59

STATEMENT of ACCOUNTS 2000 - 2001 FINANCIAL MANAGEMENT SERVICES

STATEMENT

of

ACCOUNTS

2000 - 2001

F I N A N C I A L M A N A G E M E N T S E R V I C E S

L O N D O N B O R O U G H O F S O U T H W A R K 2 0 0 0 0 1 A C C O U N T S

S T A T E M E N T O F A C C O U N T S

2 0 0 0 - 2 0 0 1

This statement of accounts is produced in accordance with the current legislation and in particular with the

Accounts and Audit Regulations 1996

The District Auditorrsquos opinion on the Accounts is included within the statement

I confirm that the Statement of Accounts presents fairly the financial position of the authority at the accounting date and its income and

expenditure for the year then ended

R A COOMBER CPFA

Chief Executive and Director of Finance

Date 20th December 2001

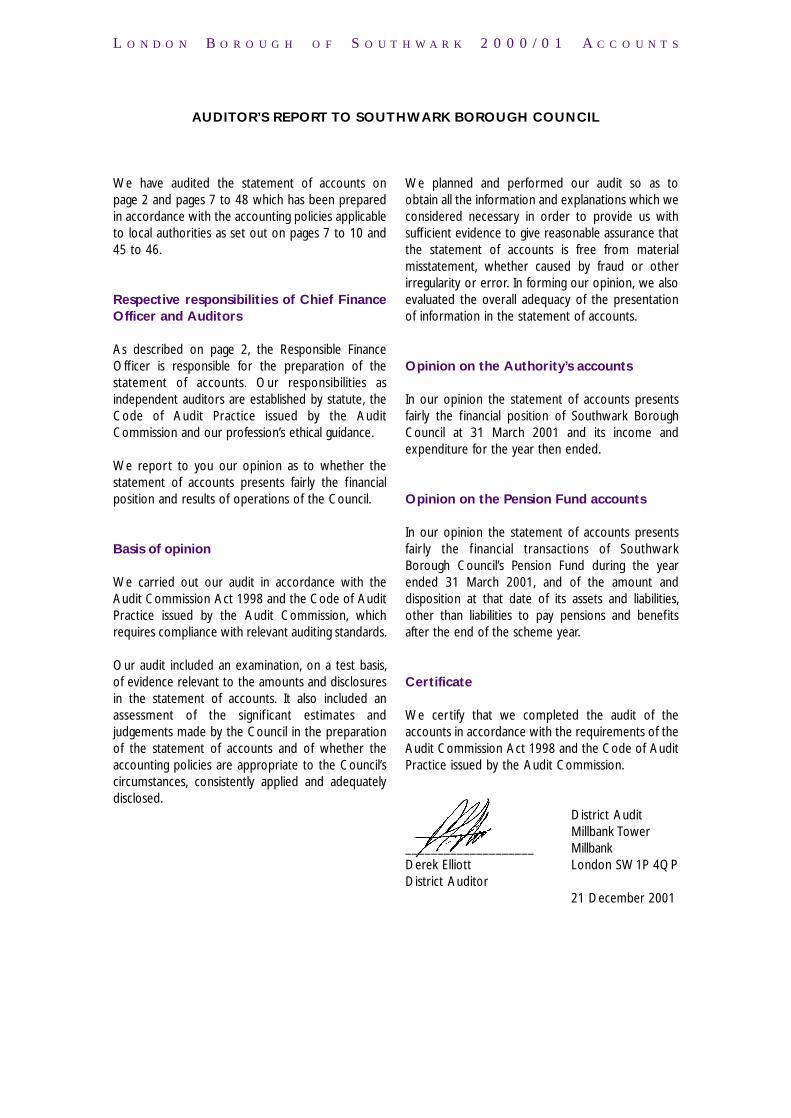

L O N D O N B O R O U G H O F S O U T H W A R K 2 0 0 0 0 1 A C C O U N T S

AUDITORrsquoS REPORT TO SOUTHWARK BOROUGH COUNCIL

We have audited the statement of accounts on page 2 and pages 7 to 48 which has been prepared in accordance with the accounting policies applicable to local authorities as set out on pages 7 to 10 and 45 to 46

Respective responsibilities of Chief Finance Officer and Auditors

As described on page 2 the Responsible Finance Officer is responsible for the preparation of the statement of accounts Our responsibilities as independent auditors are established by statute the Code of Audit Practice issued by the Audit Commission and our professionrsquos ethical guidance

We report to you our opinion as to whether the statement of accounts presents fairly the f inancial position and results of operations of the Council

Basis of opinion

We carried out our audit in accordance with the Audit Commission Act 1998 and the Code of Audit Practice issued by the Audit Commission which requires compliance with relevant auditing standards

Our audit included an examination on a test basis of evidence relevant to the amounts and disclosures in the statement of accounts It also included an assessment of the signif icant estimates and judgements made by the Council in the preparation of the statement of accounts and of whether the accounting policies are appropriate to the Councilrsquos circumstances consistently applied and adequately disclosed

We planned and performed our audit so as to obtain all the information and explanations which we considered necessary in order to provide us with suff icient evidence to give reasonable assurance that the statement of accounts is free from material misstatement whether caused by fraud or other irregularity or error In forming our opinion we also evaluated the overall adequacy of the presentation of information in the statement of accounts

Opinion on the Authorityrsquos accounts

In our opinion the statement of accounts presents fairly the f inancial position of Southwark Borough Council at 31 March 2001 and its income and expenditure for the year then ended

Opinion on the Pension Fund accounts

In our opinion the statement of accounts presents fairly the f inancial transactions of Southwark Borough Councilrsquos Pension Fund during the year ended 31 March 2001 and of the amount and disposition at that date of its assets and liabilities other than liabilities to pay pensions and benefits after the end of the scheme year

Certificate

We certify that we completed the audit of the accounts in accordance with the requirements of the Audit Commission Act 1998 and the Code of Audit Practice issued by the Audit Commission

District Audit Millbank Tower

____________________ Derek Elliott

Millbank London SW1P 4QP

District Auditor 21 December 2001

L O N D O N B O R O U G H O F S O U T H W A R K 2 0 0 0 0 1 A C C O U N T S

L O N D O N B O R O U G H O F S O U T H W A R K 2 0 0 0 0 1 A C C O U N T S

TABLE OF CONTENTS

Page

Statement of Responsibilities for the Statement of Accounts 2

Foreword 3

Statement of Accounting Policies General Principles 7 Compliance with Accounting Standards 7 Capital Accounting 8 Related Party Transactions 10

Consolidated Revenue Account 11 Best Value Accounting Statement 13 Local Government Act 1986 Section 5 Publicity Account 15

Housing Revenue Account 19

Consolidated Balance Sheet 22 Statement of Total Movement in Reserves 30 Miscellaneous Trust Funds 33

Collection Fund Accounts 37

Cash Flow Statement 40

Pension Fund 43

Glossary 49

1

L O N D O N B O R O U G H O F S O U T H W A R K 2 0 0 0 0 1 A C C O U N T S

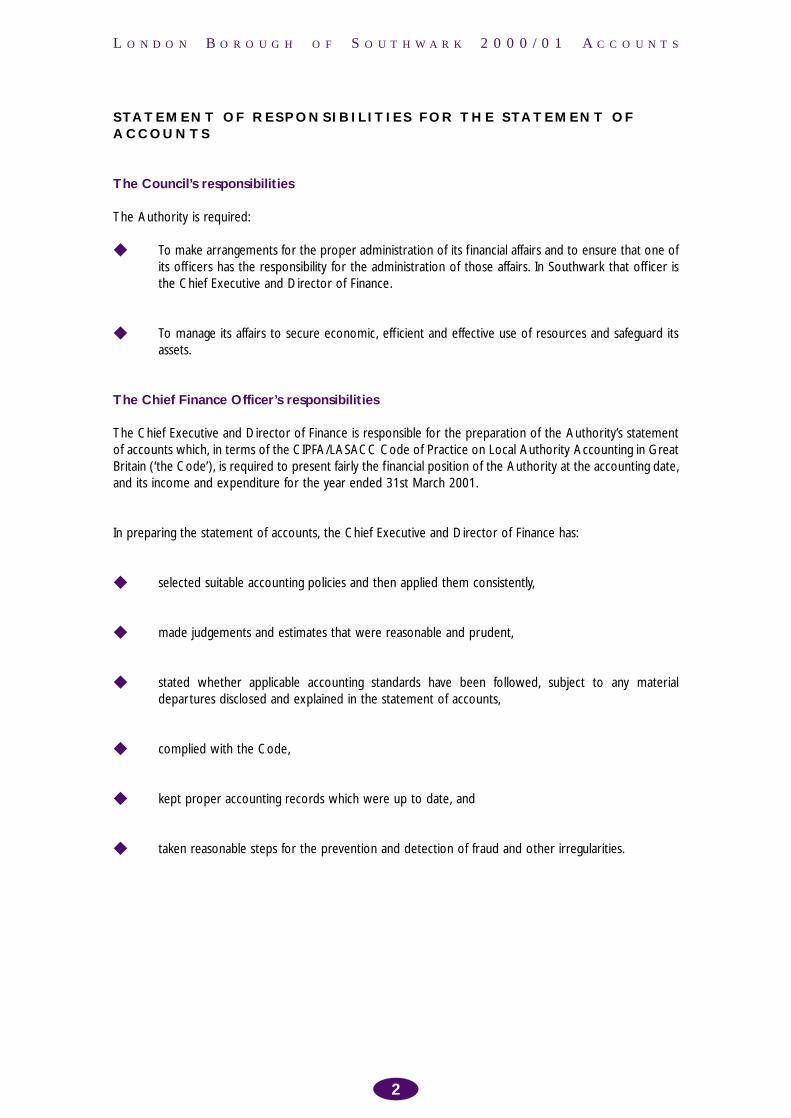

STATEMENT OF RESPONSIBILITIES FOR THE STATEMENT OF ACCOUNTS

The Councilrsquos responsibilities

The Authority is required

To make arrangements for the proper administration of its f inancial affairs and to ensure that one of its off icers has the responsibility for the administration of those affairs In Southwark that off icer is the Chief Executive and Director of Finance

To manage its affairs to secure economic eff icient and effective use of resources and safeguard its assets

The Chief Finance Officerrsquos responsibilities

The Chief Executive and Director of Finance is responsible for the preparation of the Authorityrsquos statement of accounts which in terms of the CIPFALASACC Code of Practice on Local Authority Accounting in Great Britain (lsquothe Codersquo) is required to present fairly the f inancial position of the Authority at the accounting date and its income and expenditure for the year ended 31st March 2001

In preparing the statement of accounts the Chief Executive and Director of Finance has

selected suitable accounting policies and then applied them consistently

made judgements and estimates that were reasonable and prudent

stated whether applicable accounting standards have been followed subject to any material departures disclosed and explained in the statement of accounts

complied with the Code

kept proper accounting records which were up to date and

taken reasonable steps for the prevention and detection of fraud and other irregularities

2

L O N D O N B O R O U G H O F S O U T H W A R K 2 0 0 0 0 1 A C C O U N T S

FOREWORD

1 This foreword provides a brief explanation of the f inancial aspects of the Councilrsquos activities and draws attention to the main features of the Councilrsquos f inancial position at 31st March 2001

2 The Councilrsquos Accounts for the year 200001 are set out in the following pages They consist of

reg The Consolidated Revenue Account ndash the Councilrsquos main revenue account covering income and expenditure on all services

reg The Best Value Accounting Statement ndash an alternative presentation of the Councilrsquos Total Cost of Services in accordance with Best Value principles and allowing consistent comparison between local authorities

reg The Housing Revenue Account ndash which shows income and expenditure on Council Housing

reg The Consolidated Balance Sheet ndash which sets out the f inancial position of the Council as at 31st March 2001

reg The Cash Flow Statement ndash which summarises the inflows and outflows of cash arising from transactions with third parties for revenue and capital purposes

reg The Trust Fund balances ndash which show the movements and the f inal balances on the various trusts and bequests administered by the Council

reg The Direct Service Organisations Accounts

reg The Collection Fund ndash which shows transactions of the charging authority relating to Non-Domestic Rates and Council Tax and the way these have been distributed to preceptors and the General Fund It also shows residual transactions relating to Community Charge

reg The Pension Fund ndash which sets out the f inancial position of the Councilrsquos Pension Fund

3 The attached Statements of Accounting Policies and various notes support these Accounts

3

) ) )) ) )

) ) )

) ) )

) ) )

))

)

)

)

L O N D O N B O R O U G H O F S O U T H W A R K 2 0 0 0 0 1 A C C O U N T S

FOREWORD

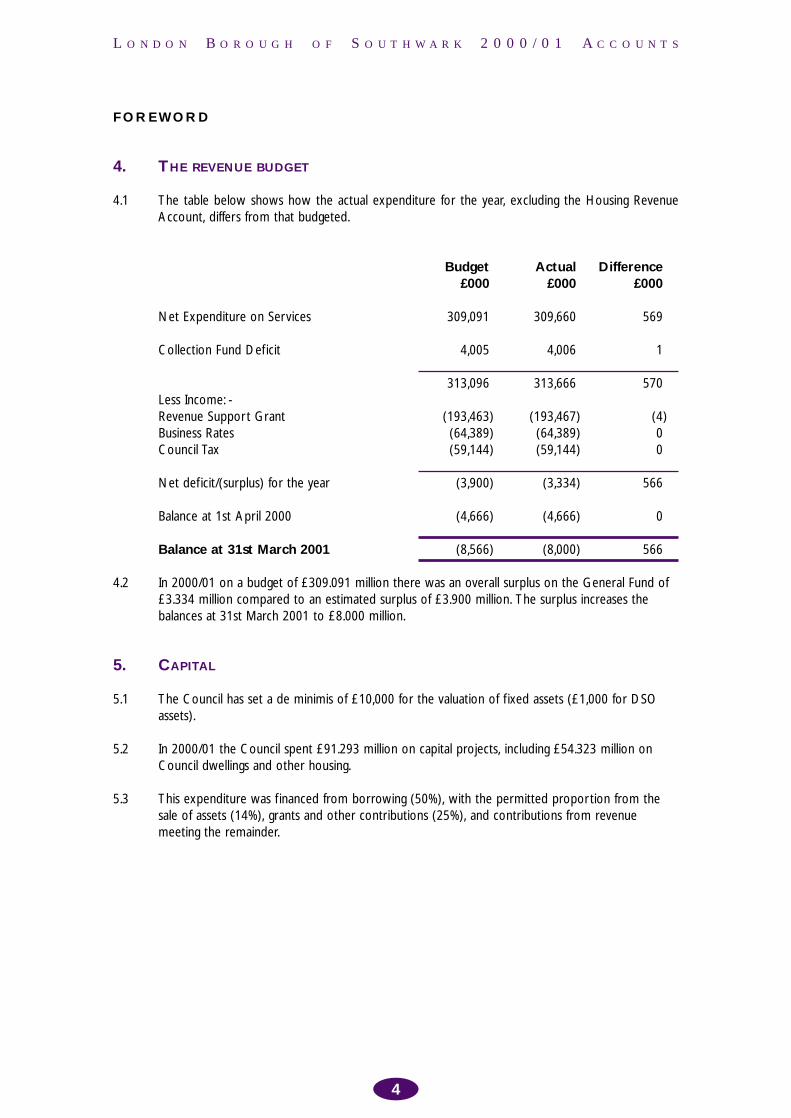

4 THE REVENUE BUDGET

41 The table below shows how the actual expenditure for the year excluding the Housing Revenue Account differs from that budgeted

Budget Actual Difference pound000 pound000 pound000

Net Expenditure on Services 309091 309660 569

Collection Fund Deficit 4005 4006 1

313096 313666 570 Less Income shyRevenue Support Grant (193463) (193467) (4) Business Rates (64389) (64389) 0 Council Tax (59144) (59144) 0

Net deficit(surplus) for the year (3900) (3334) 566

Balance at 1st April 2000 (4666) (4666) 0

Balance at 31st March 2001 (8566) (8000) 566

42 In 200001 on a budget of pound309091 million there was an overall surplus on the General Fund of pound3334 million compared to an estimated surplus of pound3900 million The surplus increases the balances at 31st March 2001 to pound8000 million

5 CAPITAL

51 The Council has set a de minimis of pound10000 for the valuation of f ixed assets (pound1000 for DSO assets)

52 In 200001 the Council spent pound91293 million on capital projects including pound54323 million on Council dwellings and other housing

53 This expenditure was f inanced from borrowing (50) with the permitted proportion from the sale of assets (14) grants and other contributions (25) and contributions from revenue meeting the remainder

4

L O N D O N B O R O U G H O F S O U T H W A R K 2 0 0 0 0 1 A C C O U N T S

FOREWORD

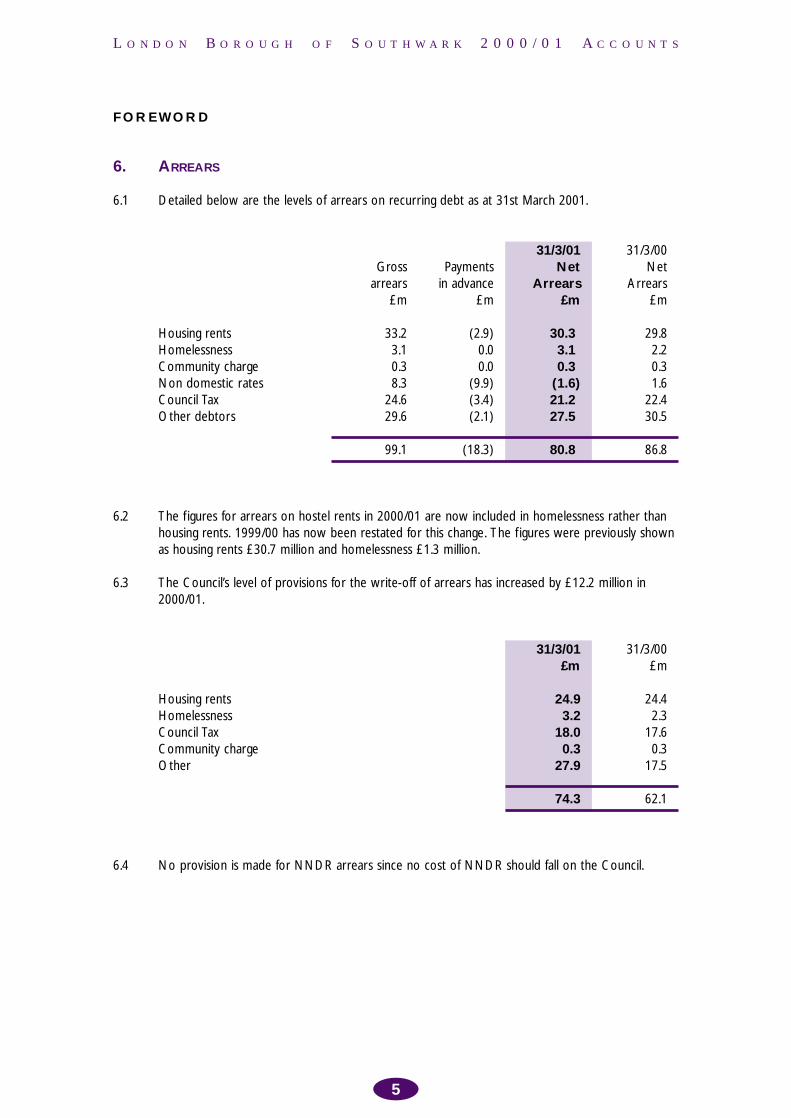

6 ARREARS

61 Detailed below are the levels of arrears on recurring debt as at 31st March 2001

Housing rents Homelessness Community charge Non domestic rates Council Tax Other debtors

31301 31300 Gross Payments Net Net

arrears in advance Arrears Arrears poundm poundm poundm poundm

332 (29) 303) 298 31 00 31) 22 03 00 03) 03 83 (99) (16) 16

246 (34) 212) 224 296 (21) 275) 305

991 (183) 808) 868

62 The f igures for arrears on hostel rents in 200001 are now included in homelessness rather than housing rents 199900 has now been restated for this change The f igures were previously shown as housing rents pound307 million and homelessness pound13 million

