 1919 with an objective to preventing

cascading effort by giving credit or refund for taxes paid by manufacturer or Dealer. But, VAT first introduced in France in 1954 and spread across the

globe.

It was limited to the boundaries of France till fifties and spread rapidly since sixties. Next to France, Ivory Coast enacted VAT in 1960. Brazil and Denmark in 1967, the Netherlands and Sweden in 1969, Belgium (1971) and Ireland (1972), Italy, UK and Austria in 1973. As of now 130 countries are adopting VAT.

VAT in IndiaIt emerges significance in India in a

different way during 1986 with a name of MODVAT which designed to cover

manufacturers by giving credit of excise duty paid on inputs. The scope was extended to services also with a

name of CENVAT.

The MODVAT was for some selected commodities, whereas CENVAT

brought in 2000-01 budget was wider giving input credit to any final product. Since VAT system was

introduced in manufacturing sector, a uniform tax system was required for

the area of sales.

Hence, Union Finance Minister constituted (1994) a committee of Stat

Finance Ministers to look into the reforms of sales tax including

introduction of VAT.Finally, VAT was introduced on

1.4.2005 by majority of states with state level legislation which are

modeled on the draft prescribed by Central Government.

As per WBVAT Act 2003

• Schedule ‘A’ General rate • Schedule ‘B’ Special rates (123

items)• Schedule ‘C’-Other special rates

(3 items)• 1 item (Tea)• Schedule AA-SEZ and 100% EOU

• In AR 2012-13 – 2126 Assessment cases wherein

• In AR 2012-13 – 21 Assessment cases wherein

• Up to November 2010 12.5%

• After November 2010 13.5%• 4%• 4%• 1%• 0%

• 4% instead of 12.5%-Short levy of Rs.1.05 crore

• 4% instead of 12.5% - short levy of Rs.3.01 crore

Tax Rates under VAT

4% Items of basic needs of society such as medicines, drugs all agricultural and industrial inputs, capital goods.

12.5% All commodities other than 4% VAT category

1% Precious stones, bullion, gold and silver ornaments

Non VAT items(discretionary to respective states)

Petrol, Diesel, ATF, Motor spirit, liquor and lottery tickets

As per WBVAT Act 2003Schedule ‘A’ General rate Up to November 2010 12.5%

After November 2010 13.5%

Schedule ‘B’ Special rates (123 items)

4%

Schedule ‘C’-Other special rates (3 items)

4%

1 item (Tea)

1%

Schedule AA-SEZ and 100% EOU

0%

In AR 2012-13 – 2126 Assessment cases wherein

4% instead of 12.5%-Short levy of Rs.1.05 crore

In AR 2012-13 – 21 Assessment cases wherein

4% instead of 12.5% - short levy of Rs.3.01 crore

Contingent liability to pay tax on some purchases

Section 12 of WBVAT 2003 stipulates that registered dealers shall pay tax on all purchases from unregistered dealers and goods of negative list.

There are 14 items in the negative list.In AR 2012-13, there are 5 cases of such purchases of Rs.1.92 crore with non/short levy of tax Rs.13.46 lakh.In AR 2013-14, there were unregistered purchase of Rs.5.46 crore with non/short levy of tax Rs.44.44 lakh.

Assessment

• Para 2.24• In AR 2012-13, the Assessing Authorities (AAs)

assessed in 10 cases the turnover as Rs.30.30 crore instead of Rs.33.60 crore due to arithmetical errors. This resulted in short levy of Rs.3.30 crore.

• Para 2.21• In AR 2013-14, the AAs assessed the turnover

as Rs.2.48 crore instead of Rs.3.25 crore, thereby short levy of tax by Rs.68.71 lakh.

Contractual transfer price

• Section 14 and 18 of WBVAT Act stipulates that goods, components of works contract is to be taxed.

• Works contractors are entitled for deduction towards labour, service charges, payment to sub-contractor.

• In case proper books of accounts are not maintained to determine the component towards labour, service charges, there is a option for adoption CTP u/s 30(2).