63 The Councilrsquos level of provisions for the write-off of arrears has increased by pound122 million in 200001

31301 31300 poundm poundm

Housing rents 249 244 Homelessness 32 23 Council Tax 180 176 Community charge 03 03 Other 279 175

743 621

64 No provision is made for NNDR arrears since no cost of NNDR should fall on the Council

5

L O N D O N B O R O U G H O F S O U T H W A R K 2 0 0 0 0 1 A C C O U N T S

FOREWORD

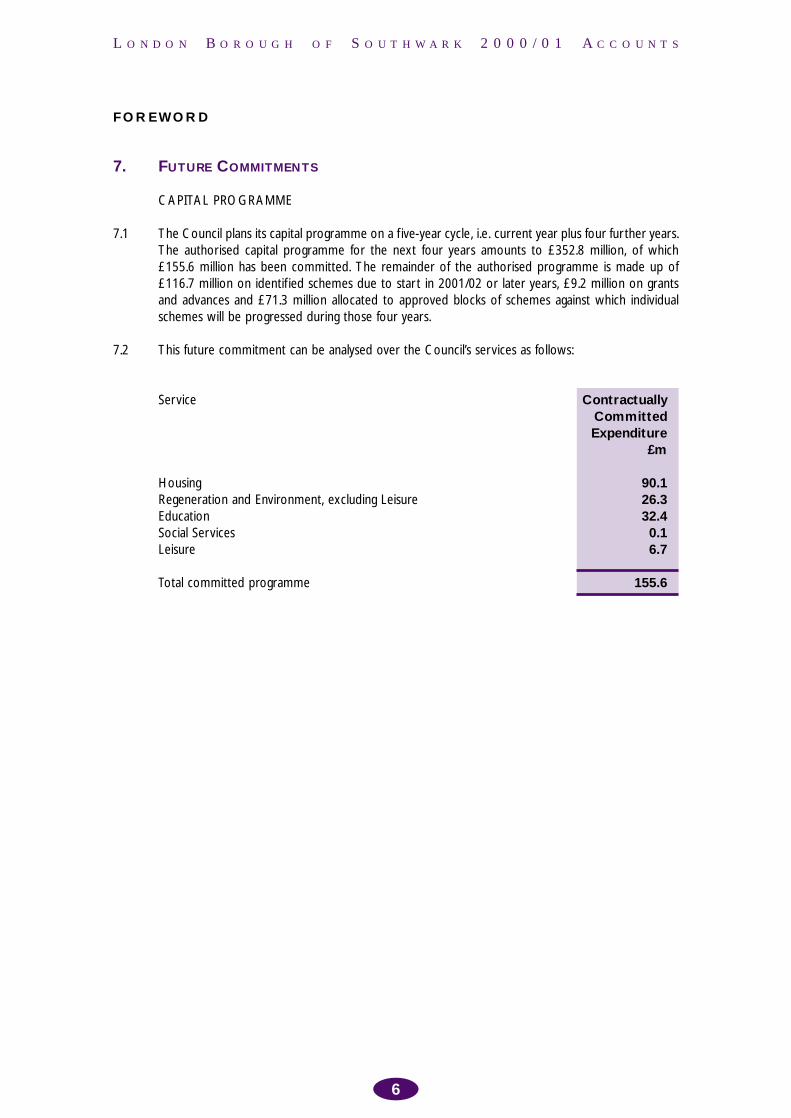

7 FUTURE COMMITMENTS

CAPITAL PROGRAMME

71 The Council plans its capital programme on a f ive-year cycle ie current year plus four further years The authorised capital programme for the next four years amounts to pound3528 million of which pound1556 million has been committed The remainder of the authorised programme is made up of pound1167 million on identif ied schemes due to start in 200102 or later years pound92 million on grants and advances and pound713 million allocated to approved blocks of schemes against which individual schemes will be progressed during those four years

72 This future commitment can be analysed over the Councilrsquos services as follows

Service Contractually Committed Expenditure

poundm

Housing Regeneration and Environment excluding Leisure Education Social Services Leisure

901 263 324 01 67

Total committed programme 1556

6

L O N D O N B O R O U G H O F S O U T H W A R K 2 0 0 0 0 1 A C C O U N T S

STATEMENT OF ACCOUNTING POLICIES

1 GENERAL PRINCIPLES

11 The general principles adopted in compiling and presenting these accounts are those contained in The Code of Practice on Local Government Accounting in Great Britain Statement of Recommended Practice (SORP) 2000 the Best Value Accounting Code of Practice and all other relevant legislation and statements of good practice

2 COMPLIANCE WITH ACCOUNTING STANDARDS

21 These statements comply with all relevant accounting standards with the exception of the following

reg SSAP 6 Extraordinary items and prior year adjustments Legislation does not empower local authorities to credit capital receipts to the General Fund Capital receipts are applied to repay outstanding loan debt f inance new capital expenditure or remain unapplied at the end of the f inancial year A statement is included at Note 173 to the Consolidated Balance Sheet (page 31)

reg SSAP 1 amp 14 Accounting for associated companies and group accounts It has not been possible to comply with this standard completely in respect of the many smaller companies and trusts in which the Council has a minority interest

reg SSAP 24 Accounting for pension costs The Council is inhibited by law from complying with this standard However in 200001 the Council paid a contribution of pound1673 million into the Pension Fund In addition it contributed pound306 million into other pension schemes Considerably increased contributions have been required since 199293 and will continue to be required in future years Further details are given under the Pension Fund accounts on page 45 and the notes to the Consolidated Revenue Account on page 16

reg SSAP 9 Stocks and long term contracts Stock held is not currently valued at the lower of cost or net realisable value but is valued in the accounts at the latest invoiced price

reg Treatment of long term loans due to be repaid The Council has not complied with the requirement to transfer long term loans due to be repaid in the next 12 months to current liabilities since this would distort the balance sheet and comparisons between the f inancial years

DEBTORS AND CREDITORS

22 The accounts are compiled on a system of recognising income and expenditure attributable to the year Therefore if goods or services have been received in the old f inancial year they are accounted for accordingly Likewise income that is due in for goods and services relating to the old f inancial year is accounted for in 200001 If any government grants are due then they are accounted for in the period to which they relate

23 Where the amount due is unknown then an estimated amount has been allowed for

24 All interest payable on external borrowing and interest receivable on investments are accounted for in the period to which they relate

7

L O N D O N B O R O U G H O F S O U T H W A R K 2 0 0 0 0 1 A C C O U N T S

STATEMENT OF ACCOUNTING POLICIES

RESERVES AND PROVISIONS

25 The Consolidated Balance Sheet contains a number of reserves and provisions Provisions are sums set aside for liabilities that are likely to arise but the exact timing and amounts are unknown Reserves are for monies set aside for meeting future expenditure that is non-specif ic at this moment in time

REPAYMENT OF DEBT

26 The Council administers a Consolidated Advances and Borrowing Pool as allowed under the Local Government and Housing Act 1989 All loans raised under these powers are paid into the pool and are advanced to meet capital expenditure on the various Council services

27 Each year the Council is required to charge to revenue a minimum amount for debt redemption as specif ied in the Local Government and Housing Act 1989

ALLOCATION OF CENTRAL ADMINISTRATION EXPENSES OVER SERVICES

28 There has been an allocation of Central Administrative Expenses over all services based on Service Level Agreements Any surpluses or deficits on these internal trading accounts are taken to the General Fund

BASIS OF VALUATION OF INVESTMENTS

29 All investments are shown at their cost price including brokerage and fees

WORKS IN PROGRESS STOCKS AND STORES

210 Works in progress are generally valued at cost (except for the stores element which is valued at average price) However if a DSO has carried out works then they are shown at the lower of valuation or cost

211 Stocks and stores are recorded and charged in the accounts at average price

3 CAPITAL ACCOUNTING

FIXED ASSETS

31 All expenditure on the acquisition creation or enhancement of f ixed assets is capitalised on an accruals basis in the accounts provided that the f ixed asset yields benefits to the Council and the services it provides for a period of more than one year This excludes expenditure on routine repairs and maintenance of f ixed assets that are charged direct to service revenue accounts

8

L O N D O N B O R O U G H O F S O U T H W A R K 2 0 0 0 0 1 A C C O U N T S

STATEMENT OF ACCOUNTING POLICIES

32 Fixed assets are valued on the basis recommended by CIPFA and in accordance with the Statement of Asset Valuation Principles and Guidance notes issued by The Royal Institution of Chartered Surveyors (RICS) Fixed assets are classif ied into the groupings required by the 2000 Code of Practice on Local Authority Accounting

reg Land operational properties and other operational assets are included in the balance sheet at the lower of net current replacement cost and net realisable value

reg Non-operational assets investment properties and assets that are surplus to requirements are included in the balance sheet at the lower of net current replacement cost and net realisable value

reg Infrastructure assets and community assets are included in the balance sheet at historical cost net of depreciation

33 Revaluations of f ixed assets are undertaken on the basis of a 5-year rolling programme although material changes to asset valuations will be adjusted in the interim period should they occur Any surpluses or deficits from revaluation are taken to the Fixed Asset Restatement Reserve

34 Assets acquired under f inance leases are also capitalised in the Councilrsquos accounts together with the liability to pay future rentals Rental payments under f inance leases are apportioned between the f inance charge and the principal element ie the reduction of the liability to pay future rentals The f inance element of rentals is charged to the Asset Management Revenue Account The Council has no f inance leases at this time

35 Rentals payable under operating leases are charged to revenue on an accruals basis

36 Income from the disposal of f ixed assets is accounted for on an accrual basis Such income that is not reserved for the repayment of external loans and forms part of the capital f inancing reserve and has not been used is included in the balance sheet as usable capital receipts

DEPRECIATION

37 Depreciation is provided for on all f ixed assets with a f inite useful life (which can be determined at the time of acquisition or revaluation) according to the following policy

reg all assets are charged with depreciation unless the amount of depreciation is immaterial

reg newly acquired assets are depreciated from the year following acquisition although assets in the course of construction are not depreciated until they are brought into use and

reg depreciation is calculated on a straight-line basis

CHARGES TO REVENUE

38 All Council accounts are charged with a capital charge for all f ixed assets used in the provision of services The total charge covers the annual provision for depreciation plus a capital f inancing charge determined by applying a specif ied notional rate of interest to net asset values The charge made to the Housing Revenue Account is an amount equivalent to the statutory capital f inancing charges

9

L O N D O N B O R O U G H O F S O U T H W A R K 2 0 0 0 0 1 A C C O U N T S

STATEMENT OF ACCOUNTING POLICIES

39 The Asset Management Revenue Account contains the reversing entry for these transactions thereby ensuring there is no overall net effect on the Accounts

DEFERRED CHARGES

310 Deferred charges represent expenditure that may properly be capitalised but does not result in the acquisition or increased value of a tangible f ixed asset Deferred charges are written back to revenue over a period not exceeding f ive years

311 Where the deferred charge forms part of a phased project or part of a bid for external or joint f inance amortisation to revenue will not commence until completion of the project

GOVERNMENT GRANTS AND CONTRIBUTIONS

312 Where the acquisition of a f ixed asset is f inanced either wholly or in part by a government grant or other contribution the amount of the grant or contribution is credited initially to the grants deferred account Amounts are released to the Asset Management Revenue Account over the useful life of the asset to match the depreciation charged on the asset to which the grant relates

4 RELATED PARTY TRANSACTIONS

41 The Council is required to disclose details of its f inancial relationship with related third parties This has been defined as where the related party has or is perceived to have real influence over any transaction between the parties

42 In addition to maintaining the register of membersrsquo interests the Council has obtained specif ic declarations from councillors ex councillors and chief off icers for the f inancial year 200001 Of the 79 declarations requested 9 councillors were members of various local voluntary organisations receiving grant aid totalling pound566000 from the Council in 200001 All of these transactions are with the Council There were no transactions involving central government joint ventures joint venture parties nor other bodies precepting on the Council Tax A summary of the transactions is available separately

43 2 councillors have not returned declarations

44 The Council register of membersrsquo interests is available for inspection together with their declarations of any related party transactions at Peckham Town Hall

5 GRANT CLAIMS

51 The Accounts are prepared on the basis of accruals for claims of grants from central government At the time of signing the Accounts a number of end-of-year grant claims had not been f inalised including material claims such as Housing Subsidy Housing Benefits Subsidy Asylum Seekers and others The Accounts are therefore presented using the best estimates available Any audit amendments to these claims may have a material effect on the Accounts presented

10

)))))

))))))

) )) )

)

)

)

)

)

)

))

)

)

)

)

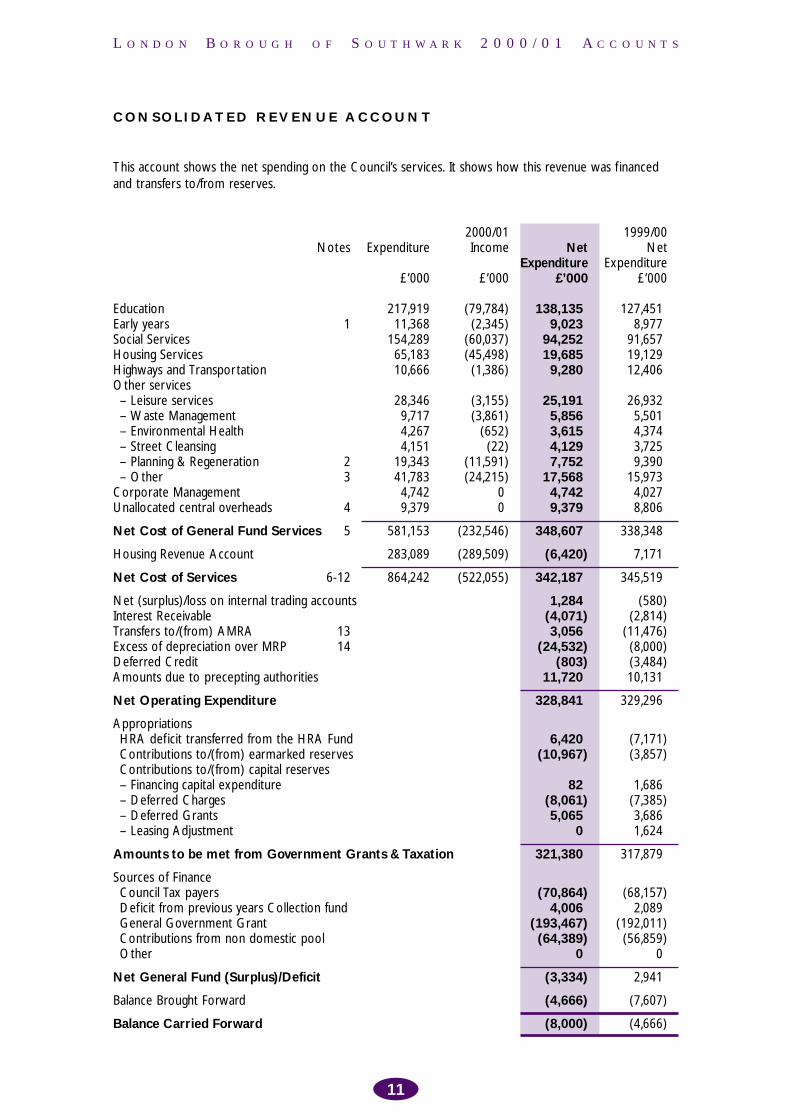

L O N D O N B O R O U G H O F S O U T H W A R K 2 0 0 0 0 1 A C C O U N T S

CONSOLIDATED REVENUE ACCOUNT

This account shows the net spending on the Councilrsquos services It shows how this revenue was f inanced and transfers tofrom reserves

200001 199900 Notes Expenditure Income Net Net

Expenditure Expenditure poundrsquo000 poundrsquo000 poundrsquo000 poundrsquo000

Education 217919 (79784) 138135) 127451 Early years 1 11368 (2345) 9023) 8977 Social Services 154289 (60037) 94252) 91657 Housing Services 65183 (45498) 19685) 19129 Highways and Transportation 10666 (1386) 9280) 12406 Other services ndash Leisure services 28346 (3155) 25191) 26932 ndash Waste Management 9717 (3861) 5856) 5501 ndash Environmental Health 4267 (652) 3615) 4374 ndash Street Cleansing 4151 (22) 4129) 3725 ndash Planning amp Regeneration 2 19343 (11591) 7752) 9390 ndash Other 3 41783 (24215) 17568) 15973

Corporate Management 4742 0 4742) 4027 Unallocated central overheads 4 9379 0 9379) 8806

Net Cost of General Fund Services 5 581153 (232546) 348607) 338348

Housing Revenue Account 283089 (289509) (6420) 7171

Net Cost of Services 6-12 864242 (522055) 342187) 345519

Net (surplus)loss on internal trading accounts 1284) (580) Interest Receivable (4071) (2814) Transfers to(from) AMRA 13 3056) (11476) Excess of depreciation over MRP 14 (24532) (8000) Deferred Credit (803) (3484) Amounts due to precepting authorities 11720) 10131

Net Operating Expenditure 328841) 329296

Appropriations HRA deficit transferred from the HRA Fund 6420) (7171) Contributions to(from) earmarked reserves (10967) (3857) Contributions to(from) capital reserves ndash Financing capital expenditure 82) 1686 ndash Deferred Charges (8061) (7385) ndash Deferred Grants 5065) 3686 ndash Leasing Adjustment 0) 1624

Amounts to be met from Government Grants amp Taxation 321380) 317879

Sources of Finance Council Tax payers (70864) (68157) Deficit from previous years Collection fund 4006) 2089 General Government Grant (193467) (192011) Contributions from non domestic pool (64389) (56859) Other 0) 0

Net General Fund (Surplus)Deficit (3334) 2941

Balance Brought Forward (4666) (7607)

Balance Carried Forward (8000) (4666)

11

L O N D O N B O R O U G H O F S O U T H W A R K 2 0 0 0 0 1 A C C O U N T S

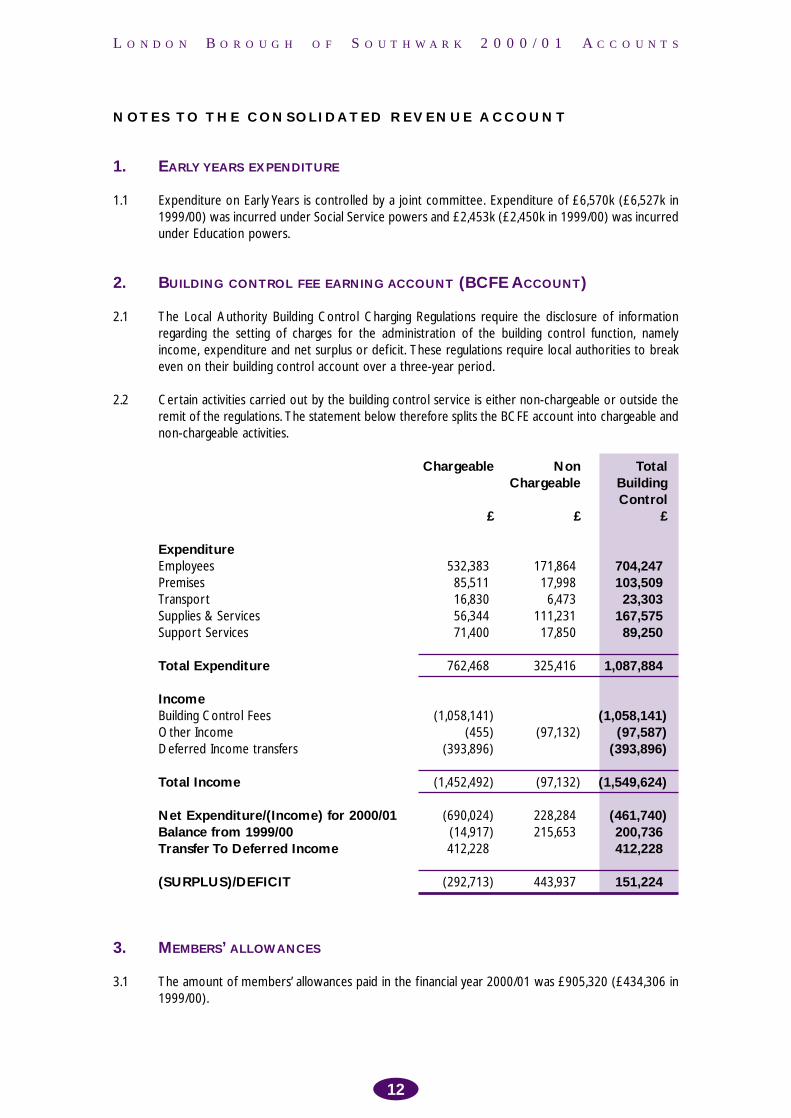

NOTES TO THE CONSOLIDATED REVENUE ACCOUNT

1 EARLY YEARS EXPENDITURE

11 Expenditure on Early Years is controlled by a joint committee Expenditure of pound6570k (pound6527k in 199900) was incurred under Social Service powers and pound2453k (pound2450k in 199900) was incurred under Education powers

2 BUILDING CONTROL FEE EARNING ACCOUNT (BCFE ACCOUNT)

21 The Local Authority Building Control Charging Regulations require the disclosure of information regarding the setting of charges for the administration of the building control function namely income expenditure and net surplus or deficit These regulations require local authorities to break even on their building control account over a three-year period

22 Certain activities carried out by the building control service is either non-chargeable or outside the remit of the regulations The statement below therefore splits the BCFE account into chargeable and non-chargeable activities

Chargeable Non Total Chargeable Building

Control pound pound pound

Expenditure Employees 532383) 171864) 704247) Premises 85511) 17998) 103509) Transport 16830) 6473) 23303) Supplies amp Services 56344) 111231) 167575) Support Services 71400) 17850) 89250)

Total Expenditure 762468) 325416) 1087884)

Income Building Control Fees (1058141) (1058141) Other Income (455) (97132) (97587) Deferred Income transfers (393896) (393896)

Total Income (1452492) (97132) (1549624)

Net Expenditure(Income) for 200001 (690024) 228284) (461740) Balance from 199900 (14917) 215653) 200736) Transfer To Deferred Income 412228) 412228)

(SURPLUS)DEFICIT (292713) 443937) 151224)

3 MEMBERSrsquo ALLOWANCES

31 The amount of membersrsquo allowances paid in the f inancial year 200001 was pound905320 (pound434306 in 199900)

12

))

)

L O N D O N B O R O U G H O F S O U T H W A R K 2 0 0 0 0 1 A C C O U N T S

NOTES TO THE CONSOLIDATED REVENUE ACCOUNT

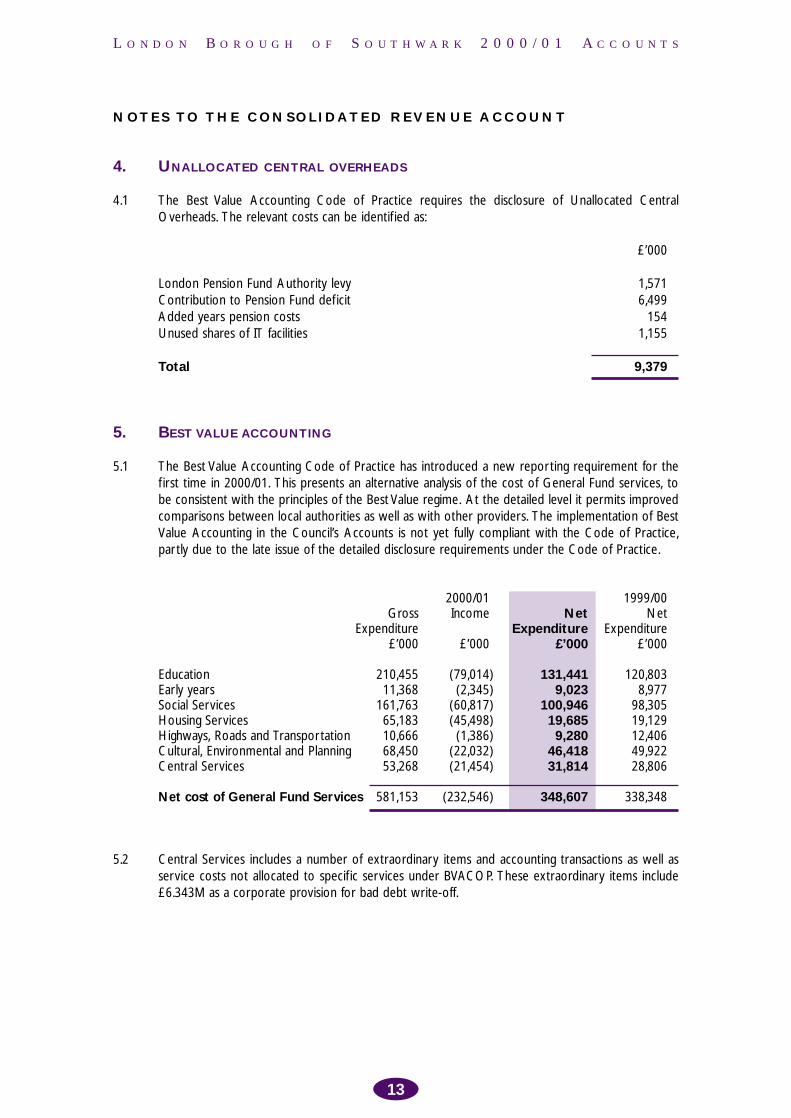

4 UNALLOCATED CENTRAL OVERHEADS

41 The Best Value Accounting Code of Practice requires the disclosure of Unallocated Central Overheads The relevant costs can be identif ied as

poundrsquo000

London Pension Fund Authority levy 1571 Contribution to Pension Fund deficit 6499 Added years pension costs 154 Unused shares of IT facilities 1155

Total 9379

5 BEST VALUE ACCOUNTING

51 The Best Value Accounting Code of Practice has introduced a new reporting requirement for the f irst time in 200001 This presents an alternative analysis of the cost of General Fund services to be consistent with the principles of the Best Value regime At the detailed level it permits improved comparisons between local authorities as well as with other providers The implementation of Best Value Accounting in the Councilrsquos Accounts is not yet fully compliant with the Code of Practice partly due to the late issue of the detailed disclosure requirements under the Code of Practice

Education Early years Social Services Housing Services Highways Roads and Transportation Cultural Environmental and Planning Central Services

Net cost of General Fund Services

200001 199900 Gross Income Net Net

Expenditure Expenditure Expenditure poundrsquo000 poundrsquo000 poundrsquo000 poundrsquo000

210455 (79014) 131441 120803 11368 (2345) 9023 8977

161763 (60817) 100946 98305 65183 (45498) 19685 19129 10666 (1386) 9280 12406 68450 (22032) 46418 49922 53268 (21454) 31814 28806

581153 (232546) 348607 338348

52 Central Services includes a number of extraordinary items and accounting transactions as well as service costs not allocated to specif ic services under BVACOP These extraordinary items include pound6343M as a corporate provision for bad debt write-off

13

)

)

)) )

)

) )

)))))

L O N D O N B O R O U G H O F S O U T H W A R K 2 0 0 0 0 1 A C C O U N T S

NOTES TO THE CONSOLIDATED REVENUE ACCOUNT

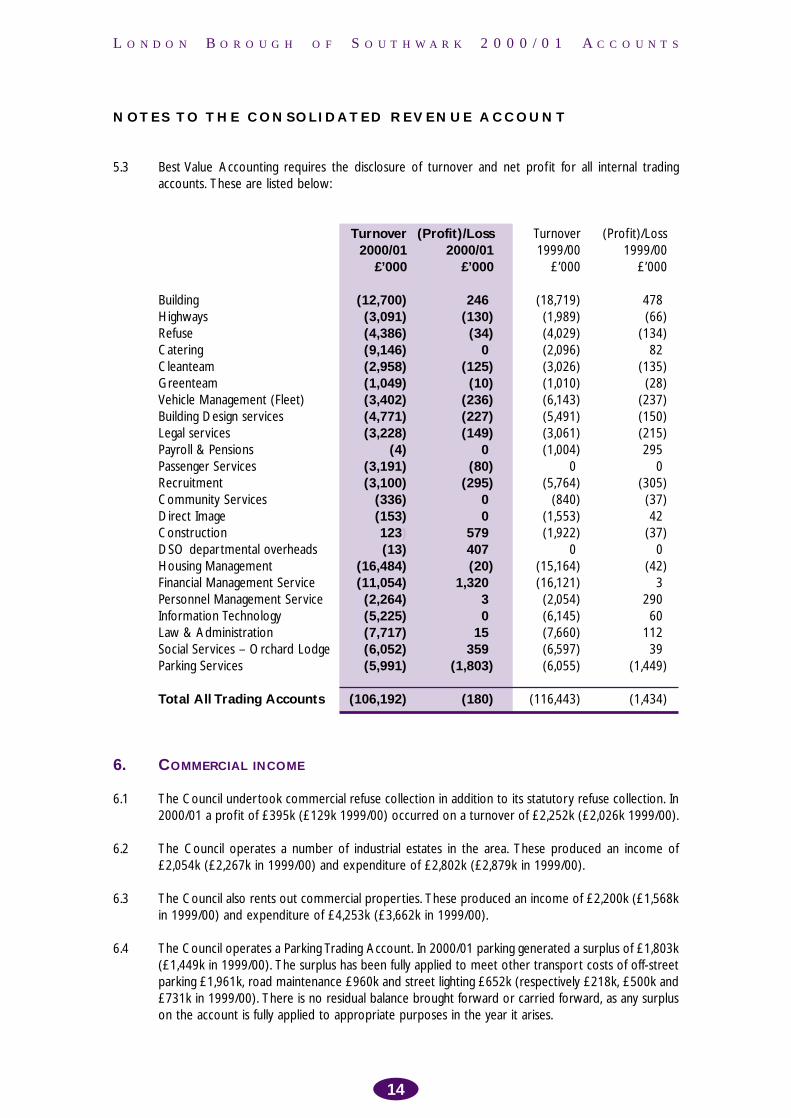

53 Best Value Accounting requires the disclosure of turnover and net profit for all internal trading accounts These are listed below

Turnover (Profit)Loss Turnover (Profit)Loss 200001 200001 199900 199900

poundrsquo000 poundrsquo000 poundrsquo000 poundrsquo000

Building (12700) 246) (18719) 478 Highways (3091) (130) (1989) (66) Refuse (4386) (34) (4029) (134) Catering (9146) 0) (2096) 82 Cleanteam (2958) (125) (3026) (135) Greenteam (1049) (10) (1010) (28) Vehicle Management (Fleet) (3402) (236) (6143) (237) Building Design services (4771) (227) (5491) (150) Legal services (3228) (149) (3061) (215) Payroll amp Pensions (4) 0) (1004) 295 Passenger Services (3191) (80) 0 0 Recruitment (3100) (295) (5764) (305) Community Services (336) 0) (840) (37) Direct Image (153) 0) (1553) 42 Construction 123) 579) (1922) (37) DSO departmental overheads (13) 407) 0 0 Housing Management (16484) (20) (15164) (42) Financial Management Service (11054) 1320) (16121) 3 Personnel Management Service (2264) 3) (2054) 290 Information Technology (5225) 0) (6145) 60 Law amp Administration (7717) 15) (7660) 112 Social Services ndash Orchard Lodge (6052) 359) (6597) 39 Parking Services (5991) (1803) (6055) (1449)

Total All Trading Accounts (106192) (180) (116443) (1434)

6 COMMERCIAL INCOME

61 The Council undertook commercial refuse collection in addition to its statutory refuse collection In 200001 a profit of pound395k (pound129k 199900) occurred on a turnover of pound2252k (pound2026k 199900)

62 The Council operates a number of industrial estates in the area These produced an income of pound2054k (pound2267k in 199900) and expenditure of pound2802k (pound2879k in 199900)

63 The Council also rents out commercial properties These produced an income of pound2200k (pound1568k in 199900) and expenditure of pound4253k (pound3662k in 199900)

64 The Council operates a Parking Trading Account In 200001 parking generated a surplus of pound1803k (pound1449k in 199900) The surplus has been fully applied to meet other transport costs of off-street parking pound1961k road maintenance pound960k and street lighting pound652k (respectively pound218k pound500k and pound731k in 199900) There is no residual balance brought forward or carried forward as any surplus on the account is fully applied to appropriate purposes in the year it arises

14

L O N D O N B O R O U G H O F S O U T H W A R K 2 0 0 0 0 1 A C C O U N T S

NOTES TO THE CONSOLIDATED REVENUE ACCOUNT

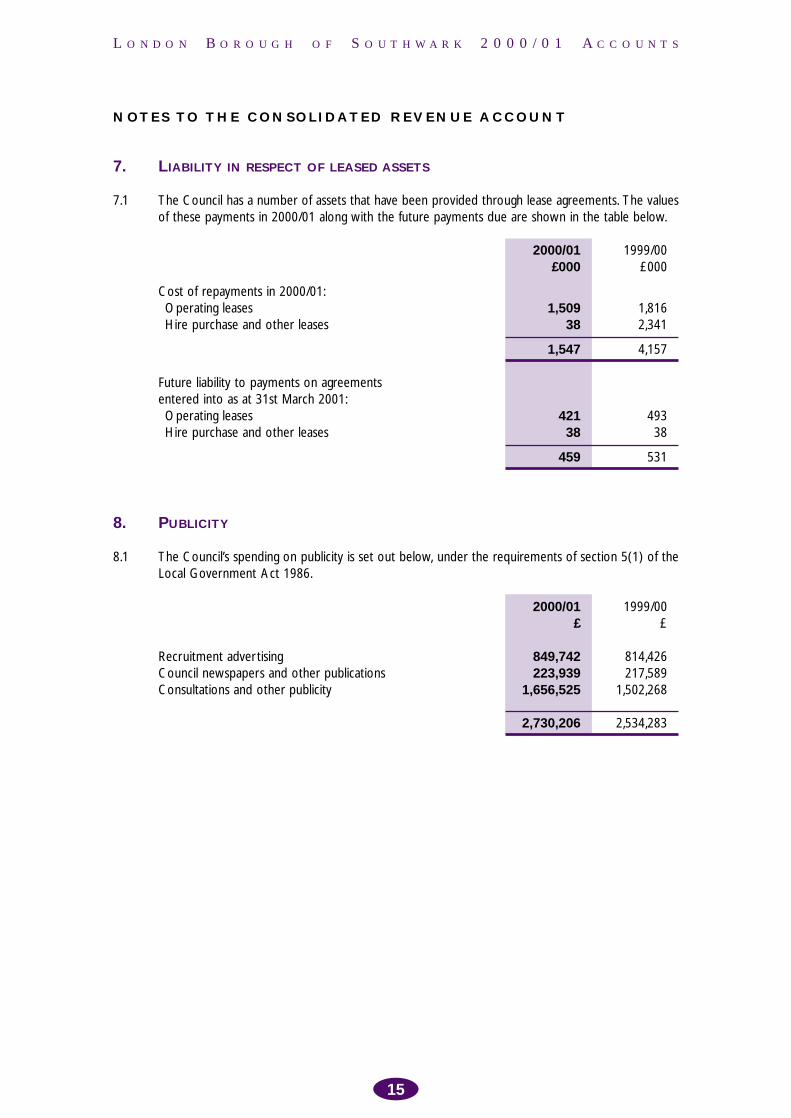

7 LIABILITY IN RESPECT OF LEASED ASSETS

71 The Council has a number of assets that have been provided through lease agreements The values of these payments in 200001 along with the future payments due are shown in the table below

200001 199900 pound000 pound000

Cost of repayments in 200001 Operating leases 1509 1816 Hire purchase and other leases 38 2341

1547 4157

Future liability to payments on agreements entered into as at 31st March 2001 Operating leases 421 493 Hire purchase and other leases 38 38

459 531

8 PUBLICITY

81 The Councilrsquos spending on publicity is set out below under the requirements of section 5(1) of the Local Government Act 1986

Recruitment advertising Council newspapers and other publications Consultations and other publicity

200001 199900 pound pound

849742 814426 223939 217589

1656525 1502268

2730206 2534283

15

L O N D O N B O R O U G H O F S O U T H W A R K 2 0 0 0 0 1 A C C O U N T S

NOTES TO THE CONSOLIDATED REVENUE ACCOUNT

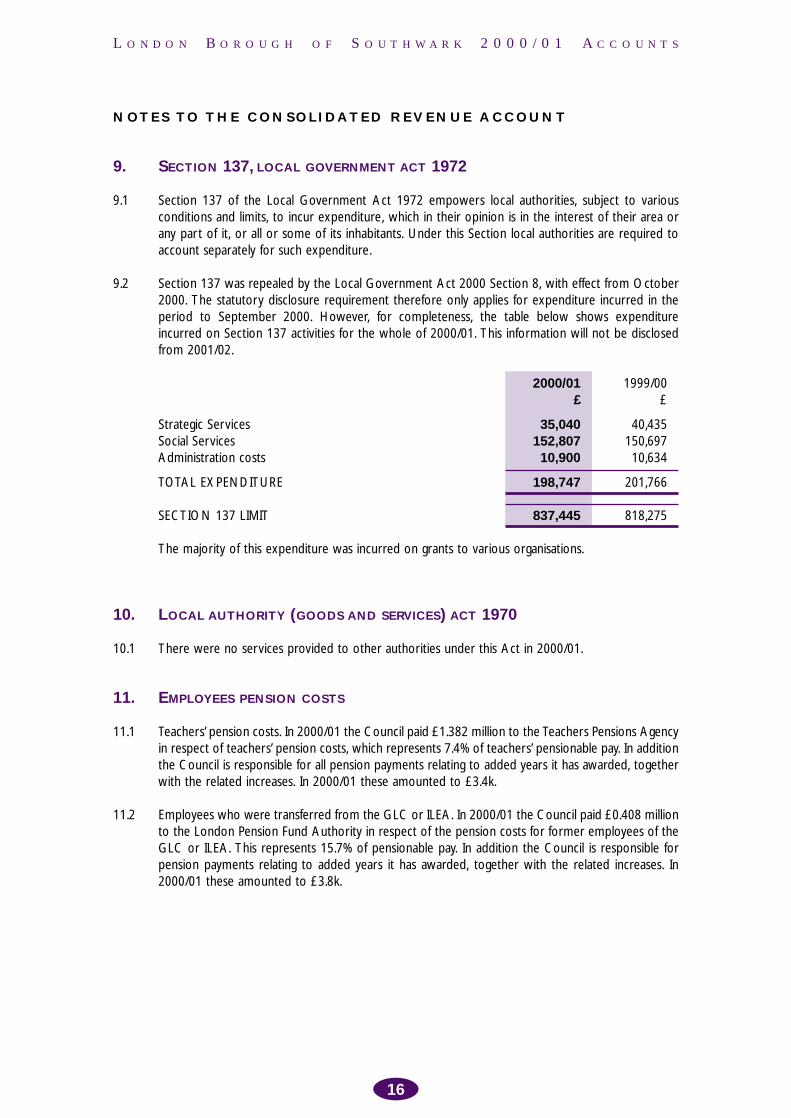

9 SECTION 137 LOCAL GOVERNMENT ACT 1972

91 Section 137 of the Local Government Act 1972 empowers local authorities subject to various conditions and limits to incur expenditure which in their opinion is in the interest of their area or any part of it or all or some of its inhabitants Under this Section local authorities are required to account separately for such expenditure

92 Section 137 was repealed by the Local Government Act 2000 Section 8 with effect from October 2000 The statutory disclosure requirement therefore only applies for expenditure incurred in the period to September 2000 However for completeness the table below shows expenditure incurred on Section 137 activities for the whole of 200001 This information will not be disclosed from 200102

200001 199900 pound pound

Strategic Services 35040 40435 Social Services 152807 150697 Administration costs 10900 10634