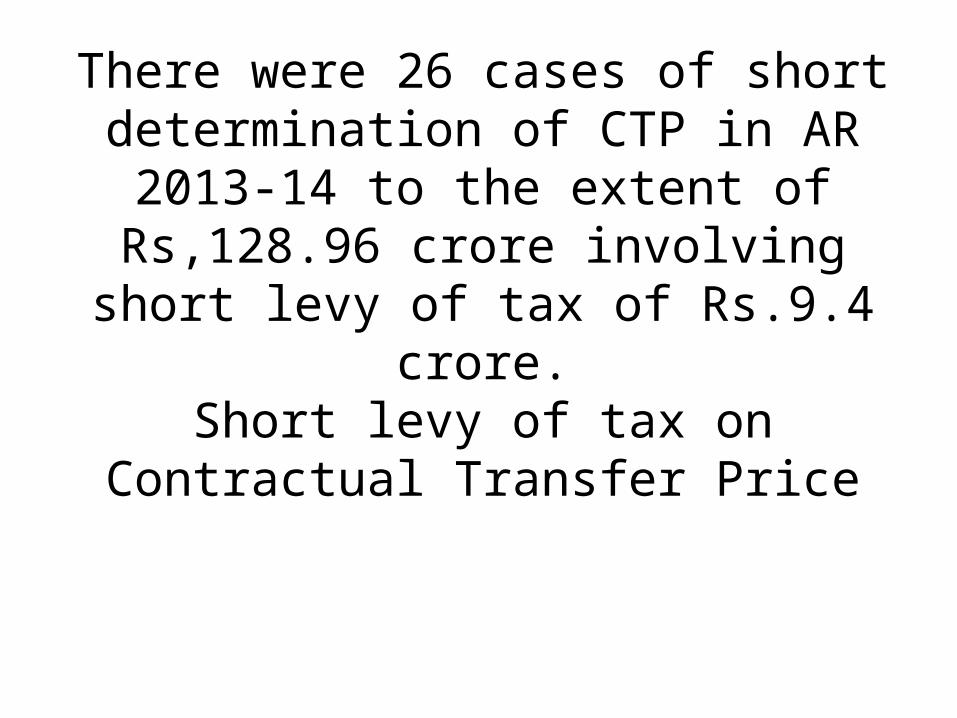

There were 26 cases of short determination of CTP in AR 2013-14

to the extent of Rs,128.96 crore involving short levy of tax of Rs.9.4

crore.Short levy of tax on Contractual

Transfer Price

Sl. No.

Nature of irregularity No. of cases

Taxable CTP assessable

Taxable CTP assessed

Under assessment of taxable CTP

Short levy of tax

Short levy of tax due to non-application of prescribed rates under Rule 30(2) of the WBVAT Rules

6 988.37 447.89 540.48 54.94

Incorrect deductions of payments to sub-contractors, salary, security deposit, installation charges, labour charges and TDS etc.

9 35,363.54 33,355.95 2,007.59 266.85

CTP assessed short than disclosed by the dealers in their returns/ books of accounts/ statement etc