TOTAL EXPENDITURE 198747 201766

SECTION 137 LIMIT 837445 818275

The majority of this expenditure was incurred on grants to various organisations

10 LOCAL AUTHORITY (GOODS AND SERVICES) ACT 1970

101 There were no services provided to other authorities under this Act in 200001

11 EMPLOYEES PENSION COSTS

111 Teachersrsquo pension costs In 200001 the Council paid pound1382 million to the Teachers Pensions Agency in respect of teachersrsquo pension costs which represents 74 of teachersrsquo pensionable pay In addition the Council is responsible for all pension payments relating to added years it has awarded together with the related increases In 200001 these amounted to pound34k

112 Employees who were transferred from the GLC or ILEA In 200001 the Council paid pound0408 million to the London Pension Fund Authority in respect of the pension costs for former employees of the GLC or ILEA This represents 157 of pensionable pay In addition the Council is responsible for pension payments relating to added years it has awarded together with the related increases In 200001 these amounted to pound38k

16

L O N D O N B O R O U G H O F S O U T H W A R K 2 0 0 0 0 1 A C C O U N T S

NOTES TO THE CONSOLIDATED REVENUE ACCOUNT

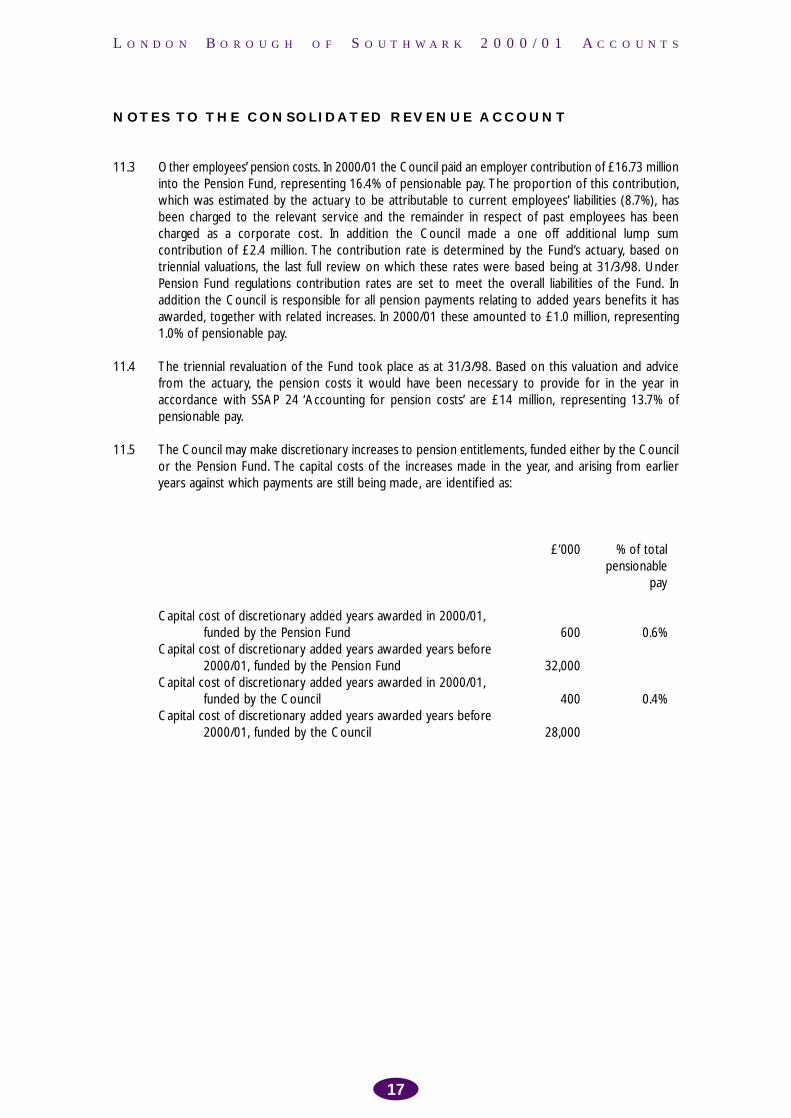

113 Other employeesrsquo pension costs In 200001 the Council paid an employer contribution of pound1673 million into the Pension Fund representing 164 of pensionable pay The proportion of this contribution which was estimated by the actuary to be attributable to current employeesrsquo liabilities (87) has been charged to the relevant service and the remainder in respect of past employees has been charged as a corporate cost In addition the Council made a one off additional lump sum contribution of pound24 million The contribution rate is determined by the Fundrsquos actuary based on triennial valuations the last full review on which these rates were based being at 31398 Under Pension Fund regulations contribution rates are set to meet the overall liabilities of the Fund In addition the Council is responsible for all pension payments relating to added years benefits it has awarded together with related increases In 200001 these amounted to pound10 million representing 10 of pensionable pay

114 The triennial revaluation of the Fund took place as at 31398 Based on this valuation and advice from the actuary the pension costs it would have been necessary to provide for in the year in accordance with SSAP 24 lsquoAccounting for pension costsrsquo are pound14 million representing 137 of pensionable pay

115 The Council may make discretionary increases to pension entitlements funded either by the Council or the Pension Fund The capital costs of the increases made in the year and arising from earlier years against which payments are still being made are identif ied as

poundrsquo000 of total pensionable

pay

Capital cost of discretionary added years awarded in 200001 funded by the Pension Fund 600 06

Capital cost of discretionary added years awarded years before 200001 funded by the Pension Fund 32000

Capital cost of discretionary added years awarded in 200001 funded by the Council 400 04

Capital cost of discretionary added years awarded years before 200001 funded by the Council 28000

17

)))

)

))

)

)

)

L O N D O N B O R O U G H O F S O U T H W A R K 2 0 0 0 0 1 A C C O U N T S

NOTES TO THE CONSOLIDATED REVENUE ACCOUNT

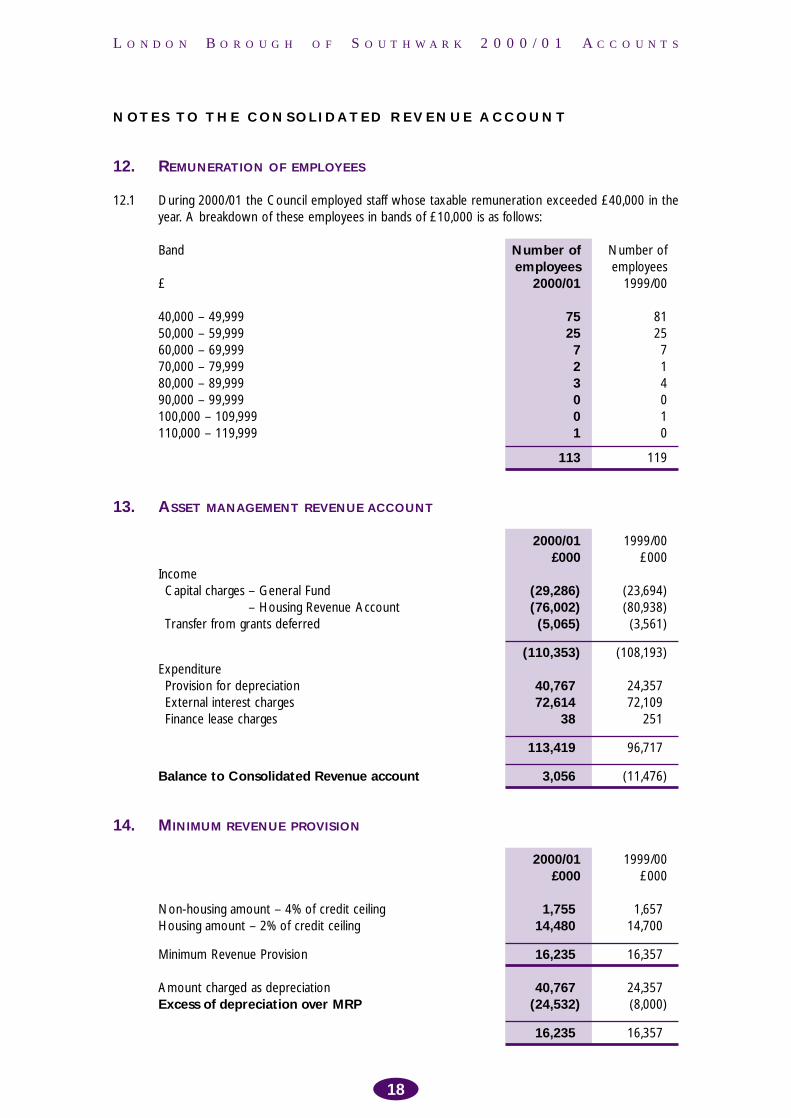

12 REMUNERATION OF EMPLOYEES

121 During 200001 the Council employed staff whose taxable remuneration exceeded pound40000 in the year A breakdown of these employees in bands of pound10000 is as follows

Band

pound

Number of employees

200001

Number of employees

199900

40000 ndash 49999 50000 ndash 59999 60000 ndash 69999 70000 ndash 79999 80000 ndash 89999 90000 ndash 99999 100000 ndash 109999 110000 ndash 119999

75 25 7 2 3 0 0 1

81 25 7 1 4 0 1 0

113 119

13 ASSET MANAGEMENT REVENUE ACCOUNT

Income Capital charges ndash General Fund

ndash Housing Revenue Account Transfer from grants deferred

Expenditure Provision for depreciation External interest charges Finance lease charges

Balance to Consolidated Revenue account

14 MINIMUM REVENUE PROVISION

Non-housing amount ndash 4 of credit ceiling Housing amount ndash 2 of credit ceiling

Minimum Revenue Provision

Amount charged as depreciation Excess of depreciation over MRP

200001 199900 pound000 pound000

(29286) (23694) (76002) (80938) (5065) (3561)

(110353) (108193)

40767) 24357 72614) 72109

38) 251

113419) 96717

3056) (11476)

200001 199900 pound000 pound000

1755) 1657 14480) 14700

16235) 16357

40767) 24357 (24532) (8000)

16235) 16357

18

)))))

))

)

)

)

))

)

L O N D O N B O R O U G H O F S O U T H W A R K 2 0 0 0 0 1 A C C O U N T S

HOUSING REVENUE ACCOUNT

The Housing Revenue Account reflects the statutory requirement under schedule 4 of the Local Government and Housing Act 1989 to account separately for local authority housing provision It shows the major elements of cost in providing and managing the Councilrsquos housing stock and how this expenditure is met from rents subsidy and other income

HOUSING REVENUE ACCOUNT 200001 199900 pound000 pound000

INCOME Rents ndash dwellings (142536) (142649)

ndash non-dwellings (5595) (6158) Charges to tenants (13461) (14374) Housing subsidy (112596) (115936) Interest on balances (2048) (2431) Interest on mortgage advances (200) (258) Other income (13073) (10953)

TOTAL INCOME (289509) (292759)

EXPENDITURE Repairs and maintenance 43188) 46740 Supervision and management 66886) 70543 Rents rates taxes and other charges 2628) 2306 Capital f inancing costs 80246) 83955 Provision for bad or doubtful debts 7780) 9102 Contributions to(from) provisions 2392) (409) Rent rebate payments 74710) 74146 Capital expenditure charged to revenue 5092) 14141

TOTAL EXPENDITURE 282922) 300524

Movement in reserves (6587) 7765

Balance of reserves at the beginning of year (13530) (21295)

Balance of reserves at the end of year (20117) (13530)

Less Earmarked reserves 12626) 12459

General working balances (7491) (1071)

HOUSING TENANTS ACCOUNTS

Arrears at 1st April 30784) 28534 Charges due in the year 148715) 149088 Rent Rebates (68145) (68424) Write off and adjustments (5112) (5665) Cash collected (75728) (72749)

Arrears at 31st March 30514) 30784

19

L O N D O N B O R O U G H O F S O U T H W A R K 2 0 0 0 0 1 A C C O U N T S

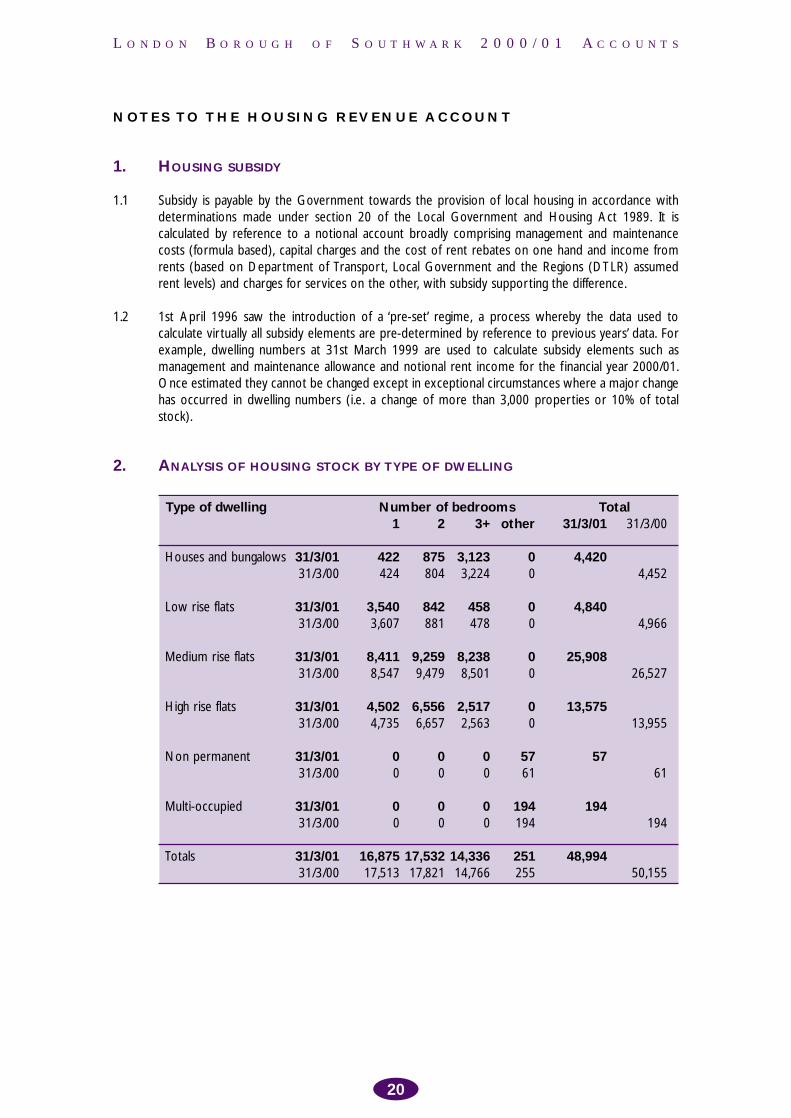

NOTES TO THE HOUSING REVENUE ACCOUNT

1 HOUSING SUBSIDY

11 Subsidy is payable by the Government towards the provision of local housing in accordance with determinations made under section 20 of the Local Government and Housing Act 1989 It is calculated by reference to a notional account broadly comprising management and maintenance costs (formula based) capital charges and the cost of rent rebates on one hand and income from rents (based on Department of Transport Local Government and the Regions (DTLR) assumed rent levels) and charges for services on the other with subsidy supporting the difference

12 1st April 1996 saw the introduction of a lsquopre-setrsquo regime a process whereby the data used to calculate virtually all subsidy elements are pre-determined by reference to previous yearsrsquo data For example dwelling numbers at 31st March 1999 are used to calculate subsidy elements such as management and maintenance allowance and notional rent income for the f inancial year 200001 Once estimated they cannot be changed except in exceptional circumstances where a major change has occurred in dwelling numbers (ie a change of more than 3000 properties or 10 of total stock)

2 ANALYSIS OF HOUSING STOCK BY TYPE OF DWELLING

Type of dwelling Number of bedrooms 1 2 3+ other

Total 31301 31300

Houses and bungalows 31301 31300

422 424

875 804

3123 3224

0 0

4420 4452

Low rise flats 31301 31300

3540 3607

842 881

458 478

0 0

4840 4966

Medium rise flats 31301 31300

8411 8547

9259 9479

8238 8501

0 0

25908 26527

High rise flats 31301 31300

4502 4735

6556 6657

2517 2563

0 0

13575 13955

Non permanent 31301 31300

0 0

0 0

0 0

57 61

57 61

Multi-occupied 31301 31300

0 0

0 0

0 0

194 194

194 194

Totals 31301 31300

16875 17532 14336 17513 17821 14766

251 255

48994 50155

20

L O N D O N B O R O U G H O F S O U T H W A R K 2 0 0 0 0 1 A C C O U N T S

NOTES TO THE HOUSING REVENUE ACCOUNT

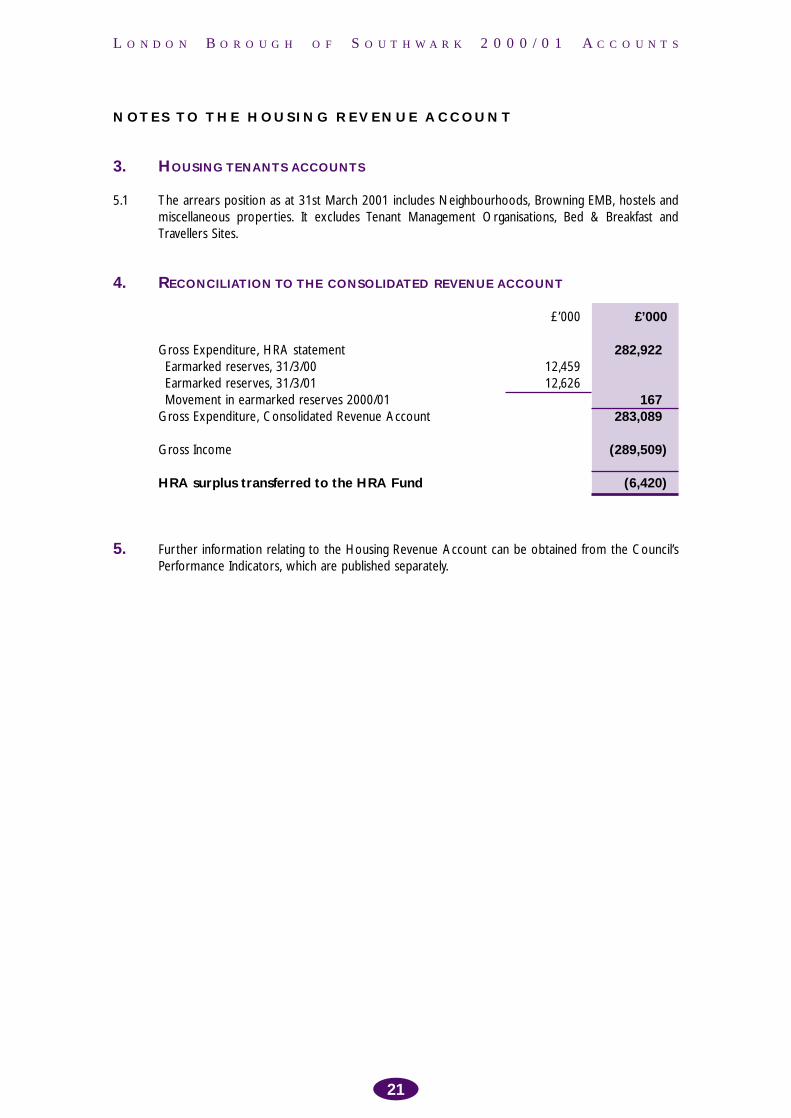

3 HOUSING TENANTS ACCOUNTS

51 The arrears position as at 31st March 2001 includes Neighbourhoods Browning EMB hostels and miscellaneous properties It excludes Tenant Management Organisations Bed amp Breakfast and Travellers Sites

4 RECONCILIATION TO THE CONSOLIDATED REVENUE ACCOUNT

poundrsquo000

Gross Expenditure HRA statement Earmarked reserves 31300 Earmarked reserves 31301 Movement in earmarked reserves 200001

Gross Expenditure Consolidated Revenue Account

12459 12626

Gross Income

HRA surplus transferred to the HRA Fund

poundrsquo000

282922)

167) 283089)

(289509)

(6420)

5 Further information relating to the Housing Revenue Account can be obtained from the Councilrsquos Performance Indicators which are published separately

21

))))))

))

)))

)

))

))

)

)

)

))))))

)

L O N D O N B O R O U G H O F S O U T H W A R K 2 0 0 0 0 1 A C C O U N T S

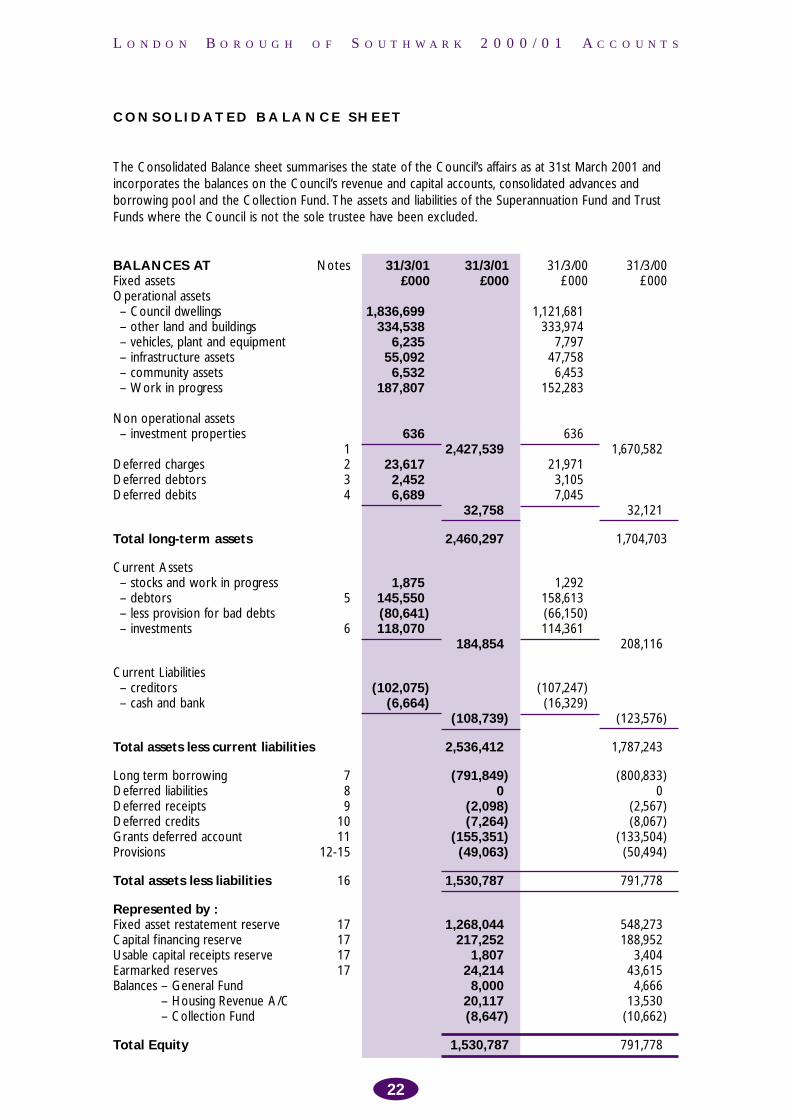

CONSOLIDATED BALANCE SHEET

The Consolidated Balance sheet summarises the state of the Councilrsquos affairs as at 31st March 2001 and incorporates the balances on the Councilrsquos revenue and capital accounts consolidated advances and borrowing pool and the Collection Fund The assets and liabilities of the Superannuation Fund and Trust Funds where the Council is not the sole trustee have been excluded

BALANCES AT Fixed assets

Notes 31301 pound000

31301 pound000

31300 pound000

31300 pound000

Operational assets ndash Council dwellings ndash other land and buildings ndash vehicles plant and equipment ndash infrastructure assets ndash community assets ndash Work in progress

1836699) 334538)

6235) 55092) 6532)

187807)

1121681 333974

7797 47758 6453

152283

Non operational assets ndash investment properties

Deferred charges Deferred debtors Deferred debits

1 2 3 4

636)

23617) 2452) 6689)

2427539)

32758)

636

21971 3105 7045

1670582

32121

Total long-term assets 2460297) 1704703

Current Assets ndash stocks and work in progress ndash debtors ndash less provision for bad debts ndash investments

5

6

1875) 145550) (80641) 118070)

184854)

1292 158613 (66150) 114361

208116

Current Liabilities ndash creditors ndash cash and bank

(102075) (6664)

(108739)

(107247) (16329)

(123576)

Total assets less current liabilities 2536412) 1787243

Long term borrowing Deferred liabilities Deferred receipts Deferred credits Grants deferred account Provisions

7 8 9

10 11

12-15

(791849) 0)

(2098) (7264)

(155351) (49063)

(800833) 0

(2567) (8067)

(133504) (50494)

Total assets less liabilities 16 1530787) 791778

Represented by Fixed asset restatement reserve Capital f inancing reserve Usable capital receipts reserve Earmarked reserves Balances ndash General Fund

ndash Housing Revenue AC ndash Collection Fund

17 17 17 17

1268044) 217252)

1807) 24214) 8000)

20117) (8647)

548273 188952

3404 43615 4666

13530 (10662)

Total Equity 1530787 791778

22

L O N D O N B O R O U G H O F S O U T H W A R K 2 0 0 0 0 1 A C C O U N T S

NOTES TO THE CONSOLIDATED BALANCE SHEET

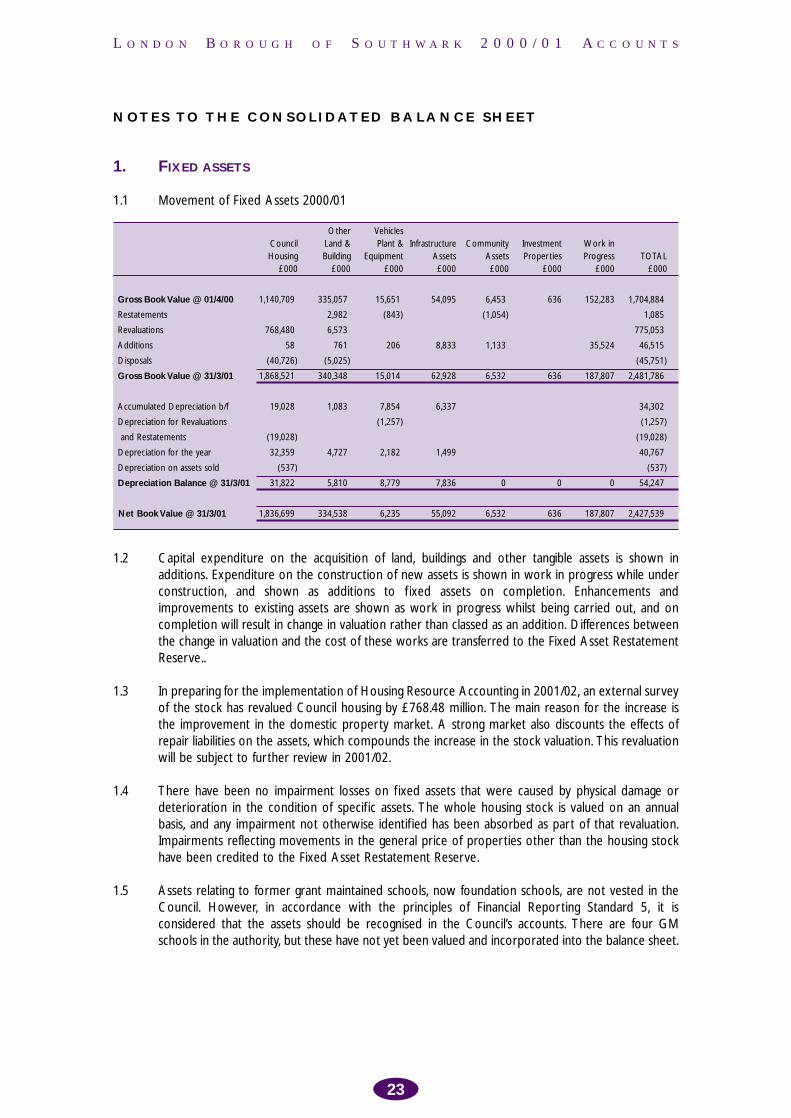

1 FIXED ASSETS

11 Movement of Fixed Assets 200001

Council Housing

pound000

Other Land amp Building

pound000

Vehicles Plant amp

Equipment pound000

Infrastructure Assets pound000

Community Assets pound000

Investment Properties

pound000

Work in Progress

pound000 TOTAL

pound000

Gross Book Value 01400

Restatements

Revaluations

Additions

Disposals

Gross Book Value 31301

1140709)

768480)

58)

(40726)

1868521)

335057)

2982)

6573)

761)

(5025)

340348)

15651)

(843)

206)

15014)

54095

8833

62928

6453)

(1054)

1133)

6532)

636

636

152283

35524

187807

1704884)

1085)

775053)

46515)

(45751)

2481786)

Accumulated Depreciation bf

Depreciation for Revaluations

and Restatements

Depreciation for the year

Depreciation on assets sold

Depreciation Balance 31301

19028)

(19028)

32359)

(537)

31822)

1083)

4727)

5810)

7854)

(1257)

2182)

8779)

6337

1499

7836 0) 0 0

34302)

(1257)

(19028)

40767)

(537)

54247)

Net Book Value 31301 1836699) 334538) 6235) 55092 6532) 636 187807 2427539)

12 Capital expenditure on the acquisition of land buildings and other tangible assets is shown in additions Expenditure on the construction of new assets is shown in work in progress while under construction and shown as additions to f ixed assets on completion Enhancements and improvements to existing assets are shown as work in progress whilst being carried out and on completion will result in change in valuation rather than classed as an addition Differences between the change in valuation and the cost of these works are transferred to the Fixed Asset Restatement Reserve

13 In preparing for the implementation of Housing Resource Accounting in 200102 an external survey of the stock has revalued Council housing by pound76848 million The main reason for the increase is the improvement in the domestic property market A strong market also discounts the effects of repair liabilities on the assets which compounds the increase in the stock valuation This revaluation will be subject to further review in 200102

14 There have been no impairment losses on f ixed assets that were caused by physical damage or deterioration in the condition of specif ic assets The whole housing stock is valued on an annual basis and any impairment not otherwise identif ied has been absorbed as part of that revaluation Impairments reflecting movements in the general price of properties other than the housing stock have been credited to the Fixed Asset Restatement Reserve

15 Assets relating to former grant maintained schools now foundation schools are not vested in the Council However in accordance with the principles of Financial Reporting Standard 5 it is considered that the assets should be recognised in the Councilrsquos accounts There are four GM schools in the authority but these have not yet been valued and incorporated into the balance sheet

23

)))

)

))

)

)

))

)

))

)

L O N D O N B O R O U G H O F S O U T H W A R K 2 0 0 0 0 1 A C C O U N T S

NOTES TO THE CONSOLIDATED BALANCE SHEET

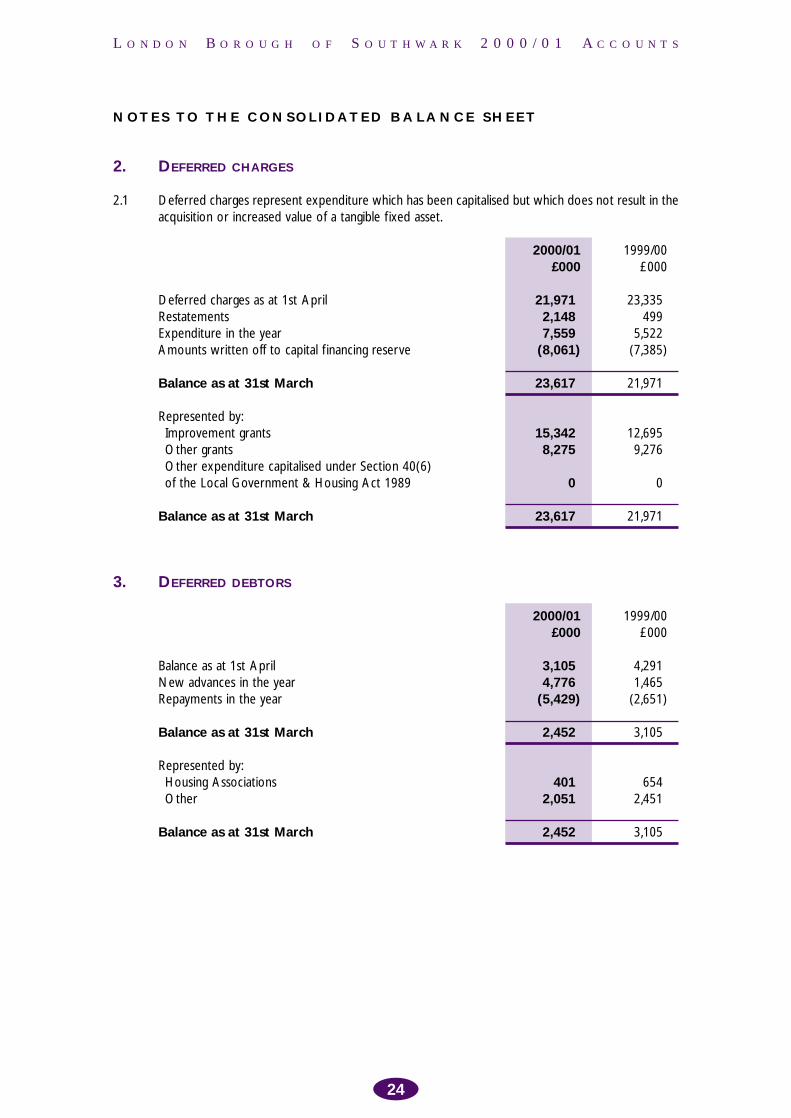

2 DEFERRED CHARGES

21 Deferred charges represent expenditure which has been capitalised but which does not result in the acquisition or increased value of a tangible f ixed asset

Deferred charges as at 1st April Restatements Expenditure in the year Amounts written off to capital f inancing reserve

Balance as at 31st March

Represented by Improvement grants Other grants Other expenditure capitalised under Section 40(6) of the Local Government amp Housing Act 1989

Balance as at 31st March

3 DEFERRED DEBTORS

Balance as at 1st April New advances in the year Repayments in the year

Balance as at 31st March

Represented by Housing Associations Other

Balance as at 31st March

200001 199900 pound000 pound000

21971) 23335 2148) 499 7559) 5522

(8061) (7385)

23617) 21971

15342) 12695 8275) 9276

0) 0

23617) 21971

200001 199900 pound000 pound000

3105) 4291 4776) 1465

(5429) (2651)

2452) 3105

401) 654 2051) 2451

2452) 3105

24

)

)

)

)

L O N D O N B O R O U G H O F S O U T H W A R K 2 0 0 0 0 1 A C C O U N T S

NOTES TO THE CONSOLIDATED BALANCE SHEET

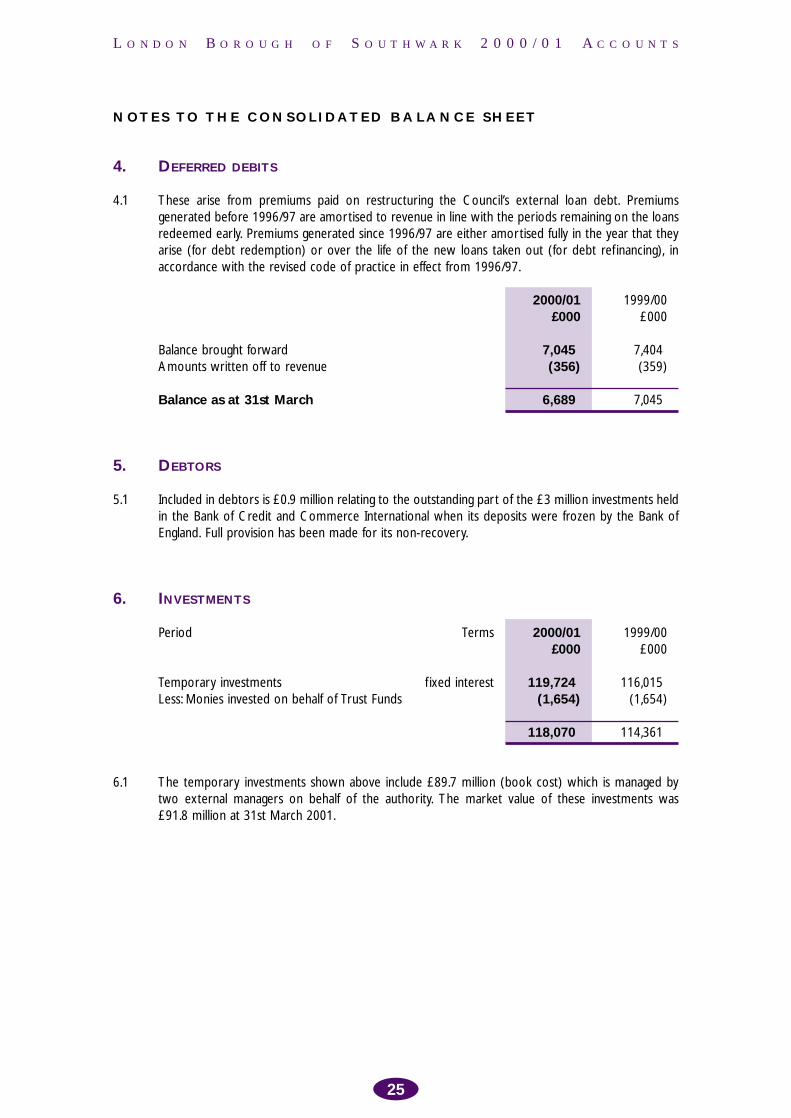

4 DEFERRED DEBITS

41 These arise from premiums paid on restructuring the Councilrsquos external loan debt Premiums generated before 199697 are amortised to revenue in line with the periods remaining on the loans redeemed early Premiums generated since 199697 are either amortised fully in the year that they arise (for debt redemption) or over the life of the new loans taken out (for debt ref inancing) in accordance with the revised code of practice in effect from 199697

199900 pound000

Balance brought forward 7404 Amounts written off to revenue (359)

Balance as at 31st March 7045

200001 pound000

7045) (356)

6689)

5 DEBTORS

51 Included in debtors is pound09 million relating to the outstanding part of the pound3 million investments held in the Bank of Credit and Commerce International when its deposits were frozen by the Bank of England Full provision has been made for its non-recovery

6 INVESTMENTS

Period Terms 199900 pound000

Temporary investments f ixed interest 116015 Less Monies invested on behalf of Trust Funds (1654)

200001pound000

119724)(1654)

118070) 114361

61 The temporary investments shown above include pound897 million (book cost) which is managed by two external managers on behalf of the authority The market value of these investments was pound918 million at 31st March 2001

25

)))

)

)))))

)

)

L O N D O N B O R O U G H O F S O U T H W A R K 2 0 0 0 0 1 A C C O U N T S

NOTES TO THE CONSOLIDATED BALANCE SHEET

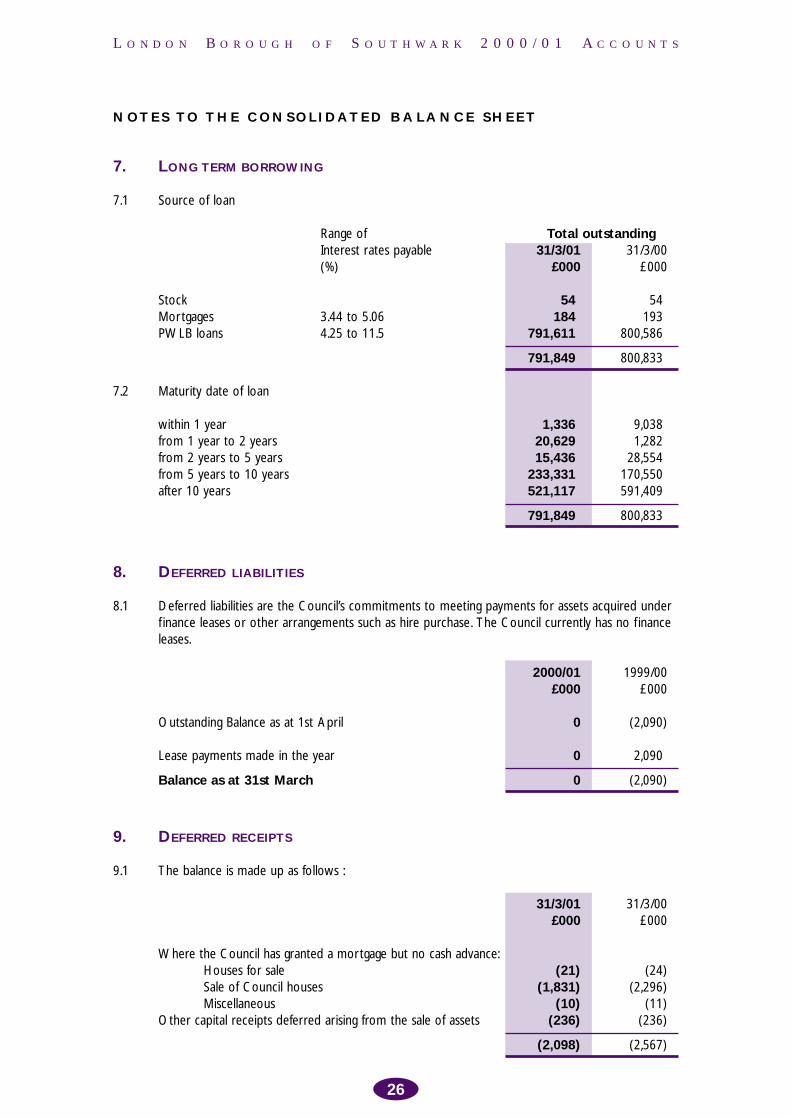

7 LONG TERM BORROWING

71 Source of loan

Range of Total outstanding Interest rates payable 31301 31300 () pound000 pound000