10 16,748.4 6,496.90 10,251.54 608.01

Tax not levied on contractual receipts of pre-registration period

1 156.36 60.26 96.10 11.50

Total 26 53,256.71 40,361 12,895.71 941.30

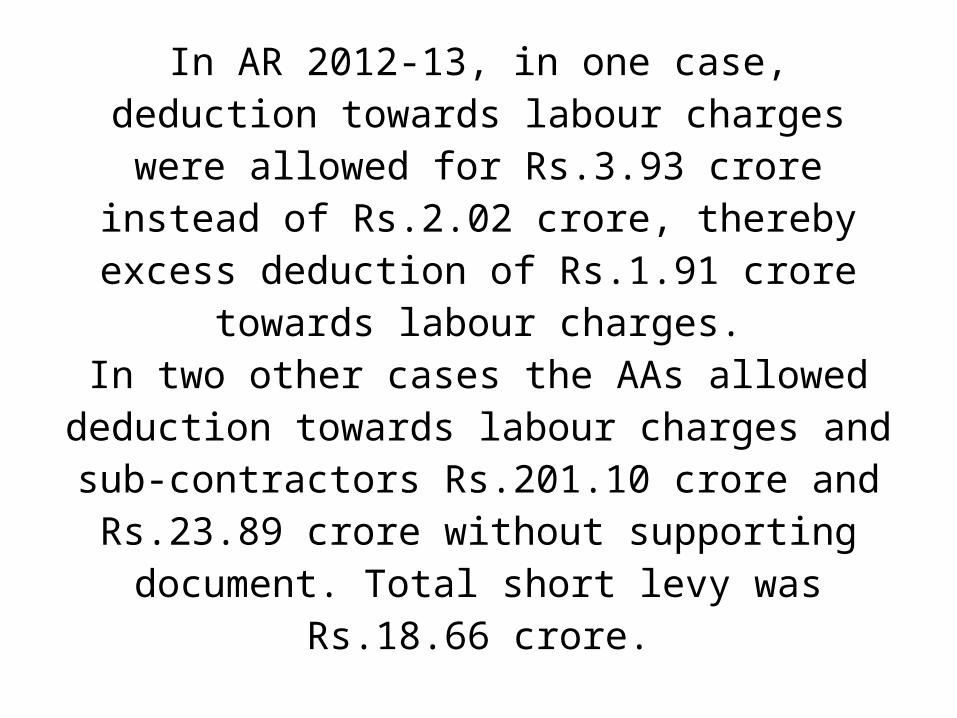

In AR 2012-13, in one case, deduction towards labour charges were allowed for

Rs.3.93 crore instead of Rs.2.02 crore, thereby excess deduction of Rs.1.91 crore

towards labour charges.In two other cases the AAs allowed

deduction towards labour charges and sub-contractors Rs.201.10 crore and Rs.23.89 crore without supporting document. Total

short levy was Rs.18.66 crore.

Irregular allowance of stock transfer due to defective ‘F’ Form

As per Section 6A of CSC Act deduction towards inter-state stock transfer are

allowable on single ‘F’ Form for a calendar month.

There was a non compliance to above provision which led to short levy of Rs.41.62

lakh.

Sl. No.

Nature of irregularity No. of cases

Stock transfer allowed

Stock transfer allowable

Excess allowance

Short levy of tax

1. Single ‘F’ form covered transactions beyond one month

2 18,896.11 18,830.20 65.91 3.39

2. Transactions not covered by ‘F’ forms

1 3,823.13 0 3,823.13 38.23

Total 3 22,719.24 18,830.20 3,889.04 41.62

(Rs. In lakh)

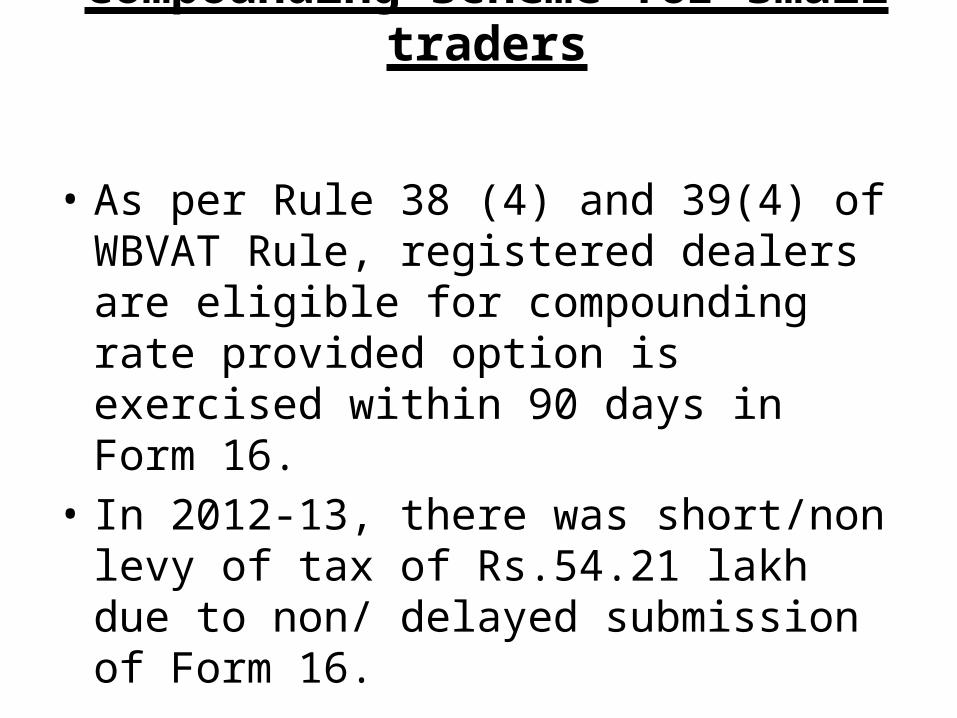

Compounding scheme for small traders

• As per Rule 38 (4) and 39(4) of WBVAT Rule, registered dealers are eligible for compounding rate provided option is exercised within 90 days in Form 16.