Stock 54) 54 Mortgages 344 to 506 184) 193 PWLB loans 425 to 115 791611) 800586

791849) 800833

72 Maturity date of loan

within 1 year 1336) 9038 from 1 year to 2 years 20629) 1282 from 2 years to 5 years 15436) 28554 from 5 years to 10 years 233331) 170550 after 10 years 521117) 591409

791849) 800833

8 DEFERRED LIABILITIES

81 Deferred liabilities are the Councilrsquos commitments to meeting payments for assets acquired under f inance leases or other arrangements such as hire purchase The Council currently has no f inance leases

200001 199900 pound000 pound000

Outstanding Balance as at 1st April 0 (2090)

Lease payments made in the year 0 2090

Balance as at 31st March 0 (2090)

9 DEFERRED RECEIPTS

91 The balance is made up as follows

31301 31300 pound000 pound000

Where the Council has granted a mortgage but no cash advance Houses for sale (21) (24) Sale of Council houses (1831) (2296) Miscellaneous (10) (11)

Other capital receipts deferred arising from the sale of assets (236) (236)

(2098) (2567)

26

)

)))

L O N D O N B O R O U G H O F S O U T H W A R K 2 0 0 0 0 1 A C C O U N T S

NOTES TO THE CONSOLIDATED BALANCE SHEET

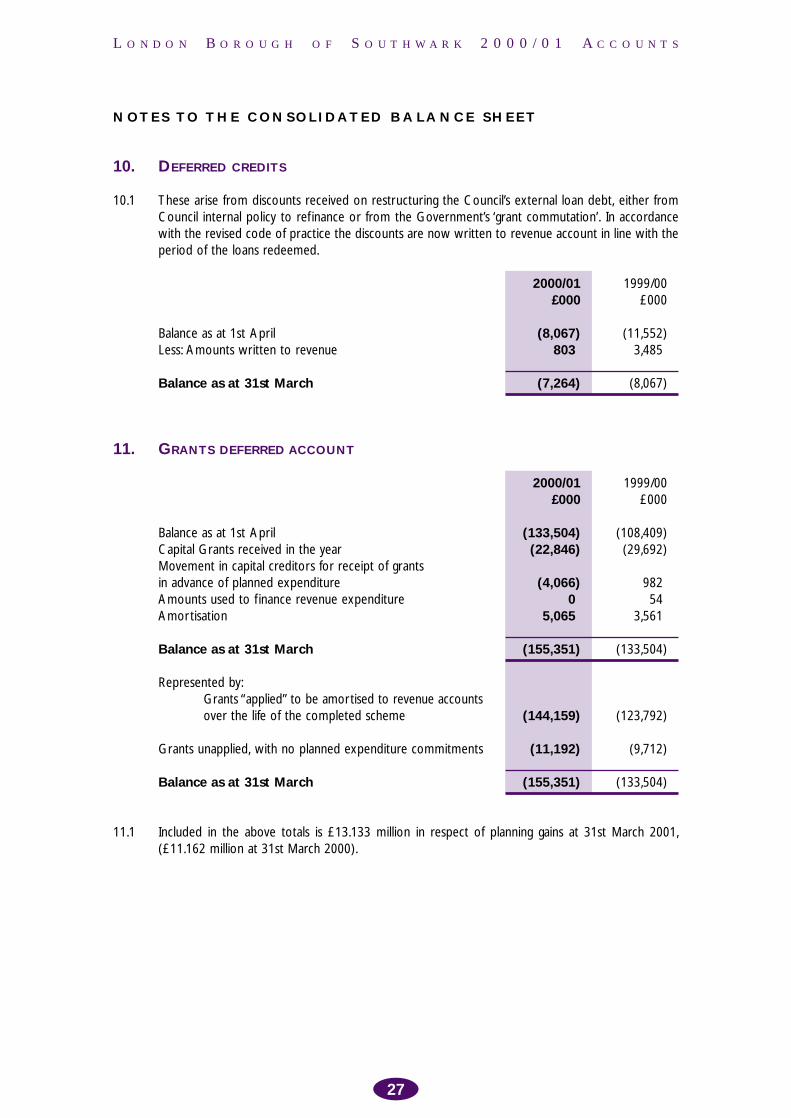

10 DEFERRED CREDITS

101 These arise from discounts received on restructuring the Councilrsquos external loan debt either from Council internal policy to ref inance or from the Governmentrsquos lsquogrant commutationrsquo In accordance with the revised code of practice the discounts are now written to revenue account in line with the period of the loans redeemed

199900 pound000

Balance as at 1st April (11552) Less Amounts written to revenue 3485

Balance as at 31st March (8067)

200001 pound000

(8067) 803)

(7264)

11 GRANTS DEFERRED ACCOUNT

199900 pound000

Balance as at 1st April (108409) Capital Grants received in the year (29692) Movement in capital creditors for receipt of grants in advance of planned expenditure 982 Amounts used to f inance revenue expenditure 54 Amortisation 3561

Balance as at 31st March (133504)

Represented by Grants ldquoappliedrdquo to be amortised to revenue accounts over the life of the completed scheme (123792)

Grants unapplied with no planned expenditure commitments (9712)

Balance as at 31st March

200001pound000

(133504)(22846)

(4066)0)

5065)

(155351)

(144159)

(11192)

(155351) (133504)

111 Included in the above totals is pound13133 million in respect of planning gains at 31st March 2001 (pound11162 million at 31st March 2000)

27

)

)))))

)

))))

)

L O N D O N B O R O U G H O F S O U T H W A R K 2 0 0 0 0 1 A C C O U N T S

NOTES TO THE CONSOLIDATED BALANCE SHEET

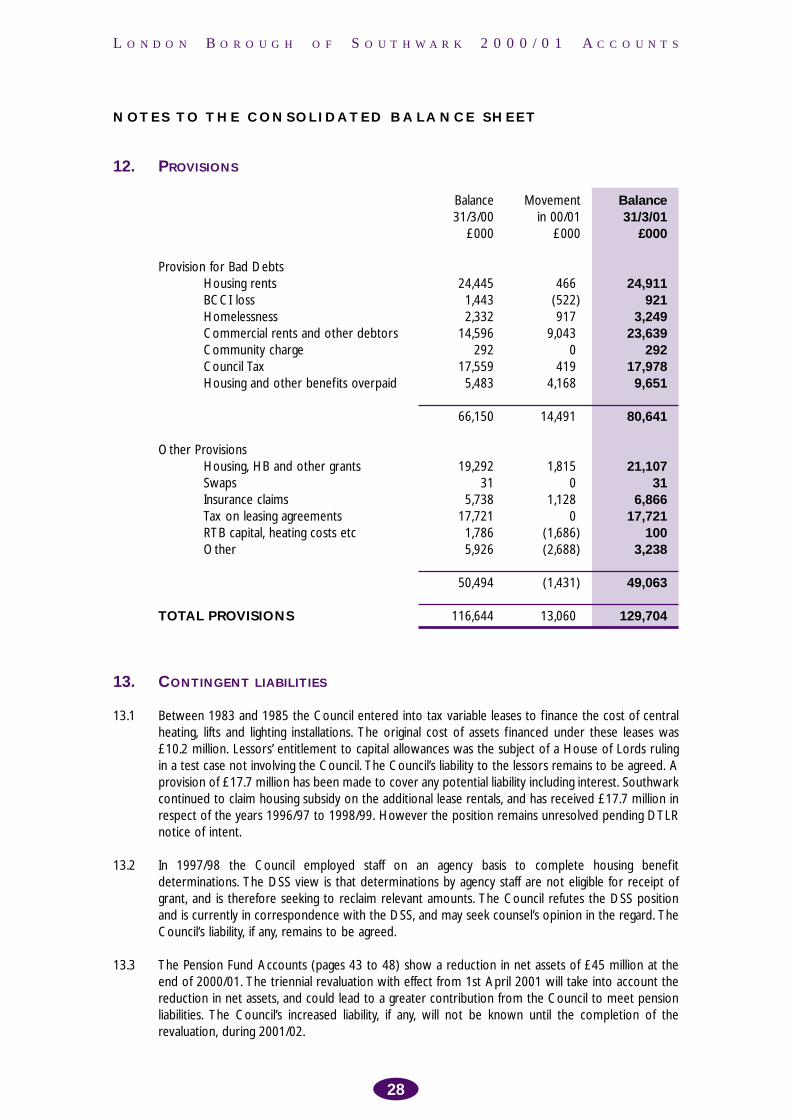

12 PROVISIONS

Balance 31300

pound000

Movement in 0001

pound000

Balance 31301

pound000

Provision for Bad Debts Housing rents BCCI loss Homelessness Commercial rents and other debtors Community charge Council Tax Housing and other benefits overpaid

24445 1443 2332

14596 292

17559 5483

466 (522) 917

9043 0

419 4168

24911 921

3249 23639

292 17978 9651

66150 14491 80641

Other Provisions Housing HB and other grants Swaps Insurance claims Tax on leasing agreements RTB capital heating costs etc Other

19292 31

5738 17721 1786 5926

1815 0

1128 0

(1686) (2688)

21107 31

6866 17721

100 3238

50494 (1431) 49063

TOTAL PROVISIONS 116644 13060 129704

13 CONTINGENT LIABILITIES

131 Between 1983 and 1985 the Council entered into tax variable leases to f inance the cost of central heating lifts and lighting installations The original cost of assets f inanced under these leases was pound102 million Lessorsrsquo entitlement to capital allowances was the subject of a House of Lords ruling in a test case not involving the Council The Councilrsquos liability to the lessors remains to be agreed A provision of pound177 million has been made to cover any potential liability including interest Southwark continued to claim housing subsidy on the additional lease rentals and has received pound177 million in respect of the years 199697 to 199899 However the position remains unresolved pending DTLR notice of intent

132 In 199798 the Council employed staff on an agency basis to complete housing benefit determinations The DSS view is that determinations by agency staff are not eligible for receipt of grant and is therefore seeking to reclaim relevant amounts The Council refutes the DSS position and is currently in correspondence with the DSS and may seek counselrsquos opinion in the regard The Councilrsquos liability if any remains to be agreed

133 The Pension Fund Accounts (pages 43 to 48) show a reduction in net assets of pound45 million at the end of 200001 The triennial revaluation with effect from 1st April 2001 will take into account the reduction in net assets and could lead to a greater contribution from the Council to meet pension liabilities The Councilrsquos increased liability if any will not be known until the completion of the revaluation during 200102

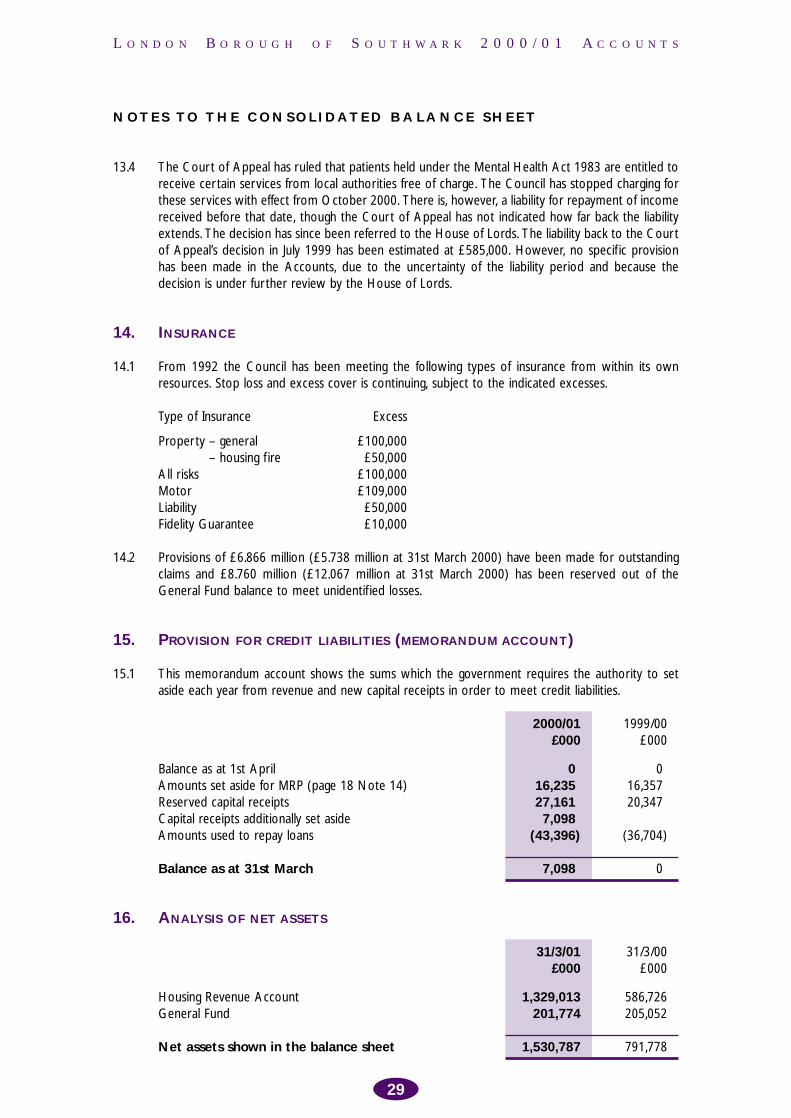

28

))))

)

L O N D O N B O R O U G H O F S O U T H W A R K 2 0 0 0 0 1 A C C O U N T S

NOTES TO THE CONSOLIDATED BALANCE SHEET

134 The Court of Appeal has ruled that patients held under the Mental Health Act 1983 are entitled to receive certain services from local authorities free of charge The Council has stopped charging for these services with effect from October 2000 There is however a liability for repayment of income received before that date though the Court of Appeal has not indicated how far back the liability extends The decision has since been referred to the House of Lords The liability back to the Court of Appealrsquos decision in July 1999 has been estimated at pound585000 However no specif ic provision has been made in the Accounts due to the uncertainty of the liability period and because the decision is under further review by the House of Lords

14 INSURANCE

141 From 1992 the Council has been meeting the following types of insurance from within its own resources Stop loss and excess cover is continuing subject to the indicated excesses

Type of Insurance Excess

Property ndash general pound100000 ndash housing f ire pound50000

All risks pound100000 Motor pound109000 Liability pound50000 Fidelity Guarantee pound10000

142 Provisions of pound6866 million (pound5738 million at 31st March 2000) have been made for outstanding claims and pound8760 million (pound12067 million at 31st March 2000) has been reserved out of the General Fund balance to meet unidentif ied losses

15 PROVISION FOR CREDIT LIABILITIES (MEMORANDUM ACCOUNT)

151 This memorandum account shows the sums which the government requires the authority to set aside each year from revenue and new capital receipts in order to meet credit liabilities

199900 pound000

Balance as at 1st April 0 Amounts set aside for MRP (page 18 Note 14) 16357 Reserved capital receipts 20347 Capital receipts additionally set aside Amounts used to repay loans (36704)

Balance as at 31st March 0

200001 pound000

0) 16235) 27161) 7098)

(43396)

7098)

16 ANALYSIS OF NET ASSETS

Housing Revenue Account General Fund

Net assets shown in the balance sheet

31301 pound000

31300 pound000

1329013 201774

586726 205052

1530787 791778

29

))))))))

)

)

)

L O N D O N B O R O U G H O F S O U T H W A R K 2 0 0 0 0 1 A C C O U N T S

NOTES TO THE CONSOLIDATED BALANCE SHEET

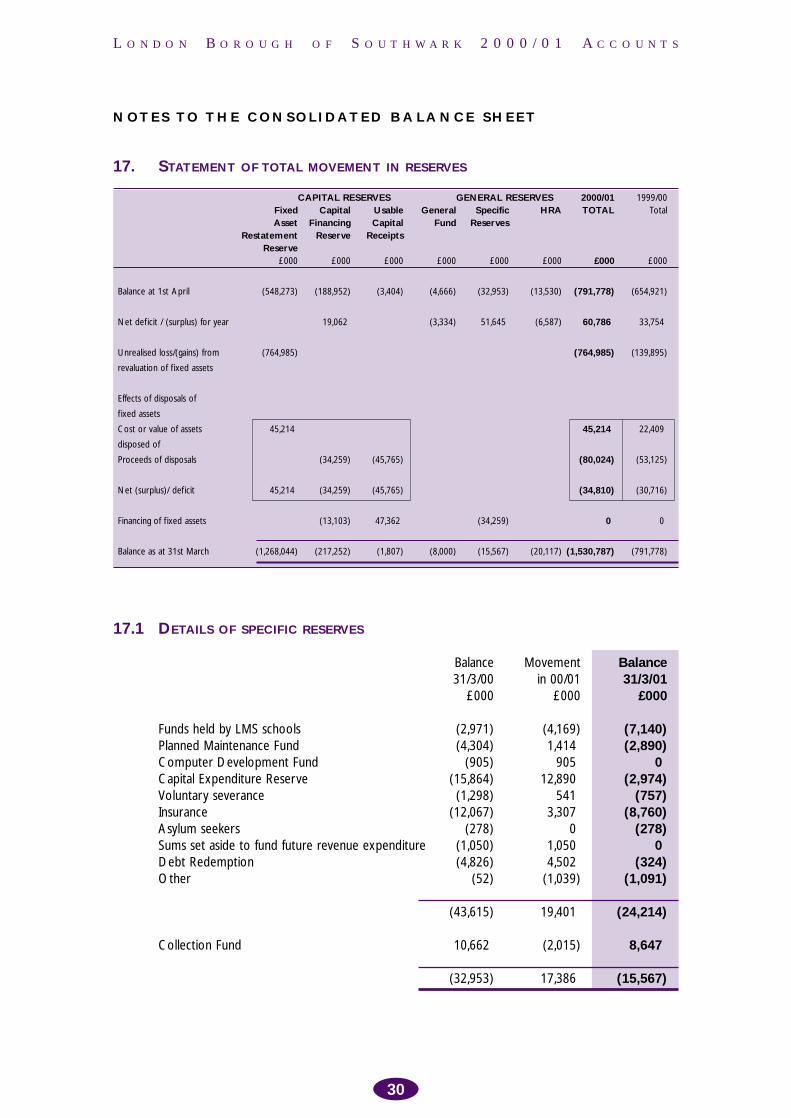

17 STATEMENT OF TOTAL MOVEMENT IN RESERVES

CAPITAL RESERVES GENERAL RESERVES 200001 199900 Fixed Capital Usable General Specific HRA TOTAL Total Asset Financing Capital Fund Reserves

Restatement Reserve Receipts Reserve

pound000 pound000 pound000 pound000 pound000 pound000 pound000 pound000

Balance at 1st April (548273) (188952) (3404) (4666) (32953) (13530) (791778) (654921)

Net deficit (surplus) for year 19062) (3334) 51645) (6587) 60786) 33754)

Unrealised loss(gains) from (764985) (764985) (139895)

revaluation of f ixed assets

Effects of disposals of

f ixed assets

Cost or value of assets 45214) 45214) 22409)

disposed of

Proceeds of disposals (34259) (45765) (80024) (53125)

Net (surplus) def icit 45214) (34259) (45765) (34810) (30716)

Financing of f ixed assets (13103) 47362) (34259) 0) 0)

Balance as at 31st March (1268044) (217252) (1807) (8000) (15567) (20117) (1530787) (791778)

171 DETAILS OF SPECIFIC RESERVES

Balance Movement 31300 in 0001

pound000 pound000

Funds held by LMS schools (2971) (4169) Planned Maintenance Fund (4304) 1414 Computer Development Fund (905) 905 Capital Expenditure Reserve (15864) 12890 Voluntary severance (1298) 541 Insurance (12067) 3307 Asylum seekers (278) 0 Sums set aside to fund future revenue expenditure (1050) 1050 Debt Redemption (4826) 4502 Other (52) (1039)

(43615) 19401

Collection Fund 10662 (2015)

(32953) 17386

Balance 31301

pound000

(7140) (2890)

0) (2974)

(757) (8760)

(278) 0)

(324) (1091)

(24214)

8647)

(15567)

30

)

)

) ) )

))

L O N D O N B O R O U G H O F S O U T H W A R K 2 0 0 0 0 1 A C C O U N T S

NOTES TO THE CONSOLIDATED BALANCE SHEET

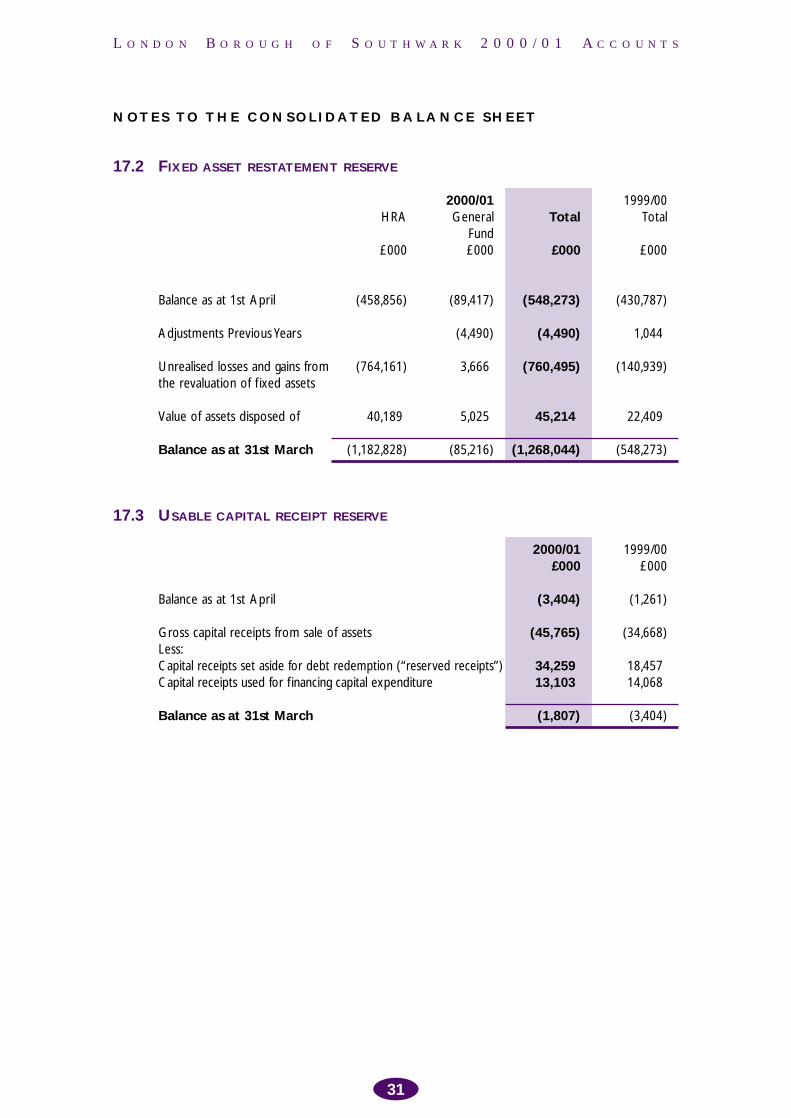

172 FIXED ASSET RESTATEMENT RESERVE

Balance as at 1st April

Adjustments Previous Years

Unrealised losses and gains from the revaluation of f ixed assets

Value of assets disposed of

Balance as at 31st March

200001 199900 HRA General Total Total

Fund pound000 pound000 pound000 pound000

(458856) (89417) (548273) (430787)

(4490) (4490) 1044

(764161) 3666 (760495) (140939)

40189 5025 45214) 22409

(1182828) (85216) (1268044) (548273)

173 USABLE CAPITAL RECEIPT RESERVE

199900 pound000

Balance as at 1st April (1261)

Gross capital receipts from sale of assets (34668) Less Capital receipts set aside for debt redemption (ldquoreserved receiptsrdquo) 18457 Capital receipts used for financing capital expenditure 14068

Balance as at 31st March (3404)

200001 pound000

(3404)

(45765)

34259) 13103)

(1807)

31

)) ) )) )

) ) )) ) )

) )

L O N D O N B O R O U G H O F S O U T H W A R K 2 0 0 0 0 1 A C C O U N T S

NOTES TO THE CONSOLIDATED BALANCE SHEET

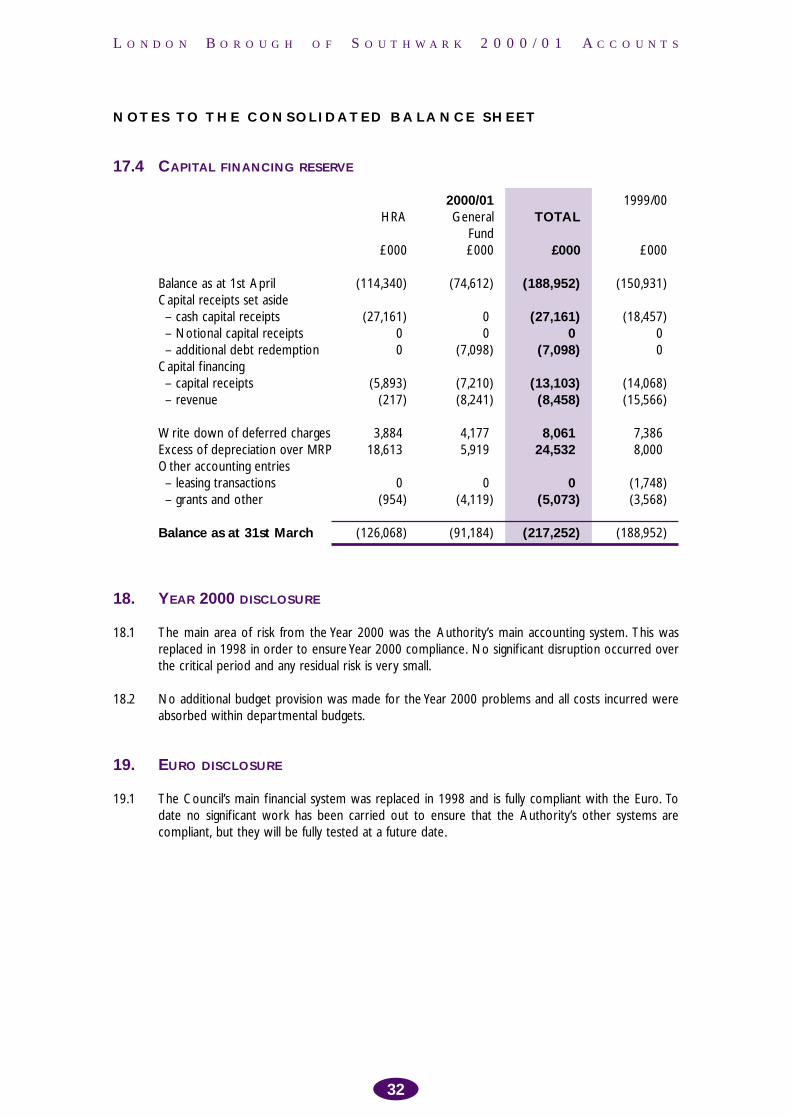

174 CAPITAL FINANCING RESERVE

200001 199900 HRA General

Fund pound000 pound000 pound000

Balance as at 1st April (114340) (74612) (150931) Capital receipts set aside ndash cash capital receipts (27161) 0 (18457) ndash Notional capital receipts 0 0 0 ndash additional debt redemption 0 (7098) 0

Capital f inancing ndash capital receipts (5893) (7210) (14068) ndash revenue (217) (8241) (15566)

Write down of deferred charges 3884 4177 7386 Excess of depreciation over MRP 18613 5919 8000 Other accounting entries ndash leasing transactions 0 0 (1748) ndash grants and other (954) (4119) (3568)

Balance as at 31st March (126068) (91184) (188952)

TOTAL

pound000

(188952)

(27161) 0)

(7098)

(13103) (8458)

8061) 24532)

0) (5073)

(217252)

18 YEAR 2000 DISCLOSURE

181 The main area of risk from the Year 2000 was the Authorityrsquos main accounting system This was replaced in 1998 in order to ensure Year 2000 compliance No signif icant disruption occurred over the critical period and any residual risk is very small

182 No additional budget provision was made for the Year 2000 problems and all costs incurred were absorbed within departmental budgets

19 EURO DISCLOSURE

191 The Councilrsquos main f inancial system was replaced in 1998 and is fully compliant with the Euro To date no signif icant work has been carried out to ensure that the Authorityrsquos other systems are compliant but they will be fully tested at a future date

32

)

))

)

)

L O N D O N B O R O U G H O F S O U T H W A R K 2 0 0 0 0 1 A C C O U N T S

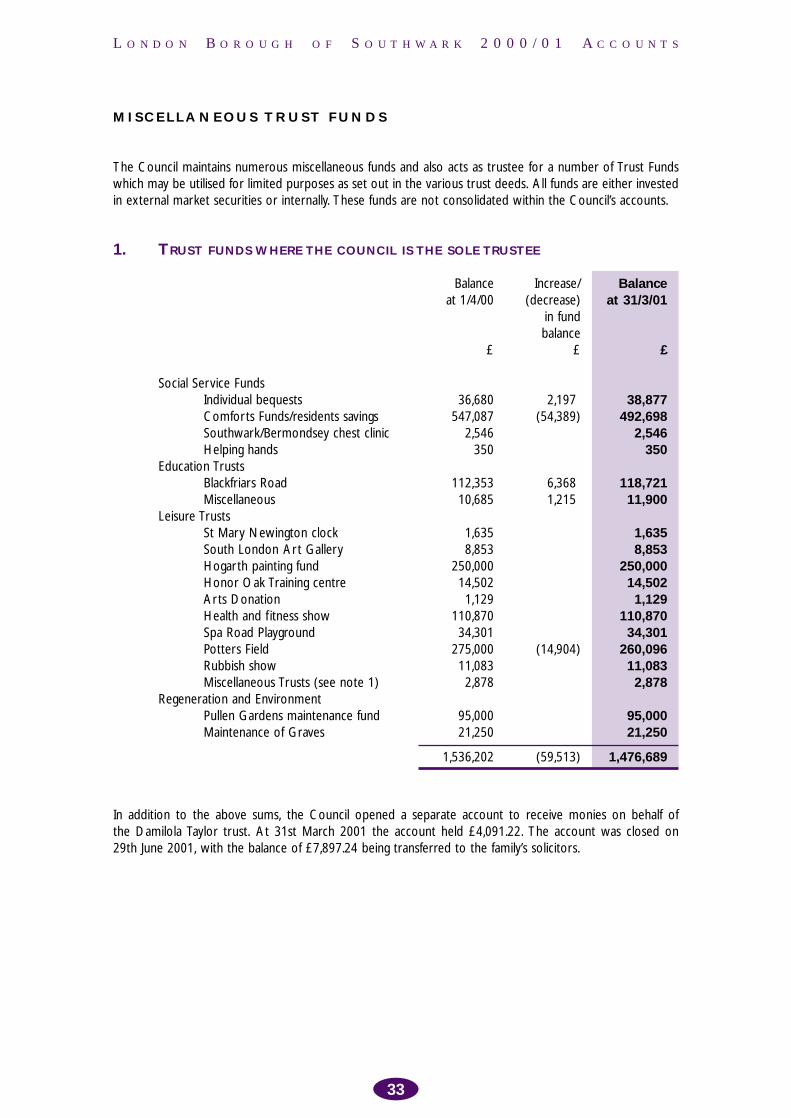

MISCELLANEOUS TRUST FUNDS

The Council maintains numerous miscellaneous funds and also acts as trustee for a number of Trust Funds which may be utilised for limited purposes as set out in the various trust deeds All funds are either invested in external market securities or internally These funds are not consolidated within the Councilrsquos accounts

1 TRUST FUNDS WHERE THE COUNCIL IS THE SOLE TRUSTEE

Balance Increase Balance at 1400 (decrease) at 31301

in fund balance

pound pound pound

Social Service Funds Individual bequests 36680 2197 38877 Comforts Fundsresidents savings 547087 (54389) 492698 SouthwarkBermondsey chest clinic 2546 2546 Helping hands 350 350

Education Trusts Blackfriars Road 112353 6368 118721 Miscellaneous 10685 1215 11900

Leisure Trusts St Mary Newington clock 1635 1635 South London Art Gallery 8853 8853 Hogarth painting fund 250000 250000 Honor Oak Training centre 14502 14502 Arts Donation 1129 1129 Health and f itness show 110870 110870 Spa Road Playground 34301 34301 Potters Field 275000 (14904) 260096 Rubbish show 11083 11083 Miscellaneous Trusts (see note 1) 2878 2878

Regeneration and Environment Pullen Gardens maintenance fund 95000 95000 Maintenance of Graves 21250 21250

1536202 (59513) 1476689

In addition to the above sums the Council opened a separate account to receive monies on behalf of the Damilola Taylor trust At 31st March 2001 the account held pound409122 The account was closed on 29th June 2001 with the balance of pound789724 being transferred to the familyrsquos solicitors

33

L O N D O N B O R O U G H O F S O U T H W A R K 2 0 0 0 0 1 A C C O U N T S

MISCELLANEOUS TRUST FUNDS

The purposes of the trust funds are listed below

Individual Bequests Joseph Taylor Ex LCC bequest

Frank Bezer To provide Christmas extras to children in the Hollies or any replacement accommodation

George Baker For the benefit of persons living in residential accommodation in Southwark

Daniel Steele To provide extras for residents of Nye Bevan Lodge

Comfort Funds Residentsrsquo Savings This comprises numerous separate funds to provide ldquocomfortsrdquo to residents of the various Social Services establishments and savings accounts administered on behalf of the residents of those establishments

SouthwarkBermondsey Chest Clinic Fund set up for the benefit of people using the chest clinicday centre in Bermondsey

Helping Hands To provide for printing costs for the Mayorrsquos Common Good Charity

Blackfriars Road To provide education and health services for Bermondsey children

Miscellaneous Bequests set up to provide prizes or f inancial assistance to students at relevant schools in the Borough

St Mary Newington Clock To provide for the maintenance of the clock at St Mary Newington

South London Art Gallery Interest to be used for the running of the Gallery

Hogarth Painting Fund Interest to be used for the arts in Southwark

Honor Oak Training Centre For winding up costs of the Centre

Arts Donations Sums donated to the Council to be used for specif ic arts purposes

Health amp Fitness Show To go towards funding of GP referral scheme and Peckham Pulse

Potters Field To maintain open space adjoining London Bridge City

Rubbish Show To go towards an exhibition at Livesey Museum

Pullens Gardens maintenance fund To meet the maintenance cost of Pullens Gardens

Maintenance of graves Moneys received for the maintenance of graves

2 TRUST FUNDS WHERE THE COUNCIL IS NOT THE SOLE TRUSTEE

Balance Increase Balance at 1400 (decrease) at 31301

in fund balance

pound pound pound

Funds for the relief of Council Tax Walworth Common Estate 917798 (8977) 908821 Borough Market Trustees 6816 (1314) 5502

Leisure Trusts Cuming Bequest 7808 7808 Miscellaneous Trusts (see note 1) 716 716

933138 (10291) 922847

34

L O N D O N B O R O U G H O F S O U T H W A R K 2 0 0 0 0 1 A C C O U N T S

MISCELLANEOUS TRUST FUNDS

Any cash not required for immediate use is invested externally either directly in approved investments or as part of the Councilrsquos short term investments

The purposes of the trust funds are listed below

Walworth Estate Common To provide rate relief in the former parish of St Mary Newington Borough Market Trustees To reduce parochial rates for the parish of St Saviour Cuming Bequest To provide for display of furniture and coins at Cuming Museum

Note 1 Miscellaneous trusts comprise old trusts that are in the process of being closed

35

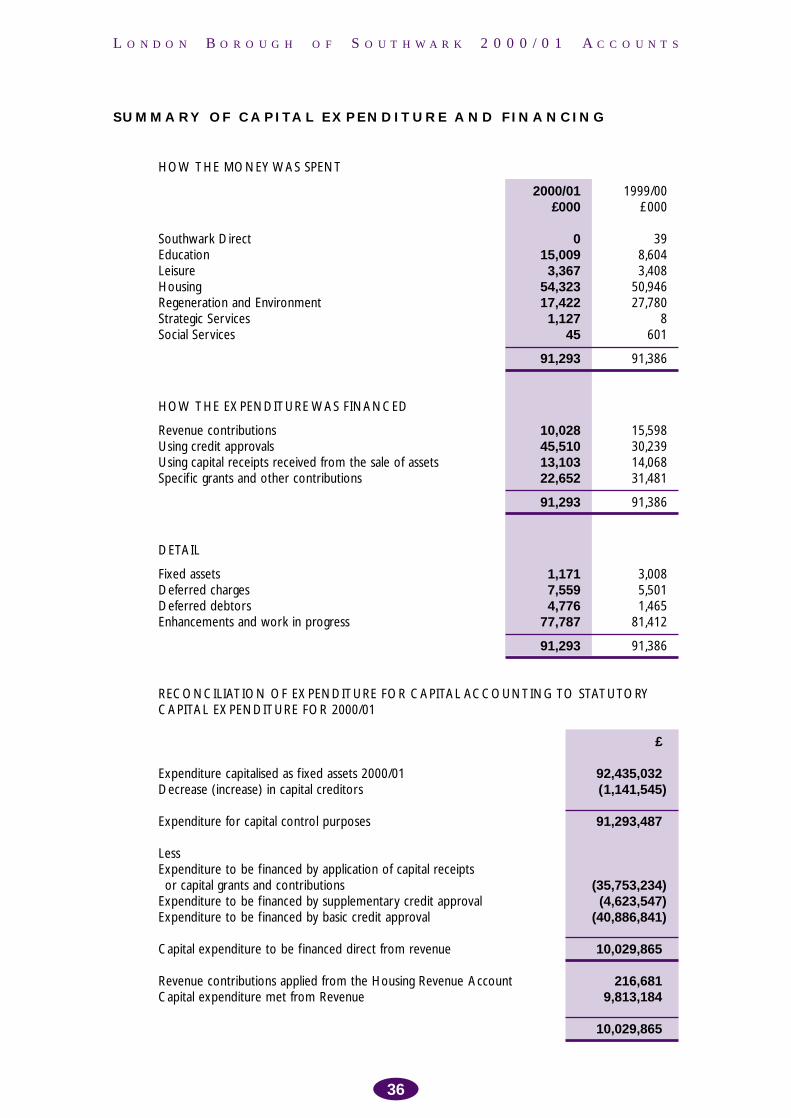

L O N D O N B O R O U G H O F S O U T H W A R K 2 0 0 0 0 1 A C C O U N T S

SUMMARY OF CAPITAL EXPENDITURE AND FINANCING

HOW THE MONEY WAS SPENT

200001 199900 pound000 pound000

Southwark Direct 0 39 Education 15009 8604 Leisure 3367 3408 Housing 54323 50946 Regeneration and Environment 17422 27780 Strategic Services 1127 8 Social Services 45 601