• In 2012-13, there was short/non levy of tax of Rs.54.21 lakh due to non/ delayed submission of Form 16.

Rule 38(a) stipulates that the concession of compounding rate is allowable till the turnover does not exceed Rs.50 lakh. Once turnover

reaches Rs.50 lakh the dealer shall pay normal rate from the succeeding

month.In 2013-14, there was short levy of

Rs.1.00 crore due to non compliance of above provisions.

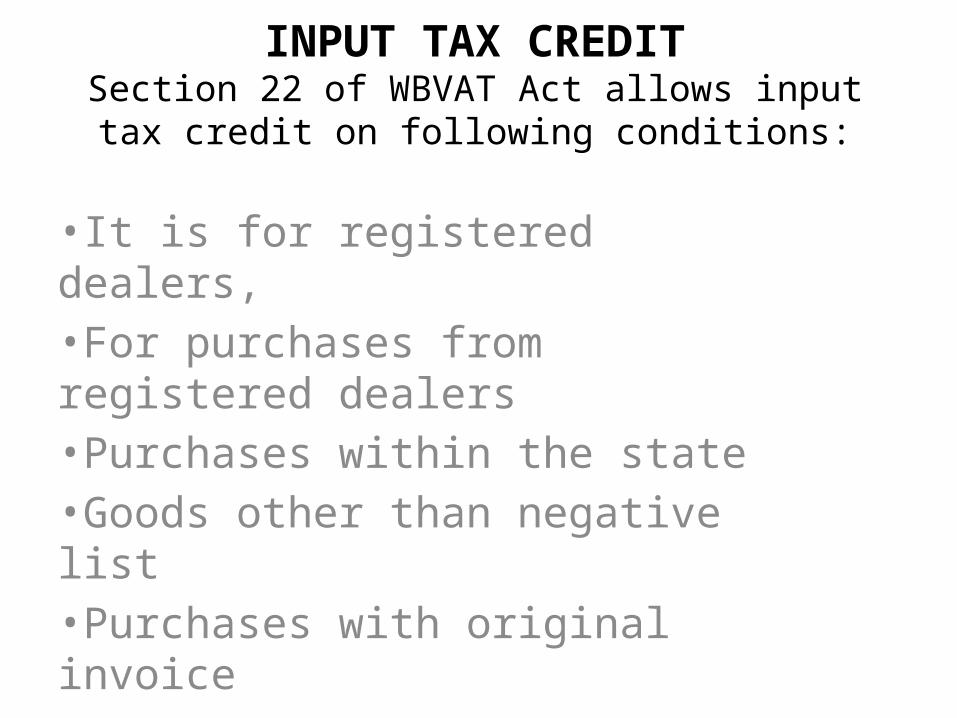

INPUT TAX CREDITSection 22 of WBVAT Act allows input tax credit

on following conditions:

•It is for registered dealers,•For purchases from registered dealers•Purchases within the state•Goods other than negative list•Purchases with original invoice

In 2012-13, there was irregular allowance of input tax credit of Rs.4.27 crore due to non compliance of any of

the above conditions.In 2013-14 there was irregular

allowance of input tax credit of Rs.1.80 crore as detailed below:

Sl. No.

Nature of irregularity No. of cases

ITC allowed

ITC allowable

Irregular allowance of ITC

ITC allowed on purchases made from dealers whose registrations were cancelled

9 162.24 149.79 12.45

ITC allowed on purchases made from dealers who filed ‘nil’ returns and sales-purchases mismatch between purchaser and seller

4 6.81 00.00 6.81

ITC allowed on purchases made from unregistered/non-existent dealers/dealers enjoying composition scheme

3 6.04 00.00 6.04

ITC allowed on tax free items/ consumable items/capital goods not capitalised

3 459.48 443.26 16.22

ITC brought forward from previous year in excess of available ITC and allowed in assessment

3 14.61 3.45 11.16

ITC allowed on non-submission of statement of transitional sock or without verification of purchase documents etc.

9 100.95 31.55 69.40

Other cases of excess allowance of ITC 8 184.77 126.67 58.10

Total 39 934.90 754.72 180.18

Irregular allowance of Input Tax Credit

(Rs. In lakh)

INTEREST

Section 31 and 32 of WBST Act and Section 33 & 34 of WBVAT Act, interest at 1% per month is

chargeable if

•Dealer does not pay tax, but files returns.•Fails to furnish return and non-payment of tax•Non reversal of inadmissible Input Tax Credit•Non payment of demand.