91293 91386

HOW THE EXPENDITURE WAS FINANCED

Revenue contributions 10028 15598 Using credit approvals 45510 30239 Using capital receipts received from the sale of assets 13103 14068 Specif ic grants and other contributions 22652 31481

91293 91386

DETAIL

Fixed assets 1171 3008 Deferred charges 7559 5501 Deferred debtors 4776 1465 Enhancements and work in progress 77787 81412

91293 91386

RECONCILIATION OF EXPENDITURE FOR CAPITAL ACCOUNTING TO STATUTORY CAPITAL EXPENDITURE FOR 200001

Expenditure capitalised as f ixed assets 200001 Decrease (increase) in capital creditors

Expenditure for capital control purposes

Less Expenditure to be f inanced by application of capital receipts or capital grants and contributions

Expenditure to be f inanced by supplementary credit approval Expenditure to be f inanced by basic credit approval

Capital expenditure to be f inanced direct from revenue

Revenue contributions applied from the Housing Revenue Account Capital expenditure met from Revenue

pound)

92435032) (1141545)

91293487)

(35753234) (4623547)

(40886841)

10029865)

216681) 9813184)

10029865)

36

)))

))

)

)

)

)

)

L O N D O N B O R O U G H O F S O U T H W A R K 2 0 0 0 0 1 A C C O U N T S

COLLECTION FUND

This statement represents the transactions of the Collection Fund a statutory fund separate from the General Fund of the Council The Collection Fund accounts independently for income relating to Council Tax and Non-domestic rates on behalf of those bodies (including the Councilrsquos own General Fund) for whom the income has been raised The costs of administering collection are accounted for in the General Fund

INCOME AND EXPENDITURE ACCOUNT

Notes 200001 pound000

200001 pound000

199900 pound000

Income Council Tax Income from Council Tax Council Tax benefits

1 (54343) (18054) (72397)

(50434) (16326)

Non-domestic rates Adjustment re prior years community charges

2 3

(78267) 0)

(63127)

Receipts from preceptors re previous years Collection Fund balance 4

(4707) (2509)

Total Income (155371) (132396)

Expenditure Precepts and Demands GLA Residual Receiver London Borough of Southwark

Non-domestic rates Payment to National Pool Cost of collection allowance

Provision for uncollectable amounts Council Tax

10308) 1412)

59079)

77643) 624)

70799)

78267)

4290)

7807 2324

57979

62505 622

8762

Total Expenditure 153356) 139999

Net Deficit(surplus) for the year (2015) 7603

Deficit(surplus) at 1st April 10664) 3061

Deficit(surplus) at 31st March 8649) 10664

37

))))))))

)

)

)

) )

) )

L O N D O N B O R O U G H O F S O U T H W A R K 2 0 0 0 0 1 A C C O U N T S

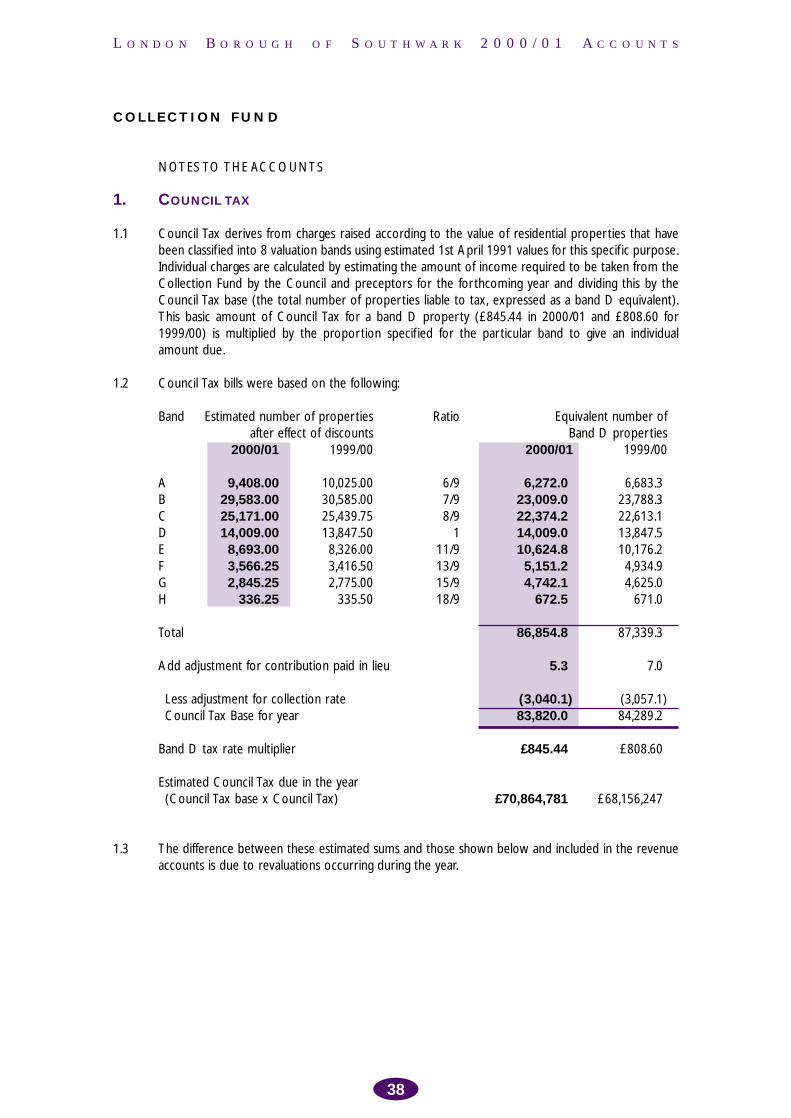

COLLECTION FUND

NOTES TO THE ACCOUNTS

1 COUNCIL TAX

11 Council Tax derives from charges raised according to the value of residential properties that have been classif ied into 8 valuation bands using estimated 1st April 1991 values for this specif ic purpose Individual charges are calculated by estimating the amount of income required to be taken from the Collection Fund by the Council and preceptors for the forthcoming year and dividing this by the Council Tax base (the total number of properties liable to tax expressed as a band D equivalent) This basic amount of Council Tax for a band D property (pound84544 in 200001 and pound80860 for 199900) is multiplied by the proportion specif ied for the particular band to give an individual amount due

12 Council Tax bills were based on the following

Band Estimated number of properties Ratio Equivalent number of after effect of discounts

200001 199900

A B C D E F G H

940800 2958300 2517100 1400900 869300 356625 284525

33625

1002500 3058500 2543975 1384750 832600 341650 277500

33550

69 79 89

1 119 139 159 189

Total

Add adjustment for contribution paid in lieu

Less adjustment for collection rate Council Tax Base for year

Band D properties 200001 199900

62720) 66833 230090) 237883 223742) 226131 140090) 138475 106248) 101762 51512) 49349 47421) 46250

6725) 6710

868548) 873393

53) 70

(30401) (30571) 838200) 842892

Band D tax rate multiplier pound84544 pound80860

Estimated Council Tax due in the year (Council Tax base x Council Tax) pound70864781 pound68156247

13 The difference between these estimated sums and those shown below and included in the revenue accounts is due to revaluations occurring during the year

38

L O N D O N B O R O U G H O F S O U T H W A R K 2 0 0 0 0 1 A C C O U N T S

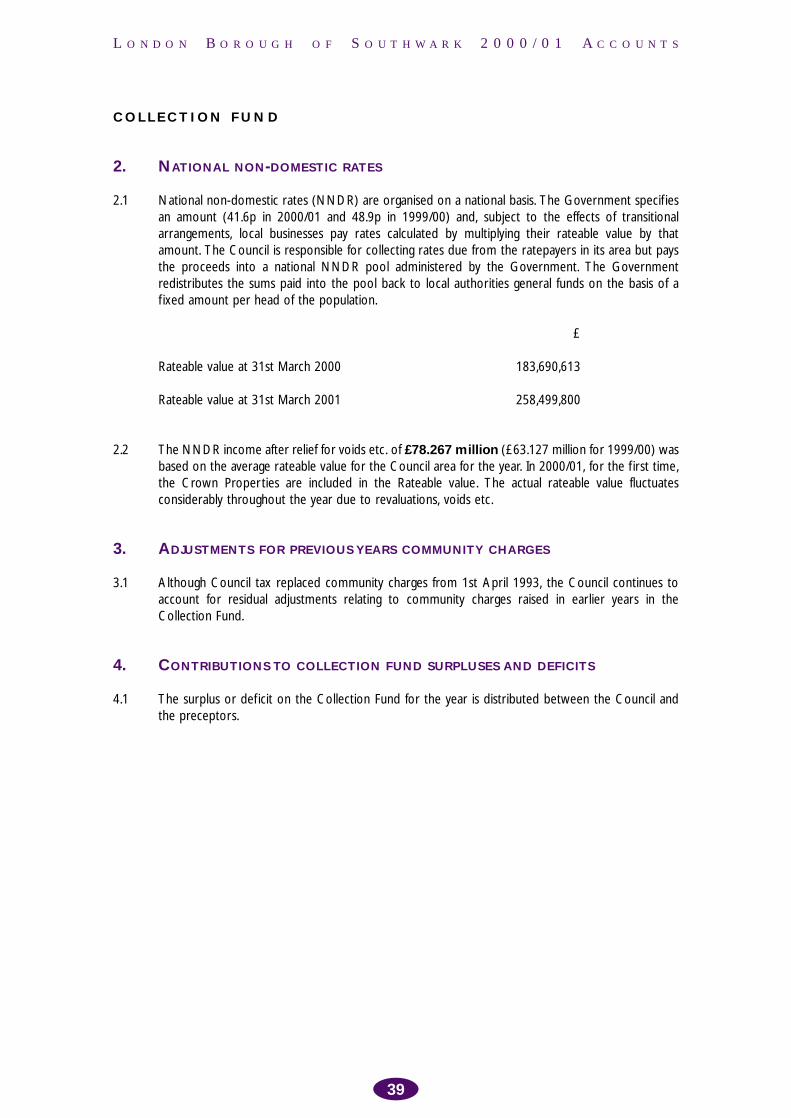

COLLECTION FUND

2 NATIONAL NON-DOMESTIC RATES

21 National non-domestic rates (NNDR) are organised on a national basis The Government specif ies an amount (416p in 200001 and 489p in 199900) and subject to the effects of transitional arrangements local businesses pay rates calculated by multiplying their rateable value by that amount The Council is responsible for collecting rates due from the ratepayers in its area but pays the proceeds into a national NNDR pool administered by the Government The Government redistributes the sums paid into the pool back to local authorities general funds on the basis of a f ixed amount per head of the population

pound

Rateable value at 31st March 2000 183690613

Rateable value at 31st March 2001 258499800

22 The NNDR income after relief for voids etc of pound78267 million (pound63127 million for 199900) was based on the average rateable value for the Council area for the year In 200001 for the f irst time the Crown Properties are included in the Rateable value The actual rateable value fluctuates considerably throughout the year due to revaluations voids etc

3 ADJUSTMENTS FOR PREVIOUS YEARS COMMUNITY CHARGES

31 Although Council tax replaced community charges from 1st April 1993 the Council continues to account for residual adjustments relating to community charges raised in earlier years in the Collection Fund

4 CONTRIBUTIONS TO COLLECTION FUND SURPLUSES AND DEFICITS

41 The surplus or deficit on the Collection Fund for the year is distributed between the Council and the preceptors

39

))))))

)))

)))

)

)

))))

)

)

)

L O N D O N B O R O U G H O F S O U T H W A R K 2 0 0 0 0 1 A C C O U N T S

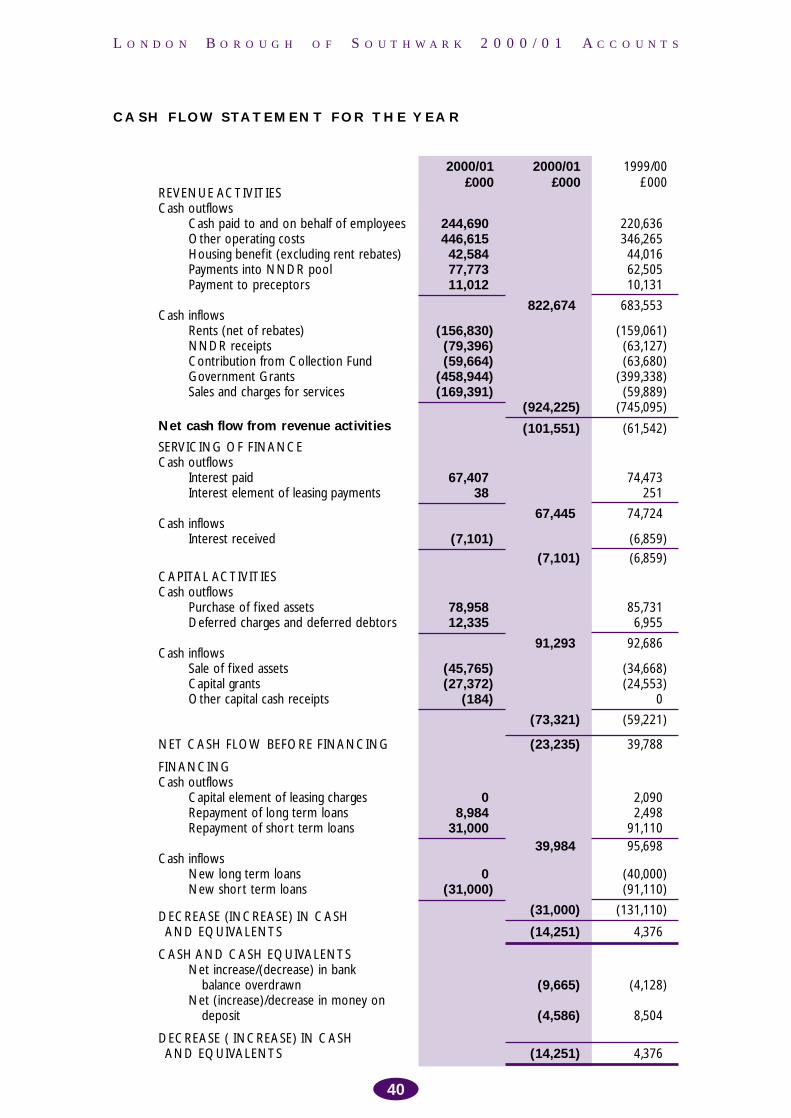

CASH FLOW STATEMENT FOR THE YEAR

200001 200001 199900 pound000 pound000 pound000

REVENUE ACTIVITIES Cash outflows

Cash paid to and on behalf of employees 244690) 220636 Other operating costs 446615) 346265 Housing benefit (excluding rent rebates) 42584) 44016 Payments into NNDR pool 77773) 62505 Payment to preceptors 11012) 10131

Cash inflows 822674) 683553

Rents (net of rebates) (156830) (159061) NNDR receipts (79396) (63127) Contribution from Collection Fund (59664) (63680) Government Grants (458944) (399338) Sales and charges for services (169391) (59889)

(924225) (745095) Net cash flow from revenue activities (101551) (61542) SERVICING OF FINANCE Cash outflows

Interest paid 67407) 74473 Interest element of leasing payments 38) 251

Cash inflows 67445) 74724

Interest received (7101) (6859)

(7101) (6859) CAPITAL ACTIVITIES Cash outflows

Purchase of f ixed assets 78958) 85731 Deferred charges and deferred debtors 12335) 6955

Cash inflows 91293) 92686

Sale of f ixed assets (45765) (34668) Capital grants (27372) (24553) Other capital cash receipts (184) 0

(73321) (59221)

NET CASH FLOW BEFORE FINANCING (23235) 39788

FINANCING Cash outflows

Capital element of leasing charges 0) 2090 Repayment of long term loans 8984) 2498 Repayment of short term loans 31000) 91110

39984) 95698 Cash inflows

New long term loans 0) (40000) New short term loans (31000) (91110)

DECREASE (INCREASE) IN CASH (31000) (131110)

AND EQUIVALENTS (14251) 4376

CASH AND CASH EQUIVALENTS Net increase(decrease) in bank

balance overdrawn (9665) (4128) Net (increase)decrease in money on

deposit (4586) 8504

DECREASE ( INCREASE) IN CASH AND EQUIVALENTS (14251) 4376

40

)))

)

)

)))))) )

)))

)

L O N D O N B O R O U G H O F S O U T H W A R K 2 0 0 0 0 1 A C C O U N T S

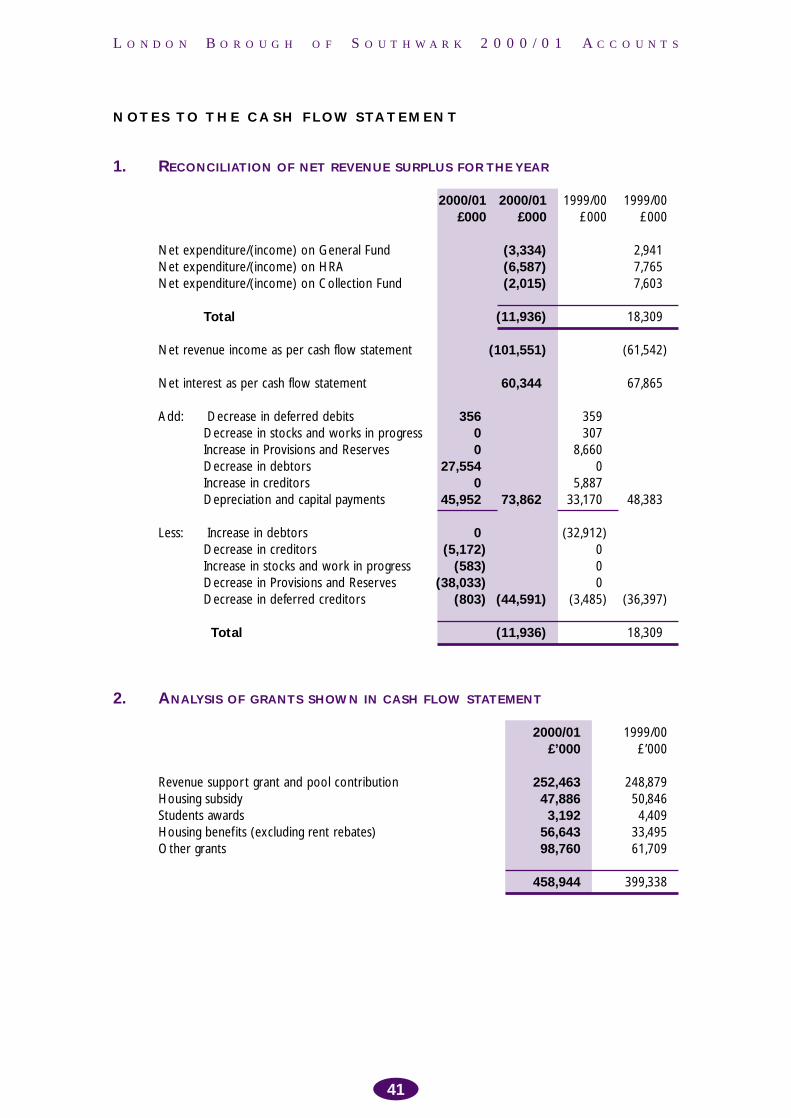

NOTES TO THE CASH FLOW STATEMENT

1 RECONCILIATION OF NET REVENUE SURPLUS FOR THE YEAR

Net expenditure(income) on General Fund Net expenditure(income) on HRA Net expenditure(income) on Collection Fund

Total

Net revenue income as per cash flow statement

Net interest as per cash flow statement

Add Decrease in deferred debits Decrease in stocks and works in progress Increase in Provisions and Reserves Decrease in debtors Increase in creditors Depreciation and capital payments

Less Increase in debtors Decrease in creditors Increase in stocks and work in progress Decrease in Provisions and Reserves Decrease in deferred creditors

Total

200001 200001 199900 199900 pound000 pound000 pound000 pound000

(3334) 2941 (6587) 7765 (2015) 7603

(11936) 18309