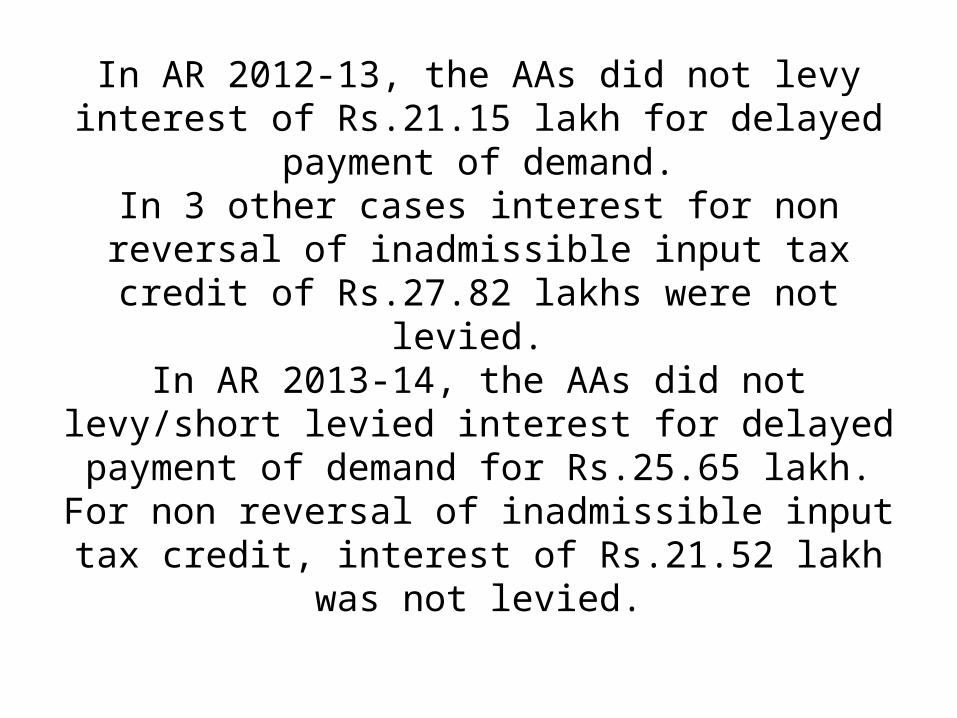

In AR 2012-13, the AAs did not levy interest of Rs.21.15 lakh for delayed payment of

demand.In 3 other cases interest for non reversal of

inadmissible input tax credit of Rs.27.82 lakhs were not levied.

In AR 2013-14, the AAs did not levy/short levied interest for delayed payment of

demand for Rs.25.65 lakh. For non reversal of inadmissible input tax credit, interest of

Rs.21.52 lakh was not levied.

PENALTY

SEC.76 (1) of WBST Act 1994 envisages levy of penalty for the suppression of turnover at the rate of 1 ½ time

to 3 times of evaded taxIn AR 2013-14, the AA did not levy minimum penalty

of Rs.1.07crore for suppression of sales of Rs.4.76 crore with tax liability of Rs.71.09 lakh.

In AR 2013-14, Penalty of Rs.1.13 crore was not levied for submission of fake Form and suppression of inter

state sales.In 5 other cases, penalty of Rs.5.12 crore was not

levied for claim of input tax credit without documents.

STAMP DUTY AND REGISTRATION FEEAvoidance of additional stamp duty by

splitting property

As per Indian Stamp Act, 1899 as amended by WB Finance Act, 2007 additional stamp duty of 1% is leviable if the market value exceeds

Rs.25 lakh. IN AR 2012-13, property with market value more than Rs.25 lakh were split in 20 cases

and stamp duty of Rs.17.53 lakh was avoided.

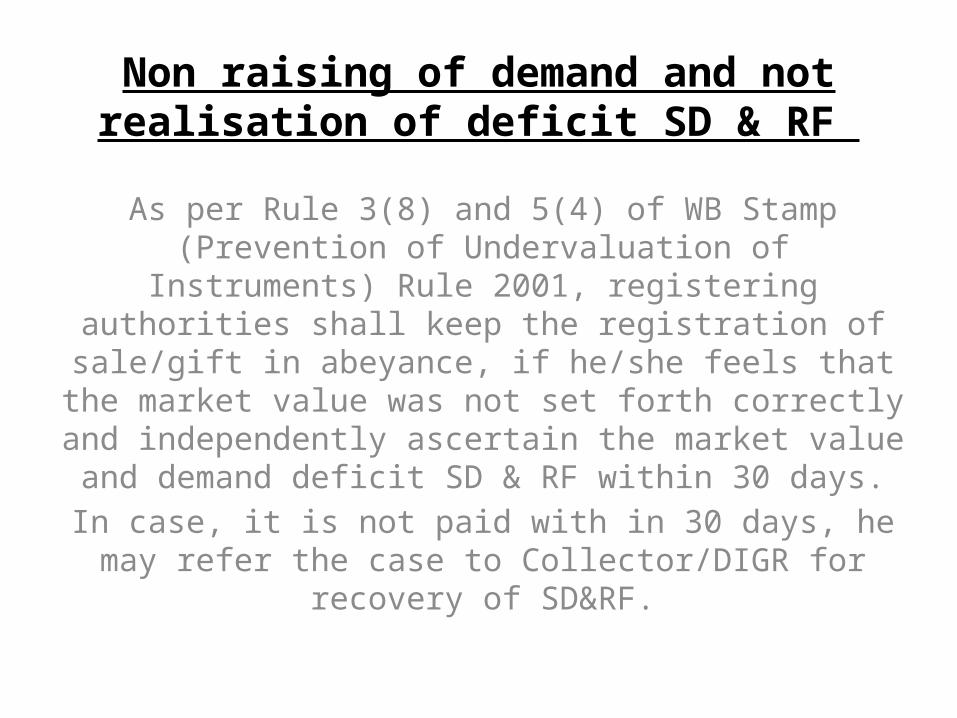

Non raising of demand and not realisation of deficit SD & RF

As per Rule 3(8) and 5(4) of WB Stamp (Prevention of Undervaluation of Instruments)

Rule 2001, registering authorities shall keep the registration of sale/gift in abeyance, if he/she feels that the market value was not set forth

correctly and independently ascertain the market value and demand deficit SD & RF within 30 days.In case, it is not paid with in 30 days, he may refer the case to Collector/DIGR for recovery of SD&RF.

In AR 2012-13, in 98 cases the RA has ascertained deficit stamp duty/RF of

Rs.2.92 crore but did not issue demand notice as the Rule does not prescribe

time limit.In 97 other cases, cases were not referred

to Collector/DIGR for determination of market value with non collection of

SD&RF of Rs.23.55 lakhs.

MOTOR VEHICLES TAXShort realisation of composite fee

As per Rule 87 (2) Central Motor Vehicle Rule, 1989 and Rule 128 (4c ) WBMV Rules 1989, for national permit (NA) Goods Carrier , composite

fee collected by other state for plying their vehicle in WB are to be sent to WB by bank draft.

In Ar 2012-13, for 10425 cases the composite fee was collected at the rate of Rs.1040 to Rs.3800 instead of Rs.3000 to Rs.5000. As a result, there was short collection of Rs.2.13 crore which was

demanded by STA of WB.

Non realisation of special fee for air-conditioned vehicle

As per Section 9B and 10 of WB additional tax and one time tax MV Act 1989, air-conditioned

vehicles are liable to pay a special tax and penalty for belated payment after 60 days.

In AR 2012-13, there was short recovery of Rs.89.31 lakh from 1370 AC vehicle.

Non/short realisation of fitness fee

Rule 62 and 81 of CMV Rule, transport vehicle shall be produced for annual inspection after two years of registration together with fitness fee.

In AR 2012-13, fitness fee of Rs.11.19 lakh was not levied from 23,439 vehicles.

Non/short realisation of permit fee

Section 66 of MV Act 1989, prescribed permit fee for transport vehicle together with late fee

for belated application.In AR 2012-13, a sum of Rs.33.30 lakh was not

collected in this regard.

Non/short realisation of audio fee

As per Schedule F to Rule 216 (2) of the WB MV rules, audio fee for motor vehicle with

audio gadget are leviable.In AR 2012-13, audio fee of Rs.29.42 lakh has

not been collected from 8788 vehicle.

THANK YOU